38

Understanding Agriculture Finance

| Date post: | 22-Oct-2015 |

| Category: |

Documents |

| Upload: | kahazam-bidyashree |

| View: | 8 times |

| Download: | 0 times |

Understanding Agriculture Finance

AGRICULTURAL FINANCE

NEED FOR AGRICULTURAL FINANCE >75% of the farmers have small holdings Farm income is not sufficient to meet

house hold expenses Crop cultivation is highly dependent on

monsoon rains (one crop in an year under dry land farming)

Cultivation expenses are going up

AGRICULTURAL FINANCE

NEED FOR AGRICULTURAL FINANCE Farmer is not sure of yields as it depends

on agro climatic conditions Leads a simple life, but spends lavishly

during marriages and festivals Requires funds to meet consumption

expenses between one harvest and another

Always in need of money and borrows from money lenders

AGRICULTURAL FINANCE

CREDIT NEEDS OF FARMERSOn the basis of timeShort term loan(0-15 months) to

meet cultivation expensesMedium term loan ( 15 months to 5

years) for deepening of wells, purchase of pump set, cattle, poultry etc

AGRICULTURAL FINANCE

Long term loan ( 5-15 years) for land development, purchase of tractor and land

On the basis of purposeProductive loansConsumption loanUnproductive purposes

AGRICULTURAL FINANCE

NON-INSTITUTIONAL SOURCESLandlordsMobile traders (Itinerant merchants)General merchants ( grocery shops)Money lenders

AGRICULTURAL FINANCE

NON-INSTITUTIONAL SOURCESKachcha arhatias( Small commission

agents)Pucca arhatias ( Big commission

agents) Indigenous bankers( shroffs) Multani shroffs, Gujarathi shroffs, Marvari

kayas, Chettiars in Tamilnadu

AGRICULTURAL FINANCE

MONEY LENDERSObtaining pro-note for a higher

amountExorbitant interest ratesDeduction of interest in advanceForcing the farmer to sell the

produce at a low price

AGRICULTURAL FINANCE

MONEY LENDERSManipulation of records and

attaching the landFarmers still prefer to go to

money lenders- hardly any paper work, immediate payment of loan amount and convenience

AGRICULTURAL FINANCE

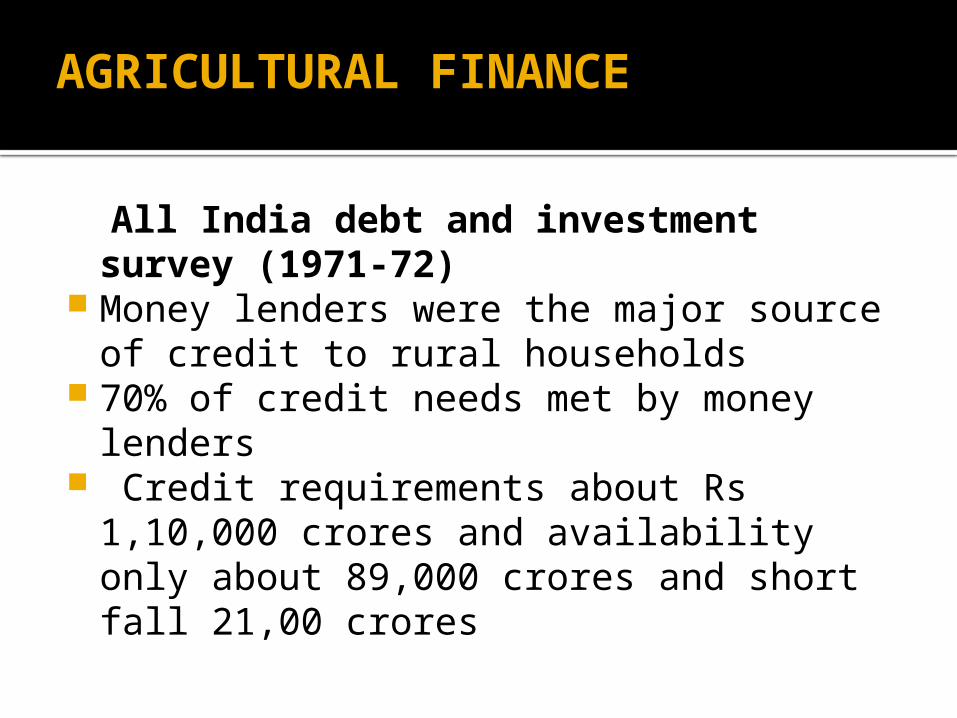

All India debt and investment survey (1971-72)

Money lenders were the major source of credit to rural households

70% of credit needs met by money lenders

Credit requirements about Rs 1,10,000 crores and availability only about 89,000 crores and short fall 21,00 crores

AGRICULTURAL FINANCE

GOVERNMENT INITIATIVES Nationalization of 14 banks in 1969 Six more banks nationalized in 1980 Established regional rural banks in 1975 National bank for agriculture and rural

development was set up in 1982 Share of institutional credit has increased

to 61% in 2002

AGRICULTURAL FINANCE

INSTITUTIONAL SOURCES CREDIT CO-OPERATIVES ( about 3

lakh societies) Credit provided about 35% of the total

credit needs of agriculture Crop loan and produce loan Arrange for sale of agri produce Supply of agricultural inputs

AGRICULTURAL FINANCE

LAND DEVELOPMENT BANKSProvide long term loanPrimary LDB at taluka/district level

and Central LDB at state levelSource of funds from share capital,

loans from banks, deposits and floating of debentures

AGRICULTURAL FINANCE

THE LEAD BANK SCHME

A particular commercial banks is entrusted with the responsibility of playing a major role in rural development in a defined area

The leading bank co-ordinates with all other financial institutions and assess the total credit requirements and identifies credit gaps and scope for institutional finance

AGRICULTURAL FINANCE

LEAD BANK SCHEME Important criteria for selecting a lead bank Resource adequacy of the bank Size of the bank and its spread in the

assigned area Syndicate bank is a lead bank in

Karnataka and it has sponsored RRBs ( Grameen banks) in Karnataka

AGRICULTURAL FINANCE

REGIONAL RURAL BANK

Taking banking services to the door steps of the rural masses particularly in unbanked areas

Provide credit to weaker section of the society who are depending on money lenders

Mobilize rural savings

AGRICULTURAL FINANCE

REGIONAL RURAL BANK

Create supplementary channel for flow of money to rural areas.

Provides loans to small and marginal farmers, labourers, petty traders, artisans etc within the notified area of the bank

AGRICULTURAL FINANCE

COMMERCIAL BANKS Crop loan upto 18 months and loan

amount normally upto Rs 50,000/- Produce marketing loan( upto 6 months)

and loan amount upto 60% of the value of the produce

Land development scheme and amount normally upto Rs one lakh

AGRICULTURAL FINANCE

COMMERCIAL BANKS Minor irrigation

Farm mechanisation scheme

Land purchase scheme Loan amount based on requirements of

funds and verification by bank

AGRICULTURAL FINANCE

CROP LOAN - SECURITY TO BE FURNISHED

Upto Rs 50,000/-hypothecation of the crops

Above Rs 50,000/- hypothecation of the crops and mortgage of the land or third party guarantee

Above Rs 1 Lakh- hypothecation of the crops and mortgage of the land

AGRICULTURAL FINANCE

MOVABLE ASSETS- SECURITY TO BE FURNISHED

Upto Rs 10,000/- based on track record and personal guarantee- Above Rs10000/- and upto Rs 50,000/- hypothecation of the asset

Above Rs50,000/- hypothecation of the asset and mortgage of the land

AGRICULTURAL FINANCE

KISAN CREDIT CARDS Farmers with good track record for two years Limit based on size of the farm, crops grown and

scale of finance required Minimum credit limit Rs 5000/- Valid for three years Loans upto Rs 5 lakhs under Kisan gold card

scheme 30 Million cards issued through co-operatives,

RRBs and Commercial banks

AGRICULTURAL FINANCE

Agricultural Insurance Company of India( 2002)

Implementing agency for the Govt National Agricultural Insurance Scheme

NABARD, General Insurance and four other insurance companies have contributed to equity

NAIS is in operation since 2000 and about 6 million farmers have been covered under the scheme

AGRICULTURAL FINANCE

About crop insurance Loanee farmers: The amount of crop

loan availed for the notified crop is the minimum amount of sum insured which has to insured on compulsory basis.

Further the farmer may opt for additional coverage up to 150% value of average yield by paying premium as communicated by AIC and notified by the State Governments.

AGRICULTURAL FINANCE

Non-loanee farmers: The value of sum insured is arrived at by multiplying the average yield with the last available Minimum Support Price (MSP) announced by Government or the market price provided by the State Government, in case MSP is not announced.

AGRICULTURAL FINANCE

Premium: For Kharif crops, the premium rate is 3.5% of sum insured for bajra and oilseeds and 2.5% for all other food crops including pulses.

For Rabi crops, premium rate is 1.5% for wheat and 2% for all other food crops and oilseeds.

AGRICULTURAL FINANCE

The premium for small and

marginal farmer is subsidized to the extent of 10% which is shared by the State Government and Government of India in equal proportion.

AGRICULTURAL FINANCE

Procedure for insurance coverage: All crop loans disbursed including those through Kisan Credit Cards or otherwise, for insured crops are automatically covered by banks.

Non-loanee farmers willing to avail insurance can contact the nearest bank before the stipulated cut off dates and submit the proposal forms along with proof of land/crop cultivated.

AGRICULTURAL FINANCE

Insurance Claims become automatically payable if there is shortfall in yield i.e. the current seasons yield is less than the prescribed yield

The shortfall is converted in to claims by multiplying the percentage shortfall with sum insured.

The claims are automated and credited to the farmers account in the banks and farmers or banks need not lodge a claim with AIC

MICROFINANCE

There are millions of people who operate small business i.e. Micro Enterprises such as making candles, papads, mudpots, bamboo baskets, selling vegetables, running grocery/tea/pan shops, cattle rearing, tailoring etc

Small enterprises require credit for raw materials and equipments

Micro credit refers to loans and credit needs of micro enterprises. It means providing poor families with small loans to engage in productive activities

MICROFINANCE

Micro credit is normally offered to a group of people or individual.

Main issue for the poor is access to credit and not of cost of credit

Example: A grocery shop with an investment of Rs 20,000/ is able to generate income of Rs 1.50 lakhs and profit of about Rs 8000/- after meeting interest and other expenses.

Grameen Bank of Bangladesh- NGOs, professionals, private and public sector

banks active in the area of microfinance

MICROFINANCE

Self employed womens association (SEVA) started Mahila seva co-operative bank (1974) in Gujarat. Provides banking services to poor, illiterate , self employed women

SKS microfinance is one of the fastest growing MFIs in the world. It has about 1500 field branches, 15,000 employees and has disbursed about Rs 9000 crores. Has tied up with companies to provide basic mobile phones, water purifiers and solar lights.

MICROFINANCE

Self Help Group Govt programme on “Development of

women and children in rural areas” Villagers require small amount to meet

household expenses/ undertake income generating activities

People from the same background and involved in similar economic activities

Cohesive group of 15-20 people

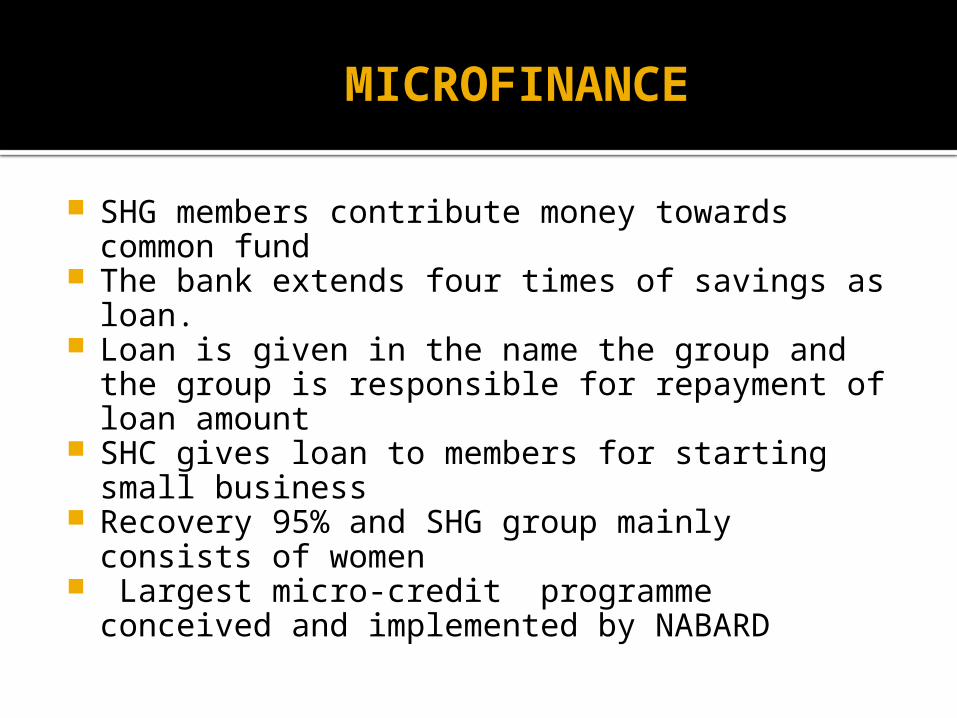

MICROFINANCE

SHG members contribute money towards common fund

The bank extends four times of savings as loan. Loan is given in the name the group and the

group is responsible for repayment of loan amount

SHC gives loan to members for starting small business

Recovery 95% and SHG group mainly consists of women

Largest micro-credit programme conceived and implemented by NABARD

AGRICULTURAL FINANCE

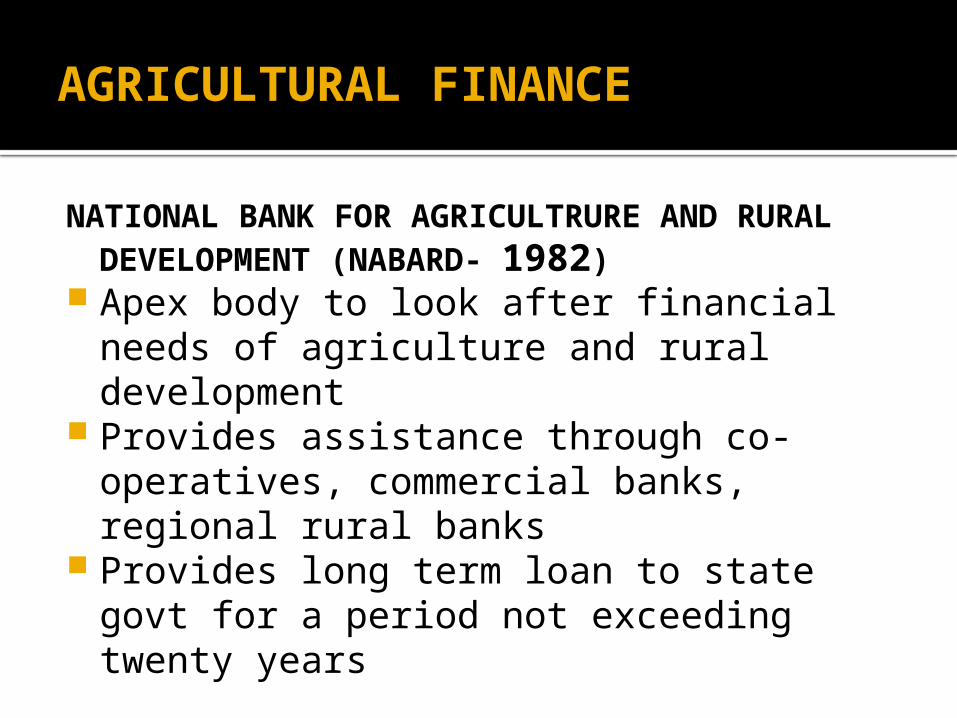

NATIONAL BANK FOR AGRICULTRURE AND RURAL DEVELOPMENT (NABARD- 1982)

Apex body to look after financial needs of agriculture and rural development

Provides assistance through co-operatives, commercial banks, regional rural banks

Provides long term loan to state govt for a period not exceeding twenty years

AGRICULTURAL FINANCE

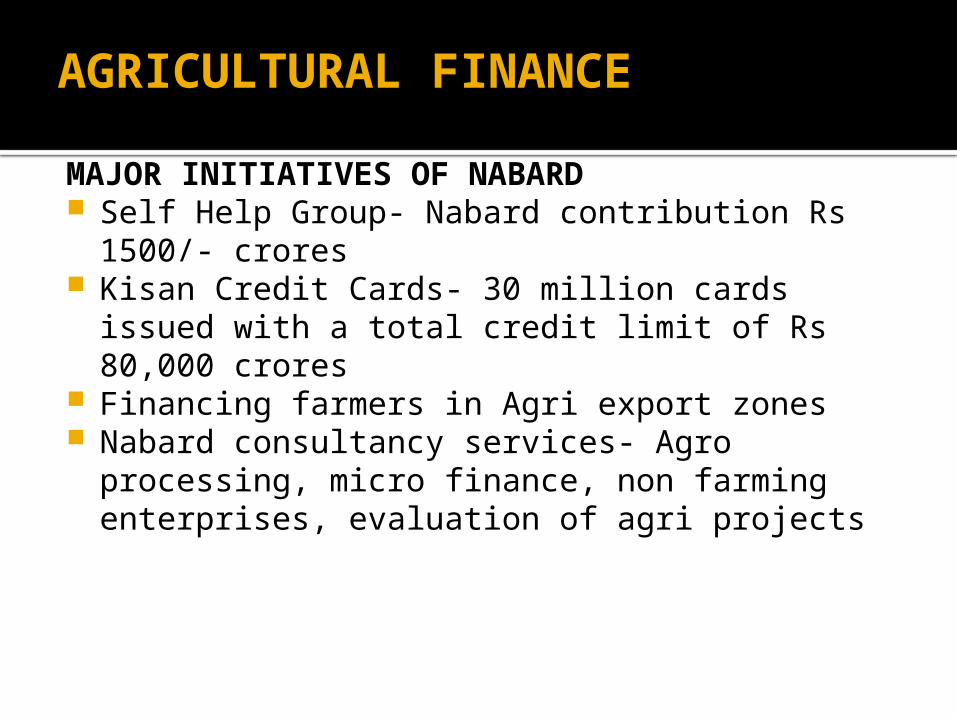

MAJOR INITIATIVES OF NABARD Self Help Group- Nabard contribution Rs 1500/-

crores Kisan Credit Cards- 30 million cards issued with a

total credit limit of Rs 80,000 crores Financing farmers in Agri export zones Nabard consultancy services- Agro processing,

micro finance, non farming enterprises, evaluation of agri projects

BANKING IN RURAL MARKET

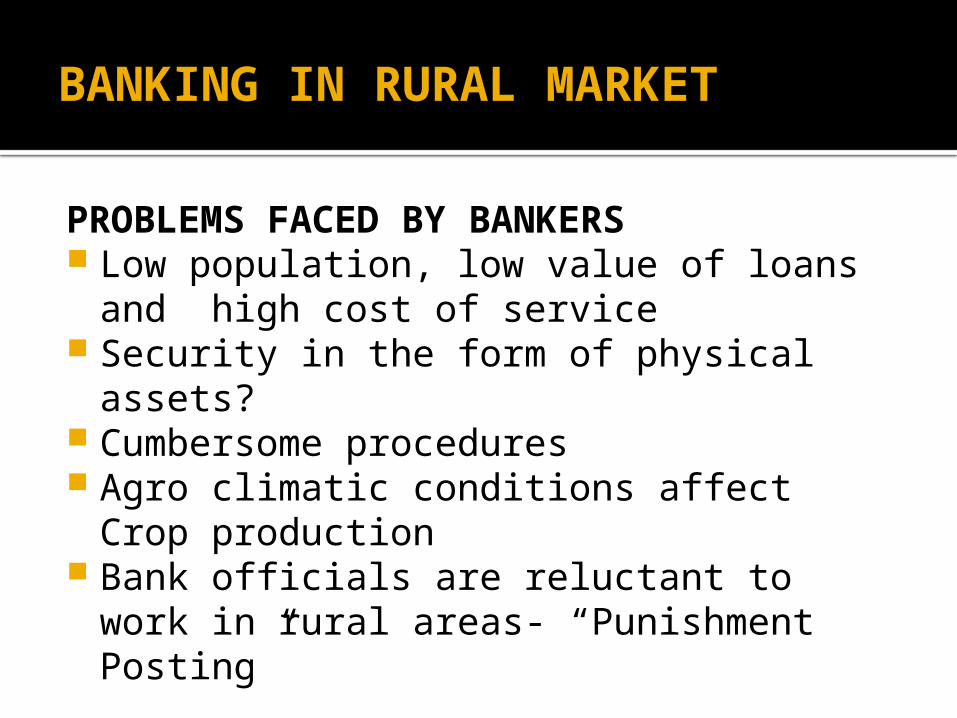

PROBLEMS FACED BY BANKERS Low population, low value of loans and

high cost of service Security in the form of physical assets? Cumbersome procedures Agro climatic conditions affect Crop

production Bank officials are reluctant to work in rural

areas- “Punishment Posting”

BANKING IN RURAL MARKET

SUGGESTIONS Lending at different interest rates based

on credit worthiness and risk profile of borrowers

Kisan credit cards- integrate with ATM Franchise model to increase reach Extend loans to SHG members in all rural

areas Finance distribution channel members Incentives to bank managers