20

AGILITY HEALTH INVESTOR PRESENTATION March 2017

| Date post: | 12-Apr-2017 |

| Category: |

Investor Relations |

| Upload: | agilityhealth |

| View: | 10 times |

| Download: | 0 times |

AGILITY HEALTH

INVESTOR PRESENTATION

March 2017

Safe Harbor

Disclosure

Certain statements contained in this presentation may be considered “forward-looking information”

as defined under applicable Canadian securities laws (“forward-looking statements”). Forward-

looking statements include, but are not limited to, statements made under the heading “Risk

Factors” of the base shelf prospectus of Agility Health, Inc. dated May 29, 2015 and other

statements concerning the objectives of Agility Health, Inc. (“Agility”), strategies to achieve those

objectives, as well as statements with respect to management’s beliefs, plans, estimates, and

intentions, and similar statements concerning anticipated future events, results, circumstances,

performance or expectations that are not historical facts. Forward-looking statements generally can

be identified by the use of forward-looking terminology such as “outlook”, “objective”, “may”, “will”,

“expect”, “intend”, “estimate”, “anticipate”, “believe”, “should”, “plans”, or “continue”, or similar

expressions suggesting future outcomes or events. Such forward-looking statements reflect

management’s current beliefs and are based on information currently available to management.

Forward-looking statements involve risks and uncertainties that could cause actual results to differ

materially from those contemplated by such statements.

No assurance can be given as to any such future results, levels of activity or achievements and

neither Agility nor any other person assumes responsibility for the accuracy and completeness of

any forward-looking statements. The factors underlying current expectations are dynamic and

subject to change. All forward-looking statements in this presentation are qualified by these

cautionary statements. Other than specifically required by applicable laws, Agility is under no

obligation and expressly disclaims any such obligation to update or alter the forward-looking

statements whether as a result of new information, future events or otherwise except as may be

required by law.

All reference to dollars in this presentation are to U.S. dollars, unless otherwise indicated.2

Who We Are

Agility Health, Inc. (“Agility”) is a leading healthcare provider with a focus on

physical rehabilitation services

3

Physical therapy, Occupational therapy,

Athletic training, Speech therapy

Growth in revenues, margins and EBITDA

Large, growing industry - highly fragmented

Differentiated business model

Capitalize on growing demand

Experienced leadership

Physical Therapy Market Overview

4

Physical therapy is a >US$30 billion industry that is expected to grow 7% annually through 2018.

Physical therapy accounts for approximately 90% of all outpatient rehabilitation spending

• Highly fragmented with largest 50 competitors comprising less than 25% of the market

Numerous, positive factors driving long-term growth:

• Expanding patient population that provides favorable tailwinds:

− Aging U.S. population − Unhealthy youth lifestyle trends − Growth in employment

• Outpatient rehabilitation is significantly less costly than surgery or hospitalization, but with similar

clinical effectiveness

U.S. Outpatient Rehabilitation Expenditures Outpatient Rehabilitation Spending by Segment

For the Years Ended and Ending December 31, 2004-2018P($ in billions)

$0

$5

$10

$15

$20

$25

$30

$40

$45

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014P 2015P 2016P 2017P 2018P

Orthopedic Physical Therapy

48%

Speech Therapy and Audiology

10%

GeneralPhysical

Therapy9%

$35

GeriatricPhysical

Therapy 9%

PediatricPhysical

Therapy

8%

Sports physical

Therapy

7%Other Specialty Neurological

Physical Therapy Physical Therapy

3% 6%90%

Source: IBISWorld.

Network of Service Sites 1+ million patient visits annually

1,100+ employees

145+ locations across 20 states

Consolidating highly fragmented

market

Proprietary operating software

Provides post-acute ‘rehabilitation

continuum of care’

Seasoned management team

Diversified portfolio: geographically and clinically

5

One of the leading providers of physical rehabilitation services in North America

Provide care and treatment for orthopedic-related disorders, sports-related injuries,

preventative care and occupational rehabilitation

Agility Health

Physical Rehabilitation Services - Overview

6

Hospital Services

Outsourced Services

Contract Terms: 1-3 Years

Reimbursement: (production or time based)

Physical Therapy (PT), Occupational Therapy (OT),

Speech Pathology (SP), Athletic Training (AT)

Good relationships

Long-Term Care Services

Outsourced Services

Contract Terms: 1-3 Years

Reimbursement: (inpatient services are time-based

and outpatient production-based)

PT, OT, and SP

Many long-term customers

Outpatient Services

Owned or Partnered

Free-standing; leased locations

PT, OT and AT services

Reimbursement: insurance and cash

Industrial Services

Contract Terms: 1-3 Years

Reimbursement: cash from client

AT prevention services

Many long-term customers

Agility Health

Business Segments

Long-Term

Care

Contract Services

Outpatient

Clinics

Hospitals

Contract Services

Industrial

Work-FitTM

7

Clinics/Facilities 56 Sites 31 Sites 36 Sites 25 Sites

LTM Revenue(1) US$31.3 M US$5.6 M US$8.0 M US$17.4 M

% LTM Revenue 50% 9% 13% 28%

1. Clinic level, financials.

Agility Health

Business Segments

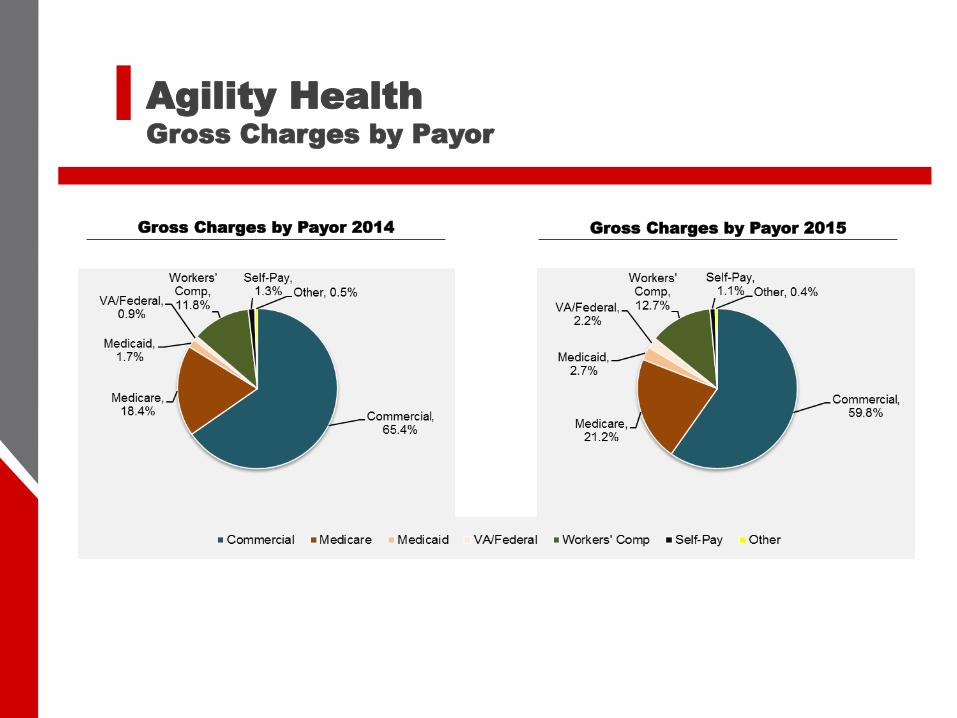

Agility Health

Gross Charges by Payor

Gross Charges by Payor 2015Gross Charges by Payor 2014

Agility Health

Financial Summary ($US)

9

2013 2014 2015 LTM Sept. 30th, 2016(Expressed in USD)Revenue $60,527,877 $62,104,509 $62,328,991 $63,021,546

Outpatient Services $24,511,369 $28,943,806 $31,235,551 $32,296,925% of Total Sales 40.50% 46.60% 50.11% 51.25%Hospital Services $10,562,115 $9,656,009 $8,231,790 $8,028,356% of Total Sales 17.45% 15.55% 13.21% 12.74%Long-Term Care $24,483,526 $18,063,717 $17,246,432 $15,450,388% of Total Sales 40.45% 29.09% 27.67% 24.52%Industrial Services $953,919 $5,416,755 $5,603,376 $7,087,289% of Total Sales 1.58% 8.72% 8.99% 11.25%Administrative $13,292 $22,109 $10,970 $158,588% of Total Sales 0.02% 0.04% 0.02% 0.25%

Cost of RevenuesSalaries and Benefits $41,302,131 $40,837,396 $40,093,117 $41,392,307Contract Labor $1,067,679 $802,113 $1,018,142 $885,340Facility $3,457,499 $3,424,663 $3,895,123 $4,118,466Supplies $798,147 $891,292 $802,671 $808,927Depreciation and Amortization $768,401 $726,829 $692,741 $655,705Provision for Bed Debts $1,077,803 $464,763 $770,408 $932,038Other $1,339,330 $1,424,005 $1,328,860 $1,419,535

Total Cost of Revenues $49,810,990 $48,571,061 $48,601,062 $50,212,318Gross Profit $10,716,887 $13,533,448 $13,727,929 $12,809,228

% of Total Sales 17.71% 21.79% 22.02% 20.33%SG&A $12,571,612 $14,313,511 $11,682,170 $11,789,733

Clinic Level EBITDA $10,531,851 $10,930,394 $12,278,811 $9,660,275

% of Total Sales 17.40% 17.60% 19.70% 15.33%

Outpatient Services $5,036,963 $5,222,542 $5,640,146 $4,950,828

% of Total Sales 47.83% 47.78% 45.93% 51.25%

Hospital Services $2,547,655 $2,532,572 $2,192,750 $2,008,985

% of Total Sales 24.19% 23.17% 17.86% 20.80%

Long-Term Care $2,770,930 $2,221,056 $2,098,817 $1,582,638

% of Total Sales 26.31% 20.32% 17.09% 16.38%

Industrial Services $176,198 $954,114 $943,013 $1,117,824

% of Total Sales 1.67% 8.73% 7.68% 11.57%

Medic Holdings Acquisition

10

February 2017 - acquisition of Medic Holdings by way of

share exchange

Medic 2016 revenues ~ CDN$16 million

EBITDA ~ CDN$1.4 million

Medic becomes wholly-owned subsidiary of Agility -

shareholders of Medic owning (fully-diluted) ~ 20% of Agility

common shares post-transaction

Restructuring of balance sheet underway - improve cash

flow, EPS

Significant expansion of orthotics business unit

Added depth to management team and Board - healthcare,

operations, M&A, capital markets (combined +60 years)

11

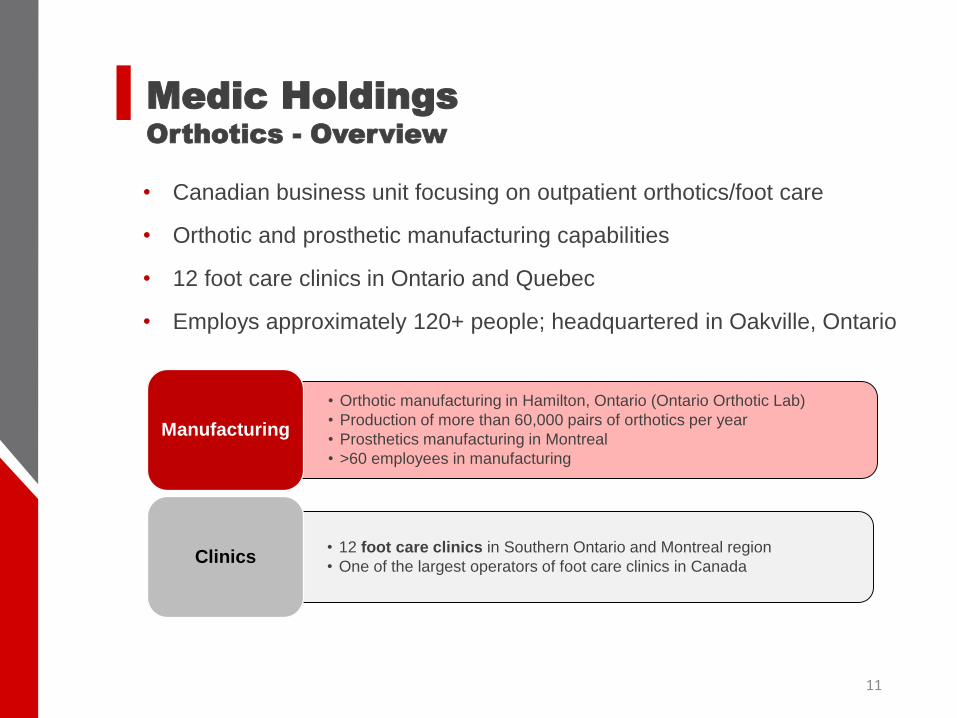

• Canadian business unit focusing on outpatient orthotics/foot care

• Orthotic and prosthetic manufacturing capabilities

• 12 foot care clinics in Ontario and Quebec

• Employs approximately 120+ people; headquartered in Oakville, Ontario

• Orthotic manufacturing in Hamilton, Ontario (Ontario Orthotic Lab)

• Production of more than 60,000 pairs of orthotics per year

• Prosthetics manufacturing in Montreal

• >60 employees in manufacturing

Manufacturing

• 12 foot care clinics in Southern Ontario and Montreal region

• One of the largest operators of foot care clinics in Canada Clinics

Medic Holdings

Orthotics - Overview

12

Ontario Orthotic Lab

• Manufactures arch supports (orthotics)

• 40 plant employees

• ~3,000 pairs of orthotics on back order

Product Offerings:

Custom-manufactured, prescription orthotic

devices for dress, athletic, casual or

diabetic footwear (compatible with Adidas,

Nike, Rockport, Drew, Asics and NAOT)

Wide variety of compression hosiery styles

and brands

Functional electrical stimulation (FES),

prosthetics, T.E.N.S pain management,

home health care and mobility aids

Medic Holdings

Business Segments

Slawner Orthotics

• Leader in field of orthotics and prosthetics

• Over 60 years of service history

• Multiple locations around Montreal; serves

multiple hospitals

Product Offerings:

Comfort shoes

Foot orthotics

Functional electrical stimulation (FES),

compression therapy, T.E.N.S. pain

management, home care and mobility aids

Highlights

13

Broad Diversified Footprint

Expands clinic network into Canada/orthotics

Diversified revenue by state/province, payers and

business line

Reduced reimbursement risk/contract reliance

Strengthened/Expanded Management and Governance

Business development, M&A/financial, capital markets

Scalable leadership/back office teams

Added skills to Board

Capital Market Profile

Increased revenue/EBITDA scale

Positive cash flow impacts from improved balance

sheet

Uplist to TSX: potential US listing

Scalable Growth Platform

Fully-invested back office infrastructure enables M&A

efficiency

Visible, near-term acquisition pipeline

Pipeline impact +50% increase in EBITDA

CDN$96.5M

TTM Revenue

CDN$8.3M

TTM EBITDA

6.7X

EV/TTM EBITDA

164

Clinic Sites US/Canada

Comparable Public Companies *

(Canadian and US w/ Rehabilitation)

14

* All figures in $US

** Prices effective February 17, 2017

Company Name(Exchange: Ticker)

Price **

MarketValue (MM)

Revenue(MM -TTM)

EBITDA(MM -TTM)

EnterpriseValue/

Revenue

EnterpriseValue/EBITDA

US Physical Therapy, Inc.(NYSE: USPH)

$74.65 $927 $352 $60 2.9x 16.9x

Select Medical Holdings Corp.(NYSE: SEM)

$12.70 $1,770 $4,279 $493 1.0x 8.9x

Kindred Healthcare, Inc.(NASDAQ: GTIV)

$7.05 $627 $7,255 $98 0.5x 39.9x

Ensign Group, Inc.(NASDAQ: ENSG)

$18.05 $916 $1,595 $119 0.7x 9.6x

Centric Health Corp.(TSX: CHH)

$0.63 $108 $128.7 $11.3 1.3x 14.6

AverageMedian

-$875$911

$2,730$1,595

$157$98

1.3x1.0x

18.0x14.6x

Agility Health, In.(TSX.V: AHI)

$0.09 $9.9 $63.0 $3.6 0.3x 4.89x

15

Growth Strategy

Same Clinic

Improvements

Expand referral volume,

enhance clinician

efficiencies

Promote cross-selling of

products and services

Move back office functions

from clinics to corporate

Perform staffing

optimization

De Novo Clinic

Expansion

Increase de novo clinic

development over next 5

years

Build market density by

clustering new clinics

New clinician partnerships

New Hospital

Contracts

Secure new hospital

contracts in existing/new

markets

Explore additional

contracts within current

hospital network

New LTC

Contracts

Leverage reputation/scope

to add new customers

Explore new markets

requiring LTC services

Expanded Sales

Platform

Develop and contract

bundled services offerings

(US)

Cross-sell new products

and services across clinic

network

Partner - Agile RPM

Software Services

Expand Work-FitTM

Program

Expand marketing program

to self-insured employers

Outreach program to Third

Party Administrators

Acquisition of existing

industrial clinics

16

Outpatient Rehabilitation is a >US$30 billion industry - Physical Therapy

accounts for approx. 90%

Highly fragmented rehabilitation services with thousands of potential targets

(N. America)

Largest 50 competitors comprise less than 25% of the market

Outpatient rehab is significantly less costly than

surgery/hospitalization – with similar clinical effectiveness

Pursue acquisitions of small rehabilitation clinic chains on margin-accretive

basis

Pursue acquisitions of pain management and foot care clinics

Near-term acquisition pipeline +50% increase in EBITDA

Track record of effectively acquiring and integrating clinic assets

• Agility has previously completed 8 acquisitions with combined

purchase price of US$23 million

• Allowed Agility to enter new service markets and significantly expand

its geographic footprint

Growth through Acquisition

17

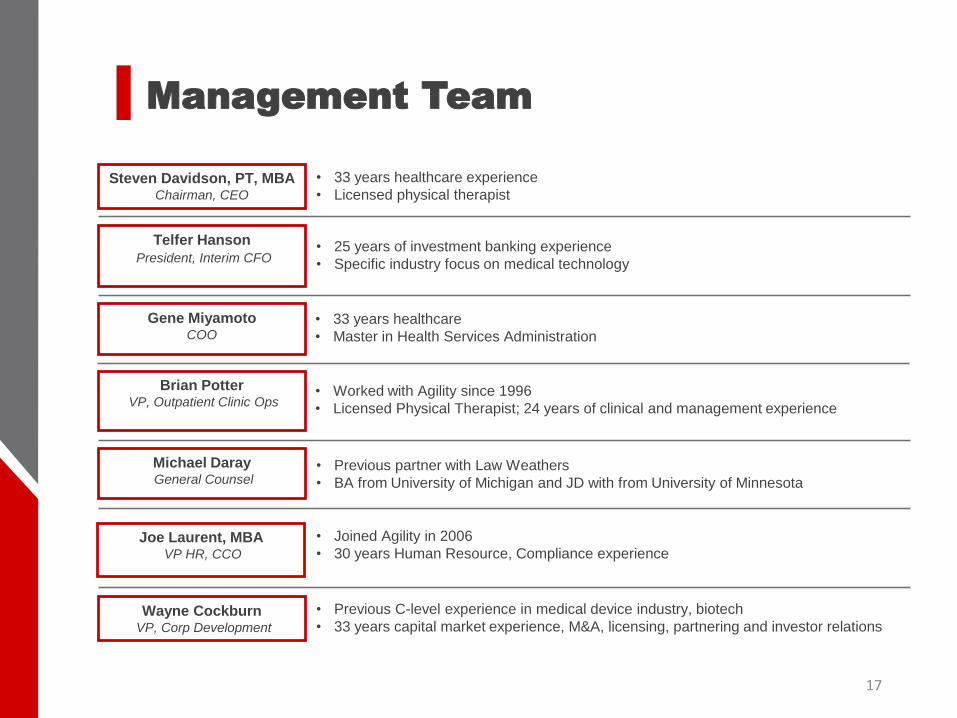

Management Team

Steven Davidson, PT, MBAChairman, CEO

Telfer Hanson

President, Interim CFO

Gene MiyamotoCOO

Brian PotterVP, Outpatient Clinic Ops

Michael DarayGeneral Counsel

Joe Laurent, MBAVP HR, CCO

Wayne CockburnVP, Corp Development

• 33 years healthcare experience

• Licensed physical therapist

• 33 years healthcare

• Master in Health Services Administration

• 25 years of investment banking experience

• Specific industry focus on medical technology

• Worked with Agility since 1996

• Licensed Physical Therapist; 24 years of clinical and management experience

• Previous partner with Law Weathers

• BA from University of Michigan and JD with from University of Minnesota

• Joined Agility in 2006

• 30 years Human Resource, Compliance experience

• Previous C-level experience in medical device industry, biotech

• 33 years capital market experience, M&A, licensing, partnering and investor relations

THANK YOU

For more information, please contact:

Wayne Cockburn

VP, Corporate Development

(905) 505-0770

APPENDIX

Agility Health - Timeline

20

AGILITY HEALTH FOUNDED

KEN SCHOLTEN JOINS AGILITY

(1989)

FOUNDER SELLS AGILITY TO MERCY HEALTH (1985)

STEVE DAVIDSON JOINS AGILITY (1989)

AGILITY FORMS ADVENT JV WITH MERCY HEALTH/ST. MARYS

HEALTH (1996)

S. DAVIDSON & K. SCHOLTEN ACQUIRE AGILITY THROUGH

MANAGEMENT BUYOUT (2003)

ACQUIRED AMATO PT & CONTINUUM (2010)

ACQUIRED BORDER THERAPY, PEAK PERFORMANCE, PANTHER

PT (2011)

RECAP WITH ALARIS (2012)

GO PUBLIC : ACQUIRED WORK-FIT & EXCEL SPORTS AND PT

(2013)

ACQUISITION OF MEDIC HOLDINGS (2017)

1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

![BOX NO PHASE EXTENSIO ACRONYM NUMBER TITLE...THE SF BAY-DELTA: MAIN REPORT, AHI, 8/26/87 [SEE AHI EXHIBIT 302 A] E 1 I A AHI 302 REVISED TABLE 45 FOR AHI EXHIBIT 302 [SUBMITTED ON](https://static.documents.pub/doc/80x56/60d209d0a7804305d0301ab9/box-no-phase-extensio-acronym-number-title-the-sf-bay-delta-main-report-ahi.jpg)