18

Confidential – not for third party distribution © Seabury Group 2015 Air Cargo 2015: Recent trends and impact on air cargo industry More insights, better decisions... 10.Mar.15

Confidential – not for third party distribution © Seabury Group 2015

Air Cargo 2015:

Recent trends and impact on air

cargo industry

More insights, better decisions...

10.Mar.15

1 Confidential – not for third party distribution © Seabury Group 2015

Air cargo back

to growth

What are the drivers

of recent growth?

What was the impact

on the market?

Sustainable growth,

or temporary peak?

Freighters

back to service

What capacity was

added to market?

What if parked

freighters return?

How is it affected by

demand growth?

Drop in

fuel prices

How are costs (and

yields) affected?

How does it affect

freighters vs. belly?

What dynamics to

expect in 2015?

Three things the industry may be thinking about... Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong

market recovery; what is the impact of these changes and what does it mean for 2015?

P

How will these trends fare in 2015?

Text from the program:

Air Cargo 2015: what is the

impact of key recent trends

to the air cargo industry?

Marco Bloemen, Senior Vice

President Seabury Group

A number of factors have

changed the air cargo

landscape in the last nine

months: fuel prices have

halved, consequently air

cargo capacity has been

resilient and market demand

saw a strong Q4 in 2014,

driven from China in

particular. What are the

effects of fuel changes? And,

will freighters that were

deemed uneconomical now

return to the marketplace? Is

the recent pick-up in demand

growth in the fourth quarter

continuing? And what role will

China continue to play as a

catalyst to air cargo growth?

2 Confidential – not for third party distribution © Seabury Group 2015

Air cargo back

to growth

What are the drivers

of recent growth?

What was the impact

on the market?

Sustainable growth,

or temporary peak?

Freighters

back to service

What capacity was

added to market?

What if parked

freighters return?

How is it affected by

demand growth?

Drop in

fuel prices

How are costs (and

yields) affected?

How does it affect

freighters vs. belly?

What dynamics to

expect in 2015?

Three things the industry may be thinking about... Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong

market recovery; what is the impact of these changes and what does it mean for 2015?

P

How will these trends fare in 2015?

3 Confidential – not for third party distribution © Seabury Group 2015

110

80

70

100

90

60

50

Oct-

2014

Jan-

2015

Jul-

2014

Apr-

2014

Jan-

2014

Oct-

2013

Jul-

2013

Apr-

2013

Jan-

2013

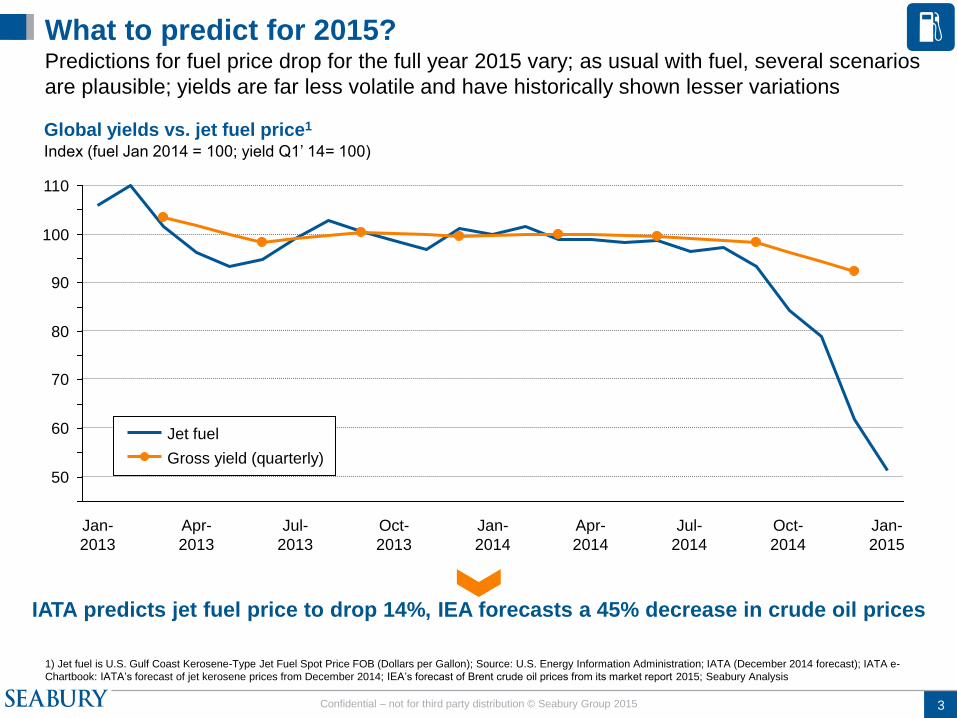

What to predict for 2015? Predictions for fuel price drop for the full year 2015 vary; as usual with fuel, several scenarios

are plausible; yields are far less volatile and have historically shown lesser variations

Global yields vs. jet fuel price1 Index (fuel Jan 2014 = 100; yield Q1’ 14= 100)

1) Jet fuel is U.S. Gulf Coast Kerosene-Type Jet Fuel Spot Price FOB (Dollars per Gallon); Source: U.S. Energy Information Administration; IATA (December 2014 forecast); IATA e-

Chartbook: IATA’s forecast of jet kerosene prices from December 2014; IEA’s forecast of Brent crude oil prices from its market report 2015; Seabury Analysis

IATA predicts jet fuel price to drop 14%, IEA forecasts a 45% decrease in crude oil prices

Jet fuel

Gross yield (quarterly)

4 Confidential – not for third party distribution © Seabury Group 2015

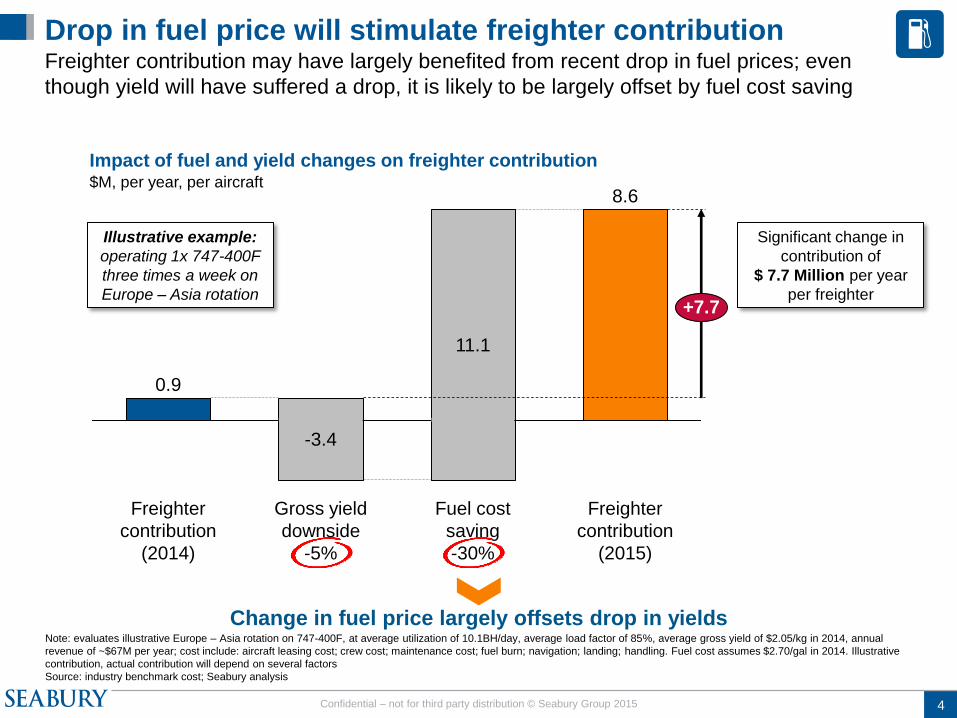

Drop in fuel price will stimulate freighter contribution Freighter contribution may have largely benefited from recent drop in fuel prices; even

though yield will have suffered a drop, it is likely to be largely offset by fuel cost saving

Impact of fuel and yield changes on freighter contribution $M, per year, per aircraft

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual

revenue of ~$67M per year; cost include: aircraft leasing cost; crew cost; maintenance cost; fuel burn; navigation; landing; handling. Fuel cost assumes $2.70/gal in 2014. Illustrative

contribution, actual contribution will depend on several factors

Source: industry benchmark cost; Seabury analysis

Gross yield

downside

-5%

Fuel cost

saving

-30%

+7.7

Freighter

contribution

(2015)

Freighter

contribution

(2014)

-3.4

11.1

0.9

8.6

Illustrative example:

operating 1x 747-400F

three times a week on

Europe – Asia rotation

Significant change in

contribution of

$ 7.7 Million per year

per freighter

Change in fuel price largely offsets drop in yields

If needed, can be

changed in aircraft cost

workbook – Tab

“Scenario”

5 Confidential – not for third party distribution © Seabury Group 2015

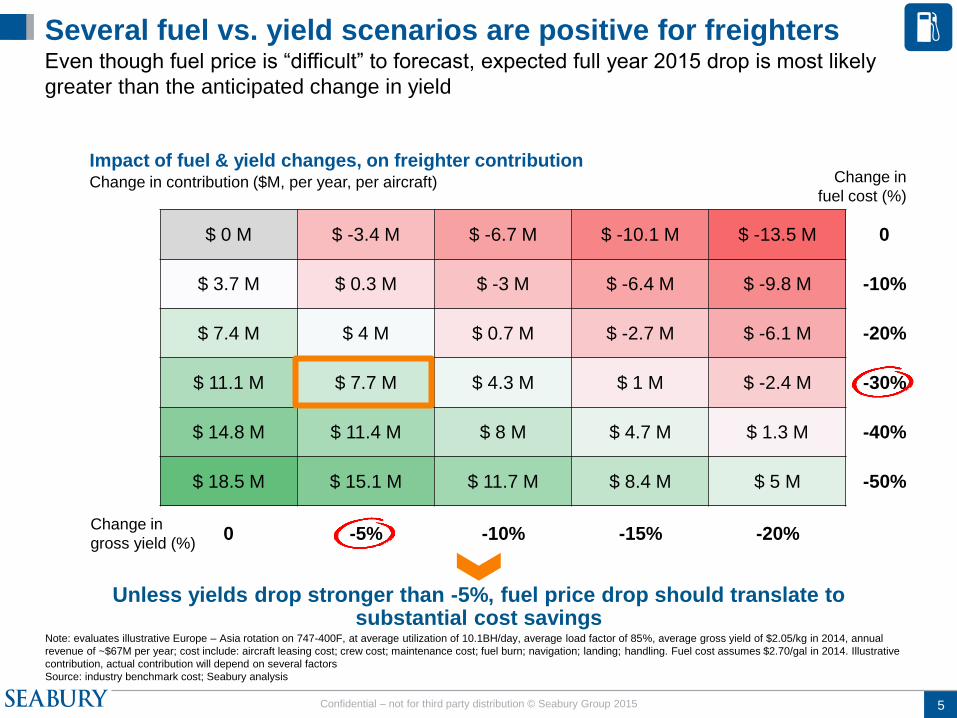

Several fuel vs. yield scenarios are positive for freighters Even though fuel price is “difficult” to forecast, expected full year 2015 drop is most likely

greater than the anticipated change in yield

Impact of fuel & yield changes, on freighter contribution Change in contribution ($M, per year, per aircraft)

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual

revenue of ~$67M per year; cost include: aircraft leasing cost; crew cost; maintenance cost; fuel burn; navigation; landing; handling. Fuel cost assumes $2.70/gal in 2014. Illustrative

contribution, actual contribution will depend on several factors

Source: industry benchmark cost; Seabury analysis

$ 0 M $ -3.4 M $ -6.7 M $ -10.1 M $ -13.5 M

$ 3.7 M $ 0.3 M $ -3 M $ -6.4 M $ -9.8 M

$ 7.4 M $ 4 M $ 0.7 M $ -2.7 M $ -6.1 M

$ 11.1 M $ 7.7 M $ 4.3 M $ 1 M $ -2.4 M

$ 14.8 M $ 11.4 M $ 8 M $ 4.7 M $ 1.3 M

$ 18.5 M $ 15.1 M $ 11.7 M $ 8.4 M $ 5 M

0

-10%

-20%

-30%

-40%

-50%

0 -5% -10% -15% -20%

Change in

fuel cost (%)

Change in

gross yield (%)

Unless yields drop stronger than -5%, fuel price drop should translate to substantial cost savings

Can be changed in

aircraft cost workbook

– Tab “Matrix”

Change tagline

6 Confidential – not for third party distribution © Seabury Group 2015

Belly contribution is substantially larger than contribution in freighter operations, in part due

to a significantly lower fuel cost component

Change in incremental belly contribution USD/kg

Change in freighter contribution USD/kg

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual

revenue of ~$67M per year; Using ACMI cost (aircraft leasing-; crew-; maintenance- and insurance cost), fuel burn and other Direct Operating Cost (navigation-; landing- and handling

cost). Fuel cost assumes $2.70/gal in 2014. Illustrative contribution, actual contribution will depend on several factors. Source: industry benchmark cost; Seabury analysis

Other DOC

Fuel (incremental)

Contribution

2015 scenario

1.95

8%

1.30

(67%)

2014 average

2.05

12%

1.33

(65%)

Average yield 1%

Contribution

1.95

40%

13%

2.05

55%

Fuel cost

Other DOC

ACMI

2015 scenario 2014 average

2015 scenario assumes:

-5% on yields

-30% on fuel cost

Recent fuel price drops generates much more contribution for freighters, compared to belly operators

Can be changed in

aircraft cost workbook

Tab “Belly”

Fuel impact is more positive for freighters than for bellies Change tagline;

original:

Fuel is a significant share of freighter

operations cost (~50-55%)and creates

significant upside in case of drop in prices

– more so than for belly

7 Confidential – not for third party distribution © Seabury Group 2015

Air cargo back

to growth

What are the drivers

of recent growth?

What was the impact

on the market?

Sustainable growth,

or temporary peak?

Freighters

back to service

What capacity was

added to market?

What if parked

freighters return?

How is it affected by

demand growth?

Drop in

fuel prices

How are costs (and

yields) affected?

How does it affect

freighters vs. belly?

What dynamics to

expect in 2015?

Three things the industry may be thinking about... Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong

market recovery; what is the impact of these changes and what does it mean for 2015?

How will these trends fare in 2015?

P

8 Confidential – not for third party distribution © Seabury Group 2015

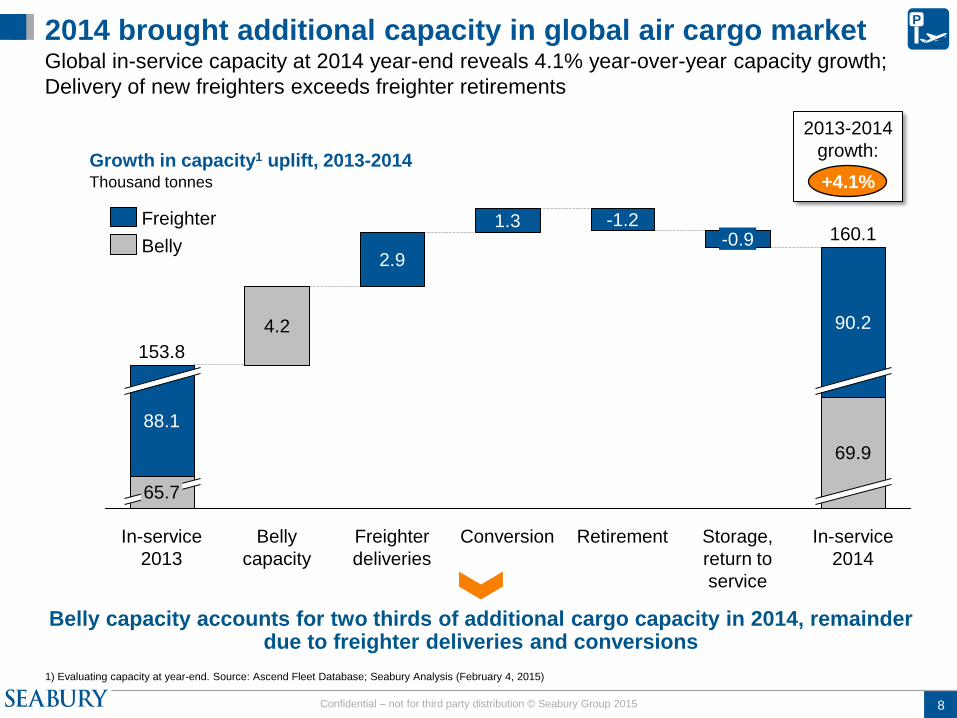

Growth in capacity1 uplift, 2013-2014

2014 brought additional capacity in global air cargo market Global in-service capacity at 2014 year-end reveals 4.1% year-over-year capacity growth;

Delivery of new freighters exceeds freighter retirements

Thousand tonnes

1) Evaluating capacity at year-end. Source: Ascend Fleet Database; Seabury Analysis (February 4, 2015)

2013-2014

growth:

+4.1%

P

Belly capacity accounts for two thirds of additional cargo capacity in 2014, remainder due to freighter deliveries and conversions

90.2

69.9

-0.9 160.1

2.9

Belly

capacity

4.2

Freighter

deliveries

1.3

Conversion In-service

2014

Storage,

return to

service

88.1

65.7

153.8

In-service

2013

-1.2

Retirement

Belly

Freighter

IATA: Market AFTK YoY

2014-2013: 4.2%

(international, NB+WB)

9 Confidential – not for third party distribution © Seabury Group 2015

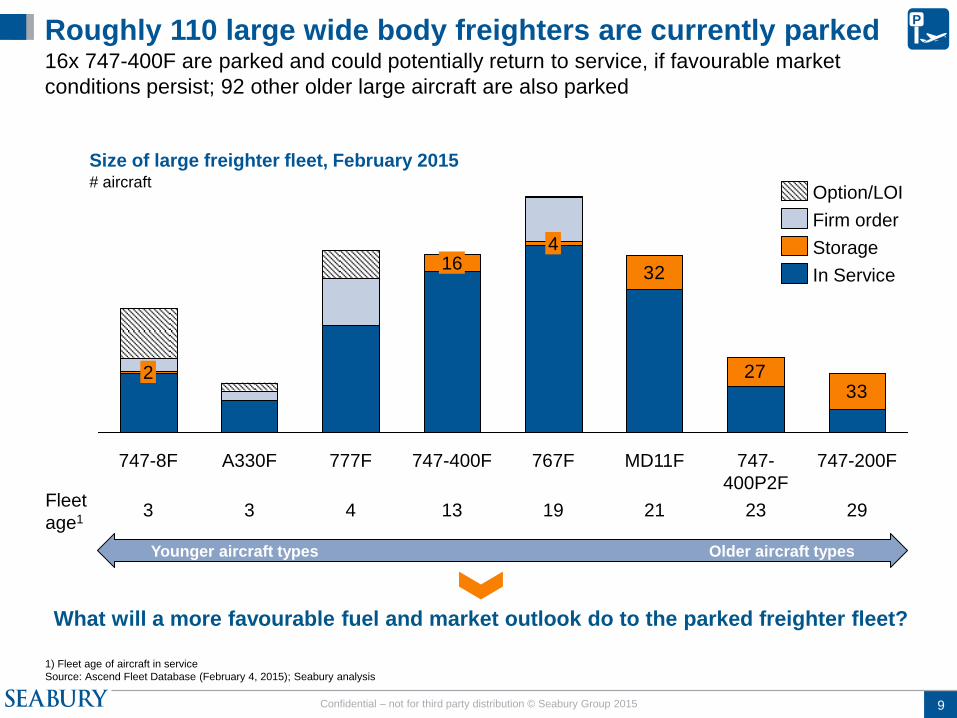

Roughly 110 large wide body freighters are currently parked 16x 747-400F are parked and could potentially return to service, if favourable market

conditions persist; 92 other older large aircraft are also parked

Size of large freighter fleet, February 2015 # aircraft

1) Fleet age of aircraft in service

Source: Ascend Fleet Database (February 4, 2015); Seabury analysis

3327

32

747-200F 747-

400P2F

MD11F 767F

4

747-400F

16

777F A330F 747-8F

2

What will a more favourable fuel and market outlook do to the parked freighter fleet?

In Service

Storage

Firm order

Option/LOI

Fleet

age1 3 3 4 13 21 29 19 23

P

Using figures from

David’s slide

(Freighters are sticky)

Younger aircraft types Older aircraft types

Owners 2x 747-8:

Operator Cargolux Boeing

AircraftManufacturer Boeing Boeing

AircraftType 747 747

AircraftSeries 8 8

AircraftVariant 8F (GE) 8F (GE)

Registration LX-VCC N770BA

SerialNumber 35807 37564

BuildYear 2010 2013

StorageLocation

Luxembourg -

Findel,

Luxembourg

Marana - Pinal

Airpark, AZ, USA

OriginalOperator Cargolux

NextOperator

ExpectedLeaseSaleDate

SaleOrLease

Manager Cargolux Boeing

Owner VCC Lease Sarl Boeing

EngineType GEnx GEnx

EngineVariant 2B67 2B67

AircraftAge 5 2

OrderDate 38671

DeliveryDate 40991

AircraftUsage Freight / Cargo Freight / Cargo

AircraftUsage2

MinorVariant 8R7F 87UF

NoiseCategory

FAA FAR Part 36

Stage 3/ICAO

Annex 16 Vol.1

Chapter 3

FAA FAR Part 36

Stage 3/ICAO Annex

16 Vol.1 Chapter 3

StorageDate 41975 41821

StoragePeriod(Years) 0.25 0.67

10 Confidential – not for third party distribution © Seabury Group 2015

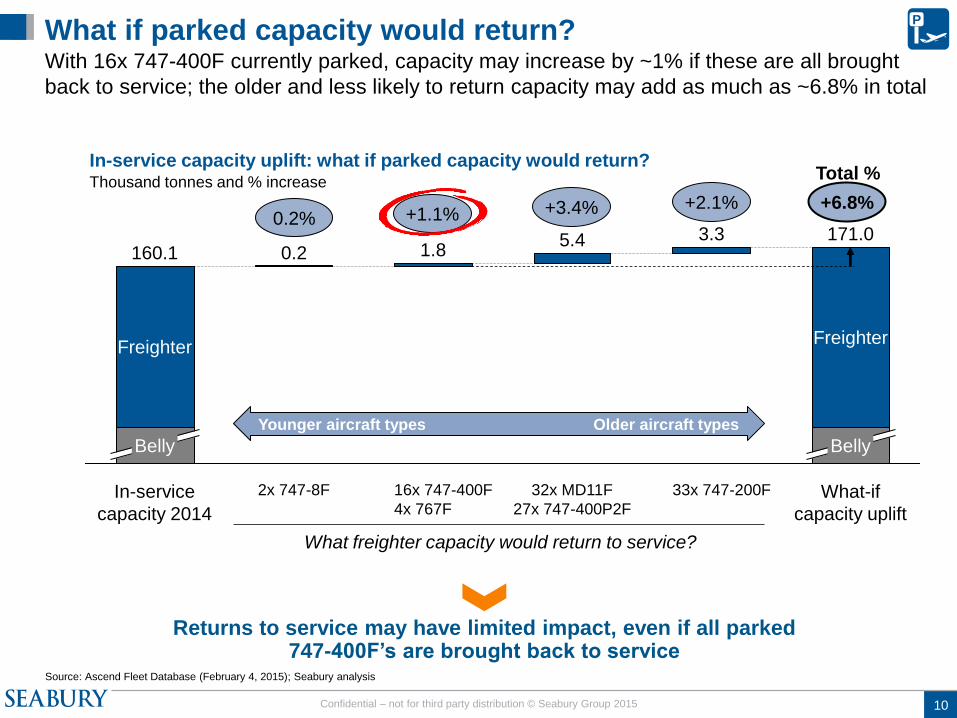

What if parked capacity would return? With 16x 747-400F currently parked, capacity may increase by ~1% if these are all brought

back to service; the older and less likely to return capacity may add as much as ~6.8% in total

In-service capacity uplift: what if parked capacity would return? Thousand tonnes and % increase

Source: Ascend Fleet Database (February 4, 2015); Seabury analysis

What-if

capacity uplift

171.0

Belly

Freighter

33x 747-200F

3.3

32x MD11F

27x 747-400P2F

5.4

16x 747-400F

4x 767F

1.8

2x 747-8F

0.2

In-service

capacity 2014

160.1

Belly

Freighter

+1.1%

What freighter capacity would return to service?

+3.4% +2.1%

P

0.2%

Returns to service may have limited impact, even if all parked 747-400F’s are brought back to service

+6.8%

Younger aircraft types Older aircraft types

Total %

Ascend data workbook

Tab:

ParkedCapacity-ByType

2015-2014 Jan-Aug Belly

growth YoY: 5.6% or

1,247,429 tonnes; from

(cap.leg database - planned

belly)

Add one decimal in graph

(otherwise 1+3+2=7)

11 Confidential – not for third party distribution © Seabury Group 2015

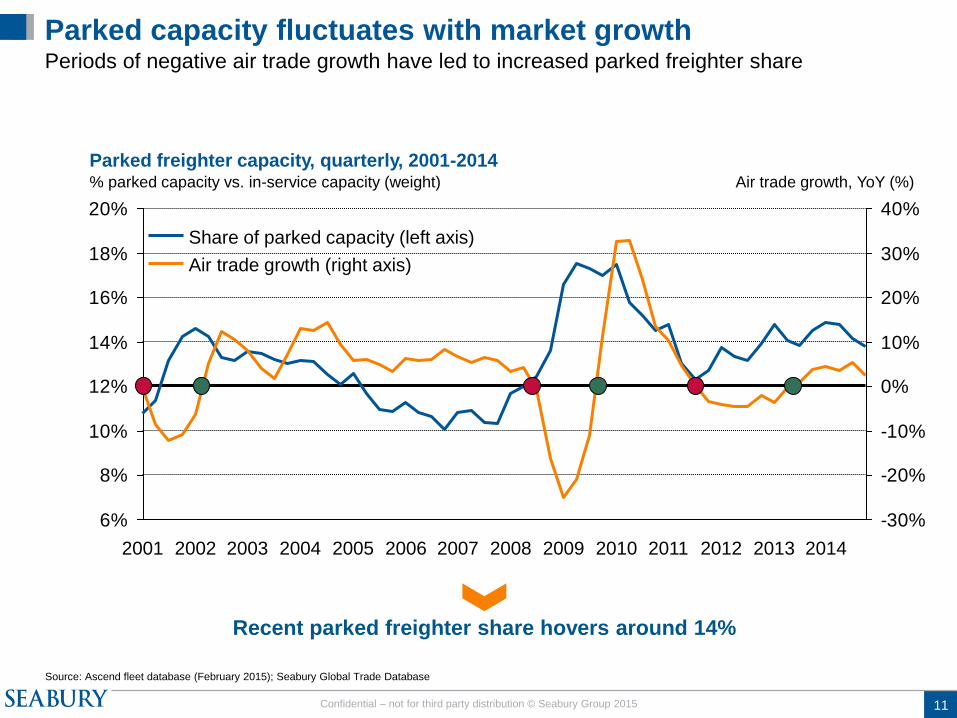

Parked capacity fluctuates with market growth Periods of negative air trade growth have led to increased parked freighter share

Parked freighter capacity, quarterly, 2001-2014 % parked capacity vs. in-service capacity (weight)

Source: Ascend fleet database (February 2015); Seabury Global Trade Database

6%

8%

10%

12%

14%

16%

18%

20%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2010 2009 2008 2011 2013 2012 2014 2001 2006 2005 2007 2004 2002 2003

Share of parked capacity (left axis)

Air trade growth (right axis)

Air trade growth, YoY (%)

Recent parked freighter share hovers around 14%

Tab:

ParkedCapacity-LongerHistory

2014 parked capacity

increase during air trade

growth: belly?

Red-green: increase in

parked freighters

Green-red: decrease in

parked freighters

12 Confidential – not for third party distribution © Seabury Group 2015

Drop in

fuel prices

How are costs (and

yields) affected?

How does it affect

freighters vs. belly?

What dynamics to

expect in 2015?

Three things the industry may be thinking about... Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong

market recovery; what is the impact of these changes and what does it mean for 2015?

How will these trends fare in 2015?

Air cargo back

to growth

What are the drivers

of recent growth?

What was the impact

on the market?

Sustainable growth,

or temporary peak?

Freighters

back to service

What capacity was

added to market?

What if parked

freighters return?

How is it affected by

demand growth?

P

13 Confidential – not for third party distribution © Seabury Group 2015

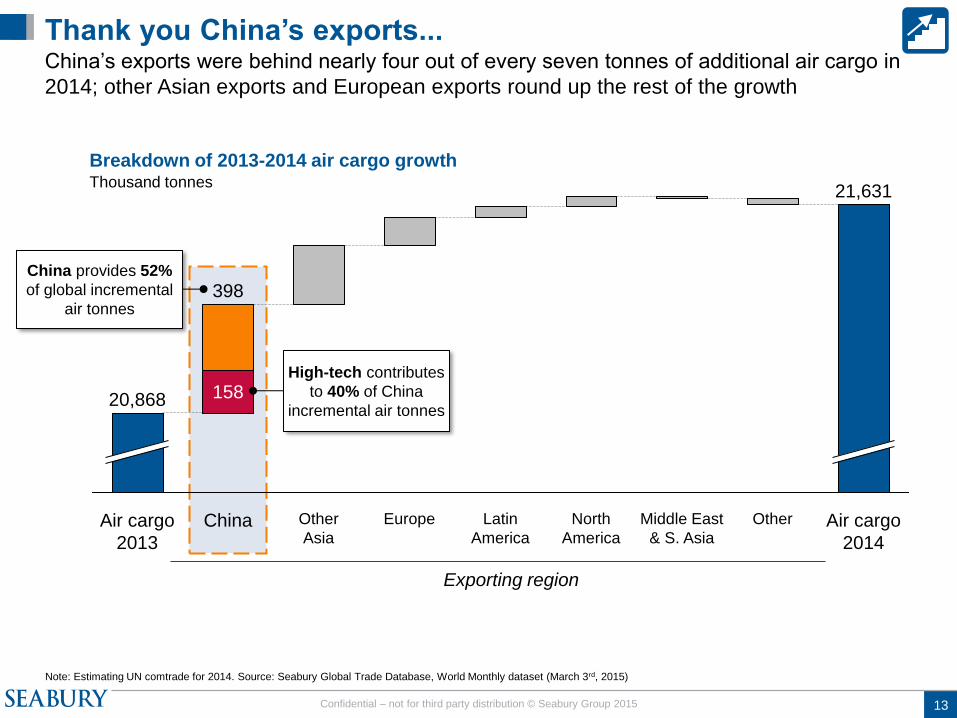

Thank you China’s exports... China’s exports were behind nearly four out of every seven tonnes of additional air cargo in

2014; other Asian exports and European exports round up the rest of the growth

Breakdown of 2013-2014 air cargo growth Thousand tonnes

Note: Estimating UN comtrade for 2014. Source: Seabury Global Trade Database, World Monthly dataset (March 3rd, 2015)

Middle East

& S. Asia

21,631

Europe

158

Air cargo

2013

China Air cargo

2014

398

Other Latin

America

North

America

20,868

Other

Asia

Exporting region

Updated with 2014

full year

- Increment of

UN comtrade

estimated

High-tech contributes

to 40% of China

incremental air tonnes

China provides 52%

of global incremental

air tonnes

Take out numbers of

other regions except

China and totals for

2013 and 2014

14 Confidential – not for third party distribution © Seabury Group 2015

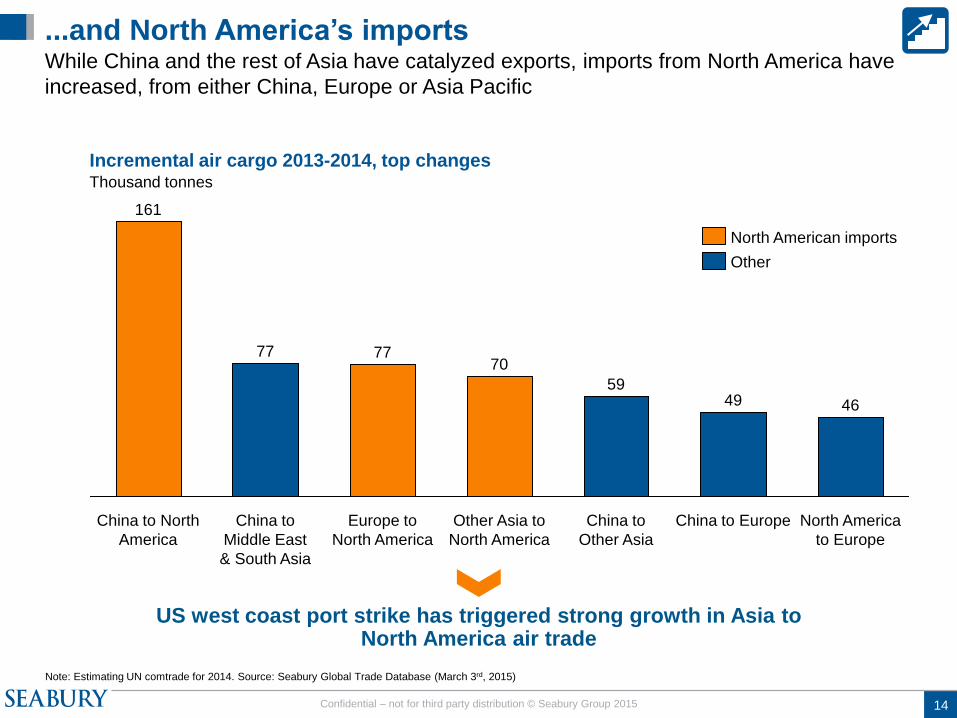

...and North America’s imports While China and the rest of Asia have catalyzed exports, imports from North America have

increased, from either China, Europe or Asia Pacific

Incremental air cargo 2013-2014, top changes Thousand tonnes

Note: Estimating UN comtrade for 2014. Source: Seabury Global Trade Database (March 3rd, 2015)

Europe to

North America

77

China to

Middle East

& South Asia

77

China to North

America

161

North America

to Europe

46

China to Europe

49

China to

Other Asia

59

Other Asia to

North America

70

North American imports

Other

Update with

2014 full year

US west coast port strike has triggered strong growth in Asia to North America air trade

15 Confidential – not for third party distribution © Seabury Group 2015

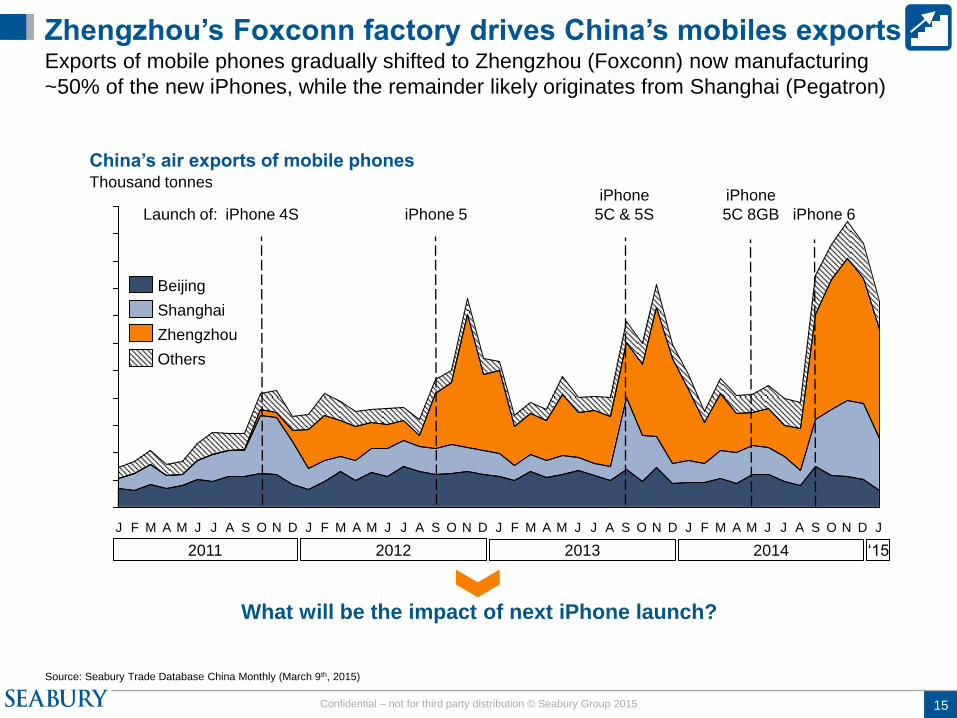

Zhengzhou’s Foxconn factory drives China’s mobiles exports Exports of mobile phones gradually shifted to Zhengzhou (Foxconn) now manufacturing

~50% of the new iPhones, while the remainder likely originates from Shanghai (Pegatron)

China’s air exports of mobile phones Thousand tonnes

Source: Seabury Trade Database China Monthly (March 9th, 2015)

J A M M F J D N O S A J J M O A S J J D N A M F J D N O S A J J M A M F J D N O S A J J M A M F J

2011 2012 2013 2014

iPhone 5

iPhone

5C & 5S

Others

Shanghai

Zhengzhou

Beijing

What will be the impact of next iPhone launch?

iPhone 4S

iPhone

5C 8GB Launch of: iPhone 6

‘15

16 Confidential – not for third party distribution © Seabury Group 2015

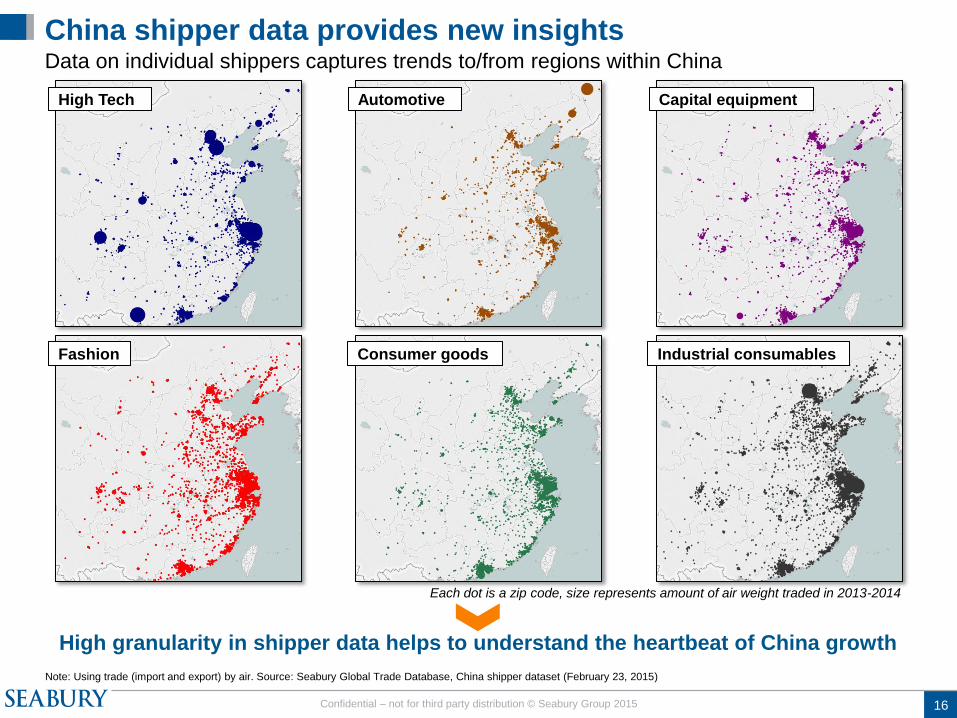

Fashion

Each dot is a zip code, size represents amount of air weight traded in 2013-2014

High Tech

Consumer goods

Automotive Capital equipment

Industrial consumables

China shipper data provides new insights Data on individual shippers captures trends to/from regions within China

Note: Using trade (import and export) by air. Source: Seabury Global Trade Database, China shipper dataset (February 23, 2015)

High granularity in shipper data helps to understand the heartbeat of China growth

- High-tech: Most

concentrated, but giant

- Automotive: very much

concentrated, especially

north

- CapEq: Still consolidated,

but not bubble sizes of high-

tech

- Fashion: fragmented,

focused especially along

coastal area

- Consumer goods similar to

fashion, slightly less

fragmented

- Industrial consumables;

quite spread out, with two

main concentration points:

Shanghai & Beijing

17 Confidential – not for third party distribution © Seabury Group 2015

Air cargo back

to growth

What are the drivers

of recent growth?

What was the impact

on the market?

Sustainable growth,

or temporary peak?

Freighters

back to service

What capacity was

added to market?

What if parked

freighters return?

How is it affected by

demand growth?

Drop in

fuel prices

How are costs (and

yields) affected?

How does it affect

freighters vs. belly?

What dynamics to

expect in 2015?

Three things the industry may be thinking about... Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong

market recovery; what is the impact of these changes and what does it mean for 2015?

P