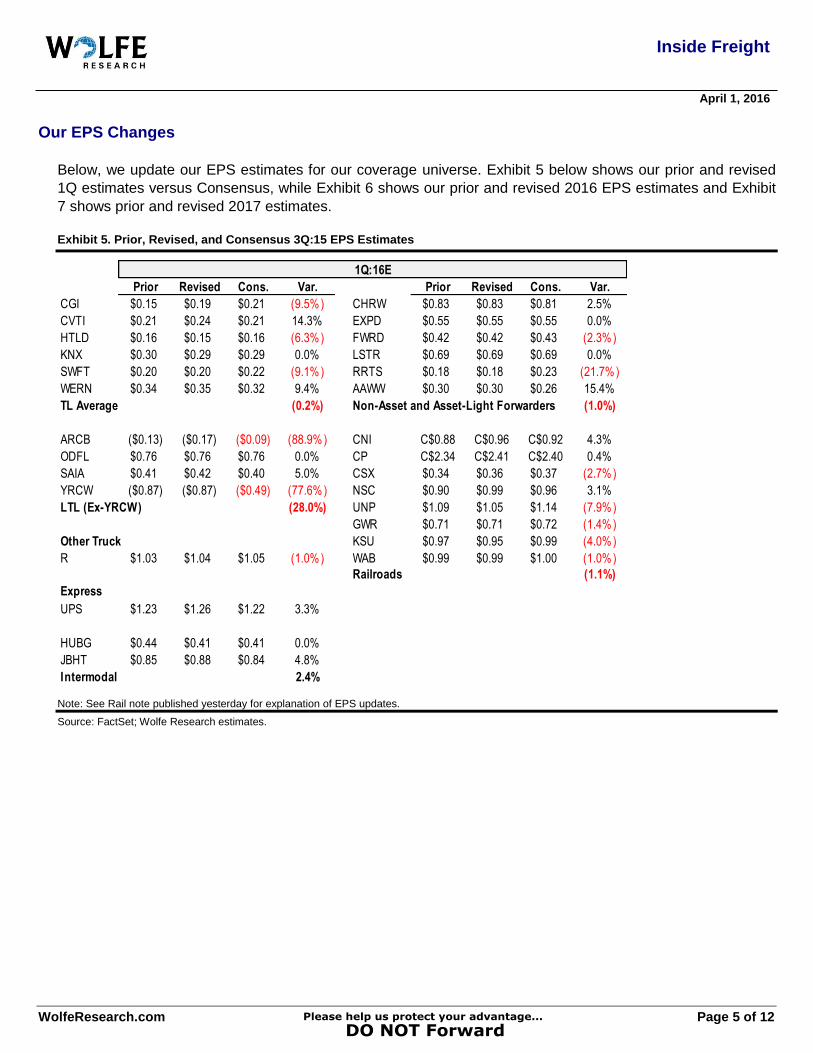

DO NOT FORWARD – DO NOT DISTRIBUTE – DOCUMENT CAN ONLY BE PRINTED TWICE This report is limited solely for the use of clients of Wolfe Research. Please refer to the DISCLOSURE SECTION located at the end of this report for Analyst Certifications and Other Disclosures. For Important Disclosures, please go to www.WolfeResearch.com/Disclosures or write to us at Wolfe Research, LLC, 420 Lexington Avenue, Suite 648, New York, NY 10170. WolfeResearch.com Page 1 of 12 April 1, 2016 INSIDE FREIGHT Transport 1Q Earnings Preview: Cautious Positioning Transports Ahead of 1Q Earnings. Our WR Transport index has surged more than 25% the past ~2 months and has outperformed the S&P 500 by more than 1,500bp over this period. While recession fears have faded, we don’t expect 1Q earnings season will be a catalyst for many upward EPS revisions. So valuations have expanded, and we think commentary on March/April freight demand could be disappointing… so we’re mostly cautious on the transports heading into earnings season. Some Puts and Takes in 1Q. Transport EPS should benefit in 1Q from mild weather, an extra operating day and an early Easter. However, asset- based transports face tough fuel comps, continued muted demand, and likely slower pricing for the TLs. Declines in TL spot rates and ocean spot rates have moderated slightly, so gross yield expansion for the brokers/forwarders could also slow a bit. See the list on the right for our expectations of beats and misses in 1Q – we’re now most above 1Q Cons. for AAWW, CVTI and WERN and most below for ARCB and YRCW. Is Freight Improving? We saw solid improvement in y/y Rail, Truck, Ocean and Air vols in Jan. and Feb. into a combination of easy comps (West Coast port issues last year) and mild weather. However, rail vols deteriorated meaningfully in March, and our channel checks with private truckers and ports suggest a similar softening into much tougher comps. How About Pricing? We continue to expect Rail pricing to hold up best this year, followed by LTL pricing, and see the most risk to TL pricing ahead. We also expect the Rails and LTLs to benefit more from any potential improvement in industrial and export end-markets ahead following recent commodity strength and dollar weakness. Lowering Ratings on CHRW and SWFT; Raising Target Price on JBHT. In separate notes today, we have lowered our ratings on CHRW and SWFT, both from Outperform to Peer Perform as both closed at or above our prior target prices. Meanwhile, we’ve raised our target price and reiterate our Outperform rating on JBHT which is seeing uniquely strong volume growth among the transports which we think deserves a higher valuation. Small List of Transport Stocks to Own. We recommend staying disciplined in transports, and now have a pretty small list of Outperform- rated stocks. Rails remain our favorite transport sub-sector, and our favorite stocks are NSC, CP, GWR, R and JBHT. On the other side, our best Underperform ideas are HTLD, CMI and PCAR. AIRFREIGHT & SURFACE TRANSPORTATION Airfreight & Logistics – Market Weight Railroads – Market Overweight Trucking – Market Weight Truck Machinery – Market Underweight ` Source: FactSet; Wolfe Research Scott H. Group (646) 845-0721 [email protected]Ivan Yi (646) 845-0724 [email protected]Vanck Zhu (646) 845-0725 [email protected]Christian Theodoropoulos (646) 845-0726 [email protected]1Q EPS Wolfe Cons. Var. BEATS AAWW $0.30 $0.26 15% CVTI $0.24 $0.21 14% WERN $0.35 $0.32 9% SAIA $0.42 $0.40 5% JBHT $0.88 $0.84 5% CNI $0.96 $0.92 4% UPS $1.26 $1.22 3% NSC $0.99 $0.96 3% CHRW $0.83 $0.81 2% IN LINE CP $2.41 $2.40 0% KNX $0.29 $0.29 0% ODFL $0.76 $0.76 0% HUBG $0.41 $0.41 0% EXPD $0.55 $0.55 0% LSTR $0.69 $0.69 0% WAB $0.99 $1.00 (1%) GWR $0.71 $0.72 (1%) R $1.04 $1.05 (1%) MISSES FWRD $0.42 $0.43 (2%) CSX $0.36 $0.37 (3%) KSU $0.95 $0.99 (4%) HTLD $0.15 $0.16 (6%) UNP $1.05 $1.14 (8%) SWFT $0.20 $0.22 (9%) CGI $0.19 $0.21 (10%) RRTS $0.18 $0.23 (22%) YRCW ($0.87) ($0.49) (78%) ARCB ($0.17) ($0.09) (89%)

Transcript

DO NOT FORWARD – DO NOT DISTRIBUTE – DOCUMENT CAN ONLY BE PRINTED TWICE This report is limited solely for the use of clients of Wolfe Research. Please refer to the DISCLOSURE SECTION located at the end of this report for Analyst Certifications and Other Disclosures. For Important Disclosures, please go to www.WolfeResearch.com/Disclosures or write to us at Wolfe Research, LLC, 420 Lexington Avenue, Suite 648, New York, NY 10170.

WolfeResearch.com Page 1 of 12

April 1, 2016

INSIDE FREIGHT

Transport 1Q Earnings Preview: Cautious

Positioning Transports Ahead of 1Q Earnings. Our WR Transport index has surged more than 25% the past ~2 months and has outperformed the S&P 500 by more than 1,500bp over this period. While recession fears have faded, we don’t expect 1Q earnings season will be a catalyst for many upward EPS revisions. So valuations have expanded, and we think commentary on March/April freight demand could be disappointing… so we’re mostly cautious on the transports heading into earnings season.

Some Puts and Takes in 1Q. Transport EPS should benefit in 1Q from mild weather, an extra operating day and an early Easter. However, asset-based transports face tough fuel comps, continued muted demand, and likely slower pricing for the TLs. Declines in TL spot rates and ocean spot rates have moderated slightly, so gross yield expansion for the brokers/forwarders could also slow a bit. See the list on the right for our expectations of beats and misses in 1Q – we’re now most above 1Q Cons. for AAWW, CVTI and WERN and most below for ARCB and YRCW.

Is Freight Improving? We saw solid improvement in y/y Rail, Truck, Ocean and Air vols in Jan. and Feb. into a combination of easy comps (West Coast port issues last year) and mild weather. However, rail vols deteriorated meaningfully in March, and our channel checks with private truckers and ports suggest a similar softening into much tougher comps.

How About Pricing? We continue to expect Rail pricing to hold up best this year, followed by LTL pricing, and see the most risk to TL pricing ahead. We also expect the Rails and LTLs to benefit more from any potential improvement in industrial and export end-markets ahead following recent commodity strength and dollar weakness.

Lowering Ratings on CHRW and SWFT; Raising Target Price on JBHT. In separate notes today, we have lowered our ratings on CHRW and SWFT, both from Outperform to Peer Perform as both closed at or above our prior target prices. Meanwhile, we’ve raised our target price and reiterate our Outperform rating on JBHT which is seeing uniquely strong volume growth among the transports which we think deserves a higher valuation.

Small List of Transport Stocks to Own. We recommend staying disciplined in transports, and now have a pretty small list of Outperform-rated stocks. Rails remain our favorite transport sub-sector, and our favorite stocks are NSC, CP, GWR, R and JBHT. On the other side, our best Underperform ideas are HTLD, CMI and PCAR.

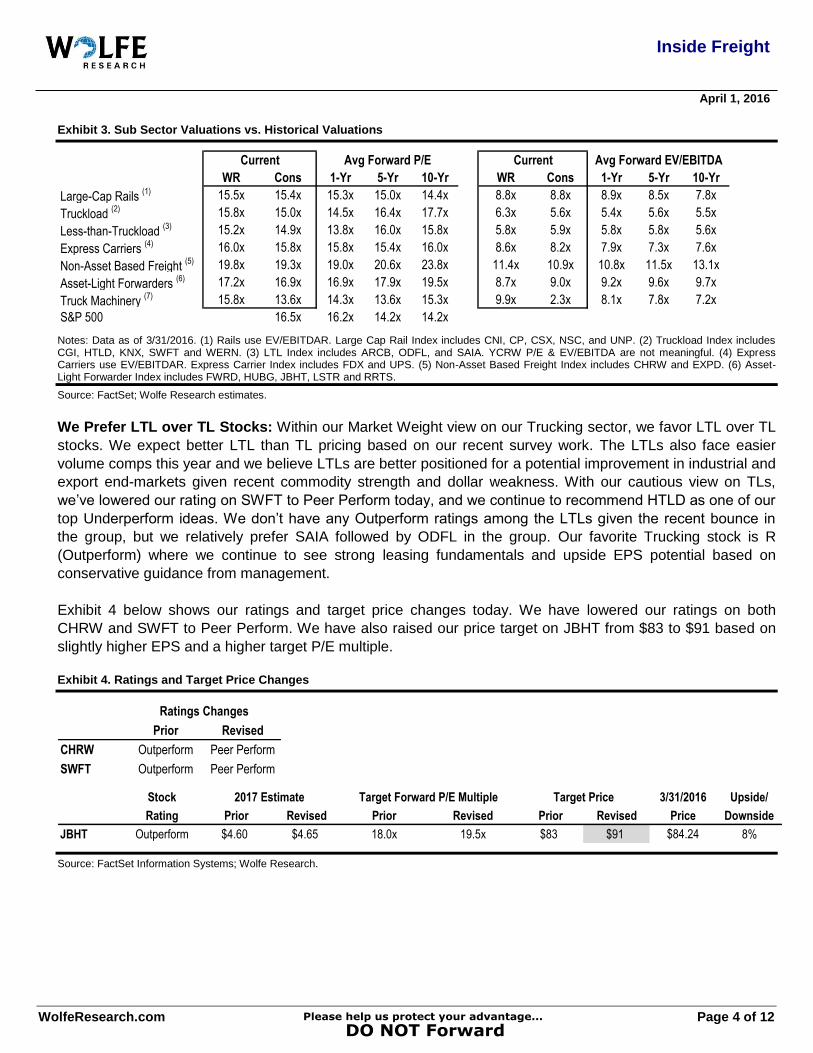

Exhibit 3. Sub Sector Valuations vs. Historical Valuations

Notes: Data as of 3/31/2016. (1) Rails use EV/EBITDAR. Large Cap Rail Index includes CNI, CP, CSX, NSC, and UNP. (2) Truckload Index includes CGI, HTLD, KNX, SWFT and WERN. (3) LTL Index includes ARCB, ODFL, and SAIA. YCRW P/E & EV/EBITDA are not meaningful. (4) Express Carriers use EV/EBITDAR. Express Carrier Index includes FDX and UPS. (5) Non-Asset Based Freight Index includes CHRW and EXPD. (6) Asset-Light Forwarder Index includes FWRD, HUBG, JBHT, LSTR and RRTS.

Source: FactSet; Wolfe Research estimates.

We Prefer LTL over TL Stocks: Within our Market Weight view on our Trucking sector, we favor LTL over TL

stocks. We expect better LTL than TL pricing based on our recent survey work. The LTLs also face easier

volume comps this year and we believe LTLs are better positioned for a potential improvement in industrial and

export end-markets given recent commodity strength and dollar weakness. With our cautious view on TLs,

we’ve lowered our rating on SWFT to Peer Perform today, and we continue to recommend HTLD as one of our

top Underperform ideas. We don’t have any Outperform ratings among the LTLs given the recent bounce in

the group, but we relatively prefer SAIA followed by ODFL in the group. Our favorite Trucking stock is R

(Outperform) where we continue to see strong leasing fundamentals and upside EPS potential based on

conservative guidance from management.

Exhibit 4 below shows our ratings and target price changes today. We have lowered our ratings on both

CHRW and SWFT to Peer Perform. We have also raised our price target on JBHT from $83 to $91 based on

slightly higher EPS and a higher target P/E multiple.

Exhibit 4. Ratings and Target Price Changes

Source: FactSet Information Systems; Wolfe Research.

Current Avg Forward P/E Current Avg Forward EV/EBITDA

R $6.05 $6.05 $6.51 (7.1%) WAB $4.85 $4.85 $4.58 5.9%

Railroads (1.1%)

FDX $11.65 $11.65 $12.13 (4.0%)

UPS $6.00 $6.00 $6.24 (3.8%)

Express (3.9%)

HUBG $2.30 $2.30 $2.43 (5.3%)

JBHT $4.60 $4.65 $4.53 2.6%

Intermodal (1.4%)

Inside Freight

April 1, 2016

WolfeResearch.com Page 8 of 12

Exhibit 8. Y/Y Transport Volume Growth by Mode

Source: Cass Information Systems, Inc.; American Trucking Associations; Association of American Railroads; Airlines for America; International Air Transport Association; Port of Los Angeles, Port of Long Beach; Port of Oakland; Bureau of Economic Analysis; Wolfe Research.

Exhibit 9. 2-Year Stacked Transport Volume Growth by Mode

Source: Cass Information Systems, Inc.; American Trucking Associations; Association of American Railroads; Airlines for America; International Air Transport Association; Port of Los Angeles, Port of Long Beach; Port of Oakland; Bureau of Economic Analysis; Wolfe Research.

Cass ATA Class I Domestic Int'l Air Combined IANA

Shipment Truck Rail Air Cargo Cargo Tonne WC Port Domestic Freight

Index Tonnage Volumes Ton Miles Kilometers Volumes Containers Average

TL and LTL Comps. The two exhibits below highlight our expectations for margins, yield growth and

volume growth for TLs and LTLs in 1Q. We expect to see a deceleration in TL pricing gains, but see

potential for utilization declines to moderate. On the LTL side, we expect strong pricing gains with mix

benefits from falling weight/shipment, and moderating tonnage declines.

Exhibit 10. TL Y/Y OR Improvement (Deterioration), Yields Net of Fuel, and Utilization (Loaded Miles/Truck)

Note: (1) Figures for CGI represent Wolfe calendar estimates as CGI ‘s fiscal year ends in June. (2) CNW TL’s segment is included until.3Q:15 (3) HTLD does provide data for yield or utilization. (4) Utilization and yield figures for JBHT represent Truckload only; OR improvement represents Truckload and Dedicated combined.

Average (3.0%) 0.8% 1.5% 1.5% 0.1% (3.3%) (4.7%) (5.9%) (3.8%)

Inside Freight

April 1, 2016

WolfeResearch.com Page 10 of 12

Exhibit 11. LTL Y/Y OR Improvement (Deterioration), Yields Net of Fuel, and Volumes (Tonnage/day, y/y)

Note: CNW is included until 3Q:15. FDX reported F3Q16 results (which we equate with C1Q). All other companies have yet to report. LTL Avg. for Daily Tonnage is calculated on a volume-weighted basis.

The analyst of Wolfe Research, LLC primarily responsible for this research report whose name appears first on the front page of this research report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the research analysts’ personal views about the subject securities or issuers and (ii) no part of the research analysts’ compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this report.

Other Disclosures:

Wolfe Research, LLC Fundamental Stock Ratings Key:

Outperform (OP): The security is projected to outperform analyst's industry coverage universe over the next 12 months.

Peer Perform (PP): The security is projected to perform approximately in line with analyst's industry coverage universe over the next 12 months.

Underperform (UP): The security is projected to underperform analyst's industry coverage universe over the next 12 months.

Wolfe Research, LLC uses a relative rating system using terms such as Outperform, Peer Perform and Underperform (see definitions above). Please carefully read the definitions of all ratings used in Wolfe Research, LLC research. In addition, since Wolfe Research, LLC research contains more complete information concerning the analyst’s views, please carefully read Wolfe Research, LLC research in its entirety and not infer the contents from the ratings alone. In all cases, ratings (or research) should not be used or relied upon as investment advice and any investment decisions should be based upon individual circumstances and other considerations.

Wolfe Research, LLC Sector Weighting System:

Market Overweight (MO): Expect the industry to outperform the primary market index for the region (S&P 500 in the U.S.) by at least 10% over the next 12 months.

Market Weight (MW): Expect the industry to perform approximately in line with the primary market index for the region (S&P 500 in the U.S.) over the next 12 months.

Market Underweight (MU): Expect the industry to underperform the primary market index for the region (S&P 500 in the U.S.) by at least 10% over the next 12 months.

Wolfe Research, LLC Distribution of Fundamental Stock Ratings (As of December 31, 2015):

Wolfe Research, LLC does not assign ratings of Buy, Hold or Sell to the stocks it covers. Outperform, Peer Perform and Underperform are not the respective equivalents of Buy, Hold and Sell but represent relative weightings as defined above. To satisfy regulatory requirements, Outperform has been designated to correspond with Buy, Peer Perform has been designated to correspond with Hold and Underperform has been designated to correspond with Sell.

Wolfe Research Securities and Wolfe Research, LLC have adopted the use of Wolfe Research as brand names. Wolfe Research Securities, a member of FINRA (www.finra.org) is the broker-dealer affiliate of Wolfe Research, LLC and is responsible for the contents of this material. Any analysts publishing these reports are dually employed by Wolfe Research, LLC and Wolfe Research Securities.

The content of this report is to be used solely for informational purposes and should not be regarded as an offer, or a solicitation of an offer, to buy or sell a security, financial instrument or service discussed herein. Opinions in this communication constitute the current judgment of the author as of the date and time of this report and are subject to change without notice. Information herein is believed to be reliable but Wolfe Research and its affiliates, including but not limited to Wolfe Research Securities, makes no representation that it is complete or accurate. The information provided in this communication is not designed to replace a recipient's own decision-making processes for assessing a proposed transaction or investment involving a financial instrument discussed herein. Recipients are encouraged to seek financial advice from their financial advisor regarding the appropriateness of investing in a security or financial instrument referred to in this report and should understand that statements regarding the future performance of the financial instruments or the securities referenced herein may not be realized. Past performance is not indicative of future results. This report is not intended for distribution to, or use by, any person or entity in any location where such distribution or use would be contrary to applicable law, or which would subject Wolfe Research, LLC or any affiliate to any registration requirement within such location. For additional important disclosures, please see www.WolfeResearch.com/Disclosures.

The views expressed in Wolfe Research, LLC research reports with regards to sectors and/or specific companies may from time to time be inconsistent with the views implied by inclusion of those sectors and companies in other Wolfe Research, LLC analysts’ research reports and modeling screens. Wolfe Research communicates with clients across a variety of mediums of the clients’ choosing including emails, voice blasts and electronic publication to our proprietary website.

This report is limited for the sole use of clients of Wolfe Research. Authorized users have received an encryption decoder which legislates and monitors the access to Wolfe Research, LLC content. Any distribution of the content produced by Wolfe Research, LLC will violate the understanding of the terms of our relationship.