AIRPORT FINANCE AND HOW GROUND TRANSPORTATION FEES FIT IN. LEIGH FISHER ASSOCIATES A Division of Jacobs Consultancy Inc. Airport Ground Transportation Association Spring Meeting, 2005. Presented by Joan Zatopek Leigh Fisher Associates. April 5, 2005. Presentation Outline. - PowerPoint PPT Presentation

27

AIRPORT FINANCE AND HOW GROUND TRANSPORTATION FEES FIT IN Presented by Joan Zatopek Leigh Fisher Associates April 5, 2005 Airport Ground Transportation Association Spring Meeting, 2005 LEIGH FISHER ASSOCIATES A Division of Jacobs Consultancy Inc.

Transcript

AIRPORT FINANCE AND HOW GROUND TRANSPORTATION FEES FIT IN

Presented by

Joan ZatopekLeigh Fisher Associates

April 5, 2005

Airport Ground Transportation Association

Spring Meeting, 2005

LEIGH FISHER ASSOCIATESA Division of Jacobs Consultancy Inc.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20052AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Presentation Outline

Airport financial overview

Historical context

How are airlines charged?

What are the funding sources?

Landside fees and considerations

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20053AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Airport Financial Overview

Airport must:

Be self-sustaining

Meet federal law and FAA mandates

Serve the needs of the community

Attract and promote air service

Maintain competitive rate structure to be able to attract any type of air carrier

Cover increasing operating expenses

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20054AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Overview of Airport Finance--Governance Structure

County15%

Regional23%

City40%

State9%

Authority4%

Other9%

Most U.S. airports are operated as either– Independent not-for-profit entities with oversight by a

politically appointed authority

– Self-sustaining enterprise fund of a city, county, or state government

Very few privately run airports in the U.S.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20055AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Factors Governing Airport Financial Operations– U.S. Airports

Capital Markets:• Bondholders• Rating agencies• Credit and liquidity providers

• Congress• FAA/DOT•TSA• NTSB• EPA• OSHA

• State government• County or local government• Governing board or authority

• Signatory air carriers• Nonsignatory air carriers• Air cargo carriers

• Merchants/vendors• Car rental franchises• Taxi/limo operators• Hotel operators• Parking garage operators• Fixed based operators

Airport Operator

Federal Regulations and Policies

Sponsor Assurances

Bond Ordinance/Resolution/

Trust Indenture

Concession/Operating

Agreements and Permits

Authorizing Legislation

Airline Use and Lease Agreement

Generallyaccepted

accountingprinciples

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20056AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

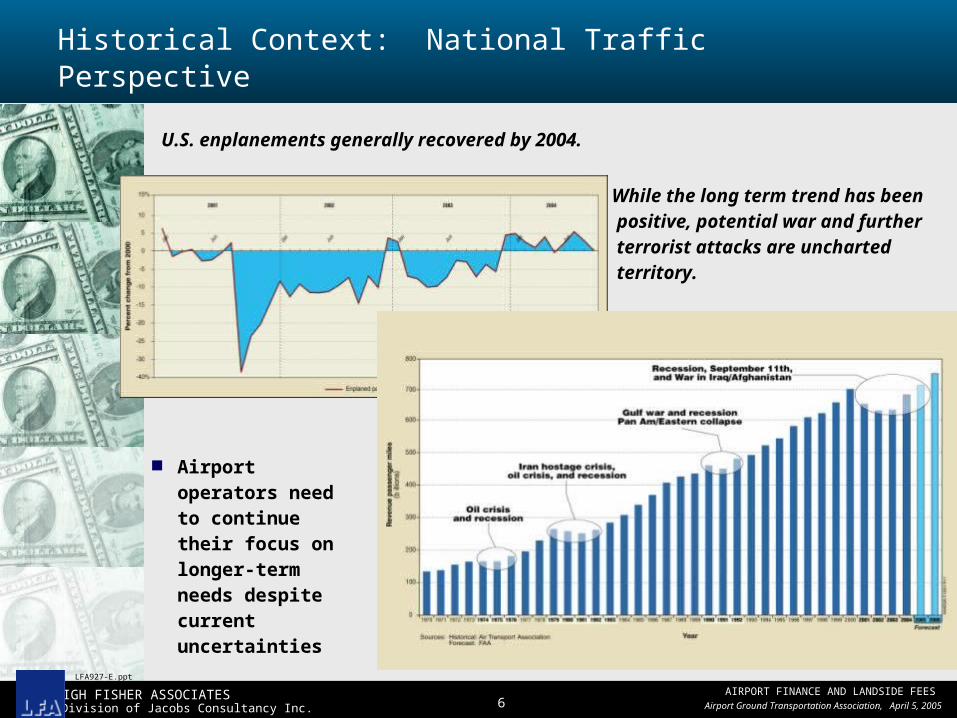

Historical Context: National Traffic Perspective

Airport operators need to continue their focus on longer-term needs despite current uncertainties

U.S. enplanements generally recovered by 2004.

While the long term trend has been positive, potential war and further terrorist attacks are uncharted territory.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20057AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Historical Context: Signs of Airline Profitability

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20058AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

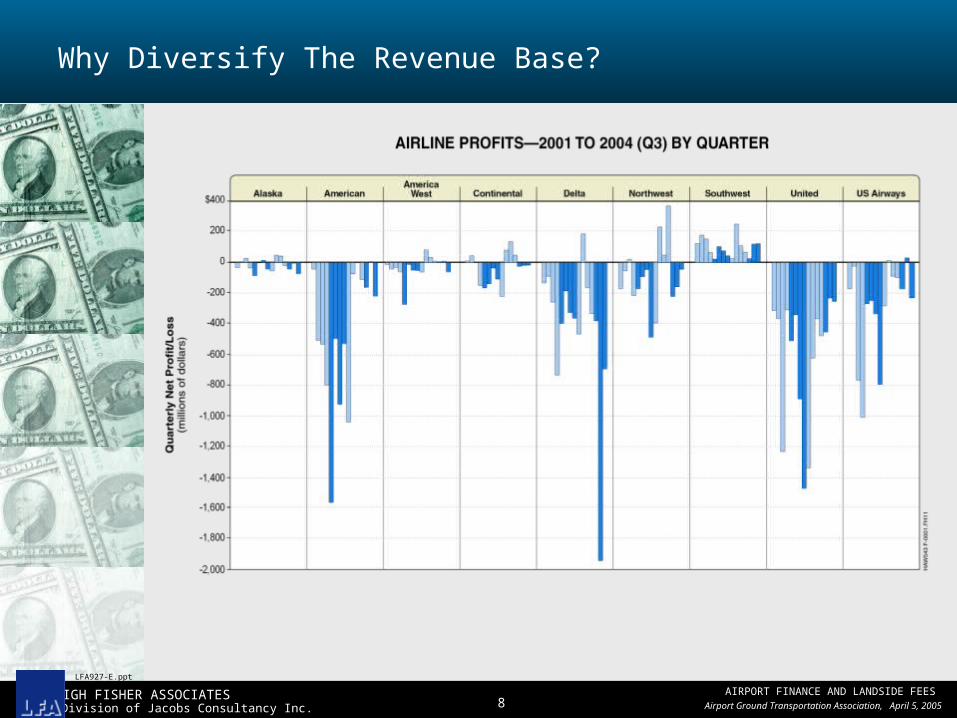

Why Diversify The Revenue Base?

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 20059AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Basic Rate-Making Methodologies

Compensatory– Recover fully allocated costs of facilities occupied

– Only pay for what you use

– Airport sponsor assumes financial risk

– Airport keeps nonairline revenues

Airport System Residual (single cash register)– Recover net costs after allowing for nonairline revenue credit

– Financial risk transferred to airlines

– Usually requires airline approval on capital investments decisions

– Airport negotiates retainage of fixed discretionary cash amount

Hybrids– Mixture of both methodologies

– Carve outs of self-supporting cost centers

– Net revenue sharing formulas (usually in return for “safety nets”)

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200510AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Compensatory Rate-Making Methodology

O&M costs,debt service

andcoverage

Airport Sponsor’s Net Cash Flow

Landing fieldrevenue

Terminal buildingrevenue

Parkingrevenue

Cargo/hangarrevenue

Commercialpropertyrevenue

General aviationrevenue

Recover fully allocated operating and capital costs from airlines for each facility occupied or used

• Airport sponsor assumes risk that nonairline revenues will cover nonairline costs, and retains for its discretionary use any net cash flow

• Airport sponsor retains control over capital investment decisions

O&M costs,debt service

andcoverage

O&M costs,debt service

andcoverage

O&M costs,debt service

andcoverage

O&M costs,debt service

andcoverage

O&M costs,debt service

andcoverage

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200511AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

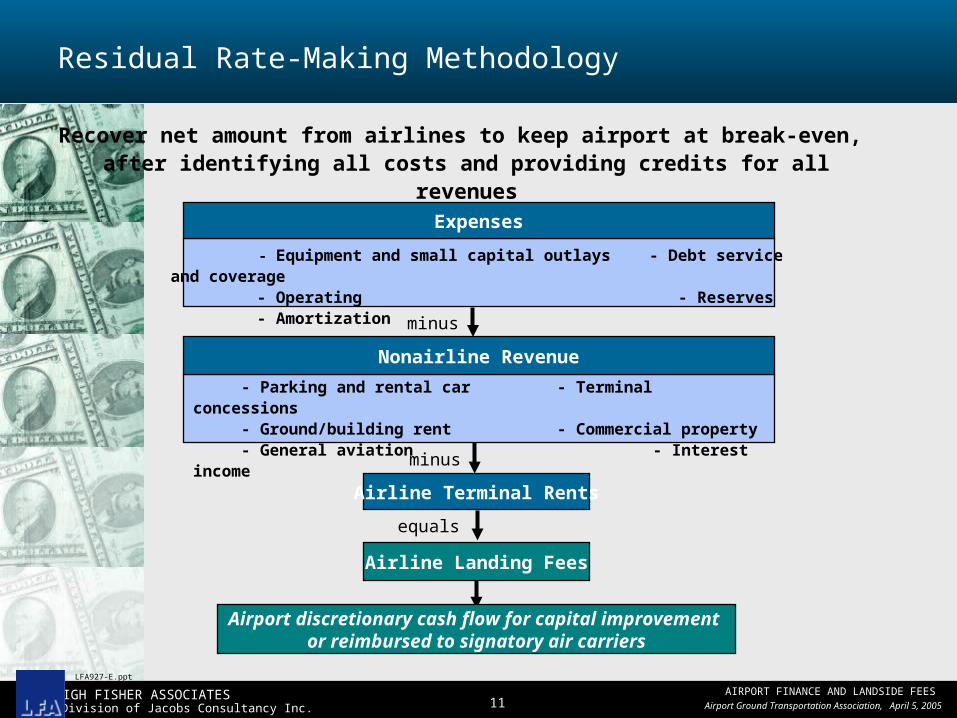

Residual Rate-Making Methodology

Recover net amount from airlines to keep airport at break-even, after identifying all costs and providing credits for all revenues

Nonairline Revenue

- Parking and rental car - Terminal concessions - Ground/building rent - Commercial property - General aviation - Interest income

- Equipment and small capital outlays - Debt service and coverage - Operating - Reserves - Amortization

Expenses

minus

equals

Airline Landing Fees

Airline Terminal Rents

Airport discretionary cash flow for capital improvement or reimbursed to signatory air carriers

minus

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200512AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

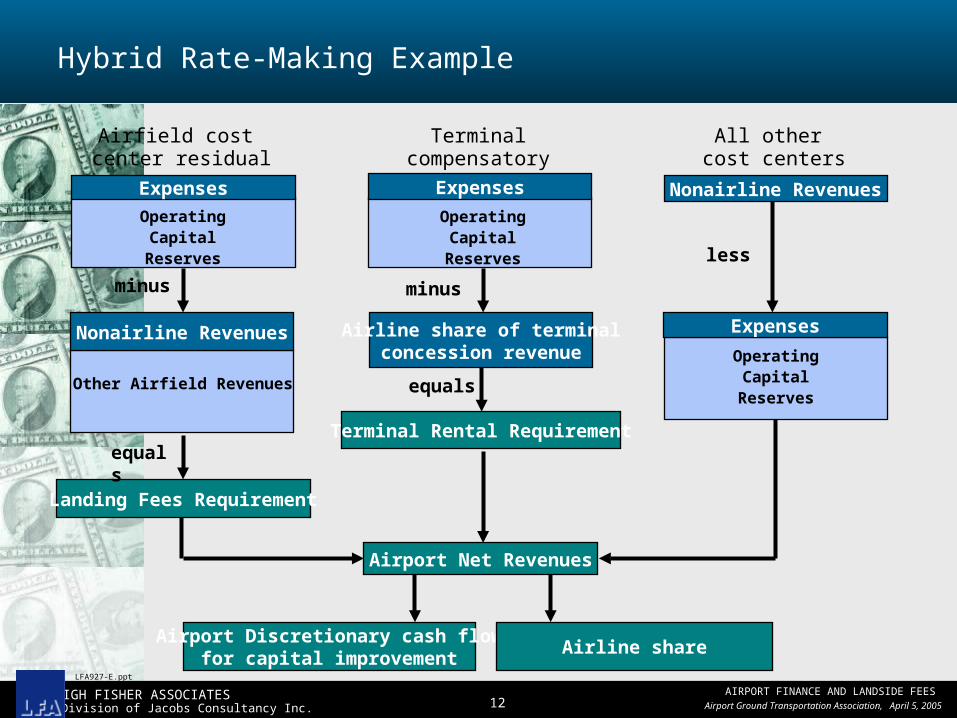

Hybrid Rate-Making Example

Airfield cost center residual

minus

Landing Fees Requirement

Terminal Rental Requirement

Airport Net Revenues

Airline share of terminalconcession revenue

OperatingCapital

Reserves

Expenses

Other Airfield Revenues

Nonairline Revenues

OperatingCapital

Reserves

Expenses

OperatingCapital

Reserves

Expenses

Nonairline Revenues

Terminalcompensatory

All other cost centers

equals

minus

equals

Airport Discretionary cash flowfor capital improvement

Airline share

less

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200513AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

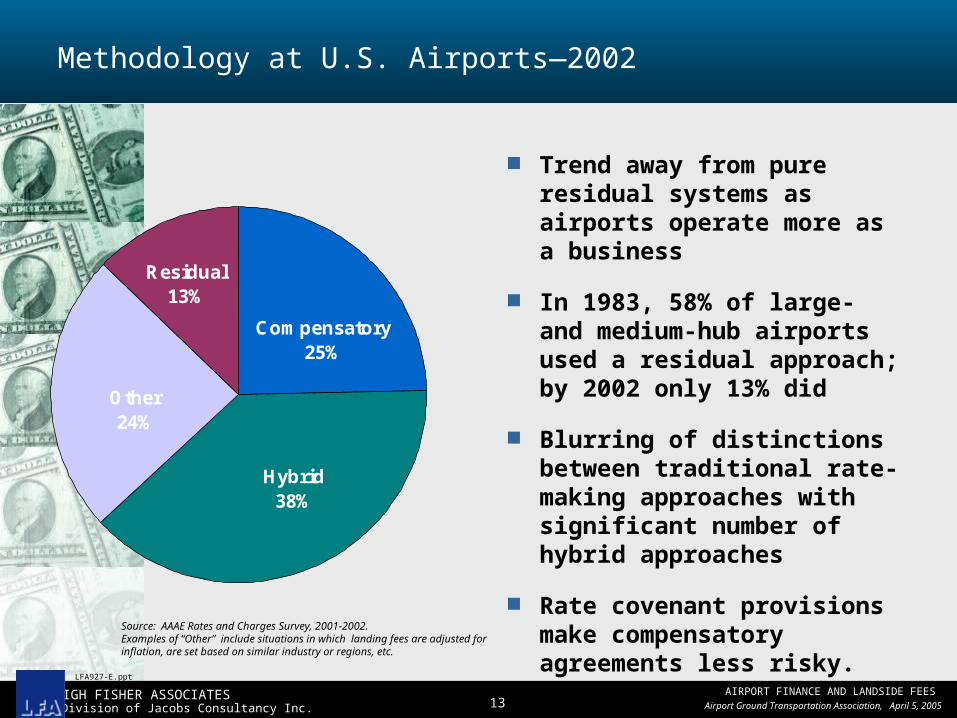

Methodology at U.S. Airports—2002

Trend away from pure residual systems as airports operate more as a business

In 1983, 58% of large- and medium-hub airports used a residual approach; by 2002 only 13% did

Blurring of distinctions between traditional rate-making approaches with significant number of hybrid approaches

Rate covenant provisions make compensatory agreements less risky.

Hybrid38%

Compensatory 25%

Residual13%

Other 24%

Source: AAAE Rates and Charges Survey, 2001-2002. Examples of “Other” include situations in which landing fees are adjusted for inflation, are set based on similar industry or regions, etc.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200514AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Example—Airline cost per enplaned passenger can range from $2.00-$12.00

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200515AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

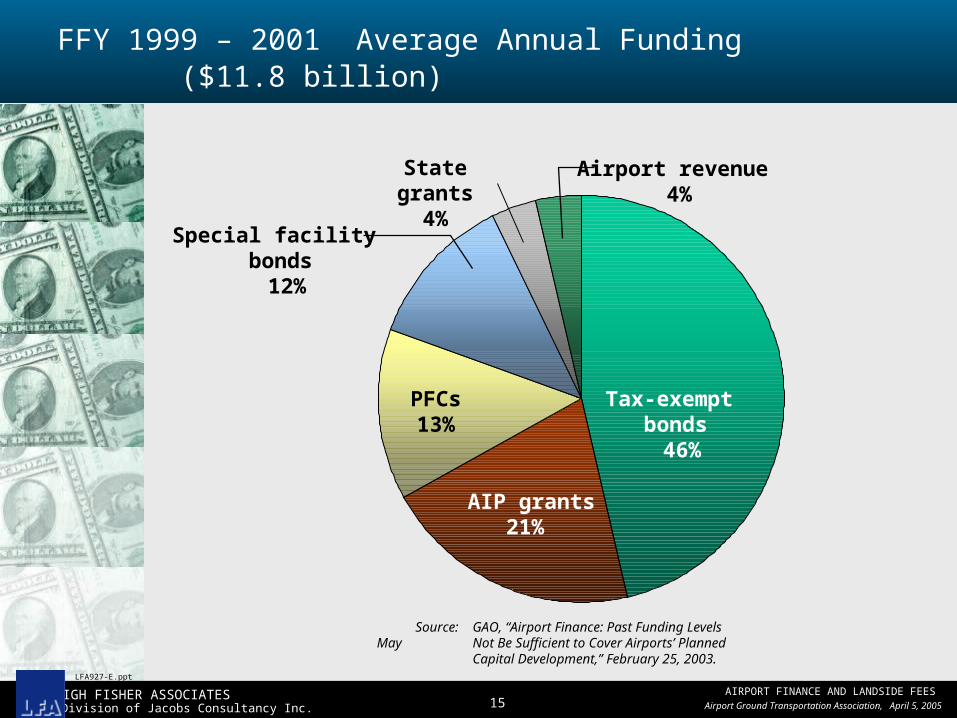

FFY 1999 – 2001 Average Annual Funding ($11.8 billion)

PFCs13%

AIP grants21%

Tax-exempt bonds 46%

Special facility bonds 12%

State grants4%

Airport revenue 4%

Source: GAO, “Airport Finance: Past Funding Levels May Not Be Sufficient to Cover Airports’ Planned Capital Development,” February 25, 2003.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200516AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

AIP Funding Levels

Fu

nd

ing

(bill

ion

s)

Federal Fiscal Year

AIR-21 Vision 100* Appropriation includes additional $175 million authorized by ATSA and

appropriated by DOD Security Appropriation for security purposes only.

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200517AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Airport Funding Sources—Federal Airport Improvement Program (AIP) Grants

Federal Airport Improvement Program (AIP) Grants

– Entitlement funds

– Discretionary funds

– FAA Letters of Intent

Eligible projects – On-airport property or within right-of-way acquired by

airport operator

– Must exclusively serve airport traffic

– Generally limited to one access road to nearest public highway

– Includes related facilities (acceleration lanes, etc.)

– Eligible transit facilities must primarily serve passengers or employees

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200518AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

Rentals, fees and charges– Passenger and cargo airlines

– Terminal concessionaires

– Rental car companies

– Other aviation tenants

– Other services (ground transportation, public telephones, carts, lockers, etc.)

Other revenue– Interest income

– Nonaviation tenants and industrial areas

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200522AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Typical Distribution Of Operating Revenues

LandingFees24%

AirlineRentals

33%

OtherAviation

2%

Other4%

In-TerminalConcessions

11%

RentalCars8%

Parking17%

Other GroundTransportation

1%

Airline Revenues57%

Large Hubs

LandingFees18%

AirlineRentals

28%

OtherAviation

4%

Other10%

In-TerminalConcessions

7%

RentalCars13%

Parking20%

Airline Revenues46%

Small Hubs

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200523AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Ground Transportation, Rental Car and Parking are 70%-85% of all Non-Airline Revenue

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200524AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Operating Revenues to Meet Operating Expenses

Typical Capital and Operation and Maintenance Expenses

Debt service for Capital projects Security Dispatching/curbside management Personnel Contractual services Utilities Maintenance and repairs Insurance Administration Public works Janitorial

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200525AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Permit fees– Monthly or annual fees

– Per company or per vehicle

Cost recovery fees– Per trip

– Vary by vehicle size

Privilege fees– Percent of gross revenues

– Other measures

Excessive dwell times

Excessive circuit

Typical Ground Transportation Fees

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200526AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Considerations when Charging Ground Transportation Fees

Assess role of ground transportation provider

–For-hire versus “courtesy”

–Enhancing flow of passengers

–Amount of benefit derived by operator

Availability of facilities and services used directly by providers

Air quality needs/incentives

Access to market–Exclusive

–Open

LFA927-E.ppt

Airport Ground Transportation Association, April 5, 200527AIRPORT FINANCE AND LANDSIDE FEES LEIGH FISHER ASSOCIATES

A Division of Jacobs Consultancy Inc.

Conclusions

Airports are required to be self-sustaining

Non-airline revenues represent >43% of total revenues

Ground transportation/parking revenues represent >70% of non-airline revenue

Important to preserve existing revenues (parking and rental car) while enhancing others as appropriate