Pengeluaran untuk perbaikan/penambahan/memperpanjang umur manfaat aktiva disebut capital expenditures.

Pengeluaran untuk perbaikan/penambahan/memperpanjang umur manfaat aktiva disebut capital expenditures.

Capital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue Expenditures

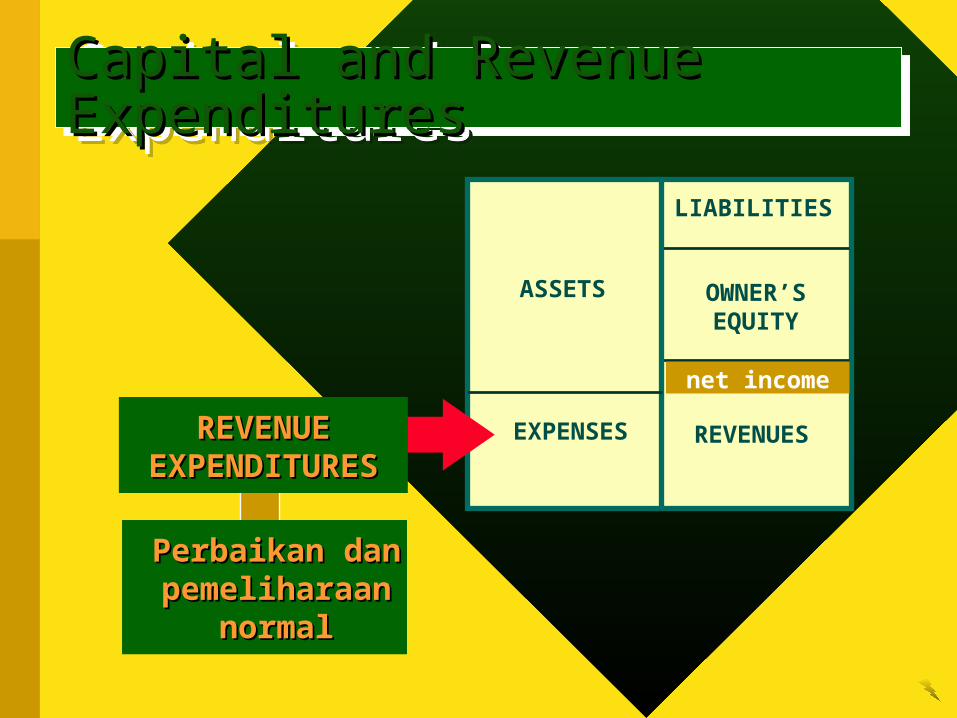

Pengeluaran untuk pemeliharaan & perbaikan normal hanya memberikan

manfaat pada periode berjalan disebut revenue expenditures.

Pengeluaran untuk pemeliharaan & perbaikan normal hanya memberikan

manfaat pada periode berjalan disebut revenue expenditures.

Capital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue Expenditures

EXPENDITURE

Increases operating

efficiency or adds to capacity?

Capital Expenditure

(Debit fixed asset account)

YesYes

Capital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue Expenditures

Increases useful life

(extraordinary repairs)?

NoNo

Capital Expenditure (Debit accumulated

depreciation account)

YesYes

Revenue Expenditure

(Debit expense account for

ordinary maintenance and repairs)

NoNo

LIABILITIES

OWNER’SEQUITY

REVENUES

ASSETS

EXPENSES

CAPITAL CAPITAL EXPENDITURESEXPENDITURES

1. Harga perolehan1. Harga perolehan2. Tambahan2. Tambahan3. Perbaikan3. Perbaikan4. Extraordinary 4. Extraordinary

repairsrepairs

1. Harga perolehan1. Harga perolehan2. Tambahan2. Tambahan3. Perbaikan3. Perbaikan4. Extraordinary 4. Extraordinary

repairsrepairs

net income

Capital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue Expenditures

LIABILITIES

OWNER’SEQUITY

REVENUES

ASSETS

EXPENSES

net income

Perbaikan dan Perbaikan dan pemeliharaan pemeliharaan

normalnormal

REVENUE REVENUE EXPENDITURESEXPENDITURES

Capital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue ExpendituresCapital and Revenue Expenditures

Accounting for Fixed Asset DisposalsAccounting for Fixed Asset DisposalsAccounting for Fixed Asset DisposalsAccounting for Fixed Asset DisposalsKetika asset sudah tidak memberikan manfaat lagi, perlakuannya ada beberapa kemungkinan:

1. Dihapuskan/Discarded,

2. Dijual/sold, or

3. Ditukarkan dengan assets serupa.

Ayat jurnal untuk mencatat pelepasan aktiva tetap dapat bervariasi tergantung dengan berbagai jenis keadaan, tetapi ayat jurnal yang selalu diperlukan adalah:

Akun akt tetap harus dikredit sebesar harga perolehan, dan akun Akumulasi depresiasi harus didebit sebesar saldonya saat pelepasan untuk menghapus dari akun

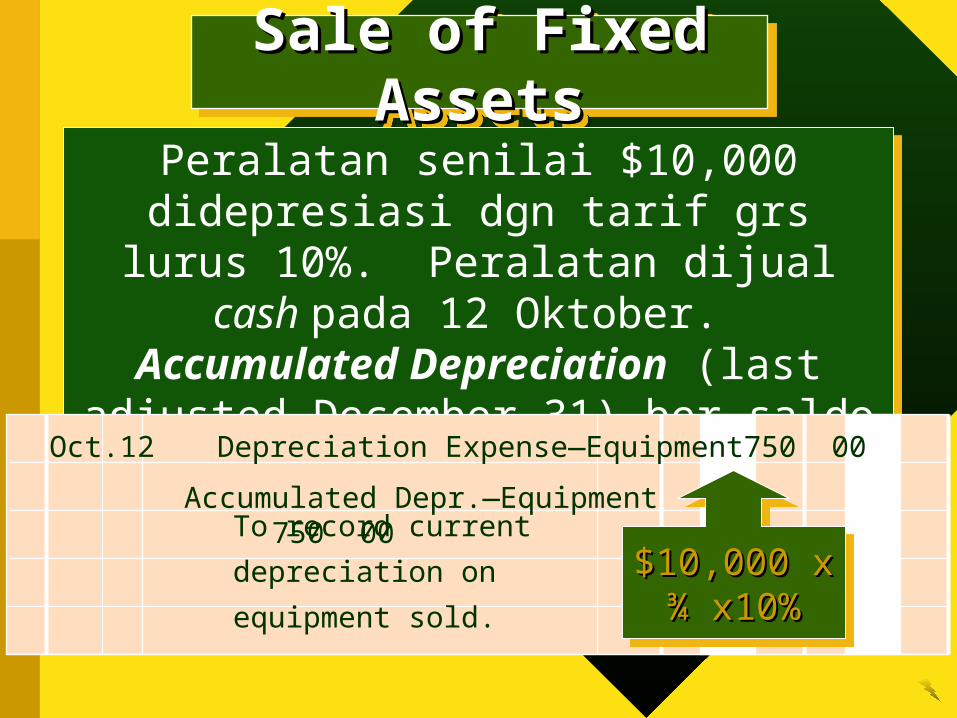

Oktober. Accumulated Depreciation (last adjusted December 31) ber saldo $7,000.

Oct. 12 Depreciation Expense—Equipment 750 00

To record current depreciation

on equipment sold.

Accumulated Depr.—Equipment 750 00

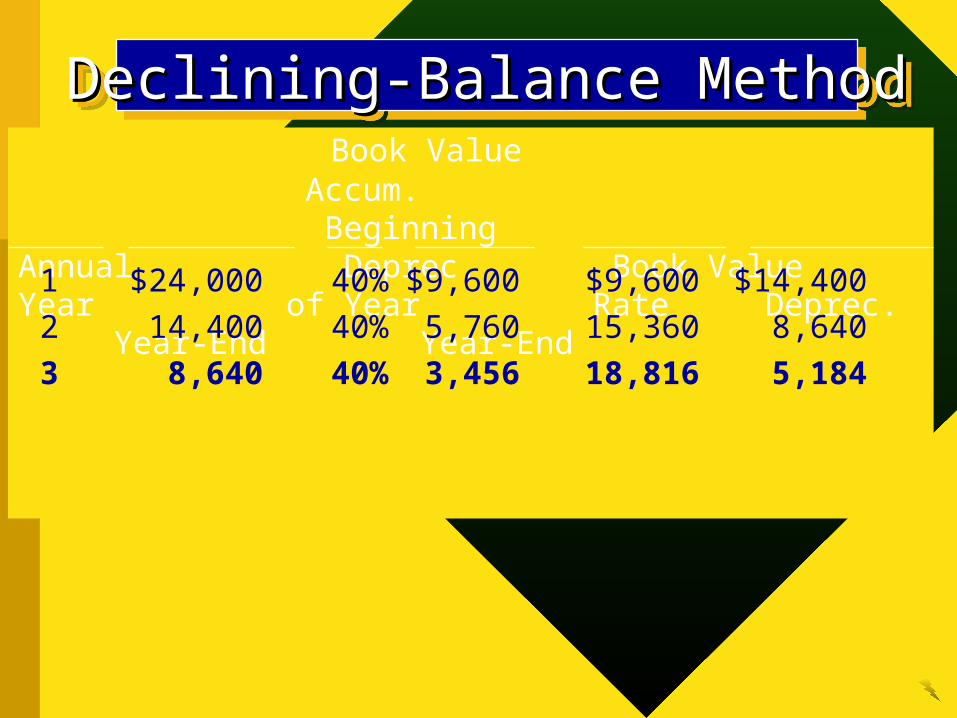

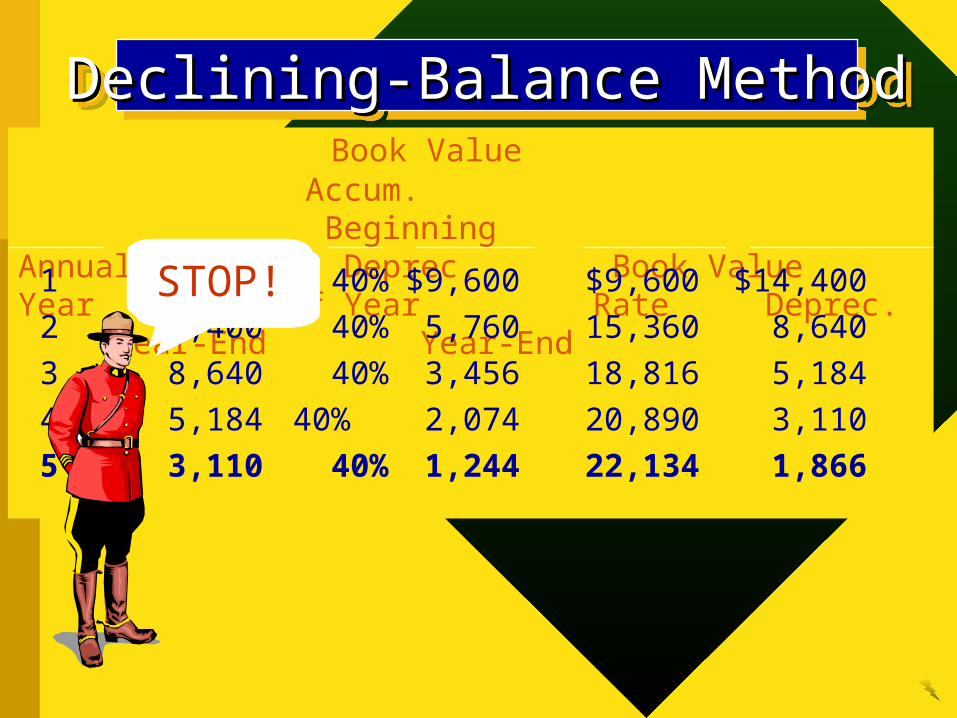

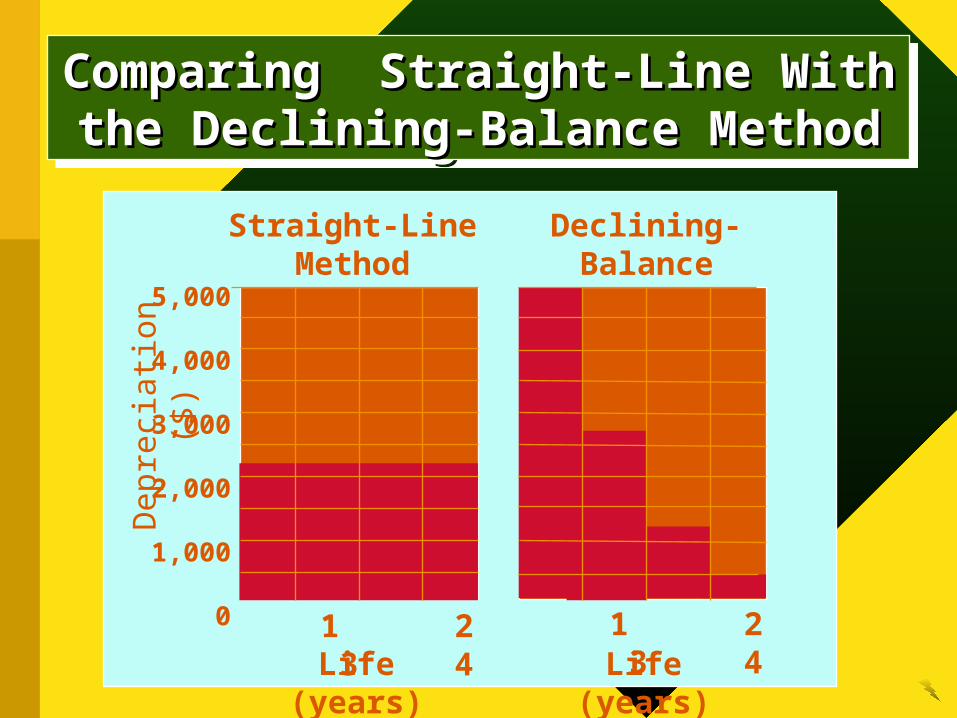

$10,000 x ¾ $10,000 x ¾ x10%x10%

$10,000 x ¾ $10,000 x ¾ x10%x10%

Sale of Fixed AssetsSale of Fixed AssetsSale of Fixed AssetsSale of Fixed Assets

Assumption 1: The equipment is sold for $2,250, so there is no gain or loss.

Assumption 1: The equipment is sold for $2,250, so there is no gain or loss.

Oct. 12 Cash 2 250 00

Sold equipment.

Accumulated Depr.—Equipment 7 750 00

Equipment 10 000 00

Sale of Fixed AssetsSale of Fixed AssetsSale of Fixed AssetsSale of Fixed Assets

Assumption 2: The equipment is sold for $1,000, so there is a loss of $1,250.

Assumption 2: The equipment is sold for $1,000, so there is a loss of $1,250.

Oct. 12 Cash 1 000 00

Sold equipment.

Accumulated Depr.—Equipment 7 750 00

Equipment 10 000 00

Loss on Disposal of Fixed Assets 1 250 00

Sale of Fixed AssetsSale of Fixed AssetsSale of Fixed AssetsSale of Fixed Assets

Assumption 2: The equipment is sold for $2,800, so there is a gain of $550.

Assumption 2: The equipment is sold for $2,800, so there is a gain of $550.

Sold equipment.

Equipment 10 000 00 Gain on Disposal of Fixed Assets 550 00

Accumulated Depr.—Equipment 7 750 00

Oct. 12 Cash 2 800 00

Exchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed Assets Trade-in Allowance (TIA)=

NilaiTukar tambah aktiva sejenis Boot – Saldo terutang untuk akt tetap baru

setelah dikurangi nilai tukar tambah. TIA > Book Value = Gain on Trade TIA < Book Value = Loss on Trade Gains tidak pernah dicatat/diakui Losses harus diakui/dicatat.

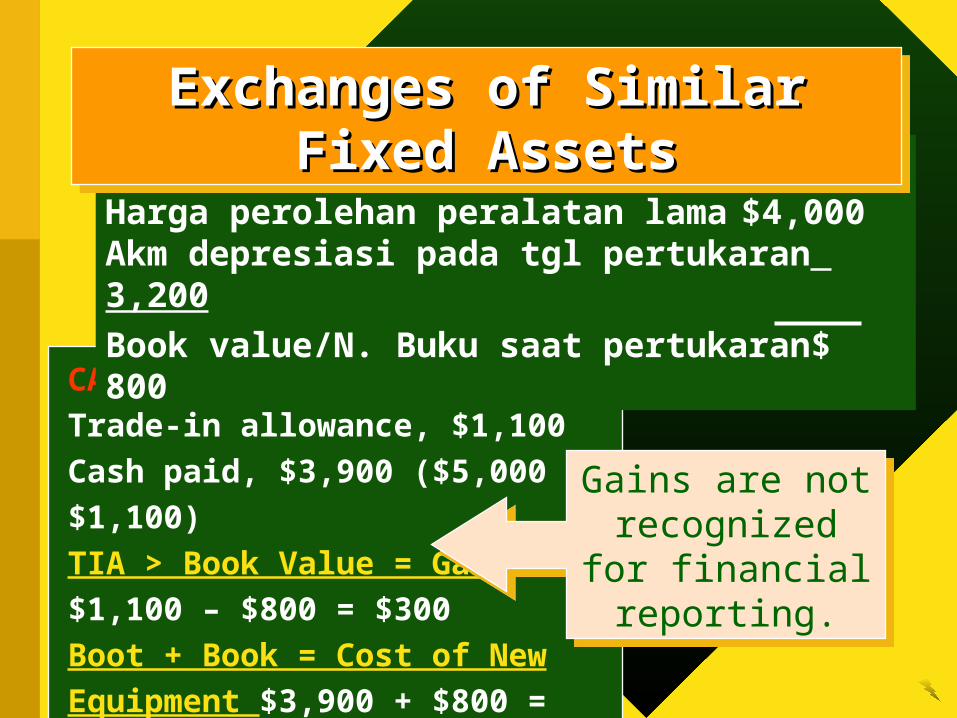

CASE ONE (GAIN):

Trade-in allowance, $1,100

Cash paid, $3,900 ($5,000 – $1,100)

TIA > Book Value = Gain

$1,100 – $800 = $300

Boot + Book = Cost of New Equipment

$3,900 + $800 = $4,700

Harga peralatan baru $5,000

Harga perolehan peralatan lama $4,000Akm depresiasi pada tgl pertukaran 3,200

Book value/N. Buku saat pertukaran $ 800

Exchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed Assets

Gains are not recognized for

financial reporting.

Gains are not recognized for

financial reporting.

Exchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed Assets

June 19 Accumulated Depr.—Equipment 3 200 00

Equipment (new equipment) 4 700 00

Equipment (old equipment) 4 000 00Cash 3 900 00

On June 19, equipment exchanged at a gain of $300.

CASE TWO (LOSS):

Trade-in allowance, $2,000

Cash paid, $8,000 ($10,000 – $2,000)

TIA<Book Value = Loss

$2,000 – $2,400 = $400

Harga peralatan baru $10,000

Harga perolehan peralatan yg ditukar $7,000Akm depresiasi saat pertukaran 4,600

Nilai Buku saat pertukaran $2,400

Exchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed Assets

Losses are recognized for

financial reporting.

Losses are recognized for

financial reporting.

Exchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed AssetsExchanges of Similar Fixed Assets

Sept. 7 Accumulated Depr.—Equipment 4 600 00

Equipment (new equipment) 10 000 00

Loss on Disposal of Fixed Assets 400 00

On September 7, equipment exchanged at a loss of $400.

Equipment (old equipment) 7 000 00

Cash8 000 00

Natural Resources and Natural Resources and DepletionDepletion

Natural Resources and Natural Resources and DepletionDepletion

Deplesi (Depletion) adalah proses transfer HPo/Cost sumber daya

alam ke rekening beban (expense).

Deplesi (Depletion) adalah proses transfer HPo/Cost sumber daya

alam ke rekening beban (expense).

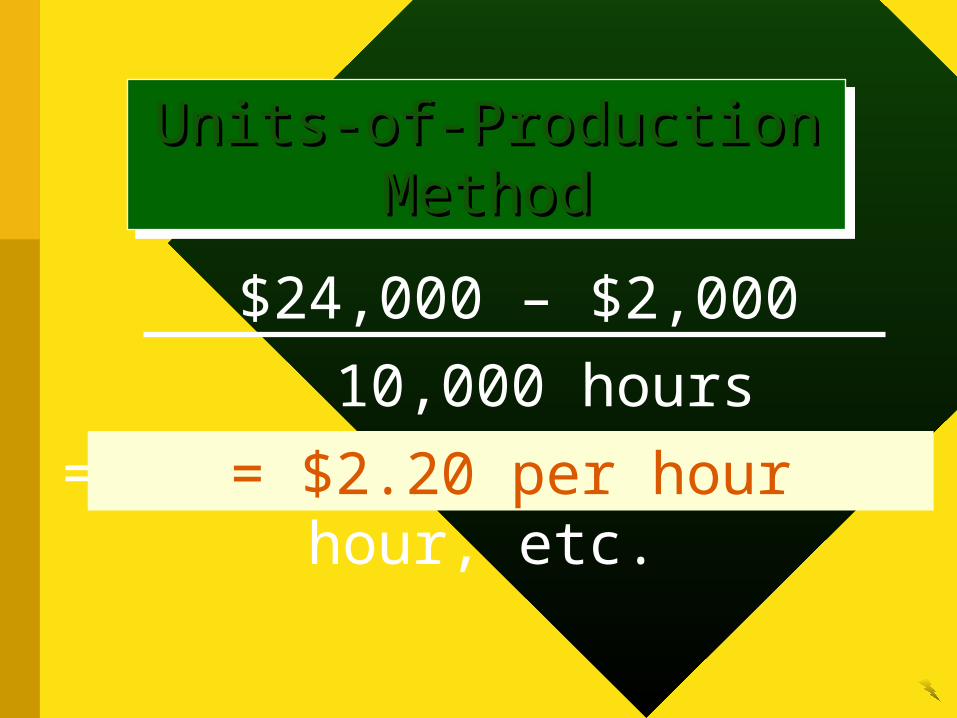

Perhitungan

Deplesi = Unit Produksi

Natural Resources and DepletionNatural Resources and DepletionNatural Resources and DepletionNatural Resources and Depletion

Perush membayar $400,000 unt

mendapatkan hak penambangan yg

diestimasikan memiliki cadangan

1,000,000 tons. Deplesi per ton $0.40

($400,000 ÷ 1,000,000 tons).

Natural Resources and DepletionNatural Resources and DepletionNatural Resources and DepletionNatural Resources and Depletion

Adjusting Entry

Akumulasi Deplesi 36 000 00

Selama setahun ditambang, 90,000 tons. Deplesi periodik = $36,000

Intangible Assets and AmortizationIntangible Assets and Amortization

Dec. 31 Beban Amortisasi 20,000Patents 20,000

Membeli hak paten $100,000. Umur paten 11 th dan pada saat dibeli telah digunakan 6 th

Amortization merupakan berkurangnya HPo/cost akt tak berwujud yg tidak nampak sec fisik dan tidak unt dijual (patents, copyrights/hak cipta, and goodwill).