42

ALBA SOLUZIONI Consultancy and information services in energy and finance Peter Crilly Energy Commodities Conference 2018 10 May 2018 The Italian gas and power markets 1

ALBA SOLUZIONI Consultancy and information services in energy and finance

Peter Crilly Energy Commodities Conference 2018 10 May 2018

The Italian gas and power markets

1

ALBA SOLUZIONI

Alba Soluzioni is an independent consultancy operating in the energy and finance sectors in Italy

• Italian gas & power market report

Gas e Elettricità Oggi ---- GeEO - Italian Gas & Power

• Italian Regulatory Alert Service

• AlbaStack power price forecasting service

• AlbaFlows daily gas service

• Consultancy services, seminars and workshops

www.albasoluzioni.com [email protected]

The Italian gas and power markets

This presentation has been prepared using publicly available information in addition to Alba Soluzioni’s proprietary Italian market price information. The interpretation of publicly available information and the analysis and conclusions derived represent Alba Soluzioni’s viewpoint as an independent observer of the markets. Whilst Alba Soluzioni has no reason to believe that there are any inaccuracies or defects in the information and analysis presented, there are no representations or warranties, express or implied, to the fitness of such information for any purpose.

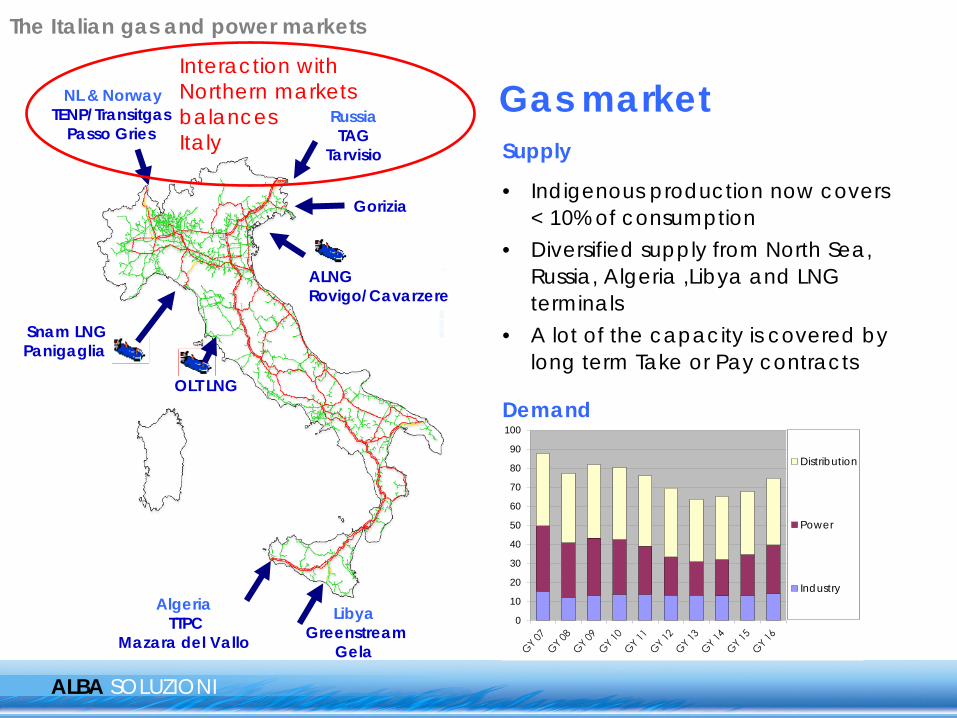

Gas market Russia TAG

Tarvisio

ALNG Rovigo/Cavarzere

Libya Greenstream

Gela

NL & Norway TENP/Transitgas

Passo Gries

Algeria TTPC

Mazara del Vallo

Snam LNG Panigaglia

Supply

• Indigenous production now covers < 10% of consumption

• Diversified supply from North Sea, Russia, Algeria ,Libya and LNG terminals

• A lot of the capacity is covered by long term Take or Pay contracts

Demand

ALBA SOLUZIONI

Gorizia

OLT LNG

0

10

20

30

40

50

60

70

80

90

100

Distribution

Power

Industry

The Italian gas and power markets

Interaction with Northern markets balances Italy

ALBA SOLUZIONI

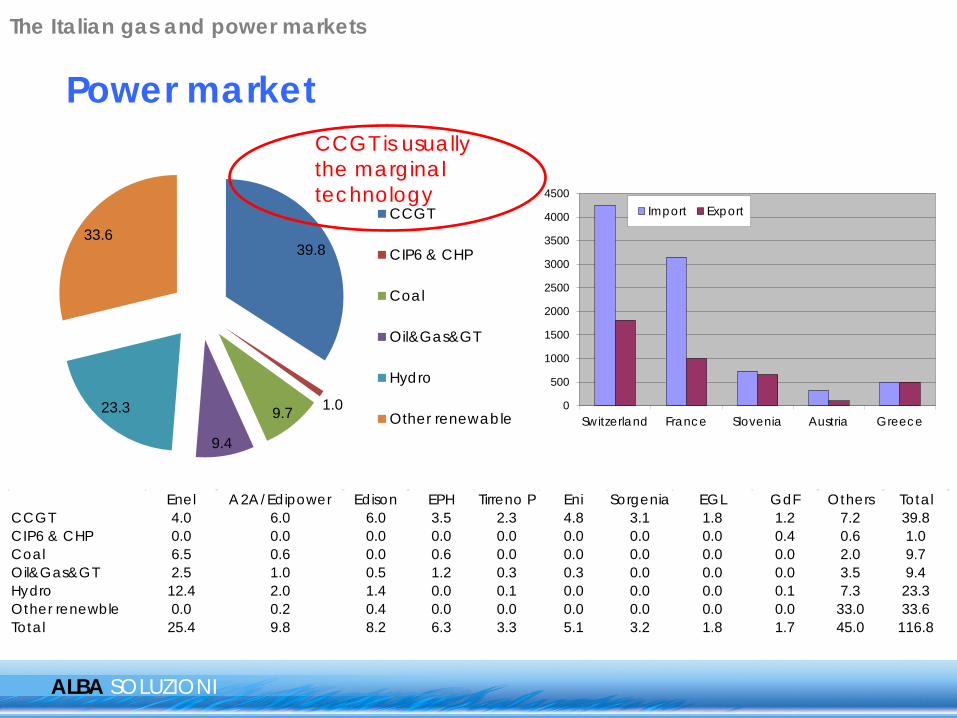

Enel A2A/Edipower Edison EPH Tirreno P Eni Sorgenia EGL GdF Others TotalCCGT 4.0 6.0 6.0 3.5 2.3 4.8 3.1 1.8 1.2 7.2 39.8CIP6 & CHP 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.4 0.6 1.0Coal 6.5 0.6 0.0 0.6 0.0 0.0 0.0 0.0 0.0 2.0 9.7Oil&Gas> 2.5 1.0 0.5 1.2 0.3 0.3 0.0 0.0 0.0 3.5 9.4Hydro 12.4 2.0 1.4 0.0 0.1 0.0 0.0 0.0 0.1 7.3 23.3Other renewble 0.0 0.2 0.4 0.0 0.0 0.0 0.0 0.0 0.0 33.0 33.6Total 25.4 9.8 8.2 6.3 3.3 5.1 3.2 1.8 1.7 45.0 116.8

39.8

1.09.7

9.4

23.3

33.6CCGT

CIP6 & CHP

Coal

Oil&Gas>

Hydro

Other renewable

Power market

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Switzerland France Slovenia Austria Greece

Import Export

The Italian gas and power markets

CCGT is usually the marginal technology

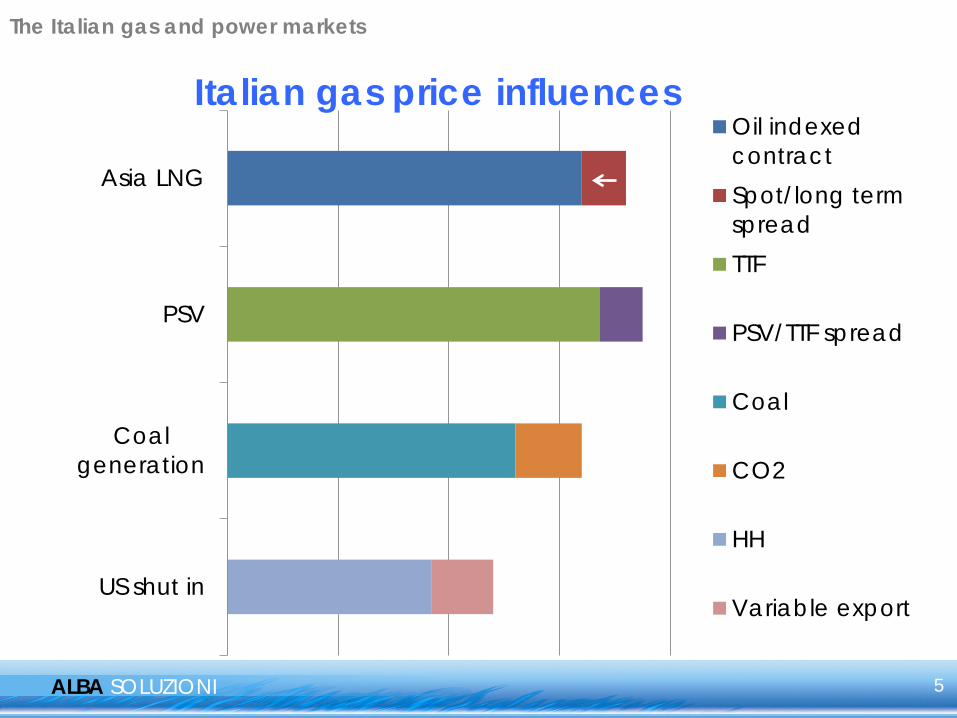

Italian gas price influences

ALBA SOLUZIONI

US shut in

Coalgeneration

PSV

Asia LNG

Oil indexedcontractSpot/long termspreadTTF

PSV/TTF spread

Coal

CO2

HH

Variable export

The Italian gas and power markets

5

Italian power

ALBA SOLUZIONI

As CCGT is usually the marginal technology, it can be helpful to look at the Italian power prices as being the sum of

• CCGT gas cost

• CCGT CO2 cost

• and the clean spark spread

Power prices respond to changes in gas and CO2 prices

Power market fundamentals drive the spark spread

0

5

10

15

20

25

30

35

40

45

50

Italian power

clean sparkspread

CO2

PSV gas

6

Italian gas and power market update

ALBA SOLUZIONI

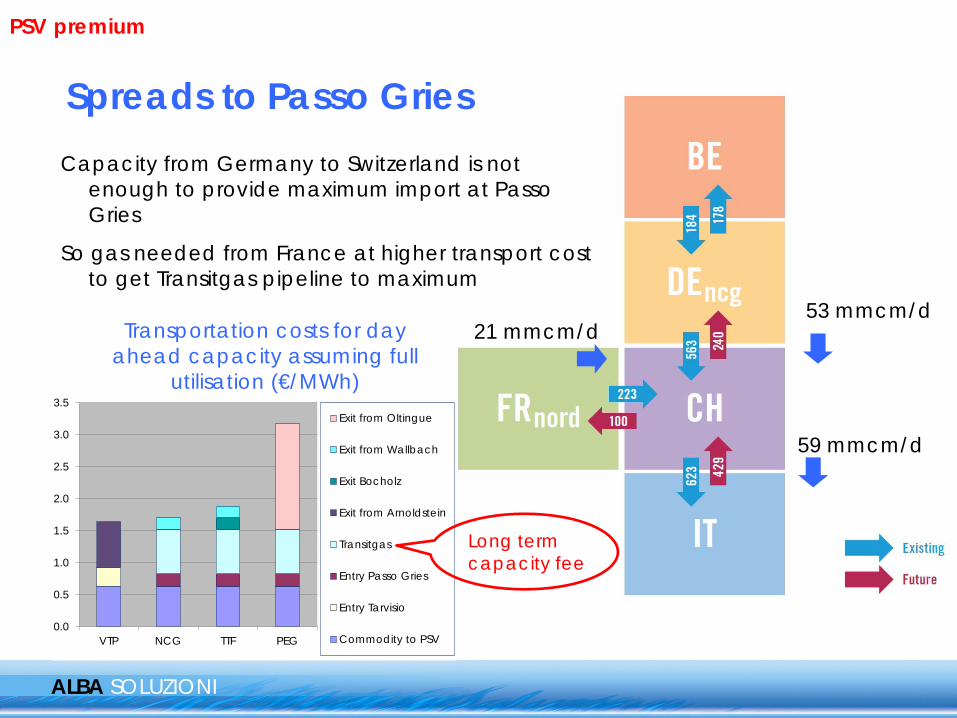

Capacity from Germany to Switzerland is not enough to provide maximum import at Passo Gries

So gas needed from France at higher transport cost to get Transitgas pipeline to maximum

Spreads to Passo Gries

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

VTP NCG TTF PEG

Exit from Oltingue

Exit from Wallbach

Exit Bocholz

Exit from Arnoldstein

Transitgas

Entry Passo Gries

Entry Tarvisio

Commodity to PSV

53 mmcm/d 21 mmcm/d

59 mmcm/d

Transportation costs for day ahead capacity assuming full

utilisation (€/MWh)

PSV premium

Long term capacity fee

121416182022242628303234

PSV

TTF

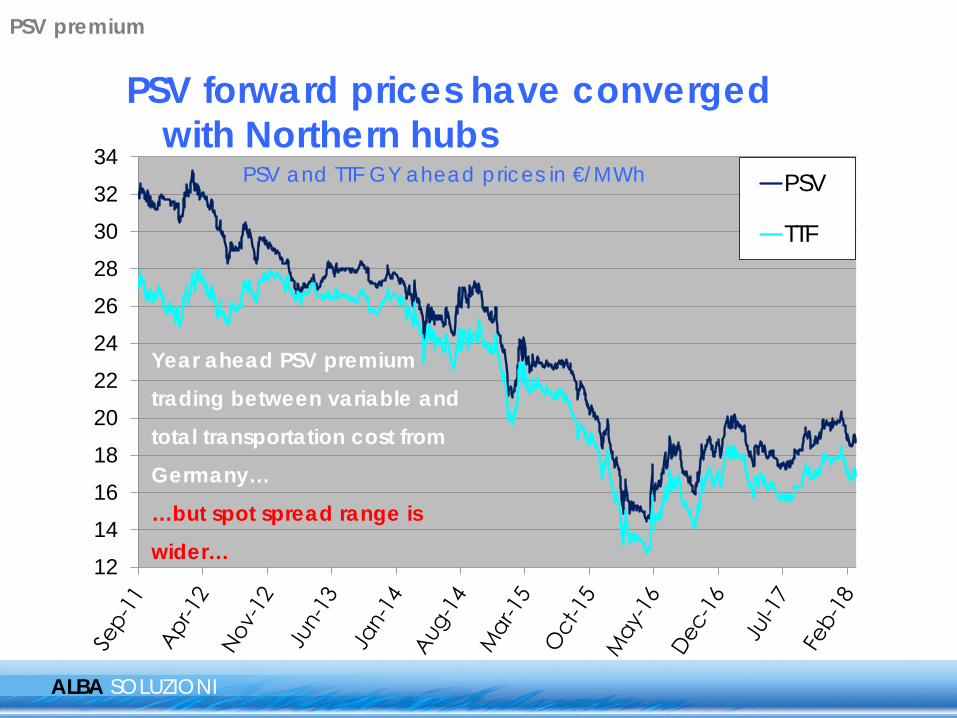

PSV forward prices have converged with Northern hubs

ALBA SOLUZIONI

Year ahead PSV premium

trading between variable and

total transportation cost from

Germany…

…but spot spread range is

wider…

PSV and TTF GY ahead prices in €/MWh

PSV premium

ALBA SOLUZIONI

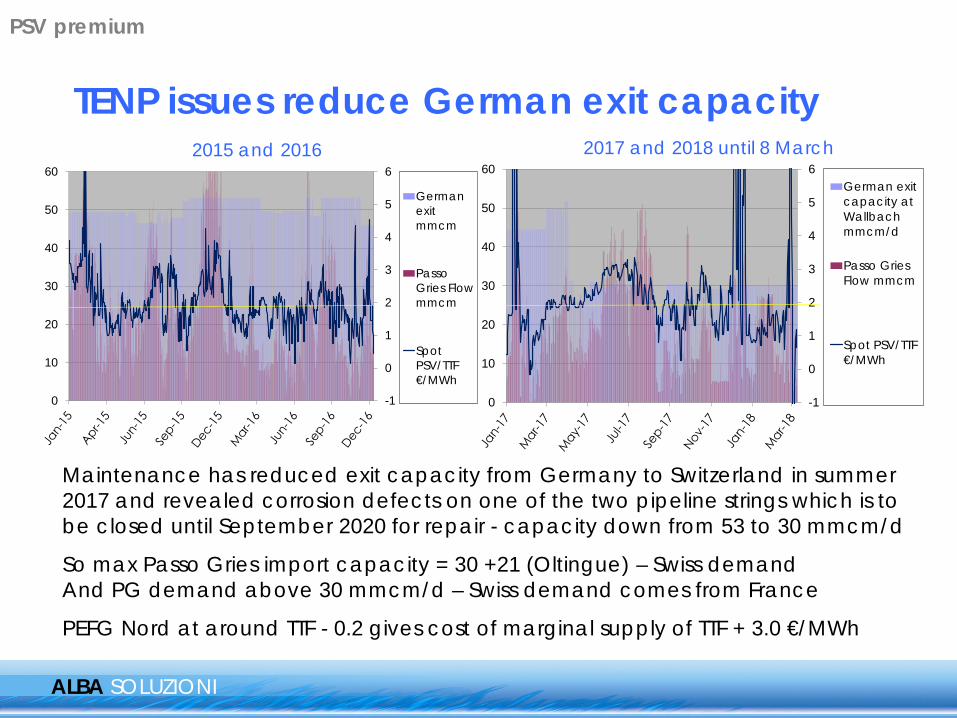

TENP issues reduce German exit capacity 2015 and 2016 2017 and 2018 until 8 March

Maintenance has reduced exit capacity from Germany to Switzerland in summer 2017 and revealed corrosion defects on one of the two pipeline strings which is to be closed until September 2020 for repair - capacity down from 53 to 30 mmcm/d

So max Passo Gries import capacity = 30 +21 (Oltingue) – Swiss demand And PG demand above 30 mmcm/d – Swiss demand comes from France

PEFG Nord at around TTF - 0.2 gives cost of marginal supply of TTF + 3.0 €/MWh

-1

0

1

2

3

4

5

6

0

10

20

30

40

50

60

Germanexitmmcm

PassoGries Flowmmcm

Spot PSV/TTF €/MWh

-1

0

1

2

3

4

5

6

0

10

20

30

40

50

60German exitcapacity atWallbachmmcm/d

Passo GriesFlow mmcm

Spot PSV/TTF €/MWh

PSV premium

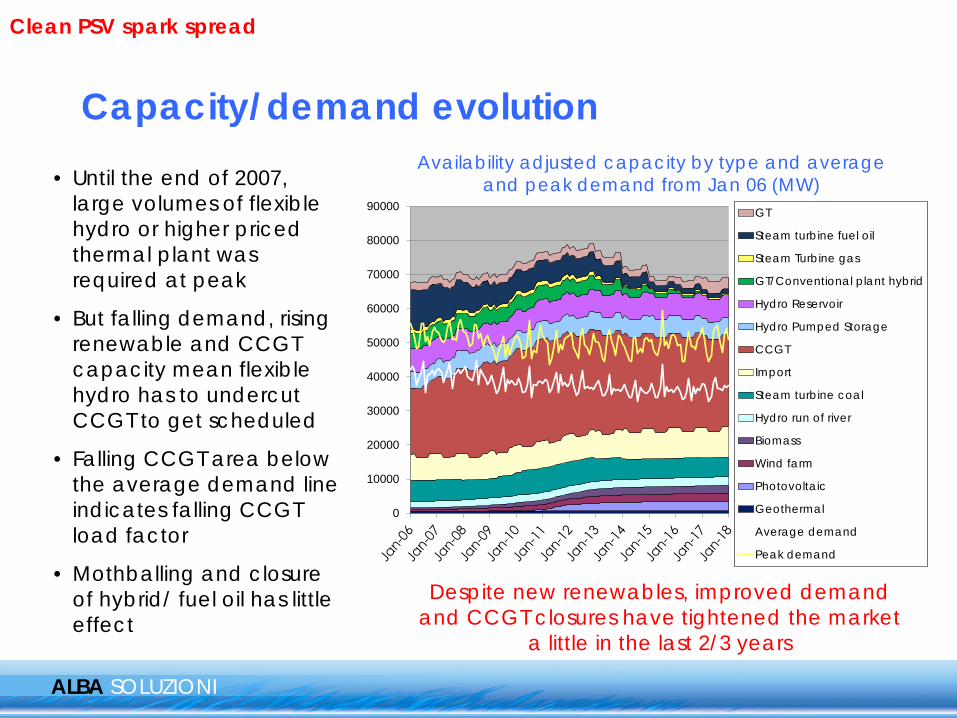

Capacity/demand evolution

ALBA SOLUZIONI

Availability adjusted capacity by type and average and peak demand from Jan 06 (MW)

• Until the end of 2007, large volumes of flexible hydro or higher priced thermal plant was required at peak

• But falling demand, rising renewable and CCGT capacity mean flexible hydro has to undercut CCGT to get scheduled

• Falling CCGT area below the average demand line indicates falling CCGT load factor

• Mothballing and closure of hybrid/ fuel oil has little effect

0

10000

20000

30000

40000

50000

60000

70000

80000

90000 GT

Steam turbine fuel oil

Steam Turbine gas

GT/Conventional plant hybrid

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Average demand

Peak demand

Despite new renewables, improved demand and CCGT closures have tightened the market

a little in the last 2/3 years

Clean PSV spark spread

ALBA SOLUZIONI

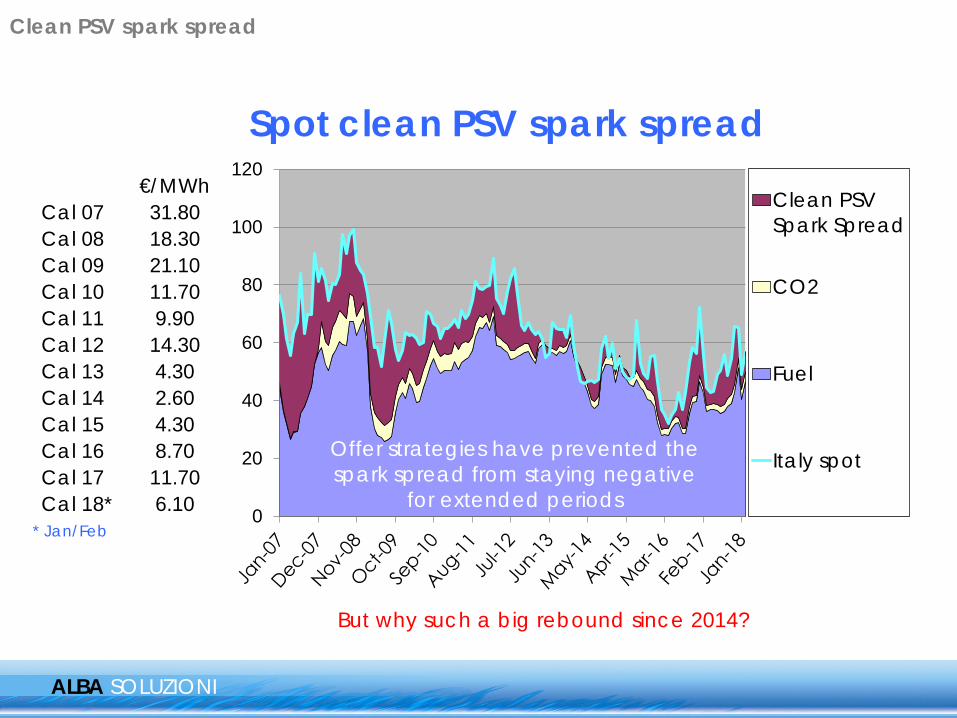

Spot clean PSV spark spread

But why such a big rebound since 2014?

Clean PSV spark spread

* Jan/Feb

€/MWhCal 07 31.80Cal 08 18.30Cal 09 21.10Cal 10 11.70Cal 11 9.90Cal 12 14.30Cal 13 4.30Cal 14 2.60Cal 15 4.30Cal 16 8.70Cal 17 11.70Cal 18* 6.10 0

20

40

60

80

100

120Clean PSVSpark Spread

CO2

Fuel

Italy spotOffer strategies have prevented the spark spread from staying negative

for extended periods

ALBA SOLUZIONI

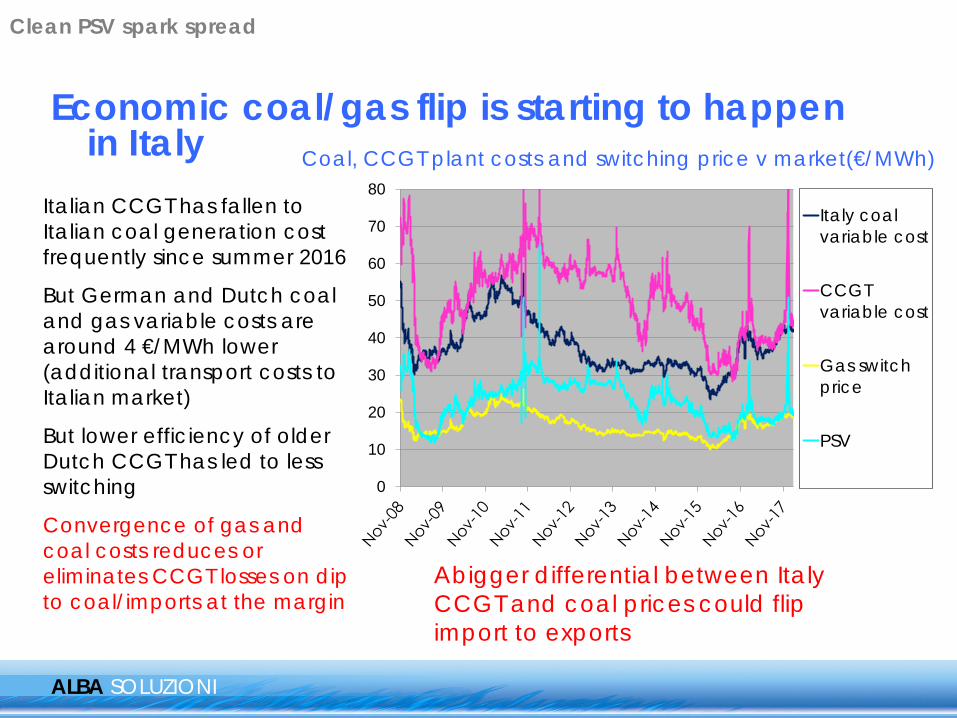

Economic coal/gas flip is starting to happen in Italy Coal, CCGT plant costs and switching price v market(€/MWh)

Italian CCGT has fallen to Italian coal generation cost frequently since summer 2016

But German and Dutch coal and gas variable costs are around 4 €/MWh lower (additional transport costs to Italian market)

But lower efficiency of older Dutch CCGT has led to less switching

Convergence of gas and coal costs reduces or eliminates CCGT losses on dip to coal/imports at the margin

Abigger differential between Italy CCGT and coal prices could flip import to exports

0

10

20

30

40

50

60

70

80Italy coalvariable cost

CCGTvariable cost

Gas switchprice

PSV

Clean PSV spark spread

ALBA SOLUZIONI

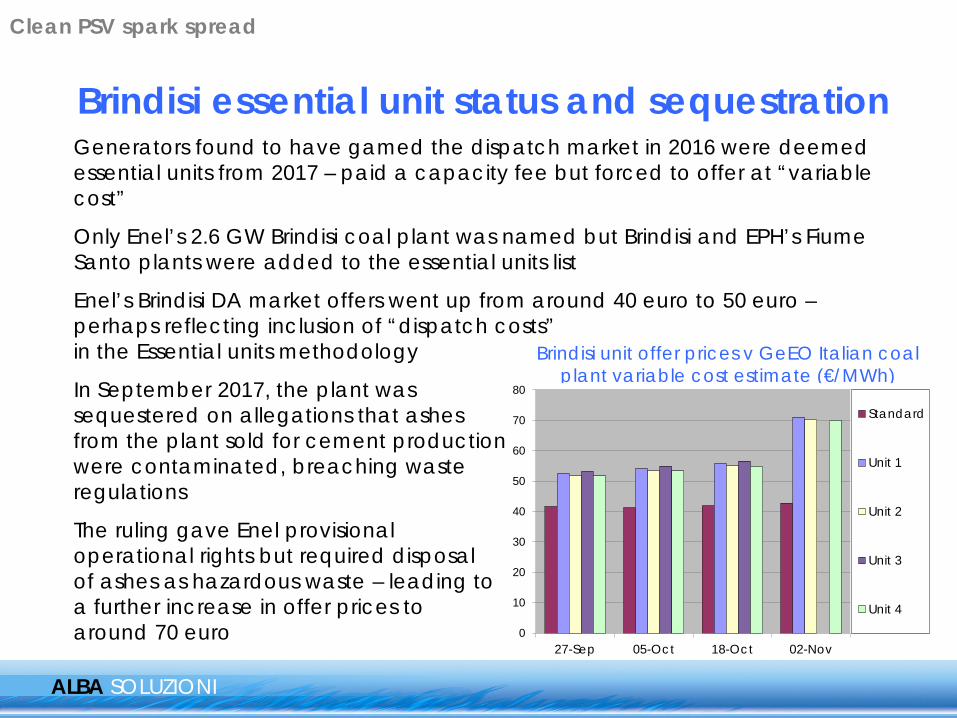

Brindisi essential unit status and sequestration Generators found to have gamed the dispatch market in 2016 were deemed essential units from 2017 – paid a capacity fee but forced to offer at “variable cost”

Only Enel’s 2.6 GW Brindisi coal plant was named but Brindisi and EPH’s Fiume Santo plants were added to the essential units list

Enel’s Brindisi DA market offers went up from around 40 euro to 50 euro – perhaps reflecting inclusion of “dispatch costs” in the Essential units methodology

In September 2017, the plant was sequestered on allegations that ashes from the plant sold for cement production were contaminated, breaching waste regulations

The ruling gave Enel provisional operational rights but required disposal of ashes as hazardous waste – leading to a further increase in offer prices to around 70 euro

Brindisi unit offer prices v GeEO Italian coal plant variable cost estimate (€/MWh)

0

10

20

30

40

50

60

70

80

27-Sep 05-Oct 18-Oct 02-Nov

Standard

Unit 1

Unit 2

Unit 3

Unit 4

Clean PSV spark spread

ALBA SOLUZIONI

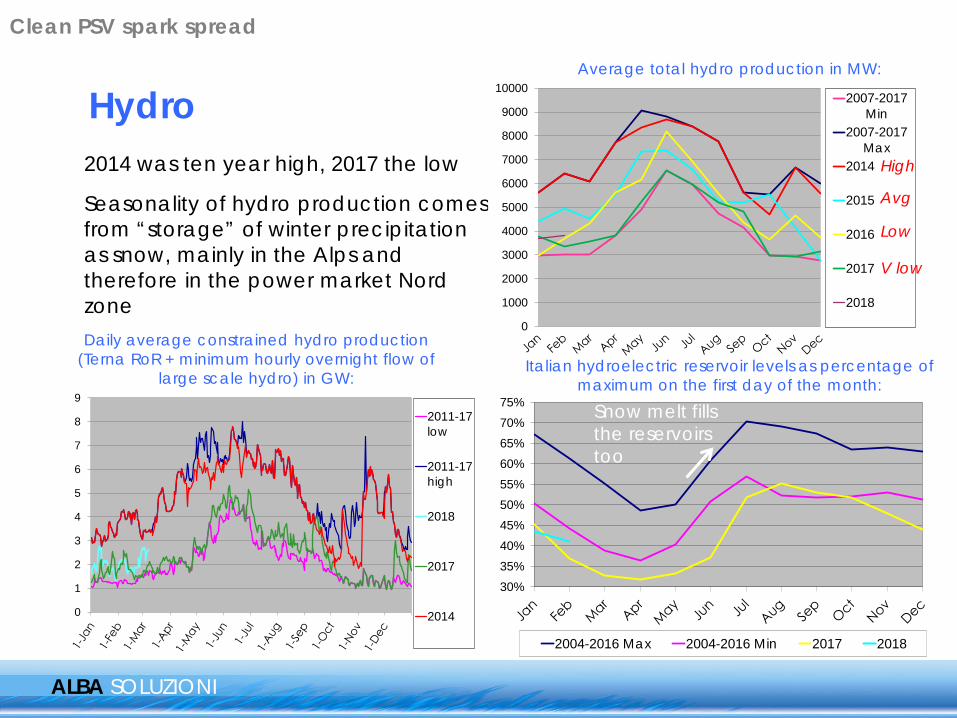

Hydro Average total hydro production in MW:

Italian hydroelectric reservoir levels as percentage of maximum on the first day of the month:

2014 was ten year high, 2017 the low

Seasonality of hydro production comes from “storage” of winter precipitation as snow, mainly in the Alps and therefore in the power market Nord zone Daily average constrained hydro production

(Terna RoR + minimum hourly overnight flow of large scale hydro) in GW:

30%35%40%45%50%55%60%65%70%75%

2004-2016 Max 2004-2016 Min 2017 2018

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

100002007-2017

Min2007-2017

Max2014

2015

2016

2017

2018

0

1

2

3

4

5

6

7

8

92011-17low

2011-17high

2018

2017

2014

Snow melt fills the reservoirs too

Clean PSV spark spread

High Avg Low V low

0

10

20

30

40

50

602015/16nuclear

2016/17nuclear

2017/18nuclear

Coal 2015/16

Coal 2016/17

Coal 2017/18

ALBA SOLUZIONI

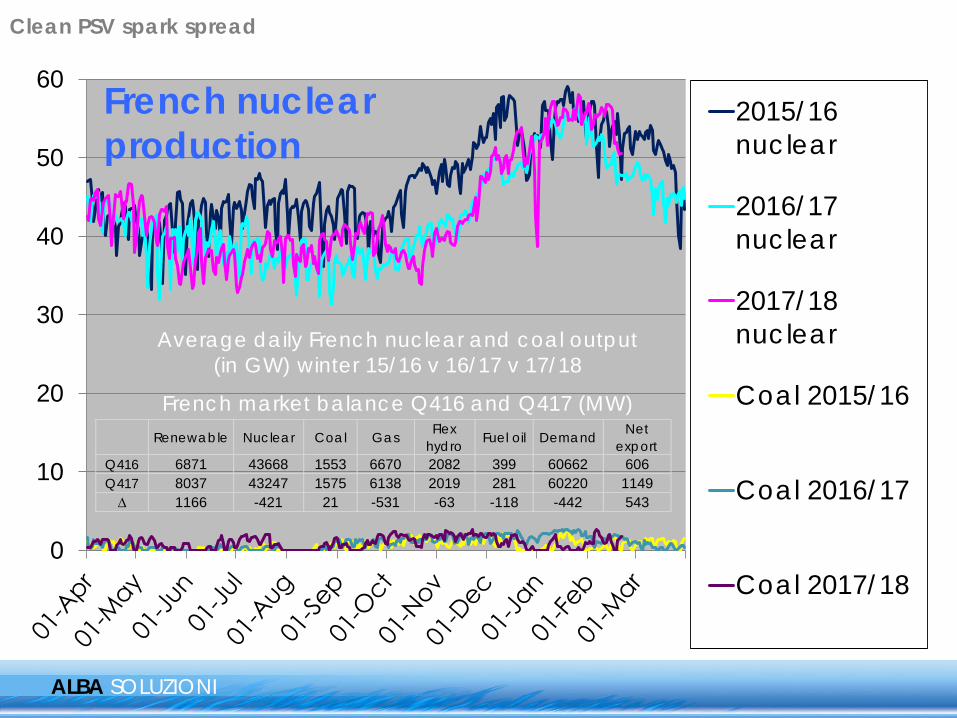

French nuclear production

Average daily French nuclear and coal output (in GW) winter 15/16 v 16/17 v 17/18

French market balance Q416 and Q417 (MW) Renewable Nuclear Coal Gas Flex

hydro Fuel oil Demand Net export

Q416 6871 43668 1553 6670 2082 399 60662 606Q417 8037 43247 1575 6138 2019 281 60220 1149∆ 1166 -421 21 -531 -63 -118 -442 543

Clean PSV spark spread

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000GT

Steam turbine fuel oil

GT/Conventional plant hybrid

Steam Turbine gas

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Peak demand

Average demand

ALBA SOLUZIONI

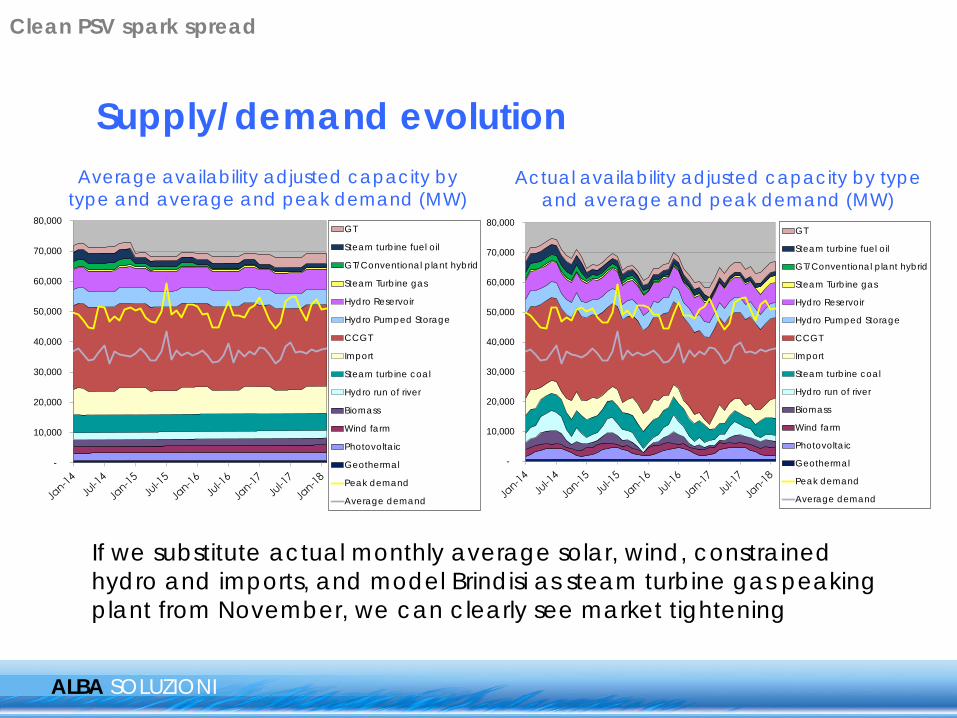

Supply/demand evolution Average availability adjusted capacity by

type and average and peak demand (MW) Actual availability adjusted capacity by type

and average and peak demand (MW)

If we substitute actual monthly average solar, wind, constrained hydro and imports, and model Brindisi as steam turbine gas peaking plant from November, we can clearly see market tightening

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000GT

Steam turbine fuel oil

GT/Conventional plant hybrid

Steam Turbine gas

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Peak demand

Average demand

Clean PSV spark spread

-6

-4

-2

0

2

4

6

Demand

Import

Hydro

Wind

Solar

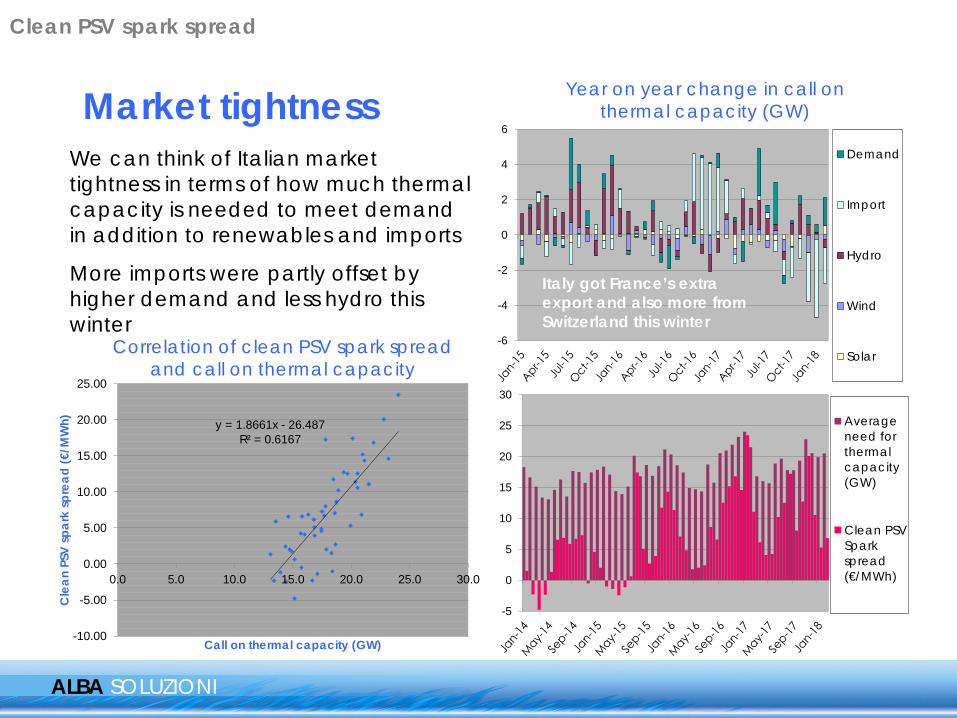

Market tightness

ALBA SOLUZIONI

We can think of Italian market tightness in terms of how much thermal capacity is needed to meet demand in addition to renewables and imports

More imports were partly offset by higher demand and less hydro this winter

Year on year change in call on thermal capacity (GW)

y = 1.8661x - 26.487R² = 0.6167

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Cle

an P

SV sp

ark

spre

ad (€

/MW

h)

Call on thermal capacity (GW)

Correlation of clean PSV spark spread and call on thermal capacity

Italy got France’s extra export and also more from Switzerland this winter

-5

0

5

10

15

20

25

30

Averageneed forthermalcapacity(GW)

Clean PSV Spark spread (€/MWh)

Clean PSV spark spread

ALBA SOLUZIONI

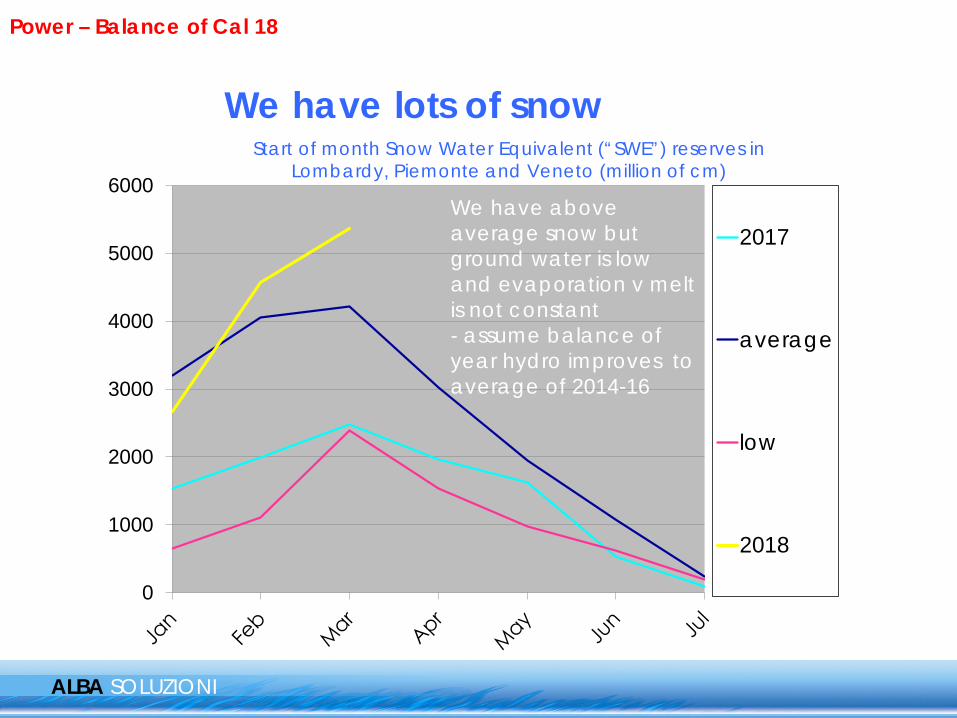

We have lots of snow

0

1000

2000

3000

4000

5000

6000

2017

average

low

2018

Start of month Snow Water Equivalent (“SWE”) reserves in Lombardy, Piemonte and Veneto (million of cm)

We have above average snow but ground water is low and evaporation v melt is not constant - assume balance of year hydro improves to average of 2014-16

Power – Balance of Cal 18

ASN has asked EdF to examine and report on the manufacturing files of components manufactured at Creusot Forge foundry in all of its 58 reactors

Only 12 have been done so far, most of the remaining 46 will close for refuelling over the summer

EdF annual production forecast is close to the four year average, so looks like some delays are anticipated due to several 10 year inspections scheduled

ALBA SOLUZIONI

French nuclear still risk for Q418?

Average daily nuclear output (in GW)

0

10

20

30

40

50

602015/16nuclear

2016/17nuclear

2017/18nuclear

Coal 2015/16

Coal 2016/17

Coal 2017/18

Annual nuclear output (in TWh)

So assume imports at average of last 4 years?

0

50

100

150

200

250

300

350

400

450

2015 2015 2016 2017 2018

Annualproduction

EdFForecast

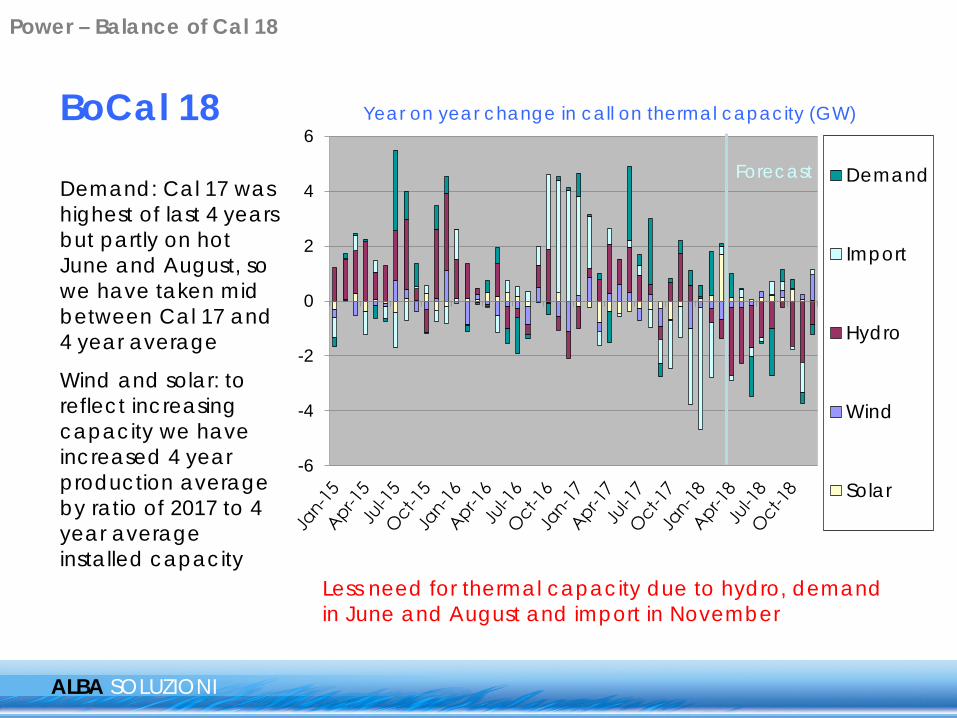

Power – Balance of Cal 18

ALBA SOLUZIONI

BoCal 18

Demand: Cal 17 was highest of last 4 years but partly on hot June and August, so we have taken mid between Cal 17 and 4 year average

Wind and solar: to reflect increasing capacity we have increased 4 year production average by ratio of 2017 to 4 year average installed capacity

-6

-4

-2

0

2

4

6

Demand

Import

Hydro

Wind

Solar

Year on year change in call on thermal capacity (GW)

Less need for thermal capacity due to hydro, demand in June and August and import in November

Forecast

Power – Balance of Cal 18

ALBA SOLUZIONI

Balance of 2018 curve v 2017 v model Curve prices on 15 March 2018 (€/MWh)

Market has already priced in an increase in hydro output

Use of 2 year correlation (less coal) takes us 1.50 euro higher

1% increase to Cal 17 level demand takes us 0.50 euro higher

Italia It/Fr It/GerClean SS PSV

CSS Cal 17 ∆ YoY Model

∆ v model

Apr 47.75 9.65 14.00 1.55 4.09 -2.54 -0.17 1.72Mag 44.60 14.15 14.55 0.10 4.25 -4.15 -0.57 0.67Giu 47.90 14.45 15.25 3.30 10.23 -6.93 2.33 0.97Q218 46.75 12.75 14.60 1.65 6.19 -4.54 0.53 1.12Q318 52.85 18.25 18.70 8.35 12.59 -4.24 6.46 1.89Sum-18 49.80 15.50 16.65 5.00 9.39 -4.39 3.49 1.51Q418 55.10 5.65 16.25 9.20 14.46 -5.26 9.67 -0.47

0.00

2.00

4.00

6.00

8.00

10.00

12.00

2-Oct 2-Nov 2-Dec 2-Jan 2-Feb 2-Mar

Q418

S18Clean PSV spark spreads in €/MWh

Power – Balance of Cal 18

April CSS outturn -0.22 €/MWh

-2000

0

2000

4000

6000

8000

10000

12000

14000Previous Min2004-2015

Previous Max2004-2015

SY16

SY17

Demand

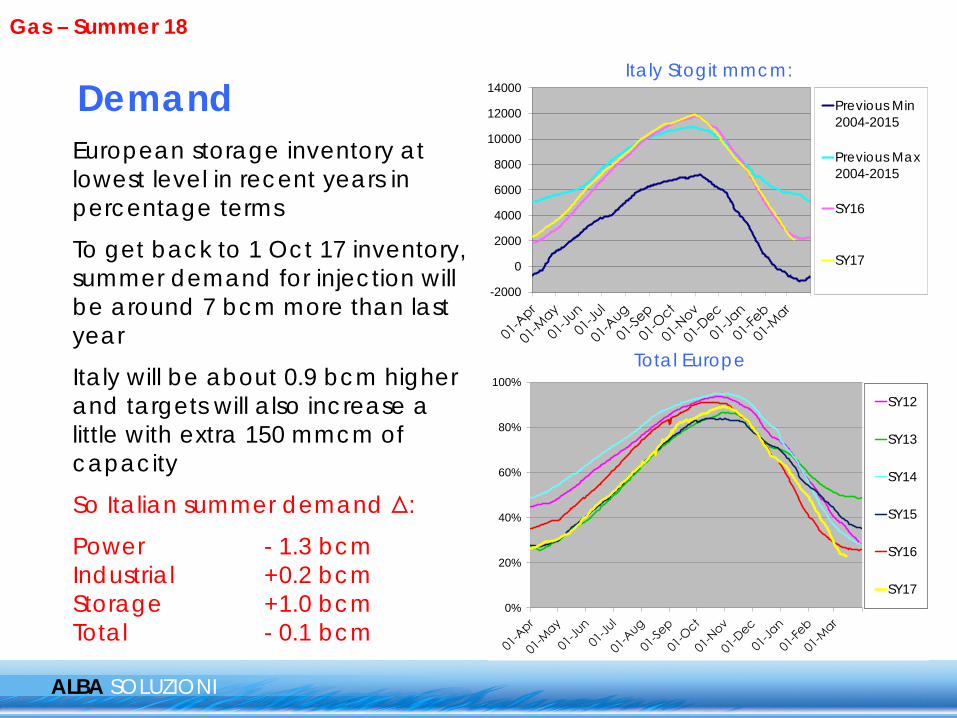

ALBA SOLUZIONI

European storage inventory at lowest level in recent years in percentage terms

To get back to 1 Oct 17 inventory, summer demand for injection will be around 7 bcm more than last year

Italy will be about 0.9 bcm higher and targets will also increase a little with extra 150 mmcm of capacity

So Italian summer demand Δ:

Power - 1.3 bcm Industrial +0.2 bcm Storage +1.0 bcm Total - 0.1 bcm

Italy Stogit mmcm:

Total Europe

0%

20%

40%

60%

80%

100%

SY12

SY13

SY14

SY15

SY16

SY17

Gas – Summer 18

ALBA SOLUZIONI

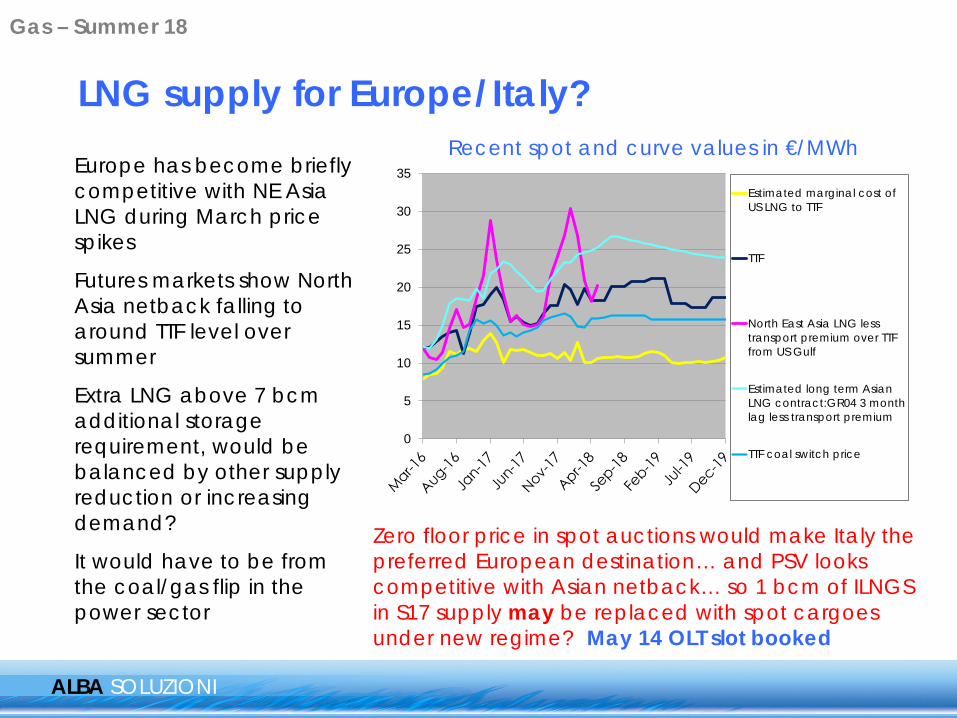

LNG supply for Europe/Italy? Recent spot and curve values in €/MWh

Europe has become briefly competitive with NE Asia LNG during March price spikes

Futures markets show North Asia netback falling to around TTF level over summer

Extra LNG above 7 bcm additional storage requirement, would be balanced by other supply reduction or increasing demand?

It would have to be from the coal/gas flip in the power sector

Zero floor price in spot auctions would make Italy the preferred European destination… and PSV looks competitive with Asian netback… so 1 bcm of ILNGS in S17 supply may be replaced with spot cargoes under new regime? May 14 OLT slot booked

Gas – Summer 18

0

5

10

15

20

25

30

35Estimated marginal cost ofUS LNG to TTF

TTF

North East Asia LNG lesstransport premium over TTFfrom US Gulf

Estimated long term AsianLNG contract:GR04 3 monthlag less transport premium

TTF coal switch price

0

10

20

30

40

50

60

70

80

90

100

Mazaradel Vallo

Tarvisio PassoGries

Gela LNG NationalProduction

Sum-13

Sum-14

Sum-15

Sum-16

Sum-17

ALBA SOLUZIONI

Long term contract supply for Italy Tarvsio supply was flat Oct-Mar – so same ToP flow over summer?

Despite short term capacity bookings and reports of new production coming on line, Algerian supply over winter was very similar to GY16 at around 70 mmcm/d so if annual contract volumes are unchanged, we would expect similar supply this year

But there could be upside if new production gives excess volumes to export?

So Italian summer supply Δ:

Russia flat Algeria possible increase LNG possible decrease Net flat?

Summer Average daily supply (mmcm/d)

0

10

20

30

40

50

60

70

80

90

100

Monthlybooking

Quarterlybooking

Annualbooking

Long termbooking

GY17 entry capacity bookings at Mazara del Vallo (mmcm/g)

Gas – Summer 18

0

10

20

30

40

50

60

70

80

90

100

Mazaradel Vallo

Tarvisio PassoGries

Gela LNG NationalProduction

Sum-13

Sum-14

Sum-15

Sum-16

Sum-17

ALBA SOLUZIONI

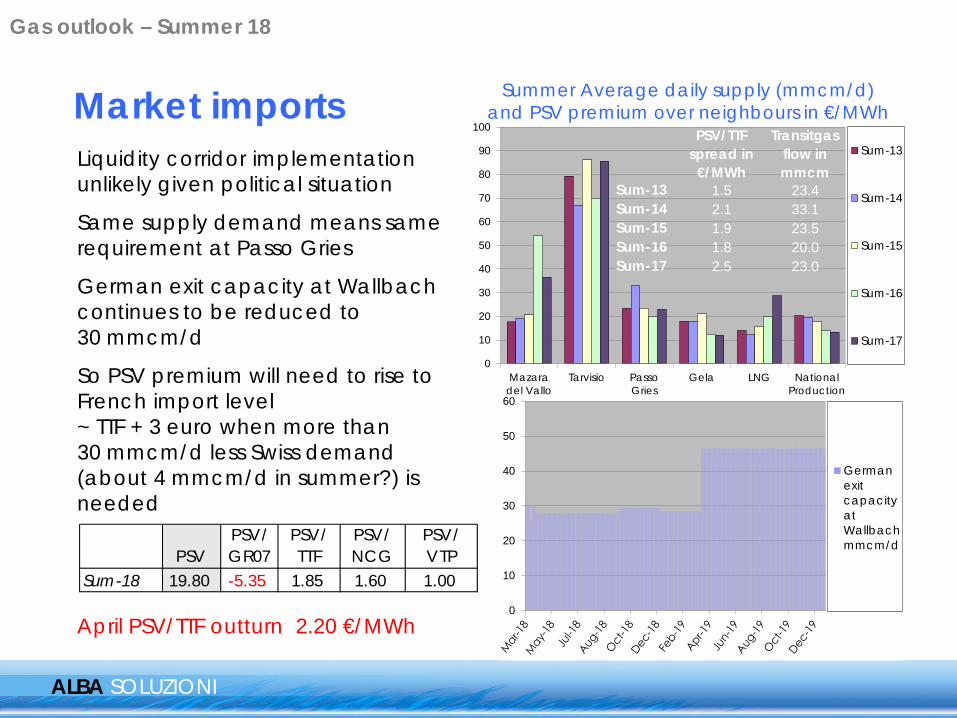

Market imports Liquidity corridor implementation unlikely given political situation

Same supply demand means same requirement at Passo Gries

German exit capacity at Wallbach continues to be reduced to 30 mmcm/d

So PSV premium will need to rise to French import level ~ TTF + 3 euro when more than 30 mmcm/d less Swiss demand (about 4 mmcm/d in summer?) is needed

Summer Average daily supply (mmcm/d) and PSV premium over neighbours in €/MWh

PSV/TTF spread in €/MWh

Transitgas flow in mmcm

Sum-13 1.5 23.4Sum-14 2.1 33.1Sum-15 1.9 23.5Sum-16 1.8 20.0Sum-17 2.5 23.0

0

10

20

30

40

50

60

GermanexitcapacityatWallbachmmcm/d

PSVPSV/ GR07

PSV/ TTF

PSV/ NCG

PSV/ VTP

Sum-18 19.80 -5.35 1.85 1.60 1.00

Gas outlook – Summer 18

April PSV/TTF outturn 2.20 €/MWh

12

13

14

15

16

17

18

19

02-Jul 02-Aug 02-Sep 02-Oct

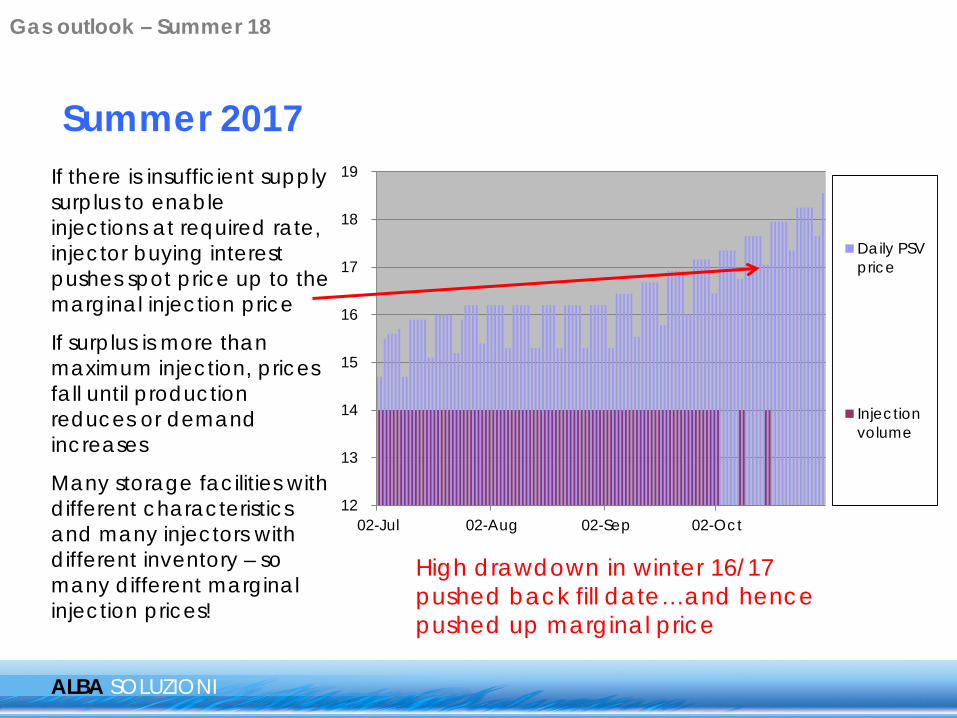

Daily PSVprice

Injectionvolume

ALBA SOLUZIONI

If there is insufficient supply surplus to enable injections at required rate, injector buying interest pushes spot price up to the marginal injection price

If surplus is more than maximum injection, prices fall until production reduces or demand increases

Many storage facilities with different characteristics and many injectors with different inventory – so many different marginal injection prices!

Summer 2017

High drawdown in winter 16/17 pushed back fill date…and hence pushed up marginal price

Gas outlook – Summer 18

14

15

16

17

18

19

20

PSV spot

PSV Oct

TTF spot

TTF Oct

ALBA SOLUZIONI

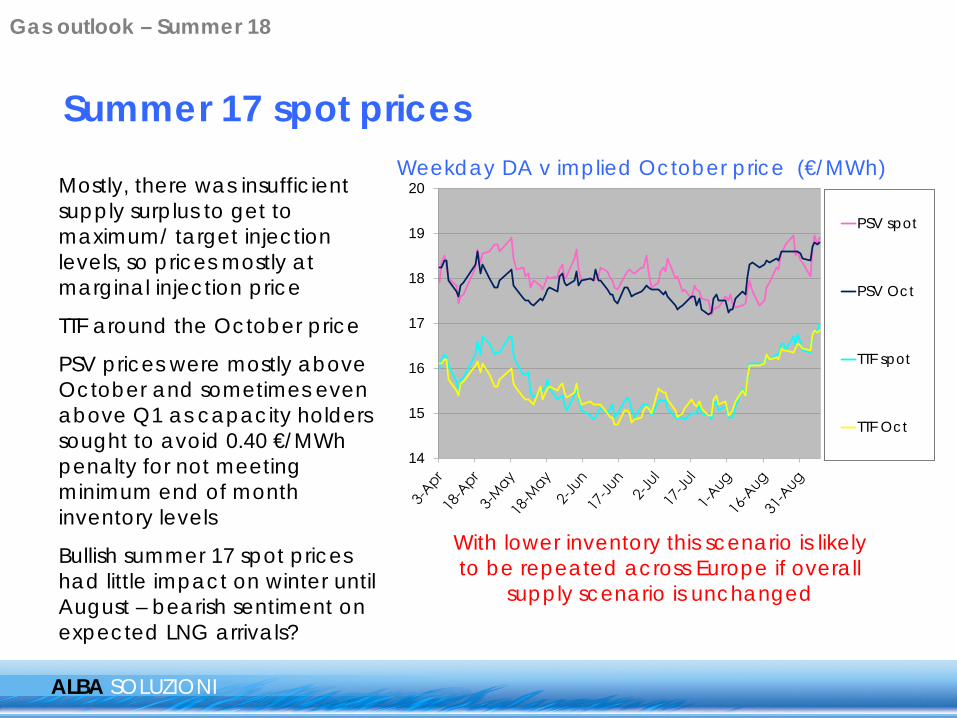

Mostly, there was insufficient supply surplus to get to maximum/ target injection levels, so prices mostly at marginal injection price

TTF around the October price

PSV prices were mostly above October and sometimes even above Q1 as capacity holders sought to avoid 0.40 €/MWh penalty for not meeting minimum end of month inventory levels

Bullish summer 17 spot prices had little impact on winter until August – bearish sentiment on expected LNG arrivals?

Summer 17 spot prices Weekday DA v implied October price (€/MWh)

With lower inventory this scenario is likely to be repeated across Europe if overall

supply scenario is unchanged

Gas outlook – Summer 18

Demand scenarios

ALBA SOLUZIONI

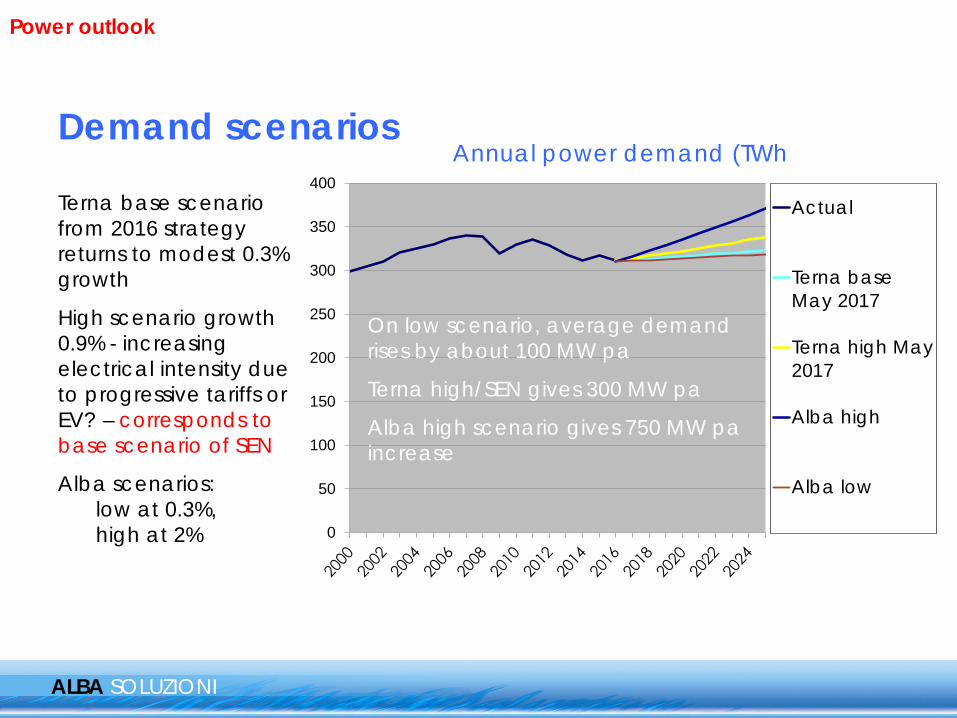

Annual power demand (TWh

Terna base scenario from 2016 strategy returns to modest 0.3% growth

High scenario growth 0.9% - increasing electrical intensity due to progressive tariffs or EV? – corresponds to base scenario of SEN

Alba scenarios: low at 0.3%, high at 2%

Power outlook

0

50

100

150

200

250

300

350

400Actual

Terna baseMay 2017

Terna high May2017

Alba high

Alba low

On low scenario, average demand rises by about 100 MW pa

Terna high/SEN gives 300 MW pa

Alba high scenario gives 750 MW pa increase

0

100

200

300

400

500

600

700

800

900

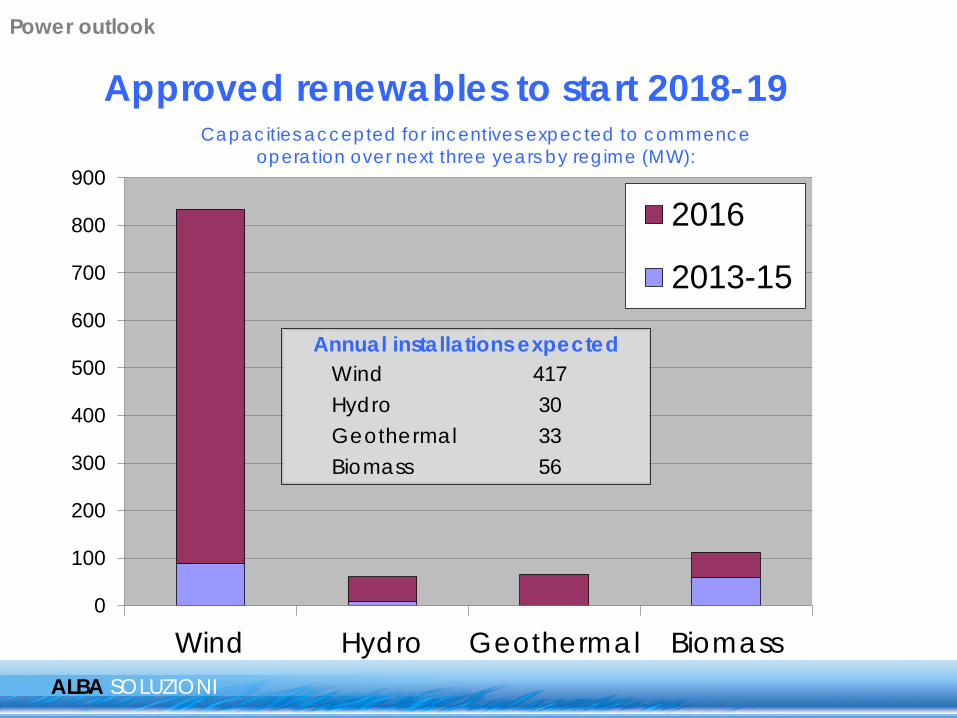

Wind Hydro Geothermal Biomass

2016

2013-15

Wind 417Hydro 30Geothermal 33Biomass 56

Annual installations expected

ALBA SOLUZIONI

Approved renewables to start 2018-19

Power outlook

Capacities accepted for incentives expected to commence operation over next three years by regime (MW):

ALBA SOLUZIONI

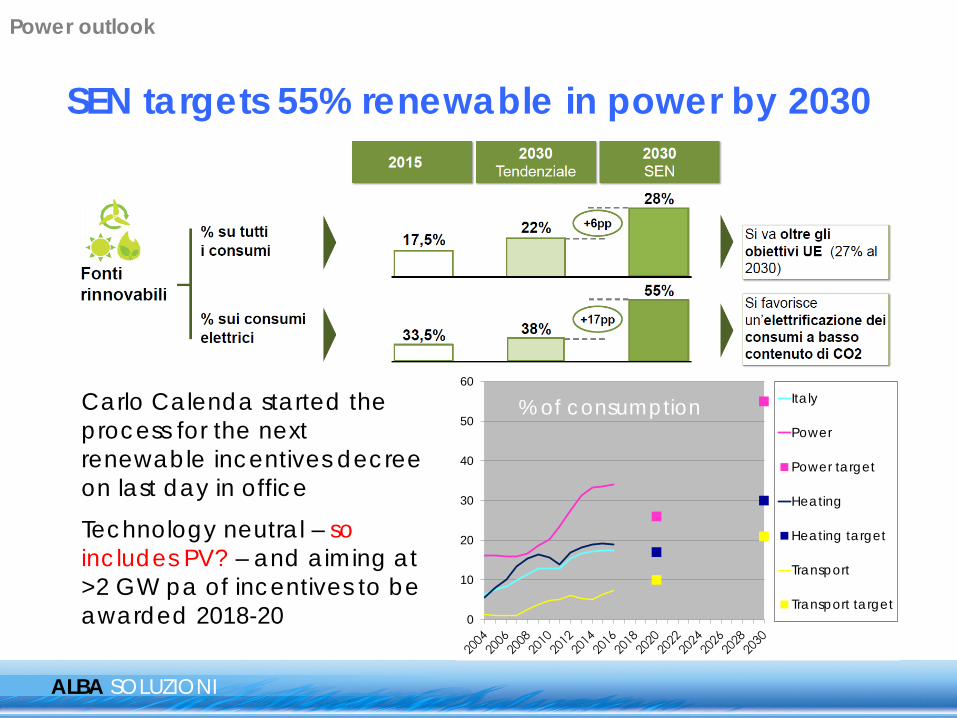

SEN targets 55% renewable in power by 2030

0

10

20

30

40

50

60Italy

Power

Power target

Heating

Heating target

Transport

Transport target

% of consumption Carlo Calenda started the process for the next renewable incentives decree on last day in office

Technology neutral – so includes PV? – and aiming at >2 GW pa of incentives to be awarded 2018-20

Power outlook

ALBA SOLUZIONI

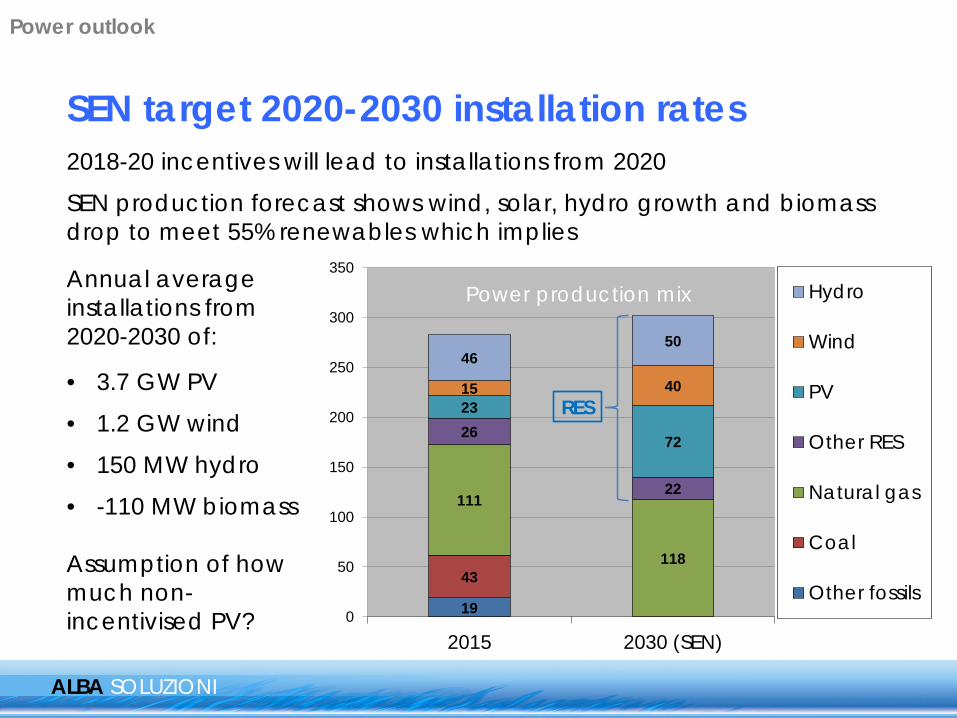

SEN target 2020-2030 installation rates

2018-20 incentives will lead to installations from 2020

SEN production forecast shows wind, solar, hydro growth and biomass drop to meet 55% renewables which implies

19

43

111

118

26

22

23

72

15 40

4650

0

50

100

150

200

250

300

350

2015 2030 (SEN)

Hydro

Wind

PV

Other RES

Natural gas

Coal

Other fossils

RES

Annual average installations from 2020-2030 of:

• 3.7 GW PV

• 1.2 GW wind

• 150 MW hydro

• -110 MW biomass Assumption of how much non-incentivised PV?

Power production mix

Power outlook

ALBA SOLUZIONI

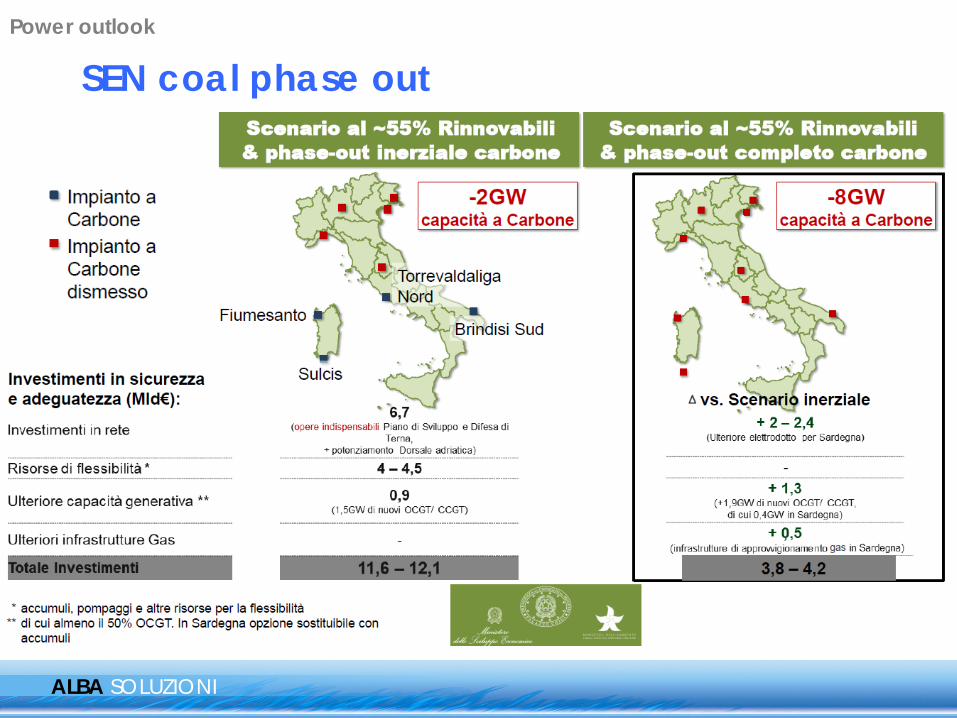

SEN coal phase out Power outlook

ALBA SOLUZIONI

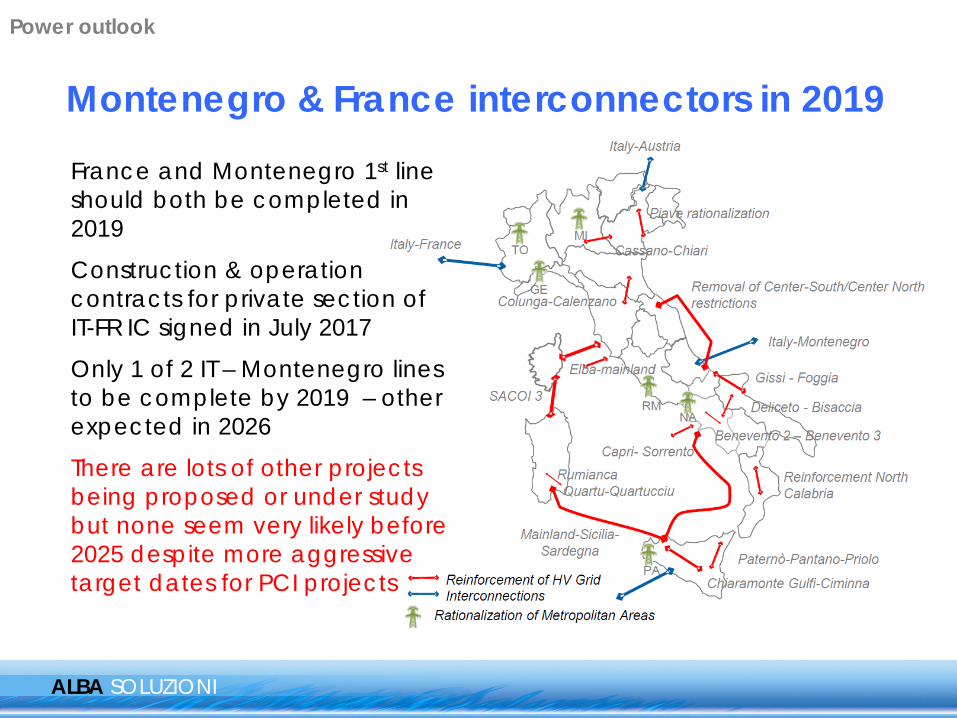

France and Montenegro 1st line should both be completed in 2019

Construction & operation contracts for private section of IT-FR IC signed in July 2017

Only 1 of 2 IT – Montenegro lines to be complete by 2019 – other expected in 2026

There are lots of other projects being proposed or under study but none seem very likely before 2025 despite more aggressive target dates for PCI projects

Montenegro & France interconnectors in 2019

Power outlook

ALBA SOLUZIONI

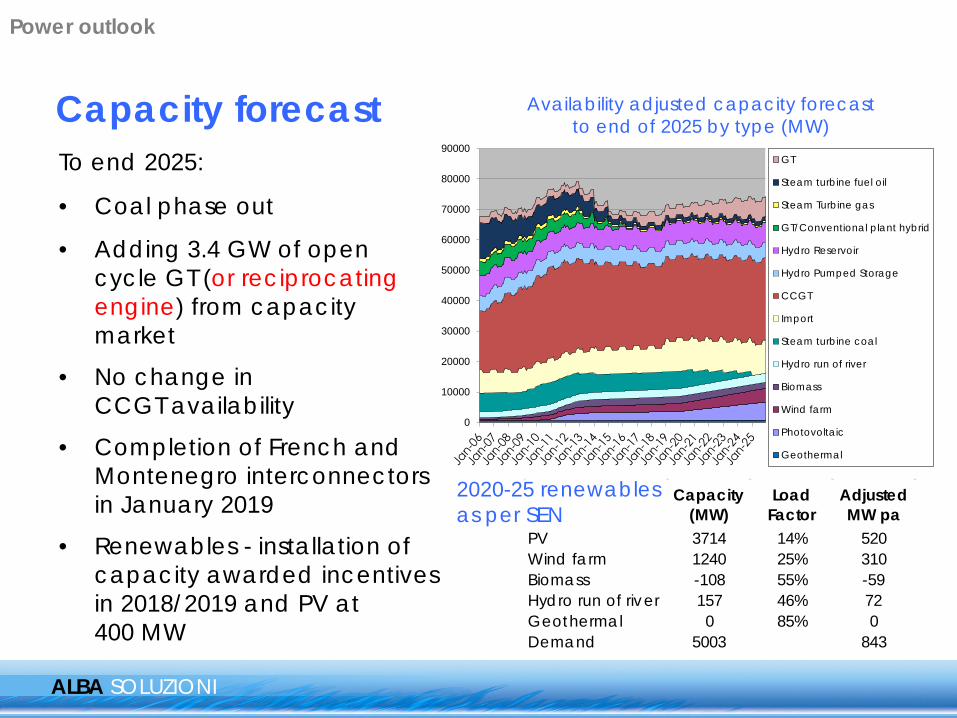

Capacity forecast Availability adjusted capacity forecast to end of 2025 by type (MW)

To end 2025:

• Coal phase out

• Adding 3.4 GW of open cycle GT (or reciprocating engine) from capacity market

• No change in CCGT availability

• Completion of French and Montenegro interconnectors in January 2019

• Renewables - installation of capacity awarded incentives in 2018/2019 and PV at 400 MW

0

10000

20000

30000

40000

50000

60000

70000

80000

90000GT

Steam turbine fuel oil

Steam Turbine gas

GT/Conventional plant hybrid

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Capacity (MW)

Load Factor

Adjusted MW pa

PV 3714 14% 520Wind farm 1240 25% 310Biomass -108 55% -59Hydro run of river 157 46% 72Geothermal 0 85% 0Demand 5003 843

2020-25 renewables as per SEN

Power outlook

0

10000

20000

30000

40000

50000

60000

70000

80000

90000GT

Steam turbine fuel oil

GT/Conventional plant hybrid

Steam Turbine gas

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Peak demand

Average demand

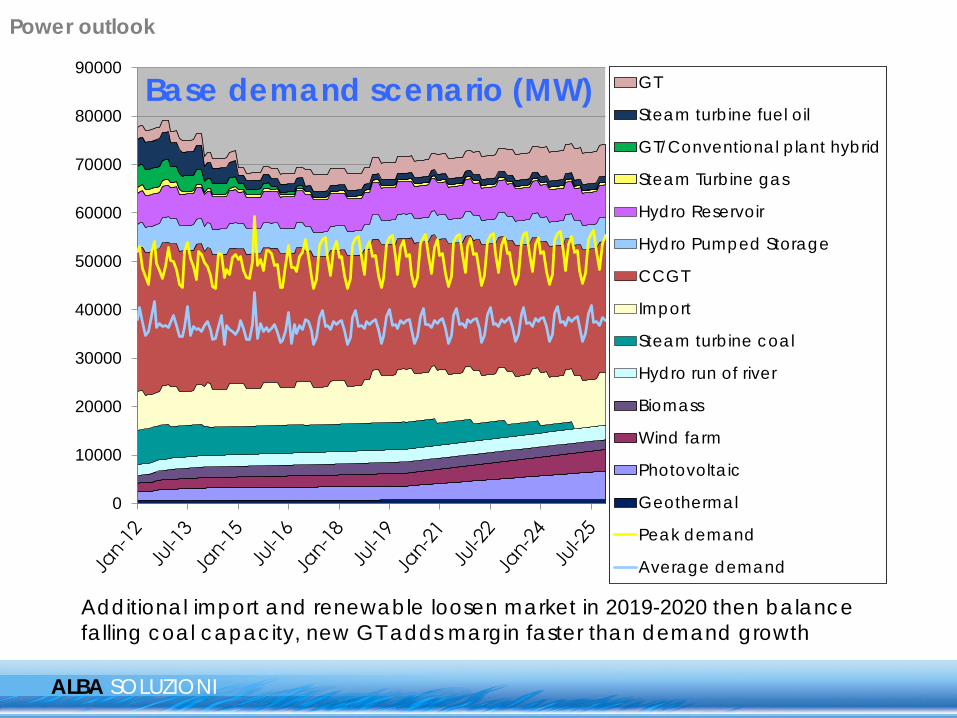

Base demand scenario (MW)

ALBA SOLUZIONI

Additional import and renewable loosen market in 2019-2020 then balance falling coal capacity, new GT adds margin faster than demand growth

Power outlook

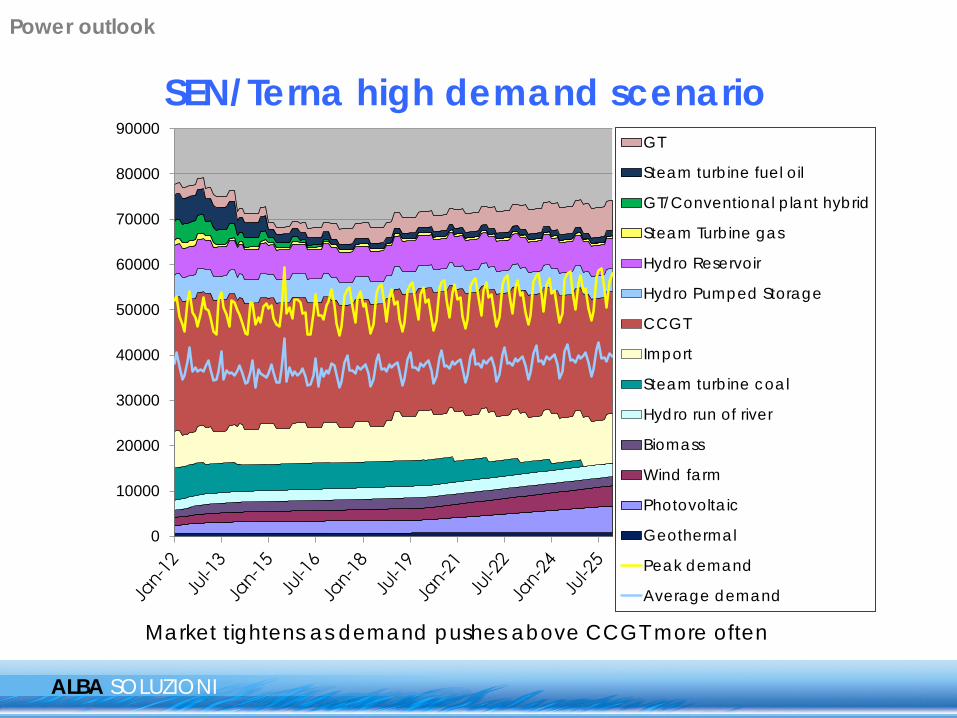

SEN/Terna high demand scenario (MW)

ALBA SOLUZIONI

Market tightens as demand pushes above CCGT more often

0

10000

20000

30000

40000

50000

60000

70000

80000

90000GT

Steam turbine fuel oil

GT/Conventional plant hybrid

Steam Turbine gas

Hydro Reservoir

Hydro Pumped Storage

CCGT

Import

Steam turbine coal

Hydro run of river

Biomass

Wind farm

Photovoltaic

Geothermal

Peak demand

Average demand

Power outlook

ALBA SOLUZIONI

Cal 18 backwardation on expected improvement in French nuclear availability and hydro

Cal 19/20 backwardation driven by new interconnectors

SEN target renewable installation rate would allow phase out of coal without overall tightening

Flexibility from storage will help smooth out diurnal profile in summer

But winter peaks on calm, cloudy days?

Conclusions - Power Average spot clean

PSV spark spread

Italia It/Fr It/GerClean SS PSV

Cal 19 48.35 8.45 13.75 5.75Cal 20 46.05 6.50 12.10 5.55

€/MWhCal 07 31.80Cal 08 18.30Cal 09 21.10Cal 10 11.70Cal 11 9.90Cal 12 14.30Cal 13 4.30Cal 14 2.60Cal 15 4.30Cal 16 8.70Cal 17 11.80Cal 18 6.10Cal 19 5.75Cal 20 5.55

Power outlook

0

5

10

15

20

25

30

35

40

45

50

Italy coal

CCGT

switch price

PSV

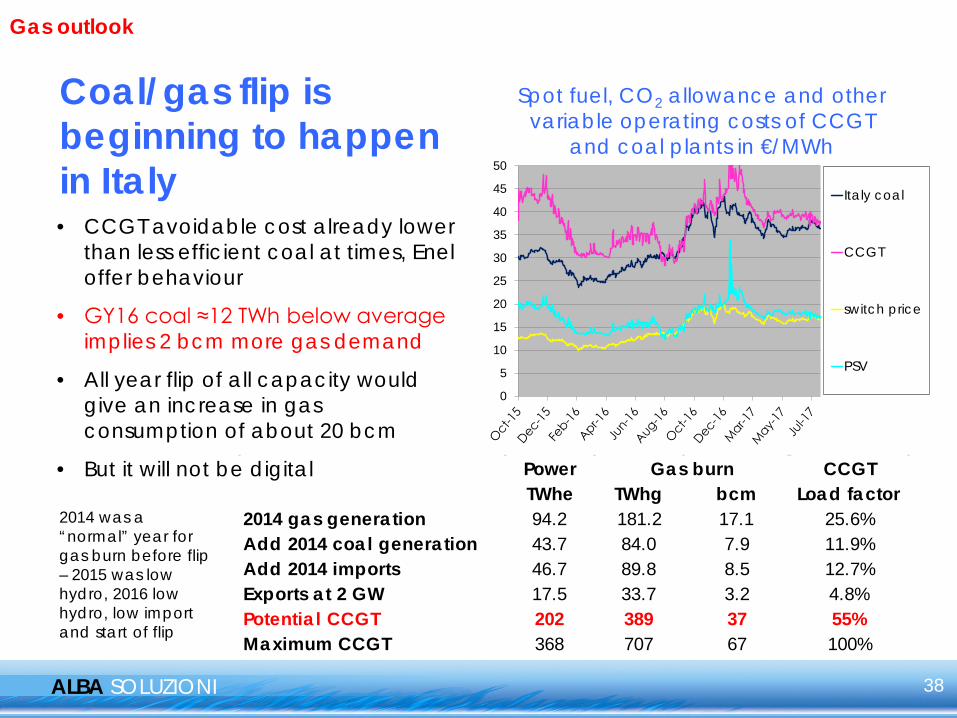

Coal/gas flip is beginning to happen in Italy

ALBA SOLUZIONI

Spot fuel, CO2 allowance and other variable operating costs of CCGT

and coal plants in €/MWh

Power CCGTTWhe TWhg bcm Load factor

2014 gas generation 94.2 181.2 17.1 25.6%Add 2014 coal generation 43.7 84.0 7.9 11.9%Add 2014 imports 46.7 89.8 8.5 12.7%Exports at 2 GW 17.5 33.7 3.2 4.8%Potential CCGT 202 389 37 55%Maximum CCGT 368 707 67 100%

Gas burn

• CCGT avoidable cost already lower than less efficient coal at times, Enel offer behaviour

• GY16 coal ≈12 TWh below average implies 2 bcm more gas demand

• All year flip of all capacity would give an increase in gas consumption of about 20 bcm

• But it will not be digital

2014 was a “normal” year for gas burn before flip – 2015 was low hydro, 2016 low hydro, low import and start of flip

38

Gas outlook

0

20

40

60

80

100

120Actual

Feb 2009 SRGforecast

2017 SRG low

2017 SRG high

Alba base

Alba flip

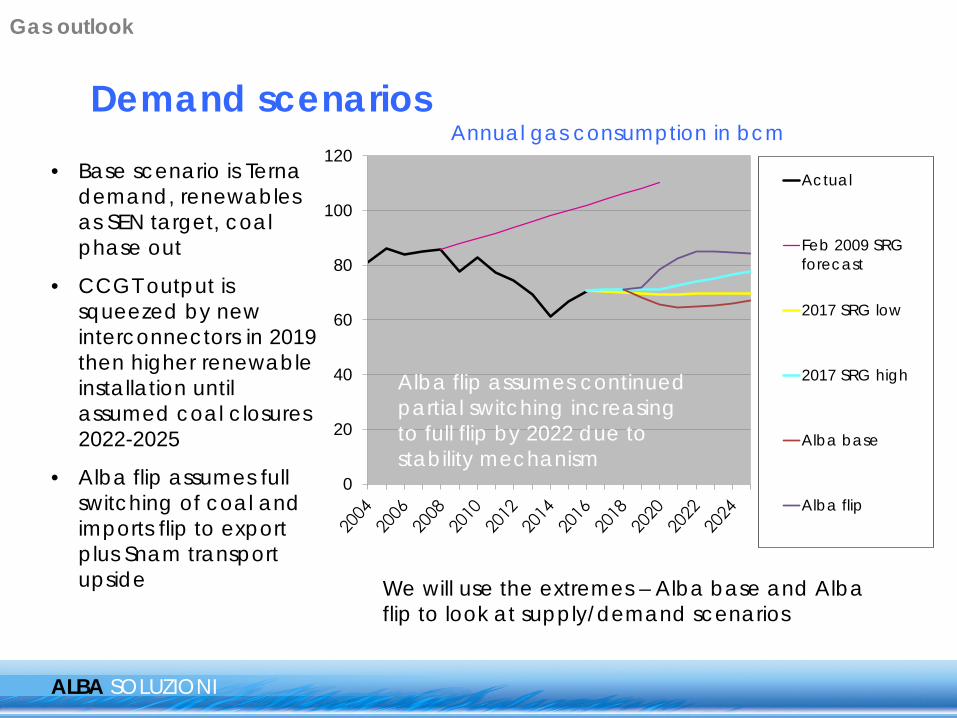

Demand scenarios

ALBA SOLUZIONI

• Base scenario is Terna demand, renewables as SEN target, coal phase out

• CCGT output is squeezed by new interconnectors in 2019 then higher renewable installation until assumed coal closures 2022-2025

• Alba flip assumes full switching of coal and imports flip to export plus Snam transport upside

Annual gas consumption in bcm

Alba flip assumes continued partial switching increasing to full flip by 2022 due to stability mechanism

We will use the extremes – Alba base and Alba flip to look at supply/demand scenarios

Gas outlook

ALBA SOLUZIONI

Long Term ToP from Algeria, Libya, TAP, LNG including outages and ToP adjustments

Annualised ToP plus northern supply capacity and demand in (bcm) - existing and committed infrastructure ToP assumed at 90% of

Libyan and TAP capacity, 6.4 bcm at ALNG/Rovigo

Algeria ToP forecast based on current supply

TAG and Transitgas included at 100% of annual supply capacity

There is still ample margin without Algerian renewal in low demand scenario Contract issues:

2019 Ukraine and Tunisian transit expiry

-

10

20

30

40

50

60

70

80

90

100 Transitgas

TAG

Back up LNG

TAP

Rovigo

Transmed

Panigaglia

Greenstream

Gorizia

Production

Alba low power/highrenewables

Alba flip

Gas outlook

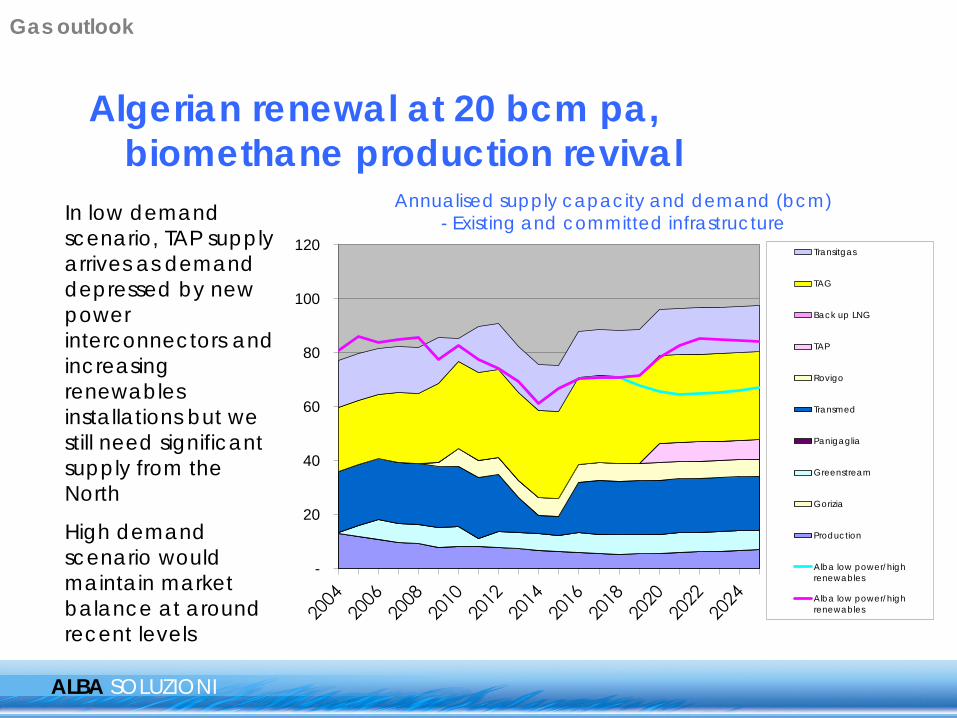

Algerian renewal at 20 bcm pa, biomethane production revival

ALBA SOLUZIONI

Annualised supply capacity and demand (bcm) - Existing and committed infrastructure In low demand

scenario, TAP supply arrives as demand depressed by new power interconnectors and increasing renewables installations but we still need significant supply from the North

High demand scenario would maintain market balance at around recent levels

-

20

40

60

80

100

120 Transitgas

TAG

Back up LNG

TAP

Rovigo

Transmed

Panigaglia

Greenstream

Gorizia

Production

Alba low power/highrenewables

Alba low power/highrenewables

Gas outlook

Conclusions - Gas

ALBA SOLUZIONI

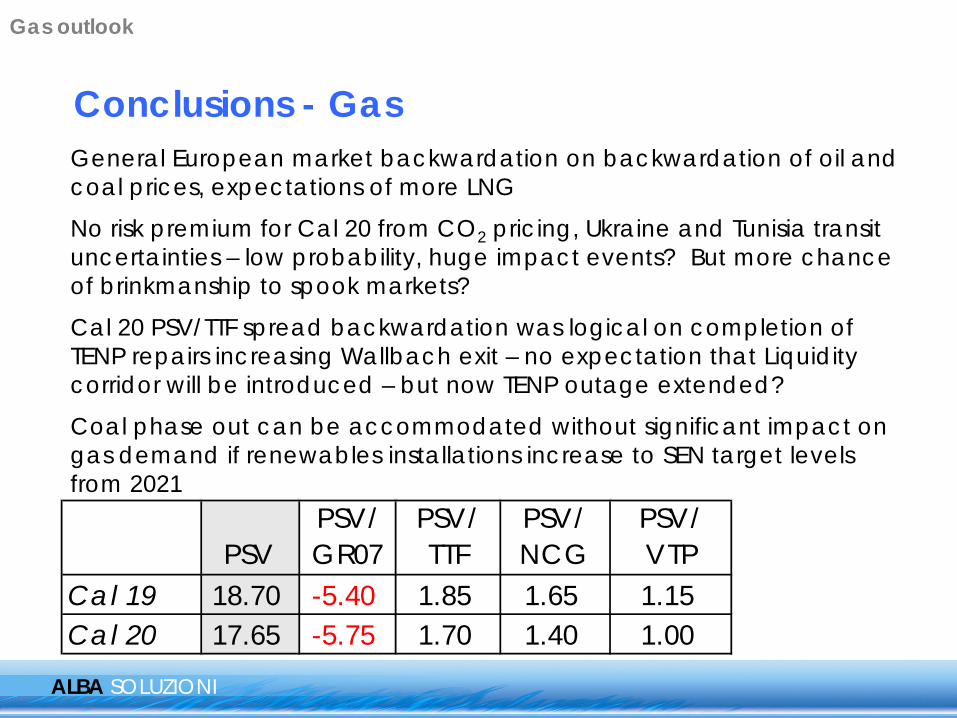

General European market backwardation on backwardation of oil and coal prices, expectations of more LNG

No risk premium for Cal 20 from CO2 pricing, Ukraine and Tunisia transit uncertainties – low probability, huge impact events? But more chance of brinkmanship to spook markets?

Cal 20 PSV/TTF spread backwardation was logical on completion of TENP repairs increasing Wallbach exit – no expectation that Liquidity corridor will be introduced – but now TENP outage extended?

Coal phase out can be accommodated without significant impact on gas demand if renewables installations increase to SEN target levels from 2021

Gas outlook

PSVPSV/ GR07

PSV/ TTF

PSV/ NCG

PSV/ VTP

Cal 19 18.70 -5.40 1.85 1.65 1.15Cal 20 17.65 -5.75 1.70 1.40 1.00