36

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION) PROJECT NO. 016-EE-031 FINANCIAL STATEMENTS June 30, 2016

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

PROJECT NO. 016-EE-031

FINANCIAL STATEMENTS

June 30, 2016

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

FINANCIAL STATEMENTS

June 30, 2016

CONTENTS

PAGES

Independent Auditors' Report 1-2

Financial Statements:

Statement of Financial Position 3-4

Statement of Activities 5-6

Statement of Changes in Net Deficit 7

Statement of Cash Flows 8-9

Notes to Financial Statements 10-14

Supporting Data Required by HUD 15-25

Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 26-27

Independent Auditors' Report on Compliance For Each Major Program and on Internal Control Over Compliance Required By The Uniform Guidance 28-29

Schedule of Expenditures of Federal Awards 30

Schedule of Findings and Questioned Costs 31

Schedule of the Status of Prior Audit Findings, Questioned Costs, and Recommendations 32

Certificate of Managing Agent 33

Certificate of Officers 34

DAMIANO, BURK & NUTTALL, P"C" Certified Public Accountants and Advisors

To the Board of Directors Allegria Court, Inc. (A Non-Profit Corporation)

Johnston, RI

INDEPENDENT AUDITORS' REPORT

Report on the Financial Statements

Kevin S. Burk, CPA Jason S. Nuttall, CPA

Paul W Damiano (retired)

We have audited the accompanying financial statements of Allegria Court, Inc. (a non-profit Corporation) HUD Project No. 016-EE-031), which comprise the statement of financial position as of June 30, 2016, and the related statements of activities, changes in net deficit and cash flows for the year then ended, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Organization's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Organization's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Allegria Court, Inc. as of June 30,2016, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

-1-

6 BLACKSTONE VALLEY PLACE· SUITE 109 • LINCOLN, RI 02865 • TEL (401) 333-2880 • FAX (401) 334-0261 • www.dbncpas.com

Other Matters

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying supplemental information shown on pages 15 to 25 is presented for purposes of additional analysis as required by the Consolidated Audit Guide for Audits of HUD Programs issued by the U.S. Department of Housing and Urban Development, Office of the Inspector General, and is not a required part of the financial statements. The accompanying schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated July 21,2016 on our consideration of Allegria Court, Inc.'s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Allegria Court, Inc.'s internal control over financial reporting and compliance.

July 21,2016 Damiano, Burk & Nuttall, PC Lincoln, RI Employer Identification #45-3085083 Engagement Principal: Jason Nuttall

-2-

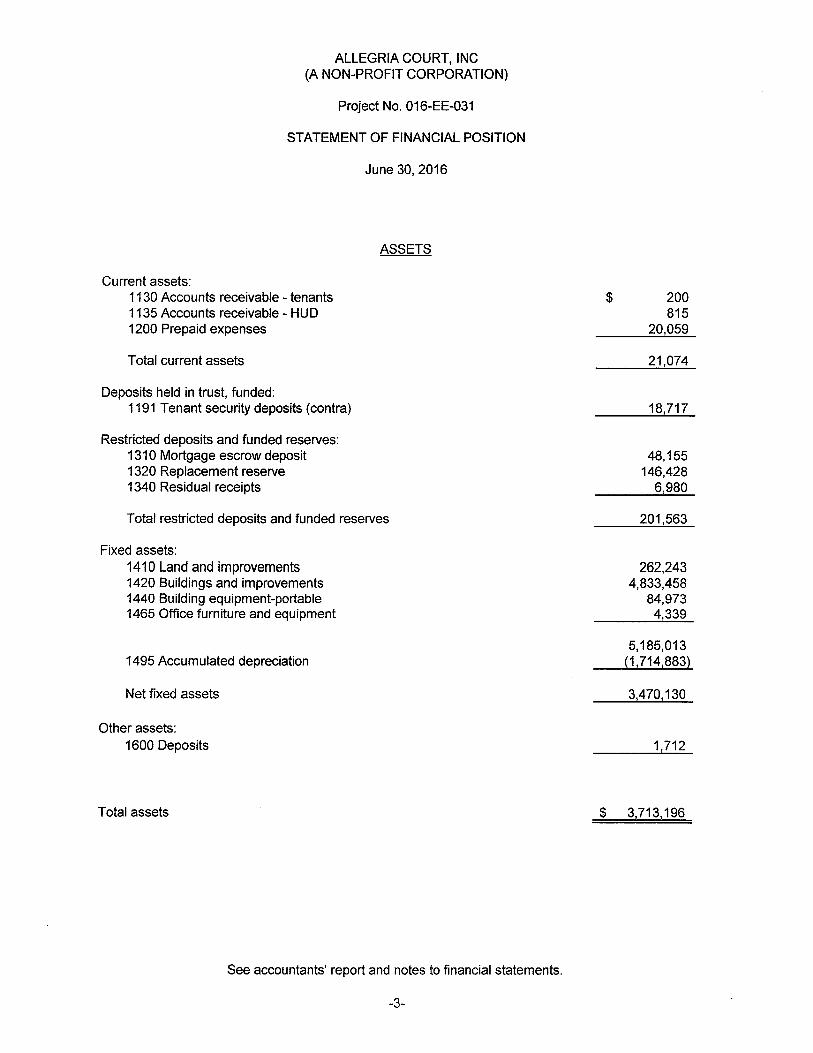

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF FINANCIAL POSITION

Current assets: 1130 Accounts receivable - tenants 1135 Accounts receivable - HU D 1200 Prepaid expenses

Total current assets

Deposits held in trust, funded: 1191 Tenant security deposits (contra)

Restricted deposits and funded reserves: 1310 Mortgage escrow deposit 1320 Replacement reserve 1340 Residual receipts

June 30, 2016

ASSETS

Total restricted deposits and funded reserves

Fixed assets: 1410 Land and improvements 1420 Buildings and improvements 1440 Building equipment-portable 1465 Office furniture and equipment

1495 Accumulated depreciation

Net fixed assets

Other assets: 1600 Deposits

Total assets

See accountants' report and notes to financial statements.

-3-

$ 200 815

20,059

21,074

18,717

48,155 146,428

6,980

201,563

262,243 4,833,458

84,973 4,339

5,185,013 (1,714,883)

3,470,130

11712

$ 317131196

Current liabilities: 2105 Bank overdraft 2110 Accounts payable

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF FINANCIAL POSITION

June 30,2016

LIABILITIES AND NET DEFICIT

2190 Miscellaneous current liabilities

Total current liabilities

Deposit liabilities: 2191 Tenant security deposits (contra)

Long-term liabilities: 2323 Capital advance

Total liabilities

Net deficit: 3131 Unrestricted

Total liabilities and net deficit

See accountants' report and notes to financial statements.

-4-

$ 2,057 41,361 13,351

56,769

18,713

5,085,300

5,160,782

(1 z447,586}

$ 3,713,196

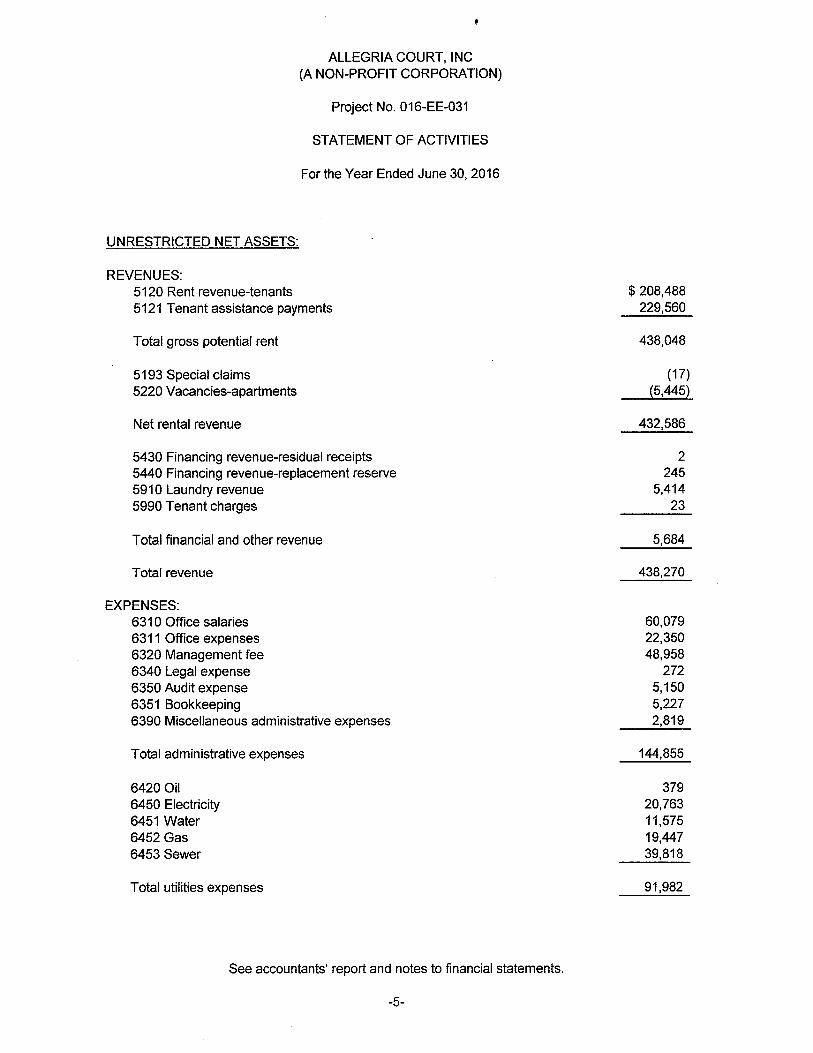

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF ACTIVITIES

For the Year Ended June 30, 2016

UNRESTRICTED NET ASSETS:

REVENUES: 5120 Rent revenue-tenants 5121 Tenant assistance payments

Total gross potential rent

5193 Special claims 5220 Vacancies-apartments

Net rental revenue

5430 Financing revenue-residual receipts 5440 Financing revenue-replacement reserve 5910 Laundry revenue 5990 Tenant charges

Total financial and other revenue

Total revenue

EXPENSES: 631 0 Office salaries 6311 Office expenses 6320 Management fee 6340 Legal expense 6350 Audit expense 6351 Bookkeeping 6390 Miscellaneous administrative expenses

Total administrative expenses

6420 Oil 6450 Electricity 6451 Water 6452 Gas 6453 Sewer

Total utilities expenses

See accountants' report and notes to financial statements.

-5-

$ 208,488 229,560

438,048

(17) (5,445)

432,586

2 245

5,414 23

5,684

438,270

60,079 22,350 48,958

272 5,150 5,227 2,819

144,855

379 20,763 11,575 19,447 39,818

91,982

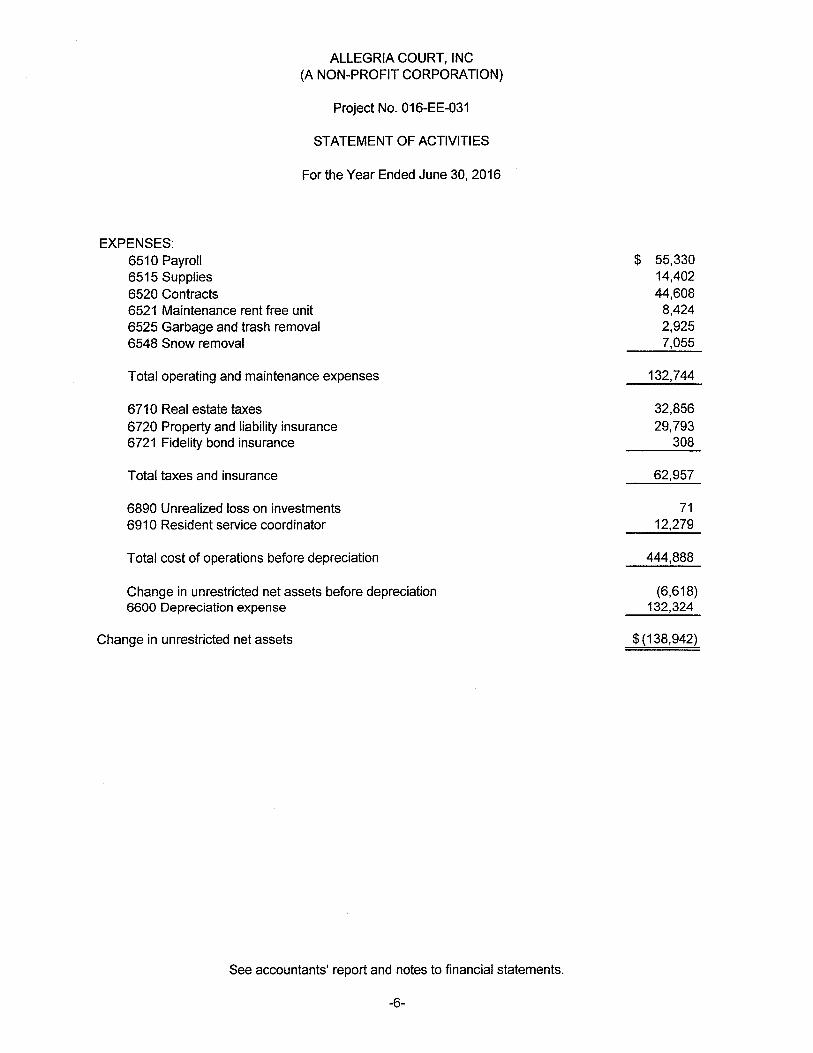

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF ACTIVITIES

For the Year Ended June 30,2016

EXPENSES: 6510 Payroll 6515 Supplies 6520 Contracts 6521 Maintenance rent free unit 6525 Garbage and trash removal 6548 Snow removal

Total operating and maintenance expenses

6710 Real estate taxes 6720 Property and liability insurance 6721 Fidelity bond insurance

Total taxes and insurance

6890 Unrealized loss on investments 6910 Resident service coordinator

Total cost of operations before depreciation

Change in unrestricted net assets before depreciation 6600 Depreciation expense

Change in unrestricted net assets

See accountants' report and notes to financial statements.

-6-

$ 55,330 14,402 44,608

8,424 2,925 7,055

132,744

32,856 29,793

308

62,957

71 12,279

444,888

(6,618) 132,324

$(138,942)

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF CHANGES IN NET DEFICIT

For the Year Ended June 30, 2016

Temporarily Unrestricted Restricted Total

Net deficit, beginning $ (1,308,644) $ $ (1,308,644)

Net loss for the year ended June 30, 2016 {138,942} {138,942}

Net deficit, ending $ {1,447,586} $ $ (1,447,586}

See accountants' report and notes to financial statements.

-7-

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF CASH FLOWS

For the Year Ended June 30, 2016

Cash flows from operating activities: Rental receipts $ 422,784 Other receipts 5,437 Interest receipts 247

Total receipts 428,468

Administrative (27,887) Management fee (56,561 ) Utilities (87,033) Salaries and wages (148,923) Operating and maintenance (81,685) Real estate taxes (32,856) Property insurance (27,053)

Total disbursements (461,998)

Net cash used by operating activities (33,530)

Cash flows from investing activities: Deposits to and interest on replacement reserve (18,872) Deposits to mortgage escrow (68,200) Withdrawals from mortgage escrow 59,602 Interest on residual receipts (2) Withdrawal from replacement reserve 43,826 Withdrawal from residual receipts 18,920 Purchase of fixed assets (2,400)

Net cash provided by investing activities 32,874

Cash flows from financing activities Increase in bank overdraft 656

Net decrease in cash

Cash, beginning of year

Cash, end of year $

(continued)

See accountants' report and notes to financial statements.

-8-

ALLEGRIA COURT, INC (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

STATEMENT OF CASH FLOWS

For the Year Ended June 30,2016

Reconciliation of change in net assets to net cash used in operating activities:

Change in net assets Adjustments to reconcile change in net assets to net cash

provided by operating activities: Depreciation Unrealized loss on investments

(Increase) decrease in: Accounts receivable - tenants Accounts receivable - HUD Prepaid expenses Tenants' security deposits

Increase (decrease) in: Accounts payable Accounts payable-H U D Accrued expenses Tenant security deposits liabilities

Net cash used in operating activities

Supplementary information: Increase in deposits included in accounts payable

See accountants' report and notes to financial statements.

-9-

$ (138,942)

132,324 71

(200) (815)

3,048 (822)

(34,066) (363)

5,413 822

$ (33,530)

$ 1,712

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

NOTES TO FINANCIAL STATEMENTS

June 30,2016

1. Nature of Activities and Summary of Significant Accounting Policies:

Business Operations and Organization:

Allegria Court, Inc. is a non-profit Corporation organized in January, 2000 under the laws of Rhode Island, for the purpose of developing and operating a 52 unit apartment complex located in Johnston, Rhode Island. The Corporation is regulated by the U.S. Department of Housing and Urban Development (HUD) as to rental charges and operating methods under the provisions of Section 202 of the National Affordable Housing Act of 1990. The project is managed by Housing Opportunities Corporation.

The Section 202 program provides assistance to the Corporation in the form of an interest free loan under the capital advance program. Under the capital advance program, to the extent the project is rented to lowincome tenants for a period of 40 years, no interest is due and the note is forgiven at maturity.

Basis of Presentation:

The Corporation is required to report information regarding its financial position and activities according to three classes of net assets: unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets. Furthermore, information is required to segregate program service expenses from support expenses. Support expenses include costs for services such as public relations, accounting, human resources, office services and computer systems.

Contributions received are recorded as unrestricted, temporarily restricted, or permanently restricted support depending on the existence and/or nature of any donor restrictions. Donor restricted contributions whose restrictions are met in the same reporting period are reported as unrestricted support in the accompanying statement of activities. Contributions received for the purchase of long-lived assets without donor stipulations about how long the assets must be used are reported as unrestricted support.

Income Taxes:

The Corporation qualified as a tax-exempt organization under Section 501 (c) (3) of the Internal Revenue Code and, therefore, has no provision for federal income taxes.

On July 1, 2010, the Corporation adopted the recognition requirements for uncertain income tax positions as required by generally accepted accounting principles, with no cumulative effect adjustment required. Income tax benefits are recognized for income tax positions taken or expected to be taken in a tax return, only when it is determined that the income tax position will more-likely-than-not be sustained upon examination by taxing authorities. The Corporation has analyzed tax positions taken for filing with the Internal Revenue Service and all state jurisdictions where it operates. Management believes that income tax filing positions will be sustained upon examination and does not anticipate any adjustments that would result in a material adverse effect to the Corporation's financial condition, results of operations or cash flows. Accordingly, the company has not recorded any reserves, or related accruals for interest and penalties for uncertain income tax positions at June 30,2016. Tax years prior to 202 have been closed for examination by taxing authorities.

Rental Income and Prepaid Rents:

Rental income is recognized for apartment rentals as it accrues. Advance receipts of rental income are deferred or classified as liabilities until earned. All leases between the Corporation and tenants of the property are operating leases. Rent increases must be approved by HUD.

-10-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

1. Nature of Activities and Summary of Significant Accounting Policies: (continued)

Fixed Assets and Depreciation:

Property and equipment are stated at cost. Expenditures for maintenance and repairs are charged to expense as incurred, expenditures for renewals and betterments which add to the value of the related assets or materially extend the life of the assets are capitalized. When sold, retired, or otherwise disposed of, the costs of assets and the related depreciation will be removed from the accounts and any gain or loss credited or charged to operations.

Depreciation is provided using principally the straight-line method over the following estimated useful lives:

ASSET CLASSI FICATION

Building and improvements Furniture and other

Use of Estimates:

RANGE OF LIVES

7-40 Years 7-10 Years

The preparation of finanCial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Tenant Receivables:

Tenant receivables are recognized in full when rents are earned and are reported at the principal balance outstanding less an allowance for doubtful accounts, if necessary. The allowance for doubtful accounts is a valuation for probable incurred credit losses, increased by the provision for doubtful accounts and decreased for write-offs less recoveries. Management estimates the allowance balance based on past loss experience, information about specific tenant situations, economic conditions and other factors. Doubtful accounts are charged to the allowance in the period they are determined to be uncollectible and receipts of accounts previously written off are credited to the allowance in the period received. As of June 30, 2016, there was no balance in the allowance for doubtful accounts.

Impairment of Long-Lived Assets:

The Corporation reviews its investment in real estate for impairment whenever events or changes in circumstances indicate that the carrying value of such property may not be recoverable. Recoverability is measured by a comparison of the carrying amount of real estate to the future net undiscounted cash flow expected to be generated by the rental property including the low-income housing tax credits and any estimated proceeds from the eventual disposition of the real estate. If the real estate is considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the real estate exceeds the fair value of such property. There were no impairment losses recognized during the year ended June 30,2016.

-11-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

1. Nature of Activities and Summary of Significant Accounting Policies: (continued)

Statement of Cash Flows:

For the purposes of the statement of cash flows, the Corporation considers all highly liquid debt instruments purchased with an original maturity of three months or less to be cash equivalents. There were no cash equivalents at June 30, 2016.

Functional Expenses:

The costs of providing various programs and other activities are summarized on a functional basis as follows:

Program services HUD-assisted elderly housing project

Supporting services General and administrative

General and administrative consists of allocated costs as follows:

Management fee Office expenses Audit expense Bookkeeping and accounting Travel and education

2. Capital Advances:

$ 360,384

84,504

$ 444,888

$ 48,958 22,350

5,150 5,227 2,819

$ 84,504

The Corporation entered into a mortgage note under the Capital Advance Program whereby HUD committed to fund development costs. The balance advanced under this program does not bear interest, or require principal payments, as long as the apartments are rented to qualifying low-income tenants for a period of 40 years. If no violations occur during the period, the note will be forgiven upon maturity in April, 2043. If the Corporation defaults under the provisions of the note, the note bears interest at a rate of 6.75% per year and will be payable on demand. The note is secured by all fixed assets, funds held by HUD and an assignment of rents. At June 30,2016, the amounts advanced under this program totaled $5,085,300.

Any surplus cash at fiscal year end must be deposited into a residual receipts account. There was no surplus cash at June 30, 2016.

-12-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

3. Rent Supplement Payments:

The Corporation receives a monthly project rental assistance contract (PRAC) rent supplement from HUD. The PRAC contract is in effect through January 2020. The Corporation earned $229,560 of rent supplement payments, which is approximately 53% of net rental income, for the year ended June 30, 2016 as follows:

Rent subsidies received FYE 06/30/16 Accounts receivable-HUD FYE 06/301116 Accounts payable-HUD FYE 06/30/15 Special Claims Vacancy reimbursement

Total subsidy

4. Restricted Cash:

$ 228,697 815 363

17 (332)

$ 229,560

The Corporation maintains restricted cash accounts for replacement reserves, residual receipts and tax and insurance escrow. In addition, all tenant security deposits are deposited into a separate bank account and held in trust for the tenants until they vacate the property. Any amounts not returned to the tenants due to lease violations are transferred to the general operating account.

Restricted cash at June 30, 2016 is as follows:

Real estate tax and insurance escrow Replacement reserve Residual receipts Tenant security deposits

$ 48,155 146,428

6,980 18,717

$ 220,280

Withdrawals from the replacement reserve and residual receipts require HUD approval.

5. Commitments/Related Party Transactions:

During the year ended June 30, 2016, a management fee of 11.58% of gross rental collections in the amount of $48,958 and payroll and other cost reimbursements amounting to $134,849 were earned by Housing Opportunities Corporation in accordance with the management contract. The balance owed for these services at June 30, 2016 was $20,688.

6. Current Vulnerability Due to Certain Concentrations:

The Corporation's sole asset is a 52 unit apartment complex. The Corporation's operations are concentrated in the multifamily real estate market. In addition, the Corporation operates in a heavily regulated environment. The operations of the Corporation are subject to the administrative directives, rules and regulations of federal, state and local regulatory agencies, including, but not limited to, HUD. Such administrative directives, rules and regulations are subject to change by an act of congress or an administrative change mandated by HUD. Such changes may occur with little notice or inadequate funding to pay for the related cost, including the additional administrative burden, to comply with a change.

-13-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

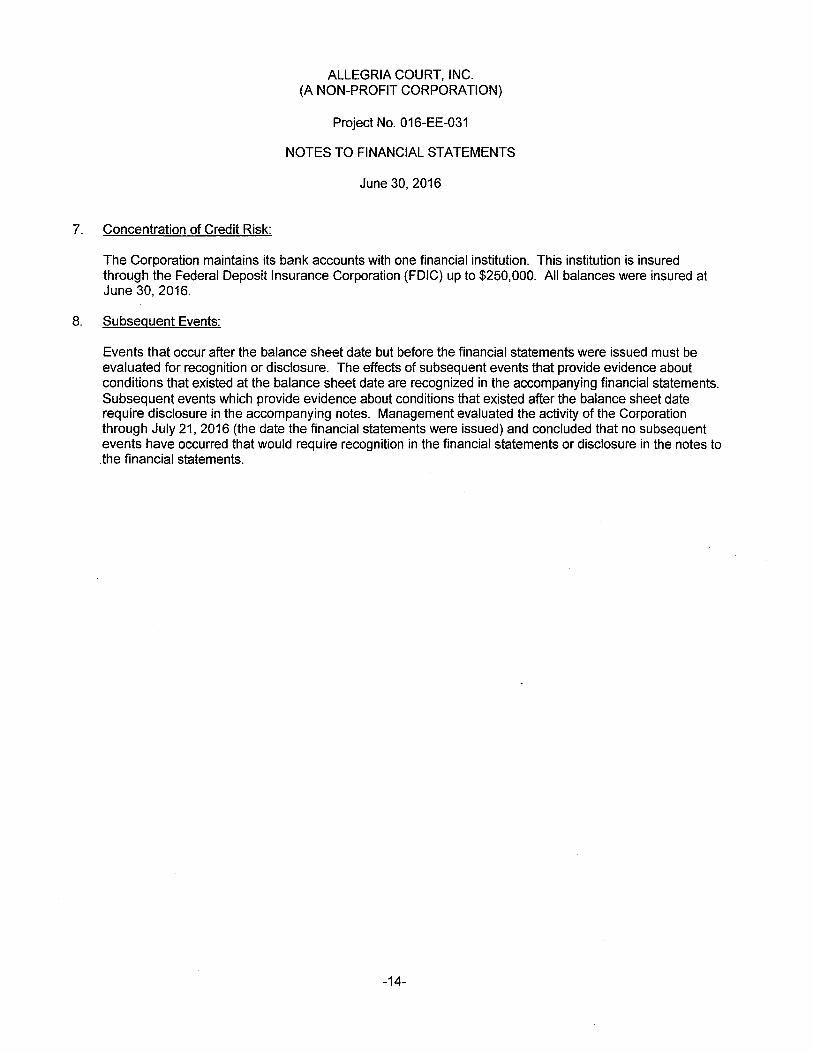

7. Concentration of Credit Risk:

The Corporation maintains its bank accounts with one financial institution. This institution is insured through the Federal Deposit Insurance Corporation (FDIC) up to $250,000. All balances were insured at June 30, 2016.

8. Subsequent Events:

Events that occur after the balance sheet date but before the financial statements were issued must be evaluated for recognition or disclosure. The effects of subsequent events that provide evidence about conditions that existed at the balance sheet date are recognized in the accompanying financial statements. Subsequent events which provide evidence about conditions that existed after the balance sheet date require disclosure in the accompanying notes. Management evaluated the activity of the Corporation through July 21,2016 (the date the financial statements were issued) and concluded that no subsequent events have occurred that would require recognition in the financial statements or disclosure in the notes to .the financial statements.

-14-

ASSETS

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Balance Sheet June 30, 2016

CURRENT ASSETS 1130 Tenant/Member Accounts Receivable (Coops) 1130N Net Tenant Accounts Receivable 1135 Accounts Receivable - HUD

1200 Miscellaneous Prepaid Expenses

I lOOT Total Current Assets

1191 Tenant/Patient Deposits Held in Trust

RESTRICTED DEPOSITS

1310 Escrow Deposits

1320 Replacement Reserve

1340 Residual Receipts Reserve

1300T Total Deposits

PROPERTY AND EQUIPMENT

1410 Land

1420 Buildings

1440 Building Equipment (Portable)

1450 Furniture for Project/Tenant Use

1400T Total Fixed Assets

1495 Accumulated Depreciation

1400N Net Fixed Assets

1590 Miscellaneous Other Assets 1500T Total Other Assets

1000T TOTAL ASSETS

-15-

$ 200 200 815

20,059

21,074

18,717

48,155

146,428

6,980

201,563

258,137

4,837,564

84,973

4,339

5,185,013

1,714,883

3,470,130

1,712 1,712

$ 3,713,196

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Balance Sheet June 30,2016

LIABILITIES AND PARTNERS' DEFICIT

CURRENT LIABIL TIES

2105 Bank Overdraft - Operations

2110 Accounts Payable - Operations

2190 Miscellaneous Current Liabilities

2122T Total Current Liabilities

2191 TenantlPatient Deposits Held In Trust (Contra)

LONG-TERM LIABILITIES

2320 Mortgage (or Bonds) Payable - First Mortgage (or Bonds)

2300T Total Long Term Liabilities

2000T Total Liabilities

NET ASSETS

3131 Unrestricted Net Assets

3130 Total Net Assets

2033T TOTAL LIABILITIES AND EQUITY

-16-

$ 2,057

41,361

13,35 I

56,769

18,713

5,085,300

5,085,300

5,160,782

(1,447,586)

(1,447,586)

$ 3,713,196

REVENUE 5120

5121

5193

5 lOOT

Vacancies

5220

5200T

5152N

ALLEGRIA COURT, INC Hun Project Number 016-EE-031

Supplemental Statement of Profit and Loss For the Year Ended June 30, 2016

Rent Revenue - Gross Potential

Tenant Assistance Payments

Special Claims Revenue

Total Rent Revenue

Apartments

Total Vacancies

Net Rental Revenue (Rent Revenue Less Vacancies)

Financial Revenue

5430 Revenue from Investments - Residual Receipts

5440

5400T

Revenue from Investments - Replacement Reserve

Total Financial Revenue

Other Revenue

5910 5990

5900T

5000T

Laundry and Vending Revenue Miscellaneous Revenue

Total Other Revenue

TOTAL REVENUE

EXPENSES Administrative Expenses

6310 Office Salaries

6311 Office Expenses

Management Fee

Legal Expense - Project

Audit Expense

6320

6340

6350

6351

6390

6263T

Bookkeeping Fees/Accounting Services

Miscellaneous Administrative Expenses

Total Administrative Expenses

Utilities Expenses

6420 Fuel Oil/Coal

6450

6451

6452

6453

6400T

Electricity

Water

Gas

Sewer

Total Utilities Expense

Operating & Maintenance Expenses

-17-

$ 208,488

229,560

(17)

438,031

5,445

5,445

432,586

2

245

247

5,414 23

5,437

438,270

60,079

22,350

48,958

272

5,150

5,227

2.819

144,855

379

20,763

11,575

19,447

39,818

91,982

6510

6515

6520

6521

6525

6548

6500T

Payroll

Supplies

Contracts

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Supplemental Statement of Profit and Loss For the Year Ended June 30, 2016

Operating and Maintenance Rent Free Unit

Garbage and Trash Removal

Snow Removal

Total Operating and Maintenance Expenses

Taxes & Insurance

6710 Real Estate Taxes

6720 Property & Liability Insurance (Hazard)

6721

6700T

Fidelity Bond Insurance

Total Taxes and Insurance

Financial Expenses

6890 Miscellaneous Financial Expenses

6800T Total Financial Expenses

6900 Nursing Homes! Assisted Living/ Board & Care/Other Elderly Care

Operating Results

6000T Total Cost of Operations before Depreciation

5060T Profit (Loss) before Depreciation

6600

5060N

Accumulated Depreciation Expenses

Operating Profit or (Loss)

CHANGE IN NET ASSETS FROM OPERATIONS

3250 Change in Total Net Assets from Operations

Part II

Total of 12 monthly deposits in the audit year into the Replacement Reserve

$

S1000-020 account, as required by the Regulatory Agreement even if payments may be $

S1000-030

temporarily suspended or reduced. Replacement Reserves, or Residual Receipts and Releases which are included $ as expense items on this Profit and Loss statement.

-18-

55,330

14,402

44,608

8,424

2,925

7,055

132,744

32,856

29,793

308

62,957

71

71

12,279

444,888

(6,618)

132,324

(138,942)

(138,942)

18,627

18,920

Sl100-060 3247

3131

S1lO0-050

3250

3130

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Statement of Equity June 30, 2016

Previous Year Unrestricted Net Assets Change in Unrestricted Net Assets from Operations

Unrestricted Net Assets

Previous Year Total Net Assets

Change in Total Net Assets from Operations

Total Net Assets

-19-

$ (1,308,644)

(138,942)

(1,447,586)

(1,308,644 )

(138,942)

$ (1,447,586)

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Statement of Cash Flows For the Year Ended June 30, 2016

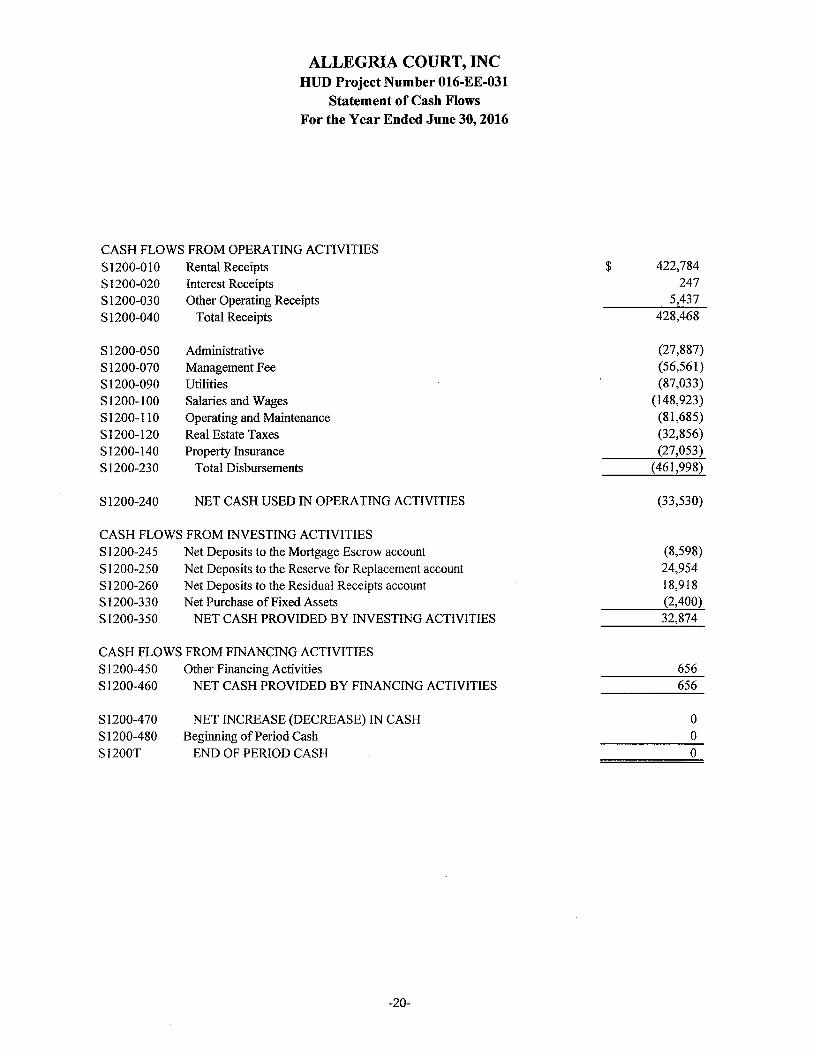

CASH FLOWS FROM OPERATING ACTIVITIES

S1200-01O S1200-020 S1200-030 S1200-040

S1200-050 S1200-070 S1200-090 S1200-100 S1200-11O S1200-120 S1200-140 S1200-230

S1200-240

Rental Receipts Interest Receipts Other Operating Receipts

Total Receipts

Administrative Management Fee Utilities Salaries and Wages Operating and Maintenance Real Estate Taxes Property Insurance

Total Disbursements

NET CASH USED IN OPERATING ACTIVITIES

CASH FLOWS FROM INVESTING ACTIVITIES S1200-245 S1200-250 S1200-260 S1200-330 S1200-350

Net Deposits to the Mortgage Escrow account Net Deposits to the Reserve for Replacement account Net Deposits to the Residual Receipts account Net Purchase of Fixed Assets

NET CASH PROVIDED BY INVESTING ACTIVITIES

CASH FLOWS FROM FINANCING ACTIVITIES S1200-450 S1200-460

S1200-470 S1200-480 S1200T

Other Financing Activities NET CASH PROVIDED BY FINANCING ACTIVITIES

NET INCREASE (DECREASE) IN CASH Beginning of Period Cash

END OF PERIOD CASH

-20-

$ 422,784 247

5,437 428,468

(27,887) (56,561) (87,033)

(148,923) (81,685) (32,856) (27,053)

(461,998)

(33,530)

(8,598) 24,954 18,918 (2,400) 32,874

656 656

0 0 0

ALLEGRIA COURT, INC Hun Project Number 016-EE-031

Statement of Cash Flows For the Year Ended June 30, 2016

RECONCILIATION OF NET LOSS TO NET CASH PROVIDED BY OPERATING ACTIVITIES

3250 Change in Total Net Assets from Operations

Adjustments to Reconcile Net Profit (Loss) to Net Cash Provided by (Used in) Operating Activities

6600 Depreciation Expenses S1200-490 Decrease (increase) in TenantlMember Accounts Receivable S1200-500 Decrease (increase) in Accounts Receivable - Other S1200-520 Decrease (increase) in Prepaid Expenses S1200-530 Decrease (increase) in Cash Restricted for Tenant Security Deposits S1200-540 Increase (decrease) in Accounts Payable S1200-560 Increase (decrease) in Accrued Liabilities S1200-580 Increase (decrease) in Tenant Security Deposits held in trust

S1200-600 Other adjustments to reconcile net profit (loss) to Net Cash provided by (used in) Operating Activities

S1200-61O NET CASH USED IN OPERATING ACTIVITIES

Supplementary Information: Increase in deposits included in accounts payable

-21-

$ (138,942)

132,324 (200) (815)

3,048 (822)

(34,429) 5,413

822

71

$ {33 25301

$ 12712

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Supplementary Data Required by HUD June 30,2016

SCHEDULE OF RESERVE FOR REPLACEMENTS 1320P 1320DT 1320INT 1320UGL 1320WT 1320

1320R

Balance at Beginning of Year Total Monthly Deposits Interest on Replacement Reserve Accounts Unrealized Gain or (Loss) Approved Withdrawals

Balance at End of Year, Confirmed by Mortgagee

Deposits Suspended or Waived Indicator

SCHEDULE OF RESIDUAL RECEIPTS 1340P 1340INT 1340UGL 1340WT 1340

Balance at Beginning of Year Interest on Residual Receipt Accounts Unrealized Gain or (Loss) Approved Withdrawals

Balance at CUlTent fiscal year end

COMPUTATION OF SURPLUS CASH, DISTRIBUTIONS, & RESIDUAL RECEIPT~

$

$

$

$

S1300-010 Cash $ 1135 S1300-030 S1300-040

S1300-075 S1300-100 2191 S1300-140

S1300-150

S1300-200

S1300-210

Tenant subsidy due for period covered by financial statement Other

Total Cash

Accounts Payable - 30 days Accrued Expenses [not escrowed] Tenant Security Deposits Liability

Total CUlTent Obligations Surplus Cash (Deficiency)

Amount Available for Distribution during next fiscal period

Deposit Due Residual Receipts

-22-

$

171,374 18,627

245

8 43,826

146,428

NO

25,977 2

(79) 18,920

6,980

18,717 815

19,532

43,418 13,351 18,713 75,482

(55,950)

o (55,950)

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Supplementary Data Required by HUD Fixed Assets

June 30, 2016

Beginning Additions Deletions Ending Balance

Balance

1410 Land $ 258,137 $ 258,137

1420 Buildings 4,837,564 4,837,564

1440 Building Equipment (portable) 82,573 2,400 84,973

1450 Furniture for Project/Tenant Use 4,339 4,339

1460 Furnishings

1465 Office Furniture and Equipment

1470 Maintenance Equipment

1480 Motor Vehicles

1490 Miscellaneous Fixed Assets

Total $ 5,182,613 2,400 5,185,013

Depreciation $ 1,582,559 132,324 1,714,883

Net Book Value $ 3,470,130

-23-

Schedule of 6900 Accounts

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

NH Assisted Living

June 30, 2016

6990 Other Service Expenses

-24-

$ 12,279

ALLEGRIA COURT, INC HUD Project Number 016-EE-031

Details June 30, 2016

Acct. Description # 1590 Misc. Other Assets

Item Description

I. DEPOSITS

Amount

1,712

Total $ 1,712

#2190 Misc. Current Liabilities

Item Description I. ACCRUED AUDIT FEE 5,150

2. ACCRUED UTILITIES 8,201

Total $ 13,351

#5990 Other Revenue

Item Description I. TENANT CHARGES 23

Total $ 23

#6390 Misc. Administrative Expenses

Item Description

I. TRAVEL 2,719

2. EDUCATION AND TRAINING 100

Total $ 2,819

#6890 Misc. Financial Expenses

Item Description

1. UNREALIZED LOSS ON INVESTMENTS 71

Total $ 71

S1200 - Other Financing Activities 450

Item Description

1. INCREASE IN BANK OVERDRAFT 656

Total $ 656

SI200 - Other adjustments to reconcile net profit (loss) to Net 600 Cash provided by (used in) Operating Activities

Item Description 1. UNREALIZED LOSS ON INVESTMENTS 71

Total $ 71

#1440 Add. to Bldg Equip. (Portable)

Item Description l. HEATING AlC UNIT - OFFICE 2,400

Total $ 2,400

-25-

DAMIANO, BURK & NUTTALL, p<>c<> Certified Public Accountant~ and Advisors

Kevin S. Burk, CPA Jason S. Nuttall, CPA

Paul W Damiano (retired)

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of Directors Allegria Court, Inc. (A Non-Profit Corporation)

Johnston, RI

We have audited, in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States, the financial statements of Allegria Court, Inc. which comprise the statement of financial position as of June 30, 2016, and the related statements of activities, changes in net deficit and cash flows for the year then ended, and the related notes to the financial statements and have issued our report thereon dated July 21, 2016 ..

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered Allegria Court, Inc.'s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Allegria Court, Inc.'s internal control. Accordingly, we do not express an opinion on the effectiveness of Allegria Court, Inc.'s internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of Allegria Court, Inc.'s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control, that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether Allegria Court, Inc.'s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

-26-

6 BLACKSTONE VALLEY PLACE· SUITE 109 • LINCOLN, RI 02865 • TEL (401) 333-2880 • FAX (401) 334-0261 • www.dbncpas.com

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of Allegria Court, Inc.'s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Allegria Court, Inc.'s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

~ ~;~/f.C. , I (

Damiano, Burk & Nuttall, P.C. Lincoln, RI July 21,2016

-27-

DAMIANO, BURK & NUTTALL, P"C" Certified Public Accountants and Advisors

Kevin S. Burk, CPA Jason S. Nuttall, CPA ~

Paul W Damiano (retired)

INDEPENDENT AUDITORS' REPORT ON COMPLIANCE FOR EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE

To the Board of Directors Allegria Court, Inc. (A Non-Profit Corporation)

Johnston, RI

Report on Compliance for Each Major Federal Program

We have audited Allegria Court, Inc.'s compliance with the types of compliance requirements described in the OMB Compliance Supplement that could have a direct and material effect on each of Allegria Court, Inc.'s major federal programs for the year ended June 30, 2016. Allegria Court, Inc.'s major federal programs are identified in the summary of auditor's results section of the accompanying schedule of findings and questioned costs.

Management's Responsibility

Management is responsible for compliance with the federal statutes, regulations, and the terms and conditions of.its federal awards applicable to its federal programs.

Auditor's Responsibility

Our responsibility is to express an opinion on compliance for each of Allegria Court, Inc.'s major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about Allegria Court, Inc.'s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances.

We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of Allegria Court, Inc.'s compliance.

Opinion on Each Major Federal Program

In our opinion, Allegria Court, Inc. complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended June 30, 2016.

-28-

6 BLACKSTONE VALLEY PLACE· SUITE 109 • LINCOLN, RI 02865 • TEL (401) 333-2880 • FAX (401) 334-0261 • www.dbncpas.com

Report on Internal Control Over Compliance

Management of Allegria Court, Inc. is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered Allegria Court, Inc.'s internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with the Uniform Guidance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of Allegria Court, Inc.'s internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identity all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance. Accordingly, this report is not suitable for any other purpose.

~/~i~/f.C. Damiano, Burk & Nuttall, P.C. Lincoln, RI July 21,2016

-29-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

FEDERAL GRANTOR

u.s. Department of Housing and Urban Development Office of Housing

Supportive Elderly Housing-Section 202

Section 202 Project Rental Assistance

Note A-Basis of Presentation:

June 30, 2016

CONTRACT NUMBER CFDANUMBER

14.157

RI43S991002 14.157

FEDERAL EXPENDITURES

$5,085,300

229,560

$5,314,860

The accompanying Schedule of Expenditures of Federal Awards includes the federal grant activity of Allegria Court, Inc. and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. Therefore, some amounts presented in this schedule may differ from amounts presented in, or used in the preparation of the basis financial statements. The Section 202 program amount is reported as a capital advance during the entire compliance period.

-30-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

June 30, 2016

Summary of Auditors' Results

1. The auditors' report expresses an unqualified opinion on the financial statements of Allegria Court, Inc. and were prepared in accordance with GAAP. .

2. No material deficiencies were identified during the audit of the financial statements.

3. No instances of noncompliance material to the financial statements of Allegria Court, Inc. were disclosed during the audit.

4. No material weaknesses were identified during the audit of the major federal award program.

5. The auditors' report on compliance for the major federal award programs for Allegria Court, Inc. expresses an unmodified opinion.

6. No audit findings were required to be reported in accordance with 2 CFR section 200.516(a).

7. The program tested as a major program consists of:

Supportive Elderly Housing section 202 (CFDA#14.157)

8. The threshold for distinguishing Types A and B programs was $750,000.

9. Allegria Court, Inc. was determined to be a low-risk auditee.

Findings-Financial Statement Audit

None

Findings-Major Federal Award Programs Audit

None

-31-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

SCHEDULE OF THE STATUS OF PRIOR AUDIT FINDINGS, QUESTIONED COSTS, AND RECOMMENDATIONS

For the Year ended June 30, 2016

Schedule of the Status of Prior Audit Findings, Questioned Costs, and Recommendations

1. There were no open findings from the prior audit report. 2. There were no reports issued by HUD Office of Inspector General or other federal agencies or

contract administrators during the period covered by this audit. 3. There were no letters or reports issued by HUD management during the period covered by this

audit.

-32-

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

CERTIFICATE OF MANAGING AGENT

June 30,2016

CERTIFICATE OF MANAGING AGENT

We hereby certify that we have examined the accompanying finpncial statements and supplemental data on

Allegria Court, Inc. and, to the best of our knowledge and belief, the same is complete and accurate.

-33-

CORPORATE OFFICER

Signature Date

Print Name

Housing Opportunities Corporation 10 # 22-2487344

ALLEGRIA COURT, INC. (A NON-PROFIT CORPORATION)

Project No. 016-EE-031

CERTIFICATE OF OFFICERS

June 30,2016

CERTIFICATE OF OFFICERS

We hereby certify that we have examined the accompanying financial statements and supplemental data of

Allegria Court, Inc., and, to the best of our knowledge and belief, the same is complete and accurate.

CORPORATE OFFICERS

Signature Date

Print Name

Signature Date

Print Name

Federal Employer Identification Number #05-0509244

-34-