76

26-11-13 Televisión Abierta y Oportunidades Comerciales Multiplataforma Brian Crotty - Director de Medios

| Date post: | 27-Jan-2015 |

| Category: |

Marketing |

| Upload: | babelfish-brian-crotty |

| View: | 110 times |

| Download: | 1 times |

26-11-13

Televisión Abierta y Oportunidades Comerciales Multiplataforma Brian Crotty - Director de Medios

Business is challenging for us all

Media Planning has changed – less reliance on TV

Other video distribution forms slowly gaining traction

Connected TV´s and Smartphones are disruptive

Although TV is still dominant

Trading desks and Data Tools changing the way media is bought

Ratings models being challenged

Beware the Middlemen

Data changing everything –segmentation at scale

Content Management Tools allowing adaptive learning

Content Brands – distributed across channels and forms

Branded content types

Online providing more varied tactics

Relative Value

Traditional product placement

Emerging Options

Outstanding Ideas

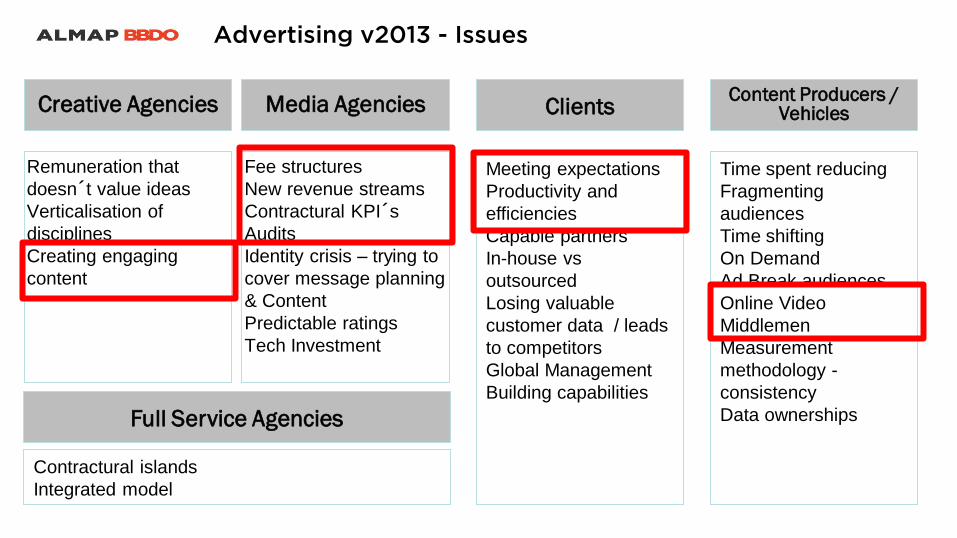

Media Agencies

Fee structures

New revenue streams

Contractural KPI´s

Audits

Identity crisis – trying to

cover message planning

& Content

Predictable ratings

Tech Investment

Creative Agencies

Remuneration that

doesn´t value ideas

Verticalisation of

disciplines

Creating engaging

content

Clients

Meeting expectations

Productivity and

efficiencies

Capable partners

In-house vs

outsourced

Losing valuable

customer data / leads

to competitors

Global Management

Building capabilities

Content Producers / Vehicles

Time spent reducing

Fragmenting

audiences

Time shifting

On Demand

Ad Break audiences

Online Video

Middlemen

Measurement

methodology -

consistency

Data ownerships

Full Service Agencies

Contractural islands

Integrated model

Advertising v2013 - Issues

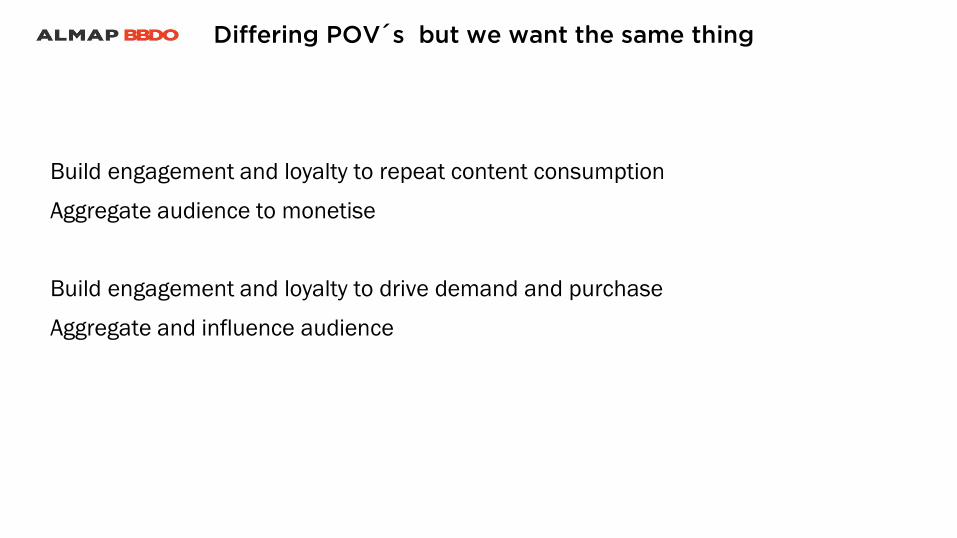

Build engagement and loyalty to repeat content consumption

Aggregate audience to monetise

Build engagement and loyalty to drive demand and purchase

Aggregate and influence audience

Differing POV´s but we want the same thing

Prime Time TV

Cable TV

Off PeakTV

Cable TV

TV Bursts

Cable TV Video

Images

Interactive

Newspaper

Magazine

OOH

Magazine

Web Campaigns

OOH

Magazine

Packaging

Web Site Web Site

Build Awareness Sustaining / Continuity

Channels for tasks

Re

ach

Prime Time TV

Cable TV

Online Video

Off PeakTV

Cable TV

Online Video

POS Video

Online Video Video

Images

Interactive

Newspaper

Magazine

OOH

Magazine

Owned Assets

(Sites, POS etc)

Social

Owned Assets

Search

POS

Packaging

Owned assets

Services

Apps, Social

Search

Build Awareness Persistent environments

Re

ach

Surgical use of Prime Time TV + Persistent presence

Single currency for video – TRP´s, R&F, CPM B

ar

- T

RP´s

Pe

r W

eek

Are

a –

Ad

sto

ck

AB

25

8-4

9

Video buys accross channels

Optimising Mix To Get Most Efficient Buy

<- $50-$75 ->

<- $15-$50 ->

<- $15-$50 ->

$10-$50 ->

<- $50-$75 ->

<- $15-$50 ->

<- $15-$50 ->

Video buys across channels – Audience targetted online

can reduce excessive frequency against heavy viewers

More competitors for entertainment share of wallet / time

Poliferation of devices and places to access content

NORTH AMERICA EUROPE ASIA-PACIFIC LATIN AMERICA

2013 51MM 55MM 151MM 9K

2014 65MM 70MM 196MM* 2MM

2015 78MM 85MM 254MM* 5MM

2016 87MM 95MM 331MM 8MM

Source: eMarketer, 2012

*Average projection of 2.3% average yearly growth

Connected TVs: Ownership Still Low but growing

Smart TV ownership is high around the world

and is expected to increase through 2016

Latam – 140 Million smartphones by end of 2013

Brazil – Base of 40 Million Smartphones in 2012. + Samsung alone expect to sell 17Million in 2013 / Total market 21.4Million

Mexico – 12.2Million in 2012, 16Million in 2013

Argentina – 5.9Million in 2012

Wifi penetration improving, but affecting more affluent – those than can afford data packages

Biggest disruptor - Smartphone penetration growing

What people are doing with their Smartphones

Simultaneously doing other things while using Smartphones

Despite all the hype – Time spent with other

devices still relatively low

63% 4%

4%

6%

11%

12%

TV ABERTA

PAY TV

RADIO

REVISTA

JORNAL

INTERNET

Source: AlmapBBDO: Brazil September 2013

49%

16%

28%

0.44% 1% 4%

63%

4%

4%

6%

11%

12%

TV ABERTAPAY TV

RADIOREVISTAJORNAL

INTERNET

Share of Time vs Share of Investment –

TV still dominates

Source: AlmapBBDO / Intermeios: Brazil September 2013

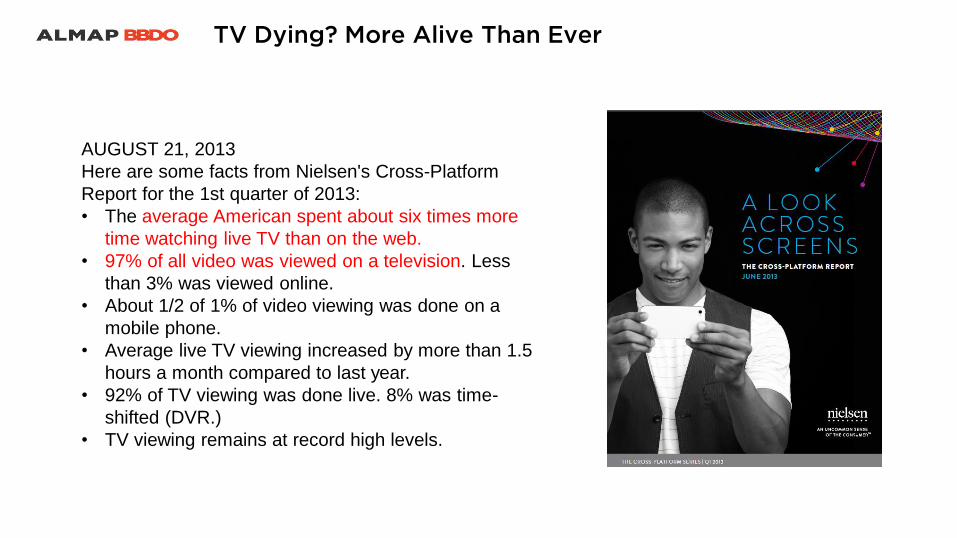

AUGUST 21, 2013

Here are some facts from Nielsen's Cross-Platform

Report for the 1st quarter of 2013:

• The average American spent about six times more

time watching live TV than on the web.

• 97% of all video was viewed on a television. Less

than 3% was viewed online.

• About 1/2 of 1% of video viewing was done on a

mobile phone.

• Average live TV viewing increased by more than 1.5

hours a month compared to last year.

• 92% of TV viewing was done live. 8% was time-

shifted (DVR.)

• TV viewing remains at record high levels.

TV Dying? More Alive Than Ever

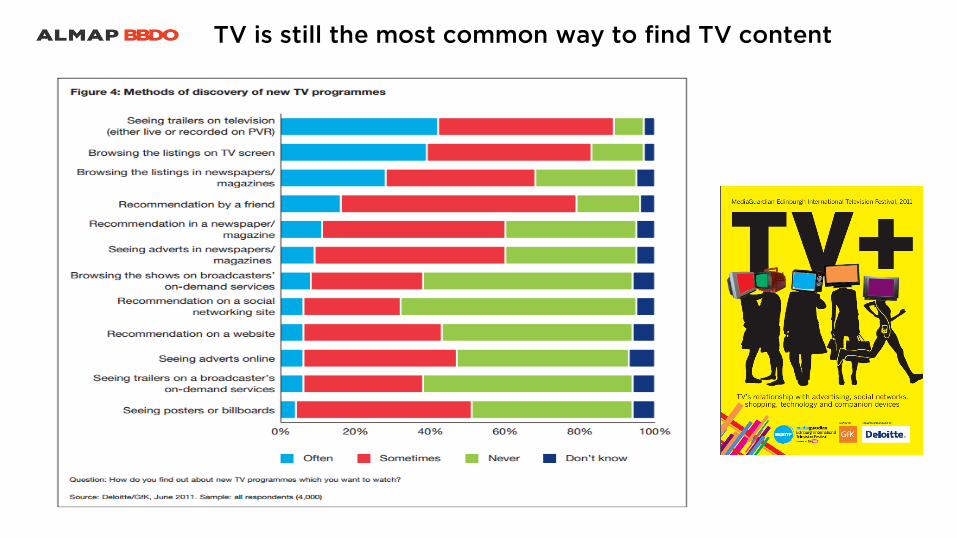

TV is still the most common way to find TV content

Multitasking not disruptive

Key findings were that multi-screening means people are more likely to stay seated through an ad break and

therefore increases ad exposure, and that people have always multi-tasked whilst watching TV, having

conversations, interacting with children and animals, reading magazines and engaging in hobbies. It was

found that except for having a conversation, orientation towards the TV was maintained through various

multi-tasking and -screening behaviour. Additionally, multi-screening may enhance enjoyment of television

as devices allow for greater engagement in the program.

Source: WARC - Multi-screen viewing behaviour, Dr Ali Goode and Neil Mortensen, Lingua Brand and Thinkbox

Multitasking is social – People stay in front of TV

MEDIA AND ENTERTAINMENT| 06.05.2013

Over the last six years, TV networks’ Twitter accounts have gone from being little more than

promotional outlets for tune-in messaging to real-time channels for networks and advertisers to Interact with highly engaged audiences.

Evan Silverman, SVP, digital media for A&E networks, says that advancements in social TV analytics are giving the industry a way to

measure the total size of the social TV audience—both those participating in the conversation and those who watch on the sidelines. And

these analytics are making the social TV opportunity real and measurable for advertisers.

At Nielsen’s Consumer 360 conference in Phoenix, Silverman discussed how A&E was able to drive audience engagement for the hi t show

“Project Runway,” which runs on its subsidiary Lifetime network, through strategic Twitter TV initiatives.

When “Project Runway” launched a “Fan Favorite” social campaign, encouraging viewers to vote for designers by using custom hashtags,

the initiative resulted in nearly five comments per unique user—more than the ratio for any other cable TV show at the time.

A&E believes that there should be a premium charge for programming with high social engagement, Silverman said.

“The most important thing we all do is to generate a linear rating for our company. However, social TV is

extremely valuable in its own right and absolutely helps amplify the conversation, helps sponsors participate in

programming,” he said.

Dedicated Twitter accounts are a relatively new industry practice: They became a mainstream in 2007, just a year after the first tweet was

sent in 2006. Last year, social TV took a big leap forward when Twitter launched Twitter Cards, which enabled partners to create interactive

experiences within tweets.

Looking at the results of a new SocialGuide study, viewers spend the majority of their Tweets during program time rather

than during commercial time. The study also found that the share of Tweets sent during commercial time was driven across genres by the share of commercial time

within a program’s airtime. In sports, for example, commercials ran during 24 percent of airtime, and 25 percent of

Tweets were sent during commercial time.

Twitter drives Audience and Stakeholder engagement

Miley Cyrus and Robin Thicke perform at the 2013 MTV VMAs

As a brand that has long had event sponsorship at the heart of its marketing formula, Pepsi

sought a more scientific way to study the correlation between TV viewing and

second-screen usage during live programming. So using research methods such as biometrics, the brand looked at consumer behavior during

the MTV Video Music Awards telecast this past August—the top-rated entertainment program on

cable among viewers aged 12-34 this year, and the most social non-sports TV event.

What emerged were some surprising differences in media usage among millennials. During

pivotal moments of the show—like Miley Cyrus’ twerk-tastic duet with Robin Thicke (which

generated a record 360,000 tweets per minute)—consumers 18-26 immediately shifted from TV

viewing to second screens. Meanwhile, those aged 27-34 stayed with the telecast, waiting to

engage in social conversations.

“The younger group already had their hands ready and immediately went to

social media to start talking,” said Chad Stubbs, senior director of marketing at PepsiCo.

“The show ebbed and flowed, and a key thing we learned was having a brand message throughout the show was important,” he added. “In the

past, maybe we said we would need a big part at the beginning or the end.”

Carolyn Kim, associate director of business intelligence at Pepsi agency OMD, pointed out that while there is not a wide disparity of ages among

the millennial set, continual advances in technology have led to behavioral differences among those consumers.

Consider this: When email became widely available in 1993, older millennials were 11 years old—but younger millennials were just 2 years old.

“Those younger viewers really grew up more with technology as an ordinary part of their everyday lives,” Kim said.

During the VMAs, Facebook was the most popular social media brand, accounting for 41 percent of consumer usage, followed by Twitter with 32

percent. And while Cyrus’ antics burned up Twitter, performances by Justin Timberlake and Katy Perry had fans taking to Facebook to discuss.

Stubbs said he thinks there was a good balance between the brand’s TV and online investment during the VMAs. But he would consider devoting

more resources to monitoring social activity. He imagines a focus group that might include a comic, an industry insider, and key millennials and

influencers in order to explore ways that the brand might respond to ultimate fans. “We know live TV is a place we need to be—it’s still incredible

appointment viewing,” he said. “But it’s not enough for an advertiser to show up with a beautiful ad and wait for everyone to come to it.”

Miley Cyrus VMA – Social Analytics – Valuable Insights

Business is challenging for us all

Media Planning has changed – less reliance on TV

Other video distribution forms slowly gaining traction

Connected TV´s and Smartphones are disruptive

Although TV is still dominant

Trading desks and Data Tools changing the way media is bought

Ratings models being challenged

Beware the Middlemen

Data changing everything –segmentation at scale

Content Management Tools allowing adaptive learning

Content Brands – distributed across channels and forms

Branded content types

Online providing more varied tactics

Relative Value

Traditional product placement

Emerging Options

Outstanding Ideas

How to optimise perishable inventory and the rise

of Agency Trading Desks

Technology Driven buying tools

• Programatic Buying

• Real Time Bidding Systems

• Data Management Platforms

• Content management

Systems

Challenge to optimise yield

without destroying value

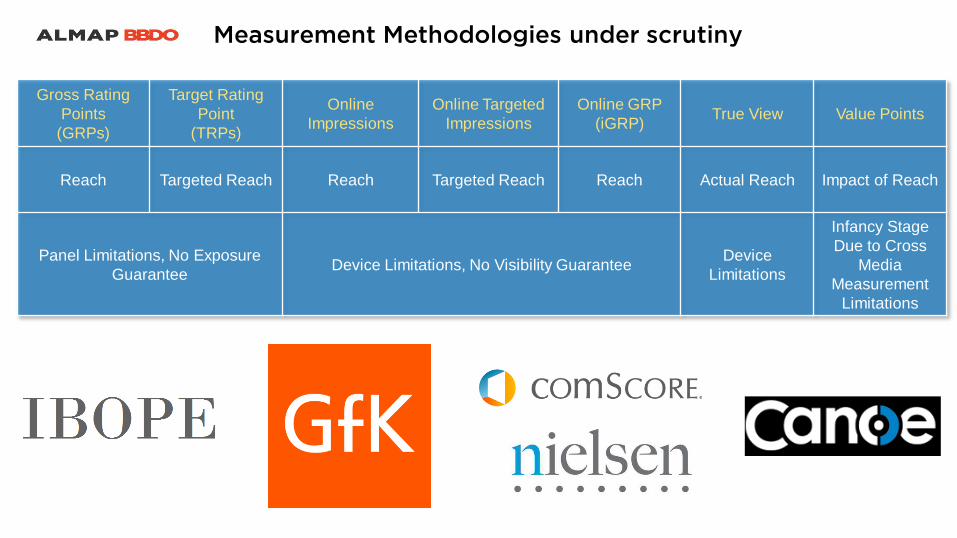

Measurement Methodologies under scrutiny

Gross Rating

Points

(GRPs)

Target Rating

Point

(TRPs)

Online

Impressions

Online Targeted

Impressions

Online GRP

(iGRP) True View Value Points

Reach Targeted Reach Reach Targeted Reach Reach Actual Reach Impact of Reach

Panel Limitations, No Exposure

Guarantee Device Limitations, No Visibility Guarantee

Device

Limitations

Infancy Stage

Due to Cross

Media

Measurement

Limitations

GroupM Trading Desk Unveils

Programmatic TV Audience Buying,

Claims Xaxis TV First To 'Sync'

Digital Campaigns With TV Ads

by Joe Mandese, Sep 9, 2013, 8:55 AM

Editor’s Note: The original version story incorrectly implied that

Xaxis TV would facilitate programmatic audience buys of

television inventory, when in fact, it will only utilize TV-like

metrics to target audience-buying in “broadcast-quality”

inventory online. Moreover, ABC has not agreed to incorporate

TV or video inventory as part of its agreement with Xaxis, just

static online display ads. For more about how Xaxis TV actually

works, read an interview with Xaxis’ Brian Gleason in RTBlog.

GroupM’s Xaxis unit, the largest of Madison Avenue’s so-called

trading desks, this morning unveiled its push into programmatic

television audience-buying with a new platform dubbed Xaxis

TV. The move comes as others, including Interpublic’s

Mediabrands, a spate of online video ad networks, and

targeted and addressable TV infrastructure players such as

Visible World and Invidi, have begun accelerating the

development of programmatic exchanges for buying and selling

TV audiences that are akin to online’s.

Xaxis TV, along with a second new platform called Xaxis Brand

Suite, is part of an ongoing push by Xaxis, “the world’s largest

audience buying company,” into traditional media. It previously

developed audience-buying exchanges covering out-of-home,

radio and conventional online video, and now it’s extending its

reach into television.

Significantly, Xaxis claims to have already gained access to

“premium inventory” from dozens of top “broadcast-quality

media owners” as part of its foray into programmatic TV

audience buying. While it did not disclose those partners, it

cited ABC as being among them.

“We are not only creating new channels and formats for

audience buying, we are connecting them, via our DMP, to the

broadcast metrics advertisers already understand,” Xaxis North

America Managing Director Brian Gleason stated, referring to

the acronym that stands for “data management platform," or

the organization that helps trading desks and DSPs identify

which users to target and serve ads to.

“The ability to measure activities across all channels together in

a single location provides a clear competitive advantage for our

clients,” he added.

One thing that differentiates Xaxis' push into TV is its privileged

access to actual TV viewers’ behavioral data via TV set-top

data agreements through its sister WPP companies, Kantar

Media Audiences and I-Behavior. As a result, Xaxis claims to

be “the first solution to allow advertisers to sync their digital

audience buying campaigns with broadcast TV ads and

programming."

Trading Desks - Treading Carefully Beyond Online

Interpublic Strikes Deals

Automating Buys With 5 Media

Giants: Covers TV, Radio,

Outdoor, Display, Video, Mobile

by Joe Mandese, Aug 20, 2013, 8:14 AM

On the heels of last week’s deal naming Adap.tv its

primary automation platform for targeting and buying TV

and video inventory, Interpublic this morning unveiled a

spate of similar deals to automate its transactions with

five big media suppliers traversing TV, radio, out-of-home,

mobile and online video and display.

Details about how the deals would be structured and how

they would work were not disclosed, but Interpublic said it

now has agreements with TV programmer A&E Networks,

cable operator Cablevision, out-of-home and radio

operator Clear Channel, local broadcaster Tribune and

online portal AOL, which is in the process of acquiring

Adap.tv, to supply assets “not previously available

through automated buying systems.”

The initiative, which was developed by Interpublic’s

Mediabrands unit, is dubbed the Magna Consortium, and

is part of the agency holding company’s mission to

automate 50% of its media-buying by 2016.

Interpublic has said it is making the push for several

reasons, including both greater operating efficiency for its

agencies and its clients as media-buying becomes hyper-

fragmented and hyper-complex, as well as greater

precision in targeting audiences it says will result by

shifting from conventional audience-buying data (ie.

Nielsen ratings, GRPs, etc.) to estimates that co-mingle

so-called first- and second-party sources of data in a

manner similar to the way agency trading desks utilize

DMPs -- or data management platforms -- to trade online

audience buys.

“The good news is that our charter members were quick

to sign on to develop a plan forward,” Magna Global

Worldwide CEO Tim Spengler stated, adding: “Our goal is

to ignite real change in the way media is transacted for

the industry.”

While programmatic trading systems are growing fast in

the online display marketplace (Magna estimates this is

currently about 25% of all online display advertising), the

growth has come largely from the emergence of an over-

supply of online inventory and auction-based media-

buying models like “RTB,” or real-time bidding, that many

“premium” suppliers are loath to embrace for fear it will

“commoditize” the value of their inventory.

However, some of the most premium online publishers

now participate in programmatic exchanges, and many of

those deals are not necessarily auction-based, but

function more like private exchanges where sellers can

set pricing “floors” and buyers can set “ceilings" to ensure

that both sides are in control of the process -- even if it’s

being processed by machines faster than humans can

manage such deal-making.

According to Frank Addante, CEO of Rubicon Project,

one of the biggest suppliers of media-buying automation

technology, the speed of such transactions is accelerating

and is now down to 30 milliseconds of processing time for

the average online buy. That’s an improvement from 300

milliseconds a year ago, and three seconds three years

ago, all thanks to improvements in data-processing

technologies.

The advances of such technologies, and the shift among

advertisers and agencies to use them to improve their

efficiency, as well as the data-driven effectiveness of

reaching their audiences, has sparked a gold rush among

media and advertising technology suppliers, many of

whom are now going public. One of the fastest-growing

and most sophisticated of those developers -- Rocket

Fuel, which utilizes artificial intelligence and robots that

can assess and bid for media value faster than any

human can -- is the latest to file for an initial public

offering.

In its filing late last week, Rocket Fuel noted that

advertisers are flocking to its technology, and that its

revenues more than doubled last year -- and more than

tripled during the first half of this one, thanks to a surge in

the number of advertisers using its platform. The filings

said Rocket Fuel currently has 784 advertisers (up from

341 last year), and that many of its existing advertisers

continue to increase the volume they trade via its

systems.

The greatest impediment to Interpublic’s goal of

automating 50% of all its media buys by 2016 is

convincing the most premium suppliers of media

inventory -- especially the major television networks --

that they won’t lose control, or value, by doing so, which

is why A&E Networks' direct involvement is so significant.

That said, at least a portion of all of the most premium TV

suppliers inventory already is being sold through

programmatic exchanges. While it’s not being sold

directly by the national TV networks themselves, the

trading desks of at least two agency holding companies

have already begun utilizing AudienceXpress, a

programmatic audience-buying exchange spun off from

target TV-ad serving developer Visible World. The portion

being traded by AudienceXpress comes from the two

minutes per hour that networks give to local cable TV

operators as part of their carriage agreements. While the

cable operators are supposed to sell that commercial time

to local or regional advertisers, AudienceXpress

effectively pools their national reach into unwired network

buys.

Since it became operational in late January,

AudienceXpress Founder and CEO Walt Horstman

estimates the two agency trading desks that have been

beta testing it have bought 2 billion TV advertising

impressions through it.

The reason why AudienceXpress has been successful

where others, including Google and Microsoft, have

failed, says Horstman, is that its platform is designed to

give suppliers 100% control over the floors they set for

selling their inventory, while giving buyers the ability to

analyze more data that will enhance the value of buying

those audiences from their perspective.

As with online publishing, the supply of unsold TV

inventory also continues to expand due to the emergence

of so-called “long-tail” networks that are not yet rated by

Nielsen, as well as a torrent of free video-on-demand

audience impressions.

Global Ad Buys Might Finally

Become a Reality - Marketing

across borders

By Lucia Moses August 18, 2013, 10:26 PM EDT

When the holding companiesPublicis and Omnicom

announced last month they were joining forces to form

the world’s largest ad agency group, they called it “a new

company for a new world.” Other, hyperbolic terms used

to describe the mega merger included “stunning,”

“seismic,” “a superstructure”—and that was just our own

reporting.

In reality, the concept of global marketing is not so earth-

shattering. It’s been around since the first merchant went

to sell his goods abroad. Yet on a larger scale, global

marketing has been much more challenging—borders

have proven to be barriers. And yet, OmniPubis just the

latest evidence that the global media buy may be

becoming more of a reality.

“We can now reach consumers globally and get feedback

globally,” IAB president and CEO Randall Rothenberg

points out. “Now, fact meets a 30-year-old theory,” he

says, referring to the rise of the idea in the ’80s that in the

age of the multinational corporation and the homogenized

consumer, marketers could (cheaply) sell the world the

same product with the same message—an idea that

would prove easier said than done.

Marketers would come to realize the monolithic global

consumer segment had its limits, as brands found that

translating ad campaigns into other cultures required

more local understanding than they had anticipated. And

even if marketers were set up to buy globally, media

weren’t. Global media conglomerates owned individual

properties that were local, regional or national, and

buying remained a market-by-market transaction.

Enter global digital giants Facebook and Google, enabling

marketers like Nestlé and Nike to reach a wide swath of

consumers. And those properties don’t just afford scale—

with their reams of consumer data, marketers found they

could pinpoint customers and update their messaging in

real time.

Top brands like Samsung, Nike and L’Oréal are already

immersed in digital as a means of getting their messages

out across borders. Most every marketer is at least

dipping a toe in. “Client after client, there’s discussion of

global media,” says Eric Bader, CMO of RadiumOne,

speaking of his previous stint at Initiative. “They want to

lower the cost of putting their message in front of

consumers. That’s what every CEO is tasked to do.”

Whether it’s a new car or motion picture being marketed,

digital offers scale and targeting, points out Carolyn

Everson, vp, global marketing solutions at Facebook.

“Some of the only ways to reach people in the Philippines

is on their mobile device,” she says.

What’s more, digital media present fewer risks with its

consistency of audience measurement worldwide, versus

traditional media and their patchwork of standards market

to market. And media sellers and agencies are setting

themselves up to follow marketers’ global shift online.

Interpublic’s IPG Mediabrands, for one, is creating a new

publishing division that will enable it to tailor global

messages to be distributed locally, in real time. Online

giants are building their digital video ad networks with an

eye on TV ad dollars. Facebook is said to be planning to

sell 15-second, TV-style ads, while Google’s YouTube

has been bankrolling premium channels, and AOL just

plunked down $405 million for a video ad platform.

Among traditional media, TV networks and sports leagues

are teaming up to facilitate global marketers buying major

events like the Olympics. The New York Times is

rebranding its International Herald Tribune as the

International New York Times, and Hearst Magazines has

created a global digital ad sales unit, Totally Global

Media, to simplify sales across sites that reach 200 million

unique visitors worldwide each month. Hearst also plans

to add its international inventory to the private online ad

exchange it operates in the U.S.

“We see these global citizens, people who are consuming

news outside their home country because they may be

traveling, owning businesses in other countries. They may

have family in other countries,” says Andy Wright, group

advertising vp at the Times. “This single brand will allow

us to build on the consumer side, but also on the success

we’ve had with advertisers.”

Even as some barriers to global ad buys have fallen

away, significant ones still remain. Not all clients are set

up to buy and carry out global ad campaigns, and much

of the time budgets are still locally controlled or multiple

agencies work on a brand. The typical ad budget is still

mostly tied up in TV, which is local in nature. And with no

accepted way of translating GRPs to click-throughs, it is

difficult to convert TV dollars to digital—one of the biggest

barriers in the shift to online media. Says Bader: “I think

there’s a lot of spending that could be globally based. TV

has been the last big iceberg that hasn’t moved over yet.”

The creative process also needs to catch up to the global

opportunity. While categories like electronics and movies

might have the same message worldwide, others,

including food and cosmetics, are regionally specific. The

theoretical ease of buying digitally doesn’t negate the

need for messaging to be tailored locally, even in search.

“One size fits all is a massive mistake,” Bader says.

But there’s scarcity in content, says Mark Renshaw, chief

innovation officer at Leo Burnett, whose clients include

global brands like Coca-Cola and McDonald’s. “YouTube

has an unlimited shelf space,” he says. “Brands are still

struggling with global content production. There’s legal

approval, production companies that may not be the most

adaptive. There’s a new dynamic, and we’ve got to

change the way we work.”

The inertia of years past is beginning to change, says

Eileen Naughton, global accounts lead at Google.

Naughton cites recent campaigns like Nike’s “Find Your

Greatness” and Dove’s “Real Beauty Sketches” that the

clients amplified on YouTube after seeing them take off

on social media. “Certain companies operate extremely

well,” she says. “The more sophisticated marketers get it.”

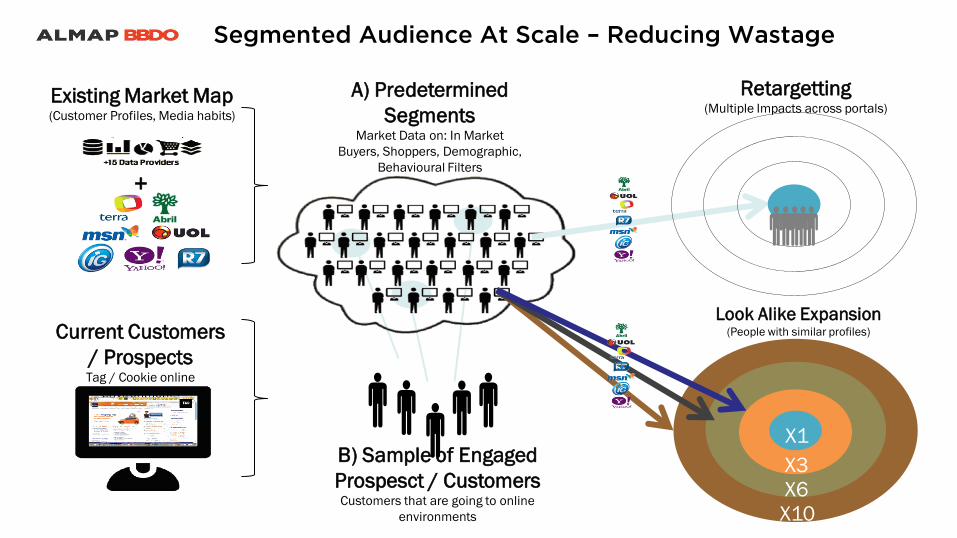

Existing Market Map (Customer Profiles, Media habits)

+

B) Sample of Engaged

Prospesct / Customers Customers that are going to online

environments

A) Predetermined

Segments Market Data on: In Market

Buyers, Shoppers, Demographic,

Behavioural Filters

Retargetting (Multiple Impacts across portals)

Look Alike Expansion (People with similar profiles)

X10

X6

X3

X1

Current Customers

/ Prospects Tag / Cookie online

environments

Segmented Audience At Scale – Reducing Wastage

Richer content form the better

Bandwidth no longer an issue

More relevant – lower quality expectation

Production costs reducing to enable lower cost segmented content

Timeliness – time sensitive content vs evergreen

First 5 seconds essential

Content production quality – Broadcast quality not

always needed

Mass Content

Segmented Content

Mass

Audience

Segmented

Audience

Addressable

Performance based (Geographic, Demographic

Behavioural, Consumption)

Mass

Exposure Based (Geographic, Demographic)

Inefficient

Ideal

A Balance

Most Practical

Test & Learn

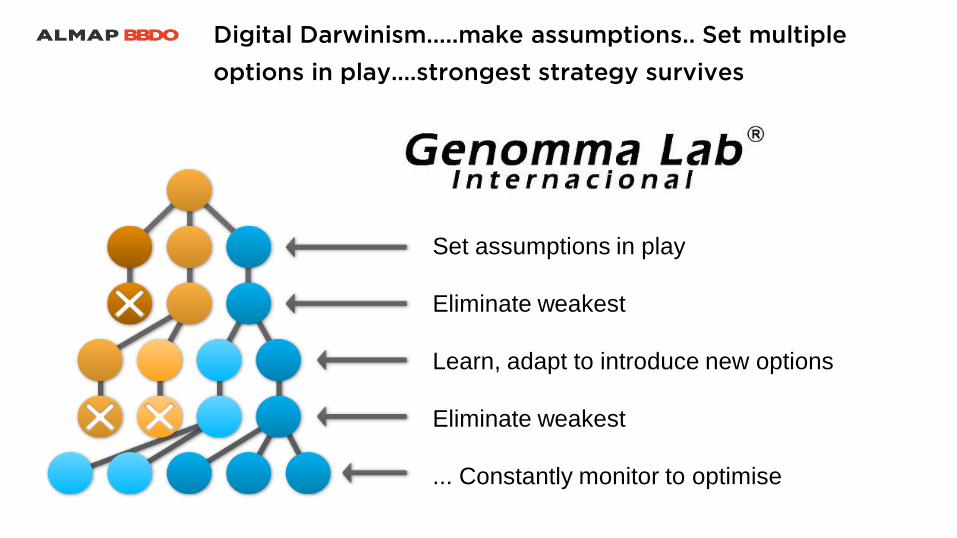

Integrating Segmented Marketing to drive performance

Set assumptions in play

Eliminate weakest

Learn, adapt to introduce new options

Eliminate weakest

... Constantly monitor to optimise

Digital Darwinism.....make assumptions.. Set multiple

options in play….strongest strategy survives

Site context - Location - Behavioral

User demo - Client data - Retargeting

Variants:

Ad size

Color

Product

Message

Call to action

Price

Social features

Dynamic Creative Optimization

Opt In Video – First 5 seconds crucial (To avoid skipping)

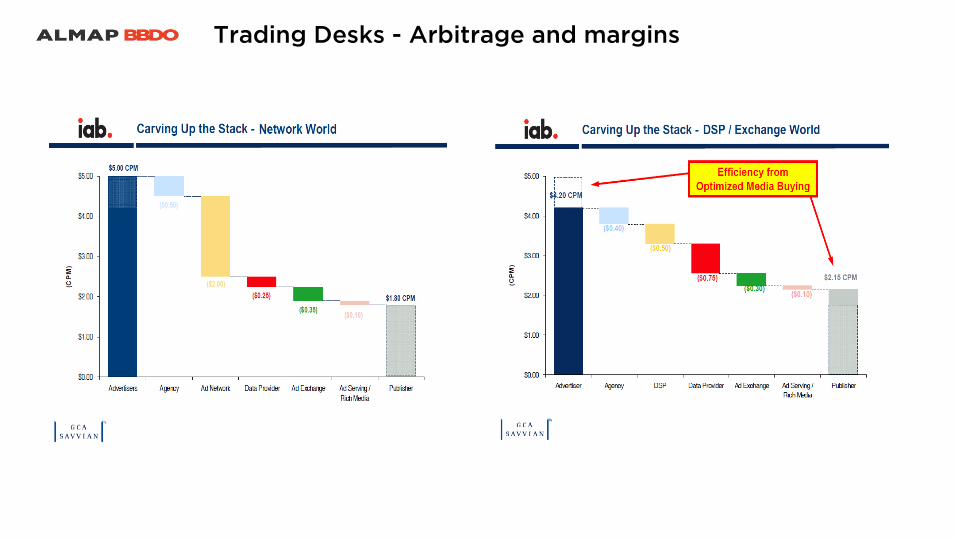

Trading Desks - Arbitrage and margins

PORTABLE DEVICES

One of the advantages of the Brazilian digital TV is mobility. You can watch digital TV

through mobile devices such as mobile phones with digital TV, mini-TVs, laptops and

other devices with screens smaller than televisions. Whether you're in a car, bus, train

or on foot: the image is always of excellent quality.

Protecting your content from middlemen

Protect your customer data

Content Brands / Mastheads / Franchises –

Distributed across content forms and channels

WOM

Trailer

Posters

Merchandising

Film

TV ads

Print ads

Star tours

Directors cuts

Samples

Digital

Games

Making of

Commentaries

User generated

Blogs

Winks

Soundtracks

Ringtones

Wallpapers

PR

Promotions

Casting competitions

Transalation casting 1. Each Film is a business in itself

2. The stakeholder are the business

owners

3. Core idea focus (Start from the

centre out)

4. Core idea scenario testing

5. Process leader / director

6. Consistent branding across all

touch / brand experience points

7. Clearly aligned process (across

multiple specialist suppliers)

8. Content planning (clear / efficient

development plan before channel

selection)

9. Source of innovation based on

ROI

10. Balance of short term and long

term brand needs

Film Marketing: Excellent example of Multiplatform content

Business is challenging for us all

Media Planning has changed – less reliance on TV

Other video distribution forms slowly gaining traction

Connected TV´s and Smartphones are disruptive

Although TV is still dominant

Trading desks and Data Tools changing the way media is bought

Ratings models being challenged

Beware the Middlemen

Data changing everything –segmentation at scale

Content Management Tools allowing adaptive learning

Content Brands – distributed across channels and forms

Branded content types

Online providing more varied tactics

Relative Value

Traditional product placement

Emerging Options

Outstanding Ideas

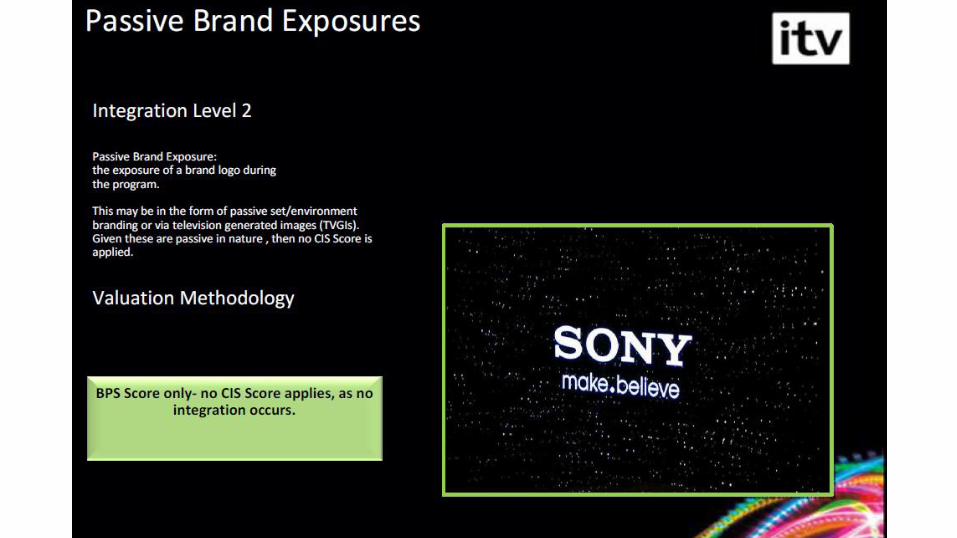

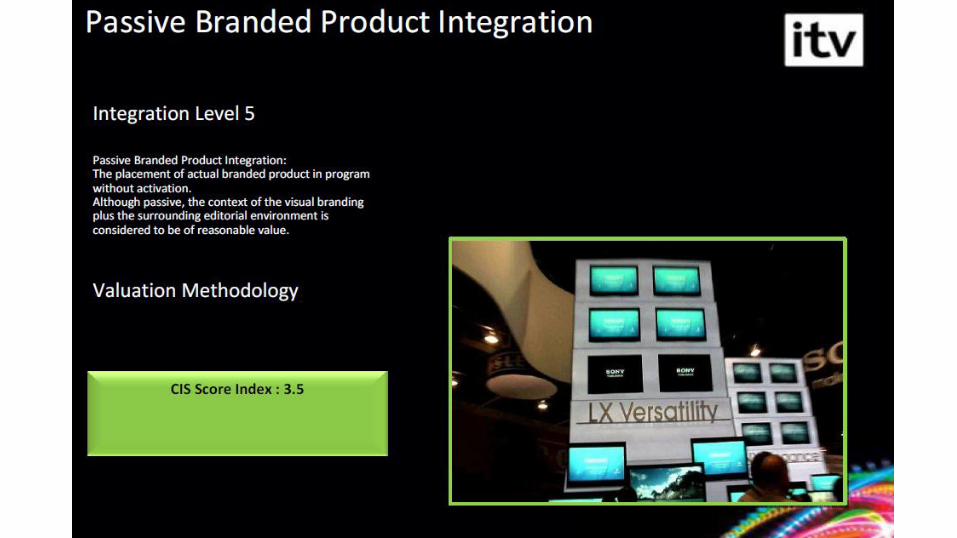

Traditional

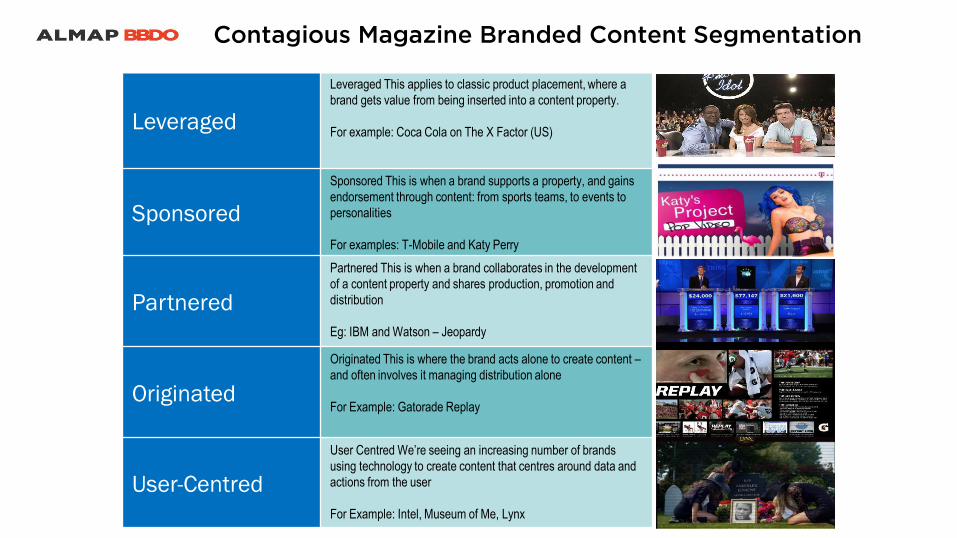

Leveraged

Leveraged This applies to classic product placement, where a

brand gets value from being inserted into a content property.

For example: Coca Cola on The X Factor (US)

Sponsored

Sponsored This is when a brand supports a property, and gains

endorsement through content: from sports teams, to events to

personalities

For examples: T-Mobile and Katy Perry

Partnered

Partnered This is when a brand collaborates in the development

of a content property and shares production, promotion and

distribution

Eg: IBM and Watson – Jeopardy

Originated

Originated This is where the brand acts alone to create content –

and often involves it managing distribution alone

For Example: Gatorade Replay

User-Centred

User Centred We’re seeing an increasing number of brands

using technology to create content that centres around data and

actions from the user

For Example: Intel, Museum of Me, Lynx

Contagious Magazine Branded Content Segmentation

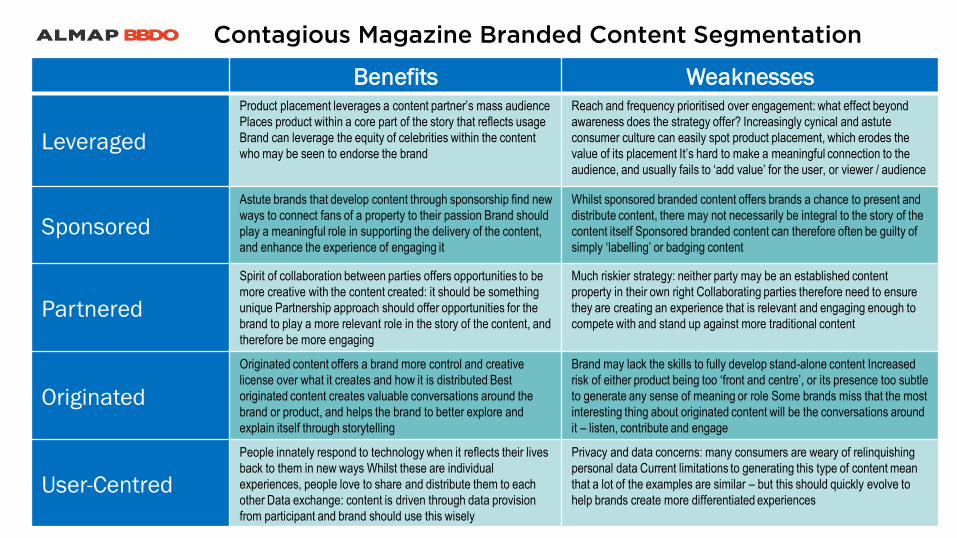

Benefits Weaknesses

Leveraged

Product placement leverages a content partner’s mass audience

Places product within a core part of the story that reflects usage

Brand can leverage the equity of celebrities within the content

who may be seen to endorse the brand

Reach and frequency prioritised over engagement: what effect beyond

awareness does the strategy offer? Increasingly cynical and astute

consumer culture can easily spot product placement, which erodes the

value of its placement It’s hard to make a meaningful connection to the

audience, and usually fails to ‘add value’ for the user, or viewer / audience

Sponsored

Astute brands that develop content through sponsorship find new

ways to connect fans of a property to their passion Brand should

play a meaningful role in supporting the delivery of the content,

and enhance the experience of engaging it

Whilst sponsored branded content offers brands a chance to present and

distribute content, there may not necessarily be integral to the story of the

content itself Sponsored branded content can therefore often be guilty of

simply ‘labelling’ or badging content

Partnered

Spirit of collaboration between parties offers opportunities to be

more creative with the content created: it should be something

unique Partnership approach should offer opportunities for the

brand to play a more relevant role in the story of the content, and

therefore be more engaging

Much riskier strategy: neither party may be an established content

property in their own right Collaborating parties therefore need to ensure

they are creating an experience that is relevant and engaging enough to

compete with and stand up against more traditional content

Originated

Originated content offers a brand more control and creative

license over what it creates and how it is distributed Best

originated content creates valuable conversations around the

brand or product, and helps the brand to better explore and

explain itself through storytelling

Brand may lack the skills to fully develop stand-alone content Increased

risk of either product being too ‘front and centre’, or its presence too subtle

to generate any sense of meaning or role Some brands miss that the most

interesting thing about originated content will be the conversations around

it – listen, contribute and engage

User-Centred

People innately respond to technology when it reflects their lives

back to them in new ways Whilst these are individual

experiences, people love to share and distribute them to each

other Data exchange: content is driven through data provision

from participant and brand should use this wisely

Privacy and data concerns: many consumers are weary of relinquishing

personal data Current limitations to generating this type of content mean

that a lot of the examples are similar – but this should quickly evolve to

help brands create more differentiated experiences

Contagious Magazine Branded Content Segmentation

Emerging

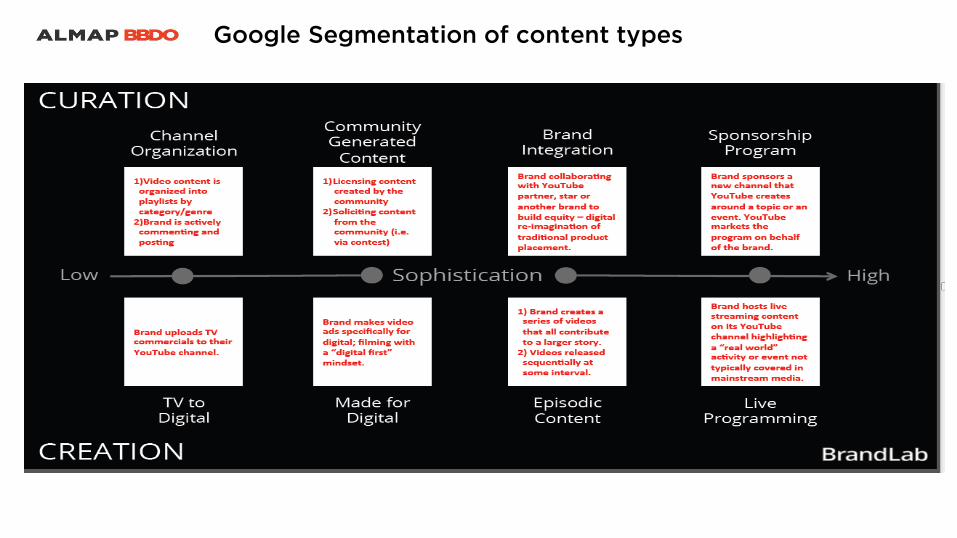

Google Segmentation of content types

Google Segmentation of content types

http://www.youtube.com/user/TheNorthFaceVideo

http://www.youtube.com/watch?v=ruav0KvQOOg

http://www.youtube.com/user/GoProCamera

http://www.youtube.com/watch?v=RP4abiHdQpc

http://www.youtube.com/watch?v=rA7IIHdY6XQ

http://www.youtube.com/watch?v=Xt6at8wCkbw

http://www.youtube.com/watch?v=NLJtCzc5POg

Relative Value

Traditional

AXN: The Firm Virtual Billboards

AXN: Hannibal Virtual Product Placement

CQC - Pepsi

• All vignettes are original from the TV Show

production and part of the context

• The content of the show is audacious and

witty, aligned with the brand essence

• The sponsorship lasts longer then the buy,

generating lots of productivity

• Alignment with target audience

• Weekly show guarantees constant awareness

generation

Syndicated

Media Delivery & Investment

504 inserts of 5” Vignettes opening and closing the program, and split all over the

network programming

581 30” spots inside the program breaks and all over the network programming

VW Logo along the Football Arena Billboards

Total delivery of 1,114 GRPs weighted in Both AB 18+ during 2013

CPP of R$ 7,450.00 (around 55% less than usual VW BTV CPP)

Investment = R$ 8,3 Million in ‘13 (+18% Vs. VW ‘12 SBT media spend)

Special Projects

Besides the regular media delivery, VW special media proprieties below:

•Team Captain Task: each episode, the winner of this task will be nominated as “O

Cara” and will receive a VW Clamp as the winner of the day;

•Second Screen: along with the BTV programming, exclusive VW digital content and

promotion, will engage the audience and create interactions, asking for tips about

who will be “O Cara” of the that episode;

•Exclusive VW Content: in every final episode, the boys have to go home and return

to the Reality Show in the other day, so, VW will transport them using VW Cars, while

interviewing the boys to hear about their dreams, idols, real life and all that inspire to

become “O Cara” (Exposition in BTV + VW Digital Platforms as YT + FB)

SBT is the

second biggest

Broadcast TV

Network in Brazil

in terms of

audience share

considering total

territory

Source: Ibope Media Workstation – Broadcast TV Nationwide

Period: 28/01 to 03/02 of 2013 / Target: Brazilian Households Criteria: weighted 5” using index of 0,375 Media delivery considering also regular media

along 2013 negotiated along with the media package

All Day Average Audience Participation %

Reality Show “Menino de Ouro”

Thousands of boys in Brazil want to be a football star, and this Reality Show, Menino de Ouro, selected 22 boys (13 to 15 years old) among 10,000 candidates, who will run several eliminating football competition tasks along the program, and only one will become the winner after 12 episodes (March 24th to June 9th 2013), becoming “O Cara”, to be hired by a big football team in the city of São Paulo.

Football DSDS – SBT/Fremantle Reality Show

RBS - Peneirinha Gillette 2012

Emerging

Fiat debut campaign with Shazam Platform allows

consumers to synchronize campaign through audio

and gain access to extra content

NATHALIE URSINI | » October 22 , 2013

Fiat is Brazil's first advertiser to try the new features

of Shazam . The campaign will debut in Shazam for

TV , was to launch the new Strada 2014 which has

squashed in music and mood communication. The

campaign premiered on television last weekend and

has creation of Fiat Agency , which includes

professionals Leo Burnett Tailor Made and

AgênciaClick Isobar .

A parody of the song Mary, who gained notoriety in

the voice and swagger of Ricky Martin, who leads

the film presents the main new features of the car:

higher volume in the hopper , new design and the

third door. The campaign films for television ,

internet and radio spots .

Shazam – Like a QR code for Audio

Master is Aired,

Signal is Broadcast

Digital signal (Watermark) is

embedded in the master

Mobile App listens,

Recognizes signal (ACR)

1

2

3 Signal triggers events

inside the app 4

Shazam links second screen to TV.

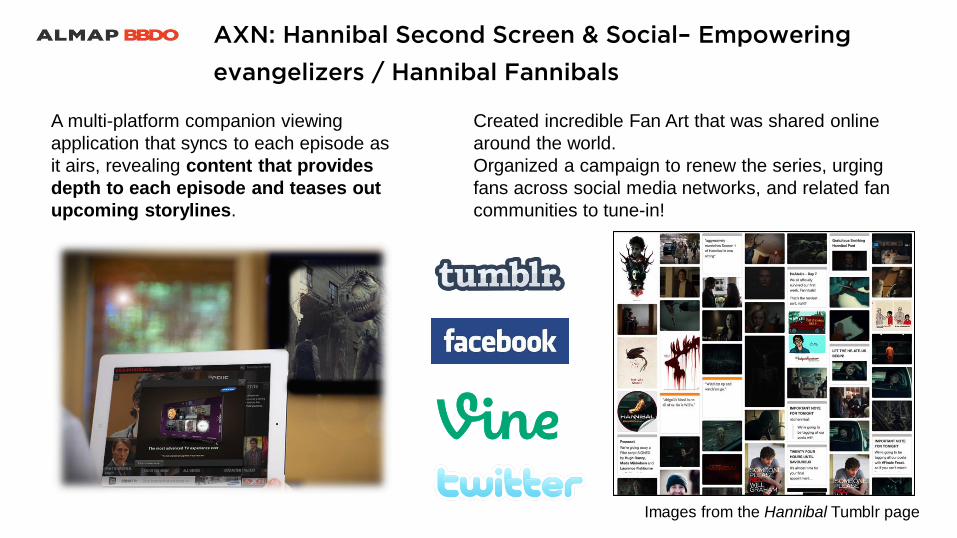

A multi-platform companion viewing

application that syncs to each episode as

it airs, revealing content that provides

depth to each episode and teases out

upcoming storylines.

AXN: Hannibal Second Screen & Social– Empowering

evangelizers / Hannibal Fannibals

Created incredible Fan Art that was shared online

around the world.

Organized a campaign to renew the series, urging

fans across social media networks, and related fan

communities to tune-in!

Images from the Hannibal Tumblr page

Outstanding Stories

We closed an unprecedented project with Globo to create a character in the novella Joia Rara.

Being a period novella, which portrays the culture of the country and of other nationalities, including

Italians, we took the opportunity to tell the story of the arrival of Panettone in Brazil, introducing Mr.

Bauducco in the plot.

Mr. Bauducco - Globo 6pm Novella

Business is challenging for us all

Media Planning has changed – less reliance on TV

Other video distribution forms slowly gaining traction

Connected TV´s and Smartphones are disruptive

Although TV is still dominant

Trading desks and Data Tools changing the way media is bought

Ratings models being challenged

Beware the Middlemen

Data changing everything –segmentation at scale

Content Management Tools allowing adaptive learning

Content Brands – distributed across channels and forms

Branded content types

Online providing more varied tactics

Relative Value

Traditional product placement

Emerging Options

Outstanding Ideas