47

Alternative Approaches to Cargo Policy: A Supplement to an Assessment of Maritime Trade and Technology August 1985 NTIS order #PB85-239887

Alternative Approaches to Cargo Policy: ASupplement to an Assessment of Maritime

Trade and Technology

August 1985

NTIS order #PB85-239887

Recommended Citation:Alternative Approaches to Cargo Policy: A Supplement to An Assessment of MaritimeTrade and Technology (Washington, DC: U.S. Congress, Office of Technology Assess-ment, OTA-BP-0-36, August 1985).

Library of Congress Catalog Card Number 85-600569

For sale by the Superintendent of DocumentsU.S. Government Printing Office, Washington, DC 20402

Foreword

The United States increasingly depends upon international trade and shipping tomaintain a healthy economy. As trade has grown in importance, so too has the FederalGovernment’s role in assuring fair and equitable U.S. participation in internationalshipping.

When OTA published An Assessment of Maritime Trade and Technology in Oc-tober 1983, one of its principal findings was that because national interests were notdefined and strategies for international negotiation had not been developed, there wasat that time no generally accepted U.S. cargo policy. The assessment stressed the pro-found influence of Federal policy and analyzed several options for congressional con-sideration, including that of clearly defining U.S. national interests and devising strate-gies and guidelines for future cargo policy initiatives.

Subsequently, the Senate and House Merchant Marine Subcommittees requestedthat OTA conduct additional analyses of cargo policy. OTA found that there is stillno generally accepted U.S. cargo policy, because U.S. interests and negotiating strate-gies have not been defined. But foreign governments have adopted such policies, whichincreases the disadvantage of U.S. shipping interests and therefore increases the intensityof the debate over U.S. cargo policy.

As part of its investigation, OTA held a two-day workshop on December 3 and4, 1984, with participants from the interested parties—shippers, operators, trading firms,and Government. The workshop focused on three topics: 1) the effects of cargo pol-icies now in force; 2) the status of new policies under consideration by the United Statesand its various trading partners; and 3) costs and benefits of existing, proposed andalternative policies. The workshop was structured around a series of presentations, fol-lowed by general discussion by participants selected on the basis of interest and exper-tise in four topic areas:

● Panel 1, Current Policy Initiatives;s Panel 2, Industry Impacts of Liner Cargo Policies;s Panel 3, Industry Impacts of Bulk Cargo Policies; andc Panel 4, Alternative Approaches to Cargo Policy.

Summaries of panelists’ presentations and discussion for each panel are presented inappendix A.

Director

,..///

OTA Project Staff—Alternative Approaches to Cargo Policy

John Andelin, Assistant Director, OTAScience, Information, and Natural Resources Division

Robert W. Niblock, Oceans and Environment Program Manager

Project Staff

Peter A. Johnson, Project Director

Nan Harllee Paul B. Phelps

Administrative Staff

Kathleen A. Beil Jacquelynne R. Mulder

iv

OTA Workshop Participants, December 3 and 4, 1984

Panelists

Charles AngevineDepartment of State

George BergAmerican Farm Bureau Federation

Gus CarasOgden Corp.

Deborah ChristieDepartment of Defense

H. Clayton CookCadwalader, Wickersham and TaftRobert EllsworthFederal Maritime Commission

Peter FinnertySea-Land Corp.

Ernst FrankelMassachusetts Institute of Technology

Brian GarbeckiU.S. International Trade Commission

Jack GoldsteinOverseas Shipholding GroupBonnie GreenAmerican President Lines

William JohnsonDepartment of Commerce

Leslie KanukBaruch College

Don Kash, Session ModeratorUniversity of Oklahoma

Kenneth KastnerChemical Manufacturers AssociationSandra KjellbergMIRAID

John LeeperSimat, Inc.

Arnold LevineDepartment of Transportation

Peter LucianoTransportation Institute

Joseph LykesLykes Bros. SS. Co.Kay McLennanDepartment of Agriculture

Sam NemirowCouncil of American Flag Ship Operators

Lewis PaineDepartment of Transportation

Robert RickertE.I. du Pont de Nemours &Co., Inc.

Emery SimonOffice of the U.S. Trade RepresentativeWilliam TuthillJoint Maritime Congress

Harlan UnmanGeorgetown University

Roger Wigen3M Co.

Gene YourchFederation of American Controlled Shipping

OTA and Congressional Staff

John AndelinOTA, Assistant Director

David DyeSenate Committee on Merchant Marine and

Fisheries

Caroline GabelHouse Committee on Public Works and

TransportationJack GibbonsOTA, Director

Chris GoebelHouse Committee on Public Works and

Transportation

John HardySenate Committee on Merchant Marine

Fisheries

Nan HarlleeOTA, Senior AnalystPeter JohnsonOTA, Project Director

Larry MallonHouse Committee on Merchant Marine

Fisheries

Bob NiblockOTA, Program Manager

and

and

Kip RobinsonHouse Committee on Merchant Marine and

Fisheries

Gerald SeifertHouse Committee on Merchant Marine and

Fisheries

Lenore SekCongressional Research ServicePeter TarpgaardCongressional Budget Office

Cyndy WilkinsonHouse Committee on Merchant Marine and

Fisheries

Alternates and Observers

Jim CaronDepartment of Agriculture

Joann DeCarloCenter for Strategic and International Studies

Judy DemetriadesDepartment of Agriculture

John GaughanMaritime AdministrationJackie IgoeAIMS

George MillerLubrizol Corp.

Steve MoodyFACS

Jack ParkCrowley Maritime Corp.

Paula PetavinoCenter for Strategic and International StudiesJanet RiceOffice of Management and Budget

William J. SmithFederal Maritime Commission

Erik StrombergFederal Maritime Commission

Joe ToraselliPrudential Lines

Brandt WagnerCASO

vi

Contents

Section Page

1.

2.

3.

INTRODUCTION . . . . .Shipping Industry . . . .Cargo Policies . . . . . . . . .Cargo Preference in the

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .United States . . . . . . . . . . . . . . . . . .

STATUS AND ISSUES IN CARGO POLICY. . . . . . . . . . . .Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .U.S. Cargo Preference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Multilateral Cargo Sharing . . . . . . . . . . . . . . . . . . . . . . . . . . . .Bilateral Cargo Sharing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Defense Needs and Cargo Policy . . . . . . . . . . . . . . . . . . . . . . .

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .U.S. Cargo Preference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Multilateral Cargo Sharing . . . . . . . . . . . . . . . . . . . . . . . . . . . .Bilateral Cargo Sharing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .National Defense and Cargo Sharing . . . . . . . . . . . . . . . . . . .

Appendixes

A.

B.

c.

Summary of Panel Presentations and Discussion . . . . . . . .Panel on Current Policy Initiatives . . . . . . . . . . . . . . . . . . . .Panel on Industry Impacts of Liner Cargo Policies. . . . . . .Panel on Industry Impacts of Bulk Cargo Policies . . . . . . .Panel on Alternative Approaches to Cargo Policy . . . . . . .Plenary Session . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Summary of Specific Country Bilateral Negotiations . . . . .Brazil . . . . . . . . . . .China . . . . . . . . . . .Malaysia . . . . . . . .Philippines. . . . . . .Glossary of Terms

Table

Table No.1. Cargoes and Routes for a Typical Chemical Parcel Tanker

Figures

Figure No.1. Principal Commodities in World Seaborne Trade, 1980..2. World Seaborne Trade, 1960-84 . . . . . . . . . . . . . . . . . . . . . . .3. Projected World Seaborne Trade, 1975-2000 . . . . . . . . . . . .4. World Grain Shipments, 1983 . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

..., . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . .

3355

99

11141820

2727272828

Page

313134363840424242424244

PageVoyage . . . . . . . . . 37

Page. . . . . . . . . . . . . . . . . . . . 3. . . . . . . . . . . . . . . . . . . . 10..., . . . . . . . . . . . . . . . . 10..., . . . . . . . . . . . . . . . ., 12

5. Number of Merchant Seamen in U.S.-Flag and USEC Fleets, 1950-85 . . . . . . . . . . . . 23

Section I

Section 1

Introduction

SHIPPING INDUSTRY

Almost all international trade in goods is trans-ported by sea. Thus, ocean shipping plays a cen-tral and essential role in the world economy andin world trade. The United States is the world’slargest trading nation, and international marketsare increasingly important to U.S. industries. Be-tween 1970 and 1980, the value of U.S. interna-tional trade more than doubled, and the ratio ofU.S. exports to gross national product rose from4.4 to 8.5 percent.

Maritime trade generally is divided into threebroad categories: liquid-bulk, dry-bulk, and gen-eral cargo (see fig. 1). Petroleum alone accountsfor nearly all of the liquid-bulk trade and foralmost half of the total world tonnage shipped.About one-fourth of world tonnage consists ofdry-bulk commodities—principally mineral ores,coal, and grain. The remaining one-fourth con-sists of the variety of manufactured goods andconsumer products called general cargo,

The two principal modes of ship operation arethe liner mode, which serves the general cargo

trade, and the bulk mode, which serves both thedry- and the liquid-bulk trades. The liner indus-try carries general cargo from port to port at fixedrates and on regular schedules. Modern containerships are typical of the vessels used in liner trade.The liner industry commonly operates within con-ferences—international groups of private linercompanies that collectively agree on routes, sched-ules, rates, and other aspects of liner service. Thebulk industry normally does not form confer-ences. It employs a variety of ships, usually ona time- or voyage-charter (rental) basis, to carrysingle, large-volume commodities (e. g., iron ore,grain, coal, crude oil) over fixed and sometimeslong periods of time. The liner industry thus tendsto manage competition among major companies,while the bulk industry operates under much moreopen competition. The liner trades involve by farthe largest portion of world trade when measuredby dollar value, while the bulk trades account forthe largest portion by volume or tonnage.

Figure 1.— Principal Commodities in World Seaborne Trade, 1980

Oilcargoes

Crudeoil

I t Oil products

OL

SOURCE Fearnleys Review, 1982

3

4

5

CARGO POLICIES

All trading nations have a self-interest in ex-panding their exports and controlling their im-ports. As nations try to manage trade policy totheir best economic advantage, they tend to in-crease governmental involvement in shipping.Shipping policies tend to mirror trade policies. Asmight be expected, increasing protectionism intrade has spawned a variety of restrictive and pro-tectionist policies in the maritime area—unilateral,bilateral, and multilateral.

Historically, all maritime nations have pro-tected their national maritime interests throughthe implementation of some forms of cargo pol-icy, generally by reserving some or all of the car-riage of certain commodities for their own na-tional carriers. In the case of established maritimecountries, this is sometimes achieved throughclosed conferences— industry groups that aresanctioned by their respective governments. Suchconferences are able to assure national lines of fullor “fair” participation in their trade. In the caseof less developed countries (LDCs), more overtgovernment intervention is usually involved, suchas government ownership of shipping lines andtrading firms, Both conferences and more overtgovernment participation have been more com-mon in the liner trades than in the bulk trades upto now.

Many nations, particularly LDCs that are at-tempting to capture more export trade and bol-ster their national-flag fleets, are pushing for theestablishment of bilateral and multilateral cargo-sharing agreements. The latter objective has re-cently been achieved for liner trades by the UnitedNations Conference on Trade and Development(UNCTAD) in the form of a Code of Conduct forLiner Operations (or UNCTAD Liner Code),which went into effect in October 1983. It callsfor an even division of liner conference cargoesbetween trading partners, with a small percent-age possibly reserved for vessels of other nations,if agreed by the national-flag lines engaged in thetrade. The United States is not a signatory to thecode and has opposed it since it was first proposedin 1972.

U.S. ship operators face a significant disadvan-tage in dealing with countries where industry andgovernment have established closer ties, andwhere national and corporate goals are bettermeshed, than in the United States. U.S. shippingcompanies find it increasingly difficult to competein markets that are protectionist. Many foreigngovernments also tend to intervene specifically onbehalf of their national interests and their owncarriers. The U.S. Government has tended to dis-avow interference in international trade and cargoallocation.

CARGO PREFERENCE IN THE UNITED STATES

The practice of cargo preference can be direct purchased on an f.o.b. basis and exports on a c.i.f.or indirect. In some cases, a country mandates basis.1 In addition, governments frequently grantthat a certain percentage of its imports or exportsmust be carried on its national-flag vessels. Pro-

— .] \l’hen Imports are purchased “tree on b(lar(i ( t (). b. I t h e cost

vision may be made for bilateral or multilateral quotcci doe~ not include ocean transp(~rtatl(~n ! r(~m the exportingcargo-sharing, with the larger shares reserved for c ~~untr},. \\’herl exports are solci “cost, in~urance and freight ( c i. t. 1,

the national-flag lines of the trading partners. In- the cost quoted includes ocean transportation. This pt)lic} allt)ws

direct cargo preference can be accomplished bya nat]on to control tran~p~)rtat]on cwt~ in all itt import and exp[lrtt ransact]on~, and therefore to retain a go~’ernment right tt~ select

a government mandate requiring imports to be ] ts own flag ships t o carr} th i~ car~(),

6

various tax deductions and other fiscal incentivesto importers and exporters that utilize theirnational-flag carriers.

The United States has enacted three cargo-preference laws concerning the movement ofGovernment-impelled (shipped by Governmentagencies) and Government-financed cargoes.These are the Cargo Preference Act of 1954, Pub-lic Resolution 73-17 (P.R. 73-17), and the Mili-tary Transport Act of 1904.

The Cargo Preference Act of 1954 mandatesthat at least 50 percent of all U.S. Government-impelled cargoes must be carried on privatelyowned U.S.-flag vessels. It applies to Governmentcargoes shipped for U.S. Government account(e.g., military support cargoes) and to any car-goes shipped under Government grant or subsi-

dized loan, such as cargoes shipped by the U.S.Agency for International Development (AID).

P.R. 73-17, passed in 1934, requires that 100percent of any cargoes financed by loans madeby the U.S. Government to foster exports mustbe carried on U.S.-flag ships, This primarily con-cerns commodities backed by loans from theExport-Import Bank. There is provision forwaiver of the law by the Maritime Administra-tion (MarAd), so that up to 50 percent of suchshipments may be carried on the flag vessels ofthe recipient nation.

The Maritime Transport Act of 1904 requiresthat all supplies shipped for use of the U.S. ArmedForces must move on U.S.-flag ships. This lawinteracts with the Cargo Preference Act, with theresult that one-half of all such military shipmentsmust move on privately owned U.S. vessels.

Section 2

Status and Issuesin Cargo Policy

Section 2

Status and Issues in Cargo Policy

OVERVIEW

Both national and international approaches tocargo policies have recently undergone changes.2

These changes stem both from industry develop-ments and from events in the public policy arena.For

●

●

●

●

●

●

●

example:

The UNCTAD Liner Code has been in effectfor over a year, and experience with it isgrowing.Both U.S. and foreign liner companies havebegun some round-the-world shipping serv-ices; intermodal services are also growing.Serious overcapacity persists world-wide,especially in bulk shipping, forcing somecompanies out of business and others to seekgovernment protection.Discussions are proceeding between the UnitedStates and its developed country trading part-ners regarding effects of the UNCTAD LinerCode and the refusal of the United States toparticipate. Agreements to help assure U.S.carriers competitive access to cargoes areunder development, especially for cross-trades. 3

Initiatives to extend U.S. cargo preference tocommercial cargoes continue to meet strongopposition. Such changes are unlikely in thenear term.There have been attempts to repeal certainexisting preference programs. Record U.S.trade deficits provide a strong argument forthose who favor maintaining the lowest pos-sible transport cost for U.S. exports.Bilateral cargo-sharing initiatives from sometrading partners have met substantial U.S.opposition and few have advanced beyondthe discussion stage. In some other trades,discussions of bilateral provisions and agree-

‘Th~ hlstc)rlcal basli for unilateral, bilateral, and multllatera] struc-tures attectlng cargo allocation are described in the IQ83 OTA assess-men t This su pplem(’nt pro~’1 des an update [>f the Le)’ La rgo p~~l IC >’t[~plc+ tlt current interest.

‘A “cros+tracie” ]s defined as trade between two natlon~ wherethe (~cean carrier is a ship operator from a third nation.

50– 3’30 0 - El 5 - 3

ments took place in 1983 and 1984. ExistingSouth American/U. S. bilateral agreements,for example, are undergoing re-evaluation.The Shipping Act of 1984 (Public Law 98-237) is considered to have some effect oncargo policies because of a provision that al-lows U.S. action against foreign operatorswhose country unfairly restricts cargo accessby U.S. carriers.UNCTAD is proceeding, slowly, toward anevaluation of perceived problems with the“open registry” system.4 Some LDCs are ex-pected to continue pressure for the phase-outof open registry, It is not clear whether theU.S. Government has developed an adequatestrategy to responds

The volume of world seaborne trade increasedin 1984 for the first time since 1979 (see fig. 2),with containerized general cargo accounting formost of the increase during 1983-84. Some con-tinued expansion in world trade appears likely inthe near term, most likely in certain selected drybulk commodities and in the container trades (fig.3). For most U.S. carriers, the container trade isthe most significant,

While this trade in general cargo is expanding,the major liner companies are both shifting andexpanding services. New, larger ships are begin-

40pen rcglst ry sometimes called ‘t lags ot cc~nvenience’ ret t’r~to the pract lce of registering ships in a country ( I. Iberia and I’and m.]are prime examples ), while corporate t>wners reside in (~ne <>t t h~’major industrialized countries. The United States is the lar~ett (~ti’nt’rof open registry tleets.

‘Some industr} participants at the OTA workshop” ciiwgreed wy -lng that the Administration has consistently opposed” thi~ Uh”CTAI )] nit iat lve, The State Department a ISC) disagrees, c la I m i ng that t hcUnited States intends to continue to work with de~el[~ped ct)untrit’iin an eftort to insure that any agreement reached would pro\ld(,rights to owners t () register vessels in the countries (~t the] r L h~~lc e( Sam Keller, Oftice of Maritime and Land Transport, U S [depart-ment of State: pers~~na I commu n Ica t ion, hlat 21, 1 Q85 I [k;rt~ndthese clalms, h o w e v e r , OTA has not been” able to (~btaln an?documentation o{ an o~erall strateg}’ or \peciflc guldel{nes tor t ht>UNCTAD neg(~tiati~~n+, If it exists, such dcKumentat ]on may’ be clas-sified and t h LI\ not a \ra i I able for use i n pub] ic p[~] i c; deba to

9

10

Figure 2.— World Seaborne Trade, 1960-84

1,500

1,000

500

/I ●

\ / \

1960 1965 1970 1975 1980 1985

Year

SOURCE OECD & Fearnleys, 1984

Figure 3.—Projected World Seaborne Trade, 1975-2000Liquid-bulk Dry-bulk General cargo

I

4,000

3,000

2,0001,000

r-l1975 1980 1985 1990 1995 2000

Year

SOURCE Wharton Econometric Forecasting Associates.

ning “round-the-world” services calling at onlymajor hub ports, and the same firms are offeringmore comprehensive intermodal rates and serv-ices. Some industry spokesmen have observed

that increased rationalization in both large- andsmall-volume trades is forcing changes in the eco-nomics of liner shipping. Some industry analystsbelieve that “fewer, larger, more efficient enter-prises will compete for market shares in futureyears. “6

The OTA cargo policy workshop, togetherwith an analysis of the key questions raised bythe workshop and other sources, has identifiedfour issues that appear to be important not onlyto the health and vitality of the U.S. shipping in-dustry, but also to other vital national interestsinvolved in world trade and U.S. participation inthat trade. These issues, discussed ining sections, are:

● U.S. cargo preference;. multilateral cargo sharing;● bilateral cargo sharing; and● defense needs that affect cargo

“Peter Finnert} in J$’orld Ports, February 1985.

the follow-

policy.

— —

U.S. CARGO PREFERENCE

11

Current Authority

Cargo preference laws in the United States havenot changed since OTA’s Assessment of MaritimeTrade and Technology was published in 1983. Inessence, current law requires U.S.-flag preferenceon Government cargoes. This ranges from 50 per-cent of Government-impelled civilian cargoes to100 percent for military cargoes. The currentAdministration has opposed any extension ofcargo preference to commercial cargoes.

Three major cargo preference statutes are pres-ently in effect. The Military Transport Act of 1904(33 Stat. 518) mandates that 100 percent of De-partment of Defense cargoes must be transportedon U.S.-flag vessels. The Cargo Preference Actof 1954 (Public Law 83-664) calls for 50 percentof U.S. Government-impelled cargoes (includingmilitary) to be carried on privately owned U.S.-flag ships. Public Resolution 73-17, passed in1934, has evolved in practice to require that 100percent of cargoes financed by loans made by theU.S. Government to encourage exports must becarried on U.S.-flag ships. Such cargoes arelargely financed by Export-Import Bank loans.However, up to 50 percent of these shipments canbe carried on the vessels of the borrower’s choiceif a waiver is granted by the U.S. MaritimeAdministration (MarAd), upon a finding of non-discrimination to U.S.-flag shipping.

Federal agencies have also made cargo prefer-ence a topic of interagency debate: those repre-senting shippers take one side, and those repre-senting operators take the other. During the OTAworkshop, however, Federal agency representa-tives stated that the current Administration favorsneither an expansion nor a reduction in existingcargo-preference laws. Most of these officials ap-peared to agree that present laws are reasonable,but that any proposals to extend preference tocommercial cargoes would be strongly opposed.

Impacts of Liner Cargo Preference

Existing cargo-preference laws are important toU.S. liner operators. For the liner industry, suchcargoes account for only 4 to 8 percent of total

carriage, but these are frequently the “base car-goes” that make operations on some trade routescommercially feasible.

Proponents argue that the added cost of U.S.cargo preference for liner cargoes is usually small,because rates are set by industry conferences andvary little from carrier to carrier. The added costmay be higher in some instances, but such differ-entials tend to be minor in the aggregate, sincepreference shipments represent less than 10 per-cent of total U.S. liner cargoes. Other industryobservers, however, claim that if a large portionof cargo in any trade were merely allocated to aconference by law, with no other competitive orregulatory controls, then prices could in fact riseunreasonably.

However, liner carriers do differ from eachother in terms of the other forms of Governmentsupport they receive. One workshop participantsuggested evaluating whether the Governmentshould take into account the operating subsidiespaid to carriers when evaluating their bids forpreference cargoes, in order to compare the totalcost to the Government. This is done for bulkshipments already and has been recommended bythe Administration for liner shipments. The De-partment of Transportation has sent to the Houseand Senate a proposal for legislation to accom-plish this by increasing insurance fees and/or re-ducing subsidy payments to operators carryingsubsidized cargoes.

Impacts of Bulk Cargo Preference

For the few U.S.-flag bulk carriers, preferencecargoes are sometimes the only cargo carried (seefig. 4). For bulk preference cargoes, rates are ne-gotiated between shipper and carrier. However,the rates must be reviewed by the responsibleagency, such as the Department of Agriculture(USDA). The agency will approve rates only upto the “fair and reasonable guideline” ceiling cal-culated by MarAd.

Spokesmen for bulk shippers at the OTA work-shop opposed cargo preference and spoke emphat-ically in opposition to any expansion of preference

12—

Figure 4.—World Grain Shipments, 1983

NOTE Main Inter-area movements in million metric tonnes (billion ton-miles in brackets) Only main routes are shown Area figures and totals including smaller routesare not shown separately Total trade 199 million tonnes (1,135 billion ton.miles)

SOURCE” Fearnleys

laws. They presented statistics on the increasedcosts that would result for agricultural exports un-der commercial cargo preference, indicating thatif a 20-percent preference had existed in 1982, agri-cultural export costs would have risen substan-tially. If U.S. goods are to be competitive and U.S.farmers to make a profit, they claim transporta-tion must be at the lowest possible cost. In ship-pers’ eyes, the current U.S. trade deficit makesit even more imperative that U.S. exporters notbe burdened further with higher transportationcosts.

The preponderance of bulk preference cargoesare shipments of agricultural commodities underPublic Law 83-480, which established major U.S.agricultural commodity aid programs. These re-quirements received significant attention duringthe OTA workshop discussions. Under the CargoPreference Act of 1954 (Public Law 83-664), U.S.food assistance to less developed countries (LDCs)is subject to a 50-percent U.S. carrier reservation.USDA, which manages the preference require-ments for these Public Law 83-480 Title I (con-

cessionary sales) shipments, cited a transporta-tion differential cost of $120 million paid forU.S.-flag carriage of food assistance cargoes in1982. MarAd pointed out that the cost differen-tial had declined to $65 million in 1983 and $76million in 1984. Comparable detailed statistics arenot available for the Title II (gifts of food) ship-ments, whose preference requirements are moni-tored by the Agency for International Development(AID). However, a GAO study estimated thatU.S.-flag liner carriage under the Public Law 480Title II program could have cost $0.73/ton morethan foreign-flag carriage in 1980. At only $600,000for 1980, the Title II cost differential was smallcompared with Title 1.7

At present the U.S.-flag bulk fleet has operat-ing costs that average two to three times thoseof certain foreign competitors. These cost differen-tials are very significant to shippers, and U.S. bulk

H..J, S. General Accounting Office, Economic Effects of Cargo-Preference Laws, GAO OCE-84-3 (Washington, DC,: GAO, Jan.31, 1984).

13

carriers are utterly dependent on preference ship-ments for their survival. Panelists also pointed outthat the U.S. bulk fleet is modernizing signifi-cantly, which could lower future costs. A MarAdstudy of Public Law 83-480 shipments to Egyptshowed that in 1981, 61 percent of Public Law83-480 shipments were on bulk carriers over 22years old, while in 1984, 63 percent of shipmentswere carried on vessels 5 years old or under.8 Thismay lead to greater efficiency and reduced dif-ferentials in the future, because the new vesselsare more automated and use less fuel; but it doesnot imply that the U.S.-flag bulk fleet is nearingprofitability. A severe depression exists worldwidein bulk shipping, and foreign competitors areoffering very low rates.

Government participants at the OTA workshopdisagreed on the actual burden imposed by prefer-ence requirements. It is clear, however, that thereare problems with the bookkeeping, both in thetimeliness of information collection and, in someinstances, of records being kept at all. Furtherstudy on the costs and benefits of cargo prefer-ence might be useful.

Implementation

Liner industry spokesmen at the OTA work-shop alleged that the “50-percent requirement” isnot being met in a single U.S. preference program.While they are not pressing for expansion ofcargo-preference laws, liner operators are ex-tremely concerned that current laws are not be-ing enforced and that U.S. carriers are not get-ting the share of cargoes they are due. Participantssuggested that part of the problem is that MarAddoes not receive information on cargo carriage un-til well after the movement; it is difficult to en-force compliance after the fact.

Concern was greatest with respect to agricul-tural cargoes, and operators claimed that whennew programs are started they are usually de-signed to avoid preference requirements. In ad-dition, a number of DOD programs are not cov-ered. Recently promulgated Federal acquisitionregulations call for 50-percent preference. For

these programs, liner operators note that the 1904Act requires that 100 percent of DOD cargoes areto be carried by U.S.-flag ships. Some ExIm Bankprograms, like the short- and medium-term guar-antee programs, do not have U.S.-flag require-ments. Finally, conversion of AID’s commodity-export program to a cash-transfer program effec-tively diminished U.S.-flag participation. Indus-try representatives made a strong plea for enforce-ment of existing laws and suggested that it wouldbe very helpful for the President to make a clearstatement in support of those laws to assure com-pliance by Federal agencies.

An example of the controversy over implemen-tation of existing laws is the litigation resultingfrom USDA’s failure to apply cargo-preferencerequirements to the “Blended Credit ”9 export pro-motion program (Transportation Institute v. Doleand USDA ). A recent U.S. District Court deci-sion found that USDA and the Department ofTransportation had violated the law by not re-quiring the use of U.S.-flag ships for this program.The Administration has appealed the decision, butit has also suspended the Blended Credit Programand announced plans for a new export promo-tion program that will not be subject to cargopreference. Legislation has also been introducedin both the House and the Senate that would ex-empt some or all agricultural commodities fromcargo-preference rules.

OTA reviewed some of the claims of noncom-pliance in cargo-preference programs during 1984.The most recent data available measuring com-pliance are for calendar year 1982, as reported byMarAd in their Fiscal Year 1983 Annual Report .’”That year’s data show fairly good compliance,with some instances of U.S.-flag carriage wellabove the 50-percent requirement. Carriers rep-resented at the OTA workshop, however, claimedthat in 1983 and 1984 many programs did notcomply with these preference quotas. Data forthese years have not yet been reported by MarAd.

9This program [Jfters a “blend” or combination of twcl type~ ~)tcredit to a n~tion purchasin; U, S agricultural exports – one typebeing direct lntertmt-t ree lodns trom the Comm[~dlt}’ Credit Corp(~-rat i (~ n and the (~ t her helng c(~m mercl a I l[~an ~ua ra n t ees

I hlar,4d IS re~p[~n~lble t(~r m(>nlt[~rlng the ~dr~(~-preference pri~-gram~ (JI ~)thc’r a~encles, \uch as DOD, L’SIIA, a n d AI[), and t(~r

14

The question of compliance or noncompliancehas been the subject of an exchange of letters be-tween MarAd and the other agencies, especiallyAID and USDA. Many of these letters concerninterpretations of how to collect and use cargo-preference data and the circumstances that mayor may not be covered by cargo preference. Forexample, MarAd has exchanged several letterswith USDA’s Foreign Agricultural Service (FAS)on the subject of whether or not FAS compliedwith the Public Law 83-480 Title 1/111 programin 1983.11 MarAd claimed that the cargo statisticsshowed only 48.2 percent of the program’s totalcargo was actually shipped by U.S.-flag carriers.FAS claimed that they approved 50.1 percent ofthe total tonnage for U.S.-flag shipment but can-not control precise loading dates at the end of eachyear; thus, actuals may be above or below their“approved” number.

Such a debate over 1983 statistics may serveto clarify the nature of the problems and the com-plexity of the rules, but it shows little promise ofresolving the basic issue of cargo-preference com-pliance, Since a major Federal responsibility is re-solving conflicts in the public interest, it wouldbe useful for the agencies to jointly formulatecompliance guidelines, methods of reporting data,and practical methods of allocating cargo beforeshipment. Since an Interagency Shipping PolicyGroup already exists, Congress could require itto bring the agencies together on this subject and

MULTILATERAL CARGO SHARING

UNCTAD Liner Code

The UNCTAD Liner Code calls for sharing ofliner conference cargoes12 between the fleets oftrading partners, with some portion reserved forthird parties (cross-traders) if agreed to by the

prepare the cargo-preference guidelines and pro-cedures.

Discussion

U.S. cargo-preference programs appear to beflawed compromises, in which no one is fullysatisfied. On the one hand, many U.S. ship oper-ators and builders view cargo preference as a ne-cessity, both for countering similar practices inother countries and for maintaining an industryvital to national defense. Operators stress not only

the need for cargo preference policies, but alsothe need for implementation. Many operatorswho participate in existing cargo-preference pro-grams claim that current laws are not properlyenforced and that cargoes are not always reservedfor U.S. operators as required. In addition, thosewho favor Federal promotion of maritime indus-tries maintain that expanding cargo preference isan equitable method of indirect subsidy that is ur-gently needed to replace the direct constructionsubsidies of the past.

On the other hand, some Government shippersas well as many commercial shippers view cargo-preference laws as an unjustified cost burden.Such policies increase program funding needs,especially for agricultural support programs; orthey reduce the funding available for what are per-ceived to be other, more important uses; or theymake U.S. shippers noncompetitive in the worldmarket. Shippers—especially those of agriculturalproducts—have been strident in their oppositionto cargo preference, claiming that existing lawshave hurt the U.S. export position and that anyexpansion would cause further damage.

national-flag lines. The Code was developed byThird World nations in an effort to capture fortheir own carriers a larger percentage of their tradewith the industrialized world. The United Statesstrongly opposed the Code and refused to ratifyit, but the Code went into force among its signa-tories in October 1983. While it is too soon to as-sess its long-term economic effects, no significantimpacts are apparent yet.

15

A recent European analysis of the potential ef-fects of the UNCTAD Liner Code, based onknown reservations (or exclusions) to the cargo-sharing principle (such as the European EconomicCommunity’s reservation and the policies of theCentrally Planned Economies), found that onlyabout one-third of all trade will be regulated.13

The study suggested that while the eventual con-sequences of the Code are still uncertain, it islikely to have only a small effect in practice.

Potential Bulk Code

Workshop participants discussed the possibil-ity of an UNCTAD bulk code, generally conclud-ing that it is unlikely to happen. Many LDCs areless interested in pushing for a bulk code than theywere because they no longer perceive that it wouldbe in their interests. Many of these nations sim-ply do not have the wherewithal to build andoperate commercial fleets. In addition, there isclear opposition on the part of most OECD coun-tries. Bulk trade, unlike liner trade, does not fol-low established routes on a regular basis. Rather,bulk trade tends to be “round the world, ” withcontract carriage of a specific cargo from one placeto another. This arrangement does not lend itselfto some forms of cargo allocation.

Open Registry

Underdeveloped countries who espoused theLiner Code and proposed bulk code, now seek tophase out open registries as well. While no ac-tion has thus far been taken on a bulk code, con-ferences on open registry were held in 1983 and1984.

At issue is an attempt to phase out “flags of con-venience”: every carrier would be required to havea “substantial relationship” with the country un-der whose flag its ships sail. Many LDCs believethat if Western lines now flying the flags of con-venience registries, such as Panama and Liberia,were required to register elsewhere, these otherLDCs would capture a substantial share of thenew registrations and the resulting economic ben-

‘ ‘T. Wergeland, “UNCTAD Liner Code, 40-40-20: Potential Redls-tributi{~nal Eftects It>r Liner l’essels, ” Llq}’d’s Shipping Economist,February 1Q85, pp &Q.

efits. Another view expressed by LDCs on thissubject is that if Western flag-of-convenience car-riers are forced to register their ships under theirown national flag and employ Western seamen,they would be unable to operate economically andthus would phase out of many trades, enablingLDCs to increase their share of the carriage.

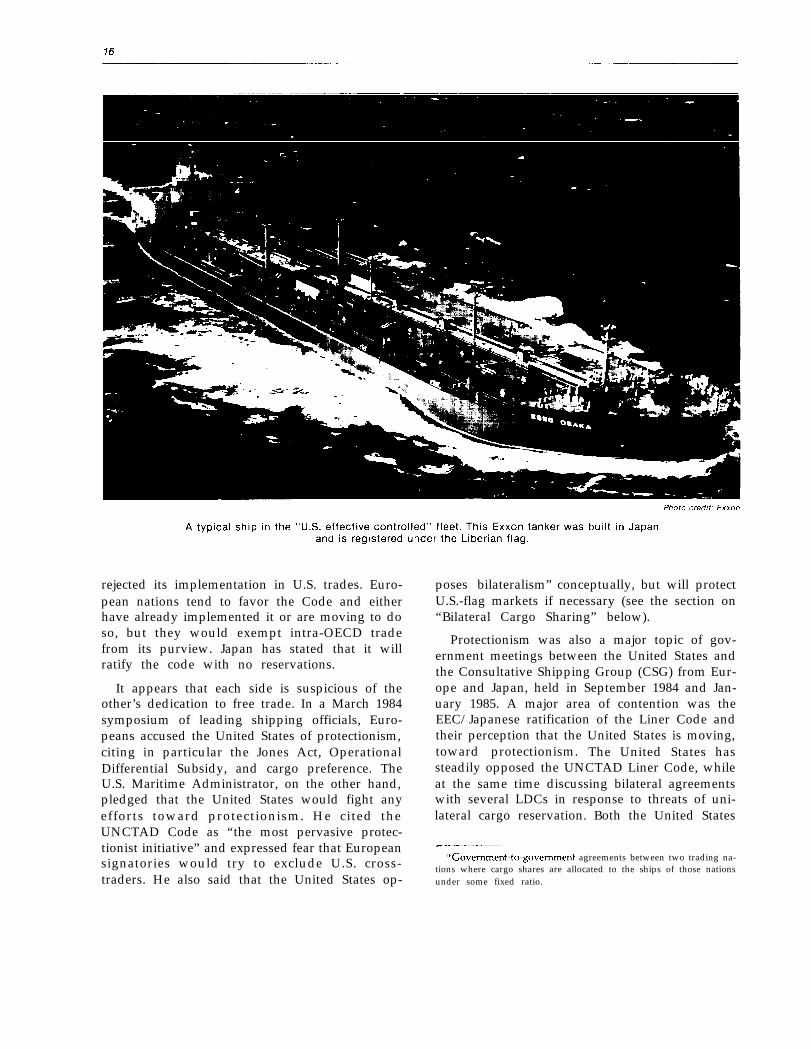

Phase-out of open registries is opposed by themajor shipping nations that make significant useof convenience flags. The “U.S. effective con-trolled” (USEC) fleet of U, S.-owned but foreign-registered vessels represents the single largest fleetof flags-of-convenience vessels in the world. TwoUNCTAD meetings, one in July/August 1984 andanother in February 1985, failed to reach any con-sensus on the open registry issue but produced anegotiating text which was considered at a July1985 session. (As this background paper was go-ing to press, reports from the open-registry talksin Geneva indicated that a compromise agreementmay be reached. ) The U.S. Administration be-lieves it is unlikely that open registry will bebanned any time soon. 14 However, efforts to doso will probably continue.

One workshop participant compared the U.S.approach to multilateral shipping agreements tothe negotiating approach that the United Stateshas taken in other areas of international marineaffairs. The issue expressed was whether U.S. tac-tics in this area will be analogous to the on-againoff-again U.S. approach to Law of the Sea, wherethe United States wound up out of sync with therest of the world; or whether it will instead beanalogous to the cooperative approach used forthe 200-mile fishery zone, which resulted in a sys-tem that requires other nations that fish in the U.S.zone to adhere to U.S. conditions. 15

Relations With Europe and Japan

Relations between the United States and its ma-jor trading partners—members of the EuropeanEconomic Community and Japan—continue to beunsettled in the wake of their adoption of theUNCTAD Liner Code. The United States resistedthe passage of the UNCTAD Liner Code and has

‘“It should be noted that U.S. officials did not think that the no;\-rat ified UNCTAD Liner Code had an~’ chance of passage either.

‘sTranscript ot OTA \4’orkshop on ‘Cargo I’olic}, p. 406.

rejected its implementation in U.S. trades. Euro-pean nations tend to favor the Code and eitherhave already implemented it or are moving to doso, but they would exempt intra-OECD tradefrom its purview. Japan has stated that it willratify the code with no reservations.

It appears that each side is suspicious of theother’s dedication to free trade. In a March 1984symposium of leading shipping officials, Euro-peans accused the United States of protectionism,citing in particular the Jones Act, OperationalDifferential Subsidy, and cargo preference. TheU.S. Maritime Administrator, on the other hand,pledged that the United States would fight anyefforts toward protectionism. He cited theUNCTAD Code as “the most pervasive protec-tionist initiative” and expressed fear that Europeansignatories would try to exclude U.S. cross-traders. He also said that the United States op-

poses bilateralism” conceptually, but will protectU.S.-flag markets if necessary (see the section on“Bilateral Cargo Sharing” below).

Protectionism was also a major topic of gov-ernment meetings between the United States andthe Consultative Shipping Group (CSG) from Eur-ope and Japan, held in September 1984 and Jan-uary 1985. A major area of contention was theEEC/Japanese ratification of the Liner Code andtheir perception that the United States is moving,toward protectionism. The United States hassteadily opposed the UNCTAD Liner Code, whileat the same time discussing bilateral agreementswith several LDCs in response to threats of uni-lateral cargo reservation. Both the United States

‘“Govemment-to-govemment agreements between two trading na-tions where cargo shares are allocated to the ships of those nationsunder some fixed ratio.

17

and the CSG, in short, perceive anticompetitiveactions on the part of the other, while at the sametime recognizing that coordination and coopera-tion are in the best interests of all parties.

The Europeans would like the United States toenter into a binding agreement under which eachsignatory would “resist protectionism .“ The spe-cifics of such an agreement are not clear, and atleast some United States representatives see nobenefit in yet another ambiguous statement on thesubject. The January 1985 CSG meeting addressedthe problem of assuring U.S. carriers access to car-goes in trades between the Third World and otherindustrialized countries. No agreement has beenreached on this point, although U.S. Governmentparticipants reported a narrowing of U.S.-CSGdifferences. These discussions are currently un-der review by the Administration. U.S.-flag lineroperators have urged the Administration to ter-minate current negotiations.

Cross-Trades

With increasing acceptance of the UNCTADLiner Code by foreign governments, some ob-servers are concerned that U.S. liner operatorscould be squeezed out of traditionally profitablecross-trades. Five U.S.-flag carriers (AmericanPresident Lines, Delta, Lykes, Sea-Land, and U.S.Lines) carried nearly 3 million long tons17 of cross-trade cargo in 1982, producing gross revenues ofalmost $300 million. Loss of such trade could haveserious consequences for U.S. carriers.

Participants at the OTA workshop liner panelstressed that cross-trading by U.S. carriers alsobenefits U.S. shippers and U.S. commerce in gen-eral. Revenues from cross-trade cargoes contrib-ute to the overall profitability of U.S. carriers,allowing them to remain competitive in the hotlycontested U.S. trade routes. Opportunities forcross-trading will also be increasingly importantas carriers develop and pursue round-the-worldtrade routes.

A study prepared by Manalytics, Inc., for theMaritime Administration concludes that the U.S.Government can effectively protect U.S. liners’

interests because a far larger percentage of U.S.trade is carried by third-flag vessels than is car-ried by U.S. carriers in foreign-to-foreign trades .18In 1982, for example, Northern European flagships lifted 12.9 million long tons of cargo ascross-traders in U.S. liner trades, while U.S. cross-traders carried less than 0.6 million long tons inthese nations’ trades. Thus, the threat of withhold-ing access to significant volumes of cargo in U.S.trades could provide leverage in negotiations overimpediments to cargo access by U. S .-flag carriersin foreign-to-foreign cross-trades. The Manalyticsstudy also noted that many of the countries whosecarriers are major cross-traders in the U.S. tradesgenerate relatively little trade of their own.

The study listed the following possible U.S.Government responses to artificial impedimentsraised to bar U.S.-flag carrier access to cross-trades:

● cancellation of cross-trade tariffs of foreigncarriers;

• discriminatory reservation of cargo againstforeign carriers;

. imposition of operating restrictions; and

. imposition of taxes or currency exchangecontrols.

Shipping Act of 1984

Section 13(b)(5) of the Shipping Act of 1984(Public Law 98-237) specifically permits Govern-ment actions in response to foreign actions thatare discriminatory to U.S.-flag carriers in foreign-to-foreign trades. OTA workshop participantsdiscussed the potential use of this provision in thefuture. Agency representatives believed that thethreat of sanctions, rather than actual imposition,would in most cases be sufficient to achieve U.S.objectives. No cases have yet been brought un-der section 13(b)(5).

Several workshop participants also stressed therole of the 1984 Shipping Act in enabling U.S. in-terests to gain market access in international linertrades. The Act allows conferences to establishintermodal rates, giving shippers the advantage

17A long ton equals 2,240 pounds.

‘8 Mana1ytics, Inc., U. S,-Flag Crosstrading, prepared for the Of-fice of Market Development, U.S. Maritime Administration, July1984 (contract No. DTMA91-83-C-30045).

50-390 0 - 85 - 4

18

of a through bill of lading. It also requires con-ferences to assure the right of independent actionfor any individual conference member, requiringa maximum of 10 days notice prior to such ac-tion. Shippers’ associations are authorized, al-though antitrust exemption does not extend tothem. The rate-approval process required by FMCis considerably accelerated and simplified.

The rights of all carriers in U.S. trades for pro-tection against discrimination is provided. TheAct retains section 19 of the Merchant Marine Actof 1920, under which the tariffs of any country’svessels may be suspended, effectively excludingthem from U.S. trades. Provisions of the Con-trolled Carrier Act of 1978 are also retained inthe new Act. Under this provision, action maybe taken against controlled carriers of any flagthat unfairly compete by offering less than com-pensatory rates. Finally, as noted above, section13(b)(5) of the new Act gives FMC power to sus-pend the tariff of any carrier in U.S. trade if thecountry whose flag it flies, or the commercialpractices of the carrier, unduly impairs the access

BILATERAL CARGO SHARING

Current Policy

The Administration’s policy toward bilateralagreements was summarized in 1984 by the Dep-uty Secretary of Transportation, speaking beforethe Maritime Law Association in New York.

Any bilateral arrangements we might ultimate-ly reach would be designed to place minimumconstraints on trade and preserve maximum mar-ketplace competition. They could also includeboth free access without Governmentally im-posed barriers for national-flag carriers and a sig-nificant role for cross-traders. Our objective isto limit the amount of trade that is arbitrarilyor Governmentally reserved to the flag carriers,while preserving equal access to reserved cargo,Naturally, our resistance to bilateral pressure willbe tempered by realism and the need to protectour carriers’ interests as well as our broader ship-ping and general trading interests. ”

19 Jame~ Burnley, U.S. Deputy Secretary of Transportation, ad-dress to the annual meeting of the Maritime Law Association, NewYork, May 4, 1984.

of U.S. carriers as cross-traders in foreign-to-foreign trade. Several participants stressed the im-portance of this latter provision, which theyviewed as vital in protecting U.S. carriers againstcertain cargo-sharing schemes in effect around theworld.

Future Strategy

The Administration’s strategy for future inter-national cargo policy negotiations is to continueresisting all forms of cargo-sharing agreements,but if resistance fails, to negotiate bilateral agree-ments with competitive elements, It may be use-ful for congressional deliberation if the Adminis-tration were to develop an explicit statement ofthese strategies, which would include: responsesto UNCTAD initiatives; positions relative to CSGdiscussions and agreements; and the intended useof U.S. provisions, such as those in the new Ship-ping Act, in response to cargo policies of othernations. Congress could call for such a strategypaper, possibly requesting that the InteragencyShipping Policy Group prepare it.

Thus it appears that, at present, the UnitedStates will only reluctantly accept cargo-sharingagreements with market-economy nations. Fewsuch agreements have been concluded over theyears, and only two are currently in effect .20 Dur-ing 1983 and 1984 one bilateral cargo-sharingagreement, involving the United States and Bra-zil, was renegotiated. Discussions of competitiveaccess have been held with three other countries,including the possibility of bilateral agreementswith more competitive provisions.

The negotiation of such “procompetitive” bi-lateral agreements that recognize the maritime-promotion objectives of U.S. trading partners isan option that the Administration may pursue,as a last resort, in cases where other nations in-sist on some form of cargo allocation as a condi-tion of trade, Such bilateral agreements may bethe only feasible compromise between free trade

20App. B contains descriptions of some specific bilateralagreements.

19

and protected trade objectives of various tradingpartners, especially for the present Administra-tion, which has objected so strenuously to multi-lateral regimes such as the UNCTAD Liner Code.

Given that bilateral cargo-sharing agreementsexist today with two U.S. trading partners, andmay be introduced with others from time to timein the future, it is important to address futurestrategies for these agreements. Strategies areneeded that will seek to satisfy the goals of effi-ciency and good service, as well as supportingeach country’s national interest. It may not bepossible to balance all conflicting interests.

Cargo Sharing and Competition

A major issue raised during the OTA workshopwas whether bilateral shipping agreements can bedevised that will preserve elements of price andservice competition. Historically, the UnitedStates has entered into such agreements only whenanother country has made it a condition for thecarriage of its cargo. The agreements with Argen-tina and Brazil are examples of the U.S. responseto those countries’ cargo-allocation policies (seeapp. B). The Federal Maritime Commission (FMC)has been investigating the competitive environ-ment in these trades since late 1984. The currentU.S.-Brazil agreement is due to expire at the endof 1985, and the Administration will soon begindiscussions with Brazilian authorities. Discussionswith Argentine officials are likely to follow.

Most workshop participants agreed that re-straint on competition is unhealthy. But they alsoagreed that restraints do exist in many countries,and that U.S. carriers and shippers must deal withthem. A possible role for the U.S. Government,therefore, is to protect shippers and operatorsfrom unfair competitive practices on the part offoreign governments and carriers, In the linertrades, for example, where price and service arefixed by conference system, competition is stillconsidered necessary. A conference must be suffi-ciently powerful to maintain stability, that is, butoutside competition should also be strong enoughto prevent the conference from earning monop-oly profits, Conferences in U.S. trades are opento any carrier desiring to join; trade is open tononconference carriers; and the right of independ-

ent action by conference members is fully pro-tected.

A radically different system was hypothesizedduring the OTA workshop panel on alternativeapproaches, in which competition would be as-sured within a bilateral agreement. Bilateral trea-ties would be negotiated without allocation offixed shares of cargo, but with third-flag carriersexcluded. Every carrier would be independent;rates would not be fixed; and carriers of eithertrading nation could compete for as much of thecargo as they could capture. Such an arrangementmight allow U, S, carriers to compete more effec-tively, or enhance overall efficiency for the traderoutes in question, z]

Government Participation

A major concern expressed by workshop par-ticipants was whether national governments wereinvolved in both regulating and operating theirinternational shipping industries. A number of in-dustry participants believed that bilateral agree-ments maintained by commercial conferenceswould neither impede trade nor work counter tothe interests of carriers and shippers. However,they raised several questions about governmentparticipation in the shipping industry, which iscommon in many other countries.

A recent analysis, prepared as part of FMC’sinvestigation of the U.S.-Brazil and U. S.-Argentina trades, identifies some of the problemsarising from bilateral agreements that involve sub-stantial government involvement.22 The staff pa-per concludes that these trades are protected bygovernment-supported cartels; that a few lineroperators carry nearly all of the cargo in thesetrades; and that these trades are marked by en-try restrictions and little or no service and pricecompetition. One of the key problems, accord-ing to the report, may be that the Brazilian andArgentine agreements themselves create an entrybarrier and that, “by mandating conference and

21 Leslie Kanuk( Baruch College, presentation to OTA WorkshopPanel on Alternative Approaches to Cargo Policy.

“Statement of Austin L. Schmitt, Chief Economist, Federal hlar-i time Commission, “Sect ion 19 Inquir}-U. S, Argentina andU.S. Brazil Trades, ” Docket P84-33, Washlngtonr D. C., Dec. 31,1984.

20—

pool memberships, set the stage for the lack ofservice and price competition.”23

The question that remains to be answered iswhat the United States can effectively do to openthese and other trades to greater competition. TheU.S. State Department has indicated that in fu-ture bilateral negotiations the United States willresist agreements that require cargo sharing.Whether this will be possible in the increasinglyprotectionist international environment remainsto be seen. Congress could also call for the de-velopment of an Administration policy strategypaper on bilateral, in a manner similar to request-ing a strategy paper on multilateral (see above).

Trade Barriers

Shipper representatives at the OTA workshopexpressed concern that all trade barriers—whethercargo preference, conference action, or bilateralor multilateral cargo reservation—are inefficientand uneconomic. They gave the example of a con-tainer shipped from the Midwest to Argentina orBrazil: via Europe, the cost is $3,400, while di-rect shipment costs $5,000. Shippers were optimis-tic that the Act addresses some of these problemsand that the new Shipping Act will result in a bet-ter balance between carriers and shippers than ex-isted under the 1916 Act. However, they remainconcerned that conferences can still set rates, poolrevenues, restrict sailings and volume capacity,and prevent competition.

“U.S. Marit ime Commission, Docket #84-33, Sect ion 19Inqui~—U. S, Argentina and U.S. /Brazil Trades, Memorandum ofLaw, p. 10.

Shippers feel that the success or failure of theAct will ultimately depend on how carriers re-spond to its independent action provision. Com-petitive opportunities are available to both ship-pers and vessel owners, including the ability toprovide intermodal services,24 independent ac-tion,25 and a prohibition against loyalty con-tracts, 26 except as allowed under antitrust law.Thus far, however, the impact of the Act has var-ied by trade area. In general, carriers in the OECDtrades have been more aggressive in seizing newopportunities than have those in LDC trades. In-dependent action has become common in the Pa-cific trades, while carriers on the North Atlanticappear afraid of starting a new rate war.

Individual shippers have taken advantage ofnew provisions, such as service contracts, to agreater or lesser degree. Shippers’ associations arenot yet common, and leaders in organizing themhave yet to come forward. Many shippers fearantitrust problems and therefore have adopted a“wait and see” posture. However, the recentlyformed Shippers for Competitive Ocean Trans-port (SCOT) has provided a means of bringingshippers’ interests into focus and representingthose interests in national and international ne-gotiations. SCOT supports a competitive regimethat will encourage good service, reasonable rates,and innovation.

Z4A contract for shipping se~ice5 covering severa] modes of trans-portation (truck, rail, ship, etc.).

“The right of a carrier in a conference to otfer independent serv-ice and rates.

2* Confidential loyalty agreements between shipper and carrier inexchange for favored rates,

DEFENSE NEEDS AND CARGO POLICY

A number of workshop participants expressed direct military support and continued support ofconcern about the ability of the U.S. merchant the civilian economy. DOD recently completedfleet to support wartime needs, today and in the a study to determine wartime logistics needs andfuture. The rationale for most forms of Federal adequacy of the merchant marine to fulfill them .27

subsidy to the maritime industry, including cargo“The stud; is classified, but Deborah Christie’s presentation to

preference, is national security. The U.S. mer- the OTA Workshop Panel on Current Policy Initiatives containedchant fleet would be tasked in wartime with both the unclassified highlights.

21

The findings were that sufficient container capac-ity exists for carriage of containerized military car-goes. However, there is a significant shortfall ofcapacity—breakbulk 28 and Ro/Ro29—to carrylarge units of equipment (such as tanks). DODhas launched two initiatives to ameliorate thisproblem: 1) purchasing older breakbulk andRo/Ro vessels on the open market and puttingthem in the National Defense Reserve Fleet(NDRF); and 2) purchasing the flat racks and seasheds needed for converting containerships, whichmake up most of the U.S.-flag liner fleet, to carrylarge equipment such as tanks.

When the liner cargo panel was told that DODis considering acquiring its own in-house fleet toprovide sealift capability, participants questionedwhether this would be cost effective compared to

zgshlp~ ~’~arry genera] cargo in a large variety of ~izes

‘9 Ships that carry vehicles or trailers that are loaded and dischargedby “rolling on and rolling of f.”

promoting the development of needed capacityin the private sector. A clear policy decision needsto be made as to whether it is desirable to havea largely nationalized fleet maintained at Govern-ment expense, or whether it would be more effi-cient to build and operate a commercial fleet withsome Government support. DOD contends, how-ever, that there are few ideas for stimulating pri-vate sector growth, and that DOD consideredthose that were around when launching itsprogram:

In fact, our program is cheaper than past pol-icies (ODS, CDS, and cargo preference), whichwere not providing the needed capability, andwe have yet to hear any suggestion that showspromise of stimulating significant growth in theflag fleet for equal cost.’”

‘“Letter from Deborah P. Christie, Division Director for Projec-tion Forces and Analytical Support, Office of the Secretary, Apr.30, 1985.

“% . “ ““%.%

*“” .3

a- -“

●

✎ ✎ ✍

Photo credit U S Manffrne Admfnfs(rat/o~

National Defense Reserve Fleet at anchor.

2 2

National defense requirements were discussedin some detail during the bulk cargo panel, sinceproduct tankers31 are valuable defense assets, TheUSEC fleet of U.S.-owned, foreign-flag ships con-tains sufficient large crude oil carriers to serve de-fense needs, in the panel’s opinion. But some par-ticipants expressed concern about the number ofusable tankers: most of the USEC tanker fleet ismade up of large crude oil carriers, which maynot be as useful militarily as smaller oil-producttankers, Because of consolidation in the world pe-troleum industry, furthermore, the tanker fleetsof U.S. oil companies and of our NATO allies aredeclining in size and significance. A separate pointraised by shipping interests was the cost ofdefense-related features of their fleet and whetherthese costs should be borne by U.S. taxpayers,rather than by a small number of shippers.

Another issue raised by workshop participantsis the adequacy of the pool of merchant seamento crew reserve fleet ships, should they be re-quired. The recent decline in number of U.S. mer-chant seamen is expected to continue due to retire-ments and the declining crew requirements ofmodern vessels (see fig. 5). As a result, severalparticipants questioned whether an adequatenumber of crew members could be found for mil-itary support operations in wartime.

I] Tankers that carw refined petroleum products, such as gaso-line, diesel, fuel oil, etc.

Workshop participants agreed that these andother defense issues merit further study. Amongthe topics mentioned were a cost-benefit analy-sis of the merchant fleet as a defense support base,the cost of defense requirements to the merchantfleet, and the crewing issue. Congress may wishto call for more specific, in-depth analyses of theseissues, possibly as part of the charter of the newlyestablished Commission on Merchant Marine andDefense. Workshop participants suggested threespecific areas in which additional analysis couldimprove future policies:

1.

2.

3.

A cost comparison of alternative approachesto providing needed military sealift capabil-ity (for example, comparing the cost of hav-ing DOD buy or build the ships they needvs. the cost of encouraging the commercialoperation of those ships through subsidyprograms, including hidden costs, multipliereffects, etc. ).An analysis of actual costs of providing de-fense features in shipbuilding, and who ulti-mately pays for them. At present the com-mercial industry is thought to be fundingcertain features and practices that supportnational defense goals, but without directDOD support.An analysis of the relative military useful-ness of the existing commercial fleet. DODclaims that it does not currently have accessto the types of vessels needed for mobiliza-tion; others claim they do.

23

Figure 5.—Seafaring Employment— U.S.-Flag Oceangoing Commercial Ships

60,000

1960 962 1964

These data are for oceangoing commercial ships

The data show a steady decline since 1968 which

966 1968 1970 1972 1974 1976 1978 1980 1982 1984

Year

onIy which Include the coastal (Jones Act) t rade but not the Inland waterways stems from a number of factors includinq a decline in the active fleet a switch to Iarger ships, a reduction in crew

sizes and the general SI urn p I n world f rade I n add It Ion these f Ig u res are for the privately o-wn ed fleet on I y and do not Inclu de the 3,000 to 4,000 jobs current Iy n the

government operated f leet (prlnclpallj MSC)

SOURCE MarAd da ta 1985

Section 3

Summary

Section 3

Summary

The current trend worldwide is toward moreand more government involvement in trade andcargo policies. These policies have taken variousforms, including unilateral declarations as well asboth bilateral and multilateral agreements or trea-ties. The United States is unusual among majormaritime and trading nations in its advocacy ofa completely free trading environment and itsreluctance to accept any form of bilateral or multi-lateral cargo-allocation regime. Many other na-tions have much more direct government involve-ment in their trading and shipping industries.

OTA’s Assessment of Maritime Trade andTechnology, published in 1983, stated that therewas at that time no generally accepted U.S. cargopolicy, and that the lack of such a policy has beendetrimental to U.S. trading and shipping interests.

U.S. CARGO PREFERENCE

The debate about cargo preference for agricul-tural commodities is especially intense as thisBackground Paper is being published. Many cur-rent legislative proposals seek to eliminate cargo-preference requirements for certain export pro-grams. In addition, maritime interests have calledfor better enforcement of existing cargo-preferencelaws. OTA’s investigation has identified three pos-sible initiatives for consideration:

c A directive requiring more specific evalua-tion of cargo-preference costs (by program

MULTILATERAL CARGO SHARING

This 1985 review of cargo policies has found lit-tle changed from 1983 except for a decided in-crease in the intensity of the debate, especially asit concerns U.S. cargo preference.

The OTA cargo policy workshop, togetherwith an analysis of the key questions raised bythe workshop and other sources, has identifiedfour issue areas that appear to be important notonly to the health and vitality of the U.S. ship-ping industry, but also to other vital national in-terests involving U.S. participation in world trade:

● U.S. cargo preference;• multilateral cargo sharing;• bilateral cargo sharing; and. national defense needs that affect cargo

policy.

and agency), as well as a clear allocation ofthose costs (e. g., for defense-related re-quirements).

• Development of comprehensive interagencyguidelines for cargo-preference complianceand reporting.

Ž A requirement to evaluate all Governmentsubsidies offered each firm, both direct andindirect, in order to gain more equity andbalance among promotional programs.

The most significant international (multilat- fused to accept this treaty, although many of oureral) agreement on cargo sharing, the United Na- trading partners have either signed it or an-tions Conference on Trade and Development nounced their intention of signing. It is too early(UNCTAD) Code of Conduct for Liner Confer- to measure any major impacts of the Liner Codeences (or UNCTAD Liner Code), has been in ef- on the shipping industry. However, UNCTAD isfeet since October 1983. The United States has re- new pursuing other initiatives such as a code for

27

2 8

bulk cargo and an effort to phase out open regis-tries (flags of convenience).

While the U.S. Government has consistentlyresisted attempts to institute cargo-sharing agree-ments, strategies to achieve such a goal have notbeen clearly defined or widely debated in the

BILATERAL CARGO SHARING

Some observers have advocated a strategy ofselective bilateral agreements on cargo policy, inlieu of a more general (or multilateral) approachinvolving many trading nations. The rationale is,first, that the United States would have a strongernegotiating position and, second, that a minimumnumber of nations would have to be accom-modated.

The United States now operates under bilateralcargo-sharing agreements with Brazil and Argen-tina, and has had such agreements with the So-viet Union and China in the past. While thepresent Administration has resisted further at-

United States. OTA investigations suggests thatthe Interagency Shipping Policy Group, or someother appropriate organization, could be directedto develop a strategy paper to guide future inter-national discussions on cargo policies.

tempts at bilateral cargo sharing, it is likely thatother nations will continue to seek forms of cargoallocation for the benefit of their own shippingindustry. OTA has identified two possible ap-proaches for consideration:

●

●

Develop a bilateral strategy for future guidancein responding to other nations’ cargo-sharinginitiatives, to be prepared by an interagencygroup.Develop a legislative framework for cargo shar-ing, including strategies for future bilateralagreements.

NATIONAL DEFENSE AND CARGO POLICY

National defense is the overriding justification ●

used for most forms of Federal support of the U.S.merchant marine, including those of funding cargo- ●

preference costs or taking actions in the interna-tional arena that would serve to strengthen theU.S. shipping industry. There is little debate aboutthe need for some defense mobilization base, butthere is considerable debate about specific defi- ●

nition of shipping needs, the cost of providingthem, and the various approaches toward Gov-ernment support of the industry. OTA’s investi-gation revealed three initiatives for consideration:

Analyze the desirability of allocating the directcosts of cargo preference to the defense budget.Evaluate the long-term desirability and costs ofdirect support for a national fleet to meet de-fense needs vs. indirect support for a commer-cial fleet, including the question of an adequatepool of merchant seamen for the future.Evaluate the long-term viability of the merchantfleets of our allies as they contend with diffi-cult competition from the Soviets and othercontrolled carriers.

Appendixes

Appendix A

Summary of PanelPresentations and Discussion

OTA Cargo Policy Workshop, Dec. 3 and 4, 1984

PANEL ON CURRENT POLICY INITIATIVES

Panelists

Charles AngevineDepartment of State

Deborah ChristieDepartment of Defense

Robert EllsworthFederal Maritime Commission

William JohnsonDepartment of Commerce

Topics for Discussion

1.

2.

3.

Trends in maritime trade, trading patterns,and shipping services; current policy initia-tives involving the interaction of trade andshipping.Present cargo preference regulations andtheir effects, including trends in U.S. policiesto promote U.S. exports.Current initiatives and responses to interna-tional cargo policies, such- as the UNCTAD

Phu/o credl~ H G M///er

OTA Workshop on Cargo Policy, meeting in the hearingroom of the House Committee on Merchant Marine and

Fisheries, Dec. 3 and 4, 1984

Arnold LevineDepartment of Transportation

Kay McLennanDepartment of Agriculture

Lewis PaineDepartment of Transportation

4.

5.

Liner Code and bilateral agreements withmajor trading partners.Current trends in the use of new ShippingAct authority to gain cargo access and theeffect of regulatory policy on U.S. cargoshares.Impacts of military readiness requirementson-cargo policies or U, S. position in tradeand shipping.

Summary of Discussion

At the first workshop panel, participants fromFederal agencies discussed current initiatives incargo policy. The agencies represented includedthe Departments of State, Agriculture, Transpor-tation, Commerce, and Defense, and the FederalMaritime Commission. The panelists presented anoptimistic outlook for both U.S. shippers and themaritime industry. They stressed that their pro-grams were directed toward goals of maximumflexibilit y for shippers along with access to cargofor U.S. carriers. A common theme expressed was“open market competition. ” On the internationallevel, the panelists believed it important to pro-tect U.S. vessels from unfair practices in order tomeet the goals of access and competition.

31

32

Shipping Act of 1984

Several participants stressed the role of the 1984Shipping Act in enabling U.S. interests to over-come barriers to market access in internationalliner trade. The Act allows conferences to estab-lish intermodal rates, giving shippers the advan-tage of a through bill of lading. It also requiresthe right of independent action for any individ-ual conference member, requiring a maximum of10 days notice prior to such action. Shippers’ asso-ciations are authorized, although antitrust exemp-tion does not extend to them. The rate-approvalprocess required by FMC is considerably acceler-ated and simplified.

The rights of all carriers in U.S. trades for pro-tection against discrimination is provided. TheAct retains section 19 of the Merchant Marine Actof 1920, under which the tariffs of any country’svessels may be suspended, effectively excludingthem from U.S. trades. Provisions of the Con-trolled Carrier Act of 1978 are also retained inthe new Act. Under this provision, action maybe taken against controlled carriers of any flagwhich unfairly compete by offering less than com-pensatory rates. Finally, section 13(b)(5) of thenew Act gives FMC power to suspend the tariffof any carrier in U.S. trade if the country whoseflag it flies, or the commercial practices of the car-rier, unduly impair the access of U.S. carriers ascross-traders in foreign-to-foreign trade. Severalparticipants stressed the importance of this latterprovision, which they viewed as vital in protect-ing U.S. carriers against certain cargo-sharingschemes in effect around the world.

Cargo Preference

There was considerable discussion of U.S. cargo-preference laws and policies. The stated Admin-istration position is that current laws should beenforced, but that no expansion of preferenceshould occur. Cargo-preference requirements onagricultural products received significant atten-tion from the group. Under the Cargo PreferenceAct of 1954 (Public Law 83-664), U.S. food assis-tance to less developed countries (LDCs) is sub-ject to a 50-percent U.S. carrier reservation.USDA, which manages the preference require-ments for these Public Law 83-480 Title I (con-

cessionary sales) shipments, cited a transporta-tion differential cost of $120 million paid forU.S.-flag carriage of food assistance cargoes in1982. The cost differential was $65 million in 1983and $76 million in 1984. Comparable detailed sta-tistics are not available for the Title II (gifts offood) shipments, whose preference requirementsare monitored by AID.

The panelists pointed out that while one-third(by tonnage) of all U.S.-flag waterborne ship-ments are preferential, only 4 to 8 percent of to-tal liner shipments are preference cargoes. In theliner sector, there is generally no differentialwithin conferences, where set rates apply to allcarriers, notwithstanding flag. Of course, this istempered by the situation in U.S. trades whereindependent action is encouraged and a numberof nonconference carriers operate. It should benoted, however, that in some instances an agri-cultural commodity rate may be “opened” by theconference, which means that a conference-widerate does not apply.

It is in the bulk area, where U.S. operating costsaverage two to three times those of certain for-eign competitors, that the cost differentials are sig-nificant. However, U.S. bulk carriers are utterlydependent on preference shipments for their sur-vival. On the other hand, panelists also pointedout that the U.S. bulk fleet is modernizing signif-icantly. A MarAd study of the large Egyptian pro-gram showed that in 1981, 61 percent of PublicLaw 83-480 shipments were on bulk carriers over22 years old, while in 1984, 63 percent of shipmentswere carried on vessels 5 years old or under. Thisdoes not imply that the U.S.-flag bulk fleet is near-ing profitability. A severe depression exists world-wide in bulk shipping, and even the lowest costcompetitors are failing to cover their costs.

Cargo Reservation

The issue of cargo reservation, whether unilat-eral, bilateral, or multilateral, was raised by sev-eral panel members. Flexibility of approach is per-ceived by several panel members as essential inassuring U.S. interests. FMC has recently insti-tuted or completed investigations into the Vene-zuelan, Brazilian, Philippine, and Argentine tradesbased on allegations of discrimination against U.S.

33

or third-flag carriers and shippers, Panelists statedthat the real threat to U.S. interests is foreign gov-ernment intervention, rather than commercial ef-forts at cargo sharing.

Most panelists also felt that the UNCTAD LinerCode has not been as detrimental thus far as waswidely feared. Some indicated that the potentialfor real harm from UNCTAD Liner Code provi-sions exists only where U.S. carriers are cross-traders in a foreign-to-foreign trade. Should thatoccur, section 13(b)(5) of the Shipping Act of 1984allows the FMC to intervene in U.S. trades to pre-vent such discrimination in foreign-to-foreigntrades. The overall opinion of the panel was thatthe UNCTAD Liner Code does not pose much di-rect threat to U.S. carriers. Were a bulk code tobe implemented, the effect on world trade wouldbe much greater, but this is not regarded as animminent possibility.