3

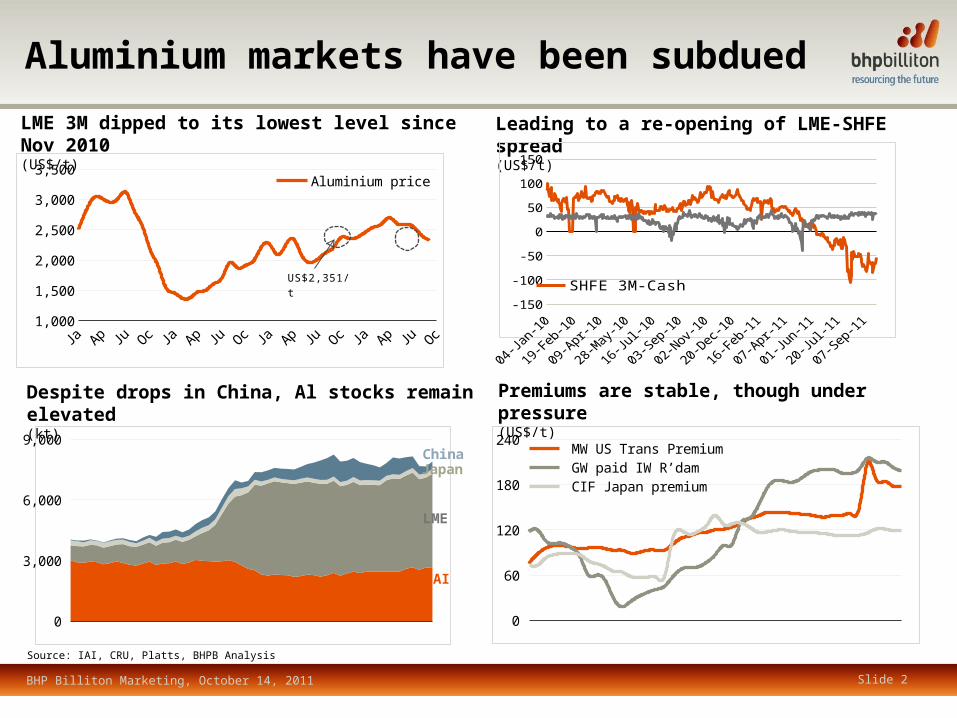

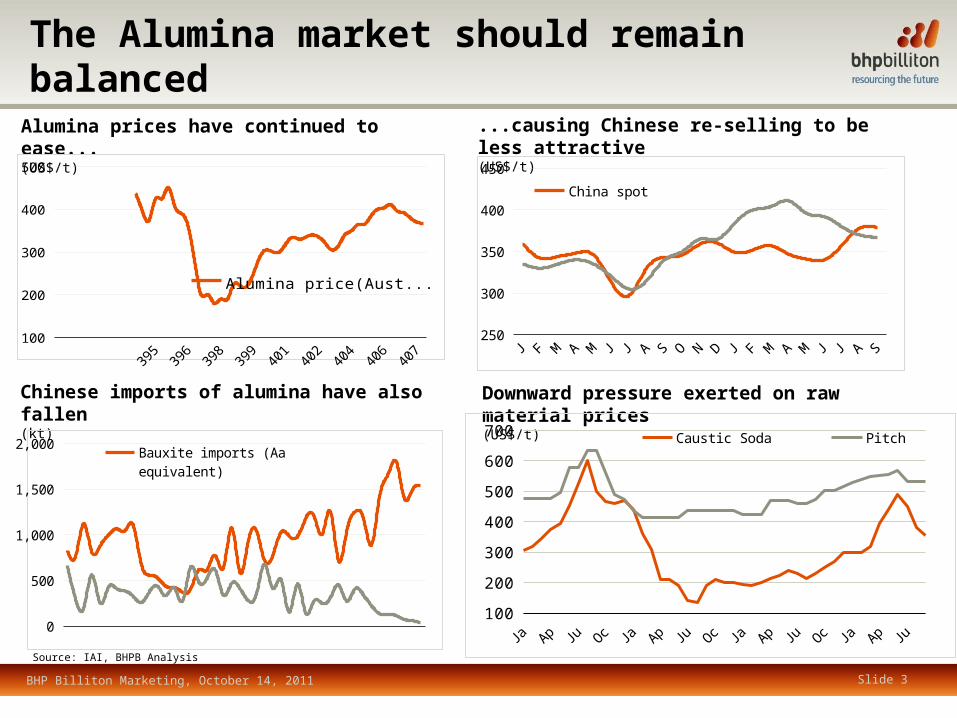

Slide 1 Aluminium / Alumina Market Outlook What’s new? Market sentiment has weighed on the LME aluminium price. In September, the LME 3M price dropped to US$2,240/t, its lowest level since November 2010. Meanwhile the Chinese SHFE aluminium price continues to be supported by power shortages and this has led to a widening of the LME-SHFE spread. Consumers are running lean inventories to avoid the risk of locking in orders if market sentiment remains subdued or demand deteriorates. Domestic Chinese inventories hit their lowest level in the past three years. While stable, LME stocks remain elevated as global production holds steady. Aluminium market premiums globally remain under pressure, with MJP and US premiums settling lower in 3Q2011. The alumina price eased from US$380/t at the end of 2Q2011, to a range of US$355/t- US$365/t towards the end of 3Q2011. Buyers have delayed September re-stocking in anticipation of lower prices. In China, supply has remained stable as increased alumina production has countered reduced imports. Near term drivers The transport sector remains strong in the US and Germany, hot weather helped underpin beverage cans demand in Asia. On the downside, housing and manufacturing sectors have struggled to grow worldwide. Power shortages in China caused smelters to cut back production, and a new mining code in Guinea has caused a minor commotion in the markets. Japanese shipments of aluminium was hit by slowing SE Asia demand and slower-than- expected domestic demand. Prices of raw materials have lowered with some prices, e.g. caustic soda, coal tar pitch and cathode down compared to 2Q2011, on the back of decreasing Chinese demand and lower oil prices. Price outlook BHP Billiton Marketing, October 14, 2011