European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0360A(COD) 5.2.2018 AMENDMENTS 686 - 935 Draft report Peter Simon (PE613.409v03-00) on the proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) No 575/2013 as regards the leverage ratio, the net stable funding ratio, requirements for own funds and eligible liabilities, counterparty credit risk, market risk, exposures to central counterparties, exposures to collective investment undertakings, large exposures, reporting and disclosure requirements and amending Regulation (EU) No 648/2012 Proposal for a regulation (COM(2016)0850 – C8-0480/2016 – 2016/0360A(COD)) AM\1144448EN.docx PE616.835v01-00 EN United in diversity EN

on the proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) No 575/2013 as regards the leverage ratio, the net stable funding ratio, requirements for own funds and eligible liabilities, counterparty credit risk, market risk, exposures to central counterparties, exposures to collective investment undertakings, large exposures, reporting and disclosure requirements and amending Regulation (EU) No 648/2012

Proposal for a regulation(COM(2016)0850 – C8-0480/2016 – 2016/0360A(COD))

AM\1144448EN.docx PE616.835v01-00

EN United in diversity EN

AM_Com_LegReport

PE616.835v01-00 2/150 AM\1144448EN.docx

EN

Amendment 686Marco Zanni, Bernard Monot, Gerolf AnnemansProposal for a regulationArticle 1 – paragraph 1 – point 88Regulation (EU) No 575/2013Chapter 5

Text proposed by the Commission Amendment

(88) In Title IV of Part Three, the Title of Chapter 5 is replaced by the following:

(88) In Title IV of Part Three, Chapter 5 is deleted.

Or. en

Justification

Chapter 5 aims to regulate the simplified IRB approach, so it must be deleted due to the position taken on IRB models.

Amendment 687Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 91Regulation (EU) No 575/2013Article 390 – paragraph 4 – subparagraph 1

Text proposed by the Commission Amendment

Institutions shall calculate exposures arising from contracts referred to in Annex II and credit derivatives directly entered into with a client in accordance with one of the methods set out in Part Three, Title II, Chapter 6, Section 3 to Section 5, as applicable.

Institutions shall calculate exposures arising from contracts referred to in Annex II and credit derivatives directly entered into with a client in accordance with one of the methods set out in Part Three, Title II, Chapter 6, Section 3 to Section 6, as applicable. Institutions with a permission to use the Internal Model Method in accordance with Article 283 may use the Internal Model Method for calculating the exposure value for all transactions for which they have received permission under Article 283.

Or. en

AM\1144448EN.docx 3/150 PE616.835v01-00

EN

Justification

The Internal model Method is still permitted to be used by banks for some products in the revised CRR. Therefore, in calculating exposure under the Large exposure regime, the IMM should be allowed.

Amendment 688Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 91Regulation (EU) No 575/2013Article 390 – paragraph 4 – subparagraph 2

Text proposed by the Commission Amendment

Exposures arising from these contracts allocated to the trading book shall also fulfil the requirements set out in Article 299.

When calculating the exposure value for the contracts referred to in the first subparagraph which are allocated to the trading book, institutions shall also comply with the principles set out in Article 299. By derogation from the first subparagraph of this paragraph, institutions with a permission to use the Internal Model Method in accordance with Article 283 may use the method referred to in Part Three, Title II, Chapter 6, Section 6 for calculating the exposure value for securities financing transactions.

Or. en

Justification

This amendment shall clarify, in line with the Basel standard for measuring LE (para 34), a derogation from the requirements for calculating exposure value of securities financing transactions for the purpose of LE. Institutions that have a permission to use the IMM under CRR Article 283 may continue using this method.

Amendment 689Costas MavridesProposal for a regulationArticle 1 – paragraph 1 – point 93Regulation (EU) No 575/2013Article 392 – paragraph 1

PE616.835v01-00 4/150 AM\1144448EN.docx

EN

Text proposed by the Commission Amendment

An institution's exposure to a client or a group of connected clients shall be considered a large exposure where its value is equal to or exceeds 10 % of its Tier 1 capital..

An institution's exposure to a client or a group of connected clients shall be considered a large exposure where its value is equal to or exceeds 10 % of its eligible capital.

Or. en

Justification

Whilst, until the CRR entered into force, a bank’s entire own funds could be taken as the basis for calculating the large exposure limit, the inclusion of Tier 2 capital was, in particular, gradually restricted to a significant extent by the CRR. In its work, the Basel Committee focuses on international banks that are active in the capital markets. This has to be borne in mind when translating Basel proposals into European law. On no account should – as proposed by the Basel Committee – the basis for calculating the large exposure limit be reduced any further. Banks without corresponding access to the capital markets can only create Tier 1 capital to a limited extent to flexibly cushion against capital squeezes. Taking solely Tier 1capital as the basis for calculating the large exposure limit is not appropriate either, as in the event of default by a borrower Tier 2 capital can also be used to cover losses where an annual loss is involved.

Amendment 690Markus FerberProposal for a regulationArticle 1 – paragraph 1 – point 94Regulation (EU) No 575/2013Article 394 – paragraph 4 – subparagraph 3

Text proposed by the Commission Amendment

Power is conferred on the Commission to adopt the implementing technical standards referred to in the first Paragraph in accordance with Article 15 of Regulation (EU) No 1093/2010.

Power is conferred on the Commission to adopt the implementing technical standards referred to in the first Paragraph in accordance with Article 15 of Regulation (EU) No 1093/2010. The implementing technical standards shall enter into force one year after their adoption by the Commission.

Or. de

AM\1144448EN.docx 5/150 PE616.835v01-00

EN

Justification

The institutions concerned should be given sufficient time to transpose the implementing technical standards on reporting obligations.

Amendment 691Markus FerberProposal for a regulationArticle 1 – paragraph 1 – point 94Regulation (EU) No 575/2013Article 394 – paragraph 5

Text proposed by the Commission Amendment

5. EBA shall develop draft regulatory technical standards to specify the criteria for the identification of shadow banking entities referred to in paragraph 2.

deleted

In developing those draft regulatory technical standards, EBA shall take into account international developments and internationally agreed standards on shadow banking and shall consider whether:

(a) the relation with an individual or a group of entities may carry risks to the institution's solvency or liquidity position;

(b) entities that are subject to solvency or liquidity requirements similar to those imposed by this Directive and Regulation (EU) No 1093/2010 shall be entirely or partially excluded from the reporting obligations referred to in paragraph 2 on shadow banking entities.

EBA shall submit those draft regulatory technical standards to the Commission by [one year after entry into force of the Amending Regulation].

Power is delegated to the Commission to adopt the regulatory technical standards referred to in the first subparagraph in accordance with Articles 10 to 14 of Regulation (EU) No 1093/2010.

Or. de

PE616.835v01-00 6/150 AM\1144448EN.docx

EN

Justification

The EBA guidelines on limits for exposures to shadow banking enterprises which carry out banking activities outside a regulatory framework (EBA/GL/2015/20) already include a definition of shadow banking entities.

Amendment 692Sven Giegold, Ernest Urtasun, Philippe LambertsProposal for a regulationArticle 1 – paragraph 1 – point 95 – point aRegulation (EU) No 575/2013Article 395 – paragraph 1 – subparagraph 4

Text proposed by the Commission Amendment

By way of derogation from the first subparagraph, an institution identified as G-SII in accordance with Article 131 of Directive 2013/36/EU shall not incur an exposure to another institution identified as G-SII the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 15 % of its Tier 1 capital. An institution shall comply with such limit no later than within 12 months after it is identified as G-SII..

By way of derogation from the first subparagraph

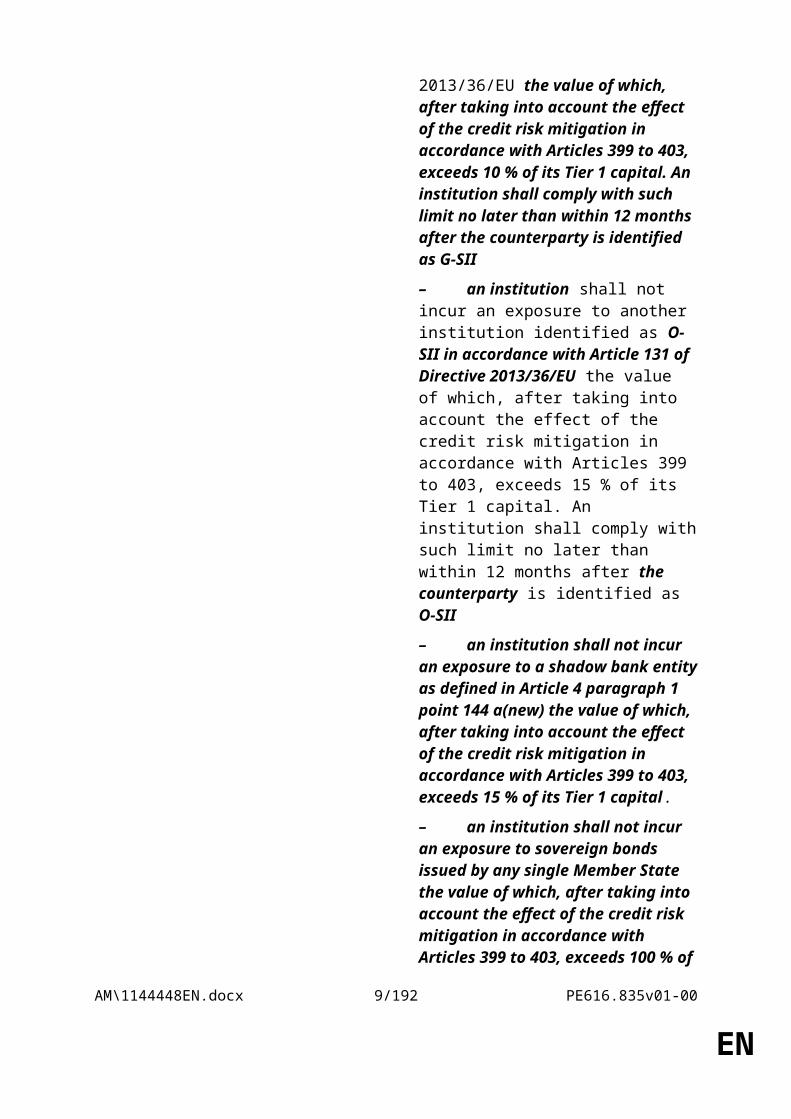

– an institution shall not incur an exposure to another institution identified as G-SII in accordance with Article 131 of Directive 2013/36/EU the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 10 % of its Tier 1 capital. An institution shall comply with such limit no later than within 12 months after the counterparty is identified as G-SII

– an institution shall not incur an exposure to another institution identified as O-SII in accordance with Article 131 of Directive 2013/36/EU the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 15 % of its Tier 1 capital. An institution shall comply with such limit no later than within 12

AM\1144448EN.docx 7/150 PE616.835v01-00

EN

months after the counterparty is identified as O-SII

– an institution shall not incur an exposure to a shadow bank entity as defined in Article 4 paragraph 1 point 144 a(new) the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 15 % of its Tier 1 capital.

– an institution shall not incur an exposure to sovereign bonds issued by any single Member State the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 100 % of its Tier 1 capital.

By way of derogation from the last indent of the preceding paragraph the exposure limit referred to shall be 200% until one year after the date of application of this Regulation and shall decrease by 20% each subsequent year until the end of the fifth year after the date of application of this Regulation.

Or. en

Amendment 693Ashley Foxon behalf of the ECR GroupBernd Lucke, Ramon Tremosa i BalcellsProposal for a regulationArticle 1 – paragraph 1 – point 95 – point aRegulation (EU) No 575/2013Article 395 – paragraph 1 – subparagraph 4 a (new)

Text proposed by the Commission Amendment

By way of derogation from the first subparagraph, an institution shall not incur aggregate exposure to non-investment grade sovereign bonds issued by any single Member State the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds [50 %] of its Tier 1 capital, unless the institution

PE616.835v01-00 8/150 AM\1144448EN.docx

EN

applies a marginal risk weight add-on of [1%] to the excess exposure.

Or. en

Amendment 694Burkhard BalzProposal for a regulationArticle 1 – paragraph 1 – point 95 – point aRegulation (EU) No 575/2013Article 395 – paragraph 1 – subparagraph 4 a (new)

Text proposed by the Commission Amendment

By way of derogation from the first subparagraph, an institution shall not incur aggregate exposure to sovereign bonds issued by any single Member State the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds [X]%1a of its Tier 1 capital, reaching the amount of [X]% after a period of [X]1b years.

__________________1a X is to be a percentage that is to be deemed appropriate after consultation of both ESRB and SSM.1b X is to be a number of years that is to be deemed appropriate after consultation of both ESRB and SSM.

Or. en

Amendment 695Sven Giegold, Ernest Urtasun, Philippe LambertsProposal for a regulationArticle 1 – paragraph 1 – point 95 a (new)Regulation (EU) No 575/2013Article 395 a (new)

Text proposed by the Commission Amendment

(95a) The following Article 395a is inserted:

AM\1144448EN.docx 9/150 PE616.835v01-00

EN

"Article 395a

Aggregate limit on exposures to shadow banking entities

An institution shall not incur a total exposure to shadow banking entities the value of which, after taking into account the effect of the credit risk mitigation in accordance with Articles 399 to 403, exceeds 25% of its Tier 1 capital. Competent authorities may set a lower limit than 25% of Tier 1 capital and shall inform EBA and the Commission thereof."

Or. en

Amendment 696Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 98 – point aRegulation (EU) No 575/2013Article 399 – paragraph 1 – subparagraph 1

Text proposed by the Commission Amendment

An institution shall use a credit risk mitigation technique in the calculation of an exposure where it has used this technique to calculate capital requirements for credit risk in accordance with Part Three, Title II and provided it meets the conditions set out in this Article.

An institution may use a credit risk mitigation technique in the calculation of an exposure where it has used this technique to calculate capital requirements for credit risk in accordance with Part Three, Title II and provided it meets the conditions set out in this Article.

Or. en

Justification

This amendment aims at removing the obligation introduced by the Commission to use the substitution approach in the large exposure regime. It can have detrimental effects on real estate market in some countries due to national specificities.

Amendment 697Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 98 – point a a (new)

PE616.835v01-00 10/150 AM\1144448EN.docx

EN

Regulation (EU) No 575/2013Article 399 – paragraph 1 a (new)

Text proposed by the Commission Amendment

(aa) The following paragraph 1a is inserted:

"1a. By way of derogation from paragraph 1, institutions that used a credit risk mitigation technique to calculate capital requirements for credit risk in accordance with Part Three, Title II may not use this technique for the purpose of article 395(1) to exposures in the form of a collateral or a guarantee provided by an official export credit agency or by an eligible protection provider referred to in Article 201 qualifying for the credit quality step 2 or above, for officially supported export credits and residential loans."

Or. en

Justification

In specific markets, such as the residential or export credit loans, the market structure is characterised by a very limited number of protection credit providers. In these specific cases, if the large exposure limits is applied, combined with a mandatory substitution approach, as set out in article 403, this might very easily lead to a breach of large exposure limits. A specific exemption for officially supported export credits and residential loans would allow banks to use CRM for fully guaranteed loans and the guaranteed portion of export credit exposures for the purpose of credit risk but would grant them a discretion for not using CRM for the purpose of large exposures. As a consequence, if banks apply this discretion, substitution would no longer be required under art. 401(4). This approach seems more prudentially sound as banks would not benefit from the CRM for the computation of their large exposure limits.

Amendment 698Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 99 – point a – point ii a (new)Regulation (EU) No 575/2013Article 400 – paragraph 1 – point k a (new)

AM\1144448EN.docx 11/150 PE616.835v01-00

EN

Text proposed by the Commission Amendment

(ka) exposures, including participations or other kinds of holdings, incurred by an institution to its parent undertaking, to other subsidiaries of that parent undertaking or to its own subsidiaries, in so far as those undertakings are covered by the supervision on a consolidated basis to which the institution itself is subject, in accordance with this Regulation, Directive 2002/87/EC or with equivalent standards in force in a third country; exposures that do not meet these criteria, whether or not exempted from Article 395(1), shall be treated as exposures to a third party.

Or. en

Justification

Change required to remove the conflicting powers afforded to Member States and Competent Authorities, as well as to enhance the ability of the SSM to exercise its powers as the common supervisory authority of the Banking Union.

Amendment 699Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 99 – point a – point ii a (new)Regulation (EU) No 575/2013Article 400 – paragraph 1 – point l a (new)

Text proposed by the Commission Amendment

(la) exposures, including participations or other kinds of holdings, incurred by an institution to its parent undertaking, to other subsidiaries of that parent undertaking or to its own subsidiaries, in so far as those undertakings are covered by the supervision on a consolidated basis to which the institution itself is subject, in accordance with this Regulation, Directive 2002/87/EC or with equivalent standards in force in a third country;

PE616.835v01-00 12/150 AM\1144448EN.docx

EN

exposures that do not meet these criteria, whether or not exempted from Article 395(1), shall be treated as exposures to a third party.

Or. en

Justification

This amendment aims at making clear that intragroup exposure are excluded. To recall, the Basel framework doesn't specifically consider the treatment of intragroup exposures.

Amendment 700Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 100Regulation (EU) No 575/2013Article 401 – paragraph 2

Text proposed by the Commission Amendment

2. For the purposes of the first paragraph, institutions shall use the Financial Collateral Comprehensive Method, regardless of the method used for calculating own funds requirements of credit risk.

deleted

Or. en

Justification

Institutions should be allowed to use own estimates of the effects of financial collateral in relation to Securities Financing Transactions, to stay consistent with the treatment allowed in credit risk.

Amendment 701Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 100Regulation (EU) No 575/2013Article 401 – paragraph 2

Text proposed by the Commission Amendment

2. For the purposes of the first 2. With the exception of institutions

AM\1144448EN.docx 13/150 PE616.835v01-00

EN

paragraph, institutions shall use the Financial Collateral Comprehensive Method, regardless of the method used for calculating own funds requirements of credit risk.

using the Financial Collateral Simple Method, for the purposes of the first paragraph, institutions shall use the Financial Collateral Comprehensive Method, regardless of the method used for calculating own funds requirements of credit risk.

By derogation from paragraph 1 and the first subparagraph of this paragraph, institutions with a permission to use the method referred to in Part Three, Title II, Chapter 6, Section 6, may continue to use this method for calculating the exposure value of securities financing transactions.

Or. en

Justification

This amendment shall clarify, in line with the Basel standard for measuring LE (para 34), a derogation from the requirements to use the FCCM for calculating exposure value of securities financing transactions for the purpose of LE. Institutions that have a permission to use the IMM under CRR Article 283 may continue using this method.

Amendment 702Thomas MannProposal for a regulationArticle 1 – paragraph 1 – point 100Regulation (EU) No 575/2013Article 401 – paragraph 4

Text proposed by the Commission Amendment

4. Where an institution reduces an exposure to a client due to an eligible credit risk mitigation technique in accordance with Article 399(1), it shall treat the part of the exposure by which the exposure to the client has been reduced as having been incurred to the protection provider rather than to the client.

deleted

Or. de

Amendment 703Markus Ferber

PE616.835v01-00 14/150 AM\1144448EN.docx

EN

Proposal for a regulationArticle 1 – paragraph 1 – point 100Regulation (EU) No 575/2013Article 401 – paragraph 4

Text proposed by the Commission Amendment

4. Where an institution reduces an exposure to a client due to an eligible credit risk mitigation technique in accordance with Article 399(1), it shall treat the part of the exposure by which the exposure to the client has been reduced as having been incurred to the protection provider rather than to the client.

deleted

Or. de

Justification

An obligatory substitution would make it difficult to monitor large-scale lending limits.

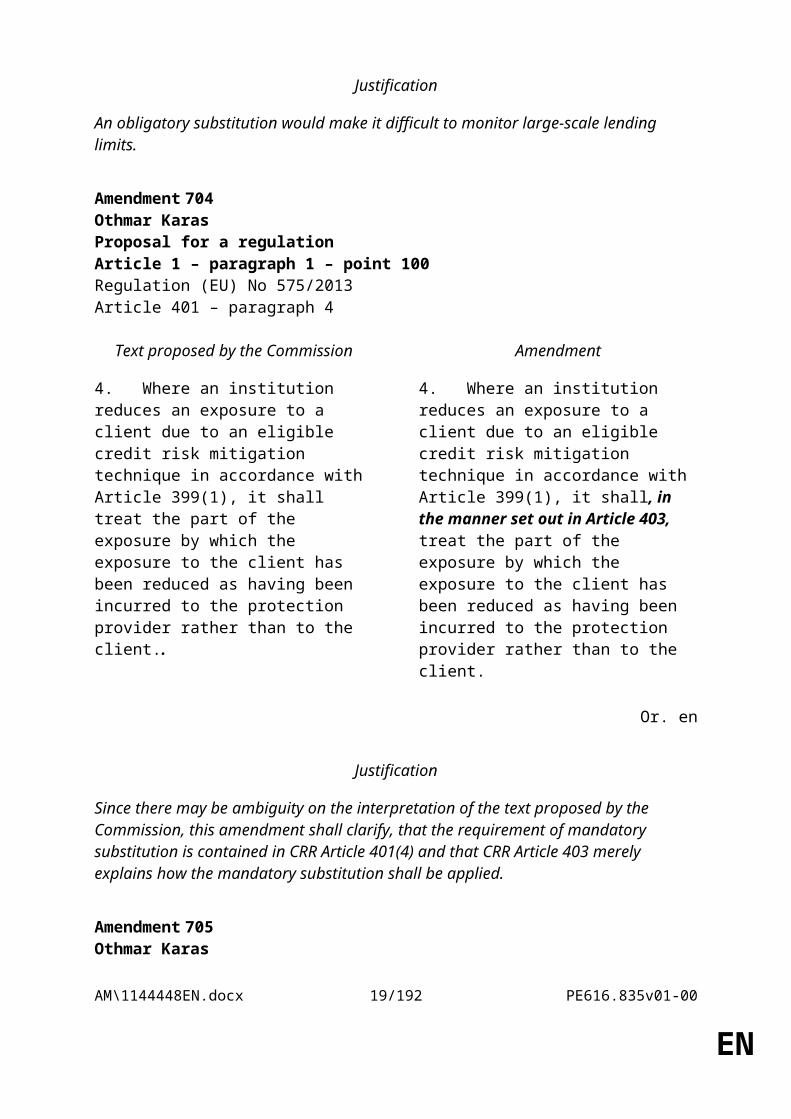

Amendment 704Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 100Regulation (EU) No 575/2013Article 401 – paragraph 4

Text proposed by the Commission Amendment

4. Where an institution reduces an exposure to a client due to an eligible credit risk mitigation technique in accordance with Article 399(1), it shall treat the part of the exposure by which the exposure to the client has been reduced as having been incurred to the protection provider rather than to the client..

4. Where an institution reduces an exposure to a client due to an eligible credit risk mitigation technique in accordance with Article 399(1), it shall, in the manner set out in Article 403, treat the part of the exposure by which the exposure to the client has been reduced as having been incurred to the protection provider rather than to the client.

Or. en

Justification

Since there may be ambiguity on the interpretation of the text proposed by the Commission, this amendment shall clarify, that the requirement of mandatory substitution is contained in

AM\1144448EN.docx 15/150 PE616.835v01-00

EN

CRR Article 401(4) and that CRR Article 403 merely explains how the mandatory substitution shall be applied.

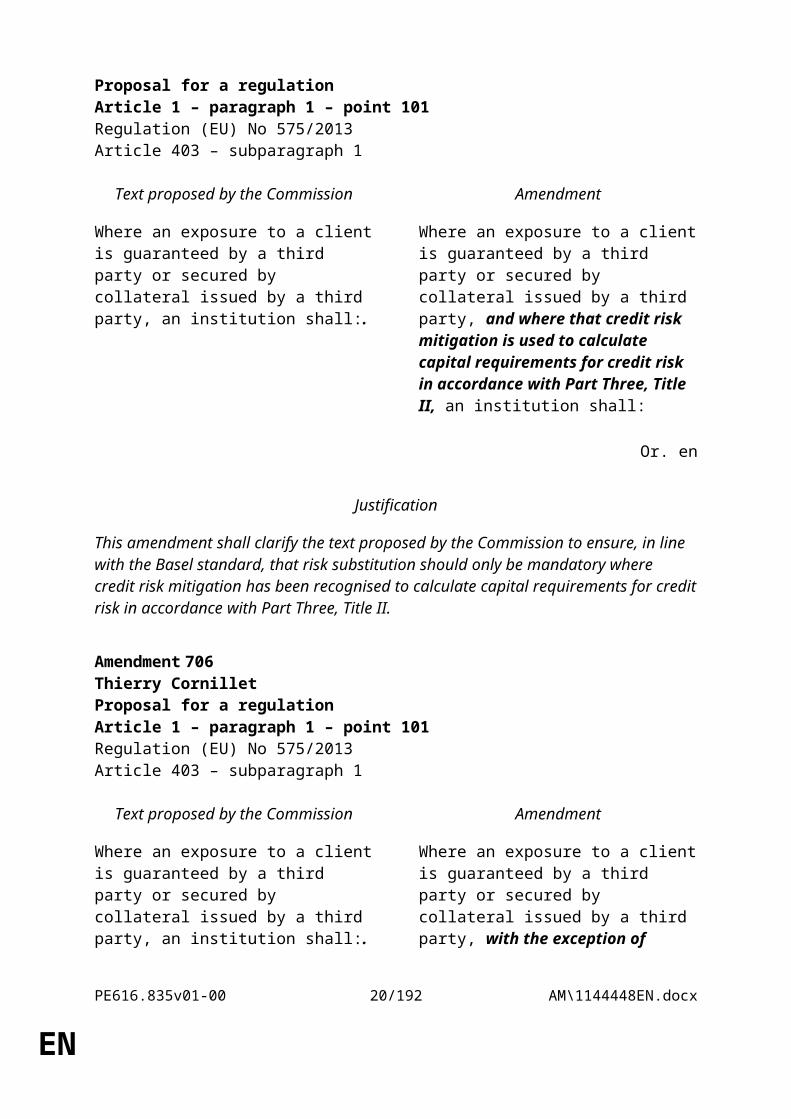

Amendment 705Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 101Regulation (EU) No 575/2013Article 403 – subparagraph 1

Text proposed by the Commission Amendment

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, an institution shall:.

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, and where that credit risk mitigation is used to calculate capital requirements for credit risk in accordance with Part Three, Title II, an institution shall:

Or. en

Justification

This amendment shall clarify the text proposed by the Commission to ensure, in line with the Basel standard, that risk substitution should only be mandatory where credit risk mitigation has been recognised to calculate capital requirements for credit risk in accordance with Part Three, Title II.

Amendment 706Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 101Regulation (EU) No 575/2013Article 403 – subparagraph 1

Text proposed by the Commission Amendment

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, an institution shall:.

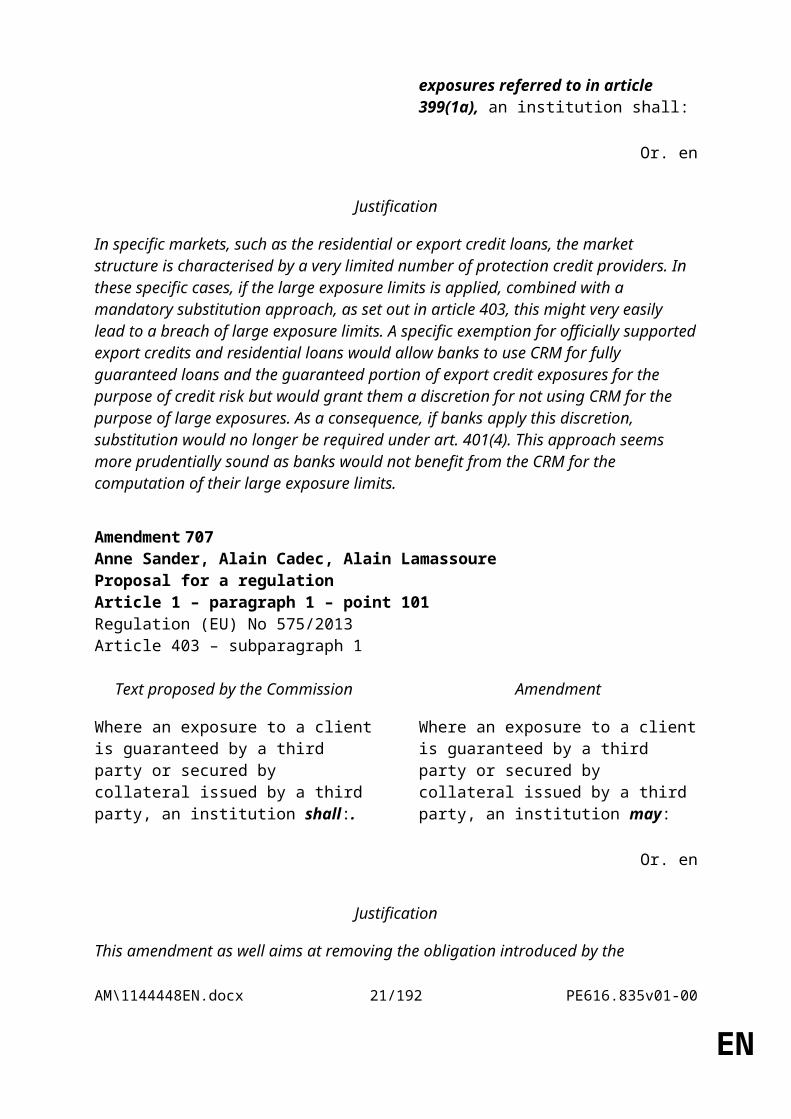

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, with the exception of exposures referred to in article 399(1a), an institution shall:

Or. en

PE616.835v01-00 16/150 AM\1144448EN.docx

EN

Justification

In specific markets, such as the residential or export credit loans, the market structure is characterised by a very limited number of protection credit providers. In these specific cases, if the large exposure limits is applied, combined with a mandatory substitution approach, as set out in article 403, this might very easily lead to a breach of large exposure limits. A specific exemption for officially supported export credits and residential loans would allow banks to use CRM for fully guaranteed loans and the guaranteed portion of export credit exposures for the purpose of credit risk but would grant them a discretion for not using CRM for the purpose of large exposures. As a consequence, if banks apply this discretion, substitution would no longer be required under art. 401(4). This approach seems more prudentially sound as banks would not benefit from the CRM for the computation of their large exposure limits.

Amendment 707Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 101Regulation (EU) No 575/2013Article 403 – subparagraph 1

Text proposed by the Commission Amendment

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, an institution shall:.

Where an exposure to a client is guaranteed by a third party or secured by collateral issued by a third party, an institution may:

Or. en

Justification

This amendment as well aims at removing the obligation introduced by the Commission to use the substitution approach in the large exposure regime. It can have detrimental effects on real estate market in some countries due to national specificities.

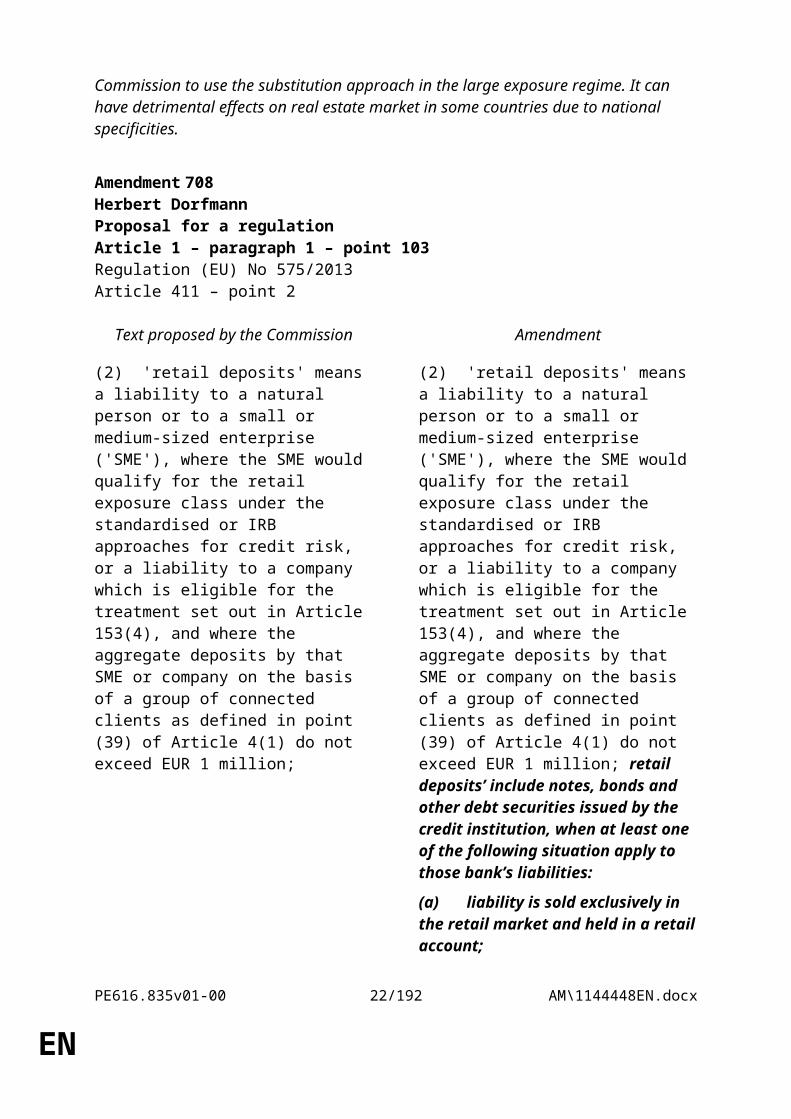

Amendment 708Herbert DorfmannProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 2

Text proposed by the Commission Amendment

(2) 'retail deposits' means a liability to a natural person or to a small or medium-sized enterprise ('SME'), where the SME

(2) 'retail deposits' means a liability to a natural person or to a small or medium-sized enterprise ('SME'), where the SME

AM\1144448EN.docx 17/150 PE616.835v01-00

EN

would qualify for the retail exposure class under the standardised or IRB approaches for credit risk, or a liability to a company which is eligible for the treatment set out in Article 153(4), and where the aggregate deposits by that SME or company on the basis of a group of connected clients as defined in point (39) of Article 4(1) do not exceed EUR 1 million;

would qualify for the retail exposure class under the standardised or IRB approaches for credit risk, or a liability to a company which is eligible for the treatment set out in Article 153(4), and where the aggregate deposits by that SME or company on the basis of a group of connected clients as defined in point (39) of Article 4(1) do not exceed EUR 1 million; retail deposits’ include notes, bonds and other debt securities issued by the credit institution, when at least one of the following situation apply to those bank’s liabilities:

(a) liability is sold exclusively in the retail market and held in a retail account;

(b) liability is held in a dossier linked to a retail account of the issuer institution and it is possible to monitor the effective holder of the instrument.

Or. en

Amendment 709Jeppe Kofod, Bendt BendtsenProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – introductory part

Text proposed by the Commission Amendment

(6) 'non-mandatory over-collateralisation' means any amount of assets which the institution is not obliged to attach to a covered bond issuance by virtue of legal or regulatory requirements, contractual commitments or for reasons of market discipline, including in particular where:

(6) 'non-mandatory over-collateralisation' means any amount of assets which the institution is not obliged to attach to a covered bond issuance by virtue of legal or regulatory requirements, contractual commitments, including in particular where:

Or. en

Amendment 710Rina Ronja KariProposal for a regulationArticle 1 – paragraph 1 – point 103

PE616.835v01-00 18/150 AM\1144448EN.docx

EN

Regulation (EU) No 575/2013Article 411 – point 6 – point b

Text proposed by the Commission Amendment

(b) pursuant to the methodology of a nominated ECAI, the assets are not required for the covered bonds to maintain their current credit assessment;

deleted

Or. en

Justification

It is not a sound principle to base the legislation on credit rating agencies.

Amendment 711Jonás FernándezProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – point b

Text proposed by the Commission Amendment

(b) pursuant to the methodology of a nominated ECAI, the assets are not required for the covered bonds to maintain their current credit assessment;

deleted

Or. en

Amendment 712Jeppe Kofod, Bendt BendtsenProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – point b

Text proposed by the Commission Amendment

(b) pursuant to the methodology of a nominated ECAI, the assets are not required for the covered bonds to maintain their current credit assessment;

deleted

AM\1144448EN.docx 19/150 PE616.835v01-00

EN

Or. en

Amendment 713Jonás FernándezProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – point c

Text proposed by the Commission Amendment

(c) the assets are not required for material credit enhancement purposes;

deleted

Or. en

Amendment 714Rina Ronja KariProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – point c

Text proposed by the Commission Amendment

(c) the assets are not required for material credit enhancement purposes;

deleted

Or. en

Amendment 715Jeppe Kofod, Bendt BendtsenProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 6 – point c

Text proposed by the Commission Amendment

(c) the assets are not required for material credit enhancement purposes;

deleted

Or. en

PE616.835v01-00 20/150 AM\1144448EN.docx

EN

Amendment 716Pervenche BerèsProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 15 a (new)

Text proposed by the Commission Amendment

(15a) "Factoring", which is to be treated as trade finance in part VI of this Regulation, means an agreement between a business (Assignor) and a financial entity (Factor) in which the Assignor assigns/sells its receivables to the Factor and the Factor provides the Assignor with a combination of one or more of the following services with regard to the receivables assigned: advance of a percentage of the amount of receivables assigned, management of receivables, collection and credit protection.

Or. en

Amendment 717Anne Sander, Alain Lamassoure, Alain CadecProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation (EU) No 575/2013Article 411 – point 15 a (new)

Text proposed by the Commission Amendment

(15a) In part VI of this regulation, factoring will be treated as trade finance. “Factoring” means an agreement between a business (Assignor) and a financial entity (Factor) in which the Assignor assigns/sells its Receivables to the Factor and the Factor provides the Assignor with a combination of one or more of the following services with regard to the Receivables assigned: Advance of a percentage of the amount of Receivables assigned, that is generally short term, uncommitted and without automatic roll-over, Receivables management, collection

AM\1144448EN.docx 21/150 PE616.835v01-00

EN

and Credit protection. Usually, the Factor administers the Assignor’s sales ledger and collects the Receivables in its own name. The Assignment can be disclosed to the Debtor.

Or. en

Justification

Factoring is a short term and uncommitted financing, with a low funding risk profile . Trade Finance is characterized by the same criteria, and as such benefit from a specific and preferential treatment, notably for Liquidity requirements, which is not explicitly the case of Factoring. Like Trade Finance, factoring is a major instrument for the financing of European corporates.

Amendment 718Thierry Cornillet, Caroline NagtegaalProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation No 575/2013/EUArticle 411 – point 15 a (new)

Text proposed by the Commission Amendment

(15a) "Factoring" means a contractual agreement between a business (assignor) and a financial entity (factor) in which the assignor assigns or sells its receivables to the factor in exchange of providing the assignor with one or more of the following services with regard to the receivables assigned:

– advance of a percentage of the amount of receivables assigned generally short term, uncommitted and without automatic roll-over,

– receivables management, collection and credit protection generally the factor administering the assignor’ sales ledger and collecting the receivables in its own name.

Or. en

PE616.835v01-00 22/150 AM\1144448EN.docx

EN

Justification

Factoring is a short term and uncommitted financing, with a low funding risk profile. Trade Finance is characterized by the same criteria, and as such benefit from a specific and preferential treatment, notably for Liquidity requirements, which is not explicitly the case of Factoring. Like Trade Finance, factoring is a major instrument for the financing of European corporates.

Amendment 719Thierry Cornillet, Caroline NagtegaalProposal for a regulationArticle 1 – paragraph 1 – point 103Regulation No 575/2013/EUArticle 411 – subparagraph 1 a (new)

Text proposed by the Commission Amendment

For the purposes of this Part, factoring shall be treated as trade finance.

Or. en

Justification

Factoring is a short term and uncommitted financing, with a low funding risk profile. Trade Finance is characterized by the same criteria, and as such benefit from a specific and preferential treatment, notably for Liquidity requirements, which is not explicitly the case of Factoring. Like Trade Finance, factoring is a major instrument for the financing of European corporates.

Amendment 720Marco ValliProposal for a regulationArticle 1 – paragraph 1 – point 104 – point -a (new)Regulation No 575/2013/EUArticle 412 – paragraph 1 a (new)

Text proposed by the Commission Amendment

(-a) the following new paragraph 1a is inserted:

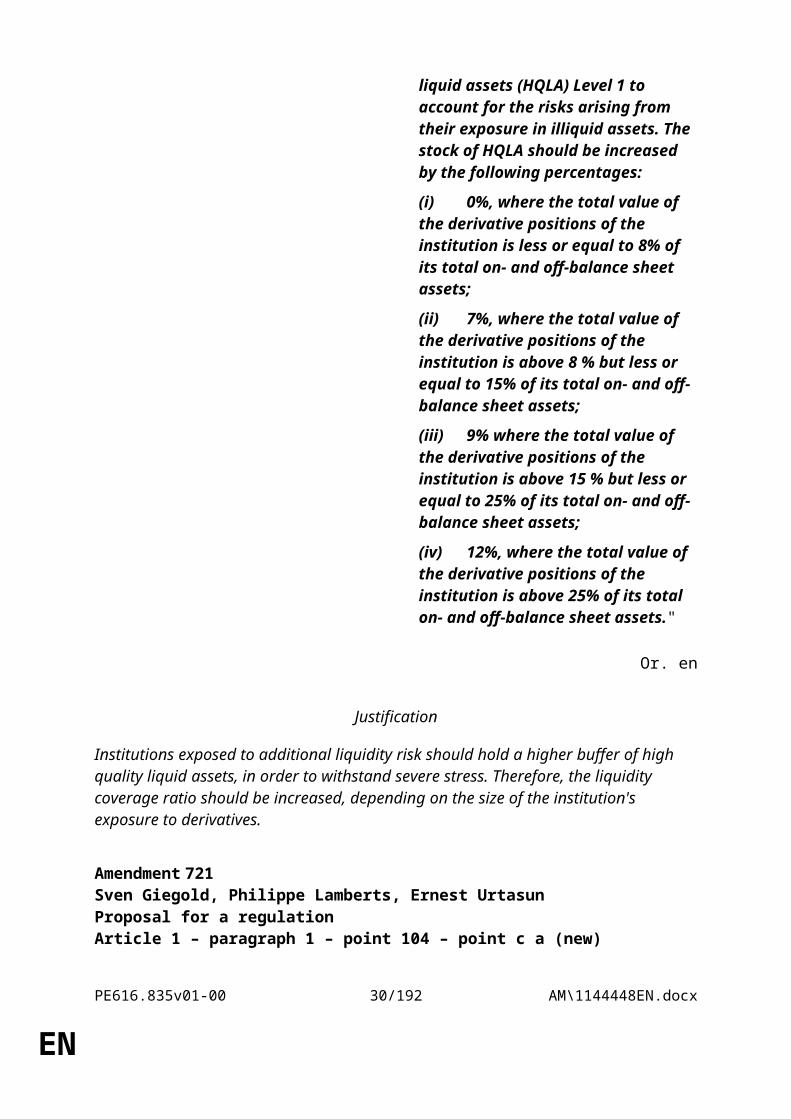

"1a. Institutions shall hold an additional amount of high quality liquid assets (HQLA) Level 1 to account for the risks arising from their exposure in illiquid assets. The stock of HQLA should

AM\1144448EN.docx 23/150 PE616.835v01-00

EN

be increased by the following percentages:

(i) 0%, where the total value of the derivative positions of the institution is less or equal to 8% of its total on- and off-balance sheet assets;

(ii) 7%, where the total value of the derivative positions of the institution is above 8 % but less or equal to 15% of its total on- and off-balance sheet assets;

(iii) 9% where the total value of the derivative positions of the institution is above 15 % but less or equal to 25% of its total on- and off-balance sheet assets;

(iv) 12%, where the total value of the derivative positions of the institution is above 25% of its total on- and off-balance sheet assets."

Or. en

Justification

Institutions exposed to additional liquidity risk should hold a higher buffer of high quality liquid assets, in order to withstand severe stress. Therefore, the liquidity coverage ratio should be increased, depending on the size of the institution's exposure to derivatives.

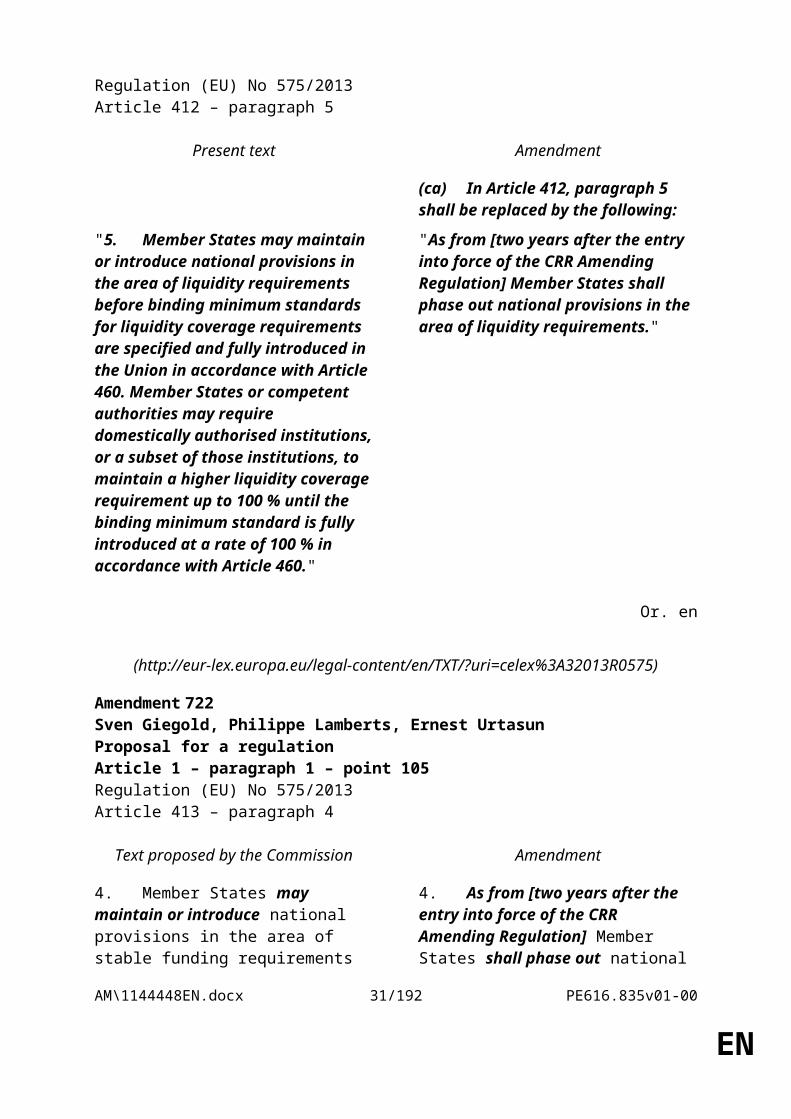

Amendment 721Sven Giegold, Philippe Lamberts, Ernest UrtasunProposal for a regulationArticle 1 – paragraph 1 – point 104 – point c a (new)Regulation (EU) No 575/2013Article 412 – paragraph 5

Present text Amendment

(ca) In Article 412, paragraph 5 shall be replaced by the following:

"5. Member States may maintain or introduce national provisions in the area of liquidity requirements before binding minimum standards for liquidity coverage requirements are specified and fully introduced in the Union in accordance with Article 460. Member States or competent authorities may require

"As from [two years after the entry into force of the CRR Amending Regulation] Member States shall phase out national provisions in the area of liquidity requirements."

PE616.835v01-00 24/150 AM\1144448EN.docx

EN

domestically authorised institutions, or a subset of those institutions, to maintain a higher liquidity coverage requirement up to 100 % until the binding minimum standard is fully introduced at a rate of 100 % in accordance with Article 460."

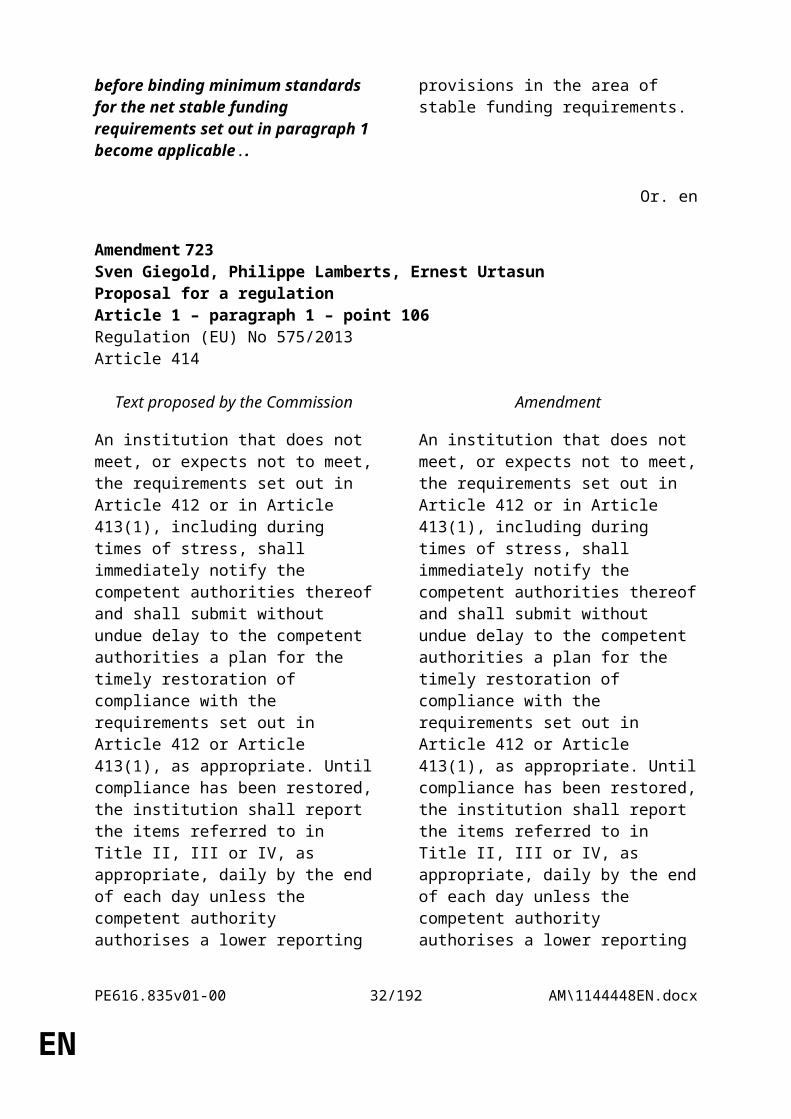

Amendment 722Sven Giegold, Philippe Lamberts, Ernest UrtasunProposal for a regulationArticle 1 – paragraph 1 – point 105Regulation (EU) No 575/2013Article 413 – paragraph 4

Text proposed by the Commission Amendment

4. Member States may maintain or introduce national provisions in the area of stable funding requirements before binding minimum standards for the net stable funding requirements set out in paragraph 1 become applicable..

4. As from [two years after the entry into force of the CRR Amending Regulation] Member States shall phase out national provisions in the area of stable funding requirements.

Or. en

Amendment 723Sven Giegold, Philippe Lamberts, Ernest UrtasunProposal for a regulationArticle 1 – paragraph 1 – point 106Regulation (EU) No 575/2013Article 414

Text proposed by the Commission Amendment

An institution that does not meet, or expects not to meet, the requirements set out in Article 412 or in Article 413(1), including during times of stress, shall immediately notify the competent authorities thereof and shall submit without undue delay to the competent authorities a plan for the timely restoration of compliance with the requirements set out

An institution that does not meet, or expects not to meet, the requirements set out in Article 412 or in Article 413(1), including during times of stress, shall immediately notify the competent authorities thereof and shall submit without undue delay to the competent authorities a plan for the timely restoration of compliance with the requirements set out

AM\1144448EN.docx 25/150 PE616.835v01-00

EN

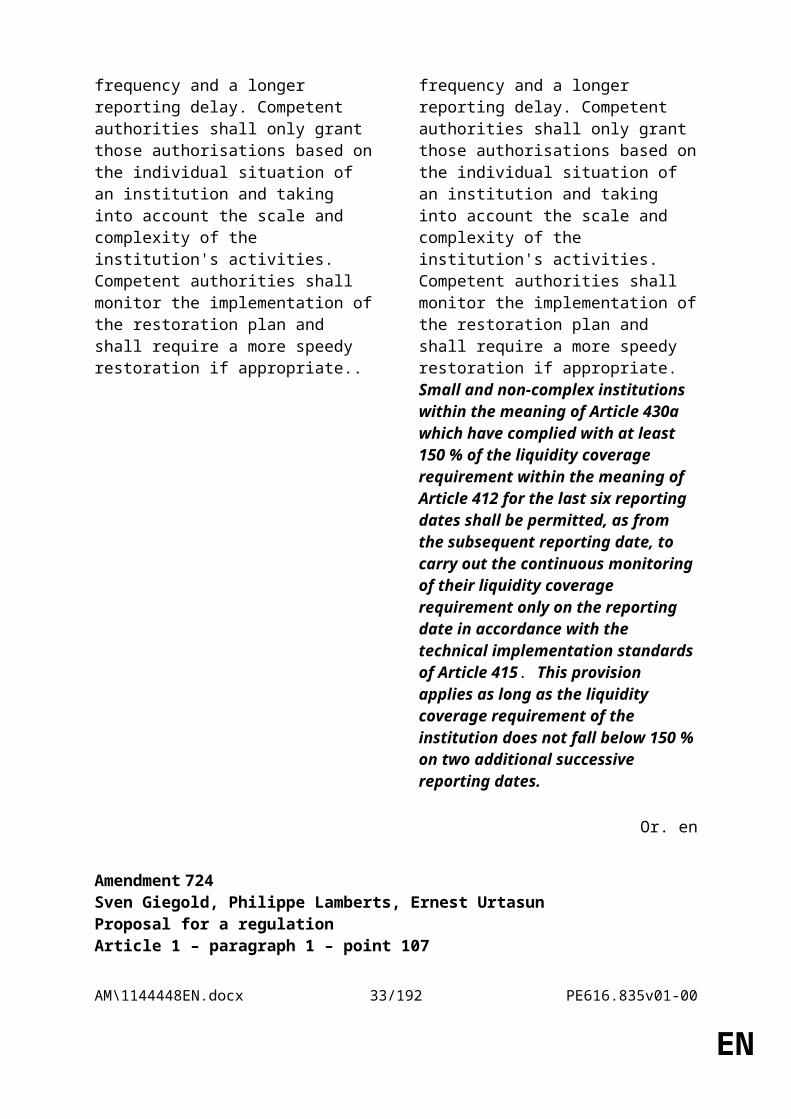

in Article 412 or Article 413(1), as appropriate. Until compliance has been restored, the institution shall report the items referred to in Title II, III or IV, as appropriate, daily by the end of each day unless the competent authority authorises a lower reporting frequency and a longer reporting delay. Competent authorities shall only grant those authorisations based on the individual situation of an institution and taking into account the scale and complexity of the institution's activities. Competent authorities shall monitor the implementation of the restoration plan and shall require a more speedy restoration if appropriate..

in Article 412 or Article 413(1), as appropriate. Until compliance has been restored, the institution shall report the items referred to in Title II, III or IV, as appropriate, daily by the end of each day unless the competent authority authorises a lower reporting frequency and a longer reporting delay. Competent authorities shall only grant those authorisations based on the individual situation of an institution and taking into account the scale and complexity of the institution's activities. Competent authorities shall monitor the implementation of the restoration plan and shall require a more speedy restoration if appropriate. Small and non-complex institutions within the meaning of Article 430a which have complied with at least 150 % of the liquidity coverage requirement within the meaning of Article 412 for the last six reporting dates shall be permitted, as from the subsequent reporting date, to carry out the continuous monitoring of their liquidity coverage requirement only on the reporting date in accordance with the technical implementation standards of Article 415. This provision applies as long as the liquidity coverage requirement of the institution does not fall below 150 % on two additional successive reporting dates.

Or. en

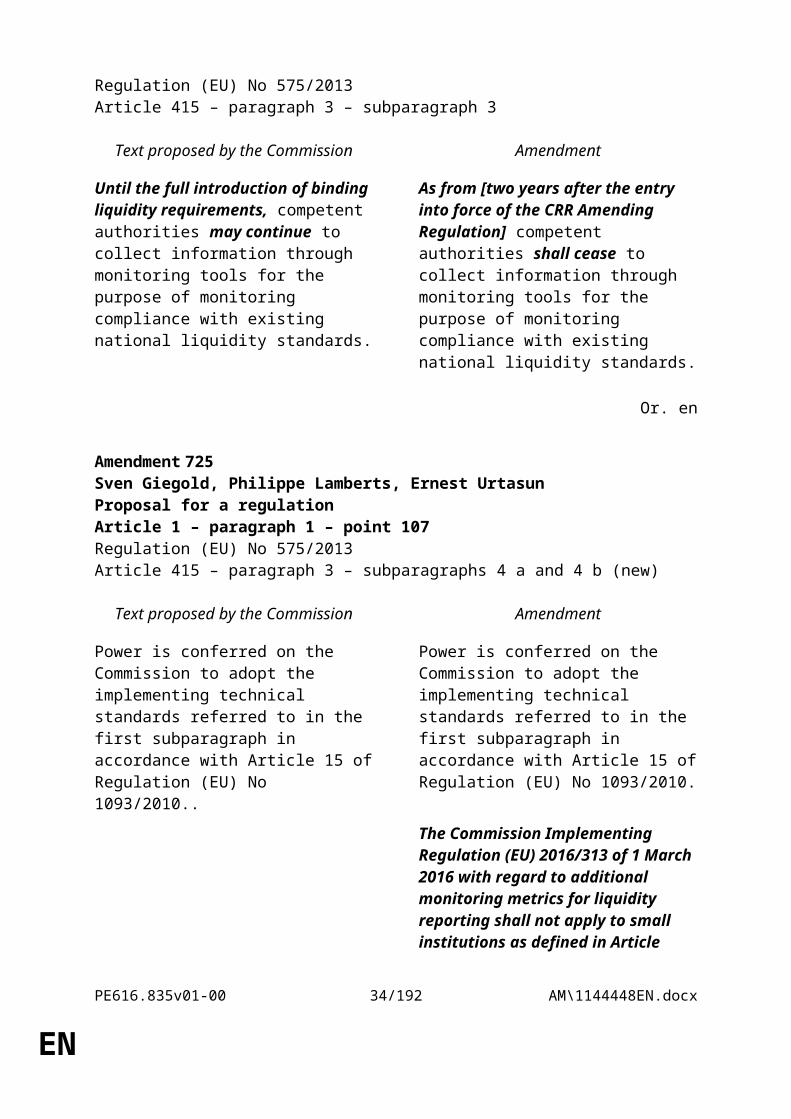

Amendment 724Sven Giegold, Philippe Lamberts, Ernest UrtasunProposal for a regulationArticle 1 – paragraph 1 – point 107Regulation (EU) No 575/2013Article 415 – paragraph 3 – subparagraph 3

Text proposed by the Commission Amendment

Until the full introduction of binding liquidity requirements, competent authorities may continue to collect information through monitoring tools for the purpose of monitoring compliance with

As from [two years after the entry into force of the CRR Amending Regulation] competent authorities shall cease to collect information through monitoring tools for the purpose of monitoring compliance with

PE616.835v01-00 26/150 AM\1144448EN.docx

EN

existing national liquidity standards. existing national liquidity standards.

Or. en

Amendment 725Sven Giegold, Philippe Lamberts, Ernest UrtasunProposal for a regulationArticle 1 – paragraph 1 – point 107Regulation (EU) No 575/2013Article 415 – paragraph 3 – subparagraphs 4 a and 4 b (new)

Text proposed by the Commission Amendment

Power is conferred on the Commission to adopt the implementing technical standards referred to in the first subparagraph in accordance with Article 15 of Regulation (EU) No 1093/2010..

Power is conferred on the Commission to adopt the implementing technical standards referred to in the first subparagraph in accordance with Article 15 of Regulation (EU) No 1093/2010.

The Commission Implementing Regulation (EU) 2016/313 of 1 March 2016 with regard to additional monitoring metrics for liquidity reporting shall not apply to small institutions as defined in Article 430a if their refinancing is based on deposits with a high degree of granularity and if their assets are sufficiently diversified.

The EBA shall issue regulatory technical standards to define “deposits with a high degree of granularity” and “sufficiently diversified assets” as condition for the exemption of small institutions from additional monitoring metrics for liquidity reporting.

Or. en

Amendment 726Wolf KlinzProposal for a regulationArticle 1 – paragraph 1 – point 108 – point bRegulation (EU) No 575/2013Article 416 – paragraph 5 – subparagraph 1

AM\1144448EN.docx 27/150 PE616.835v01-00

EN

Text proposed by the Commission Amendment

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that more than 75% of the CIU's investments, apart from derivatives to mitigate interest rate or credit or currency risk, are in liquid assets as referred to in paragraph 1 of this Article.

Or. en

Amendment 727Werner LangenProposal for a regulationArticle 1 – paragraph 1 – point 108 – point bRegulation (EU) No 575/2013Article 416 – paragraph 5 – subparagraph 1

Text proposed by the Commission Amendment

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Shares or units in CIUs may be treated as liquid assets up to a total amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Or. de

Justification

The above Regulation in its current form discriminates against small banks trying to guarantee regulatory LCR crediting (by means of liquid assets) and current income (by means of other assets) via one and the same investment fund. Since Article 418(3a) ensures that only those assets can be recognised which have been identified as such, the so-called ‘look-through principle’ already offers a more gentle approach which justifies deleting the word ‘only’ in Article 416(6).

PE616.835v01-00 28/150 AM\1144448EN.docx

EN

Amendment 728Thomas Mann, Werner LangenProposal for a regulationArticle 1 – paragraph 1 – point 108 – point bRegulation (EU) No 575/2013Article 416 – paragraph 5 – subparagraph 1

Text proposed by the Commission Amendment

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Shares or units in CIUs may be treated as liquid assets up to a total amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, invests in liquid assets as referred to in paragraph 1 of this Article.

Or. de

Amendment 729Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 108 – point bRegulation (EU) No 575/2013Article 416 – paragraph 5 – subparagraph 1

Text proposed by the Commission Amendment

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, invests in liquid assets as referred to in paragraph 1 of this Article.

Or. en

Justification

Since Art. 418(3)(a) ensures that only those assets can be recognized under the LCR which have been identified as liquid assets by means of a look-through-approach, the Commission proposal on Art. 416(5) can be considered unproportionate for smaller institutions which

AM\1144448EN.docx 29/150 PE616.835v01-00

EN

would have to achieve a return and regulatory recognition by one and the same CIU. In this context, the deletion of the word “only” aims to avoid a regulatory disincentive to contribute to a risk diversification by means of a CIU.

Amendment 730Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 108 – point bRegulation (EU) No 575/2013Article 416 – paragraph 5 – subparagraph 1

Text proposed by the Commission Amendment

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, only invests in liquid assets as referred to in paragraph 1 of this Article.

Shares or units in CIUs may be treated as liquid assets up to an absolute amount of EUR 500 million in the portfolio of liquid assets of each institution provided that the requirements in Article 132(3) are met and that the CIU, apart from derivatives to mitigate interest rate or credit or currency risk, invests in liquid assets as referred to in paragraph 1 of this Article.

Or. en

Amendment 731Matt Carthy, Martin SchirdewanProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 b – paragraph 2

Text proposed by the Commission Amendment

2. Institutions shall maintain a net stable funding ratio of at least 100%.

2. Institutions other than G-SIIs shall maintain a net stable funding ratio of at least 100%.

Or. en

Amendment 732Matt Carthy, Martin SchirdewanProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 b – paragraph 2 a (new)

PE616.835v01-00 30/150 AM\1144448EN.docx

EN

Text proposed by the Commission Amendment

2a. G-SIIs shall maintain a net stable funding ratio of at least 120%.

Or. en

Amendment 733Matt Carthy, Martin SchirdewanProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 b – paragraph 3

Text proposed by the Commission Amendment

3. Where at any time the net stable funding ratio of an institution has fallen or can be reasonably expected to fall below 100%, the requirement laid down in Article 414 shall apply. The institution shall aim at restoring its net stable funding ratio to the level referred to in paragraph 2. Competent authorities shall assess the reasons for non-compliance with the level referred to in paragraph 2 before taking, where appropriate, any supervisory measures.

3. Where at any time the net stable funding ratio of an institution has fallen or can be reasonably expected to fall below the thresholds specified in paragraph 2 and 2a (new) of this Article, the requirement laid down in Article 414 shall apply. The institution shall aim at restoring its net stable funding ratio to the levels referred to in paragraph 2 and 2a (new). Competent authorities shall assess the reasons for non-compliance with the level referred to in paragraph 2 and 2a (new) before taking, where appropriate, any supervisory measures.

Or. en

Amendment 734Markus FerberProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 c – paragraph 3a (new)

Text proposed by the Commission Amendment

3a. Institutions providing services concerned with the resolution of precious-metal transactions do not take into account precious-metal exposures which

AM\1144448EN.docx 31/150 PE616.835v01-00

EN

result from these services when calculating the Net Stable Funding Ratio.

Or. de

Justification

Precious-metal positions which are offered in order to provide settlement services should not be brought into play in the calculation of the Net Stable Funding Ratio.

Amendment 735Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 d – paragraph 2

Text proposed by the Commission Amendment

2. By way of derogation from Article 428c(1), institutions shall take into account the accounting value of derivative positions on a net basis where those positions are included in the same netting set that fulfils the requirements set out in Articles 295, 296 and 297. Where that is not the case, institutions shall take into account the accounting value of derivative positions on a gross basis and they shall treat those derivatives positions as their own netting set for the purpose of Chapter 4 of this Title.

2. By way of derogation from Article 428c(1), institutions shall take into account the market value of derivative positions on a net basis where those positions are included in the same netting set that fulfils the requirements set out in Articles 295, 296 and 297. Where that is not the case, institutions shall take into account the market value of derivative positions on a gross basis and they shall treat those derivatives positions as their own netting set for the purpose of Chapter 4 of this Title.

Or. en

Justification

This amendment shall clarify an inconsistency between paragraph 2 and paragraph 3 of CRR Article 428d, which may be misleading since in paragraph 3 reference is made to the market value of a netting set, and thus allow for an consistent treatment across banks in the Union.

Amendment 736Peter SimonProposal for a regulationArticle 1 – paragraph 1 – point 114

PE616.835v01-00 32/150 AM\1144448EN.docx

EN

Regulation (EU) No 575/2013Article 428 d – paragraph 2

Text proposed by the Commission Amendment

2. By way of derogation from Article 428c(1), institutions shall take into account the accounting value of derivative positions on a net basis where those positions are included in the same netting set that fulfils the requirements set out in Articles 295, 296 and 297. Where that is not the case, institutions shall take into account the accounting value of derivative positions on a gross basis and they shall treat those derivatives positions as their own netting set for the purpose of Chapter 4 of this Title.

2. By way of derogation from Article 428c(1), institutions shall take into account the market value of derivative positions on a net basis where those positions are included in the same netting set that fulfils the requirements set out in Articles 295, 296 and 297. Where that is not the case, institutions shall take into account the market value of derivative positions on a gross basis and they shall treat those derivatives positions as their own netting set for the purpose of Chapter 4 of this Title.

Or. en

Justification

(See the ECB's opinion (CON/2017/46)). There is an inconsistency between paragraph 2 and paragraph 3 of Article 428d, since in paragraph 3 reference is made to the market value of a netting set. It may therefore be misleading to refer to the accounting value in paragraph 2 as this may result in inconsistent treatment across banks. Reference should thus be made to the market value to ensure that the treatment of derivatives in the NSFR is independent from the relevant accounting scheme.

Amendment 737Caroline Nagtegaal, Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 d – paragraph 4

Text proposed by the Commission Amendment

4. All derivative contracts referred to in points (a) to (e) of paragraph 2 of Annex II that involve a full exchange of principal amounts on the same date shall be calculated on a net basis across currencies, including for the purpose of reporting in a currency that is subject to a separate reporting in accordance with Article

4. All derivative contracts referred to in points (a) to (e) of paragraph 2 of Annex II that involve a full exchange of principal amounts on the same date shall be calculated on a net basis across currencies, even where those transactions are not included in the same netting set that fulfils the requirements set out in Articles 295,

AM\1144448EN.docx 33/150 PE616.835v01-00

EN

415(2), even where those transactions are not included in the same netting set that fulfils the requirements set out in Articles 295, 296 and 297.

296 and 297.

Or. en

Amendment 738Pervenche BerèsProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 e

Text proposed by the Commission Amendment

By way of derogation from Article 428c(1), assets and liabilities resulting from secured lending transactions and capital market-driven transactions as defined in Article 192(2) and (3) with a single counterparty shall be calculated on a net basis, provided that those assets and liabilities respect the netting conditions set out in Article 429b(4).

In the application of point (b) of Article 428s and point (a) of Article 428u(1) and by way of derogation from Article 428c(1), assets and liabilities resulting from secured lending transactions and capital market-driven transactions as defined in Article 192(2) and (3) shall be calculated on a net basis, provided that the transactions explicit final settlement dates are below six months.

Or. en

Amendment 739Othmar KarasProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 1 – introductory part

Text proposed by the Commission Amendment

1. Subject to prior approval of competent authorities, an institution may consider that an asset and a liability are interdependent, provided that all of the following conditions are fulfilled:

1. If competent authorities agree through a prior approval process, an institution may consider that an asset and a liability are interdependent, provided that all of the following conditions are fulfilled:

Or. en

PE616.835v01-00 34/150 AM\1144448EN.docx

EN

Justification

This amendment shall ensure that the prior approval process for interdependent assets and liabilities shall remain in the sole discretion of the competent authorities.

Amendment 740Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – introductory part

Text proposed by the Commission Amendment

2. Assets and liabilities directly linked to the following products or services shall be considered to meet the conditions of paragraph 1 and be considered as interdependent :

2. Assets and liabilities directly linked to the following products or services shall be considered to meet the conditions of paragraph 1 and be considered at both the individual and consolidated levels :

Or. en

Amendment 741Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – point c

Text proposed by the Commission Amendment

(c) covered bonds as referred to in Article 52(4) of Directive 2009/65/EC;

(c) covered bonds as referred to in Article 52(4) of Directive 2009/65/EC and covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists non-discretionary extendable maturity triggers on the covered bonds of one year or more until the term of the underlying loans in the event of refinancing failure at the maturity date of the covered bond, or where national legislation adequately limits refinancing risk for covered bond issuers including through limitations on

AM\1144448EN.docx 35/150 PE616.835v01-00

EN

maturity mismatch between assets and liabilities;

Or. en

Justification

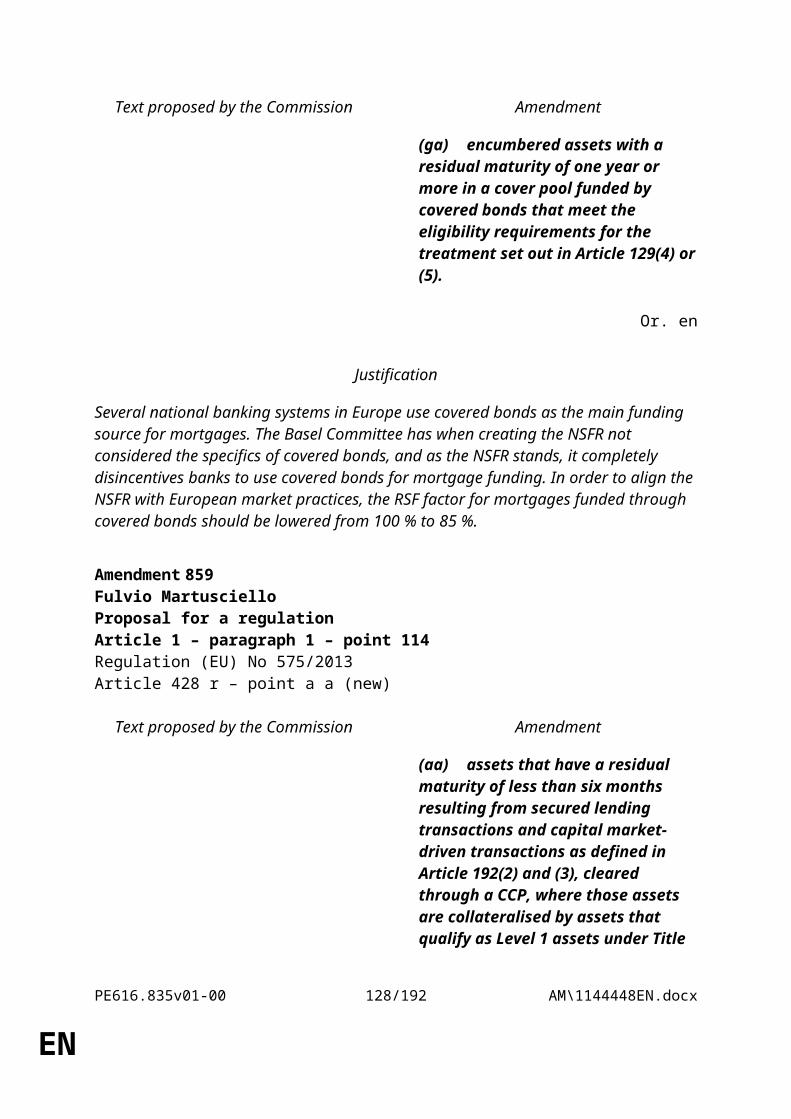

This amendment aims at recognizing covered bonds as interdependent assets and liabilities for the NSFR. The modification aims at ensuring that the NSFR is not over penalizing covered bonds

Amendment 742Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – point c

Text proposed by the Commission Amendment

(c) covered bonds as referred to in Article 52(4) of Directive 2009/65/EC;

(c) covered bonds as referred to in Article 52(4) of Directive 2009/65/EC; or that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), and (7) of the Regulation (EU) No 575/2013;

Or. en

Amendment 743Pervenche BerèsProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – point d

Text proposed by the Commission Amendment

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists non-discretionary extendable maturity triggers on the covered bonds of one year or more

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists non-discretionary extendable maturity triggers on the covered bonds of one year or more

PE616.835v01-00 36/150 AM\1144448EN.docx

EN

until the term of the underlying loans in the event of refinancing failure at the maturity date of the covered bond ;

until the term of the underlying loans in the event of refinancing failure at the maturity date of the covered bond, or where national legislation adequately limits refinancing risk for covered bond issuers, including through limitations on maturity mismatch between assets and liabilities;

Or. en

Amendment 744Stanisław OżógProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – point d

Text proposed by the Commission Amendment

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists non-discretionary extendable maturity triggers on the covered bonds of one year or more until the term of the underlying loans in the event of refinancing failure at the maturity date of the covered bond ;

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists contractual or legal provisions to manage refinancing risk.

Or. en

Justification

In our opinion, the COM approach is inconsistent, since it treats covered bonds preferentially in case of LCR (which targets short-term liquidity shocks), but does not provide the same in case of the NSFR, which are long-term liquidity ratio. Therefore, we see a strong need to adequately adjust current approach to better calibrate NSFR to EU market specificities and ensure level playing field across Members States with different covered bonds frameworks. Possible solution is to extend the scope of interdependent assets and liabilities by revising Article 428f (2)(d) of the CRR as above

Amendment 745Dariusz Rosati

AM\1144448EN.docx 37/150 PE616.835v01-00

EN

Proposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 f – paragraph 2 – point d

Text proposed by the Commission Amendment

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists non-discretionary extendable maturity triggers on the covered bonds of one year or more until the term of the underlying loans in the event of refinancing failure at the maturity date of the covered bond ;

(d) covered bonds that meet the eligibility requirements for the treatment set out in Article 129(4) or (5), as appropriate, where the underlying loans are fully matched funded with the covered bonds issued or where there exists contractual or legal provisions to manage refinancing risk;

Or. en

Amendment 746Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – introductory part

Text proposed by the Commission Amendment

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities may on a case-by-case basis authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities shall authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and both granted or received committed credit or liquidity facilities where all of the following conditions are fulfilled:

Or. en

Justification

The Commission's wording creates additional funding needs at solo level, which do not exist at group level. The preferential intragroup treatment must be granted, not subject to competent authority’s authorization.

PE616.835v01-00 38/150 AM\1144448EN.docx

EN

Amendment 747Marco ValliProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – introductory part

Text proposed by the Commission Amendment

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities may on a case-by-case basis authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities shall authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

Or. en

Amendment 748Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – introductory part

Text proposed by the Commission Amendment

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities may on a case-by-case basis authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities shall authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

Or. en

Justification

Solo level requirements at NSFR level, will be impacted by many asymmetries on RSF/ASF rates on operations between financial counterparts. This asymmetry makes no sense, as it concerns the same lending / borrowing operation, which is considered at the same time, as

AM\1144448EN.docx 39/150 PE616.835v01-00

EN

rolled in one scenario, and not in the second. It creates additional funding needs at solo level, which do not exist at group level. We therefore suggest that the preferential intragroup treatment be granted, not subject to competent authority’s authorization.

Amendment 749Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – introductory part

Text proposed by the Commission Amendment

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities may on a case-by-case basis authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

1. By way of derogation from Article 428g and from Chapters 3 and 4 of this Title, competent authorities shall authorise institutions to apply a higher available stable funding factor or a lower required stable funding factor to assets, liabilities and committed credit or liquidity facilities where all of the following conditions are fulfilled:

Or. en

Amendment 750Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point a – point v a (new)

Text proposed by the Commission Amendment

(va) the counterparty is located within the same Member State or in a different Member State;

Or. en

Amendment 751Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point a – point v a (new)

PE616.835v01-00 40/150 AM\1144448EN.docx

EN

Text proposed by the Commission Amendment

(va) the counterparty is located within the same Member State or in a different Member State;

Or. en

Justification

Solo level requirements at NSFR level, will be impacted by many asymmetries on RSF/ASF rates on operations between financial counterparts. This asymmetry makes no sense, as it concerns the same lending / borrowing operation, which is considered at the same time, as rolled in one scenario, and not in the second. It creates additional funding needs at solo level, which do not exist at group level. We therefore suggest that the preferential intragroup treatment be granted, not subject to competent authority’s authorization.

Amendment 752Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114 (new)Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point a – point v a (new)

Text proposed by the Commission Amendment

(va) the counterparty is located within the same Member State or in a different Member State.

Or. en

Justification

The Commission's wording creates additional funding needs at solo level, which do not exist at group level. The preferential intragroup treatment must be granted, not subject to competent authority’s authorization.

Amendment 753Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point b

AM\1144448EN.docx 41/150 PE616.835v01-00

EN

Text proposed by the Commission Amendment

(b) there are reasons to expect that the liability or committed credit or liquidity facility received constitutes a more stable source of funding or that the asset or committed credit or liquidity facility granted requires less stable funding within the one-year horizon of the net stable funding ratio than the same liability, asset or committed credit or liquidity facility with other counterparties;

deleted

Or. en

Justification

Solo level requirements at NSFR level, will be impacted by many asymmetries on RSF/ASF rates on operations between financial counterparts. This asymmetry makes no sense, as it concerns the same lending / borrowing operation, which is considered at the same time, as rolled in one scenario, and not in the second. It creates additional funding needs at solo level, which do not exist at group level. We therefore suggest that the preferential intragroup treatment be granted, not subject to competent authority’s authorization.

Amendment 754Barbara KappelProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point b

Text proposed by the Commission Amendment

(b) there are reasons to expect that the liability or committed credit or liquidity facility received constitutes a more stable source of funding or that the asset or committed credit or liquidity facility granted requires less stable funding within the one-year horizon of the net stable funding ratio than the same liability, asset or committed credit or liquidity facility with other counterparties;

deleted

Or. en

PE616.835v01-00 42/150 AM\1144448EN.docx

EN

Amendment 755Marco ValliProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point b

Text proposed by the Commission Amendment

(b) there are reasons to expect that the liability or committed credit or liquidity facility received constitutes a more stable source of funding or that the asset or committed credit or liquidity facility granted requires less stable funding within the one-year horizon of the net stable funding ratio than the same liability, asset or committed credit or liquidity facility with other counterparties;

deleted

Or. en

Amendment 756Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point b

Text proposed by the Commission Amendment

(b) there are reasons to expect that the liability or committed credit or liquidity facility received constitutes a more stable source of funding or that the asset or committed credit or liquidity facility granted requires less stable funding within the one-year horizon of the net stable funding ratio than the same liability, asset or committed credit or liquidity facility with other counterparties;

deleted

Or. en

Justification

The Commission's wording creates additional funding needs at solo level, which do not exist

AM\1144448EN.docx 43/150 PE616.835v01-00

EN

at group level. The preferential intragroup treatment must be granted, not subject to competent authority’s authorization.

Amendment 757Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point d

Text proposed by the Commission Amendment

(d) the institution and the counterparty are established in the same Member State.

deleted

Or. en

Justification

The Commission's wording creates additional funding needs at solo level, which do not exist at group level. The preferential intragroup treatment must be granted, not subject to competent authority’s authorization.

Amendment 758Anne Sander, Alain Cadec, Alain LamassoureProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 1 – point d

Text proposed by the Commission Amendment

(d) the institution and the counterparty are established in the same Member State.

deleted

Or. en

Justification

Solo level requirements at NSFR level, will be impacted by many asymmetries on RSF/ASF rates on operations between financial counterparts. This asymmetry makes no sense, as it concerns the same lending / borrowing operation, which is considered at the same time, as rolled in one scenario, and not in the second. It creates additional funding needs at solo level, which do not exist at group level. We therefore suggest that the preferential intragroup

PE616.835v01-00 44/150 AM\1144448EN.docx

EN

treatment be granted, not subject to competent authority’s authorization.

Amendment 759Marco ValliProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 2

Text proposed by the Commission Amendment

2. Where the institution and the counterparty are established in different Member States, competent authorities may waive the condition set out in point (d) of paragraph 1 where, in addition to the criteria set out in paragraph 1, the following criteria are fulfilled:

deleted

(a) there are legally binding agreements and commitments between group entities regarding the liability, asset or committed credit or liquidity facility;

(b) the funding provider presents a low funding risk profile;

(c) the funding risk profile of the funding receiver has been adequately taken into account in the liquidity risk management of the funding provider.

The competent authorities shall consult each other in accordance with point (b) of Article 20(1) to determine whether the additional criteria set out in this paragraph are met.

Or. en

Amendment 760Thierry CornilletProposal for a regulationArticle 1 – paragraph 1 – point 114Regulation (EU) No 575/2013Article 428 h – paragraph 2

Text proposed by the Commission Amendment

2. Where the institution and the deleted

AM\1144448EN.docx 45/150 PE616.835v01-00

EN

counterparty are established in different Member States, competent authorities may waive the condition set out in point (d) of paragraph 1 where, in addition to the criteria set out in paragraph 1, the following criteria are fulfilled:

(a) there are legally binding agreements and commitments between group entities regarding the liability, asset or committed credit or liquidity facility;

(b) the funding provider presents a low funding risk profile;

(c) the funding risk profile of the funding receiver has been adequately taken into account in the liquidity risk management of the funding provider.

The competent authorities shall consult each other in accordance with point (b) of Article 20(1) to determine whether the additional criteria set out in this paragraph are met.

Or. en

Justification

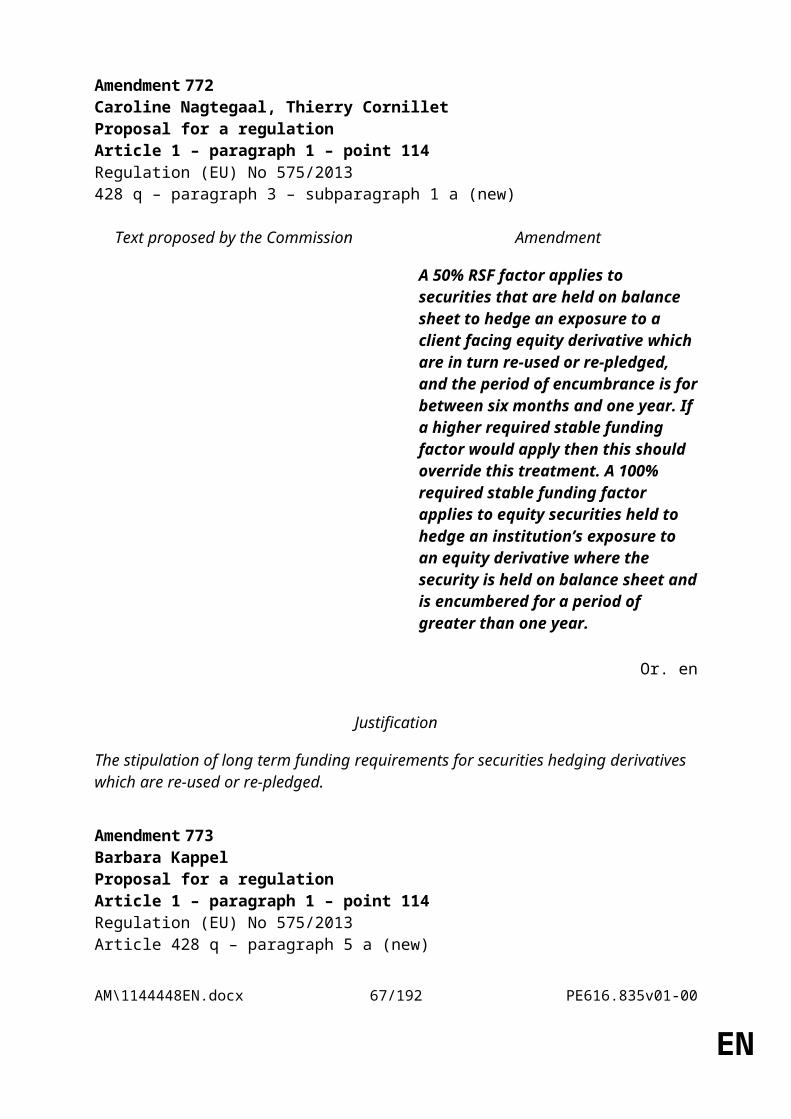

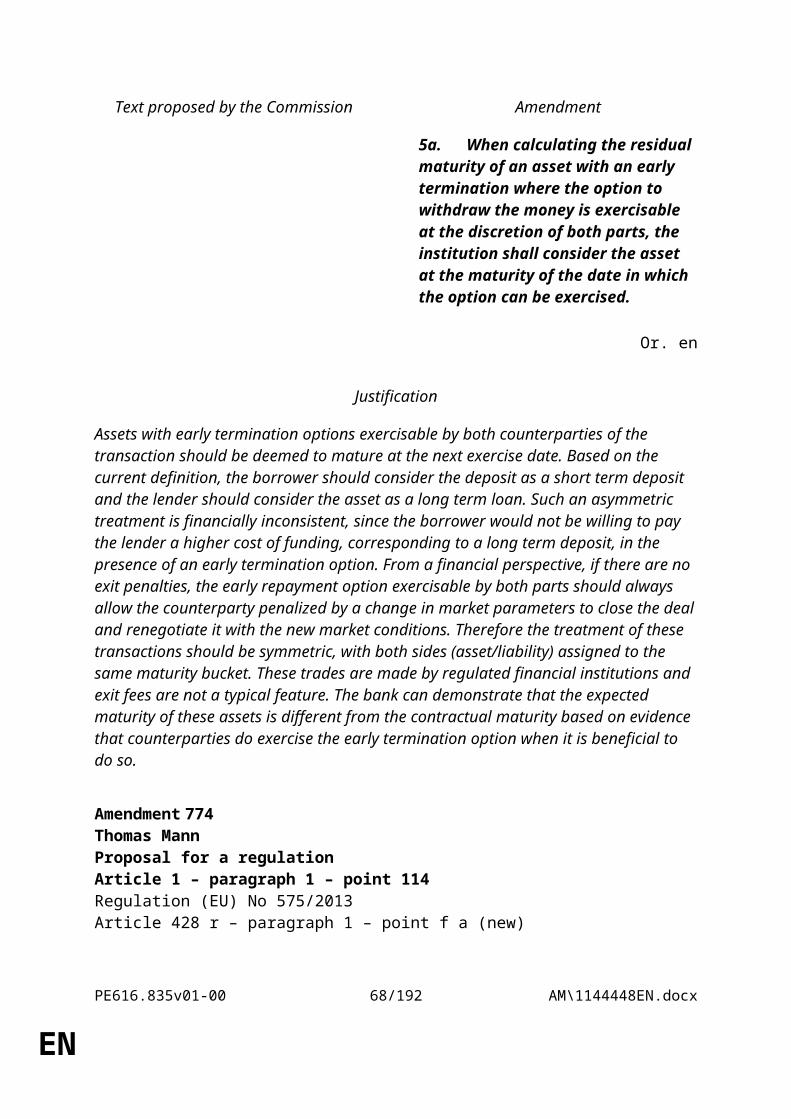

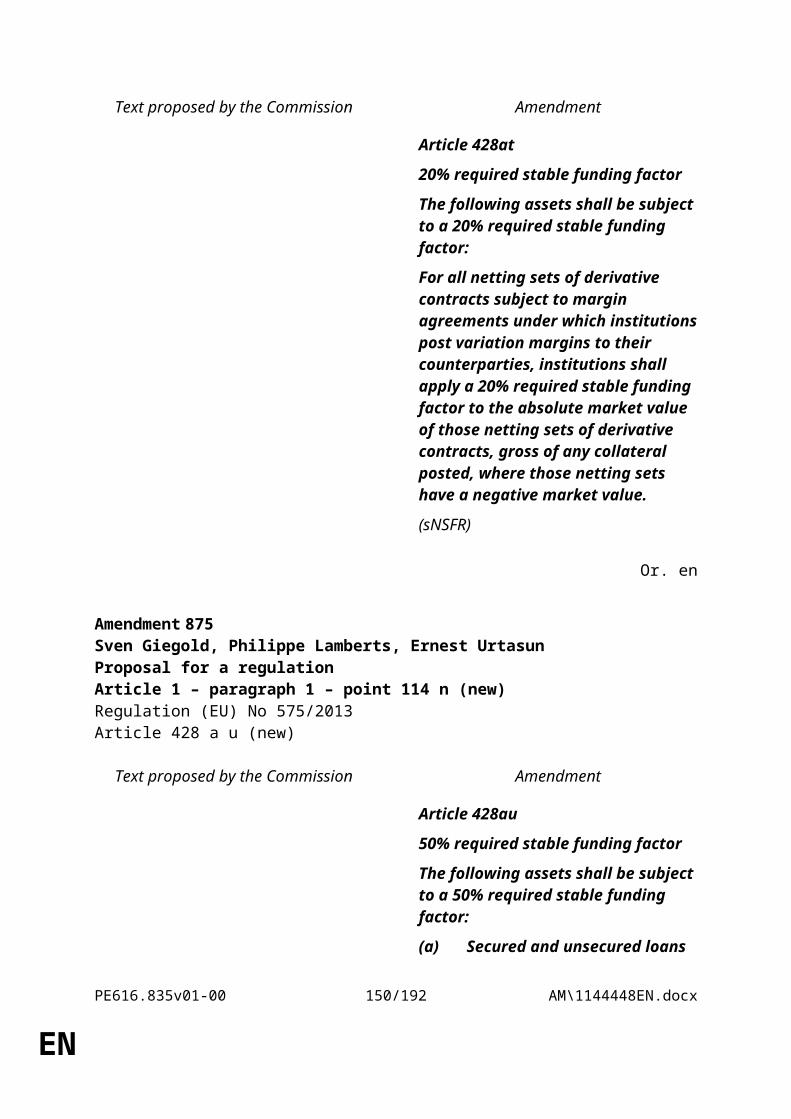

The Commission's wording creates additional funding needs at solo level, which do not exist at group level. The preferential intragroup treatment must be granted, not subject to competent authority’s authorization.