Report of Independent Auditors in Accordance with Uniform Guidance and Financial Statements with Supplementary Information for American Samoa Medical Center Authority Lyndon B. Johnson Tropical Medical Center (A Component Unit of the American Samoa Government) Pago Pago, American Samoa September 30, 2016 and 2015

Transcript

Report of Independent Auditorsin Accordance with Uniform Guidance

and Financial Statements withSupplementary Information for

American Samoa Medical Center AuthorityLyndon B. Johnson Tropical Medical Center

(A Component Unit of the American Samoa Government)Pago Pago, American Samoa

REPORTOFINDEPENDENTAUDITORSTotheBoardofDirectorsAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenterPagoPago,AmericanSamoaReportontheFinancialStatementsWehaveauditedtheaccompanyingfinancialstatementsofAmericanSamoaMedicalCenterAuthorityLyndonB.Johnson Tropical Medical Center (“LBJ” or “Medical Center’’), a component unit of the American SamoaGovernment,asofandfortheyearsendedSeptember30,2016and2015,andtherelatednotestothefinancialstatements,whichcollectivelycompriseLBJ'sbasicfinancialstatementsaslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatementsManagementisresponsibleforthepreparationandfairpresentationofthesefinancialstatementsinaccordancewith accounting principles generally accepted in the United States of America; this includes the design,implementation,andmaintenanceofinternalcontrolrelevanttothepreparationandfairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor’sResponsibilityOurresponsibilityistoexpressanopiniononthesefinancialstatementsbasedonouraudits.Weconductedouraudits in accordance with auditing standards generally accepted in the United States of America and thestandardsapplicable to financialauditscontained inGovernmentAuditingStandards, issuedbytheComptrollerGeneraloftheUnitedStates.Thosestandardsrequirethatweplanandperformtheauditstoobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancialstatements.Theproceduresselecteddependontheauditor’sjudgment,includingtheassessmentoftherisksofmaterialmisstatementof the financialstatements,whetherdue to fraudorerror. Inmaking thoseriskassessments, theauditorconsiders internalcontrolrelevanttotheentity’spreparationandfairpresentationofthefinancialstatementsinordertodesignauditproceduresthatareappropriateinthecircumstances,butnotforthepurposeofexpressinganopinionontheeffectivenessoftheMedicalCenter’sinternalcontrol.Accordingly,weexpressnosuchopinion.Anauditalso includesevaluatingtheappropriatenessofaccountingpoliciesusedandthe reasonableness of significant accounting estimatesmadebymanagement, aswell as evaluating the overallpresentationofthefinancialstatements.We believe that the audit evidencewe have obtained is sufficient and appropriate to provide a basis for ourqualifiedauditopinion.

2

BasisforQualifiedOpinionWe were unable to obtain sufficient appropriate audit evidence about the recorded amounts and relateddisclosures for patient accounts receivable and net patient services revenue as of and for the years endedSeptember30,2016and2015.Consequently,wewereunable todeterminewhetheranyadjustments to theseamountswerenecessary.QualifiedOpinionInouropinion,exceptforthepossibleeffectsofthematterdescribedintheBasisforQualifiedOpinionparagraph,the financial statements referred to above present fairly, in allmaterial respects, the financial position of theMedicalCenterasofSeptember30,2016and2015,andthechangesinfinancialpositionand,whereapplicable,itscashflowsthereoffortheyearsthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.EmphasisofaMatterAsdiscussedinNote9tothefinancialstatements,in2015,theMedicalCenteradoptedGovernmentalAccountingStandardsBoard(GASB)StatementNo.68,AccountingandFinancialReporting forPensions–anamendmentofGASBStatementNo.27andGASBStatementNo.71,PensionTransitionforContributionsMadeSubsequenttotheMeasurementDate–anamendmentofGASBStatementsNo.68.Ouropinionisnotmodifiedwithrespecttothismatter.OtherMattersRequiredSupplementaryInformationAccountingprinciplesgenerallyacceptedintheUnitedStatesofAmericarequirethatthescheduleoftheMedicalCenter's proportional share of the net pension liability on page 26 and the schedule of the Medical Center'scontributionsonpage27bepresentedtosupplementthebasicfinancialstatements.Suchinformation,althoughnot a part of the basic financial statements, is required by GASB, who considers it to be an essential part offinancialreportingforplacingthebasicfinancialstatementsinanappropriateoperational,economic,orhistoricalcontext.Wehaveapplied certain limitedprocedures to the required supplementary information inaccordancewith auditing standards generally accepted in the United States of America, which consisted of inquiries ofmanagement about themethods of preparing the information and comparing the information for consistencywithmanagement'sresponsestoourinquiries,thebasicfinancialstatements,andotherknowledgeweobtainedduringourauditofthebasicfinancialstatements.Wedonotexpressanopinionorprovideanyassuranceontheinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.Managementhasomittedthemanagement'sdiscussionandanalysisandbudgetarycomparisoninformationthataccountingprinciplesgenerallyacceptedintheUnitedStatesofAmericarequiretobepresentedtosupplementthebasicfinancialstatements.Suchmissinginformation,althoughnotapartofthebasicfinancialstatements,isrequiredbyGASB,whoconsiders it tobeanessentialpartof financial reporting forplacing thebasic financialstatements in an appropriate operational, economic, or historical context. Our opinion on the basic financialstatementsisnotaffectedbythismissinginformation.

3

SupplementaryInformationOur audit was conducted for the purpose of forming an opinion on the financial statements that collectivelycompriseLBJ'sbasicfinancialstatements.ThescheduleofexpendituresoffederalawardsasrequiredbyTitle2,U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and AuditRequirementsforFederalAwardsispresentedforpurposesofadditionalanalysisandisnotarequiredpartofthebasicfinancialstatements.Thescheduleofexpendituresof federalawards istheresponsibilityofmanagementandwasderivedfromandrelatesdirectly to theunderlyingaccountingandother recordsused toprepare thebasic financial statements.Such information has been subjected to the auditing procedures applied in the audit of the basic financialstatementsandcertainadditionalprocedures, includingcomparingandreconcilingsuchinformationdirectlytothe underlying accounting and other records used to prepare the basic financial statements or to the basicfinancialstatementsthemselves,andotheradditionalproceduresinaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica.Inouropinion,thescheduleofexpendituresoffederalawardsisfairlystated,inallmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedApril28,2017onourconsiderationoftheMedicalCenter’sinternalcontroloverfinancialreportingandonourtestsofitscompliancewithcertainprovisionsof laws,regulations,contracts,andgrantagreementsandothermatters.Thepurposeofthatreportistodescribethescopeofourtestingofinternalcontroloverfinancialreportingandcomplianceandthe results of that testing, and not to provide an opinion on internal control over financial reporting or oncompliance. That report is an integral part of an audit performed in accordance with Government AuditingStandardsinconsideringtheMedicalCenter'sinternalcontroloverfinancialreportingandcompliance.

Note1–DescriptionofOperationsAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenter(theMedicalCenterorLBJ) is a128‐bedgeneral acute carehospitalwhichprovideshealth care to theTerritoryofAmericanSamoa. LBJ is a component unit of the American Samoa Government (ASG), and the results of LBJ’soperationsareincludedinASG’sbasicfinancialstatements.Thecriteriausedtodetermineinclusioninthefinancialreportingentity includesfinancial interdependency,selectionofgoverningauthority,designationofmanagement,andaccountabilityforfiscalmatters.LBJwasopenedin1968toprovidepatient focused,comprehensive,highquality,andcosteffectivehealthcare and related services that address the health needs of the people of American Samoa. The facility isfunded through federal appropriations, patient service revenue, and Medicaid reimbursements. LBJ wasformallygrantedsemiautonomousstatusasanindependentagencyoftheExecutiveBranchoftheAmericanSamoanGovernment through anExecutiveOrder on September22, 1997, and then by LegislativeAct onFebruary26,1998,inordertosatisfyfederalrequirements.LBJisgovernedbyafive‐memberBoardofDirectors.TheBoardmembersareappointedbytheGovernorofAmericanSamoaandmustreceiveapprovaloftheLegislaturetoservethetwo‐yearterm.Note2–SummaryofSignificantAccountingPoliciesBasisofaccounting–Theaccompanyingfinancialstatementshavebeenpreparedontheaccrualbasisofaccountingusing theeconomic resourcesmeasurement focus.Under thismethodofaccounting, revenuesare recognized when earned and expenses are recorded when liabilities are incurred without regard toreceiptordisbursementofcash.Accounting standards – The operations of theMedical Center are presented in the accompanying basicfinancialstatementsasasingleproprietaryfund.TheMedicalCenterhasnocomponentunits.ThefinancialstatementshavebeenpreparedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica(GAAP)asprescribedbytheGovernmentAccountingStandardsBoard(GASB).Netposition–Netpositionof theMedicalCenter represents the residual interest in assets anddeferredoutflows of resources after liabilities are deducted and are classified into three components. The netinvestment in capital assets component of net position consists of capital assets, net of accumulateddepreciation, reduced by the outstanding balances of related debt that is attributable to the acquisition,construction, or improvementof thoseassets.Netposition is reportedas restrictedwhenconstraints areimposedbythirdpartiesorenablinglegislation.Theaccountsshownasrestrictednetpositionareamountsthat can be spent only for the specific purposes stipulated by constitutional provisions or enablinglegislation,orimposedbycreditors,grantors,orotherexternalresourceproviders.Allothernetpositionisunrestricted.

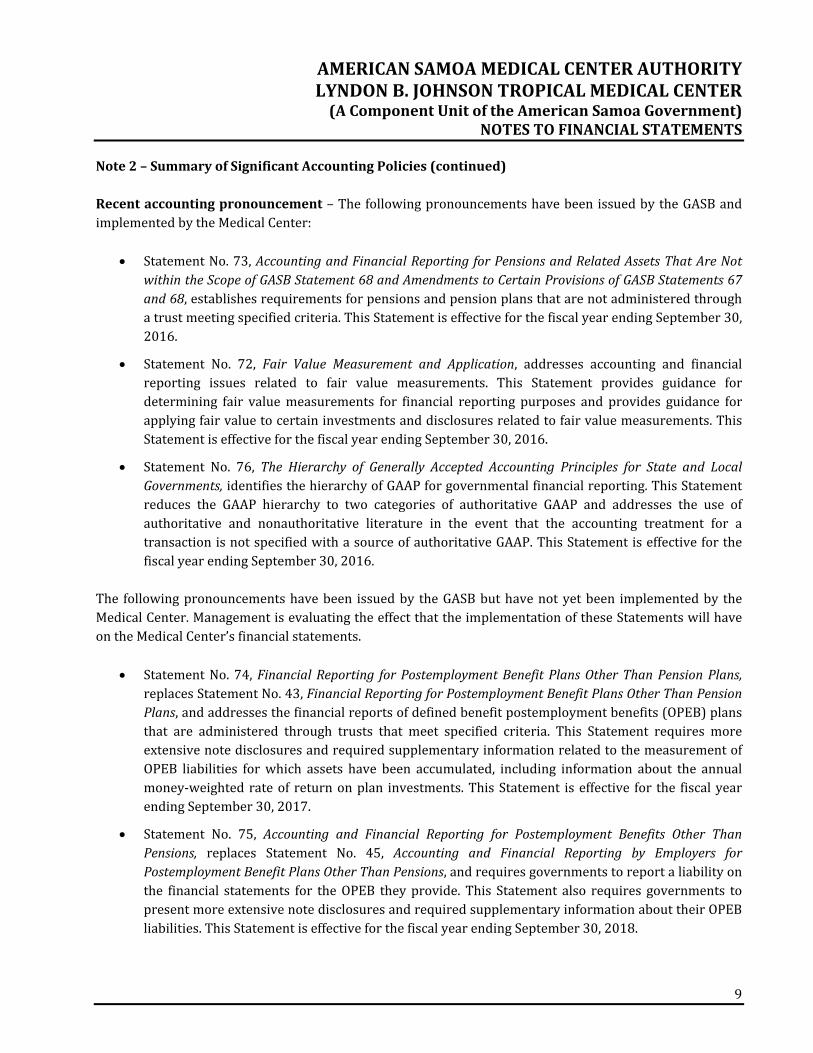

Statement No. 72, Fair Value Measurement and Application, addresses accounting and financialreporting issues related to fair value measurements. This Statement provides guidance fordetermining fair valuemeasurements for financial reporting purposes and provides guidance forapplyingfairvaluetocertaininvestmentsanddisclosuresrelatedtofairvaluemeasurements.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2016.

Statement No. 76, The Hierarchy of Generally Accepted Accounting Principles for State and LocalGovernments,identifiesthehierarchyofGAAPforgovernmentalfinancialreporting.ThisStatementreduces the GAAP hierarchy to two categories of authoritative GAAP and addresses the use ofauthoritative and nonauthoritative literature in the event that the accounting treatment for atransactionisnotspecifiedwithasourceofauthoritativeGAAP.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2016.

The followingpronouncementshavebeen issuedby theGASBbuthavenotyetbeen implementedby theMedicalCenter.ManagementisevaluatingtheeffectthattheimplementationoftheseStatementswillhaveontheMedicalCenter’sfinancialstatements.

StatementNo.74,FinancialReporting forPostemploymentBenefitPlansOtherThanPensionPlans,replacesStatementNo.43,FinancialReportingforPostemploymentBenefitPlansOtherThanPensionPlans,andaddressesthefinancialreportsofdefinedbenefitpostemploymentbenefits(OPEB)plansthat are administered through trusts that meet specified criteria. This Statement requires moreextensivenotedisclosuresandrequiredsupplementaryinformationrelatedtothemeasurementofOPEB liabilities forwhich assets have been accumulated, including information about the annualmoney‐weightedrateof returnonplan investments.ThisStatement iseffective for the fiscalyearendingSeptember30,2017.

Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other ThanPensions, replaces Statement No. 45, Accounting and Financial Reporting by Employers forPostemploymentBenefitPlansOtherThanPensions,andrequiresgovernmentstoreportaliabilityonthe financial statements for theOPEB theyprovide. This Statement also requires governments topresentmoreextensivenotedisclosuresandrequiredsupplementaryinformationabouttheirOPEBliabilities.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2018.

StatementNo.77,TaxAbatementDisclosures,requiresnewfinancialstatementdisclosuresabouttaxabatementagreementsbetweenagovernmentandanindividualorentityinwhichthegovernmentpromisestoforgotaxrevenuesandthe individualorentitypromisestotakeaspecificactionthatcontributestotheeconomicdevelopmentorotherwisebenefitsthegovernmentoritscitizens.ThisStatementrequiresdisclosureoftaxabatementinformationofthereportinggovernment’sowntaxabatement agreements and agreements entered into by other governments that reduce thereporting government’s tax revenues. This Statement is effective for the fiscal year endingSeptember30,2017.

Statement No. 78, Pensions Provided through Certain Multiple‐Employer Defined Benefit PensionPlans, amends the scope and applicability of Statement No. 68 to exclude pensions provided toemployees of state or local governmental employers through cost‐sharing multiple‐employerdefinedbenefit plans that are not state or local governmental pensionplans, are used to providebenefitstobothgovernmentalandnon‐governmentalemployers,andhavenopredominantstateorlocalgovernmentalemployer.ThisStatementalsoestablishesnewrequirementsfortherecognitionof pension expenditures and liabilities and additional footnote disclosures and requiredsupplementaryinformationforpensionsthathavethesecharacteristics.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2017.

StatementNo.79,CertainExternalInvestmentPoolsandPoolParticipants,establishescriteriaforanexternal investment pool to qualify for making the election to measure all of its investments atamortized cost for financial reporting purposes and additional footnote disclosures requirementsforgovernmentsthatparticipate inthosepools. If theexternal investmentpooldoesnotmeetthecriteriaofthisStatement,thepool’sparticipantsshouldmeasuretheirinvestmentsinthepoolatfairvalue,asprovidedinStatementNo.31,AccountingandFinancialReportingforCertainInvestmentsandforExternalInvestmentPools,asamended.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2017.

Statement No. 80, Blending Requirements for Certain Component Units – An Amendment of GASBStatementNo. 14, amends the blending requirements for the financial statement presentation ofcomponent units of state and local governments. The additional criteria require blending of acomponentunitincorporatedasanot‐for‐profitcorporationinwhichtheprimarygovernmentisthesolecorporatemember.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2018.

Statement No. 81, Irrevocable Split‐Interest Agreements, provides recognition and measurementguidance for situations in which a government is a beneficiary of an irrevocable split‐interestagreement,agivingarrangementusedbydonorstoprovideresourcestotwoormorebeneficiaries.ThisStatementiseffectiveforthefiscalyearendingSeptember30,2018.

Statement No. 83, Certain Asset Retirement Obligations, will enhance comparability of financialstatementsamonggovernmentsbyestablishinguniformcriteriaforgovernmentstorecognizeandmeasure certain AROs, including obligations that may not have been previously reported. ThisStatement also will enhance the decision‐usefulness of the information provided to financialstatementusersbyrequiringdisclosuresrelatedtothoseAROs.ThisStatement iseffectiveforthefiscalyearendingSeptember30,2019.

Use of estimates – The preparation of the financial statements in conformity with GAAP requiresmanagementtomakeestimatesandassumptionsthataffectthereportedamountsofassetsandliabilitiesanddisclosureof contingentassetsand liabilitiesat thedateof the financial statementsand thereportedamounts of revenues and expenses during the reporting period. Actual results could differ from thoseestimatesandassumptions.

Cash and cash equivalents – LBJ considers all highly liquid investment instruments with an originalmaturityofthreemonthsorlesstobecashequivalents.

AsofSeptember30,2016,thecarryingamountofLBJ’stotalcashandcashequivalentswas$855,930andthecorrespondingbankbalanceswere$1,316,333.AsofSeptember30,2016,bankdepositsintheamountof $726,412 were Federal Deposit Insurance Corporation (FDIC) insured. LBJ does not requirecollateralization of its cash deposits; therefore, deposit levels in excess of FDIC insurance coverage areuncollateralized.Accordingly, thesedepositsareexposed to custodial credit risk.LBJhasnotexperiencedanylossesonsuchaccountsandmanagementbelievesitisnotexposedtoanysignificantcreditriskonitsdeposits.

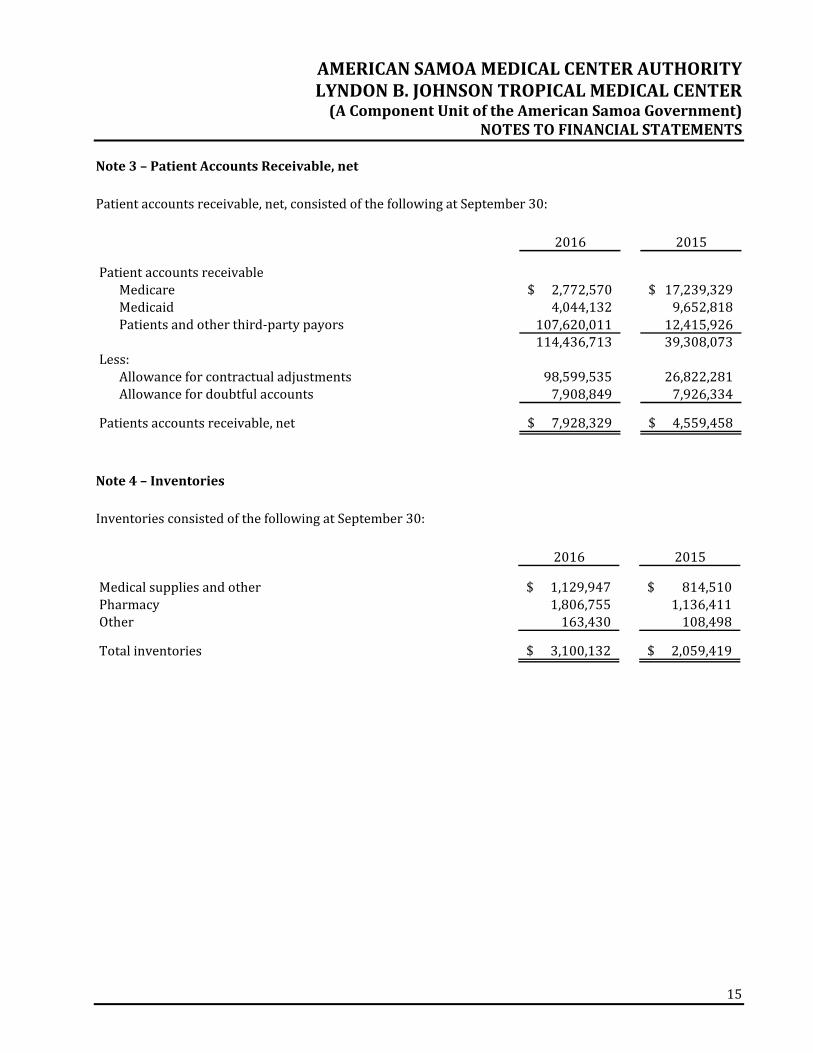

Patientaccountsreceivable–Accountsreceivableareuncollateralizedpatientobligations,mostofwhomarelocalresidentsinsuredunderMedicaidagreements,andarestatedattheamountmanagementexpectsto collect fromoutstandingbalances. LBJbills third‐partypayorson thepatients’behalf, or if apatient isuninsured, the patient is billed directly. Once claims are settled with the primary payor, any secondaryinsurance is billed, and patients are billed for copay and deductible amounts that are the patients’responsibility.Paymentsonpatientaccounts receivableareapplied to the specific claim identifiedon theremittanceadviceorstatement.LBJdoesnothaveapolicytochargeinterestonpastdueaccounts.

Thecarryingamountsofpatientaccountsreceivablearereducedbyallowancesthatreflectmanagement’sbestestimateoftheamountsthatwillnotbecollected.Managementprovidesforcontractualadjustmentsundertermsofthird‐partyreimbursementagreementsthroughareductionofgrossrevenueandacredittopatient receivables. In addition, management provides for probable uncollectible amounts, primarilyuninsuredpatientsandamountspatientsarepersonallyresponsiblefor,throughachargetooperationsandacredittoavaluationallowancebasedonitsassessmentofhistoricalcollectionlikelihoodandthecurrentstatus of individual accounts. Balances that are still outstanding after management has used reasonablecollection efforts are written off through a charge to the provision for bad debt and a credit to patientaccountsreceivable.

Related‐partyreceivable –The related‐party receivable representsanamountowed from theAmericanSamoaGovernment(ASG)asreimbursement forgrant‐relatedexpenses,2%wagetax,andotheramountsdue from ASG. LBJ considers the receivable at September 30, 2016 and 2015 to be fully collectible;accordingly,noallowancefordoubtfulaccountsisrequired.

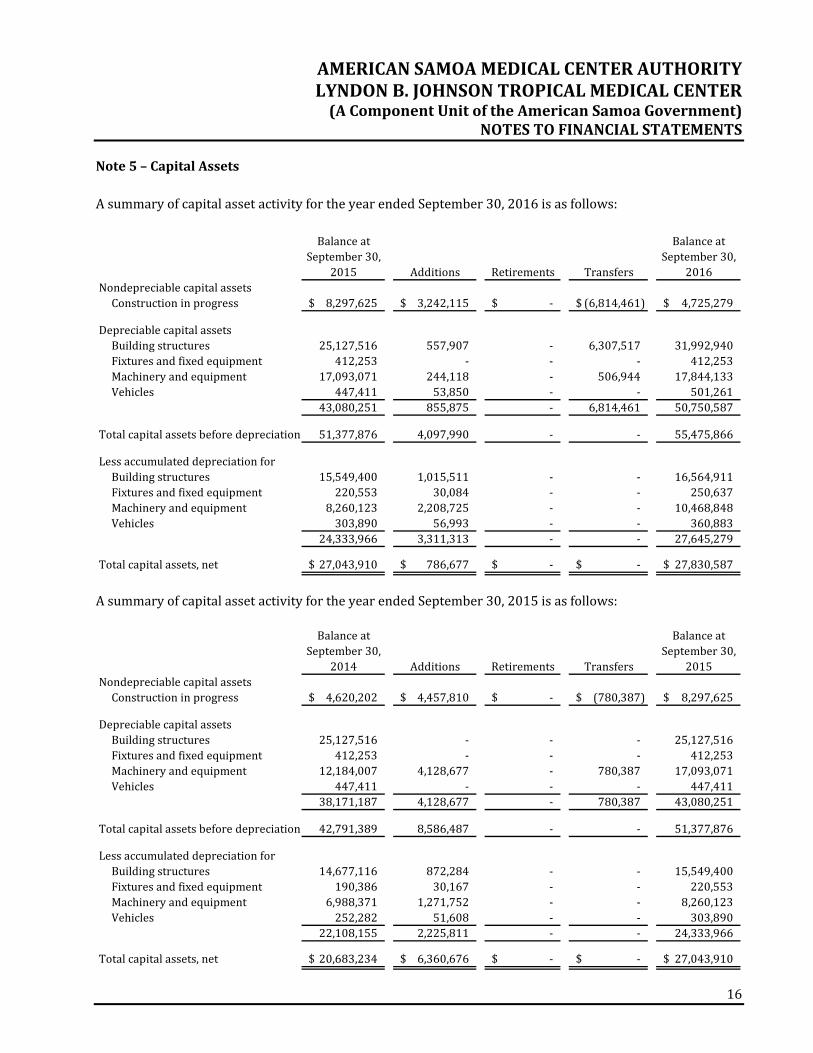

Capital assets are reviewed for impairment when events or changes in circumstances suggest that theservice utility of the capital asset may have significantly and unexpectedly declined. Capital assets areconsidered impaired ifboththedecline inserviceutilityof thecapitalasset is large inmagnitudeandtheeventorchangeincircumstanceisoutsidethenormallifecycleofthecapitalasset.Sucheventsorchangesincircumstancesthatmaybeindicativeof impairmentincludeevidenceofphysicaldamage,enactmentorapproval of laws or regulations or other changes in environmental factors, technological changes orevidence of obsolescence, changes in themanner or duration of use of a capital asset, and constructionstoppage.Thedeterminationoftheimpairmentlossisdependentupontheeventorcircumstanceinwhichthe impairmentoccurred. Impairment losses, if any, are recorded in the statementsof revenue, expenses,andchangesinnetposition.TherewerenoimpairmentlossesrecordedintheyearsendedSeptember30,2016and2015.

Pensions–Forpurposesofmeasuringthenetpensionliability,deferredoutflowsofresourcesandpensionexpense, information about the fiduciary net position of the American Samoa Government Employees’RetirementFund(theFund)andadditionsto/deductionsfromtheFund'sfiduciarynetpositionhavebeendetermined on the same basis as they are reported by the Fund. For this purpose, benefit payments(includingrefundsofemployeecontributions)arerecognizedwhendueandpayableinaccordancewiththebenefitterms.Investmentsarereportedatfairvalue.

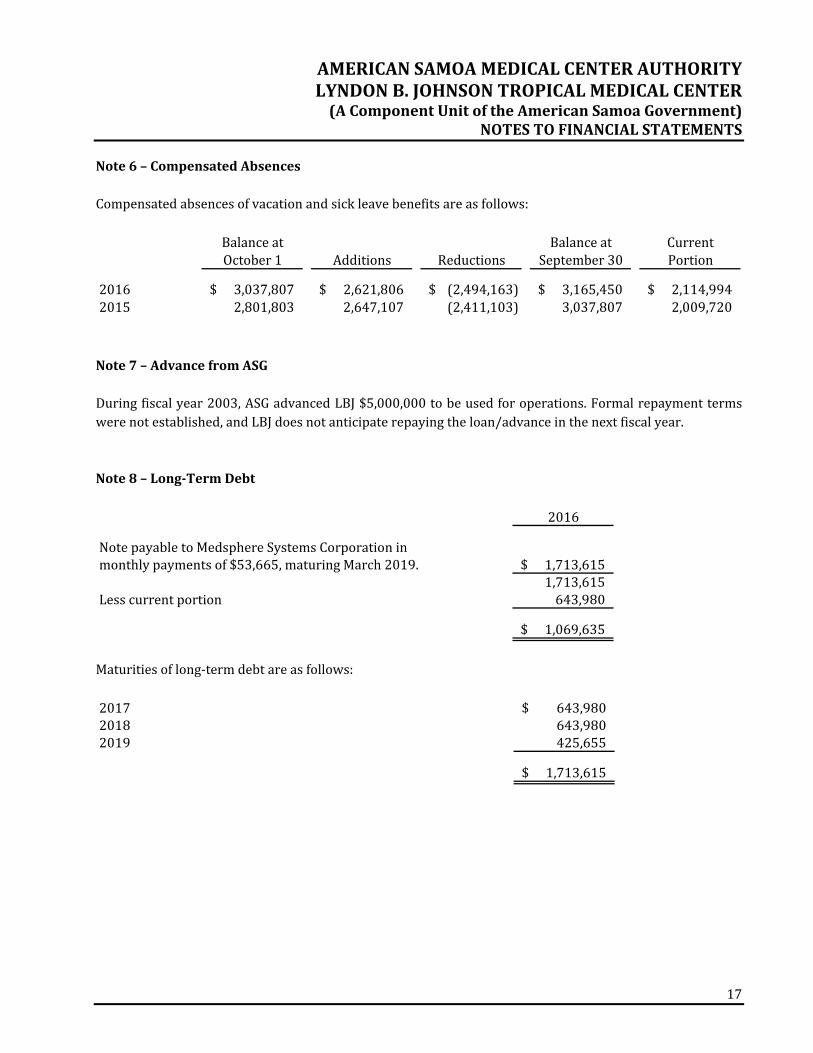

Note2–SummaryofSignificantAccountingPolicies(continued)Compensatedabsences – It is the policy of LBJ to permit employees to accumulate earned but unusedvacationbenefits,whichwillbepaidtotheemployeesuponseparationfromservice.Vacationleaveisfullyvestedwhenearned,butaccumulatedleavecannotexceed60daysatthebeginningofanycalendaryear.Sickleaveisvestedwhenearnedandtheaccumulationisnotlimited.Employeesseparatedfromservicearecompensated forunusedaccruedsick leaveat therateof50percentofsick leave inexcessof239hours.Retiring employees with less than 30 years of service may apply accumulated sick leave for additionalservicecredits.Netpensionliability–NetpensionliabilityhasbeenrecognizedinaccordancewithGASBNo.68andthemost recent Fund actuarial measurement date (see Note 9). The net pension liability is measured as aportionof thepresent valueof projectedbenefits tobeprovided through theFund to current active andinactive employees attributed to those employees’ past periods of service less the Fund’s fiduciary netpositionasofthemeasurementdate.Netpatientservicerevenue–NetpatientservicerevenueandMedicaidreimbursementsarereportedatthe estimated realizable amounts from patients, third‐party payors, and others for services renderedincludingestimatedsettlementsunderreimbursementagreements.TheMedicalCenterhasagreementswiththird‐partypayorsthatprovideforpaymentstotheMedicalCenterat amounts different from its established rates. Payment arrangements include prospectively determinedratesperdischarge,reimbursedcosts,discountedcharges,andperdiempayments.Retroactiveadjustmentsareaccruedonanestimatedbasisintheperiodtheservicesarerenderedandadjustedinfutureperiodsasfinalsettlementsaredetermined.Differencesbetweentheestimatedamountsaccruedandinterimandfinalsettlements are reported in operations in the year of settlement. Estimated third‐party payor settlementamountsincludedintheaccompanyingstatementofnetpositionapproximatefairvalue.Operating revenueandexpenses– LBJ’s statements of revenue, expenses, and changes in net positiondistinguishesbetweenoperatingandnonoperatingrevenueandexpenses.Operatingrevenueresults fromexchange transactions associated with providing health care services – LBJ’s principal activity.Nonexchange revenue, including taxes, grants, and contributions received forpurposesother than capitalasset acquisition, are reported asnonoperating revenue.Operating expenses are all expenses incurred toprovidehealthcareservices.Donated services and goods –A substantial number of volunteers have donated hours to the MedicalCenter'sprogramservicesandfund‐raisingcampaignsduringtheyear;however,thesedonatedservicesarenot reflected in the financial statementssince theservicesdonot requirespecializedskills.Materialsandotherassetsreceivedasdonationsarerecordedandreflectedintheaccompanyingfinancialstatementsattheirfairvaluesatthedateofreceipt.Incometaxes–LBJisacomponentunitoftheASGandisexemptfromfederalincometaxesonoperationsoractivitiesunderSection115oftheInternalRevenueCode.

Note2–SummaryofSignificantAccountingPolicies(continued)Contributions,governmentappropriations,andgrants–Contributions,governmentappropriations,andgrants are considered available for unrestricted use unless specifically restricted by the donor orgovernmentagency.Revenues from contributions, government appropriations, and grants (including contributions of capitalassets) are recognized when all eligibility requirements, including time requirements, are met.Contributions, government appropriations, and grants may be restricted for either specific operatingpurposesorforcapitalpurposes.Fundsthatareunrestrictedorthatarerestrictedtoaspecificpurposearereported as nonoperating revenue. Amounts restricted to capital acquisitions are reported afternonoperatingrevenueandexpenses.Riskmanagement – LBJ is exposed to various risks of loss related to torts; theft of, damage to, anddestructionofassets;errorsandomissions;businessinterruption;employeeinjuriesandillnesses;naturaldisasters;medicalmalpractice;andemployeehealth,dental,andaccidentbenefits.LBJcarriescommercialinsurancefortheserisksofloss.Settledclaimsresultingfromtheseriskshavenotexceededthecommercialinsurancecoverageinanyofthepastthreeyears.Restricted resources –When LBJ has both restricted and unrestricted resources available to finance aparticularprogram,itisLBJ'spolicytouserestrictedresourcesbeforeunrestrictedresources.Deferredoutflowsofresources–Deferredoutflowsofresourcesrepresentconsumptionofnetpositionthatapplies to futureperiodsas theresultofpensionactivityandwillnotberecognizedasanoutflowofresources(expense)untilthosefutureperiods.Reclassification – Certain amounts reported in the September 30, 2015 financial statements have beenreclassifiedtoconformtotheSeptember30,2016financialstatementpresentation.Subsequentevents – Subsequent events are eventsor transactions thatoccurafter the statementof netposition date but before financial statements are available to be issued. LBJ recognizes in the financialstatements the effects of all subsequent events that provide additional evidence about conditions thatexisted at the date of the statement of net position, including the estimates inherent in the process ofpreparing the financial statements. LBJ’s financial statements do not recognize subsequent events thatprovideevidenceaboutconditionsthatdidnotexistatthedateofthestatementofnetpositionbutaroseafterthestatementofnetpositiondateandbeforefinancialstatementsareissued.LBJhasevaluatedsubsequenteventsthroughApril28,2017,whichisthedatethefinancialstatementsareissued,andconcludedthattherewerenoeventsortransactionsthatneedtobedisclosed.

Note9–NetPensionLiabilityandRelatedDeferredOutflowsofResourcesGeneralInformationabouttheDefinedBenefitPensionPlan(ASGEmployees’RetirementFund):Plandescription–TheAmericanSamoaGovernmentEmployees’RetirementFund(theFund),ablendedcomponent unit of the American Samoa Government, is a cost‐sharing, multiple‐employer, contributorydefinedbenefitretirementplanestablishedin1971toprovideretirementbenefitstotheemployeesofthegovernment.LBJisasponsoringemployeroftheplan.Allfull‐timecareerserviceLBJemployeesarecoveredby the Fund. The Fund issues a publicly available comprehensive annual financial report that includesfinancialstatementsandrequiredsupplementaryinformation.Thisreportmaybeobtainedbycontacting:

Aqualifiedjointandsurvivorannuity(actuariallyreduced)Deathbenefits–Asurviving spouseofanactivememberwhodiesbefore retirementbutafter attainingeligibility for retirement may receive either a refund of employee contributions with interest or a lifeannuityequal toone‐half the retirementannuity thatwouldhavebeenpaid to thedeceasedmember.Anadditional lump‐sum death benefit of $2,500 to $10,000, based on years of service, is also payable tosurvivors of activemembers of the Fund. A lump‐sumdeath benefit of $1,500 is payable to survivors ofretiredmembersoftheFund.

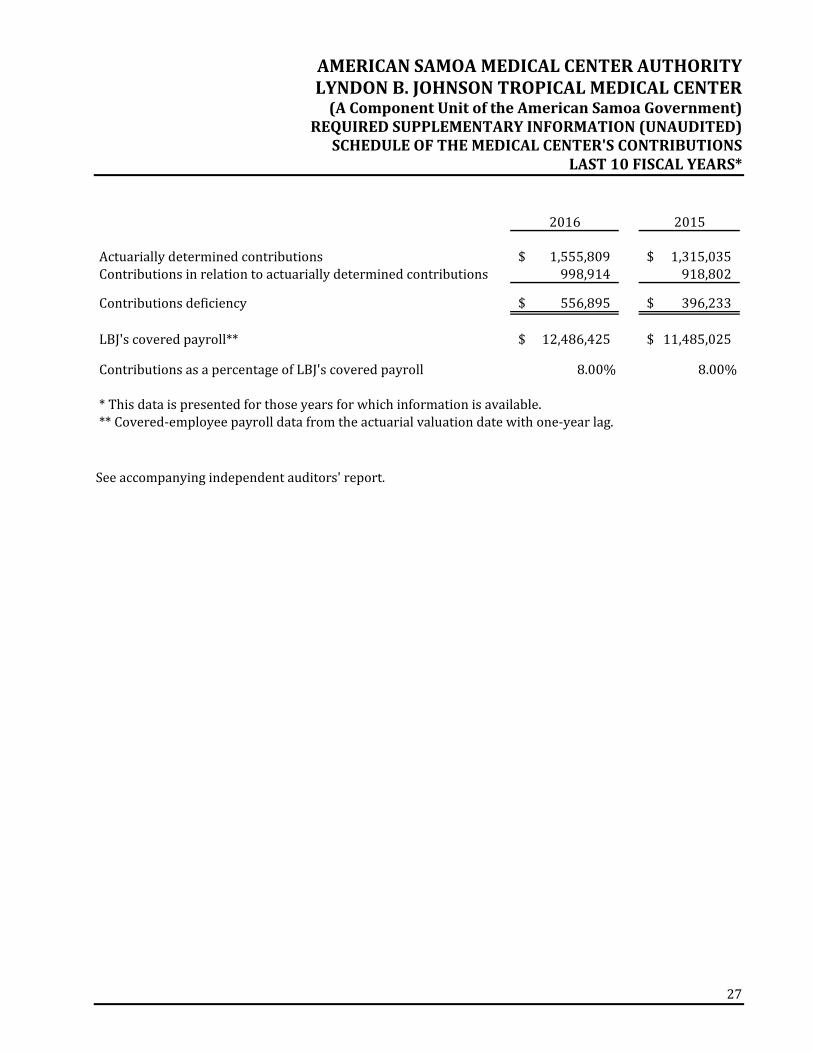

Note9–NetPensionLiabilityandRelatedDeferredOutflowsofResources(continued)Contributions–EachmemberoftheFundcontributes3%ofregularearningsandearnsinterestat1.5%compounded annually. Employee contributions are made through payroll deductions. Employeecontributions and the related interest earned are refunded in full to members whose employment isterminated for any reason other than retirement and as a death benefit to the survivors of deceasedemployeesnotyeteligibleforretirement.Employeesarefullyvestedintheemployerportionaftertenyearsofparticipationinthefund.Anemployercontributionof8%ofemployees’earningsisfundedbyLBJandis includedasanexpenseinthe statements of revenue, expenses, and changes in net position. The contributions are remitted to theretirement office, which administers the retirement fund. Contributions made in the fiscal years endedSeptember 30, 2016 and2015,were $996,046 and $944,216, respectively, andwere equal to the annualrequiredcontributionamounts.PensionLiabilities,PensionExpense,andDeferredOutflowsofResourcesRelatedtoPensions:LBJ adopted GASB No. 68 during the year ended September 30, 2015. These standards establish newfinancial reporting requirements for LBJ’s sponsorship of the Fund and require the Medical Center torecognizeitslong‐termobligationforpensionbenefitsandmorecomprehensivelymeasuretheannualcostofpensionbenefitsforitsemployees.AtSeptember30,2016,LBJreportedanetpensionliabilityof$26,341,853foritsproportionateshareoftheFund’snetpensionliability.ThenetpensionliabilitywasmeasuredasofSeptember30,2015,andthetotalpension liabilityused tocalculate thenetpension liabilitywasdeterminedbyanactuarialvaluationasofOctober1,2014androlledforwardtotheSeptember30,2015measurementdate.LBJ'sproportionofthenetpension liabilitywasbasedonLBJ’s shareof contributions to theFund for fiscalyear2015.Asof themeasurementdateofSeptember30,2015,LBJ’sproportionwas12.46%,whichwasanincreaseof0.76%fromitsproportionmeasuredasofOctober1,2014.

Note9–NetPensionLiabilityandRelatedDeferredOutflowsofResources(continued)For the year ended September30, 2016, LBJ recognized pension expense totaling $2,003,846. AtSeptember30, 2016, LBJ reported deferred outflows of resources related to pensions from the followingsources:

LBJ’s employer contributions related to fiscal year 2016 have been reported as deferred outflows ofresources and will be recognized as a reduction of the net pension liability in fiscal year 2017. Otheramounts reported as deferred outflows of resources related to pensions will be recognized in pensionexpenseasfollows:

Mortality RP‐2000CombinedMortalityTablesetforwardsixyearsActuarialvaluationsofanongoingplaninvolveestimatesofthevalueofprojectedbenefitsandassumptionsabouttheprobabilityofeventsfarintothefuture.Actuariallydeterminedamountsaresubjecttocontinualrevisionasactualresultsarecomparedtopastexpectationsandnewestimatesaremadeaboutthefuture.Themethodsandassumptionsshownabovearebasedonanexperiencestudyconductedforthefive‐yearperiodendedSeptember30,2013.Long‐termexpectedrateofreturn–Thelong‐termexpectedrateofreturnontheFund’sinvestmentswasdeterminedusing a building‐blockmethod inwhichbest‐estimate ranges of expected future real rates ofreturn (expected returns, net of investment fees and inflation) are developed for eachmajor asset class.These ranges are combined to produce the long‐term expected rate of return byweighting the expectedfuturerealratesofreturnbythetargetassetallocationpercentageandbyaddingexpectedinflation.AsofSeptember30,2015,measurementdate, thegeometricmeanratesofreturnofbenchmarksforeachmajorinvestmentclassintheFund’sportfolioareasfollows:

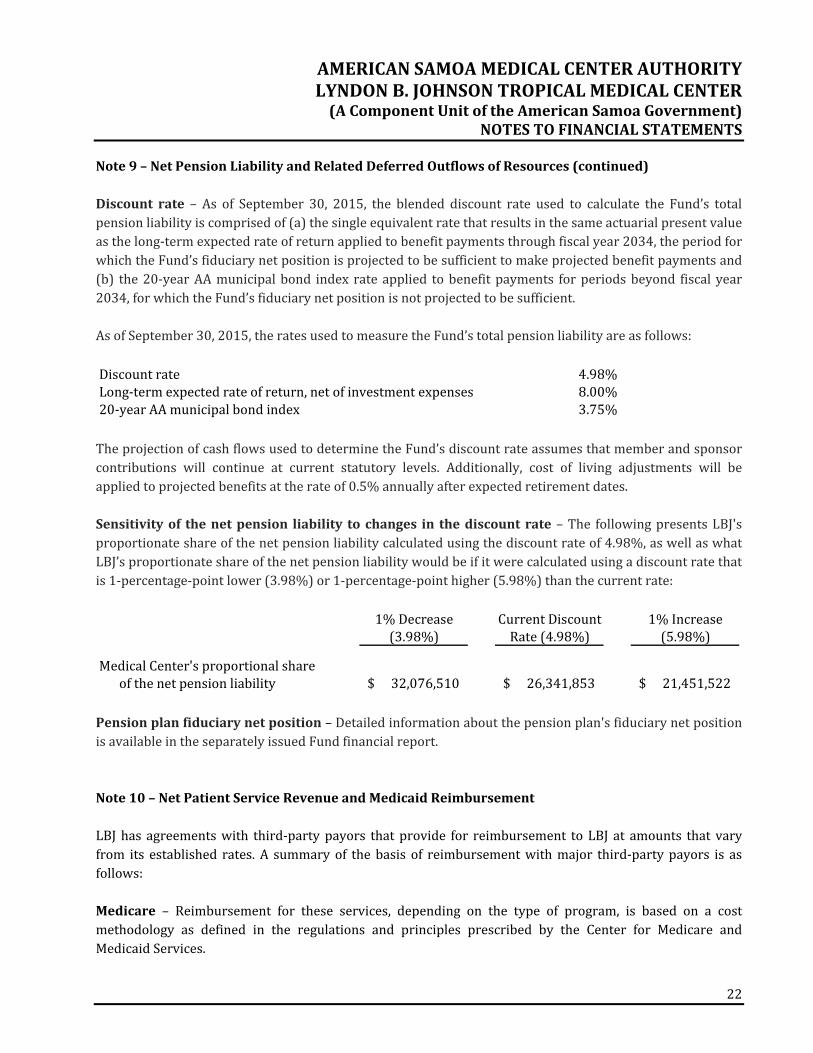

Note9–NetPensionLiabilityandRelatedDeferredOutflowsofResources(continued)Discount rate – As of September 30, 2015, the blended discount rate used to calculate the Fund’s totalpensionliabilityiscomprisedof(a)thesingleequivalentratethatresultsinthesameactuarialpresentvalueasthelong‐termexpectedrateofreturnappliedtobenefitpaymentsthroughfiscalyear2034,theperiodforwhichtheFund’sfiduciarynetpositionisprojectedtobesufficienttomakeprojectedbenefitpaymentsand(b) the20‐yearAAmunicipalbond index rate applied tobenefitpayments forperiodsbeyond fiscal year2034,forwhichtheFund’sfiduciarynetpositionisnotprojectedtobesufficient.AsofSeptember30,2015,theratesusedtomeasuretheFund’stotalpensionliabilityareasfollows:Discountrate 4.98%Long‐termexpectedrateofreturn,netofinvestmentexpenses 8.00%20‐yearAAmunicipalbondindex 3.75% TheprojectionofcashflowsusedtodeterminetheFund’sdiscountrateassumesthatmemberandsponsorcontributions will continue at current statutory levels. Additionally, cost of living adjustments will beappliedtoprojectedbenefitsattherateof0.5%annuallyafterexpectedretirementdates.Sensitivityof thenetpension liability tochanges in thediscountrate –The followingpresentsLBJ'sproportionateshareofthenetpensionliabilitycalculatedusingthediscountrateof4.98%,aswellaswhatLBJ’sproportionateshareofthenetpensionliabilitywouldbeifitwerecalculatedusingadiscountratethatis1‐percentage‐pointlower(3.98%)or1‐percentage‐pointhigher(5.98%)thanthecurrentrate:

Pensionplanfiduciarynetposition–Detailedinformationaboutthepensionplan'sfiduciarynetpositionisavailableintheseparatelyissuedFundfinancialreport.Note10–NetPatientServiceRevenueandMedicaidReimbursementLBJhas agreementswith third‐partypayors thatprovide for reimbursement toLBJ at amounts that varyfrom its established rates.A summaryof thebasis of reimbursementwithmajor third‐partypayors is asfollows:Medicare – Reimbursement for these services, depending on the type of program, is based on a costmethodology as defined in the regulations and principles prescribed by the Center for Medicare andMedicaidServices.

Note10–NetPatientServiceRevenueandMedicaidReimbursement(continued)Medicaid – Services provided to Medicaid program beneficiaries are reimbursed under a costreimbursement methodology. Reimbursement is determined prospectively based on the ratio of LBJ’saggregatecosttoaggregatecharges.Revenue from the Medicare and Medicaid programs accounted for approximately 42% and 47%,respectively, of the Medical Center’s patient revenue for the year ended September30, 2016, andapproximately 25% and 58%, respectively, of the Medical Center's patient revenue for the year endedSeptember30,2015.Lawsandregulationsgoverning theMedicareandMedicaidprogramsareextremelycomplex and subject to interpretation.As a result, there is at least a reasonablepossibility that recordedestimateswillchangebyamaterialamountinthenearterm.Other–LBJhasalsoenteredintopaymentagreementswithcertaincommercialinsurancecarriers,healthmaintenance organizations, and preferred provider organizations. The basis for payment under theseagreementsincludesprospectivelydeterminedratesperdischarge,discountsfromestablishedcharges,andprospectivelydetermineddailyrates.NetpatientservicerevenueconsistedofthefollowingfortheyearsendedSeptember30:

Accountingforcontractualarrangements–LBJisreimbursedforcertaincost‐reimbursableitemsataninterim rate, and final settlements are determined after audit of LBJ’s related annual cost reports by therespective Medicare and Medicaid fiscal intermediaries. Estimated provisions to approximate the finalexpected settlements after review by the intermediaries are included in the accompanying financialstatements. LBJ’s cost reports have been audited by the Medicare fiscal intermediaries throughSeptember30,2014.Medicaid reimbursement – American Samoa uses a concept of presumptive eligibility, which does notinvolve individual eligibility determination based on personal income and citizenship status. Rather, byutilizingvariouscensusdata,andmakingcertainadjustmentsfor illegalandnonresidentaliens,AmericanSamoawillannuallyestimatethenumberofindividualsandthepercentageofthepopulationthatfallbelowtherespectiveincomethresholdsforMedicaid,CHIP,andAmericanSamoa’sEnhancedAllotmentPlan(EAP)for Medicare prescription drug coverage. These percentages are further utilized to calculate respectiveclaiming percentages for Medicaid, CHIP, and EAP eligible costs incurred at LBJ, American Samoa’s onlyMedicaidprovider.LBJ receivesamonthlypayment fromMedicaidbasedon the resultsof thesemonthlycalculations.

Note11–CharityCareAlthoughtheMedicalCenterhasnoformalpolicies,itprovidescaretopatientswholackfinancialresources,someofwhommeettherequirementstobeconsideredindigentbylocalgovernmentprograms.TheMedicalCenter also provides charity care to patients through its Financial Assistance Program. Residents ofAmericanSamoaqualifyforvaryinglevelsofdiscountsbasedontheirincomequalificationsandnumberoffamily members. Sliding fee scale discounts are established using the Federal Poverty Guidelines. Suchprograms pay amounts that are less than the cost of the services provided to the recipients. Totaluncompensatedcare,includingcharitycareandgovernmentalindigentcareprograms,totaled$11,838,243and$7,628,196in2016and2015,respectively.Note12–RiskManagementLegalproceedings–LBJdoesnotmaintainprofessional liability insurancecoverage.PerASGstatute,LBJcannotbesued.Allclaimsand legalactionsarebroughtsolelyagainstASG.Therefore, it is theopinionofmanagement,andconfirmedthroughtheASGAttorneyGeneral’soffice,thattheultimatedispositionofthesematterswillnothaveamaterialadverseeffectonLBJ'sfinancialposition,resultsofoperations,orliquidity.Insurance – LBJ records a liability for risk financing and insurance related to property losses if it isdetermined that a loss has been incurred and the amount can be reasonably estimated and is less than$25,000.For fiscalyears2016and2015, thereareno liabilities for risk financingor insurance related topropertylosses.Alllossesinexcessof$25,000aretheresponsibilityofASG.Contingent liabilities – LBJ is the recipient of various federal grants and, as such, is subject to audits ofthesegrants that could result indisallowanceofgrantexpenditures.LBJ isunawareofanydisallowancesandexpectssuchamounts,ifany,tobeimmaterial.Lawsandregulations–Thehealthcareindustryissubjecttonumerouslawsandregulationsoffederalandlocalgovernments.These lawsandregulations include,butarenotnecessarily limitedto,matterssuchaslicensure, accreditation, government health care program participation requirements, reimbursement forpatientservices,andbillingregulations.Governmentactivitywithrespecttoinvestigationsandallegationsconcerningpossibleviolationsofsuchregulationsbyhealthcareprovidershasincreased.Violationsoftheselaws and regulations could result in expulsion from government health care programs togetherwith theimpositionofsignificantfinesandpenalties,aswellassignificantrepaymentsforpatientservicespreviouslybilled. Management believes that LBJ is in substantial compliance with applicable government laws andregulations.WhilenosignificantregulatoryinquirieshavebeenmadeofLBJ,compliancewithsuchlawsandregulationscanbe subject to futuregovernment reviewand interpretations, aswell as regulatoryactionsunknownorunassertedatthistime.

Note13–ConcentrationofCreditRiskFinancial instruments that potentially subject LBJ to credit risk consist principally of accounts receivableandcashdepositsinexcessofinsuredlimitsinfinancialinstitutions.Accounts receivable consists of amounts due from patients, their insurers, or governmental agencies(primarilyMedicareandMedicaid)forhealthcareprovidedtothepatients.The Medical Center grants credit without collateral to its patients, most of whom are local residents.Managementbelievesthatestimatesmadefortheallowancefordoubtfulaccountsareadequate.Becauseofthe uncertainty regarding the ultimate collectability of patient accounts receivable, there is at least areasonable possibility that recorded estimates of the allowance for doubtful accounts will change by amaterialamountinthenearterm.Themixofreceivablesfrompatientsandthird‐partypayorswasasfollowsatSeptember30:

Note14–WageTaxRevenueDuring2012,theLegislativebody(“Fono”)establishedPublicLawNo.32.6,anactincreasingtherevenuesof the American Samoa Government and the Medical Center by instituting a 2% wage tax on all wagesearnedintheTerritory.AccordingtoPublicLawNo.32.6,Section1(e),theTreasurycollectstherevenuegeneratedfromthiswagetaxandaccumulatedproceedswerefirstusedtorepaya$3,000,000loanfromtheASGWorkersCompensation fund. Following repayment of the loan, the accumulatedproceeds of the2%wagetaxarethentobetransferredtotheMedicalCenterasfollows:50%totheMedicalCenteroperationand50%toaspecialaccountusedtosupporttheOff‐IslandMedicalReferralProgram.FortheyearsendedSeptember30,2016and2015,revenuescollectedunderthe2%wagetaxwere$4,760,000and$5,906,422,respectively,andarerecordedaswagetaxrevenueonthestatementofrevenues,expenses,andchangesinnetposition.AmountsduetotheMedicalCenterasofSeptember30,2016and2015totaled$5,826,402and$7,349,601,respectively,andareincludedinrelated‐partyreceivablesonthestatementofnetposition.Note15–CommitmentsandContingenciesCommitments – TheMedical Center has signed contracts that have committed it to construction cost ofapproximately$3,678,000.

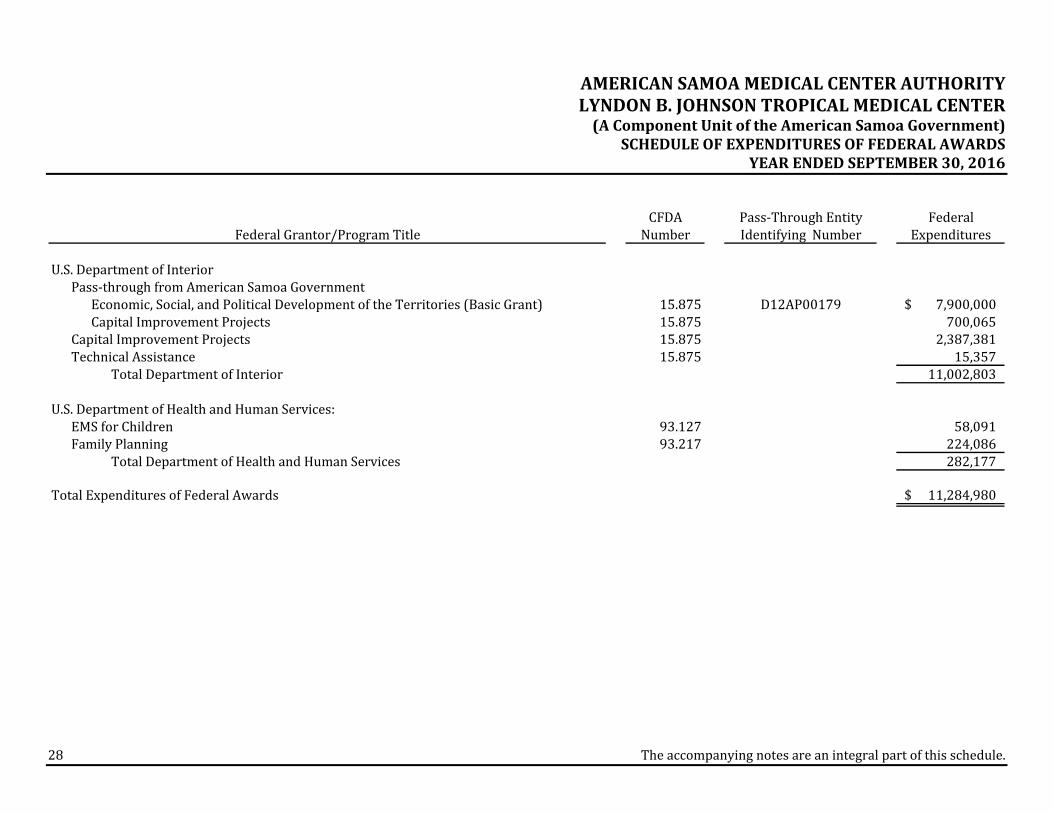

Note1–BasisofPresentationTheaccompanyingscheduleofexpendituresoffederalawards(the"Schedule")includesthefederalawardactivity of American Samoa Medical Center Authority Lyndon B. Johnson Tropical Medical Center underprograms of the federal government for the year ended September30, 2016. The information in thisScheduleispresentedinaccordancewiththerequirementsofTitle2,U.S.CodeofFederalRegulations(CFR)Part200,UniformAdministrativeRequirements,CostPrinciples,andAuditRequirements forFederalAwards(UniformGuidance).Because theSchedulepresentsonlyaselectedportionof theoperationsofAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenter,itisnotintendedtoanddoesnotpresentthefinancialposition,changesinnetposition,orcashflowsofAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenter.Note2–SummaryofSignificantAccountingPoliciesExpendituresreportedontheSchedulearereportedontheaccrualbasisofaccounting.SuchexpendituresarerecognizedfollowingthecostprinciplescontainedinOMBCircularA‐87,CostPrinciplesforState,Local,andIndianTribalGovernments,andTitle2U.S.CodeofFederalRegulationsPart200,UniformAdministrativeRequirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), whereincertain types of expenditures are not allowable or are limited as to reimbursement. Pass‐through entityidentifyingnumbers are presentedwhere available.AmericanSamoaMedical CenterAuthorityLyndonB.Johnson TropicalMedical Center elected to not use the 10‐percent deminimis indirect cost rate allowedundertheUniformGuidance.

PERFORMEDINACCORDANCEWITHGOVERNMENTAUDITINGSTANDARDSTheBoardofDirectorsAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenterPagoPago,AmericanSamoaWehaveaudited,inaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmericaandthestandardsapplicabletofinancialauditscontainedinGovernmentAuditingStandards issuedbytheComptroller General of the United States, the financial statements of American Samoa Medical CenterAuthority Lyndon B. Johnson Tropical Medical Center (LBJ or Medical Center), a component unit of theAmericanSamoaGovernment,asofandfortheyearendedSeptember30,2016,andtherelatednotestothefinancialstatements,whichcollectivelycomprisetheMedicalCenter’sbasicfinancialstatements,andhaveissuedourreportthereondatedApril28,2017.Inourreportonthefinancialstatements,ourauditopinionwasmodifiedbecause,asdescribedinthe“Basisfor Qualified Opinion” paragraph, we were unable to obtain audit evidence to support patient accountsreceivableandnetpatientservicerevenueasofandfortheyearendedSeptember30,2016.InternalControlOverFinancialReportingIn planning and performing our audit of the financial statements, we considered the Medical Center’sinternal control over financial reporting (internal control) to determine the audit procedures that areappropriateinthecircumstancesforthepurposeofexpressingouropiniononthefinancialstatements,butnot for thepurposeofexpressinganopinionon theeffectivenessof theMedicalCenter’s internalcontrol.Accordingly,wedonotexpressanopinionontheeffectivenessoftheMedicalCenter’sinternalcontrol.Ourconsiderationofinternalcontrolwasforthelimitedpurposedescribedintheprecedingparagraphandwas not designed to identify all deficiencies in internal control that might be material weaknesses orsignificantdeficienciesand, therefore,materialweaknessesorsignificantdeficienciesmayexist thatwerenot identified.However, asdescribed in the accompanying scheduleof findings andquestioned costs,weidentifiedcertaindeficienciesininternalcontrolthatweconsidertobematerialweaknessesandsignificantdeficiencies.

31

Adeficiencyininternalcontrolexistswhenthedesignoroperationofacontroldoesnotallowmanagementoremployees,inthenormalcourseofperformingtheirassignedfunctions,toprevent,ordetectandcorrect,misstatements on a timely basis. Amaterialweakness is a deficiency, or a combination of deficiencies, ininternal control such that there is a reasonable possibility that a material misstatement of the entity'sfinancial statementswillnotbeprevented, ordetected and corrected, on a timelybasis.We consider thedeficienciesdescribed in theaccompanyingscheduleof findingsandquestionedcostsas items2014‐003,2014‐004,2014‐005,and2014‐006tobematerialweaknesses.Asignificantdeficiencyisadeficiency,oracombinationofdeficiencies,ininternalcontrolthatislessseverethanamaterialweakness,yetimportantenoughtomeritattentionbythosechargedwithgovernance.Weconsiderthedeficienciesdescribedintheaccompanyingscheduleoffindingsandquestionedcostsasitems2014‐001,2014‐002,and2015‐002tobesignificantdeficiencies.ComplianceandOtherMattersAspartofobtainingreasonableassuranceaboutwhethertheMedicalCenter’sfinancialstatementsarefreefrom material misstatement, we performed tests of its compliance with certain provisions of laws,regulations, contracts,andgrantagreements,noncompliancewithwhichcouldhaveadirectandmaterialeffectonthedeterminationoffinancialstatementamounts.However,providinganopiniononcompliancewiththoseprovisionswasnotanobjectiveofouraudit,andaccordingly,wedonotexpresssuchanopinion.Theresultsofour testsdisclosedno instancesofnoncomplianceorothermatters thatare required tobereportedunderGovernmentAuditingStandards.TheMedicalCenter’sResponsetoFindingsTheMedicalCenter’s responses to the findings identified inouraudit aredescribed in theaccompanyingschedule of findings and questioned costs. The Medical Center’s responses were not subjected to theauditingproceduresappliedintheauditofthefinancialstatementsand,accordingly,weexpressnoopiniononthem.PurposeofthisReportThepurposeofthisreportissolelytodescribethescopeofourtestingofinternalcontrolandcomplianceand the result of that testing, and not to provide an opinion on the effectiveness of theMedical Center’sinternalcontroloroncompliance.ThisreportisanintegralpartofanauditperformedinaccordancewithGovernment Auditing Standards in considering the Medical Center’s internal control and compliance.Accordingly,thiscommunicationisnotsuitableforanyotherpurpose.

REQUIREDBYTHEUNIFORMGUIDANCETheBoardofDirectorsAmericanSamoaMedicalCenterAuthorityLyndonB.JohnsonTropicalMedicalCenterPagoPago,AmericanSamoaReportonCompliancefortheMajorFederalProgramWehave auditedAmericanSamoaMedical CenterAuthorityLyndonB. JohnsonTropicalMedical Center’s(LBJorMedicalCenter),acomponentunitoftheAmericanSamoaGovernment,compliancewiththetypesofcompliance requirements described in the OMB Compliance Supplement that could have a direct andmaterialeffectontheMedicalCenter'smajorfederalprogramfortheyearendedSeptember30,2016.TheMedical Center's major federal program is identified in the summary of auditor's results section of theaccompanyingscheduleoffindingsandquestionedcosts.Management’sResponsibilityManagementisresponsibleforcompliancewithfederalstatutes,regulations,andthetermsandconditionsofitsfederalawardapplicabletoitsfederalprogram.Auditor’sResponsibilityOurresponsibility is toexpressanopiniononcompliance for theMedicalCenter’smajor federalprogrambasedonourauditof thetypesofcompliancerequirementsreferredtoabove.Weconductedourauditofcompliance inaccordancewithauditingstandardsgenerallyaccepted intheUnitedStatesofAmerica; thestandards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States; and the audit requirements of Title 2, U.S. Code of FederalRegulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements forFederalAwards(UniformGuidance).ThosestandardsandtheUniformGuidancerequirethatweplanandperform the audit to obtain reasonable assurance about whether noncompliance with the types ofcompliancerequirementsreferredtoabovethatcouldhaveadirectandmaterialeffectonamajorfederalprogram occurred. An audit includes examining, on a test basis, evidence about the Medical Center’scompliancewiththoserequirementsandperformingsuchotherproceduresasweconsiderednecessaryinthecircumstances.Webelievethatourauditprovidesareasonablebasisforouropiniononcomplianceforthemajorfederalprogram.However,ourauditdoesnotprovidealegaldeterminationoftheMedicalCenter'scompliance.

33

OpinionontheMajorFederalProgramIn our opinion, the Medical Center complied, in all material respects, with the types of compliancerequirementsreferredtoabovethatcouldhaveadirectandmaterialeffectonthemajorfederalprogramfortheyearendedSeptember30,2016.ReportonInternalControlOverComplianceManagementoftheMedicalCenterisresponsibleforestablishingandmaintainingeffectiveinternalcontrolovercompliancewiththetypesofcompliancerequirementsreferredtoabove.Inplanningandperformingourauditofcompliance,weconsideredtheMedicalCenter'sinternalcontrolovercompliancewiththetypesofrequirementsthatcouldhaveadirectandmaterialeffectonthemajorfederalprogramtodeterminetheauditingproceduresthatareappropriateinthecircumstancesforthepurposeofexpressinganopiniononcompliance for themajor federal program and to test and report on internal control over compliance inaccordancewiththeUniformGuidance,butnotforthepurposeofexpressinganopinionontheeffectivenessof internalcontrolovercompliance.Accordingly,wedonotexpressanopinionontheeffectivenessoftheMedicalCenter'sinternalcontrolovercompliance.A deficiency in internal control over compliance exists when the design or operation of a control overcompliancedoesnotallowmanagementoremployees, in thenormal courseofperforming theirassignedfunctions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of afederalprogramonatimelybasis.Amaterialweaknessininternalcontrolovercomplianceisadeficiency,orcombinationofdeficiencies,ininternalcontrolovercompliance,suchthatthereisareasonablepossibilitythat material noncompliance with a type of compliance requirement of a federal program will not beprevented, or detected and corrected, on a timely basis. A significant deficiency in internal control overcomplianceisadeficiency,oracombinationofdeficiencies,ininternalcontrolovercompliancewithatypeof compliance requirement of a federal program that is less severe than amaterialweakness in internalcontrolovercompliance,yetimportantenoughtomeritattentionbythosechargedwithgovernance.

Our consideration of internal control over compliancewas for the limited purpose described in the firstparagraph of this section and was not designed to identify all deficiencies in internal control overcompliance that might be material weaknesses or significant deficiencies and, therefore, materialweaknessesorsignificantdeficienciesmayexistthatwerenotidentified.Weidentifiedcertaindeficienciesininternalcontrolovercompliance,asdescribedintheaccompanyingscheduleoffindingsandquestionedcostsasitems2014‐008and2015‐001thatweconsidertobematerialweaknesses.TheMedicalCenter'sresponsestotheinternalcontrolovercompliancefindingsidentifiedinourauditaredescribedintheaccompanyingscheduleof findingsandquestionedcosts.TheMedicalCenter'sresponseswere not subjected to the auditing procedures applied in the audit of compliance and, accordingly, weexpressnoopinionontheresponses.ThepurposeofthisreportoninternalcontrolovercomplianceissolelytodescribethescopeofourtestingofinternalcontrolovercomplianceandtheresultsofthattestingbasedontherequirementsoftheUniformGuidance.Accordingly,thisreportisnotsuitableforanyotherpurpose.

SectionII–FinancialStatementFindings2014‐001–PreparationofFinancialStatements–SignificantDeficiencyinInternalControlsCriteria –Good internal control over the financial closing process requires that theMedical Center haveadequatelydesignedinternalcontrolsoverthepreparationofthefinancialstatementsbeingaudited.Condition/Context – Currently, the Medical Center does not have personnel with the training and/orexperiencenecessary todraft the financial statements inaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.Cause/Effect–Withoutthefinancialstatementdraftingtrainingand/orexpertise,thereisanincreasedriskofmaterialmisstatementsoromissionsinthefinancialstatements.Recommendation–WerecommendtheBoardofDirectorsandexecutiveteamreviewthecurrentsituationtodeterminethepropercourseofaction.ManagementResponse–Weconcurwiththisfinding.AmericanSamoaMedicalCenterAuthority(ASMCA)isworking on this corrective action plan by sourcing an outside consultant towork directlywith the staffeverymonthon thepreparationofall thestatementswith theappropriate footnotesrequiredandwithingenerally accepted accounting principles. Additionally, there is a new financial system implementationcoming to ASMCA that is currently in process that will also help support this corrective action inprogrammingthese financialstatementsasset templates for the financestaff tobetterpreparethem.ThetimelinetocompletethiscorrectiveplanwillbeSeptember2017.2014‐002–PoliciesandProcedures–SignificantDeficiencyinInternalControlsCriteria – A good internal control system has a clear written set of policies and procedures, which arereviewed and updated on a regular basis by appropriate personnel. Accounting functions rely on properpolicies and procedures to ensure accurate and timely accounting and to define appropriate internalcontrolsandsegregationofduties.Condition/Context–Whileperformingourinternalcontroltesting,wenotedseveraloftheMedicalCenter’spolicies and procedures had not been updated for several years. However, we noted progress had beenmadeduringthefiscalyearendedSeptember30,2016.Cause/Effect–Awell‐devised set of documentation for critical financial processes canhelp to prevent orreducemisunderstandings,errors,duplicatedoromittedprocedures,andothersituationsthatcanresultininaccurateoruntimelyaccountingrecords.Thatdocumentationcanalsoensurethatsimilartransactionsaretreatedconsistently,thataccountingprinciplesusedareproper,andthatrecordsareproducedintheformdesiredbymanagement.

Recommendation – We recommend the Medical Center update or create new policy and proceduredocumentsthatdelineateresponsibilitiesandlimitationstoreducefinancialerrorsand/orfraud.ManagementResponse–Weconcurwith this finding.ASMCA’splanof correction is tocreatepoliciesandprocedures that will address the deficiency in internal controls. The timeline in which to complete thiscorrectiveactionwillbebySeptember2017.2014‐003– InformationTechnology,PatientRevenues,andAccountsReceivableLedger–MaterialWeaknessinInternalControlsCriteria – Management should continue to work with their billing software vendor to provide accuratedetailedreportsofpatientrevenueandindividualpatientaccounts.Also,theaccountsreceivablebypayorreportbalanceshouldreconciletothepatientdetailbalanceinallinstances.Condition/Context – The Medical Center was historically unable to obtain accurate patient revenue andaccountsreceivablereportsasofyear‐end.Cause/Effect – The Medical Center’s computer system was an extremely antiquated DOS system, noupgradeswereavailable,andvendorsupportstrugglestoproducereportsthatprovidecorrect,satisfactory,andrequiredinformationtomeettheMedicalCenter’sinternalneedsaswellasthoseofexternalreportingagencies. The billing system was separate from the general ledger accounting system requiring manualjournalentriesinsteadofbeingintegrated.Thesoftwaredoesnotallowfortrackingandmonitoringunbilledaccountsreceivable.Reportsprovidedbythethreesystemsmaynotbeprovidingaccurateinformation,andtheMedicalCenter’sfinancialstatementsmaybemateriallymisstated.TheMedicalCenterpurchasedanewcomputersystemduringthefiscalyear;however,ithasnotbeenfullyimplementedwiththegeneralledgerasofSeptember30,2017.Recommendation–WerecommendtheMedicalCentercontinueworkingonimplementingthenewsystemto ensure accurate financial statement reporting, and meet the Federal Electronic Health Recordrequirements.Management Response – We concur with this finding. A new system of electronic health record wasimplementedinJune2015.Withinthissystem,therearetwosub‐systemsthatworktogethertocapturetheclinical and financialdocumentation.The correctiveactionplan is to reconcile the sub ledger in accountsreceivabletothegeneralledger.Withinthenewlyimplementedsystem,thefinancialcomponenthasnotyetbeeninterfacedtothegeneralledgerasofthisaudit.ASMCAiscurrentlyworkingdiligentlyonitandwillbeundergoing a new financial system implementation in fiscal year 2017 which will complete the linkagenecessarytoreconcilethesubledgeraccountsreceivabletothegeneralledger.Thecompletiondatewillbebeyondthenextfiscalyearaudittoincludeayearofoperatingexperiencepostthisimplementation.

2014‐004–InformationTechnology–MaterialWeaknessinInternalControlsCriteria–Toensureproperreporting,anintegratedcomputersystemshouldproduceaccuratereportswithsufficient detail to complywithMedicare reporting requirements, and produce accurate inventory detailreports.Condition/Context –While performing internal control testing, we noted that the accounting system isoutdatedandnot integrated.Thisresults ina largeamountofmanualentries,aswellassome inaccurateand/or inaccessiblereports.TheMedicalCenterpurchasedanewcomputersystemduringthefiscalyear;however,ithasnotbeenfullyimplementedwiththegeneralledgerasofSeptember30,2016.Cause/Effect –Material misstatements could occur without being noticed, and inappropriate accountingtransactionscouldbeconcealedinthefinancialrecords.Recommendation –We recommend theMedical Center continue updating its current accounting systemsandcontinueworkingonimplementingthenewcomputersystem.ManagementResponse–Weconcurwiththisfinding.ASMCAhasthreenon‐integratedsystemsforpatientbilling,pharmacyinventory,andsupply inventory.Withthenewelectronichealthrecordsystemthatwasimplemented in June 2015, where the clinical documentation is now operational and the financialcomponent is pending linkage to our soon to be interfaced, Financial Edge System, that will roll out inSeptember 2017. ASMCA is working on this corrective action. The completion time will be the same asfinding2014‐003.2014‐005 – Segregation of Duties and Other Internal Control Findings – MaterialWeakness inInternalControlsCriteria–Internalcontrolsaredesignedtosafeguardassetsanddetectlossesfromemployeedishonestyorerror.Afundamentalconceptinagoodsystemofinternalcontrolisthesegregationofduties:inparticular,segregatingaccess,custody,andauthorizationoftransactions.Condition/Context – While performing our internal control testing, internal control deficiencies wereidentifiedasfollows:CashReceiptsforOff‐IslandReferrals

Payroll checks are produced without an authorizing signature other than a computer‐generatedsignatureandtherearenocontrolsoverthisprintertechnology,whichwouldallowanypersonwithaccesstothepayrollsystemtoproduceandsignchecks.

CashReceipts

One employee opens themail, collects any checks received, and takes themoney to the bank fordeposit.Noindependentreviewofthecashreceivedinthemailisdonetoensurewhatwasreceivedwasdepositedatthebank.

AccountsPayable

There is no indication of a supervisory review of monthly accounts payable subsidiaryreconciliations.

Cause/Effect –Adequate policies and procedures have not been developed or implemented to guaranteeappropriateinternalcontrolsandsegregationofduties.Anemployeeorgroupcouldbeinapositiontobothperpetrateandconcealerrorsorfraudinthenormalcourseoftheirduties,andtheseerrorsorfraudmayremainundetected.Recommendation–Werecommendmanagementdevelopandimplementpoliciesandprocedurestoaddressthe internalcontroldeficienciesthatwouldincreasethe likelihoodthatunauthorizedorfalsetransactionswillbepreventedordetectedinatimelymannerandpreventmateriallymisstatedfinancialstatements.ManagementResponse–Weconcurwith this finding.Progress isbeingmadeand thecorrectiveplanwilladdress these material weaknesses in internal control by the implementation of the financial system,FinancialEdge,whichwillbe inSeptember2017.Thecompletionof thisplanwillbe thesameas finding2014‐003.

2014‐006–InformationTechnologyPharmacy–MaterialWeaknessinInternalControlsCriteria–Toensureproper reporting, an integratedpharmacy computer systemshouldprovideaccuratereportswithsufficientinventorydetail.Condition/Context–Whileperformingour internalcontroltesting,wenotedthattheaccountingsystemisoutdatedandisnotintegrated.Thisresultsinsomeinaccurateand/orinaccessiblereports.Cause/Effect –Material misstatements could occur without being noticed and inappropriate accountingtransactionscouldbeconcealed.Recommendation–WerecommendtheMedicalCenterconsiderupdatingitscurrentaccountingsystemsinthepharmacydepartment.Management Response – We concur with this finding. ASMCA’s corrective action will be from theimplementationofthenewFinancialEdgeSoftwareinSeptember2017whichwill integratewiththenewelectronichealthrecordsystemthatisinplacenow.Thecompletiondateforthiscorrectiveactionplanwillbethesameas2014‐003.2015‐002–AccountsPayableandAPAdvancePayments–SignificantDeficiencyinInternalControlsCriteria –Management is responsible for the selection and use of appropriate accounting policies. Expensesshouldberecognizedandaccruedinthepriorperiodtoensurethecompletenessoftheaccountspayable.Condition/Context–Duringourdetailtestofsubsequentdisbursements,itwasdiscoveredtherewasamaterialinstanceofimpropercutoffrelatedtoaccountspayable.Cause/Effect–Managementhasnotimplementedtheproperaccountingpoliciesandproceduresoveraccountspayable.ExpensesarenotappropriatelyreportedinthecorrecttimeperiodperGAAPandaccountspayableareunderstated.Recommendation –We recommendmanagement implement appropriate accounting policies to identify andrecognizeexpensesasanaccountpayableintheproperperiod.ManagementResponse–Weconcurwiththisfinding.ASMCA’scorrectiveactionwillbetoreconciletheAPadvancepaymentsmonthlytothegeneralledger.AstandardofpracticewillbecreatedtoshowworkflowandprocessestoensurethereisnooutstandingAPadvancethatisunreconciledorreceivedwithoutproperreceivingdocumentation.ThisSOPwillshowwhoisresponsibleforthismonthlyreconciliationandwhoistoapproveit.ThecompletiondateforthiscorrectiveactionisSeptember2017.

SectionIII–FederalAwardFindingsandQuestionedCosts2014‐008 – Allowable Cost, Payroll Segregation of Duties (Also see Section II. Financial StatementFindingsItem2014‐005)–MaterialWeaknessinInternalControls

Criteria – The Uniform Guidance requires institutions to have internal controls in place to monitor thatexpendituresareonlyforallowableactivitiesandthatthecostsofgoodsandserviceschargedtotheFederalawardareallowablepertheapplicablecostprinciples.Condition/Context–Referto2014‐005.QuestionedCost–Nonetobereported.Cause/Effect – Refer to 2014‐005. The lack of segregation of duties identified for payroll may result inunallowablecostsbeingchargedtotheFederalprogram.Repeatfinding–Yes,2014‐008Auditor'sRecommendation–Referto2014‐005.ManagementResponse–Weconcurwiththisfinding.ASMCA’scorrectiveactionwilladdressthisdeficiencyby implementing a new financial system, Financial Edge, in September 2017. This will clearly delineatepayrollsegregationofdutiesbetweentheonboardingofemployeesbyHumanResourcesDepartment(HR)and the running of bi‐weekly payrollwith necessary updates by Finance‐payroll. The allowable costwillflowproperlyandwithoutanycompromisetotheintegrityofthepayrolldatawhichwillcomplywithOMBCircularA‐133requiringinstitutionstohaveinternalcontrolsinplacetomonitorthattheexpendituresareonlyforallowableactivitiesandthecostofgoodsandserviceschargedtotheFederalawardareallowablepertheapplicablecostprinciples.

Criteria–Federalregulationsrequiregranteesthathavepurchasedcapitalequipmentwithfederalfundingtoconductaphysicalinventoryofassetspurchasedwithfederalfundsatleastonceeverytwoyears.Condition/Context–TheMedicalCenterdoesnothavedocumentationfortherequiredphysicalinventoryofallapplicablecapitalassetsinthelasttwoyears.Inaddition,wenotedthattheMedicalCenter’scapitalassetlistingdidnotidentifywhichassetswerepurchasedusingfederalfunds.Cause/Effect–Therearenopoliciesrequiringseparateidentificationofassetspurchasedwithfederalfunds.AlthoughtheMedicalCenterdidaphysicalcountattheendofthefiscalyear,therewasnodocumentationtosupport the count. Without a physical inventory of capital assets, it is possible that assets could bemisappropriatedwithoutdetection.Repeatfinding–Yes,2015‐001Auditor’s Recommendation – The capital asset listing should separately identify assets purchased withfederal funds. The listing should be updated throughout the year as assets are purchased and disposed.Additionally,aphysicalinventoryshouldbeconductedanddocumentedatleasteverytwoyears.Management Response – We concur with this finding. ASMCA’s corrective action is to write a properstandard of practice to require a physical inventory every 2 years and documentation of the process. Itshould cite who is to perform this inventory, and how it is documented and approved. All federallypurchased fixed assetswill be identifiedwithin this physical inventory. The completion of the correctiveactionwillbeSeptember2017..

2014‐001–PreparationofFinancialStatements–SignificantDeficiencyinInternalControlsCondition/Context – Currently, the Medical Center does not have personnel with the training and/orexperiencenecessary todraft the financial statements inaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.Recommendation–WerecommendtheBoardofDirectorsandexecutiveteamreviewthecurrentsituationtodeterminethepropercourseofaction.CurrentStatus–Repeatedasfinding2014‐001.2014‐002–PoliciesandProcedures–SignificantDeficiencyinInternalControlsCondition/Context–Whileperformingourinternalcontroltesting,wenotedseveraloftheMedicalCenter’spolicies and procedures had not been updated for several years. However, we noted progress had beenmadeduringthefiscalyearendedSeptember30,2015.Recommendation – We recommend the Medical Center update or create new policy and proceduredocumentsthatdelineateresponsibilitiesandlimitationstoreducefinancialerrorsand/orfraud.CurrentStatus–Repeatedasfinding2014‐002.2014‐003– InformationTechnology,PatientRevenues,andAccountsReceivableLedger–MaterialWeaknessinInternalControlsConditionandContext–TheMedicalCenterwashistoricallyunabletoobtainaccuratepatientrevenueandaccountsreceivablereportsasofyear‐end.Recommendation–WerecommendtheMedicalCenterconsiderpurchasinganewsystemthatcanensureaccuratefinancialstatementreporting,consolidatesthethreecurrentsystemsintoonesystem,andmeettheFederalElectronicHealthRecordrequirements.CurrentStatus–Modifiedandrepeatedasfinding2014‐003.

2014‐004–InformationTechnology–MaterialWeaknessinInternalControlsCondition/Context –While performing internal control testing, we noted that the accounting system isoutdatedandnot integrated.Thisresults ina largeamountofmanualentries,aswellassome inaccurateand/orinaccessiblereports.Recommendation–WerecommendtheMedicalCenterconsiderupdatingitscurrentaccountingsystems.CurrentStatus–Modifiedandrepeatedasfinding2014‐004.2014‐005 – Segregation of Duties and Other Internal Control Findings – MaterialWeakness inInternalControlsCondition/Context – While performing our internal control testing, internal control deficiencies wereidentifiedasfollows:CashReceiptsforOff‐IslandReferrals

One employee opens themail, collects any checks received, and takes themoney to the bank fordeposit.Noindependentreviewofthecashreceivedinthemailisdonetoensurewhatwasreceivedwasdepositedatthebank.

2014‐009–Procurement,Suspension,andDebarment–MaterialWeaknessinInternalControlsFederalProgram–BasicOperations,CIP,andOperationsandMaintenanceFederalAgency–DepartmentoftheInteriorConditionandContext–WenotedduringourtestingoftheMedicalCenter’smajorprogramthattherewasnoevidence or documentation being maintained showing that vendors are being checked for suspension ordebarredontheEPLS/SAMwebsite.Auditor’sRecommendation–WerecommendthattheMedicalCenterdevelopandimplementpoliciestoensurethatpriortoenteringintoacontractwithavendor,theychecktheEPLS/SAMwebsitetoensurethevendorisnotsuspendedordebarredandthatdocumentationoftheverificationismaintained.CurrentStatus–Cleared2015‐001–Procurement,SuspensionandDebarment–MaterialWeaknessinInternalControlsFederalProgram–BasicOperations,CIP,andOperationsandMaintenanceFederalAgency–DepartmentoftheInteriorCondition/Context–TheMedicalCenterdoesnothavedocumentationfortherequiredphysicalinventoryofallapplicablecapitalassetsinthelasttwoyears.Inaddition,wenotedtheMedicalCenter’scapitalassetlistingdidnotidentifywhichassetswerepurchasedusingfederalfunds.Auditor’sRecommendation–Thecapitalasset listingshouldseparately identifyassetspurchasedwith federalfunds.Thelistingshouldbeupdatedthroughouttheyearasassetsarepurchasedanddisposed.Additionally,aphysicalinventoryshouldbeconductedanddocumentedatleasteverytwoyears.CurrentStatus–Repeatedasfinding2015‐001