16

Presentation of Q2 2019 26 August 2019 American Shipping Company ASA

Presentation of Q2 201926 August 2019

American Shipping Company ASA

Important information

Nothing herein shall create any implication that there has been no change in the affairs of American Shipping Company ASA ("AMSC" or the "Company") as of the date of this Company Presentation. This Company Presentation contains forward-looking statements relating to the Company's business, the Company's prospects, potential future performance and demand for the Company's assets, the Jones Act tanker market and other forward-looking statements. Forward-looking statements concern future circumstances and results and other statements that are not historical facts, sometimes identified by the words "believes", "expects", "predicts", "intends", "projects", "plans", "estimates", "aims", "foresees", "anticipates", "targets", and similar expressions. The forward-looking statements contained in this Company Presentation, including assumptions, opinions and views of the Company or cited from third party sources, are solely opinions and forecasts which are subject to risks, uncertainties and other factors that may cause actual events to differ materially from any anticipated development.

Second Quarter 2019 Highlights

* Net profit after tax, adjusted for non-recurring items, currency fluctuations, mark-to-market of derivatives and changes to deferred tax ** Includes DPO, reported EBITDA for Q2 19 is USD 21.0 million

3

Adjusted net profit of USD 2.5 million*

Normalized EBITDA** of USD 21.9 million

• No profit share

• DPO of USD 0.9 million

Declared Q2 dividend of USD 0.08 per share, consistent with prior guidance

• Ex-dividend date of 30 August 2019 with payment on or about 10th

September 2019

• Classified as a return of paid in capital

Stable market conditions for Jones Act tankers

Normalized EBITDA* (USD millions) Normalized EBITDA* per quarter (USD millions)

4

• Normalized EBITDA* of USD 21.9 million in Q2 19 (USD 21.5 million in Q2 18)• No profit share in Q2 19 or Q2 18• DPO of USD 0.9 in Q2 19 (USD 0.9 million in Q2 18)

* Including Profit Share (except 2018 and 2017 where profit share was 0 for the full year) and DPO. Reported EBITDA for Q2 19 is USD 21.0 million

85 85 85 84

3 4 411 10

0102030405060708090

100

2016 20182015 2017

4

Profit Share DPO Reported EBITDA

21 21 21 21 21 21 21 21 21 21

02468

1012141618202224

11

Q2 17Q1 17

1 11

Q3 17 Q4 17

1

Q1 18

1

Q2 18

1

Q3 18 Q4 18 Q1 19

1

Q2 19

1

Profit Share DPO Reported EBITDA

Stable, Predictable EBITDA

Long-term fixed rate bareboat charters to OSG secures cash flow

Fleet Deployment Overview

5

Firm Charter Options

Houston

Long Beach

Los Angeles

New York

Texas City

Boston

Nikiski

Martinez

Tampa

Anacortes

Vessel End users

• AMSC’s fleet is on firm BB Charters to OSG with evergreen extension options

• AMSC receives fixed annual bareboat revenue of USD 88 million + ~50% of the profits generated by OSG under the time charter contracts

• OSG time charters the vessels to oil majors for U.S domestic trade

BBC exp. 2022

BBC exp. 2022

BBC exp. 2022

BBC exp. 2022

BBC exp. 2022

Exp. ‘20

Exp. ‘20

Exp. ‘20

Exp. ‘20

BBC Options

BBC Options

BBC Options

BBC Options

BBC Options

BBC Options

BBC Options

BBC Options

BBC Options

OptionsBBC exp. 2025

A Critical Part of Oil Majors’ Transportation Logistics

6

Jones Act Tanker Routes:

Gulf Coast refineries to Florida and East Coast (Clean)

Alaska and Intra-west coast movements (Clean/Dirty)

Cross-Gulf movements (Dirty)

4

BAKKEN

EAGLE FORD

PERMIAN

Patoka, IL

US GULF

Key US Oilfields

Clean Pipeline

Barges

Crude Pipeline

5

3

2

1

1 6

Primary trade routes for Jones Act crude oil and products

Pipeline project Start Incremental capacity

Total capacity

Current capacity 2.80

Local refining 0.50 3.30

Sunrise Q2 ’19 0.12 3.51

Cactus 2 Q4 ’19 0.67 4.18

Gray Oak Q1 ’20 0.70 4.88

EPIC Q2 ’20 0.40 5.28

Enterprise NGL Q2 ’20 0.10 5.38

Permian to Gulfcoast Q3 ’20 0.60 5.98

ExxonMobil Q4 ’20 1.00 6.98

Source: Navigistics’ Wilson Gillette Report May 2019

The Permian Pipeline Crunch

2

3

Delaware Bay Lightening (Dirty)

Shuttle tankers from deep water U.S. Gulf to Gulf Coast Refineries (Dirty)

Gulf Coast crude to Northeast refineries (Dirty)

4

5

6

1

Permian Pipeline Capacity – New Projects and Production Growth, MBDs

Permian production growth has surpassed pipeline

takeaway capacity –additional volumes to drive

tanker demand

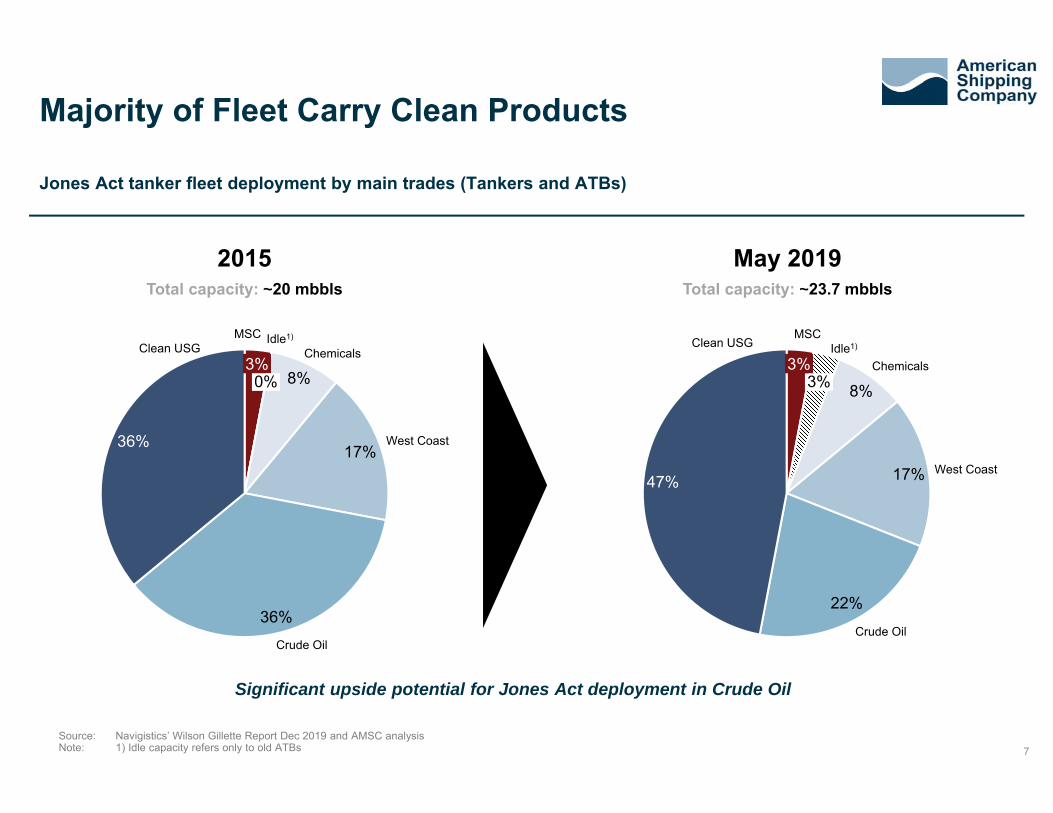

Jones Act tanker fleet deployment by main trades (Tankers and ATBs)

7Source: Navigistics’ Wilson Gillette Report Dec 2019 and AMSC analysisNote: 1) Idle capacity refers only to old ATBs

Majority of Fleet Carry Clean Products

8%

17%

36%

36%

Chemicals3%

MSC

0%

Idle1)Clean USG

Crude Oil

West Coast

8%

17%

22%

47%

Crude Oil

Chemicals

MSC

3%

Idle1)

3%

West Coast

Clean USG

2015Total capacity: ~20 mbbls

Significant upside potential for Jones Act deployment in Crude Oil

May 2019Total capacity: ~23.7 mbbls

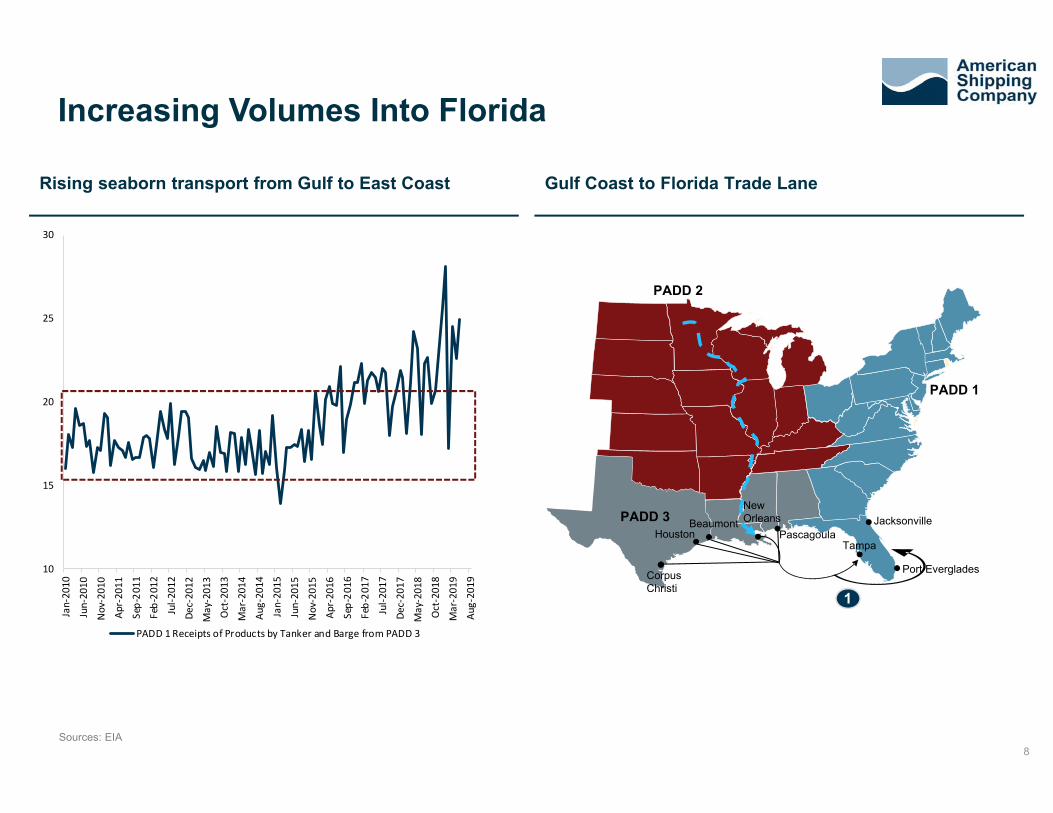

Rising seaborn transport from Gulf to East Coast Gulf Coast to Florida Trade Lane

Increasing Volumes Into Florida

8Sources: EIA

1

PADD 1

PADD 3

PADD 2

Jacksonville

Port Everglades

Tampa

Corpus Christi

HoustonBeaumont

New Orleans

Pascagoula

Mbbls per month

10

15

20

25

30

Jan‐20

10

Jun‐20

10

Nov‐201

0

Apr‐20

11

Sep‐20

11

Feb‐20

12

Jul‐2

012

Dec‐20

12

May‐201

3

Oct‐201

3

Mar‐201

4

Aug‐20

14

Jan‐20

15

Jun‐20

15

Nov‐201

5

Apr‐20

16

Sep‐20

16

Feb‐20

17

Jul‐2

017

Dec‐20

17

May‐201

8

Oct‐201

8

Mar‐201

9

Aug‐20

19

PADD 1 Receipts of Products by Tanker and Barge from PADD 3

PADD 3 to PADD 1 Crude Oil Moves by Tanker and Barge

Trade lane carrying Crude from Gulf Coast to U.S. Northeast

9Source: EIA, Marine Traffic and AMSC analysis

PADD 1

6

PADD 3

PADD 2

Jacksonville

Port Everglades

Tampa

Corpus Christi

HoustonBeaumont

New Orleans

Pascagoula

Washington

New YorkPhiladelphia

Boston

Crude Returning to Peak Levels on East Coast

East Coast volumes back to ~6 tankers, up from ~1 tanker during 2017

Volumes driven by spread in pricing of U.S. oil vs international alternatives

0

1

2

3

4

Mbb

l

PADD 3 to PADD 1 Movements of Crude by Tanker (3M Rolling Ave)

PADD 3 to PADD 1 Crude Oil Moves by Number of Tanker Liftings

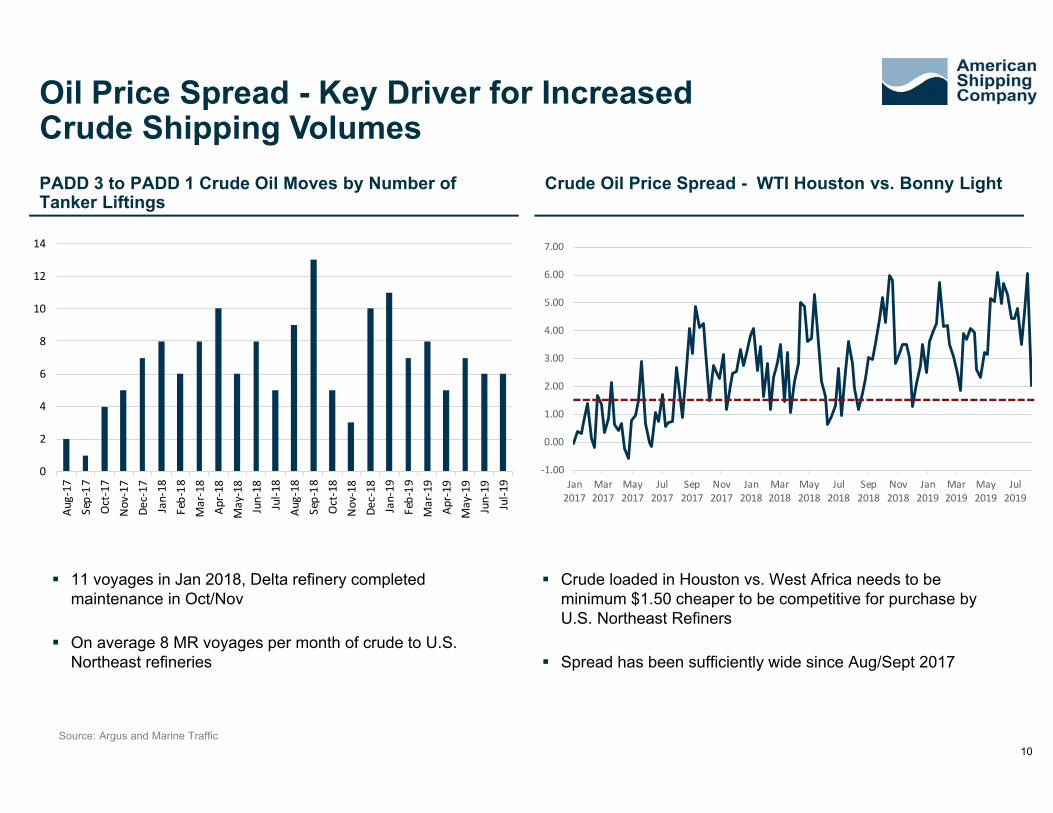

Crude Oil Price Spread - WTI Houston vs. Bonny Light

10Source: Argus and Marine Traffic

11 voyages in Jan 2018, Delta refinery completed maintenance in Oct/Nov

On average 8 MR voyages per month of crude to U.S. Northeast refineries

Crude loaded in Houston vs. West Africa needs to be minimum $1.50 cheaper to be competitive for purchase by U.S. Northeast Refiners

Spread has been sufficiently wide since Aug/Sept 2017

Oil Price Spread - Key Driver for Increased Crude Shipping Volumes

0

2

4

6

8

10

12

14

Aug‐17

Sep‐17

Oct‐17

Nov‐17

Dec‐17

Jan‐18

Feb‐18

Mar‐18

Apr‐18

May‐18

Jun‐18

Jul‐1

8Au

g‐18

Sep‐18

Oct‐18

Nov‐18

Dec‐18

Jan‐19

Feb‐19

Mar‐19

Apr‐19

May‐19

Jun‐19

Jul‐1

9

‐1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Jan2017

Mar2017

May2017

Jul2017

Sep2017

Nov2017

Jan2018

Mar2018

May2018

Jul2018

Sep2018

Nov2018

Jan2019

Mar2019

May2019

Jul2019

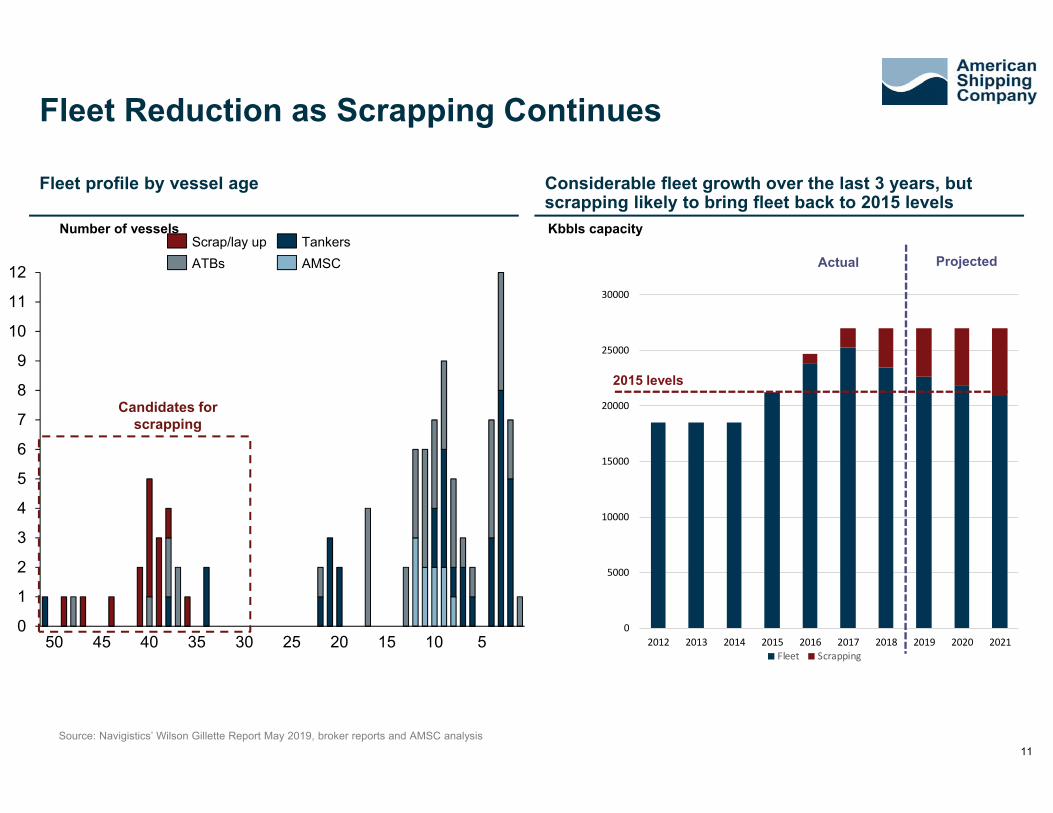

Fleet profile by vessel age Considerable fleet growth over the last 3 years, but scrapping likely to bring fleet back to 2015 levels

0

1

2

3

4

5

6

7

8

9

10

11

12

50 30 152045 40 35 25 10 5

AMSCTankersScrap/lay up

ATBs

11Source: Navigistics’ Wilson Gillette Report May 2019, broker reports and AMSC analysis

Fleet Reduction as Scrapping Continues

Number of vessels

Candidates for scrapping

Kbbls capacity

0

5000

10000

15000

20000

25000

30000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021Fleet Scrapping

Actual Projected

2015 levels

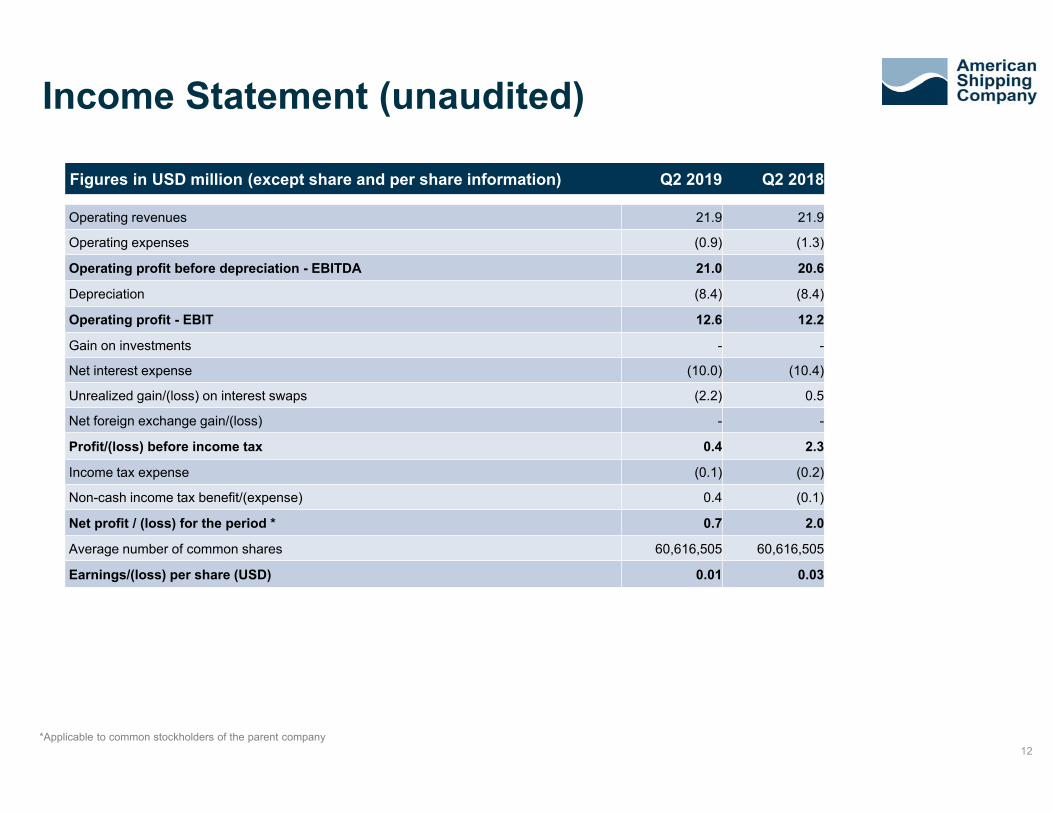

*Applicable to common stockholders of the parent company

Figures in USD million (except share and per share information) Q2 2019 Q2 2018

Operating revenues 21.9 21.9

Operating expenses (0.9) (1.3)

Operating profit before depreciation - EBITDA 21.0 20.6

Depreciation (8.4) (8.4)

Operating profit - EBIT 12.6 12.2

Gain on investments - -

Net interest expense (10.0) (10.4)

Unrealized gain/(loss) on interest swaps (2.2) 0.5

Net foreign exchange gain/(loss) - -

Profit/(loss) before income tax 0.4 2.3

Income tax expense (0.1) (0.2)

Non-cash income tax benefit/(expense) 0.4 (0.1)

Net profit / (loss) for the period * 0.7 2.0

Average number of common shares 60,616,505 60,616,505

Earnings/(loss) per share (USD) 0.01 0.03

12

Income Statement (unaudited)

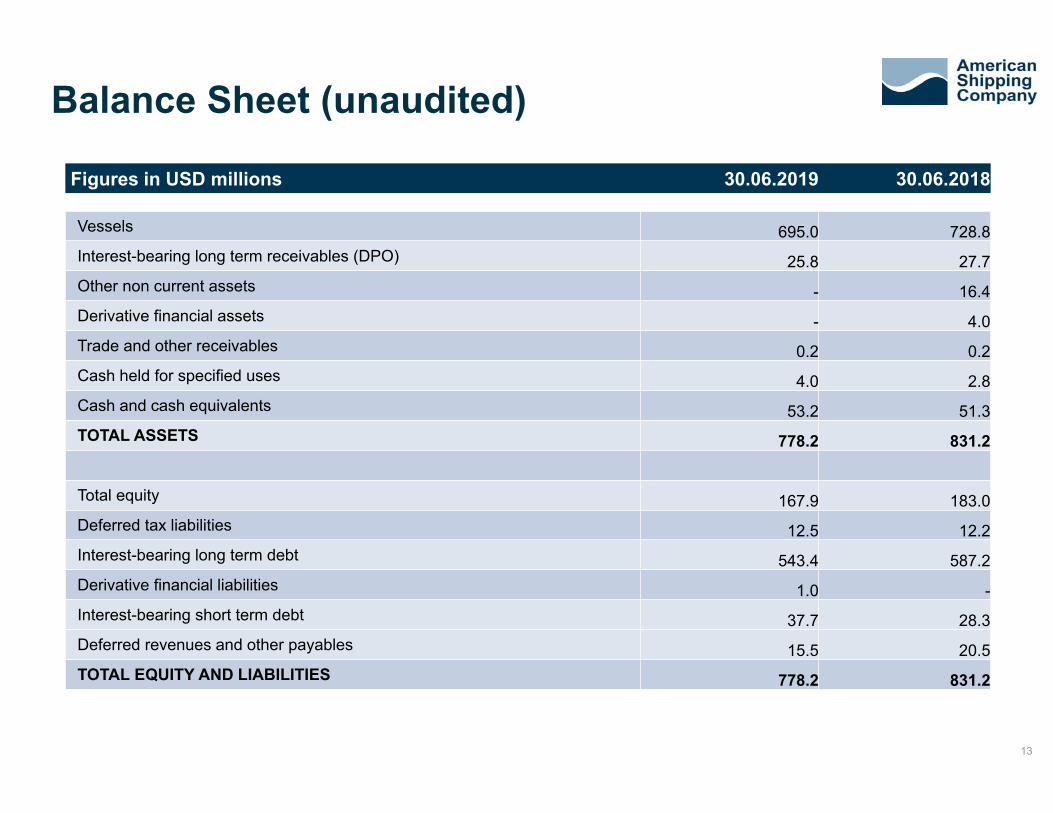

Figures in USD millions 30.06.2019 30.06.2018

Vessels 695.0 728.8Interest-bearing long term receivables (DPO) 25.8 27.7Other non current assets - 16.4Derivative financial assets - 4.0Trade and other receivables 0.2 0.2Cash held for specified uses 4.0 2.8Cash and cash equivalents 53.2 51.3TOTAL ASSETS 778.2 831.2

Total equity 167.9 183.0Deferred tax liabilities 12.5 12.2Interest-bearing long term debt 543.4 587.2Derivative financial liabilities 1.0 -Interest-bearing short term debt 37.7 28.3Deferred revenues and other payables 15.5 20.5TOTAL EQUITY AND LIABILITIES 778.2 831.2

13

Balance Sheet (unaudited)

CASH DEVELOPMENT IN 2Q 19 (USD millions)

14

52.1

21.0

4.4

7.6

4.8 0.9 57.2

AmortizationInterestOB Cash EBITDA OtherDividends CB Cash

Cash position increased during the quarter

15

Highlights

Investment HighlightsComments

INCREASING DEMAND IN KEY TRADES

Stable crude shipments from U.S. Gulf to the U.S. Northeast

Growing clean trade into Florida

Jones Act time charter rates approaching USD 60,000 per day

REDUCING FLEET CAPACITY

Scrapping of older tonnage continues with 2 MRs and 5 ATBs retired in 2018 and two additional ATBs to date in 2019

10 tankers and ATBs approaching 35 years or older in 2020; with Special Surveys coming up

Slim orderbook with only two barges for delivery in 2020

LEADING MARKET POSITION WITH STABLE CASH FLOWS

Bareboat contracts provide stable cash flows with profit share upside potential

Existing modern fleet that is integral to OSG’s business

Well positioned to take advantage of growth opportunities in a strengthening market

FLEET WELL POSITIONED TO BENEFIT FROM MARKET

UPSIDE

OSG is to redeploy nine AMSC owned vessels on new time charters during 2019 and early 2020

The fleet is well positioned to capitalise on increased time charter rates through the profit split