The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty‟s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk. May 2012 AMMB HOLDINGS BERHAD Proposed up to RM2 billion Medium-Term Notes Programme

Transcript

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty‟s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

May 2012

AMMB HOLDINGS BERHAD

Proposed up to RM2 billion Medium-Term Notes Programme

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty‟s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

CREDIT RATING RATIONALE

CORPORATE RATINGS

MAY 2012

AMMB HOLDINGS BERHAD

– Initial Rating

Summary

RAM Ratings has assigned respective long- and short-term corporate credit

ratings (“CCRs”) of A1 and P1 to AMMB Holdings Berhad (“AMMB” or “the

Company”). Concurrently, RAM Ratings has also assigned respective final long-

term ratings of A1 and A2 to the senior medium-term notes (“MTN”) and

subordinated MTN to be issued under the Company‟s Proposed up to RM2 billion

MTN Programme (“Proposed Issue”). All the long-term ratings have a stable

outlook. The 1-notch differential between the rating of the subordinated MTN and

the senior MTN reflects the former‟s subordination in terms of rights and priority

of payment over all the senior obligations of AMMB.

As a non-operating investment-holding company, AMMB‟s earnings are highly

dependent on dividend income from its subsidiaries to service its financial

obligations. In this regard, AMMB‟s key banking subsidiaries, i.e. AmBank (M)

Berhad (“AmBank”), AmIslamic Bank Berhad (“AmIslamic”) and AmInvestment

Bank Berhad (“AmInvestment”) (all rated AA3/Stable/P1 by RAM Ratings)1, are

regulated financial institutions. AMMB‟s ratings are anchored by the credit

strength of its key banking subsidiaries, apart from its own company-level credit

metrics. The 1-notch differential between AMMB‟s long-term CCR and the ratings

of its key subsidiaries reflects the Company‟s structural subordination given that

it has lower priority as a shareholder compared to the direct creditors of its key

subsidiaries; it also incorporates AMMB‟s sound stand-alone credit fundamentals

and comfortable financial leverage ratios.

Moving forward, AMMB and its subsidiaries (collectively, “the AMMB Group” or

“the Group”) is envisaged to continue receiving firm operational support from its

largest substantial shareholder, Australia and New Zealand Banking Group

Limited (“ANZ”), which owns a 23.8%-stake. Notably, ANZ has been actively

participating in the strategic direction and operations of the Group through its

representation in the latter‟s key management line-up and board.

1 RAM Ratings reaffirmed the AA3/Stable/P1 financial institution ratings of AmBank, AmIslamic and

AmInvestment in December 2011.

Analysts: Kwan Ji-Ling (603) 7628 1115 [email protected] Chan Yin Huei (603) 7628 1180 [email protected] Principal Activity: AMMB Holdings Berhad is an investment-holding company Instruments: Proposed Senior Medium-Term Notes (“MTN”) and/or Subordinated MTN under the Proposed up to RM2 billion MTN Programme Ratings: Corporate Credit Ratings: A1/P1 [Assigned] Senior MTN: A1 [Assigned] Subordinated MTN: A2 [Assigned] Rating Outlook: Stable Coupon Rate: To be determined prior to each MTN issuance Tenure: Up to 30 years for each MTN issuance Lead Arranger: AmInvestment Bank Berhad Trustee: Pacific Trustees Berhad

AMMB Holdings Berhad 2

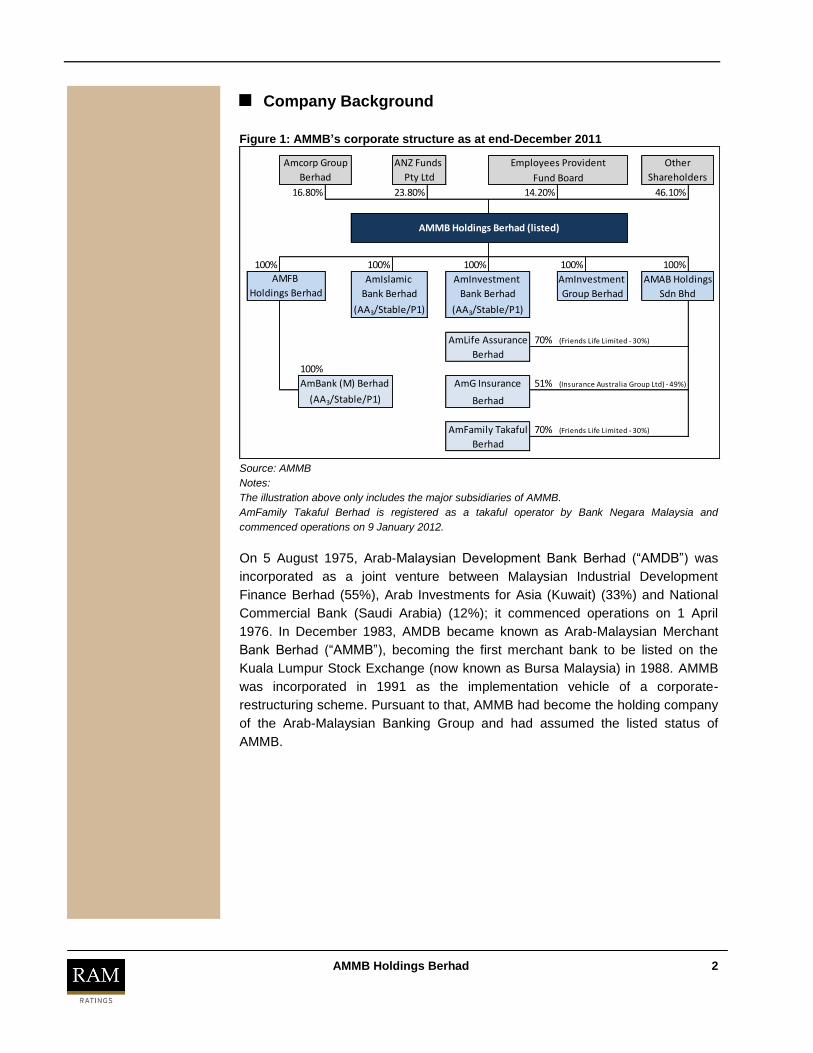

Company Background

Figure 1: AMMB’s corporate structure as at end-December 2011

23.80% 46.10%

100% 100% 100% 100% 100%

70% (Friends Life Limited - 30%)

100%

AmBank (M) Berhad 51% (Insurance Australia Group Ltd) - 49%)

70% (Friends Life Limited - 30%)

Other

Shareholders

Bank Berhad

AmInvestment

Group Berhad

Berhad

16.80%

AMMB Holdings Berhad (listed)

ANZ Funds

Pty Ltd

Berhad

Bank Berhad

AMFB AMAB Holdings

Sdn Bhd

AmLife Assurance

AmIslamic

(AA3/Stable/P1) (AA3/Stable/P1)

AmInvestment

(AA3/Stable/P1) Berhad

AmG Insurance

AmFamily Takaful

Berhad

Employees Provident

Fund Board

14.20%

Holdings Berhad

Amcorp Group

Source: AMMB

Notes:

The illustration above only includes the major subsidiaries of AMMB.

AmFamily Takaful Berhad is registered as a takaful operator by Bank Negara Malaysia and

commenced operations on 9 January 2012.

On 5 August 1975, Arab-Malaysian Development Bank Berhad (“AMDB”) was

incorporated as a joint venture between Malaysian Industrial Development

Finance Berhad (55%), Arab Investments for Asia (Kuwait) (33%) and National

Commercial Bank (Saudi Arabia) (12%); it commenced operations on 1 April

1976. In December 1983, AMDB became known as Arab-Malaysian Merchant

Bank Berhad (“AMMB”), becoming the first merchant bank to be listed on the

Kuala Lumpur Stock Exchange (now known as Bursa Malaysia) in 1988. AMMB

was incorporated in 1991 as the implementation vehicle of a corporate-

restructuring scheme. Pursuant to that, AMMB had become the holding company

of the Arab-Malaysian Banking Group and had assumed the listed status of

AMMB.

AMMB Holdings Berhad 3

As at end-December 2011, ANZ, via its wholly owned subsidiary – ANZ Funds

Pty Ltd - remained the largest shareholder of the AMMB Group with a 23.8%-

stake; its other major shareholders comprised Amcorp Group Berhad (16.8%)2

and the Employees Provident Fund Board (14.2%). ANZ came in as a strategic

partner and major investor of the AMMB Group in May 2007, and entered into a

technical services agreement with AmBank in November 2008. The partnership

has led to ANZ‟s active support during the AMMB Group‟s business

transformation, with the provision of technical expertise through the appointment

of ANZ representatives as key senior management personnel and board

members to facilitate the Group‟s long-term growth.

Following the completion of a reorganisation exercise on 28 February 2011,

AmIslamic is now directly held by AMMB, instead of being wholly owned by

AmBank. The corporate reorganisation represents part of AMMB‟s capital-

management strategy - aimed to improve AmBank‟s capitalisation and to prepare

for stricter capital requirements under the impending Basel III framework.

AMMB is principally a non-operating investment-holding company, the principal

assets of which comprise investments in banks and non-bank subsidiaries

engaged in a wide range of conventional and Islamic financial services such as

retail and business banking, corporate and institutional banking, investment

banking including funds management and stockbroking, general and life

insurance, as well as takaful. Within AMMB, key banking activities have been

streamlined into 4 principal business groups under its universal-banking platform:

the Banking Group, the Capital-Markets Group, the Asset-Management Group

and the Insurance Group. As at end-December 2011, AMMB ranked sixth out of

the total of 8 domestic banking groups, based on its asset base of RM107.2

billion.

Objectives of the Proposed Issue

The proceeds from the Proposed Issue have been earmarked for AMMB‟s capital

expenditure, investments, working capital, payment of fees and expenses in

relation to the debt facility, and the general funding requirements of AMMB

and/or its subsidiaries.

2 Indirect interest held by YBhg Tan Sri Azman Hashim.

AMMB – investment-holding

company

ANZ – strategic

shareholder

AMMB Holdings Berhad 4

Business Strategies

Following its strategic partnership with ANZ in mid-2007, the AMMB Group has

embarked on various improvement initiatives by leveraging on the former‟s

international best practices and capabilities. Continuous efforts in tightening

underwriting standards and risk-management capabilities have translated into a

significant improvement in AmBank‟s asset quality. Notably, ANZ has been

actively participating in the Group‟s strategic direction and operations, with

representation in AMMB‟s key management line-up and board of directors.

AMMB‟s Medium Term Aspirations is to become Malaysia's preferred banking

group with international connectivity while expanding its cross-border operations

– by leveraging on ANZ‟s growing regional footprint.

As part of the Group‟s loan portfolio rebalancing and diversification strategy

initiated since 2008, the Group‟s lending focus has shifted to the business and

corporate segments, which are viewed to yield better risk-adjusted returns and

greater cross-selling opportunities. Over the past 2 years, these segments have

been the key growth drivers for both AmBank and AmIslamic. This has

augmented the Group‟s loan exposure to non-individuals, from 40% as at end-

March 2010 to 46% as at end-December 2011, while its share of floating-rate

loans has risen from 44% to 55%. Corporate loans will be targeted at project

financing with government support, government-linked companies, and multi-

national corporations.

In line with the Group‟s focus on risk-adjusted returns, AmBank and AmIslamic

have maintained their less aggressive strategy in pursuing automobile financing

amid the stiff price competition. This, coupled with their efforts to diversify into

other segments for a more balanced portfolio, had resulted in a noticeable

decline in AmBank‟s and AmIslamic‟s combined proportion of automobile

financing to around 32% as at end-December 2011 (end-March 2010: 36%).

Similarly, competition among banks in the residential mortgage market has been

rife, with aggressive pricing still seen in the market. Against this backdrop, the

management expects retail lending growth to remain modest in FYE 31 March

2012 (“FY Mar 2012”).

Moving ahead, the management will continue emphasising deposit growth to

improve AmBank‟s funding profile. This has been reinforced with key

performance indicators being put in place to promote deposit growth across all

business units, supported by the adoption of a fund-transfer-pricing mechanism.

Other initiatives include launching new deposit products, increasing the utilisation

of cash-management facilities and trade services, and cross-selling to the

Group's customers.

ANZ – formidable strategic partner with international connectivity

Focus on risk-adjusted returns instead of purely market-share

expansion

Ongoing emphasis on deposit growth

Continue rebalancing loan

portfolio

AMMB Holdings Berhad 5

The Group‟s priorities in FY Mar 2012 include expanding its non-interest income.

In this regard, the Group intends to derive at least one-third of its gross income

from non-interest income sources (FY Mar 2011: 28%) over the medium term by

seeking to capture opportunities in areas such as transaction banking, which

focuses on cash management and international trade, as well as wealth

management and bancassurance. In collaboration with ANZ, AMMB will continue

to expand its product offerings and distribution platform for its foreign exchange

(“forex”) and derivatives businesses, to better cater to the needs of its small- and

medium-sized enterprise (“SME”) and corporate clients. Forex and derivatives

businesses generated close to 3% of the Group‟s gross income in FY Mar 2011,

and are expected to further diversify its earnings base in future.

Loans to deposits ratio (%) 88.73 92.37 93.45 97.39

Overall RWCAR (%) 14.62 14.91 14.09 14.55

Source: AmBank

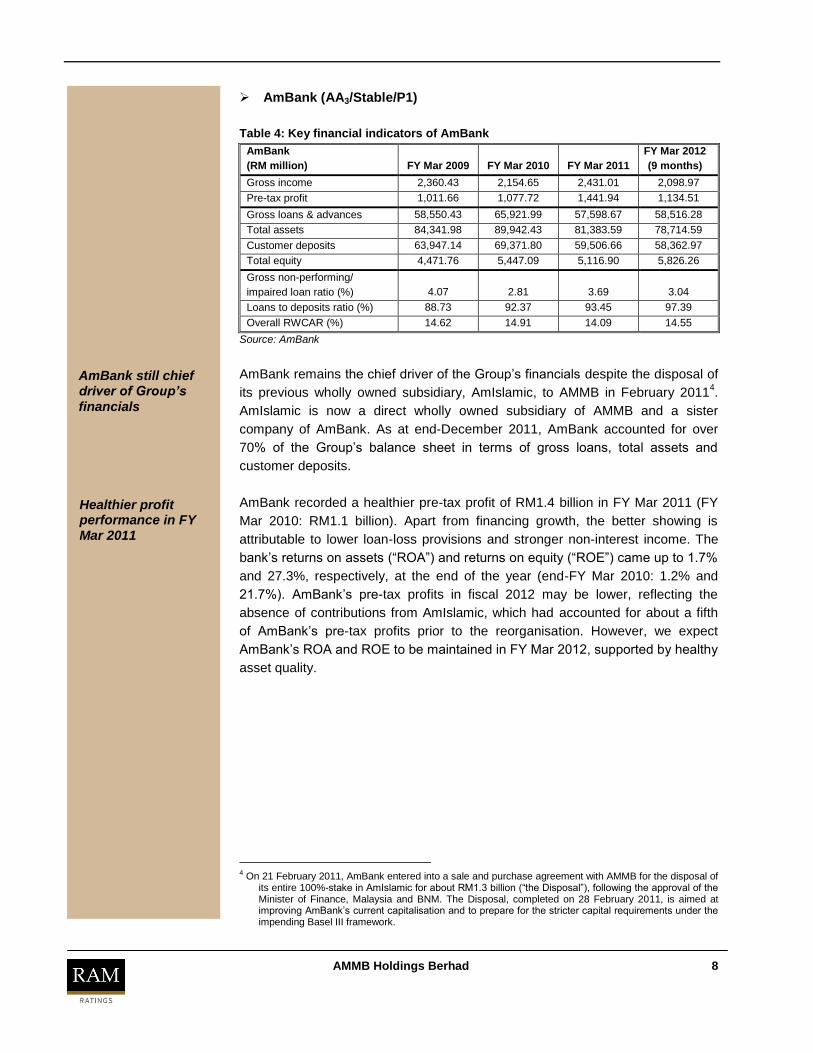

AmBank remains the chief driver of the Group‟s financials despite the disposal of

its previous wholly owned subsidiary, AmIslamic, to AMMB in February 20114.

AmIslamic is now a direct wholly owned subsidiary of AMMB and a sister

company of AmBank. As at end-December 2011, AmBank accounted for over

70% of the Group‟s balance sheet in terms of gross loans, total assets and

customer deposits.

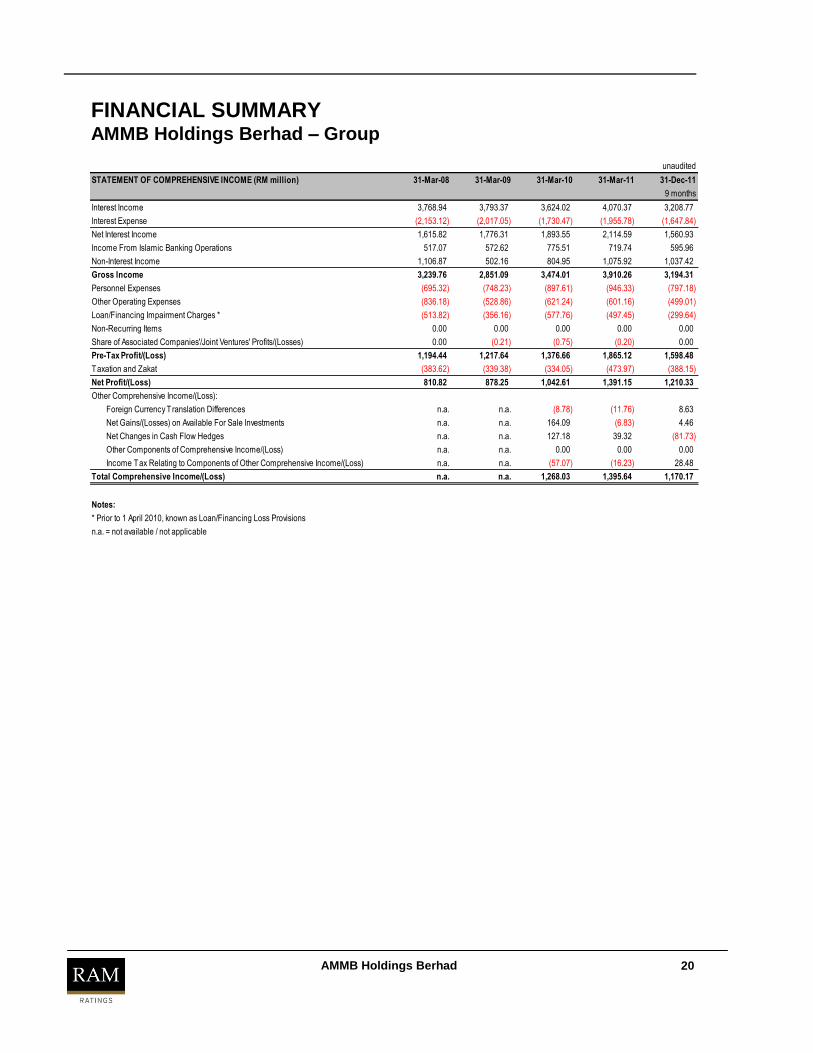

AmBank recorded a healthier pre-tax profit of RM1.4 billion in FY Mar 2011 (FY

Mar 2010: RM1.1 billion). Apart from financing growth, the better showing is

attributable to lower loan-loss provisions and stronger non-interest income. The

bank‟s returns on assets (“ROA”) and returns on equity (“ROE”) came up to 1.7%

and 27.3%, respectively, at the end of the year (end-FY Mar 2010: 1.2% and

21.7%). AmBank‟s pre-tax profits in fiscal 2012 may be lower, reflecting the

absence of contributions from AmIslamic, which had accounted for about a fifth

of AmBank‟s pre-tax profits prior to the reorganisation. However, we expect

AmBank‟s ROA and ROE to be maintained in FY Mar 2012, supported by healthy

asset quality.

4 On 21 February 2011, AmBank entered into a sale and purchase agreement with AMMB for the disposal of

its entire 100%-stake in AmIslamic for about RM1.3 billion (“the Disposal”), following the approval of the Minister of Finance, Malaysia and BNM. The Disposal, completed on 28 February 2011, is aimed at improving AmBank‟s current capitalisation and to prepare for the stricter capital requirements under the impending Basel III framework.

AmBank still chief driver of Group’s

financials

Healthier profit performance in FY Mar 2011

AMMB Holdings Berhad 9

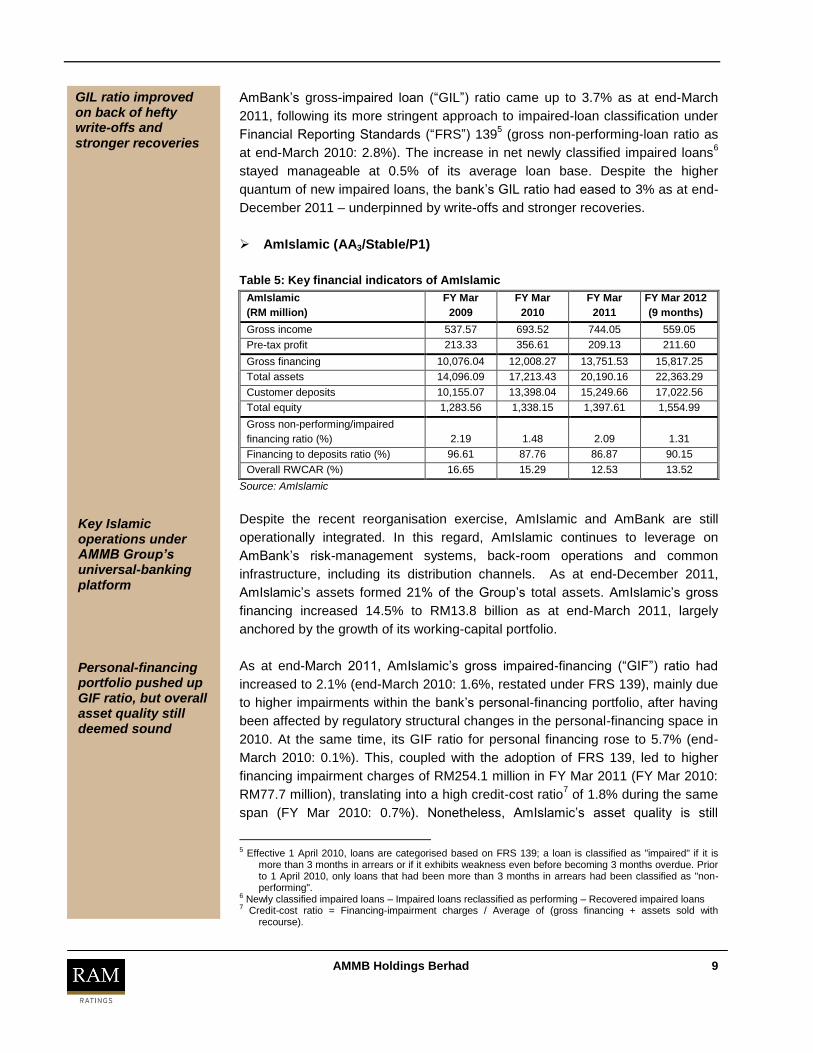

AmBank‟s gross-impaired loan (“GIL”) ratio came up to 3.7% as at end-March

2011, following its more stringent approach to impaired-loan classification under

Financial Reporting Standards (“FRS”) 1395 (gross non-performing-loan ratio as

at end-March 2010: 2.8%). The increase in net newly classified impaired loans6

stayed manageable at 0.5% of its average loan base. Despite the higher

quantum of new impaired loans, the bank‟s GIL ratio had eased to 3% as at end-

December 2011 – underpinned by write-offs and stronger recoveries.

Financing to deposits ratio (%) 96.61 87.76 86.87 90.15

Overall RWCAR (%) 16.65 15.29 12.53 13.52

Source: AmIslamic

Despite the recent reorganisation exercise, AmIslamic and AmBank are still

operationally integrated. In this regard, AmIslamic continues to leverage on

AmBank‟s risk-management systems, back-room operations and common

infrastructure, including its distribution channels. As at end-December 2011,

AmIslamic‟s assets formed 21% of the Group‟s total assets. AmIslamic‟s gross

financing increased 14.5% to RM13.8 billion as at end-March 2011, largely

anchored by the growth of its working-capital portfolio.

As at end-March 2011, AmIslamic‟s gross impaired-financing (“GIF”) ratio had

increased to 2.1% (end-March 2010: 1.6%, restated under FRS 139), mainly due

to higher impairments within the bank‟s personal-financing portfolio, after having

been affected by regulatory structural changes in the personal-financing space in

2010. At the same time, its GIF ratio for personal financing rose to 5.7% (end-

March 2010: 0.1%). This, coupled with the adoption of FRS 139, led to higher

financing impairment charges of RM254.1 million in FY Mar 2011 (FY Mar 2010:

RM77.7 million), translating into a high credit-cost ratio7 of 1.8% during the same

span (FY Mar 2010: 0.7%). Nonetheless, AmIslamic‟s asset quality is still

5 Effective 1 April 2010, loans are categorised based on FRS 139; a loan is classified as "impaired" if it is

more than 3 months in arrears or if it exhibits weakness even before becoming 3 months overdue. Prior to 1 April 2010, only loans that had been more than 3 months in arrears had been classified as "non-performing".

6 Newly classified impaired loans – Impaired loans reclassified as performing – Recovered impaired loans 7 Credit-cost ratio = Financing-impairment charges / Average of (gross financing + assets sold with

recourse).

Key Islamic operations under AMMB Group’s universal-banking platform

Personal-financing portfolio pushed up GIF ratio, but overall asset quality still deemed sound

GIL ratio improved on back of hefty write-offs and stronger recoveries

AMMB Holdings Berhad 10

deemed sound despite the setback in its personal-financing portfolio. The bank‟s

GIF coverage stood at a strong 209.1% as at end-December 2011 (end-March

2010: 137.0%). Following higher write-offs in the first nine months of FY Mar

2012 (“9M FY Mar 2012”), the bank‟s GIF ratio had declined to 1.3% as at end-

December 2011 while its credit-cost ratio had eased to 1% (annualised).

AmIslamic‟s profit performance in FY Mar 2011 had been affected by higher

financing impairment charges. The bank‟s pre-tax profit fell to RM209.1 million

last year, dragging its ROA down to 1.1% (FY Mar 2010: 2.3%). We expect its

profit performance to pick up in fiscal 2012, on the back of reduced financing-

impairment charges. The bank recorded a pre-tax profit of RM211.6 million in 9M

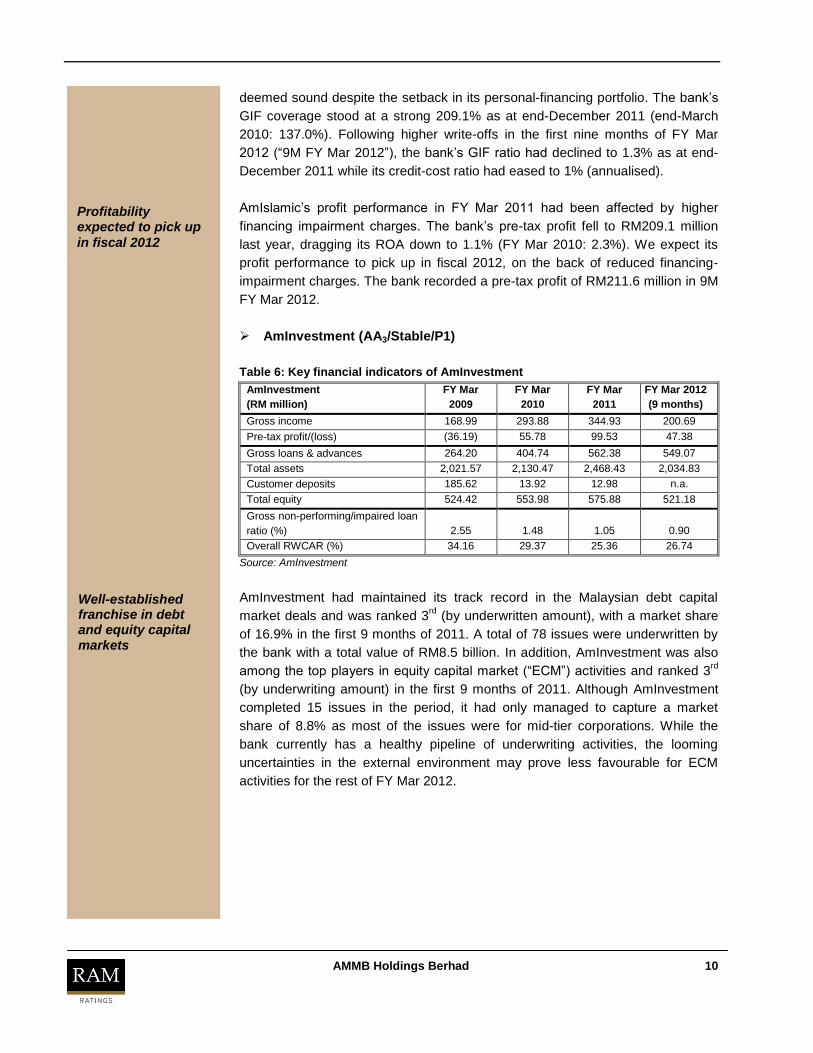

AmInvestment had maintained its track record in the Malaysian debt capital

market deals and was ranked 3rd

(by underwritten amount), with a market share

of 16.9% in the first 9 months of 2011. A total of 78 issues were underwritten by

the bank with a total value of RM8.5 billion. In addition, AmInvestment was also

among the top players in equity capital market (“ECM”) activities and ranked 3rd

(by underwriting amount) in the first 9 months of 2011. Although AmInvestment

completed 15 issues in the period, it had only managed to capture a market

share of 8.8% as most of the issues were for mid-tier corporations. While the

bank currently has a healthy pipeline of underwriting activities, the looming

uncertainties in the external environment may prove less favourable for ECM

activities for the rest of FY Mar 2012.

Profitability expected to pick up

in fiscal 2012

Well-established franchise in debt and equity capital markets

AMMB Holdings Berhad 11

AmInvestment‟s pre-tax profits almost doubled to RM99.5 million in FY Mar 2011

(FY Mar 2010: RM55.8 million), largely driven by contributions from its equity

derivatives businesses of around RM28 million. Equity derivatives income was

previously booked entirely under AmBank; this income is now shared based on a

50:50 arrangement8 between AmBank and AmInvestment. The better showing

was also attributable to higher corporate advisory fees as well as gains from the

disposal of available-for-sale investments. As a result, AmInvestment‟s ROA and

ROE both rose to 4.3% and 17.6%, respectively, in FY Mar 2011 (FY Mar 2010:

2.7% and 10.4%). Nevertheless, in 9M FY Mar 2012, AmInvestment reported a

30% year-on-year (“y-o-y”) decline in pre-tax profit to RM47.4 million (9M FY Mar

2011: RM67.3 million) due to a drop in fee income from corporate advisory and

loans.

For more details on AmBank, AmIslamic and AmInvestment, please refer to their

respective rating rationales published in February 2012.

AmG

AmG is one of the larger general insurers in Malaysia and ranked 8th based on

gross premium as at end-June 2011 (5th by net premium). Motor policies account

for 79% of AmG‟s portfolio and there is a clear strategy to diversify its business

by expanding its non-motor to 30% by 2015, driven by strong growth in its

commercial business lines.

AmG recorded a 20% y-o-y increase in its pre-tax profit to RM48.9 million in 1H

FY Mar 2012 (1H FY Mar 2011: RM40.6 million). Meanwhile, its claims ratio9 and

combined ratio10

stood at a respective 67% and 92% in 1H FY Mar 2012 (FY Mar

2011: 68% and 94%). Its CAR is above the regulatory minimum of 130% under

BNM‟s risk-based capital (“RBC”) framework.

AmG is a joint partnership between AMMB (51%)11

and Insurance Australia

Group Ltd (“IAG”) (49%). The strong strategic partnership allows AmG to

leverage on IAG‟s technical expertise, strategic planning, as well as sales and

business development capabilities. Its board of directors, senior management

(including its chief executive officer (“CEO”), Duncan Brain) and consultants also

consist of personnel from IAG.

8 On all realised and unrealised gains and losses arising from the trading and investment of equity

derivatives. 9 (Claims paid + changes in provision for outstanding claims) / Earned premiums

10 (Claims + Expenses) / Earned premiums 11

Via its wholly-owned subsidiary, AMAB Holdings Berhad.

Among top 5 players in motor

insurance

Leveraging on strategic partnership with

IAG

Pre-tax profit almost doubled in FY Mar 2011

AMMB Holdings Berhad 12

On 12 April 2012, AmG entered into a conditional sale and purchase agreement

with Kurnia Asia Berhad for the proposed acquisition of a 100% equity interest in

Kurnia Insurans (Malaysia) Berhad (“Kurnia Insurans”). The cash purchase price

of RM1.55 billion will be funded by AmG with capital injections from its

shareholders based on their respective shareholdings. The combined business of

AmG and Kurnia Insurans will emerge as the largest domestic general insurer

and market leader in motor insurance. RAM Ratings will continue monitoring the

progress of the proposed acquisition.

Kurnia Insurans, a wholly-owned subsidiary of Kurnia Asia Berhad, is among the

top 5 general insurers in Malaysia with a strong footing in motor insurance. In 1H

FY Dec 2011, it recorded a pre-tax profit of RM57 million (-1% y-o-y) with gross

earned premiums of RM518 million. It recorded a claims ratio of 69% in 1H FY

Dec 2011 (FY Dec 2010: 76%) while its combined ratio stood at 99% (end-FY

Dec 2010: 105%).

AmLife

AmLife, which is ranked eleventh in the market by total new business premiums,

is currently undergoing an internal review of its business operating model. A new

CEO is expected to be appointed before the end of FY Mar 2012. Meanwhile,

AmLife‟s current Deputy CEO, Adrian John Nurse, is the Acting CEO.

Besides filling the gap at top management level, the internal review and

restructuring also involve a turnaround plan for the company‟s agency force,

which has contracted to about 2,000 agents from around 4,000 in 2010. The

contraction resulted from the company‟s efforts to retain quality agents who are

productive and provide exemplary service to policyholders. The turnaround plan,

which is expected to be completed by June 2012, aims to build a stronger pool of

agents by ensuring that training programmes are up to par and agents act in full

compliance in their course of duties.

Apart from AmBank, AmLife entered into a new bank distribution agreement with

Alliance Bank Berhad in January 2012. Other key partners besides AmBank are

Standard Chartered Bank Malaysia Berhad, Bank Simpanan Nasional and

Malaysia Building Society Berhad.

In 1H FY Mar 2012, AmLife‟s gross premiums declined 39% y-o-y to RM194.9

million (1H FY Mar 2011: RM318.8 million), following the cessation of the sale of

its structured-notes products, a slowdown in the growth of AmBank‟s mortgage

and automobile loans, and the contraction of its agency force.

The drop in gross premiums had led to a net underwriting loss of RM25.8 million

in 1H FY Mar 2012, despite lower claims incurred. The lower gross premiums

had also translated into a weaker pre-tax profit in 1H FY Mar 2012, which slid

Among smaller players in life insurance

Weaker gross premium growth in

1H FY Mar 2012

Proposed acquisition of

Kurnia Insurans

AMMB Holdings Berhad 13

14% y-o-y to RM45 million; this made up 4% of the Group‟s pre-tax profit during

the same period. Meanwhile, its claims ratio and combined ratio came up to a

respective 71% and 112% in 1H FY Mar 2012 (FY Mar 2011: 76% and 113%)

while its CAR as at end-June 2011 was well above the regulatory minimum of

130% required under BNM‟s RBC framework.

Apart from the 70%-shareholding of AMMB via AMAB Holdings Berhad, the

remaining 30% is owned by the United Kingdom‟s Friends Life Limited (“Friends

Life”). AmLife‟s board of directors, senior management and consultants also

consist of personnel from Friends Life.

Tapping strategic partnership with global insurance

partner

AMMB Holdings Berhad 14

Corporate Information – AMMB Holdings Berhad

Date of Incorporation:

15 August 1991

Commencement of Business:

1991

Major Shareholders (as at 31 December 2011):

ANZ Funds Pty Ltd Amcorp Group Berhad Employees Provident Fund Board

23.8% 16.8% 14.2%

Directors (as at 31 December 2011):

Tan Sri Azman Hashim Dato‟ Azlan Hashim Tun Mohammed Hanif Omar Tan Sri Datuk Clifford Francis Herbert Tan Sri Datuk Dr Aris Othman Datuk Rohana Tan Sri Mahmood Dato‟ Izham Mahmud (resigned with effect from 15 October 2011) Alexander Vincent Thursby Dr Robert John Edgar Mark David Whelan Cheah Tek Kuang (resigned with effect from 2 April 2012) Ashok Ramamurthy (appointed with effect from 2 April 2012) Soo Kim Wai Alistair Marshall Bulloch (alternate director to Alexander Vincent Thursby and Mark David Whelan) Mark Timothy Robinson (alternate director to Dr Robert John Edgar)

Auditor:

Ernst & Young

Listing:

Main Market of Bursa Malaysia

Group Key Management:

Cheah Tek Kuang Ashok Ramamurthy Datuk Mohamed Azmi Mahmood Dato‟ James Lim Cheng Poh Kok Tuck Cheong Pushpa Rajadurai Yvonne Phe Kheng Peng Teng Chean Choy Duncan Victor Brain Datuk Mahdi Murad Dato‟ Wan Zamri bin Wan Zain Adrian John Nurse Andrew Strain Kerr Ross Neil Foden Charles Tan Keng Lock Thein Kim Mon Wong Jee Seng Sim How Chuah Tan Chin Aun

Group Managing Director (resigned with effect from 2 April 2012) Deputy Group Managing Director and Chief Financial Officer (appointed as Group Managing Director with effect from 2 April 2012) Managing Director, Retail Banking Managing Director, Business Banking Managing Director, Investment Banking Managing Director, Corporate & Institutional Banking Managing Director, Markets Division Managing Director, Group Managing Director‟s Office Chief Executive Officer – AmG Insurance Berhad Chief Executive Officer – AmIslamic Bank Berhad Chief Executive Officer – AmFamily Takaful Berhad Acting Chief Executive Officer – AmLife Insurance Berhad Chief Risk Officer Chief Operations Officer Chief Information Officer Chief Internal Auditor Senior General Manager, Group Corporate Strategy Senior General Manager, Business Banking Senior General Manager, Transaction Banking

Major Subsidiaries:

AmBank (M) Berhad AmIslamic Bank Berhad AmInvestment Bank Berhad AMFB Holdings Berhad AMAB Holdings Sdn Bhd AmInvestment Group Berhad AmG Insurance Berhad AmLife Insurance Berhad AmFamily Takaful Berhad

100% 100% 100% 100% 100% 100% 51% 70% 70%

***** ***** - ***,***

AMMB Holdings Berhad 15

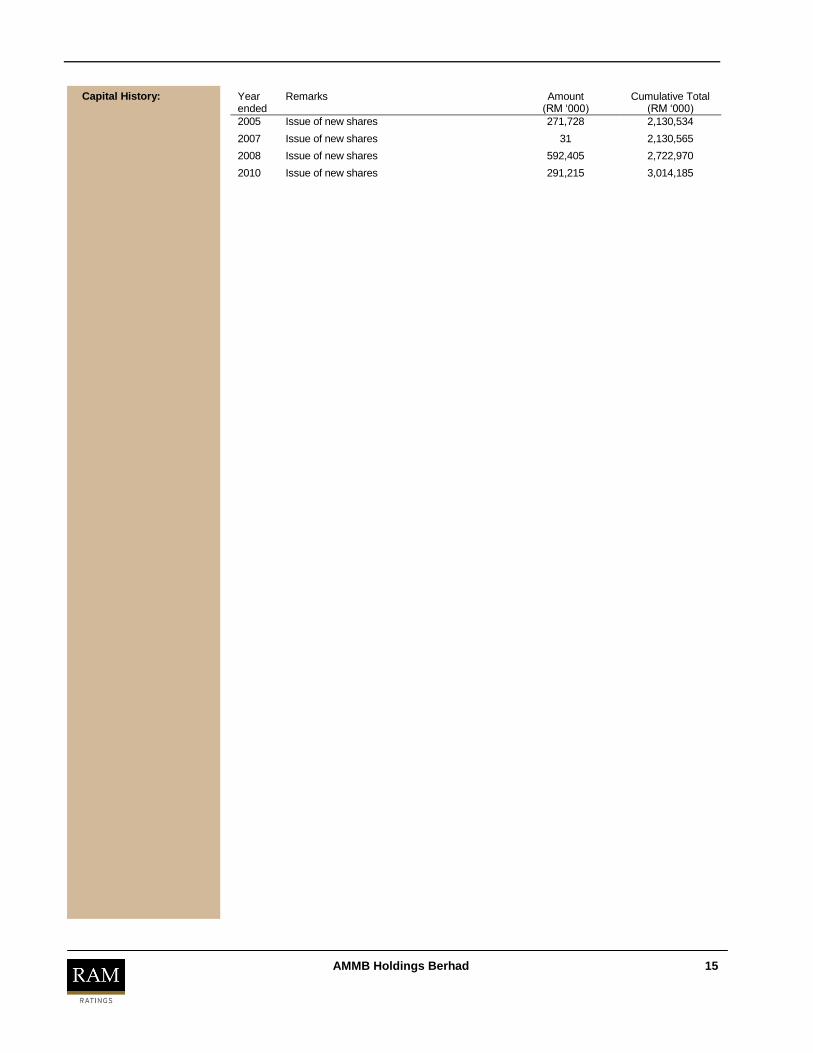

Capital History:

Year ended

Remarks Amount (RM „000)

Cumulative Total (RM „000)

2005 Issue of new shares 271,728 2,130,534

2007 Issue of new shares 31 2,130,565

2008 Issue of new shares 592,405 2,722,970

2010 Issue of new shares 291,215 3,014,185

AMMB Holdings Berhad 16

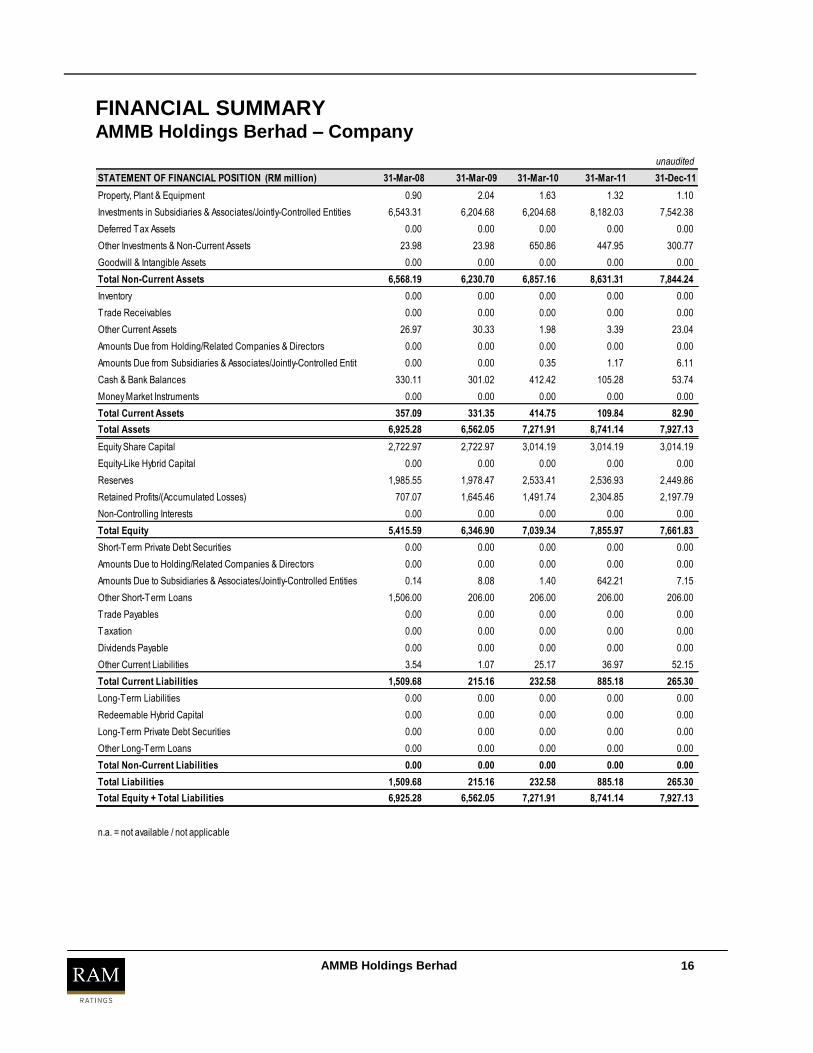

unaudited

STATEMENT OF FINANCIAL POSITION (RM million) 31-Mar-08 31-Mar-09 31-Mar-10 31-Mar-11 31-Dec-11

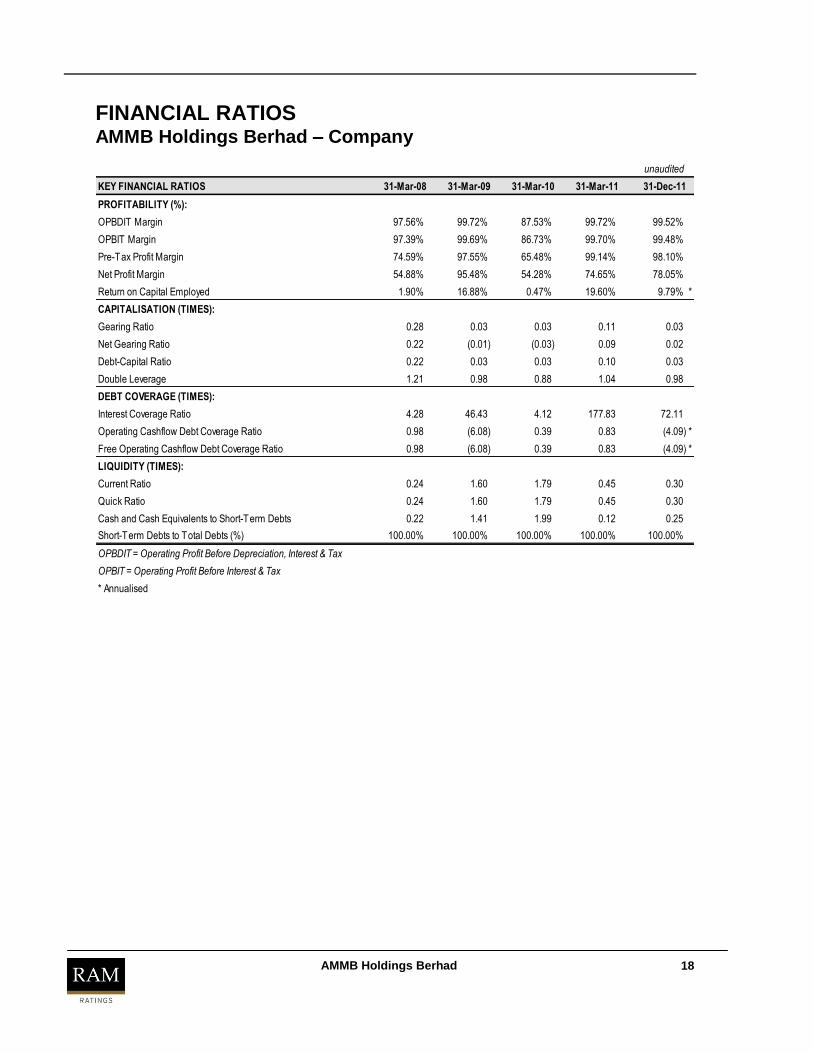

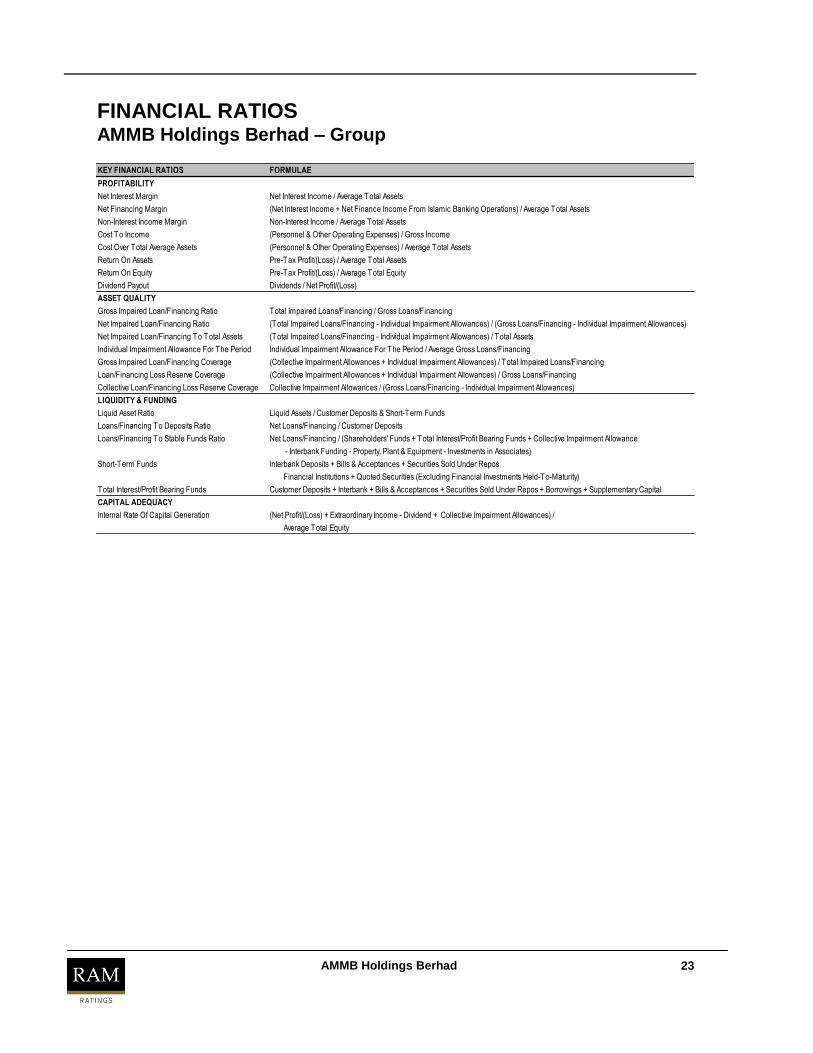

Loans/Financing To Deposits Ratio Net Loans/Financing / Customer Deposits

Loans/Financing To Stable Funds Ratio Net Loans/Financing / (Shareholders' Funds + Total Interest/Profit Bearing Funds + Collective Impairment Allowance

Total Interest/Profit Bearing Funds Customer Deposits + Interbank + Bills & Acceptances + Securities Sold Under Repos + Borrowings + Supplementary Capital

CAPITAL ADEQUACY

Internal Rate Of Capital Generation (Net Profit/(Loss) + Extraordinary Income - Dividend + Collective Impairment Allowances) /

Average Total Equity

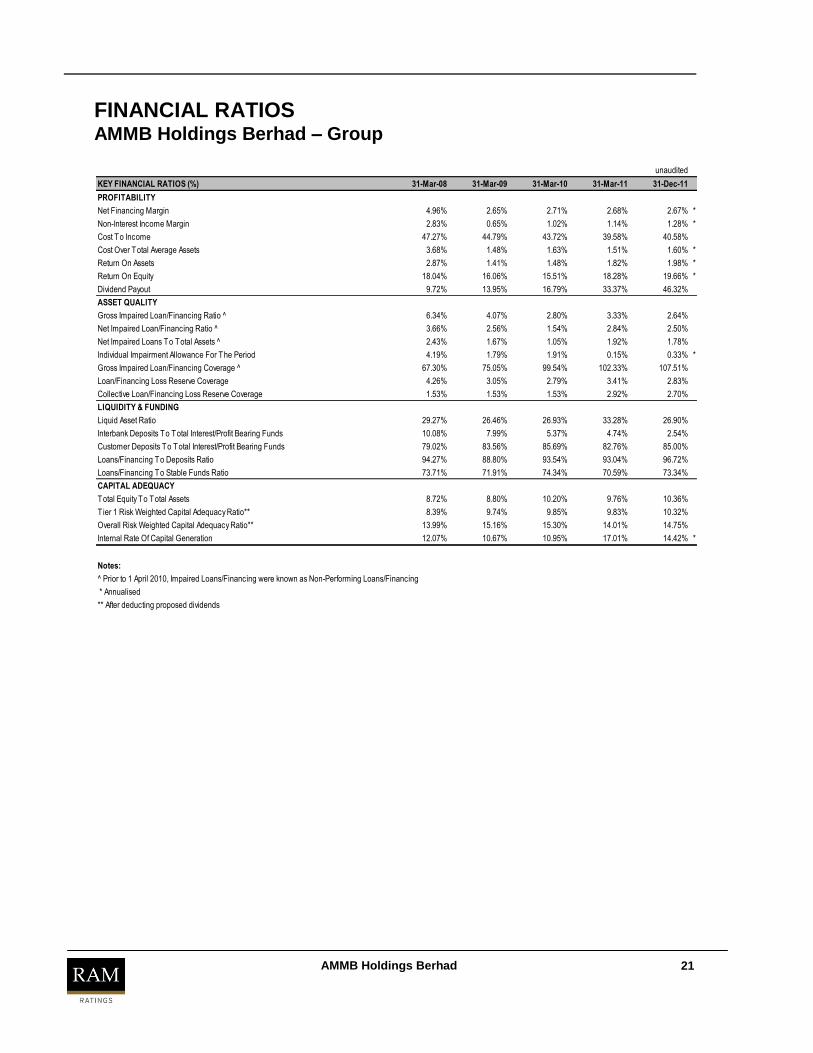

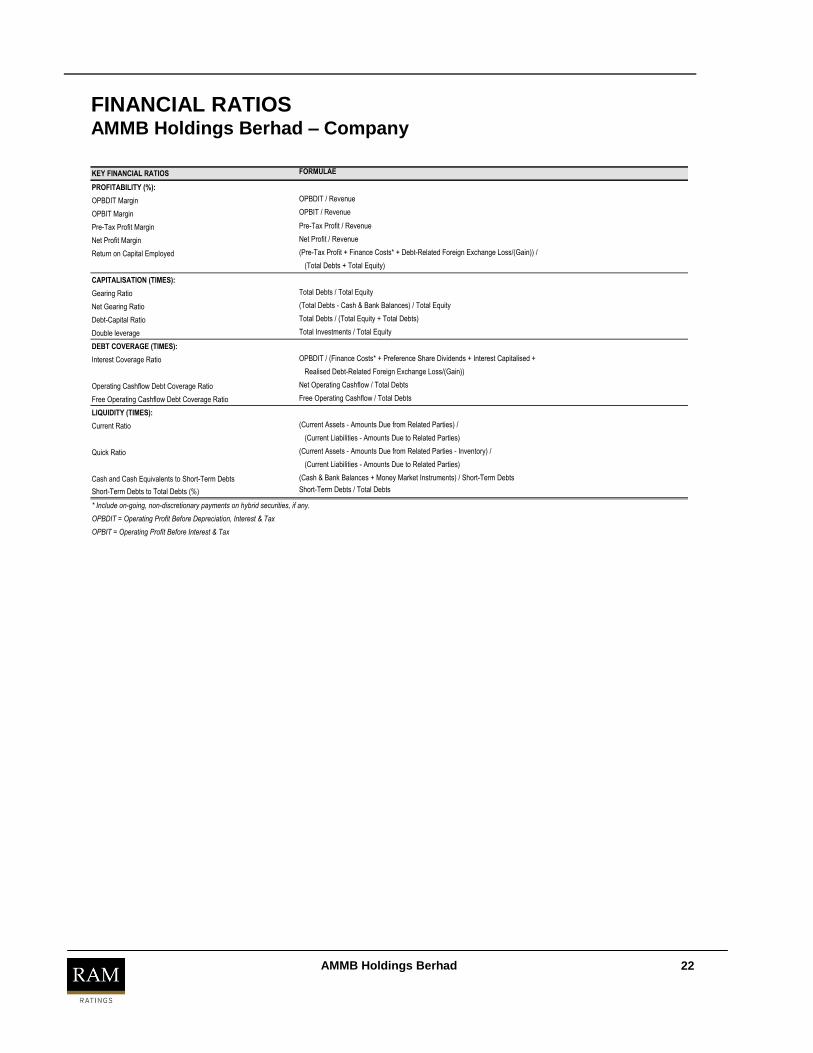

FINANCIAL RATIOS AMMB Holdings Berhad – Group

AMMB Holdings Berhad 24

CREDIT RATING DEFINITIONS

Corporate Credit Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

An entity rated AAA has a superior capacity to meet its financial obligations. This is the highest long-term CCR assignedby RAM Ratings.

An entity rated AA has a strong capacity to meet its financial obligations. The entity is resilient against adverse changesin circumstances, economic conditions and/oroperating environments.

An entity rated A has an adequate capacity to meet its financial obligations. The entity is more susceptible to adversechanges in circumstances, economic conditions and/or operating environments than those in higher-rated categories.

An entity rated BBB has a moderate capacity to meet its financial obligations. The entity is more likely to be weakened byadverse changes in circumstances, economic conditions and/or operating environments than those in higher-rated

categories. This is the lowest investment-grade category.

An entity rated BB has a weak capacity to meet its financial obligations. The entity is highly vulnerable to adversechanges in circumstances, economic conditions and/or operating environments.

An entity rated B has a very weak capacity to meet its financial obligations. The entity has a limited ability to withstandadverse changes in circumstances, economic conditions and/oroperating environments.

An entity rated C has a high likelihood of defaulting on its financial obligations. The entity is highly dependent onfavourable changes in circumstances, economic conditions and/or operating environments, the lack of which would likely

result in it defaulting on its financial obligations.

An entity rated D is currently in default on either all or a substantial portion of its financial obligations, whether or notformally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the entity that

could jeopardise thepayment of financial obligations.

An entity rated P1 has a strong capacity to meet its short-term financial obligations. This is the highest short-term CCRassigned by RAM Ratings.

An entity rated P2 has an adequate capacity to meet its short-term financial obligations. The entity is more susceptible tothe effects of deteriorating circumstances than those in the highest-rated category.

An entity rated P3 has a moderate capacity to meet its short-term financial obligations. The entity is more likely to beweakened by the effects of deteriorating circumstances than those in higher-rated categories. This is the lowest

investment-grade category.

An entity rated NP has a doubtful capacity to meet its short-term financial obligations. The entity faces major uncertaintiesthat could compromise its capacity forpayment of financial obligations.

An entity rated D is currently in default on either all or a substantial portion of its financial obligations, whether or notformally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the entity that

could jeopardise thepayment of financial obligations.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that theentity ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3 indicates that the

entity ranks at the lower end of its generic rating category.

A Corporate Credit Rating (“CCR”) is RAM Ratings' current opinion on the overall capacity of an entity to meet its financialobligations. The opinion is not specific to any particular financial obligation, as it does not take into account the expressedterms and conditions of any specific financial obligation.

AMMB Holdings Berhad 25

CREDIT RATING DEFINITIONS

Issue Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

An issue rated AAA has superior safety for payment of financial obligations . This is the highest long-term Issue Rating

assigned by RAM Ratings .

An issue rated AA has high safety for payment of financial obligations . The issuer is resilient against adverse changes in

An issue rated C has a high likelihood of default . The issuer is highly dependent on favourable changes in circumstances ,

economic conditions and/or operating environments, the lack of which would likely result in it defaulting on a particular

debt issue .

An issue rated D is either currently in default or faces imminent default on its financial obligations, whether or not formally

declared . The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise the payment of a particular debt issue .

An issue rated P1 has high safety for payment of financial obligations in the short term . This is the highest short -term

Issue Rating assigned by RAM Ratings .

An issue rated P2 has adequate safety for payment of financial obligations in the short term . The issuer is more

susceptible to the effects of deteriorating circumstances than those in the highest -rated category .

An issue rated P3 has moderate safety for payment of financial obligations in the short term . The issuer is more likely to

be weakened by the effects of deteriorating circumstances than those in higher -rated categories . This is the lowest

investment -grade category.

An issue rated NP has doubtful safety for payment of financial obligations in the short term . The issuer faces major

uncertainties that could compromise its capacity for payment of a particular debt issue .

An issue rated D is either currently in default or faces imminent default on its financial obligations, whether or not formally

declared . The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise the payment of a particular debt issue .

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that the

issue ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking ; and the subscript 3 indicates that the

issue ranks at the lower end of its generic rating category . In addition, RAM Ratings applies the suffixes (bg) or (s) to ratings which have

been enhanced by a bank guarantee or other supports, respectively .

An Issue Rating is RAM Ratings' current opinion on the creditworthiness of a particular debt issue. It reflects the overallcapacity and willingness of an issuer to meet the financial obligations on a particular debt issue on a full and timely basis,taking into account its expressed terms and conditions .

AMMB Holdings Berhad 26

RAM Ratings receives compensation for its rating services, normally paid by the issuers of such securities or the rated entity, and sometimes

third parties participating in marketing the securities, insurers, guarantors, other obligors, underwriters, etc. The receipt of this compensation has

no influence on RAM Ratings‟ credit opinions or other analytical processes. In all instances, RAM Ratings is committed to preserving the

objectivity, integrity and independence of its ratings. Rating fees are communicated to clients prior to the issuance of rating opinions. While RAM

Ratings reserves the right to disseminate the ratings, it receives no payment for doing so, except for subscriptions to its publications.

RAM Ratings, its rating committee members and the analysts involved in the rating exercise have not encountered and/or are not aware of any

conflict of interest relating to the rating exercise. RAM Ratings will adequately disclose all related information in the report if there are such

instances.

Published by RAM Rating Services Berhad

Reproduction or transmission in any form is prohibited except by