39

An assessmen Stability in Trin using micro and indic Varuna L PhD. Ca SALISES, UWI nt of Financial nidad & Tobago macroprudential cators L. Ramlal andidate I, St. Augustine

| Date post: | 29-Apr-2018 |

| Category: |

Documents |

| Upload: | phungkhanh |

| View: | 214 times |

| Download: | 1 times |

An assessment of Financial Stability in Trinidad & Tobago

using micro and indicators

Varuna L. PhD. Candidate

SALISES, UWI, St. Augustine

An assessment of Financial Stability in Trinidad & Tobago

using micro and macroprudentialindicators

L. RamlalPhD. Candidate

SALISES, UWI, St. Augustine

Financial Stability (FS)

Schinasi (2004) identified 4 key elements:

1. The broadness of FS must be considered and this includes its effects on the various aspects such as the types of institutions, market structures.

2. The efficiency of the payment system FS in an economy.

3. Financial stability ensures not only an financial crisis, but an ability of the system to repair crises as they begin to occur.

4. Financial stability affects the workings of the economy in general and has far-reaching consequences that extend beyond the activity of the firm

Financial Stability (FS)

(2004) identified 4 key elements:

of FS must be considered and this includes its effects on the various aspects such as the types of institutions, market structures.

efficiency of the payment system is imperative to

Financial stability ensures not only an absence of ability of the system to repair

as they begin to occur.

Financial stability affects the workings of the economy reaching consequences that

extend beyond the activity of the firm.

FS defined in TT

Andrew Crockett (2005) “Financial stability requires that (i) the key institutions in the financial system are stablehigh degree of confidence that they can continue to meet their contractual obligations without interruption or outside assistance, and (ii) the key markets are stableparticipants can confidently transact in them at prices that reflect fundamental forces and that do not vary substantially over short periods when there have been no changes in fundamentals.”

FS defined in TT

Andrew Crockett (2005) “Financial stability key institutions in the

financial system are stable, in that there is a high degree of confidence that they can continue to meet their contractual obligations without interruption or outside assistance, and

key markets are stable, in that participants can confidently transact in them at prices that reflect fundamental forces and that do not vary substantially over short periods when there have been no changes in

Financial

� Financial stability: ability of the market to withstand shocks that stem from the financial system without experiencing major upheaval

� Indicators of financial stability usually calculated at the micro level and macro level

� Microprudential indicators: individual financial institutions' health

� Macroprudential indicators: health of the system as a whole

Financial Stability

Financial stability: ability of the market to withstand shocks that stem from the financial system without experiencing major upheaval

Indicators of financial stability usually calculated at the micro level and macro level

Microprudential indicators: individual financial

Macroprudential indicators: health of the system

Importance of FS

� The recent global financial crisis has encouraged interest in the area of financial stability and central banks now conduct stress tests regularly to determine how well the system can withstand financial upheaval

� In Trinidad & Tobago the CBTT produces a FS report every six months

Importance of FS

The recent global financial crisis has encouraged interest in the area of financial stability and central banks now conduct stress tests regularly to determine how well the system can withstand financial upheaval

In Trinidad & Tobago the CBTT produces a FS report every six months

Assessment of FS

� Microprudential indicators, usually aggregated; CAMELS (Evans et al 2000)

� C – Capital adequacy

� A – Asset quality

� M – Management soundness

� E - Earnings

� L - Liquidity

� S – Sensitivity to market risk

Assessment of FS

Microprudential indicators, usually aggregated; CAMELS (Evans et al 2000)

Management soundness

Sensitivity to market risk

Assessment of FS cont'd

� Macroprudential and macroeconomic indicators

� Economic growth

� BOP

� Inflation

� Interest and exchange rates

� Lending and asset price booms

� Contagion effects

� Other factors

Assessment of FS cont'd

Macroprudential and macroeconomic indicators

Interest and exchange rates

Lending and asset price booms

Indicators used in TT

� TT follows the CAMELS structure included for each section

� TT also reports major macroeconomic indicators

� According to Evans et al (2000) this is the best approach to properly determine FS in an economy

Indicators used in TT

TT follows the CAMELS structure – indicators included for each section

TT also reports major macroeconomic

According to Evans et al (2000) this is the best approach to properly determine FS in an

Regulation in TT

� Insurance Act (1980) and Insurance Amendements (2004, 2007, 2009)

� Companies Act (1995), amended in 1999, 2003

� Central Bank Act (and amendments)

� Securities Industry Act

� Finance Act and amendments

� Financial Institutions Act

� Also various other CB guidelines which are not mandatory but strongly suggested

Regulation in TT

Insurance Act (1980) and Insurance (2004, 2007, 2009)

Companies Act (1995), amended in 1999, 2003

Bank Act (and amendments)

Finance Act and amendments

Financial Institutions Act

Also various other CB guidelines which are not mandatory but strongly suggested

GENERAL MACROECONOMIC ENVIRONMENT IN TRINIDAD & TOBAGO

GENERAL MACROECONOMIC ENVIRONMENT IN TRINIDAD & TOBAGO

Graph showing growth in TT

1998 2000 2002 2004 2006 2008

-10

-5

0

5

10

15

20

25

30

35

Growth Rates - TT 2000 to 2010 - Selected Sectors

Graph showing growth in TT

2010 2012

Growth Rates - TT 2000 to 2010 - Selected Sectors

Real GDP Growth - Non-Petroleum Sector - 2000=100

Real GDP Growth - Finance Insurance & Real Estate - 2000=100

Real GDP Growth - Petroleum Sector - 2000=100

Real GDP Growth - Total - 2000=100

Trade summary TT

1998 2000 2002 2004 2006

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Net Exports 2000-2010

Trade summary TT

2006 2008 2010 2012

Net Exports 2000-2010

Balance of Trade

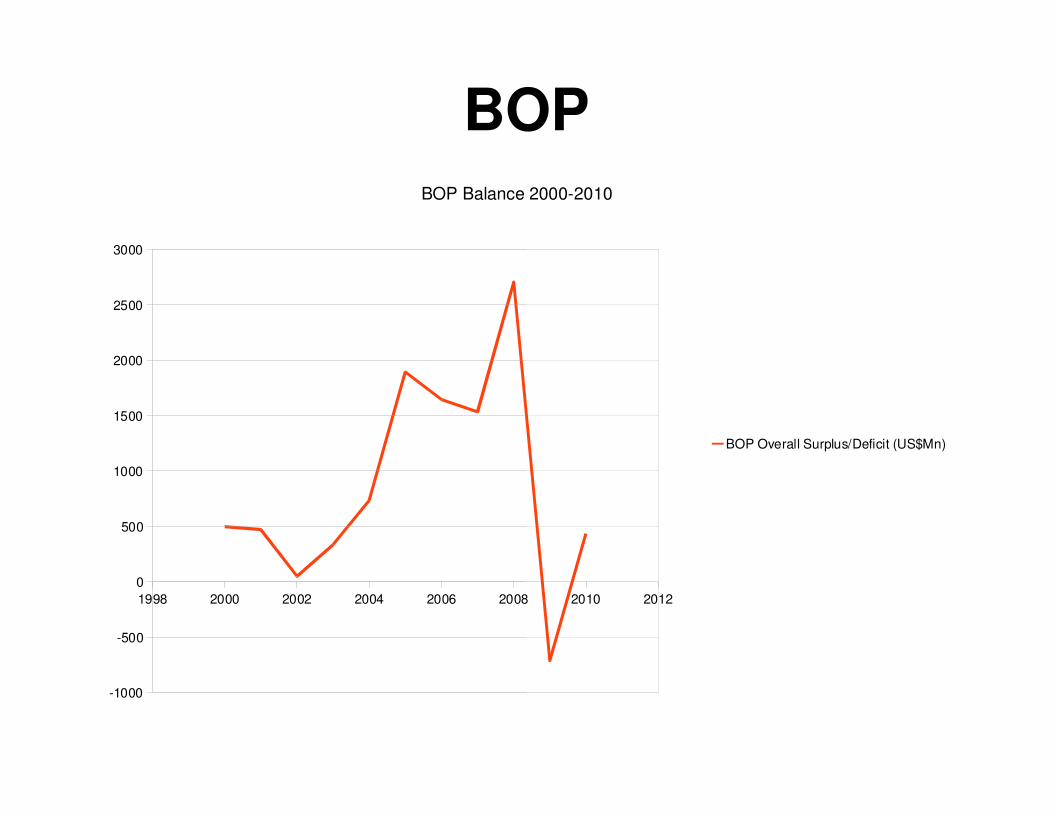

BOP

1998 2000 2002 2004 2006 2008

-1000

-500

0

500

1000

1500

2000

2500

3000

BOP Balance 2000-2010

BOP

2008 2010 2012

BOP Balance 2000-2010

BOP Overall Surplus/Deficit (US$Mn)

Unemployment Rate TT

1998 2000 2002 2004 2006

0

2

4

6

8

10

12

14

Unemployment Rate 2000-2010

Unemployment Rate TT

2008 2010 2012

Unemployment Rate 2000-2010

Unemployment Rate (%)

Employment

1998 2000 2002 2004 2006 2008

0

50

100

150

200

250

300

350

400

Employment in TT 2000 to 2010 - Selected Sectors

Employment - Sector

2010 2012

Employment in TT 2000 to 2010 - Selected Sectors

Employment in Agriculture (000's)

Employment in Construction (incl.Electricity & Water) - (000's)

Employment in Manufacturing (000's)

Employment in All Other Sectors (000's)

Employment in Petroleum & Gas (000's)

Government

1998 2000 2002 2004 2006 2008

-10000000

-5000000

0

5000000

10000000

15000000

Central Government Fiscal Balance

Government

2008 2010 2012

Central Government Fiscal Balance

Central Gov't Overall Fiscal Balance (TT$000s)

Gov't

1998 2000 2002 2004 2006 2008

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

Central Government Revenue - Oil and Non-Oil

Gov't

2008 2010 2012

Central Government Revenue - Oil and Non-Oil

Central Gov't Current Revenue Non Oil (TT$000s)

Central Gov't Current Revenue - Oil (TT$000s)

Gov't

1998 2000 2002 2004 2006 2008

0

5000

10000

15000

20000

25000

30000

35000

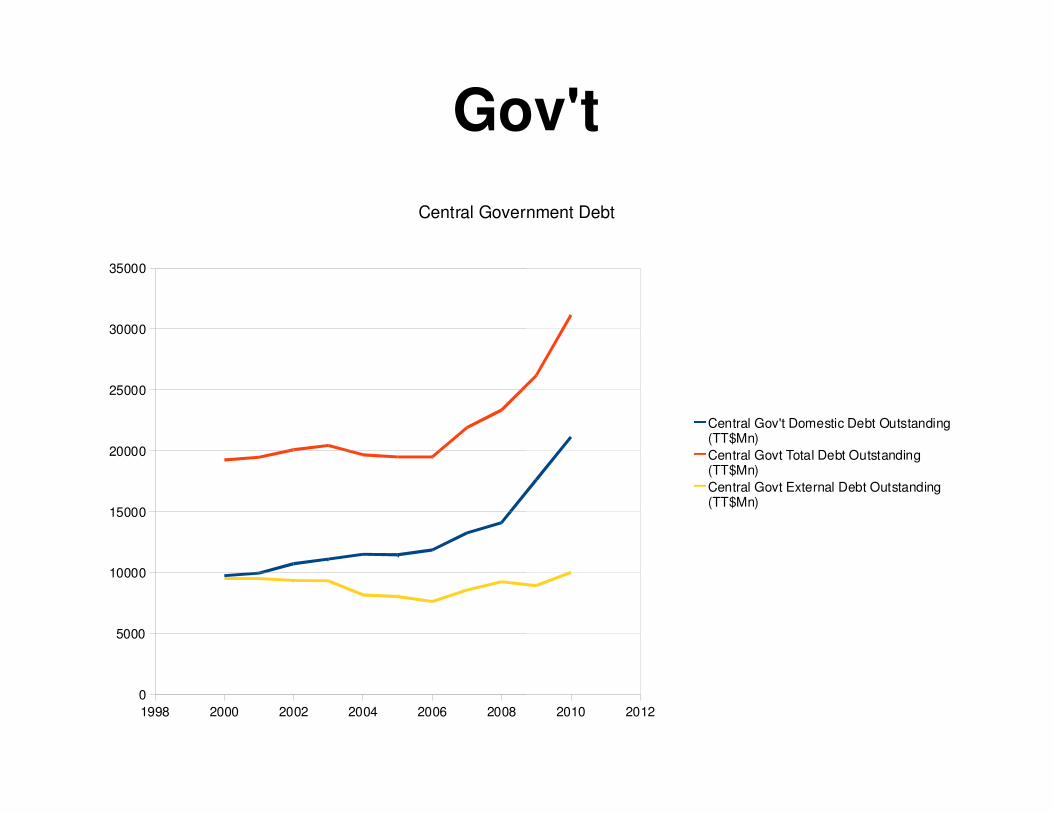

Central Government Debt

Gov't

2010 2012

Central Government Debt

Central Gov't Domestic Debt Outstanding (TT$Mn)

Central Govt Total Debt Outstanding (TT$Mn)

Central Govt External Debt Outstanding (TT$Mn)

Gov't

1998 2000 2002 2004 2006 2008

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

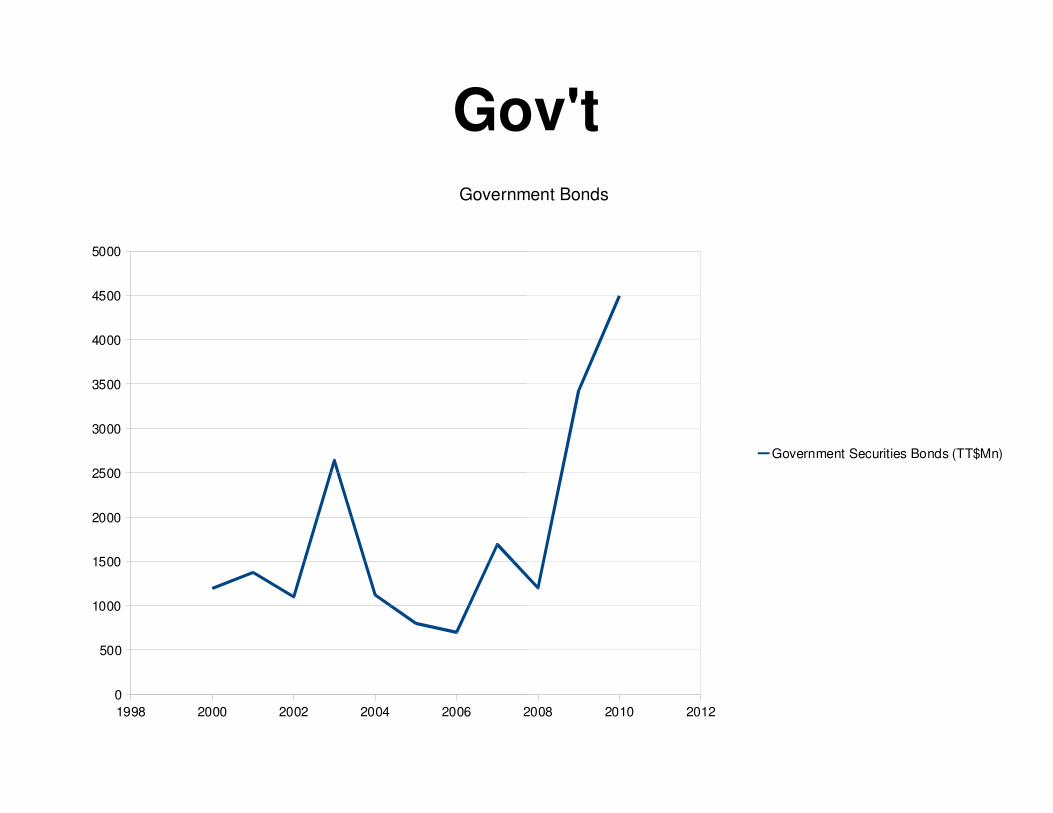

Government Bonds

Gov't

2008 2010 2012

Government Bonds

Government Securities Bonds (TT$Mn)

Reserves

1998 2000 2002 2004 2006 2008

0

2000

4000

6000

8000

10000

12000

Foreign Reserves TT

Reserves

2008 2010 2012

Foreign Reserves TT

T&T Net Foreign Position - US$ Millions

Net Official Reserves - US$ Millions

AGGREGATED

MICROPRUDENTIAL

INDICATORS

AGGREGATED

MICROPRUDENTIAL

INDICATORS

C – Capital Adequacy

2000 2002 2004 2006 2008

0

5

10

15

20

25

30

Capital Adequacy

Capital Adequacy

2010 2012

Capital Adequacy

Regulatory capital to risk-weighted assets

Regulatory Tier1 Capital to Risk-Weighted Assets

Regulatory Tier2 Capital to Risk-Weighted Assets

Regulatory capital to total assets

A - Assets

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005 2006 2007

Non - Performing Loans

Assets

2007 2008 2009 2010 2011

Performing Loans

NPLs: Gross loans

NPL(net of prov) to K

A – Assets

2000 2002 2004 2006 2008

-20

0

20

40

60

80

100

120

140

Asset Quality

Assets

2008 2010 2012

Asset Quality

NPLs: Gross loans

NPL(net of prov) to K

Specific prov: impaired assets

Specific prov: gross lending

A - Assets

2000 2002 2004 2006 2008

0

5

10

15

20

25

30

35

40

45

Asset Structure - Banking Sector

Assets

2010 2012

Asset Structure - Banking Sector

Loans to Hhs: Total Loans

Fin. Sector Loans: Total Loans

Oil and gas loans: Total loans

Construction loans: total loans

Transport and communication loans: total loans

Non-resident loans: total loans

A - Assets

0

10000

20000

30000

40000

50000

60000

70000

80000

1998 2000 2002 2004 2006 2008

Commercial Banks

Assets

2010 2012

Commercial Banks

Commercial Banks: Total Deposits (TT$Mn)

Commercial Banks: Total Loans - TT$Mn

M – Management Soundness

2000 2001 2002 2003 2004 2005 2006 2007

0

50

100

150

200

250

300

No. of Financial Institutions

Management Soundness

2007 2008 2009

No. of Financial Institutions

Comm. Banks

Fin. Companies & Merch Banks

Trust & Mortgage Fin Companies

Dev. Banks

Cr. unions

Ins. Companies

Thrift Instit'ns

NIB

Stk. Ex.

Unit Trust Corp

Home Mortg. Bank

Priv. Registered Pension Plans

M – Mgt. Soundness

2000 2001 2002 2003 2004 2005 2006

0

2

4

6

8

10

12

14

Financial Institutions

Excl. Cr. Unions, Ins. Cos and Pension Plans

Mgt. Soundness

2007 2008 2009

Financial Institutions

Excl. Cr. Unions, Ins. Cos and Pension Plans

Comm. Banks

Fin. Companies & Merch Banks

Trust & Mortgage Fin Companies

Dev. Banks

Thrift Instit'ns

NIB

Stk. Ex.

Unit Trust Corp

Home Mortg. Bank

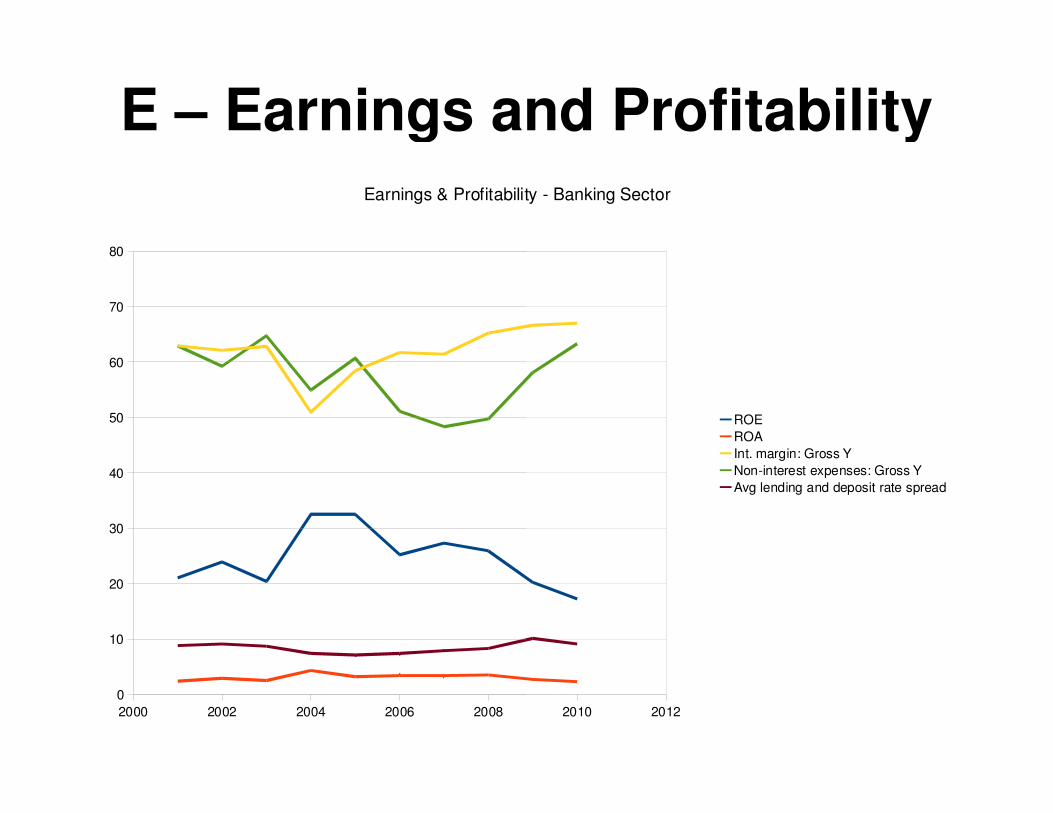

E – Earnings and Profitability

2000 2002 2004 2006 2008

0

10

20

30

40

50

60

70

80

Earnings & Profitability - Banking Sector

Earnings and Profitability

2010 2012

Earnings & Profitability - Banking Sector

ROE

ROA

Int. margin: Gross Y

Non-interest expenses: Gross Y

Avg lending and deposit rate spread

L - Liquidity

2000 2002 2004 2006 2008

0

20

40

60

80

100

120

140

160

180

Liquidity

Liquidity

2010 2012

Liquidity

LA:TA

LA:Srun Liab

Cust dep: total loans(excl interbank)

For. Currency liab:total liab

S – Sensitivity to Risk

2003 2004 2005 2006 2007 2008 2009

0

50

100

150

200

250

300

350

400

RPI 2000 to 2010

Sensitivity to Risk

2009 2010 2011

RPI 2000 to 2010

Index of Retail Prices - Food - (Jan. 03=100)

Index of Retail Prices - Housing - (Jan. 03=100)

Index of Retail Prices - Core (Jan. 03 = 100)

Interest rates TT

1998 2000 2002 2004 2006 2008

0

2

4

6

8

10

12

14

16

18

Commercial Banks Interest Rates

Interest rates TT

2010 2012

Commercial Banks Interest Rates

Commercial Banks: Demand Loans Rate (%)

Commercial Banks: Ordinary Savings Deposit Rate (%)

Commercial Banks: Basic Prime Lending Rate (%)

Exchange Rates TT

1998 2000 2002 2004 2006

0

2

4

6

8

10

12

14

Exchange Rates

Exchange Rates TT

2006 2008 2010 2012

Exchange Rates

US Selling

Barbados Selling Rate

Canadian Selling Rate

EC Selling

Euro Selling

Pound Selling

Stock market index TT

1998 2000 2002 2004 2006 2008

0

200

400

600

800

1000

1200

TT Composite Stock Price Index - Annual: 2000-2010

Stock market index TT

2008 2010 2012

TT Composite Stock Price Index - Annual: 2000-2010

Composite Stock Price Index (1983=100)

Stock Market

1998 2000 2002 2004 2006 2008

0

50

100

150

200

250

300

350

400

450

Volume of Shares Traded

Stock Market - TT

2008 2010 2012

Volume of Shares Traded

Volume of Shares Traded - TTSE ($Mn)

Financial stability

� Financial stability indicates an ability to recover from financial turmoil and a resilience to resist major negative effects of a financial crisis

� The economy of Trinidad & Tobago was not immune to the recent financial crisis of 2008

� Reaction was delayed but significant

� Recovery process still proceeding

� Financial system remained mostly stable

Financial stability

Financial stability indicates an ability to recover from financial turmoil and a resilience to resist major negative effects of a financial crisis

The economy of Trinidad & Tobago was not immune to the recent financial crisis of 2008

Reaction was delayed but significant

Recovery process still proceeding

Financial system remained mostly stable

FS -

� 2009 was the difficult year here

� Some negatives seen in deficit, growth rates fell, unemployment rising, fiscal balance negative

� Our exchange rate remained fairly stable good, indicates strong reserve

� Some recovery in 2010

- TT

2009 was the difficult year here – CLICO crisis

Some negatives seen in macroeconomy: BOP deficit, growth rates fell, unemployment rising, fiscal balance negative

exchange rate remained fairly stable –good, indicates strong reserve position

Some recovery in 2010

Policy Suggestions

� Improve regulation

� Boost investor & firm awareness

� Educate the general public

Policy Suggestions

& firm awareness

Educate the general public

The EndThe End