an economic impact and future growth study of Ontario’s high-value insurance sector over 300 firms firms with less than 10% employment growth projected over next 3 years firms with more than 10% employment growth projected over next 3 years

Transcript

for more information visit www.insureconomy.ca

an economic impact and future growth study of Ontario’s high-value insurance sector

over 300 �rms

�rms with less t

han 10% employment growth projected over next 3

years

�rms with more than 10% employment growth projected over n

ext 3 years

�is document is a summary of two reports prepared for the Insurance Bureau of Canada. �e �rst was prepared by the Conference Board of Canada and is entitled Assessing the Impact of Ontario’s P&C Insurance Industry: An economic footprint analysis (2011). In this report, the Conference Board has developed a broad economic impact assessment of the property and casualty insurance industry in Ontario including direct and indirect employment, gross domestic product, direct and indirect tax bene�ts to government and other impacts of the industry on the provincial economy.�e second report, prepared by Jupia Consultants Inc., is entitled Ontario's P&C Insurance Industry: Strengthening �e Cluster (2011), and includes an assessment of the size and scope of the industry, its regional impacts across Ontario and its potential for future growth. �e report also highlights some of the challenges facing the industry moving forward.

Prepared for:

Prepared by:

Report Partner:

JULY 2011

Ontario Insurance Industry: Summary Report

1. Insurance Matters: A Critical Service for Residents and Businesses 1

2. An Important Economic Engine for Ontario 2

3. A National/International Economic Footprint 4

4. Insurance Spending in Ontario Stays in Ontario 5

5. Providing Economic Benefit to All Regions of Ontario 6

6. Insurance Brokers: Local Economic Impact Across Ontario 7

7. An Industry Dominated by Small and Medium Sized Businesses 7

8. Ontario: A Global Insurance Hub 8

9. Prospects for Further Growth 10

10. Top Challenges Facing the Industry 11

11. Conclusion 11

: Table of Contents

Ontario Insurance Industry: Summary Report

Insurance plays a critical role in the Ontario economy by assuming part of the financial risk inherent in running a business, driving a car, or owning or renting a home. The property and casualty (P&C) insurance industry touches the lives of just about every resident and business across Ontario by providing insurance protection for most homes, motor vehicles and commercial enterprises. The business of insurance is to limit the risk of unexpected events.

The P&C insurance industry, in addition to paying for losses, works to prevent them. For decades, P&C insurers and the Insurance Bureau of Canada (IBC) have worked in partnership with communities and officials on road safety, fire prevention, anti-theft campaigns and many other projects. Most recently, the industry has encouraged governments nationwide to develop a comprehensive strategy to deal with the effects of the increasing number of severe weather events resulting from climate change.

In 2009, the property and casualty insurance industry paid out in Ontario over $14.5 billion in net claims for personal property, commercial property, auto, liability as well as other types of insurance coverage.

1. Insurance Matters: a critical service for residents and businesses

1

did you know?

Ontario Insurance Industry: Summary Report

The insurance industry in Ontario is made up of over 6,000 business establishments employing more than 77,000 people. Nearly 47,000 of these jobs are in the insurance carrier sector and over 30,000 are in the insurance agencies, brokerages and other insurance related activities sector. More than two out of every hundred people employed in the private sector in Ontario works for the insurance industry. This is more employed Ontarians than in the real estate sector, the accommodation sector and the architectural, engineering and related services sector, to name a few.

The insurance industry as a whole contributes more gross domestic product (GDP) to the Ontario economy than the motor vehicle parts manufacturing sector, the entire agriculture, forestry, fishing and hunting sectors combined and the province’s universities sector.

Property & Casualty Insurance: Economic Footprint

In 2009, the P&C insurance industry employed 22,000 people in Ontario. The Conference Board estimates that this created 41,000 additional jobs, bringing the total number of direct, indirect, and induced jobs created specifically by the P&C insurance industry to 63,000 people.

In total, the property & casualty insurance industry in Ontario directly contributed $4.1 billion to real gross domestic product (GDP) in 2009. The economic multiplier (GDP boost) for the industry is 1.81. Including the direct, indirect and induced impacts, $7.5 billion in real GDP can be attributed to the P&C insurance sector.

In 2009, the P&C insurance industry in Ontario generated $944 million in corporate income tax, nearly $1.2 billion in personal income tax, and $852 million worth of indirect tax revenues for the federal and provincial governments. This estimate does not include an estimated $563 million in premium taxes paid by P&C insurers, nor does it include $142 million in health care levies and $30.2 million in payroll and employee benefit taxes.

ONTARIO’S INSURANCE INDUSTRY: AT A GLANCE

OVER 360 Business Establishments(THE MAJORITY OF THE INDUSTRY’S HEAD OFFICES ARE LOCATED IN TORONTO)

PROPERTY & CASUALTY INSURANCE:

OVER 250 Business EstablishmentsLIFE & HEALTH INSURANCE:

Ontario is home to 63% of Canada’s Reinsurance Business Establishments. �ere are 43 FIRMS in this sector across Ontario.

REINSURANCE:

�ere are OVER 5,300 Insurance Agencies, Brokerages and Related Businesses Establishments in Ontario.

INSURANCE BROKERAGES, AGENCIES & OTHER SERVICES:

2

ECONOMIC IMPACT OF ONTARIO’S P&C INSURANCE INDUSTRY (2009)

$4.1 BILLION REAL GDP - DIRECT

$3.7 BILLION PERSONAL DISPOSABLE INCOME

$2.6 BILLION CORPORATE, PERSONAL AND INDIRECT TAXES*

$4.6 BILLION PERSONAL INCOME

$7.5 BILLION REAL GDP - TOTAL

* includes over $700 million in premium taxes, health care levies and payroll taxes paid by P&C insurers.Source: Conference Board of Canada.

2. An Important Economic Engine for Ontario

Ontario Insurance Industry: Summary Report

TAXES GENERATED $ MILLION (2009) IN ONTARIO PROPERTY AND CASUALTY INSURANCE INDUSTRY INCL. DIRECT, INDIRECT & INDUCED IMPACTS

While not captured in the Conference Board study, the insurance industry also provides at least $150 million in property tax revenue used to support municipal government across the province.1

The impact of the insurance industry goes well beyond direct employment and economic activity. Many jobs in the legal, construction, auto repair, and other sectors are indirectly linked to the sector. Indeed the sector is a necessary enabler of business and community activity of all kinds.

The impact of this economic activity is felt across multiple sectors of the economy. For example, the insurance industry supported $448 million worth of retail sales spending in 2009 across Ontario. The industry also supported $233 million worth of economic activity in the information and cultural industries segment of the provincial economy. Another $751 million was spent in the community, business and personal services segment of the economy.

Using Statistics Canada data from the household spending survey, we can estimate how the personal income generated from the P&C insurance industry is spent in the economy. The industry generates some $452 million worth of food sales each year (including restaurants) and another $1.3 billion on housing related expenses (mortgage payments, household operation and furnishings). The P&C insurance industry supports over one thousand housing starts each year across Ontario.

Some $610 million is spent on vehicles and their maintenance, public transportation and other related expenditures. Nearly a quarter of a billion dollars in recreation spending is induced by the economic activity of the P&C insurance industry.

3

Source: Conference Board and Insurance Bureau of Canada.

The average weekly earnings for the insurance industry in 2010 was $1,167 (including overtime) - an annualized salary of nearly $61,000 - the highest of the 10 provinces across Canada. The insurance industry is in the top quartile for wages among major industry groups in Ontario - 17 percent higher than manufacturing, 22 percent higher than banking and 18 percent higher than the education sector.

1 Estimated based on both personal and corporate property taxes paid.

did you know?

Ontario Insurance Industry: Summary Report

ONTARIO P&C INSURANCE FIRMS SERVING MARKETS OUTSIDE THE PROVINCE (% of total �rms)

INTERNATIONAL MARKETS 18%CANADA 79%

The majority of Ontario’s P&C insurance firms are serving more than just the provincial market from their Ontario operations. In the survey completed for this report, nearly 80 percent of P&C insurance firms indicated they provide products and/or services outside the Ontario market. Five firms work in international markets from Ontario. The average P&C insurance firm in Ontario generates more than a quarter of its total revenue from markets outside Ontario.

4

The majority of Canada’s insurance industry is headquartered in Ontario including industry leaders such as Intact Insurance, TD Insurance, Aviva Canada Inc., State Farm, RBC Insurance, Royal & Sun Alliance Insurance Company of Canada, The Dominion of Canada General Insurance Company and AXA Insurance.

3. A National/International Economic Footprint

Source: Survey of IBC member companies (Spring 2011).

did you know?

Ontario Insurance Industry: Summary Report

When an Ontarian purchases an iPod or television, buys clothing or goes to the movies most of the economic activity associated with those purchases leaves the province to support economic development elsewhere. Not so with the insurance industry. For every dollar of premium paid by a customer, upwards of 80 cents is spent within the province either directly through the cost of operations (payroll, facilities, etc.) or indirectly through the cost of claim payouts (auto body shops, law firms, medical practitioners, etc.).

5

4. Insurance Spending in Ontario Stays in Ontario

The insurance industry has one of the largest employment multipliers of any industry in Ontario. For every direct job in the insurance carrier sector, 2.8 jobs are created across the economy. Industries such as the film sector, software publishing and engineering services have far smaller employment multipliers across the province.

did you know?

ARCHITECTURAL, ENGINEERING AND RELATED

TOTAL EMPLOYMENT SUPPORTED PER DIRECT JOB (FTE)*Direct and Indirect Employment Across Ontario

4.5

2.9 2.8

2.4

2.01.91.6

1.3

MOTOR VEHICLE MANUFACTURING

NEWSPRINT MILLS INSURANCE CARRIERS

DISTILLERIES

FORESTRY & LOGGING FILM INDUSTRYPHARMACEUTICAL MANUFACTURING SOFTWARE PUBLISHERS

* FTE= Full Time Equivalent Source: Statistics Canada Input/Output tables (2007).

Ontario Insurance Industry: Summary Report

ONTARIO’S INSURANCE INDUSTRY: Firms by Geographic Region (2010)

Employment and economic activity in the insurance industry is widely distributed across the province of Ontario. Nearly half of total industry employment is located outside the Toronto metropolitan area. Adjusted for the population size, there are more insurance industry business establishments in the Hamilton to Windsor corridor than in the Toronto area.

The P&C insurance industry has a broad geographic footprint across Ontario. In the survey, 16 firms said they have more than one in around the province. Seven firms have between two and four offices in Ontario and six firms have between five and seven offices. Three companies have eight or more offices across the province.

6

5. Providing Economic Benefit to All Regions of Ontario

Source: Statistics Canada. Canadian Business Patterns ( June 2010).

Adjusted for the size of the labour force, there are more people employed by the insurance industry in the Kitchener and London metropolitan areas than in Toronto. There is also a significant concentration of insurance industry employment in places such as Guelph, Hamilton, Kingston, Oshawa, Ingersoll and Kenora.

did you know?

Ontario Insurance Industry: Summary Report

2 Estimated number of brokers derived from IBAO data. The total number of insurance agencies and brokerages in Ontario is taken from Statistics Canada’s Canadian Business Patterns ( June 2010).3 Based on Statistics Canada’s Survey of Household Spending (2009) estimate of charitable contributions.

The network of insurance brokers across Ontario is a vital part of the industry. There are an estimated 14,000 insurance brokers in Ontario working in 4,400 insurance brokerages and agencies throughout the province2 matching clients with products offered by insurance companies, and providing a variety of support services from insurance selection through to the claims process. According to Statistics Canada, there are an estimated 30,000 people directly working for insurance brokerages and other insurance related activities throughout Ontario.

A 2010 survey conducted by the Insurance Brokers Association of Ontario (IBAO) found that insurance brokers generate an annual payroll in excess of $924 million and also pay an estimated $40.8 million in business taxes per annum and another $12.6 million in annual business property taxes. There is a direct economic impact in local communities as well. The average IBAO broker purchases 82 percent of personal goods and services within their local community and the remaining 18 percent within the province of Ontario. At the firm level, the average IBAO brokerage firm purchases over 86 percent of its goods and services within their local community.

7

6. Insurance Brokers: local economic impact across ontario

According to the IBAO survey, brokerage principals and employees contribute an average of 4.3 percent of their personal income to charities, well above the one percent contributed by the average household in Ontario.3 In addition, 100 percent of the survey respondents were involved in various organizations in the community (i.e. religious, fraternal, sports, service, cultural, charitable, education or business organizations).

There are insurance industry business establishments located in over 250 Ontario communities.

Ontario is fortunate to be the head office location for most of Canada’s largest insurance companies. At the same time the vast majority of the industry’s firms are small and dispersed around the province. More than three-quarters of them have less than 10 employees and 95 percent employ fewer than 50 people.

Over 98 percent of the province’s insurance agency and brokerage establishments have less than 50 employees and 96 percent of the firms providing claims adjustment services have less than 50 employees.

7. An Industry Dominated by Small and Medium Sized Businesses

Source: Statistics Canada. Canadian Business Patterns ( June 2010).

INSURANCE FIRMS IN ONTARIO BY EMPLOYMENT LEVEL (2010)

200+ EMPLOYEES

50-199 EMPLOYEES

10-49 EMPLOYEES

UNDER 10 EMPLOYEES

did you know?

did you know?

Ontario Insurance Industry: Summary Report 8

7. An Industry Dominated by Small and Medium Sized Businesses

Based on the rankings in the Global Financial Centres Index, Toronto is a top ten global financial centre. Among the index’s sub-indices, as a location for the global insurance industry, Toronto ranks eighth in the world ahead of Sydney, Zurich and Geneva. Toronto scores well for the quality of its talent pool, business environment, infrastructure, market access and general competitiveness.

The majority of the industry’s Canadian head office activity is in Toronto and other urban centres in the province, making Ontario the locus for industry decision making. This concentration of industry activity is a catalyst for the clustering effect.

Ontario firms provide the bulk of the Canadian insurance industry’s value added, higher end back office functions. According to the survey conducted for this report, over 80 percent of firms provide claims adjudication, three-fourths of the firms provide risk management, 65 percent conduct analytics and over half undertake fraud analysis from their Ontario facilities.

The industry pulls talent from Ontario’s network of universities and colleges. Ontario is also the Canadian hub for insurance industry training led by the Insurance Institute, the educational arm of the property and casualty insurance industry.

8. Ontario: A Global Insurance Hub

GLOBAL FINANCIAL CENTRES INDEX (2011)Industry sector sub-indices (changes from last ranking in brackets)

1. LONDON HONG KONG (-)

2. NEW YORK SHANGHAI (-)

3. HONG KONG NEW YORK (-)

4. SINGAPORE LONDON (+1)

=5. SHANGHAI SINGAPORE (-1)

=5. TOKYO TOKYO (-)

7. CHICAGO CHICAGO (+1)

8. ZURICH TORONTO (+5) 9. GENEVA SYDNEY (-)

=10. TORONTO ZURICH (-3)

=10. SYDNEY GENEVA (-1)

OVERALL RANK INSURANCE

Source: Z/Yen Group. The Global Financial Centres Index (March 2011).

According to Statistics Canada, 47 percent of Canada’s mathematicians, statisticians and actuaries and 49 percent of the country’s insurance underwriters are located in Ontario.

did you know?

Ontario Insurance Industry: Summary Report

CORPORATE AND IT SERVICES OPERATING COST COMPARISON

FRANKFURT, GER

123.8

TORONTO, CAN

100.0

CHICAGO, USA

108.2

SAN FRANCISCO, USA 118.1

BOSTON, USA

112.9

NEW YORK, USA

114.4 PARIS, FRA

122.4

LONDON, UK

114.4

According to the KPMG Competitive Alternatives report for 2010, Ontario offers a significant overall cost advantage for back office operations. For example, compared to other global financial centres such as New York and London in the United Kingdom, Toronto is a very competitive location. Other smaller urban centres such as Kingston, Windsor and St. Catharines also offer a reasonable cost environment for back office, customer service and information technology centres. The cost advantages include lower payroll costs, lower facilities costs and a reduced tax burden.

9

For Locations Sensitive Costs.Source: KPMG Competitive Alternatives 2010.

Ontario Insurance Industry: Summary Report

4 Partnership and Action: Mobilizing Toronto’s Financial Sector for Global Advantage. Boston Consulting Group. November 2009.

The insurance industry has been growing steadily in Ontario since 2005. Insurance carriers have increased their workforce by 18 percent since 2005. Overall, the insurance industry increased total employment by over 12 percent - well above the overall provincial employment growth rate of only four percent. Between 2005 and 2010, the gross domestic product generated by the insurance sector increased by more than 15 percent, outstripping the majority of other sectors in the economy.

The P&C segment of the insurance industry has been leading this employment expansion. According to the survey conducted for this report, two thirds of the firms have increased their employment in the past three years and only 10 percent cut their total employment. Seventy percent of the firms have plans to expand their workforce over the next three years.

The insurance industry has potential for significant further growth by adding more value added services and expanding its national and international reach. In its 2009 report for the Toronto Financial Services Alliance4, the Boston Consulting Group identified six activities with potential for insurance industry expansion in the Toronto area including:

• Risk management analytics

• Premium calculation

• Claim adjudication

• Fraud analysis

• Statistical risk calculation

• Web/phone/channel customer service/sales

However, according to the survey conducted for this report, the P&C insurance companies had a mixed outlook for their business prospects in Ontario. The longer term (4-5 years) outlook for the industry is stronger than the short term (next 24 months) outlook.

9. Prospects for Further Growth

0

4% 36% 57% 4%

26% 67% 7%

4%4% 4% 89%

20 40 60 80 100

LONGER TERM

MEDIUM TERM

SHORT TERM

POOR FAIR GOOD EXCELLENTOUTLOOK FOR ONTARIO’S P&C INDUSTRY (% of rms)

EMPLOYMENT TRENDS: LAST THREE YEARS (% of �rms)

66% INCREASING

10% DECREASING

24% STAYING THE SAME

10

* Based on feedback from 28 firms.

Ontario Insurance Industry: Summary Report

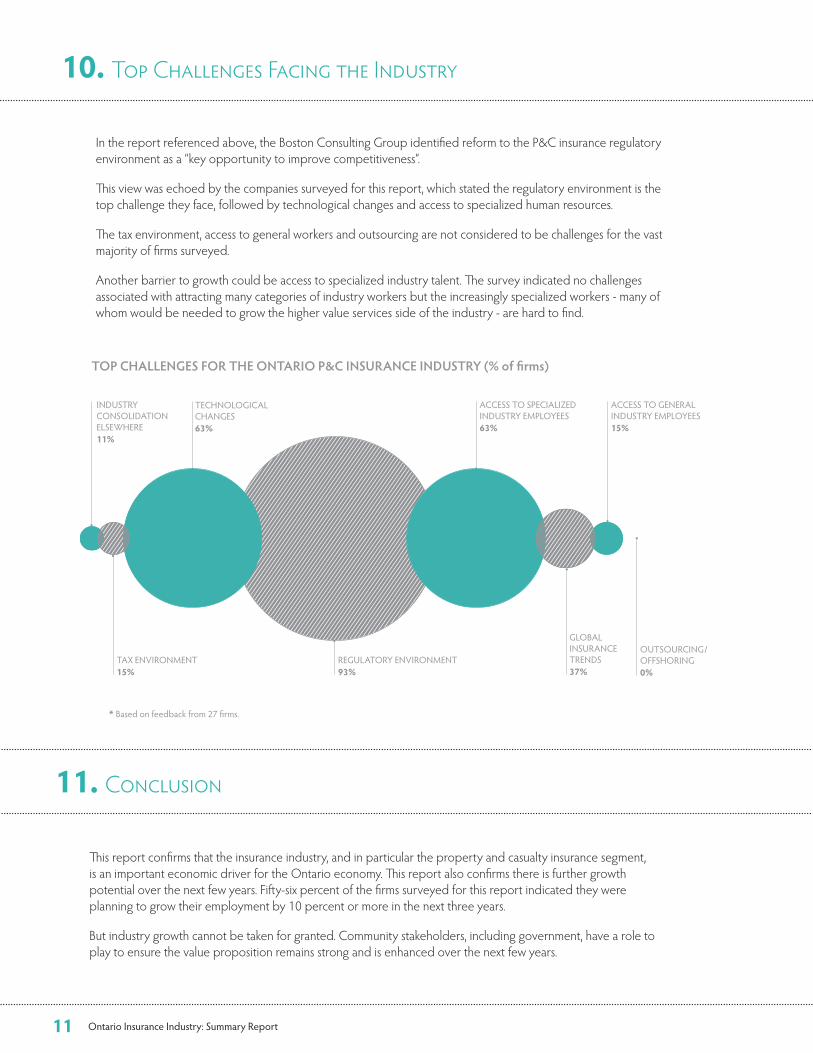

In the report referenced above, the Boston Consulting Group identified reform to the P&C insurance regulatory environment as a “key opportunity to improve competitiveness”.

This view was echoed by the companies surveyed for this report, which stated the regulatory environment is the top challenge they face, followed by technological changes and access to specialized human resources.

The tax environment, access to general workers and outsourcing are not considered to be challenges for the vast majority of firms surveyed.

Another barrier to growth could be access to specialized industry talent. The survey indicated no challenges associated with attracting many categories of industry workers but the increasingly specialized workers - many of whom would be needed to grow the higher value services side of the industry - are hard to find.

10. Top Challenges Facing the Industry

This report confirms that the insurance industry, and in particular the property and casualty insurance segment, is an important economic driver for the Ontario economy. This report also confirms there is further growth potential over the next few years. Fifty-six percent of the firms surveyed for this report indicated they were planning to grow their employment by 10 percent or more in the next three years.

But industry growth cannot be taken for granted. Community stakeholders, including government, have a role to play to ensure the value proposition remains strong and is enhanced over the next few years.

11. Conclusion

TOP CHALLENGES FOR THE ONTARIO P&C INSURANCE INDUSTRY (% of �rms)

REGULATORY ENVIRONMENT93%

ACCESS TO SPECIALIZED INDUSTRY EMPLOYEES63%

TECHNOLOGICAL CHANGES63%

GLOBAL INSURANCE TRENDS37%

TAX ENVIRONMENT 15%

ACCESS TO GENERAL INDUSTRY EMPLOYEES15%

INDUSTRY CONSOLIDATION ELSEWHERE 11%

OUTSOURCING/OFFSHORING0%

11

* Based on feedback from 27 firms.

10. Top Challenges Facing the Industry

11. Conclusion

�is document is a summary of two reports prepared for the Insurance Bureau of Canada. �e �rst was prepared by the Conference Board of Canada and is entitled Assessing the Impact of Ontario’s P&C Insurance Industry: An economic footprint analysis (2011). In this report, the Conference Board has developed a broad economic impact assessment of the property and casualty insurance industry in Ontario including direct and indirect employment, gross domestic product, direct and indirect tax bene�ts to government and other impacts of the industry on the provincial economy.�e second report, prepared by Jupia Consultants Inc., is entitled Ontario's P&C Insurance Industry: Strengthening �e Cluster (2011), and includes an assessment of the size and scope of the industry, its regional impacts across Ontario and its potential for future growth. �e report also highlights some of the challenges facing the industry moving forward.

Prepared for:

Prepared by:

Report Partner:

JULY 2011

for more information visit www.insureconomy.ca

an economic impact and future growth study of Ontario’s high-value insurance sector

over 300 �rms

�rms with less t

han 10% employment growth projected over next 3

years

�rms with more than 10% employment growth projected over n