Page 1

ANALYSIS OF INTERNAL CONTROL ON

PURCHASING ACTIVITY AT PT.XYZ

SKRIPSI

By

REGINA JAYA

008201000063

Presented to

The Faculty of Business, President University

In partial fulfillment of the requirements

for

Bachelor Degree in Economics, Major in Accounting

PRESIDENT UNIVERSITY

CikarangBaru – Bekasi

Indonesia

2014

Page 2

i

ANALYSIS OF INTERNAL CONTROL ON

PURCHASING ACTIVITY AT PT.XYZ

SKRIPSI

By

REGINA JAYA

008201000063

Presented to

The Faculty of Business, President University

In partial fulfillment of the requirements

for

Bachelor Degree in Economics, Major in Accounting

PRESIDENT UNIVERSITY

CikarangBaru – Bekasi

Indonesia

2014

Page 3

ii

PANEL OF EXAMINERS APPROVAL SHEET

Herewith, the Panel of Examiners declares that the skripsi entitled “ANALYSIS

OF INTERNAL CONTROL ON PURCHASING ACTIVITY AT PT.XYZ”

submitted by Regina Jaya, Accounting Study Program, Faculty of Business, has

been assessed and proved to pass the Oral Examination on Friday, March 14th

,

2014.

Chairman, Panel of Examiner,

Dr. Sumarno Zain, SE, Ak., MBA

Examiner 1,

Misbahul Munir, MBA, Ak., CPMA

Examiner 2,

Dr. Fachruzzaman, SE, MDM, Ak., CA

Page 4

iii

RECOMMENDATION LETTER OF SKRIPSI

ADVISOR

The skripsi prepared and submitted by

Name : Regina Jaya

Student ID : 008201000063

Faculty : Business

Study Program : Accounting

Skripsi Title : ANALYSIS OF INTERNAL CONTROL ON

PURCHASING ACTIVITY AT PT.XYZ

has been reviewed and found to have satisfied the necessities for Oral Defense as

partial fulfillment of the requirements for Bachelor Degree in Economics – Major

in Accounting.

Cikarang, Indonesia, March 3rd

2014

Acknowledge Skripsi Advisor,

Dr. SumarnoZain, SE, Ak, MBA Misbahul Munir, MBA, Ak.,CPMA

Head, Accounting Study Program Advisor

Page 5

iv

DECLARATION OF ORIGINALITY

I hereby declare that the skripsi entitled “ANALYSIS OF INTERNAL

CONTROL ON PURCHASING ACTIVITY AT PT XYZ” is originally

written by myself based on my own research and has never been used for any

other purpose before. I, therefore, request for Oral Defense of the skripsi.

Cikarang, Indonesia, March 10th

2014

Researcher,

Regina Jaya

008201000063

Page 6

v

ANALYSIS OF INTERNAL CONTROL ON

PURCHASING ACTIVITY AT PT XYZ

ABSTRACT

The company should be aware of the importances of internal control in

their activities to reduce the possibility of missappropriation, fraud, or human

error. The objectives of this research is to evaluate the internal control on

purchasing activity at PT XYZ. How the implementation, identify the weaknesses,

and give recommendation to overvome those weaknesses.

The scope of this research is focused on the control activities. The research

method used is qualitative method using case study approach. The researcher does

literature review and gathers actual primary data from the object research. During

the research, researcher gets primary data through interview, documentation, and

observation.

During the research process, researcher found several weaknesses of

internal control. First, the there is no written standard operating procedure (SOP),

so the employee does not have any formal and compulsory instruction in doing

their activities. Second, there is no receiving department, so there is no other

department that able to cross check the purchasing activity that do by purchasing

department. Third, Purchase Requisition does not show the date when spare part

needed, so the purchasing department only purchases the first Purchase

Requistion that came to them without knowing specific Purchase Requisition that

might need to be prioritizes after severals Purchase Requisition. Fourth, copy of

Purchase Order is not sent to the warehouse, so the warehouse migh confuse

whether their request has been received or not and decide to send a new request

that is meant for one request that lead the purchasing department to purchase

incorrectly.

For the better improvement in the company’s internal control system, there

are several recommendations from the researcher. The company should make a

written standard operating procedure for all activities, create a receiving

department, create Purchase Requisition form with date columns or state the date

when the spare part needed, send the copy of purchase order to the warehouse.

Key words: Internal control, control activities, purchasing activity

Page 7

vi

ACKNOWLEDGEMENT

“Believe in yourself! Have faith in your abilities! Without a humble but

reasonable confidence in your own powers you cannot be successful or happy.”

“Don’t run away from your problem. Stand still and face them! Always

remember, God never leave us.”

Thanks and gratitude to God Almighty for hope, love, strength, and for

everything that he has given to me. Without Him, I would not be able to finish this

skripsi and not be able to graduation with my friends.

I also realize that without the support and assistance from the people around

me, I may not be able to finish this skripsi. Therefore I would like to give special

thanks for what they have given to me.

1. To my parents, my father Putra Jaya and my mother Fransiska Gozali as

my inspiration on motivation to make me always try my best. Thank you

so much for the support, patience, believe, and love.

2. To my wonderful brothers, Kevin Pratama Jaya and Nico Permana Jaya.

Thank you for always being my little brothers who always stand up for

me.

3. To Mr. Misbahul Munir, MBA, Ak, CPMA as my advisor. Thank you for

the guidance, criticism, and patience that you had given to me that make

me able to learn a lot more than just write my skripsi.

4. To Mr. Sumarno Zain, SE, AK., MBA., as the head of accounting study

program. Thank you for taking care of all accounting students in President

University and your help in organizing the accounting study program.

Page 8

vii

5. To all the lecturers in President University. Thank you for your time to

teach and share your knowledge during our study.

6. To PT XYZ for giving me permission to do observation for my research.

7. To my roommate Lusy, Catherine, and Caroline. Thanks for moment that

we share together and thanks for advices that make me a better person.

8. To my dormitory gang at President Dormitory. Anthony, Hendy, Kris,

Michael, Rio, and Tobias. Thanks for every stupid moment that make my

campus life become colourful. Thanks for accepting me for the way I am

since the first time we met until now.

9. To Felani Angela Hermatang. Thanks for always being beside me in happy

or sad moment. Thanks for always see the kindness in me.

10. To my accounting gang at President University. Tia, Philip, Daniel, Irvin ,

James. Thank you for super time that we spend together start from our

study in President University until our internship. Thanks for always

support me in making my skripsi.

11. To my kost-mate, Carla and Cilla. Thanks for our time when we cheer up

each other in up and down situation while making our skripsi. Thanks for

that short yet beautiful moment.

12. To all accounting students batch 2010. Thank you for the friendship and I

am glad to know and be friend to all of you

13. To all people whom I cannot mention one by one. Thank you for your

support, help and advice.

Page 9

viii

Table of Contents

TITLE ....................................................................................................................... i

PANEL OF EXAMINERS APPROVAL SHEET .................................................. ii

SKRIPSI ADVISOR RECOMMENDATION LETTER ....................................... iii

DECLARATION OF ORIGINALITY .................................................................. iv

ABSTRACT ............................................................................................................. v

ACKNOWDLEGMENT ........................................................................................ vi

LIST OF FIGURES ................................................................................................. x

CHAPTER 1 : INTRODUCTION...........................................................................1

I.1 Research Background ................................................................. 1

I.2 Problem Identification and Satetement ....................................... 2

I.3 Research Objectives .................................................................... 2

I.4 Research Scope and Limitation .................................................. 3

I.5 Research Benefits ....................................................................... 3

I.6 Research Method........................................................................4

CHAPTER II: LITERATURE REVIEW.................................................................6

II.1 Internal Control ......................................................................... 6

II.1.1 Definitions of Internal Control ................................... 6

II.1.2 Internal Control Objectives ........................................ 7

II.1.3 Components of Internal Control ................................. 9

II.1.4 Limitations of Internal Control ................................. 19

II.1.5 Roles and Responsibilities ........................................ 22

Page 10

ix

II.2 Purchasing Procedure .............................................................. 25

II.2.1 Definitions of Purchasing ......................................... 25

II.2.2 Functions in Purchasing ........................................... 26

II.2.3 Documents in Purchasing ......................................... 27

II.2.4 Purchasing Procedure ............................................... 29

II.3 Internal Control Over Purchasing Activity.............................. 31

CHAPTER III: METHOD OF DATA PROCESSING AND COMPANY’S

EXISTING CONDITION......................................................................................37

III.1 Data Collecting and Processing ............................................. 37

III.2 Company’s Background ......................................................... 39

III.2.1 Background ............................................................. 39

III.2.2 Organization Structure ............................................ 41

III.2.3 Job Description........................................................ 42

III.3 Company’s Purchasing Process ............................................. 48

CHAPTER IV: ANALYSIS AND EVALUATION.............................................54

IV.1 Best Practices Done by The Company................................... 54

IV.2 Findings ................................................................................. 55

CHAPTER V: CONCLUSION AND RECOMMENDATION.............................60

V.1 Conclusion ............................................................................... 60

V.2 Recommendation ..................................................................... 63

BIBLIOGRAPHY .................................................................................................. 65

APPENDICIES......................................................................................................66

COMPANY’S CONFIRMATION LETTER.........................................................70

Page 11

x

List of Figures

Figure 3.1 Organization Structure of PT XYZ- Head Office ................................ 41

Figure 3.2 Organization Structure of PT XYZ- Manufacture...............................42

Figure 3.3 Flow Chart of Purchasing Process.......................................................49

Page 12

1

Chapter I

Introduction

I.1. Research Background

In this day, the business world has developed. This is also increases the

competition among companies. Thus, the company should be able to develop their

business so that they can survive in this business world. The more a company

develops, the more complex the activities. This increase the difficulty for the

company’s leader to control their business activities. Therefore, companies need

internal control system that can help them to control their activities. Internal

control system is a system and procedure designed by the management to provide

reasonable assurance regarding effectiveness and efficiency of operations,

reliability of financial reporting, compliance with applicable laws and regulations,

and safeguarding assets.

One of the most important activities of the company, one of them is

purchase activity. The purpose of this activity is to provide the needs of the

company to run its business. There are few things to be considered in purchasing

activities, such as whether the materials purchased are materials needed by the

company, whether the materials are purchased with the best price, and whether the

materials received are what the company’s order. Therefore, a company needs an

internal control to ensure that its activities had been carried out properly and in

accordance with procedures.

Page 13

2

PT. XYZ is one of palm oil companies in Riau that produces CPO. This

company is in the change phase, from conventional into modern, so that many

activities within the company still needs a lot of improvement. Moreover, this

company has already existed for more than 10 years and it seems that there is no

development in its business. Everything is almost the same as when it was started

PT XYZ has purchased spareparts for its production machines. Based on

explanation above, the researcher decided to conduct a research with title

“ANALYSIS OF INTERNAL CONTROL ON PURCHASING ACTIVITY

AT PT.XYZ”

I.2. Problem Identification and Statement

To clarify the understanding of the discussion from the research

conducted, researcher identified problems are as follows:

a. Whether the spare parts purchased are what the company needs?

b. Whether the spare parts have been purchased with the best price?

c. Whether the spare parts that have been received have been checked

properly?

d. Whether the documents used in purchasing activity has been used

properly?

e. Whether all departments related to purchasing activity have functioned

properly?

Page 14

3

I.3. Research Objectives

The purpose of this research is to see the problems, the causes, and the

effects on the company activity, and then makes recommendations or suggestions

to help the company overcome the problems based on knowledge from the

literature review. Some objectives that must be achieved in this research are:

a. To evaluate and understand the internal control on purchasing activity

b. To identifty the weaknesses in the internal control on purchasing activity

c. To formulate recommendation needed to overcome those weaknesses and

to improve the internal control on purchasing activity

1.4 . Research Scope and Limitation

The researcher limits the scope of the discussion on internal control of

purchasing spare parts. The discussion about internal control is limited on one of

COSO’s components of internal control which is control activity. The categories

of control activity discussed in this research are transaction authorization,

segregation of duties, documentation, and access control.

The researcher is not allowed to take any quantitative data related to

financial aspects and accounting report as well as some important informations

claimed as confidential.

1.5. Research Benefits

1.5.1. Research Benefits for Company

This research can give some give feedback to the company

about the weaknesses and problems in their purchasing process and

Page 15

4

finally some recommendations to improve their purchasing

process.

1.5.2. Research Benefits for Author

This research gives a real experience of implementation of

the theories that have learned during class sessions. The research

will increase author’s knowledge about the implementation of

internal control in purchasing process in the real life.

1.5.3. Research Benefits for Readers

This research hopefully is able to expand the reader’s

knowledge about the implementation of internal control on

purchasing. This research may also help another researcher as

reference for their researches.

1.6. Research Method

This is qualitative research with case study approach. Researcher did

literature review and field research. In literature review, researcher got reference

or relevant theories from text books, internet, journal, and other scientific sources

in order to get criteria in assessing the existing conditions of the company. In the

field research, researcher came to the company to get the primary data.

In doing field research, the researcher using types of audit evidence

methods which are:

Page 16

5

Interview

Consist of seeking information from knowledgeable persong, both

financial and nonfinancial, throughout the company or outside the

company.

Observation

Consists of looking at a process or procedure being performed by the

company. The activity may be the routine process to see that the employee

are performing their assigned duties in accordance with company policies

and procedure.

Documentation

Consists of looking the evidence such document being used by the

company in their activity to get better understanding with the company

activity. Rechecking of transfers of information involves seeing if

information is recorded consistently in the accounting records

Page 17

6

Chapter II

Literature Review

II.1. Internal Control

II.1.1. Definitions of Internal Control

COSO framework quoted by Boynton, William C., and Johnson (2006)

stated that, “Internal control is a process, effected by an entity’s board of

directors, management, and other personnel, designed to provide reasonable

assurance regarding the achievement of objectives in the following categories :

Reliability of financial reporting

Compliance with applicable laws and regulations

Effectiveness and efficiency of operations”. (p.391)

Moeller (2009) stated that, “Internal control are process, implemented by

management, that are designed to provide reasonable assurance; compliance with

policies and procedures plans, laws, rules and regulations; safeguarding of assets;

operational efficiency; achievement of an established mission, objectives and

goals for enterprise operations; and integrity and ethical values.” (p.24).

Meanwhile, Reeve, Warren, and Duchac (2007) write, “ Internal control

are policies and procedures that protect assets from missuse, ensure that business

information is accurate, and ensure that laws and regulations are being followed.”

(p.231).

Page 18

7

Based on the definitions above, internal control is a plan, process,

procedure, and policies designed by the management to give a reasonable

assurance towards achievement of the efficiency and effectiveness of operations,

reliability of financial reporting, safeguarding the assets, conformity to the laws,

policies and other regulations.

II.1.2. Internal Control Objectives

An internal control system consists of the entire system and procedure that

established by a company to provide reasonable assurance of the achievement of

the company’s objectives. Refers to Hall (2011) there are four objectives of

internal control:

To safeguard assests of the firm

Internal control designed by the management is used to prevent fraud and

miss-use of company’s assets because assets are important resources of

company to do their operation

Reliability of financial reporting

Financial report is prepared by management for internal and external

users, which makes the informations in the financial report must be

reliable to reflect the actual condition of the company. Good internal

control will produce good and sufficient transaction’s evidence that

affected the information contained in financial report.

Page 19

8

Efficiency and effectiveness of operations

Internal control in a company avoids unnecessary activity being performed

and encourages efficient use of resources to optimize company’s goals.

Compliance with laws and regulations

Internal control encourages all people work in a company to comply with

applicable laws and also rules and regulations established by the company.

Moreover, the main objectives of an internal control system are also

summarised from the Auditing Practices Board (APB) and the COSO guidelines

are as follows:

To ensure that business operation has been carried out orderly and

efficiently as a result from the fully implemented system designed by

management. Controls help the business processes and transactions to run

without interference or with less risk which will adds value and creates

shareholder value.

To safeguard the company’s assets. Assets include tangibles and

intangibles, and controls are necessary to ensure they are optimally utilized

and protected from miss-use, fraud, misappropriation or theft.

To prevent and detect fraud. Controls are necessary to show up any

operational or financial dicrepancy that might be the result of theft or

fraud. This might include unbalanced sheet financing or the use of

unauthorized accounting policies, inventory controls, use of company

property.

Page 20

9

To ensure the completeness and accuracy of accounting records. Ensuring

that all accounting transactions are fully and accurately recorded, that

assets and liabilities are correctly identified and valued, and that all costs

and revenues can be fully accounted for.

To ensure the timely preparation of financial information which applies to

statutory reporting (of year end accounts, for example) and also

management accounts, if appropriate, for the facilitation of effective

management decision-making.

II.1.3. Components of Internal Control

Based on COSO’s Internal Control- Integrated Framework, there are five

components of internal control which are control environment, risk assessment,

control activity, information and communication, and monitoring.

Control Environment

Elder, Beasley, and Arens (2012) explained that, ”To understand and

assess the control environment, auditors should consider the most important

control subcomponents.

a. Integrity and Ethical Values

Integrity and ethical values are the product of the entity’s ethical

and behavioral standards, as well as how they are communicated

and reinforced in practice. They include management’s actions to

remove or reduce incentives and temptations that might prompt

personnel to engage in dishonest, illegal, or unethical acts. They

Page 21

10

also include the communication of entity values and behavioral

standards to personnel through policy statements, codes of conduct,

and by example.

b. Commitment to Competence

Competence is the knowledge and skills necessary to accomplish

tasks that define an individual’s job. Commitment to competence

includes management’s consideration of the competence levels for

specific jobs and how those levels translate into requisite skilss and

konwledge

c. Board of Director or Audit Committe Participation

The board of directors is essential for effective corporate

governance because it has ultimate responsibility to make sure

management implements proper internal control and financial

reporting processes. An effective board of directors is independent

of management, and its members stay involved in and scrutinize

management’s activities. Although the board delegates

responsibililty for internal control to management, it must regularly

assess the controls. In addition, an active and objective board can

often reduce the likelihood that management overrides existing

controls.

d. Management’s Philosophy and Operating Style

Managements, through its activities, provides clear signals to

employees about the importance of internal control. For example,

Page 22

11

does management take significant risks, or is it risk averse? Are

sales and earning targets unrealistics, and are employees

encouraged to take aggressive actions to meet those targets? Can

management be described as “fat and bureaucratic”, “lean and

mean”, dominated by one or few individuals, or is it “just right”?

Understanding these and similar aspects of management’s

philosophy and operating style, the auditor sense of management’s

attitude about internal control.

e. Organization Structure

The entity’s organizational structure defines the existing lines of

responsibility and authority. By understanding the client’s

organizational structure, the auditor can learn the management and

functional elements of the business and perceive how controls are

implemented.

f. Human Resource Policies and Practices

The most important aspect of internal control is personnel. If

employees are competent and trustworhty, other controls can be

absent, and reliable financial statements will still results.

Incompetent or dishonest people can reduce the system to a

shambles-even if there are numerous controls in place. Honest,

efficient people are able to perform at a high level even when there

are few other controls to support them. However, even competent

and trustworthy people can have shortcomings. For example, they

Page 23

12

can become bored or dissatisfied, personal problems cand disrupt

their performance, or their goals may change.” (p.295-296).

From explanation above, we can see that control environment sets the tone

for the organization and influence the control awareness from its management and

employees. Control environment is the foundation for all other components of

internal control as well as providing discipline and structure.

Risk Assessment

Elder, Beasley, and Arens (2012) stated that, “ Risk assessment for

financial reporting is management’s identification and analysis of risks that might

happen when the preparation of financial statements in conformity of appropriate

accounting standards.” (p.297).

Based on Hall (2011), “Risks can arise from changed circumstances:

a. Changes in the operating environment that needed new or change

competitive pressures of the organization.

b. New worker who have a different understanding of internal control

c. New person who handle information systems that might affect

transaction processing.

d. The implementation of something new like technology into the

production process or information system that has impacts for

transaction processing.

e. The introduction of new product or activities that the organization has

little experience

Page 24

13

f. Organizational restructuring resulting in the reduction or reallocation

of worker that have impact in operations and transaction.

g. Entering into foreign markets that may impact operations, such as risks

associated with foreign currency transactions.

h. Adoption of a new accounting principle that impacts the preparation of

financial statements.” (p.133).

From description above, we can see that every organization faces variety

type of risks both externally and internally in preparing their financial report. That

is why the management has to identify or assess the risk that might disrupt their

process in making financial report in accordance with the accounting standard.

Control Activity

Refer to Hall (2011), control activity is grouped into two categories:

computer controls and physical controls. Computer controls are controls concern

in IT environment and IT audit. As for physical controls, these controls concern

toward human activities in the accounting procesws. Physical controls fall into six

categories, they are transaction authorization, segregation of duties, supervision,

accounting records, access control, and independent verification.

a. Transaction authorization

Every transaction must be authorized before getting processed. The

purpose of this control is to ensure that every transaction are valid and

in accordance with procedure applied in the organization. So there are

no transaction that not known by authorized person. There are two

types of authorization which are general authorization and specific

Page 25

14

authorization. General authorization is an authorization for daily basis

transactions such as purchase inventory when the amount of inventory

already in predetermined reorder points. Meanwhile, specific

authorization is an authorization for non-routine transaction or special

case transaction. For example, a manufacturing company sell one of

their production machine.

b. Segregation of duties

The purpose of this control is to reduce the ability of the employee to

has excessive authority in transaction of certain assets. There are three

guidelines for segregation of duties to prevent fraud and error in an

organization:

Segregation of duties between authorizing a transaction and

processing that transaction

Separation between the one who has custody of assets with the

one who reponsilbe in recording those assets

Separation responsibility of accounting records, between the

one who record journals, subsidiary ledgers, and general

ledger.

c. Supervision

To have a good internal control, all assets and documents must be

protected, so they can not be stolen, damaged, changed, or lost. For a

small company who does not have enough employees to make

segregation of duties in order to maintain its assets and documents,

Page 26

15

supervision is important to control the activities of employees toward

those assets or documents. Moreover, supervision also can be done by

security tools to safeguard the assets and documents and electronic

tools in recording the transactions.

d. Accounting records

This control is to ensure that all documents related with economic

transactions are complete and all notes about the information of those

transactions are made in detail. The purpose of this control is to make

the informations related with the transaction are trustworthy in order

to ensure that transaction able to be recorded properly. This control

also provides audit trail that help auditor to trace all transactions

process from beginning until the financial statement.

e. Access control

The objective of access control is to safeguard the assets by restricting

access to them which is only authorized personnel that able to access

the company’s assets. The access toward assets can be direct and

indirect. Direct access can be controlled by physical security tools,

such as locks and fences. As for indirect access is about having access

or authority toward documents that control the use of assets. This

indirect access can be controlled by segregate the duties between

employees so there is no employee has excessive access toward a

certain assets.

Page 27

16

f. Independent verification

Independent verification is an independent check toward accounting

transactions to identify any errors that might happened. This control

should be made periodicaaly by independent personnel such as

internal auditor. This control can be done by reconciling documents of

transaction with control accounts or by comparing the amount of

inventory with its record.

Elder, Beasley, and Arens (2012) defined control activities of internal

control as follows, “ Control activities are the policies and procedures, in addition

to those include in the other four components, that help ensure that necesary

actions are taken to addres risks in the achievement of the entity’s objectives.”

(p.298).

Control activities generally fall into five types, as follows:

1. Adequate separation of duties

a. The person who performs to custody company’s assets must

be different with the person who performs accounting

function.

b. The person who authorized the transactions must be

different with the person who custody the related assets.

c. The person who has operational responsibility must be

different with the person who has record-keeping

responsibility.

Page 28

17

d. The person who has IT duties must be different with the

user departments.

2. Proper authorization of transactions and activities

a. General authorization.

b. Specific authorization.

3. Adequate documents and records

a. The documents must be pre-numbered.

b. The documents and records must be prepared at the time of

transaction is happened.

c. The documents and records must be designed for multiple

uses.

d. The construction of documents and records must be

designed to encourage correct preparation.

4. Physical control over assets and records

a. Physical control over assets and records is important to

safeguarding company’s assets and records.

5. Independent checks on performance

a. Internal control tends to change overtime. Unless there is a

mechanism for frequent review of company, it is necessary

to conduct independent verifications.

Page 29

18

Information and communication

Messier (2008) explained that, “An information system consists of

infrastructure (physical and hardware components), software, people, procedures

(manual and automated) and data.” (p.227).

The information system in the company help management in making a

financial report that consist of infrastructure, software, people, procedure, and

data. The infrastructure such as computer, printer, copy machine, and other tools

needed for the operation. Software components are computer’s program such as

excel, word, powerpoint, etc and accounting system used by the company that

helps management in making a financial report.

People are the employees that have ability, skill and konwledge to running

the software and make a financial report. Procedure is steps that has to be done

when making a financial report. Data is an input or information to make an output

or financial report

Messier (2008) also explained that, “Communication involves providing

an understanding of individual roles and responsibilities pertaining to internal

control over financial reporting.” (p.228)

This is about how the management communicate with the employess and

make sure the employees understand their activities that related with financial

reporting system and understand their activities relate to work of others both

inside and outside the organization. Communication can be made through policy

manuals, accounting and financial reporting manuals, a chart of accounts,

memoranda, or can be made electronically, orally, and through management’s

actions.

Page 30

19

Monitoring

Messier (2008) writes, “ Monitoring can be done through ongoing

activities or separate evaluations. Ongoing monitoring procedures are built into

the normal, recurring activities of the entity and include regular management and

supervisory activities. For example, production managers at the corporate or

divisional levels of an entity can monitor operations at lower levels by reviewing

activity reports and questioning reported activity that differs significantly from

their knowledge of operations. In many entities, the information system produces

much of the information used in monitoring. If management assumes that data

used for monitoring are accurate, errors may exist in the information, potentially

leading management to incorrect conclusions.” (p.229).

Meanwhile, Bodnar and Hopwood (2010) write, “ Monitoring is

accomplished through ongoing activities, separate evaluations, or some

combination of the two. Ongoing activities would include management

supervisory activities and other actions that personnel might take to ensure an

ongoing effective internal contro process.” (p.148).

From the definition above, monitoring is an ongoing activities in

evaluating internal control toward normal operation activities, includes regular

management, supervisory, and other personnel activities in performing their jobs.

II.1.4. Limitations of Internal Control

Boynton, William C., and Johnson (2006) stated that, ”No matter how well

designed, implemented and conducted, an internal control can provide only

Page 31

20

reasonable assurance to management and the board of directors regartding

achievement of an entity’s control objectives. The achievement is affected by

limitations inherent in all systems of internal control. there are severals limitations

in internal control, as follows:

Mistakes in judgment

Occasionally, management and other personnel may exercise poor

judgment in making business decisions or in performing routine

duties because of inadequate information, time constraints, or other

procedure.

Breakdowns

Breakdowns in established control may occur when personnel

misunderstand instructions or make errors owing to carelesness,

distractions, or fatigue. Temporary or permanent changes in

personnel or in systems or procedures may also contribute to

breakdowns.

Collusion

Individuals acting together, such as an employee who performs an

important control acting with another employee, customer, or

supplier, may be able to perpetrate and conceal fraud so as to

prevent its detection by internal control. For example, collusion

among three employees from personnel, manufacturing, and

payroll departments to initiate payments to fictitious employees, or

Page 32

21

kick-back schemes between an employee in the purchasing

department and a supplier or between an employee in the sales

department and a customer.

Management override

Management can overrule prescribed policies or procedures for

illegitimate purposes such as personal gain or enhanced

presentation of an entity’s financial condition or compliance status.

For example:

inflating reported earnings to increase a bonus payout or the

market value of the entity’s stock, or to

hide violations of debt covenant agreements or

noncompliance with laws and regulations.

Override practices include making deliberate misrepresentations to

auditors and others such as by issuing false documents to support

the recording of fictitious sales transactions.

Cost versus benefits

The cost of an entity’s internal control should not exceed the

benefits that are expected to ensue. Because precise measurement

of both costs and benefits usually is not possible, management

must make both quantitative and qualitative estimates and

judgments in evaluating the cost-benefit relationship. For example,

an entity could eliminate losses from bad checks by accepting only

certified or cashier’s checks from customers. However, because of

Page 33

22

the possible adverse effects of such a policy on sales, most

companies believe that requiring identificsation from the check

writer offers reasonable assurance against this type of loss.”

(p.393).

From explanations above we can see that there are several limitations in

internal control. First is human weaknesses. From those weaknesses, some

decisions made maybe less satisfactory or maybe need to be change. Second, a

well-designed system of internal control also able to break down caused by

personnel who misunderstand the instructions, commit errors due to carelessness,

distractions, being asked to focus on too many tasks, or changes in personnel or

system. Third, limitation might come from some people who working together for

their benefits to create flaws in the internal control, so they able to do fraud

without get detected by system.

Fourth, management also able to do things that are not in accordance with

the applicable rule and regulations for their benefits or to increase the look of

company’s performance. The last, sometimes the limitation come from the

company itself. The company does not want to have costs that exceeds the

benefits they receive. Therefore, management must do calculations to see how

much benefit they get with the cost that might incurred.

II.1.5. Roles and Responsibilities

The COSO report that quoted by Boynton, William C., and Johnson

(2006) concludes that, “In an organization has some responsibility, and is actually

Page 34

23

a part of, the organization’s internal control. Several responsible parties and their

roles are as follows:

Management

It is management responsibility to establish effective internal

control. In particular, senior management should set the “tone at

the top” for control consciousness throughout the organization and

see that all the components of internal control are in place. Senior

management in charge of organization units. Should be

accountable for the resource in their units. The CEO and CFO of

publics companies must also make an assessment of the adequacy

of internal controls over financial reporting

Board of director and audit committee

Board members, as part of their general governance and oversight

responsibilities, should determine that management meets its

responsibilities for establishing and maintaining internal control.

The audit committee (or in its absence, the board itself) has an

important oversight role in the financial reporting process.

Internal Auditors

Internal auditors should periodically examine and evaluate the

adequacy of an entity’s internal control and make

recommendations for improvements. They are part of the

monitoring component of internal control, and active monitoring

by internal auditors may improve the overall control environment.

Page 35

24

Other entity personnel

The roles and responsibilities of all other personnel who provide

information to, or use information provided by, systems that

include internal control should understand that they have a

responsibility to communicate any problems with noncompliance

with control or illegal acts of which they become aware to a higher

level in the organization

Independent auditors

When performing risk assessment procedures, an independent

auditor may discover deficiencies in internal control that he or she

communicates to management and the audit committee, together

with recommendations for improvements. This applies primarily to

financial reporting controls, and to a lesser extent to compliance

and operations controls.

Other external parties

Legislators and regulators set minimum statutory and regulatory

requirements for establishing internal control by certain entities.”

(p.394).

Form explanation above, we can see that everyone both internally and

externally related with the organization have their own roles and responsibilities

on organizations’s internal control. From internal there are management, board of

directors and audit committee, internal auditors, and other entity personnel.

Management reponsible to set the internal control, board of directors and audit

Page 36

25

committee have role and responsible to monitor the management’s responsibilities

in setting internal control, internal auditor responsible to evaluate the internal

control’s adequacy and make recommendations, other entity personnel

responsible to communicate to higher level if there is any problem in the internal

control.

From external, there are independent auditor and other external parties.

Independent auditor has role and reponsibility to make recommendation for any

deficiencies in internal control while performing risk assessment procedure, and

other external parties have role and responsibilities to make as rule and regulation

for organization in establish internal control.

II.2. Purchasing Procedure

II.2.1. Definitions of Purchasing

Bodnar and Hopwood (2010) also stated that, “ Procurement is the

business process of a selecting source, ordering, and acquiring goods or services.

The goods or services might be obatined internally if the goods are produced by

another entity in the company. Purchasing is a synonym for procurement.”

(p.308).

Hall (2011) stated that, “ Purchasing is responsible for ordering inventory

from vendors when inventory levels fall to theri reorder point.” (p.19).

From definitions above, it can be concluded that purchasing is a process of

buying goods from vendors when the stock is running out whether to be used in

the business’s operations or sell to another party.

Page 37

26

II.2.2. Functions in Purchasing

According to Mulyadi (2008), there four functions related in purchasing

system which are warehouse function, purchasing function, receiving function,

and accounting function.

Warehouse function

In purchasing accounting systems, warehouse function is responsible for

the purchase request in accordance with the position of existing inventory in the

warehouse and to store goods that have been received by the receiving function.

For items directly used (no inventory held in the warehouse), purchase requests

submitted by the users.

Purchasing function

Purchasing function is responsible for obtaining information on the price

of goods, define the selected suppliers in the procurement of goods, and issue a

purchase order to the selected supplier.

Receiving funtion

In purchasing accounting systems, this function is responsible for

conducting the examination of the type, quality and quality of goods received

from the supplier in order to determine whether or not the item being received by

the company. This function is also responsible for receiving goods from the buyer

derived from sales return transactions.

Page 38

27

Accounting function

Accounting functions that related to the purchase activity is a recording

debt and recording inventory. In purchase accounting systems, function of

recording debt is to record purchasing transactions into registers as proof of cash

out and to organize source documents (proof of cash out) as notes to subsidiary

ledger. In purchase accounting systems, function of recording inventory is to

record the cost of inventory purchased into inventory card.

II.2.3. Documents in Purchasing

According to Mulyadi (2008) there are six documents used in purchasing

system. They are purchase requisition, price quotation, purchase order, receiving

report, change order, and voucher.

Purchase requisition

This document is a form that made by the warehouse or user to request

purchasing department to purchase goods with the type, quantity, and quality as

mentioned in the purchase requisition form. The purchase requisition form is

usually made in two copy, one copy sent to the purchasing department, and one

the other copy as archive for the warehouse or user.

Price quotation

This document is used to request a price for the goods which the

procurement are not repeatedly, which involves the purchase of a large amount of

dollars.

Page 39

28

Purchase order

This document is prepared by the purchasing department based on

purchase requisition received. This document used to order goods to selected

supplier. This document was created in five copies with the following objectives:

The first copy is sent to the selected supplier

The second copy is being kept by purchasing department as archive

The third copy is sent to the user who request the goods as

information that the purchase has been made

The fourth copy is sent to the receiving department as basis

comparison when the goods came.

The fifth is sent to the accounting department as the basis for

recording the liability

Receiving report

This document is created by a receiving department to indicate that the

goods received from the supplier has met the type, specification, quality and

quantity as specified in the purchase order.

Change of purchase order

Sometimes change in purchase order that has been sent is necessary. Such

changes in quantity, goods delivery schedules, specifications, replacement or

other matters concerned with changes in design or business. Usually the changes

are formally notified to the supplier using a change of purchase order form.

Change of purchase order form made in the same copy amount anddistributed to

the same parties who have a purchase order form.

Page 40

29

Voucher

This document was created by accounting department as basic recording

for the purchase transaction. This document also serves as a cash disbursement

orders for the payment of debts to suppliers and also serves as a notified to

creditors regarding payment intent.

II.2.4. Purchasing Procedure

Messier (2003) stated that, “ A purchase transaction usually begins with a

purchase requisition being generated by a department or support function. The

purchasing department prepares a purchase order for the purchase of goods or

services from a vendor. When the goods are received or the service have been

rendered, entity records a liability to the vendor. Finally, the entity pays the

vendor.” (p.425).

According to Mulyadi (2008), there are five procedures that form

purchasing process. They are purchase request procedure, offering price and

supplier selection procedure, purchase order procedure, receiving goods

procedure, and liability recording procedure

Purchase request procedure

In this procedure the warehouse make a purchase requisition form and

send it to the purchasing department. The need for goods based on economic order

quantity calculation (EOQ) and re-order point. If the goods are not stored in

warehouse, for example goods that directly used, the user make a purchase

requisition form and directly send it to the purchasing department

Page 41

30

Offering price and supplier selection procedure

Purchasing department select suppliers from supplier records and send the

price quotation and availability of the goods to the supplier to obtain information

on the prices of goods and other purchase terms. If already obtained the prices and

the availability of the goods, the purchasing department select the most

competitive supplier and make purchase orders form to be sent to that supplier,

accounting department, receiving department, warehouse ( inventory controller),

and purchasing department as archive. At the receiving department, quantity and

price of the goods column must be cleared to ensure the receiver who the check

goods received not knowing the price of goods to avoid the act of theft.

Purchase order procedure

In this procedure the purchasing department sent a purchase order to

selected supplier and the copies to accounting department, receiving department,

warehouse (inventory controller), and purchasing department as archive. At the

receiving department, quantity and price of the goods column must be cleared to

ensure that the receiver who the check goods received not knowing the price of

goods to avoid the act of theft.

Receiving goods procedure

In this procedure the receiving department check the type, quantity, and

quality of goods received, and then make a report to acknowledge the receipt of

goods from the supplier. This report is given to the purchasing department,

warehouse, and as archive at receiving department. Then send the goods received

to the warehouse and listed on the stock card.

Page 42

31

Liability recording procedure

In this procedure the accounting department has two functions that is to

check the documents related to the purchase (purchase order, receiving report, and

invoice from supplier) and make a record of debt from that purchase. Then

summarize the purchase journal to the journal and then post it to the general

ledger. The second function as inventory control is to record the receipt into the

inventories card

II.3. Internal Control Over Purchasing Activity

According to Messier (2003), there are some internal control procedures in

purchasing activities, as follows:

To avoid purchase recorded goods that are not ordered or received.

Management should have a clear segregation of duties, purchase not

recorded without approved purchase order and receiving report, also check

if there is any cancellation of documents.

To avoid purchase made but not recorded

The staff should match the receiving report with vendor invoices and

entered in the purchase journal.

To avoid purchase transaction recorded in wrong period

The management should reconcile to daily account payable listing, all

receiving report should be given to account payable department every day,

recording the purchases as soon as possible after the goods received.

To avoid purchase goods not authorized

Page 43

32

There must be an approved purchase requisition, approval and acquisition

consistent with the limit amount from supplier.

To avoid vendor invoice improperly priced or incorrectly calculated

Checking the accuracy of vendor invoice, purchase order agreed to

purchase order, receiving report, and invoice.

According to Mulyadi (2008), there are three main elements of internal

control on purchasing. Those three elements are organization, authorization

system and recording procedures, and healthy practices.

Organization

To have a good internal control on purchasing, there are two main points

in designing an organization. First, an organization must separate three main

functions which are accounting function, warehouse, and operational function.

Second, there is no activity done by only one personnel from beginning until the

end. There are four applications of these two maint points:

1. Purchasing funtion must be separated from receiving function

Purchasing function is a function that responsible in getting trusted

supplier for company. Receiving function is a function to do the

independent checking on goods receied from suppliers. The separation of

purchasing and receiving function will reduce the risks of receiving goods

that are not ordered by vompany, receiving goods which quantity, quality,

and specification are not in accordance with purchase order, and not

receiving goods at the time stated in purchase order.

Page 44

33

2. Purchasing function must be separated from accounting function

Accounting function is responsible to record the accound payable and

inventory and the purchasing function is the operational function to

purchase material neede by the company. The purpose of separation of this

functions is to protect company’s assets and to ensure the reliability of

information in accounting data.

3. Receiving function must be separated from warehouse function

Receiving function is responsible to receive the goods from supplier.

Warehouse function is responsible in storing and managing goods that

already received by the receiving function. The purpose of separation of

this functions is to make the receiving and storing activities handled by

functions that skilled in their field, so it will increase the reliablity of

information in receiving goods and inventory record.

4. Transaction must be done by more than one personnel or more than one

function

It is necessary to have more than one personnel or more than one function

in a transaction so there is an internal checking wihtin each function.

Authorization system and recording procedures

In a company, every transaction should have proper authorization and

accounting records. To authorize a transaction, the authorized person must write

his signature on the main and supporting documents of transaction. To provide

accounting records, all transaction have to be recorded in accounting record based

Page 45

34

on procedure that applied in the company. Thus, company’s assets will be secured

and guaranteed and the accounting data will be accuracy and reliable.

a. Purchase Requisition has to be authorized by warehouse function

The purpose is to ensure that the purchase requisition issued for requested

goods are the goods needed by the company.

b. Purchase Order has to be authorized by purchasing function or higher

management

Purchase order is an initial procurement transactions. With this purchase

order company initiated the procurement process that will resulted in the

receipt of goods purchased and result on the emergence of the company's

obligations to outsiders. Therefore, authorization by purchasing function or

higher management to reduce the possibility to receive of goods and

liabilities that are not required by the company.

c. Receiving Report has to be authorized by receiving function

Receiving function give the authorization signature on the receiving report

as proof of receiving goods from suppliers. The document sent by the

receiving function to the accounting function as a proof that the

examination has been done, thus the goods received from the supplier in

accordance with the purchase order that issued by the purchasing function.

d. Cash disbursement voucher has to be authorized by accounting function or

higher management.

Page 46

35

In a purchase transaction, the accounting function accepts a variety of

documents from the following sources:

A copy of the purchase order from the purchasing function is a proof

that the company has been ordered goods by the number, type,

specification, quantity and quality of goods, and the delivery time as

stated in the document.

Copy of receiving report from receiving function is that the goods

have been ordered have been received and in accordance with the

goods ordered in the purchase order

Invoice from a supplier which is proof that company’s obligations has

occurred as a result from ordering goods and receiving goods

Documents above is used by accounting function accounting as basis for

recording accounts payable and addition of inventory. Also all accounting

transaction in purchasing must be recorded by authorized person. Thus, the

responsibility for changing accounting records can be attributed to a particular

employee, so there is no changes the accounting records that are not accounted

for.

Healthy practices

There are several healthy practices in purchasing, as follows:

1. Using prenumbered forms, especially in purchase requisition, purchase

order, and receiving report, so the use of the documents can be acounted to

managers who have the authority to use that forms.

Page 47

36

2. Suppliers selected bases on the analysis of prices from various supplier,

not only because the company has special relation with the supplier but

because the price offered with the same quality is more competitive than

other supplier.

3. Receiving function will receive and inspect the good after get the copy of

purchase order from purchasing function.

4. Receiving function compares the goods received with purchase order copy

from purchasing function. To ensure that the company receive goods that

already ordered.

5. Accounting function verifies the information such as price and purchasing

terms, and calculate the invoice before preparing cash disbursement

voucher.

6. Periodically reconciles accounts payable ledger with its control account

from general ledger.

7. All invoices are paid within stipulated time to get cash discount.

8. Cash disbursement voucher and its supporting documents are stamped

“Paid” by cash disbursement function after the check has been sent to

supplier. To avoid the use of supporting document more than one as basis

for cash disbursement voucher.

Page 48

37

CHAPTER III

METHOD OF DATA PROCESSING

AND COMPANY’S EXISTING CONDITION

III.1 Data Collecting and Processing

In this research, researcher gets primary data directly from the company’s

sources. Writer did some audit procedure for collecting and processing primary

data as follows : inquiries of the clients, observation, and documentation. The

colection was done in December 2013.

1. Interview.

In this procedure, writer asked for the information that was obatined

through oral interviews and discussions with the management of the company.

Inquiries process will allows the interviewees to answer from their point of

view rather than focusing on a structural question with limited answer. The

interviewees can also express their thought or answer freely.

In this research, writer interviews the interviewees directly one by one.

Before question and answer section, writer already prepared the question first.

During the interview, writer ask additional questions out of questions list,

depend’s on interviewees’s response to the question.

Writer interviewed all parties that related directly or indirectly to the

purchasing process. They are head of purchasing department, purchasing staff,

Page 49

38

and human resource department. Interviewees gave information about company

profile, job description, and standard operation of purchasing process.

2. Observation

Researcher did observation to gather the data by seeing, hearing, and

feeling to assess certain activities in the company. Writer is doing observation

by attending the place observed and observing the management’s daily

activities, especially activities in purchasing. Observation is done starting on

December 23, 2013 until January 10, 2013 and take place at the company’s

office at Jl. Prof M. Yamin SH, No. 42 A Pekanbaru, Riau. By doing this

observation, wrtiter knows working environment, actual activities and

processes, and real condition in the company related with purchasing

activities. Writer can also identify the strength and weaknesses occured during

the observation.

3. Documentation

Documentation is the process of tracking down evidences either internal or

external evidences of transactions or activities being researched. The

researcher tracked down several purchasing documents, such as request note,

purchase requisition, purchase order, sending and receiving form. In thic case,

the researcher tried to obtain the understanding of those document in PT.

XYZ, the person who create and authorize, and the detail that stated in the

documents.

Page 50

39

The result of data collection process is as follow:

III.2 Company’s Background

III.2.1. Background

PT. XYZ is a private company established on May 1st, 1993 at Pekanbaru,

Riau, Indonesia with notary Tajib Raharjo, SH, No. C2- 1300 HT. 01. 01- TH.

1993. There are several changes on management of the company, the last changes

happened at July 9th

, 2012. Regarding the changes and replacement of Directors

and Commisioners.

This company involves in two activities which are plantation and

manufacturre that producing CPO (Crude Palm Oil). The plantation and

manufacture located in Petapahan Jaya Village, Riau Province and the headquarter

office located in Jl. Prof.M.Yamin No.42 A, Pekanbaru, Riau.

PT. XYZ has motto 3P :

1. Performance : The achievement

What had been done

2. Potential : Plan and opportunities

What should been done

3. Passion : Desire

Sense of belonging

Vision :

“The Best Palm Oil Company in Indonesia”

Page 51

40

Mision :

1. Managing the palm oil business in a professional manner to produce the

product with quality that based on market desired

2. Implement the palm oil cultivation with environmentally friendly

technology and society empowerment.

3. Creating a mutually beneficial partnership that synergy with justice and

the absence of oppression

4. Having a professional, disciplined, reliable, faithful and religious human

resource.

5. Become a producer of palm oil that competitive, profitable and useful for

the nation and the State.

III.2.2. Organization Structure

The researcher gets to know the information about company’s

structure organization and job description by interviewing the management of

the company. The organization structure for head office can be seen on figure

3.1 and the organization structure for manufacture can be seen on figure 3.2

Page 52

41

Figure 3.1 Organization Structure of PT. XYZ - Head Office

Director

Finance Manager

Accounting

Chasier

Operational Manager Sales

Production Manager

Purchasing Manager Purchasing Staff

Human Resource

Page 53

42

Figure 3.2 Organization Structure of PT. XYZ - Manufacture

III.2.3. Job Description

Below is the job descriptions for each department in the head office:

a. Director

Job description :

Determine the company’s goals

Establish policies in achieving company’s goal

Production Manager

Traksi

Workshop

Transportation

Administrative Office

Warehouse

Cashier

Administration Operator

Laboratory

Page 54

43

Lead, coordinate, and supervise all company’s operations

Responsibility for the work implementation and achievement of

company’s goal.

Hire proficient managers

Oversee the operational report, operasional report, and financial

report

b. Finance Manager

Job description :

Manage and control every financial activities in the company

Supervise activities regarding cash receipts and cash payments

Head of cashier and accounting department

Managing budgets

c. Accounting

Job description :

Making financial report in accordance with rule and regulation

Calculate tax, ensure the payment, make report, and other tax

requirments

Verify and check all documents that related in payment and receipt

activities

d. Cashier

Job description :

Arrange payments and receipts for both cash and credit

Page 55

44

Responsibility for petty cash

Make cash and bank reconciliation

e. Operational Manager

Job description:

Monitoring operational jobs to ensure the activity in the company

works properly.

Communicating with other departments in making decision related

with operational activity.

Supervise the sales activity

f. Sales Staff

Job description:

Maintaining and deaveloping the realtionship with existing

customer

Find a link to a new customer

Maintain the good record of order from existing customer.

g. Puchasing Manager

Job description:

Negotiating and agreeing offer with the supplier.

Approve the purchase order.

Build a good relationship with the suppliers

Follow up every price update.

Page 56

45

h. Purchasing Staff

Job description :

Find and choose the best products and suppliers in terms of price,

delivery schedules and quality

Make purchase order to the selected supplier

Coordinate the receiving activities of material purchased

Arrange the sending activities of material received to the

manufacture

Make a recapitulation of purchase order based section in plantation

i. Human Resource

Job description:

Organiza the recruitment, employment, and placement of new

employess

Coordinating the implementation employee benefits, such as obtain

of employement and social insurance

Supervising the ethical conduct of employees in the company

Maintain the attendance report of the employees

Moreover, below is job decriptions in the manufacture :

a. Production Manager

Job description:

Ensuring continuity in quality of product

Ensuring that production is cost effective

Page 57

46

Ensure implementation of safety procedure

Monitoring product standard and implementing quality control

program

Ensure that planning of efficiency and performance are met even

exceed.

Manage the manufacturing operation consistent with the company

guidelines.

b. Traksi

Job description:

Maintain all machines and equipment in order to make them ready

to operate

Maintain and repair the manufacture infrastructure.

Plan the preparation of spare part for machines and equipments

Asking spare part needed to the warehouse

c. Workshop

Job description:

Set the mechanic in accordance with their skills.

Maintain and repair all manufacture equipment and machine.

Maintain the cleanliness and environmental security of workshop.

Page 58

47

d. Transportation

Job description:

Set up and check the transportation in order to make them ready to

operate

Make daily report about tranportation problems.

Control the continuity of daily transportation.

e. Administration

Job description:

Responsibility of administrative matters related to manufacture.

Help and control the continuity of production activity.

Give regular report to the head office.

f. Warehouse

Job description:

As a place to store the spare part and other support equipment

needed by the manufacture

As a place to receive the spare part or other support equipment

from the purchase department

g. Operator

Job description:

Responsibility to do daily check to the production machine

Make daily job report.

Responsibility for the state of production machine

Page 59

48

h. Laboratory

Job description:

As control center towards the quality of CPO produced during and

after the production process.

III.3. Company’s Purchasing Process

The discussion is about the purchasing process of spare parts in the

manufacture that applied by PT XYZ . Purchasing by credit is an activity that

is routinely performed by this company. This company does not have written

standard operation procedure (SOP) so the researcher gets to know the

procedure by interviewing purchasing staff of PT XYZ.

The detail of purchasing process can be seen on the flow chart

below:

Page 61

50

A. Documents Used in Purchasing Process :

1. Demand and Taking Out Stock Form (NPPB/ Nota Permintaan dan

Pengeluaran Barang)

Traksi staff who require spare parts send this form to the

warehouse. This form consists of name of product, the requested amount

and received amount, section who will use the spare part, and the date and

form’s number which is wrote manually.

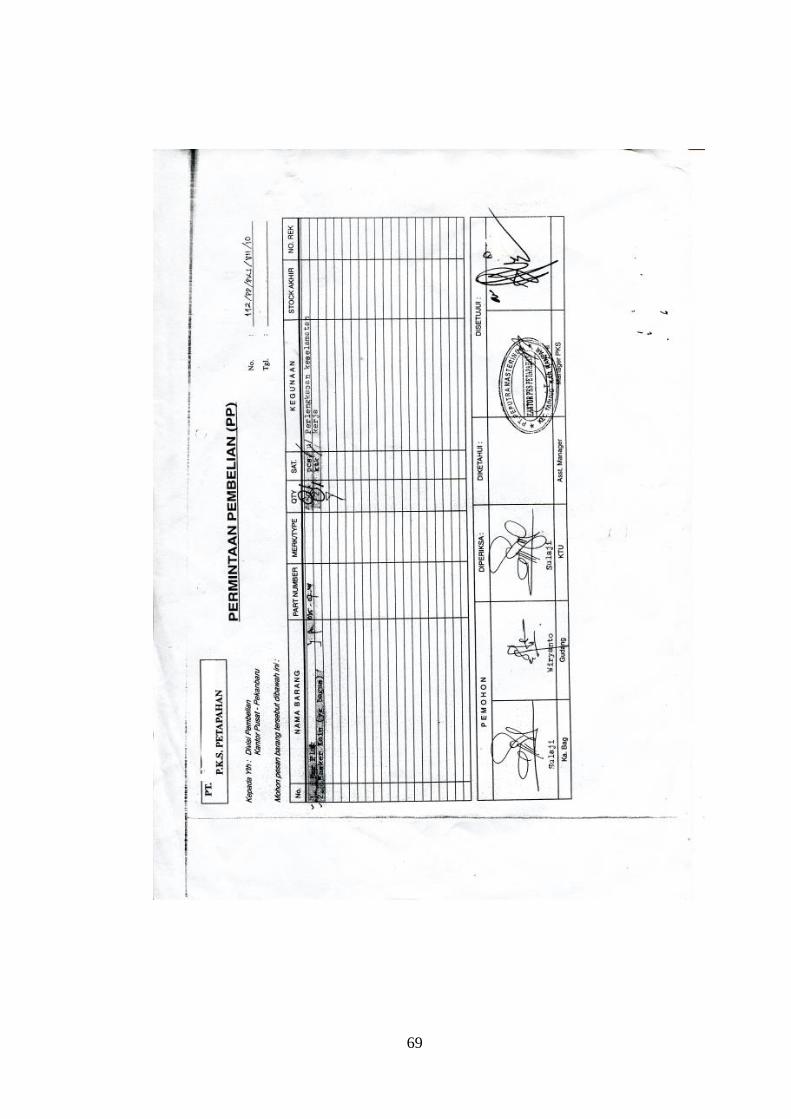

2. Purchase Requisition

This form is create by traksi to the purchasing department. This

form identify the items information being ordered such as the name/type,

the quality, the quantity, the use, the last stock amount in the warehouse,

and form number that written manually.

3. Quotation

The purchasing department who receives the purchase requisition

from the warehouse will ask quotations from three suppliers. The

information requested from the suppliers are informations contained in the

purchase requisition form. The information given by supplier usually by

phone, email, or fax.

4. Purchase Order

After receiving back the quotations from supplier, the Purchasing

manager will select one supplier and agree with the information given.

After that the purchasing department issuing the purchase order to that

Page 62

51

supplier. Purchase order contains information about the name of the

supplier, name of goods (brand, type, quality), the amount, price, purchase

requisition number, taxes incurred (PPN, PPH), date, and purchase order

number which is written manually.

5. Sending and Receiving Report (SPPB/ Surat Pengantar dan

Permintaan Barang)

After receive spare part ordered from the supplier, purchasing staff

check and compare the spare part received with the purchase order. If

already accordance with the purchase order, then purchasing staff arrange

the delivery by driver to the warehouse. The delivery must be

accompanied by sending and receiving form that created by purchasing

department. The informations contained in the form are the name or type

of spare part, the quantity, purchase request number, purchase order

number, date, and form number which is written manually.

B. Purchasing Process

1. The request came from the traksi staff. Traksi staff has job to routinely

check the spare part used in the machine and make a request when the

spare part needed, and also responsible for the use of spare part. Head

of traksi using demand and taking out stock form for request and give

it to the warehouse. In order to be valid, this form has to be signed by

head of traksi, administrative office, and production manager. This

form is made in three copies

Page 63

52

a) 1st copy to the accounting

b) 2nd copy to the warehouse

c) 3rd copy as file for traksi staff

2. After receive the demand and taking out stock form (NPPB), the

warehouse staff will check the availability of the spare part. If the

spare part is available then it will go directly to the traksi staff who

requires it, if there is no stock or the amount of stock is low, then the

warehouse staff makes a purchase requisition (PR). After that the

purchase requisition send to the purchasing department. In order to be

valid, purchase requisition form should be signed by the head of the

warehouse, administrative office, and production manager. Purchase

requisition form is made in two copies

a) 1st copy to the purchasing department

b) 2nd copy as file for warehouse

3. After receive the purchase requisition, the purchasing staff will ask

quotation from three suppliers. After receive the three quotations, the

head of purchasing department decide which supplier to be choose.

This activity done by phone, fax, or email.

4. After decide the supplier, then purchasing staff create a purchase order

and send it to that supplier. Purchase order is valid after signed by the

purchasing manager and approved by finance or director. Purchase

Order (PO) is made in 4 copies

Page 64

53

a) 1st copy to supplier

b) 2nd copy kept by purchasing department

c) 3rd and 4th copy to accounting department

5. Spare parts ordered by the purchasing department directly sent by the