SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA – “Journal of Management Research” “Journal of Management Research” “Journal of Management Research” “Journal of Management Research” Vol 2 Vol 2 Vol 2 Vol 2, Issue 1 ssue 1 ssue 1 ssue 1 March March March March 2014 2014 2014 2014 www.eecmbajournal.in www.eecmbajournal.in www.eecmbajournal.in www.eecmbajournal.in 114 ANALYSIS OF RELATIONSHIP OF ADR AND GDR PRICES WITH THE NATIONAL AND INTERNATIONAL MARKET Sharmistha Ghosh, Assistant Professor Department of Commerce, Shri Shikshayatan College, Kolkata Abstract The capital market of a country holds great significance with respect to its economic growth. Capital markets in India as well as across the globe are progressively getting interconnected. The new financial instrument for tapping the international markets may be termed as Depository Receipts (DRs). A depositary receipt is a negotiable financial instrument issued by a bank to represent a foreign company's publicly traded securities. It is a type of negotiable (transferable) financial security that is traded on a local stock exchange but represents a security, usually in the form of equity that is issued by a foreign publicly listed company. Recently, Depository Receipts, especially, American Depository Receipts (ADR) and Global Depository Receipts (GDR) have become a popular investment alternative for the investors in India. ADR were first issued in 1927 and they account for the maximum number of trades in comparison to GDRs. Both ADRs and GDRs help investors looking to tap a new investor base, expand awareness, or raise capital. In this context, this paper aims at discussing the role of ADR and GDRs issuance. It also showcases the different aspects of Depository Receipt issues along with their relationship with the Indian and International securities market. Key Words: Depository Receipts, American Depository Receipt, Global Depository Receipt, Foreign Direct Investment, Regulation S. Introduction As the country grows and expands with the globalization of the economy, one important aspect with regard to the investment opportunities available to investors is the introduction of Depository Receipts (DRs) as an investment alternative. A DR is a tradable instrument that represents an ownership interest in securities of a foreign issuer typically trading outside its

Transcript

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

ANALYSIS OF RELATIONSHIP OF ADR AND GDR PRICES WITH THE

NATIONAL AND INTERNATIONAL MARKET

Sharmistha Ghosh, Assistant Professor

Department of Commerce, Shri Shikshayatan College, Kolkata

Abstract

The capital market of a country holds great significance with respect to its economic growth.

Capital markets in India as well as across the globe are progressively getting interconnected.

The new financial instrument for tapping the international markets may be termed as

Depository Receipts (DRs). A depositary receipt is a negotiable financial instrument issued by a

bank to represent a foreign company's publicly traded securities. It is a type of negotiable

(transferable) financial security that is traded on a local stock exchange but represents a

security, usually in the form of equity that is issued by a foreign publicly listed company.

Recently, Depository Receipts, especially, American Depository Receipts (ADR) and Global

Depository Receipts (GDR) have become a popular investment alternative for the investors in

India. ADR were first issued in 1927 and they account for the maximum number of trades in

comparison to GDRs. Both ADRs and GDRs help investors looking to tap a new investor base,

expand awareness, or raise capital. In this context, this paper aims at discussing the role of ADR

and GDRs issuance. It also showcases the different aspects of Depository Receipt issues along

with their relationship with the Indian and International securities market.

Key Words: Depository Receipts, American Depository Receipt, Global Depository Receipt,

Foreign Direct Investment, Regulation S.

Introduction

As the country grows and expands with the globalization of the economy, one important aspect

with regard to the investment opportunities available to investors is the introduction of

Depository Receipts (DRs) as an investment alternative. A DR is a tradable instrument that

represents an ownership interest in securities of a foreign issuer typically trading outside its

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

home market. Most common types of Depository Receipts are the American Depository

Receipts (ADRs) and Global Depository Receipts (GDRs). ADRs are issued by the United States

(US) in lieu of a non-US company’s shares which are traded on the US exchange although the

companies itself are not listed on the US exchange. The DRs which are not listed on US

exchange but in other country’s exchanges most commonly in London or Luxembourg are

termed as Global depository Receipts (GDRs). A depositary receipt where the issuing bank is

European will sometimes be called a European Depositary Receipt (EDR). While by creating a

depositary receipts program, the companies are able to gain the flexibility and access they need

to achieve the company’s strategic goals it also hold special appeal for investors because they

make investing in a company beyond the investor’s home borders easy and convenient. This

attribute fuels investor appetite, which in turn has driven explosive growth in the depositary

receipt market. So, from an investor’s point of view the ADR or GDR is essentially a certificate

issued by a bank that gives the owner rights over a foreign share. It can be listed on a stock

exchange and bought and sold just like a normal share. The holder of an ADR or GDR is entitled

to all benefits such as dividends and rights issues from the underlying shares but they are

sometimes though not always able to vote. Initially, most of the issues were done through

private placement route during the 1990’s but afterwards the exchange traded ADRs were

introduced. In this respect this paper is organized as follows. Section 2 gives an overview of

depository receipts and their benefits. Section 3 draws an analysis of ADR and GDR prices and

studies their relation with the different market indices. Section 4 states the regulations

regarding ADR GDR issue and divestment of shares in India. And finally the last section is

devoted to conclusion and recommendations.

Overview of Depository Receipts

While depositary receipt (DR) programs can be structured in a variety of ways, there are two

basic options: American Depositary Receipt (ADR) programs, which give companies access to

the US capital markets, and Global Depositary Receipt (GDR) programs, which provide exposure

to the global markets outside the issuer’s home market and the institutional investor market in

the US.

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

American Depositary Receipts (ADRs) offer the issuing company access to the world’s largest

and most active capital market. Correspondingly, ADRs provide investors in the US with a

convenient way to directly invest in international companies while avoiding the risks

traditionally associated with securities held in other countries. ADRs are dollar-denominated

securities that trade, clear and settle like any other US security. Whether traded over-the-

counter or on one of the major US exchanges, ADRs are a mainstream and popular option for

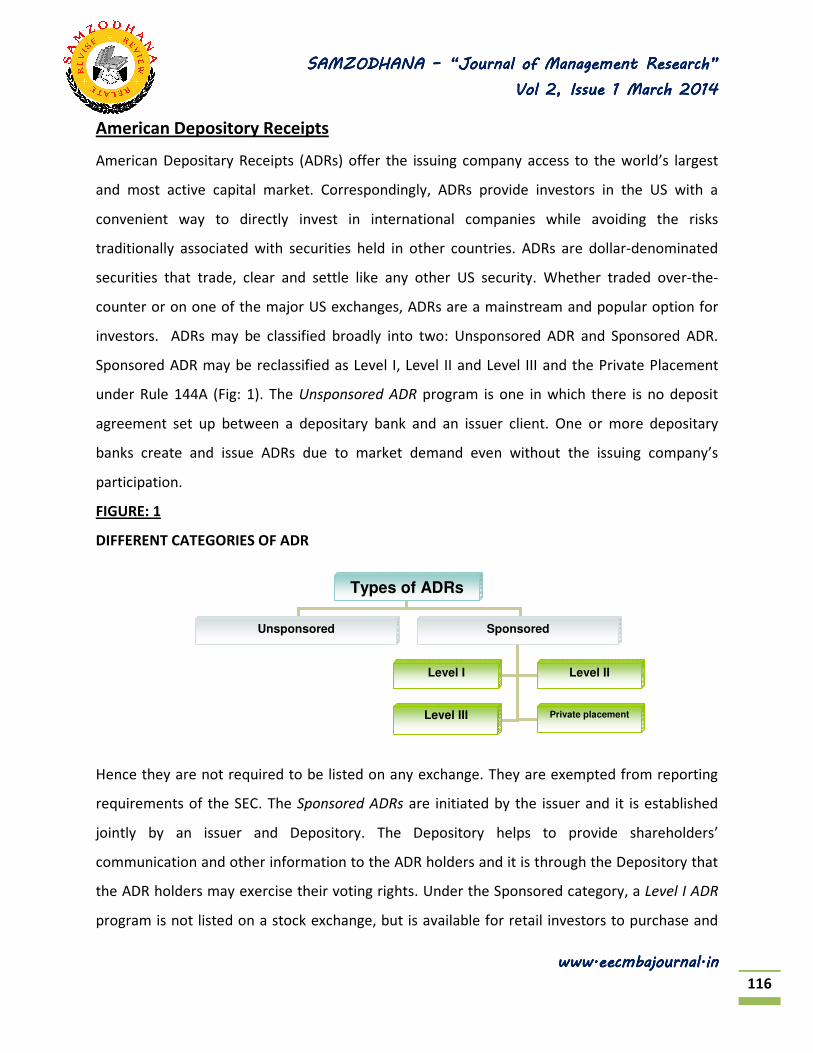

investors. ADRs may be classified broadly into two: Unsponsored ADR and Sponsored ADR.

Sponsored ADR may be reclassified as Level I, Level II and Level III and the Private Placement

under Rule 144A (Fig: 1). The Unsponsored ADR program is one in which there is no deposit

agreement set up between a depositary bank and an issuer client. One or more depositary

banks create and issue ADRs due to market demand even without the issuing company’s

participation.

FIGURE: 1

DIFFERENT CATEGORIES OF ADR

Hence they are not required to be listed on any exchange. They are exempted from reporting

requirements of the SEC. The Sponsored ADRs are initiated by the issuer and it is established

jointly by an issuer and Depository. The Depository helps to provide shareholders’

communication and other information to the ADR holders and it is through the Depository that

the ADR holders may exercise their voting rights. Under the Sponsored category, a Level I ADR

program is not listed on a stock exchange, but is available for retail investors to purchase and

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

trade in the over-the-counter market via NASDAQ’s Pink Sheets. A Level I program does not

create new capital in the US; rather, it gives the company an opportunity to develop or expand

its shareholder base by establishing a foothold in the US market. It maintains home market

accounting and disclosure standards. They use existing shares to satisfy investor demand and

liquidity. New DRs are created by issuing and canceling ordinary shares in the issuer’s home

market. These Level I ADRs are registered with the US Securities and Exchange Commission. A

Level II ADR uses existing shares to satisfy investor demand and liquidity. New ADRs are created

from deposits of ordinary shares in the issuer’s home market. Because these securities are

listed or quoted on a major US exchange, Level II ADRs reach a broader universe of potential

shareholders and gain increased visibility through reporting in the financial media. These are

more expensive than the Level I ADRs. Listed securities can be promoted and advertised, and

may be covered by analysts and the media. In addition, listed securities can be used to

structure incentives for an issuer’s US employees, or could be used to facilitate US mergers and

acquisitions. Level III ADRs are a public offering of new shares into the US markets. These

capital raisings have a high profile and are most expensive. They are followed closely by the

financial press and other media, often generating significant visibility for the issuer. Apart from

all these, the Rule 144A ADR is the unique one. It is the quickest, easiest, and most cost-

effective way to raise capital in the United States. New, restricted shares are created and then

privately placed with institutional investors. Rule 144A facilitates the resale of privately placed

securities to Qualified Institutional Buyers (QIBs) in the US. These do not need to conform to

the full SEC reporting and registration requirements.

Global Depository Receipts

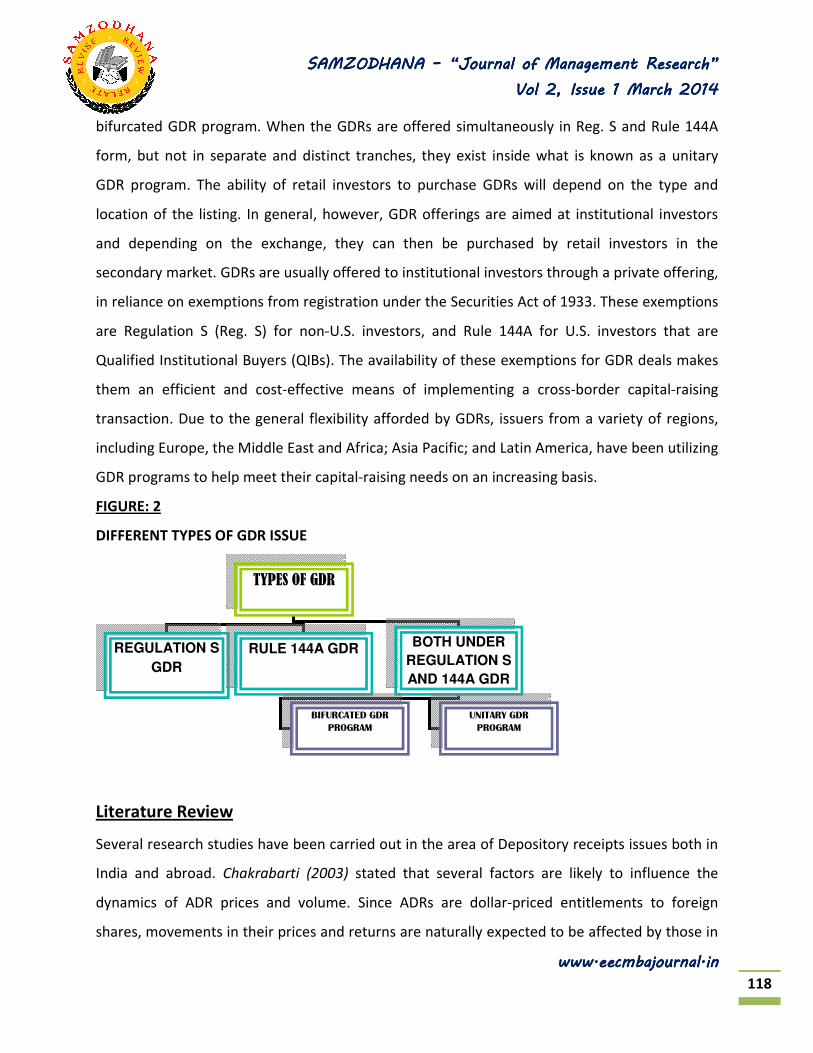

The typical GDR structure offers DRs in Europe or other non-US markets pursuant to Regulation

S (Reg. S) promulgated under the US Securities Act of 1933. The predominant listing venues for

Reg. S GDRs are the London and Luxembourg Stock Exchanges, with GDRs having also been

listed on the Singapore Exchange, Frankfurt Stock Exchange and Nasdaq Dubai. Rule 144A GDRs

trade in the U.S. over-the-counter market. When GDRs are offered simultaneously in Reg. S and

Rule 144A form, but in separate and distinct tranches, they exist inside what is known as a

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

bifurcated GDR program. When the GDRs are offered simultaneously in Reg. S and Rule 144A

form, but not in separate and distinct tranches, they exist inside what is known as a unitary

GDR program. The ability of retail investors to purchase GDRs will depend on the type and

location of the listing. In general, however, GDR offerings are aimed at institutional investors

and depending on the exchange, they can then be purchased by retail investors in the

secondary market. GDRs are usually offered to institutional investors through a private offering,

in reliance on exemptions from registration under the Securities Act of 1933. These exemptions

are Regulation S (Reg. S) for non-U.S. investors, and Rule 144A for U.S. investors that are

Qualified Institutional Buyers (QIBs). The availability of these exemptions for GDR deals makes

them an efficient and cost-effective means of implementing a cross-border capital-raising

transaction. Due to the general flexibility afforded by GDRs, issuers from a variety of regions,

including Europe, the Middle East and Africa; Asia Pacific; and Latin America, have been utilizing

GDR programs to help meet their capital-raising needs on an increasing basis.

FIGURE: 2

DIFFERENT TYPES OF GDR ISSUE

Literature Review

Several research studies have been carried out in the area of Depository receipts issues both in

India and abroad. Chakrabarti (2003) stated that several factors are likely to influence the

dynamics of ADR prices and volume. Since ADRs are dollar-priced entitlements to foreign

shares, movements in their prices and returns are naturally expected to be affected by those in

TYPES OF GDR

REGULATION S

GDR

RULE 144A GDR BOTH UNDER

REGULATION S

AND 144A GDR

BIFURCATED GDR

PROGRAM

UNITARY GDR

PROGRAM

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

the underlying shares and the relevant exchange rate. The host country (the US) market

becomes the natural candidate for such a factor, since American investors, who are obviously

affected by the movements in the US market, trade ADRs. Thus, the US market movements

constitute a usual suspect in the study of ADR prices and returns. He further empirically

investigated that how much of the variation in ADR prices may be explained by different

variables affecting them and found that ADR issuance often has a temporary positive effect on

the underlying stock price, but usually does not materially alter the stock’s relationships with

the US and Indian markets. Saxena (2005) analyzed the trend in ADR premiums and the

movement in ADR premium levels over 2001-2005 period. He also analyzed the relation in

movement of ADR prices with the prices of underlying equity and concluded that ADR prices do

not move in lock-step with underlying equity prices. A study conducted by Bank of New York,

Mellon (2007) to provide an independent, robust analysis of the value and liquidity effects of

depositary receipts (DRs) established by companies from emerging markets analysed DR

programs of 628 firms covering the period 1980-2007. The study covered the BRIC countries of

Brazil, Russia, India and China along with Asia, Eastern Europe, Middle East countries and Africa.

It was shown empirically that DR programmes established by firms in emerging markets add

significant value and improve home-market liquidity to the benefit of both issuers and

investors. DRs additionally provide a strong signal of willing disclosure, greater transparency

and superior governance, particularly important from emerging, less-regulated markets.

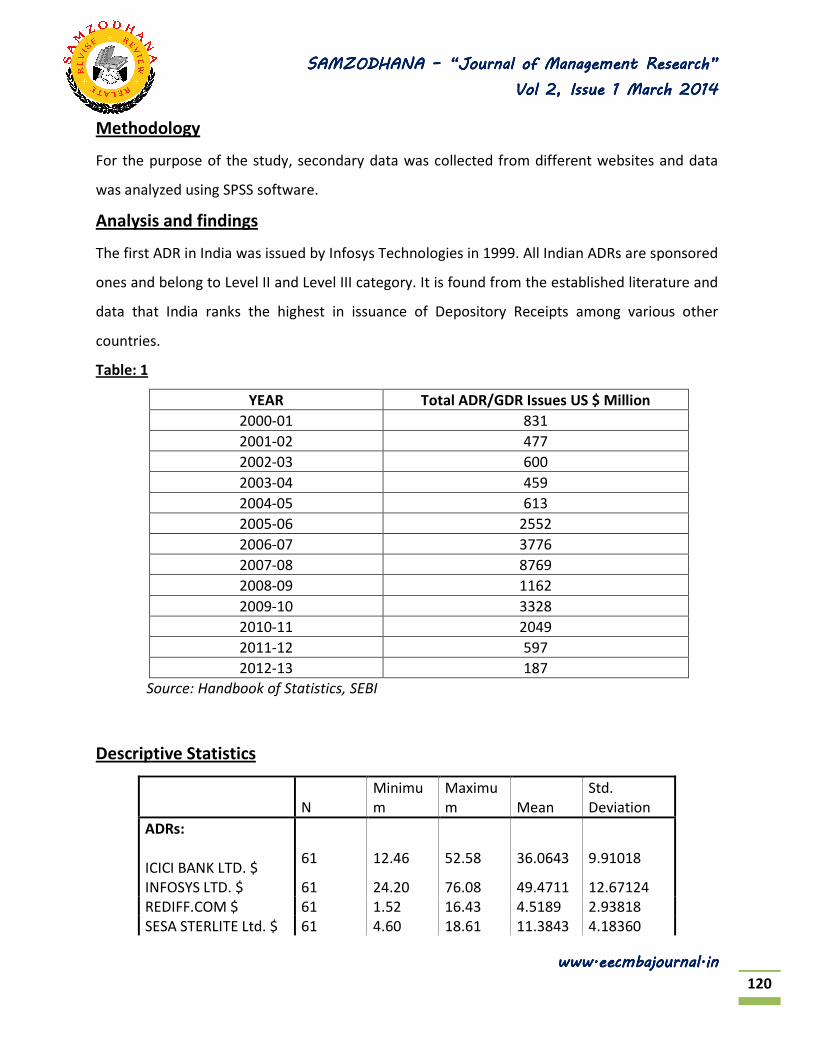

Likewise, several research studies were carried out on various aspects of ADR/GDR issues but

not much work has been done in Indian context. The present study aims at fulfilling this

vaccum.

Objective of study

The paper aims to analyze the relationship between the ADR prices with their underlying equity

prices and the S&P 500 Index. It also tries to show the sensitivity of the underlying equity prices

to one of the Indian stock market index i.e. BSE Sensex. In addition, the paper draws the

relationship between the different Indian stock market Indices (CNX Nifty and BSE Sensex) to

the US stock market Index S&P 500.

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

HDFC BANK LTD. Rs. 61 177.0 703.7 429.104 150.2343

TATA MOTORS LTD.

Rs. 61 136.35 1306.30

528.840

2 361.12928

WIPRO Rs. 61 207.4 706.8 425.366 116.3902

MTNL Rs. 61 17.3 104.2 53.865 26.0023

Valid N (listwise) 61

N

Minimu

m

Maximu

m Mean Std. Deviation

INDICES:

S & P BSE SENSEX

61

8891.61

0

20509.0

90

16597.9

26

3011.808

CNX NIFTY 61 2802.3 6134.5

4990.10

5 893.3480

S & P 500 61 735.09 1630.74

1215.39

18 210.70744

Valid N (listwise) 61

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

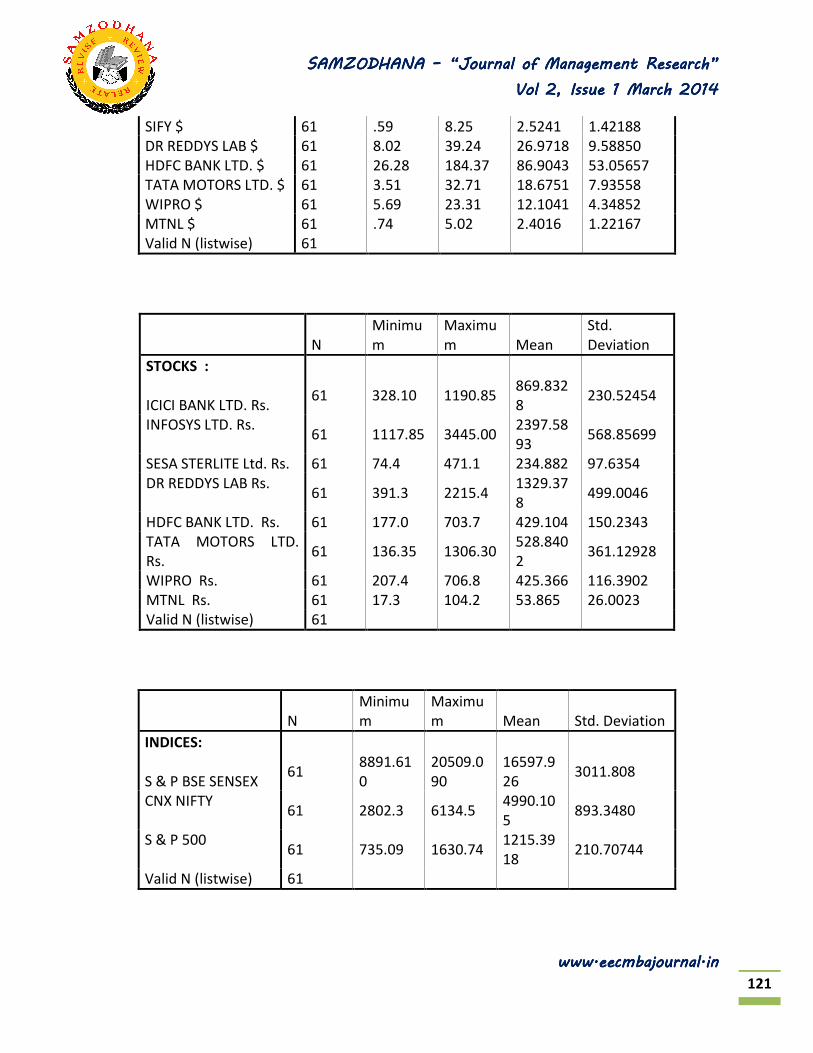

It is observed that HDFC Bank ADR is having the highest average price among the others with

the highest standard deviation as well. While in the domestic market Infosys ltd. shares has the

highest mean price. In case of indices, S&P 500 has the lowest deviation from its mean.

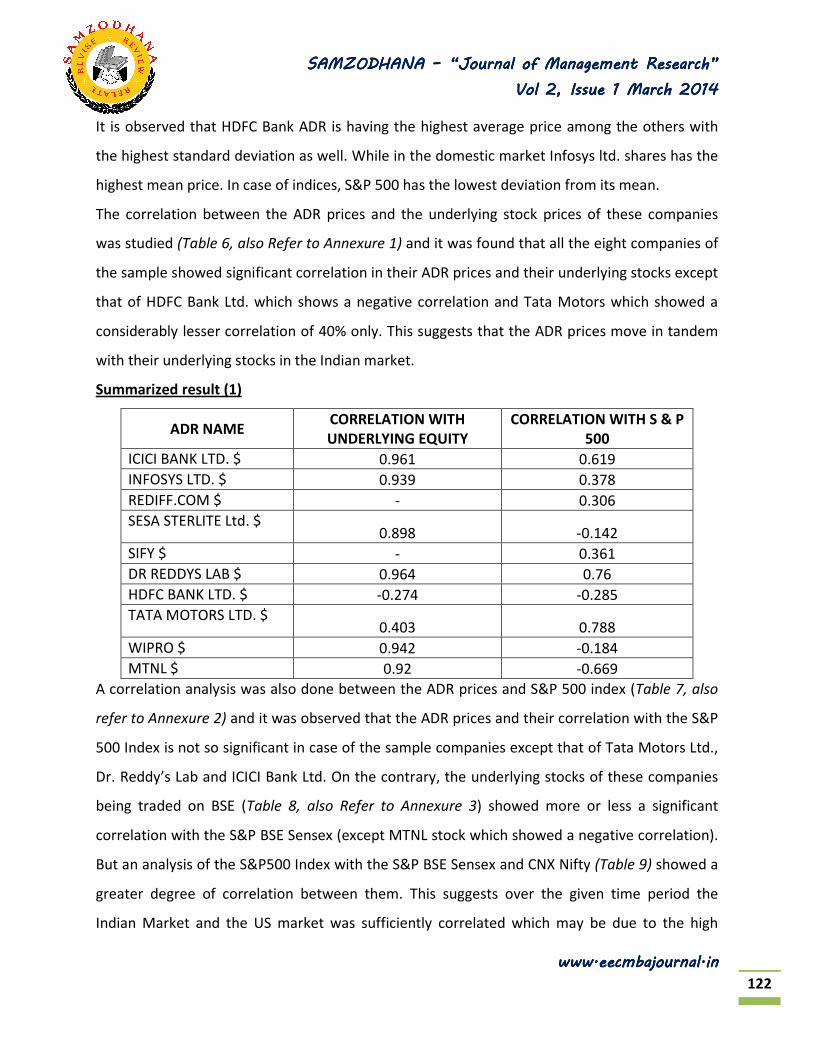

The correlation between the ADR prices and the underlying stock prices of these companies

was studied (Table 6, also Refer to Annexure 1) and it was found that all the eight companies of

the sample showed significant correlation in their ADR prices and their underlying stocks except

that of HDFC Bank Ltd. which shows a negative correlation and Tata Motors which showed a

considerably lesser correlation of 40% only. This suggests that the ADR prices move in tandem

with their underlying stocks in the Indian market.

Summarized result (1)

ADR NAME CORRELATION WITH

UNDERLYING EQUITY

CORRELATION WITH S & P

500

ICICI BANK LTD. $ 0.961 0.619

INFOSYS LTD. $ 0.939 0.378

REDIFF.COM $ - 0.306

SESA STERLITE Ltd. $ 0.898 -0.142

SIFY $ - 0.361

DR REDDYS LAB $ 0.964 0.76

HDFC BANK LTD. $ -0.274 -0.285

TATA MOTORS LTD. $ 0.403 0.788

WIPRO $ 0.942 -0.184

MTNL $ 0.92 -0.669

A correlation analysis was also done between the ADR prices and S&P 500 index (Table 7, also

refer to Annexure 2) and it was observed that the ADR prices and their correlation with the S&P

500 Index is not so significant in case of the sample companies except that of Tata Motors Ltd.,

Dr. Reddy’s Lab and ICICI Bank Ltd. On the contrary, the underlying stocks of these companies

being traded on BSE (Table 8, also Refer to Annexure 3) showed more or less a significant

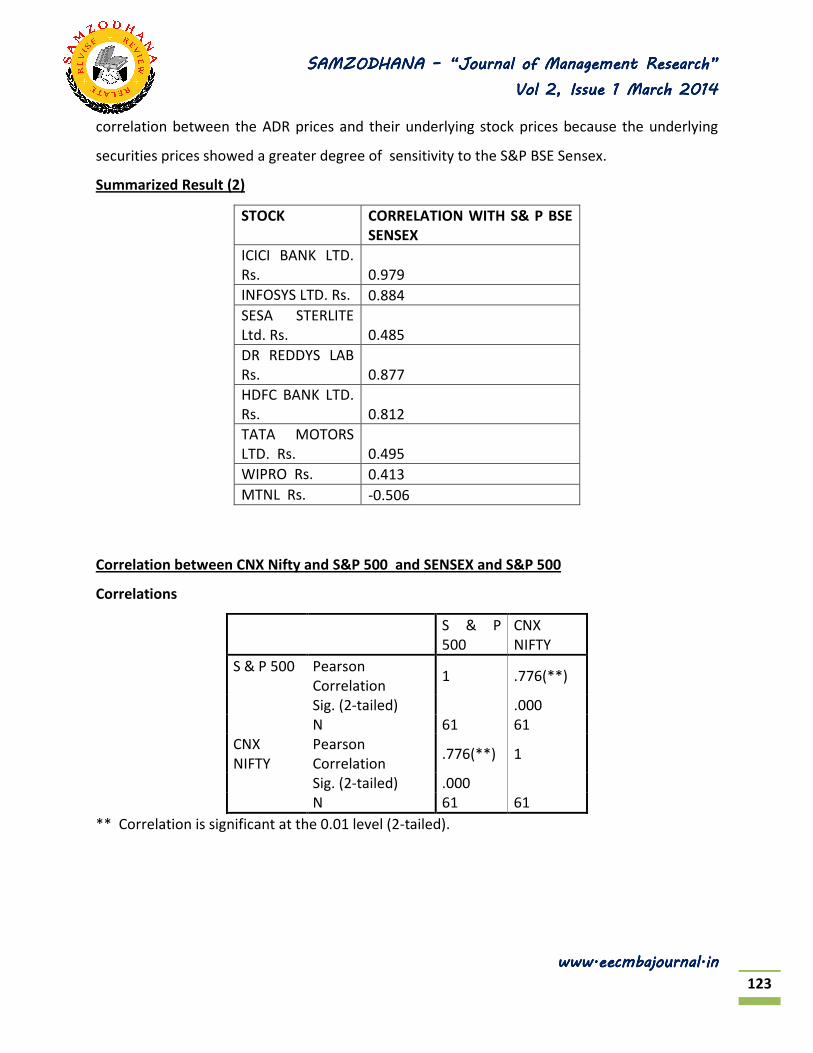

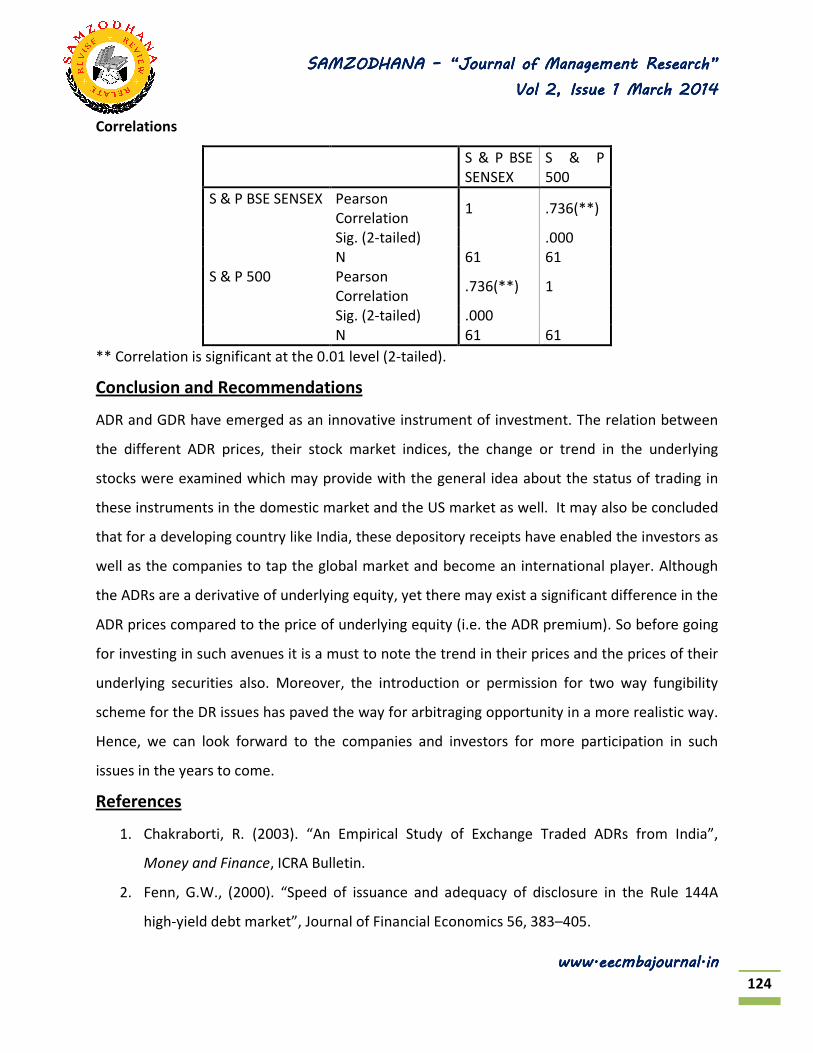

correlation with the S&P BSE Sensex (except MTNL stock which showed a negative correlation).

But an analysis of the S&P500 Index with the S&P BSE Sensex and CNX Nifty (Table 9) showed a

greater degree of correlation between them. This suggests over the given time period the

Indian Market and the US market was sufficiently correlated which may be due to the high

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

correlation between the ADR prices and their underlying stock prices because the underlying

securities prices showed a greater degree of sensitivity to the S&P BSE Sensex.

Summarized Result (2)

Correlation between CNX Nifty and S&P 500 and SENSEX and S&P 500

Correlations

S & P

500

CNX

NIFTY

S & P 500 Pearson

Correlation 1 .776(**)

Sig. (2-tailed) .000

N 61 61

CNX

NIFTY

Pearson

Correlation .776(**) 1

Sig. (2-tailed) .000

N 61 61

** Correlation is significant at the 0.01 level (2-tailed).

STOCK CORRELATION WITH S& P BSE

SENSEX

ICICI BANK LTD.

Rs. 0.979

INFOSYS LTD. Rs. 0.884

SESA STERLITE

Ltd. Rs. 0.485

DR REDDYS LAB

Rs. 0.877

HDFC BANK LTD.

Rs. 0.812

TATA MOTORS

LTD. Rs. 0.495

WIPRO Rs. 0.413

MTNL Rs. -0.506

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”

** Correlation is significant at the 0.01 level (2-tailed).

Conclusion and Recommendations

ADR and GDR have emerged as an innovative instrument of investment. The relation between

the different ADR prices, their stock market indices, the change or trend in the underlying

stocks were examined which may provide with the general idea about the status of trading in

these instruments in the domestic market and the US market as well. It may also be concluded

that for a developing country like India, these depository receipts have enabled the investors as

well as the companies to tap the global market and become an international player. Although

the ADRs are a derivative of underlying equity, yet there may exist a significant difference in the

ADR prices compared to the price of underlying equity (i.e. the ADR premium). So before going

for investing in such avenues it is a must to note the trend in their prices and the prices of their

underlying securities also. Moreover, the introduction or permission for two way fungibility

scheme for the DR issues has paved the way for arbitraging opportunity in a more realistic way.

Hence, we can look forward to the companies and investors for more participation in such

issues in the years to come.

References

1. Chakraborti, R. (2003). “An Empirical Study of Exchange Traded ADRs from India”,

Money and Finance, ICRA Bulletin.

2. Fenn, G.W., (2000). “Speed of issuance and adequacy of disclosure in the Rule 144A

high-yield debt market”, Journal of Financial Economics 56, 383–405.

SAMZODHANA SAMZODHANA SAMZODHANA SAMZODHANA –––– “Journal of Management Research”“Journal of Management Research”“Journal of Management Research”“Journal of Management Research”