25

By: Agrawal Bhavin 02 Jaydeep Gandhi 20 Nitin Madhavi 28 Jignesh Soni 32

| Date post: | 17-Jul-2015 |

| Category: |

Data & Analytics |

| Upload: | bhavin-agrawal |

| View: | 81 times |

| Download: | 6 times |

By:

Agrawal Bhavin 02

Jaydeep Gandhi 20

Nitin Madhavi 28

Jignesh Soni 32

•TATA STEEL LTD Established in 1907 as Asia's first integrated private

sector steel company

•Tata Steel Limited was the 12th largest steel producing company in the

world in 2012, with an annual crude steel capacity of 23.8 million tones

• The second largest private-sector steel company in India (measured by

domestic production) with an annual capacity of 9.7 million tonnes after

SAIL and JSW Steel

•Tata Steel has manufacturing operations in 26 countries, including

Australia, China, India, the Netherlands, Singapore, Thailand and the

United Kingdom

Cont… As on 31 March 2013, Tata Group held 31.35% shares in Tata Steel.

Over 1 million individual shareholders hold approx. 21% of its

shares Life Insurance Corporation of India is the largest non-

promoter shareholder in the company with 14.98% shareholding.

In 2013, Tata Steel was ranked India's 7th most admired company by

Fortune magazine. It was India's most admired company in 2012.

ANALYSIS OF BALANCE SHEET

70000

72000

74000

76000

78000

80000

82000

84000

86000

88000

Asset

2012

2013

2014

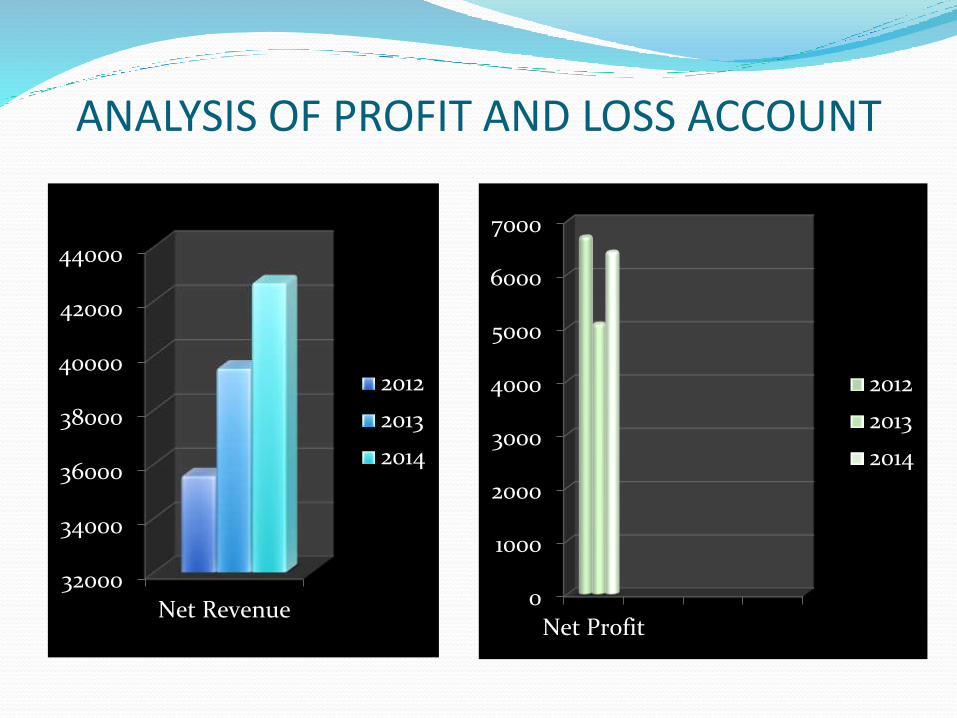

ANALYSIS OF PROFIT AND LOSS ACCOUNT

32000

34000

36000

38000

40000

42000

44000

Net Revenue

2012

2013

2014

0

1000

2000

3000

4000

5000

6000

7000

Net Profit

2012

2013

2014

Ratio Analysis :

Meaning: Ratio analysis is a tool brought into play by

individuals to carry out an evaluative analysis of information in

the financial statements of a company

These ratios are calculated from current year figures and then

compared to past years, other companies, the industry, and also

the company to assess the performance of the company.

Besides, ratio analysis is used predominantly by proponents of

financial analysis

WORKING CAPITAL RATIO

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2011-2012 2012-2013 2013-2014

Ratio

Ratio

0.93

0.86

0.57

Current Ratio

Acid Test Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2011-12 2012-13 2013-14

Ratio

Ratio

1.161.04

0.68

Debtors Turnover Ratio

0

10

20

30

40

50

60

2011-12 2012-13 2013-2014

Ratio

37.533

47.93354.113

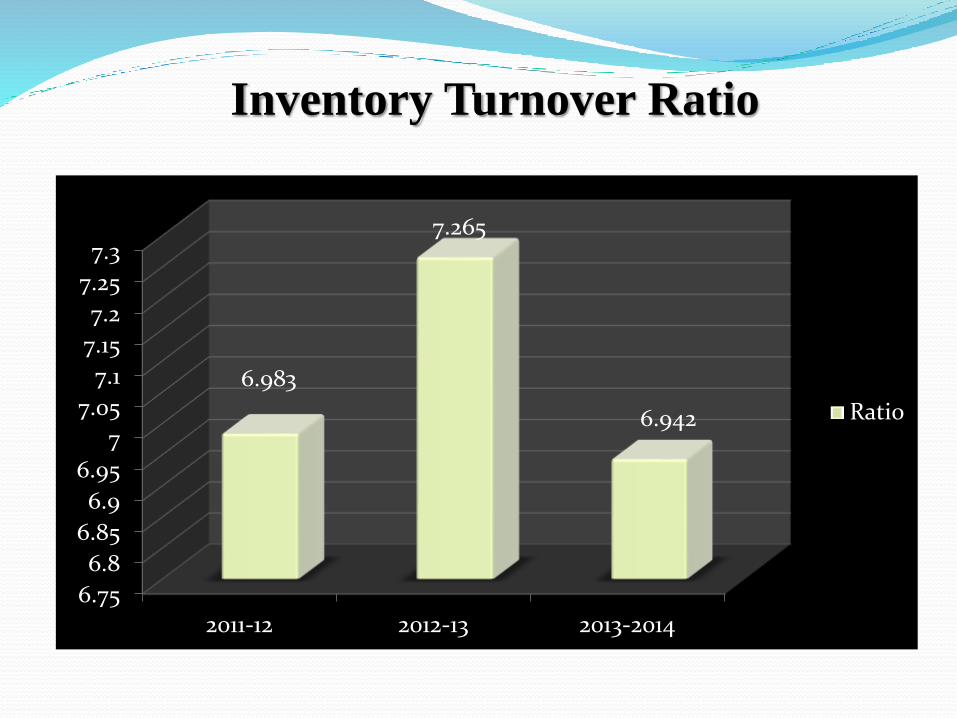

Inventory Turnover Ratio

6.75

6.8

6.85

6.9

6.95

7

7.05

7.1

7.15

7.2

7.25

7.3

2011-12 2012-13 2013-2014

Ratio6.942

6.983

7.265

Debt Equity Ratio

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

2011-12 2012-13 2013-2014

Ratio

0.450

0.078 0.071

Interest Coverage Ratio

0

1

2

3

4

5

6

7

8

2011-12 2012-13 2013-2014

Ratio

7.3946.717

6.049

Gross Profit Ratio

Ratio

0

10

20

30

40

2011-122012-13

2013-2014

Ratio

24.809 27.911

32.442

Net Profit Ratio

0

2

4

6

8

10

12

14

16

18

2011-12 2012-13 2013-2014

Ratio

12.605

13.823

16.464

Working CapitalParticular 2011-12` 2012-13 2013-14

Current Assets

Short term loan and advances 1829.25 2207.83 1299.2

Current investments 3204.17 3434.94 2343.24

Inventories 7522.99 6257.94 6007.81

Trade receivables 1904.3 1151.92 770.81

Cash and Bank Balances 3946.99 4192.36 3000.02

Other current assets 76.09 615.8 182.38

Total Assets (A) 18483.79 17860.79 13603.46

Current Liabilities

Short-term borrowings 65.62 70.94 43.69

Trade payables 7921.43 8524.01 10,930.61

Other current liabilities 9716.57 10616.79 10,888.89

Short-term provisions 2172.38 1544.26 1,902.81

Total Current Liabilities (B) 19876 20756 23766

Working Capital (A-B) -1392.09 -2894.95 -10162.18

COMMON SIZE STATEMENT

CAPM APPROACH CAPM measures the required rate of return.

CAPM is the most widely used risk return model because it is simple and

intuitively appealing and its basic message that diversifiable risk does not matter

is accepted by nearly everyone.

In the CAPM model, Beta defined as the risk of the investment in which its

compare market risk with the particular stock how much varies with respect to

market.

Expected return can be measure by the average of the variation in the market.

The CAPM formula is: Required return = Rf+ beta (E(Rm)-Rf)

Where:

rrf = the rate of return for a risk-free security

rm = the broad market's expected rate of return

Ba = beta of the asset

Stock data as per slope method average of 3 years

7.5352833

Expected Return Taken as the average of last 3 year

0.0396338

Required return =Rf+ beta(E(Rm)-Rf)

7.8984

DIVIDEND POLICY

Walter Model 2011-2012 2012-2013 2013-2014Dividend per share 12 8 8

Earning per share 67.84 50.28 66.02Rate of return on investment 10.48 12.81 12.72

cost of equity 13.82 13.82 13.82

valuation 3.93231982 3.414621734 4.442974694

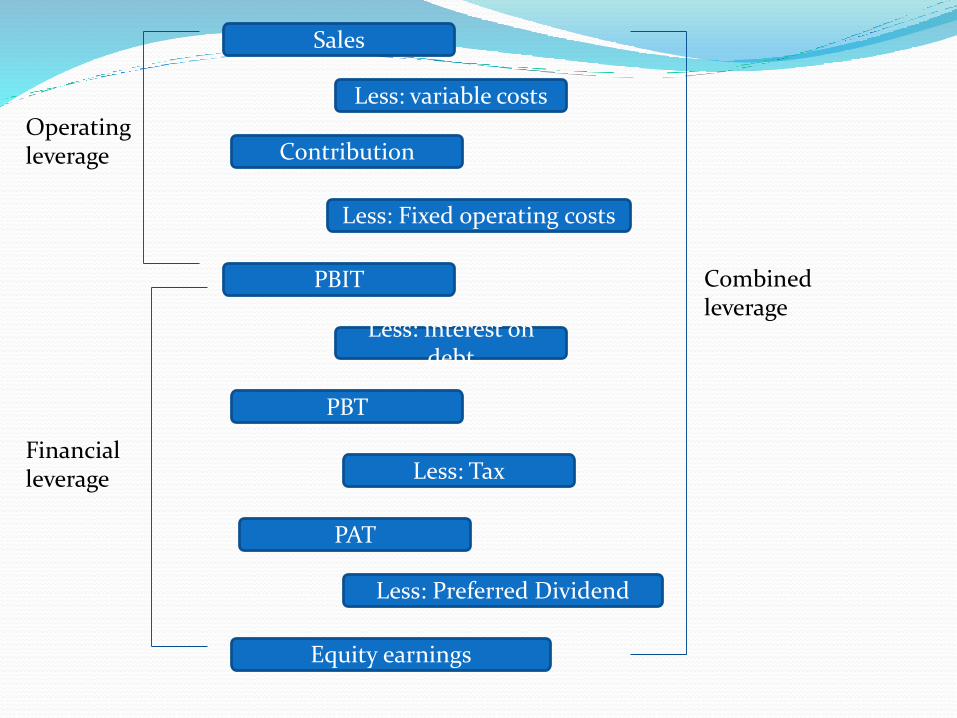

Sales

Less: variable costs

Contribution

Less: Fixed operating costs

PBIT

Less: interest on debt

PBT

Less: Tax

PAT

Less: Preferred Dividend

Equity earnings

Operating leverage

Financial leverage

Combined leverage

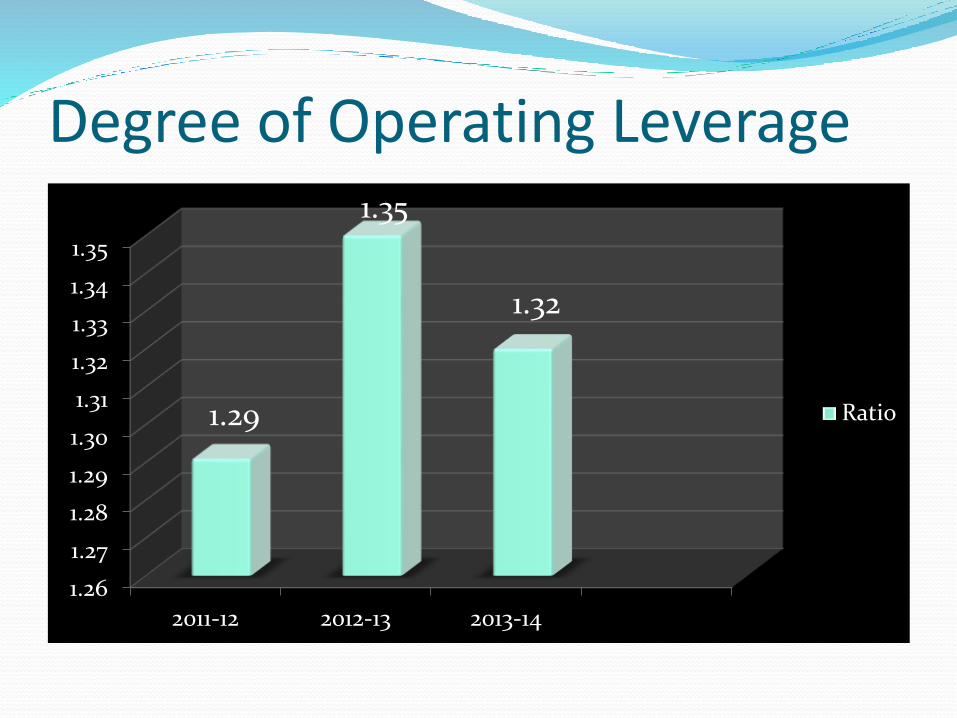

Degree of Operating Leverage

1.26

1.27

1.28

1.29

1.30

1.31

1.32

1.33

1.34

1.35

2011-12 2012-13 2013-14

Ratio1.29

1.35

1.32

Degree of Financial Leverage

0

0.2

0.4

0.6

0.8

1

1.2

2011-12 2012-13 2013-14

Ratio

1.05 1.08

0.76

Degree of Combine Leverage

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2011-12 2012-13 2013-14

Ratio

1.361.45

1.01

Conclusion

As we all know that Tata steel is an ethical company that not only focus on gaining profit but also provide constant dividend to their shareholders and satisfy their employee. In last three years company’s assets are increased that shows the company is healthy but in front of that Current liability of the company is also increased in last 3 years which is not good for any big organization. Tata steel has also tried to increased in sales in 2014 but as a result expense of production or interest on debt also increased so that not much increase in net profit of the company.