107

National Bank of Poland Payment Systems Department Analysis of the functioning of the interchange fee in cashless transactions on the Polish market Warsaw, January 2012

National Bank of Poland

Payment Systems Department

Analysis of the functioning

of the interchange fee in cashless transactions

on the Polish market

Warsaw, January 2012

2

TABLE OF CONTENTS

Introduction ......................................................................................................................... 4

Chapter 1. Description of the payment card market ......................................................... 6

1.1. Types of payment cards .......................................................................................... 6

1.2. Payment card systems ............................................................................................ 7

1.2.1. Types of systems and business models ............................................................... 7

1.2.2. Examples of schemes .........................................................................................10

1.3. Importance of the payment card market for its participants and the development

of cashless transactions .........................................................................................11

Chapter 2. The development of the payment card market in Poland compared

to other countries ............................................................................................17

2.1. Selected indicators of the development of the Polish payment card market ...........17

2.2. Selected indicators of the development of the payment card market - Poland

against other EU countries .....................................................................................22

Chapter 3. Factors determining the development of the payment card market

in Poland ...........................................................................................................26

3.1. SEPA .....................................................................................................................26

3.2. Payment services directive .....................................................................................29

3.3. Act on Payment Services .......................................................................................30

3.4. Payment card organisations in Poland ...................................................................31

3.4.1. “Visa cards accepted everywhere” programme ...................................................31

3.4.2. „Innovation for Poland” programme.....................................................................32

3.5. Interchange fee policy of the European Commission and European Central Bank .32

3.5.1. European Commission's Action ..........................................................................32

3.5.2. Activities of the European Central Bank ..............................................................38

Chapter 4. Description of the interchange fee ..................................................................42

4.1. Definition of the interchange fee .............................................................................42

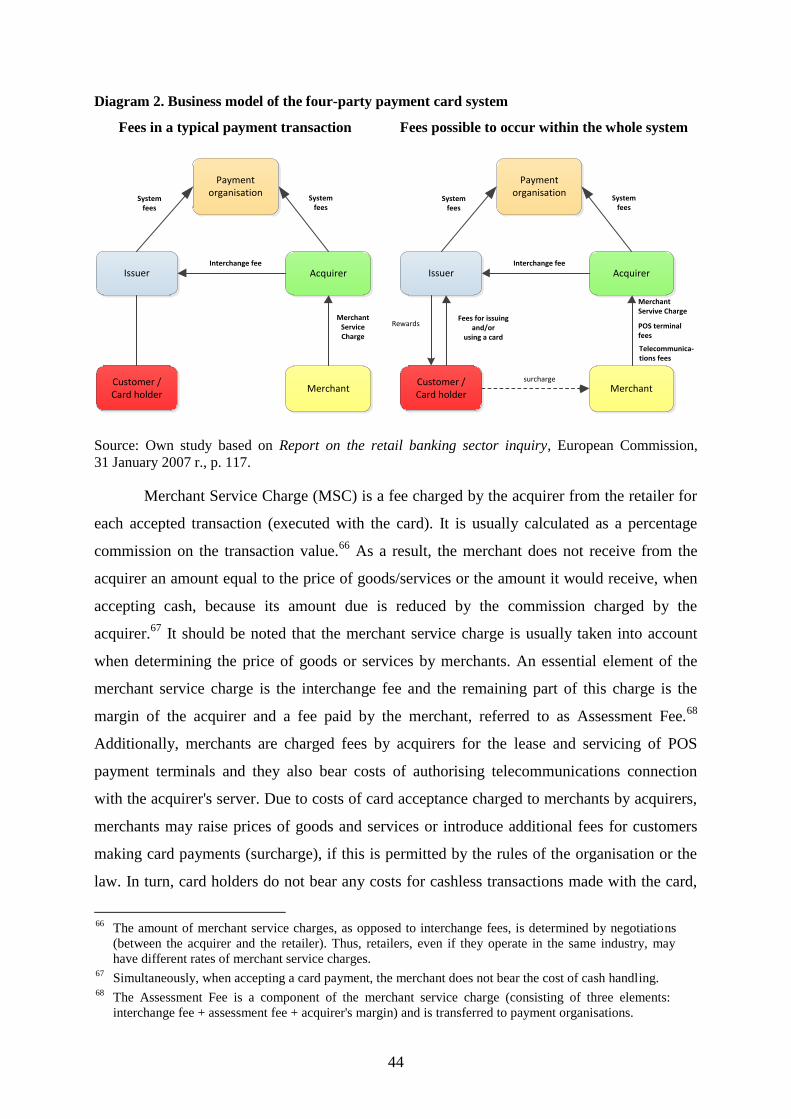

4.2. Outline of fees on the payment card market ...........................................................43

4.3. Justification for the introduction of interchange fee from the point of view

of payment organisations .......................................................................................45

4.4. Economic concepts concerning the payment card market ......................................46

Chapter 5. Level of interchange fees and other fees charged in the Polish market .....49

5.1. Rates of interchange fees in the Visa system .........................................................49

5.1.1. Cross-border fees ...............................................................................................49

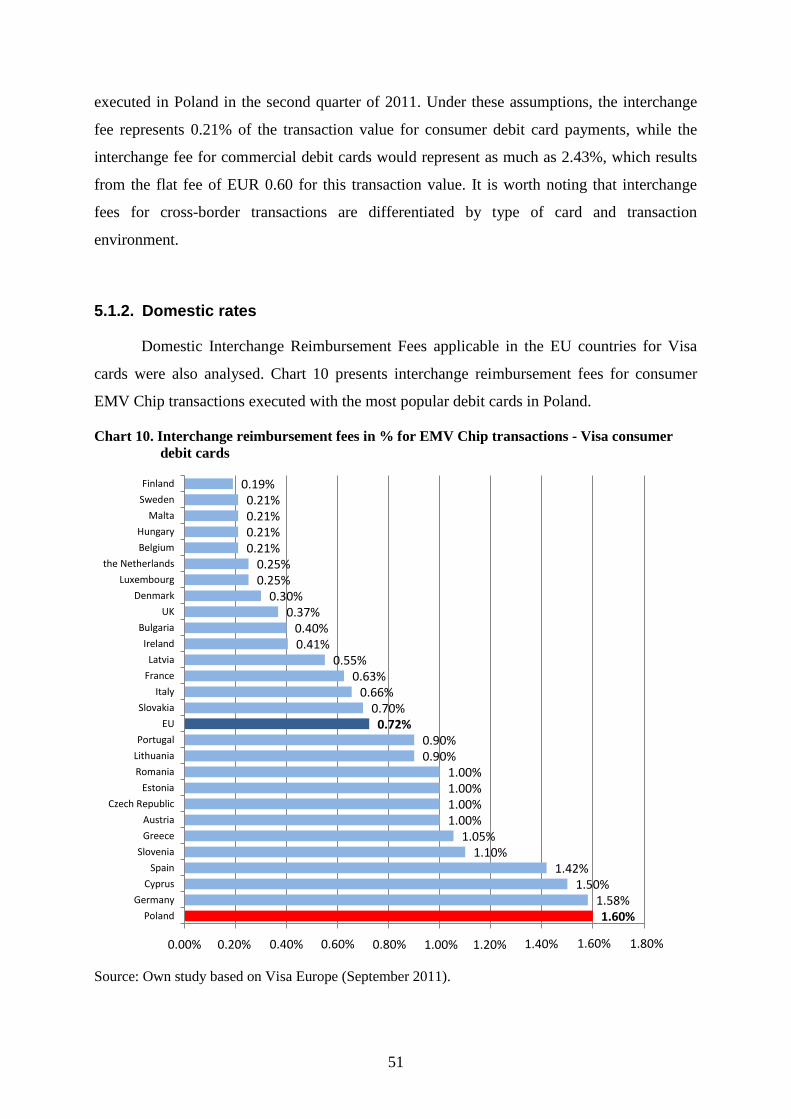

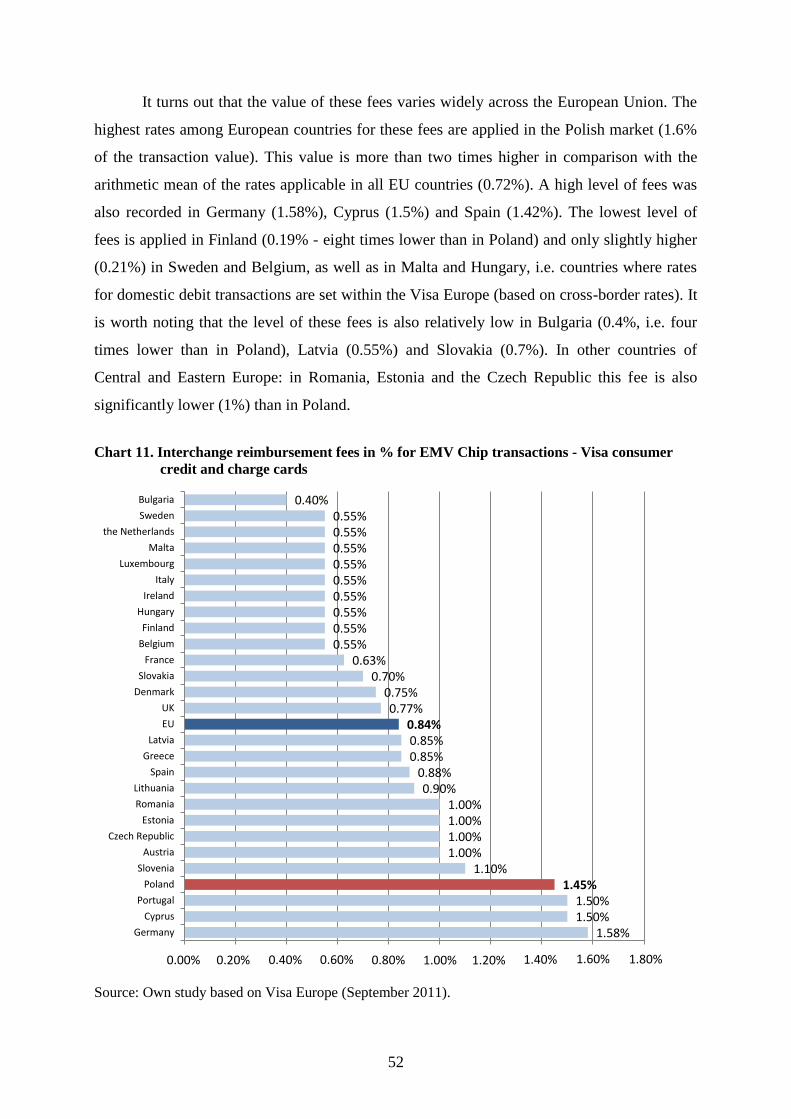

5.1.2. Domestic rates ....................................................................................................51

5.2. Rates of interchange fees in MasterCard system ...................................................54

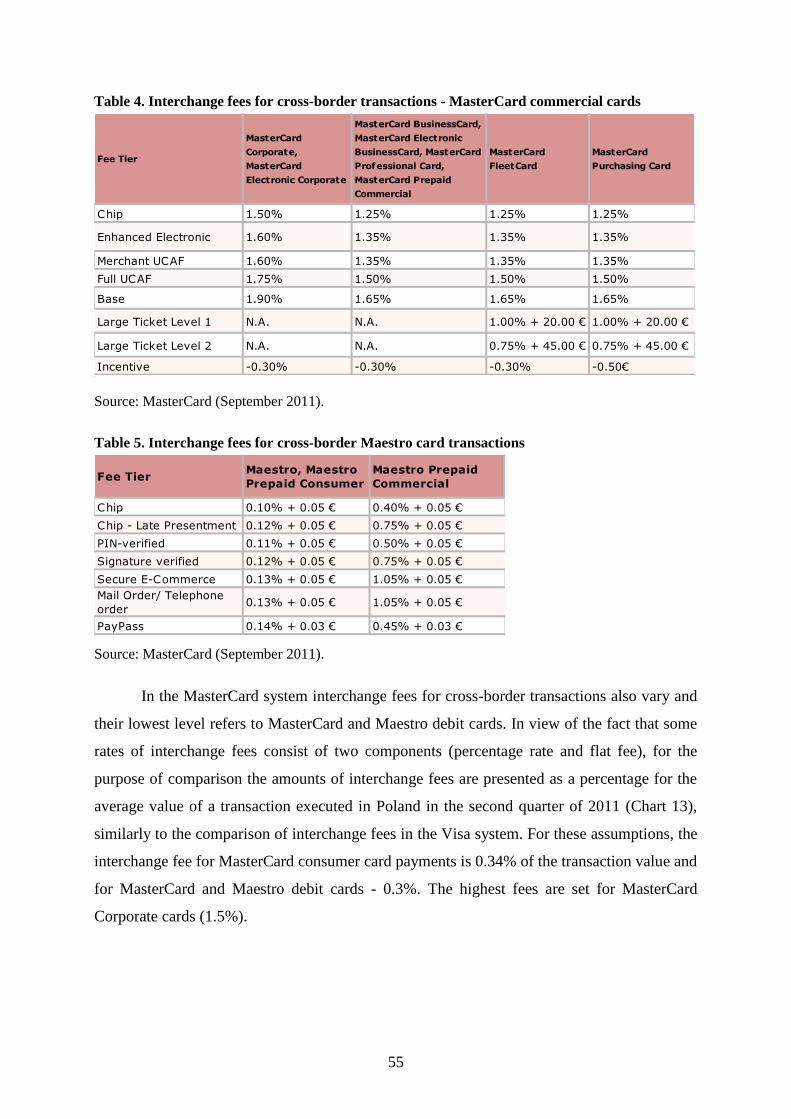

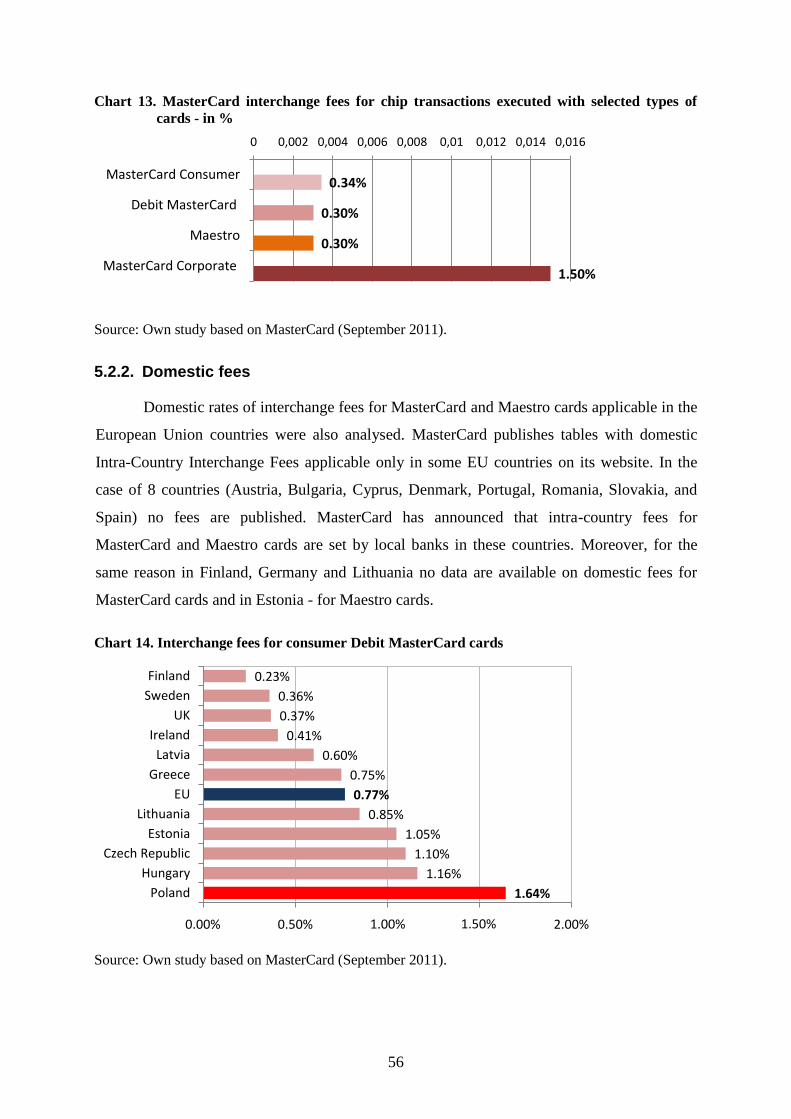

5.2.1. Cross-border fees ...............................................................................................54

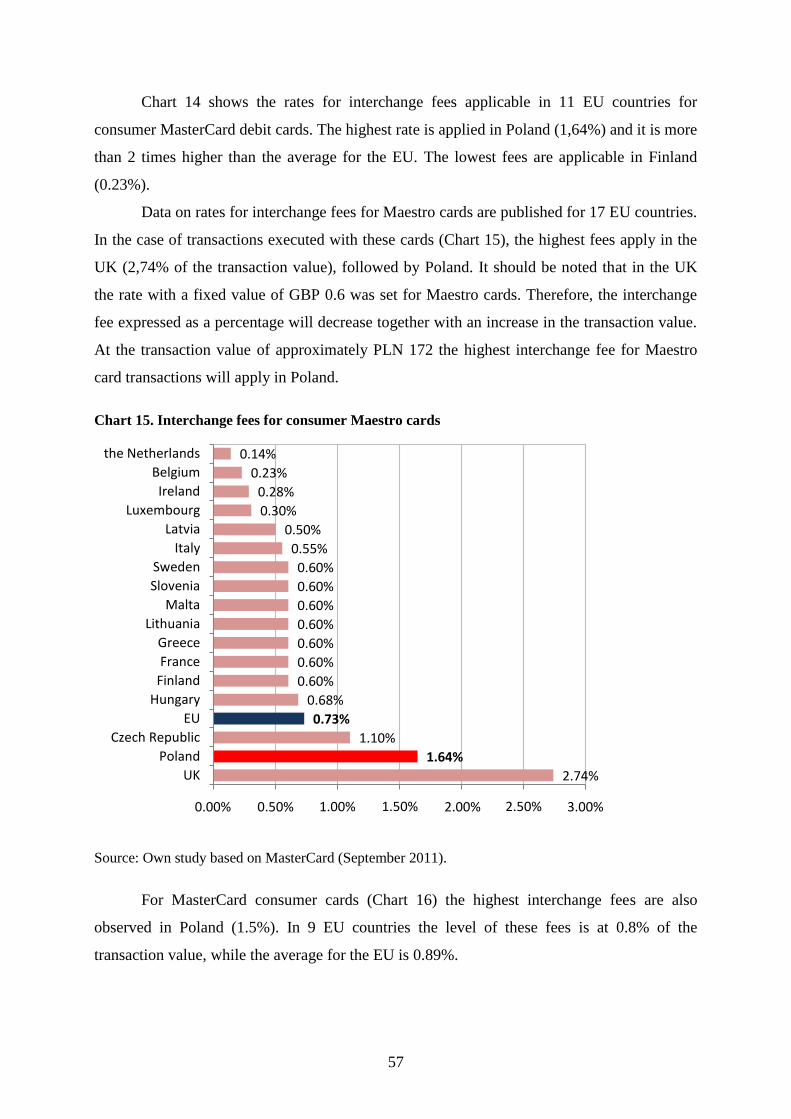

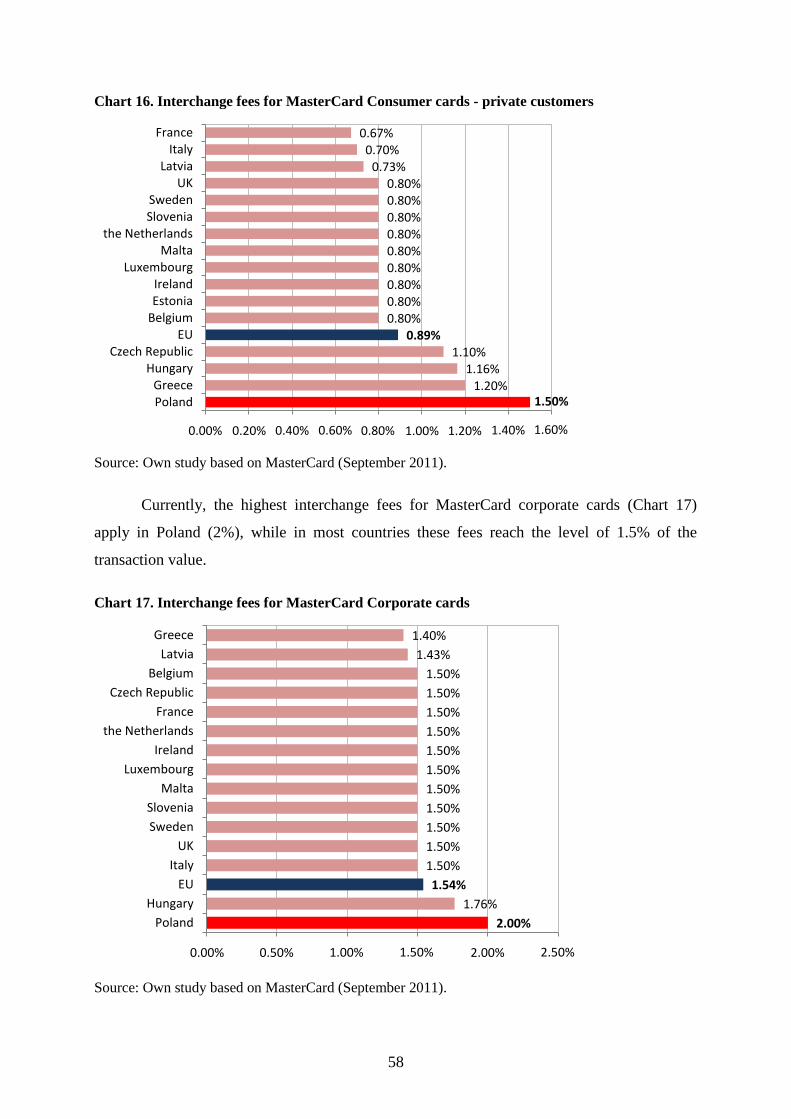

5.2.2. Domestic fees .....................................................................................................56

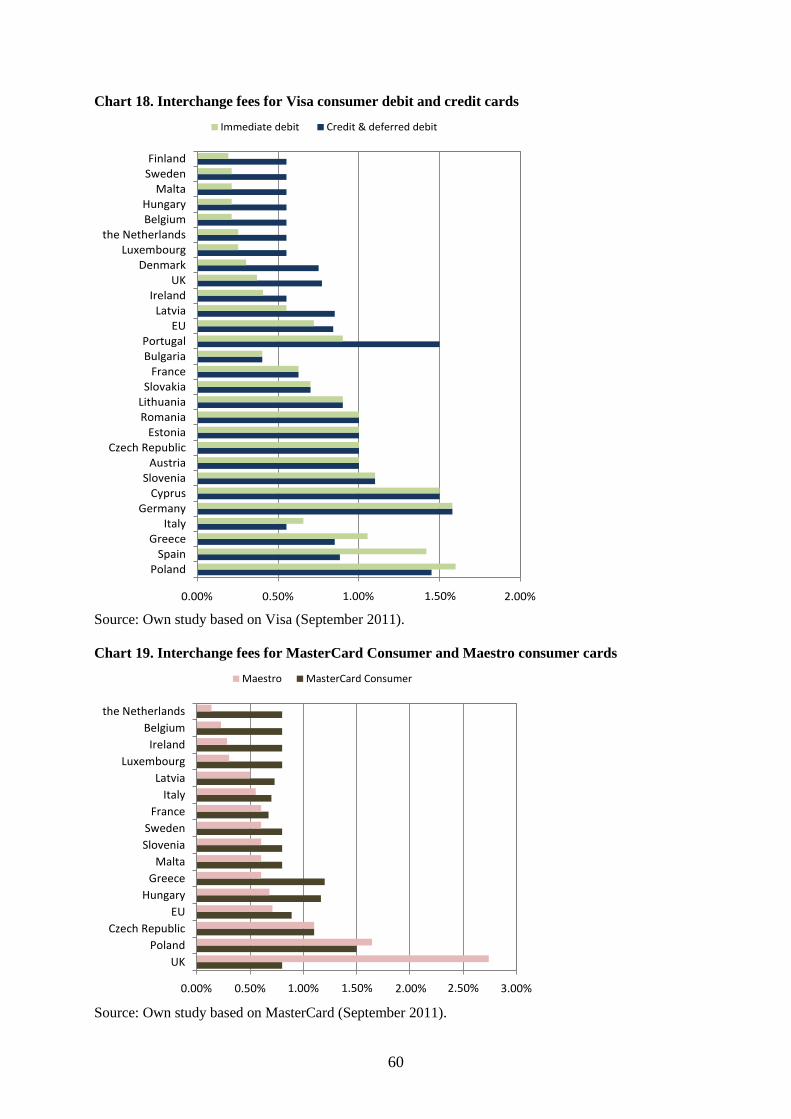

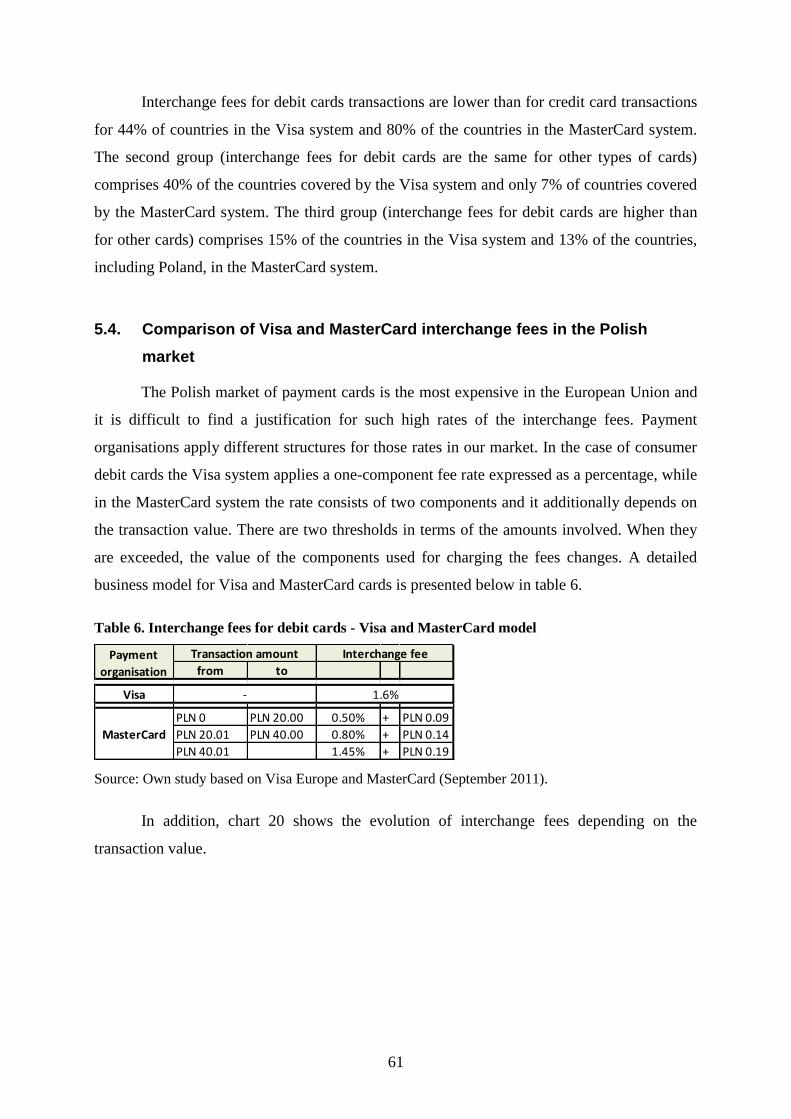

5.3. Comparison of interchange fees of Visa and MasterCard in the European market .59

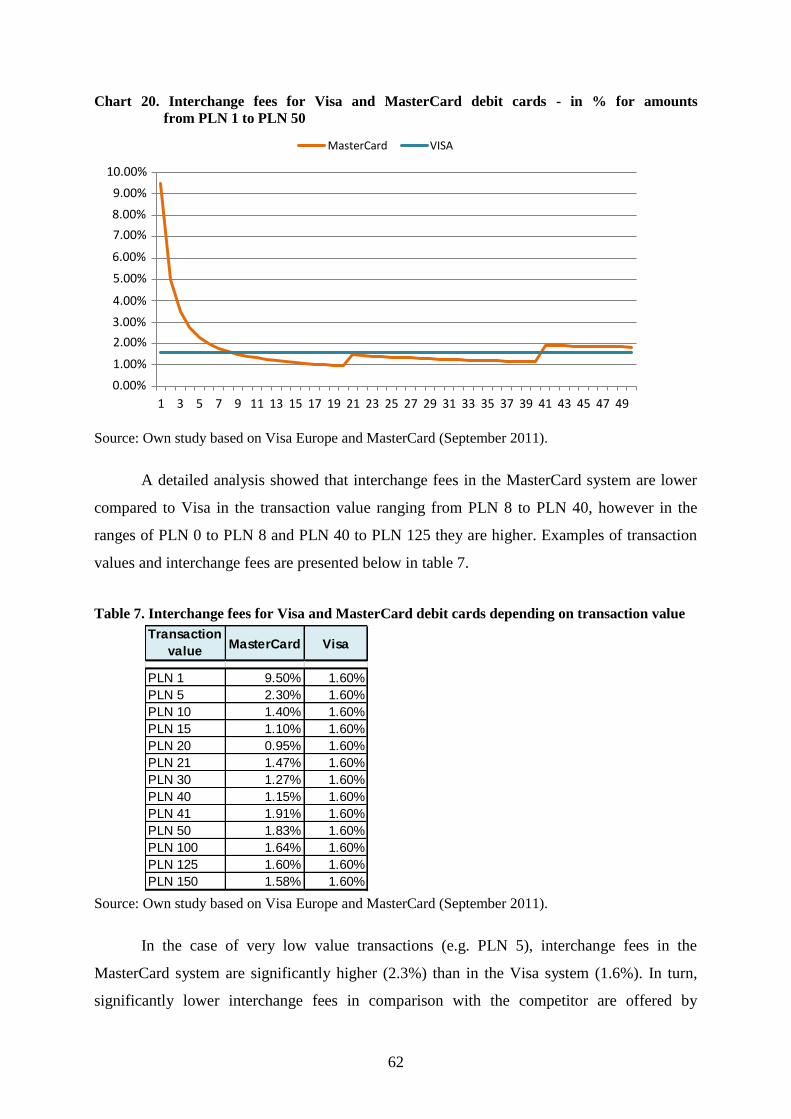

5.4. Comparison of Visa and MasterCard interchange fees in the Polish market ...........61

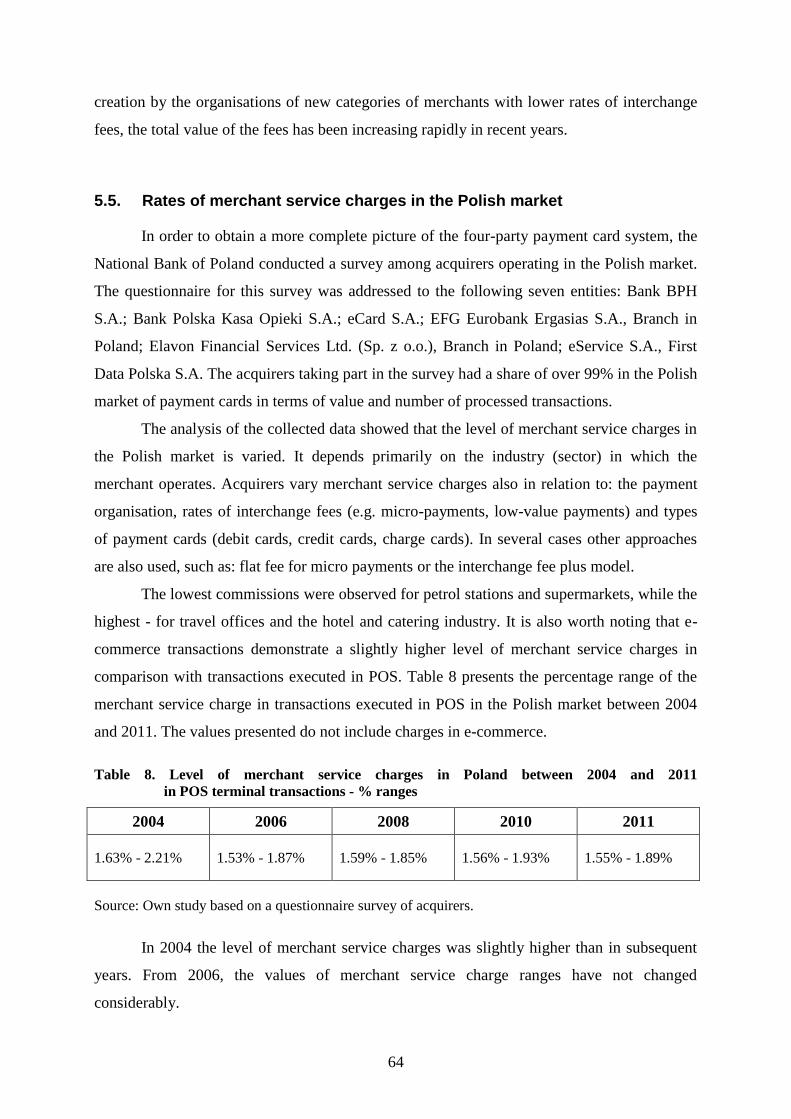

5.5. Rates of merchant service charges in the Polish market ........................................64

5.6. Other fees determining the level of the merchant service charge ...........................65

3

Chapter 6. Overview of interchange fee in Poland ...........................................................67

6.1. Decision of the Office of Competition and Consumer Protection.............................67

6.2. NBP Report on interchange fee in 2007 .................................................................69

6.3. Programme for the Development of Cashless Transactions in Poland

in 2011-2013 ..........................................................................................................71

6.4. Parliamentary work related to the Act on Payment Services ...................................74

6.5. Activities of the Payment System Council at the NBP and establishment

of the Interchange Fee Task Force .........................................................................80

Chapter 7. Examples of countries which introduced changes to the level or manner

of setting the interchange fee .........................................................................82

7.1. Hungary .................................................................................................................82

7.2. Spain ......................................................................................................................84

7.3. Australia .................................................................................................................86

7.4. United States ..........................................................................................................89

Chapter 8. Scenarios for the development of the payment card market in Poland

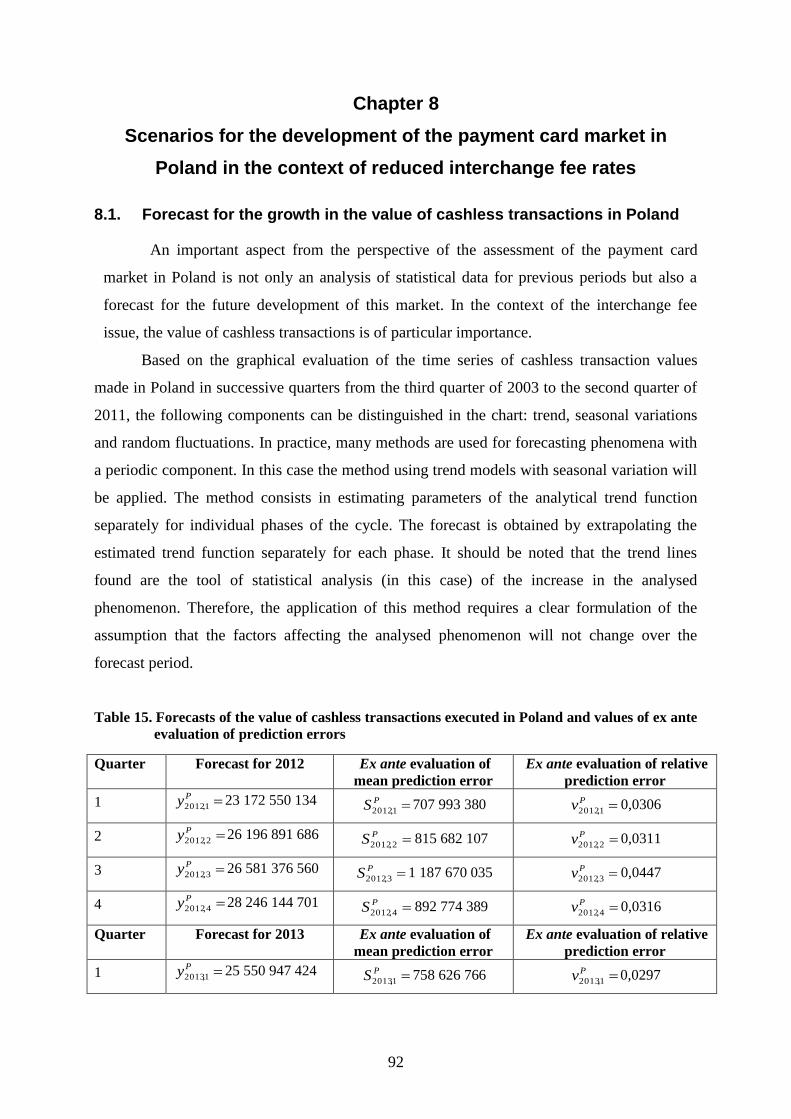

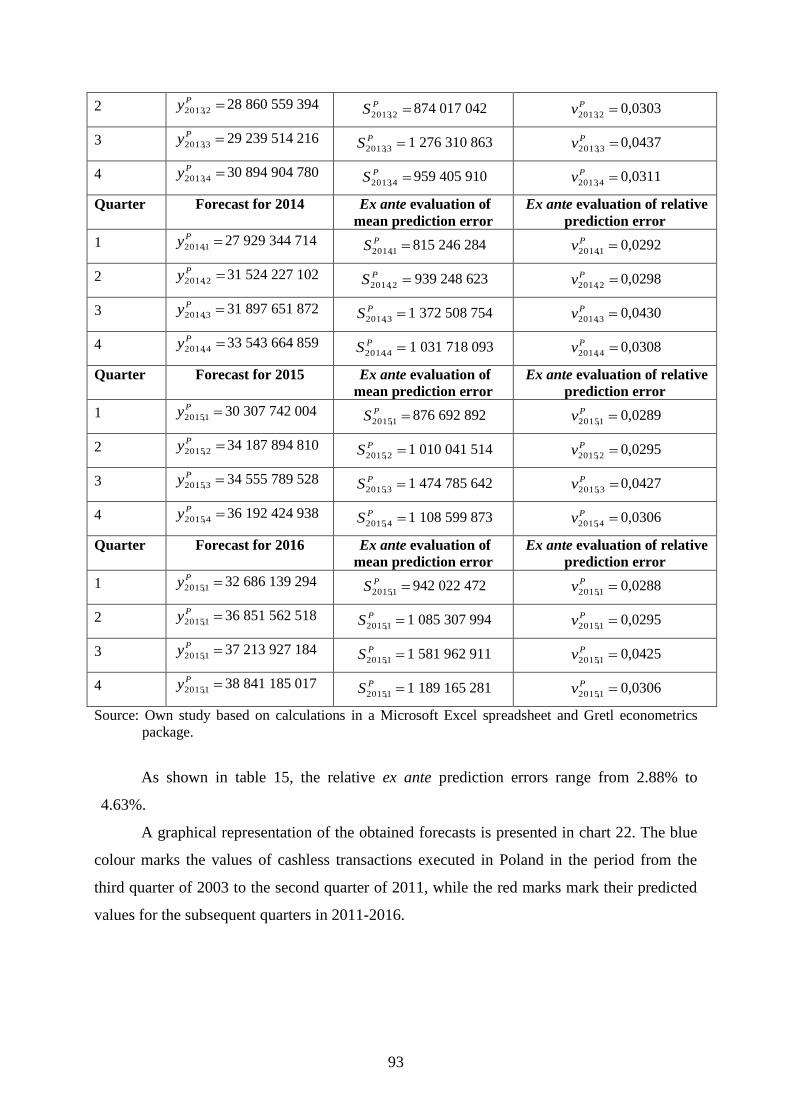

in the context of reduced interchange fee rates .............................................92

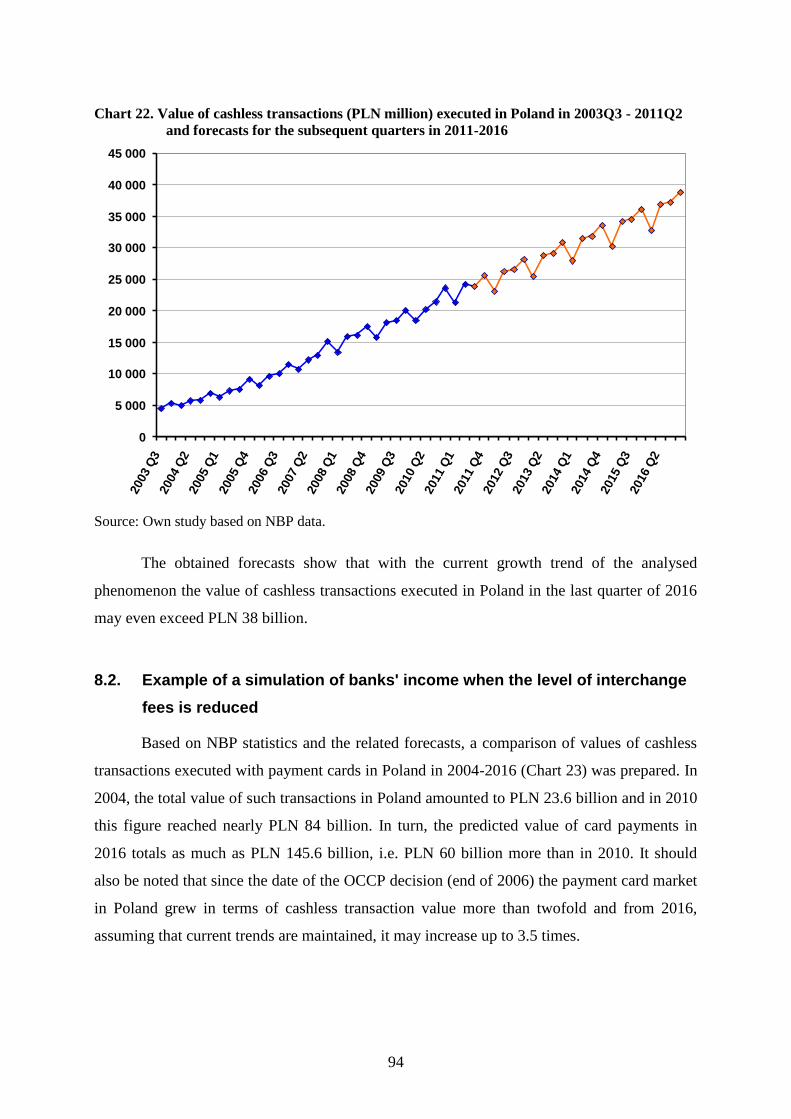

8.1. Forecast for the growth in the value of cashless transactions in Poland .................92

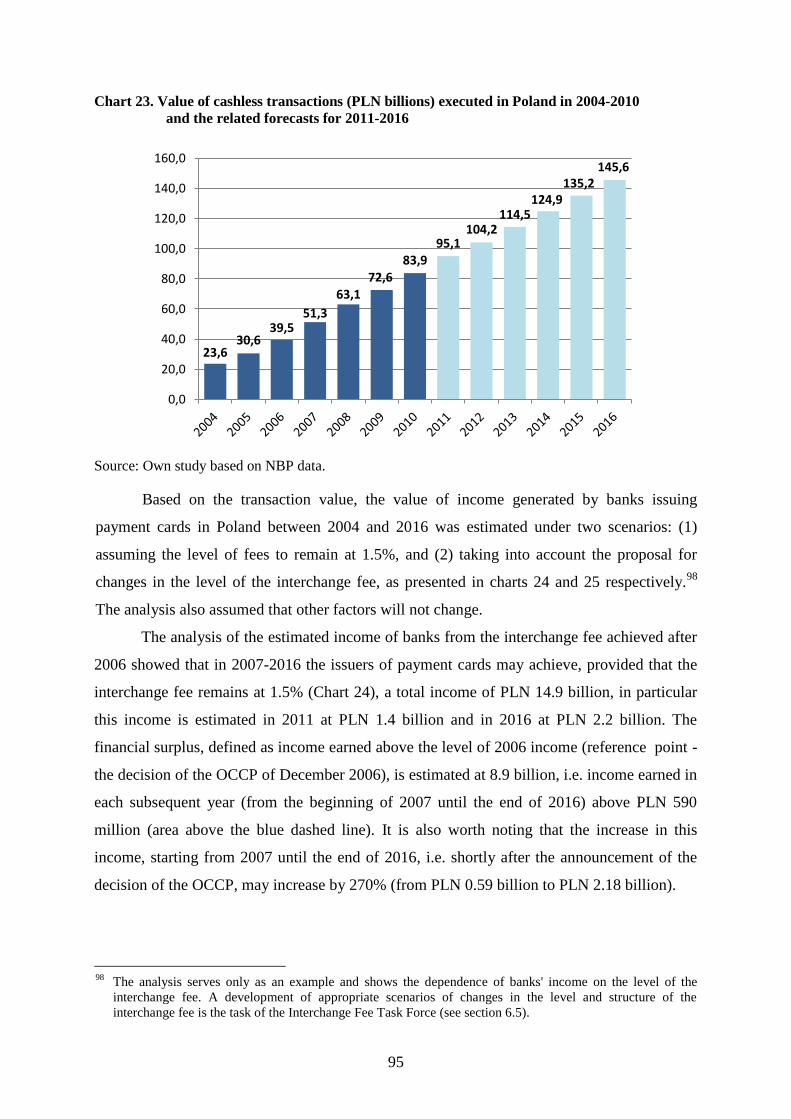

8.2. Example of a simulation of banks' income when the level of interchange fees

is reduced ..............................................................................................................94

8.3. Interchange fee reduction - scenario analysis.........................................................97

Conclusions ...................................................................................................................... 101

4

Introduction

Payment card market in Poland has been growing rapidly for more than a dozen years.

Consumers use their cards more and more often to pay for goods and services, including low-

value payments, which until now were dominated by cash. The number of retailers that accept

credit cards on the domestic market is also rising steadily. The development of this market is

determined by many factors. One of them is the cost of accepting payment cards. This issue

was clearly highlighted for the first time on the Polish market in the proceedings carried out

by the Office of Competition and Consumer Protection (OCCP) at the request of the Polish

Trade and Distribution Organisation with regard to the application of competition restricting

practices, consisting in the conclusion of pricing agreements and setting the interchange fee,

an essential component of the merchant's fee, jointly by banks associated in Visa and

MasterCard card issuers association. The decision made by the President of the OCCP on 29

December 2006 recognised the practice consisting in banks' participation in the agreement

restricting competition in the market for acquiring services through joint determination of the

interchange rates as a practice restricting competition and prohibited its use. This dispute,

following an appeal by banks and organisations, has not been resolved until today, however

the problem of high merchant fees remains. Dissatisfaction among merchants because of the

fees increased when the requirement to publish interchange rates had been imposed on

payment organisations. It was also reflected during parliamentary debates on the act on

payment services. Large retailer associations demanded that changes be made to the act which

- in the opinion of the NBP - could restrict the development of cashless transactions in Poland.

The Payment Systems Department, fulfilling such basic functions of the National

Bank of Poland as the organisation of monetary clearing (pursuant to Article 3(2)(1) of the

Act on the National Bank of Poland of 29 August 1997 - Journal of Laws of 2005 No. 1, item

2, as amended), oversight of payment systems in Poland (in accordance with the Act of 24

August 2001 on Settlement Finality in Payment and Securities Settlement Systems and the

Rules of Oversight of these Systems - Journal of Laws No. 123 item, 1351, as amended) and

oversight of authorisation and clearing systems operated by acquirers other than banks (in

accordance with the Act on Electronic Payment Instruments of 12 September 2002 - Journal

of Laws No. 169, item 1385, as amended), prepared a report presenting an analysis of the

interchange fee functioning for cashless transactions in the market of payment cards in Poland

against other European Union countries.

5

The results of two surveys conducted among two groups of entities operating on the

Polish market constitute an important element of the report. The first survey was addressed to

payment organisations, while the second one was addressed to seven largest acquirers with a

99% share in the payment card market in terms of the number and value of transactions. The

survey (project, survey questionnaire, data collection and analysis) was prepared by the NBP.

Some data obtained in the survey is protected by business secret clauses. Therefore, despite

the fact that extensive statistical data were collected, the report contains only the analysis of

selected issues.

The main purpose of the report was to diagnose the payment card market in Poland in

the context of issues related to interchange fee, with particular emphasis on the role and place

of this fee in the Polish system of payment cards, rates and fee amount in comparison with

other countries as well as identification of possible courses of action aimed at accelerating the

development of the payment card market in Poland. It is not the purpose of the report to

propose specific solutions to the interchange fee problem in Poland because it is the task of a

separate Interchange Fee Task Force established in October 2011 at the Payment System

Council, a consultative and advisory body to the NBP Management Board. However, the

Payment Systems Department of NBP hopes that this report will contribute to the introduction

of changes in the payment card market which will have a beneficial effect on its further

development.

6

Chapter 1

Description of the payment card market

Payment cards enjoy a great and constantly growing popularity. During several

decades of their functioning, they underwent significant transformations, from cards issued in

the form of metal plates with customer data (in the early twentieth century) to the currently

offered multifunction smart cards or virtual cards (with no material form, in the form of a

string of digits used in the banks' ICT systems). This chapter presents the classification of

cards, business models and main systems operating in the card market, as well as the

significance of the card market for its participants and for the development of cashless

transactions.

1.1. Types of payment cards

Currently there are many types of payment cards in the market, primarily owing to the

dynamic development of modern technologies and the financial services market. These

instruments can be classified in accordance with several criteria.

From the perspective of the method of transaction settlement, cards can be divided

into debit, charge and credit cards. A debit card is a payment instrument that allows to execute

transactions only up to the amount of funds available in the account. A credit card allows to

execute transactions resulting in credit which is repaid in accordance with the terms agreed

with the bank. A charge card offers a deferred payment deadline and the resulting liability is

to be repaid in full at the end of settlement period, usually once a month. In addition, a

prepaid card can be distinguished which can be used only if the account to which the card is

assigned is previously supplied with funds.

Another criterion for the card breakdown is their function. In this context ATM cards,

payment-only cards and payment cards with an ATM cash withdrawal function may be

distinguished. Currently, payment cards with cash withdrawal function are the world's most

widely used cards, while cards equipped with only one of these functions (ATM cards,

payment cards without cash withdrawal function) play a marginal role.

Taking into account the technology of data recording, payment cards can be grouped

into cards with a magnetic stripe, smart cards, hybrid cards (equipped with both magnetic

stripe and chip) and virtual cards. The migration of cards to EMV smart cards standard which

has become common in recent years, particularly in Europe, results from adjustments of the

7

banking sector and payment services to the requirements of the SEPA (Single Euro Payments

Area) project. The principle of liability shift was made an element supporting the above

mentioned process of technological changes.1

When speaking of the method of card's contact with the card reader, smart cards,

contactless (proximity) cards and cards equipped with both technologies may be

distinguished. It should be noted that payment instruments with the contactless feature only

usually take an alternative form of payment cards. These can be items or gadgets equipped

with a chip and an antenna such as key rings, watches or phones with a small-sized card

placed under the telephone cover. Due to their unusual shapes and sizes alternative forms of

payment cards: (1) can now be used only for making payments in points of sale equipped with

proximity card readers, which may pose a certain limitation for users due to the moderate

albeit rapidly and systematically growing network of terminals with the proximity function;

(2) may not be used for cash withdrawals in ATMs. However, there are no technical obstacles

to using the gadgets for the cash back service. Payment organisations are currently testing this

solution.

Another criterion for the breakdown of cards is the card functioning mode at the

time of making a payment by the customer. These may be cards that function on-line and off-

line mode. The first solution has been functioning globally for many years on a wide scale,

while the second solution is much less popular. It can be used in contactless, low-value

transactions that do not require a confirmation of the transaction with PIN.2

Currently issued payment cards can be equipped with many functions. For instance,

the following payment instruments that are available in banks' offer may be listed: chip

contactless credit card, prepaid card with a magnetic stripe or, less commonly, a combination

of a debit and credit function in one card. A wide variety of payment cards reflects their rapid

and continuous development.

1.2. Payment card systems

1.2.1. Types of systems and business models

Payment cards are issued under payment card schemes. These schemes form the

1 SEPA Cards Framework, European Payment Council, 16 December 2009, p. 16-17; More in: M. Polasik, K.

Maciejewski, Innowacyjne usługi płatnicze w Polsce i na świecie, Materiały i Studia, No. 241, National Bank of

Poland, Warsaw 2009, p. 31. 2 In Poland, such transactions are below PLN 50.

3 W. Chmielarz, Systemy elektronicznej bankowości, Difin, Warsaw 2005, p. 104.

4 T. Kokkola, The payment system, European Central Bank, 2010, p. 56.

2 In Poland, such transactions are below PLN 50.

8

payment card market and constitute an essential pillar of the market for payment services in

developed economies. Due to its specific nature involving the use and continuous

development of a complex ICT infrastructure, the payment card market is one of the most

innovative areas of the payment services market.3

The participants of the payment card market usually include:

• Consumers – card holders making card payments for goods or services in certain

retail trade and service outlets,

• Merchants - retailers receiving payment for goods or services effected with the use

of payment cards,

• Acquirers - clearing centres (banks or non-bank entities) which have signed

agreements with merchants on accepting payments with the use of payment cards.

An acquirer also settles transactions between card issuers and merchants.

• Issuers of payment cards - entities (mostly banks) issuing payment cards to card

holders,

• Payment card organisations - embrace card issuers (e.g. as members or customers)

who issue cards with the logo of the organisation, provide the technical

infrastructure to enable immediate authorisation of transactions, set the rules for

accepting and clearing cards, elaborate and develop standards for payment cards as

well as services and products related to payment cards, implement and develop

payment card technologies, advertise and promote the brand of their products

among card holders and merchants.

There are two main business models for payment cards: three-party schemes (closed)

and four-party schemes (open).4 They are presented in figure 1 below. In addition, there are

also two-party schemes which, however, play a marginal role in the market for payment

services.

3 W. Chmielarz, Systemy elektronicznej bankowości, Difin, Warsaw 2005, p. 104.

4 T. Kokkola, The payment system, European Central Bank, 2010, p. 56.

9

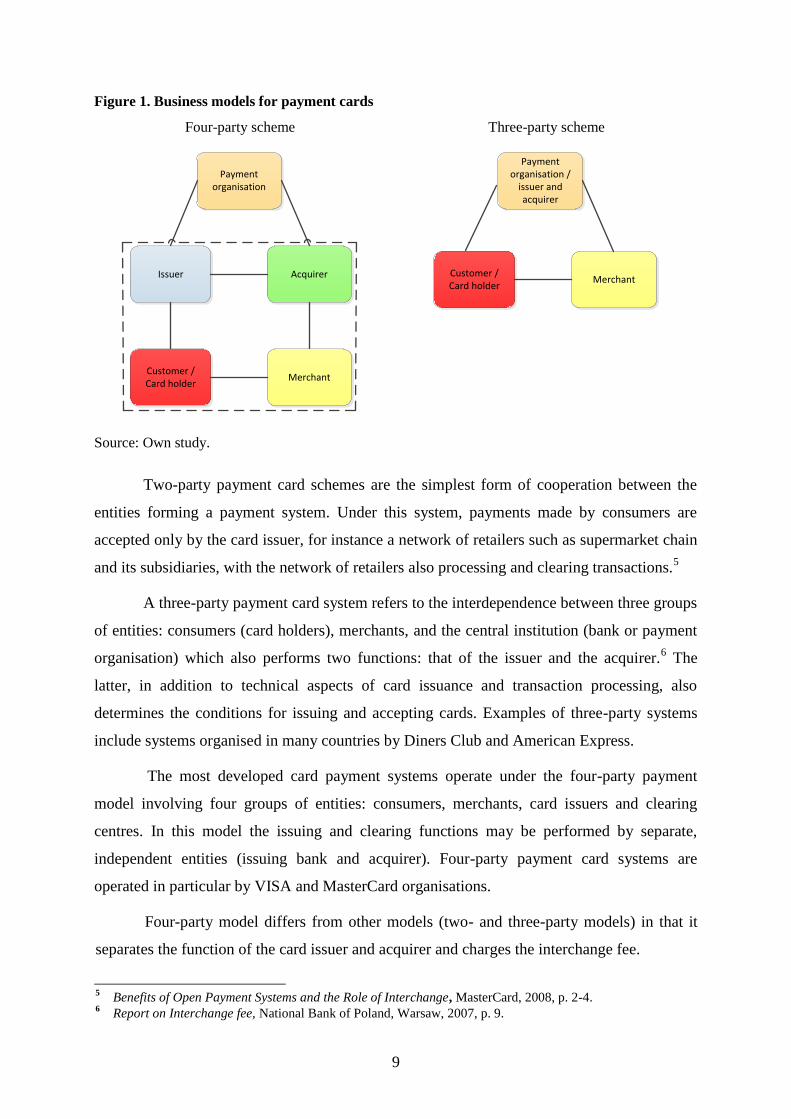

Figure 1. Business models for payment cards

Four-party scheme Three-party scheme

MerchantCustomer /Card holder

AcquirerIssuer

Payment organisation

MerchantCustomer /Card holder

Payment organisation /

issuer and acquirer

Source: Own study.

Two-party payment card schemes are the simplest form of cooperation between the

entities forming a payment system. Under this system, payments made by consumers are

accepted only by the card issuer, for instance a network of retailers such as supermarket chain

and its subsidiaries, with the network of retailers also processing and clearing transactions.5

A three-party payment card system refers to the interdependence between three groups

of entities: consumers (card holders), merchants, and the central institution (bank or payment

organisation) which also performs two functions: that of the issuer and the acquirer.6 The

latter, in addition to technical aspects of card issuance and transaction processing, also

determines the conditions for issuing and accepting cards. Examples of three-party systems

include systems organised in many countries by Diners Club and American Express.

The most developed card payment systems operate under the four-party payment

model involving four groups of entities: consumers, merchants, card issuers and clearing

centres. In this model the issuing and clearing functions may be performed by separate,

independent entities (issuing bank and acquirer). Four-party payment card systems are

operated in particular by VISA and MasterCard organisations.

Four-party model differs from other models (two- and three-party models) in that it

separates the function of the card issuer and acquirer and charges the interchange fee.

5 Benefits of Open Payment Systems and the Role of Interchange, MasterCard, 2008, p. 2-4.

6 Report on Interchange fee, National Bank of Poland, Warsaw, 2007, p. 9.

10

With regard to the range of operations, the following three types of payment card

systems can be distinguished: local, national and international. Local systems operate as part

of one or more banks in a limited geographical area, such as a small chain of stores located in

one or several cities. A national payment card system represents a more developed

infrastructure. It includes processing of transactions in a particular country where payment

cards accepted by retail outlets may be those issued under domestic and international payment

systems. On the other hand, international payment card systems process transactions around

the world, regardless of the country in which cards were issued. Due to the fact that the

development of the infrastructure and card acceptance network on a global scale is a costly

and lengthy process, there are only several international card schemes.

1.2.2. Examples of schemes

There are many payment card schemes around the world. The best known

international systems include: VISA, MasterCard, Amex (American Express), Diners Club,

JCB (Japan Credit Bureau) and China UnionPay. All the above mentioned systems, except for

JCB and China UnionPay, have their origins in the U.S. market. The largest payment card

organisations in the world are VISA7 and MasterCard.

8 VISA operates as an association of

card issuers. Within this organisation there are decision-making structures at the national

level in Poland, i.e. Visa Forum Polska. The Forum comprises representatives of issuing

banks and acquirers, with the voting right available only to card issuers and the number of

votes available depends on the number of cards issued or the value of card transactions

handled by a given system. MasterCard operates as a joint-stock company listed on the stock

exchange and it groups together issuers who are both its shareholders and customers. All

decisions concerning the Polish market are made solely by MasterCard.9

The organisations that play a lesser role in the global payment card market are Diners

Club, Amex and JCB. They operate in the form of clubs and issue mostly T&E (Travel and

7 More on the history of the Visa organisation in: Visa Inc. Corporate Overview,

http://corporate.visa.com/_media/visa-corporate-overview.pdf (December 2011);

History of Visa, http://corporate.visa.com/about-visa/our-business/history-of-visa.shtml (December 2011). 8 More on the history of the MasterCard organisation in: Corporate Overview,

http://www.mastercard.com/us/company/en/docs/CorporateOverview_FINAL.pdf (December 2011); The

MasterCard Story, http://www.mastercard.com/us/company/en/ourcompany/the_mastercard_story.html

(December 2011). 9 Until 2008 the Forum of MasterCard Member Banks operated which constituted a decision-making

structure for Poland, however it was dissolved when MasterCard became a listed company.

11

Entertainment) cards. The average value of transactions executed with cards of these

organisations is clearly higher than in the case of Visa and MasterCard cards. Currently,

Diners Club Polska, member of Diners Club International, deals with Diners Club cards on

the Polish market. American Express is a publicly listed company. In Poland, Amex cards are

accepted at most retail and service outlets equipped with payment terminals. JCB organisation

has its roots in Japan where it has had a predominant position for many years. Cards of this

organisation are issued and accepted also on international markets. JCB cards are, as in the

case of Amex cards, widely accepted on the Polish market, however they are not issued in

Poland. By contrast, China UnionPay cards may be used in the Polish market in ATMs of

Citibank Handlowy.

There are many payment card schemes with a local reach. The most popular include:

Dankort (Denmark), Carte Bleue and Cartes Bancaires (France), BankAxept (Norway),

Geldkarte (Germany), Chipknip and PIN (the Netherlands).

1.3. Importance of the payment card market for its participants and the

development of cashless transactions

Payment cards offer many benefits to the participants of the payment services

market.10

They compete not only against cash but also against other payment instruments

such as credit transfers, direct debits and cheques.

Benefits for consumers (users of payment cards);11

- Payment card users have a continuous and extensive access to cash, both at home

and abroad. Using the card they can make purchases at retail and service outlets

equipped with POS terminals (regardless of the amount of cash possessed) and can

obtain cash at ATMs anywhere in the world where cards of a particular card issuing

organisation are accepted. An important advantage of payment cards is the possibility

of making purchases via the Internet (in Poland and abroad) which have become

increasingly popular for several years. The card user can make a purchase at a

10

More information on various benefits for each party of the payment card system can be found in: T. J.

Zywicki, The economics of Payment Card Interchange Fees and the Limits of Regulation, International Center for Law and Economics, ICLE Financial Regulatory Program White Paper Series, June 2010.

11 R. J. Keating, Credit Cards and Small Business: The Benefits, Opportunities and Policy Debate, The

Small Business & Entrepreneurship Council’s Small Business Policy Series, Analysis 34, March 2009, p. 9-10.

12

distance, without leaving home.

- Payment organisations and issuing banks have developed financially attractive terms

and conditions of using payment cards for individual customers. Card holders

generally do not pay any fees for executing cashless transactions.12

However, they

may have to pay fixed charges related to issuing or possessing a card. More and more

banks in the Polish market offer reward or loyalty schemes for card holders,

encouraging them to execute a large number of card transactions in retail and service

outlets. By participating in such initiatives customers may, in addition to being

exempted from charges for possessing the card, count on having a portion of

expenses on shopping made with the use of the card13

refunded or receiving

discounts at selected retailers (e.g. Payback).

- Payment cards offer higher security than cash. When the wallet with cash is stolen,

the cash may come into the thief’s possession without any obstacles, while access to

cash with the use of a payment card requires, apart from the possession of the card, the

knowledge of the PIN.

- The advantage of payment cards over cash and bank transfers in respect of the security

of the transaction is also reflected in the chargeback used in the international payment

card systems. Chargeback consists in refunding card payments to customers under the

claim procedure when no purchase of goods or services was made.14

- Making payments with the use of a payment card is easier. This means a higher level

of comfort for the user of this instrument. There is no need to search for and count

cash (banknotes, coins). On the customer's side, this process is reduced to handing the

card over to the retailer and entering the PIN on the payment terminal or signing the

terminal printout. In the case of a proximity card the process is even more convenient

and faster, since the user only places the card in front of the reader at a several

centimetres distance and the transaction is executed, without having to hand the card

12

There is indeed a phenomenon of a surcharge in the world, i.e. the merchant charges the customer for a

commission on a card transaction. However this solution is not widely used. More information on the impact

of the surcharge on consumer behaviour in the domestic market using the Netherlands as an example: W.

Bolt, N. Jonker, C. Van Renselaar, Incentives at the Counte: An empirical analysis of surcharging card

payments and payment behaviour in the Netherlands, DNB Working Paper No. 196, December 2008. 13

Even up to 5% of the transaction value, i.e. at the level exceeding the value of the interchange fee, more

information in: R. Grzyb, Na konto nie wróci więcej niż 2 proc., Dziennik Gazeta Prawna, 23-08-2011. 14

More information can be found in: M. Polasik, K. Maciejewski, Innowacyjne usługi płatnicze w

Polsce i na świecie, Materiały i Studia, No. 241, Narodowy Bank Polski, Warsaw 2009, p. 55.

13

over to the retailer or entering the PIN15

, in just a few seconds16

.

- The use of payment cards gives the user a greater control over the expenses

incurred. Consumers may examine and analyse their transactions not only on the slips

received at the cash desk but also in the bank account (assigned to the card).

Benefits for retailers (merchants):

- By accepting payment cards retailers may have a higher turnover for several reasons.

The customers' access to additional funds (especially in the case of credit card users)

promotes the growth of customers' total spending. In addition, by accepting cards

retailers have the opportunity to participate in loyalty programs or co-branding

projects and thus to expand the offer to customers and make it more attractive.

- Acceptance by retailers of payment methods that are convenient for customers, i.e.

payment cards, increases customer satisfaction. This results in strengthening the

customer – retailer relationship, perceiving the retailer as a modern company, who

cares for the interests of the customer, and consequently leads to revenue growth.

- The increase in payment card acceptance also reduces the number of fraud

transactions executed with counterfeit banknotes. The correctness of card

transactions is guaranteed by the acquirer who is controlled by supervisory authorities

(e.g. the central bank).

- In the case of payments made with the contactless card, a shorter transaction

execution time than in the case of cash payment or another type of a payment card is

beneficial not only for the consumer but also for the merchant who is able to manage

the line of cash more effectively and limit queues (POS terminals accepting proximity

cards can generate approximately 10% more transactions than other terminals).17

Benefits for card issuers:

- Issuance of payment cards to customers allows banks to increase revenues from

many sources, e.g. from the interchange fee (on each transaction paid out by the

15

For low-amount transactions, in Poland up to PLN 50. 16

If the transaction is executed off-line, i.e. without having to connect to the authorisation centre. 17

M. Polasik, E. Starogarska, Polski rynek płatności zbliżeniowych – rok 2011, Wydawnictwo – Transakcyjność

– Innowacje, Polasik Research, Toruń 2011.

14

acquirer) and fees for card issuance (one-off fee paid by the customer) or for the use of

the card (fee charged to the customer periodically, usually every month). Owing to

such a structure of revenues in the area of payment cards, the increased use of

payment cards by customers results in higher revenues for banks. Moreover, banks

may increase their revenues by cross-selling other products and services to credit card

holders.

- Banks can also enhance their image and position by participating in new market

segments, e.g. promoting the use of payment cards in the areas of the economy until

now dominated by cash (public transportation, mass events), by issuing proximity

cards. Such actions also contribute to the growth of issuing banks’ revenues.

- Offering payment cards to customers reduces queues and customer service costs in

banks' branches. Owing to the provision of ATMs to customers, the number of cash

register transactions has decreased and employees of banks' branches can perform

operations that are more profitable for the bank than the cash pay out (e.g. lending,

advisory services).

Benefits for acquirers:

The most important benefit for acquirers is generation of revenues as operations of these

entities are oriented to making profit from processing transactions executed with payment

cards. The acquirer generates revenues from fees for the lease of the terminal and from

commissions on transactions. Due to the increasing competition in the area of payment card

acceptance, acquirers compensate for declining margins by intensively developing the

acceptance network. This enables them to increase revenues or at least to maintain them at the

current level.

Benefits for the public sector and the economy:

- The growth of cashless transactions, associated with the development of payment

cards, brings significant benefits to the state. It contributes to the reduction of the

costs of cash issuing and handling. Cashless forms of money, as opposed to cash,

are not subject to damage, do not need to be manufactured, transported, counted or

physically stored. The costs of cash issuing and handling are significant.

According to the existing estimates, they can amount to as much as approximately

15

1% of GDP.18

- Wider popularity of electronic payments in a particular country facilitates the

economic growth in this country.19

- One of the main objectives of cashless transactions promotion by the public sector

is an attempt to reduce the “grey zone” in the economy and to combat money

laundering.20

The results of analyses showed that the growth of electronic

payments contributes significantly to the reduction of the size of the shadow

economy.21

In 2005, the “grey area” in Poland reached the level of 29% of GDP,

while in 2009 it accounted for 26% of GDP. In terms of the value, the unofficial

economy in our country reached the value of EUR 70.1 billion (with GDP of EUR

244 billion) and in 2009 - EUR 80 billion (with GDP of EUR 310 billion).

Therefore, even a partial reduction of the shadow economy is of great importance

to the state budget revenues.

- The cashless turnover also allows to reduce operating costs of the public

sector. An example of the benefits achieved by the public sector owing to the

popularisation of cashless transactions include, for instance, a reduction in the high

costs of retirement and disability benefits cash payments by increasing the range of

various types of benefits paid by the Social Insurance Institution to beneficiaries'

bank account or the distribution of benefits as part of the social assistance in the

form of cards.22

- It should also be noted that the popularisation of cashless transactions, particularly

in retail trade, may contribute to the reduction in the costs of Poland's entry to

the euro area related to the production of banknotes and coins and costs to be

borne by the private sector.

The use of payment cards does not only generate benefits for the participants but also

18

Obrót bezgotówkowy. Zalety i wady wynikające z jego upowszechnienia, NBP, Warsaw, 2008, p. 17. 19

The Virtuous Circle: Electronic Payments and Economic Growth, Visa International, Global Insight Inc., p.

4-5; M. Zandi, V. Singh, The Impact of Electronic Payments on Economic Growth, Moody's Analytics,

March 2010, p. 7. 20

H. Brits, C. Winder, Payments are no free lunch, Occasional Studies, Vol. 3, Nr 2, 2005, De Nederlandsche

Bank, p. 32-33. 21

AT Kearney and F. Schneider, The shadow economy in Europe. Using electronic payment systems to combat

the shadow economy, Visa Europe, 2009, p. 8; AT Kearney and F. Schneider, The Shadow Economy in

Europe, 2010. Using electronic payment systems to combat the shadow economy, Visa Europe 2011, p. 7-8. 22

Obrót bezgotówkowy. Zalety i wady wynikające z jego upowszechnienia, NBP, Warszawa 2008, p. 20-23.

16

produce costs, with costs of one group of the payment card system participants constituting, at

the same time, benefits for another group of participants of the system in many cases. Selected

cost-related issues are addressed later in this paper.

Although cash transactions dominate in many economies in the world payment cards

have been an alternative to banknotes and coins for many years, mainly in transactions

executed in retail and service outlets. The importance of payment cards has been increasing

steadily. They have become the most widely used payment instrument among cashless

methods of payment in the European Union. In 2006, the share of cashless transactions

executed with payment cards in the Community amounted to 34.4% (credit transfer 30%,

direct debit 25.2%, cheques 9.2%, electronic money and other instruments 1.3%), and in 2010

card transactions already accounted for 39.2% of the total number of cashless transactions in

the EU (credit transfer 27.8%, direct debit 25.5%, cheques 5.8%, electronic money and other

instruments 1.6%).23

We believe that the importance of payment cards in the world will

continue to grow.

23

Statistical Data Warehouse, European Central Bank, http://sdw.ecb.europa.eu, (September 2011).

17

Chapter 2

The development of the payment card market in Poland compared

to other countries

The concept of a payment card originated in the United States in the early twentieth

century. Cards from this period were usually made of metal and included customer data used

for confirming rights to receive goods and debiting the customer's credit account. Before the

outbreak of World War II, charge cards enabling deferred payment for goods were issued by

larger chains of shops and petrol stations, however they were accepted only in retail outlets of

their issuers.24

The first company to have been successful on the payment card market was

Diners Club. Soon competitors appeared on the market, such as American Express which

offered the world's first plastic card, or Bank of America which issued the world's first credit

card in California.25

The Polish payment card market is relatively young. Although credit cards appeared

in Poland in the late 1960s, they were cards issued by foreign banks and used by tourists for

making payments in a small number of outlets (mainly in outlets related to the Orbis travel

agency, exclusive hotels and restaurants). The domestic market for payment cards began to

develop in Poland as late as in the 1990s.26

This was mainly due to the reforms implemented

in our country after 1989 which also shaped he domestic banking sector. The reforms also had

a direct effect on the transformation of retail banking. At that time banks started to offer new

types of products and services to customers, including payment cards.27

2.1. Selected indicators of the development of the Polish payment card

market

The development of the payment card market can be described on the basis of an

analysis of several key areas, such as:

24

R. Janowicz, Rynek kart płatniczych w Polsce na tle rozwiniętych rynków w krajach Unii Europejskiej. Stan

obecny i perspektywy rozwoju, Materiały i Studia, no. 116, NBP, Warsaw 2001, p. 9. 25

K. Żwiruk, Historia kart płatniczych na świecie, http://kartyonline.pl, 7 July 2003. 26

More information can be found in: R. Janowicz, Rynek kart płatniczych w Polsce na tle rozwiniętych

rynków w krajach Unii Europejskiej. Stan obecny i perspektywy rozwoju, Materiały i Studia, no. 116,

NBP, Warsaw 2001, p. 12. 27

Rynek kart płatniczych w Polsce, NBP, Warsaw 2003, p. 6.

18

- the number and structure of payment cards issued,

- the value of transactions executed with payment cards,

- the acceptance network measured by the number of POS terminals, retail and service

outlets equipped with POS terminals or merchants.

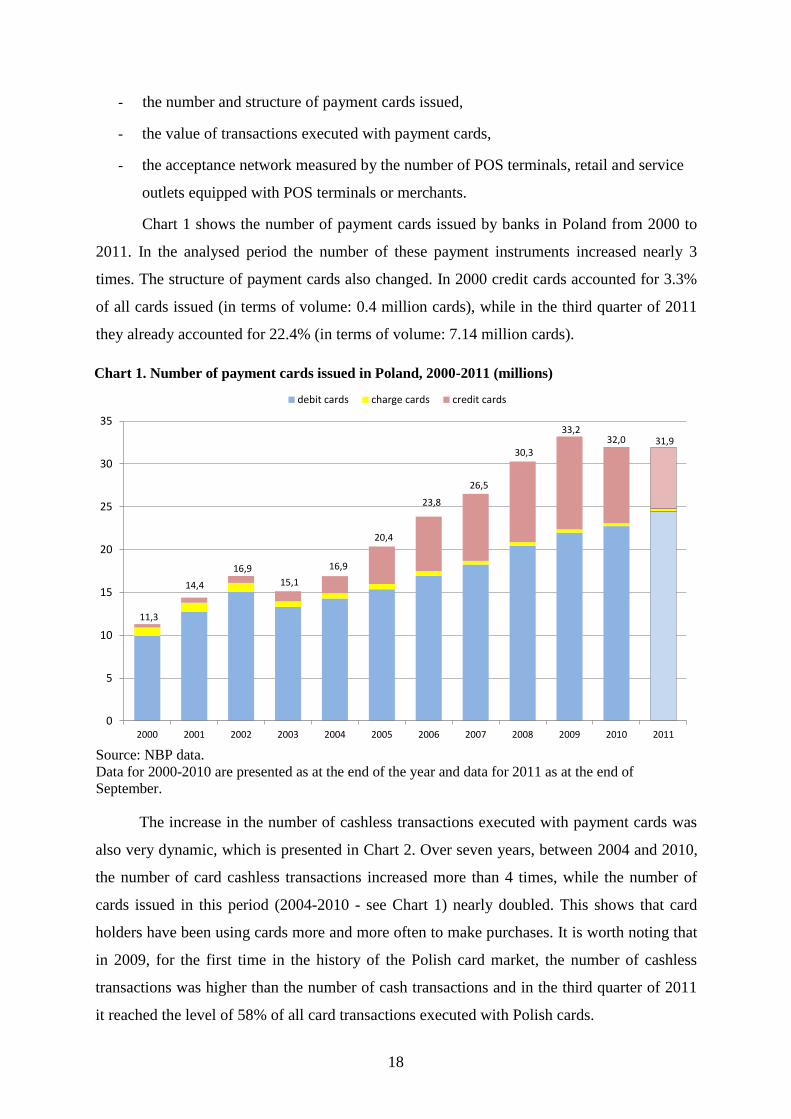

Chart 1 shows the number of payment cards issued by banks in Poland from 2000 to

2011. In the analysed period the number of these payment instruments increased nearly 3

times. The structure of payment cards also changed. In 2000 credit cards accounted for 3.3%

of all cards issued (in terms of volume: 0.4 million cards), while in the third quarter of 2011

they already accounted for 22.4% (in terms of volume: 7.14 million cards).

Chart 1. Number of payment cards issued in Poland, 2000-2011 (millions)

Source: NBP data.

Data for 2000-2010 are presented as at the end of the year and data for 2011 as at the end of

September.

The increase in the number of cashless transactions executed with payment cards was

also very dynamic, which is presented in Chart 2. Over seven years, between 2004 and 2010,

the number of card cashless transactions increased more than 4 times, while the number of

cards issued in this period (2004-2010 - see Chart 1) nearly doubled. This shows that card

holders have been using cards more and more often to make purchases. It is worth noting that

in 2009, for the first time in the history of the Polish card market, the number of cashless

transactions was higher than the number of cash transactions and in the third quarter of 2011

it reached the level of 58% of all card transactions executed with Polish cards.

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

debit cards charge cards credit cards

16,9

15,1

16,9

20,4

23,8

26,5

30,332,0

33,2

14,4

11,3

31,9

19

Chart 2. Number of cashless transactions executed with payment cards, 2004-2010 (millions)

Source: NBP data.

Between 2004 and 2010 the value of transactions also increased steadily (Chart 3). In

2004, consumers executed transactions with the use of cards issued in Poland for the total

value of PLN 25 billion, of which payments executed abroad amounted to PLN 1.6 billion. In

2010, the total value of card transactions was nearly PLN 90 billion and transactions executed

abroad constituted 6.6% of this amount, i.e. PLN 6 billion.

Chart 3. Value of cashless transactions executed with payment cards, 2004-2010 (PLN billions)

Source: NBP data.

In Poland, a continuous development of the payment card acceptance network has

been observed. As presented in Chart 4, the fastest growth was recorded in the number of card

0

100

200

300

400

500

600

700

800

900

2004 2005 2006 2007 2008 2009 2010

domestic transactions transactions executed abroad

198

264

354

462

577

704

844

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009 2010

domestic transactions transactions executed abroad

20

accepting devices (mainly terminals and imprinters in a lower number), while the increase in

the number of retail and service outlets equipped with card accepting devices was slower. The

increase in the number of merchants was the slowest: from 60 thousand in 2003 to 110

thousand in the third quarter of 2011. This means that terminals are installed more often in

commercial establishments which had accepted cards before - as additional card accepting

devices - than at new merchants.

Chart 4. Number of POS terminals in Poland and retail and service outlets (RSO) equipped with

POS terminals, 2000-2011

Source: NBP data.

Data for 2003-2010 are presented as at the end of the year and data for 2011 as at the end of

September.

It should be noted that the growth rate of the acceptance network in Poland is much

lower than the growth rate of the number of payment cards and the number and value of card

transactions, as presented in chart 5.

It may be concluded that the much slower development of the payment card

acceptance network than the rise in the number of payment cards or the number of

transactions constitutes an increasing barrier to further faster growth of card payments.

Attention should be also drawn to the saturation of the acceptance network. Data published by

the Central Statistical Office (GUS) show that in 2009 there were 371,839 shops and 9,738

petrol stations in Poland, i.e. 381,577 such entities.28

However, it seems that there are many

more potential retail and service outlets in Poland that could accept payment cards. Experts

estimate that the number of such outlets could be between 500 thousand to 1 million. This

28

Rynek wewnętrzny w 2009 r., Central Statistical Office, Trade and Services Department, Warsaw 2010.

60 69 76 78 70 8293

104 110101

119134 136 135

153176

189206

133143

166176 186

212231

253 258

0

50

100

150

200

250

300

2003 2004 2005 2006 2007 2008 2009 2010 2011

Merchants RSO Devices

21

means that the saturation of the market in Poland with retail and service outlets accepting

payment cards ranges from 19% to 38%, i.e. it is relatively low. Due to the fact that the

saturation of the Polish society with payment cards is much higher (according to the 2009

NBP survey, the share of Poles holding payment cards was 70%), this small share of

merchants accepting payment cards in the total number of retail and service outlets in Poland

means that an increasingly higher number of Poles holding cards will use them practically

only with the group of merchants used now. Card holders will encounter increasing

difficulties in using cards to make payments in new retail and service outlets because they are

faced with the barrier of non-acceptance.

Chart 5. Growth rate of acceptance network and the number of cards and cashless transactions,

2003-2010

Source: NBP data.

It should also be noted that the network of POS terminals in Poland is unevenly

developed territorially, not only in geographical terms (the saturation with POS terminals per

number of inhabitants is generally higher in the western part of Poland than in the eastern

part), but also within individual provinces (much denser acceptance network in large and

medium-sized cities than in small towns and rural areas). Due to the above factors, a

relatively common inability to use cards to make payments in retail and service outlets has a

parallel effect on the continuation of financial exclusion in Poland, calculated as the

percentage of people having a bank account, at a relatively high level in comparison with

other EU countries. People who live in places where there are no shops accepting payment

cards will not be interested in opening a bank account and receiving a payment card which in

22

practice cannot be used. A poor development of the acceptance network in Poland is therefore

one of the major barriers to reducing the financial exclusion and the development of cashless

transactions in Poland.

The analysis of factors affecting the acceptance of payment cards was the subject of a

merchant survey conducted in 2008 on behalf of the NBP.29

Among the factors that determine

whether to start accepting a particular payment method, cost factors were decisive for the

management of large-area stores (a total of 57% of the weight, including the amount of

commission charged on the value of accepted transactions - 14.9%, and fixed costs of

accepting a particular payment method - 37.4%). Yet, in the case of additionally selected

entities, cost factors accounted for 35.1% of the weight, including the commission on the

transaction value standing at 18% (it was the most important factor for this group of surveyed

entities) and fixed costs of accepting a particular payment method at 17.1%. The results of

this survey point to the crucial importance of the level of merchant fees as the factor

determining whether the retailer chooses to accept payment cards or not.

2.2. Selected indicators of the development of the payment card market -

Poland against other EU countries

The indicators presented in this part of the report are based on statistical data

published periodically by the European Central Bank in the Statistical Data Warehouse as

well as in the form of reports, the so-called Blue Book, which cover 27 Member States of the

European Union. Statistical data are presented in the form of charts with indicators describing

and comparing the level of use of payment cards per capita in the EU countries.

Chart 6 shows the number of payment cards per one inhabitant in Poland and other

EU countries in 2010. The group of seven countries with the lowest number of payment cards

per capita in the European Union comprised post-socialist countries of Central and Eastern

Europe. Regretfully, Poland comes out poorly even in comparison with those countries and

with the ratio of just 0.84 payment card per capita it surpassed only Romania (0.59 card per

capita). The highest level of saturation of the payment card market was in Luxembourg where

there were 2.64 cards on average per 1 inhabitant as well as in the UK (2.37 cards per capita)

29

M. Polasik, K. Maciejewski, Innowacyjne usługi płatnicze w Polsce i na świecie, Materiały i Studia, No. 241,

National Bank of Poland, Warsaw 2009, p. 124-125.

23

and Sweden (2.15 cards per capita). In Europe's largest economy - Germany - this ratio was

1.56 card per capita. In the EU countries the average was 1.45 cards per 1 inhabitant.

Chart 6. Number of payment cards per capita issued in Poland and other EU countries in 2010

Source: Own study based on Statistical Data Warehouse, European Central Bank,

http://sdw.ecb.europa.eu, (September 2011).

The highest indicator of the number of card payments per 1 inhabitant was observed in

Sweden and Denmark (197 transactions), as presented in chart 7. In the EU the average level

of payment card use was much lower and amounted to 68 cashless transactions per capita. In

Poland the number of cashless transactions executed with the use of a card was 3 times lower

in comparison with the EU average. Only residents of countries such as Hungary (21), Czech

Republic (20), Greece (7), Romania (5) and Bulgaria (3) used cards for making purchases less

frequently than in Poland.

0

0,5

1

1,5

2

2,5

3

Lu

xe

mb

ou

rg UK

Sw

ed

en

Po

rtu

gal

the N

eth

erl

an

ds

Be

lgiu

m

Slo

ven

ia

Cy

pru

s

Ma

lta

Germ

an

y

Sp

ain

De

nm

ark

Esto

nia

Fin

lan

d

Fra

nce

Lit

hu

an

ia

Au

str

ia

Gre

ece

Irela

nd

Italy

Latv

ia

Bu

lga

ria

Slo

vak

ia

Czec

h R

ep

ub

lic

Hu

ng

ary

Po

lan

d

Ro

ma

nia

UE average 1.45

24

Chart 7. Number of cashless transactions executed with payment cards issued in Poland and

other EU countries in 2010, per capita

Source: Own study based on Statistical Data Warehouse, European Central Bank,

http://sdw.ecb.europa.eu, (September 2011).

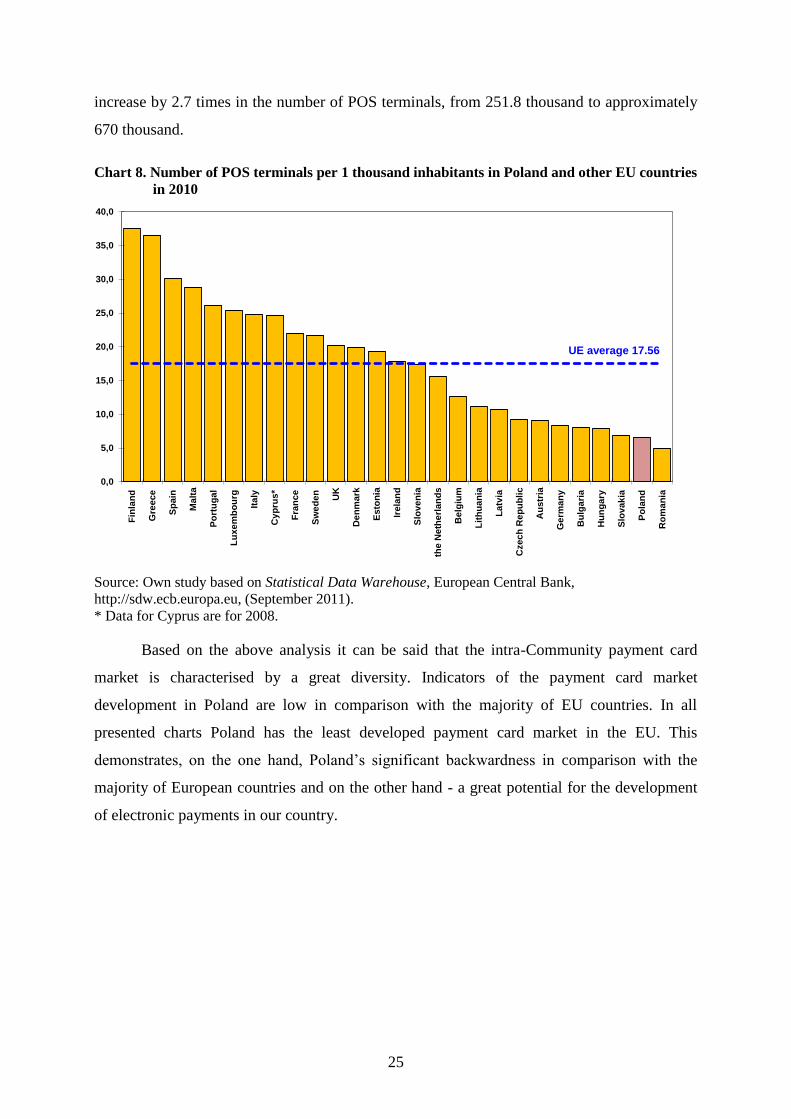

In terms of the card payment infrastructure, Poland also looked very poorly compared

to other EU countries (Chart 8). There were only 6.6 POS terminals per one thousand

inhabitants in our country. A lower rate was recorded only in Romania (5.0). The largest

number of terminals in relation to the number of inhabitants was observed in Finland (37.5

terminals per 1 thousand inhabitants). It is worth noting that this country recorded a very

dynamic growth in devices that accept payment cards. Even in 2006 this indicator was 19.9

which means that in 5 years as many as 18 terminals per one thousand of inhabitants were

installed, while in Poland there were 4.6 terminals per 1 thousand of inhabitants in 2006 and

by 2010 this number increased by 2 terminals per one thousand of inhabitants. The following

countries ranked high in this list: Greece and Spain (respectively 36.5 and 30.1 devices per 1

thousand of inhabitants), i.e. tourist traffic-oriented countries. Among ten countries with the

lowest level of accessibility to terminals there were eight former socialist countries as well as

Germany and Austria. It is worth mentioning that the establishment of a POS terminal

network in our country with the density at the current EU level (17.56) would require an

0

20

40

60

80

100

120

140

160

180

200

Sw

ed

en

De

nm

ark

Fin

lan

d

UK

the N

eth

erl

an

ds

Lu

xe

mb

ou

rg

Esto

nia

Fra

nce

Po

rtu

gal

Be

lgiu

m

Irela

nd

Slo

ven

ia

Au

str

ia

Sp

ain

Latv

ia

Cy

pru

s

Germ

an

y

Ma

lta

Lit

hu

an

ia

Italy

Slo

vak

ia

Po

lan

d

Hu

ng

ary

Czec

h R

ep

ub

lic

Gre

ece

Ro

ma

nia

Bu

lga

ria

UE average 68

25

increase by 2.7 times in the number of POS terminals, from 251.8 thousand to approximately

670 thousand.

Chart 8. Number of POS terminals per 1 thousand inhabitants in Poland and other EU countries

in 2010

Source: Own study based on Statistical Data Warehouse, European Central Bank,

http://sdw.ecb.europa.eu, (September 2011).

* Data for Cyprus are for 2008.

Based on the above analysis it can be said that the intra-Community payment card

market is characterised by a great diversity. Indicators of the payment card market

development in Poland are low in comparison with the majority of EU countries. In all

presented charts Poland has the least developed payment card market in the EU. This

demonstrates, on the one hand, Poland’s significant backwardness in comparison with the

majority of European countries and on the other hand - a great potential for the development

of electronic payments in our country.

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

Fin

lan

d

Gre

ece

Sp

ain

Ma

lta

Po

rtu

ga

l

Lu

xe

mb

ou

rg

Ita

ly

Cy

pru

s*

Fra

nc

e

Sw

ed

en

UK

De

nm

ark

Es

ton

ia

Ire

lan

d

Slo

ve

nia

the

Ne

the

rla

nd

s

Be

lgiu

m

Lit

hu

an

ia

Latv

ia

Cze

ch

Re

pu

bli

c

Au

str

ia

Ge

rma

ny

Bu

lga

ria

Hu

ng

ary

Slo

va

kia

Po

lan

d

Ro

ma

nia

UE average 17.56

26

Chapter 3

Factors determining the development of the payment card market

in Poland

Factors determining the development of the payment card market in Poland can be

considered at various levels. These factors may be external and internal. They may be

national, local - arising from the specificity of our economy, as well as international.

Conditions for the development of the payment card market may also relate to business,

regulatory, legal and technical issues. The most important of them are presented below in the

form of comprehensive projects undertaken in the payment services market.

3.1. SEPA

In recent years many initiatives have emerged which are aimed at developing and

regulating the market for payment services. Currently, large projects are being implemented

in the European market which address the integration of the retail payments market.30

In

connection with Poland's integration with the European Union the banking industry and

market regulators are facing a major challenge posed by intra-Community diversification of

the payment services markets (in terms of the structure, operating principles and the legal and

institutional environment) which hinders cross-border payments in particular,

One of the major projects in this regard is the establishment of the Single Euro

Payments Area (SEPA) which was preceded by a long period of preparations undertaken by

many actors and institutions connected with the European payments industry. In line with the

vision of the project initiators, i.e. the European Commission, the European Central Bank and

the European Payment Council (EPC), SEPA is to be an area in which consumers, businesses

and other participants of the economic life will be able to make and receive both domestic and

cross-border payments in euro, within Europe, under the same, simple principles, rights and

obligations, regardless of their location.31

The SEPA project which was launched on 28 January 2008 marks another stage of the

integration of the European financial market, following the introduction of the single euro

30

A. Borcuch, Globalny system pieniężny, CeDeWu, Warsaw, 2009, p. 105-111. 31

Single Euro Payments Area (SEPA). Integrated retail payments market, European Central Bank, 2006, p.7

27

currency and TARGET large-value payments. Its coverage includes mostly euro-area

countries but it also applies to other EU states and 4 countries from the European Free Trade

Association (EFTA) countries, i.e. Iceland, Norway, Liechtenstein and Switzerland. In total,

SEPA covers 31 countries in Europe. It should be noted at this point that the SEPA project

was intended to be of a self-regulatory character, which means that it was to be implemented

without any formal orders or prohibitions from EU or national authorities.32

The SEPA project consists of several components, such as: the single currency, a

single set of euro payment instruments, efficient infrastructure for euro payments, common

technical standards, common business practices, harmonised legal basis, and ongoing

development of customer-oriented services.

The primary component of the Single Euro Payments Area is a set of new SEPA

payment instruments: SEPA credit transfer, SEPA direct debit and SEPA card payments.

These are non-cash instruments offered to customers in accordance with harmonised

standards and principles. From the official launch of the project until the end of 2010, the so-

called transitional period was in force under which SEPA instruments were to be introduced

gradually and coexist with the existing national solutions. According to program guidelines,

starting from 2011 a full migration to SEPA standards should take place.33

The adaptation of payment cards to the SEPA requirements is implemented in

accordance with the principles laid down in the SEPA Cards Framework (SCF). The main

objective of establishing the SCF principles is to create an environment free from

technological, legal and commercial barriers to the issuance of payment cards and to

processing, accepting and executing card transactions. In accordance with the SCF, from 1

January 2008 tol 31 December 2010, i.e. during the transitional period, a gradual migration to

the EMV standard should take place, consisting in replacing magnetic stripe cards with cards

based on the microprocessor technology and adapting the infrastructure of POS terminals and

ATMs so as to handle cards in the EMV standard. In the same transitional period all payment

terminals and ATMs were also to be adapted to accept EMV cards. After this period, i.e. from

1 January 2011, all general purpose payment cards in circulation, issued by SEPA banks

should comply with the SEPA Cards Framework. This means that magnetic stripe cards

32

D. Duziak, R. Kaszubski, Nowe regulacje europejskiego rynku usług płatniczych to korzyść dla polskich

klientów, "Gazeta Prawna" of 12 June 2008, http://biznes.gazetaprawna.pl. 33

Polish Banks Association, SEPA Poland Service, http://sepapolska.pl (December 2009).

28

issued in the SEPA area should be withdrawn from circulation.34

According to the European Commission, in the fourth quarter of 2010 a total of 81%

of payment cards, 96% of ATMs and 90% of POS terminals in the EU countries were

equipped with a chip compliant with the EMV standard.35

In Poland the process of adapting

the infrastructure of POS terminals to the EMV standard is also progressing quite well (80%

of terminals), while migration of ATMs to these standards is much faster (98% of devices).

However, until 2010 the process of equipping payment cards with a chip was slower than the

EU average because the percentage of cards compliant with EMV standard amounted to

49.6% as at the end of 2010, although it increased significantly by June 2011 to 61%.

A payment card transaction consistent with the SEPA principles is a transaction

executed with a "general purpose" payment card (debit, credit or charge card) issued in one of

the SEPA countries, in the area covered by SEPA and with the participation of a SEPA bank.

This may be a payment transaction (at a retail and service outlet or a remote transaction) or

cash withdrawal at an ATM, however always with the use of EMV technology (except for

remote transactions) and settled in euro (the account may be operated in any currency).

Payments will be executed with one card throughout the SEPA area, yet retailers will be able

to impose restrictions on the acceptability of individual brands of cards. It is worth noting that

the SCF guidelines do not include the electronic money and prepaid cards, which creates

opportunities for the development of niche solutions such as: local payments, fees for public

transportation or gift cards. Poland, like other non-euro area Member States and EFTA

countries, may and does participate in the SEPA as part of euro payments and will be able to

adopt SEPA standards for payment instruments in the national currency.

An important element of the SEPA project is the incorporation in the SCF of

provisions prohibiting application of different prices for domestic and cross-border services.

In addition, each system should have a transparent pricing structure, uniform for the whole

SEPA area that will allow the largest possible number of actors to participate in the system.

Consequently, this means a prohibition to differentiate scheme fees geographically (e.g.

depending on the country)36

. Imposing such a shape of pricing policy on card schemes means

34

R. Kaszubski, D. Duziak (edit.), Jednolity Obszar Płatności w Euro - SEPA. Wpływ zmian na rynku

płatności na podmioty prowadzące działalność gospodarczą, Polish Banks Association, 2008, p. 19,

http://www.sepapolska.pl (October 2008). 35

3rd progress report on the state of SEPA migration, European Commission, DG Internal Market and

Services, Brussels, 17 May 2011,

http://ec.europa.eu/internal_market/payments/docs/sepa/progress_report_2010_en.pdf (August 2011). 36

SEPA Cards Framework, European Payment Council, 16 December 2009, p. 14.

29

that they must change their existing beneficial business model, mainly because of the freedom

in setting fees for the participation in the system. Therefore, it can be assumed that the

organisations will attempt to evade the requirements imposed on them.37

However, attention

should be drawn to the provision pursuant to which each payment card scheme is responsible

for its interchange fee, which means that the SCF has not introduced regulations relating to

the interchange fee and that setting it remains, as before, at the discretion of a particular

scheme associating card issuers.38

This approach is explained with the role of the interchange

fee which is to compensate for the costs of operating the scheme, and also with the fact that

the fee is calculated multilaterally, and therefore it applies to all entities participating in the

network. In turn, in the opinion of the European Central Bank a long-term continuation of

rates differentiated geographically is in conflict with the pro-integrative concept of SEPA.39

3.2. Payment services directive

The second project, in addition to SEPA, aimed at creating an integrated market for

payment services is the Payment Services Directive (PSD). The Directive was adopted by the

European Parliament and the Council of the European Union in 2007, and Member States

were required to implement the regulation by 1 November 2009. However, not all countries,

including Poland, met the deadline.40

This document establishes a common legal framework

for the provision of payment services in the European Union which until now were governed

by regulations of separate legal systems of Member States.

The major areas governed by the PSD regulations include;41

- right of public provision of payment services, meaning the harmonisation of

conditions for market entry to be met by non-bank entities intending to provide

payment services. This is to ensure a level playing field for all market participants and

stimulate increased innovation and competitiveness of national markets;

- requirements for transparency of information defining a set of harmonised information

37

J. Chaplin, SEPA – changing the game for cards, First Data International, 2007, http:\\\www.firstdata.com. 38

SEPA Cards Framework, European Payment Council, 16 December 2009, p. 16. 39

5th Progress Report (July 2007), SEPA - from concept to reality, European Central Bank, p. 13. 40

Poland was the last country in the European Union to have implemented the provisions of the Directive into

national law as late as on 24 October 2011, i.e. simultaneously with the entry into force of the Act on

Payment Services of 19 August 2011. 41

Single Euro Payments Area (SEPA), European Central Bank, http://www.ecb.int/pub/pdf/other/sepa_brochure_2009pl.pdf (February 2010).

30

requirements that will have to be presented by all payment service providers;

- rights and obligations of users and providers of payment services which are explained

in the Directive in detail and finally.

The objectives of the Directive which include the support for consumer rights and

integration of national systems as well as the promotion of the transparency and competition

in the market for payment services greatly support the creation of the Single Euro Payments

Area.42

The Directive does not provide for requirements for determining the level of

interchange fees. As far as national options are concerned, only activities related to the

introduction of the surcharge are permitted.

3.3. Act on Payment Services

The Polish Act on Payment Services implements the Payment Services Directive. The

final text of the Act was determined by the Parliament after the consideration of the Senate's

amendments on 19 August 2011.43

The Act on Payment Services was published in the Journal

of Laws on 23 September 2011, and its basic provisions entered into force on 24 October

2011. It is worth noting that the implementation of the Payment Services Directive took a

very long time in our country. Poland is the last EU country to implement the Directive into

the national law. The delays resulted from a very long process of consultations and a large

number of comments and amendments reported at various stages of work on the act. The

provisions of the Act relate to the market which until now has not been regulated in its major

part (except for regulations on, among other things, payment systems, acquirers and

authorisation and clearing systems). According to the Act, payment services and the provision

of such services will no longer be provided, as before, as free economic activity and will be

subject to the supervision of the Polish Financial Supervision Authority.

The Act specifies the conditions for the provision of payment services, in particular in

respect of the transparency of contractual provisions and requirements for informing about

42

(1) Making SEPA a Reality. Implementing the Single Euro Payments Area, European Payment Council, Doc: EPC066-06, Brussels, 28 June 2006, (2) Joint statement by the European Central Bank and the European Commission concerning the adoption by the European Parliament of the Payment Services Directive, European Central Bank, 24 April 2007, http://www.ecb.int/press/pr/date/2007/html/pr070424.pl.html (August 2011).

43 Polish Parliament, Payment Services Act of 19 August 2011, text of the act determined finally after

consideration of Senate amendments,

http://orka.sejm.gov.pl/opinie6.nsf/nazwa/4217_u/$file/4217_u.pdf

31

payment services; the rights and obligations of the parties arising from contracts on the

provision of payment services, as well as the responsibilities of providers in respect of the

performance of payment services and principles for conducting the activity by payment

institutions and payment services agencies, including through agents of these entities, and the

principles for supervision of these entities.

As part of parliamentary debates on the Act, one of the items discussed was the

problem of the surcharge and interchange fees, which is further described in section 6.3.

3.4. Payment card organisations in Poland

Regulations and standards set by VISA and MasterCard which must be observed as

part of civil law contracts by: (i) banks issuing payment cards with the logo of these

organisations, (ii) acquirers and (iii) merchants accepting these cards, are in fact one of the

main factors that contributed to the development of this market. The regulations of these

organisations determine the business model which functions on the basis of a four-party

payment system which requires the involvement of specialised entities operating under

strictly defined rules. There is no competitive national card payment system in Poland,

therefore the Polish payment card market is highly dependent on the regulations of

international payment organisations.

3.4.1. “Visa cards accepted everywhere” programme

One of the recent major projects of the Visa organisation is the programme launched

at the beginning of 2010 aimed at developing a payment card acceptance network, called

"Visa cards accepted everywhere”. The programme aims to double the number of POS

terminals in Poland, i.e. from approximately 200 thousand to 400 thousand terminals in 2015.

The launch of the programme was preceded by market consultations, both with banks issuing

VISA cards and acquirers. The program, which is funded by the banks issuing cards, is

focused on attracting retail and service outlets which so far have not accepted payment cards.

Funds are transferred to acquirers in the form of a subsidy to the installation of new terminals.

Under this programme, Visa member banks in Poland will allocate more than PLN 200

million over 5 years to support the growth of card acceptance. By the end of September 2011

approximately 56 thousand new POS terminals had been installed at nearly 38 thousand

merchants who had not previously accepted payment cards.

32

3.4.2. „Innovation for Poland” programme

MasterCard organisation launched the "Innovation for Poland" programme which

aims at supporting banks issuing payment cards with the MasterCard logo which intend to

introduce innovative products such as: proximity cards, NFC mobile payments, cards with a

display or multi-application cards. Funding may be obtained for a particular project on the

basis of an application submitted by the bank to the MasterCard organisation. Decisions on

granting the financing are made by the group of MasterCard experts, i.e. representatives of

the local market representing the MasterCard office in Warsaw and European experts

responsible for innovative products.

The programme was launched on 1 January 2011 pursuant to the decision of the

MasterCard organisation. The program is expected to create a fund financed by acquirers who

are required to pay an additional fee of 0.025% of the value of transactions executed with

payment cards. It is estimated that in 2011 acquirers will pay approximately EUR 5 million to

the fund.

3.5. Interchange fee policy of the European Commission and European

Central Bank

3.5.1. European Commission's Action

The issue of the interchange fee has been the subject of analyses of the European

Commission for many years. The first complaint which accused Visa and Europay

International of restricting competition through specific arrangements concerning interchange

fees charged for cross-border transactions, was submitted by the British Retail Consortium in

1992. The second complaint, concerning, inter alia, multilaterally agreed interchange fees in

Visa and MasterCard systems, was filed in 1997 on the initiative of EuroCommerce

association representing retail, wholesale and international sellers in the European Union.

The first significant event was the decision of 24 July 2002 on inter-regional

interchange fee determined multilaterally under the Visa Europe association. In this decision

the Commission approved, as an exemption to the competition rules (Article 81 clause 3 of

the Treaty establishing the European Community), the use by Visa of interchange fees for

cross-border transactions, subject to acceptance by Visa of new rules which related to:

- reduction of the interchange fee; for debit cards the interchange fee will be reduced

33

gradually over a period of five years with this reduction amounting to over 50%; for

credit cards the reduction of the interchange fee will also be gradual, so that in 2007

the level of 0.7% is reached; income of banks from charging this fee will fall

gradually to approximately 20% in relation to the income that would have been

achieved if the above mentioned change had not been introduced.

- objectivity, i.e. the use of three cost categories to set the interchange fee:

• transaction processing costs,

• costs of providing customers with a free funding period,

• costs of the so-called "payment guarantee",

- transparency; at the request of the owners of retail and service outlets, Visa member

banks will be required to disclose their rates of the interchange fee and the percentage

share of the above mentioned three cost categories in that fee,

- setting a separate interchange fee for transactions executed by mail or telephone, due

to differences in costs in relation to transactions executed via POS.44

The said exemption expired on 31 December 2007. By this date the adjustment of the

Visa system to the competition rules should have been completed. In March 2008, the

Commission initiated proceedings against Visa Europe to verify the method of determining