14

HD and Digital Programming Bolsters Global Demand for Video and Ad Insertion Servers Research PREVIEW for the Analysis of the Global Video and Ad Insertion Server Market @FS_ITVision

| Date post: | 15-Jul-2015 |

| Category: |

Technology |

| Upload: | frost-sullivan |

| View: | 567 times |

| Download: | 0 times |

HD and Digital Programming Bolsters Global

Demand for Video and Ad Insertion Servers

Research PREVIEW for the

Analysis of the Global Video and Ad Insertion Server

Market

@FS_ITVision

Sample of Key Highlights

• Insert no more than six brief research bullet points to summarize basic

findings

• Avoid repeating data found in press release

• Include proper spacing to give adequate white space

• Provide a true preview by refraining from listing out the TOC; however,

some bullets on scope of research, definitions or explanations welcome

• Include this year or future data vs. outdated statistics

Source: Frost & Sullivan analysis.

Contents

Section Slide Number

Executive Summary 4

Market Overview 12

External Challenges: Drivers and Restraints—Total Video and Ad Insertion Server Market 19

Market and Technology Trends 22

Forecasts and Trends 34

Market Share and Competitive Analysis—Video Server Market 45

Market Share and Competitive Analysis—Ad Insertion Server Market 66

Cable Video and Ad Insertion Server Segment Breakdown 72

Telco Video and Ad Insertion Server Segment Breakdown 104

Broadcast Video and Ad Insertion Server Segment Breakdown 137

Hot Company Watchlist 174

The Last Word 180

Appendix 183

Executive Summary

• The evolution in digital technology has led television broadcast facilities through a phase of

transition. Upgrades from analog to digital transmission and to high-definition (HD) content

have resulted in more opportunities for advertisers, broadcasters, service providers, and

equipment manufacturers.

• As a result, consumers not only have access to more high-quality audio and video content

through diverse media such as cable, satellite, Internet protocol television (IPTV), and

mobile and Web-based networks, but they can receive and interact with advertisements

that are highly tailored to suit their interests and are engaging.

• Personalized and interactive services such as video on demand (VOD) have transformed

the way consumers watch television. The success of on-demand television has further led

to the birth of more enhanced capabilities such as pause live TV and catch up TV

functions, networked personal video recorders (NPVRs), and interactive advertising.

• This proliferation in content services is expected to drive broadcasters and service

providers to install state-of-the-art ad insertion technology in their facilities over the

forecast period to augment their revenue streams.

Source: Frost & Sullivan

Executive Summary (continued)

• There has been an increasing uptake of digital video services through multiple channels

and platforms worldwide. Broadcasters and cable operators have been migrating to all-

digital networks, thus catering to their subscribers’ growing needs for digital content. The

transition from standard-definition (SD) to HD and proliferation of VOD content and

libraries have increased the focus on developing appropriate advertising models and

technology that offers operators the ability to provide interactive and addressable

commercials.

• Further, major sports events such as the Sochi Olympics in Russia and the FIFA World

Cup in Brazil in 2014, as well as all studio productions globally, are increasingly recorded

in HD and Ultra-HD. These events have helped shorten the sales cycles for purchasing

digital media technology but at the same time are expected to increase the demand for

digital equipment, including video server systems, for effective and efficient distribution of

content to the consumer.

• The global server market has experienced 3 straight years of growth despite the

macroeconomic challenges in the Europe, Middle East, Africa (EMEA) region and is

expected to record revenue of nearly $2.0 billion by 2019.

Source: Frost & Sullivan

Executive Summary—CEO’s Perspective

2

Cable and telco companies that do not upgrade their server solutions to distribute video over multiple media such as Internet and mobile/tablets risk falling behind the competitive curve.

3

The video server market has witnessed significant consolidation among vendors over the last 5 years; the cable segment is most fragmented, and telco and broadcast should expect further M&A activity.

4 Interactive services such as NPVR, time-shifted TV, and VOD continue to be key differentiators for cable MSOs and telco operators. Dynamic ad insertion driven by analytics is the game changer.

5

As North America and Western Europe have been leading the way in terms of infrastructure upgrades and workflow digitization, demand from these regions is expected to be relatively weak over the forecast period.

1

Service providers must necessarily focus on deriving a greater share of revenue from their advertisement business to monetize investments in interactive services.

Source: Frost & Sullivan

Market Overview—Key Questions This Study Will Answer

Will the market continue to grow at its present rate? Will growth slow down as the industry matures over the long term, especially in the developed markets?

How are the existing competitors structured in the cable, telco, and broadcast segments? Are there too many competitors at present? Are they well positioned to meet current and future customer needs?

Will there be further consolidation over the next 4 to 5 years? Will the market continue to be attractive for mergers and acquisitions?

Where does video and ad server technology stand today? What are the primary challenges faced by vendors and new deployers in this market? What are the drivers and restraints for growth?

What are the major technology trends under consideration? How do pricing models differ by category—cable, telco, and broadcast?

What are the revenue breakdowns for the Americas, EMEA, and Asia-Pacific regions? Which are the fastest-growing regions?

Source: Frost & Sullivan

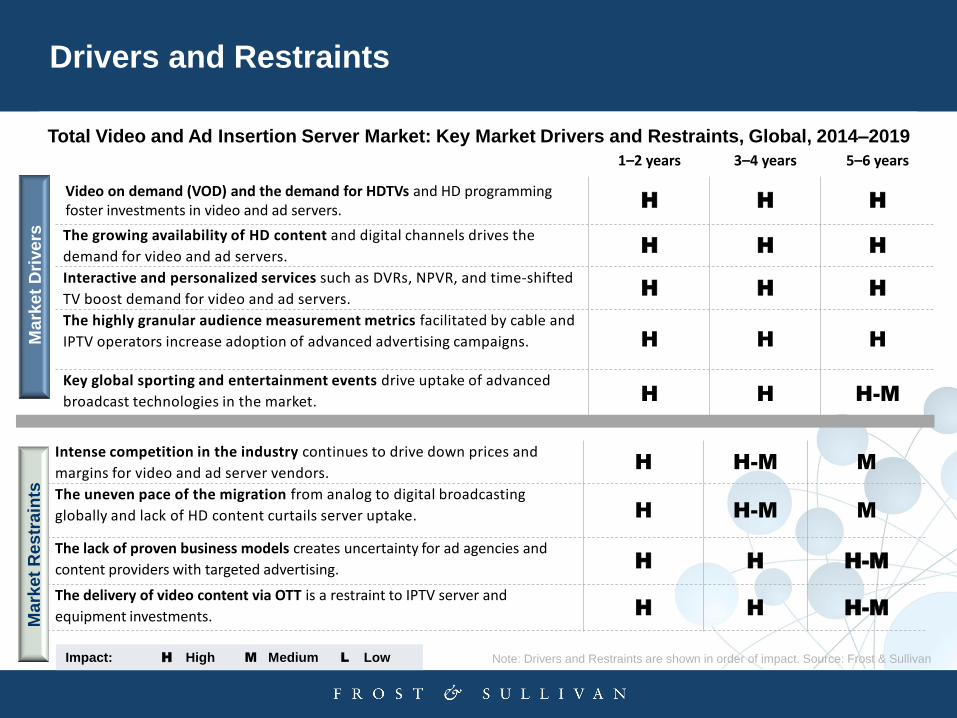

Drivers and Restraints

Total Video and Ad Insertion Server Market: Key Market Drivers and Restraints, Global, 2014–2019

Intense competition in the industry continues to drive down prices and

margins for video and ad server vendors. H H-M M

The uneven pace of the migration from analog to digital broadcasting

globally and lack of HD content curtails server uptake. H H-M M

The lack of proven business models creates uncertainty for ad agencies and

content providers with targeted advertising. H H H-M

The delivery of video content via OTT is a restraint to IPTV server and

equipment investments. H H H-M

1–2 years 3–4 years 5–6 years

Video on demand (VOD) and the demand for HDTVs and HD programming foster investments in video and ad servers. H H H

The growing availability of HD content and digital channels drives the

demand for video and ad servers. H H H

Interactive and personalized services such as DVRs, NPVR, and time-shifted

TV boost demand for video and ad servers. H H H

The highly granular audience measurement metrics facilitated by cable and

IPTV operators increase adoption of advanced advertising campaigns. H H H

Key global sporting and entertainment events drive uptake of advanced

broadcast technologies in the market. H H H-M

Note: Drivers and Restraints are shown in order of impact. Source: Frost & Sullivan

Mark

et

Dri

vers

M

ark

et

Restr

ain

ts

Impact: H High M Medium L Low

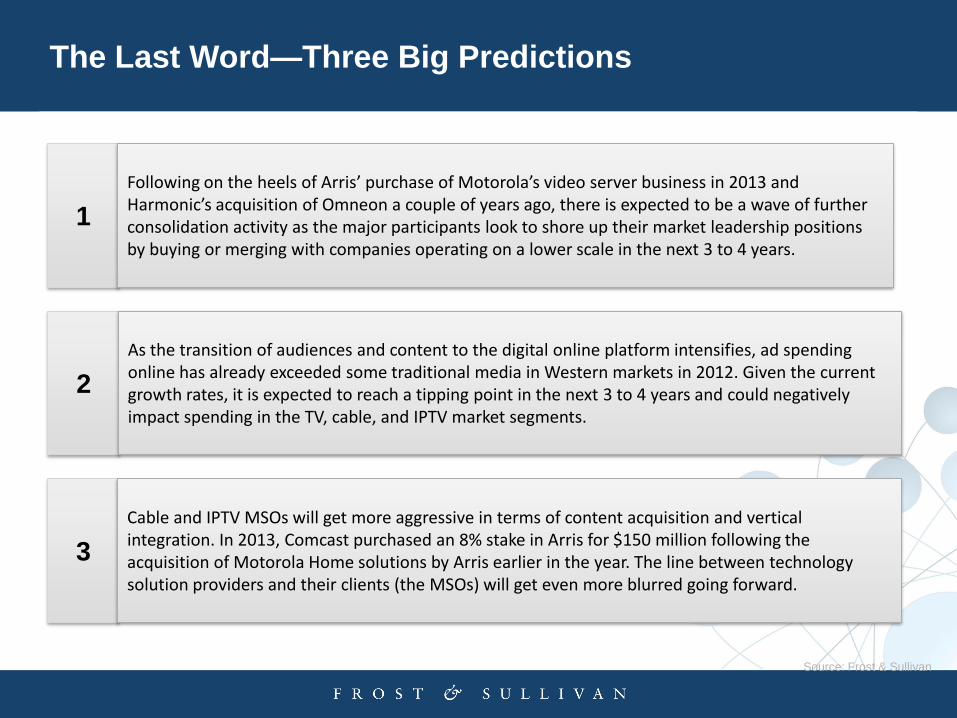

The Last Word—Three Big Predictions

2

As the transition of audiences and content to the digital online platform intensifies, ad spending online has already exceeded some traditional media in Western markets in 2012. Given the current growth rates, it is expected to reach a tipping point in the next 3 to 4 years and could negatively impact spending in the TV, cable, and IPTV market segments.

3

Cable and IPTV MSOs will get more aggressive in terms of content acquisition and vertical integration. In 2013, Comcast purchased an 8% stake in Arris for $150 million following the acquisition of Motorola Home solutions by Arris earlier in the year. The line between technology solution providers and their clients (the MSOs) will get even more blurred going forward.

1

Following on the heels of Arris’ purchase of Motorola’s video server business in 2013 and Harmonic’s acquisition of Omneon a couple of years ago, there is expected to be a wave of further consolidation activity as the major participants look to shore up their market leadership positions by buying or merging with companies operating on a lower scale in the next 3 to 4 years.

Source: Frost & Sullivan

Partial List of Companies Interviewed

• Avid

• Anevia

• Arris / Motorola

• Cisco / Arroyo / NDS

• Concurrent Computer

• Edgeware

• EVS

• Espial/Kasenna

• Grass Valley

• Harmonic/Omneon

• Harris Broadcast

• Quantel

• SeaChange International / XOR Media

• UTStarcom

• 360 Systems

Source: Frost & Sullivan

Associated Multimedia

Visionary IT Portal Frost & Sullivan's Interactive ICT Community http://visionary-it.gilcommunity.com/

Analyst Blogs Information & Communication Technologies http://bit.ly/1e7xG3R

Analyst Briefings Complimentary ICT Webinars http://bit.ly/1f9CZV6

SlideShare - Frost & Sullivan’s Technology Presentations http://slidesha.re/1oMWgy4

Market Insight Articles Complimentary ICT Analyst Insights http://bit.ly/KqH4Xp

GIL Talks Frost & Sullivan Thought Leadership Videos http://www.gilcommunity.com/gil-talks

Interested in Full Access? Connect With Us

Clarissa Castaneda Corporate Communications

(210) 477-8481

Research Authors

Lead Analyst

Aravindh Vanchesan

Program Manager, Digital Media

Frost & Sullivan

Research Director

Mukul Krishna

Senior Global Director, Digital Media

Frost & Sullivan

Facebook https://www.facebook.com/FrostandSullivan

LinkedIn Group https://www.linkedin.com/company/frost-&-sullivan

SlideShare http://www.slideshare.net/FrostandSullivan

Twitter https://twitter.com/Frost_Sullivan

Frost & Sullivan Events Upcoming Events Calendar

GIL Community http://visionary-it.gilcommunity.com/

Global Perspective 40+ Offices Monitoring for Opportunities and Challenges

Industry Convergence Comprehensive Industry Coverage Sparks Innovation Opportunities

Automotive &

Transportation

Aerospace & Defense Measurement &

Instrumentation

Information &

Communication Technologies

Healthcare Environment & Building

Technologies

Energy & Power

Systems

Chemicals, Materials

& Food

Electronics &

Security

Industrial Automation

& Process Control

Automotive

Transportation & Logistics

Consumer

Technologies

Minerals & Mining

![NoTube: Ad Insertion [compatibility mode]](https://static.documents.pub/doc/80x56/5456af8fb1af9fb66e8b501e/notube-ad-insertion-compatibility-mode.jpg)