ANALYST CORNER LED cost cutting propels package designs A sk a member of the general public to draw an LED, and you’ll probably still get a picture of the two-pin domed through-hole format widely used as indicators. But in lighting up small displays and TVs, packages have evolved dramatically, becoming unrecognisable when laid against their ancestor. Now, to address their third growth cycle, where revenue increases will be driven by general illumination, these packages must offer better performance for their cost. And with packaging comprising up to 45 per cent of the cost of a packaged LED, it’s unsurprising that it’s now a major focus of those efforts. “The industry needs further lm/$ cost of ownership improvements,” stressed Eric Virey, market analyst at Yole Développement. “To improve that, you have two levers: improve the performance of each individual package so you can reduce the number of packages then at system level; or decrease manufacturing cost.” LED producers are now pushing on the cost lever harder than ever before, Virey added. “This drive towards a better lm/$ has changed the high power package design philosophy, at least for some manufacturers. In most cases, until maybe a year ago, we were seeing a lot of effort toward improving performance, even at the expense of added complexity. Now, what we’ve observed in some cases has been a focus on ways to design cost reduction into their packaging.” A notable example of this shift comes in the orientation in which Durham, North Carolina headquarted LED maker Cree, Inc. places LED chips into its packages. “The trend for many high power LED manufacturers was to use vertical LEDs, where the initial sapphire or SiC substrate is removed and the LED structure bonded onto another carrier wafer,” Virey explained. “I would say a year or two ago, most of Cree’s high power LEDs were designed that way.” Cree’s latest XB-D family of XLamp high brightness LEDs, launched in January 2012, revisits a simpler approach used in previous generations: flip-chip packaging. “It’s just a flip-chip structure, where they keep the initial substrate, and they’ve found ways to improve the light extraction by texturing the back side of the initial SiC epitaxial substrates after it is thinned down,” Virey said. “Texturing the substrate is not new, a lot of players have been using patterned sapphire substrates, but Cree is using an even simpler and cheaper design. They create grooves, we Manufacturers are exploring many alternatives of package substrate, format and phosphor as they try and balance the price/performance equation for solid state lighting, according to Yole Développement’s Eric Virey and Pars Mukish. DECEMBER 2012 ISSUE N°6 18 i LED Eric Virey Senior Analyst, LED, Yole Développement Others (assembly, housing…) IC Driver / Power Supply Mechanical / Thermal LED Packages Optics Packaging 53% 45% 20% 19% 5% 11% Front-End 47% Economy package: As packaging makes up a significant part of packaged LED and luminaire costs, manufacturers are trying to drive down its cost. Pars Mukish, Technology Market Analyst, LED, Yole Développement LED downlight luminaire cost breakdown 1W packaged LED cost breakdown (Source: LED Packaging report, to be released beginning of 2013, Yole Développement)

Transcript

A N A L Y S T C O R N E R

LED cost cutting propels package designs

Ask a member of the general public to draw an LED, and you’ll probably still get a picture of the two-pin domed through-hole

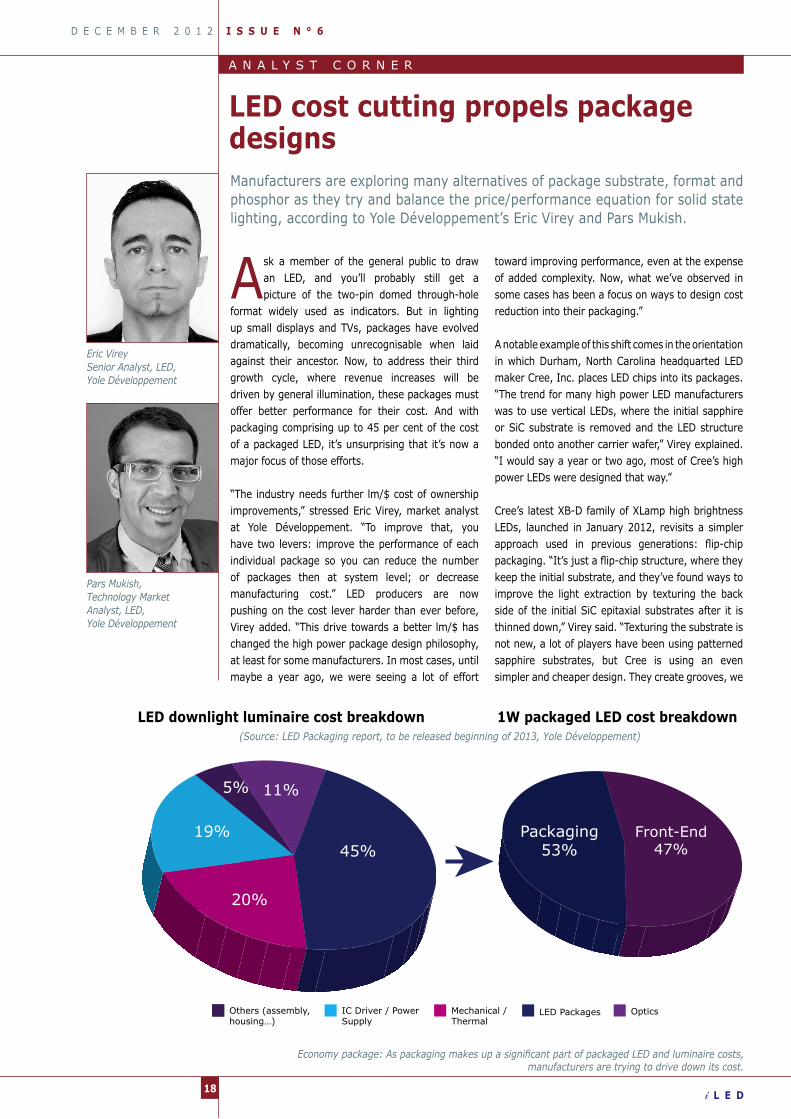

format widely used as indicators. But in lighting up small displays and TVs, packages have evolved dramatically, becoming unrecognisable when laid against their ancestor. Now, to address their third growth cycle, where revenue increases will be driven by general illumination, these packages must offer better performance for their cost. And with packaging comprising up to 45 per cent of the cost of a packaged LED, it’s unsurprising that it’s now a major focus of those efforts.

“The industry needs further lm/$ cost of ownership improvements,” stressed Eric Virey, market analyst at Yole Développement. “To improve that, you have two levers: improve the performance of each individual package so you can reduce the number of packages then at system level; or decrease manufacturing cost.” LED producers are now pushing on the cost lever harder than ever before, Virey added. “This drive towards a better lm/$ has changed the high power package design philosophy, at least for some manufacturers. In most cases, until maybe a year ago, we were seeing a lot of effort

toward improving performance, even at the expense of added complexity. Now, what we’ve observed in some cases has been a focus on ways to design cost reduction into their packaging.”

A notable example of this shift comes in the orientation in which Durham, North Carolina headquarted LED maker Cree, Inc. places LED chips into its packages. “The trend for many high power LED manufacturers was to use vertical LEDs, where the initial sapphire or SiC substrate is removed and the LED structure bonded onto another carrier wafer,” Virey explained. “I would say a year or two ago, most of Cree’s high power LEDs were designed that way.”

Cree’s latest XB-D family of XLamp high brightness LEDs, launched in January 2012, revisits a simpler approach used in previous generations: fl ip-chip packaging. “It’s just a fl ip-chip structure, where they keep the initial substrate, and they’ve found ways to improve the light extraction by texturing the back side of the initial SiC epitaxial substrates after it is thinned down,” Virey said. “Texturing the substrate is not new, a lot of players have been using patterned sapphire substrates, but Cree is using an even simpler and cheaper design. They create grooves, we

Manufacturers are exploring many alternatives of package substrate, format and phosphor as they try and balance the price/performance equation for solid state lighting, according to Yole Développement’s Eric Virey and Pars Mukish.

D E C E M B E R 2 0 1 2 I S S U E N ° 6

18 i L E D

Eric VireySenior Analyst, LED,Yole Développement

Others (assembly,housing…)

IC Driver / PowerSupply

Mechanical /Thermal

LED Packages Optics

Packaging53%45%

20%

19%

5% 11%

Front-End47%

Economy package: As packaging makes up a signifi cant part of packaged LED and luminaire costs, manufacturers are trying to drive down its cost.

Pars Mukish,Technology Market Analyst, LED,Yole Développement

LED downlight luminaire cost breakdown 1W packaged LED cost breakdown(Source: LED Packaging report, to be released beginning of 2013, Yole Développement)

19i L E D

believe just by using a mechanical saw, at a certain angle that maximises the extraction. That still seems very effi cient in terms of generating and extracting the light. It’s a clever design that maximises lm/$.”

While LED producers like Cree, Regensburg, Germany, headquartered, Osram Opto Semiconductors and San Jose California’s Philips Lumileds, all want to improve cost of ownership, their approaches otherwise remain quite different. “Osram still seems to be using vertical LED structures, and Lumileds still seem to favour thin fi lm fl ip-chips, where they also remove the sapphire,” Virey said. “Cree has also been using a different type of bonding technology for the fl ip-chip. While Lumileds is using gold stud bumps, Cree seems to be using some sort of eutectic which might further reduce the cost and maybe improve the thermal contacts. We’re still not seeing much standardisation.”

TV trouble’s lighting payoff

Before lighting, LCD TV backlighting was the last application to drive an expansion in LED sales. That expansion has been slower than many expected, creating excess supply of mid-power LEDs that TVs use. But it’s turned out to be a surprise boost for cost-of-ownership in illumination. “Mid-power LEDs are a fairly simple PLCC – plastic leaded chip carrier – package,” Virey said. “I don’t think initially anybody was thinking about using them in lighting, except for the linear fl uorescent replacements, which need a more distributed light from a multitude of sources that are not too bright individually. But those medium power LEDs have got into applications where people were previously only considering the high power LEDs, like light bulb replacements or downlights.”

That unintended benefi t shows how working to align products around a particular format can be advantageous, Virey added. “First of all for LED TVs, the dimension of the package was standardised,

which is fairly unusual in the LED industry,” he said. “This allowed better economy of scale. Because the LCD TV market was not as strong as anticipated and there have been vast amounts of capacity installed oversupply of those mid-power LEDs has led to further cost reduction. The $/lm fi gure of this type of package has become very compelling for some applications.”

Cost versus performance considerations also factor into whether LED manufacturers seek to satisfy customer preferences for quality of light. Desire for ‘warmer’ light is driving interest beyond yttrium aluminium garnet (YAG) phosphors that have become relatively uniformly used across the industry. Companies are looking to supplement YAG’s ability to create a cool white LED by converting some blue light produced by GaN emitters to yellow. “YAG and its silicate substitutes are still the phosphor kings – the combination of a blue chip plus YAG phosphor is still the number one type of package,” Virey underlined. “However, with the industry gearing more toward serving lighting, there is an increasing need for a high colour rendering index.”

To do this, they have added a red component in two ways. First, at the system level, manufacturers can add a red LED chip to a standard blue chip paired with a YAG phosphor. Cree uses this approach,

calling it ‘TrueWhite’ technology, Virey noted, as does Osram. Second, they can add phosphors that emit red light, which are typically nitride compounds. “It’s application driven, but for warm colors in high brightness LEDs, the production of these phosphors is very signifi cant,” Virey said. “The problem is that the nitride phosphors are still extremely expensive and very diffi cult to make. They are ten to twenty

Cutting edge: Cree has adopted fl ip-chip mounting and simple texturing of its SiC substrates with saws in its XB-D XLamp packages. (Cree- Xlamp® XB-D Cool White LED reverse costing

analysis, April 2012, System Plus Consulting)

I S S U E N ° 6 D E C E M B E R 2 0 1 2

“Until maybe a year ago, we were seeing a lot of effort toward improving performance, even at the expense of added complexity. Now, what we’ve observed in some cases has beena focus on ways to design cost reduction into their packaging,”Eric Virey said.

D E C E M B E R 2 0 1 2 I S S U E N ° 6

i L E D20

“They might manufacture high

performance devices using either fl ip-chip or vertical LEDs, but currently exporting these LEDs outside of China could be a challenge, because

they don’t havethe IP,”

Eriv Virey notes.

Phosphor materials timeline(Source: LED Phosphors report, October 2012,Yole Développement)

YAG

TAG

Yellow Silicates

Green Silicates

Sulfides (CaS)

Oxynitrides

Green Aluminate

Orange/Red Silicates

Nitrides

Quantum Dots?

Quantum Dots?

LuAG

Carbidonitrides?

Carbidonitrides?

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Into the pink: Nitride-based red phosphors have recently become important for delivering “warm white” LED lighting.

times more expensive in some cases than the YAG phosphor. To deliver yellow phosphors, if you have a licence from Nichia, you can use YAG. If you don’t have a licence from Nichia, you can use a silicate phosphor. But for the red, the market is dominated by Mitsubishi Chemical and its nitride phosphors.”

On board

Chip-on-board (COB) arrays are another way in which LED producers have been improving cost-of-ownership, said Virey’s colleague Pars Mukish. “COB proceeds by mounting LEDs as bare dies directly onto the PCB, which is traditionally FR4, ceramic, or metal core PCB, and equipping it with connectors,” he said. “This passes directly from the die level to the module level of the supply chain, skipping the stage where a packaged LED is made. Subsequent packaging assembly operations, such as adding lenses, the phosphor or ESD protection, are carried out at the PCB level.”

While skipping a step promises lower costs, currently there are fi nancial trade-offs, Mukish commented. “You have lower material costs, and high packaging densities,” he said. “The drawback is a higher assembly cost as they don’t benefi t signifi cantly from economies of scale at the moment.” However, COB also offers a number of technical advantages that translate to additional fi nancial benefi ts. “The benefi ts of this type of packaging technology centre on thermal management,” Mukish said. “You have fewer material interfaces at the packaging level

and a thinner material stack between the chip and heat sink. Another indirect advantage of the COB is that it uses small die, which has two benefi ts. First, manufacturing yields are higher. Second, because you have a multitude of small die, you also have some averaging effect which reduces the burden on the binning specifi cation. So properly designing a package indirectly reduces front end manufacturing cost.”

Power LED package formats are also being developed to use technical advantages to modify costs. “Traditional high brightness LEDs, the typical 1-3W package with one single die, are evolving from Al2O3 to AlN substrates,” Virey explained. “But it’s not completely systematic, because it’s a compromise between cost and performance. AlN is typically 7-10 times more expensive than Al2O3 at the material level. But because they deliver better thermal performance, the substrate can be much smaller. So if it’s four times more expensive on a per surface area basis, the total material cost might be just 2x.”

Adoption of AlN is another indication of a manufacturer’s preference for the cost and performance levers. “Major manufacturers of high brightness packages, like Philips Lumileds, Cree, and Osram, have been using AlN in pretty much all their high power LEDs,” Virey noted. “For Chinese companies I’m still seeing mostly Al2O3 rather than AlN, even for high brightness.” Virey adds that for Chinese LED companies, the cost/performance balance is driven largely by the fact that their focus has to be on the domestic market. “In terms of the

Eric Virey holds a Ph-D in Optoelectronics from the national Polytechnic Institute of Grenoble. In the last 12 years, he’s held various R&D, engineering, manufacturing and marketing positions with Saint-Gobain. Most recently, he was Market Manager at Saint-Gobain Crystals, in charge of Sapphire and Optoelectronic products.

Pars Mukish holds a master degree in Materials Science & Polymers (ITECH - France) and a master degree in Innovation & Technology Management (EM Lyon – France). He works at Yole Développement as Market and Technology Analyst in the fi elds of LED, Lighting Technologies and Compound Semiconductors to carry out technical, economic and marketing analysis. Previously, he has worked as Marketing Analyst and Techno-Economic Analyst for several years at the CEA (French Research Center).

I S S U E N ° 6 D E C E M B E R 2 0 1 2

chip structure, intellectual property is a challenge for these companies,” he said. “They might manufacture high performance devices using either fl ip-chip or vertical LEDs, but currently exporting these LEDs outside of China could be a challenge, because they don’t have the IP.”

Ultimately, even though $/lm has become the LED industry’s main focus, there’s a diverse set of approaches to delivering it. Beyond the different aspects of LED packaging that can even be seen in system designs, Virey underlined. “Bulb replacements are a good example of that,” he said. “We’re seeing them made with all kinds of packages, from mid-power to COB and high power LED.”

www.yole.fr

Hunting reds: Red phosphors, like these developed by Siemens and Osram, are becoming increasingly important in LED packages.