36

9/23/2015 1 Analyst Visit - Davidstow 22 & 23 September 2015 Dairy Crest update Mark Allen Chief Executive 22 September 2015

9/23/2015

1

Analyst Visit - Davidstow

22 & 23 September 2015

Dairy Crest update Mark Allen

Chief Executive

22 September 2015

9/23/2015

2

WE EXPECT THE SALE OF DAIRIES TO MULLER WILL COMPLETE IN 2015

No

vem

ber

20

14

Sale announced

Dec

emb

er 2

01

4

Shareholder approval received

Ap

ril 2

01

5

Dairies separated

26

Ju

ne

20

15

CMA consider undertakings by Muller

Au

gust

20

15

CMA indicates it proposes to accept undertakings

Deadline extended to October 2015

● CMA’s consultation now closed

● CMA hoping to reach decision before October

● We continue to anticipate the sale will complete in 2015

3

Transformational sale for Dairy Crest and wider Dairy sector

THE SALE OF DAIRIES WILL COMPLETE A 20 YEAR JOURNEY

● Cumulative losses* of £143 million since 2011

● Only partly offset by property profits of £48 million

● Cash outflow* since 2011 of £78 million

● £16 million trading loss in 2014/15

● No signs of markets improving

4

Dairy Crest’s Dairies performance has offset progress elsewhere in the business

*Including exceptional costs of restructuring, excluding property profits

19

96

- 2

00

6

Phase 1: Commodities

Floated as a supply driven business processing Britain’s surplus milk

20

06

- 2

01

4

Phase 2: Key brands

Increased focus on 4 key brands

Establish enviable track record of innovation

Consistent drive for cost savings

20

15

-

Phase 3: Profitable growth

Driven by increasingly strong brands & entry into fast-growing global markets

Well invested assets

Simple & efficient supply chain

Co

mm

ence

sa

le o

f

Dai

ries

Exit

co

mm

od

ity

ch

eese

9/23/2015

3

NEW DAIRY CREST

• A SIMPLE BUSINESS

• DELIVERING GROWTH

• GENERATING CASH

5

DAIRY CREST IS WELL POSITIONED FOR PROFITABLE AND SUSTAINABLE GROWTH

● Cheese and Spreads businesses have delivered long term profit growth despite

─ Volatile farmgate milk prices ─ Difficult food retail environment

● Simple, well-invested supply chains

● Margin 2014/15 > 15%

● High barriers to entry – cost to replicate cheese &

whey business alone around £500 million

● Potential for further growth – Greater focus after sale of Dairies

– Build on established brands – New revenue streams

– Growth through acquisitions

● Opportunity to further streamline overheads

6

9/23/2015

4

WITH A CLEAR STRATEGY TO IMPROVE RETURNS

OLD DAIRY CREST

To build market leading positions in branded and added value markets To focus on cost reduction and efficiency improvements To improve quality of earnings and reduce risk To make acquisitions and disposals where they will generate value

NEW DAIRY CREST

To generate growth by building strong positions in branded and added value markets

To simplify, make more resilient and reduce costs

To generate cash and reduce risk To make acquisitions where they will generate value

7

WITH A CLEAR STRATEGY TO IMPROVE RETURNS – TOP LINE GROWTH

A growing top line

•To generate growth by building strong positions in

branded and added

value markets

•Increase focus on innovation

Growing our key brands • Cathedral City • Clover • Country Life • Frylight

Cathedral City is the UK’s 16th largest brand with an impressive track record and an increasingly strong market share

IRI retail sales data to March 2015

9/23/2015

5

WITH A CLEAR STRATEGY TO IMPROVE RETURNS – TOP LINE GROWTH

A growing top line

•To generate growth by building strong positions in branded and added value markets

•Increase focus on

innovation

9

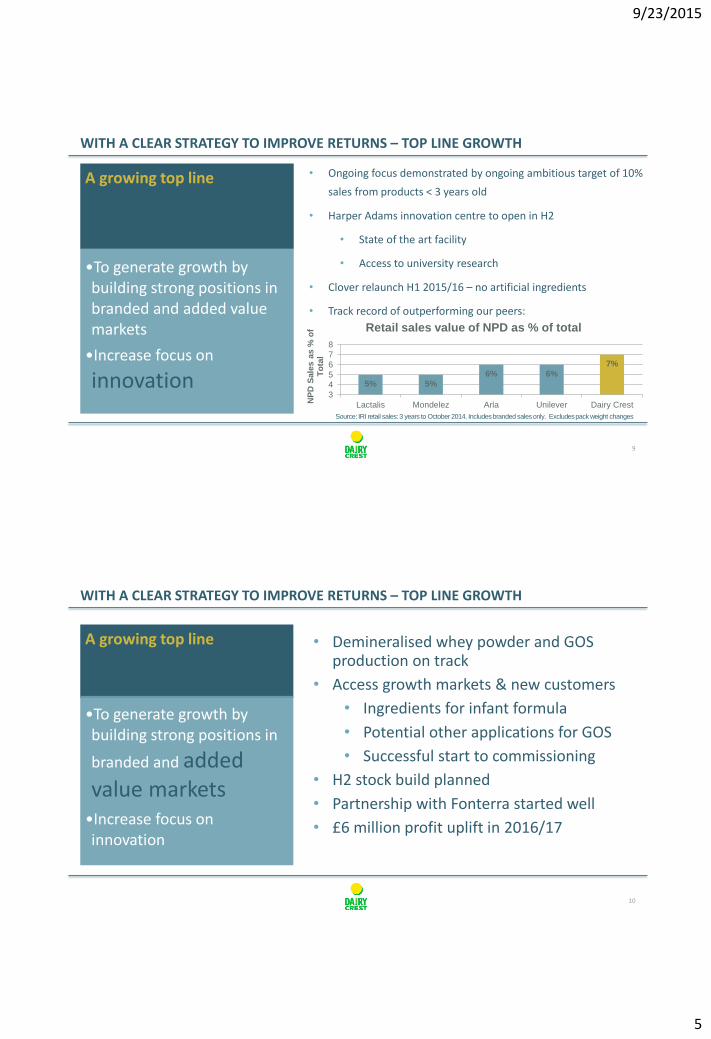

• Ongoing focus demonstrated by ongoing ambitious target of 10%

sales from products < 3 years old

• Harper Adams innovation centre to open in H2

• State of the art facility

• Access to university research

• Clover relaunch H1 2015/16 – no artificial ingredients

• Track record of outperforming our peers:

5% 5%

6% 6%

7%

3

4

5

6

7

8

Lactalis Mondelez Arla Unilever Dairy CrestNP

D S

ale

s a

s %

of

To

tal

Retail sales value of NPD as % of total

Source: IRI retail sales: 3 years to October 2014. Includes branded sales only. Excludes pack weight changes

WITH A CLEAR STRATEGY TO IMPROVE RETURNS – TOP LINE GROWTH

A growing top line

•To generate growth by building strong positions in

branded and added value markets

•Increase focus on innovation

10

• Demineralised whey powder and GOS production on track

• Access growth markets & new customers

• Ingredients for infant formula

• Potential other applications for GOS

• Successful start to commissioning

• H2 stock build planned

• Partnership with Fonterra started well

• £6 million profit uplift in 2016/17

9/23/2015

6

WITH A CLEAR STRATEGY TO IMPROVE RETURNS – MAINTAIN FOCUS ON COSTS

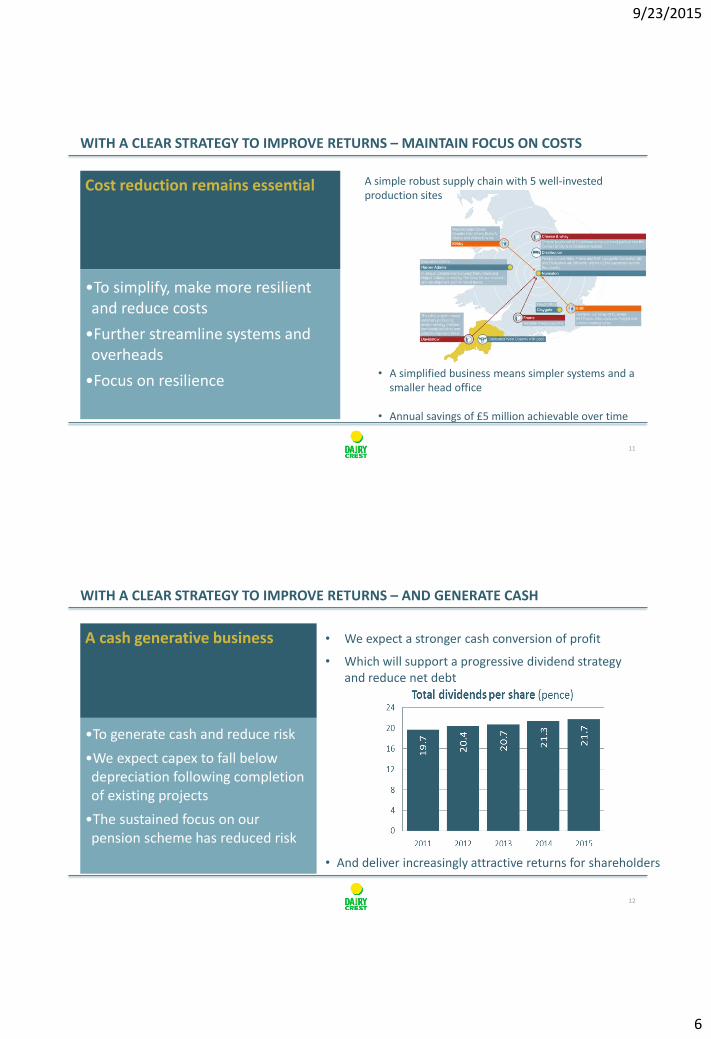

Cost reduction remains essential

•To simplify, make more resilient and reduce costs

•Further streamline systems and overheads

•Focus on resilience

11

A simple robust supply chain with 5 well-invested production sites

• A simplified business means simpler systems and a smaller head office

• Annual savings of £5 million achievable over time

WITH A CLEAR STRATEGY TO IMPROVE RETURNS – AND GENERATE CASH

A cash generative business

•To generate cash and reduce risk

•We expect capex to fall below depreciation following completion of existing projects

•The sustained focus on our pension scheme has reduced risk

12

• We expect a stronger cash conversion of profit

• Which will support a progressive dividend strategy and reduce net debt

• And deliver increasingly attractive returns for shareholders

9/23/2015

7

WITH A CLEAR STRATEGY TO IMPROVE RETURNS

Acquisitions contribute to growth

•To make acquisitions where they will generate value

•We will still seek appropriate acquisitions to supplement organic growth

•We have a strong track record of making acquisitions – and making those acquisitions work

Mendip Foods – Cathedral City

MH Foods – Frylight

St Hubert – £90 million profit

•Any acquisitions we do make will have to meet strict criteria

13

• Unlikely to make major acquisitions in the near future

• Focus on smaller acquisitions such as MH Foods • Only with a compelling strategic or synergistic

rationale

DAIRY CREST WELL POSITIONED FOR PROFITABLE AND SUSTAINABLE GROWTH - SUMMARY

14

● Complete sale of Dairies as soon as possible – 26 December 2015 at latest

● New Dairy Crest

● Increased focus

● Well-invested

● Established brands with track record of innovation

● New revenue streams from high growth markets

● Proven track record on costs

● Improved cash conversion providing attractive opportunities

● Interims announcement 5 November 2015

9/23/2015

8

Trading update Tom Atherton

Group Finance Director

22 September 2015

H1 – Ongoing deflation

● World, European and UK dairy markets have seen substantial deflation

● Reflected in farmgate milk prices

– Davidstow -25% v 1 yr ago

– Liquid -26% vs 1 yr ago

Source: DairyCo – July 2015 v July 2014

● Cost of sales yet to fully reflect this due to maturity profile of cheese

● Also reflected in lower whey returns

16

-

1,000

2,000

3,000

4,000

5,000

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

European dairy commodity prices - September 2012 - August 2015

Butter € / tonne

Skimmed milk powder € / tonne

Whey powder € / tonne

Source: DairyCo

9/23/2015

9

We expect brand performance similar to Q1

17

Volume Value

Cathedral City

Clover

Country Life

Frylight

● Overall key brand sales flat in a deflationary market

● Cathedral City and Frylight performing strongly

● Tougher going for Clover and Country Life

● New ‘nothing artificial’ Clover expected to improve H2 performance

Anticipated key brand growth H1 2015/16

FINANCIAL POSITION

18

9/23/2015

10

Dairies operations expected to be ‘discontinued’ at half year

19

● Expect Dairies sale to complete in H2

● Results of Dairies expected to be reported as discontinued in Interims

– Dairies numbers stripped out of revenue, cost of sales and profit from continuing operations and comparatives restated

– Post tax result of Dairies at foot of income statement

– Assets and liabilities at 30 September “held for sale” on balance sheet

– Dairies cash flows shown separately

● Remaining business continues as one segment

● We will continue to voluntarily disclose revenue and profits by product group (cheese and spreads)

Cheese stock accounting

Tom Atherton

Finance Director

22 September 2015

9/23/2015

11

MARGINS IN CHEESE BUSINESS REFLECT FUNDAMENTALS

● Sales volumes/mix

● Selling prices

● Milk purchase prices

● Milk yields

● Conversion costs including packing and packaging

● Profits from by-products

● Marketing expenditure

● Overheads

Reported profits also reflect timing differences between:

● Milk purchase price changes

● Selling price changes

● Cheese maturation periods

21

KEY POINTS

● Cost of milk represents the majority of the cost of cheese production

● Cheese matures for on average c12 months

● Cheese produced today held in stock on the balance sheet at cost until sold

● Cheese selling prices reflect market conditions/cost of manufacture today

● BUT – when cheese sold it comes out of stock and into P&L at historic cost

● ie Cost of Sales in P&L reflects cost of cheese when it was made NOT what it would cost to make today (being the replacement or cash cost)

● Therefore differences between reported margins and cash margins – the balancing element being movement in cheese stock value on balance sheet

22

9/23/2015

12

4 ILLUSTRATIVE EXAMPLES

The following 4 charts are theoretical examples which illustrate the mechanics of

cheese stock accounting

23

ILLUSTRATIVE EXAMPLE 1 – STEADY STATE

24

0

500

1000

1500

2000

2500

3000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

Year 1 Year 2 Year 3

Flat selling prices and milk purchase prices 100,000 tonnes pa Margin £500/tonne

Sales (£/tonne) Milk cost (£/tonne) Cost of sales (£/tonne)

Reported Gross margin (£ million)

H1 H2 H1 H2 H1 H2

25 25 25 25 25 25 Cash margin (£ million)

25 25 25 25 25 25

Stock value (£ million)

200 200 200 200 200 200

9/23/2015

13

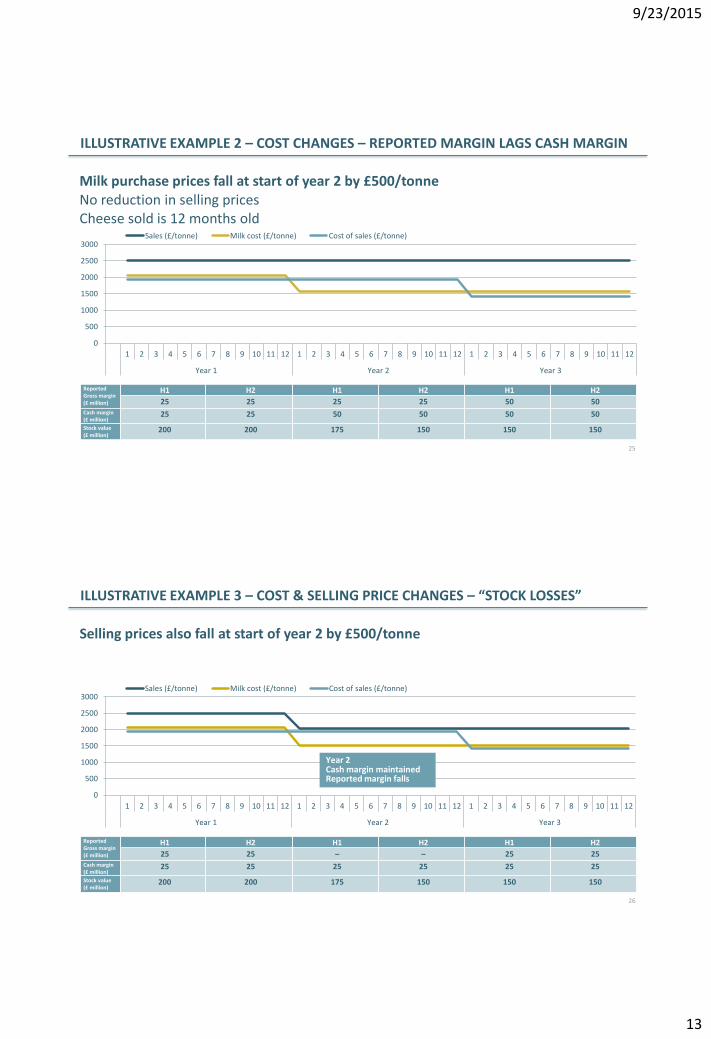

ILLUSTRATIVE EXAMPLE 2 – COST CHANGES – REPORTED MARGIN LAGS CASH MARGIN

25

Reported Gross margin (£ million)

H1 H2 H1 H2 H1 H2

25 25 25 25 50 50 Cash margin (£ million)

25 25 50 50 50 50

Stock value (£ million)

200 200 175 150 150 150

0

500

1000

1500

2000

2500

3000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

Year 1 Year 2 Year 3

Milk purchase prices fall at start of year 2 by £500/tonne No reduction in selling prices Cheese sold is 12 months old

Sales (£/tonne) Milk cost (£/tonne) Cost of sales (£/tonne)

0

500

1000

1500

2000

2500

3000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

Year 1 Year 2 Year 3

Selling prices also fall at start of year 2 by £500/tonne

Sales (£/tonne) Milk cost (£/tonne) Cost of sales (£/tonne)

ILLUSTRATIVE EXAMPLE 3 – COST & SELLING PRICE CHANGES – “STOCK LOSSES”

26

Year 2 Cash margin maintained Reported margin falls

Reported Gross margin (£ million)

H1 H2 H1 H2 H1 H2

25 25 – – 25 25 Cash margin (£ million)

25 25 25 25 25 25

Stock value (£ million)

200 200 175 150 150 150

9/23/2015

14

ILLUSTRATIVE EXAMPLE 4

27

Reported Gross margin (£ million)

H1 H2 H1 H2 H1 H2 H1 H2

25 25 12.5 12.5 – 25

Cash margin (£ million)

25 25 25 37.5 25 25

Stock value (£ million)

200 200 200 175 150 150

0

500

1000

1500

2000

2500

3000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

Year 0 Year 1 Year 2 Year 3

A more complicated scenario Milk purchase prices increase halfway through year 0 then fall at start of year 1 and halfway through year 2 Selling price reduction in year 2 lags milk price reduction by 3 months

Sales (£/tonne) Milk cost (£/tonne) Cost of sales (£/tonne)

28

P&L Stock valuation

Milk input cost inflation

Reported margin increase as selling price increases sought before full impact of higher cost milk impacts cost of sales “Stock gain”

Increases Older cheese gets sold and replaced with new cheese made with more expensive milk

Milk input cost deflation

Reported margin decrease as selling price deflation given before beneficial impact of lower milk costs fully comes through cost of sales “Stock loss”

Decreases Older, more expensive cheese sold and replaced with new cheese made with cheaper milk

9/23/2015

15

SUMMARY

● Dairy Crest manages Cheese business on a ‘cash margin over milk’ basis

This improves in line with:

– Brand strength

– Operational efficiencies

– Value added by-products

● In periods of deflation reported gross margins can disguise the good progress we are making

29

Generating growth by building strong positions in cheese and infant formula ingredients

Richard Jones Managing Director - Functional Ingredients

Mike Barrington Supply Chain Director

23 September 2015

9/23/2015

16

DAVIDSTOW – KEY TO OUR GROWTH ASPIRATIONS

● Davidstow - state of the art cheddar manufacturing facility

● Home to market-leading Cathedral City

● High quality whey stream - historically sold to food manufacturers

● Dedicated milk pool assists our products to command a premium

– Short supply chain

– Robust traceability

● Investment to produce ingredients for infant formula

– Growing world demand

– Demineralised whey

– Galacto-oligosaccharide (GOS)

● New sales channel for Dairy Crest

● Strategic partnership established with Fonterra instead of investing in an international sales force

31

STATE OF THE ART MANUFACTURING PLANT

● Davidstow today:

– 65 years of high quality cheese making

– 48k tonnes cheddar, 26k tonnes whey powder

– Around 100 employees

– 365 days/24 hour production

– Accredited to internationally recognised standards

32

9/23/2015

17

DAVIDSTOW: SETTING THE STANDARD FOR QUALITY IN BOTH CHEESE AND WHEY

● Awarded The Danisco Prize for The Supreme Champion – 12 times in the last 14 years!

● May 2014 Consumer Watchdog rated ‘Davidstow 3 year Reserve’ best buy in consumer taste tests

● Davidstow sweet whey powder is recognised for high quality and is bought by a number of leading confectionery companies as a key ingredient for chocolate production

33

DAVIDSTOW HAS A LONG HISTORY OF QUALITY MANUFACTURING

34

In the 1950’s developed by Cow & Gate…

In the 1970’s as part of the MMB (Milk Marketing Board)…

In the 1980’s as Dairy Crest…

As it expands in 2014…

9/23/2015

18

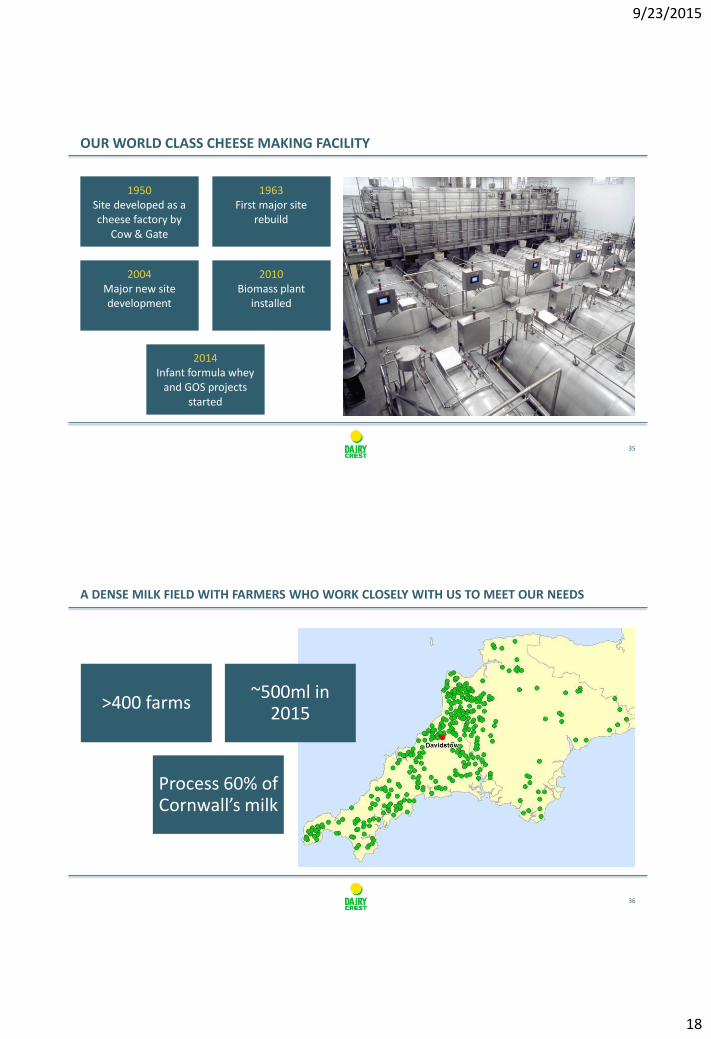

OUR WORLD CLASS CHEESE MAKING FACILITY

35

1950 Site developed as a cheese factory by

Cow & Gate

1963 First major site

rebuild

2004 Major new site development

2010 Biomass plant

installed

2014 Infant formula whey

and GOS projects started

A DENSE MILK FIELD WITH FARMERS WHO WORK CLOSELY WITH US TO MEET OUR NEEDS

36

>400 farms ~500ml in

2015

Process 60% of Cornwall’s milk

9/23/2015

19

CHEESE PROCESS OVERVIEW

37

Milk

Pasteurisation

Curd making

Cheddaring

Salting

Final pressing

Packing and Maturation

Cheese

WHAT IS INFANT FORMULA?

● Infant formula is made from a mixture of dairy and other ingredients and is designed to mimic human milk as closely as possible

● Although it is made to a common international codex, formulation ingredients vary

● Key common ingredients are: Water, Skim Milk Powder, Lactose, Vegetable Oils, Whey Protein and Galacto-oligosaccharide (GOS)

● Different brands, for example, Abbott Similac and Nestle NAN HA Gold 2 infant formula then have up to an additional 40 ingredients which together make up <2% of total ingredients

38

9/23/2015

20

PAEDIATRIC CATEGORY IS WORTH $50bn WITH STRONG GLOBAL GROWTH FORECAST

39

CAGR 13:23

15%

17%

12%

4%

6%

5%

Source: Euromonitor Milk Formula Market, updated to 2013, 2023 is projected based on current CAGR’s Projected CAGR ‘13-’23: +12.4% value; +6.6% volume. Paediatric category includes all baby food and drinks

Fonterra focus geographies

CAGR +12%

DEMINERALISED WHEY POWDER & GOS ARE BOTH PRIMARILY SOURCED FROM WHEY

40

Whey

Solids 6.6%

Water 93.4%

Fat 0.1%

Solids Non Fat 6.5%

Protein 0.8%

Curds Cheese

Whole Milk

Lactose 4.8%

Minerals 0.9%

Demineralised whey powder contains lactose and whey protein

Lactose is mixed with a proprietary enzyme to produce GOS

9/23/2015

21

WHAT DOES GALACTO-OLIGOSACCHARIDE (GOS) DO?

● GOS is a prebiotic i.e. non digestible fibres that stimulate the growth of specific, healthy bacteria in the digestive system

41

1 Prebiotics contained in foods or supplements

are consumed

2 Prebiotics are not

digested in the stomach or small intestine

3 Prebiotics remain intact until they pass into the

large bowel

4 Prebiotics are used as

food by beneficial bacteria in the large

intestine

5 Increased beneficial bacteria in the large intestine lead to a

variety of health effects

GOS IS ADDED TO INFANT FORMULA TO BETTER MATCH HUMAN MILK

42

● GOS is readily available in human milk but not in that of cows

● Health promoting benefits

– Inhibition of the growth of harmful bacteria

– Stimulation of immune functions

– Absorption of essential nutrients

– Synthesis of certain vitamins

Oligosaccharides: Less than 0.1%

9/23/2015

22

GOS HAS OTHER POTENTIAL APPLICATIONS

● There are potential applications for GOS in markets other than infant formula

● These markets include adult human nutrition, animal feed and pharmaceuticals

● GOS can play a role in all of these areas by improving gut health

● We are investigating some of these application areas with partners including commercial contacts and academic institutions

● At an early stage of laboratory trials – encouraging results to date

43

DAVIDSTOW PROJECT – SUMMARY

● The project was approved in November 2013 and comprises three main elements plus other essential site infrastructure projects:

– Demineralised whey (D90) manufacture

– Galacto-oligosaccharide (GOS) manufacture

– Enabling projects (waste water treatment plant

and a new site laboratory)

– Related investments (e.g. fire protection)

● The demineralised whey process plant has the capability to produce c 30,000 tonnes per annum of 90% demineralised whey powder (D90)

● The GOS Process Plant will be capable of manufacturing 13,500 tonnes per annum with further capacity expansion if required

● We are currently in the commissioning phase for D90 and GOS and plan to move to production ramp up in the next few weeks

44

9/23/2015

23

DEMINERALISED WHEY (D90)

● The scope of the Demineralised Whey Project is to upgrade the existing Sweet Whey plant, in order to produce Demineralised Whey Powder (D90) for sale to the global infant formula market

● The plant will have the capacity to process 80 tonnes of D90 per day and the process will incorporate high levels of care, consistent with production of infant formula

● The main components of the project are:

– A new demineralisation process

– Modifications to the existing sweet whey powder operations

– New packing facilities

– An upgraded waste water treatment plant

– A new laboratory

● We are currently in the commissioning phase and plan to move to production ramp up over the next few weeks

45

DEMINERALISED WHEY (D90) PROCESS OVERVIEW

46

Milk

Cheese

Whey, the by-product of cheese

manufacture

Separation

Demineralisation

Remove 90% of minerals = D90

Evaporation

Drying

Packing operations

Demineralised Whey finished

product

9/23/2015

24

GALACTO-OLIGOSACCHARIDE (GOS)

● This project is to build a new processing plant to enable Dairy Crest to produce GOS

● The plant will initially have the capacity to produce 13.5 k tonnes pa of infant formula GOS syrup per annum

● Modular build can grow capacity to 30,000 tonnes

● The new plant will be capable of producing GOS syrup at 57% polymer level which is the level required for use as an infant formula nutritional ingredient

● This plant is completely independent of the cheese manufacturing process

● Timetable in line with D90 47

GOS PROCESS OVERVIEW

48

Lactose + Hot Water

Dissolving Process

Reaction Tanks

Enzymatic Reaction Carbon Removalon / Filtration stages

Four stage Evaporation &

Cooling

GOS finished product

9/23/2015

25

FURTHER IMPROVEMENTS TO DAVIDSTOW - WASTE WATER TREATMENT PLANT

● The demineralised whey powder & GOS processes will double the volume and loadings of organic waste to the waste water treatment plant

● To meet Dairy Crest’s environmental aims, the existing waste water treatment plant has been upgraded and extended to install a water recovery system, which will process up to 1.7m litres (50% of total flow) per day of waste water into process water

49

FURTHER IMPROVEMNTS TO DAVIDSTOW - LABORATORY FACILITIES

● In support of the D90 and GOS projects we have a new laboratory

● The laboratory will also handle the testing requirements of the existing Cheese process

● Laboratory fully operational on existing chemistry testing and GOS polymer analysis

● The first parts of ISO 22000 and external CLAS accreditation were passed during June 2015

● We expect to bring external micro testing “in-house” by end of 2015

50

9/23/2015

26

PROJECT UPDATE

● The project is now reaching a key phase of activity as it moves from installation through to manufacture

● Fonterra have been involved in reviewing the design of the plant and are providing on-going technical and commissioning assistance, including a number of individuals seconded from NZ who are based in Davidstow during this period of time

● The focus is firmly on how we commission and commercialise the investments and we have a highly experienced commissioning team in place to deal with this

● Commissioning is just one of 11 work streams which are being driven through an operational readiness programme in order to ensure that all activities are aligned in order to meet the start up criteria

● The site’s behavioural programme “We are Davidstow” is being led by the Davidstow Site Director to ensure that we make the required “mind set” cultural change in relation to the production of Infant Formula

● The teams are firmly focused on creating a facility, in addition to our world-class cheese process, that we can be proud of and that serves the business and our customers well in the years ahead

51

IN PARTNERSHIP WITH FONTERRA AND FAYREFIELD

● World’s largest dairy exporter

– Over 40% of the global dairy trade and a turnover in excess of £10bn

– New Zealand based co-operative with more than 10k farmers who process 23bn litres of milk p.a.

– Responsible for sales and marketing of GOS and demineralised whey to the global Infant Formula industry

● UK’s largest independent dairy trading company

– £250m sales p.a.

– Specialists in dairy and healthy eating products

– Internationally recognised experts in food innovation

– 3 UK sites and international presence

– Providing technical expertise and access to patented enzyme technology

52

9/23/2015

27

WE FOLLOWED A RIGOROUS PROCESS IN SELECTING FONTERRA

53

Contract was signed with Fonterra in July 2014 for a 5 year period (from start of production) for global marketing and sales of demineralised whey and GOS for infant formula and food use

At final selection stage Fonterra’s proposal illustrated a strong fit with our strategy and a joint desire to maximise the potential of our products over the longer-term

Assessed a number of key criteria e.g. sales and marketing capability/reach, manufacturing experience, technical expertise, regulatory support

Conducted a strategic partner tender process with 5 key players

In contact with all the relevant major dairy players

THE DAIRY CREST/FONTERRA PARTNERSHIP IS PROGRESSING WELL

● With prebiotics and digestive health featuring in many new product launches, GOS and D90 are key to Fonterra’s paediatric portfolio

● Fonterra is actively engaging with global, Far Eastern and European companies to drive the sales pipeline

● Fonterra has provided regulatory support to influence emerging legislation

● Fonterra is providing commissioning and technical support on site at Davidstow

● We have a joint team working on new product development

54

9/23/2015

28

EXPECTED RETURNS FROM BOTH INVESTMENTS IN LINE WITH INITIAL ASSUMPTIONS

● Demineralised whey powder increases returns over sweet whey by c£5 million (EBITDA £9m)

– Whey powder and demineralised whey powder prices under pressure but differential remains

● GOS is a new venture

– markets less developed

– £0.5 million PBT increase (EBITDA £2.5m)

– applications other than infant formula have potential to increase returns

55

SUMMARY

● Exciting investment to enter new growing markets

● Pleased with choice of partners to market and sell our new products

● Returns on this investment are in line with initial forecasts

● On track to deliver full year uplift in 2016/17

56

Another step which

generates growth by

building strong

positions

in branded and added

value markets in line

with our strategy

9/23/2015

29

Cathedral City – A World Class Brand Adam Braithwaite

Group Commercial Director

23 September 2015

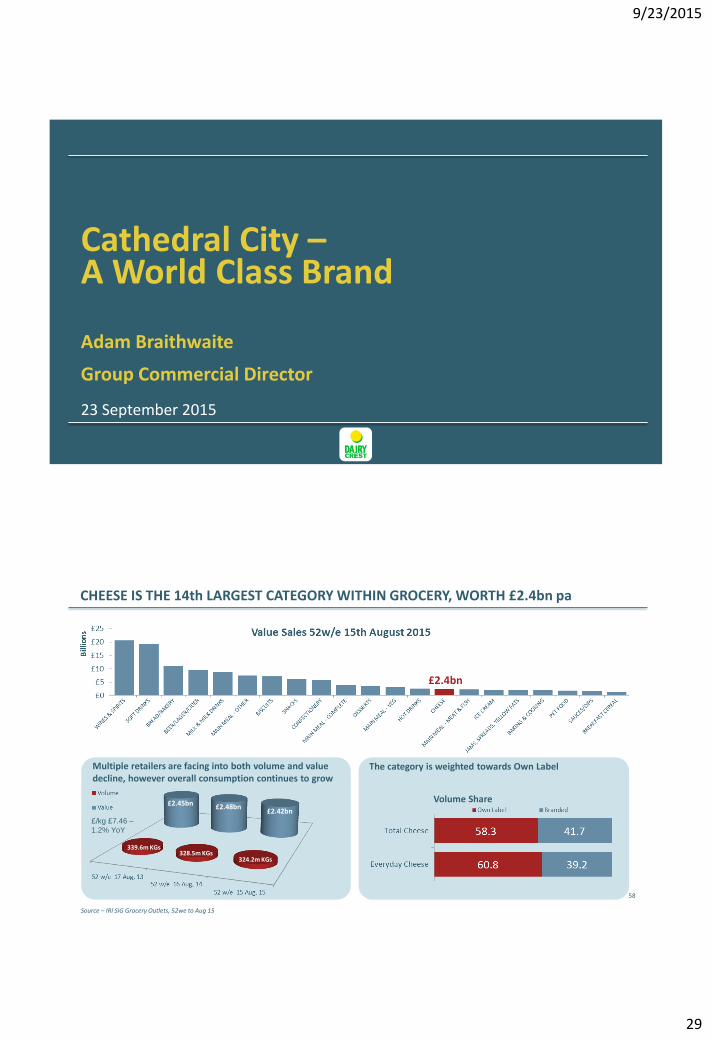

CHEESE IS THE 14th LARGEST CATEGORY WITHIN GROCERY, WORTH £2.4bn pa

£/kg £7.46 –

1.2% YoY

The category is weighted towards Own Label

58

£2.4bn

339.6m KGs 328.5m KGs

324.2m KGs

£2.45bn £2.48bn £2.42bn

Volume Share

Multiple retailers are facing into both volume and value decline, however overall consumption continues to grow

Source – IRI SIG Grocery Outlets, 52we to Aug 15

9/23/2015

30

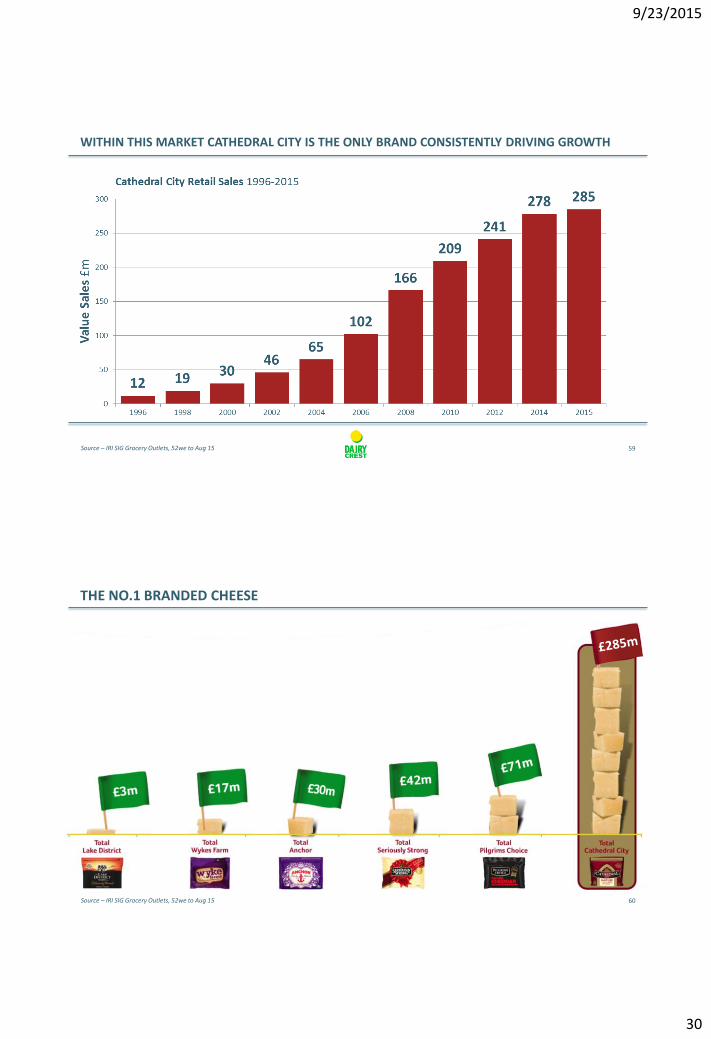

WITHIN THIS MARKET CATHEDRAL CITY IS THE ONLY BRAND CONSISTENTLY DRIVING GROWTH

59 Source – IRI SIG Grocery Outlets, 52we to Aug 15

THE NO.1 BRANDED CHEESE

60 Source – IRI SIG Grocery Outlets, 52we to Aug 15

9/23/2015

31

…AND NOW

● The 16th largest grocery brand in the UK, and the 7th largest online brand

61 Source: The Grocer ‘Top 100 Brands’ & CheckoutSmart ‘Top 100 Online Brands’ June 2015

WITH ONE OF THE STRONGEST PENETRATIONS OF GROCERY BRANDS

62

More than half of UK households buy

Cathedral City

58.4%

Source – Kantar WPO, Penetration, data to 29 Aug 2015

9/23/2015

32

WE COMMAND A PREMIUM TO OWN LABEL AND ADD VALUE TO THE OVERALL CATEGORY

● Cathedral City pricing stands at +19% v Retail Own Label EDC

63

● Our promotions drive stronger incremental category sales than competitors

● Category volume % uplifts are 3-4 times higher when Cathedral City is promoted vs. other branded packs, generating higher uplifts for the category at every stage

CATHEDRAL CITY ALSO LEADS THE CONTRIBUTION TO CATEGORY NPD

64 Source: Branded NPD, 3yrs to June ‘15, IRI Total Grocery Outlets

(Anchor £38.6m)

30% of all Branded Cheese NPD in last 3 years

(Philadelphia £21m)

9/23/2015

33

OUR SUCCESS IS BUILT ON 4 KEY FOUNDATIONS

65

Consistent Consumer Communication

Consumer Understanding

Product & Packaging Innovation

World Class Supply Chain & Consistent Quality

A WORLD CLASS SUPPLY CHAIN

66

Dedicated farms & farmers Around 400 local dairy farmers supply milk

Davidstow Creamery Rebuilt in 2004, Davidstow is Europe’s leading mature cheddar creamery

Prize winning cheese Dairy Crest holds around £130 million maturing cheese stocks

Optimum packing The packing hall at Nuneaton was built in 2009 with technology from around the world

9/23/2015

34

WE UNDERSTAND THE CONSUMER AND WHERE FUTURE CATEGORY GROWTH WILL COME FROM

67

Dairy for Life is a category strategy that is based on increasing consumption through changing consumer and shopper behaviour.

Reigniting consumers love for block and

spreadable cheese. Celebrating its

versatility and worth

Removing the health barriers that prevent

people giving themselves permission to buy and

consumer cheese

Drive the unparalleled desire for cheese

pleasure moments, exploring and

discovering cheese

Cheese is the kitchen’s friend – its versatility

helps make an ordinary meal more appealing

and tasty

Drive the relevance for cheese in snacking both in home and on the go,

for kids and adults

WHICH DRIVES OUR INNOVATIVE CULTURE (Over 70% of growth has come from new products)

68

Other block Snacking Spreadable Baked Bites

Lighter Kids Adult

Launch Date 2008 2011 2012 2014 2014

2015 Retail Sales £27m £8m £7m £2m £4m

Mature block

Other block

Sliced/grated

Snacking Spreadable Baked Bites

150.0

170.0

190.0

210.0

230.0

250.0

270.0

290.0

An

nu

al R

eta

il Sa

les

£m

illio

n

£166m

£285m

2008 2015

9/23/2015

35

SUPPORTED BY CONSISTENT PACKAGING INNOVATION

●We have come a long way since 1996

●First brand with recloseable packaging – Convenient – Branding

●And now easy opening

69

AND CONSISTENT MEDIA INVESTMENT

70

Advert from 1994 Our most recent

9/23/2015

36

LOOKING FORWARD, WE ARE NOT GOING TO CHANGE A WINNING MODEL

● Continue doing what we do well;

– Operational excellence, delivering outstanding quality

– Identify consumer needs and usage occasions

– Innovation – product & packaging

– Marketing & communication investment

– Price positioning & POP activity that drives overall category value

● Complemented by new opportunities

– Cathedral City: only 12% of total UK retail cheese

– Relevant export markets & partners

– Complementary category/product partnerships

71

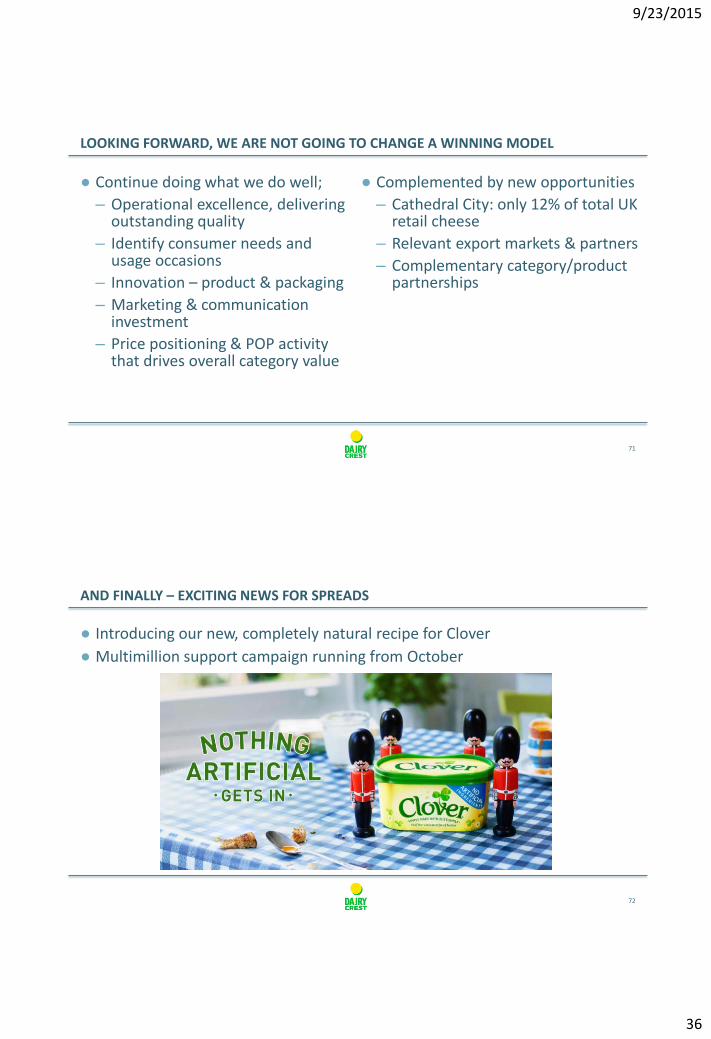

AND FINALLY – EXCITING NEWS FOR SPREADS

● Introducing our new, completely natural recipe for Clover

● Multimillion support campaign running from October

72