Analyzing Cyber Incidents from a Risk Assessment Perspective Jay P. Kesan, Ph.D., J.D. Professor and H. Ross & Helen Workman Research Scholar University of Illinois at Urbana-Champaign All work on SSRN, http://www.ssrn.com

Transcript

Analyzing Cyber Incidents from a Risk Assessment Perspective

Jay P. Kesan, Ph.D., J.D.Professor and H. Ross & Helen Workman Research Scholar

University of Illinois at Urbana-ChampaignAll work on SSRN, http://www.ssrn.com

Cybersecurity Concern• Cybersecurity is tied to the health of the U.S. economy. Malicious

cyberattacks could throw the financial industry into chaos.• The World Economic Forum estimates that ineffective cybersecurity may cost the

world’s economy as much as $3 trillion by 2020.• Cybersecurity is also national security. Critical infrastructure systems, from

transportation to nuclear power, are vulnerable to cyberattacks.• Hospitals and police departments have been targeted with ransomware that severs

access to vital information. • The primary focus of our work is the private sector and on improving cyber

security in the private sector through market-oriented solutions.• Proper risk assessment and management can improve companies’

resilience against cyber risks through market-based solutions

Data Description and Methodology

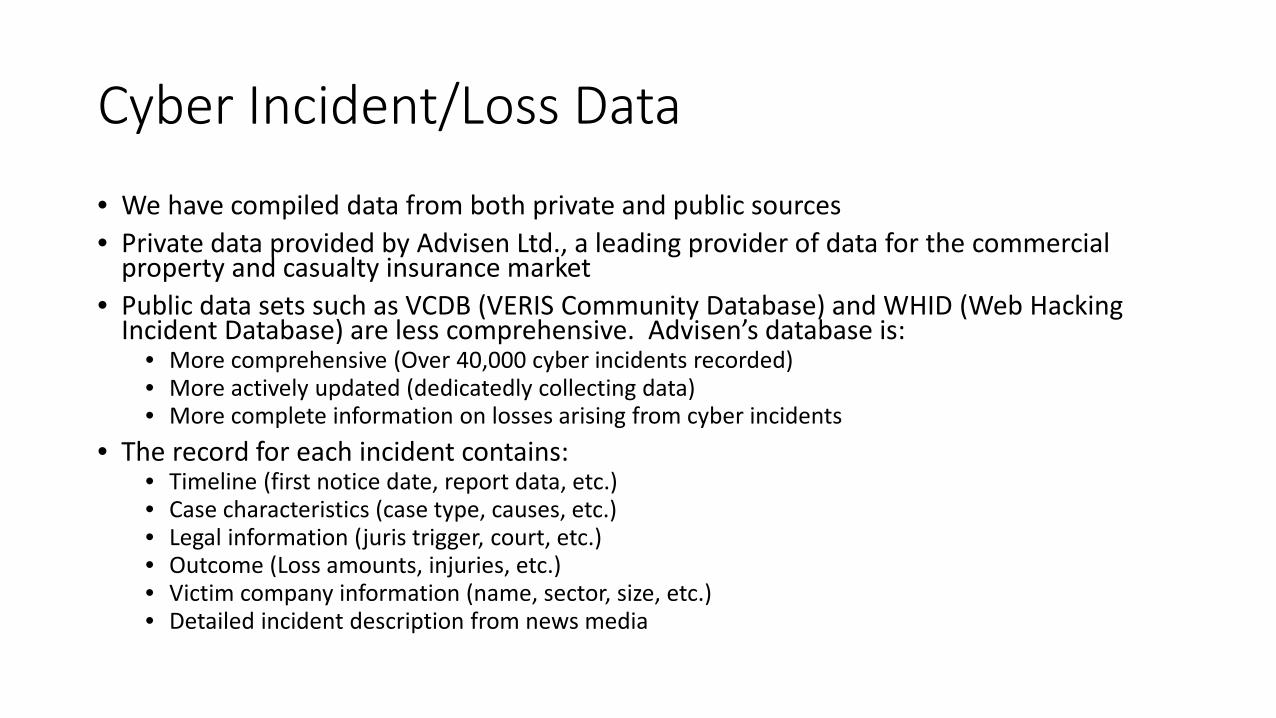

Cyber Incident/Loss Data

• We have compiled data from both private and public sources • Private data provided by Advisen Ltd., a leading provider of data for the commercial

property and casualty insurance market• Public data sets such as VCDB (VERIS Community Database) and WHID (Web Hacking

Incident Database) are less comprehensive. Advisen’s database is:• More comprehensive (Over 40,000 cyber incidents recorded)• More actively updated (dedicatedly collecting data)• More complete information on losses arising from cyber incidents

• The record for each incident contains:• Timeline (first notice date, report data, etc.)• Case characteristics (case type, causes, etc.) • Legal information (juris trigger, court, etc.) • Outcome (Loss amounts, injuries, etc.)• Victim company information (name, sector, size, etc.)• Detailed incident description from news media

Combining Cyber Incident Data with Company Financial Data• We link Advisen’s data with CompuStat, a database widely used in

corporate finance analysis• Over 1000+ companies from both databases are matched• Few studies try to explore the relation between cyber incidents and the

fundamentals of victim companies • With the combined data, we are able to study a number of interesting

research questions, such as: • What corporate financial factors affect the frequency of cyber incidents?• Does it matter how a company is positioned at the time of a cyber incident?• How big is the impact of cyber incidents on companies?• What are the types of impact – change in stock prices, loss of reputation, etc…

Cyber Risk and Incidents

Cyber Risk Overview

• We use a broad definition of cyber risk, which includes not only attacks performed by malicious actors, but also unintentional actions that relate to information systems and cause damage to an organization.

• e.g., Gitlab’s massive data loss in February

• Advisen’s dataset has 15 cyber incident categories based on incident cause:

1. Cyber Extortion 9. IT - Configuration/Implementation Errors2. Data - Malicious Breach 10. IT - Processing Errors3. Data - Physically Lost or Stolen 11. Network/Website Disruption4. Data - Unintentional Disclosure 12. Phishing, Spoofing, Social Engineering5. Denial of Service (DDOS)/System Disruption 13. Privacy - Unauthorized Contact or Disclosure6. Digital Breach/Identity Theft 14. Privacy - Unauthorized Data Collection7. Identity - Fraudulent Use/Account Access 15. Skimming, Physical Tampering8. Industrial Controls & Operations

Cyber Risk Overview (cont.)

0

1000

2000

3000

4000

5000

6000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cyber incident Affected company

Cyber risk is a growing concern for companies and organizations

During the 10-year period from 2005 to 2014:1. Number of incidents have grown by

24.4% each year2. Number of affected companies have

increased by 22.5% each year 3. Incident/Company ratio has

increased from 1.37 in 2005 to 1.59 in 2014, indicating that some companies are becoming more frequently affected by cyber incidents

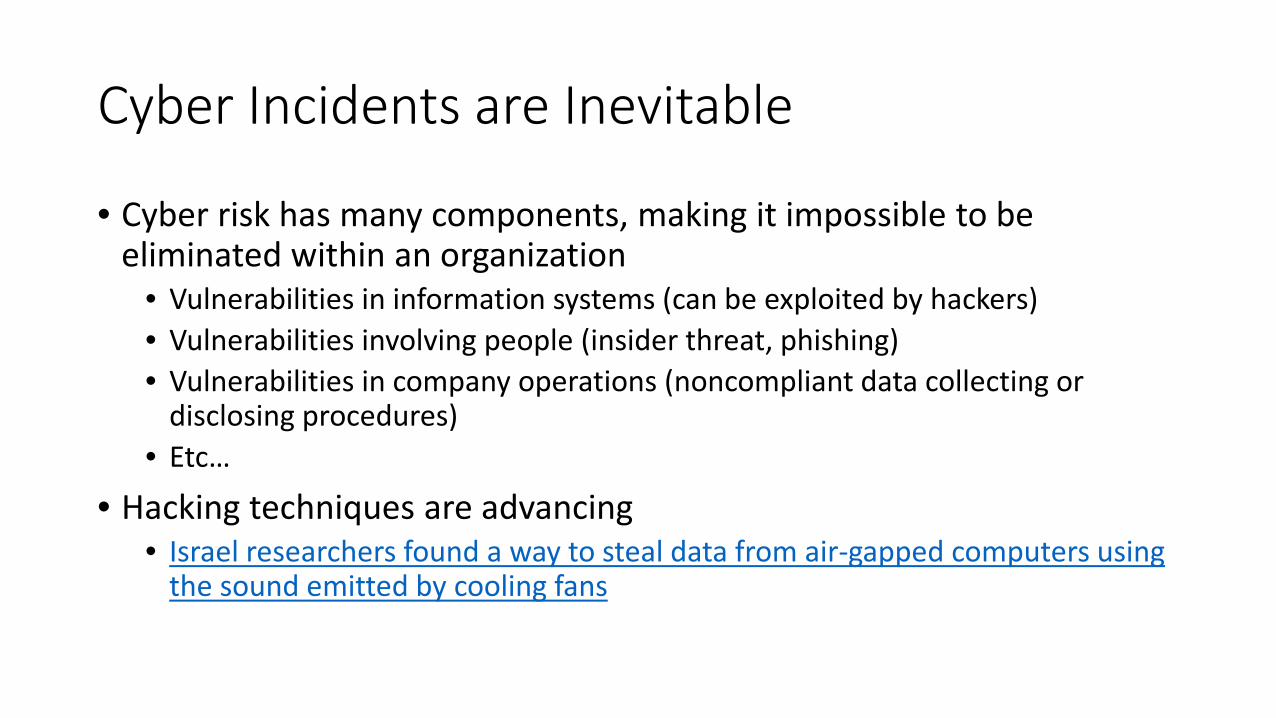

Cyber Incidents are Inevitable

• Cyber risk has many components, making it impossible to be eliminated within an organization

• Vulnerabilities in information systems (can be exploited by hackers)• Vulnerabilities involving people (insider threat, phishing)• Vulnerabilities in company operations (noncompliant data collecting or

disclosing procedures)• Etc…

• Hacking techniques are advancing• Israel researchers found a way to steal data from air-gapped computers using

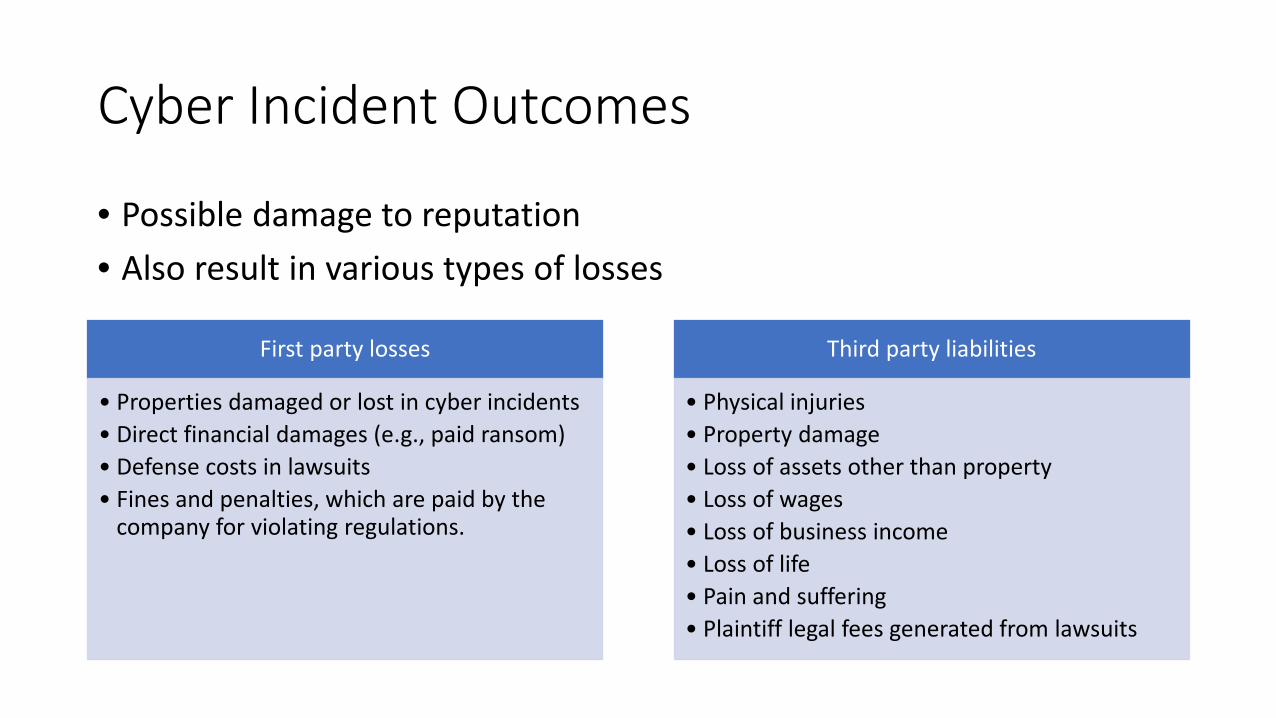

• Possible damage to reputation• Also result in various types of losses

First party losses

• Properties damaged or lost in cyber incidents• Direct financial damages (e.g., paid ransom)• Defense costs in lawsuits• Fines and penalties, which are paid by the

company for violating regulations.

Third party liabilities

• Physical injuries• Property damage• Loss of assets other than property• Loss of wages• Loss of business income• Loss of life• Pain and suffering• Plaintiff legal fees generated from lawsuits

Cyber Incident Outcomes (cont.)

• 3,895 loss amounts are recorded in Advisen’s dataset• About 1/3 (1273/3895 = 32.7%) of the cyber incidents do not result in any measurable losses• The log10-scaled losses follows a normal distribution with mean 5.41 and standard deviation 1.25

0

100

200

300

400

500

00.

5 11.

5 22.

5 33.

5 44.

5 55.

5 66.

5 77.

5 88.

5 99.

5 1010

.5 1111

.5 12M

ore

Loss Distribution

Losses Sample from normal distribution

1273

2622

No loss Loss

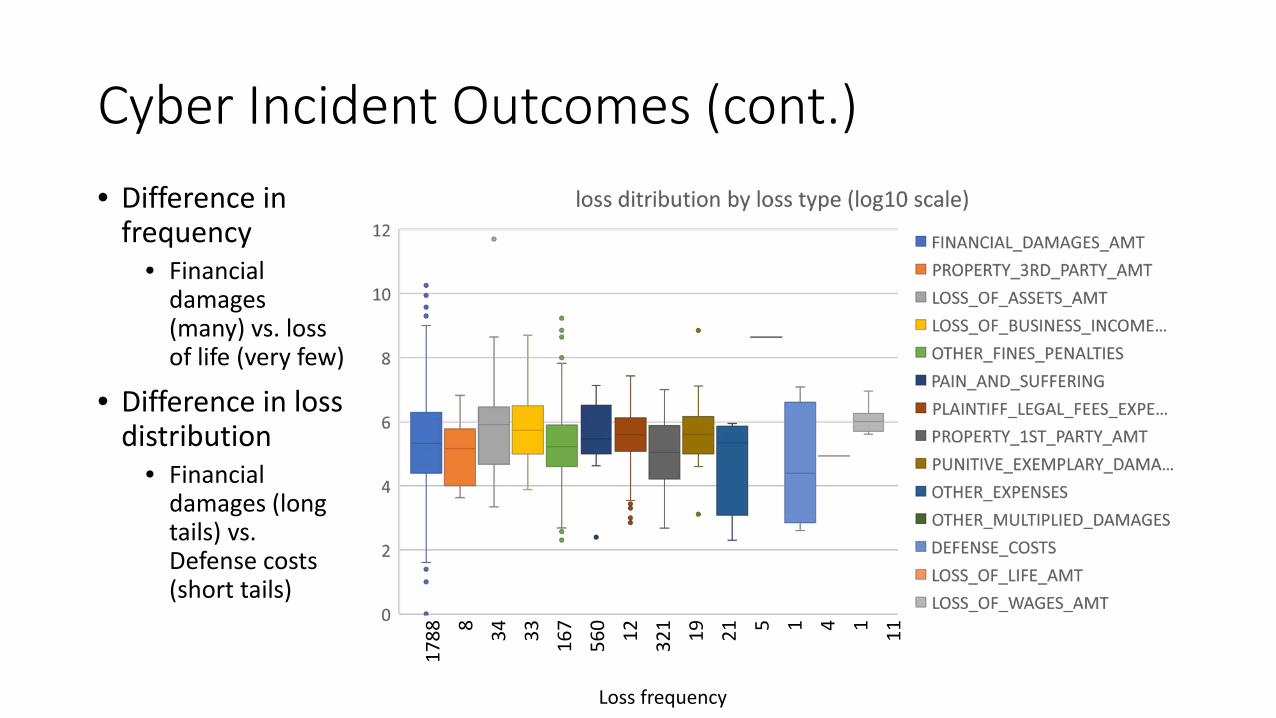

Cyber Incident Outcomes (cont.)• Difference in

frequency• Financial

damages (many) vs. loss of life (very few)

• Difference in loss distribution

• Financial damages (long tails) vs. Defense costs (short tails)

1788 8 34 33 16

756

0 12 321 19 21 5 1 4 1 11

Loss frequency

Cyber Insurance for Risk Management

Cyber Insurance

• Cyber insurance is a risk transference vehicle• Complement to cybersecurity enhancement• Help insured businesses quickly recover from cyber incidents

• The market is still in its infancy• U.S. penetration level of insureds is less than 15% (less than 1% in other

regions)• Less than 5% of small and medium sized businesses purchase cyber insurance

in the U.S.• The market is growing fast

• $1.7 billion written premium in 2015• 30% annual growth rate since 2011

Cyber Insurance Coverages and ExclusionsBasic Cyber Coverage

• Privacy Liability• Network Security Liability• Network Business Interruption• Cyber Extortion• Data Asset Restoration

Expanded Cyber Coverage• Dependent Business Interruption• System Failure• Supply Chain Interruption

Extension of Cyber Coverage• Cyber Related Property and Casualty Loss

Other Common Coverages• Computer Forensic Costs• Notifications and Additional Services to Affected

Individuals• Claims Expenses, Penalties, Defense, and

Settlement Costs

Typical Exclusions• Criminal Activities• Disregard for Computer Security• Loss of Internet Not Operated by You• Bodily Injury• Act of Terrorism/War• Contractual Liability

Issues With Cyber Insurance Market

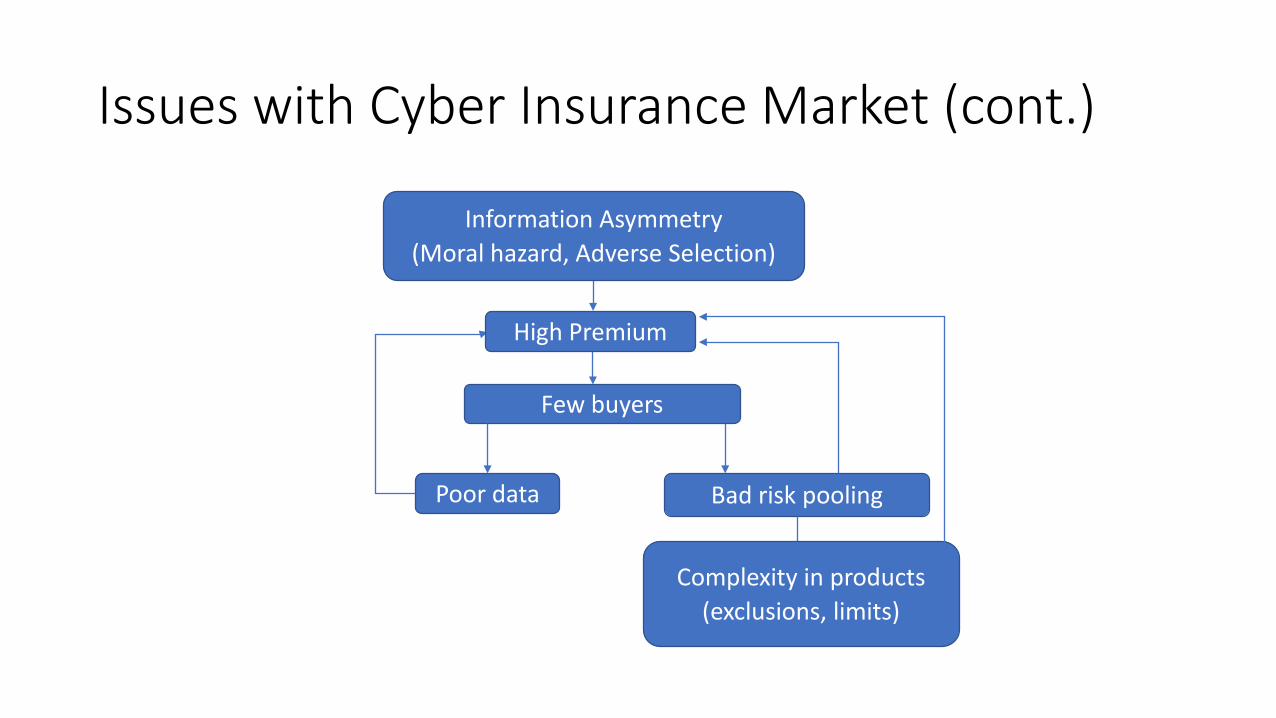

• Problems with cyber insurance

Data scarcity

• Short history of collecting cyber incident data

• Takes time to improve this situation

Difficult to distinguish different

risk levels

• 50% of cyber insurance policies are using flat rates

• We can improve this through better risk assessment

Moral hazard and adverse selection

problem

• Insureds lack of incentive to improve cybersecurity

• Insurers increase premium rates for higher risk in portfolio

Issues with Cyber Insurance Market (cont.)

Few buyers

Poor data Bad risk pooling

Complexity in products(exclusions, limits)

Information Asymmetry (Moral hazard, Adverse Selection)

High Premium

Bridging Cyber Incidents and Insurance

Attributes of Cyber Incidents

• Cyber incidents have many attributes:

• Causes• Actors• Motivations• Affected assets• Losses• Etc.

• Which ones are the most important from a cyber insurance perspective?

Cyber incidents

Causes

Affected assets

ActorsMotivations

Losses

From Incident to Claim

Incident occurs

Covered peril?

No Claim

Loss 1

Loss 2

Loss N

Claim

Yes

No

Any covered losses? Yes

No

From Insurance to Claim (cont.)

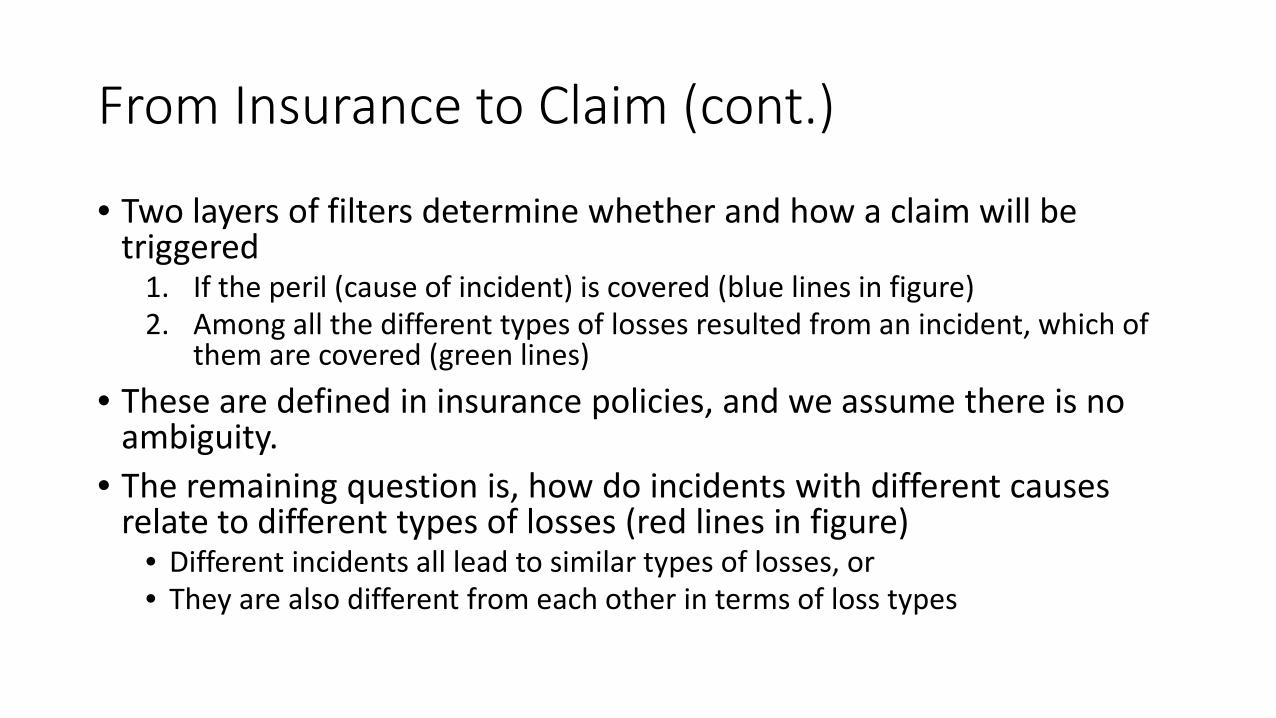

• Two layers of filters determine whether and how a claim will be triggered

1. If the peril (cause of incident) is covered (blue lines in figure)2. Among all the different types of losses resulted from an incident, which of

them are covered (green lines)• These are defined in insurance policies, and we assume there is no

ambiguity.• The remaining question is, how do incidents with different causes

relate to different types of losses (red lines in figure)• Different incidents all lead to similar types of losses, or• They are also different from each other in terms of loss types

Loss Frequency by Loss Type

FIN

ANCI

AL

DAM

AGES

OTH

ER

OTH

ER F

INES

PE

NAL

TIES

PLAI

NTI

FF LE

GAL

FE

ES E

XPEN

SES

LOSS

OF

ASSE

TS

PRO

PERT

Y 1ST

PART

YLO

W O

CCU

RREN

CE

LOSS

ES

Cyber ExtortionData - Malicious BreachData - Physically Lost or StolenData - Unintentional DisclosureDenial of Service (DDOS)/System DisruptionDigital Breach/Identity TheftIdentity - Fraudulent Use/Account AccessIndustrial Controls & OperationsIT - Configuration/Implementation ErrorsIT - Processing ErrorsNetwork/Website DisruptionPhishing, Spoofing, Social EngineeringPrivacy - Unauthorized Contact or DisclosurePrivacy - Unauthorized Data CollectionSkimming, Physical Tampering

• Darker color represents higher frequency of occurrence of the corresponding loss type (in column)

• Most Incidents result in financial damage

• Some incidents, such as unintentional disclosure of data very often bring many other types of losses

• Some incident types have similar loss profiles (e.g., Cyber extortion and Identity –Fraudulent Use/Account Access)

Grouping Similar Incidents

Given the fact that although some incidents have different causes, they are similar in terms of the losses that they result in, we try to group together different incident types with such similaritiesBenefits of grouping:• Highlights the similarity shared by different incident types in the same

group • No need to distinguish incidents if they pass both filters (peril and loss) and

result in similar insurance claims (applicable coverages)• Creates larger samples

• Very small sample sizes for some categories in original dataset, (e.g., only 8 records for DDoS incidents), is impractical for statistical analysis

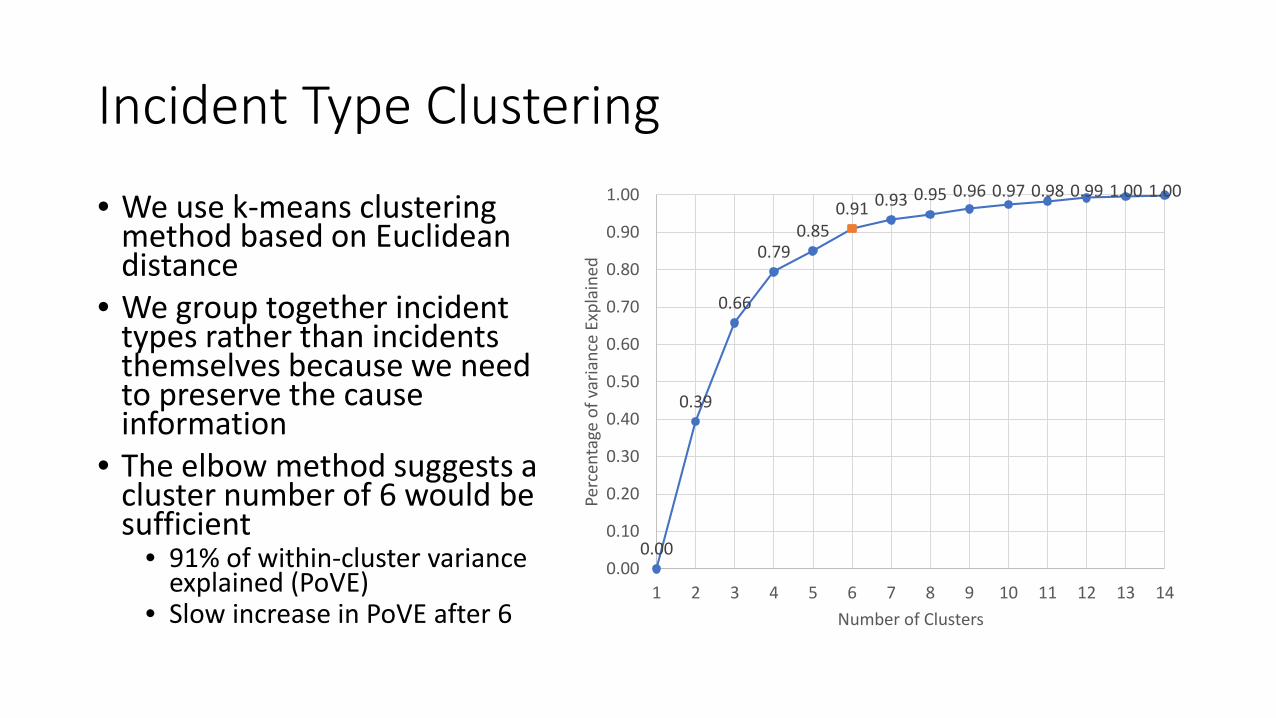

Incident Type Clustering

• We use k-means clustering method based on Euclidean distance

• We group together incident types rather than incidents themselves because we need to preserve the cause information

• The elbow method suggests a cluster number of 6 would be sufficient

• 91% of within-cluster variance explained (PoVE)

• Slow increase in PoVE after 6

0.00

0.39

0.66

0.790.85

0.91 0.93 0.95 0.96 0.97 0.98 0.99 1.00 1.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14Pe

rcen

tage

of v

aria

nce

Expl

aine

dNumber of Clusters

Incident Type Clustering (cont.)

After the clustering, we have:Group Parent Type Child Type

1 Privacy ViolationPrivacy - Unauthorized Contact or DisclosurePrivacy - Unauthorized Data Collection

2 Cyber disruptionsDenial of Service (DDOS)/System DisruptionNetwork/Website Disruption

Data - Malicious BreachData - Physically Lost or StolenIT - Configuration/Implementation ErrorsIT - Processing Errors

6 Unintentional data disclosure Data - Unintentional Disclosure

Incident Type Clustering (cont.)

• Losses associated with each parent type, darker color represents higher frequency of occurrence of the corresponding loss type (in column)

• Only three types of losses frequently appear (‘OTHER’ excluded), and they distribute differently for each of the six groups

• Unintentional data disclosure should be treated differently from other types of data breaches because it results more often in fines and penalties

FIN

ANCI

AL D

AMAG

ES A

MT

OTH

ER F

INES

PEN

ALTI

ES

PLAI

NTI

FF LE

GAL

FEE

S EX

PEN

SES

OTHE

R

LOW

OCC

URR

ENCE

LOSS

ES

Privacy Violation

Cyber disruptions

Industrial Controls & Operations

Cyber extortion & Fraudulent activities

Malicious data breach & IT failures

Unintentional data disclosure

Risk Assessment through Resampling

Objective and Assumptions

Objective: • Estimate the cyber incident rate in a group of companies (i.e., number of cyber

incidents per company in a given period)• In an insurance setting, number of possible claims arising from a pool of

policyholdersAssumptions: • Every incident results in a claim • Claims are all covered.• Portfolios are static (not changing in different years) • This analysis can be seen as the worst scenario; in actual insurer’s portfolio, the

rate is expected to be much lower

Data and Methodology

Generate a list of publicly traded companies in the U.S.• We choose public companies because their information can be easily

obtained, and we know the population size• Cyber insurance has a relatively higher penetration level among public

companies, so in actual insurer’s portfolios, we would expect to see lots of public companies as policyholders

• Further research will be carried out on whether public and private companies have different risk characteristics in terms of cyber-security

• Exchanges we considered include Nasdaq, NYSE and AMEX• 5700+ companies in total after removing duplications

• Different classes of stock or different divisions from the same company are seen as duplications.

• 6600+ companies before removal• Data source: NASDAQ(http://www.nasdaq.com/screening/companies-by-

• We randomly sample 1000 companies from the list to form a portfolio of policyholders

• Assuming each company has the same likelihood of purchasing cyber-insurance• Repeat the process a 1000 times to create 1000 portfolios.

• We look up the companies from each portfolios in the Advisen’s database to see how many of them have cyber incidents in a given year

• We use data points from 2011 to 2014, since they have the best quality

• Record the cyber incident number for each portfolio. Since we have 1000 portfolios in each year, we get a pretty good distribution of portfolio risk in terms of claim counts.

larger variance, so the portfolios are getting riskier.

• The main cyber incident rate for public companies is 2.8% in 2014

• The maximum rate is 4.5%; since the assumptions are made based on the worst scenario, we would expect that the claims from real-world insurer’s portfolio to be below this rate

Ongoing ResearchCyber incidents and business reputation

Different Opinions

• Cyber incidents are often believed to have negative impact on companies’ reputation

• Such belief is held by people on both sides of a company (i.e., managers and customers)

• In 2011, Experian, along with Ponemon Institute, surveyed over 800 senior-level individuals, and most of them agreed on that reputation is one of their most valuable assets, and a cyber incident like a data breach can do damage to it. They also estimate that the impact can last as long as a year

• In a survey conducted by OnePoll, 87% of 2000 respondents said that they were “not at all likely” or “not very likely” to do business with an organization that had suffered a data breach involving credit or debit card details. The numbers were slightly lower if home and email addresses and telephone numbers had been lost.

Different Opinions (cont.)

• Little empirical evidence is found to support the respondents’ statements in OnePoll’s survey that data breaches are going to hurt the customer loyalty of a business in a meaningful way

• If the majority of people stop doing business with companies that had data breaches, we would expect to see reductions in earnings for these companies

• 2013 Target data breach or 2014 Home Depot data breach did not have much impact on their earnings

• With the combined data from Advisen and CompuStat, we are able to gain more insights into how cyber incidents actually affect the reputation of a company.

Data

• Over 1000 companies can be found in both Advisen and CompuStat dataset• Among all the cyber incidents experienced by these companies, we choose

the ones with FIRST_NOTICE_DATE recorded (the date when incident is known to the public)

• Based on these dates, we search for the last quarterly earnings before the incident, and subsequent quarterly earnings reports after the incident (discard the ones with missing quarterly reports)

• To have a better control on the length of time between the date of incident and the date of next earnings, we divide these incidents into three groups:

• Taking place 2-3 months before the next earnings • Taking place 1-2 months before the next earnings • Taking place 0-1 months before the next earnings

Methodology• Goodwill as the proxy for reputation:

• Usually only has book value in mergers and acquisitions • Represents the amount of money that buyer is willing to pay for a company’s good

name• But we try to estimate it with excess earnings method, which is a common practice in

accounting• Because we only care about the change value in goodwill, some issues with this

method, such as choosing a proper capitalization rate is negligible• Other indicators as alternative references

• Earnings quality• Market to book ratio

• Control group – Other companies in the same industry which have similar characteristics but do not have cyber incidents in the same period

• Industry-wise effects (e.g., holiday season in retail industry)

Target Corp. as an Example

12/19/2013, 100

0102030405060708090

100

12/0

1/13

12/0

3/13

12/0

5/13

12/0

7/13

12/0

9/13

12/1

1/13

12/1

3/13

12/1

5/13

12/1

7/13

12/1

9/13

12/2

1/13

12/2

3/13

12/2

5/13

12/2

7/13

12/2

9/13

12/3

1/13

01/0

2/14

01/0

4/14

01/0

6/14

01/0

8/14

01/1

0/14

01/1

2/14

01/1

4/14

01/1

6/14

01/1

8/14

01/2

0/14

01/2

2/14

01/2

4/14

01/2

6/14

01/2

8/14

01/3

0/14

Interest over time from Google Trends

Definition of Interest:Numbers represent search interest relative to the highest point on the chart for the given region and time. A value of 100 is the peak popularity for the term.

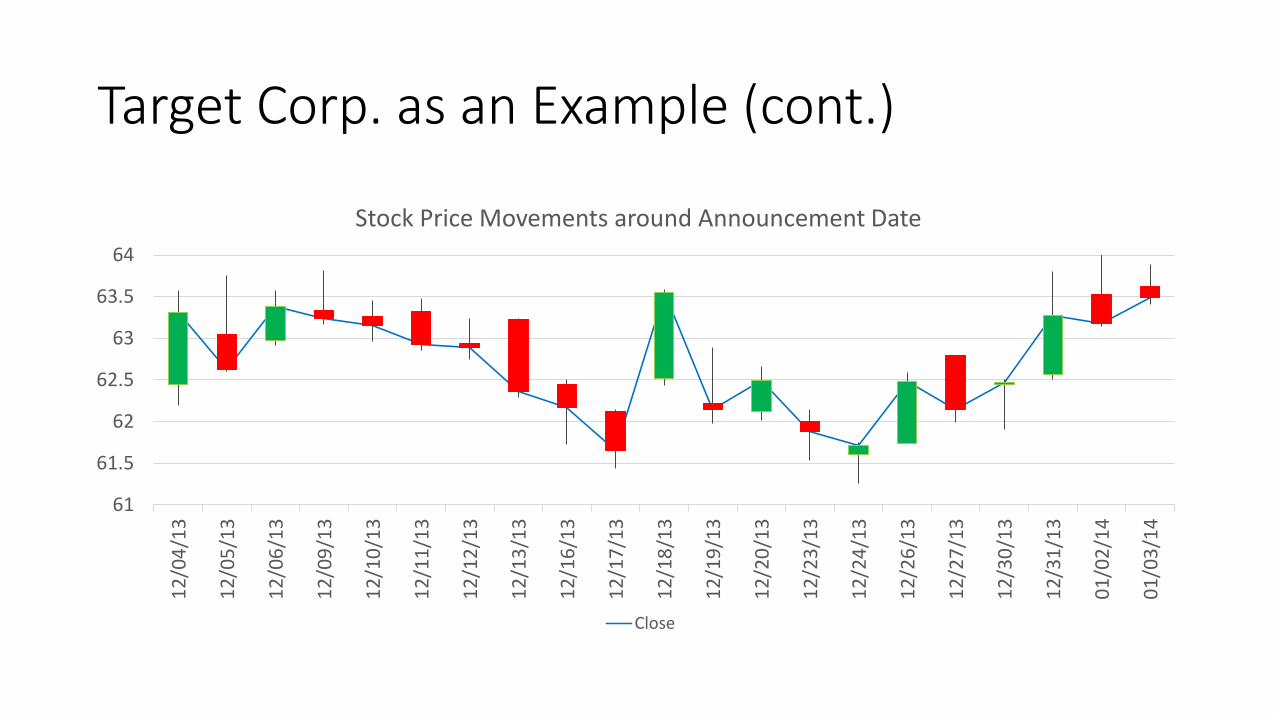

• Target announced the data breach on Dec 19, 2013

Target Corp. as an Example (cont.)

61

61.5

62

62.5

63

63.5

64

12/0

4/13

12/0

5/13

12/0

6/13

12/0

9/13

12/1

0/13

12/1

1/13

12/1

2/13

12/1

3/13

12/1

6/13

12/1

7/13

12/1

8/13

12/1

9/13

12/2

0/13

12/2

3/13

12/2

4/13

12/2

6/13

12/2

7/13

12/3

0/13

12/3

1/13

01/0

2/14

01/0

3/14

Stock Price Movements around Announcement Date

Close

Target Corp. as an Example (cont.)• Data breach was announced

1 month after 2013Q3 and 2 months before 2013Q4

• The quarterly earnings after data breach showed growth in both sales and net income, though it might be due to the holiday season

• No strong evidence suggests that the company’s capability to generate revenues was affected

200

250

300

350

400

450

500

550

15

16

17

18

19

20

21

22

11/2/2013 2/1/2014 5/3/2014 8/2/2014 11/1/2014

2013Q3 2013Q4 2014Q1 2014Q2 2014Q3

Mill

ions

Billi

ons

Sales Net income

Summary• Cyber risk is hard to eliminate within companies• Companies can purchase cyber insurance to transfer risk of cyber loss• Cyber insurance market is still in its infancy, and it has many issues

• Data scarcity• Ineffective pricing (leads to moral hazard, adverse selection)

• Although it is hard to fix the data scarcity problem in the short term, insurers can undertake better risk assessment to improve their products

• We are working on improving portfolio risk assessment: • Understand cyber losses as a function of relevant parameters • Utilize cyber incident data more efficiently• Have a better understanding of the cyber risk in their portfolios

• Our work complements other assessments of risk – technological and legal

Recognizing the Team

Sachin Shetty (Co-PI)Associate Professor, Virginia Modeling, Analysis and Simulation Center, Old Dominion University

MD Ali Reza Al AminGraduate student, Virginia Modeling, Analysis and Simulation Center, Old Dominion University

Yu WangSoftware Developer, Virginia Modeling, Analysis and Simulation Center, Old Dominion University

Jay Kesan (PI)Professor, Law & ECE, University of Illinois

David M. Nicol (Co-PI)Professor, ECE, University of Illinois

Carol Hayes Postdoc, University of Illinois

Linfeng ZhangRes. Associate, University of Illinois