31

1 André Vanoli IARIW 2006 1993 SNA update Provisional recommendations discussant

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | rosaline-watkins |

| View: | 216 times |

| Download: | 0 times |

1

André Vanoli IARIW 2006

1993 SNA update

Provisional recommendations

discussant

2

André Vanoli IARIW 2006

Welcome recommendations

Issue 2 : Private employers’ pension schemes

Issue 3 : Employee stock options

Issue 5 : Non-life insurance

Issue 6a : Financial services• allocation of FISIM and volume measure of output• output of market making services• further investigation : role of expected holding gains

and losses

Issue 6b : output of central banks, measure and allocation

IARIW 2006

3

André Vanoli IARIW 2006

group of issues on intangible assets

Issue 9 : R&D

Issue 11 : Originals and copies

Issue 12 : Databases

Issue 21 : Contracts, leases and licences

Issue 22 : Goodwill and marketing assets

IARIW 2006

4

André Vanoli IARIW 2006

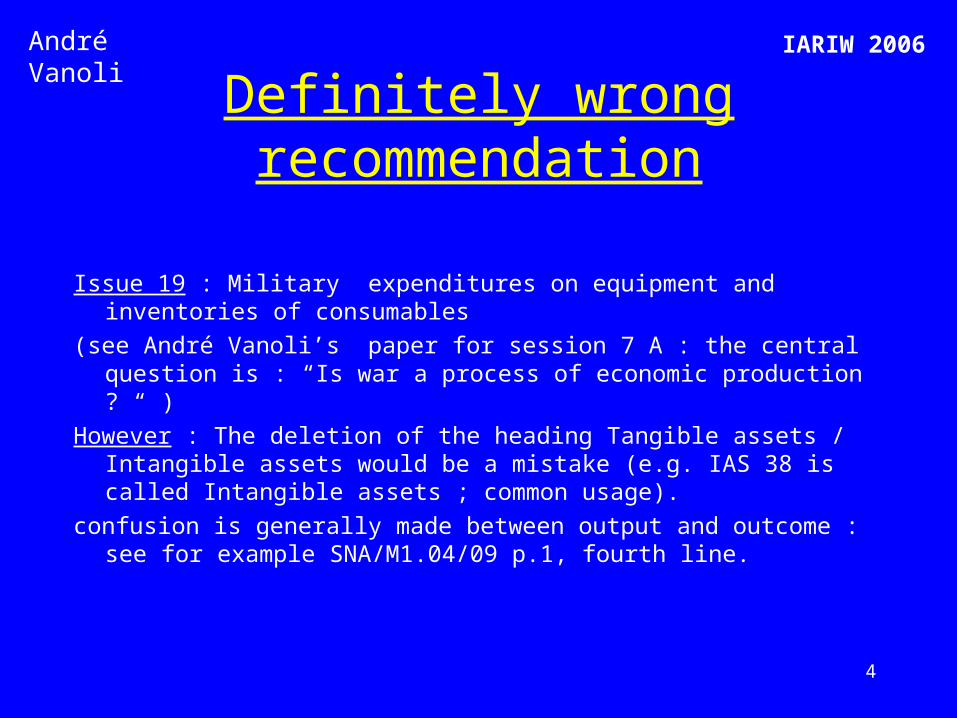

Definitely wrong recommendation

Issue 19 : Military expenditures on equipment and inventories of consumables

(see André Vanoli’s paper for session 7 A : the central question is : “Is war a process of economic production ? “ )

However : The deletion of the heading Tangible assets / Intangible assets would be a mistake (e.g. IAS 38 is called Intangible assets ; common usage).

confusion is generally made between output and outcome : see for example SNA/M1.04/09 p.1, fourth line.

5

André Vanoli IARIW 2006

Ambiguous recommendation

Issue 15 : Cost of capital servicesno changes to the standard entries in the accounts, in relation with

capital services : OK.a new chapter on capital services in the 1993 SNA Rev 1 ?

= an ambiguous compromise (a Trojan horse ?)strong conceptual objections against the inclusion in the SNA of

the concept of capital services (see specific slide).

However : including an opportunity cost of capital for fixed assets owned in the estimate of non-market output is welcome (Issue 16)

6

André Vanoli IARIW 2006

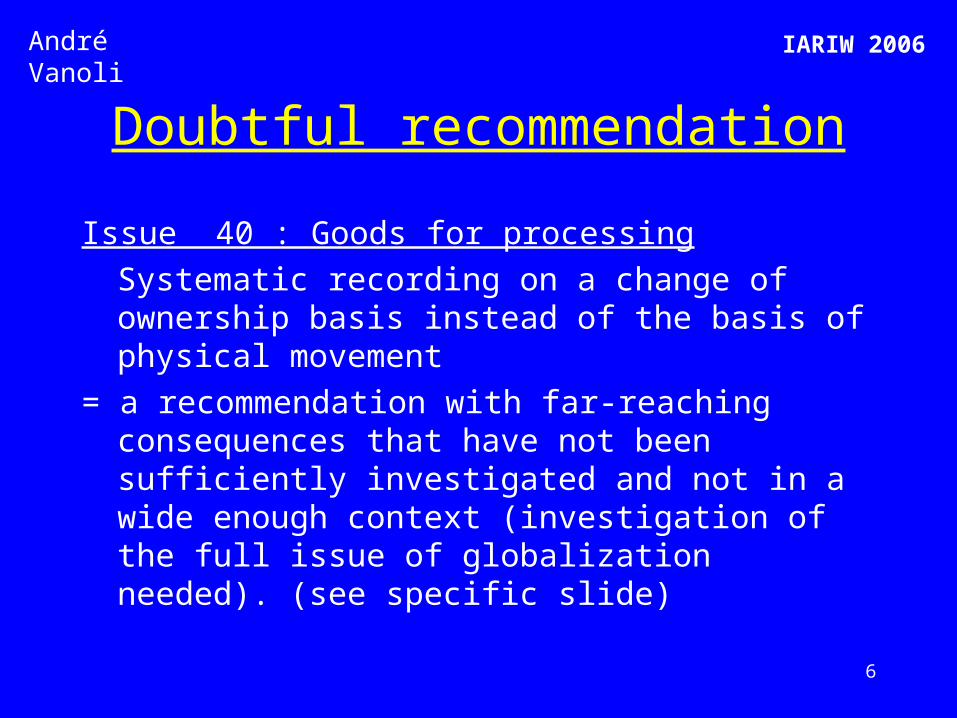

Doubtful recommendation

Issue 40 : Goods for processing

Systematic recording on a change of ownership basis instead of the basis of physical movement

= a recommendation with far-reaching consequences that have not been sufficiently investigated and not in a wide enough context (investigation of the full issue of globalization needed). (see specific slide)

7

André Vanoli IARIW 2006

Issues not satisfactorily solvedIssue 4 : Non-performing loans• no change recommendation (with complementary information) : lack of

boldness

• need to reinterpret the implication of the quadruple entry principle in this context

Issue 28 : Amortization of intangible non-produced assets (mobile phone licences)

• no agreement apparently (unless something new happened in the recent period).

• is the issue well stated in terms of intangible (non financial) non produced assets ?

• why not follow a simple approach in terms of up-front payment as an advanced payment of a stream of annual rents

• annual rents recorded as property income between the licensee and the licensor.

8

André Vanoli IARIW 2006

Miscellaneous

1. Consumption of fixed capital replaced by Depreciation ? No, in my view :

• What relation with the update orientation ?• Depreciation : ambiguous status versus the treatment of

holding gains/losses• CFC more specific to NA which is a very good thing ; any

possible extension (see issue 28) to be carefully investigated • See A History of National Accounting, box 58, p.327-8

2. Classification and terminology of assets• Deletion of the umbrella terms,tangible assets, intangible

assets is lamentable (see previously)• « intellectual property assets » : too narrow, too legal ?

9

André Vanoli IARIW 2006

3. Definition of economic assets, of economic benefits• No substantial decision taken in this respect apparently, which

is ok• In my view, the 1993 SNA does not need any substantial

change• Possible redrafting temptation could be a source of confusion

(see paper M1.06 14)• Additionally, economic benefits wrongly understood

sometimes (see paper M1.04/09 on military expenditures)

4. Costs of ownership transfer (issue 14)• Clarification on terminal costs, etc, welcome• Rediscussion of the all issue to please some people : a loss of

time and energy

10

André Vanoli IARIW 2006

Important outstanding questions• Treatment of the extraction of non-renewable natural resources

– discussion not reopened apparently (issue never fully taken in any process of updating/revising the SNA)

– central issue in my view : the refusal to accept both the idea of the proceeds of the extraction (the resource component) as being sales of assets and the notion of an (oil) rent economy, with consequences on both GDP and NDP

HoweverClarifications on issue 17 : Mineral exploration are useful and some badsolutions have been avoided (e.g.the “ developed natural asset” approach formineral deposits);

• Interest and inflationstill on the research agenda : no progress

• Concept of general price changeflows and stocks

• Apparently « free of charge » servicesfor instance, medias services financed through advertising

11

André Vanoli IARIW 2006More on :Capital services

(Issue 15 : Cost of capital services)

1. Borderline between National Accounting as an observation system (even if : imputations needed, some modelling unavoidable like consumption of fixed capital) and research work (analyses) like Productivity estimates.

2. Tensions between assumptions and recommendations of economic theory and observation of real economies.See for instance Hulten, March 2005, p.28-29 :

- assumptions of the « zero-rent economy » (Hall 2001)- in a more realistic world (the « Nonzero-Rent Economy ») monopoly power,

infra-marginal efficiency rents, persistent disequilibrium, imperfect information, or uncertainty

- « Any attempt to impose the zero-rent economy rules in this world results in a biased estimate of the return to the specific capital assets included in the analysis ».

(by the way where does the notion of “pure economic rent” used in the presentation of issue 15 come from ?)

12

André Vanoli IARIW 2006

3. “ Concrete capital” (equipments, etc…)versus financial capital

See for instance Frisch and Aukrust (1949) sharp distinction between natural interest on real capital and financial interest on financial capital (cf. box 25, p.154, in A History of National Accounting).

4. Capital services as productive services of equipments (in a broad sense) versus capital income as income of financial capital

5. Manifold meanings of the term « Service »

6. Multifactor productivity analysis and NA

• representation of enterprises within an institutional framework (NA) based on a certain empirical approach ; for example categories, like income from property and entrepreneurship, corporate profits, mixed income, entrepreneurial income, property income, are preferred to more abstract ones, like labour income and capital income

13

André Vanoli IARIW 2006

• more abstract representation, based on labour and capital categories, very often in economic theory (marxist theory, neo-classical theory) and MFPA.

• a good case in point : MFPA requires mixed income decomposed into labour and capital components ; a controversial issue among economists in the context of MFP and primary distribution of income analyses ; no reason for NA to settle the question

• a certain ambiguity in MFPA about the meaning of productivity change (cf. Jorgenson and Griliches 1967 : “ if real product and real factor input are accurately accounted for, the observed growth in total factor productivity is negligible” ; this shifts the problem towards the upstream sources of knowledge and innovation)

• anyway, the best contribution of statisticians and NA to MFPA would be to extend to all capital products a proper measure of their volume based on their performances and to tend towards a better coverage of intangible capital products in GFCF.

14

André Vanoli IARIW 2006

7. NA could have been asked to make use of the concept of cost of capital in market activities and to break up, of course by industry, its gross operating surplus between consumption of fixed capital, opportunity cost of capital or normal return to capital, and residual item covering economic rents, in a broad sense, in a nonzero-rent economy (similarly to what we do when estimating the value of the resource rent from extracting non-renewable subsoil resources). Obviously, many difficulties involved, both conceptual and practical ones). (see relations with the exogeneous rate of return approach)

8. NA should not suppose all such difficulties solved and introduce a catch-all concept of capital services that would be deceptive.

Such a conclusion does not prevent capital and MFP analysts from developing a standardized framework for their calculations, in order to harmonize as far as possible research work in these fields. The OECD Manuals obviously intend to play this role. However, such a function should not be confused with the purposes of NA.

15

André Vanoli IARIW 2006

More on :Goods for processing and globalization

Issues 40 : Goods for processing

« 41 : Merchanting

« 25 a : Ancillary units

« 25 c : Multi-territory enterprises

« 25 d : Non-resident unincorporated units

I take the issue more broadly than processing itself.

16

André Vanoli IARIW 2006

1. Intra-enterprise (inter-establishment) deliveries inside the national economy.• reference in the recommendation to change of ownership basis is not

relevant in this case.• relevant when exchanges or gifts are concerned• however, NA covers what is relevant for its purposes, including some

internal flows (internal to an institutional unit) : e.g. consumption of fixed capital, changes in inventories of produced goods,

intermediate consumption.• no change of ownership is to be imputed for internal flows, if the 1993 SNA

is correctly interpreted• if we want to say ; recording inter-establishment deliveries is not useful for

SNA purposes, it is a different question to be taken as such, in connection with I-0 tables, product statistics, regional statistics, etc... concerns (see for instance issue 25 a – Ancillary units about regional accounts concern).

• to be clear : even if the “pure” change of ownership basis was chosen for exchanges and gifts, this should not imply any consequence for intra-enterprise (inter-establishment) deliveries.

17

André Vanoli IARIW 2006

2. Intra-enterprise deliveries between establishments located in different economies

• as two different economies are concerned, a change of ownership is to be imputed according to SNA 1993.

• however, the question should be raised in the context of the SNA institutional framework : an establishment located in a country different from the country of the parent is treated as a notional resident institutional unit of the country of location (see issue 25 d)

• as a consequence : all flows between the non-resident establishment ad the parent enterprise, or between different non-resident establishments of a parent enterprise are to be recorded as if they were between different enterprises.

18

André Vanoli IARIW 2006

• changing this, in order to apply a pure change of ownership basic, would probably imply redefining the concept of economic territory in order to include establishments located abroad in the national economy of the parent enterprise

• if this is what we like, it is an issue to be discussed in itself.• such a reflection should take place having in mind possible similar

requirements for relations internal to groups of corporations, even though in this case changes of ownership occur.

3. processing activities between different (non-notional) institutional units resident in different economies.

• is the question well formulated in terms of choice between change of ownership or physical movement ?

• the real issue is : « What representation of the process is the best in order to fulfill the SNA (possibly conflicting) purposes ?

• the change of ownership basis seems to be taken as a kind of talisman permitting to better reflect the « real life ». Is it true ? In many cases, change of ownership occurs as a consequence of very formal changes in the organization of enterprise activities (see for instance the Dutch paper for session 2A of this Conference, notably category c) p.7-8).

19

André Vanoli IARIW 2006

• Disturbing cases :

• when the whole process of production is sub-contracted elsewhere by the owner of the good ; consequence : a strange production account (see table 7, p.12, of M1.05/16), this extreme case is « an increasingly common one » (§49).

• the Dutch issue of re-exports, after minor processing, if a change of ownership occurs (the Dutch paper is not totally clear to me in this respect).

• I did not find in the AEG documentation a study really permitting to take position, probably because documentation too much focussed on the change of ownership versus physical movement issue, too much emphasis on BOP concerns, no wide enough consultation.

20

André Vanoli IARIW 2006

• Provisionally at least, I would be inclined :

- to treat all three cases, (A to B, back to A ; A to B1, then to B2 ; A to B, then to C), in the same way.

- to investigate more the feasibility of a mixed-type solution (cf. SNA 93, § 14.64) distinguishing significant processing and unsignificant processing.

- to require that the whole issue of globalization be investigated in a broad concept, including questions raised by the working of groups of corporations and in a multilateral coordination process.

21

André Vanoli IARIW 2006

4. processing activities between different institutional units located in the same economy

. investigate the feasibility of a mixed-type solution, as suggestion in 3. above.

22

André Vanoli IARIW 2006

Update/revision strategy

I. The 1993 update strategy not optimal :

• Too many issues opened for discussion • Too many changes proposed• Danger of extensive redrafting

Consequences : 1. Update well beyond the orientation decided at the beginning –

now increasingly, revision (ex : military weapons)2. Difficulties for intellectually mastering the whole process,

embracing all connected issues and making statistical coordination fully efficient (ex : goods for processing

23

André Vanoli IARIW 2006

3. Above difficulties implying significant reorientations of the system on a casual piecemeal basis

• Ex :

- borderline between a system of accounting and a research framework ( cf.issues connected with productivity measurement concerns, like capital services)

- purposes of NA measurement blowed up :

Eg : a certain confusion between legal (more broadly institutional)/economic :

- economic owners vs legal owners : too much emphasis

- change of ownership basis : here too much emphasis on legal aspects perhaps ?

so called economic transformation vs technological processes (abusively restricted to technical coefficients)

emphasis on financial/capital aspects vs actual production

24

André Vanoli IARIW 2006

all this, with contradictory aspects of course :

- emphasis on production when financial services are concerned : ok - - sometimes, emphasis on physical aspects (durables are durable) vs

economic production analysis(ex : military durables) : not ok

4. Difficulties for countries, except (perhaps) the most developed statistically ones, to implement too frequent and too extended system changes, in a context where experienced national accountants are not many

25

André Vanoli IARIW 2006

From an organizational point of view :

• The Advisory Expert Group (AEG), apparently central, not central actually - too many members

- unbalanced influences from various sides :- obviously, the Canberra II group and the « coup » attempted on the capital

services issue - BOP people on goods for processing ?• too weak vs the ISWGNA (and the Canberra II group ? )• Unbalance due to Eurostat’s eclipse :

burden of current work in the EUlack of conceptual investment in NA eurostat crisis

• Was there a pilot in the plane ?• As a consequence : a lot of work and devotion, but a mixed feeling as to the outcome

26

André Vanoli IARIW 2006

II The original intentions, during the first years after the SNA 1993 publication were better

1. Some punctual limited issues needing clarification or real updating (e.g. financial derivatives, output of central banks), resulting in a one by one decision and simulaneously all changes to be made to the text of the 1993 SNA

2. Some big issues needing deep investigations, a single one or a very few of them at the same time

for example, R&D expenditures

3. The process led by the ISWGNA with the help of a permanent group of experts PEG ( my understanding was : a limited group of experts, selected only or nearly only on the basis of experience and knowledge)

27

André Vanoli IARIW 2006

III An advice for the future : improve, but follow the best of the above original orientation

1. There are lessons to be derived from the IASB working procedure, not slavishly of course

2. ISWGNA with a permanent core expert group, with five to ten members

3. Punctual limited issues ; taken one by one, solutions prepared by the ISWGNA and the PEG , with necessary advices from outside ; decisins and changes to the SNA text prepared simultaneously (see II 1 above )

28

André Vanoli IARIW 2006

4. Big innovating issues :

i. one by one, or a very small numbers in parallel

ii. for each, an ad hoc group of experts (limited in number) under the ISWGNA and the PEG supervision

iii. each such group of experts being in charge of preparing an elaborated complete report with a full set of recommendations and more important changes needed to the text

iv. on the basis of this report, however only on this basis, public discussion as wide as possible, with EDG, etc…, and at a certain point of time a wider expert meeting or seminar or conference

v. an adapted process of decision including the complete necessary changes to the SNA text fully drafted

vi. introduction of changes due to one or two big issues, let’s say, every five years

29

André Vanoli IARIW 2006

5. Every twenty-five years, rethink the conceptual framework as a whole

6. Encourage research work, without any immediate implications for short term or short sighted changes, in various circles like the IARIW ; suggested topics, for example,

i. output and outcome, process of production and process of consumptionii. NA and capital theoryiii. NA and business accounting in the context of the development of

international business standardsiv. NA and globalization (also a possible candidate for 4 above)v. NA and the concept and measurement of well-being( see also above

output and outcome), including reflections on economic value, utility, monetary and / or physical dimensions

vi. NA and interest : theories and practices (all aspects including discounting)

30

André Vanoli IARIW 2006

Orientations and essential issues

(see also update revision strategy , part III / 6)

• Autonomy of NA , versus (though connections with) :

- economic theory

- business accounting and public sector accounting

- social analysis and measurement

- environmental analysis and measurement

- other statistical frameworks (BOP, government finance, etc…)

Does it remain a conceptual coordination function for a system of national accounting ? In front of many candidates, like economic theory (which variant? ) in the first place ? On what basis ?

31

André Vanoli IARIW 2006

• Observation systems and theoretical systems

many aspects : measurement without theory ? measurement without history ? theory without history ? Lessons from theory and empirical evidence ? Soft modelling and hard modelling in the context of accounting ?

• Thinking by ourselves, as national accoutants