17

Copper: Five things to look for in 2017 International Copper Study Group Industry Advisory Panel Thursday 27 April 2017 Lisbon, Portugal Trusted commercial intelligence www.woodmac.com

| Date post: | 22-Jan-2018 |

| Category: |

Business |

| Upload: | oscar-frias-martinelli |

| View: | 133 times |

| Download: | 2 times |

Copper: Five things to look

for in 2017

International Copper Study Group

Industry Advisory Panel

Thursday 27 April 2017

Lisbon, Portugal

Trusted commercial intelligence www.woodmac.com

Trusted commercial intelligence www.woodmac.com

2

Copper: Five things to look for in 2017

Introduction

Trump or China?

What will drive demand in 2017?

Where now for copper costs

and margins?

Global macro economic outlook

The changing supply story

Copper on the turn in 2017

Trusted commercial intelligence www.woodmac.com

3

Global economic growth rebounding from 2016 low

Real global GDP growth

Source: Wood Mackenzie, World Bank

Commodity recovery and strong US consumption drive improved outlook, but European

fragility remains a concern

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USA Europe China Commodity producers Other Global

2.3% 2.5% 2.5%

2.6%

Trusted commercial intelligence www.woodmac.com

4

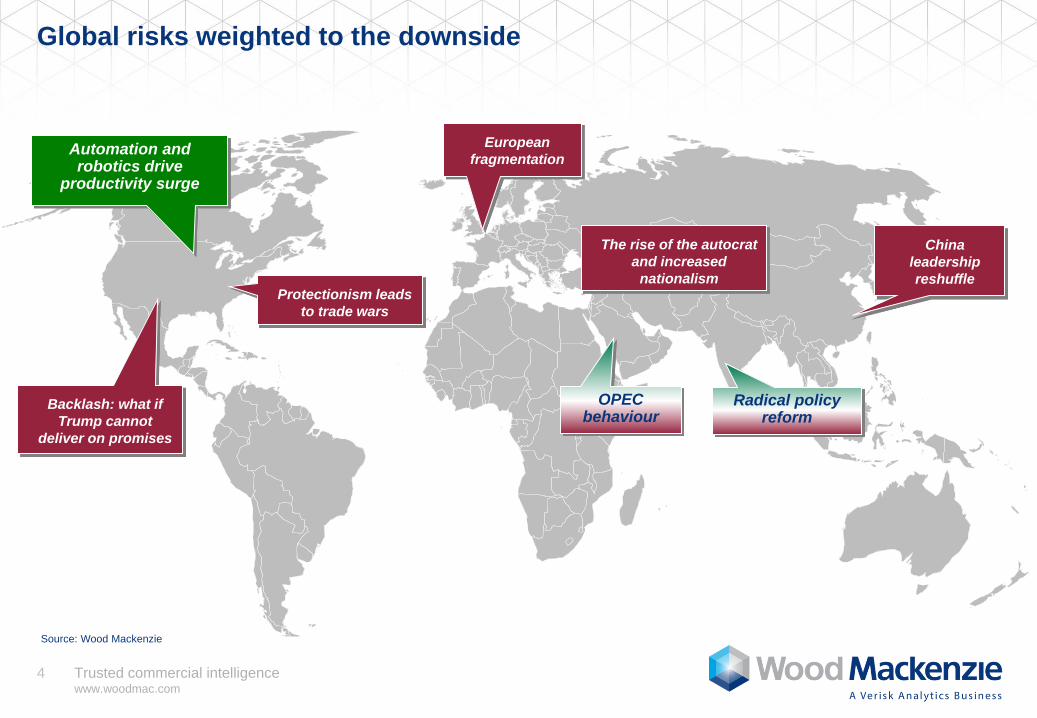

Global risks weighted to the downside

The rise of the autocrat

and increased

nationalism

Backlash: what if

Trump cannot

deliver on promises

Automation and robotics drive

productivity surge

European

fragmentation

China

leadership

reshuffle Protectionism leads

to trade wars

Radical policy reform

OPEC behaviour

Source: Wood Mackenzie

Trusted commercial intelligence www.woodmac.com

5

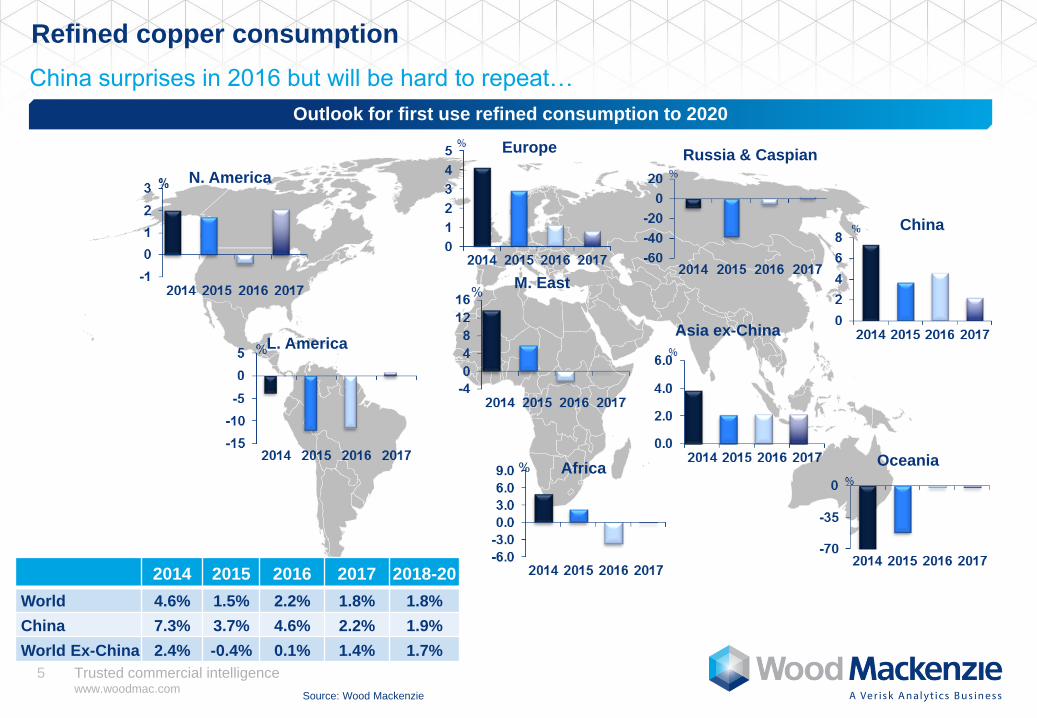

Refined copper consumption

N. America

L. America

Africa

M. East

Europe Russia & Caspian

Asia ex-China

China

Oceania

Outlook for first use refined consumption to 2020

2014 2015 2016 2017 2018-20

World 4.6% 1.5% 2.2% 1.8% 1.8%

China 7.3% 3.7% 4.6% 2.2% 1.9%

World Ex-China 2.4% -0.4% 0.1% 1.4% 1.7%

Source: Wood Mackenzie

China surprises in 2016 but will be hard to repeat…

Trusted commercial intelligence www.woodmac.com

6

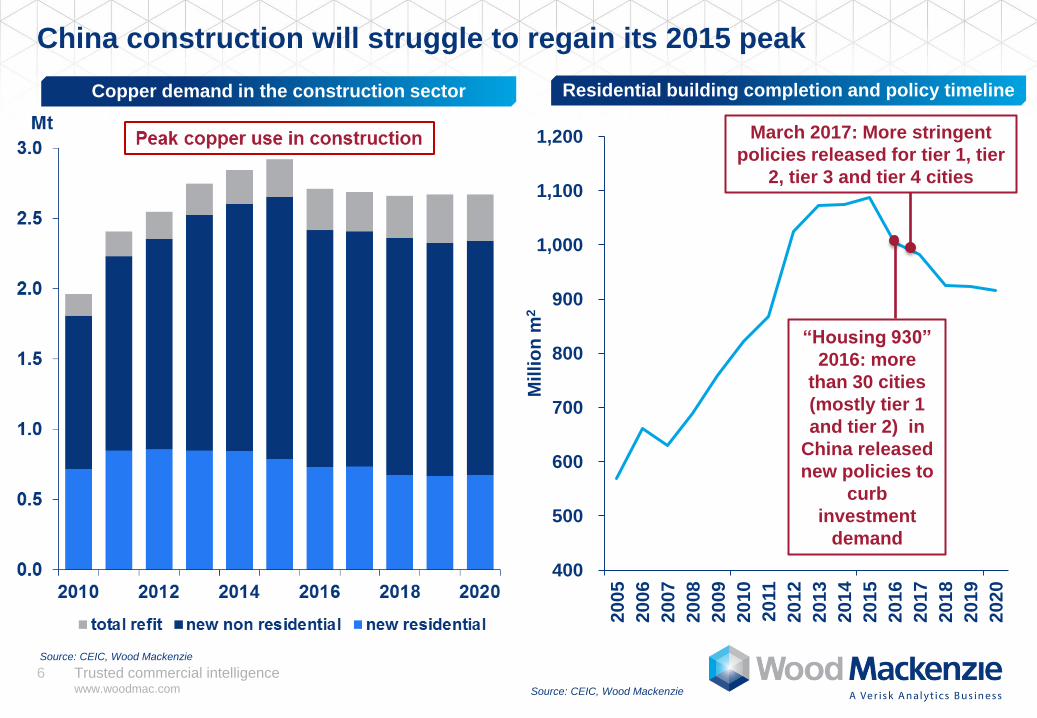

China construction will struggle to regain its 2015 peak

Residential building completion and policy timeline

400

500

600

700

800

900

1,000

1,100

1,200

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Milli

on

m2

“Housing 930”

2016: more

than 30 cities

(mostly tier 1

and tier 2) in

China released

new policies to

curb

investment

demand

March 2017: More stringent

policies released for tier 1, tier

2, tier 3 and tier 4 cities

Source: CEIC, Wood Mackenzie

Copper demand in the construction sector

Source: CEIC, Wood Mackenzie

Trusted commercial intelligence www.woodmac.com

7

Auto: copper demand from passenger cars will grow much

faster than production growth due to increasing EV penetration

Passenger car production vs copper consumption

Source: CEIC, Wood Mackenzie

Increasing share of public service and commercial

building

Passenger car production

Copper

Passenger car prod.

Trusted commercial intelligence www.woodmac.com

8

Trump policies have caused uncertainty over North American demand

2017 US infrastructure rating - in need of an upgrade Current auto output forecast – US and Mexico

0

2

4

6

8

10

12

14

2000 2005 2010 2015 2020

Mn units

US Mexico

Source: Wood Mackenzie

Trusted commercial intelligence www.woodmac.com

9

Despite lower growth, on a tonnage basis, it’s still all about China

Source: Wood Mackenzie

Changes in refined copper consumption by region: 2016-2020

22.4

0.9

0.4 0.1 0.1 0.1 0.0 (0.1) 0.1 24.0

20

21

22

23

24

2520

16

Ch

ina

Ind

ia &

Ase

an

Mid

dle

Eas

t

La

tin

Am

eri

ca

No

rth

Am

eri

ca

Eu

rop

e

No

rth

Ea

st

As

ia RO

W

20

20

Millio

n to

nn

es

Trusted commercial intelligence www.woodmac.com

10

Mine production growth set to pause this year

Mine production (forecasts after 5% disruption allowance)

Source: Wood Mackenzie

15

16

17

18

19

20

21

22

23

24

25

26

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Min

e s

up

ply

(M

t c

op

per)

ProbableProjects

HighlyProbableProjects

Existingsupply

Kamoto/KOV Restart (+365kt/a)

Cobre Panama (+320kt/a)

Escondida 3rd Mill (+250kt/a)

Las Bambas (+100kt/a)

Sentinel (+135kt/a)

Mopani (+100kt/a)

Toquepala Expn (+100kt/a)

Aktogay (+80kt/a)

Trusted commercial intelligence www.woodmac.com

11

Requirement for additional mine supply from 2020 peak

Mine production (forecasts after 5% disruption allowance)

15

16

17

18

19

20

21

22

23

24

25

26

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Min

e s

up

ply

(M

t c

op

per)

ProbableProjects

HighlyProbableProjects

Existingsupply

mine supply

growth to

pause

base case

mine supply

to peak

additional

supply

required

Trusted commercial intelligence www.woodmac.com

12

Copper prices recover on the back of supply disruptions and higher demand

Source: Wood Mackenzie, LME, Thompson Reuters Datastream

The influence of macro and other events on copper prices

3500

4000

4500

5000

5500

6000

6500

7000

7500

8000

Trump stimulus;Production losses

andUpgraded Chinese

demand

Greek debt crisis

Glencore announces

cuts at Katanga

and MopaniFresh

Chinese

stimulus package

Weak China

PMI

Large deliveries into

Asian LME warehouses

Brexitvote

Copper sell off by

US/Chinese funds

Escondida strike

Grasberg closure

Trusted commercial intelligence www.woodmac.com

13

Annual average copper price set to recover

Source: Wood Mackenzie

Global stocks of refined copper and annual average copper price

0

50

100

150

200

250

300

350

400

450

0

10

20

30

40

50

60

70

80

90

100

Co

pp

er

pri

ce (c

/lb

)

Glo

ba

l me

tal s

toc

ks

(d

ay

s)

Other stocks SRB stocks Price - Q1 2017 estimate

Source: Wood Mackenzie, LME, Comex, SHFE

Average stocks

Trusted commercial intelligence www.woodmac.com

14

Where now for copper costs and margins?

Global residual cash flow for primary copper mines

1.98 1.300.76

1.63

1.57 0.600.33

0.29

0.19

0.260.56 0.70 0.88 1.12 1.55 1.86

0.0

1.0

2.0

3.0

4.0

5.0

2007 2009 2011 2013 2015 2017 2019 2021 LT

Co

st / M

arg

in ($

/lb

pa

id c

op

per)

Expansion Capex Sustaining Capex Indirect Costs

Mine Site Costs Net Revenue

Base case and probable projects only

Source: Wood Mackenzie Q1 2017

Trusted commercial intelligence www.woodmac.com

15

Key conclusions

Global growth has improved from a year ago. The short-term outlook is

relatively positive, owing to a stronger US economy and a recovery in

commodities, but Europe remains a cause for concern.

Prices have been lower, but so has opex and capex. As prices improve

from 2017, we would expect healthier margins. This should support a

new cycle of investment.

Demand growth in the world ex-China should improve on 2016. Overall

refined demand will remain subdued, in part reflecting a stronger

contribution from scrap, yet China is still the main driver for growth.

Source: Wood Mackenzie

Mine supply forecast to pause during 2017 before recovering to peak in

2020. Additional mine production capability is required from ~2020. There

is a lack of advanced development stage projects to meet this need.

The combination of slower supply growth and moderate demand growth

will push the refined market into deficit this year. With global stocks set

to decline, we would expect annual average prices to trend higher.

Trusted commercial intelligence www.woodmac.com

16

Disclaimer

This report has been prepared for the ICSG – Industry Advisory Panel by Wood

Mackenzie Limited. The report is intended solely for the benefit of this meeting and its

contents and conclusions are confidential and may not be disclosed to any other

persons or companies without Wood Mackenzie’s prior written permission.

The information upon which this report is based on our own experience, knowledge and

databases as well as any information publicly available. The opinions expressed in this

report are those of Wood Mackenzie. They have been arrived at following careful

consideration and enquiry but we do not guarantee their fairness, completeness or

accuracy. The opinions, as of this date, are subject to change. We do not accept any

liability for your reliance upon them.

Strictly Private & Confidential

Trusted commercial intelligence www.woodmac.com

17

Europe +44 131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Website www.woodmac.com

Wood Mackenzie* is a global leader in commercial intelligence for the energy, metals and mining industries.

We provide objective analysis and advice on assets, companies and markets, giving clients the insight they

need to make better strategic decisions. For more information visit: www.woodmac.com

*WOOD MACKENZIE is a Registered Trade Mark of Wood Mackenzie Limited