Page 1

1

Angola - Economic Report

Index I. Assumptions on National Policy and External Environment ................................................ 2

II. Recent Trends ........................................................................................................................ 3

A. Real Sector Developments .................................................................................................... 3

B. Monetary and Financial sector developments ...................................................................... 5

Monetary Base .............................................................................................................................. 7

Monetary Aggregates .................................................................................................................... 8

Claims to the Economy .................................................................................................................. 9

Inflation Rate ............................................................................................................................... 10

C. Fiscal Sector Developments ................................................................................................ 11

D. External Sector Developments ............................................................................................ 12

Current Account .......................................................................................................................... 12

Exchange Rate ............................................................................................................................. 13

International Reserves ................................................................................................................ 14

III. Forecast Summary –Policy issues and Uncertainties ...................................................... 15

IV. Summary Table for forecast ............................................................................................ 16

Page 2

2

I. Assumptions on National Policy and External Environment

The current global economic situation is raising concerns due to the negative downtrend

observed in the commodity prices, especially the oil prices, which is becoming an

enormous challenge for the growth of the Angolan economy.

To be more specific, the current economic environment enhanced by the reduction of oil

prices in international markets, led to a sharp decrease in exports of crude oil and

consequently a decrease in the accumulation of foreign exchange reserves. This

decrease in foreign exchange reserves has caused great difficulties to obtain foreign

currency for settlement of transactions with the outside, whether at company level or

individual level. Thus, exchange rate of the primary market suffered a decline year on

year. Furthermore, this shortage of foreign exchange and its consequent depreciation is

even more visible if it is taken into account depreciation in the informal market.

Therefore, in 2015, Angolan economy suffered a major structural shock with the oil

price drop in a context where there is a great dependence on the oil export revenues,

macroeconomic imbalances were recorded, and the forecasts for the coming years are

filled with uncertainty in what the evolution of the main country export product is

concern.

For 2016, the available information is too preliminary, what make it difficult to predict

accurately the behavior of the economy.

It is important to mention that despite the oil price decline had been more intense in

2008/2009, the policy responses were faster in 2015. In a short period of time the

Government Budget was adjusted from a oil price of USD 81 to USD 53; a committee

to coordinate the Fiscal and Monetary Policies was established in order to accompany

and supervise with high regularity the monetary and exchange rate developments as

well as the dynamics of the fiscal policy table, which was largely influenced by

developments in the domestic market of debt securities.

Overall, it was avoided a significant drop in external reserves, enabling significant

currency depreciation, ensuring with this the external solvency of the economy in more

than six months of imports and the control of public debt trajectory.

In the Monetary policy side, the BNA implemented several policies, where, among

others, one can mention the reduction of the interest rate Overnight Absorption Facility;

the change in the reserve requirement ratio in national currency from 15% in January

2015 to 25% in June; the increased sales of foreign currency in the exchange market;

the devaluation of the national currency at 5,75%, the Mandatory establishment of

captive accounts by commercial banks in national currency with the BNA, Changing the

Operating Rules of Money Exchange, allowing the sale of foreign currency to exchange

residents and the increased of Liquidity Lending Facility interest rate.

Page 3

3

Therefore, the macroeconomic environment was marked by the fiscal, monetary and

exchange rate tightening. Nevertheless, as the economy suffered a structural shock,

there is still a need for structural reforms in order to recover economic growth,

accelerate and sustain it, with job creation, diverse production of goods and services and

lower structural inflation.

Finally, the non-oil sector has been registering higher GDP growth rates than the oil

sector in recent years, though it still represents a smaller portion of total domestic

production. Government’s medium term strategy is intended to reverse this position and

reduce dependency on a narrow range of commodities, thus protecting domestic

economy from international oil price volatility.

II. Recent Trends

A. Real Sector Developments

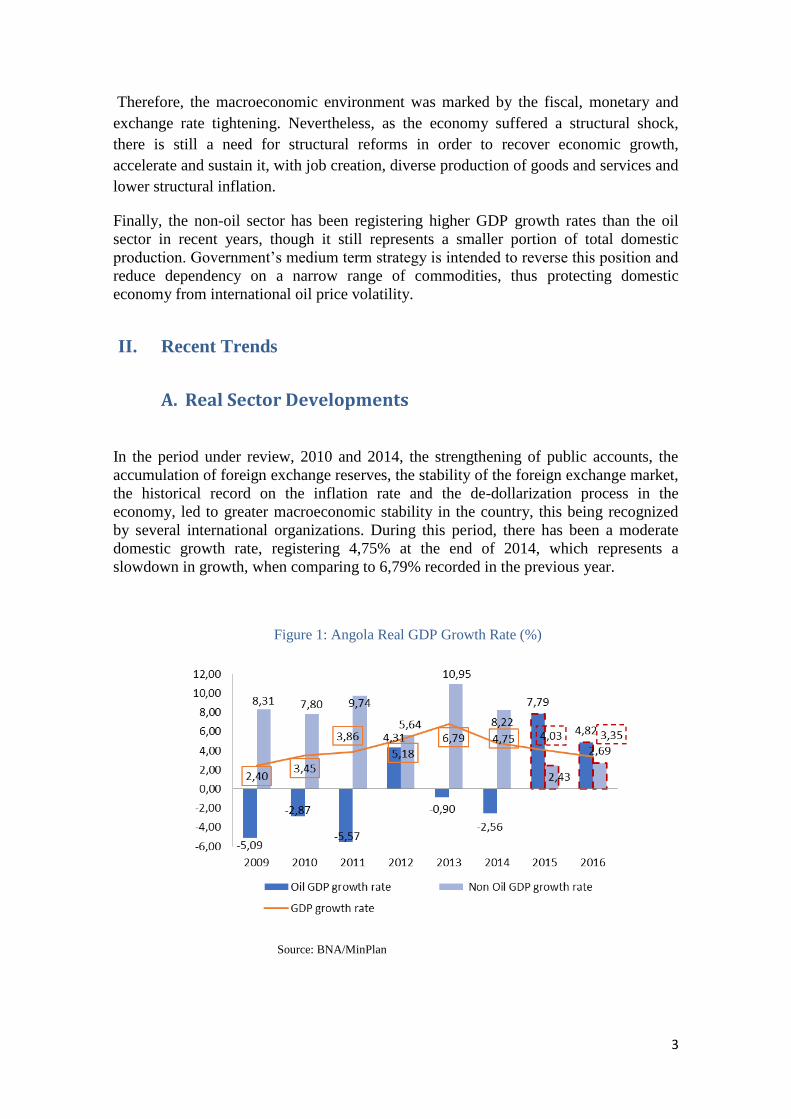

In the period under review, 2010 and 2014, the strengthening of public accounts, the

accumulation of foreign exchange reserves, the stability of the foreign exchange market,

the historical record on the inflation rate and the de-dollarization process in the

economy, led to greater macroeconomic stability in the country, this being recognized

by several international organizations. During this period, there has been a moderate

domestic growth rate, registering 4,75% at the end of 2014, which represents a

slowdown in growth, when comparing to 6,79% recorded in the previous year.

Figure 1: Angola Real GDP Growth Rate (%)

Source: BNA/MinPlan

Page 4

4

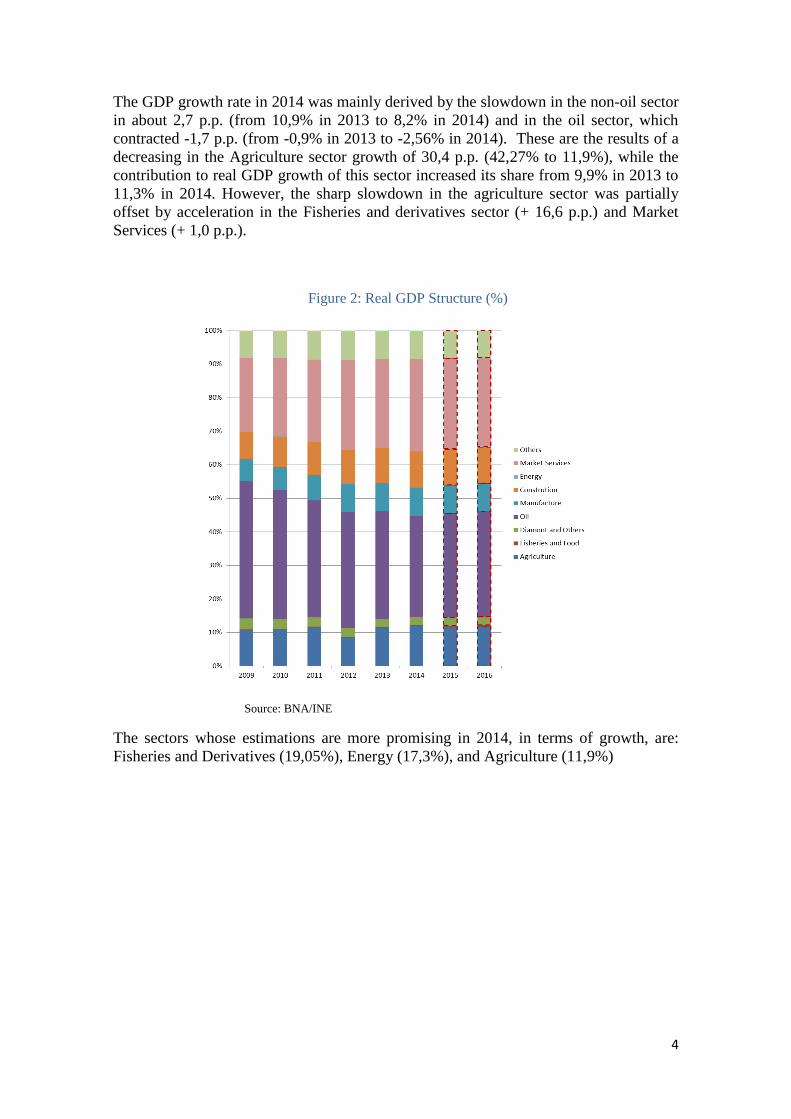

The GDP growth rate in 2014 was mainly derived by the slowdown in the non-oil sector

in about 2,7 p.p. (from 10,9% in 2013 to 8,2% in 2014) and in the oil sector, which

contracted -1,7 p.p. (from -0,9% in 2013 to -2,56% in 2014). These are the results of a

decreasing in the Agriculture sector growth of 30,4 p.p. (42,27% to 11,9%), while the

contribution to real GDP growth of this sector increased its share from 9,9% in 2013 to

11,3% in 2014. However, the sharp slowdown in the agriculture sector was partially

offset by acceleration in the Fisheries and derivatives sector (+ 16,6 p.p.) and Market

Services (+ 1,0 p.p.).

Figure 2: Real GDP Structure (%)

Source: BNA/INE

The sectors whose estimations are more promising in 2014, in terms of growth, are:

Fisheries and Derivatives (19,05%), Energy (17,3%), and Agriculture (11,9%)

Page 5

5

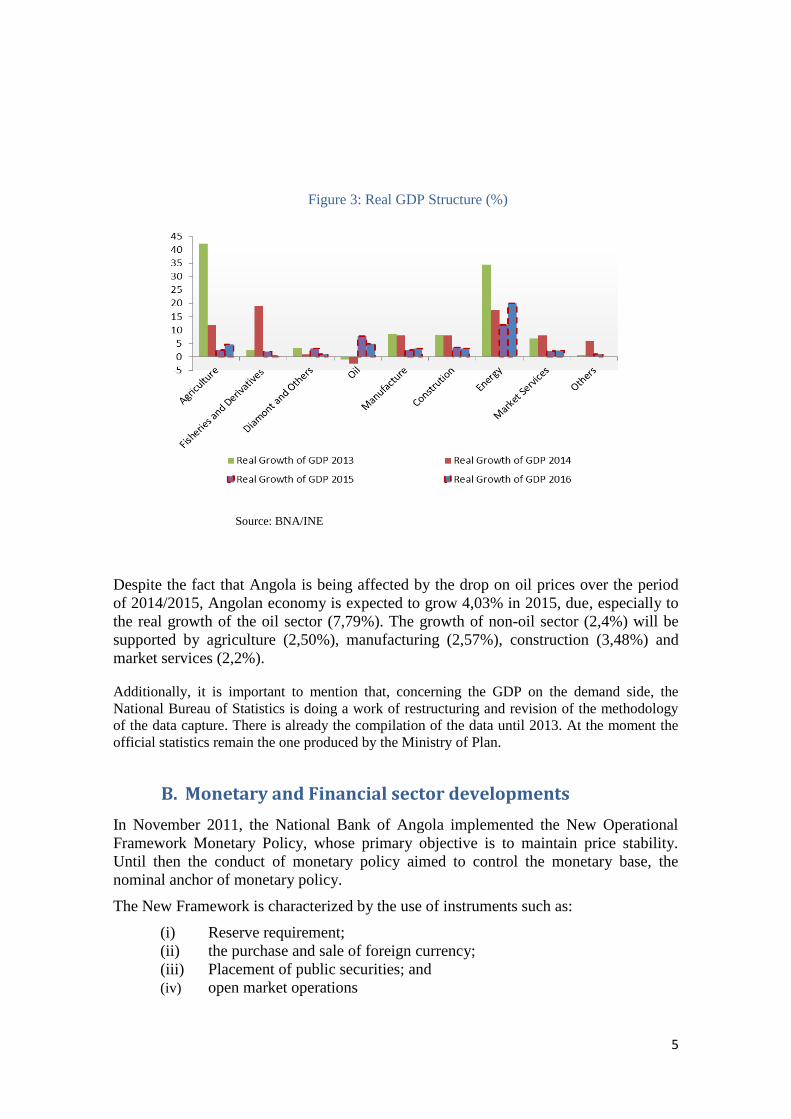

Figure 3: Real GDP Structure (%)

Source: BNA/INE

Despite the fact that Angola is being affected by the drop on oil prices over the period

of 2014/2015, Angolan economy is expected to grow 4,03% in 2015, due, especially to

the real growth of the oil sector (7,79%). The growth of non-oil sector (2,4%) will be

supported by agriculture (2,50%), manufacturing (2,57%), construction (3,48%) and

market services (2,2%).

Additionally, it is important to mention that, concerning the GDP on the demand side, the

National Bureau of Statistics is doing a work of restructuring and revision of the methodology

of the data capture. There is already the compilation of the data until 2013. At the moment the

official statistics remain the one produced by the Ministry of Plan.

B. Monetary and Financial sector developments

In November 2011, the National Bank of Angola implemented the New Operational

Framework Monetary Policy, whose primary objective is to maintain price stability.

Until then the conduct of monetary policy aimed to control the monetary base, the

nominal anchor of monetary policy.

The New Framework is characterized by the use of instruments such as:

(i) Reserve requirement;

(ii) the purchase and sale of foreign currency;

(iii) Placement of public securities; and

(iv) open market operations

Page 6

6

In the context of monetary policy, decisions are made in the Monetary Policy

Committee, which meets monthly to analyze the economic developments.

In order to ensure effectiveness and operability of the monetary policy transmission

mechanism and ensure price stability, the new framework introduced the concept of

Basic Interest Rate, the BNA rate, which serves as a signal to the market, of monetary

policy stance and simultaneously reference to the rates offered in the interbank money

market.

Since 2012, BNA has been maintaining an accommodative monetary policy and

reduced the BNA interest rate by 1,50 p.p. to 9,00% in 2014, following the favorable

evolution of the main economic indicators, among them the continued slowdown in

inflation rate. In 2014, Angola kept the one digit inflation rate (7,48%), as a result of the

good performance of the monetary policy.

However, the international oil price fell, which led to a lack of foreign currency in the

country to settle external transactions and, consequently, led to exchange rate

devaluation. This exchange rate devaluation originated higher inflation levels, forcing

the central bank to take another approach and to increase BNA interest rate to 10,5% in

the second half of 2015.

Apart from the increase in the interest rate, the National Bank of Angola decided on

other monetary tightening measures, which are presented below:

Reduction of the interest rate Overnight Absorption Facility to 0% in the

Monetary Policy Committee of February 2015 in order to promote lending by

commercial banks and some slack in terms of liquidity for the placement of

government securities;

Change in the reserve requirement ratio in national currency for 25% of which

10% can be met through Government Bonds issued from January 2015, belonging

to the respective bank's portfolio and weighted according to maturities as

Instructional 8/2015, with the aim of reducing the liquidity of the financial system

and create at the same time, conditions for financing the state budget;

Increased sales of foreign currency in the exchange market in order to partially

satisfy demand for foreign exchange that has been observed by reducing the

negative effects on the real economy;

Devaluation of the national currency at 5.75%, at June 5, 2015 and increased

direct sale this week for USD 836 million and USD 100 million auction;

Mandatory establishment of captive accounts by commercial banks in national

currency with the BNA, with a corresponding balance the need to buy foreign

currency for the following week, according to the Instruction 10/2015;

Resumption of OMA in order to make a fine control of liquidity of the financial

system;

Page 7

7

Changing the Operating Rules of Money Exchange, allowing the sale of foreign

currency to exchange residents up to the amount of USD $ 5,000.00, according to

Instruction No. 07/2015 of 28 May, in order to promote transparency in the

exchange market;

Increased of Liquidity Lending Facility interest rate to 12.5% in the Monetary

Policy Committee remarkable held in September 2015;

Increased of Interest Rate Overnight Absorption Facility to 1.75% in the

Monetary Policy Committee extraordinary conducted in September 2015;

Monetary Base

Between December 2010 and December 2014, the monetary base expanded 45,78%.

Foreign Net Assets in the reporting period increased 77.30%, to move from Kz

1.731.026,45 in December 2010 to Kz 3.069.093,01, in December 2014, while the

Internal Net assets grew 115.48%, to move from Kz 947.203,63 in December 2010 to

Kz 2.041.022,93 in December 2014. This trend may be being influenced especially by

the ability to mobilize external resources, due to the weight of the oil sector on GDP and

a bit for maintaining the equilibrium of the balance of payments, than the natural

combination of monetary and fiscal policies.

During the reporting period, the ratio relating to the degree of liquidity of the economy

(M2 / GDP), weight indicator of bank deposits and currency in circulation over the

whole economy, increased by 6.80 p.p. , from 34.15% in 2010 to 40.95% in 2014. This

figure is slightly below the average for sub-Saharan Africa (45.2%) and well below the

average for the advanced economies (80%). Whereas in 2014, 50.98% of Angola's

population now has access to banking services, it is unquestionable the dynamics and

growth potential of the economy.

Figure 4: Monetary Basis

Source: BNA

In the first eight months of the year, observed an expansion of monetary basis at 13.46%

and a growth of monetary basis in national currency at 58.96%.

Page 8

8

It is estimated for December 2015 and December 2016, a monetary base (broad) of Kz

1.680.467,40 Million and Kz 1.811.339,13 Million, respectively, which represents a

growth of 6,32% and 7,79%. In respect to the restricted monetary base, in December

2015 it is expected Kz 1.600.043,93 Million and December 2016 it is expected Kz

1.726.296,76, growth 29,28% and 7,89, respectively.

Monetary Aggregates

Between December 2010 and December 2014 the monetary aggregates M1 and M2

expanded from Kz 1.663.640,46 Million and Kz 2.589.839,20 Million, to Kz

3.096.861,62 Million and Kz 5.103.482,93, respectively, with the variation in M1

(82.16%) lower than M2 (94.33%). With regard to M3, this expanded 90.80% in the

same period. This behavior may reflect the slight increase in the preference for liquidity

and increased savings of economic agents and the conduct of monetary policy that has

been accommodative.

In light of the economic stability achieved in recent years, improvements in the

management of monetary policy were observed, with the introduction of new

operational framework of monetary policy and regulation (credit limitation in foreign

currency and New Foreign Exchange Law of the Petroleum Sector) in the period under

review. The national currency has gained more weight in the calculation of total

deposits, while foreign currency have reduced.

In 2010, the foreign currency deposits represent 54.16% of total deposits, while deposits

in national currency constituted only 45.84%; as a result of dedollarization policy of the

economy, there was an inversion in the structure of deposits by currency through

deposits in national currency representing 64.48% of total deposits and foreign currency

35.52%, representing a gain to the national economy reflecting the improved of

monetary policy conduct and scope of credit objectives in national currency.

Until August 2015, the Monetary M3 expanded by 5.40%, closing at kz 5.350.850,00

Million, this increase may be associated with expansion of net credit to the Central

Government in 134.63%. Although the observed expansion, the M3 is below the

programmed value for the year 2015, in which it is expected an increase of 11.45%.

Relative to M1 and M2, there is an increase of 4.30% and 5.48% respectively in the first

eight months of 2015.

Page 9

9

Figure 5: Monetary Aggregates

Source: BNA

The perspectives to December 2015 point to growth of M3 in 11,45% for 5.695.301,35

and an acceleration of 2.12 p.p. in 2016.

Claims to the Economy

The claims on the Economy are in an important measure of economic growth. The

current scenario shows an exponential growth of this indicator, between December 2010

and December 2014. With an increase of 77,91% over the last four years, claims on the

economy rose from Kz 1.656.245,31 Million in December 2010 to Kz 2.946.702,35

Million, in December 2014.

The private sector which constitutes the leverage engine of economic growth in any

economy, has seen its credit grow at 89,39%, changing from Kz 1.505.898,54 Million,

in December 2010 to 2.852.043,17 Million in December 2014, against the decline of

claims on the public sector in 37,04% (Kz 150.346,77 Million in 2010 to Kz 94.659,18

Million in 2014.

The claims on the Central Government growth at 983,29% between December 2010 and

December 2014. This reflected the Government’s response to the necessity of

investment in infrastructure in order to boost economic activity by creating a favorable

environment for domestic and foreign private investment.

Figure 6: Claims to the Economy

Page 10

10

Source: BNA

In 2015 claims to the economy grew 9,12%, due to increased claims on the private

sector (9,15%) and the claims on the public sector (7,97%).

The perspectives to December 2015 show a growth of 10,70% of claims to the

economy, supported by the growth of public claims and private in 45,125 and 9,56%,

respectively. For 2016, the previsions about the claim to the economy point a

deceleration of 0,31 b.p. to 2015

Inflation Rate

As monetary authority, the main purpose of the BNA has been, over 2014, to promote

price stability in Angola. In fact, inflation remained until June a continuous downward

trend, the month in which reached its historic low of 6,89%. After reaching this point,

inflation reversed to an upward trend that holds up to the present day. Annual inflation

closed the year of 2014 standing at 7,48%.

Figure 7: Annual I nflation Rate (%)

Source: BNA/INE

Page 11

11

The stability of the exchange rate Kz/USD throughout the first three quarters of 2014

was due to the food international prices at the international market and the performance

of the monetary policy.

However, the devaluation of the currency that has been observed, more sharply since

the last quarter of 2014 until today, has been one of the causes that seem to be pushing

the price level up. This devaluation was due to the shortage of foreign currency to enter

into the economy, therefore, the currency had to adjust its value until a balance between

demand and supply of foreign currency, anticipating the need to prevent deterioration of

international reserves.

After three years of single digit inflation and a significant deceleration, it is expected for

2015 a two digit inflation rate, 13,80% almost the same as the inflation registered in

2009 (13,99%).

However, the tight monetary policy, it’s helping to maintain the general level of prices

not higher than the actual levels.

C. Fiscal Sector Developments

Angola’s debt outlook appears manageable, as it is under 60.0%. According to the

government budget, Angola registered a debt of 37,78% in 2010, 30,64% in 2011,

27,53% in 2012, 24,53% in 2013 and 30,99% in 2014. For 2015 it is anticipated, again,

a rise that will result in a 43,99% of GDP.

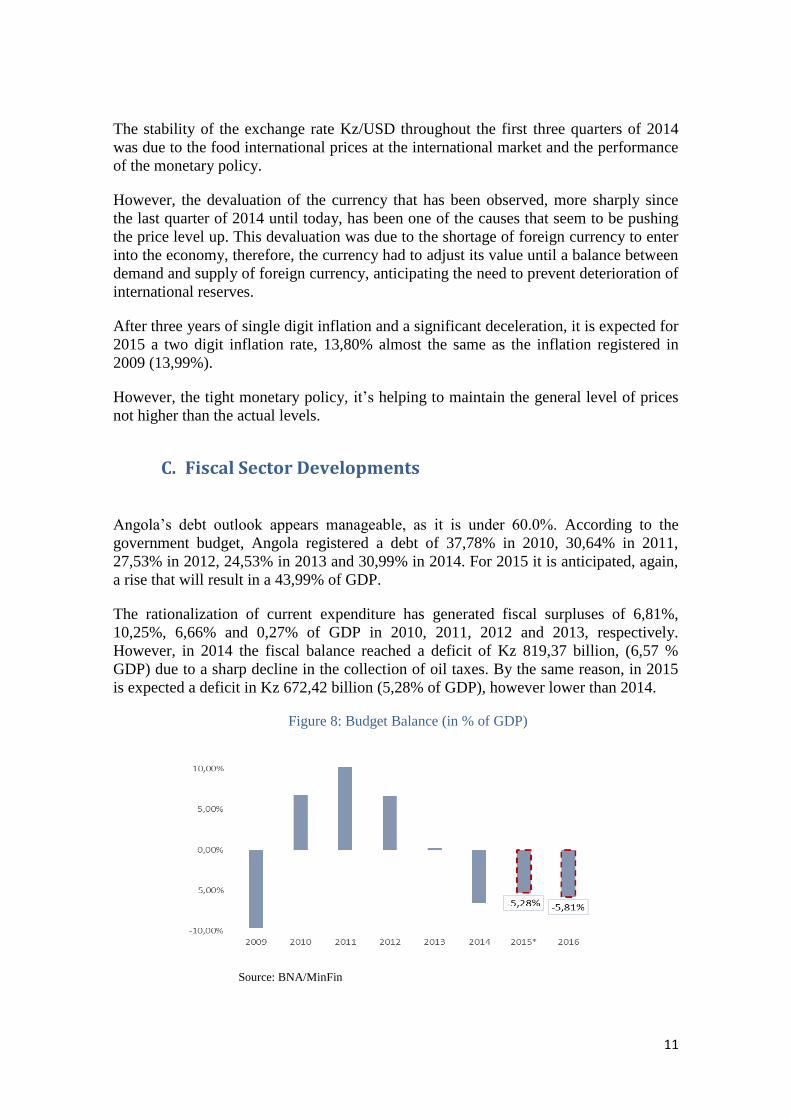

The rationalization of current expenditure has generated fiscal surpluses of 6,81%,

10,25%, 6,66% and 0,27% of GDP in 2010, 2011, 2012 and 2013, respectively.

However, in 2014 the fiscal balance reached a deficit of Kz 819,37 billion, (6,57 %

GDP) due to a sharp decline in the collection of oil taxes. By the same reason, in 2015

is expected a deficit in Kz 672,42 billion (5,28% of GDP), however lower than 2014.

Figure 8: Budget Balance (in % of GDP)

Source: BNA/MinFin

Page 12

12

Finally, reforms have been made in the tax system in order to allow an efficient

inspection of taxes collection. A new system is being implemented in order to increase

the non-oil taxes.

D. External Sector Developments

Current Account

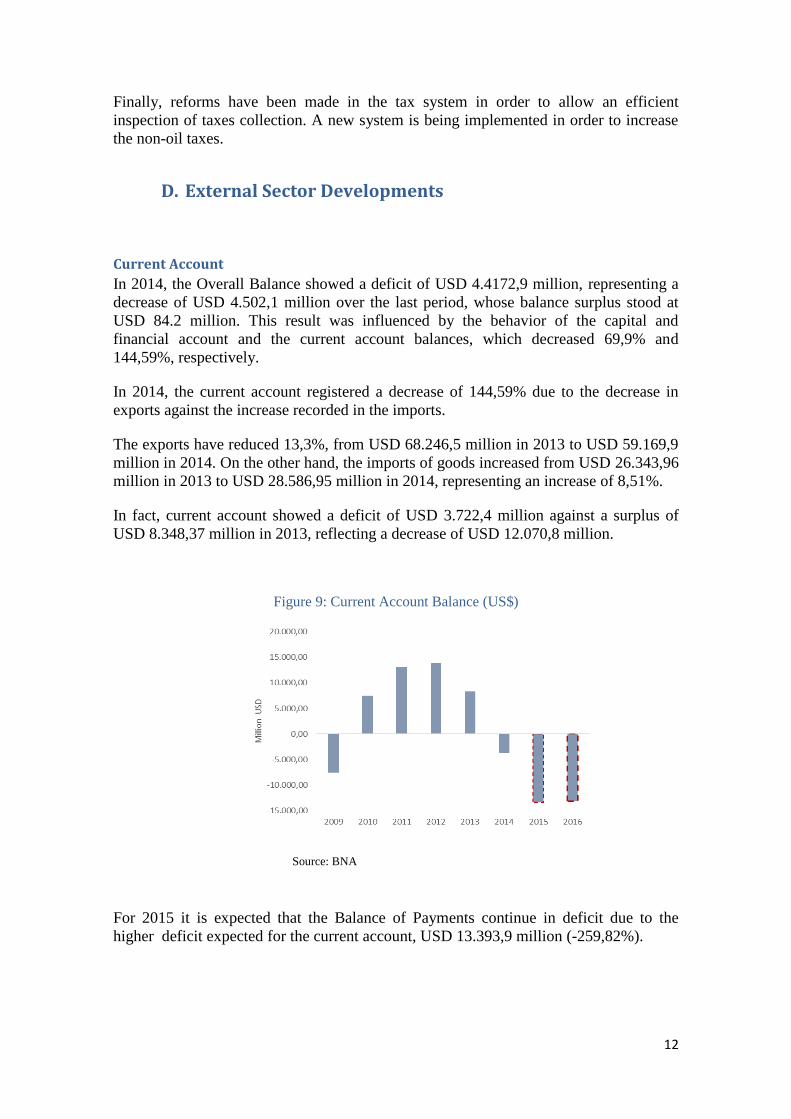

In 2014, the Overall Balance showed a deficit of USD 4.4172,9 million, representing a

decrease of USD 4.502,1 million over the last period, whose balance surplus stood at

USD 84.2 million. This result was influenced by the behavior of the capital and

financial account and the current account balances, which decreased 69,9% and

144,59%, respectively.

In 2014, the current account registered a decrease of 144,59% due to the decrease in

exports against the increase recorded in the imports.

The exports have reduced 13,3%, from USD 68.246,5 million in 2013 to USD 59.169,9

million in 2014. On the other hand, the imports of goods increased from USD 26.343,96

million in 2013 to USD 28.586,95 million in 2014, representing an increase of 8,51%.

In fact, current account showed a deficit of USD 3.722,4 million against a surplus of

USD 8.348,37 million in 2013, reflecting a decrease of USD 12.070,8 million.

Figure 9: Current Account Balance (US$)

Source: BNA

For 2015 it is expected that the Balance of Payments continue in deficit due to the

higher deficit expected for the current account, USD 13.393,9 million (-259,82%).

Page 13

13

Exchange Rate

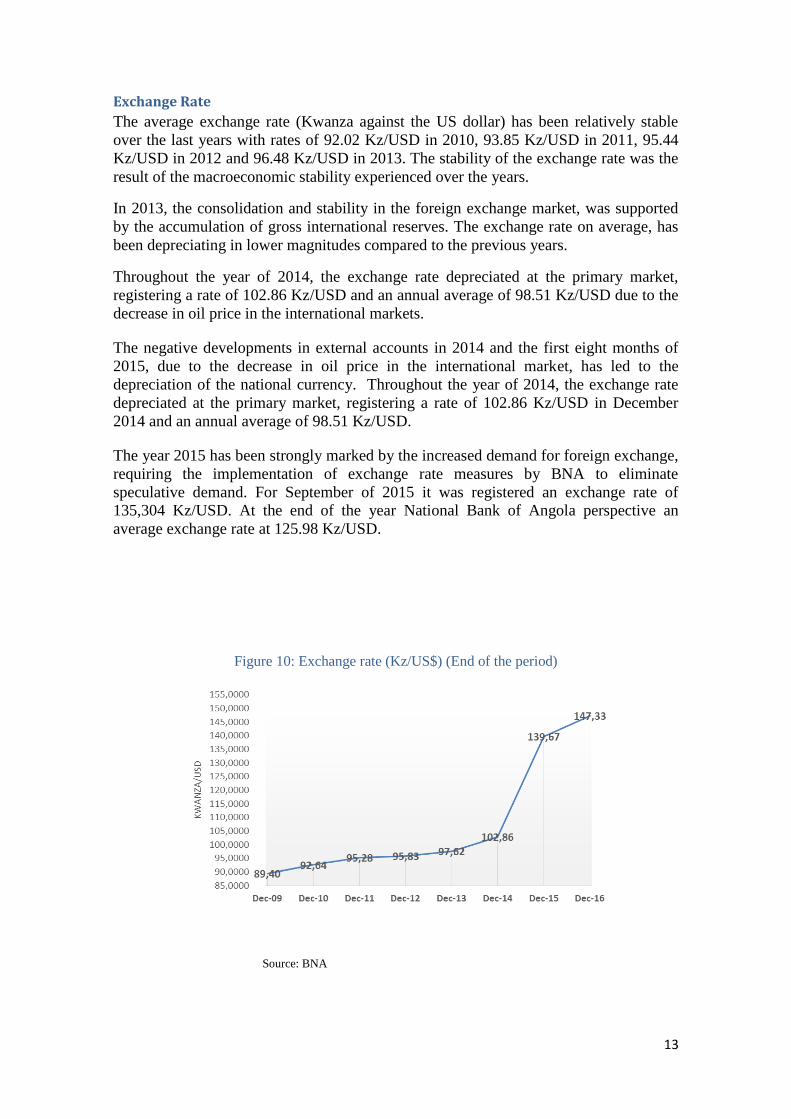

The average exchange rate (Kwanza against the US dollar) has been relatively stable

over the last years with rates of 92.02 Kz/USD in 2010, 93.85 Kz/USD in 2011, 95.44

Kz/USD in 2012 and 96.48 Kz/USD in 2013. The stability of the exchange rate was the

result of the macroeconomic stability experienced over the years.

In 2013, the consolidation and stability in the foreign exchange market, was supported

by the accumulation of gross international reserves. The exchange rate on average, has

been depreciating in lower magnitudes compared to the previous years.

Throughout the year of 2014, the exchange rate depreciated at the primary market,

registering a rate of 102.86 Kz/USD and an annual average of 98.51 Kz/USD due to the

decrease in oil price in the international markets.

The negative developments in external accounts in 2014 and the first eight months of

2015, due to the decrease in oil price in the international market, has led to the

depreciation of the national currency. Throughout the year of 2014, the exchange rate

depreciated at the primary market, registering a rate of 102.86 Kz/USD in December

2014 and an annual average of 98.51 Kz/USD.

The year 2015 has been strongly marked by the increased demand for foreign exchange,

requiring the implementation of exchange rate measures by BNA to eliminate

speculative demand. For September of 2015 it was registered an exchange rate of

135,304 Kz/USD. At the end of the year National Bank of Angola perspective an

average exchange rate at 125.98 Kz/USD.

Figure 10: Exchange rate (Kz/US$) (End of the period)

Source: BNA

Page 14

14

Although the high depreciation of the national currency, the National Bank Of Angola

has taken a conservative approach to international reserves, in line with developments

on the oil price in the international markets, opting to make a rigorous and prudent

management, in order to remain at stable levels, being able to absorb the existing

imbalances in balance of payments and not compromise future sustainability.

International Reserves

In 2015 the gross international reserves declines to USD 24.772 Million, while the

liquid international reserves decline to USD 24.510 Million, however its lowest value

was reached in July, USD 24.170 Million

Figure 11: Net International Reserves & Months of Imports

Source: BNA

Although the imbalance in balance of payments, resulting in inflows of foreign currency

lower than outflows and causes the reduction of international reserves, months of

imports stand at 6.70 in August 2015 showing a positive change from to 6.50 observed

at the beginning of the year and perspective that at the end of the year are located in

6.61, which indicates that international reserves are stable and remain at adequate levels

given the country's external needs and functioning as capital buffers to ensure national

needs and the resilience of the economy to external shocks.

The latest estimates for 2015 suggest international reserves equivalent to 6.61 months,

Gross Reserves / GDP of 22.4% and Debt Service / Gross Reserves of 26.8%. Although

estimates of international reserves in general reflect deterioration compared to 2014,

they are above the limit of six months recommended by the SADC, and the golden rule

of three months recommended by the IMF, indicating that the external sustainability it’s

assured.

Page 15

15

In the end of 2016, the National Bank of Angola perspective an exchange rate of 147.32

Kz/USD and an average exchange rate of 143.82 Kz/USD. For the Net International

Reserves and month of imports expect for next year a reduction to Usd 17.924,40

Million and 5,40 months, respectively.

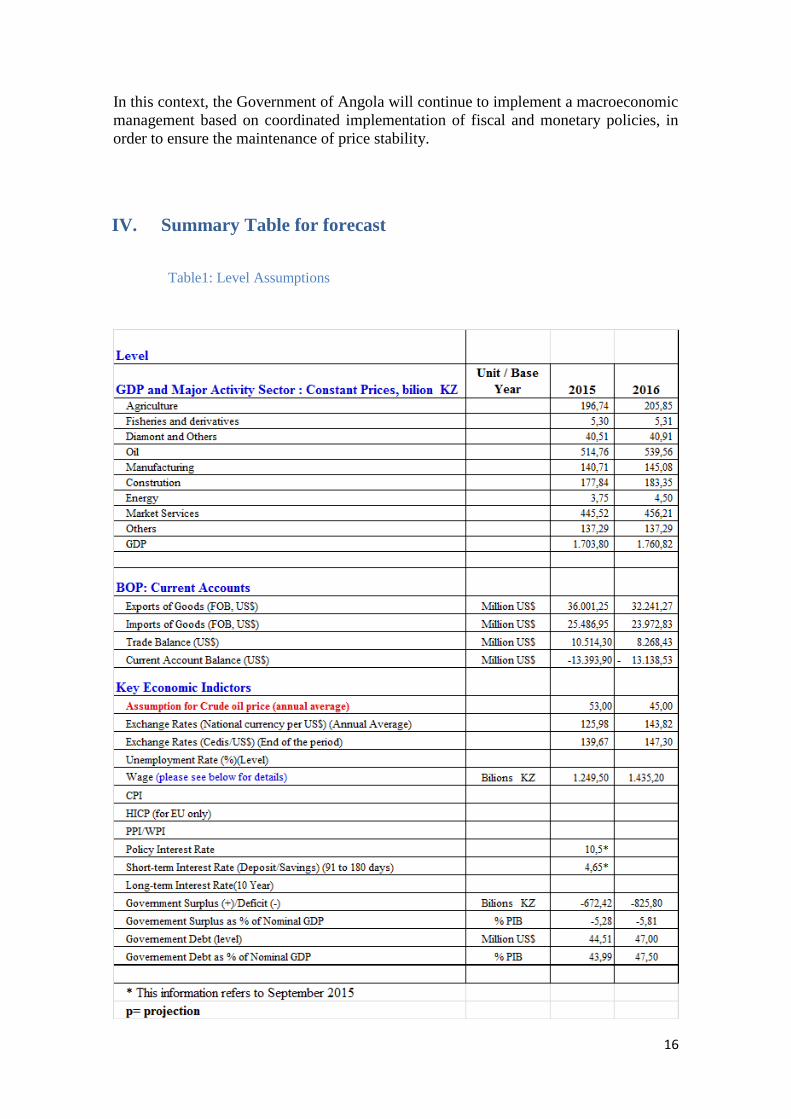

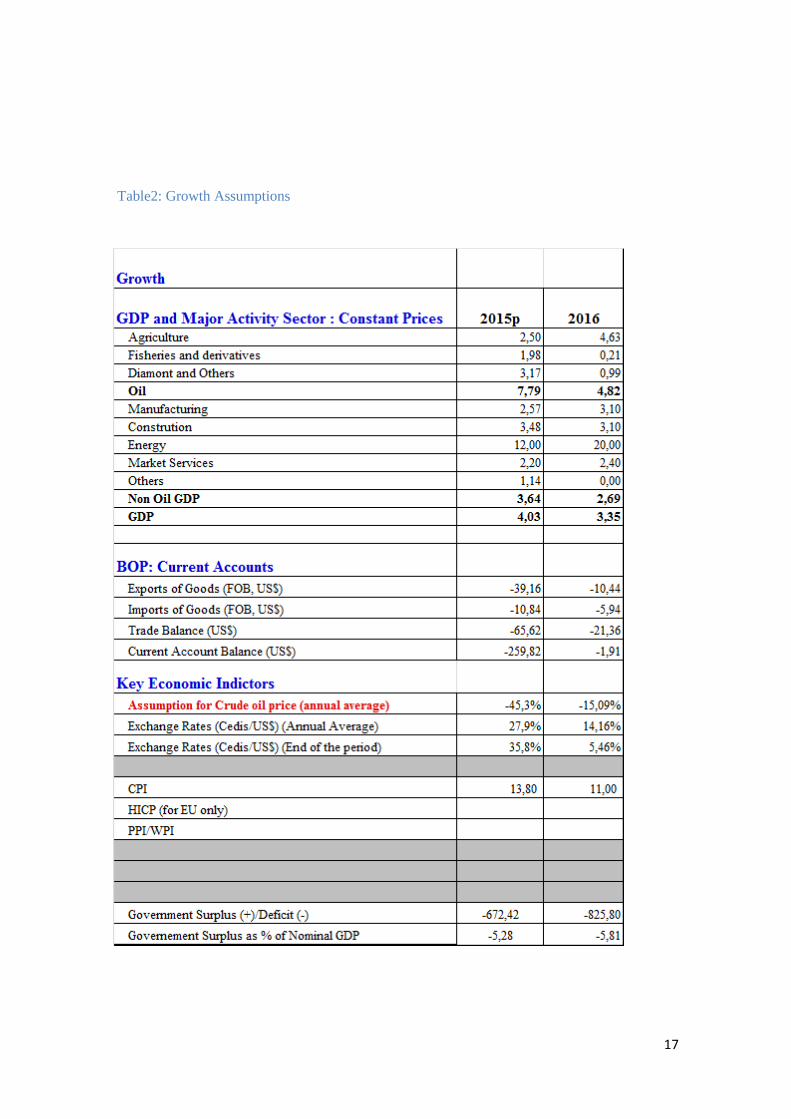

III. Forecast Summary –Policy issues and Uncertainties

The year 2015 will be a challenging year for the Angolan economy. The reduction in the

price of oil, accounting for about 95% of Angolan exports and the high dependence on

foreign imports, despite the gradual increase in domestic production, puts a special

attention to the Angolan economy, due to a slowdown in the economic growth and the

current account deficit. Therefore, for the oil prices, in 2015 and 2016 it is predicted

USD 53 and USD 45 respectively.

In 2015 is expected a slightly lower growth of the Angolan economy (4,03%) compared

to 2014 (4,75%), scenario that could have been worse, if not for the real growth of the

oil sector (7,79%). For 2016, it is expected an even lower growth of 3,35%

It is also anticipated a not so good scenario for the fiscal and external position in 2015,

where can be foreseen a deficit for both the Budget Kz 672,42 billion (5,28% of GDP),

and the Balance of payments mainly due to the current account deficit USD 13.393,9

million (-259,82% compared to 2013). For 2016 the Budget will register a deficit of Kz

825, 80 billion and the current account a deficit of USD -13.138,53 million.

For 2015 and 2016 it is anticipated, again, a rise of the debt that will result in a 43,99%

and 47,50% of GDP, respectively, coming from a position of 30,99% of GDP in 2014,

in a context were estimates for 2015 suggest international reserves equivalent to 6.6

months and 5,4 for 2016 . Although estimates of international reserves in general reflect

deterioration compared to 2014, in 2015 they are above the limit of six months

recommended by the SADC, and the golden rule of three months recommended by the

IMF, indicating that the external sustainability it’s assured.

And finally, at the end of the current year National Bank of Angola perspective an

average exchange rate of 125.98 Kz/USD and 143,82 Kz/USD for 2016. A two digit

inflation rate is predicted for 2015, 13,80% almost the same as the inflation registered in

2009 (13,8%). Nevertheless, for 2016 the prevision indicates a lower inflation of 11%

even though, this entire scenario is putting some pressure to the authorities.

In this sense the Executive is studying the implementation of a set of measures to

increase the diversification of the Angolan economy, with a view to increase even more

the domestic production and reduce the dependence on imports of goods and services as

well as the oil sector weight in the national economy. The reduction in the oil sector

activity, leading provider of dollars of Angola's economy, will be a constraint on

business activity.

Page 16

16

In this context, the Government of Angola will continue to implement a macroeconomic

management based on coordinated implementation of fiscal and monetary policies, in

order to ensure the maintenance of price stability.

IV. Summary Table for forecast

Table1: Level Assumptions

Page 17

17

Table2: Growth Assumptions