160

ANNUAL REPORT 2017 2018

ANNUALREPORT

20172018

Service Excellence Honesty and Integrity Respect Social Responsibility

To be a major player in Energy Sector development, nationally and regionally.

To meet the needs of our customers in a sufficiently profitable and environmentally sound way through providing reliable and safe power supply of acceptable quality.

MISSION

CORE VALUES

VISION

Keepingcustomers

informed andeducated

Continuouslydelivering

value

Being there when our customers need us

Delivering secure,

affordable and sustainable

solutions

OUR ENERGY GOES INTO:

Directors’ Responsibility Statement 66

Independent Auditor’s Report 67

Directors’ Report 70

Statement of Comprehensive Income 74

Statement of Financial Position 75

Statement of Changes in Equity 76

Statement of Cash Flows 77

Notes to the Financial Statements 78 -154

1

CONTENTSOVERVIEWAbout This Report 2

The Ministry in Charge of EEC 5

From EEC to Customer 6

Highlights - Key Indicators 8

Facts and Figures 10

Key Statistics 11

Technical Performance 12

GOVERNANCE Board of Directors 14

Executive Management 16

BUSINESS REVIEWChairperson’s Statement 18

Managing Director’s Report 21

Operations Report 25

Customer Service Report 35

Human Capital Report 42

Sustainability Report 52

Corporate Social Investment 59

FINANCIAL STATEMENTS

OVERVIEW | ABOUT THIS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

2

ABOUT THIS REPORT

mong the major changes experienced in the

Company was the change of name and re-

branding from the Swaziland Electricity Company

(SEC) to EEC. Other than that, there have been no

significant changes in terms of size, structure, ownership

and supply chain.

Our external auditors have provided a realistic scrutiny of

our financial performance. This report follows a reporting

framework that is in line with best practice. It links our

strategic objectives, governance and financial performance

with the societal, sustainability and economic context in

which EEC operates.

We aim to provide our stakeholders with greater and better

insight into how we implement our strategy and how this

impacts society. While our approach in compiling this

Annual Report is guided by global standards, we seek

to apply the universal principles in a manner that makes

sense to our local environment. We will continue to mature

this format of reporting in future years.

CORE BUSINESS

EEC is a power generating, transmitting and distributing

company that operates in the Kingdom of Eswatini. It is

a public company accountable to Their Majesties and the

people of Eswatini. This is given life through a variety of

clearly defined laws, codes and moral obligations. The

company is wholly owned by the Government of the

Kingdom of Eswatini. The Ministry of Natural Resources

and Energy is the shareholder representative. There

are regular and formal interactions between EEC and

the Ministry to discuss governance and strategic issues.

EEC operations are largely supported by over 85 sub-

contractors owned by emaSwati, who, in turn, provide

employment to close to a thousand people. We currently

have over 200 000 customers who include agricultural,

industrial, commercial and residential households.

In 2007 EEC transformed from being the Swaziland

Electricity Board (SEB) to become a company governed

under the Swaziland Companies Act 2009. In 2018 the

company was renamed EEC in line with the official change

This Annual Report sets out how Eswatini Electricity

Company (EEC) performed in the 2017/18 financial

year ended 31 March 2018. This report fulfils one

of our key responsibilities being accountable to

all our stakeholders, namely, the shareholder,

customers, employees, business partners and the

general public. This is an important principle which

speaks to our long-lived ethos to be a model and

transparent corporate citizen. To create value for

our stakeholders, it is essential for us to know what

issues are important to them. To ascertain that,

we have carried out what may be described as a

materiality analysis and included it in this report. We

focus on those aspects that are of great significance

to our strategy and stakeholders.

A

of name for the country from the Kingdom of Swaziland

to the Kingdom of Eswatini. Other pieces of legislation

at play in EEC is the Eswatini Electricity Company Act,

2007; The Electricity Act, 2007; Companies Act 2009;

The Energy Regulatory Act, 2007, as well as the Public

Enterprises Unit (Control and Monitoring) Act, 1989.

HUMAN CAPITAL

As a sustainability-focused company, EEC always

places high priority on the development of human talent

by investing in local specialists whose skills are up to

global standards. Human resources is the decisive factor

for the success and growth of any company. In the

year under review, EEC had a staff complement of 674

permanent employees and an additional 36 contracted

employees. The EEC employee body is highly unionised

with 85% subscribed to formal bargaining representation.

The Swaziland Electricity Supply Maintenance and

Allied Workers Union (SESMAWU) had 559 members,

representing 89% of non-managerial employees.

Meanwhile the National Electricity Supply Maintenance

and Allied Staff Association (NESMASA) had 25

members.

To that end, EEC has devised human resource systems

geared towards enabling its employees at all levels to

excel in a conducive and empowering environment. This is

in line with the country’s Vision 2022 for skills development,

training and creation of sustainable jobs. In addition, the

employees are evaluated, rewarded and compensated

based on their performances. The growth opportunities

have created a unique position for EEC to be among the

employers of choice in the Kingdom of Eswatini.

In order to continuously enhance results and reach our

goals, EEC has adopted processes and management

tools focused on standardising procedures and

operations, prioritising critical processes and rigid cost

control. The targets for each employee and team from

all areas and at each level of the hierarchy are defined

annually in accordance with the guidelines set by the

Board of Directors.

METHOD

A majority of the quantitative information contained in this

report has been specifically measured. Any information

that has been obtained by other means (for instance by

estimation or extrapolation) is identified as such. To a

considerable extent, all quantitative information in this

report is accompanied by comparative information from

prior years. In order to mirror the broad societal role of

EEC, the Board of Directors consists of external members

with a wide range of experience and knowledge from their

previous and current roles in areas such as engineering,

public administration, corporate governance and finance.

Through the efforts of our Board, Executives, a number

of other professional employees and consultants, we

have captured a summary of what can be considered

international best practice. This was an attempt to

capture ongoing discussions from various platforms and

synthesise them into best practice.

Highlights of 2017/18

The implementation of new processes and technologies has

resulted in continued operating efficiency gains throughout

the company’s operations. Based on the strategic initiatives

to drive operational efficiency, management continues to

monitor and implement austerity measures. Further, the

company is monitoring its financial liabilities and there is

no reason to believe that it will not be able to settle them

as they arise.

• EEC made revenue amounting to E2.25 billion

compared to E 1.8 billion in 2017; that is an increase

of 25%.

• The number of customers increased by 12% from

182,562 in March 2017 to a total of 203,584 customers

in March 2018.

• Operating profit stands at E603 million in 2018

compared to E148 million in 2017.

• Total non-current assets were E3.033 billion in 2018

compared to E2.839 billion in 2017.

• Internal generation production increased from

118.9GWh in 2017 to 207.8GWh, as at 31 March

2018. On average, internal generation contributes

20% of the total annual energy demand for the

country and the balance is imported.

• Maguga Hydro Power has improved its contribution to

34.3% compared to 4% in the previous year.

• There was a significant increase of electricity traded

in the SAPP Markets (DAM) from 6% to 14% due to

favourable prices and availability.

• There was improvement in EEC’s safety record in the

2017/18 period. The number of reportable injuries fell

by a further 4.76% and the number of minor public

injuries fell by 100% when compared to 2016/17.

• The company also identified a strategic plan to

transition from Occupational Health and Safety

Management Standard (OHSAS 18001:2007) to ISO

45001:2018.

OVERVIEW | ABOUT THIS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

3

The Honourable Minister of Natural Resources and Energy Senator Jabulile Mashwama

Ministry of Natural Resources and Energy Principal Secretary Mrs Winnie Stewart

THE MINISTRY IN CHARGE

OVERVIEW | THE MINISTRY IN CHARGE

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/185

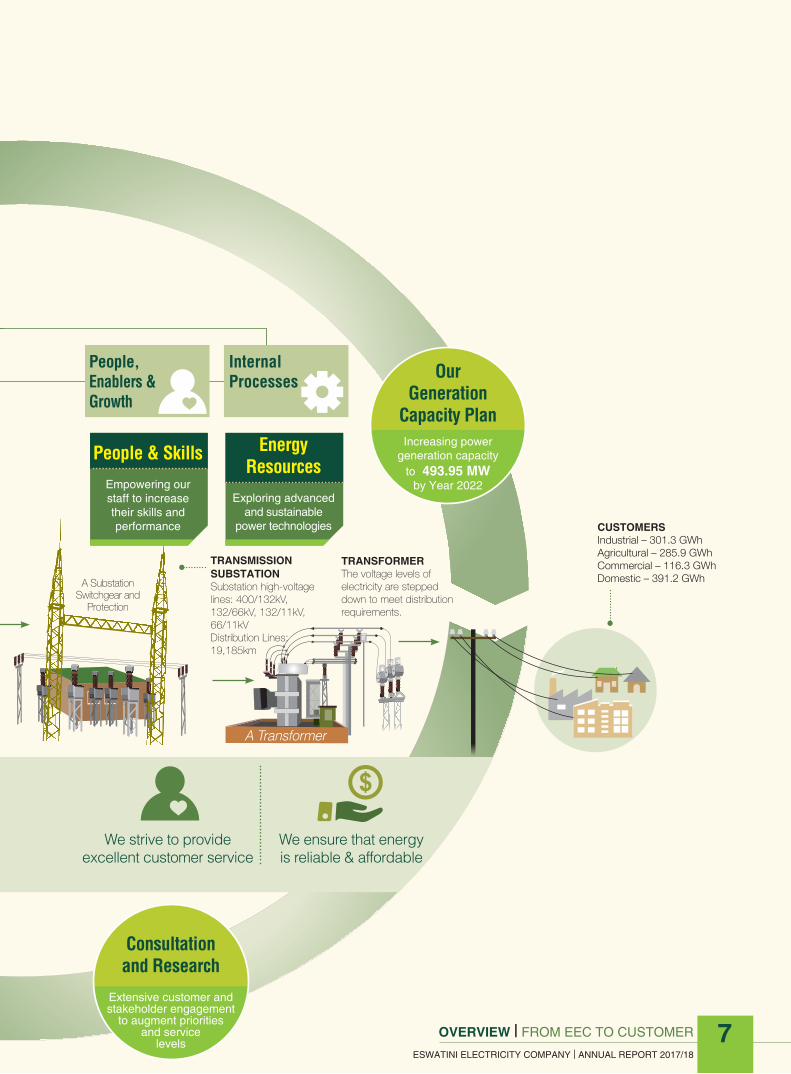

FROM EEC TO CUSTOMER

OVERVIEW | FROM EEC TO CUSTOMER

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

6

Taking Responsibility for Energy,

our People and the Environment

Balanced Scorecard Objectives

We understand our impact on the environment and act

responsibly

We offer free information on energy saving methods

Our Five-Year

PlanMaintaining and enhancing

services to efficientlymeet customers’

priorities

POWER GENERATIONOutput: Total electricity generated – 119.0 GWh

TRANSMISSION HIGH VOLTAGE LINESAlternating Current (AC ) - 400kV - 146.83 kmAlternating Current (AC ) - 132kV - 296 kmAlternating Current (AC ) - 66kV - 969.68 km

Funding

Dependent on customer

affordability and our financeability

Resources

Managing our resources profitably

and sustainably

Power Station

Customer Benefits

Financial Results

OVERVIEW | FROM EEC TO CUSTOMER

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

7

Balanced Scorecard Objectives

We ensure that energy is reliable & affordable

People, Enablers & Growth

Internal Processes

We strive to provideexcellent customer service

Consultationand Research

Extensive customer andstakeholder engagement

to augment prioritiesand service

levels

Our Generation

Capacity PlanIncreasing power

generation capacity to 493.95 MW

by Year 2022

TRANSFORMERThe voltage levels of electricity are stepped down to meet distribution requirements.

TRANSMISSION SUBSTATIONSubstation high-voltage lines: 400/132kV, 132/66kV, 132/11kV, 66/11kVDistribution Lines: 19,185km

CUSTOMERS Industrial – 301.3 GWhAgricultural – 285.9 GWhCommercial – 116.3 GWhDomestic – 391.2 GWh

People & Skills

Empowering ourstaff to increasetheir skills andperformance

Energy Resources

Exploring advancedand sustainable

power technologies

A Substation Switchgear and

Protection

A Transformer

HIGHLIGHTS - KEY INDICATORS

OVERVIEW | HIGHLIGHTS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

8

2015/16 2016/17 2017/182014/152013/14

350

300

250

200

150

100

50

0

35%

30%

25%

20%

15%

10%

5%

0

9,6%

16,8%

10,0%

Internal Generation (GWh) Contribution to System (%)

Con

tribu

tion

to S

yste

m %

GW

hG

Wh

26,0%

25,0%

Internal Generation (GWh) and Contribution to System (%)

Figure 1

Figure 2

Figure 3

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

40

35

30

25

20

15

10

5

0

Monthly Energy Generation, GWh

2014/15 2015/16 2016/17 2017/18

120

100

80

60

40

20

0

2013/14

Ezulwini Edwaleni MaguduzaMaguga

2014/15 2015/16 2016/17

GW

h

Annual Generation Per Station

2017/18

OVERVIEW | HIGHLIGHTS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

OVERVIEW | HIGHLIGHTS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

9

Total Customers

Total Number of Customers

Total Electricity Revenue (E-Million)

Annual Sales Revenue

Annual Unit Sales (GWh)

Num

ber

of U

nits

Annual Unit Sales

1,100.0

1,050.0

1,000.0

950.0

900.0

850.0

Average Market Price Increase vsApproved Tariff Price Increases

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

Average Increase (Import) Approved Increase

15.3% 10.0% 9.9% 2.7%13.2%8.3% 5.0% 11.7% 11.7% 14.6%

% In

crea

se

Figure 4 Figure 5

Figure 6 Figure 7

Figure 8 Figure 9

1,08

4.1

1,62

4.0

1,9

45.9

1,07

4.4

1,03

4.2

2017/18 Station Contribution to Internal Generation (%)

Ezulwini

Maguga Edwaleni

Maguduza

2013/14 2014/15 2015/16 2016/17 2017/18

2013/14 2014/15 2015/16 2016/17 2017/18

Rev

enue

Am

ount

(Mill

ions

)

20,000.018,000.016,000.014,000.012,000.010,000.0

800.0600.0400.0200.0

0

1,6

24.1

1,49

7.8

1,9

45.9

1,33

7.2

1,17

5.3

2013/14 2014/15 2015/16 2016/17 2017/18

Num

ber

of C

usto

mer

s 240,000220,000200,000180,000160,000140,000120,000100,00080,00060,00040,00020,000

0

164,

231

182,

562

203

584

150,

668

134,

765

2013/14 2014/15 2015/16 2016/17 2017/18

10.09.08.07.06.05.04.03.02.01.0

0

2014/15 2016/17 2017/182015/162013/14

M3 /S

ecLuphohlo Dam Monthly Average Inflows

34%

11%

34%

21%Apr-1

7

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

FACTS AND FIGURES

OVERVIEW | FACTS AND FIGURES

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

10

2018 2017 2016 2015 2014 E’000 E’000 E’000 E’000 E’000 INCOME STATEMENT

Energy Sales (GWh) 1 094.8 1 058.4 1 084.1 1 074.4 1 034.6

Revenue 2 253 819 1 786 407 1 586 476 1 474 681 1 264 528

Other Income (excluding grant armotisation) 12 105 13 933 20 528 13 400 18 000

2 265 924 1 800 340 1 607 004 1 488 081 1 282 528

Operating Expenses 1 517 340 1 524 483 1 468 894 1 234 967 1 087 938

Depreciation 131 591 133 327 117 318 116 118 104 458

Amortisation of Grants (15 408) (43 084) (27 349) (12 613) (10 456)

Net Finance Cost 21 913 35 450 34 448 26 840 22 921

Other (Gains)/Losses 28 992 37 273 (70 100) 2 703 23 845

Share of Profit in Joint Venture (31 850) (40 273) (48 965) (43 413) (27 318)

Taxation 76 285 9 015 38 505 22 523 2 570

Total Costs 1 728 863 1 656 191 1 512 751 1 347 125 1 203 958

Profit 537 061 144 149 94 253 140 956 140 956

BALANCE SHEET Property, Plant and Equipment 2 233 996 2 056 047 1 839 759 1 750 822 1 525 748

Capital Work in Progress 75 953 40 233 69 861 68 138 54 654

Investment in Joint Venture 324 182 361 174 407 485 312 404 261 888

Derivative Financial Instruments 24 273 32 256 55 218 42 396 59 018

Investment in Sinking Fund 209 156 183 925 187 023 58 120 30 000

Other Assets 27 788 4 810 6 242 28 206 23 064

Retirement Benefits Assets 3 557 4 141 7 181 6 432 796

Ubombo Sugar Ltd Electricity Prepayment 70 000 80 000 90 000 100 000 110 000

Embedded Derivative Asset 63 959 76 796 84 366 38 725 2 538

Current Assets 608 073 336 931 279 083 305 339 328 041

Total Assets 3 640 937 3 176 313 3 026 218 2 720 582 2 395 747

Current Liabilities (480 435) (552 069) (444 189) (377 419) (297 692)

3 160 506 2 624 244 2 582 029 2 343 163 2 098 055

FUNDS EMPLOYED Borrowings 241 527 261 175 323 652 311 970 352 119

Embedded Derivative Liability 145 116 148 055 163 038 151 871 122 230

Deferred Grant Income 299 916 306 971 282 661 251 834 192 687

Other Deferred Income 27 788 4 810 6 242 28 206 23 064

Derivative Financial Instruments 785 1 059 1 412 2 662 3 310

Deferred Tax Liability 289 680 237 261 239 710 184 391 156 169

Shareholder’s Funds 2 155 694 1 664 913 1 565 314 1 412 229 1 248 476

3 160 506 2 624 244 2 582 029 2 343 163 2 098 055

2018

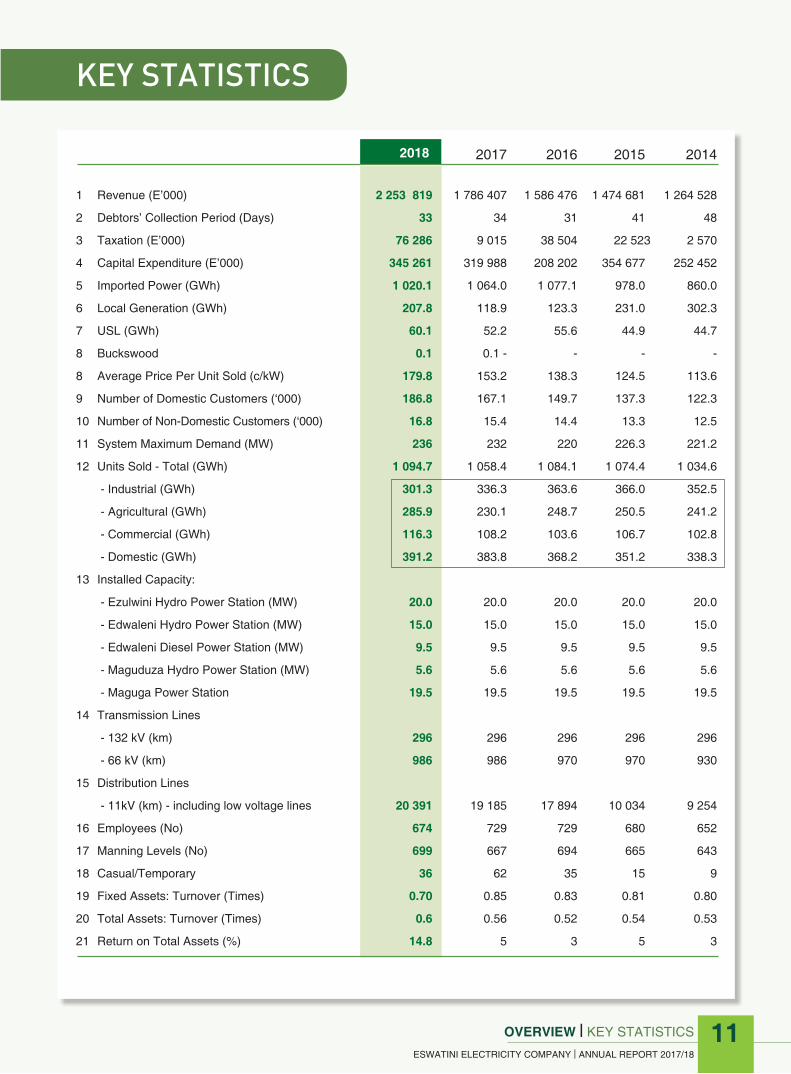

KEY STATISTICS

OVERVIEW | FACTS AND FIGURES

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

OVERVIEW | KEY STATISTICS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

11

2017 2016 2015 2014

1 Revenue (E’000) 2 253 819 1 786 407 1 586 476 1 474 681 1 264 528

2 Debtors’ Collection Period (Days) 33 34 31 41 48

3 Taxation (E’000) 76 286 9 015 38 504 22 523 2 570

4 Capital Expenditure (E’000) 345 261 319 988 208 202 354 677 252 452

5 Imported Power (GWh) 1 020.1 1 064.0 1 077.1 978.0 860.0

6 Local Generation (GWh) 207.8 118.9 123.3 231.0 302.3

7 USL (GWh) 60.1 52.2 55.6 44.9 44.7

8 Buckswood 0.1 0.1 - - - -

8 Average Price Per Unit Sold (c/kW) 179.8 153.2 138.3 124.5 113.6

9 Number of Domestic Customers (‘000) 186.8 167.1 149.7 137.3 122.3

10 Number of Non-Domestic Customers (‘000) 16.8 15.4 14.4 13.3 12.5

11 System Maximum Demand (MW) 236 232 220 226.3 221.2

12 Units Sold - Total (GWh) 1 094.7 1 058.4 1 084.1 1 074.4 1 034.6

- Industrial (GWh) 301.3 336.3 363.6 366.0 352.5

- Agricultural (GWh) 285.9 230.1 248.7 250.5 241.2

- Commercial (GWh) 116.3 108.2 103.6 106.7 102.8

- Domestic (GWh) 391.2 383.8 368.2 351.2 338.3

13 Installed Capacity:

- Ezulwini Hydro Power Station (MW) 20.0 20.0 20.0 20.0 20.0

- Edwaleni Hydro Power Station (MW) 15.0 15.0 15.0 15.0 15.0

- Edwaleni Diesel Power Station (MW) 9.5 9.5 9.5 9.5 9.5

- Maguduza Hydro Power Station (MW) 5.6 5.6 5.6 5.6 5.6

- Maguga Power Station 19.5 19.5 19.5 19.5 19.5

14 Transmission Lines

- 132 kV (km) 296 296 296 296 296

- 66 kV (km) 986 986 970 970 930

15 Distribution Lines

- 11kV (km) - including low voltage lines 20 391 19 185 17 894 10 034 9 254

16 Employees (No) 674 729 729 680 652

17 Manning Levels (No) 699 667 694 665 643

18 Casual/Temporary 36 62 35 15 9

19 Fixed Assets: Turnover (Times) 0.70 0.85 0.83 0.81 0.80

20 Total Assets: Turnover (Times) 0.6 0.56 0.52 0.54 0.53

21 Return on Total Assets (%) 14.8 5 3 5 3

2018

TECHNICAL PERFORMANCE

OVERVIEW | TECHNICAL PERFORMANCE

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

12

2018 2017 2016 2015 2014 1 System Requirements (GWh) Sent Out 1 289.9 1 217.2 1 256.0 1 255.4 1 205.22 Units Sold (GWh) 1 094.71 1 058.4 1 084.1 1 074.4 1 034.63 System Losses (%) 14.9 14.2 13.7 14.4 14.24 EEC Internal Generation (GWh) 208.0 119.0 123.3 231.0 302.35 EEC Internal Generation (%) 16.1 9.6 9.8 19 256 System Maximum Demand (MW) 236 232 220 226.8 221.2

Ratios and Statistics 1 Net Income to Revenue (%) 23.8 8.1 5.9 9.6 6.2 2 Operating Income to Revenue 26.8 8.3 7.5 10.0 6.1 3 Return on Equity 24.9 8.7 6.0 10.0 6.3 4 Return on Capital Employed 19.3 5.5 3.7 6.0 3.7 5 Return on Total Assets 14.8 4.5 3.1 5.2 3.3

Debt Management Ratios 1 Debt/Equity 0.2 0.2 0.2 0.2 0.3 2 Annual Debt Service (Times) 18.4 22.0 17.1 16.1 12.3

Liquidity Ratios 1 Current Ratio 1.3 0.6 0.6 0.8 1.1 2 Acid Test Ratio 1.2 0.5 0.5 0.7 0.9

Training 1 Training Expenditure (E’000) 7 216 8 199 9 797 12 731 8 954

Other 1 Consumer Price Index (%) 5.0 6.0 7.8 4.7 5.1 2 EEC Tariff Increase (%) 14.6 11.7 11.7 5.0 8.3

OVERVIEW | TECHNICAL PERFORMANCE

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

GOVERNANCE | BOARD OF DIRECTORS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/1814

BOARD OF DIRECTORS

MR S’THOFENI GININDZA (Chairperson)

Business Leadership – Stanford University, USA

MA Economics – Ottawa, Canada BA Economics – UNISWA

CHIEF VELAMUVA MASEKO (Non–Executive Director)

N3 & N4 Pulp and Paper Technology – Pretoria Technikon

Member of Usuthu Royal Trust – Tibiyo Taka Ngwane

Member of Senate (2008-2013)

PRINCESS LOMAJUBA (Non–Executive Director)

BSc – Western Kentucky University (USA)

Associate Degree in Science (Hotel

Management) – Vincent’s University

(USA)

ServSafe Food Protection Certification

– Vincent’s University Junior College

(USA)

MR MESHACK KUNENE (Managing Director)

B. Eng (Electrical and Electronics Engineering) – UK

Electricity Distribution Management – Sweden

Executive Development Programme (Stanford University) – USA

Member of the South African Institute of Electrical Engineers (MSAIEE)

GOVERNANCE | BOARD OF DIRECTORS

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

15

MR VUSI DLAMINI (Non–Executive Director)

Masters Degree (Economics of Education) – University of London

BA Degree – University of Swaziland

MS LINDIWE DLAMINI (Non–Executive Director)

MSc (Geography, Archaeology & Environment) – University of Witwatersrand

BSc Honours (Environmental Management) – University of South Africa

BSc Chemical Engineering – University of Cape Town

MR DUMISANI DLAMINI(Non–Executive Director)

Masters in Accounting and Finance – University of Stirling (UK) Bachelor of Commerce (B.com)

University of Swaziland Diploma in Accounting & Business

Studies – University of Botswana and Swaziland

ACCA and Research Attachment – De Montfort University (UK)

Short-Term Insurance – The Insurance Institute of South Africa

MR VELAPHI DLAMINI(Legal Counsel & Company Secretary)

Admitted Attorney Certificate in Conflict Management Certificate in Legislative Drafting LLB – UNISWA BA Law – UNISWA International Environmental Law

- Certificate from the University of Witwatersrand Climate Change and Energy Law

- Certificate from the University of Witwatersrand

MS DUDU NYEMBE (Non–Executive Director)

MBA – University of Pretoria (GIBS) Association of Certified Chartered

Accountants (ACCA) (Professional Level)

Bachelor of Commerce (B.Com) Accounting – University of Swaziland

MR JOSEPH SHILUBANE (Non–Executive Director)

Human Resource Management Training – UNISA

Management Development Programme – SBL

Trainer Development Programme – Maccauvlei

Mech. Eng. Technician – City & Guilds Exective Development Programme (WBS)

B. Eng (Electrical and Electronics Engineering) – UK

Electricity Distribution Management – Sweden

Executive Development Programme (Stanford University) – USA

Member of the South African Institute of Electrical Engineers (MSAIEE)

MSc Electrical Engineering – University of Cape Town

MBA Marketing – Regent Busi-ness School, RSA

Higher National Diploma (HND) – Electrical and Electronics Engineering, UK

Ordinary National Diploma (OND) – Engineering, UK

Management of Electric Power Utilities, Sweden

Member of The Institution of Engineering and Technology (MIET), UK

Masters in Investment & Risk Finance – UK

BCompt. Honours (Accounting Sciences) – UNISA

Post-Graduate Diploma in Accounting Sciences – UNISA

Bachelor of Commerce – UNISWA

Chartered Accountant Swaziland – CA (SD)

Chartered Accountant South Africa – CA (SA)

Executive Development Programme (INSEAD)

B.Comm Management Sciences – UNISWA

Leadership Development Programme – GIBS

Certified Global Remuneration Practitioner (GRP)

Leading Change (LCOR) – Harvard

Member IPM (SD)

MR LAWRENCE NSIBANDZEGeneral Manager Finance

MS NONCEDO MAMBAGeneral Manager

Corporate Services

MR MESHACK KUNENEManaging Director

MR LUKE MSWANEGeneral Manager

Resources & Strategy

GOVERNANCE | EXECUTIVE MANAGEMENT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/1816

ResponsibilitiesCorporate Strategy & Vision, Capital Allocation and Team Building.

ResponsibilitiesResearch & Development, Coordination of IPP Projects, Power System Planning, Corporate Strategy.

ResponsibilitiesFinance, Information Technology and Procurement.

ResponsibilitiesFacilities Management, Human Capital Management & Development and Employee Relations.

EXECUTIVE MANAGEMENT

BA (Honours) – Accounting and Finance – UK

Master of Business Administration – UK

Executive Development Programme (INSEAD)

Fellow Association of Certified Chartered Accountants (FCCA) – UK

Registered Accountant (SD)

MBA – University of Pretoria (GIBS)

B.Comm Accounting – UNISWA Fellow Certified Chartered

Accountant (FCCA) Chartered Accountant Swaziland –

CA (SD) Fellow Certified Internal Auditor

(FCIA)

Masters in Engineering (Engineering Management) – University of Pretoria – SA

MBA - University of Stellenbosch – SA

BSc Engineering – University of the Witwatersrand SA

BSc & CDE – UNISWA Supervisory Development

Programme – Maccuavlei Middle Management

Development Programme – University of Johannesburg – SA

MBA – University of Pretoria (GIBS)

BSc Electrical Engineering – University of Cape Town

BSc Physics and Maths – UNISWA

Executive Development Programme (INSEAD)

MR ERNEST MKHONTAGeneral Manager

Operations

MR VUSI GAMAGeneral Manager Customer Service

MR PATRICK MATHUNJWAGeneral Manager Support Services

MS ELIZABETH MABUZAHead of Audit

GOVERNANCE | EXECUTIVE MANAGEMENT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

17

ResponsibilitiesSHERQ Management, GIS and Survey, Fleet Management, Outsourced Services.

ResponsibilitiesEvaluation of controls in governance and risk management processes.

ResponsibilitiesSystem Operation, Generation, Transmission and Distribution.

ResponsibilitiesCustomer Service, Key Accounts, Marketing & Commercial Services and Billing & Revenue Protection.

Mr S’thofeni Ginindza

CHAIRPERSON’SSTATEMENTMr S’thofeni Ginindza

Chairman

BUSINESS REVIEW | CHAIRPERSON’S STATEMENT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/1818

As a long-term player in the Kingdom

of Eswatini, we will continue with

our efforts to provide quality service,

strengthen partnerships with all

stakeholders and all with whom we

have come into contact.

he past year has been momentous for our country and its people; we reached the 50-year milestone since independence. This is

a significant moment to take stock of progress made over the years and look ahead to future plans aimed at fulfilling our country’s vision to bring about an export-driven, knowledge-based and industrialised economy. This vision, which we all embrace, seeks to ensure inclusive economic growth and a better life for all the people.

Coming as it does in this landmark period, I find honour in presenting our Annual Report for the year ended 31 March 2018. The information relating to our financial performance reflects significant achievements, not just for our company but the country as a whole.

New IdentityEmboldened by His Majesty King Mswati III’s pro-nouncement during the 50/50 Double Celebrations on 19th April 2018 that the country would henceforth revert to its original identity as the Kingdom of Eswatini, we have embraced the renewed momentum for growth by changing our name to Eswatini Electricity Company (EEC). At EEC, we embrace the new identity and we see it as a powerful tool for national cohesion, growth and development. We believe this is a crucial step for emaSwati to appreciate the true measure of their strength, including their ability to adapt to the severe economic and social headwinds sweeping through the continent. This change presents opportunities that can have a domino-effect on us to improve confidence in the country’s economy and spur sustainable and inclusive growth.

EEC’s Financial PositionJudging from our inspiring performance in the year under review, we have every reason to look to the

future with optimism. We are ready to play our part in renewed efforts to boost the country’s economy. Our fundamental purpose has always been to help power economic growth and raise the living standards of the people of Eswatini.

To that end, EEC is in a strong financial position, with assets valued at E3 billion, representing 7% increase from the previous year.

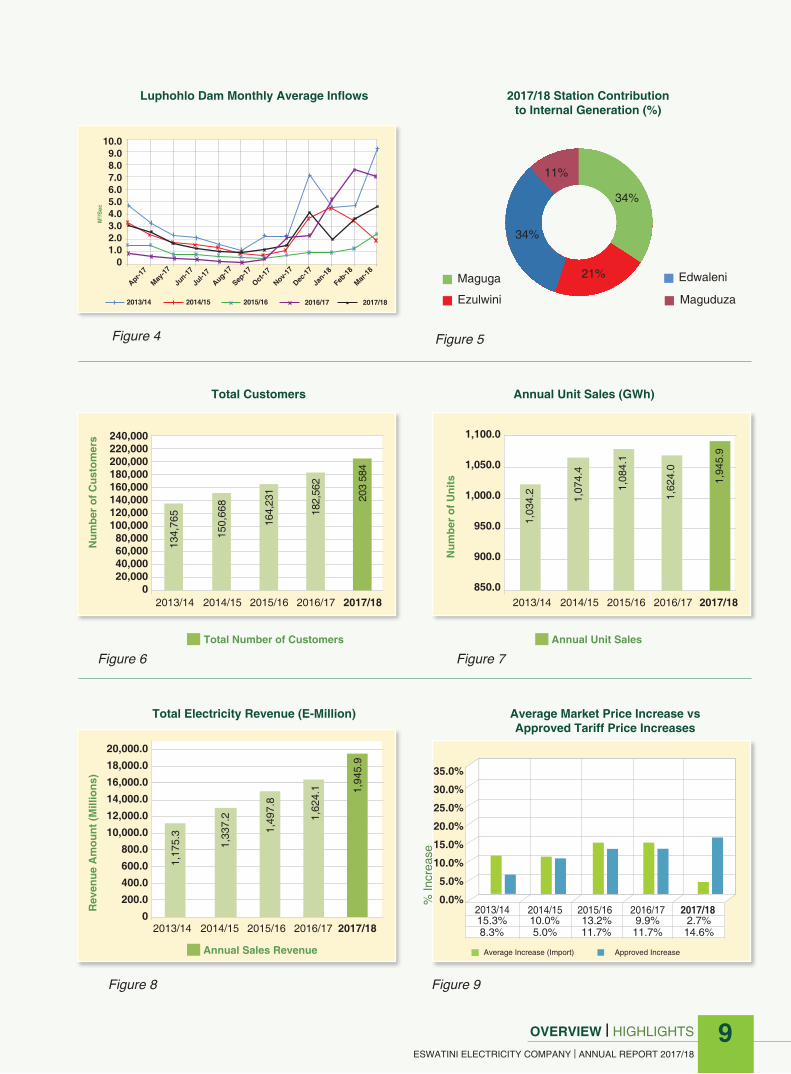

In line with our strategy to grow the company, improve efficiencies and reduce unnecessary costs, we were able to realise E2.25 billion in revenue this year. This represents an increase of 25% compared to the E1.8 billion in 2017. This is attributable to the efficiency measures we implemented, aimed at ensuring that we draw maximum returns from all the available resources. We are proud of the great team we have at all levels.

Additional savings came from a cash-flow manage-ment strategy that yielded 10% savings in total operational costs.

The increase in tariffs by 14.65% coupled with new connections also contributed to our stable financial position. We attracted a 12% increase in our customer base and in doing so, reached over 200,000 users. The increase in capital contribution revenue contributed significantly to the net profit figures.

Costs of sales stood at E1.353 billion in 2018 compared to E1.388 billion in 2017, showing a decrease of 2.5%. This is attributable to a strategic decision taken by EEC to purchase power from the Southern African Power Pool (SAPP) Day Ahead Market at prices lower than conventional bilateral rates from ESKOM.

BUSINESS REVIEW | CHAIRPERSON’S STATEMENT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

Emboldened by His Majesty King Mswati III’s pronouncement during the 50/50 Double Celebrations on 19th April 2018 that the country would henceforth revert to its original identity as the Kingdom of Eswatini, we have embraced the renewed momentum for growth by changing our name to Eswatini Electricity Company (EEC).

“

“

T

19

BUSINESS REVIEW | CHAIRPERSON’S STATEMENT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

20

Profit for the year under review stands at E537 million compared to E144 million in 2017. This shows an increase of 273% and it was made possible by the combination of tariffs hike and savings in total costs.

Rural ElectrificationThe year has seen massive expansion of the distribution network to communities that previously had no access to electricity. These projects can be attributed to funding from the Ministry of Natural Resources and Energy under the Rural Electrification Programme sponsored by the Republic of China on Taiwan, the Regional Development Programme supported by the Tinkhundla Ministry and Micro Projects. In the year under review we also constructed a new transmission line from River Bank to St. Philip’s. The cumulative distance covered by the electricity delivery infrastructure shows an overall increase from 19 323 to 20 391. This represents over 1 000 km of new lines.

Technological AdvancementsDespite the impressive financial performance, EEC, like many other companies in the region, faced a tough year. The industry as a whole is experiencing uncertain future characterised by continual drought, and challenging global, regional and local economic environments. Climate change has already increased the number and strength of some of the extreme events such as heat waves, severe storms and droughts. The heat and drought deplete already scarce water resources and contribute to billions of Emalangeni in direct losses to our economic sectors, particularly agriculture. Moreover, the world of electricity is experiencing costly, instant and ubiquitous technological advancements. These eventualities compel us to dig deep into our resources to innovate at rapid speed if we are to be in sync with the global changes.

Our survival is premised on the conscious decision we took to be highly disciplined whilst not losing focus on our priority to have reliable, safe, efficient and accessible operations. We continue to evolve and tackle the challenges that face our industry head-on. Our strategy focuses on improved performance and accountability at all levels of the business, cost reduction, customer value and more active management of our resources.

This is why our business is well positioned and in good operating shape. EEC has placed a premium investment in skills development of our personnel. The long standing expertise supporting our operations is highly regarded, and the Board of Directors’ fiduciary oversight has become the benchmark among clients and business associates.

There is no room for complacency and as a company we will continue to diversify our sources of energy portfolio. The world is changing and so should we. The energy mix is changing with growing emphasis on renewable energy and the green economy. EEC stands ready to provide leadership in the Kingdom of Eswatini in terms of energy security. We will continue to seek out and support start-ups, entrepreneurs and technology companies with the potential to advance both low-carbon energy and industrial efficiency.

Conclusion

As a long-term player in the Kingdom of Eswatini, we

will continue with our efforts to provide quality service,

strengthen partnerships with all stakeholders and all

with whom we have come into contact. Our Managing

Director, Mr Meshack Kunene, and the entire responsive

and dedicated employees will continue to implement the

EEC forward-looking strategy with determination.

On behalf of the Board of Directors, Management and

Employees, I wish to thank Their Majesties for their

guidance and support as they helped us to adapt positively

and with purpose to the changing needs of society.

MR. S’THOFENI GININDZAChairperson

CHAIRPERSON’S STATMENT - continued

GOVERNANCE | MANAGING DIRECTOR’S REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

21

MANAGINGDIRECTOR’SREPORT

Mr Meshack KuneneManaging Director

Despite the challenging economic

environment we operate in, I am

happy to indicate that our forward-

looking investment approach

resulted in improvements in our

overall performance.

MANAGING DIRECTOR’S REPORT- continued

BUSINESS REVIEW | MANAGING DIRECTOR’S REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

22

he year 2017-18 was a mixed bag of triumphs and challenges for Eswatini Electricity Company (EEC). The focus was on mainly improving

our performance and building resilience in a way that prioritised creating value for our stakeholders, particularly customers.

Despite the challenging economic environment we operate in, I am happy to indicate that our forward-looking investment approach resulted in improvements in our overall performance.

While the country is showing signs of recovery from an incessant drought that reached its peak in the 2015 and 2016 period, the serious aftermaths continue to hamper efforts for growth in all sectors of the economy. Indeed, the serious effects of climate change and the attendant extreme weather patterns such as drought, severe storms, flooding, high speed winds and heatwaves continued to hit us hard. As we all are aware, EEC is heavily dependent on hydro-power. These weather patterns, particularly the drought, always have a negative effect on our power production, forcing us to rely heavily on imported electricity to meet demand.

Drought and Economic Slump

EEC owns and operates four hydro-power stations whose ability to generate electricity depends on good amounts

of rainfall. Three of these hydro-power stations, namely Ezulwini, Edwaleni and Maguduza are operated on the Lusushwana and Usuthu River Basins catchment area and the fourth one is under the Komati Basin Water Authority (KOBWA); Maguga Dam. Both catchment systems are on the way to full recovery following the dry spell. Maguga Power Station was out of the grid for nine of 12 months in the 2016/17 financial year. Not only did this curtail EEC revenue, it also came at a heavy cost to business and domestic customers as we were compelled to engage in regular load management programmes to limit system demand that may have led to high import costs.

The agriculture sector, which is one of the biggest contributors to the economy, was also dealt a heavy blow by the drought. The generalised weakness of the agriculture sector had a telling effect across most other segments of the economy. All these factors contributed to the tough operating environment for EEC considering that energy used in agricultural activities account for a significant share of our revenue. A typical example was the Ingwavuma River that supplies agricultural water to Nsoko in the South-East of the country. This river completely dried out and there was no activity in the area.

To compound matters, the world economy is stuttering along and struggles to sustain its growth momentum. As a result of these global factors and the drought in the Kingdom of Eswatini, the domestic economy is

“

“

I am extremely proud of the EEC team that has brought about this transformation over the past two years, and our customers with whom we share a long-term and trusted relation- ship. We hope not to lose sight of the fact that the environment we operate in remains uncertain, so we must maintain our focus, discipline and commitment to excellence.

T

more subdued. The fluctuation of the Lilangeni against the US Dollar adds to the instability of the markets and subsequent strain on EEC. Such currency volatility led to EEC suspending crucial imports from the Mozambican energy utility, Electricidade de Moçambique (EDM). The pricing in the Dollar denominated EDM arrangement continues to be unfavourable due to depreciation of the Lilangeni against the US Dollar.

Forward-Looking Strategy

Despite the challenging economic environment, we have achieved improved results compared to the previous years. The long-term strategy which we adopted and intensified in 2016 is producing tangible results as seen in the improvement of the company’s asset base to over E3 billion. Our operating profit in the year under review also showed an impressive growth of E603 million in 2018 compared to E148 million in 2017. This 307% growth was a result of a combination of factors, among which were the savings from intensifying purchases of electricity from the Day Ahead Spot Market. The latter offers favourable rates when compared to the normal supply from bilateral contracts. Revenue improvements combined with close monitoring and control of operating expenditure and implementation of the listed austerity measures had a positive impact on the company’s bottom line.

Annual units sold grew slightly to 1,094.8 GWh from 1,058.4 GWh from the previous financial year. The slight growth was as a result of increases in domestic and major customer units whilst on the other hand both small commercial and major customers indicated a decline during the 2017-18 financial year compared to the 2016-17 financial year.

I am extremely proud of the EEC team that has brought about this transformation over the past two years, and our customers with whom we share a long-term and trusted relationship. We hope not to lose sight of the fact that the environment we operate in remains uncertain, so we must maintain our focus, discipline and commitment to excellence.

We also need to move at the supersonic speed with which our industry is changing by adapting positively to innovation. One way in which EEC is responding to its mandate of delivering efficient and reliable electricity is through interventions to increase internal generation capacity. Discussions with an Independent Power Producer (IPP) to implement the Lower Maguduza

Hydro project are at an advanced stage. Preparations to construct a 10MW solar plant at Lavumisa are well underway and a contract to conduct a feasibility study for the proposed thermal coal plant at Lubhuku is about to be signed.

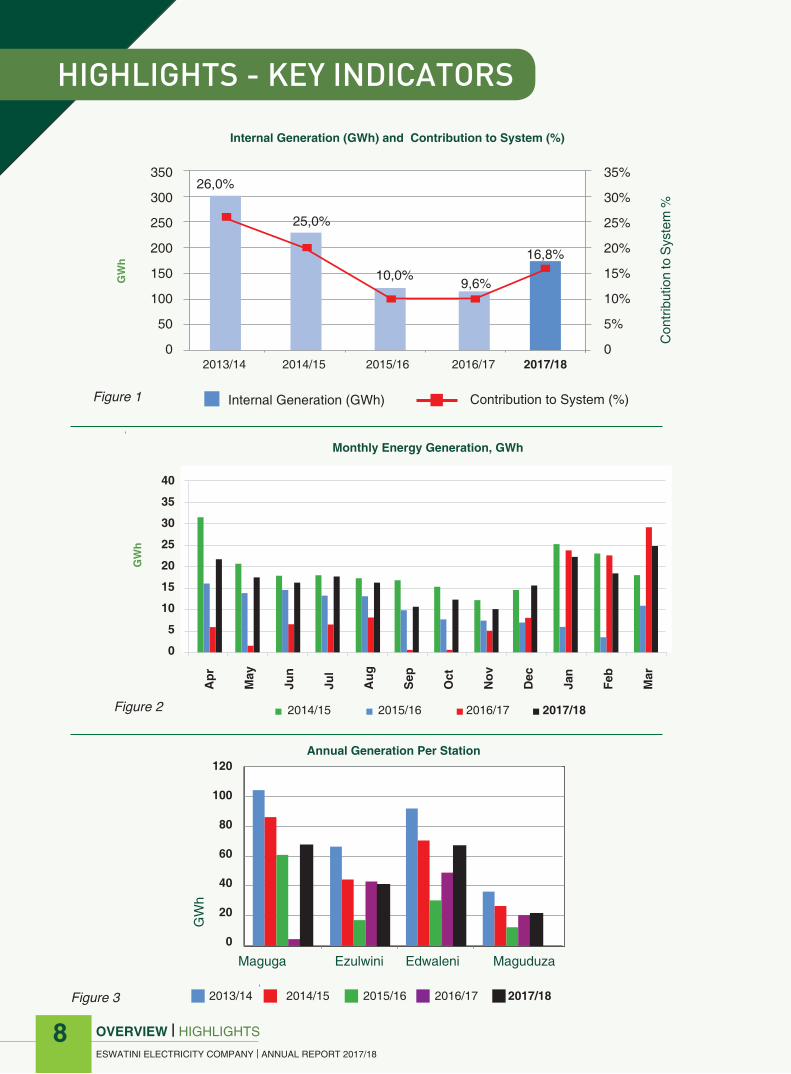

The ending of the drought resulted in improved internal generation performance this financial year. The results demonstrate that internal generation production increased from 118.9GWh in 2017 to 207.8GWh, as at the 31st of March 2018. This shows that generation figures for the year ending March 2018 are lower than the capability. They are also lower than what was achieved at the end of the financial year in March 2015, which preceded the drought. On average, internal generation contributes 20% of the total annual energy demand for the country and the balance is imported.

We remain optimistic that the drought situation has been broken with the river flows increasing. Currently, imports from Eskom account for 65% (80% in 2017) of Eswatini’s electricity needs while EEC increased its contribution from 10% to 16% compared to the previous year. Trading from the SAPP markets increased this financial year and accounted for 14% of total imported power (6% in 2017). The increased trading activities mitigated the overall costs of supply by taking advantage of lower electricity prices from the SAPP spot markets.

Major Capital Projects

There clearly is a need to move full steam ahead to increase and diversify our internal generation capacity. Coupled with that, we continue to make major strides in optimising current opportunities whilst developing a range of innovative new partnerships across the energy value chain.

To that end, we have made significant progress in our interaction with IPPs. I am happy to report on the completion of the Dwaleni II – Stonehenge 132kV Line Design, which is targeted at improving capacity in the capital city, Mbabane, and surrounding areas. There is also the LUSIP Phase I along the Usuthu River bank, which is a strategic intervention in a largely agricultural sector. Another milestone is the Lavumisa Solar PV Project to exploit renewable energy. The planned construction of this E120 million plant is progressing well and is earmarked to generate 10 MW of electricity. Moreover, the goal to increase power generation within the Kingdom of Eswatini is bolstered by a thermal project earmarked to produce about 300 MW.

BUSINESS REVIEW | MANAGING DIRECTOR’S REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

23

MANAGING DIRECTOR’S REPORT- continued

Innovating the Customer Experience

EEC remains focused on satisfying customer needs by building on trust, relationships and excellence. We believe in constant engagement with our customers and in redefining the customer experience. We also leverage on technology to improve the Outage Management System (OMS) and overall activity in social media platforms to reach out to our customers. We will continue to improve our Call and Service Centres to meet the dynamic needs of our customers. With technological innovations changing the way we live, work and play on a daily basis, EEC will continue to leverage on the latest technology to enhance customer satisfaction.

It is through such interventions that our customer base continues to grow year on year. EEC’s customer base rose from 182,562 in March 2017 to a total of 203,584 in March 2018. This shows a 12% growth from the previous financial year. A bulk of the customers are in the domestic sector. We continue to take bold action to increase coverage of rural and remote areas as electricity is a great catalyst to fulfil the country’s development agenda.

The Board of Directors has instructed us to improve equitable access to electricity and make sure that customers get value for money. We are working on packages designed to help the indigent, pensioners, the elderly and those living below minimum wage to gain access to electricity.

EEC places a high premium on the safety of the dedicated men and women who work hard, sometimes in challenging weather conditions to keep the lights on. In 2017/18, we continued to see an overall improvement in

our safety performance. The number of reportable injuries fell by a further 4.76% and the number of minor public injuries fell by 100% when compared to 2016-17. We have also made significant improvements in the number of near misses reported (up by over 20%) and have also started to capture man hours free of incidents. Our safety performance has continued to improve following a period of significant organisational strategy change.

The company is committed to upholding health and safety. We rely on a powerful tool: safety and health programs that focus on prevention, identifying and fixing the hazards before they cause harm. This is a shared responsibility of management, the labour formations and contractors. Together we have established strong systems to ensure security and safety for our employees as reflected in the ISO certifications of the integrated management systems we have secured. This extends to our commitment to be good stewards of the environment.

Call to Action

The country continues to lose millions of Emalangeni each year due to vandalism, electricity theft and copper theft. Such acts hamper economic development and negatively affect the quality of life of the people.

MR. MESHACK KUNENEManaging Director

BUSINESS REVIEW | MANAGING DIRECTOR’S REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

24

SUMMARYGENERATION SYSTEM DEMAND FOR THE YEAR UNDER REVIEWRIVER FLOWS AT GS15SYSTEM PERFORMANCE IMPROVEMENTNETWORK EXTENSIONSAPP PARTICIPATION

26263031343434

OPERATIONSREPORT

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

25

- EFFECTIVE DELIVERY OF ENERGY, THROUGH RELIABLE AND EFFICIENT PROCESSES

Distribution Lines

Internal Power Generated

System Max. Demand

20,391KM

236 MW

16%

OPERATIONS REPORT- continued

Summary

he financial year under review had less challenges for the Operations Division regarding hydro power generation as it was a relatively wet year. Following improved dam levels, the resumption of activity at Maguga Hydro Power Station increased internal generation to better levels compared to the previous financial year. As a result, EEC

did not implement load management programmes to curtail system demand due to the availability of water for internal generation.

The foreign exchange rate level continues to be a challenge with respect to energy for those imports that are dollar denominated. This has meant that EEC’s Power Supply Agreement with Mozambican energy utility, Electricidade de Moçambique (EDM) remains suspended as the costs continued to surpass the selling price. The river flows remained encouraging during the financial year and internal generation was sustained at all hydro power stations to mitigate peak loads.

However, the improvement in weather conditions came with another challenge. The increase in inclement weather led to an increase in network outages affecting both the transmission and distribution lines. The company is preparing budgets to implement the Network Master Plan designed to increase network reliability through infrastructure development projects. Improvement of the quality of supply is among the top priorities for the Operations Division.

Generation

EEC owns and operates four hydro power stations. Three of these are operated on the Usuthu River Basin catchment area and the fourth from the Komati Basin Water Authority (Maguga Dam). The effects of drought began to show waning signs this financial year, as the results demonstrate that internal generation production increased from 118.9GWh in 2017 to 207.8GWh, as at the 31 March 2018.

Figure 1 above shows the generation levels month-on-month for the last five financial years. The impact of the 2016/17 drought is seen up to December 2016. Improvement on weather conditions and the resulting benefits to local generation are seen throughout 2017/18, with March 2018 recording the highest local generation output for the year.

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

40

35

30

25

20

15

10

5

0

Monthly Energy Generation, GWh

2014/15 2015/16 2016/17 2017/18

Figure 1: Monthly Generation for the last five years

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

26

T

Figure 2 shows that the cumulative generation figures for the year ending March 2018 are lower than the capability and lower than what was achieved at the end of the year in March 2015, which preceded the drought. It also shows an improving generation performance as the hydro power production ramped up, from December 2017 to March 2018. We remain optimistic that the current drought situation has been broken with the river flows increasing.

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

350

300

250

200

150

100

50

0

2014/15 2015/16 2016/172013/14 2017/18

GW

h

Cumulative Energy Generated (GWh)

Figure 2: Year on Year Cumulative Generation GWh for the last five years

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

27

An EEC Technician inspecting a 10 MVA transformer

OPERATIONS REPORT- continued

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

28

Figure 3 shows the contribution by each hydro power site under EEC operations. Maguga Hydro Power has improved its contribution to 34.3% compared to 4% in the previous year. This was due to an increase in the level of the dam following better summer rainfall than in the previous year. The overall performance for internal generation improved in the current financial year due to more favourable rain conditions and the high level of plant performance.

Figure 4 shows a year-on-year production per hydro power station. The graphs indicate that there was progressive decline in generation production between 2013 and 2018, though the latest financial year saw a better performance. The graphs in Figure 4 show that 2013/14 was the best year for internal electricity generation than the year under review. Maguga Hydro Power contributed significantly once again this financial year.

Figure 3: Internal Generation Contribution by Power Station

Ezulwini

Maguga Edwaleni

Maguduza

2017/18 Plant Contribution toInternal Generation (GWh, %)

34%

11%

34%

21%

Figure 4: Annual Generation According to Hydro Power Station

120

100

80

60

40

20

0

2013/14

Ezulwini Edwaleni MaguduzaMaguga

2014/15 2015/16 2016/17

GW

h

Annual Generation Per Station

2017/18

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

29

350

300

250

200

150

100

50

0

GW

hInternal Generation (GWh) & Contribution to System (%)

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

173.

1

150.

1 246.

1

288.

1 334.

0

278.

5

240.

115.6%14.0%

21.0%

24.3%

29.5%

25.7% 22.1%

25.1%

18.4%

GWh Contribution to System (%)

9.8% 9.8%

16.3%

302.

6

321.

0

123.

3

118.

9

207.

8

35%

30%

25%

20%

15%

10%

5%

0%

Con

tribu

tion

to S

yste

m %

Figure 5: Trends showing contribution of internal generation to energy demand

Figure 5 shows the trend for the contribution to annual energy demand by internal generation. The trend follows the weather climatic conditions and it is useful as an input to generation planning for the following year. On average, internal generation contributes 20% of the total annual energy demand for the country and the balance is imported.

Table 1 below demonstrates the total monthly electricity usage for the country by source. The imports from EDM continued to be temporarily suspended due to the escalation of prices and owing to the depreciation of the Lilangeni against the US Dollar.

Table 1 Monthly Electricity Usage and Demand

MONTH ESKOM (MWh)

EDM (MWh)

DAM (MWh)

EEC (MWh)

USL (MWh)

Buckswood (MWh)

Total Energy (MWh)

Maximum Demand (MW)

Apr-17 59,635.64 25,264.20 21,908.06 2,166.78 13.54 108,988.22 223.33

May-17 60,149.13 12,765.30 17,728.28 8,463.38 12.57 99,118.66 204.19

Jun-17 56,501.77 18,735.70 16,525.09 8,819.70 11.63 100,593.89 201.75

Jul-17 49,789.81 25,311.70 17,869.61 9,106.65 8.82 102,086.59 205.09

Aug-17 50,776.64 25,441.40 16,668.87 8,734.57 13.97 101,635.45 200.09

Sep-17 73,190.98 7,876.00 10,860.02 8,025.08 12.89 99,964.97 215.10

Oct-17 85,499.53 2,785.00 12,368.79 7,260.10 15.20 107,928.62 221.18

Nov-17 72,962.97 10,042.20 10,384.25 6,790.56 16.47 100,196.44 216.47

Dec-17 86,287.61 3,538.00 15,707.35 737.95 12.89 106,283.80 218.46

Jan-18 92,778.15 4,440.00 24,222.57 0.00 0.00 121,440.72 236.06

Feb-18 74,061.29 16,227.00 18,521.23 0.00 0.00 108,809.52 233.70

Mar-18 56,848.27 29,834.30 24,995.32 0.00 0.00 111,677.89 232.68

TOTAL 818,481.9 182,260.0 207,759.4 60,104.7 117.98 1,268,723.98 236.06

OPERATIONS REPORT- continued

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

30

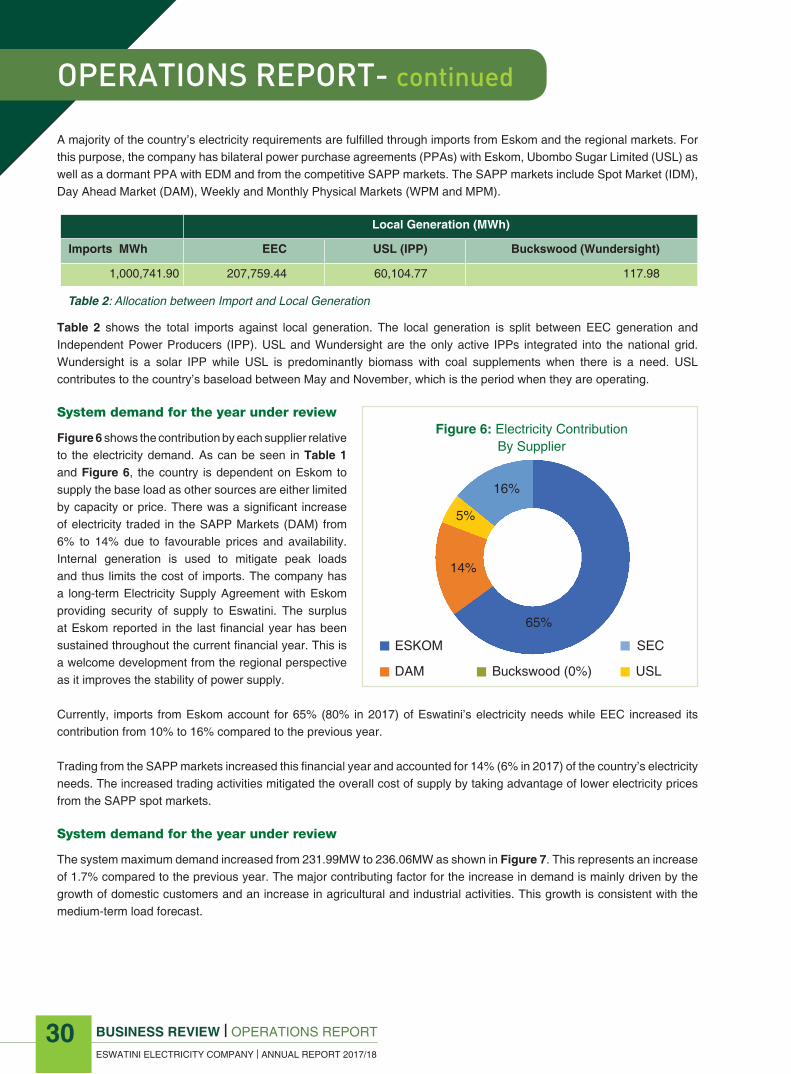

A majority of the country’s electricity requirements are fulfilled through imports from Eskom and the regional markets. For this purpose, the company has bilateral power purchase agreements (PPAs) with Eskom, Ubombo Sugar Limited (USL) as well as a dormant PPA with EDM and from the competitive SAPP markets. The SAPP markets include Spot Market (IDM), Day Ahead Market (DAM), Weekly and Monthly Physical Markets (WPM and MPM).

Table 2 shows the total imports against local generation. The local generation is split between EEC generation and Independent Power Producers (IPP). USL and Wundersight are the only active IPPs integrated into the national grid. Wundersight is a solar IPP while USL is predominantly biomass with coal supplements when there is a need. USL contributes to the country’s baseload between May and November, which is the period when they are operating.

System demand for the year under review

Figure 6 shows the contribution by each supplier relative to the electricity demand. As can be seen in Table 1 and Figure 6, the country is dependent on Eskom to supply the base load as other sources are either limited by capacity or price. There was a significant increase of electricity traded in the SAPP Markets (DAM) from 6% to 14% due to favourable prices and availability. Internal generation is used to mitigate peak loads and thus limits the cost of imports. The company has a long-term Electricity Supply Agreement with Eskom providing security of supply to Eswatini. The surplus at Eskom reported in the last financial year has been sustained throughout the current financial year. This is a welcome development from the regional perspective as it improves the stability of power supply.

Currently, imports from Eskom account for 65% (80% in 2017) of Eswatini’s electricity needs while EEC increased its contribution from 10% to 16% compared to the previous year.

Trading from the SAPP markets increased this financial year and accounted for 14% (6% in 2017) of the country’s electricity needs. The increased trading activities mitigated the overall cost of supply by taking advantage of lower electricity prices from the SAPP spot markets.

System demand for the year under review

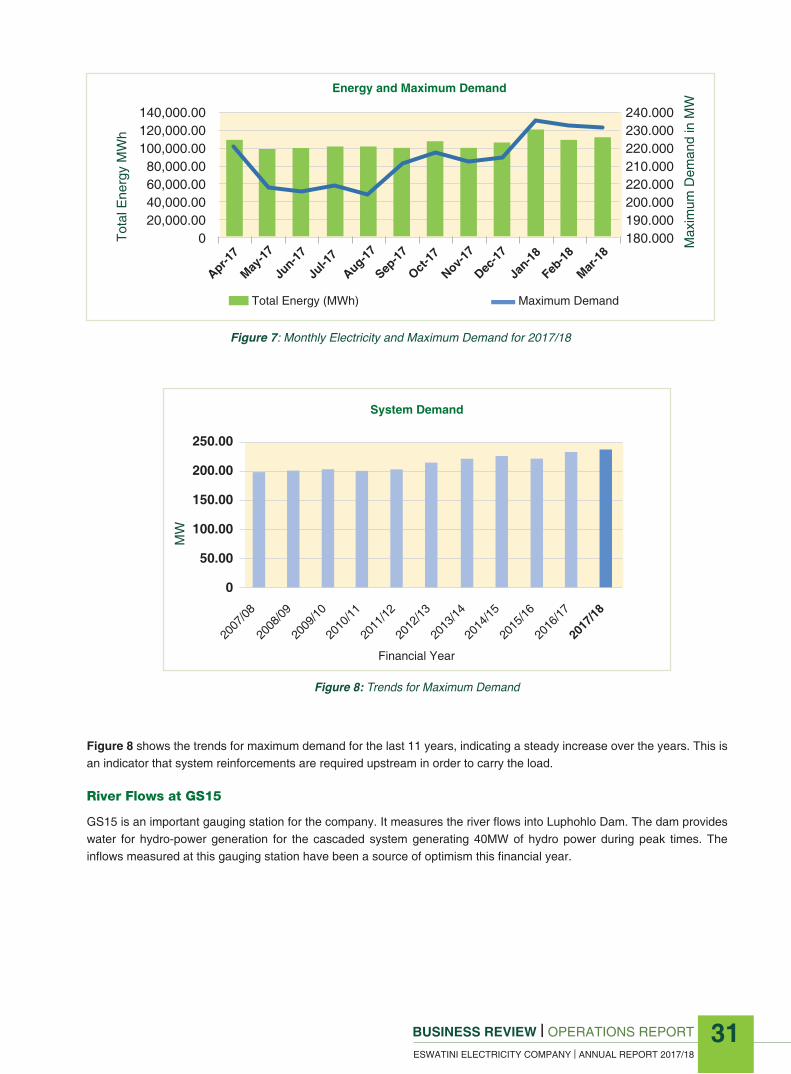

The system maximum demand increased from 231.99MW to 236.06MW as shown in Figure 7. This represents an increase of 1.7% compared to the previous year. The major contributing factor for the increase in demand is mainly driven by the growth of domestic customers and an increase in agricultural and industrial activities. This growth is consistent with the medium-term load forecast.

Local Generation (MWh)

Imports MWh EEC USL (IPP) Buckswood (Wundersight)

1,000,741.90 207,759.44 60,104.77 117.98

Table 2: Allocation between Import and Local Generation

Figure 6: Electricity Contribution By Supplier

SECESKOM

USLBuckswood (0%)DAM

5%

14%

65%

16%

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

31

Apr-17

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

140,000.00120,000.00100,000.0080,000.0060,000.0040,000.0020,000.00

0

240.000230.000220.000210.000220.000200.000190.000180.000

Energy and Maximum Demand

Tota

l Ene

rgy

MW

h

Max

imum

Dem

and

in M

W

Total Energy (MWh) Maximum Demand

Figure 7: Monthly Electricity and Maximum Demand for 2017/18

Figure 8: Trends for Maximum Demand

MW

System Demand

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

250.00

200.00

150.00

100.00

50.00

0

Financial Year

Figure 8 shows the trends for maximum demand for the last 11 years, indicating a steady increase over the years. This is an indicator that system reinforcements are required upstream in order to carry the load.

River Flows at GS15

GS15 is an important gauging station for the company. It measures the river flows into Luphohlo Dam. The dam provides water for hydro-power generation for the cascaded system generating 40MW of hydro power during peak times. The inflows measured at this gauging station have been a source of optimism this financial year.

OPERATIONS REPORT- continued

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

32

Figure 9 shows the trends for Lusushwana River flows at GS15. The trends indicate that the river flows improved in the year under review compared to previous years despite that the flows were lower at the end of the financial year.

Figure 10 shows the trends for the level at Luphohlo Dam. The dam level follows the season and its operation over the years, which have not changed significantly. The priority is to conserve water for the high season in order to maintain generation at full capacity during peak times.

10.0

9.0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0

2013/14 2015/16 2016/172014/152012/13

Apr-17

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Luphohlo Monthly FIows (m3/s)

Figure 9: Luphohlo Flow Trends at GS15

A view of Luphohlo Dam at Siphocosini

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

33

Luphohlo Dam % Volume

% V

olum

e

100

80

60

40

20

0

Apr-17

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

2013/14 2015/16 2016/172014/152012/13

Figure 10: Luphohlo Dam Profile

The trend for 2017-18 at Maguga Dam in Figure 11 shows that the level has been falling until November 2016 and began to rise again as the summer rains arrived. The level rose to about 90% at the end of the financial year, which has been consistent with the performance of the hydro power station at this site.

Maguga Dam % Volume

% V

olum

e

100

80

60

40

20

0

Apr-17

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

2016/17 2017/182015/16

Figure 11: Maguga Dam Level Trends

OPERATIONS REPORT- continued

BUSINESS REVIEW | OPERATIONS REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

34

System Performance Improvement Projects

Our organisation continues to improve the performance of the system. In the year under review, a number of capital projects were implemented in order to improve system reliability and operational effectiveness. During the year under review, the company began implementation of the transmission reinforcement project between Big Bend and Maloma T. About E18 million was spent on the project. The first phase of the project is between Big Bend and Ncandweni, which is to be followed by Ncandweni to Maloma T.

The line will be constructed on galvanised steel monopoles for reliability. Although the capital costs are higher for steel structures, their maintenance intervals are longer and lower in costs. This project further reinforces the communication systems through the introduction of an optical fibre link between Big Bend and Maloma T. This will also improve the performance of communication and information technology systems, and enhance the company’s position in the telecommunications infrastructure industry. Designs and environmental studies for the second 132kV line to reinforce the Western grid at Stonehenge were completed. Network Extension

The year has seen more activities on the distribution network extension projects to communities that previously had no access to electricity. These projects can be attributed to funding from the Ministry of Natural Resources and Energy under the Rural Electrification Programme sponsored by the Republic of China on Taiwan, Regional Development Programme under the Tinkhundla Ministry, and Micro Projects. The projects include a new transmission line from River Bank to St Philip’s. The table (right) shows the cumulative distance covered by the electricity delivery infrastructure. There was an overall increase from 19 323 to 20 391, which is over 1 000km of new lines.

SAPP Participation

EEC continues to participate in the Southern African Power Pool (SAPP), where it is also recognised as an operating member. Besides the semi-annual meetings, the company benefited from SAPP-sponsored training for electricity traders on the Day Ahead Market and Intra-Day Market, Weekly Physical Market and Monthly Physical Market. The company also sent a delegate to a planners training workshop. The SAPP Capacity Building programme continues to benefit utilities in the region, particularly on markets and transmission planning.

Description Overall Distance Covered (km)

Transmission Lines - 132kV Transmission Lines (km) 296

- 66kV Transmission Lines (km) 986

Distribution Lines - 11kV Lines (km) 11,186

- Low Voltage Lines (km) 9,205

20,391

Table 3: Network Line Statistics

Table 3 shows the overall extent of the network.

A side view of Maguga Dam

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

35

MAJOR CUSTOMERS’ CONTRIBUTION COMPARED TO DOMESTIC AND SMALL COMMERCIAL CUSTOMERSCUSTOMER QUOTATIONSCALL CENTRECUSTOMER EDUCATIONDEBT MANAGEMENTVENDINGSYSTEM LOSSES & METER INSPECTIONCUSTOMER FEEDBACK

36

40404141414141

CUSTOMERSERVICE

REPORT- BUILDING STRONGER RELATIONSHIPS

WITH OUR STAKEHOLDERS

Turnover for the Year

Annual Unit Sales

Total Customers

3.56%

203 584

1,095 GWh

CUSTOMER SERVICE REPORT- continued

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

36

1. MAJOR CUSTOMERS’ CONTRIBUTION COMPARED TO DOMESTIC AND SMALL COMMERCIAL CUSTOMERS

bout 1% of EEC’s customer base (major customers) contributed 57% of the sales revenue (E1 114M) in the year under review whereas 92% of the customers (domestic customers) contributed only 30% of the revenue (E583M). Small commercial customers, who form 8% of the customer base, contributed 13% of the sales revenue (E249M).

a. GROWTH IN NUMBERS

As of the end of the year under review, EEC had a total of 203 584 customers, which represents 12% growth from the previous financial year. Figure 1 below shows the total number of customers over the years.

Major customers grew slightly to 1 177 in the 2017/18 financial year from 1 161 in 2016/17. This represents a 1.3% growth. Small commercial and domestic customers grew by 7.6% and 12.1%, respectively. On the overall, domestic customers have grown significantly over the last five years by 52.7% from 122 428 to 187 052, while small commercial customers grew by 36.6% from 11 240 to 15 355. Major customers grew by 7.2% from 1 097 to 1 177, as shown in Figure 2.

Figure 1: Customer Growth in Past 5 years

250,000

200,000

150,000

100,000

50,000

0

Num

ber o

f Cus

tom

ers

Total Number of Customers

2014 2015 2016 2017 2018

203,584182,251164,213150,668134,765No. of Customers

A

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

b. GROWTH IN SALES UNITS

Annual units sold grew slightly to 1 094.8 GWh from 1 058.4 GWh recorded in the previous financial year. The slight growth was as a result of an increase in domestic and major customer units whilst, on the other hand, small commercial customers showed a decline during the 2017/18 financial year compared to 2016/17. Figure 3 below shows the growth in units over the past years.

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

37

Number of Customers by Customer Tariff Category

Num

ber

of C

usto

mer

s

Domestic

2014

2015

2016

2017

2018

122,428

137,335

149,744

167,822

187,052

11,240

12,203

13,320

14,268

15,355

1,097

1,130

1,149

1,161

1,177

MajorSmall Commercial

200,000180,000160,000140,000120,000100,00080,00060,00040,00020,000

0

Figure 2: Number of Customers per Category

Figure 3: Annual Unit Sales Growth in GWh

1,100.00

1,090.00

1,080.00

1,070.00

1,060.00

1,050.00

1,040,00

1,030.00

1,020.00

1,010.00

1,000.00

GW

h

Annual Unit Sales (GWh)

2014 2015 2016 2017 2018

1,0951,0581,0841,0741,034Annual Unit Sales

Unit sales grew by 2.0% in the domestic category from 383 GWh in 2016/17 to 391 GWh in 2017/18. There was a drop in the small commercial customer bracket of 0.8% whilst the major customer category increased by 5.2%. Figure 4 shows a decrease in small commercial customer sales whilst the major customer and domestic customer categories increased in the financial year under review.

CUSTOMER SERVICE REPORT- continued

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

38

Unit sales grew by 15.8% in the domestic customer category in the last five years and by 9.6% in the small commercial customer category. Meanwhile, the major customer category declined by 0.4%.

c. GROWTH IN SALES REVENUE

The overall sales revenue for the financial year 2017/18 was E1 946 million, which reflects an increase of 19.8% from the E1 624 million recorded in 2016/17. Figure 5 shows the trend in sales revenue over the years.

Unit Sales by Customer Category

Num

ber

of U

nits

(E-M

illio

n)

Domestic

2014

2015

2016

2017

2018

338,070,927

352,183,804

368,241,191

383,794,670

391,466,452

97,909,804

103,395,067

103,624,834

108,195,361

107,333,003

598,259,226

618,543,650

612,250,402

566,407,802

595,967,804

MajorSmall Commercial

700,000,000

600,000,000

500,000,000

400,000,000

300,000,000

200,000,000

100,000,000

-

Figure 4: Units sold per Customer Category

Figure 5: Annual Unit Sales Revenue

250,000,000

200,000,000

150,000,000

100,000,000

50,000,000

0

Ann

ual S

ales

Annual Sales Revenue (E-Million)

2014 2015 2016 2017 2018

1,945,949,2591,624,163,2921,499,300,9591,338,141,4581,175,261,338Annual Sales Revenue (E)

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

Major customer sales grew by 20.1% from E926 million in 2016/17 to E1 113 million in 2017/18. This is attributable mainly to the tariff increase. Domestic customer sales revenue grew by 21.0% from E481 million to E582 million in 2017/18. This is mainly attributable to growth in the number of customers by about 20 230. Small commercial customers also contributed 16.8% from E214 million to E250 million in the year under review. Figure 6 below shows the sales revenue growth by tariff category.

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

39

Sales Revenue by Customer Category

SalesRevenue (E)

Domestic

301,465,640

351,405,823

413,175,665

481,222,864

582,507,502

140,632,659

163,415,068

184,468,140

213,974,794

249,600,962

733,163,038

823,320,566

901,657,15

926,785,063

1,113,840,795

Major

1,200,000,000

1,000,000,000

800,000,000

600,000,000

400,000,000

200,000,000

-Small Commercial

2014

2015

2016

2017

2018

Excellent Customer Service is central to our operations

CUSTOMER SERVICE REPORT- continued

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

40

2. CUSTOMER QUOTATIONS

A total of 21 791 quotations were processed by EEC in the 2017/18 financial year. The Manzini region had more quotations compared to the other regions. On average, each region had about 5 000 quotations processed. The increase in the number of quotations was as a result of accessible funding from Micro-projects, the Rural Development Fund, Ministry of Natural Resources and Energy as well as the Republic of China (Taiwan). Some customers self-fund their projects, more especially business and domestic customers who urgently need supply and cannot wait for the process of funded schemes as well as those who cannot form group schemes. The turn-around time in processing quotations has drastically improved after engaging more staff at the EEC Service Centres.

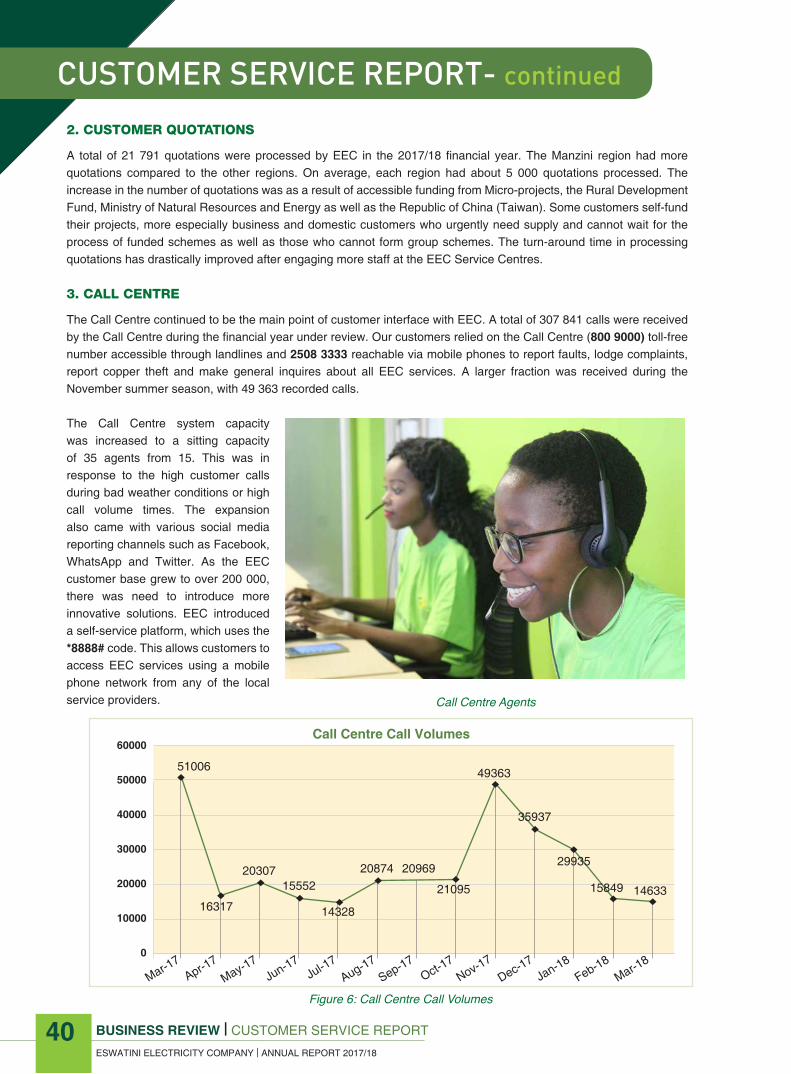

3. CALL CENTRE

The Call Centre continued to be the main point of customer interface with EEC. A total of 307 841 calls were received by the Call Centre during the financial year under review. Our customers relied on the Call Centre (800 9000) toll-free number accessible through landlines and 2508 3333 reachable via mobile phones to report faults, lodge complaints, report copper theft and make general inquires about all EEC services. A larger fraction was received during the November summer season, with 49 363 recorded calls.

The Call Centre system capacity was increased to a sitting capacity of 35 agents from 15. This was in response to the high customer calls during bad weather conditions or high call volume times. The expansion also came with various social media reporting channels such as Facebook, WhatsApp and Twitter. As the EEC customer base grew to over 200 000, there was need to introduce more innovative solutions. EEC introduced a self-service platform, which uses the *8888# code. This allows customers to access EEC services using a mobile phone network from any of the local service providers.

Figure 6: Call Centre Call Volumes

Call Centre Call Volumes60000

50000

40000

30000

20000

10000

0

Jan-18Feb-18

Mar-18

Dec-17Nov-17

Oct-17

Sep-17Jul-17

Aug-17Jun-17

May-17Apr-1

7Mar-1

7

51006 49363

2030715552

20874 20969

14633

35937

29935

1584921095

1432816317

Call Centre Agents

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

4. CUSTOMER EDUCATION

The marketing department continued to vigorously educate customers about the services offered by the company. We educate our customers through various platforms such as radio shows, road shows, trade shows, billboards, press adverts and community meetings. The main focus of our education programs are safety, using electricity economically, demand side management, copper theft, curbing electricity theft, quotations process and the EEC operations in general. This provided EEC with valuable feedback on customer perceptions and the quality of its service delivery.

5. DEBT MANAGEMENT

The year under review was closed with a total debtors position of E141.6 million from E164.7 million the previous year. A total of E20 million was written off as bad debt. Debtors’ days were at 33 as at the end of March 2018.

6. VENDING

EEC is continuing to increase the number of prepaid vending stations countrywide for its customers to purchase electricity and to sufficiently meet their needs.

7. SYSTEM LOSSES AND METER INSPECTION

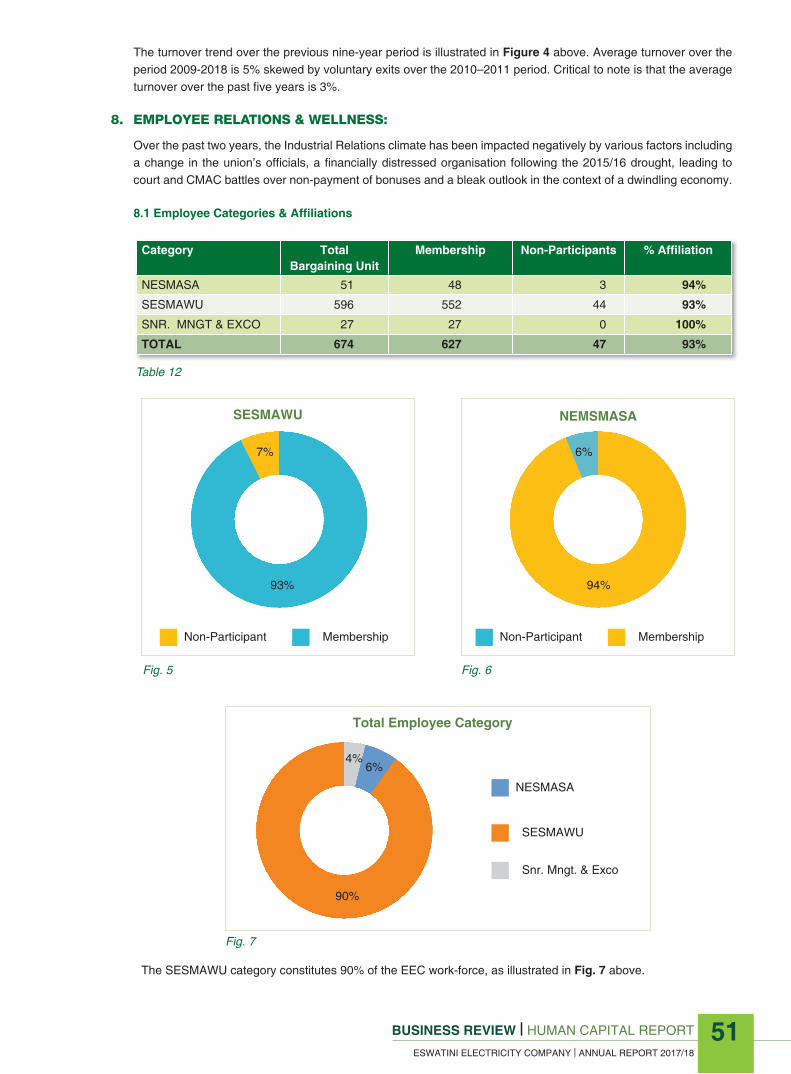

Notable incidents of electricity theft are on the rise despite EEC’s efforts to mitigate such bad conduct. Both the technical and commercial losses have increased from 14.20% to 14.93%. The total commercial losses have decreased from 2.87% in the last financial year to 2.84% in the year under review. The technical losses have increased from 11.34% in the previous year to 12.09%. This is attributed to an increase in the distribution infrastructure, which is mainly driven by Government support for rural electrification.

8. CUSTOMER FEEDBACKSeveral stakeholder engagements were held with customers. These were meant to provide feedback and update customers on what the company was doing to continuously improve the quality of supply and service in general. We also shared information on future tariff migration. The meetings were also meant to ascertain customer concerns and future business plans in order to correctly position EEC to satisfy their needs.

One major concern from the customers was the occasional request from EEC major suppliers to reduce load, especially during morning and evening peak times. EEC was encouraged to speed up its internal generation expansion plan to ensure self-sufficiency to stabilise supply and control of the tariff increases.

BUSINESS REVIEW | CUSTOMER SERVICE REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

41

15.20%15.00%14.80%14.60%14.40%14.20%14.00%13.80%13.60%13.40%13.20%13.00%

14,16%14,41%

14,20%

14,93%

13,75%

2013/14 2014/15 2015/16 2016/17 2017/18

Loss Rate

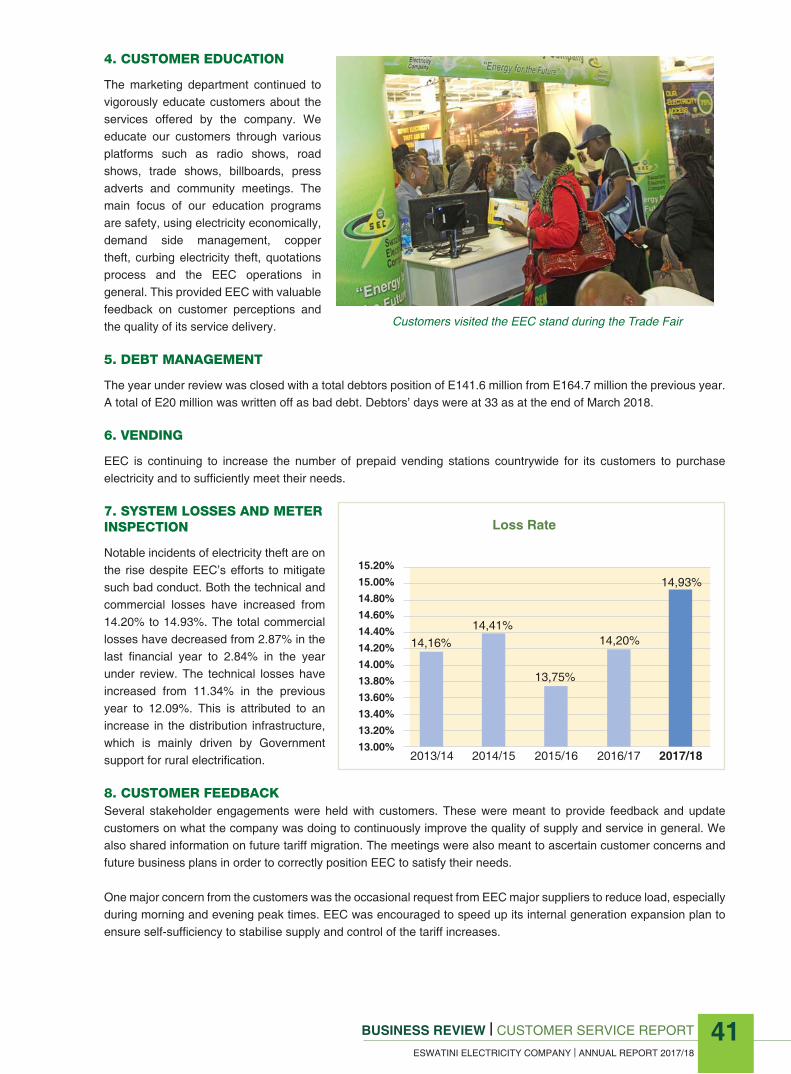

Customers visited the EEC stand during the Trade Fair

HIGHLIGHTSLOWLIGHTSTALENT MANAGEMENTHUMAN CAPITAL DEVELOPMENTHR ADMINISTRATIONHR MAINTENANCETURNOVEREMPLOYEE RELATIONS & WELLNESS

4345454647495051

HUMAN CAPITAL

REPORT

BUSINESS REVIEW | HUMAN CAPITAL REPORT

ESWATINI ELECTRICITY COMPANY | ANNUAL REPORT 2017/18

42

- EFFECIENCY THROUGH RESPONSIBLE AND PRODUCTIVE HUMAN RESOURCES

Wellness Members

PermanentEmployees

Peer Educators Trained

340

38

674

HIGHLIGHTS: