7

4 TH ANNUAL Global Transfer Pricing Conference: PARIS EXECUTIVE SUMMARY

4TH ANNUAL

Global Transfer Pricing Conference: PARISEXECUTIVE SUMMARY

COPYRIGHT © 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC.2

4th Annual Global Transfer Pricing Conference: PARIS — Executive Summary

On March 14 and 15, 2016, Bloomberg BNA and Baker & McKenzie co-hosted the 4th Annual Global Transfer Pricing Conference: Paris, drawing together speakers from the governments of France, Mexico, the United States, and Brazil; NGOs such as the World Customs Organization, the OECD, and the United Nations; and leaders from some of the largest multinational corporations on the planet.

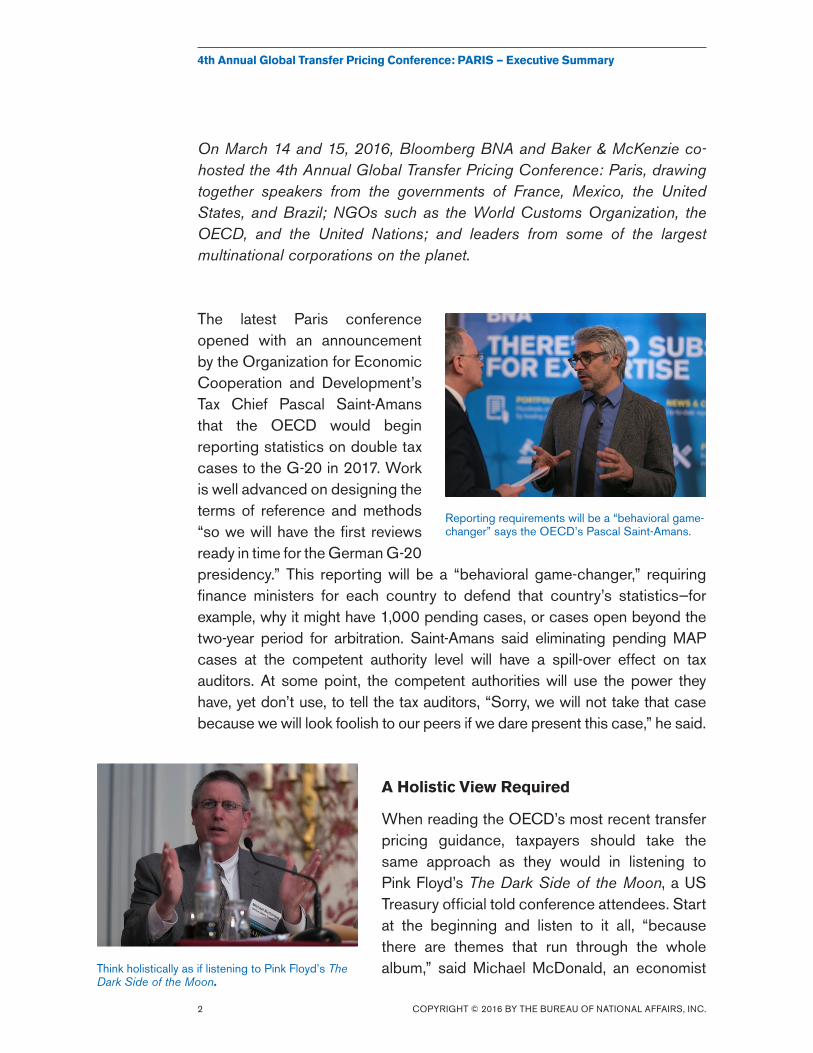

The latest Paris conference opened with an announcement by the Organization for Economic Cooperation and Development’s Tax Chief Pascal Saint-Amans that the OECD would begin reporting statistics on double tax cases to the G-20 in 2017. Work is well advanced on designing the terms of reference and methods “so we will have the first reviews ready in time for the German G-20 presidency.” This reporting will be a “behavioral game-changer,” requiring finance ministers for each country to defend that country’s statistics—for example, why it might have 1,000 pending cases, or cases open beyond the two-year period for arbitration. Saint-Amans said eliminating pending MAP cases at the competent authority level will have a spill-over effect on tax auditors. At some point, the competent authorities will use the power they have, yet don’t use, to tell the tax auditors, “Sorry, we will not take that case because we will look foolish to our peers if we dare present this case,” he said.

A Holistic View Required

When reading the OECD’s most recent transfer pricing guidance, taxpayers should take the same approach as they would in listening to Pink Floyd’s The Dark Side of the Moon, a US Treasury official told conference attendees. Start at the beginning and listen to it all, “because there are themes that run through the whole album,” said Michael McDonald, an economist

Reporting requirements will be a “behavioral game- changer” says the OECD’s Pascal Saint-Amans.

Think holistically as if listening to Pink Floyd’s The Dark Side of the Moon.

COPYRIGHT © 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC.3

4th Annual Global Transfer Pricing Conference: PARIS — Executive Summary

in the US Treasury’s Office of Tax Analysis. “I am hearing about selective interpretation of guidance that should be read in a holistic way,” he added, saying his kids take the same approach to listening to music.

Risk Allocation

On the topic of risk allocation, McDonald asserted that the OECD guidance, while more expansive, aligns with US rules on the topic. Under both sets of guidance, risk allocation will be respected if it comports with economic substance. “Typically, we are very pithy in the US. We just throw out a sentence that covers what the OECD takes 50 paragraphs to say,” he quipped, adding that risk is a difficult transfer pricing issue, which explains why the OECD devoted so much to the subject in its final report.

According to McDonald, risk should be analyzed under the OECD’s six-step analytical framework under which multinationals:

• identify economically significant risks with specificity;

• determine the contractual allocation of risk;

• determine through a functional analysis how the associated related parties assume and manage specific, economically significant risks;

• determine whether the contractual assumption of risk is consistent with the conduct of the related parties;

• apply the guidance on allocating risk if the related party assuming risk doesn’t control the risk or doesn’t have the financial capacity to assume the risk; and,

• price the transaction, taking into account financial and other consequences of risk assumption, as appropriately allocated, and appropriately compensate risk management functions.

He noted that the US Section 482 on transfer pricing doesn’t get into some of the conceptual difficulties that are inherent in dealing with risk. However, the part of the US regulations that covers identification of contractual terms states that the extent to which each controlled taxpayer exercises managerial or operational control over business activities influences the amount of loss. Conceptually, McDonald said, the US “is attempting to reach the same type of answer or analysis that is found in the OECD guidance.”

COPYRIGHT © 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC.4

In allocating and analyzing risk, he said, it’s important to start with related-party contracts. The final OECD report states that an ex ante conceptual assumption of risk provides clear evidence of a commitment to assume risks. The contract provides documentary evidence of how the bets are placed with respect to risk – an important point because audits occur years after the fact. Though contracts provide important information, there is evidence in the guidance that they are not determinative.

Country-by-Country Reporting: The French Perspective

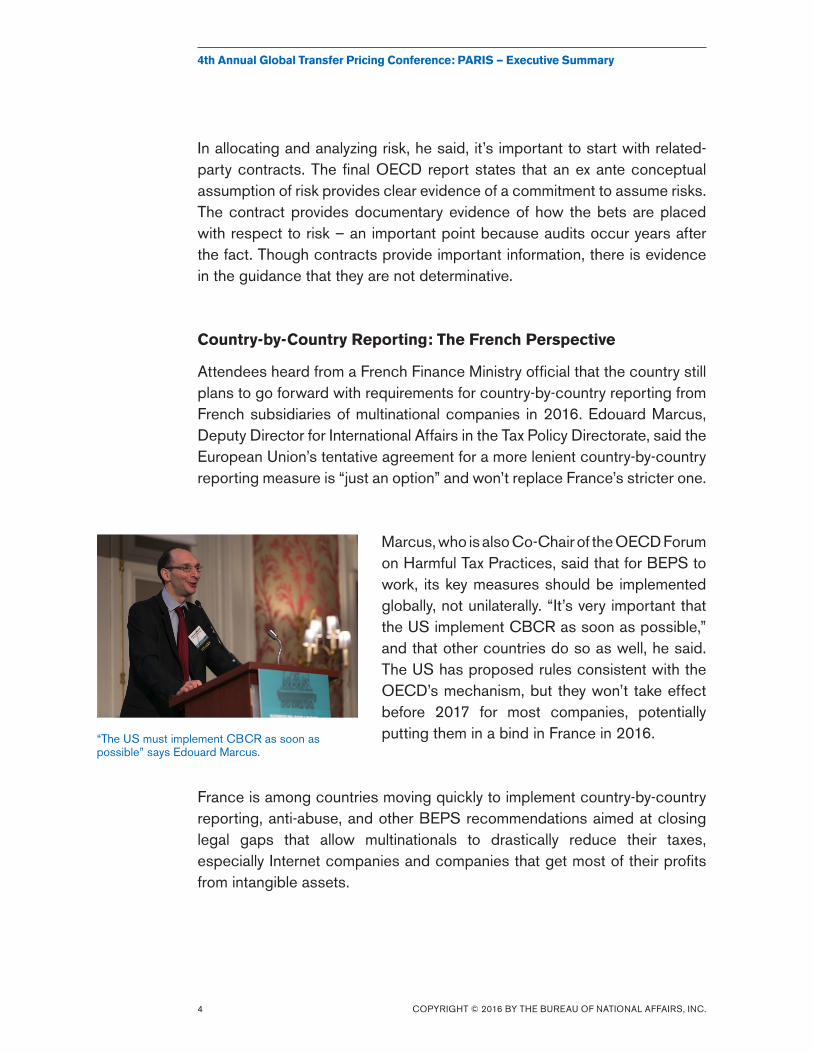

Attendees heard from a French Finance Ministry official that the country still plans to go forward with requirements for country-by-country reporting from French subsidiaries of multinational companies in 2016. Edouard Marcus, Deputy Director for International Affairs in the Tax Policy Directorate, said the European Union’s tentative agreement for a more lenient country-by-country reporting measure is “just an option” and won’t replace France’s stricter one.

Marcus, who is also Co-Chair of the OECD Forum on Harmful Tax Practices, said that for BEPS to work, its key measures should be implemented globally, not unilaterally. “It’s very important that the US implement CBCR as soon as possible,” and that other countries do so as well, he said. The US has proposed rules consistent with the OECD’s mechanism, but they won’t take effect before 2017 for most companies, potentially putting them in a bind in France in 2016.

France is among countries moving quickly to implement country-by-country reporting, anti-abuse, and other BEPS recommendations aimed at closing legal gaps that allow multinationals to drastically reduce their taxes, especially Internet companies and companies that get most of their profits from intangible assets.

4th Annual Global Transfer Pricing Conference: PARIS — Executive Summary

“The US must implement CBCR as soon as possible” says Edouard Marcus.

COPYRIGHT © 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC.5

Country-by-Country Reporting: The China Perspective

A Chinese practitioner, meanwhile, told attendees that country-by-country reporting requirements in China aren’t likely to take effect before May 31, 2017. Shanwu Yuan of Baker & McKenzie in New York (and a former SAT official) said the requirements will be contained in the transfer pricing circular due out later this year. Chinese officials, he said, are convinced that foreign multinationals aren’t paying their proper share of tax on income earned in China, and the new circular will look to remedy this through greater use of the profit split method, which he anticipates will be the default transfer pricing method for royalties, rather than calculating an arm’s-length price. “The common thread in all this is that multinationals will have to pay more tax in China,” he said.

Guidance to Come on Profit Split Method, OECD Says

Melinda Brown, a transfer pricing adviser with the OECD, gave an update on pending transfer pricing work at the organization, including guidance on the use of the profit split method. Saying it’s “incredibly difficult” to apply the method properly, Brown indicated there’s little appetite for widening the scope of its application. “This is not to say it shouldn’t be used if it is appropriate,” she added.

4th Annual Global Transfer Pricing Conference: PARIS — Executive Summary

Multinationals will have to pay more in China, says Baker & McKenzie Partner Shanwu Yuan.

Melinda Brown comments on the Profit Split Method.

COPYRIGHT © 2016 BY THE BUREAU OF NATIONAL AFFAIRS, INC.6

A World Customs Perspective

In a luncheon keynote address on Day 1, Liu Ping, Director of the World Customs Organization’s Tariff and Trade Affairs Directorate, called for more cooperation between tax and customs officials. One problem he cited was inconsistency in customs treatment of transfer pricing documentation. Efficient ways of addressing both sets of obligations include joint audits and joint advance pricing agreements, Liu said.

The latest Global Transfer Pricing Conference: Paris drew the largest audience to date in that city, with strong attendance on both days and vigorous discussion among panelists and attendees. The Bloomberg BNA and Baker & McKenzie Global Transfer Pricing Conference Series continues in Washington, DC on June 8 and 9; Toronto on August 29 and 30; and Hong Kong on September 19 and 20.

For more information on the series, please visit: www.bna.com/global-transfer-pricing-conference-series

Transfer pricing colleagues network at the Paris reception.

0416-JO19654 © 2016 The Bureau of National Affairs, Inc.