24

Annual Report 1997

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 pfc1Ticket No.: 23707 Date: 5.8.97 SW Status: 1

Annual Report 1997

Registered Office

Level 1, 48 Martin Place,

Sydney NSW 2000

Telephone (02) 9378 2000

Facsimile (02) 9378 3317

Company Secretary

J D Hatton

Investor Relations

Level 7, 48 Martin Place,

Sydney NSW 2000

Telephone (02) 9378 2638

Facsimile (02) 9378 2344

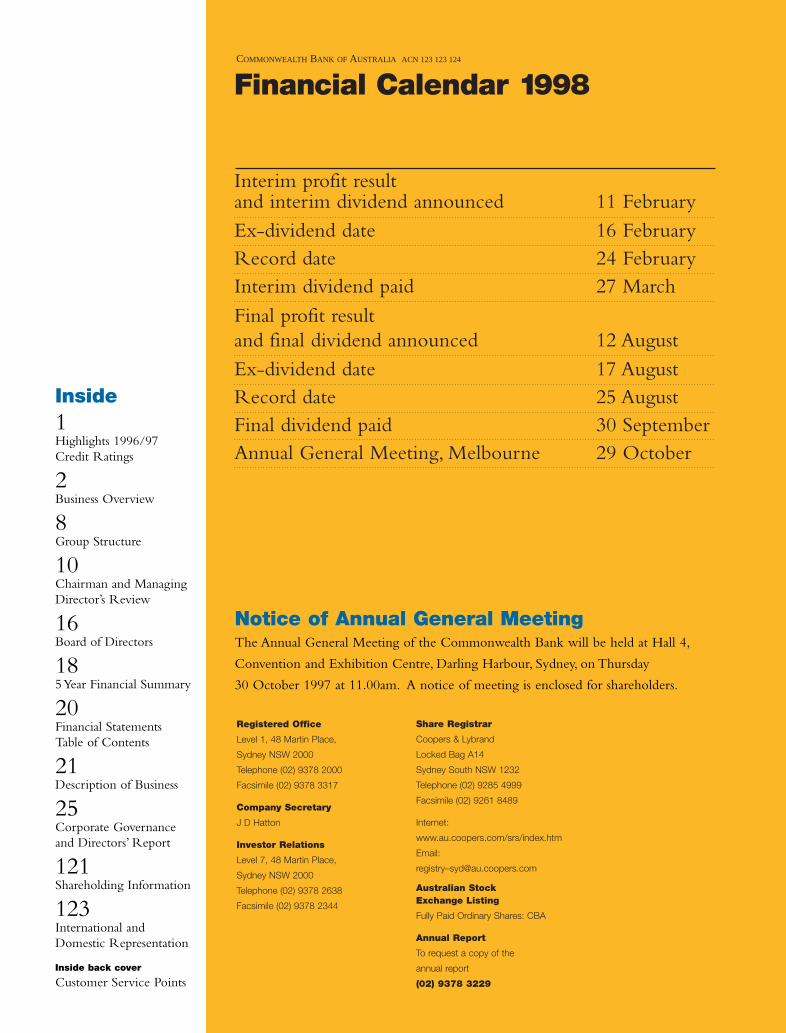

Financial Calendar 1998

Interim profit result and interim dividend announced 11 FebruaryEx-dividend date 16 FebruaryRecord date 24 FebruaryInterim dividend paid 27 March

Final profit result and final dividend announced 12 AugustEx-dividend date 17 AugustRecord date 25 AugustFinal dividend paid 30 SeptemberAnnual General Meeting, Melbourne 29 October

Notice of Annual General MeetingThe Annual General Meeting of the Commonwealth Bank will be held at Hall 4,

Convention and Exhibition Centre, Darling Harbour, Sydney, on Thursday

30 October 1997 at 11.00am. A notice of meeting is enclosed for shareholders.

Inside1Highlights 1996/97Credit Ratings

2Business Overview

8Group Structure

10Chairman and ManagingDirector’s Review

16Board of Directors

185 Year Financial Summary

20Financial StatementsTable of Contents

21Description of Business

25Corporate Governance and Directors’ Report

121Shareholding Information

123International and Domestic Representation

Inside back cover

Customer Service Points

COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 pBTicket No.: 23707 Date: 9.9.97 GR Status: 4

Share Registrar

Coopers & Lybrand

Locked Bag A14

Sydney South NSW 1232

Telephone (02) 9285 4999

Facsimile (02) 9261 8489

Internet:

www.au.coopers.com/srs/index.htm

Email:

registry–[email protected]

Australian Stock Exchange Listing

Fully Paid Ordinary Shares: CBA

Annual Report

To request a copy of the

annual report

(02) 9378 3229

Jun 92

Dec 92

Jun93

Dec 93

Dec 94

Jun95

Dec 95

Jun96

Dec 96

Jun97

Earnings per Share and Dividends per Share

Dividends per Share Earnings per Share(before abnormals)

0

10

20

30

50

70

Jun94

40

60

cents per share

1

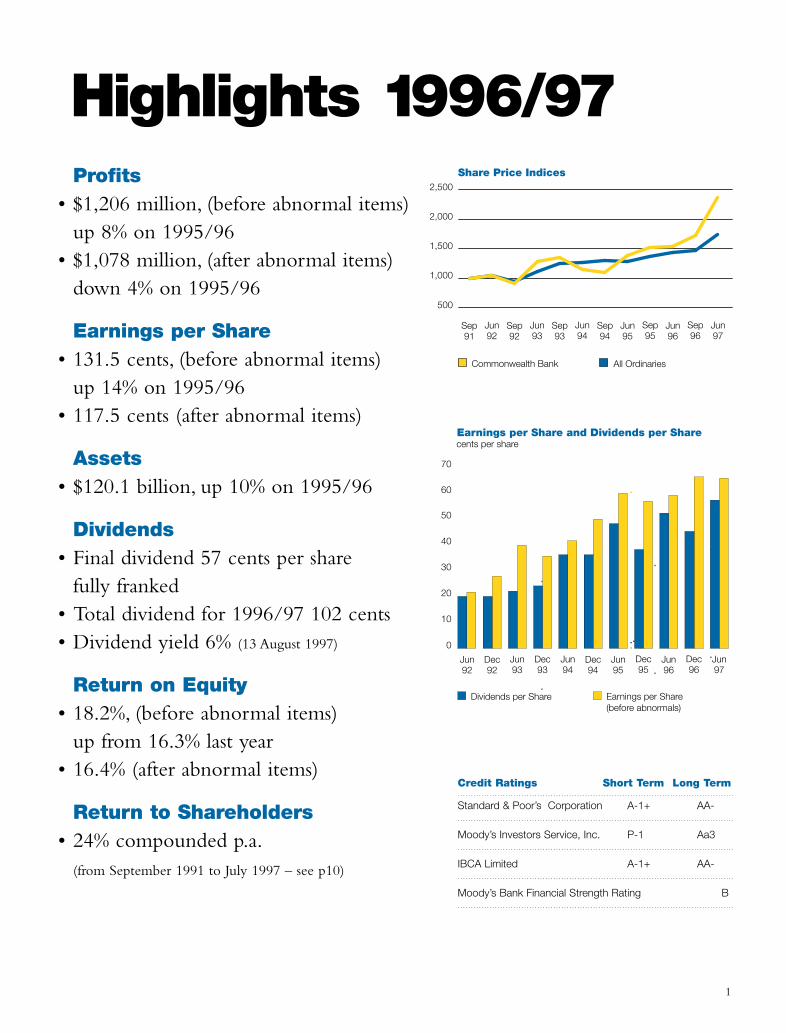

Profits• $1,206 million, (before abnormal items)

up 8% on 1995/96• $1,078 million, (after abnormal items)

down 4% on 1995/96

Earnings per Share• 131.5 cents, (before abnormal items)

up 14% on 1995/96 • 117.5 cents (after abnormal items)

Assets• $120.1 billion, up 10% on 1995/96

Dividends• Final dividend 57 cents per share

fully franked• Total dividend for 1996/97 102 cents• Dividend yield 6% (13 August 1997)

Return on Equity• 18.2%, (before abnormal items)

up from 16.3% last year • 16.4% (after abnormal items)

Return to Shareholders• 24% compounded p.a.

(from September 1991 to July 1997 – see p10)

Highlights 1996/97Share Price Indices

All OrdinariesCommonwealth Bank

500

1,000

1,500

2,000

2,500

Sep 91

Sep 92

Jun92

Jun93

Sep 93

Jun94

Sep 94

Sep 95

Jun96

Sep 96

Jun97

Jun95

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p1Ticket No.: 23707 Date: 27.8.97 GR Status: 3

Credit Ratings Short Term Long Term

Standard & Poor’s Corporation A-1+ AA-

Moody’s Investors Service, Inc. P-1 Aa3

IBCA Limited A-1+ AA-

Moody’s Bank Financial Strength Rating B

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p2Ticket No.: 23707 Date: 2.9.97 GR Status: 4

An Overview of the Bank’s Business

2

The Business

Australia’s largest retail bank,providing a full range of

lending and deposit productsto over 6 million customers.Services are provided throughthe largest branch and agencynetwork in the country,complemented by an expanding array of electronic, telephone andonline banking services, aswell as mobile sales teams.

Personal BankingHighlights

Over 800,000 Australians have a home loan withthe Commonwealth Bank. Between May 1996

and July 1997, the Commonwealth Bank cut home loaninterest rates by 370 basis points compared with a250 basis point reduction in cash rates by the ReserveBank.The result has been a 39% increase in grosshome loan approvals, and a sustained improvementin market share of home loan outstandings.

“True Awards” was launched in early July 1997, allowingeligible credit card clients to accumulate award pointsby using their cards; points can be redeemed for arange of benefits including discounts on bankproducts, shopping, entertainment, travel – or asa charity donation.For depositors, the Bank introduced “AwardSaver”in October 1996.This is a savings product offeringrewards, including bonus interest rates and fee discounts.NetBank, providing internet banking, was launchedin February 1997. NetBank enables CommonwealthBank customers to conduct secure banking activities,including access to statements and account balances,funds transfer and payment of bills over the internet.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p3Ticket No.: 23707 Date: 2.9.97 GR Status: 4

3

Established in 1995, this whollyowned subsidiary provides insurance

for house buildings and contents.Gross written premiums increased by24% to $84 million. CommonwealthConnect covers more than 330,000buildings and 80,000 contents risks,with the number of contents policiesdoubling during 1996/97.Commonwealth Connect willincreasingly meet the general insuranceneeds of Commonwealth Bank’s personaland business clients by offering theconvenience of access througheither the branch network or directby telephone.

Commonwealth Connect

Looking to the Future

The continuation of low inflationand more competitive markets will

see ongoing refinement of interestmargins and fees for services among allservice providers.To provide its servicesto all Australians, the CommonwealthBank will continue to invest in a range oftraditional branch based services and new

electronic or self service access points.The sustainability of the Bank’s

investment in these services willdepend on the adequacy ofrevenue from interest marginsand fees.Transaction serviceswill be priced on an activitybasis, with rewards for clients

conducting more of theirbusiness with the Bank.

The Commonwealth Bank will beworking to make it easier forcustomers to undertake bankingand other financial services relatedactivities through expansion of:

– the ATM network, which has alreadyincreased by over 50% over the pastthree years, and which will include anincreasing range of facilities;

– telephone banking, including theintroduction of “BPay”, allowingcustomers to pay bills to over 400companies from their telephonesat home;

– low cost EFTPOS merchant terminals,providing a convenient means ofpayment and access to cash;

– mobile sales teams providing customerswith the option of discussing banking andfinancial business at home or the office.

4

The Business

Australia’s fourth largest fund manager and secondlargest retail fund manager, with total funds

under management in excess of $23 billion. CFSprovides a comprehensive range of managedproducts, covering superannuation,retirement income and investment,along with life insurance products.Financial advice and products are available throughCommonwealth Bank branches and InvestmentCentres.A team of 160 nationwide specialistfinancial advisers provides customers withindividually tailored financial plans.As part of thestrategy to integrate financial services distribution,175 branch based personal bankers have also beentrained and “properly authorised” to advisecustomers on their investment needs.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p4Ticket No.: 23707 Date: 2.9.97 GR Status: 2

Highlights

Retail funds under managementgrew by 28% to $11 billion –

with strongest growth inCommonwealth Investment Fundsand the Cash Management Trust.In May 1997, the CommonwealthBank acquired a 50% equity share inIPAC Securities, a leading financialplanning firm. IPAC will provideaccess to the high growth portfoliomanagement and independentfinancial advice sector.

In December 1996, theCommonwealth Bank acquiredCommonwealth Funds ManagementLimited, increasing funds undermanagement by approximately$7 billion.Commonwealth SuperOption waslaunched in February 1997.Thisproduct is designed to assist thebusiness superannuation market,providing employers with a simple andflexible superannuation solution, whileoffering employees a choice ofinvestment strategies.

CommonwealthFinancial Services

An Overview of the Bank’s Business continued

5

The Business

A 75% owned subsidiary, meeting the banking,financial services and investment requirementsof some 800,000 New Zealanders.New Zealand’s most technologically advancedbank,ASB operates through a branch network,mobile bankers and phone banking facilities,together with well-established automated andelectronic channels.

Highlights

ASB recorded strong growth in all parts of itsbusiness.The Bank has achieved a main bankshare of 15% of the personal banking marketand is a leading provider of home loan finance.In addition,ASB maintained its leadershipposition in electronic banking throughthe introduction of new services, such asNew Zealand’s first electronic commercepayment system and internet banking service.

Looking to the Future

In keeping with its commitment to providecustomers with a broad range of financialservices,ASB Bank will introduce amore diversified range of managedfunds services.

During 1997/98,ASB Bank will furtheradvance the provision of direct banking services.

ASB Bank Limited

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p5Ticket No.: 23707 Date: 2.9.97 GR Status: 4

Looking to the Future

Consumers are now more awareand accepting of the need to be

financially self-sufficient throughouttheir lives, particularly into retirement,and are seeking investment choiceand control.CFS is extending its distributionnetwork and providing a range ofproducts and services that meets

customers’ needs.

Rapid evolution oftechnology, including theinternet, will createopportunities for CFSto provide innovativesolutions which

enhance customer service.Government initiatives, focusingon savings and superannuation,including superannuation memberinvestment choice, will result in anincreasing number of customersseeking financial advice. CFS isenhancing its investment advicecapabilities and will continue to workwith employers to provide flexibleand efficient solutions that meet theirsuperannuation obligations.

The Business

Establishing preferred financialservices relationships with the top

1,000 corporations, institutions andgovernment entities in Australasia,focusing on delivery of sophisticatedand valued banking andfinancial services.International operations includean increasing focus on Asia, wherethe Commonwealth Bank iscontinuing to develop its presencein selected markets.

An Overview of the Bank’s Business continued

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p6Ticket No.: 23707 Date: 2.9.97 GR Status: 4

Highlights

Significant incremental income fromfinancial market products and other

services. Successful positioning inrecent government privatisationsresulted in favourable outcomesin tenders for:

– Hazelwood Power Station, offeredvia trade sale by the VictorianGovernment;

– Brisbane Airport, as part of aconsortium which included Dutchgroup Schiphol, a manager of majorinternational airports world wide.

In June 1997, Indonesian authoritiesgranted the banking licence requiredfor the 50/50 joint venture betweenCommonwealth Bank and BankInternasional Indonesia to beginoperations. Initially operations willbe targeted at the commercialmarket, with a progressive move intothe rapidly growing retail market.

Looking to the Future

Recognising that excellencein service execution is critical

in winning and maintaining highquality business in Australia,Institutional Banking will continueits commitment to further developthe skills base, innovation and tradingabilities required for a successfulcombination of commercial andinvestment banking. Assessmentand management of risk will beconsistent with the complexityof the business targeted by theBank and product developmentswithin the market.

Institutional Banking

6

Queens landBRISBANE

7

The Business

The focus is on working with small tomedium businesses to achieve their

business and financial goals. Business Bankinghas over 120,000 client relationships.Over 50,000 are managed through 600Business Banking relationship managers in92 Business Banking Centres withapproximately 70,000 small businessesmanaged through the branch network.

CBFC offers secured debenture investments toretail investors, and is a specialist provider ofvehicle and equipment finance. CBFC operatesthrough Bank branches and Business BankingCentres, as well as through a team of fieldmanagers and accredited brokers.

Highlights

Business Banking lending approvalstotalled $12.8 billion to commercial

clients, an increase of 17% on the previousyear. Equipment finance through CBFCincreased by 34%.

Reflecting the Bank’s view that manybusinesses are moving away from fixed assets to“know how” to generate competitive advantage,an innovative form of lending – BusinessAsset Finance – was introduced. BusinessAsset Finance provides business with accessto finance based upon the “cash drivers” ofthe business.

Looking to the Future

Asignificant array of opportunities areavailable to the Commonwealth Bank and

its commercial clients based on informationsharing.The Bank will continue to designvalue added products and services based oninformation, as well as developing its traditionalrange of services.

Business Banking

Commonwealth Securities Limited– Share Direct – is a wholly owned

stockbroking subsidiary, whichcommenced activities in July 1995.During 1996/97, the customer basedoubled to over 110,000.

As part of Share Direct’s objective ofdelivering low cost transaction services,internet trading now complementsthe telephone based service, withinvestors able to monitor share pricesand place buy and sell orders directlyover the internet. (www.comsec.com.au)

Share Direct

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p7Ticket No.: 23707 Date: 2.9.97 GR Status: 4

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p8Ticket No.: 23707 Date: 5.8.97 SW Status: 1

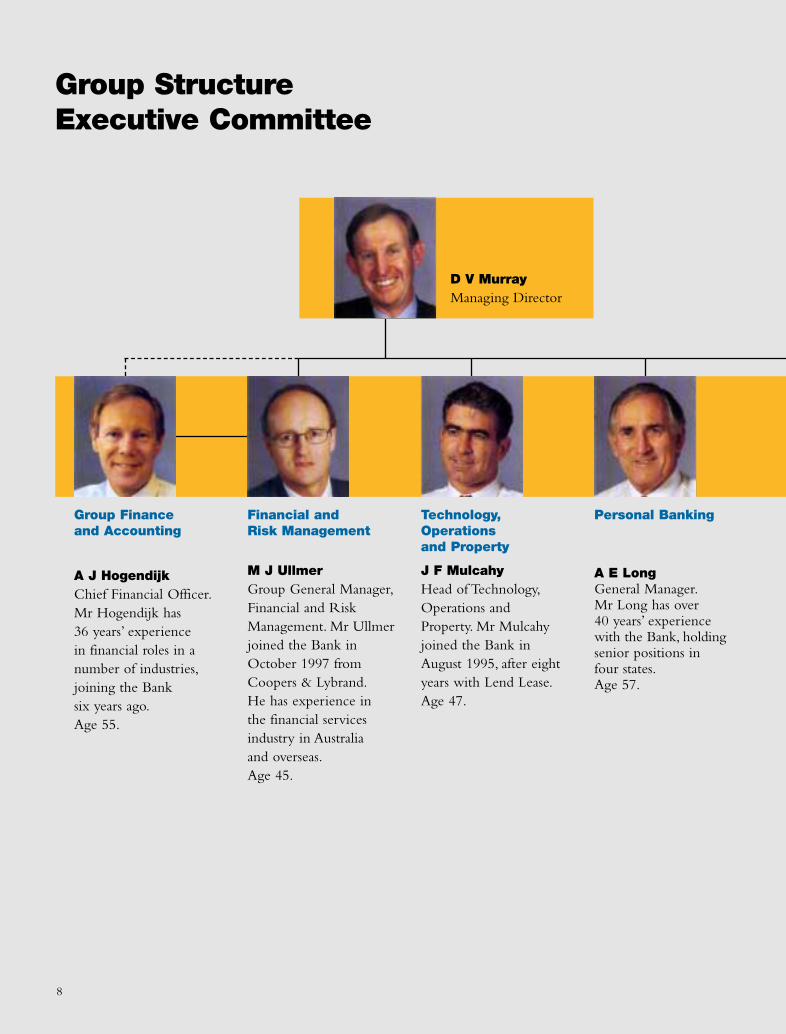

Technology,Operationsand Property

J F Mulcahy Head of Technology,Operations andProperty. Mr Mulcahyjoined the Bank inAugust 1995, after eightyears with Lend Lease.Age 47.

Group StructureExecutive Committee

8

Group Financeand Accounting

A J HogendijkChief Financial Officer.Mr Hogendijk has36 years’ experiencein financial roles in anumber of industries,joining the Banksix years ago.Age 55.

Personal Banking

A E LongGeneral Manager.Mr Long has over40 years’ experiencewith the Bank, holdingsenior positions infour states.Age 57.

D V MurrayManaging Director

Financial and Risk Management

M J UllmerGroup General Manager,Financial and RiskManagement. Mr Ullmerjoined the Bank inOctober 1997 fromCoopers & Lybrand.He has experience inthe financial services industry in Australiaand overseas.Age 45.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p9Ticket No.: 23707 Date: 5.8.97 SW Status: 1

9

Business Banking

N J CoxGeneral Manager.Mr Cox has 33 years’experience with theBank, appointed toestablish BusinessBanking in January1993. Chairman ofCBFC Ltd andMicrOpay Pty Ltd.Age 50.

InstitutionalBanking

M A KatzHead of InstitutionalBanking. Mr Katzjoined the Bank in1993 with investmentbanking experiencein Europe and Japan.Age 45.

CommonwealthFinancial Services

J St G D RawlinsGeneral Manager.Appointed in April1993, with over 30years’ experiencein banking, financeand insurance. DeputyChairman of LifeInsurance andSuperannuationAssociation.Age 57.

Group HumanResources

L G CupperGeneral Manager.Has had over 25 years’experience in seniorhuman resources roles.Mr Cupper joinedthe Bank in January1996, following12 years withCRA Limited.Age 48.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p10Ticket No.: 23707 Date: 9.9.97 GR Status: 6

Reflecting the Bank’s increasing competitiveness,growth in lending assets, particularly in home loans, was amajor contributor to the 10% increase in Group assets, to$120 billion. Operating profit before abnormals grew by8% to $1,206 million. Return on shareholders’ equitybefore abnormals increased from 16.3% to 18.2%.

A fully franked final dividend of 57 cents per sharebrought the dividend for 1996/97 to 102 cents per share.Returns to shareholders, based on the accumulationindex, have grown at an annual compound rate of 24%since listing in September 1991.

After careful analysis of the capital needed to sustaincompetitive advantage, directors proposed a $650 millionshare buy back to be conducted following the conversionof the instalment receipts to fully paid ordinary sharesin November 1997. A final decision to proceed will beannounced in November, subject to no material adversechange in the Bank’s current or prospective capitalposition.

The buy back is likely to represent 4% of the Bank’scurrent shares on issue, and is expected to increaseearnings per share by around 2%. Following the buyback, on a proforma basis, the capital ratio would be 10%and the Tier 1 ratio 7.9%.

Directors have also decided to eliminate the discounton the Dividend Reinvestment Plan, commencing withthe 1998 interim dividend.

Both measures are designed to increase shareholdervalue by optimising the capital position of the Bankwhile not limiting the capacity to reinvest for futuresustainable competitive advantage.

The Commonwealth Bank’s Next Phase

Commonwealth Bank now enters another phaseof its development during which important

investment decisions will position the institution intothe next century.

Key principles that will guide the Group’s businessstrategy are:• to provide convenient, affordable integrated

banking and financial services, offering clientschoice and reward;

• to manage risk;• to provide effective leadership of our people.

The positioning of the Commonwealth Bank will beundertaken in an environment in which the Australianfinancial services industry is becoming increasinglycompetitive, and in which each part of the value chainis effectively open to entry by new competitors.

Chairman and Managing Director’s Review

10

1997marks the successful completionof the Commonwealth Bank’srepositioning following

privatisation in 1991.The key objectives set over that sixyear period have been met, with the Bank reclaiming marketshare in the home loan market, achieving a strong increasein the revenue contribution from investment banking,integrating financial services, increasing operating efficiency,and bringing capital and risk management practices to levelscomparable with major competitors.

Pictured left to right M A Besley, AO (Chairman) D V Murray, (Managing Director)

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p11Ticket No.: 23707 Date: 2.9.97 GR Status: 5

This follows a transition within the industry froma regulated market in the mid 1980s, where banks wereinvolved in most elements of the value chain, through aperiod in which most gains were made via productivityimprovement within this traditional system.

Cash flow return to investors, made possible by lowinflation, and aided by recovery from the cyclical troughin earnings of the late 1980s and early 1990s, has beenstrong during this transition.

The current environment is characterised

by changing demands on management, with

technological change, low inflation, an increase in

savings and an aging population, shifts in capital

management, and changing patterns of capital

investment. At the same time, return on

shareholders’ equity is relatively strong.

The key issue, then, is how to obtain sustainable

competitive advantage given the trade off between

cash returns and investment for growth.

Technological innovation

Increasingly, the driver of the growth of non bank assetswill be technological change, particularly technology

affecting the transfer of financial assets.In addition, ease of information exchange will allow

a very different relationship to develop between thefinancial services organisation and the customer.Information technology will enable organisations todevelop relationships with customers without atraditional branch network.

Introduction of self-service technology, providinggreater convenience for customers and efficiency gainsfor suppliers, will further strengthen the growth ofnon bank financial intermediation.

Low inflation

In recent years, substantial improvements have beenmade to credit risk management techniques.These

techniques are being extended to more scientificcalculation of both expected and unexpected loss, thelatter leading to a better understanding of the amount ofequity required to support the credit risk portfolio.Generally, the loss experience used in these calculations is

over the most recent business cycles, since longer runsof these data are rarely available.

In Australia, the last business cycle coincided withboth the deregulation of the banking system andhistorically high inflation. It is unlikely that the lossexperience over this cycle will be repeated in the currentcycle, which is characterised by low inflation.As a result,if the low inflationary environment is maintained, theloss experience could remain lower than some observersexpect, provided major structural change does notmaterially increase risk.

Savings and the aging population

Since deregulation the growth of bank intermediatedassets has not kept pace with the growth of non bank

assets, with banks growing by about 11% compoundsince 1985 (with most of that skewed to the late 1980s)and non banks (at a steadier rate) by about 16%.

This has been driven in Australia, as elsewhere, by anaging population and technological change.

Over the next five years, non bank assets will probablygrow at 1.5 times the bank assets.This trend, reinforcedby the government’s retirement incomes policy, isaccompanied by increasing demand for managementof personal wealth for retirement.

Capital management

Current levels of capital generation are high,reflecting the dramatic improvement in earnings

since the later 1980s/early 1990s, and changes in capitalmanagement practices, particularly in relation to theassessment of the equity underpinning needed forfinancial intermediation.

At the same time, the combination of low inflationand the introduction of dividend imputation isencouraging the trend towards increasing cash flowreturns to shareholders.

Changing patterns of capital investment

The financial services industry has been characterisedby a comparatively low ratio of capital expenditure

to earnings.To maintain existing businesses at theircurrent scale, financial services organisations are spending

11

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p12Ticket No.: 23707 Date: 2.9.97 GR Status: 5

Chairman and Managing Director’s Review continued

12

approximately one third of earnings on capital investment– with a large part of this going into operatingexpenditure through software.

This compares with a ratio of capital expenditureto earnings of close to 75% for industrial companiesin Australia.

Capital expenditure in the financial services industrywill increase over the next few years, as the industryinvests in new businesses and new distribution systems.

Positioning Commonwealth Bank

Given the factors prompting change within theindustry, Commonwealth Bank is being positioned

to provide a choice of bank, non bank and managed fundfinancial services, sourced either from within or outsidethe Group.That is, the Bank is shifting from being acustodian of savings to a manager of wealth.

Since 1993, the Bank has been investing acrossa number of fronts, designed to:• maximise efficiency and leverage scale;• segment client bases and differentiate service

according to value;• increase customer financial (investment and credit)

balances through integrated distribution of allproducts, provision of client advice, differentiation onbrand and information and convenience of access;

• diversify revenue sources by business and bygeographic region;

• change the management culture by using planningsystems dedicated to growth in value and by makingmanagers accountable for their team’s targets andleadership of their people.The ensuing commentary reviews progress in the

six businesses of the Bank.

1. Personal Banking and the

Home Mortgage Market

Four major changes were designed to repositionthis business.

First, the Bank needed to change the method ofdistribution, away from the emphasis on branches toautomatic teller machines, electronic funds transfer

terminals, and increasingly, telephone and internetbased capabilities.

Branch numbers have been reduced from close to1800 to 1334, the number of ATMs has doubled andelectronic funds transfer terminals trebled.

Second, the Bank had to remove back officeprocessing from the branches – this took two years,and reduced full time equivalent staff numbers by 8000.The result is ongoing increases in processing efficiency.

Third, a sales and service focus was needed. Newstandards of performance were established and a salesand service culture embedded.

Fourth, the product mix needed to be changed.New products have been introduced, old ones mademore flexible.

Over the past 18 months, the Bank has faced up toa critical issue that affects it more than any otherparticipant in the Australian financial services industry– cross subsidies between home loan borrowers anddepositors, including transaction account holders.

In May 1996, the Bank announced that it had takensteps to remain a key provider of home loans in theAustralian market.This came from a determination thathome loans were an important product in the total suiteof financial services to which the Bank was adapting.

In addition, the Bank was aware that in other markets,the value chain had broken into distinct segments – andthat the banks had given away their leading position asmortgage originators and had therefore potentially alsogiven away their position as a complete financialservices provider.

Since May 1996, the Bank has made two priceadjustments in addition to those following cuts inofficial cash rates by the Reserve Bank of Australia.

The consequence of these changes has been anincrease in business volumes, particularly in the homeloan market, where strong growth in originations hastranslated into sustained improvement in the Bank’sshare of balances outstanding.

The cost of the price adjustment has been partlyoffset by volume growth and by a lengthening in the

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p13Ticket No.: 23707 Date: 2.9.97 GR Status: 5

duration of the mortgage book. However, there are evenmore important factors in play.

For example, reducing the mortgage spread caused achange in the competitive profile for all retail deposits.With a well established financial services arm, this hasstrengthened the Commonwealth Bank’s competitivepositioning going forward, notwithstanding the costof the adjustment.

2. Financial services integration

Financial services will continue to grow much morequickly than traditional bank services.Already,

Commonwealth Financial Services is the fourth largestfund manager in Australia and the second largest retailfunds manager.

This business is producing solid returns and theoutlook for earnings growth is reasonably strong throughthe potential to increase “share of wallet” of existingpersonal banking customers.The Bank currently receives,on average, just over 50% of the profit generated by thesecustomers to the financial services industry; this hasimproved by about one percentage point, year-by-yearfor the last four years.The greatest potential to increase“share of wallet” is amongst clients generating the highestlevels of profit to the industry.

In funds management, growth has been acceleratingin the retail market, where Commonwealth Bank isable to successfully leverage off its distribution network.

In late 1996, the Bank acquired CommonwealthFunds Management, a wholesale fund manager,increasing funds under management by approximately$7 billion. In 1997, the Bank acquired a 50% interest inIPAC, providing growth prospects from the portfoliomanagement and independent advice sector.

3. Business Banking

The challenge of building customer relationshipswhile increasing efficiency and diversifying revenue

sources is being met through a combination ofreductions in operating costs, repricing and increasingproduct sales per customer.

Reflecting the Bank’s view that many businesses aremoving away from fixed assets to intellectual property togenerate competitive advantage, an innovative form oflending (Business Asset Finance) has been introducedwhere business is financed without reliance ontraditional security.

The integration of Commonwealth DevelopmentBank and CBFC into Business Banking, plus the moveinto payroll services and fleet management, has enhancedthe delivery of integrated services to commercial clients.

To get further growth, new services need to be added.The Bank’s belief is that these new services should be

based on information sharing between the client and theBank, so that, for example, credit processes can be furtherenhanced for both the Bank and its clients.

4. Institutional Banking

The institutional banking market will continueto face pressure from increased competition from

foreign banks and from general disintermediation. Creditspreads for better quality assets are therefore unlikely toimprove. In addition, the stable, low inflationenvironment and the globalisation of financial marketswill continue to squeeze profitability in traditionalbalance sheet activities.

In this environment, to improve return on equity, andachieve a better use of economic equity, the Bank hasmoved to a hybrid of corporate and investment banking.This has required building skills in structured financingand distribution, upgrading trading capability and marketrisk management and establishing an equities group.

The Bank’s initial focus was on financing infrastructuredevelopments, in particular toll roads. From this, the Bankwas able to successfully bid for roles in the privatisationof the electricity industry and airports.The Bank is nowwell positioned for involvement in further infrastructuredevelopments and privatisations, with the capacityto underwrite, sell and distribute both debt andequity instruments.

13

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p14Ticket No.: 23707 Date: 2.9.97 GR Status: 5

5. Processing efficiency

The Bank’s Technology, Property and Operationsgroup has become a profit centre.The group

manages the Bank’s information technology strategy,$1.4 billion property portfolio, and item and loanprocessing operations. Performance is driven by securinglower unit costs through productivity improvements, andincreasing scale through acquisition of greater volumes.

Best practice benchmarks are used to ensure the Bankhas the necessary understanding of what is happening ateach point in the value chain.This, in turn, will be thebasis for decisions about insourcing, outsourcing orfurther joint venture arrangements.

In item processing, the Bank has scale, and is alreadyhighly efficient as measured against best practice. Here, anoption is to insource as the Australian industry looks forways to aggregate its business.

In loan processing, the Bank is close to its targetbenchmarks, and again insourcing is an option.

In August 1997, the Bank announced a decision tonegotiate a strategic technology partnership with a globalinformation technology company, EDS.The Bankproposes to take a 35% equity position in this partnershipthrough EDS Australia.

The major benefits to the Bank will be substantial,and include:• cost reductions, and a switch from fixed to

variable costs;• ongoing productivity improvements;• better application of technology;• speed to market with new products;• reduction of risk; and• a share in earnings growth from the rapidly growing

outsourcing industry in Australia, as well as theAsia Pacific region where EDS already has astrong presence.The proposed contract will be for 10 years, with

two five year options. Over the 10 year period, the valueof the contract to EDS Australia will be approximatelyA$5 billion.

All IT functions, both developmental and operational,are to be included in the proposed technologypartnership.A small group within the Bank will maintaincontrol of the Bank’s technology strategy.

6. Geographic diversification

– New Zealand and Asia

ASB Bank has produced strong growth in assets andprofits since acquisition in 1989. It is continuing to

grow its business organically and through diversification.As in Australia, factors affecting New Zealand banking

are driving fundamental change. Competition is intense,not only between existing banks but also due toemerging market entrants.ASB will continue to leverageits major share of the Auckland personal market throughits competitive use of banking technology.

Sustained rapid growth in Asia will continue topresent opportunities for Commonwealth Bank inproviding financial services to the region.

In June 1997, Indonesian authorities granted thebanking licence required for the 50/50 joint venturebetween Commonwealth Bank and Bank InternasionalIndonesia to begin operations. Initial operations will betargeted at the commercial market, with a progressivemove into the rapidly growing retail market.

Implications for growth and returns

Cross subsidies within the banking industry areyet to be worked through.

If this results ultimately in fairer returns for investmentin transaction services then revenue will increase and/orservicing costs will fall.

However, if cross subsidies are maintained, the Bankwill face a decision about whether or not to continueto provide the gamut of transaction services.

Over the medium term, the Bank is repositioning itsdistribution system, so that in modifying the branchnetwork and growing the new, clients’ range of needsare well met.

At the same time, the Bank must continue to investin the development of rapidly expanding businesses,such as financial services, in order to maintainearnings momentum.

14

Chairman and Managing Director’s Review continued

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p15Ticket No.: 23707 Date: 2.9.97 GR Status: 5

15

Growth in net interest earnings will continue to betempered by margin squeeze. Productivity growth willcome predominantly from pricing signals andopportunities for insourcing, outsourcing and jointventures. Organisational change – moving to a functionalcost centre structure that identifies the performance of allcomponents of the value chain – also represents apotential source of productivity gain.

The Bank needs to invest to strengthen its

competitive position.

Its acquisition appetite is focused. It will continue toassess opportunities in New Zealand and Asia. InAustralia, the Bank already has scale in its traditionalbusinesses and will focus on opportunities thatcomplement existing operations.

Outlook for 1997/98

In 1997/98, the Commonwealth Bank expectsreasonable levels of demand for finance to support

continuing asset growth.Competition in all markets is likely to remain keen.

Pressure on margins will continue, heightened by theflow through of the significant reductions to home loanmargins during 1996/97, as well as by the distortionsinherent in the deeming arrangements.

Anticipated further growth of income from financialservices and investment banking will increase thecontribution from non interest income.

The Bank’s cost structure, although the subject ofcontinuing emphasis on productivity gain, will remainunder pressure from labour costs,Year 2000 systemsmodifications and continuing reinvestment in distributionsystems and new businesses.

Credit quality remains sound overall and the bad debtexpense is expected to remain cyclically low. However,a slowing in writebacks means that the bad debt expenseis likely to be higher than in 1996/97.

Competition is set to intensify with implementationof the recommendations of the Wallis Inquiry into theFinancial System. However, the detail of regulatorychanges has yet to be completed and implementationis to be phased over the next two years.The majorcompetitive effects are therefore expected to materialisebeyond 1997/98.

Overall, the market environment during 1997/98is expected to be testing. However directors see noreason why a relatively strong payout cannot bemaintained for the time being.

Acknowledgements

During the year, two members of the Board retired.Mr J J Kennedy left the Board in order to pursue

other interests and Mr I K Payne, an executive director,retired from the Bank. Both directors shared a verylengthy period of service during one of the Bank’shistorically significant and successful phases ofdevelopment.The Board thanks them for theircontribution.

The Board welcomes two new members, Mr F J Swanand Mr K E Cowley,AO. In accordance with the Bank’sArticles of Association, both will stand for electionas directors at the Annual General Meeting on30 October 1997.

The Bank’s results reflect dedicated teamwork amongstmanagement and staff, teamwork that is vital to ensuringthat the Bank has the necessary flexibility to meet clients’requirements for convenient and affordable banking andfinancial services.The Board extends its thanks for a jobwell done.

Finally, the Board would like to thank shareholders fortheir continuing support and encouragement.

M A Besley, AOCHAIRMAN

D V MurrayMANAGING DIRECTOR

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p16Ticket No.: 23707 Date: 5.8.97 SW Status: 1

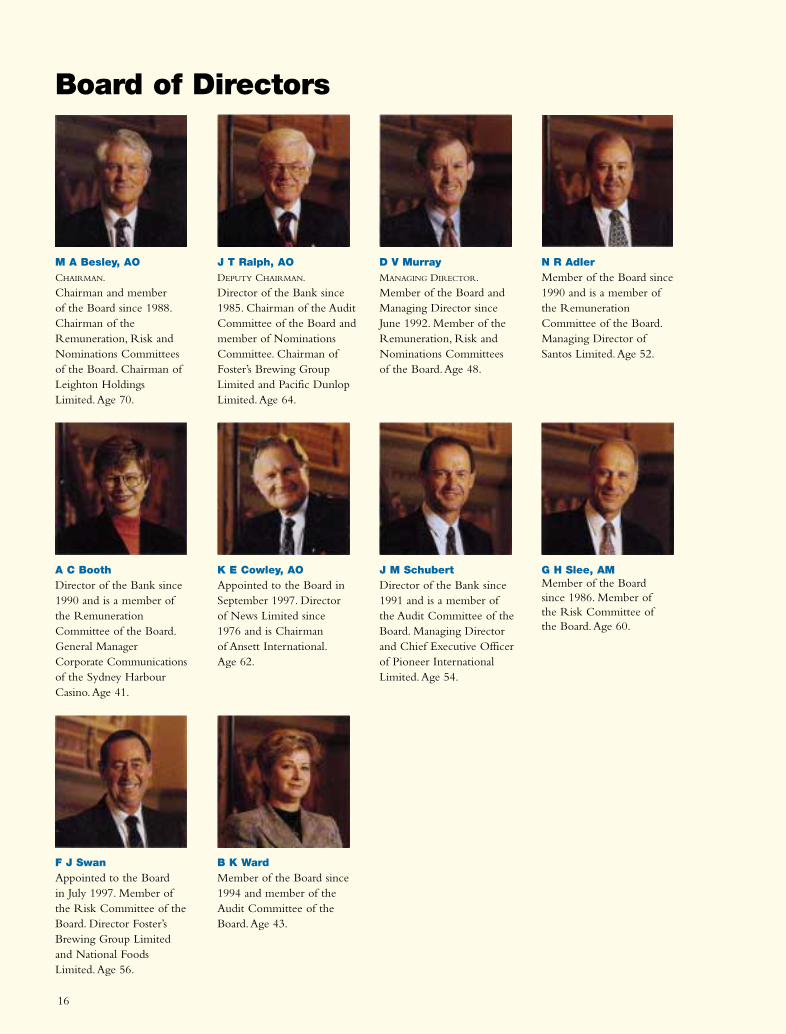

Board of Directors

16

A C BoothDirector of the Bank since1990 and is a member ofthe RemunerationCommittee of the Board.General ManagerCorporate Communicationsof the Sydney HarbourCasino.Age 41.

J T Ralph, AODEPUTY CHAIRMAN.

Director of the Bank since1985. Chairman of the AuditCommittee of the Board andmember of NominationsCommittee. Chairman ofFoster’s Brewing GroupLimited and Pacific DunlopLimited.Age 64.

D V MurrayMANAGING DIRECTOR.

Member of the Board andManaging Director sinceJune 1992. Member of theRemuneration, Risk andNominations Committeesof the Board.Age 48.

N R AdlerMember of the Board since1990 and is a member ofthe RemunerationCommittee of the Board.Managing Director ofSantos Limited.Age 52.

K E Cowley, AOAppointed to the Board inSeptember 1997. Directorof News Limited since1976 and is Chairmanof Ansett International.Age 62.

J M SchubertDirector of the Bank since1991 and is a member ofthe Audit Committee of theBoard. Managing Directorand Chief Executive Officerof Pioneer InternationalLimited.Age 54.

G H Slee, AMMember of the Boardsince 1986. Member ofthe Risk Committee ofthe Board.Age 60.

F J SwanAppointed to the Boardin July 1997. Member ofthe Risk Committee of theBoard. Director Foster’sBrewing Group Limitedand National FoodsLimited.Age 56.

B K WardMember of the Board since1994 and member of theAudit Committee of theBoard.Age 43.

M A Besley, AOCHAIRMAN.

Chairman and memberof the Board since 1988.Chairman of theRemuneration, Risk andNominations Committeesof the Board. Chairman ofLeighton HoldingsLimited.Age 70.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p17Ticket No.: 23707 Date: 5.8.97 SW Status: 1

1997 Financial Statementsas at 30 June

17

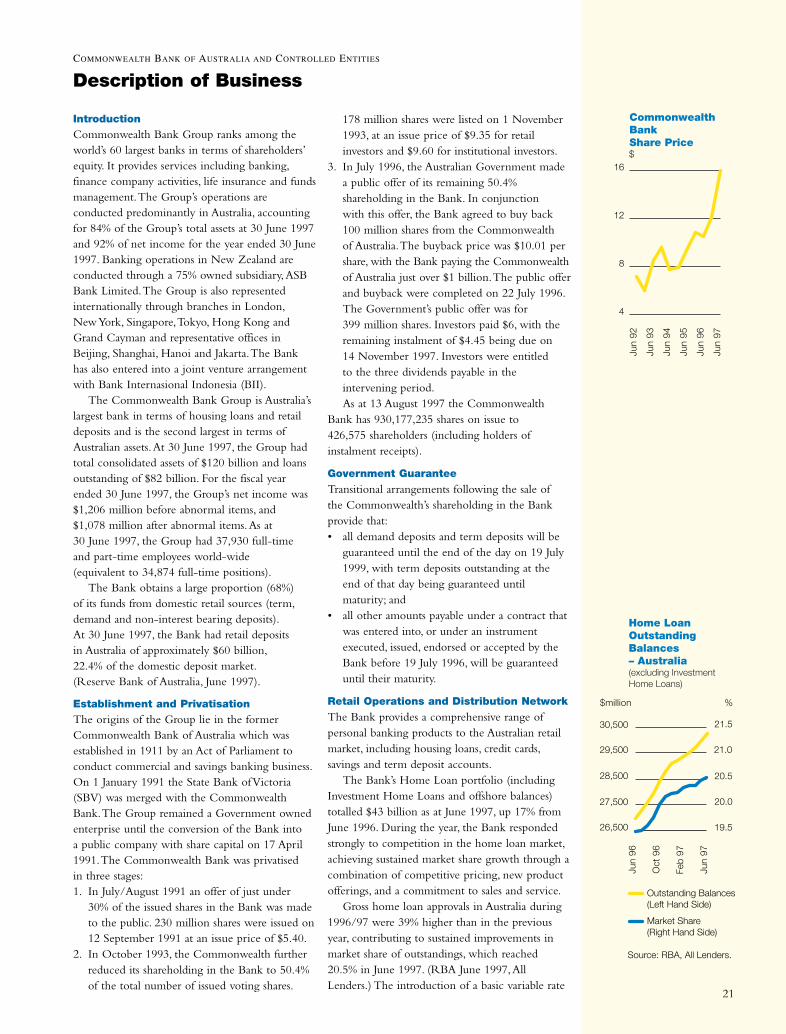

IntroductionCommonwealth Bank Group ranks among theworld’s 60 largest banks in terms of shareholders’equity. It provides services including banking,finance company activities, life insurance and fundsmanagement.The Group’s operations areconducted predominantly in Australia, accountingfor 84% of the Group’s total assets at 30 June 1997and 92% of net income for the year ended 30 June1997. Banking operations in New Zealand areconducted through a 75% owned subsidiary,ASBBank Limited.The Group is also representedinternationally through branches in London,NewYork, Singapore,Tokyo, Hong Kong andGrand Cayman and representative offices inBeijing, Shanghai, Hanoi and Jakarta.The Bankhas also entered into a joint venture arrangementwith Bank Internasional Indonesia (BII).

The Commonwealth Bank Group is Australia’slargest bank in terms of housing loans and retaildeposits and is the second largest in terms ofAustralian assets.At 30 June 1997, the Group hadtotal consolidated assets of $120 billion and loansoutstanding of $82 billion. For the fiscal yearended 30 June 1997, the Group’s net income was$1,206 million before abnormal items, and$1,078 million after abnormal items.As at30 June 1997, the Group had 37,930 full-timeand part-time employees world-wide(equivalent to 34,874 full-time positions).

The Bank obtains a large proportion (68%)of its funds from domestic retail sources (term,demand and non-interest bearing deposits).At 30 June 1997, the Bank had retail depositsin Australia of approximately $60 billion,22.4% of the domestic deposit market.(Reserve Bank of Australia, June 1997).

Establishment and PrivatisationThe origins of the Group lie in the formerCommonwealth Bank of Australia which wasestablished in 1911 by an Act of Parliament toconduct commercial and savings banking business.On 1 January 1991 the State Bank of Victoria(SBV) was merged with the CommonwealthBank.The Group remained a Government ownedenterprise until the conversion of the Bank intoa public company with share capital on 17 April1991.The Commonwealth Bank was privatisedin three stages:1. In July/August 1991 an offer of just under

30% of the issued shares in the Bank was madeto the public. 230 million shares were issued on12 September 1991 at an issue price of $5.40.

2. In October 1993, the Commonwealth furtherreduced its shareholding in the Bank to 50.4%of the total number of issued voting shares.

178 million shares were listed on 1 November1993, at an issue price of $9.35 for retailinvestors and $9.60 for institutional investors.

3. In July 1996, the Australian Government madea public offer of its remaining 50.4%shareholding in the Bank. In conjunctionwith this offer, the Bank agreed to buy back100 million shares from the Commonwealthof Australia.The buyback price was $10.01 pershare, with the Bank paying the Commonwealthof Australia just over $1 billion.The public offerand buyback were completed on 22 July 1996.The Government’s public offer was for399 million shares. Investors paid $6, with theremaining instalment of $4.45 being due on14 November 1997. Investors were entitledto the three dividends payable in theintervening period.As at 13 August 1997 the Commonwealth

Bank has 930,177,235 shares on issue to426,575 shareholders (including holders ofinstalment receipts).

Government Guarantee

Transitional arrangements following the sale ofthe Commonwealth’s shareholding in the Bankprovide that:• all demand deposits and term deposits will be

guaranteed until the end of the day on 19 July1999, with term deposits outstanding at theend of that day being guaranteed untilmaturity; and

• all other amounts payable under a contract thatwas entered into, or under an instrumentexecuted, issued, endorsed or accepted by theBank before 19 July 1996, will be guaranteeduntil their maturity.

Retail Operations and Distribution Network

The Bank provides a comprehensive range ofpersonal banking products to the Australian retailmarket, including housing loans, credit cards,savings and term deposit accounts.

The Bank’s Home Loan portfolio (includingInvestment Home Loans and offshore balances)totalled $43 billion as at June 1997, up 17% fromJune 1996. During the year, the Bank respondedstrongly to competition in the home loan market,achieving sustained market share growth through acombination of competitive pricing, new productofferings, and a commitment to sales and service.

Gross home loan approvals in Australia during1996/97 were 39% higher than in the previousyear, contributing to sustained improvements inmarket share of outstandings, which reached20.5% in June 1997. (RBA June 1997,AllLenders.) The introduction of a basic variable rate

COMMONWEALTH BANK OF AUSTRALIA AND CONTROLLED ENTITIES

Description of Business

21

12

8

Commonwealth Bank Share Price

Jun

92

Jun

95

Jun

93

Jun

94

Jun

97

Jun

96

16

4

$

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p21

Ticket No.: 23707 Date: 1.9.97 GR Status: 3

26,500

27,500

28,500

29,500

30,500

19.5

20.0

20.5

21.0

21.5

Home LoanOutstanding Balances– Australia(excluding Investment Home Loans)

$million %

Jun

96

Jun

97

Oct

96

Feb

97

Outstanding Balances (Left Hand Side)

Market Share (Right Hand Side)

Source: RBA, All Lenders.

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p22Ticket No.: 23707 Date: 9.9.97 SW Status: 3

COMMONWEALTH BANK OF AUSTRALIA AND CONTROLLED ENTITIES

Description of Businesscontinued

22

home loan product, the “Economiser”, has provedpopular with customers who do not require awider range of options.

The proportion of home loan balances inarrears (over 90 days) fell from 0.9% in June 1996to 0.6% in June 1997 (includes investment homeloans).This has been achieved by tightermanagement of delinquent accounts and bycontinuing attention to credit quality in a highlycompetitive environment.

The Bank is the largest holder of retail depositsin Australia with a market share of 22.4% as atJune 1997. (RBA, June 1997).The Bank’sAustralian retail deposit base grew by 9.4% overthe past 12 months to stand at approximately$60 billion as at 30 June 1997.Approximately 60%of retail deposits are held in on-demand productsand 40% in term deposits.The CommonwealthBank has the largest share of pensioner deemingaccounts with balances of over $7.5 billion as atJune 1997.

The Bank is the largest issuer of credit cards inAustralia. Competition within the credit cardmarket is keen, and has been heightened by theentry of new market participants. Nevertheless, theBank’s credit card outstandings grew by 9.8% overthe past 12 months to stand at $1.8 billion as at30 June 1997, representing a market share of23.5%. (Australian Bankers Association, June1997.) The quality of the credit card portfolio hasremained steady, with delinquencies in dollarterms increasing in line with the growth inoutstanding balances.

The Bank is an original global foundingshareholder in the Mondex smart card system andhas been participating in MasterCard and Visapilots of stored value cards – microchip basedsmart cards offering an electronic alternative tocash for small transactions. Smart card technologyhas the potential to offer significant benefits interms of processing efficiencies and, via thepotential integration of customer informationwithin the microchip, offers wider opportunitiesin terms of customer relationship development.The Bank’s distribution network provides serviceto over 6 million customers through over 70,000service points, including the largest branch andagency network in the country (1,334 branchesand 4,205 agencies, including 3,852 in AustraliaPost Offices).The Bank continues to invest in thedevelopment and expansion of its direct andelectronic distribution channels, to providecustomers with greater convenience at lower cost.There has been a steady shift in transactionalactivity from branches to alternative distribution

channels, with the ratio of branch to electronictransactions carried out by customers improvingfrom 40/60 in June 1995, to 30/70 in June 1997.Highlights include:• Autobank – the Bank maintains the largest

proprietary ATM network in the country, withCommonwealth Bank terminal numbersincreasing by 9% from June 1996, to 2,301 asat 30 June 1997. Including interchangearrangements, the Bank’s customers haveaccess to over 5,500 terminals Australia-wide.The Bank’s ATM network handled 16% moretransactions in 1996/97 compared with theprevious year.

• EFTPOS – total terminal numbers as at30 June 1997 of 63,370 represent an increaseof 45% over the last 12 months, or a 200%increase from June 1995. Since theintroduction of the Comm2000 EFTPOSterminal in September 1994, the Bank’s shareof the total EFTPOS terminal population inAustralia has increased from 13% to almost40% as at June 1997.

• Maestro and Cirrus internationalATM/EFTPOS networks – providingcustomers with access to over 315,000 ATM’sand over 1.4 million EFTPOS terminals world-wide.

• NetBank – the Bank’s Internet bankingservice launched in February 1997, withusage growing.

• Telephone banking – three customer servicecentres now handle in excess of 700,000customer calls per week, an increase of 50%over the previous year.The service was furtherexpanded to include direct home loan salesin NSW from August 1996 – extending toan Australia-wide service by March 1997.

• Supermarket banking – in January 1996 theCommonwealth Bank was the first bank inAustralia to launch a supermarket branch.The Bank now has five supermarket branches,offering personal banking services, includingdeposit, investment, credit card, personal andhome lending products.

• Mobile salesforce – mobile bankers are nowavailable to call on customers at a time andplace most convenient to them, with furtherexpansion planned. Mobile bankers account forover 20% of all home loan approvals (by value).

Increase in EFTPOS Terminals

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

Jun

97M

ar 9

7D

ec 9

6S

ep 9

6Ju

n 96

Mar

96

Dec

95

Sep

95

Jun

95

Comm2000 Terminals

Non Comm2000 Terminals

Changes in Customer Behaviourmillion

0

50

100

200

300

150

250

95 9694 97

EFTPOS

Transactions

ATM

TELLER

Commonwealth ConnectCommonwealth Connect Insurance Limited is awholly owned subsidiary of the Bank offeringinsurance for house buildings and contents.Insurance risks are underwritten byCommonwealth Connect, with reinsurance treatiesarranged through external reinsurers.Commonwealth Connect complies with theGeneral Insurance Code of Practice and issupervised by the Insurance and SuperannuationCommission. Over 70% of new business isgenerated through the Bank’s branch/mobilelender network, with the Bank acting as agent forCommonwealth Connect.The remainder ofbusiness is written via Commonwealth Connect’s7 day per week telephone service.

Commonwealth Connect has more than330,000 building risks as well as 80,000 contentsrisks, with the number of contents policiesdoubling during 1996/97.

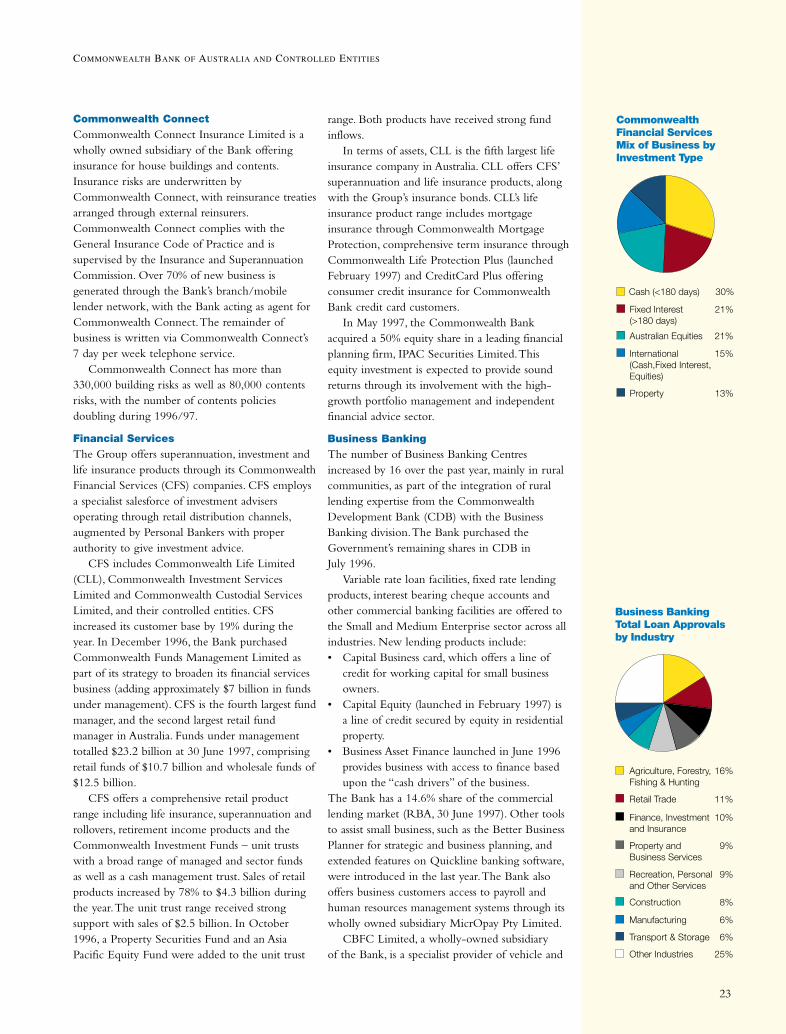

Financial ServicesThe Group offers superannuation, investment andlife insurance products through its CommonwealthFinancial Services (CFS) companies. CFS employsa specialist salesforce of investment advisersoperating through retail distribution channels,augmented by Personal Bankers with properauthority to give investment advice.

CFS includes Commonwealth Life Limited(CLL), Commonwealth Investment ServicesLimited and Commonwealth Custodial ServicesLimited, and their controlled entities. CFSincreased its customer base by 19% during theyear. In December 1996, the Bank purchasedCommonwealth Funds Management Limited aspart of its strategy to broaden its financial servicesbusiness (adding approximately $7 billion in fundsunder management). CFS is the fourth largest fundmanager, and the second largest retail fundmanager in Australia. Funds under managementtotalled $23.2 billion at 30 June 1997, comprisingretail funds of $10.7 billion and wholesale funds of$12.5 billion.

CFS offers a comprehensive retail productrange including life insurance, superannuation androllovers, retirement income products and theCommonwealth Investment Funds – unit trustswith a broad range of managed and sector fundsas well as a cash management trust. Sales of retailproducts increased by 78% to $4.3 billion duringthe year.The unit trust range received strongsupport with sales of $2.5 billion. In October1996, a Property Securities Fund and an AsiaPacific Equity Fund were added to the unit trust

range. Both products have received strong fundinflows.

In terms of assets, CLL is the fifth largest lifeinsurance company in Australia. CLL offers CFS’superannuation and life insurance products, alongwith the Group’s insurance bonds. CLL’s lifeinsurance product range includes mortgageinsurance through Commonwealth MortgageProtection, comprehensive term insurance throughCommonwealth Life Protection Plus (launchedFebruary 1997) and CreditCard Plus offeringconsumer credit insurance for CommonwealthBank credit card customers.

In May 1997, the Commonwealth Bankacquired a 50% equity share in a leading financialplanning firm, IPAC Securities Limited.Thisequity investment is expected to provide soundreturns through its involvement with the high-growth portfolio management and independentfinancial advice sector.

Business BankingThe number of Business Banking Centresincreased by 16 over the past year, mainly in ruralcommunities, as part of the integration of rurallending expertise from the CommonwealthDevelopment Bank (CDB) with the BusinessBanking division.The Bank purchased theGovernment’s remaining shares in CDB inJuly 1996.

Variable rate loan facilities, fixed rate lendingproducts, interest bearing cheque accounts andother commercial banking facilities are offered tothe Small and Medium Enterprise sector across allindustries. New lending products include:• Capital Business card, which offers a line of

credit for working capital for small businessowners.

• Capital Equity (launched in February 1997) isa line of credit secured by equity in residentialproperty.

• Business Asset Finance launched in June 1996provides business with access to finance basedupon the “cash drivers” of the business.

The Bank has a 14.6% share of the commerciallending market (RBA, 30 June 1997). Other toolsto assist small business, such as the Better BusinessPlanner for strategic and business planning, andextended features on Quickline banking software,were introduced in the last year.The Bank alsooffers business customers access to payroll andhuman resources management systems through itswholly owned subsidiary MicrOpay Pty Limited.

CBFC Limited, a wholly-owned subsidiaryof the Bank, is a specialist provider of vehicle and

COMMONWEALTH BANK OF AUSTRALIA AND CONTROLLED ENTITIES

Business BankingTotal Loan Approvalsby Industry

Agriculture, Forestry, 16%Fishing & Hunting

Construction 8%

Manufacturing 6%

Retail Trade 11%

Finance, Investment 10%and Insurance

Property and 9%Business Services

Recreation, Personal 9%and Other Services

Other Industries 25%

Transport & Storage 6%

Commonwealth Financial ServicesMix of Business byInvestment Type

Cash (<180 days) 30%

Fixed Interest 21%(>180 days)

Australian Equities 21%

International 15%(Cash,Fixed Interest, Equities)

Property 13%

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p23Ticket No.: 23707 Date: 1.9.97 GR Status: 3

23

equipment finance to the business sector. Hirepurchase, finance and operating leases, includingfleet leasing and management arrangements, arethe major product groups. CBFC is active as anissuer of secured debentures and unsecured notesto retail and wholesale investors to fund its assets.At 30 June 1997, CBFC had finance receivables ofmore than $4 billion, representing growth of 22%compared to June 1996. New business volumes,totalling $2.3 billion, were 34% ahead of last yearand profits are at record levels.The acquisitions ofthe external fleet management business of TNTFleet Management and the Leaseway fleetmanagement business added 17,000 motor vehiclesto the Bank’s fleet management division andconsolidated the Bank’s position as a leadingprovider of operating leases.

Institutional BankingThis division focuses on the top 1,000corporations in Australasia and selected offshoreclients, engaging in corporate lending, tradefinance, project finance, securities underwriting,payments and transaction services, and financialmarkets activities dealing in products such asforeign exchange, fixed income, futures andderivatives.

During the year ended 30 June 1997, non-interest income from institutional bankingactivities amounted to 56% of the division’s totalnet income.Total operating income increased by8% during the financial year.

Financial Market revenues grew by 15%compared to 1995/96. Implementation of anumber of risk management systems will help theBank improve its ability to service client needswith a range of risk management products.

Factors contributing to this result wereinvestment banking fees from large structuredfinancing transactions:• Hazelwood Power Station – through its

participation in the acquisition, in both a debtand equity capacity, the Bank demonstratedits capacity to structure significant transactions,manage financial markets strategy and thetrading of strategic equity investment ininfrastructure projects.

• Brisbane Airport – a consortium whichincluded Amsterdam Airport Schiphol,Commonwealth Financial Services, Portof Brisbane Corporation and the Brisbane CityCouncil. Commonwealth Bank acted in therole as arranger and underwriter, equityinvestor and derivative product provider.

Other fee generating deals include:• First Kangaroo bond to raise $150 million for

the Korea Development Bank in Australia; and• Development of a new product called ‘Flexible

Forwards’ which is designed to givecommercial clients the opportunity to useinnovative hedging solutions traditionallyaccessed only by the wholesale market.

Share Broking

Commonwealth Securities Limited is theBank’s wholly owned stockbroking subsidiarywhich commenced activities in July 1995.The Company’s primary business activity is theprovision of non-advisory stockbrokingservices, conducted under the business nameof Share Direct.

Share Direct is an easy-to-use service whichprovides convenient, low cost access to theAustralian stockmarket. Internet trading nowcomplements the Company’s existing telephonebased stockbroking service.

New Zealand Operations

ASB Bank is a 75% owned subsidiary ofCommonwealth Bank and is New Zealand’s oldestlocally established bank, and celebrated its 150thanniversary in June this year.The Bank isheadquartered in Auckland and as at 30 June 1997employed 2,400 people (on a full-time equivalentbasis).ASB Bank’s operations provide personal,business and rural banking services through anation-wide network of 123 branches, as well asselected corporate banking services.ASB Bank’sprimary business is personal banking whichrepresents over two-thirds of the Bank’s advancesand deposits.As at 30 June 1997,ASB Bank hadtotal assets of NZ$11.0 billion, an increase of morethan 20% over the previous year.ASB Bank’s netprofit after tax for the year ended 30 June 1997was NZ$92.5 million, an increase of 29% over ayear earlier.

24

Institutional Banking Index of Contribution to Other Income%

1995

/96

1994

/95

Trading Income

Other

Lending Fees

1996

/97

42

40

18 20 21

42

37

39

41

CBFC LimitedNew Business$million

0

100

300

200

500

400

600

700

DecQtr

MarQtr

SeptQtr

JunQtr

1994/95

1995/96

1996/97

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p24Ticket No.: 23707 Date: 9.9.97 GR Status: 4

COMMONWEALTH BANK OF AUSTRALIA AND CONTROLLED ENTITIES

Description of Businesscontinued

Client: Horniak & Canny Disk: H&C / AUG 97 Tape: 23707-1/CB089 p25Ticket No.: 23707 Date: 3.9.97 SW Status: 3

13 2221For your everyday bankingcall 13 2221 automated service from 7 am to 11 pm (EST) any day of theweek for account information includingcredit cards, funds transfers, and majorforeign exchange rates. From overseascall +61 13 2221.

13 2221 Telephone staffare available from 8 am to 8 pm,Monday to Friday, to set up a password,explain how to use the automatedservice and for all other enquiries. From overseas call +61 13 2221.

13 2224 To apply for a home loan or to openan account call 13 2224 between 8 am and 10 pm, any day of the week.

13 1998 Business Line For information on the full rangeof business banking solutions including:professional packages, franchising,rural finance, international trade finance,business asset finance, vehicle andequipment finance. Available 8 am to 8 pm, Monday to Friday.

1 800 811 446 CBFCEnquiries and quotes on leasingand hire purchase for vehiclesand equipment 8 am to 5 pm.

1 800 805 923 CBFCFleet leasing and management, andnovated leasing for motor vehicles 8 am to 5 pm (EST).

1 800 023 925 CBFC Enquiries, prospectus copies and interestrates for debenture and unsecureddeposit note investments 8 am to 5 pm (EST).

13 2015 CommonwealthFinancial ServicesFor general enquiries on retirement/superannuation products, life insuranceor managed investments 8 am to 8 pm,Monday to Friday (EST)

13 1519 Share Direct The low cost easy-to-use stockbrokingservice, available from 8 am to 8 pm,Monday to Friday (EST), or at anytime viathe Internet (www.comsec.com.au)

Commonwealth Bank Web SiteFor information on the Bank’s productsand services, current interest rates andforeign exchange rates, visitwww.commbank.com.au

The Bank’s Internet banking service,NetBank, allows access to a wide rangeof transactions on statement and creditcard accounts. More information atwww.commbank.com.au/netbank

13 2423 Commonwealth ConnectCustomer ServiceFor information, advice and quotes onhomeowner insurance, available 8 am to 8 pm, Monday to Friday (EST).

13 2420 Commonwealth ConnectClaims ServiceFor homeowner insurance claimsassistance, 24 hours a day, 7 daysa week.

Annual Report To request a copy of the annualreport visit the web site or call (02) 9378 3229.

Customer Service Points