78

Annual Report 2005

Annual Report 2005

Contents

Financial Summary 2001-2005 3 A Brief Presentation 4 Major Events 2005 5 Board of Directors’ Report 2005 7-11 Accounts Fred. Olsen Energy Group 13-45

Income Statement 13

Balance Sheet 14-15

Cash Flow 16

Notes 17-45 Accounts Fred. Olsen Energy ASA 46-63

Income Statement 46

Balance Sheet 47

Cash Flow 48

Notes 49-60

Auditor’s Report 61 Investor Information 62-65 Corporate Governance 66-67 Contract Overview 68-69 The Offshore Drilling Market 70-71 Management Report 72-75

Offshore drilling 72-74

Engineering and fabrication 75 Quality, Health, Safety and Environment 76 Addresses 78 . . .at a glance

Fred. Olsen Energy ASA - Annual Report 20052

2

Financial Summary 2001-2005

IFRS NGAAP

Income Statement Data All amounts in NOK mill 2005 2004 2003 2002 2001

Revenues 2 882.9 2 345.8 1 696.6 2 528.0 3 066.2

Operating profit before depreciation and other items (EBITDA) 920.7 566.4 389.8 581.3 1 050.5

Net result after tax (15.7) 419.8 (464.3) (969.5) 8.7

Assets

Current assets 1 700.2 1 257.6 937.2 991.7 1 800.0

Non-current assets 5 539.6 5 180.6 8 271.2 9 244.3 11 525.3

Net assets discontinued operations 51.9 203.5 383.2

Total assets 7 239.8 6 438.2 9 260.3 10 439.5 13 708.5

Liabilities and equity

Interest bearing debt 3 295.3 3 164.0 3 498.5 4 575.8 6 438.9

Total liabilities 4 289.2 4 196.4 4 281.4 5 141.2 7 155.4

Equity 2 950.6 2 241.8 4 978.9 5 298.3 6 472.7

Total liabilities and equity 7 239.8 6 438.2 9 260.2 10 439.5 13 708.5

Key Figures Definitions 2005 2004 2003 2002 2001

Market capitalization 1 14 864.1 5 276.3 1 718.6 572.9 2 653.2

Net interest bearing debt 2 2 578.2 2 565.3 3 139.5 4 027.8 5 196.6

Enterprise value 3 17 442.3 7 841.6 4 858.1 4 600.6 7 849.8

Debt/Book equity ratio 1.12 1.41 0.70 0.86 0.98

Debt/Market capital ratio 0.22 0.62 2.04 7.99 2.43

Current ratio 4 1.30 1.37 0.73 0.69 1.45

EBITDA margin 5 31.9 % 24.1 % 23.0% 23.0% 34.3%

Average number of shares outstanding 61.2 mill 57.4 mill 57.3 mill 57.5 mill 59.8 mill

Share price at year end 6 243.0 87.5 28.5 9.5 44.0

Basic earnings per share (EPS) 7 (0.3) 7.3 (8.1) (16.9) 0.1

Net investment per share (8.8) 2.0 9.4 (6.2) (6.3)

Price/Basic earnings 8 neg. 12.0 neg. neg. 302.4

Price/Book 9 5.0 2.4 0.3 0.1 0.4

EV/EBITDA 18.9 13.8 12.5 7.9 7.5

1 Closing price * number of shares at year-end

2 Short-term debt+Long-term debt-Cash and cash equivalents

3 Market capitalisation+Net interest bearing debt

4 Current assets/Current liabilities

5 EBITDA /Revenues

6 Last trade on last trading day of the year

7 Net profit/average number of shares outstanding

8 Closing price/Basic EPS

9 Closing price/Book value per share

Fred. Olsen Energy ASA - Annual Report 2005�

�

Fred. Olsen Energy – Group

A Brief Presentation

Fred. Olsen Energy ASA (The Company) is listed on the Oslo Stock Exchange and is a leading provider of exploration and production services to the oil and gas

industry. The Company is based on more than 150 years experience in shipping and over 35 years in offshore driling, and provides competitive solutions to the

benefit of our customers, employees and shareholders.

The Company is headquartered in Oslo with offices in Norway, the UK, Singapore, Bermuda, Mexico and US (agent).

Revenues 2005

3 000 NOK mill

2 400

1 800

1 200

600

0

Offices

Semisubmersibles

Deepwater Drillship

EBITDA 2005

1 000 NOK mill

800

600

400

200

0

Assets per 31.12.2005

8 000 NOK mill

6 400

4 800

3 200

1 600

0

Employees per 31.12.2005

1 000

800

600

400

200

0

2 756

127

880

40 104

837

95

7 143

Offshore drilling

Engineering and fabrication

March 05

Five months drilling contract with Peak Well Management Ltd. for Bredford Dolphin.

Five months drilling contract with Chevron Texaco North Sea Ltd. for Borgsten Dolphin.

Two months drilling contract with Total for Bredford Dolphin.

April 05

Six months accommodation contract with Shell U.K. Ltd. for Borgholm Dolphin.

June 05

Acquisition of Ocean Liberator, renamed Blackford Dolphin.

August 05

5 wells drilling contract, estimated to 210 days, with Equator for Bulford Dolphin.

September 05

Three years drilling contract with Anadarko Petroleum Corporation for Belford Dolphin.

Three months drilling contract with CNR for Borgsten Dolphin.

Three years drilling contract with Statoil for Borgsten Dolphin.

October 05

12 months drilling contract with Equator for Bulford Dolphin.

November 05

275 days drilling contract with CNR for Byford Dolphin.

720 days drilling contract with Tullow/Nexen for Borgsten Dolphin.

December 05

260 days accommodation contract with Shell/Talisman for Borgholm Dolphin.

3 wells drilling contract, estimated to 90 days, for Bredford Dolphin.

Events after 31.12.05

January 06

Three years drilling contract with Drilling Production Technology as for Bredford Dolphin.

March 06

Secured contract with Keppel FELS for upgrading of Blackford Dolphin.

Two months drilling contract with Peak Well Management Ltd. for Bredford Dolphin.

Three years drilling contract with Reliance Industries Ltd. for Blackford Dolphin.

Early redemption of NOK 760 million bonds 2004/09

Established new credit facility of USD 600 million.

Major Events in 2005

�

�

Fred. Olsen Energy ASA - Annual Report 2005

Fred. Olsen Energy ASA - Annual Report 2005�

�

�

�Fred. Olsen Energy ASA - Annual Report 2005

�

Board of Directors’ Report 2005

The operating activities of Fred. Olsen Energy

ASA and its subsidiaries (“The Group”) consist

of offshore drilling as well as engineering and

fabrication services. The Group has its corporate

headquarters located in Oslo, Norway. The par-

ent company of the Group is Fred. Olsen Energy

ASA (“The Company”). The Group manages its

activities from offices in Norway, the UK, Singa-

pore, Bermuda and Mexico and has a branch

office in India. Engineering and fabrication serv-

ices consist of activities related to the Harland &

Wolff (H&W) shipyard located in Belfast, North-

ern Ireland.

Gross revenues in 2005 were NOK 2 883 million,

an increase of NOK 540 million from the previ-

ous year. The Group achieved earnings before

interest, taxes, depreciation and amortization

(EBITDA) and other items of NOK 921 million

compared to an EBITDA before other items of

NOK 568 million in 2004.

Net interest bearing debt at 31.12.2005 for the

Group was NOK 2 578 million.

Markets and prospects

The market for offshore services continues

to be strong. Globally, the balance between

supply and demand for offshore drilling units

tightened in all segments. This development

has been reflected in significant increases in

day rates. The high demand for offshore drilling

services is expected to continue during the next

few years as a result of renewed focus on reserve

replacement supported by high demand for oil

and gas and expectations of continued high

energy prices.

During 2005 a number of contracts for construc-

tion of new floating drilling units have been

signed. Several of these new builds have been

Oil Price

70 USD/Barrel

60

50

40

30

01.01.2004 31.03.200630

40

50

60

70

contracted on speculative basis, i.e. there are no

drilling contracts in place before construction

commences. During 2006-2008 the new units

will actively seek drilling contracts to secure cash

flow, which is expected to cause an impact on

the day rates.

The deepwater upgrade of Blackford Dolphin will

make a profitable addition to the Group’s fleet of

drilling units. When the upgrade has been com-

pleted mid 2007, the offshore fleet will consist

of two deepwater units and six mid water semi

submersible drilling rigs in addition to an ac-

commodation unit. Two of the semi submersible

units are considerably upgraded and qualified for

operations in Norway. By late 2006 the Group will

have three units operating in Norwegian waters.

Geographically, the Group currently operates in

Norway, the UK, India, Mexico and West Africa.

From 2007 the deepwater region of the US Gulf

will also be an area of operation.

The Group will continuously explore investment

opportunities to enhance shareholders’ value.

To the extent economically viable investment

projects are not found and to the extent per-

mitted by the financial situation of the Group,

dividend payments as well as share buy back

programmes will be considered.

At year-end, all of the Group’s operated units,

except Blackford Dolphin, which is being up-

graded, were on contract. During the last 15

months, the Group has secured new contracts

with a total value of approximately USD 2 200

million. At the beginning of 2006, the average

contract length of the Group’s offshore fleet was

approximately 27 months. Three units are avail-

able for new contracts in 2007, comprising Bid-

eford Dolphin, Bulford Dolphin and Borgholm

Dolphin.

Offshore Drilling

The drilling activities generated revenues of NOK

2 756 million compared to NOK 2 130 million in

2004. Within this segment, the Group achieved

an EBITDA before other items of NOK 880 mil-

lion. In 2004, the corresponding profit was NOK

576 million.

Borgland Dolphin continued operations off-

shore Norway under the current contract with

Statoil, expiring at the end of December 2006. In

September 2005 a new contract for the rig was

entered into with Statoil ASA for operations in

the Tampen area on the Norwegian continental

shelf. The contract period is for three years expir-

ing at the end of 2009.

Bideford Dolphin continued operations offshore

Norway under a contract with Norsk Hydro esti-

mated to expire in mid 2007.

The deepwater drill ship Belford Dolphin con-

tinued operations under a three-year drilling

contract with ONGC in India, expiring in early

2007. In September 2005 a contract was entered

into with Anadarko Petroleum Corporation for

three years. The new contract will follow in direct

continuation from the present Belford Dolphin

contract with ONGC.

Borgny Dolphin continued operations under a

contract with Pemex in Mexico, expiring early

2008.

Bulford Dolphin (owned by First Olsen Lim-

ited and being operated in pool with four of

the Group’s own units) commenced a drilling

programme for Equator Exploration Ltd. offshore

West Africa in November 2005. The contract is

estimated to expire in September 2007.

Fred. Olsen Energy ASA - Annual Report 2005�

�

Fred. Olsen Energy ASA - Annual Report 2005

Board of Directors’ Report 2005

USD Interest Rate, 3 Month Libor

5 %

4

3

2

1

02.01.2004 04.04.20061

2

3

4

5

Bredford Dolphin completed a drilling program

offshore Spain for Escal and British Gas, respec-

tively, in March 2005. Subsequently, several short-

term contracts have been entered into for drilling

programs in the UK with an estimated duration to

3rd quarter 2006. In January 2006 a drilling con-

tract for the rig was entered into with Drilling Pro-

duction Technology as, on behalf of themselves

and a consortium of licensees on the Norwegian

continental shelf. The duration of the contract is

three years with estimated commencement in

second half 2006 following a compulsory class

renewal survey and upgrade for Norwegian re-

quirements. Following completion of the drilling

programs in the UK, the rig will move to Belfast

where preparation work will be carried out for the

following 3 year drilling contract in Norway.

A drilling program for Byford Dolphin com-

menced in February 2005 under a contract with

CNR International (U.K.) Limited after a compul-

sory five-year class renewal survey at the H&W

yard. CNR has exercised their options and the

contract is now estimated to expire in 2nd quar-

ter 2007. An agreement with CNR was entered

into in November 2005 on a further extension of

the contract for 275 days in direct continuation

from the present contract.

Borgsten Dolphin secured a contract with Chev-

ronTexaco North Sea Ltd. in March for a drilling

program in the UK North Sea, which com-

menced after completion of the compulsory

five-year class renewal survey at the H&W yard.

In September a new contract for the rig was

secured with CNR International (U.K) Ltd for an

approximate three months drilling programme

in the UK commencing in March 2006. In De-

cember 2005 contracts were entered into with

Nexen Petroleum UK Ltd. and Tullow Oil plc, re-

spectively, for drilling operations in the UK North

Sea. The drilling programmes have an estimated

duration of 720 days of combined activity from

approximately May 2006 in direct continuation

from the unit’s existing contract commitments.

Borgholm Dolphin continued operations under

a contract with Shell U.K. Ltd. for accommoda-

tion support in the UK sector of the North Sea

from July 2005 until January 2006. Further con-

tracts for accommodation support in the UK

were entered into with Talisman Energy (UK)

Ltd. and Shell U.K Ltd commencing in February

2006 following a short standby period. The con-

tracts will result in combined activity to the end

of October 2006 with options for a further two

months extension thereafter.

In June 2005, the Group acquired the semi-sub-

mersible drilling rig Ocean Liberator from Ense-

nada Internacional S.A., a subsidiary of Diamond

Offshore Drilling Inc., for a consideration of USD

14 mill. The unit has been renamed Blackford

Dolphin.

The Blackford Dolphin is an Aker H-3 design built

in 1974 and had been cold stacked in Saldanha

Bay north of Cape Town since November 2002.

The rig is being upgraded to a deepwater drill-

ing unit for 7000 ft. of water with a new high

capacity drilling package and an innovative

deck layout. Keppel FELS and Keppel Shipyard

in Singapore and Keppel Verolme in Rotterdam,

the Netherlands, will undertake the yard work

jointly. Delivery from the yard in Rotterdam is

mid 2007. Contracts for construction of the ac-

commodation- and power modules have been

awarded to the H&W yard. The cost for the up-

grade is estimated at USD 400 million. In March

2006 a letter of award was received for a three

years drilling contract for the rig commencing

after completion of the deepwater upgrade.

Engineering and Fabrication

Following the sale of property interests in Titanic

Properties and Titanic Quarter as well as T.I. Solu-

tions in 2004, the division consists of activities

related to the H&W shipyard located in Belfast.

Total revenues within the engineering and fab-

rication division amounted to NOK 207 million

and EBITDA was NOK 51 million. In 2004, the cor-

responding figures were total revenues of NOK

269 million and a loss before other items of NOK

8 million. Most of the improvement in EBITDA

was due to reduced costs relating to positive

changes in the valuation of the H&W pension

scheme’s assets and changes in the actuarial

assumptions used in estimating the scheme’s

liabilities. One of the changes in the actuarial as-

sumptions arose as a result of a settlement offer

with cash payments to the deferred pensioners.

The H&W yard continued its operations in en-

gineering, ship repair and shipbuilding. A large

project during the last part of the year has been

utilisation of the yard as logistics and assembly

base for Barrow Windfarm Project. During the

year the yard has carried out work related to the

class renewal surveys for several of the Group’s

drilling rigs. The core workforce was stable at 95

employees.

Financial result and balance sheet at year end

Consolidated revenues of NOK 2 883 million

represent an increase of 23% compared to 2004,

primarily reflecting increased revenues from off-

shore drilling services.

EBITDA before other items for the Group were

NOK 921 million, an increase of NOK 352 million

or 62% compared to 2004. After depreciation

and amortization of NOK 618 million and other

Fred. Olsen Energy ASA - Annual Report 2005 �

�

Fred. Olsen Energy ASA - Annual Report 2005

Board of Directors’ Report 2005

items of NOK 34 million, the operating profit was

NOK 269 million, compared with an operating

profit of NOK 77 million the previous year.

Net financial expense was NOK 281 million. The

corresponding items in 2004 resulted in a profit

of NOK 36 million. Net loss before taxes was NOK

12 million compared to a profit of NOK 113 mil-

lion in 2004 for continuing operations. The net

result for the year was a loss of NOK 16 million

against a profit of NOK 420 million in 2004.

At year-end, the Group had consolidated assets

of NOK 7 240 million. The ratio of net interest

bearing debt to total assets was 36 % compared

to 40 % at the beginning of the year. Book value

of the equity was NOK 2 951 million. Cash flow

generated from continuing operations was NOK

369 million against NOK 85 million in 2004. Cash

and cash equivalents increased by NOK 118 mil-

lion during the year, from NOK 599 million to

NOK 717 million at the end of the year.

Fred. Olsen Energy ASA provides holding com-

pany and management services for the subsidi-

ary companies within the Group. The Company

had NOK 1 million in revenues – the same as in

2004. EBITDA for the year was a loss of NOK 40

million compared with NOK 37 million in 2004.

Net loss was NOK 32 million compared to a loss

of NOK 106 million in 2004.

The annual accounts of the parent company

and the consolidated accounts are based on

the assumption of continued operation.

International Financial Reporting

Standards (IFRS)

The consolidated financial statements have

been prepared in accordance with the Norwe-

gian Accounting Act and International Financial

Reporting Standards (IFRS) as adopted by EU and

interpretations adopted by the International Ac-

counting Standards Board (IASB). These are the

Group’s first consolidated financial statements in

accordance with IFRS and IFRS 1: First-time Adop-

tion of International Financial Reporting Standards

has been applied. An explanation of how the

transition to IFRS has affected the reported fi-

nancial position, financial performance and cash

flows of the Group, is provided in note 27.

Investment and capital resources

Capital expenditures amounted to NOK 519 mil-

lion in the year compared to NOK 355 million

in 2004. The capital expenditures were mainly

related to the upgrade of Blackford Dolphin,

including the purchase of the rig and engineer-

ing work and the class renewal surveys of Byford

Dolphin, Borgsten Dolphin and Belford Dolphin,

respectively.

The Group’s debt consists of several loans. The

largest is a USD 300 million credit facility, which

was established in 2004 with final maturity in

2008. The outstanding amount under the credit

facility at year-end was USD 273 million. In

addition, a short-term credit facility of USD 30

million was established in 2005 with matu-

rity in March 2006. Further, the Company has

outstanding unsecured senior debt notes

totalling NOK 869 million, of which NOK 109

million are due in 2006 and NOK 760 million

in 2009. In addition, the Company has issued

NOK 435 million in subordinated convertible

bonds, due in 2009. The holders of the convert-

ible bonds have the right to convert bonds into

shares in the Company at a conversion price

of NOK 68 per share. Following conversion of

bonds into shares in Fred. Olsen Energy ASA

during 2005, the outstanding amount under

the convertible bond loan at year-end was NOK

373 million. The loan agreements contain opera-

tional and financial covenants typical for credit

arrangements of this nature.

In March 2006 the USD 300 million credit facility

will be replaced by a new 7 years credit facility

of USD 600 million. The new credit facility will

also refinance the NOK 760 million senior debt

notes mentioned above, following the exercise

of an early redemption option, and the short-

term credit facility of USD 30 million.

As per 22 March 2006, the Group is in com-

pliance with all covenants in the loan agree-

ments.

Financial risks

The Group is exposed to certain financial risks

related to its activities. These are mainly foreign

exchange risks, interest rate risks and credit risks.

The Group continually monitors its financial risks

and applies from time to time financial deriva-

tives to hedge its exposure.

Foreign exchange

The Group’s financial statements are denomi-

nated in NOK. The Group’s revenues consist pri-

marily of NOK and USD with USD as the most

dominant currency. The Group’s expenses are

primarily in NOK, GBP and USD. As such, the

Group’s earnings are exposed to fluctuations in

the currency market. The Group’s future foreign

exchange exposure is dependent upon the

currency denomination of revenues, however,

in the longer term, a substantial portion of the

USD/NOK exposure is neutralised through the

majority of the Group’s debt being denominated

in USD.

USD/NOK

7.2

7.0

6.8

6.6

6.4

6.2

6.0

02.01.2004 31.03.20066,0

6,2

6,4

6,6

6,8

7,0

7,2

Fred. Olsen Energy ASA - Annual Report 200510

10

Fred. Olsen Energy ASA - Annual Report 2005

Board of Directors’ Report 2005

Deepwater Units Supply > 3000 feet by area (31.03.2006)

30 Source: Fearnley

25

20

15

10

5

0

Gulf of Mexico South America West Africa North Sea Southeast Asia Indian subcontinent Mediterranean

30

20

17

6 5 4 3

Interest rate

The Group is exposed to fluctuations in interest

rates for USD and NOK. At 31 December 2005

more than 50% of the Group’s interest expense

was based on fixed interest rate through finan-

cial derivatives and fixed rate loans. The remain-

ing portion of the debt was based on floating in-

terest rates (USD LIBOR or NIBOR) plus a margin.

Credit risk

Due to the nature of the Group’s operations,

revenues and related receivables are typically

concentrated amongst a relatively small cus-

tomer base of major international oil and gas

companies. The Group continually evaluates

the credit risk associated with customers and,

when considered necessary, requires certain

guarantees. As such, the credit risk is considered

to be low.

Corporate Governance

The Company emphasizes the importance of

maintaining and further developing its corpo-

rate governance policy and supports the princi-

ples set out in the Norwegian Code of Practice

for Corporate Governance. The Company has

implemented written guidelines to the Board of

Directors as a practical tool for the Board in its

exercise of good corporate governance.

All shares in the Company have equal rights

and all shareholders have the right to attend

the shareholders’ meeting. The Company has

no restrictions on ownership or voting.

The Board of Directors has an authorization from

the Annual General Meeting in 2005 to increase

the share capital by 30 000 000 shares. The proxy

expires on 19 May 2006.

The Company provides information to the

market through quarterly and annual reports,

investor- and analyst presentations open to the

media and by making operational and financial

information available on the company’s website.

Events of importance are made available to the

stock market through notification to the Oslo

Stock Exchange in accordance with the Stock

Exchange regulations. Information is provided

in Norwegian and English.

The Board of Directors consists of 5 board mem-

bers who are elected for a two-year period. All of

the Directors are independent of the Company’s

management and two of them are independ-

ent also in relation to the Company’s main share-

holders, Ganger Rolf ASA and Bonheur ASA. The

Board of Directors had 13 meetings during the

year. Each Director is remunerated by an annual

fee.

The current composition of Directors reflects ad-

equate competence relative to the main busi-

ness areas of the Group.

The Board of Directors has appointed an Au-

dit Committee consisting of the two Directors

independent of the main shareholders of the

Company. The charter of the audit committee

is to assist the Board in fulfilling its responsibili-

ties concerning the financial reporting process,

internal controls, management of financial risks,

the audit process, and the Group’s process for

monitoring compliance with applicable laws

and regulations.

The Board of Directors has appointed a Com-

pensation Committee comprising three Direc-

tors, including the two independent Directors.

The Compensation Committee discusses and

recommends to the Board salary and benefits for

the Chief Executive Officer as well as the man-

agement incentive schemes for the Group.

The compensation to the Chief Executive Officer

comprises salary, pension scheme, company car,

stock options and performance bonus pay.

In past years, the Company has retained all earn-

ings to support and develop operations, and has

therefore not paid dividends. Going forward,

dividend payments will be considered to the

extent economically viable investment projects

are not found and to the extent permitted by

the financial situation of the Group.

Share Capital Issues

The Annual General Meeting in May 2005 au-

thorized the Board of Directors to issue up to

30 000 000 new shares in the Company for a pe-

riod of up to one year in order to strengthen its

business within the offshore segment. An increase

in the share capital may be brought about either

by issuing new shares or by raising loans with

rights to subscribe for new shares. As of 22 March

2006 the authorization had not been used.

At 1.1.2005, the Company owned 2 901 394 of

its own shares, representing 4.8 % of the share

capital. In February 2005, the Company sold

2 623 227 of those shares.

At 31.12.2005 the Company’s share capital

amounted to NOK 1 224 million, corresponding to

61 205 950 shares at par value NOK 20, - each. At

year-end the Company owned 84 336 own shares.

Safety, work environment, organization

and equal opportunities

The Group has a strong focus on safe working

environments for its employees and its custom-

Fred. Olsen Energy ASA - Annual Report 2005 11

11

Fred. Olsen Energy ASA - Annual Report 2005

Board of Directors’ Report 2005

Oslo, 31 December 2005 / 22 March 2006

Fred. Olsen Energy ASA

Anette S. Olsen John C. Wallace Ivar J. Saunes Mårten Lunde Øivin Fjeldstad Helge Haakonsen

Chairman Chief Executive Officer

ers. Continuous efforts involve planning, training

of personnel and careful selection of subcon-

tractors. The Group maintains a “zero accident”

objective and is closely monitoring its estab-

lished procedures for operations, projects and

worksites both onshore and offshore.

The lost time accident frequency (LTA) for off-

shore drilling and related services in 2005 was

1.8 per million working hours. In 2004 LTA was 5,

of which 4 were minor injuries.

In order to maintain and continuously improve

the working environment the Group in 2005

performed several activities related to HSE train-

ing, HSE trend analyses and established HSE

goals with corresponding improvement action

plans.

In 2005 further measures have been taken in order

to prevent spills to the external environment. The

international environmental standard ISO 14001

has been implemented whereas environmental

goals, aspects, update of management systems

and technical actions are key measures.

It is the Group’s policy to conduct business in

accordance with the letter and spirit of the law

and with the overriding ethical standards of ac-

cepted business conduct. The working environ-

ment both offshore and onshore is considered

to be good. Absence due to illness was 3.71 %

and 1.70 % for the group and the parent com-

pany, respectively. The Group continues to focus

on reducing absence due to illness.

The Group aims to be a workplace with equal

opportunities, offering challenging and motivat-

ing jobs to all personnel, regardless of national-

ity, culture, religion and gender. The division of

genders within the Group reflects the available

recruitment base for offshore work, which tradi-

tionally is dominated by men, being the nature

of the offshore industry worldwide. However,

the Group’s policy is to offer equal opportuni-

ties for males and females and in connection

with new employments efforts are made to at-

tract females for technical positions. Assuming

all other qualifications equal, the Group gives

priority to the underrepresented gender within

each job category.

One out of five Board Directors is a female, be-

ing the Chairman of the Board. At year-end 2005

the Group had 932 employees, including 10 in

the parent company. 75 of the employees were

women. Ten percent of leading personnel within

the Group are female.

Legal matters

In December 2005 the final tranche of the Navis

ASA share purchase in 2000-2001 was settled by

a final assessment of Borgarting lagmannsrett

(a Norwegian Court of Appeals) in the dispute

between the Company and an assignee to the

position of a previous minority shareholder in

Navis ASA who did not accept the offer related

to the compulsory redemption made in Febru-

ary 2001. The minority shareholder claimed dur-

ing the hearings that approximately NOK 21,-

per share would be a fair price, whilst Borgarting

lagmannsrett arrived at a redemption price of

NOK 14.50 per share. The minority shareholder

represented 8 848 140 shares, corresponding to

6.6% of the total shares in Navis ASA.

After having commenced proceedings in the

redemption case the previous minority share-

holder in 2003 commenced separate proceed-

ings against the Company seeking damages on

the basis of the Company’s mandatory bid for

Navis shares in November 2000. In December

2005 the Oslo tingrett (a Norwegian City Court)

ruled against these claims following which the

plaintiff in January 2006 appealed the ruling. See

Note 22 for further information.

External Environment

The Group’s operations may involve activities

that entail potential risks to the external environ-

ment. The discharge produced from processes

and operations in the offshore oil-and gas-drill-

ing industry, directly and indirectly through

chemical interaction can upset the balance

of our environment. The Group is careful in its

approach to the environment and continually

strives to reduce the use of hazardous chemi-

cals and materials to minimize negative effects

and continually seeks alternative products to

safeguard the environment.

Allocation of profit

The Board does not propose a dividend for 2005.

The net loss of the parent company of NOK

32 million has been covered by other equity. The

parent company’s unrestricted equity was NOK

3 175 million at year-end.

Annual General Meeting

The date of the Annual General Meeting is 29

May 2006.

Events after year-end

Operational events after year-end are included

above. For further information see note 28.

Fred. Olsen Energy ASA - Annual Report 200512

12

1�Fred. Olsen Energy ASA - Annual Report 2005

1�

Consolidated Income Statement

For the years ended 31 December 2005 2004

Continuing Continuing Discontinued

Amounts in NOK 000’s Note operations operations operations Total

Revenues 2,3,20,24 2 882 880 2 342 834 2 950 2 345 784

Materials (53 564) (129 624) 0 (129 624)

Salaries and other personnel costs 3,4 (749 848) (635 929) (1 321) (637 250)

Other operating expenses 3,5,20 (1 158 812) (1 009 230) (3 246) (1 012 476)

Operating profit before depreciation, amortisation, other

items and financing costs 920 656 568 051 (1 617) 566 434

Navis Settlement 6 (33 683) 0 0 0

Reversal of restructuring charge 6 0 20 771 0 20 771

Depreciation and amortisation 3,9,10 (618 265) (511 416) (111) (511 527)

Operating profit before financing costs 268 708 77 406 (1 728) 75 678

Financial income 118 311 414 002 0 414 002

Financial expense (398 878) (378 026) 37 (377 989)

Net financing costs 3,7,11 (280 567) 35 976 37 36 013

Profit/(loss) before tax and gain on discontinued operation (11 859) 113 382 (1 691) 111 691

Income tax expense 8 (3 820) (47 376) 0 (47 376)

Profit/(loss) after tax before gain on discontinued operation (15 679) 66 006 (1 691) 64 315

Gain on sale of discontinued operation 3 0 0 355 500 355 500

Profit/(loss) for the period (15 679) 66 006 353 809 419 815

Attributable to:

Equity holder of the parent (15 679) 66 006 353 809 419 815

Profit/(loss) for the period 14 (15 679) 66 006 353 809 419 815

Basic earnings per share 26 (0.26) 1.15 6.17 7.32

Diluted earnings per share 26 (0.26) 1.15 6.15 7.30

Consolidated statement of recognised income and expense

For the years ended 31 December

Amounts in NOK 000’s Note 2005 2004

Exchange differences on translation of foreign operations 395 385 (234 405)

Net income/(expense) recognised directly in equity 395 385 (234 405)

Profit/(loss) for the period (15 679) 419 815

Total recognised income and expense for the period 379 706 185 410

Attributable to:

Equity holders of the parent 379 706 185 410

Total recognised income and expense for the period 14 379 706 185 410

The notes represent an integral part of the financial statements.

Fred. Olsen Energy – Group

Fred. Olsen Energy ASA - Annual Report 200514

14

Fred. Olsen Energy ASA - Annual Report 2005

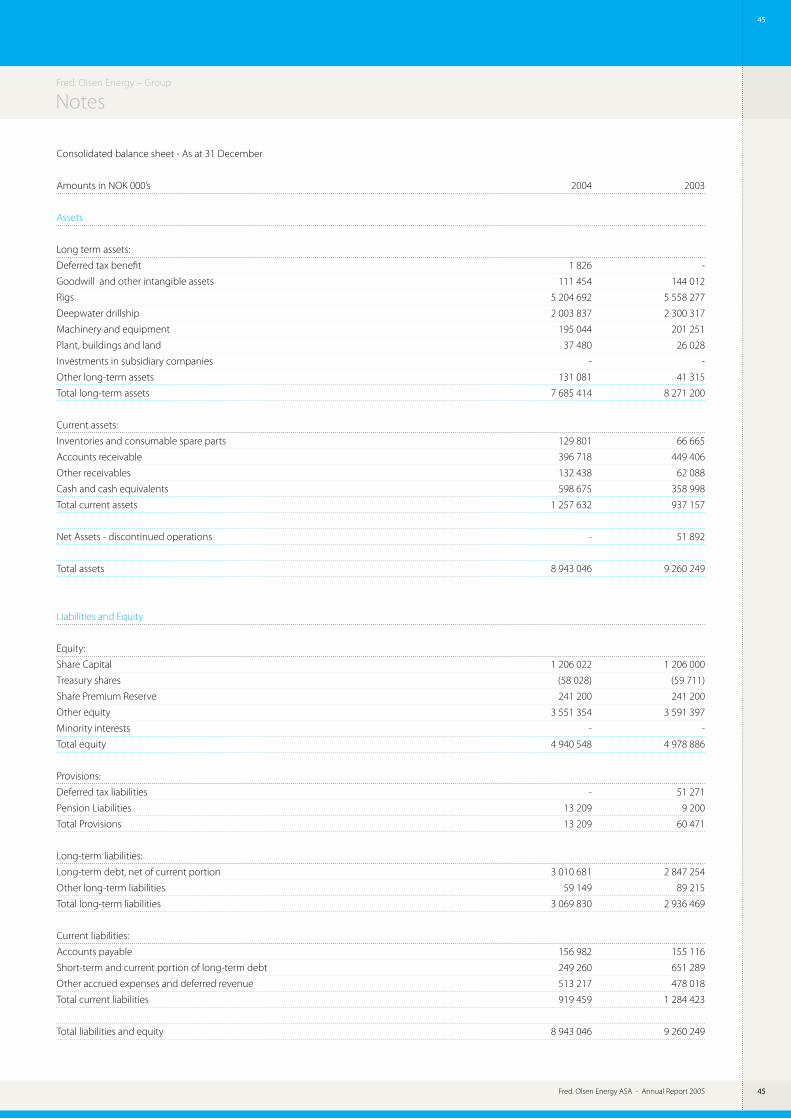

Consolidated Balance Sheet

As at 31 December

Amounts in NOK 000’s Note 2005 2004

Assets

Property, plant and equipment 9,16 5 391 018 4 930 495

Intangible assets 10 98 577 119 600

Other investments 17,20 8 084 973

Financial instruments 11 38 692 127 717

Deferred taxes 12 3 211 1 838

Total non-current assets 5 539 582 5 180 623

Inventories and consumable spare parts 9 177 174 129 801

Financial instruments 11 0 7 657

Trade and other receivables 20 805 946 521 499

Cash and cash equivalents 13 717 110 598 675

Total current assets 1 700 230 1 257 632

Total assets 7 239 812 6 438 255

The notes represent an integral part of the financial statements.

Fred. Olsen Energy – Group

Fred. Olsen Energy ASA - Annual Report 2005 1�

1�

Fred. Olsen Energy ASA - Annual Report 2005

Consolidated Balance Sheet

As at 31 December

Amounts in NOK 000’s Note 2005 2004

Equity

Issued capital 1 224 119 1 206 022

Share premium 284 687 241 253

Capital reserves 187 171 45 475

Translation reserves 160 992 (234 393)

Treasury shares (1 687) (58 028)

Retained earnings 1 095 306 1 041 476

Total equity 14 2 950 588 2 241 805

Liabilities

Interest-bearing loans and borrowings 15,16 2 687 401 2 914 710

Employee benefits 17 268 293 303 132

Deferred taxes 12 1 683 0

Financial instruments 11 19 579 59 149

Total non-current liabilities 2 976 956 3 276 991

Interest-bearing loans and borrowings 15,16 607 909 249 260

Trade and other payables 20 198 579 156 982

Provisions 18 172 439 136 929

Financial instruments 11 2 589 0

Other accrued expenses and deferred revenue 330 753 376 288

Total current liabilities 1 312 268 919 459

Total liabilities 4 289 224 4 196 450

Total equity and liabilities 7 239 812 6 438 255

The notes represent an integral part of the financial statements.

Fred. Olsen Energy – Group

Oslo, 31 December 2005 / 22 March 2006

Fred. Olsen Energy ASA

Anette S. Olsen John C. Wallace Ivar J. Saunes Mårten Lunde Øivin Fjeldstad Helge Haakonsen

Chairman Chief Executive Officer

Fred. Olsen Energy ASA - Annual Report 20051�

1�

Fred. Olsen Energy ASA - Annual Report 2005

For the year ended 31 December

Amounts in NOK 000’s Note 2005 2004

Cash flows from operating activities

Profit/(loss) before income tax (11 859) 113 382

Adjustment for:

Depreciation and amortisation 9 618 265 511 416

Interest expense 7 201 277 202 397

(Gain)/Loss on sale of property, plant and equipment 0 (247)

Unrealised currency (gains)/losses 0 (242 744)

Changes in trade and other receivables (268 296) 34 995

Changes in trade and other payables (2 949) 12 506

Changes in other balance sheet items 13 634 (415 109)

Cash generated from operations 550 072 216 596

Interest paid (178 165) (127 812)

Income taxes paid (2 579) (3 968)

Net cash from operating activities 369 328 84 816

Cash flows from investing activities

Purchases of property, plant and equipment (535 390) (277 149)

Proceeds from sale of equipment 0 4 388

Proceeds from sale of discontinued operation 0 386 780

Net cash (used)/from investing activities (535 390) 114 019

Cash flows from financing activities

Proceeds from interest bearing loans 196 239 2 805 400

Proceeds from the issue of convertible notes 0 435 000

Repayments of interest bearing loans (254 942) (3 214 073)

Sale of treasury shares 273 542 3 054

Net cash from financing activities 214 839 29 381

Net cash flow discontinued operations 0 (4 370)

Net increase in cash and cash equivalents 48 777 228 216

Cash and cash equivalents at 1 January 598 675 358 998

Effect of exchange rate fluctuations on cash held 69 658 11 461

Cash and cash equivalents at 31 December 717 110 598 675

The notes represent an integral part of the financial statements.

Fred. Olsen Energy – Group

Consolidated Statement of Cash Flows under indirect method

Fred. Olsen Energy ASA - Annual Report 2005 1�

1�

Fred. Olsen Energy ASA - Annual Report 2005

Notes to the Consolidated Financial StatementsFred. Olsen Energy – Group

Note 1 – Significant accounting policies

Fred. Olsen Energy ASA (the “Company”) is a

company domiciled in Norway.

The consolidated financial statements of the

Company for the year ended 31 December

2005 comprise the Company and its subsidiar-

ies (together referred to as the “Group”).

The financial statements were authorised for is-

sue by the directors on 22 March 2006.

Statement of compliance

The consolidated financial statements have

been prepared in accordance with the Nor-

wegian Accounting Act, International Financial

Reporting Standards (IFRS) and interpretations

adopted by the International Accounting Stand-

ards Board (IASB) and the European Union. These

are the Group’s first consolidated financial state-

ments in accordance with IFRS and IFRS 1: First-

time Adoption of International Financial Report-

ing Standards has been applied.

An explanation of how the transition to IFRSs

has affected the reported financial position,

financial performance and cash flows of the

Group is provided in note 27.

Basis of preparation

The financial statements are presented in Nor-

wegian Kroner (NOK), rounded to the nearest

thousand. They are prepared on the historical

cost basis except that derivative financial instru-

ments and financial instruments held for trading

are stated at their fair value and the rig values

have been measured at the fair value (Broker

Assessments) at the date of transition and used

as the deemed cost.

The preparation of financial statements in con-

formity with IFRS requires management to make

judgements, estimates and assumptions that

affect the application of policies and reported

amounts of assets and liabilities, income and

expenses. The estimates and associated as-

sumptions are based on historical experience

and various other factors that are believed to be

reasonable under the circumstances. The esti-

mates and underlying assumptions are reviewed

regularly. Actual results may differ from these

estimates.

Judgements made by management in the appli-

cation of IFRSs that have significant effect on the

financial statements and estimates with a signifi-

cant risk of material adjustment in the next year

are discussed below.

The accounting policies set out below have been

applied consistently to all periods presented in

these consolidated financial statements and in

preparing an opening IFRS balance sheet at 1

January 2004 for the purposes of the transition

to IFRSs. See note 27 for discussion of the transi-

tion to IFRS.

The accounting policies have been applied con-

sistently by Group entities.

Basis of consolidation

Subsidiaries

Subsidiaries are entities controlled by the Com-

pany. Control exists when the Company has the

power, directly or indirectly, to govern the finan-

cial and operating policies of an entity so as to

obtain benefits from its activities.

Transactions eliminated in consolidation

All material intercompany transactions, any

unrealised gains and losses and intragroup bal-

ances have been eliminated in preparing the

consolidated financial statements.

Minority Interest

Minority interests in the net assets of consoli-

dated subsidiaries are identified separately from

the Group’s equity therein. Minority interests

consist of those interests at the date of the

original transaction and the minority’s share of

changes in equity since that date. Losses appli-

cable to the minority in excess of the minority’s

interest in the subsidiary’s equity are allocated

against the interests of the Group as there is no

obligation to make an additional investment to

cover the losses.

Foreign currency

Foreign currency transactions

The individual financial statements of each

Group entity are presented in the currency of

the primary economic environment in which

the entity operates (its functional currency).

For the purpose of the consolidated financial

statements, the results and financial position

of each entity are presented in NOK, which is

the functional currency of the Company, and

the presentation currency of the consolidated

financial statements. During 2005, certain of the

Company’s subsidiaries changed their functional

currencies due a re-evaluation of the underlying

economic environments in which the subsidiar-

ies operate. As a result, the functional currencies

changed from NOK to USD for Dolphin Interna-

tional AS and Fred. Olsen Drilling AS (now merged

into Dolphin International AS) and for Dolphin

Drilling Ltd and Perforadora Dolphin Mexicana

from GBP to USD as from 1 January 2005.

In preparing the financial statements of the in-

dividual entities, transactions in foreign curren-

cies are translated at the foreign exchange rate

at the date of the transaction. Monetary assets

and liabilities denominated in foreign curren-

cies are translated to the functional currency at

the foreign exchange rate at the balance sheet

date. Foreign exchange differences arising on

translation are recognised in the income state-

ment. Non-monetary assets that are measured

in terms of historical cost in a foreign currency

are translated using the exchange rate at the

date of the transactions. Non-monetary assets

and liabilities denominated in foreign currencies

that are stated at fair value are translated using

the exchange rates ruling at the dates the fair

value was determined.

Financial statements of foreign operations

The assets and liabilities of foreign subsidiaries

are translated into NOK at the foreign exchange

rate at the balance sheet date. The revenues

and expenses of foreign subsidiaries are trans-

lated using average monthly foreign exchange

rate, which approximates the foreign exchange

rates on the dates of the transactions. Foreign

exchange differences arising on translation are

recognised directly as a separate component of

equity.

Financial Instruments

Financial assets and financial liabilities are rec-

ognized on the Group’s balance sheet when the

Group becomes a party to the contractual provi-

sions of the instruments.

Derivative financial instruments

The Group uses derivative financial instruments

to manage its exposure to foreign exchange

and interest rate risks arising from operational,

financing and investment activities. In accord-

ance with its treasury policy, the Group does not

hold or issue derivative financial instruments for

Fred. Olsen Energy ASA - Annual Report 20051�

1�

Fred. Olsen Energy ASA - Annual Report 2005

Fred. Olsen Energy – Group

Notes

trading purposes. However, derivates that do

not qualify for hedge accounting are accounted

for as trading instruments.

Derivative financial instruments are recognised

initially at cost. Subsequent to initial recognition,

derivative financial instruments are stated at fair

value. The gain or loss on re-measurement to

fair value is recognised in profit or loss. There

are no derivatives to which hedge accounting

is applied.

The fair value of interest rate swaps is the esti-

mated amount that the Group would receive

or pay to terminate the swap at the balance

sheet date. The fair value of forward exchange

contracts is their quoted market price at the bal-

ance sheet date, being the present value of the

quoted forward price.

Trade and other receivables

Trade and other receivables are stated at their

amortised cost less impairment losses.

Cash and cash equivalents

Cash and cash equivalents include cash, bank

deposits and other short-term highly liquid

assets that are readily convertible to known

amounts of cash and which are subject to insig-

nificant changes in value.

Financial liabilities and equity

Financial liabilities and equity instruments issued

by the Group are classified according to the sub-

stance of the contractual arrangements entered

into and the definitions of a financial liability and

an equity instrument. An equity instrument is

any contract that evidences a residual interest

in the assets of the Group after deducting all of

its liabilities. The accounting policies adopted

for specific financial liabilities and equity instru-

ments are set out below as applicable.

Interest-bearing borrowings

Interest-bearing borrowings are recognised

initially at fair value less attributable transaction

costs. Subsequent to initial recognition, interest-

bearing borrowings are stated at amortised cost

with any difference between cost and redemp-

tion value being recognised in the income state-

ment over the period of the borrowings on an

effective interest basis.

Convertible bonds

Convertible bonds that can be converted to

share capital at the option of the holder, where

the number of shares issued does not vary with

changes in their fair value, are accounted for as

compound financial instruments consisting of a

liability component and an equity component.

The equity component of the convertible bonds

is calculated as the excess of the issue proceeds

over the present value of the future interest and

principal payments, discounted at the market

rate of interest applicable to similar liabilities that

do not have a conversion option. The interest ex-

pense recognised in the income statement then

reflects the market rate for bonds without con-

version. Converted options during the year are

split between liability and equity accordingly.

The interest expense on the liability component

is calculated by applying the prevailing market

interest rate at the time of transaction for similar

non-convertible debt to the liability component

of the instrument at the time of transaction. The

difference between this amount and the inter-

est paid is added to the carrying amount of the

convertible bond.

Trade and other payables

Trade and other payables are stated at cost.

Equity instruments

Equity instruments issued by the Group are

recorded at the proceeds received, net of direct

issue costs.

Property, plant and equipment

Owned assets

Property, plant and equipment are stated at

cost less accumulated depreciation and impair-

ment losses. The cost of self-constructed assets

and modifications includes the cost of material,

direct labour and other direct attributable cost

to bring the asset to a working condition for its

intended use.

The rig values have been revalued to fair value

on 1 January 2004, the date of transition to IFRS,

and are measured on the basis of deemed cost,

being the revalued amount at the transition

date.

Where components of an item of property, plant

and equipment have different useful lives, they

are accounted for separately.

Subsequent expenditures are capitalised when

it is probable that they will give rise to future

economic benefits. Other costs are recognised

in the income statement as incurred.

Leased assets

Leases in terms of which the Group assumes

substantially all the risks and rewards of the

ownership are classified as finance leases. All

other leases are classified as operating leases.

Assets recorded under finance leases are stated

at an amount equal to the lower of its fair value

and the present value of the minimum lease

payments at inception of the lease, less accumu-

lated depreciation and any impairment losses.

Depreciation

Depreciation is charged to the income state-

ment on a straight-line basis over the estimated

useful life of each component of property, plant

and equipment. The estimated useful lives,

residual values and decommissioning costs

are reviewed at each financial year end. No

decommissioning costs have been recorded to

date, and the presence of any obligations is re-

viewed at each financial year end. Any changes

are accounted for prospectively as a change in

accounting estimate.

The estimated useful lives are as follows:

Rigs 15 to 25 years

Deepwater Drillship 25 years

Major components 5 to 15 years

Plant and Buildings 5 to 50 years

Machinery and Equipment 3 to 10 years

Repairs and Maintenance

Costs for special periodic surveys/class renewal

surveys (SPS/RS) on offshore units required by

classification societies are capitalised and de-

preciated over the anticipated period between

surveys, generally five years. Other maintenance

and repair costs are expensed as incurred.

Intangible assets

Goodwill

All business combinations are accounted for by

applying the purchase method. Goodwill rep-

resents amounts arising on the acquisition of

subsidiaries, and is the difference between the

cost of the acquisition and the fair value of the

net assets acquired.

In respect of acquisitions prior to the transition

to IFRS, goodwill is included on the basis of its

deemed cost, which represents the amount re-

corded under previous GAAP. The classification

and accounting treatment of business combi-

nations that occurred prior to the transition to

IFRS has not been reconsidered in preparing the

Group’s opening IFRS balance sheet at 1 Janu-

ary 2004.

Fred. Olsen Energy ASA - Annual Report 2005 1�

1�

Fred. Olsen Energy ASA - Annual Report 2005

NotesFred. Olsen Energy – Group

Goodwill is stated at cost less any accumulated

impairment losses. Goodwill is allocated to cash

generating units and is no longer amortised but

is tested annually for impairment.

Research and development

Expenditures on research activities, undertaken

with the prospect of gaining technical know-

ledge and understanding, is recognised in the

income statement as an expense as incurred.

Other intangible assets

Other intangible assets that are acquired by the

Group are stated at cost less accumulated am-

ortisation and any impairment losses. Other in-

tangible assets consist of a management agree-

ment which is amortised over 5 years.

Inventories and consumable spare parts

The Group categorizes spare parts into two

groups, spare parts and spare assets. A spare

part is a consumable that is not depreciated,

but expensed when used against repair and

maintenance cost. A spare asset is a larger spare

item that is recorded as a rig component and

depreciated. Consumables are recorded at cost

less a reserve for overstocked items.

Impairment

The carrying amounts of the Group’s assets,

other than inventories and deferred tax assets

are reviewed at each balance sheet date to

determine whether there is any indication of

impairment. If any such indication exists, the

asset’s recoverable amount is estimated. When

considering impairment indicators, the Group

considers both internal (e.g. adverse changes in

performance) and external sources (e.g. adverse

changes in the business environment). These

are analyzed by reviewing day rates and broker

valuations. The recoverable amount of an asset

is the higher of its fair value less costs to sell and

value in use. The value in use is calculated as the

present value of the expected future cash flows

for the individual units.

The value in use is used for the annual impair-

ment test for goodwill, which is the present val-

ue of the future cash flows from continuing use

and ultimate disposal expected to be derived

from the cash generating unit. Fair value is not

readily determinable.

An impairment loss is recognised if the carry-

ing amount of an asset exceeds the recoverable

amount.

Employee benefits

Pensions

The Company and certain of its subsidiaries have

pension plans for employees which provide for

a defined pension benefit upon retirement. The

benefit to be received by employees generally

depends on many factors including length of

service, retirement date and future salary in-

creases. The Group’s net obligation in respect of

defined benefit pension plans is calculated sep-

arately for each plan by estimating the amount

of future benefit that employees have earned in

return for their services in the current and prior

periods. That benefit is discounted to determine

its present value, and the fair value of any plan

assets is deducted. The discount rate is the yield

at the balance sheet date reflecting the maturity

dates approximating to the terms of the Group’s

obligations. The calculation is performed by a

qualified actuary.

All actuarial gains and losses as at 1 January

2004, the date of transition to IFRS, were rec-

ognised. In respect of actuarial gains and losses

that arise subsequent to 1 January 2004 in cal-

culating the Group’s obligation in respect of a

plan, to the extent that any cumulative unrec-

ognised actuarial gain or loss exceeds 10 per

cent of the greater of the present value of the

defined benefit obligation and the fair value of

plan assets, that portion is recognised in the

income statement over the expected average

remaining working lives of the employees par-

ticipating in the plan. Otherwise, the actuarial

gain or loss is not recognised.

In addition, employees of some subsidiaries

are covered by multi-employer pension plans

administered by trade unions and by plans ad-

ministered by related companies. Costs related

to these plans are expensed as incurred.

Share based payment transactions

In 1998, the Company’s shareholders resolved to

grant the Board of Directors authority to issue up

to 3 million shares to be used for an employee

incentive compensation plan designed to align

the interest of management with those of its

shareholders. All share based payment awards

are settled by the physical delivery of shares.

The company has elected to use the voluntary

exemption available for share based payment

transactions from the general requirement for

retrospective application of IFRS. The recogni-

tion and measurement requirements of IFRS 2:

Share-based Payment is therefore not applied

retrospectively to equity instruments that were

granted on or before 7 November 2002.

Social security tax is calculated for share options

in the money at year end and is recognised as

expense over the vesting period.

Provisions

A provision is recognised in the balance sheet

when the Group has a present legal or construc-

tive obligation as a result of a past event, and it

is probable than an outflow of economic ben-

efits will be required to settle the obligation.

Revenue

Charter rate contracts

Revenue derived from charter-hire contracts

or other service contracts is recognised in the

period that services are rendered at rates estab-

lished in the relevant contracts. Certain contracts

include mobilisation fees payable at the start of

the contract. In cases where the fee covers a

general upgrade of a rig or equipment which

increases the value of the rig or equipment be-

yond the contract period, the fee is recognised

as revenue over the contract period whereas

the investment is depreciated over the remain-

ing lifetime of the asset. In cases where the fee

covers specific upgrades or equipment specific

to the contract, the mobilisation fees are recog-

nised as revenue over the estimated contract pe-

riod. The related investment is depreciated over

the estimated contract period. In cases where

the fee covers specific operating expenses at the

start up of the contract the fees are recognised

in the same period as the expenses.

Long-term engineering and fabrication contracts

Revenues on long-term contracts are recognised

using the percentage of completion method

throughout the performance period of the

contract when the outcome can be measured

reliably. The percentage of completion is typi-

cally calculated based on the ratio of contract

costs incurred to date to total estimated con-

tract costs after providing for all known or an-

ticipated costs. On certain contracts the Group

may use the ratio of incurred to total estimated

direct labour hours to determine the percent-

age of completion. Costs include material, direct

labour and engineering. Selling, general and ad-

ministrative expenses are charged to operations

as incurred. The effect of changes in estimates of

contract costs is recorded currently. An expected

loss on a contract is recognised immediately in

the income statement.

Fred. Olsen Energy ASA - Annual Report 200520

20

Fred. Olsen Energy ASA - Annual Report 2005

Fred. Olsen Energy – Group

Notes

Costs and estimated earnings in excess of bill-

ings on uncompleted contracts represent rev-

enues earned under the percentage of comple-

tion method but not yet billable under the terms

of the contract. Amounts billed in advance of

satisfying revenue recognition criteria on long

term contracts are classified as billings in excess

of costs and estimated earnings on uncomplet-

ed contracts.

Generally, contract revenues become billable

upon the Group attaining certain contract mile-

stones. The Group typically does not require

collateral from customers except in situations

where warranted due to assessments of risk

factors.

Government grants

Governmental grants related to capital expen-

ditures are deferred and recognised as income

over the useful lives of related capital expendi-

ture. Grants related to specific contracts are

recognised as income over the period contract

work is performed.

Expenses

Pool income/expense

Certain rig owning subsidiaries have entered

into a five-rig pool agreement with the owner

of the Bulford Dolphin, where net earnings be-

fore depreciation are equalised amongst the rig

owners. The net pool income or pool expenses

from the Group’s four rigs included in the pool

are netted against the bareboat/time charter

fees paid to the owner of the Bulford Dolphin.

Operating lease expenses

Payments made under operating leases are rec-

ognised in the income statement on a straight-

line basis over the term of the lease.

Finance lease payments

Minimum lease payments are apportioned be-

tween the finance charge and the reduction of

the outstanding liability. The finance charge is

allocated to each period during the lease term so

as to produce a constant periodic rate of interest

on the remaining balance of the liability.

Net financing costs

Net financing costs comprise interest payable

on borrowings calculated using the effective

interest rate method, interest receivable, foreign

exchange gains or losses, and gains and losses

on financial instruments.

Income tax

Income tax on the profit or loss for the year

comprises current and deferred tax. Income tax

is recognised in the income statement except

to the extent that it relates to items recognised

directly in equity, in which case it is recognised

in equity.

Current tax is the expected tax payable on the

taxable income for the year and any adjustment

to tax payable in respect of previous years.

Deferred tax is provided using the balance

sheet liability method. Deferred tax assets and

liabilities are recognised for the future tax conse-

quences attributable to differences between the

carrying amounts of existing assets and liabilities

in the financial statements and their respective

tax bases. The amount of deferred tax provided

is based on the expected manner of realisation

or settlement of the carrying amount of assets

and liabilities, using tax rates enacted or enacted

at the balance sheet date.

A deferred tax asset is recognised only to the

extent that it is probable that future taxable

profits will be available against which the asset

can be utilised. Deferred tax assets are reduced

to the extent that it is no longer probable that

the related tax benefit will be realised.

Segment reporting

A segment is a distinguishable component of

the Group that is engaged in either providing

products or services (business segment), or in

providing goods or services within a particular

economic environment (geographical seg-

ment), which is subject to the risks and rewards

that are different from those of other segments.

The Group provides services and operates within

the two business segments; offshore drilling and

engineering and fabrication.

Borrowing Costs

Under IFRS, borrowing costs may be capitalized

as part of the cost on certain qualifying assets,

however, the Group has not applied this op-

tion.

Earnings per share

Basic

Basic earnings per share is calculated by dividing

the profit attributable to equity holders of the

Company by the weighted average number of

ordinary shares in issue during the year, exclud-

ing ordinary shares purchased by the Company

and held as treasury shares.

Diluted

Diluted earnings per share is calculated by ad-

justing the weighted average number of ordi-

nary shares outstanding to assume conversion

of all dilutive potential ordinary shares. The Com-

pany has two categories of dilutive potential

ordinary shares: convertible bonds and share

options. The convertible bonds are assumed to

have been converted into ordinary shares and

the net profit is adjusted to eliminate the interest

expense less the tax effect. For the share options,

a calculation is done to determine the number

of shares that could have been acquired at fair

value (determined as the average annual mar-

ket share price of the Companies shares) based

on the monetary value of the rights attached

to outstanding share options. The number of

shares calculated as above is compared with

the number of shares that would have been is-

sued assuming the exercise of the share options.

Potential ordinary shares that are anti-dilutive

are excluded from the calculation.

New accounting pronouncements

At the date of authorization of these financial

statements, the following standards and inter-

pretations that were potentially applicable to

the Group were issued but not yet effective:

IAS 19 (Amendment), Employee Benefits

(effective from 1 January 2006)

This amendment introduces the option of an

alternative recognition approach for actuarial

gains and losses. It may impose additional rec-

ognition requirements for multi-employer plans

where insufficient information is available to ap-

ply defined benefit accounting. It also adds new

disclosure requirements. As the Group does not

intend to change the accounting policy adopt-

ed for recognition of actuarial gains and losses

and does not participate in any multi-employer

plans, adoption of this amendment will only

impact the format and extent of disclosures

presented in the accounts. The Group will apply

this amendment from annual periods beginning

1 January 2006.

IAS 39 (Amendment), The Fair Value Option

(effective from 1 January 2006)

This amendment changes the definition of finan-

cial instruments classified at fair value through

profit or loss and restricts the ability to designate

Fred. Olsen Energy ASA - Annual Report 2005 21

21

Fred. Olsen Energy ASA - Annual Report 2005

NotesFred. Olsen Energy – Group

financial instruments as part of this category. The

Group believes that this amendment should not

have a significant impact on the classification of

financial instruments, as the Group should be

able to comply with the amended criteria for the

designation of financial instruments at fair value

through profit and loss. The Group will apply this

amendment from annual periods beginning 1

January 2006.

IFRS 7, Financial Instruments: Disclosures, and

a complementary amendment to IAS 1, Pres-

entation of Financial Statements – Capital Dis-

closures

(effective from 1 January 2007)

IFRS 7 introduces new disclosures to improve

the information about financial instruments. It

requires the disclosure of qualitative and quan-

titative information about exposure to risks

arising from financial instruments, including

specified minimum disclosures about credit

risk, liquidity risk and market risk, including sen-

sitivity analysis to market risk. It replaces IAS 30,

Disclosures in the Financial Statements of Banks

and Similar Financial Institutions, and disclosure

requirements in IAS 32, Financial Instruments:

Disclosure and Presentation. It is applicable to

all entities that report under IFRS. The amend-

ment to IAS 1 introduces disclosures about the

level of an entity’s capital and how it manages

capital. The Group assessed the impact of IFRS

7 and the amendment to IAS 1 and concluded

that the main additional disclosures will be the

sensitivity analysis to market risk and the capital

disclosures required by the amendment of IAS

1. The Group will apply IFRS 7 and the amend-

ment to IAS 1 from annual periods beginning 1

January 2007.

IFRIC 4, Determining whether an Arrangement

contains a Lease

(effective from 1 January 2006)

IFRIC 4 requires the determination of whether an

arrangement is or contains a lease to be based

on the substance of the arrangement. It requires

an assessment of whether: (a) fulfillment of the

arrangement is dependent on the use of a

specific asset or assets (the asset); and (b) the

arrangement conveys a right to use the asset.

Management is currently assessing the impact

of IFRIC 4 on the Group’s operations.

Accounting estimates and judgements

Estimates and judgements are continually evalu-

ated and are based on historical experience and

other factors, including expectations of future

events that are believed to be reasonable under

the circumstances.

Critical accounting estimates and assumptions

For accounting purposes the Group makes esti-

mates and assumptions concerning the future.

The resulting accounting estimates may differ

from the eventual outcome, but are regarded as

the best estimate at balance sheet date. The es-

timates and assumptions that have a significant

risk of causing a material adjustment to the car-

rying amounts of assets and liabilities within the

next financial year are discussed below.

I) Revenue recognition

The Group uses the percentage-of-completion

method in accounting for its engineering and

fabrication contracts. Use of the percentage-of-

completion method requires the Group to esti-

mate the work performed to date as a propor-

tion of the total work to be performed.

II) Income taxes

The Group is subject to income taxes in numer-

ous jurisdictions. Significant judgement is re-

quired in determining the worldwide provision

for income taxes. There are many transactions

and calculations for which the ultimate tax deter-

mination is uncertain during the ordinary course

of business. The Group recognises liabilities for

anticipated tax issues based on best estimate of

whether additional taxes will be due. Where the

final tax outcome of these matters is different

from the amounts that were initially recorded,

such difference will impact the income tax and

deferred tax provisions in the period in which

such determination is made.

III) Pension benefits

The present value of the pension obligations

depends on a number of factors that are de-

termined on an actuarial basis using a number

of assumptions. The assumptions used in de-

termining the net cost (income) for pensions

include the discount rate. Any changes in these

assumptions will impact the calculated pension

obligations. The Group determines the appropri-

ate discount rate at the end of each year. This

is at interest rate that should be used to deter-

mine the percent value of estimated future cash

outflows expected to be required to settle the

pension obligations. The rate is based on a 10

years government bonds which was 3.64% at

31 December 2005 representing the average

expected period of service. Other key assump-

tions for pension obligation are based on cur-

rent market conditions.

IV) Estimates for rigs and drill ship

At each balance sheet date judgement is used

to determine whether there is any indication of

impairment of the Group fleet of rigs and the

drill ship. If any such indication exists, the as-

set’s recoverable amount is estimated. When

considering impairment indicators, the Group

considers both internal (e.g. adverse changes in

performance) and external sources (e.g. adverse

changes in the business environment). These

are analyzed by reviewing day rates and broker

valuations. If an indicator of impairment is noted,

further management estimate is required to de-

termine the amount, if any, of impairment. In

order to measure for potential impairment, the

carrying amount of the rigs and drill ship would

be compared to the recoverable amount, which

is the value in use. The value in use is calculated

as the present value of the expected future cash

flows for the individual units, requiring signifi-

cant management estimates of the proper dis-

count rates as well as the length and amounts

of cash flows. An impairment loss would then be

recognised to the extent the carrying amount

exceeds the recoverable amount.

V) Estimated impairment of goodwill

In accordance with the accounting policy the

Group tests annually whether goodwill has suf-

fered any impairment. The recoverable amounts

of cash-generating unit have been determined

based on a value-in-use calculation. This calcula-

tion requires the use of estimates and is based

on assumptions that are consistent with the

market valuation of the Group.

Fred. Olsen Energy ASA - Annual Report 200522

22

Fred. Olsen Energy ASA - Annual Report 2005

Fred. Olsen Energy – Group

Notes

Note 2 – Segment reporting

Segment information is presented in respect of the Group’s business and geographical segments. The primary format, business segments, is based on the

Group’s management and internal reporting structure.

Inter-segment pricing is determined on an arm’s length basis.

Business segments

The Group comprises the following main business segments:

Offshore drilling provides exploration drilling services to the offshore oil and gas industry. The operating expenses within Fred.Olsen Energy ASA is