138

Annual Report 2009 Robeco Groep N.V.

Annual Report 2009

Robeco Groep N.V.

Corporate Statements 2009

2 Annual Report 2009 Robeco Groep N.V.

3Corporate Statements 2009

Corporate Statements

01 Preface

02 General information

03 Report of the Supervisory Board

04 Corporate & fund governance

05 Report of the Management Board

Robeco profile and key figures

Chapter 1 Market environment

Chapter 2 Strategy

Chapter 3 Organization

Chapter 4 Investment performance

Chapter 5 Business development 2009

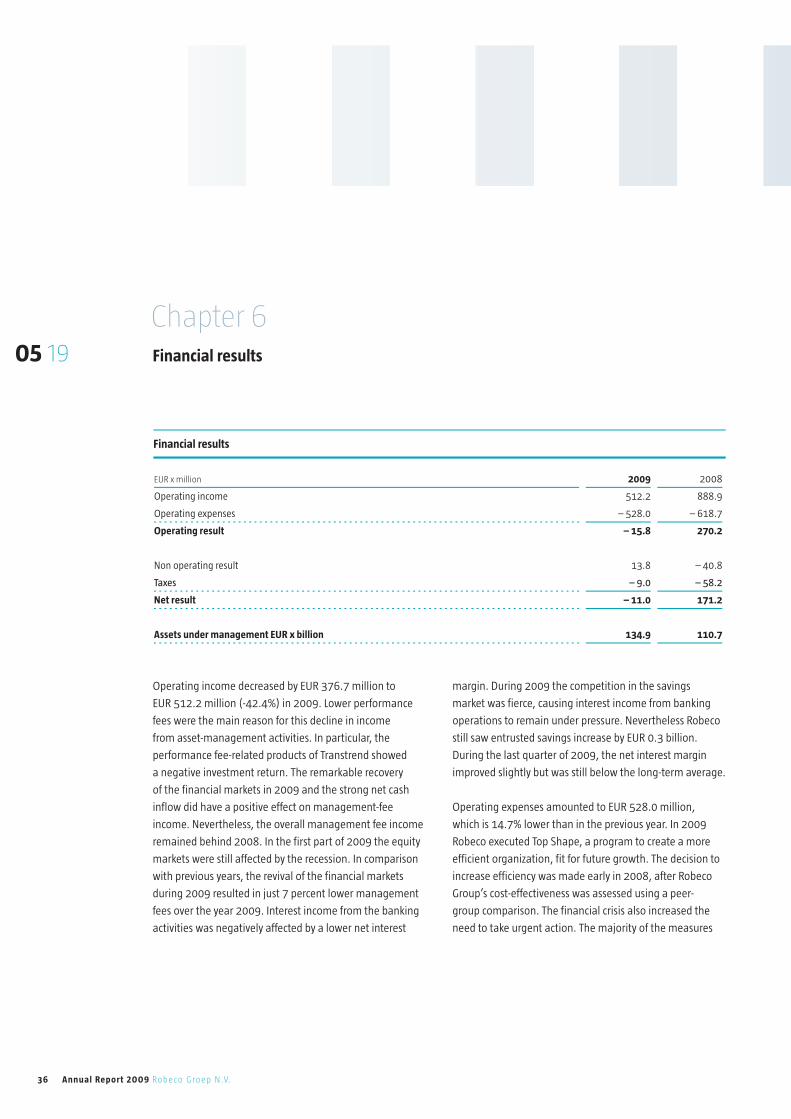

Chapter 6 Financial results

Chapter 7 Compliance & Risk management

Chapter 8 Responsible Investing & Corporate responsibility

Chapter 9 Robeco in 2010

06 Special: Emerging Markets

07 Addresses

Financial Statements

5

6

8

12

18

20

22

29

29

32

36

38

49

52

54

58

61

Contents

4 Annual Report 2009 Robeco Groep N.V.

01 1

5Corporate Statements 2009

For Robeco, 2009 has been a year of mixed blessings.

For our clients, both returns and relative performance

have been good to excellent; a very welcome (albeit not

complete) rebound from the disastrous investment

year of 2008. Also, the record inflow of new money

(EUR 7.5 billion net) as well as the fact that clients

are daring to take risks again are both clearly positive

factors. However, it is a big disappointment to have

to announce Robeco’s first ever annual loss, amounting

to EUR 13.3 million.

The year 2009 can be described as a roller-coaster ride from

various perspectives. Financial markets, more specifically

equities, got off to a very negative start, followed by a

remarkably strong rebound from mid-March. Many markets

and also many of our funds and mandates were able to

record double-digit returns for the year. Investments that

took a big hit in 2008, like high-yield bonds and emerging-

markets equities, enjoyed excellent performance in 2009,

gaining 53% and 85% respectively and rewarding those

clients who stayed the course with us.

Robeco’s operations failed to produce a profit in 2009.

This is not so much a feature of last year alone, but in

previous years this failure to make profits was more than

offset by the performance fees generated by our subsidiary,

Transtrend. Although performance fees are indeed

pleasing, since we only receive them when our clients

are enjoying excellent returns, Robeco as an investment

manager may not solely rely on them to run a profitable

business.

In 2010, a year of change, Robeco will establish a new

strategy. It will build on our heritage, make use of our

skill sets and focus on the interests of our clients. We will

streamline our product offering, close a number of offices

and consolidate various business activities. Robeco will also

strengthen its market position, both internationally and in

the Netherlands. In addition to our recognized capabilities

in the equity and fixed-income markets, Robeco will

continue to offer clients innovative investment solutions.

A number of these will be geared towards producing

attractive inflation-adjusted returns, others will benefit

from the expertise and the network of our parent company,

Rabobank, in the Food & Agri business.

Over the next five years, greater efficiency, innovation and

growth will first benefit current and future clients, both

retail and wholesale, and will also contribute to producing

a healthier bottom line. To succeed with this, Robeco will

rely on the talent, creativity and energy of our employees.

Based on my first six months with ‘The Investment

Engineers’, I am confident of a favorable outcome.

Roderick Munsters

CEO Robeco Groep N.V.

Preface

6 Annual Report 2009 Robeco Groep N.V.

Composition of the Supervisory Board

D.P.M. (Dick) Verbeek, Chairman

P. J.A. (Piet) van Schijndel, Vice Chairman

A. (Bert) Bruggink (as from 1 April 2009)

W.H. (Willem) Buiter (1 April - 31 December 2009)

J.C. (Hans) ten Cate

G. (Gilles) Izeboud

Ph. (Philip) Lambert

D.J.M.G. (Rik) Baron van Slingelandt (until 1 May 2009)

Composition of the Management Board

R.M.S.M. (Roderick) Munsters, Chairman and CEO

as from 1 September 2009

G.A. (George) Möller, Chairman and CEO

until 1 September 2009

L.M.T. (Leni) Boeren

H.W.D.G. (Hester) Borrie (as from 5 November 2009)

S. (Sander) van Eijkern (until 1 February 2010)

C.T.L. (Constant) Korthout

F.L. (Frank) Kusse (until 1 October 2009)

J.L.N.A. (Jean-Louis) Laurens (20 February - 1 June 2009)

H.A.A. (Hans) Rademaker (as from 1 February 2010)

Company Secretary

D.H. (Dave) Cross

Members of the Supervisory Board

D.P.M. (Dick) Verbeek, Chairman (male, 59)

Dutch nationality. Appointed in 2001 and last reappointed

in 2007. Scheduled to resign and eligible for reappointment

in 2011. Former member of the Executive Board of Aon

Group in Chicago and former chairman/CEO of the Executive

Board of Aon Holdings in Rotterdam. Supervisory Director of

Aegon N.V., Robeco N.V., Rolinco N.V. and Rorento N.V.

P.J.A. (Piet) van Schijndel, Vice Chairman (male, 59)

Dutch nationality. Appointed in 2006. Scheduled to

resign and eligible for reappointment in 2010. Member of

the Executive Board of Rabobank Nederland.

A. (Bert) Bruggink (male, 46)

Dutch nationality. Appointed in 2009. Member of

the Executive Board of Rabobank Nederland, professor in

Financial Management and Business Administration at

Twente University.

J.C. (Hans) ten Cate, (male, 63)

Dutch nationality. Appointed in 2001 and last reappointed

in 2009. Former member of the Executive Board of

Rabobank Nederland.

G. (Gilles) Izeboud (male, 67)

Dutch nationality. Appointed in 2004 and reappointed in

2008. Scheduled to resign and eligible for reappoint ment in

2012. Partner and board member at Pricewater houseCoopers

(1977/2002). Former member of the Corporate Governance

Committee in the Netherlands. Deputy Justice at the Enter-

prise Section of the Amsterdam Court of Appeal. Supervisory

Director of Robeco N.V., Rolinco N.V. and Rorento N.V.

02 1

General information

7Corporate Statements 2009

Ph. (Philip) Lambert (male, 63)

Dutch nationality. Appointed in 2005 and last

reappointed in 2009. Scheduled to resign and eligible

for reappointment in 2013. Former Head of Corporate

Pensions at Unilever N.V. and PLC in London. Member

of the Investment Committee of the ABN AMRO Pension

Fund. Supervisory Director of Robeco N.V., Rolinco N.V. and

Rorento N.V.

Committees of the Supervisory Board

– Audit & Compliance Committee:

Gilles Izeboud (Chairman)

Bert Bruggink

Dick Verbeek

– Nomination, Remuneration & Corporate Governance

Committee:

Hans ten Cate (Chairman)

Philip Lambert

Dick Verbeek

– Investment Committee (started 1 January 2010):

Philip Lambert (Chairman)

Bert Bruggink

Dick Verbeek

Members of the Management Board

R.M.S.M. (Roderick) Munsters (male, 46)

Dutch and Canadian nationality. Employed at Robeco since

September 2009. Former member of the Executive Board

and Chief Investment Officer of APG All Pensions Group and

member of the Executive Board (investments) of PGGM.

Member of the Capital Market Committee of the Dutch

regulator Autoriteit Financiële Markten (AFM). Chairman

and Chief Executive Officer since September 2009.

L.M.T. (Leni) Boeren (female, 46)

Dutch nationality. Employed at Robeco since January 2005.

Former Managing Director of Information Services and

member of the Operational Committee of Euronext N.V.

Head of Robeco Direct N.V. since January 2005 and Chief

Operating Officer as of 1 January 2009.

H.D.W.G. (Hester) Borrie (female, 40)

Dutch nationality. Employed at Robeco since October

2009 as head of Global Distribution and Marketing.

Formerly held several sales positions at Morgan Stanley

in Amsterdam/London and was an associate in Corporate

Finance & Capital Markets at MeesPierson.

C.T.L. (Constant) Korthout (male, 47)

Dutch nationality. Employed at Robeco since 1992.

Chief Financial Officer since 2002, became member of

the Management Board in 2004.

H.A.A. (Hans) Rademaker (male, 48)

Dutch nationality. Employed at Robeco since February 2010

as head of Mainstream Investments. Former Director of

Fiduciary Management at Kempen Capital Management,

Director of Asset Management and head of Financial

Investments and Treasury at Mn Services.

General information

N.B. Supervisory directorships at listed companies only are given above.

8 Annual Report 2009 Robeco Groep N.V.

Composition of the Supervisory BoardMr. A. Bruggink and Mr. W.H. Buiter were appointed as

members of the Supervisory Board as of 1 April 2009.

Mr. D.J.M.G. Baron van Slingelandt resigned as member of

the Supervisory Board as of 1 May 2009. He has been

a member of the Supervisory Board since 1 June 2002.

We thank him for his valuable contribution during those

years. In the General Meeting of Shareholders held on

24 June 2009, Mr. J.C. ten Cate resigned as member of

the Supervisory Board, but was reappointed for the period

of one year with immediate effect.

Mr. Buiter, who became Chief Economist of Citigroup as

of 1 January 2010, resigned per the same date.

The supervisory directors, except Messrs. Bruggink, Ten Cate

and Van Schijndel are independent within the meaning

of the Dutch Corporate Governance Code. For information

about each of the supervisory directors, please refer to the

General Information in this annual report.

Meetings of the Supervisory BoardIn 2009 the Supervisory Board met five times. Most

of the Supervisory Board meetings were attended by

almost all the Supervisory Board members and by all

the Management Board members. The members of the

Management Board were not, however, present when their

performance and remuneration were discussed. The CEO

did attend these meetings but did not attend the discussion

on his own performance and remuneration. The meeting

in April, in which the 2008 annual report was discussed,

was also attended by the external auditor, Ernst & Young

Accountants LLP.

In September, the Supervisory Board met at the offices of

Robeco Investment Management (RIM) in Boston. Prior to

this meeting, the managers of RIM, Harbor Capital Advisors

03 1 (HCA) and Sage gave presentations and exchanged

ideas with the Supervisory Board on various issues, such

as business development, investment policies and the

situation in the markets where these entities operate.

The Supervisory Board used detailed, regularly updated

reports for its discussions with the Management Board

on the company’s quarterly and year-end results in terms

of budgetary targets, investment results and assets

under management. Based on reports from its Audit &

Compliance Committee, the Supervisory Board discussed

subjects such as the risks relating to investment policies and

the instruments to control these risks as well as financial

accounting, (internal-) audit and compliance-related issues.

Various strategic issues were extensively discussed,

particularly those relating to possible business

opportunities and synergies with third parties.

The Supervisory Board’s July meeting started with

a presentation of market observations given by an external

advisor, after which the members discussed possible

strategic opportunities.

The Supervisory Board paid considerable attention to

the project to integrate the various back-office and ICT

operations. As reported last year, this is a project that spans

several years, and is considered to be an important building

block in the process of internationalization through

the establishment of foreign operations.

The Supervisory Board evaluated the results of measures

taken to create a more efficient organization, which

resulted in considerable, structural cost reductions.

Responsible investing was a regular agenda item at

meetings of the Supervisory Board and the Management

Board’s proposed exclusion policy was a particularly

important issue which was discussed and approved.

Supervisory Board

Report of the Supervisory Board

9Corporate Statements 2009

Supervisory Board Committees

Audit & Compliance Committee

In 2009 the Audit & Compliance Committee met seven

times. The meetings of the Committee were attended by

the CEO and the CFO, together with the head of Internal

Audit and the external auditor Ernst & Young Accountants

LLP. These meetings were preceded by private sessions with

the external auditor. Discussions on compliance-related

issues were attended by the head of Corporate Compliance.

The follow-up to the recommendations made by

the internal and external auditor were also discussed.

On the basis of quarterly reports, the Audit & Compliance

Committee discussed various internal-audit and compliance

issues. Due attention was paid to the analysis of incidents

that had occurred and the consequences these may have

for processes and clients.

In the context of the Robeco fund-governance principles,

there was especially discussion on the issue of securities

lending.

The head of Group Risk Management gave a presentation

on the scope and activities of the risk-management

department, including the increasing role of operational

risk management.

Other subjects discussed included pending litigation issues,

the progress on integrating the back-office operations and

the HP/EDS transformation (see page 37 and 44).

The Audit & Compliance Committee agreed to the proposal

to change its charter to reflect the fact that from now on it

will also act as the audit committee of Robeco Direct N.V..

Nomination, Remuneration & Corporate Governance

Committee

In 2009, the Nomination, Remuneration & Corporate

Governance Committee met four times, in the presence

of the CEO, the head of Human Resources and, depending

on the subject discussed, the CFO.

The composition of the Management Board and proposals

for the appointment of new members were discussed.

The remuneration of the members of the Management

Board was discussed, including bonus and E-notes

allocation, while key performance indicators were also

an agenda item.

The group-wide bonus policy and the 2009 E-notes

allocation were both discussed, primarily in the context of

market circumstances.

Other issues on the agenda were succession and continuity

planning and talent development, while an analysis of

Robeco’s pension plan was also discussed.

Composition of the Management BoardThe composition of the Management Board changed

considerably in 2009 and was the subject of discussion

both in the Nomination, Remuneration & Corporate

Governance Committee and the full Supervisory Board.

Mr. George A. Möller resigned as CEO and was succeeded

by Mr. Roderick M.S.M. Munsters, both effective on

1 September 2009.

Mr. Jean-Louis Laurens, who was responsible for

Mainstream Investment Management, resigned from

the Management Board for personal reasons as of 1 June

Supervisory Board

10 Annual Report 2009 Robeco Groep N.V.

2009. Mr. Sander van Eijkern, who was responsible for

Alternative Investments and CEO of SAM, stepped down

from his position as of 1 February 2010.

Mr. Hans Rademaker was appointed head of Investments

as of 1 February 2010.

Mr. Frank Kusse, who was responsible for Marketing,

Sales and Distribution resigned as of 1 October 2009.

He was succeeded by Mrs. Hester W.D.G. Borrie who was

appointed as of 5 November 2009.

We thank all former members of the Management Board

for their contribution to the development of the company.

Remuneration report

Robeco’s remuneration policy

The structure of the remuneration policy for members

of the Management Board is in line with Robeco Groep

N.V.’s general remuneration policy. The objective of the

remuneration policy is to position Robeco Groep N.V.

competitively in the international asset-management

market, enabling it to attract and retain employees who

perform well and are expected to make an important

contribution to the firm. The employment package and

remuneration systems are also structured to promote

a long-term relationship between employees and

the organization. The Supervisory Board’s Nomination,

Remuneration & Corporate Governance Committee

decides on the employment benefits for the individual

members of the Management Board. The remuneration

package consists of the following components: fixed

remuneration, variable short-term remuneration (bonus),

variable long-term remuneration (equity notes) and fringe

benefits.

Fixed remuneration

The fixed-remuneration component aims to provide

a good, competitive base remuneration relative to

the international asset-management market, taking

into account the relevant function’s level of responsibility,

results and competences. The level of responsibility is

established using the Hay function-valuation system.

Variable remuneration (bonus)

The variable remuneration component for the

Management Board depends on Robeco Groep N.V.’s

gross result (worldwide) and the inflow of new assets

under management. If Management Board members

are responsible for an operational unit, this component

is also linked to the financial results relating to their

responsibilities. The ratio between the actual results

and the budgeted results determines the level of the

eventual payment. All bonus payments are made in

three installments. In the first year (after the applicable

financial year), 60% is paid, followed by two other

deferred portions. A 30% portion is paid in the second

year and a 10% portion in the third year. Both the

deferred portions are converted into Equity Notes (see

below) in the first year at the time when the 60% is paid.

These E-notes vest at the end of these deferred periods in

years two and three. If the recipient is no longer employed

by Robeco Groep N.V. or hands in his notice when the

60% payment is made – either on, or before the day of

vesting of the E-notes – his right to this remuneration

component lapses.

Equity notes (E-notes)

A limited group of employees (less than 5% of the total

workforce), including the Management Board, is given the

03 3

Report of the Supervisory Board - Remuneration report

11Corporate Statements 2009

opportunity to participate directly in Robeco’s future growth

through virtual shares in Robeco Groep N.V. E-notes are a

way of additionally rewarding key employees with the aim

of increasing their long-term commitment to the group.

In the case of the Management Board, the Nomination,

Remuneration & Corporate Governance Committee decides

whether or not to grant E-notes and on the quantity to

be granted. In the case of all other eligible employees,

the Management Board defines the group of personnel

that becomes eligible for E-notes and determines at its

discretion the level of allocation. The allocation of E-notes

is not only linked to the employee’s individual performance,

but also to the contribution they have made to achieving

the strategic targets of their own business unit and of

the Robeco Group as a whole. The E-notes represent a

value that, like shares, directly corresponds to the value of

Robeco Groep N.V., and is based on ‘profit from continuing

operations adjusted downward for the expenses related to

the long-term incentive plans and adjusted for the results

related to the foreign-currency hedge’. E-notes have a

maximum life of six years with a vesting period of at least

four years. During the vesting period E-notes cannot be

exercised.

Investment notes (I-notes)

In addition to the E-notes scheme, there is also

an Investment notes (I-notes) scheme. This scheme

enables employees, who are granted E-notes, to make

investments themselves in additional ‘virtual shares’.

Like E-notes, the I-notes are linked to the value/earnings

development of Robeco Groep N.V. I-notes have

a maximum life of 5 years, during which dividend is

generated. If I-notes are held for the full 5 years

investors receive a loyalty premium.

Fringe benefits

Robeco offers a competitive package of fringe benefits,

which may include a lease car, expense allowance,

insurance, supplementary mortgage benefit, and

a pension plan made up of a final-salary plan (defined

benefit, to a certain maximum) and a defined-contribution

scheme.

Recommendation to adopt the annual financial statementsThe Supervisory Board has taken note of the contents of

the report presented by Ernst & Young Accountants LLP,

which have given an unqualified opinion on the annual

financial statements as presented and recommend

approval thereof. We concur with the Management Board’s

proposal to distribute no dividend.

Rotterdam, 8 April 2010

The Supervisory Board

12 Annual Report 2009 Robeco Groep N.V.

As in previous years, in 2009 corporate governance

remained a widely discussed subject. Although Robeco

Groep N.V. is not a listed company and, as such, is

not bound by the Dutch Corporate Governance Code

(hereafter referred to as the Code), Robeco Groep

N.V. does find it important to comply with the Code’s

principles and best-practice provisions where possible.

Robeco strives to implement any amendments to the

Code if these are applicable. It should be noted here

that the shares of Robeco Groep N.V. are all held by

one shareholder, the Coöperatieve Centrale Raiffeisen-

Boerenleenbank B.A. (‘Rabobank Nederland’). This

means that those Code principles that relate to multiple

shareholders do not apply. Below an overview is given of

the issues covered by the Code that are most relevant to

Robeco Groep N.V.

The principles and best-practice provisions of

the Code that Robeco Groep N.V. does not or cannot

apply and the current corporate-governance structure

are also described and explained.

Compliance and enforcement of the CodeThe corporate-governance policy of Robeco Groep N.V. is

established in the company’s Articles of Association and

in the shareholder agreement between Robeco Groep

N.V. and Rabobank Nederland, which was entered into

in 1997 and amended in 2004. Within this framework,

Robeco Groep N.V.’s Management and Supervisory

Boards are responsible for the company’s corporate-

governance structure and compliance with the Code. They

are accountable to Robeco Groep N.V.’s only shareholder,

Rabobank Nederland. Robeco Groep N.V. intends to comply

as fully as possible with the Code.

04 1 The Management BoardRobeco Groep N.V. is managed by a Management Board,

currently consisting of five members. The Management

Board is supervised by a Supervisory Board. According to

the appointment procedure, a proposal is put forward at

the General Meeting of Shareholders and this should be

approved by the Supervisory Board before a member of the

Management Board is appointed at the General Meeting

of Shareholders. The Supervisory Board has undertaken

not to reject proposals for appointments without good

reason. On account of the above mentioned nature of the

company, the maximum four-year membership term for

board members recommended by the Code is not complied

with and some of the Robeco Groep N.V. Management

Board members are appointed for an indefinite period.

After prior consultation with the Supervisory Board, the

General Meeting of Shareholders appoints one of the

members of the Management Board as chairman. The

General Meeting of Shareholders is authorized to suspend

or dismiss any member of the Management Board at any

time. Dismissal terms for Management Board members are

determined reasonably and fairly on a case-by-case basis.

The Management Board is responsible for formulating and

executing the approved strategic and operational policy

of the company as well as managing its daily operations.

The Management Board reports to the Supervisory Board

and to the General Meeting of Shareholders. Furthermore,

the Management Board is also responsible for compliance

with all relevant legislation and regulations, for risk

management and for the financing of all corporate

activities. Finally, the Management Board is responsible for

providing the Supervisory Board with information, relating

to the company’s activities and on any developments

affecting the Robeco Group as a whole. The Supervisory

Corporate & fund governance

Corporate Governance

13Corporate Statements 2009

Board needs this information to carry out its supervisory

responsibilities in a satisfactory way. As recommended by

the Code, Robeco Groep N.V.’s regulatory environment and

its risk-management structure are explained in the Report

of the Management Board in the chapter Compliance &

Risk management. The remuneration policy for members

of the Management Board is explained in the Report of the

Supervisory Board. The way in which this policy has been

applied in this reporting period is explained in the notes to

the annual financial statements. The remuneration policy is

published on the company’s website and forms an integral

part of the Annual Report. The remuneration per individual

board member is found in the notes to the annual

financial statements. The value of the options granted to

the Management Board and staff is also shown there. An

explanation of how this is calculated can be found in the

Accounting Policies in the Annual Financial Statements.

As explained in the remuneration report, members of the

Management Board and certain employees are granted

E-notes. The number of options granted depends on an

employee’s income. The exercise price is based on the price

of the underlying shares at the time when the options are

granted. The company does not grant loans or guarantees

to members of the Management Board. Robeco Direct

N.V., which is a wholly-owned subsidiary of Robeco Groep

N.V. and a credit institution, can grant loans to members

of the Management Board under the same conditions

that apply to other Robeco employees. In the opinion

of the Management Board, there were no conflicts of

interest or semblance thereof between the company and

the members of the Management Board in 2009. Robeco

Groep N.V. does not have separate regulations covering

securities transactions by members of the Management

Board. The applicable ‘Rules and regulations regarding

private investment transactions by employees and insiders

of Robeco Nederland B.V.’ is published on the company’s

website. These rules should ensure that any insider trading

or a semblance thereof, and any mixing of business and

private interests is avoided. The company is continuously

striving to strengthen its internal risk-management and

control framework.

The Supervisory BoardIt is the duty of the Supervisory Board to supervise

the Management Board’s activities and any general

developments at the company and its affiliated enterprises.

The Supervisory Board also advises the Management

Board. Robeco Groep N.V. has laid down the specific tasks

of the Supervisory Board in the Articles of Association of

the company and in the above mentioned shareholder

agreement. These tasks are not, therefore, documented

in separate regulations. Information on the Supervisory

Board’s activities in the past financial year and the

information required by the Code can be found in the

Report of the Supervisory Board on pages 10 through 13

The Robeco Groep N.V.’s Supervisory Board consists of nine

persons: four supervisory directors A, four supervisory

directors B and one chairman. There are currently three

vacancies. The chair cannot be held by a supervisory

director B or by an employee of Rabobank Nederland.

Supervisory directors A cannot be or have been supervisory

directors B, nor can they be employees of Rabobank

Nederland. The General Meeting of Shareholders appoints

the supervisory directors and is authorized to dismiss any

supervisory director at any time. Supervisory directors will

be appointed on the basis of a binding proposal consisting

of at least two candidates, formulated by the Supervisory

Board. The Supervisory Board is structured in such a way

Corporate & fund governance

14 Annual Report 2009 Robeco Groep N.V.

that it can satisfactorily fulfill its tasks and that its members

can operate critically and independently of each other,

the Management Board and any other participating

interests. It should be noted that two of the supervisory

directors B are employed by Rabobank Nederland. In line

with the principle of the Code, each Robeco Groep N.V.

supervisory director is able to assess the general overall

policy and has the necessary expertise to fulfill his task. The

Supervisory Board meets the Code’s recommendation to

have at least one financial expert as supervisory director;

please refer to the short CVs of the supervisory directors in

the section General Information. In order to get a proper

insight into Robeco Groep N.V. and its activities, newly

appointed members of the Supervisory Board follow a

customized introduction program. All members of the

Supervisory Board also meet the recommendation on the

maximum number of supervisory directorships at Dutch

listed companies (please refer to the information regarding

supervisory directors in the section General Information)

and all the supervisory directors (except for Messrs.

Bruggink, Ten Cate and Van Schijndel ) are independent

within the meaning of the Code. In accordance with the

Articles of Association and the recommendation of the

Code, the Supervisory Board has drawn up a retirement

schedule. According to this schedule, supervisory directors

should, in principle, resign on the day of the General

Meeting of Shareholders four years after they were

appointed. Reappointment can take place with immediate

effect but only after careful consideration and not if the

person involved has reached or will reach the age of 72 in

that year. In contrast to the recommendation of the Code,

no maximum term is applied for supervisory directors. The

company publishes the retirement schedule on its website.

In close consultation with and after approval by the

Supervisory Board, the General Meeting of Shareholders

appoints a chairman and one of the supervisory directors

B as vice chairman. As mentioned above, the chairman

may not be a supervisory director B or an employee of

Rabobank Nederland. The chairman chairs the meetings

of the Supervisory Board and ensures that the Supervisory

Board functions satisfactorily. Furthermore, the chairman

of the Supervisory Board has regular contact with the

CEO on all issues relating to the responsibilities of the

Supervisory Board. The company secretary assists the

chairman of the Supervisory Board with the actual

organization of Supervisory Board meetings. In 2004 a

presidium was formed consisting of the chairman and the

vice chairman of the Supervisory Board. The vice chairman

is a supervisory director B who, in contrast to a supervisory

director A, may be an employee of Rabobank Nederland.

The CEO, in particular, keeps the presidium informed and

discusses issues with them. Prior to the meetings of the

Supervisory Board, the Audit & Compliance Committee and

the Nomination, Remuneration & Corporate Governance

Committee, the items on the agenda are discussed with

the presidium. The Supervisory Board has appointed

an Audit & Compliance Committee and a Nomination,

Remuneration & Corporate Governance Committee

from among its members. In conformity with the Code’s

recommendations, the two committees are not chaired by

the chairman of the Supervisory Board. Both committees

consist of three persons (see “General Information”).

The Audit & Compliance Committee, the Nomination,

Remuneration & Corporate Governance Committee and

the Investment Committee (as per 1 January 2010) have

taken on tasks recommended by the Code. The Report of

the Supervisory Board gives details about the composition

of the committees, the number of meetings and the main

04 3

Corporate Governance

15Corporate Statements 2009

items discussed in these meetings. In the opinion of

the Management Board there were no conflicts of interest

or semblance thereof between the company and the

members of the Management Board in 2009.

The remuneration for supervisory directors is agreed on at

the General Meeting of Shareholders. This remuneration is

not linked to the company’s results. The notes to the annual

financial statements contain the information required by

Dutch law (articles 2:383c through 2:383e of the Dutch

Civil Code) on the level and structure of the remuneration

for each supervisory director. The supervisory directors of

Robeco Groep N.V. do not receive shares and/or rights to

shares in the company as remuneration. The company does

not grant loans or guarantees to its supervisory directors.

Shareholders and the General Meeting of ShareholdersEach year within six months of the close of the financial

year, the General Meeting of Shareholders of Robeco Groep

N.V. is held in Rotterdam. At this meeting the reports of

the Management and Supervisory Boards are discussed,

the annual financial statements are approved/adopted and

decisions are taken on the proposed dividend and other

items on the agenda. The minutes of the General Meeting

of Shareholders are made available to the shareholder

within three months of the meeting, in accordance with

the Code’s recommendations. As Robeco Groep N.V. has

only one shareholder, the recommendations of the Code

relating to proxy voting are irrelevant. The company does

follow the other recommendations of the Code relating

to dividend and discharge. The Code’s recommendations

on the supply of information to the General Meeting of

Shareholders on price sensitive information or analysts’

reports do not apply, as Robeco Groep N.V. is not a listed

company. Finally, the recommendations relating to

the responsibilities of institutional investors do not apply

to Rabobank Nederland in its capacity as shareholder of

Robeco Groep N.V.

Robeco does pursue an active voting policy for most of its

investment funds and institutional mandates, on the basis

of which, voting rights are exercised on the underlying

stocks. For more information on this subject, please see

the company’s website and the Chapter Responsible

Investing & Corporate Responsibility of this report.

Financial reportingThe Management Board is responsible for the quality and

completeness of the published financial reports and the

Supervisory Board ensures that the Management Board

takes this responsibility. Each year at the General Meeting

of Shareholders, the external auditor is commissioned

to audit the annual financial statements, on the

recommendation of the Supervisory Board.

The external auditor reports his findings to the shareholder,

the Supervisory Board and the Management Board. Robeco

Groep N.V. complies with the Code’s recommendations

relating to internal and external auditors. Robeco Groep

N.V.’s annual financial statements are published on

the company’s website.

16 Annual Report 2009 Robeco Groep N.V.

Fund Governance

Fund GovernanceRobeco is committed to operating its fund-management

activities in a fair and responsible manner; that is in the

best interests of its customers. Several years ago, Robeco

adopted its own principles on fund governance in which it

addresses how conflicts of interest in its fund-management

activities should be handled.

In 2008, the Dutch Fund and Asset Management

Association (DUFAS) established a regulatory framework

on fund governance and Robeco’s principles were used as

a basis for this industry standard. This framework has now

been formally established as an effective self-regulatory

industry standard.

Robeco subscribes to the DUFAS principles and has

integrated them into its own principles on fund governance.

These principles, which also describe a number of potential

conflicts of interest, have been published on www.robeco.

com/corporate information/corporate governance.

MonitoringCorporate Compliance monitors these principles by

performing regular dedicated examinations in which

one or more potential conflicts of interest are reviewed.

The approach used for these examinations is divided

into three phases.

1. The selected potential conflict of interests is described

and the impact on the parties involved (fund/

participants versus fund-management company)

is analyzed. The measures and techniques that

can be used to manage this conflict of interests are

documented.

2. The international laws and regulations applicable

in a number of European countries and the United

States of America are reviewed with respect to these

types of conflicts of interest. Regulatory concepts

supported by industry networks such as IOSCO, EFAMA

and DUFAS are also taken into account. This review

provides us with a good insight into international

best practice.

Subsequently, the practices in place in Robeco’s

related business lines are reviewed. For practical

reasons, priority is given to Robeco’s Dutch and

Luxembourg-based funds.

3. Finally, Robeco practices are compared with

international best practice and legal frameworks.

On the basis of this comparison, Robeco’s principles

are assessed in terms of their content, implementation

and level of compliance.

Results of the examinationsCorporate Compliance has reported the outcome of these

examinations to the Audit and Compliance Committee.

The examination conducted in the course of 2009 dealt

with securities-lending transactions as an area of potential

conflicts of interest. The general conclusion of this

examination was that Robeco adheres to its principles

on securities lending as described in Robeco’s Principles

on Fund Governance.

04 5

17Corporate Statements 2009

18 Annual Report 2009 Robeco Groep N.V.

Robeco, established in Rotterdam in 1929, offers

investment products and services to institutional and

private investors worldwide. Assets under management

amounted to EUR 135 billion as of 31 December 2009.

Robeco advocates responsible investing. Environmental,

social and governance factors are integrated into the

investment processes, and there is an exclusion policy

in place. Robeco makes active use of its voting right and

enters into dialogue with the companies in which it invests.

The product range encompasses equity and fixed-

income investments, money-market funds and alternative

investments, including private equity, hedge funds and

structured products. The various strategies are managed

from Rotterdam (head office), Paris, Zurich, Boston,

New York and Hong Kong.

To service institutional and business clients, Robeco has

offices in Bahrain, Belgium, mainland China, Germany,

France, Hong Kong, Japan, Korea, Luxembourg, the

Netherlands, Singapore, Spain, Taiwan, the United States

and Switzerland. Through SAM Group Robeco also has a

sales office in Australia. Robeco has a license to operate as

a bank in France and the Netherlands, which enables it to

sell its products directly to private clients in those countries.

Robeco holds its interests through fully owned subsidiaries

or branches.

Robeco now holds a 100% interest in – amongst others –

Corestone (Zug, Switzerland), Harbor Capital Advisors

(Chicago, USA), SAM Group (Zurich, Switzerland), Robeco

Investment Management, Inc. (RIM, Boston and New

York) and Transtrend (Rotterdam, the Netherlands).

05 1 Furthermore, Robeco holds a 51% interest in Robeco Teda

(Tianjin) Investment Management Co Ltd. (Tianjin, China),

a 49% interest in Canara Robeco Investment Management

(Mumbai, India) and a 40% interest in AIM Trading N.V.

(Rijmenam, Belgium).

Robeco is part of Rabobank Group, one of the few privately

owned banks in the world with the highest credit ratings

from Moody’s and Standard & Poor’s. Furthermore, within

the banking sector, Rabobank is one of the global leaders in

terms of corporate social responsibility and sustainability.

The Management Board

Management Board

Report of the Management Board – Robeco Profile and key figures

19Corporate Statements 2009

Assets under Management

EUR x billion

2005

622.8

2006 2007 2008 2009

657.5

819.6

888.9

512.2

Operating income

EUR x million

2005

233.6

2006 2007 2008 2009

221.0

276.6 270.2

–15.8

Operating result

EUR x million

Net result

EUR x million

Key figures

2005

152.0

2006 2007 2008 2009

193.0 200.2

174.5

–13.3

2005

131.6

2006 2007 2008 2009

141.7145.8

110.7

134.9

Management Board

20 Annual Report 2009 Robeco Groep N.V.

Bailing out the economyAlthough it is too soon to draw firm conclusions, 2009

may very well go down in history as the year in which the

worst recession since the 1930s came to an end. In the

first few months of the year, the economic outlook was still

very bleak - the economy had ground to a halt, industrial

production plummeted and it was extremely difficult to

obtain bank loans as the capital markets were frozen.

Concerns about the possibility of widespread bankruptcies

and mass unemployment caused companies to reduce

inventories on a massive scale and cut back production.

Fortunately, the situation turned out better than expected.

This was largely attributable to the decisive action taken

by central banks and governments, in the form of highly

stimulative policies. In the second half of 2009, global

economic growth exceeded expectations, whereas inflation

showed a downward trend. By the end of the year, the

decline in housing prices in the United States appeared to

have come to a standstill.

Equity markets rallyEquity markets got off to a very poor start. By the time

markets hit their lows on 9 March 2009, the Euro Stoxx

50 had lost 26% and the S&P 500 had plunged 25%.

Thereafter, the situation took a turn for the better. Several

reports on first-quarter corporate earnings turned out

to be better than anticipated. Capital markets started

to open up again. Companies were able to refinance

by issuing corporate bonds. Although some concerns

remained, stock prices recovered. Over the year as a

whole, the MSCI World Index gained a handsome 27%.

However this figure was surpassed by some considerable

margin by the performance in emerging markets: the

MSCI Emerging Markets Index (net return) soared by 73%.

At the end of the year, average stock-market valuations

were neutral.

Government bonds suffer after a flight to safety in 2009Government-bond yields showed a mixed picture over

the course of the year under review. They rose in the first

quarter, especially in the United States. This was partly

a correction following the bond rally of the last few months

of 2008, and also partly driven by worries about the

enormous supply of government bonds. However, the US

10-year yield took a nosedive following the Federal Reserve

Bank’s historical announcement in March that it would

purchase US Treasuries to support lending to consumers

and companies.

Later on in the year, government bonds came under

pressure again. Several positive reports on the economy

boosted optimism that the worst of the economic crisis

was over. As a result, risky assets such as stocks and credits

recovered. The situation was made worse by the fact that

significant fiscal and monetary stimulus pushed up long-

term inflation expectations, and the market had trouble

absorbing the new supply of US government bonds.

05 3

Chapter 1Market environment

21Corporate Statements 2009

Halfway through the year, long-term interest rates

started to decline again. The large supply of liquidity from

central banks pushed returns on cash to levels close

to zero, causing investors to turn to bonds. Despite this,

in December, US Treasuries were hit by favorable US labor-

market data, which supported investors’ belief in a global

economic recovery.

On balance, German ten-year bond yields rose from 2.96%

to 3.39% in 2009, while US ten-year Treasuries were hit

even harder, as yields surged from 2.84% to 3.84%.

Record issuance of corporate bondsThe corporate-bond market showed a strong rally.

Many companies were able to issue new bonds, making

2009 a record year for non-financial corporate issuance.

The Barclays Capital Euro Corporate Index gained 16%.

High-yield bonds performed even better. The benchmark

used by Robeco European Currencies High Yield Bonds

(EUR)1, for example, rocketed by 16%. Both institutional

and private investors started to invest in high yield again.

After the summer, the market was dominated by a large

number of bond issues, including issues by an increasing

number of low-rated companies. As a result, the number

of bankruptcies declined, boosting sentiment among

investors.

1 Barclays Capital Pan-European High Yield Corporate ex Financials 2.5% Issuer Constraint (hedged into EUR).

22 Annual Report 2009 Robeco Groep N.V.

Robeco’s ambition for 2005-2009 was to be a leading

international asset manager with a strong pan-European

base and prominent operations in the US, which

serves its clients by delivering best-in-class asset-

management capabilities in the major financial centers

and selected emerging markets worldwide. The main

strategic objectives in the past years were to strengthen

selected investment capabilities; optimize Robeco’s

global footprint; increase efficiency; and strengthen

Robeco’s position in the field of responsible investing.

These objectives have been realized to a great extent

(see below). In September 2009 Roderick Munsters

succeeded George Möller as Robeco’s CEO. Robeco’s

strategy for the coming years (see Robeco in 2010) was

established during a strategy review in Q4 of 2009 and

Q1 of 2010.

Strengthen selected investment capabilitiesIn the past years Robeco has strengthened several

investment capabilities, including its Emerging Markets

team and especially its sustainability investing capabilities;

its acquisition of SAM in 2006 was a major development in

this area. In 2007, Corestone Investment Managers AG, a

Swiss-based and independently operating asset manager,

was established. Corestone manages multi-discipline

open-architecture portfolios for institutional investors and

is an important feature of Robeco’s fiduciary-management

proposition. In 2009 Robeco transformed its sector funds

into theme funds, converted Rolinco into a pure thematic

growth fund and strengthened its Global Equities and

Credits capabilities.

Theme funds and Rolinco

Robeco believes that investing in themes is the best way to

benefit from the long-term changes occurring throughout

the world. This is the reason why Robeco transformed its

sector funds into theme funds at the end of 2009. Investors

in sector funds often end up with exposure to subsectors

that have very little to do with the underlying theme. One

example of this is the infrastructure theme. In the past

investors simply bought an industrials sector fund to exploit

the prevailing trend. The problem is that this included

positions in subsectors like employment agencies and

airlines, which in Robeco’s opinion are not directly relevant

to the infrastructure theme. This undesirable side effect can

be eliminated if investors buy into pure themed funds. The

conversion of our sector funds to themed funds will provide

our clients with a wide range of options, that enable them

to profit from long-term trends in a focused way. The global

equity growth fund Rolinco started to take a pure thematic

approach in 2009. It invests in the Robeco theme funds

as well as in the thematic funds managed by SAM out of

Switzerland. By investing in thematic funds, Rolinco offers

a well-diversified approach using thematic investment

strategies and aims to benefit from the long-term trends

and investment opportunities that arisein a continuously

changing world.

05 5

Chapter 2Strategy

23Corporate Statements 2009

Global Equities

Robeco strengthened its Global Equities capability in the

course of 2009. The sector coverage was enhanced by

adding dedicated analysts to the Global Equities team.

The team responsible for managing the Robeco fund,

the Robeco Global Stars high-conviction fund and global

institutional mandates, now consists of four portfolio

managers and ten analysts fully focused on global

developed equity markets. The team has the benefit

of a sound track record over the past five years and an

investment philosophy and process that has proven

itself over this period. Expanding this team will further

strengthen Robeco’s global equities capability.

Credits

Robeco’s Credits team was further strengthened in 2009.

This multi-national team now consists of five portfolio

managers and nine dedicated analysts, most of whom are

senior analysts. Each analyst focuses on a specific sector

and covers the entire rating spectrum within that sector.

All analysts have extensive experience in their sector. The

portfolio managers, who work as a team, are specialized in

either investment grade or high yield. In March 2009 the

range of credits’ strategies was expanded with the addition

of Robeco Investment Grade Corporate Bonds, which

invests in euro-denominated investment-grade corporate

bonds, excluding financials. This new strategy attracted

around EUR 600 million of investor money in the first year

of its existence.

Improve global distribution powerIn the past years, Robeco has opened offices in Tokyo,

Shanghai and Hong Kong, and established Canara Robeco

Asset Management in India. In 2009, Robeco’s efforts to

improve its global distribution power were focused on Asia,

especially Greater China and South Korea.

Greater China

In March, Robeco and TEDA International (Holding)

Corporation Limited announced the establishment of

Robeco TEDA (Tianjin) Investment Management Company.

TEDA International, a newly established company under

Tianjin Investment Holdings, is mandated to hold all the

financial assets under the Tianjin Government and is

responsible for the development of all financial-service

related areas. TEDA International is developing into the

national leader in sustainability as well as a national center

for private-equity investing by fully leveraging its position

in Tianjin, an ambition which is fully endorsed by Chinese

Government. For Robeco, TEDA International is a strong

partner with intimate knowledge of the Chinese market,

based in the heart of Tianjin Municipality. Robeco TEDA

will function as a platform for joint business development

in China, focused on Tianjin. Fund raising for the first

product, the Robeco TEDA Sustainable Private Equity Fund,

is currently underway and a significant close is expected

in Q3 2010. This fund will be the first yuan-denominated

cross-border private-equity fund with a focus on sustainable

investments. It brings together TEDA International’s unique

24 Annual Report 2009 Robeco Groep N.V.

knowledge and expertise in China and the international

clean tech investment expertise of Robeco and SAM.

In addition, Robeco has expanded into the Taiwanese

market, where it is targeting both the retail and the

institutional markets. In an important step forward, the

Securities & Futures Bureau granted Robeco a license to

open a local distribution and client service office, Robeco

Taiwan Ltd., in October 2009. Robeco has teamed up with

Shin Kong Investment Trust, Co., Ltd., part of the renowned

Shin Kong Financial Holding Group to handle the local

distribution of the Luxembourg fund range. In February

2010, the Taiwanese authorities approved a first batch

of five Robeco funds for distribution and Robeco and Shin

Kong are now finalizing the last administrative issues before

the implementation of Robeco’s retail distribution strategy

in Taiwan can commence in earnest.

On the institutional front, much progress was made in

2009. Robeco currently advises on five white-label products

for Taiwanese clients, based on capabilities such as

Emerging Markets, and Consumer Trends. The first offshore

mandate based on Robeco’s Indian equities capabilities

was realized through a China-India mandate that Robeco

advises for one of its local partners. A dedicated advisory

service team has been set up in Robeco’s regional head

office in Hong Kong to service Robeco’s Taiwanese advisory

partners.

South Korea

In August 2009 Robeco opened a representative office in

Seoul, South Korea, which operates under Robeco Japan’s

supervision. Robeco has been active in the Korean Market

since 2006 and these activities were increased at the end of

2007. The local team focuses on both institutional and B2B

clients. Robeco’s presence in Korea enables the company

to further enhance its relationship with the prestigious

institutional clients that it has gained over the years,

including a large bank and the National Pension Service.

Having a local presence also makes it easier to expand our

institutional clientele, and to further develop distribution

relationships for our top products with leading Korean

asset-management and securities companies. In April 2009

Korea Investment Corporation, South Korea’s sovereign-

wealth fund, awarded a US largecap value mandate to

Robeco Japan/Korea. In November 2009 a prestigious

distribution deal was formalized with Korea’s largest

independent asset-management company, Mirae Asset.

A specially tailored vehicle has been set up to give Korean

institutional investors direct exposure to Transtrend’s

Diversified Trend Program. In January 2010 this vehicle was

amongst the first hedge funds, being the only CTA in the

group, to receive formal approval from the Korean Financial

Regulator FSS for direct on-shore distribution.

05 7

Report of the Management Board – Strategy

25Corporate Statements 2009

Responsible Investing On 1 February 2010 Robeco introduced a comprehensive

policy on Responsible Investing (RI). An important pillar of

this policy is the integration of environmental, social and

governance (ESG) criteria into our investment processes.

We believe that this will add value by improving

the long-term risk-return profile of our clients’ portfolios.

The implementation of Robeco’s RI policy follows thorough

consultation with clients and years of research. For Robeco,

RI consists of five interrelated elements:

1. Active ownership (constructive dialogue and voting);

2. Transparency about risk, return and costs;

3. Sustainability theme investments;

4a. ESG integration;

4b. Exclusion policy;

5. Corporate Responsibility.

You can find more detailed information in the chapter

about Responsible Investing.

Optimizing organizational efficiencyAt the end of 2008, Robeco launched a program

(Top Shape) aimed at creating a more efficient

organization. Virtually all the initiatives relating to this

program had been realized by the end of 2009; some

outsourcing measures will be completed in 2010.

Top Shape will ultimately result in an annual saving of

EUR 78 million in operational costs and a more streamlined

and agile organization.

26 Annual Report 2009 Robeco Groep N.V.

05 9

In October 2008, Robeco launched a program

(Top Shape) to increase Robeco Group’s cost-effectiveness.

The decision to increase cost-effectiveness was made in

the first half of 2008, after a peer-group comparison proved

that our overhead costs are high compared with those of

our international competitors. So far, the execution of this

program has been successful. The Management Board

thanks the Works Council for the constructive cooperation

in particular with respect to the efforts in the context of

Top Shape.

The Management Board acts on the basis of shared

responsibility on the understanding that all members have

their own focus areas, per 1 March as follows.

Investments activities are headed by Hans Rademaker.

This includes equity, fixed-income, money-market

investment and securities lending activities in Europe,

the US (Robeco Investment Management) and Hong Kong.

Hans Rademaker is responsible for Pension Solutions and

Responsible Investing too.

All sales and marketing activities are concentrated in

Sales & Marketing, headed by Hester Borrie. Concentrating

all the sales and marketing activities increases client focus

and efficiency, stimulates cross-border cooperation and

improves the organization’s capacity to translate client

demand into product specifications for the Investments

division.

All IT and operating and support activities are grouped

together under Leni Boeren, the Chief Operating Officer.

Consolidation of all these operations creates a strong

focus on delivery. A sound infrastructure will give Robeco

a firm base enabling the company to benefit from the

consolidation opportunities within the asset-management

industry. Leni Boeren is also responsible for RIM, SAM and

the private equity activities.

Constant Korthout is the CFO, he is also responsible

for HCA, Robeco Sage, Robeco France and Canara Robeco.

Roderick Munsters, the CEO and Chairman, is also

responsible for product management and Transtrend.

Subsidiaries and joint ventures associates

Robeco Direct N.V.

Robeco’s direct distribution channel. In the Netherlands,

the bank serves approximately half a million retail clients

via Internet and telephone, and offers a wide range of

financial products and services which include mutual funds,

savings products, mortgages, insurances and brokerage

services. Robeco Direct also has a 100% subsidiary in

France: Banque Robeco SA.

AIM Trading N.V.

Belgium-based systematic high-frequency data currency

trader, that uses quantitative models to determine its

trading strategy (40% stake).

Chapter 3Organization

27Corporate Statements 2009

Canara Robeco Asset Management Company Ltd.

Joint venture with Canara Bank, one of the largest banks

in India (49% stake). Canara Robeco’s assets under

management amount to around EUR 1.3 billion

(at 31 December 2009).

Corestone Investment Management A.G.

Swiss-based independently operating investment

manager, Corestone manages multi-discipline open-

architecture portfolios for institutional investors

(100% stake).

Harbor Capital Advisors Inc.

Chicago-based Harbor Capital Advisors offers a family

of mutual funds through selecting and monitoring best-

of-breed external managers. HCA provides management

services to Harbor Funds, a mutual-fund complex,

and to institutional segregated accounts. HCA’s assets

under management amount to around EUR 33.9 billion

(at 31 December 2009).

Robeco Teda (Tianjin) Investment Management Co. Ltd

Joint venture with TEDA International Holding Corporation

Limited (51% stake), based in Tianjin, China. TEDA

International, a newly established company under Tianjin

Investment Holdings, is mandated to hold all the financial

assets under the Tianjin Government and is responsible

for the development of all financial service related

areas. TEDA International, the financial holding arm of

the Tianjin government, is developing into the national

leader in sustainability as well as a national center for

private equity investing by fully leveraging its position in

Tianjin, an ambition which is fully endorsed by the Chinese

Government.

SAM Group Holding AG

SAM is a Swiss based global investment boutique

focused exclusively on Sustainability Investing. The firm’s

offering comprises asset management, indexes and clean

tech private equity. SAM partners with Dow Jones Indexes

and STOXX Ltd. in the publication and development of

the Dow Jones Sustainability Indexes (DJSI). As of

31 December 2009, SAM’s total assets amount to

EUR 10.3 billion (100% stake).

Transtrend B.V.

Rotterdam-based research-driven and system-based

managed-futures trader, with track record going

back to 1992 (100% stake). Transtrend’s assets under

management amount to around EUR 6 billion

(at 31 December 2009).

28 Annual Report 2009 Robeco Groep N.V.

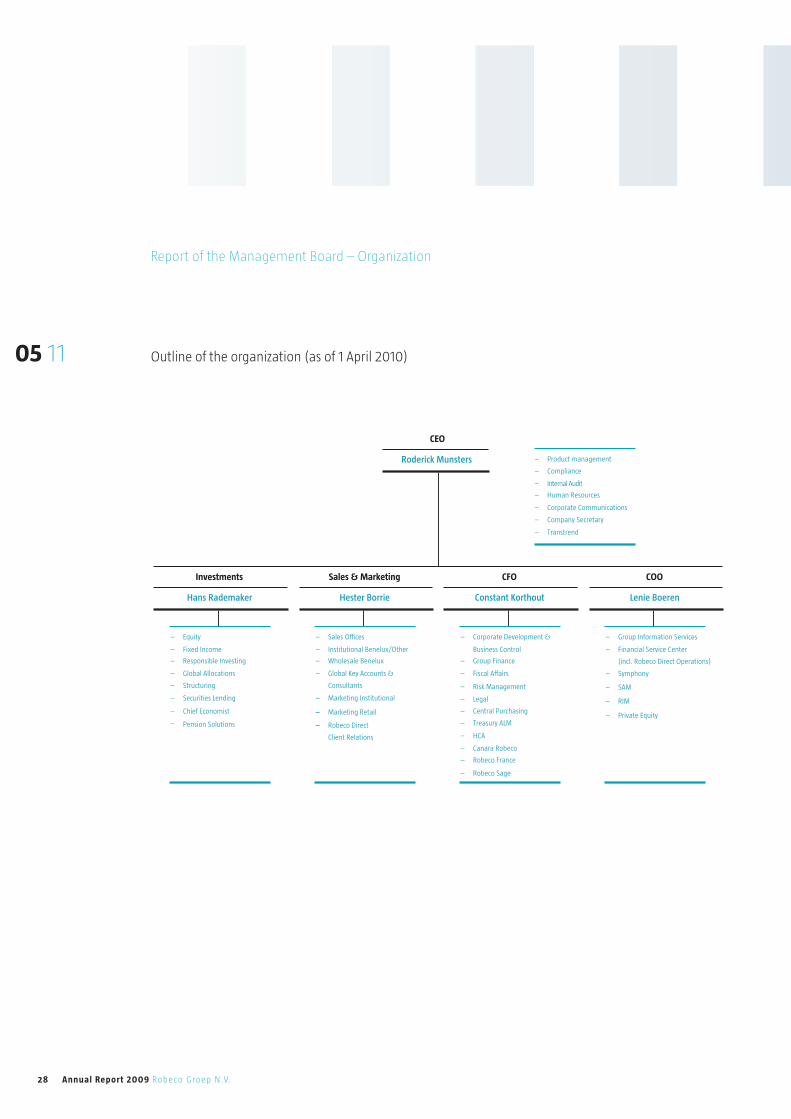

05 11 Outline of the organization (as of 1 April 2010)

CEO

Roderick Munsters – Product management

– Compliance

– Internal Audit

– Human Resources

– Corporate Communications

– Company Secretary

– Transtrend

Investments

Hans Rademaker

– Equity

– Fixed Income

– Responsible Investing

– Global Allocations

– Structuring

– Securities Lending

– Chief Economist

– Pension Solutions

Sales & Marketing

Hester Borrie

– Sales Offices

– Institutional Benelux/Other

– Wholesale Benelux

– Global Key Accounts &

Consultants

– Marketing Retail

– Marketing Institutional

– Robeco Direct

Client Relations

CFO

Constant Korthout

– Corporate Development &

Business Control

– Group Finance

COO

Lenie Boeren

– Group Information Services

– Financial Service Center

(incl. Robeco Direct Operations)

– Symphony

– SAM

– RIM

– Private Equity

– Fiscal Affairs

– Risk Management

– Legal

– Central Purchasing

– Treasury ALM

– HCA

– Canara Robeco

– Robeco France

– Robeco Sage

Report of the Management Board – Organization

29Corporate Statements 2009

Chapter 4Investment performance

Group performancePerformance is dependent on general market

developments and on the outperformance and

underperformance of the different investment programs.

Market developments are covered in detail elsewhere in

this report. At group level, in 2009, 73% (2008: 44%) of

the assets under management outperformed compared

to the relevant benchmark.

Equity:

A very positive year both in absolute and relative terms

The year 2009 was a very positive year for equity

investments. At group level, 89% of equity investments

outperformed their benchmark on a gross-of-fee basis.

At business-line level, the percentage of outperforming

equity assets was 81% for Mainstream Investments

Rotterdam, 100% for Mainstream Investments Gestions,

86% for Mainstream Investments RIM, 98% for HCA, 89%

for SAM and 88% for Canara Robeco Asset Management.

The Harbor International Fund, the largest Robeco

Group fund (EUR 18.6 billion) added another year of

outperformance to its very impressive long-term track

record. The excess return versus the benchmark was

6.0% gross of fees. The Harbor Capital Appreciation Fund

outperformed by 4.1% over 2009.

The Robeco fund outperformed its benchmark by

3.8%, Rolinco by 2.0% and Robeco Emerging Markets

Equities by 7.2%. Robeco European Equities achieved an

outperformance of 2.0% and Robeco Chinese Equities

realized an excess return of 5.7% over 2009.

The two largest products managed in Boston by Main-

stream Investments RIM, BPAM Large Cap Value and

BPAM Premium Equity outperformed their benchmarks by

5.9% and 11.2% respectively.

The two largest funds managed by SAM both outperformed

the MSCI World Index. SAM Sustainable Water Fund

realized an excess return of 8.5% while SAM Smart Energy

Fund achieved an outperformance of 44 % over 2009.

Fixed Income:

Difficult year for Lux-o-rente and Rorento;

high absolute returns for High Yield

Most Robeco fixed-income products generated a positive

absolute return in 2009, 46% of the assets outperformed

the benchmark. Over a three-year period this figure is

41%. Robeco Lux-o-rente had a difficult year; its absolute

return was –1.6%, underperforming the benchmark by

2.4%. Rorento realized an excess return of –1.3% over

2009. Robeco All Strategy Euro Bonds outperformed the

benchmark by 1.5%. HCA Bond Fund achieved an excess

return of 8.1%.

Absolute returns for the high-yield funds are high; the

absolute return for Robeco High Yield Bonds was 53.0%, on

a relative basis the fund underperformed the benchmark

by 1.3%.

30 Annual Report 2009 Robeco Groep N.V.

Alternatives:

Negative results for Transtrend; positive returns for Sage

Transtrend’s Enhanced Risk USD had a very difficult year

with a performance of -11.3% net of fees. Robeco Multi

Market Bonds (which are largely invested in a Transtrend

product) were affected by these results. The hedge fund

of funds Robeco Sage Capital International realized an

absolute return of 12.0% net of fees over 2009.

Returns of Robeco´s flagships

In order to highlight the general developments in

the market in 2009, an overview of the absolute returns

of Robeco´s flagships is given in the table below.

The table shows the gross-of-fee absolute returns of

the most important funds (net of fees for alternatives)

arranged according to investment type and assets under

management. The excess returns indicated are the out- or

underperformance of the fund versus its benchmark.

* As of 31 December 2009** Returns in USD*** No appropriate benchmark available

05 13

Flagship StrategyAuM

in bn EUR*

Absolute Return

(in currency) Excess return

Harbor International Equity - Large Cap Value 18.6 39.7** 6.0**

Harbor Capital Appreciation Equity - Large Cap Growth 6.2 42.8** 4.1**

Robeco Equity - Global 4.1 31.5 3.8

Robeco Emerging Markets Equities Equity - Emerging Markets 2.2 85.4 7.2

BPAM Premium Equity composite Equity - Premium Equity 1.4 33.1** 11.2**

SAM Sustainable Water Equity - Global Sustainability 1.2 36.7 8.5

Robeco Emerging Stars Equities Equity - Emerging Markets Focus 0.8 99.9 15.6

Rolinco Equity - Thematic Investing 0.7 34.9 2.0

Harbor Bond Fixed Income - US 4.3 14.5** 8.1**

Robeco Lux-o-rente Fixed Income - Quantative Global 2.7 -1.6 –2.4

Rorento Fixed Income - Global 1.9 4.8 –1.3

Robeco High Yield Bonds Fixed Income – Global High Yield 1.7 53.0 –1.3

Robeco Euro Cash Fixed Income - Money Market 1.5 1.2 0.5

Transtrend Enhanced Risk USD Alternative Investments – Diversified Trend Program 3.3 –11.3** ***

Report of the Management Board – Investment performance

Performance of Robeco’s flagships

31Corporate Statements 2009

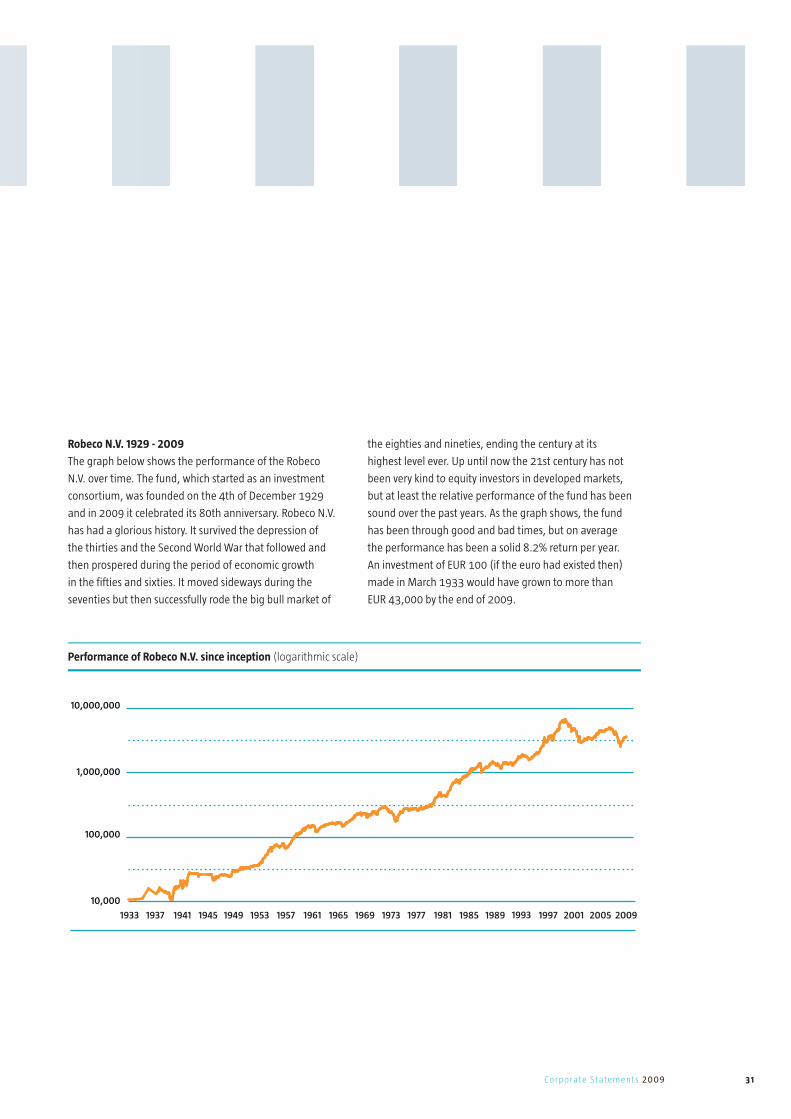

Robeco N.V. 1929 - 2009

The graph below shows the performance of the Robeco

N.V. over time. The fund, which started as an investment

consortium, was founded on the 4th of December 1929

and in 2009 it celebrated its 80th anniversary. Robeco N.V.

has had a glorious history. It survived the depression of

the thirties and the Second World War that followed and

then prospered during the period of economic growth

in the fifties and sixties. It moved sideways during the

seventies but then successfully rode the big bull market of

the eighties and nineties, ending the century at its

highest level ever. Up until now the 21st century has not

been very kind to equity investors in developed markets,

but at least the relative performance of the fund has been

sound over the past years. As the graph shows, the fund

has been through good and bad times, but on average

the performance has been a solid 8.2% return per year.

An investment of EUR 100 (if the euro had existed then)

made in March 1933 would have grown to more than

EUR 43,000 by the end of 2009.

1933 1937 1941 1945 1949 1953 1957 1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009

10,000,000

1,000,000

100,000

10,000

Performance of Robeco N.V. since inception (logarithmic scale)

32 Annual Report 2009 Robeco Groep N.V.

05 15

Global business development

EUR x billion

AuM at opening date

Investment result

Net cash flow

Other gains / losses

AuM at closing date

Total

110.7

19.2

7.5

– 2.5

134.9

2009

Retail

52.9

10.8

3.9

– 0.5

67.1

Institutional

57.8

8.4

3.6

– 2.0

67.8

Total

145.8

– 29.1

0.6

– 6.6

110.7

2008

Retail

71.8

– 19.5

1.4

– 0.8

52.9

Institutional

74.0

– 9.6

– 0.8

– 5.8

57.8

Chapter 5Business development 2009

Growth of assets under management

Robeco’s assets under management showed a growth

of 21.9% in 2009. This increase resulted from a positive

net investment result of EUR 19.2 billion and a net cash

inflow of EUR 7.5 billion. The remarkable recovery in the

financial markets in 2009 affected Robeco’s assets under

management considerably. The investment result was

negatively affected by a EUR 1.2 billion loss caused by the

depreciation of the US dollar. Annual dividend payments

and interest distributions as well the fact that a fee-

generating agreement for Robeco CDO VII was unwound at

maturity, caused a EUR 2.5 billion decline in assets under

management.

Net cash flow

In terms of net cash flow, Robeco saw its best annual

performance ever in 2009. The net cash inflow of EUR 7.5

billion was well diversified over products and continents.

The retail cash inflow was strong in the US, particularly

into the mutual funds of Harbor Capital Advisors. Also in

Europe, cash inflow into retail products was strong but

was negatively affected by the fact that some structured

products were unwound at maturity. The net cash inflow

from European institutional business was strong, with

positive cash inflow particularly in emerging-markets

products. In Europe, managed-futures investment advisor

Transtrend, was able to attract significant net cash

inflow, despite the fact that its Diversified Trend Program

experienced negative returns.

33Corporate Statements 2009

European business development

EUR x billion

AuM at opening date

Investment result

Net cash flow

Other gains / losses

AuM at closing date

2009

79.0

9.8

3.8

– 2.5

90.1

2008

96.5

– 12.5

– 2.4

– 2.6

79.0

In 2009, institutional products generated considerable

cash inflows with Emerging Market Equity, Quant Equity

and High Yield Bonds being the most successful. On the

retail business side, all European wholesale distribution

channels generated substantial inflow into Emerging

Markets Equities and Value Equity in particular. However,

the fact that some structured products including Robeco

CDO VII were unwound at maturity resulted in considerable

cash outflow in 2009. Robeco Lux-o-rente received the

Morningstar 2009 Manager of the Year award in the

Netherlands and Robeco US Premium Equities received

this award in Belgium. These awards highlighted the good

performance of these funds in 2008. Robeco US Premium

Equities contributed well to the inflow that was generated

in 2009. The traditional Dutch equity funds Robeco and

Rolinco also outperformed their benchmarks last year.

Compared with previous years there was hardly any cash

outflow for these equity funds.

Specialty products distributed in Japan generated

significant profitable inflow with the Transtrend product

range, in particular, attracting new investments.

34 Annual Report 2009 Robeco Groep N.V.

05 17 US business development

EUR x billion

AuM at opening date

Investment result

Net cash flow

Other gains / losses

AuM at closing date

2009

30.5

9.0

3.1

0.0

42.6

2008

47.8

– 16.2

2.9

– 4.0

30.5

Harbor Capital Advisors contributed substantial new

investment from clients. The Harbor International Fund

together with the Harbor Bond fund were the main

beneficiaries of the net cash inflow. Harbor International

fund is Robeco’s largest fund (EUR 18.6 billion asstes under

management) and has shown outstanding and stable

performance results. The Harbor Bond fund showed an

excellent outperformance versus its benchmark and with

a net cash inflow of EUR 1.1 billion, this mutual fund had

EUR 4.3 billion in asstes under management by the end of

2009. Robeco Investment Management generated cash

inflow after some difficult years and its overall investment

results outperformed the benchmarks.

Report of the Management Board – Business Development 2009

Rest of the World business development

EUR x billion

AuM at opening date

Investment result

Net cash flow

Other gains / losses

AuM at closing date

2009

1.2

0.4

0.6

0.0

2.2

2008

1.5

– 0.4

0.1

0.0

1.2

Joint venture company Canara Robeco performed well