43

ANNUAL REPORT 2010-11 RGVN (NORTH EAST) MICRO FINANCE LIMITED

AnnuAl report 2010-11

RGVN (NORTH EAST) MICRO FINANCE LIMITED

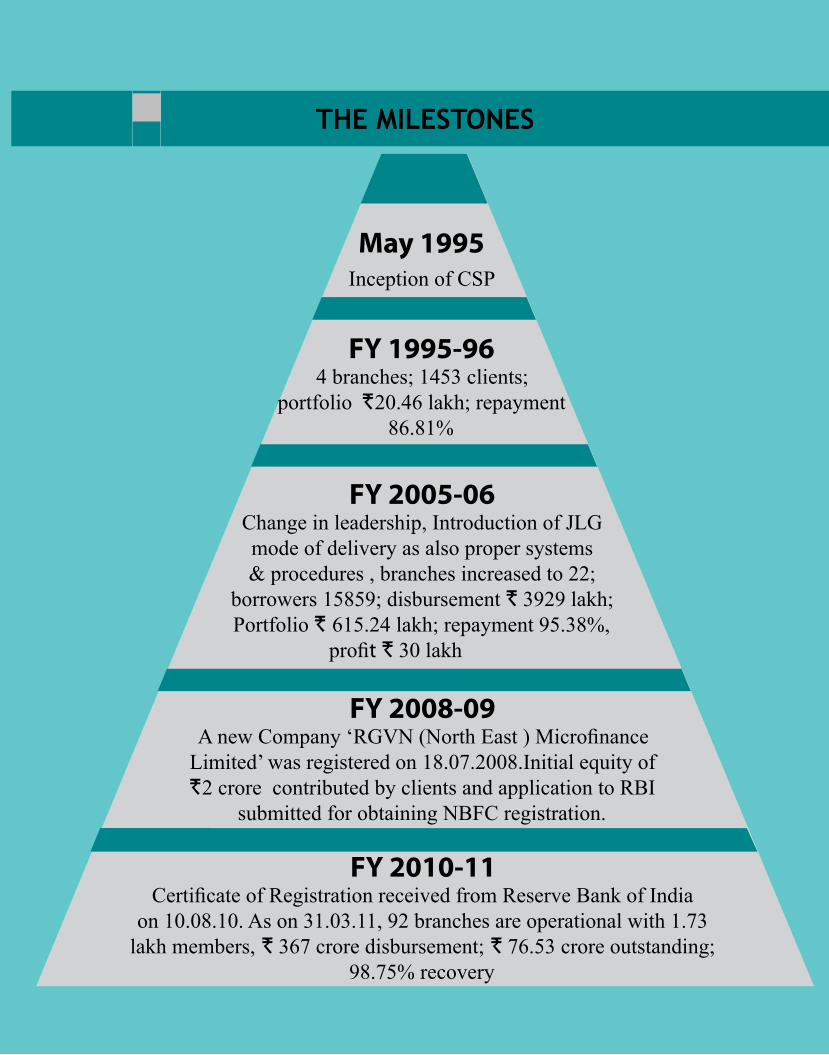

May 1995Inception of CSP

FY 1995-964 branches; 1453 clients;

portfolio R20.46 lakh; repayment 86.81%

FY 2005-06Change in leadership, Introduction of JLG mode of delivery as also proper systems & procedures , branches increased to 22;

borrowers 15859; disbursement R 3929 lakh; Portfolio R 615.24 lakh; repayment 95.38%,

profit R 30 lakh

FY 2010-11Certificate of Registration received from Reserve Bank of India

on 10.08.10. As on 31.03.11, 92 branches are operational with 1.73 lakh members, R 367 crore disbursement; R 76.53 crore outstanding;

98.75% recovery

THE MILESTONES

FY 2008-09A new Company ‘RGVN (North East ) Microfinance

Limited’ was registered on 18.07.2008.Initial equity of R2 crore contributed by clients and application to RBI

submitted for obtaining NBFC registration.

OUR COMMITMENT AND INVOLVEMENT

MISSION

Provide financial and other support services to the underprivileged households in the Northeast to improve their quality of life

VISION

Serving entire North Eastern region and impacting two million lives by the year 2015 and facilitate better access to health, education and livelihood opportunities

VALUES

Good governanceProfessionalismIntegrity & transparencyClient satisfactionCommunity orientation

»»»»»

�

AnnuAl report 2010-11

�

MESSAGE FROM THE CHAIRpERSON

The Financial Year 2010-11 was historic for RGVN (North East) Microfinance Limited since in this year the new Company commenced operating as a full-fledged NBFC after receiving licence from Reserve Bank of India and commencement certificate from the Registrar of Companies, Shillong.

Despite the ‘teething problems’ in view of the disturbances in the microfinance sector and meltdown in the economic scenario across the globe, RGVN (North East) Microfinance Limited achieved a growth of over 40% in its portfolio and significant increase in the client base. A lot of credit for the satisfactory performance goes to the management & staff of the company as well as lenders particularly NEDFi and Dia Vikas who had consistently backed this new entity with loan as well as equity support in order to reach financial assistance to very large number of clients in North East. Immediately after formation of NBFC, it reviewed the human resource practices, developed appropriate HR structure & regularized the existing staff. A strong internal audit team was constituted besides strengthening the credit monitoring system to identify and track stressed accounts on a regular basis. These measures have

already helped in significant reduction in the non performing assets of the company & improved efficiency.

At the end of fiscal 2010-11, upon inheriting the assets and liabilities of the erswhile RGVN-CSP (Society), RGVN(North East) Microfinance Limited has now a network of 92 branches covering 26 districts of Assam, Meghalaya and Arunachal Pradesh, extending services to 1,72,987 members, out of which about 98% are women, disbursing `367 crore (cumulative) with portfolio outstanding of `76.53 crore. The new company is mandated to serve all the eight North Eastern States & committed to reach financial services to 5 lakh clients in next 4 years.

With the business projected to increase significantly, it is necessary to have a strong capital base to leverage loan resources from funders. However, as the company is committed to be client centric & is keen to work for the inclusive growth of its clients, it has decided to seek equity from social investors like Dia Vikas & development institutions like NEDFi/SIDBI/BCDT besides its clients who are willing to back the mission rather than expecting good commercial return. RGVN(North East) Microfinance, has already on cards, a number of development initiatives which include:

Development of in house cadre for financial literacy of all its clients on an ongoing basis;Credit plus services including health, sanitation, education etc;Transparency in operations and adherence to code of ethics including client protection;Ethical collection practices & respect to clients & relief in the event of death of spouse; Livelihood advisory support to its clients;Venture into underserved pockets of Northeast India

I take this opportunity to thank RGVN especially Chairman, Dr. Jayanta Madhab, equity investors and funders viz., NEDFi, Dia Vikas, State Bank of India, Ananya, my colleagues on the Board, Rupali Kalita, Managing Director & her committed team at RGVN(NE)MFL for their excellent cooperation & look forward to their continued support in reaching financial & development services to large underserved segments of NER populace. The coming years should see emergence of RGVN(North East) into a new generation RBI compliant microfinance institution fully committed to service its clients with empathy & efficiency.

(Brij Mohan)

� AnnuAl report 2010-11

Mr. Brij Mohan is the former executive director of the Small Industries Development Bank of India. He is the chairman of Ananya Finance for Inclusive Growth Ltd-a wholesaler in microfinance as well as the chairman of Access Development Services & chairman and Managing Trustee of MicroSave India. He is also Vice- chairperson of Rashtriya Gramin Vikas Nidhi. Mr. Mohan is a director on the Boards of Micro Rating International Ltd -a MF rating institution and Micro, Small & Medium Enterprise Foundation-a UNIDO promoted cluster development group.

THE GOVERNANCE

CHAIRpERSON

Mr. Brij Mohan

DIRECTORS

A Rural Development Banker with more than 20 years of working experience in the banking sector who was instrumental in spreading the outreach of the microcredit wing of RGVN into many pockets of Assam, Meghalaya and Arunachal Pradesh and with the consistent growth in business enabled transformation of the institution into an NBFC. She has been working for empowerment of the less privileged women in rural as well as urban sector through financial intermediation by persistently encouraging them to build up their confidence and to emerge as successful entrepreneurs.

Mr. Deep Joshi

An Indian social worker and NGO activist. Recognised for his vision and leadership in bringing professionalism to the NGO movement in India. Co-founded a non-profit organisation, Professional Assistance for Development Action (PRADAN) of which he was the former Executive Director. Was awarded the 2009 Magsaysay award for Community Leadership for his work for “development of rural communities”, winner of ‘Padmashree’ award of the Government of India in 2010 and member of National Advisory Committee

Mr. K. N. Hazarika

Former Chairman and Managing Director of NEDFi, Guwahati, served the State Bank of India for 33 years. Also associated with NERAMAC Ltd., which is engaged in marketing/processing of agricultural products [not an NBFC].

Chief Executive Officer of Dia Vikas Capital Private Limited, a social venture capital fund supporting microfinance and livelihood institutions in India. Served MicroSave as the Senior Microfinance Specialist. Was a development banker with the Small Industries Development Bank of India (SIDBI) where she was instrumental in the establishment of the SIDBI Foundation for Micro Credit (SFMC).

Dr. Amiya Kr. Sharma

Presently the Executive Director of Rashtriya Gramin Vikas Nidhi (RGVN), Guwahati. An alumnus of Delhi School of Economics, Dr Sharma has taught in various Universities like Tezpur University, Rutgers University, University of Delhi and also served in the Indian Statistical Institute, New Delhi. Dr. Sharma is actively involved in various activities related to the voluntary sector and has assisted in development of many NGOs in the region. At present he holds the position of the Co- Chairman of Sa-Dhan (the Association of Community Development Finance Institutions).

Ms. K.C. Ranjani

Ms. Rupali Kalita

�

AnnuAl report 2010-11

�

The Board of Directors of RGVN (North East) Microfinance Limited take pride and pleasure in compiling and releasing this First Annual Report of the Company for the FY 2010-11.

This fiscal has been a combination of ‘ebbs & tides’ for the organization since many hurdles were crossed paving inroads for a full-fledged NBFC which has been made operational during the year.

Being the largest MFI in the Northeast India, RGVN(NE)MFL with its base in Guwahati, has been serving around 1.73 lakh members through a network of 92 branches in three Northeastern States viz. Assam, Meghalaya and Arunachal Pradesh thereby trying to unleash the potentials of the un-served poor populace of society by playing a catalytic role in supporting the economic growth of the State.

As a premier development financial institutuion in the Northeastern region, RGVN(NE)MFL has played a pro-active role in churning out entreprenuers out of the educated unemployed youth of Assam by providing trainings on various topics through effective and prominent participation in the Employment Generation Programme of Government of Assam.

Human Resource being the core department of an organization, utmost care is taken to pool up qualified and experienced personnel in the respective departments and build managerial skills and capabilities to upgrade talents of the staff and strengthen the organizational structure. Risk Mitigation being a focussed area, the revamped internal audit and audit machinery has been playing the ‘whilstle blower’ role in a planned and structured mode.

The conversion to the much expected NBFC injecting dynamism at the core of the organization to vigorously tap the unexplored opportunites of the Northeast and capitalize on the strengths of the organization through the dedicated staff who have relentlessly worked, has taken the organization forward.

The Board of Directos shall provide adequate support to the entire RGVN(NE)MFL team to identify with the vision/mission statements and through combined efforts, one and all would strive hard and ensure that the organization scales newer heights.

REpORT FROM THE BOARD OF DIRECTORSRGVN (NORTH EAST) MICROFINANCE LIMITED

Number of Branches 92

Number of Districts 26

Total Staff Strength 495

Number of Credit Officers 251

Number of Centres 4,350

Number of Groups 39,077

Number of Members 1,72,987

Cumulative Loan Disbursed [Rin crore] 367.00

Loan Portfolio [R in crore] 76.53

Repayment Rate 98.06%

Portfolio At risk> 60 days 3.33%

Borrower Per Credit Officer 511

Outstanding per Credit Officer [R in lakh] 30.25

Outstanding per branch [R in lakh] 83.19

Operational Self Sufficiency 117%

Financial Self Sufficiency 107%

Yield on portfolio 26.89%

OPERATIONAL HIGHLIGHTS AS AT THE END OF MARCH 2011

� AnnuAl report 2010-11

The year 2010-11 carries significance in the history of the organization since the transformation process was completed and RBI registration obtained [on 10.08.2010] for operating as a Non Banking Financial Company under the banner ‘RGVN (North East) Microfinance Limited’.

The road to transformation from a department of Rashtriya Gramin Vikas Nidhi [RGVN] known as RGVN(CSP) to an NBFC was not smooth. However, with the relentless efforts put in by the entire team as also guidance provided by the Governing Board members of RGVN, the RBI licence to carry on the microcredit intervention through an NBFC was obtained. A brief of the transformation from a Society to an NBFC is provided hereinunder :

In the year 1995 RGVN, a registered Society pioneering NGO movement in the Northeast, had initiated Micro Finance with a view to reach out to more poor and unbanked people with Revolving Fund Assistance from SIDBI under the title ‘Credit & Savings Programme (RGVN-CSP)’. All the major banks in the Northeast viz. State Bank of India, SIDBI, IDBI, HDFC Bank, Indian Bank, Central Bank, NEDFi etc. have helped RGVN-CSP by providing loan funds for development of microcredit in the area. The mission of RGVN-CSP was to make credit available to that segment of the Society which does not have access to formal credit. RGVN being a non-profit Society, the intention of starting this for-profit operation was to make micro-credit available at the door-steps of the people and at the same time to plant the seeds for a viable Microfinance Institution in the Northeast.

As per mandate of the Governing Board of RGVN, upon receipt of Certificate of Registration,from RBI the Company viz. RGVN (North East) Microfinance Limited has taken over the microfinance portfolio of RGVN-CSP-the erstwhile microfinance programme of RGVN [Society]

on 30.09.2010. As a complementary to banking systems, the Company focuses on providing small doses of credit to the under-priviledged sections of the society. Presently operating in three States of the Northeast – Assam, Meghalaya and Arunachal Pradesh – through a network of 92 branches, covering a clientele of more than 1,29,000 with a member base of 1,72,987, loan outstanding has touched `76.53 crore against a total disbursement of `367 crore [cumulative] as on March 2011. With the growth graph scaling higher year after year, coupled with the back-up provided by well experienced and professional Board of Directors and dedicated staff, this new entity has the pride of being the largest microfinance organization in the Northeastern part of India.

The FY 2010-11 was a challenging year for the microfinance sector because of the prevailing uncertainly for microfinance institutions all over the country with anticipation of siginificant policy change by Government of India and the RBI resulting in reluctance on the part of the lenders to extend support to MFIs. In spite of that, the Company achieved a growth of 40% in its portfolio and significant increase in the client base when most of the other MFIs in the country have been struggling to maintain their portfolio status. A lot of credit for the satisfactory performance goes to funders like NEDFi and Dia Vikas because both the institutions stood by the Company to mitigate the challenges faced in view of its transparent operational policy and excellent past track records.

CHApTER 1 : INTRODUCTION/GENESIS

The Managing Director with the RBI licence

AnnuAl report 2010-11

�

DGM-NEDFi handing over the disursement cheque along with passbook to client

CHApTER 2: DEpTH OF OUTREACH

GAINING MOMENTUM

OFF-THE-SHELF pRODUCTS:

During the year under review, as many as 27 new branches were opened, increasing the total number of branches to 92 at the end of the year. Out of these 27 branches, 25 branches were opened in the State of Assam. It is the first time that a branch has been opened in the State of Arunachal Pradesh at Itanagar. While Shillong, the capital of Meghalaya, was also included in the branch network, efforts will be made to extend the outreach in these two States besides opening outlets in other Northeastern States like Sikkim and Nagaland.

The strategy of branch expansion plan for the year was to open branches in hitherto unexplored areas, bifurcation of branches because of increasing business beyond limit set, increasing the proximity of new branches of the isolated region.

The extension of branch network was supported by opening of new Area Offices. As at the end of March 2011, the number of Area Offices increased to 12. The 12 Area Offices, detailed below, are functioning as an extended arm of Head Office to guide, supervise and monitor a group of branches :

[1] Guwahati-1 [10 branches]

[2] Guwahati-2 [ 8 branches]

[3] Kamrup [11 branches]

[4] Barpeta/Nalbari [9 branches]

[5] Bongaigaon [7 branches]

[6] Goalpara [7 branches]

[7] Dibrugarh/Tinsukia [3 branches]

[8] Jorhat/Golaghat [7 branches]

[9] Sibsagar [5 branches]

[10] Lakhimpur [6 branches]

[11] Tezpur [9 branches]

[12] Nagaon [10 branches]

RGVN started the process of microcredit intervention in the year 1995 with a single mode of operation, i.e., the SHG model. Over a period of time, taking into consideration the desires, aspirations and the capability of its members, it was decided that a bunch of different client-friendly loan products can be introduced for bringing in more clientele under the fold. These technical innovations are also found to be of much practical significance of serving the entire northeast region covering five lakh clients in the next four years and facilitate better access to health, education and livelihood opportunities. Again, being a prominent microfinance organization, RGVN(NE)MFL is committed to issues like women empowerment, entrepreneurship development and a higher standard of living among its beneficiaries so that the level can be maintained in the long-run, the mission decided to operate with a range of products so that the requirements of its member base can be effectively addressed.

The purpose of the loan products introduced can be listed as below:

For meeting the household need,

Smoothening cash flow,

Diversifying income sources by investing in livelihood activities,

Promoting entrepreneurial spirit,

Making an effort to meet certain special cases of cash requirements in events like marriage, education, etc. among the members

� AnnuAl report 2010-11

The following reasons can be cited to comprehend the decisive change of bringing more clientele under our fold :

Delivery mode of our financial services: RGVN(NE)MFL is keen in providing services at the doorstep,making it easy for the clients to avail financial products thus offered.

Our mode and style of repayment: We have weekly/fortnightly and monthly repayment schedules based on the frequency of the cash flow generated. The clients may choose the appropriate style of repayment which also takes care of the seasonal fluctuation in income in productive sectors and the vulnerability aspect of petty trade.

Loan products introduced to meet the clients’ need: RGVN(NE)MFL introduces loan products to meet clients’ household needs, smoothening cash flow, and diversifying income sources by investigating in livelihood activities. The organization also takes adequate care to fulfill the entrepreneurial aspirations of its clients. For this, Entrepre-neurship Development Loan (EDL) and Micro-Enterprise loan(ME) are being provided to graduate clients with good repayment track-record. Also to create the largest possible financial inclusion, RGVN(NE)MFL, through the Joint Liability product (JLG), provides loans to both male and female members of this region so that client cover-age is enhanced.

In order to satisfy the needs of its clients in a systematic manner, steps have been taken to extend loans for personal consumption, education and health, working capital requirements and repayments of costly debt.Being client-centric, our earnest efforts are to ensure that our clientele are benefited through the range of products which are structured based on the client needs.

CREDIT DELIVERY VEHICLES :

1) Self Help Group (SHG): : The number of SHGs formed has increased from 490 in March 2007 to 651 in March 2011. Since the growth is not upto expection, in order to encourage formation of adequate number of SHGs, steps have been taken to enhance the quantum of first cycle loan at par with JLG loan. Besides exhaustive guidelines, workshops in SHG finance is proposed to be held frequently to train the field level employees.

2) Joint Liability Group (JLG): A JLG is formed preferably comprising mostly of 3-5 women having similar income and cash flows. This is the most dominant mode of credit delivery and the number of JLG members which was only 86,365 in March 2010 has increased to as high as 1,22,200 in March 2011. The number of JLGs availing loan has also increased from 22,042 to 33,759 during the corresponding period. The amount disbursed through JLG mode was of the order of ` 117.65 Crore during the year under report as compared to ` 76.35 Crore in the previous year [2009-10]

3) Entrepreneurship Development Loan (EDL): EDL is yet another mode of finance which offers higher quantum of finance of `50,000/- individually with minimum entry amount of loan of `15,000/-. The EDL is provided to clients showing good repayment track record in the last two loan cycles.

4) Micro Enterprise Loan (MEL): Loans are also provided to successful borrowers with proven track record evincing entrepreneurial ability. Loan is provided for income generating activities to persons with appropriate capability who are willing to start their own enterprise. Such EDL/MEL individual loans has increased from 217 in 2007 to 2445 as at the end of March 2011.

5) Employment Generation Mission (Phase-I): The first phase of Employment Generation Mission [EGM] of Govt. of Assam was in the completion stage under which 681 youth were trained in various sectors depending on their experiences and expertise involving `2.58 crore as loan sanctioned. In order to assess the impact of the programme on the beneficiaries, an Evaluation Study was outsourced to a leading Research Body named ‘SPEED’. In their evaluation report, the study team featured their findings and suggestions commenting on overall positive impact of the programme and at the same time, recorded about the need for still higher quantum of finance to satisfy the increasing ‘credit hunger’.

1.

2.

3.

4.

AnnuAl report 2010-11

10

DISBURSEMENT & OUTSTANDING

The average outstanding loan size being even less than ̀ 6,000/- substantiates that RGVN(NE)MFL has served primarily people of small income and a large number of needy people have been assisted out of its limited resources. Activities like animal husbandry as well as handloom & handicraft which are basically rural products involving less investment accounts for 24.47% & 24.10% respectively of total credit Portfolio with petty trade involving 42.96%.

ACTIVITIES FINANCED

LOAN COMMITTEE

CLIENT COVERAGE

The concept of Loan Committee has been developed during the reporting year to ensure speedy disposal of the proposals. The system also helped in appropriate scrutiny of each proposal sanctioned by the Branch Manager. The Committee is made area-wise headed by concerned Area Manager alongwith the Branch Managers on rotational basis and they meet atleast twice in a month.

The efficacy of the system and the satisfaction of our members can be gauged on the basis of increasing number of member borrowers. The number of members which stood at 35,000 as on March 2006 has increased to 1.73 lakh in end March 2011. Similarly the number of active borrowers increased from 15,589 to 1.29 lakh during the corresponding period. During the year under review the number of active borrowers increased by about 28%. as compared to the previous fiscal.

The quantum of deployment of credit increased significantly with growing trust of our members, backed by operational efficiency of staff. The amount of loan disbursed which was a meagre R39.28 crore at the end of March 2006 increased to R367 crore at the end of March 2011. During the year under review the disbursement increased by 44% from R239 crore in March 2010 to R367 crore in March 2011. Correspondingly, the outstanding portfolio increased from R56.55 crore in March 2010 toR76.53 crore as on March 2011.

11 AnnuAl report 2010-11

The year under review is marked by substantial improvement in the recovery rate of loans. Percentage of on-time portfolio has improved from 94.42% in March 2010 to 98.06% at the end of March 2011. There is a corresponding decline in arrear/overdue percentage from 4.18% to 3.37%. The amount of impaired assets over ‘0’ days which was `4.13 crore in March 2010 has come down to `3.72 crore in March 2011. The overall improvement in recovery climate indicates the constant follow-up and monitoring made by the controlling officers and branch staff. The annual monthwise recovery plans of arrear amounts and account according to different time period are

reviewed every month with the Area Managers and quarterly with all Branch Managers and necessary modifications in plans are made. It is worth mentioning that more than adequate provisions have been built-up in relation to impaired assets. As against an arrear/overdue amount of `2.58 crore as at end of March 2011, the amount of bad debt provisions was of the order of `3.07 Crore, registering more than full coverage.

RECOVERY OF LOANS

pARTNERS IN STRENGTH

CApITAL STRUCTURE

RGVN(NE)MFL plays a crucial role in nuturing its clients and providing financial support which has only been made possible by the partnership extended by leading financial institutions by providing timely release of funds, specially during the peak seasons viz. festivities like Bihu, Eid, Diwali, Puja etc. This has, in turn, enabled the organization to support its clients at the hour of need & increase their income level considerably. RGVN (NE) MFL acknowledges the back-up extended by [1] Small Industries Development Bank of India [SIDBI], [2] North East Development Finance Corporation [NEDFi], [3] State Bank of India [SBI], [4] Ananya Finance for Inclusive Growth Pvt.Ltd.[ANANYA], [5] Industrial Development Bank

of India [IDBI], [6] Dia Vikas Capital Pvt.Ltd. [an Indian subsidiary of Opportunity International (Australia)], [7] Central Bank of India[CBI], [8] HDFC Bank, [9] Indian Bank

Having a strong capital base enables an MFI to leverage funds from financial institutions in order to continue with its efforts to serve the clientele. Against this backdrop, RGVN(NE)MFL has made an earnest effort in exploring possibilities of having an equity partnership with both national and international social investors. Also, being a client-oriented organization, it was felt that having clients as stakeholders of the Company would distinguish this organization from other MFIs. Furnished below is the chart reflecting the paid-up/proposed capital against a proposed authorized capital of `25 crore. The subscription of clients were raised through 7 Mutual Benefit Trusts [MBTs] located at Guwahati, Barpeta, Nalbari, Mangaldai, Goalpara, Nagaon and Tezpur. The total number of member shreholders being over 53,300, the allotted amount to clients was `1.03 crore while RGVN made matching contribution of `1.03 crore.

Delegates from International funding organizationbeing felicitated

AnnuAl report 2010-11

12

RGVN(NE)MFL has been rendering financial services to the poor and underprivileged segment of the society through its dedicated and committed workforce which has grown from strength to strength over the years. As on March 2011, the total staff strength stood at 495. The breakup of staff is as below:

The organization has adopted a standard HR Policy and has been following a transparent system of recruitment to build an employee base comprising rural youth with a vision and inclination to work towards the development of the society. The organization has always patronized local youth from BPL and rural background to join hands in its mission of building a strong back-up support team for providing quality services to the poor. At the management and administrative level, RGVN(NE)MFL has been able to pool talent from various professional spheres as well as engage the services of experienced bankers to guide them in orderly growth of the newly formed Company.

RGVN(NE)MFL has always maintained a pro-employee stand and strongly advocates the sharing of the profits earned among its employees as much as with its member -clients. Along with providing employees a conducive work environment, it has also endowed them with various benefits and incentives other than salary in order to safeguard their greater interests. Four salary revisions in six years stand testimony to its pro-employee approach. During the past financial year, albeit the occasional scaling down in operations due to the mishaps in the microfinance sector; RGVN(NE)MFL introduced a revised comprehensive and structured ‘Compensation Package’ effective from January 1, 2011 for its employees. This package was designed in consultation with MicroSave and offers reasonable and competitive compensation to employees. Apart from salary benefits, the package provides non-salary benefits like Provident Fund, Gratuity, Health Cover, Risk Insurance Cover and Group Savings cum Life Cover. An annual incentive christened as Performance Pay is also payable to staff.

Field Staff 356i Credit Officers 251

ii Asst. Branch Managers 15iii Branch Managers 90

Managerial Staff 43i Area Managers 13

ii Head Office Staff 30Support Staff

i General Purpose Staff 96Total Staff 495

HUMAN RESOURCE – AN INSIGHT

Name of shareholdersPaid up capital

` in crore

Proposed Authorized Capital ` in crore

Client/Promoters [paid] 2.11 2.11BCDT [paid] 1.00 1.00SIDBI 6.00Dia Vikas [paid] 3.00 6.00NEDFi 1.50 3.00Agora [sanctioned] 6.00Others 0.89

Total 7.61 25.00

1� AnnuAl report 2010-11

Name of shareholdersPaid up capital

` in crore

Proposed Authorized Capital ` in crore

Client/Promoters [paid] 2.11 2.11BCDT [paid] 1.00 1.00SIDBI 6.00Dia Vikas [paid] 3.00 6.00NEDFi 1.50 3.00Agora [sanctioned] 6.00Others 0.89

Total 7.61 25.00

In order to upgrade the skills of the staff as well as clients, trainings are conducted at regular intervals, as per details furnished below :A) STAFF - INTERNAL

[a] Two-day Initial Orientation programme for newly recruited Credit Officers providing information about the organization and its style of working; [b] Induction Training programme for Credit Officers at the end of the 3-month hands-on training at the field and branch [c] Refresher Course for Area Managers, Branch Managers and Credit Officers is conducted from time to time to improve effectiveness and bring in enthusiasm in performing the jobs assigned.

During FY2010-11, besides a number of Orientation Programme and Induction Training for newly recruited Credit Officers, MICROSAVE imparted Accounts training to the Branch Managers of RGVN(NE)MFL and Internal Audit & Control Training to the Area Managers and Head Office staff.

STAFF WELFARE

TRAINING & CApACITY BUILDINGThe organization endorses the need for quality improvement of its employees through training and capacity building programmes. The Training Cell follows an extensive training calendar with the objective to expose each employee of the Company at least to one training programme once in a year. The training modules for different grades of staff are designed to accommodate both technical as well as soft skills based on the needs and profile of work. These trainings have been instrumental in building the expertise of staff in the spheres of – Financial Management, Delinquency Management, Client Retention, Time Management, Communication Skills etc. Employees are also sent to attend workshops and trainings at reputed training organizations like BIRD-Lucknow; and IRMA-Anand, among others.

As a measure of staff welfare, employees have already been covered under Group Medical Insurance cover which is renewed every year. The extent of coverage is `1 lakh per employee with an annual premium of about `4 lakh. The policy reimburses expenses of hospitalization and/or domiciliary hospitalization expenses for illness/diseases or injury sustained during the policy period.Besides, the personnel Accidents and Disability coverage insurance scheme has become a source of staff comfort particularly for the field staff where each employee is covered risk upto ` 1 lakh. In order to help the employees in case of emergencies like health, housing, education etc. a scheme of providing personal loan to the extent of `1 lakh [max.] at concessional rate of 9% interest p.a. has been introduced. For the field level functionaries, motorcycle loan upto `40,000/- is provided at concessional rate to ease field movement.A multi-tier organizational structure with ample opportunity for internal growth of employees has proved to be a performance booster.

In the long run, the organization aims at realizing its vision with the support of a strong team built on the guiding principles of transparency, good ethics and by winning goodwill of clients and stakeholders.

C) CLIENTS 1. SHG LEADERS & MEMBERS: Trainings are imparted to the SHG leaders & members on health, education,

water & sanitation and on livestock development in order to create awareness and develop skills in scientific management of dairy, poultry, piggery, cattle, etc.

2. ENTREPRENEURSHIP DEVELOPMENT PROGRAMME (EDP): Under Employment Generation Mission-2007 of the Government of Assam, the erstwhile RGVN-CSP has embarked upon entrepreneurship development of the educated unemployed poor youth of Assam. Started in August 2007 through this project 681 clients have been trained under the 1st phase of EGM training programme. The training module was designed in such a way that it comprised both classroom & practical sessions. The 1st phase training was held for three days, with two days training on capacity building of the entrepreneurs on entrepreneurship development and the third day for exposure visit to various successful enterprises. In the 2nd phase of the training the candidates were provided with practical training in his/her line of interest with collaboration of various renowned institutions.

A) INSURANCE: Along with the initiatives towards alleviation of poverty, efforts also have been made to save the investments, assets and future income of the member borrowers arising out of death or permanent or partial disablement. The insurance coverage has been designed in such a way that besides making the borrowers free of his/her debt obligations, the policy also provides some additional amounts as relief to the deceased/handicapped family at a minimal cost of 0.5% of loan taken. In order to provide proper safety to each member borrower there has been a tie-up with two Insurance Companies namely ICICI Prudential and New India Assurance Company. During the period August 2010-March 2011, the number of borrowers provided insurance cover is about 86,011.

B) WELFARE: A Risk & Welfare Fund has been built up to cover the death and disablement of the borrowers during the currency of the loan which are not eligible for cover under normal insurance scheme. The fund is also used for providing relief to women borrowers because of death of their spouse ranging from part or full waiver of outstanding loan and even to the extent of providing additional fund in case of eligible cases.

B) STAFF – EXTERNAL Based on requirement, staff members are sent for capacity building trainings both within and outside the state - organizations selected for the purpose are like BIRD-Lucknow, APMAS-Hyderabad, AMI-Jaipur, EDA Rural Systems-Gurgaon, Microsave-Lucknow, IRMA-Anand etc. During the period under review, RGVN(NE)MFL officials attended four training programmes in BIRD-Lucknow and three programmes in IRMA-Anand.

WELFARE MEASURES

1�

Transparency Absolute transparency is being maintained in interest rate charges and other charges levied on the clients

Collection practices • No coercive collection •No overdue interest •No hidden charges

Social audit • Social Performance Assessment team, independent of operations • Feed back on multiple loans and staff behavior • Grievances Redressal mechanism • No dues raised in case of death of borrower • Extra moratorium is given in case of death of spouse • Waiver of financial assistance in case of death of borrower/spouse

Defaults• Adopt [a] peer pressure [b] frequent visits to the households • Defaults due to natural calamities are dealt with by re-phasing repayment

schedule

Penalty• There is no penalty for arrears • In case of bandh, the repayment is always rescheduled with no additional

interest charged

CLIENT pROTECTION MEASURES

1� AnnuAl report 2010-11

Rating Efficiently Run Well Run Satisfactorily Run Non Satisfactorily Run Total

1st round 16 19 6 3 44

2nd round 7 8 18 4 37

Total 23 27 24 7 81

INTERNAL AUDIT RGVN(NE)MFL introduced the Internal Audit Department in September 2009 with a view to mitigate the various risks including operating cost arising out of delivery of financial/ social services to the people of below poverty line. To safeguard the assets of the company, also to ensure appropriate systems & procedures and put adequate control in place, Risk focused Internal Audit (RFIA) has been introduced. The RFIA has two layers viz ARF(Audit report format) and DRM(Deviation in Risk Management). ARF includes CRM (Credit Risk Management), ORM (Operation Risk Management). Efforts have been made to cover all risks pertaining to the MFI. Scoring & General Efficiency Rating of branches have also been introduced. The Audit department has formulated internal audit manual for incorporating detailed guidelines for operating staff. During the period under report the Audit department has conducted internal audit of 81 branches in addition to few snapshot audit, credit Audit and expenditure audit of head office.

The details of General Efficiency Ratings, awarded to the 81 branches for the FY: 2010-11 is given below

ADDRESSING ISSUES OF WOMEN EMpOWERMENT

Since a development-based organization like RGVN(NE)MFL represents an effort of empowering the weaker section of the society, the prevailing circumstances favor focus on women. The development paradigm based on two reasons:

[a] Firstly, we have seen across our 14 years of journey that poverty has a female face. In the context of our organization, the female borrower base stands at 1,24,735. This shows our exclusive and consistent focus on female domain that has been in process since inception, for in the first financial year of the mission only 50% of members were women and today a stage is reached when this share touches a figure of around 96.58%.

b. Secondly, not only are there numerically more poor women than poor men, but women also experience poverty in more exacerbated forms than men do.

RGVN(NE)MFL wants to induce features of empowerment in a female client making her aware of rights which she is entitled to and gaining control over the resources around her,being self- confident and preparing her for active participation in the social process.

Group leader addressing the gathering on International Women’s Day 2010

Operational Self Sufficiency 117%Return on Performing Assets 14.06%Current Ratio 5.74%Capital Adequacy Ratio 13.13%

CRISIL RATING

FINANCIAL RESULTS

A rating exercise was conducted by CRISIL in March 2011 covering the period till January 2011. CRISIL’s microfinance institution (MFI) grading awarded to RGVN(NE)MFL is MFR4 on a eight-point scale. The grading includes a traditional creditworthiness analysis using the CRAMEL approach, modified to be applicable to the microfinance sector - The acronym MICROS stands for Management, Institutional arrangement, Capital adequacy and asset quality, Resources and asset-liability management, Operational effectiveness, and Scalability and sustainability.

Income: The total income of the company during the FY 2010-11 [6 months since the Company, after transfer of assets & liabilities has started functioning as a single service provider from October 1, 2010] stands at `9,30,89,428/- the expenditure being `7,87,16,833/- [excluding tax] and the net profit after Tax, Depreciation and Provision is `92, 88,082/-.

The performance of the company during the FY 2010-11:

1�

Victory belongs to the most persevering

Hiron Das – 47 years – client under Morigaon Branch Office. Prior to receiving support from us, Ms. Das was finding it difficult to ‘make both ends meet’ since the only source of income for her family [comprising of children, husband and self] was through her husband who was a daily wage labourer. Ms. Hiron Das did not even possess a piece of land to opt for cultivation. At a point of time when she was desperately looking for a means to earn her living, she was told by the women-folk in the village about the microcredit intervention of RGVN. Then, she became a member of the SHG named “Dipsikha SHG” ‘in the year 2000. Initially she had availed a loan of ̀ 2000/- [first cycle] in the year 2000 to start her Pitha-making business which is an Assamese delicacy. On

successful completion of the first loan cycle, Ms. Das availed the second cycle loan of `4000/- to expand her business venture. Thus, with incremental loans of `6000/- , `8000/-, `10,000/- and `12,000/-in subsequent loan cycles and in view of her excellent pay-back track records, she was able to take a 10th cycle of loan upto `20,000/-. Through the loans, Ms. Hiron Das had comfortably increased her income levels. The profits earned have been used to improve her living condition since she has repaired her house, procured household items and has also installed hand pumps for safe drinking water in addition to educating her children. Ms. Das has purchased a rickshaw which her husband utilizes to earn additional income to the family.

CASE STUDIES

1� AnnuAl report 2010-11

15 women who belong to Karbi tribe have been members of JLG groups JLG/123, JLG/124 & JLG/125 with 5 members each of loanee borrowers.Except small patches of cultivable land, they do not posses any assets and have no exposure to education. Out of 15, 10 have taken loan for pig fattening.Since fattening process is 7/8 months, to keep family resources in tact, these tribal ladies make beer [liquor] from rice, sell it at `150/- for 5 litres daily in the local market. Piglets are fed with the residue rice [which has a fattening ingredient].The loan is repaid in weekly intervals from the daily income. And, after 7-8 months, the piglets which are fully grown, are sold at `7000/- to `8000/- each. The profits earned have been utilized for procuring household items,

fixing a bore-well to get safe drinking water, constructing sanitary latrines, repairing the dwelling place depending on the priorities of the client[s]. This is the typical example of the inherent spirit of woman entrepreneurship and their intrinsic ability to diversify the resources.

Mr. Bashiruddin – 27 years is a client of our Bohori Branch Office. He could not continue his studies beyond Matriculation. Palhaji-his village is inhabited mostly by non-vegetarians and hence he decided to start poultry business in view of the demand. He was enrolled under Enterpreneurship Development project enabling him to avail exposure to successful enterprises besides attending skill development programme on livestock in Meghalaya. He was provided ̀ 40000/- as enterprise loan in 2008 which was invested in his poultry business. His hard efforts fetched him net income of around ̀ 15000-18000 per month. He is now able to provide employment to a few deserving youths in his business. Apart from this, Mr.Bashiruddin is also in a position to meet his family requirements. The training imparted has helped him in gaining knowledge on business management as also scientific management of poultry.

Inherent talents uncapped

Making a beginning with the end in mind

AnnuAl report 2010-11

1�

Ms. Abala Basumatary is a weaver from Goreswar branch with her education upto Class X. Considering her weaving skills RGVN had provided her a Micro Enterprise loan of `35,000 in the year 2006. After providing her training on design development and enhancing her weaving skills, she started with 4 looms. In subsequent years she has graduated from `40000 in 2008; `45000 in 2009 and `50000 in April 2010 and number of looms increased from 4 to 14. She takes pride in employing 14 women in her outlet which has enabled them to improve the living standards of the loom-workers. The monthly turnover through this weaving business works out to `24000/-. She intends to further expand her business and the RGVN intervention has definitely had a positive impact in the life of Ms. Basumatary , both financially as well as socially.

Hard efforts translate into success

Weaving her way to gloryMs. Anju Nath – 30 years – client under Rampur Branch Office has passed Class X. Hers is a weaving unit weaving mekhela chadors, gamochas, pat/muga products run by 3 family members and herself – during peak seasons, she hires expert weavers to complete the orders and give it back to her clients within a specified timeframe. Ms. Nath has been with RGVN since 5 years and started off with a first cycle loan of `2000/-. In view of the zeal shown by Ms. Nath and also taking the good repayment track records, she was selected under EGM-2007 project – she was provided `50,000/- to expand her weaving outlet. Although initially she had 2 looms, she now owns 8 looms and has hired 4 workers to support her in the business. The net monthly profits earned have gone upto `10,000/- which varies depending on the demand and season. Ms.Nath feels that with higher loan size she will be able to expand her business and if training is imparted on the latest techniques/designs etc. she would be able to attract more customers.

Hard work translated into success

Dipak Kumar Nath, born on 19 May 1979, comes from village Bhalukdubi in Goalpara district, and now lives in Bapuji Nagar, ward no. 16 of Goalpara town. He has a sister also. His father worked in State Government Corporation.

While he was pursuing his higher education in Goalpara College, he came to know about a three-month computer training center at Goalpara. This three-month training was the turning point in the life of Dipak. He found something, which can be used for earning a living for him. The seed of his entrepreneurship was sown. He is thus a self-motivated person, who wanted to pursue entrepreneurial activity primarily for economic gain, and economic gain, he has been getting.

1�

Dipak needed money to start the venture. RGVN-CSP gave him ̀ 10,000 and started the unit in 2003. After repayment of first loan, Dipak got another loan of `20,000, which he repaid. The RGVN (NE) MFL provided him another loan of `25,000/- to purchase one computer with printer and photography facility.

Second unit was started by Dipak on a rented building and with an investment of about ̀ 50,000 plus security deposit of `15,000 for the rented accommodation. In this unit, Dipak and another casual employee have been working. The other important assets in the unit are four computers, four printers, colour and laser, one motorbike worth `50,000/- and one second hand scooter worth `10,000 and inverter.

With the money from earnings, profit and savings of the 2 – in – 1 enterprise the two partners have purchased 3 kathas of land in Goalpara town and started construction of building on the same. The construction is still under progress. This is purely the effect of RGVN’S initial and other investments.

Though there are about four such enterprises in Goalpara town, they are the pioneers and leaders. Both have qualities of entrepreneurship such as commitment, determination, confidence and future orientation. However, Dipak has good organizing capability and the leadership quality to make him success in his entrepreneurial venture.

“Personification of determination”Anu Rabha (34 years) hailing from Thekachu in Goalpara district had a very painful childhood. She lost her parents when she was hardly three years old. She has two brothers and one sister. The two sisters were brought up by her Pehi (father’s married sister).

She repaid the first loan received from the erstwhile RGVN-CSP within stipulated period of time. Seeing a good client in Rabha, upon repayment of the first cycle of loan, she was awarded another loan of ̀ 20,000, strengthening her ties with the organization, enabling her to be chosen in the EGM programme for skill development in entrepreneurship.

After the training the erswhile RGVN-CSP, gave her another loan of `50,000. By mid 2010, the capital investment in her unit was worth `1,05,000. She has six machines in her unit

employing three girls on a regular basis besides herself and four girls on casual basis. She also offers training in tailoring to the poor girls. The unit runs full time observing holiday on Thursday. Her average monthly sale earnings is `30,000.

Anu is now a well-established entrepreneur, a recognized trainer with dedication to her enterprise. With earnings and savings from her unit, she has married out her younger sister. She has the urge to achieve more with a vision to enlarge her unit. She wants to replace her old machines, buy more and new ones and install more showcases. She also wants training in design, marketing and quality management.

AnnuAl report 2010-11

20

ACKNOWLEDGEMENT

The Board of Directors put on record their gratitude for the valued assistance received from Reserve Bank of India. They also express thanks for the trust reposed and support provided by investors through equity participation in the Company. The lenders like Dia Vikas & NEDFi have extended financial assistance during difficult times deserve special acknowledgement. The continuous lending support extended by other financial institutions are also acknowledged with thanks. The Board of Directors also express thanks to the thousands of clientele and wishes for their unstinted co-operation and support. The members of the Board also recognize and appreciate the dedicated service rendered by the entire RGVN(NE)MFL team in taking the organization forward.

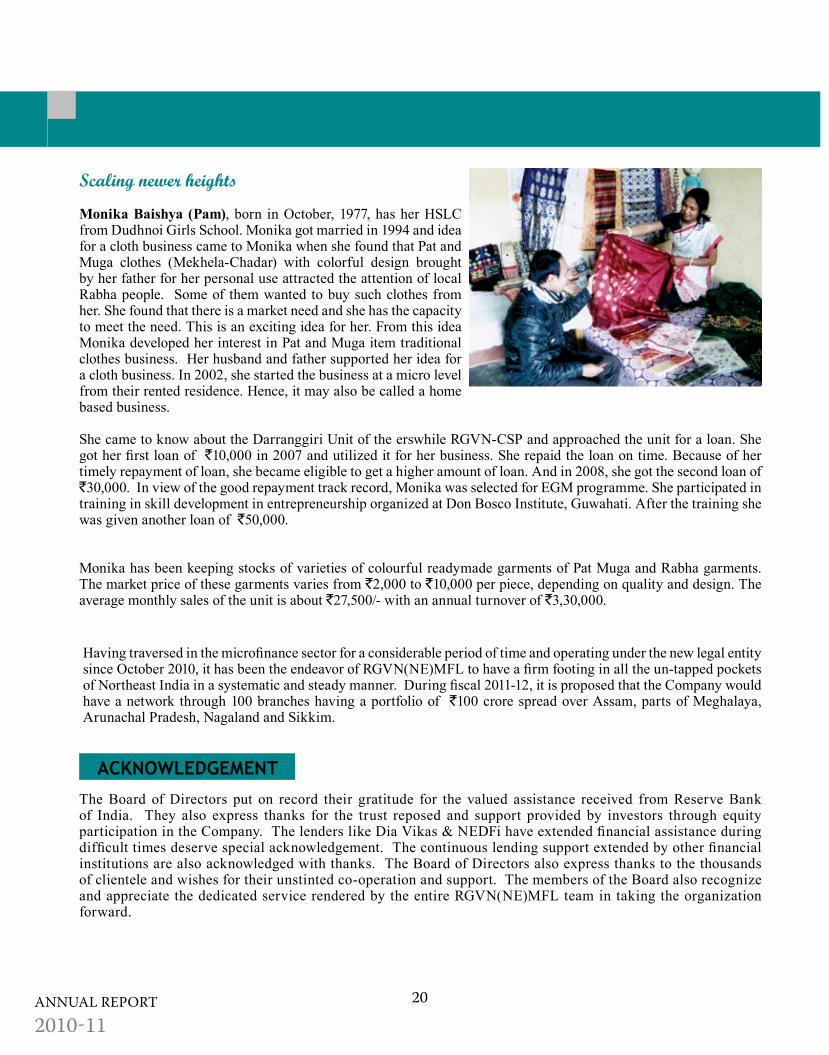

Scaling newer heights

Monika Baishya (Pam), born in October, 1977, has her HSLC from Dudhnoi Girls School. Monika got married in 1994 and idea for a cloth business came to Monika when she found that Pat and Muga clothes (Mekhela-Chadar) with colorful design brought by her father for her personal use attracted the attention of local Rabha people. Some of them wanted to buy such clothes from her. She found that there is a market need and she has the capacity to meet the need. This is an exciting idea for her. From this idea Monika developed her interest in Pat and Muga item traditional clothes business. Her husband and father supported her idea for a cloth business. In 2002, she started the business at a micro level from their rented residence. Hence, it may also be called a home based business.

She came to know about the Darranggiri Unit of the erswhile RGVN-CSP and approached the unit for a loan. She got her first loan of `10,000 in 2007 and utilized it for her business. She repaid the loan on time. Because of her timely repayment of loan, she became eligible to get a higher amount of loan. And in 2008, she got the second loan of `30,000. In view of the good repayment track record, Monika was selected for EGM programme. She participated in training in skill development in entrepreneurship organized at Don Bosco Institute, Guwahati. After the training she was given another loan of `50,000.

Monika has been keeping stocks of varieties of colourful readymade garments of Pat Muga and Rabha garments. The market price of these garments varies from `2,000 to `10,000 per piece, depending on quality and design. The average monthly sales of the unit is about `27,500/- with an annual turnover of `3,30,000.

Having traversed in the microfinance sector for a considerable period of time and operating under the new legal entity since October 2010, it has been the endeavor of RGVN(NE)MFL to have a firm footing in all the un-tapped pockets of Northeast India in a systematic and steady manner. During fiscal 2011-12, it is proposed that the Company would have a network through 100 branches having a portfolio of `100 crore spread over Assam, parts of Meghalaya, Arunachal Pradesh, Nagaland and Sikkim.

21 AnnuAl report 2010-11

AUDITOR’S REPORT TO THE MEMBERS OF RGVN (NORTH EAST) MICROFINANCE LTD.

1. We have audited the attached Balance Sheet of RGVN (NORTH EAST) MICROFINANCE LTD., Zoo

Road Tiniali, Padma Path, Guwahati - 781024, Assam, as at 31st March, 2011 and also the Profit & Loss Account and the Cash Flow Statement of the Company for the year ended on that date annexed hereto. These financial statements are the responsibility of Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

2. We conducted our audit in accordance with auditing standards generally accepted in India. Those

standards requires that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes, assessing the accounting principles used and significant estimates made by the management, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

3. Further, as required by the Companies (Auditor’s Report) Order,2003 issued by the Company Law Board in terms of Section 227(4A) of the Companies Act,1956, we enclose in the Annexure a statement on the matters specified in Paragraph 4 & 5 of the said order in so far as they are applicable to the co.

4. Further to our comments in the Annexure referred to above, we report that :-

1. We have obtained all the information and explanations which to the best of our knowledge and belief, were necessary for the purpose of our audit.

2. In our opinion, proper books of accounts as required by law have been kept by the Company, so far as it appears from our examinations of those books.

3.The Balance Sheet ,Profit & Loss Account and the Cash Flow Statement dealt with by this report are in agreement with the books of account.

4.In our opinion the Balance Sheet and Profit & Loss Account dealt with by this report comply with the accounting standards referred to in Sub-section (3C) of Section 211 of the Companies

Act, 1956.

Contd......

5. On the basis of written representations received from the directors as on 31st March,2011 and taken on record by the Board of Directors, we report that none of the Directors is disqualified as on 31st March,2011 from being appointed as a director in terms of clause (g) of Sub-section (1) of Section 274 of the Companies Act, 1956

6. In our opinion and to the best of our information and according to the explanations given to us, the said accounts read together with significant Accounting Policies and Notes on Accounts thereon, give the information as required by the Companies Act, 1956 in the manner so required and give a true and fair view:

1.In so far as it related to the Balance Sheet of the State of Affairs of the Company as at 31st March, 2011

2.In so far as it related to the Profit & Loss Account of the Company, of the Profit of the company for the year ended on that date.

3.In so far as it related to the Cash Flow Statement of the Company, of the cash flows of the company for the year ended on that date.

For SANJOY K. DAS & CO. CHARTERED ACCOUNTANTS.

Place : Guwahati (S. K. DAS)Date : 30.06.2011 PROPRIETOR MEMBERSHIP NO-050691

ANNEXURE REFERRED TO IN PARAGRAPH 3 OF OUR REPORT OF EVEN DATE ON THE ACCOUNTS OF RGVN(NORTH EAST) MICROFINANCE LTD., Zoo Road Tiniali, Padma

Path, Guwahati - 781024, Assam, as at 31st March, 2011

1. The Company has maintained proper records showing full particulars, including quantitative details and situation of fixed assets.

2. It has been represented to us that physical verification of fixed assets has been carried out by the Management at reasonable intervals during the year and such verification has not revealed any discrepancies.

3. No substantial part of fixed assets has been disposed off during the year 4. The company is a Non-Banking Financial company(NBFC) engaged in the business of giving loans

and does not maintain any inventory. Therefore the provision of Clause 4(ii) of the order are not applicable to the company.

5. In respect of loans, secured or unsecured, granted or taken by the Company during the year, from any companies, firms or other parties listed in the register maintained under section 301 of the Companies Act, 1956 -

a) The Company has not taken any unsecured loan from its directors during the year. b)The Company has not granted any secured or unsecured loan to companies, firms or other parties

during the year.

6. In our opinion and according to the information and explanations given to us during the course of audit, there are adequate internal control procedures commensurate with the size and nature of business of the company relating to purchase fixed assets and rendering of services. The activities of the company do not involve purchases of inventory and the sale of goods.

7. In our opinion & as per the Information & Explanations given to us, the company has not entered into any contracts or arrangements referred to in section 301 of the act that needed to be entered into a Register in pursuance of section 301 of the Company’s Act.

8. In our opinion and according to information and explanation given to us the company has not accepted any deposit from public.(u/s 58A & 58AA).

9. In our opinion, the company has an adequate internal audit system commensurate, with the size and nature of its business.

10. In our opinion and according to the explanation given to us, the company has no accumulated losses at the end of the financial year. The company has not incurred any loss during the year.

Contd......

11. The Company is exempt from maintaining cost records prescribed under section 209(1) (d) of the Companies Act,1956 read with the Cost Accounting Records ( Industrial Gases ) Rules, 1996.

12. In our opinion and according to information and explanations produced before us, the company is regular in depositing undisputed statutory dues including provident fund, income tax, wealth

tax, sales tax, customs duty, excise duty and any other statutory dues with the appropriate authorities. According to information and explanation given to us, the company has not any

disputed statutory dues. 13. Company has not defaulted in repayment of due to any Financial Institution or Bank. There is no

debenture holder of the company.

14. Company has not granted any loan and advance on the basis of security by way of pledge of shares, debentures and other securities.

15. In our opinion and according to the information and explanations given to us, the company is not a chit fund/ nidhi/ mutual benefit fund/ society.

16. The Company is not dealing or trading in shares, securities, debentures and other investment.

17. The Company has not given any guarantee or loans taken by others from Bank or Financial Institution.

18 To the best of our knowledge and belief and according to the information given to us, Term Loans availed by the company were applied by the company for purposes for which the loans were obtained.

19. Company had not made any long term investment by using funds raised on short term Basis according

to the information and explanation given to us.

20. Company has not made any preferential allotment of shares during the year.

21. Company is not having any debentures.

22. Company has not raised any money through public issue during the year.

23. According to the information and explanations given to us, no fraud on or by the company has been noticed or reported during the year except the following-

a) one case of cash embezzlement by the employee of the company aggregating `32,758/- was reported during the year. We have been intimated that the employee was absconding.

and the Company is in thr process of taking legal action.

For SANJOY K. DAS & CO. CHARTERED ACCOUNTANTS.

Place : GUWAHATI ( S. K. DAS ) Date : 30.06.2011. PROPRIETOR MEMBERSHIP NO-050691

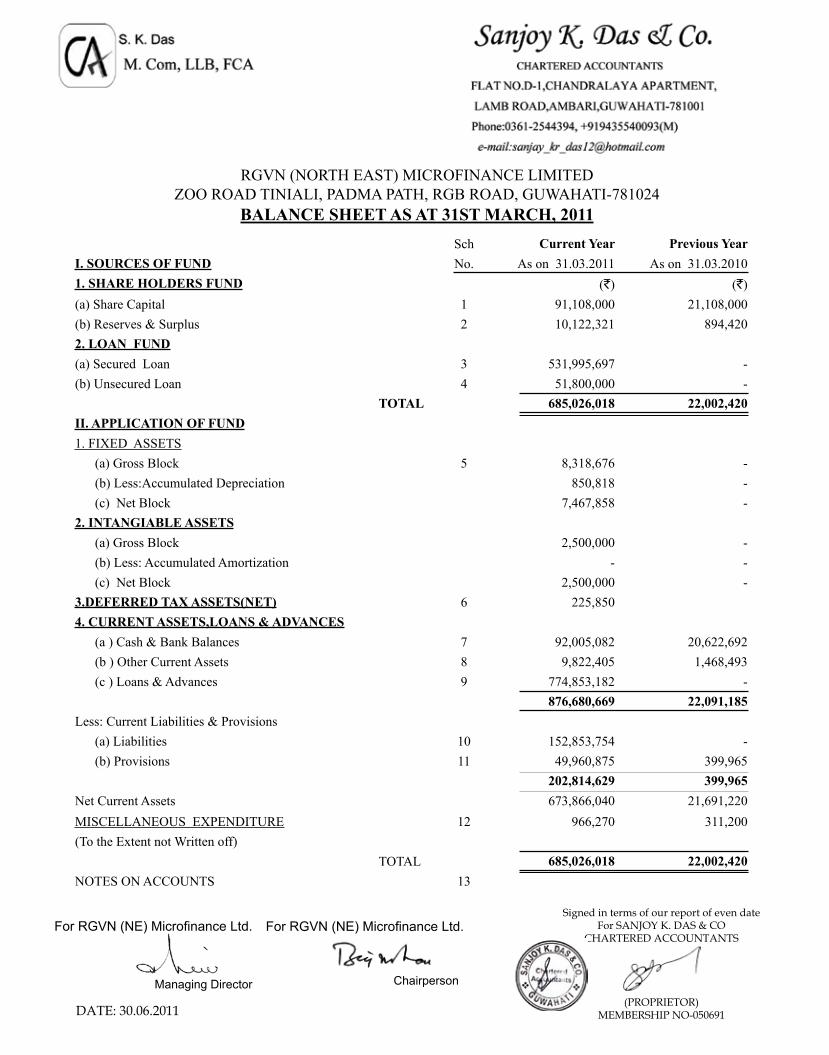

Sch Current Year Previous YearI. SOURCES OF FUND No. As on 31.03.2011 As on 31.03.20101. SHARE HOLDERS FUND (`) (`)(a) Share Capital 1 91,108,000 21,108,000 (b) Reserves & Surplus 2 10,122,321 894,420 2. LOAN FUND(a) Secured Loan 3 531,995,697 - (b) Unsecured Loan 4 51,800,000 -

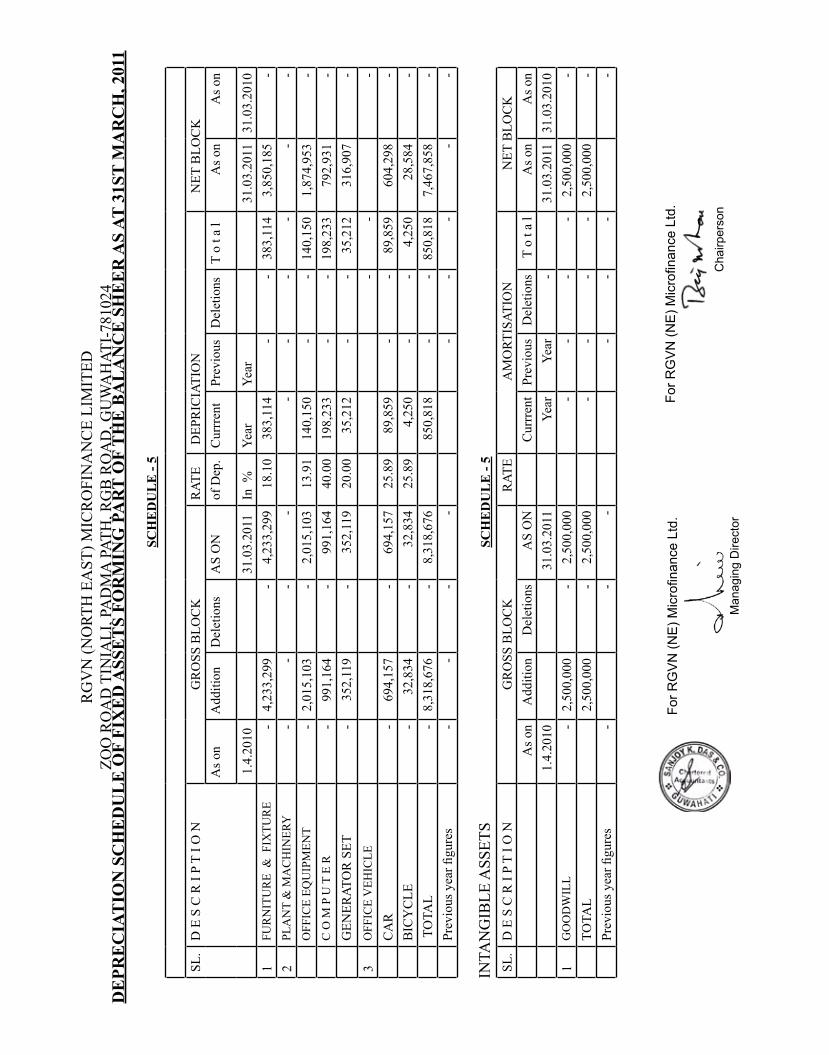

TOTAL 685,026,018 22,002,420 II. APPLICATION OF FUND1. FIXED ASSETS (a) Gross Block 5 8,318,676 - (b) Less:Accumulated Depreciation 850,818 - (c) Net Block 7,467,858 - 2. INTANGIABLE ASSETS (a) Gross Block 2,500,000 - (b) Less: Accumulated Amortization - - (c) Net Block 2,500,000 - 3.DEFERRED TAX ASSETS(NET) 6 225,850 4. CURRENT ASSETS,LOANS & ADVANCES (a ) Cash & Bank Balances 7 92,005,082 20,622,692 (b ) Other Current Assets 8 9,822,405 1,468,493 (c ) Loans & Advances 9 774,853,182 -

876,680,669 22,091,185 Less: Current Liabilities & Provisions (a) Liabilities 10 152,853,754 - (b) Provisions 11 49,960,875 399,965

202,814,629 399,965 Net Current Assets 673,866,040 21,691,220 MISCELLANEOUS EXPENDITURE 12 966,270 311,200 (To the Extent not Written off)

TOTAL 685,026,018 22,002,420 NOTES ON ACCOUNTS 13

Signed in terms of our report of even date For SANJOY K. DAS & CO

CHARTERED ACCOUNTANTS

(PROPRIETOR)MEMBERSHIP NO-050691DATE: 30.06.2011

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

BALANCE SHEET AS AT 31ST MARCH, 2011

SCH. Current year Previous YearNO. As on 31.03.2011 As on 31.03.2010

I N C O M E (`) ( ` )Income from Operation K 87,672,219 - Other Income L 5,417,209 1,468,493

Total 93,089,428 1,468,493 EXPENDITUREFinancial Expenses M 41,654,705 750 Personnel Expenses N 28,366,616 - Administrative & Other Expenses O 7,167,157 95,558 Depreciation 5 850,818 - Provision and Write off P 677,537 77,800

Total 78,716,833 174,108 Profit Before Tax 14,372,595 1,294,385 Prior Year income 174,108Profit Before Tax 14,546,703Provision for Tax: Current Tax 5,484,471 399,965 Deferred Tax -225,850 - Profit after Tax 9,288,082 894,420 Previous year surplus 894,420 - Balance Carried to Balance Sheet 10,182,502 894,420

T O T A L 10,398,526 894,420

Signed in terms of our report of even date For SANJOY K. DAS & CO

CHARTERED ACCOUNTANTS

(PROPRIETOR)MEMBERSHIP NO-050691DATE: 30.06.2011

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

PROFIT AND LOSS ACCOUNT AS AT 31ST MARCH, 2011

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

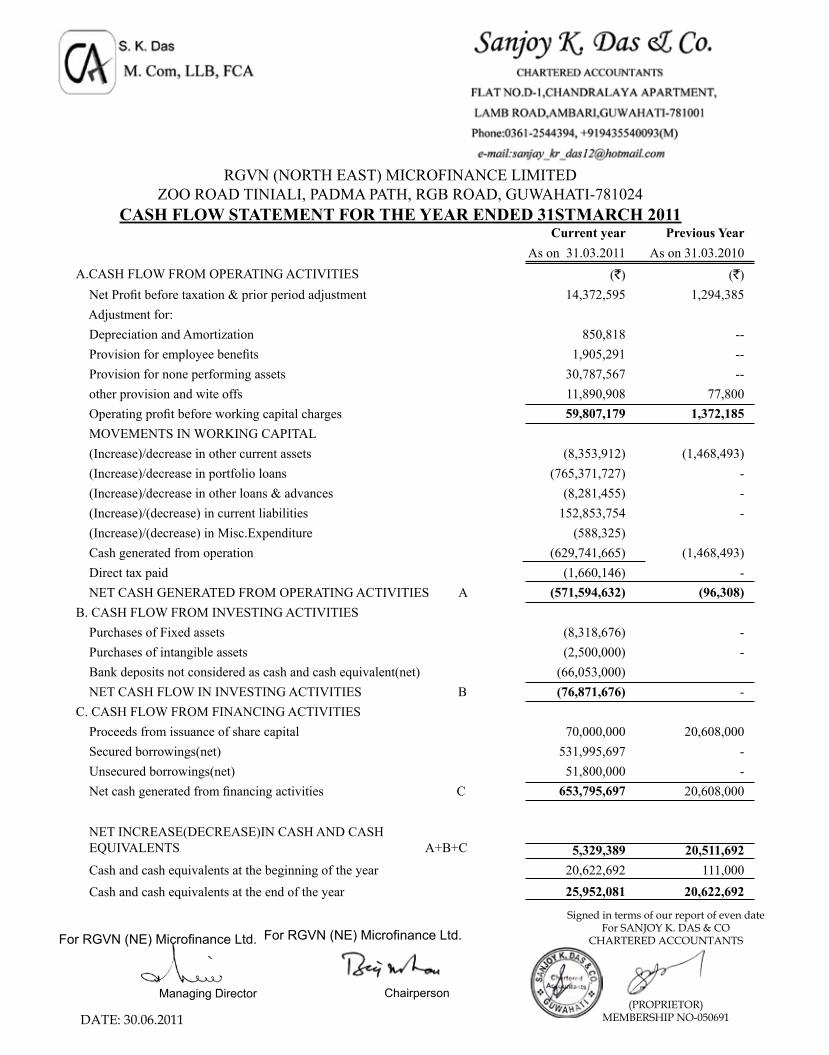

CASH FLOW STATEMENT FOR THE YEAR ENDED 31STMARCH 2011Current year Previous Year

As on 31.03.2011 As on 31.03.2010A.CASH FLOW FROM OPERATING ACTIVITIES (`) (`) Net Profit before taxation & prior period adjustment 14,372,595 1,294,385 Adjustment for: Depreciation and Amortization 850,818 -- Provision for employee benefits 1,905,291 -- Provision for none performing assets 30,787,567 -- other provision and wite offs 11,890,908 77,800 Operating profit before working capital charges 59,807,179 1,372,185 MOVEMENTS IN WORKING CAPITAL (Increase)/decrease in other current assets (8,353,912) (1,468,493) (Increase)/decrease in portfolio loans (765,371,727) - (Increase)/decrease in other loans & advances (8,281,455) - (Increase)/(decrease) in current liabilities 152,853,754 - (Increase)/(decrease) in Misc.Expenditure (588,325) Cash generated from operation (629,741,665) (1,468,493) Direct tax paid (1,660,146) - NET CASH GENERATED FROM OPERATING ACTIVITIES A (571,594,632) (96,308)B. CASH FLOW FROM INVESTING ACTIVITIES Purchases of Fixed assets (8,318,676) - Purchases of intangible assets (2,500,000) - Bank deposits not considered as cash and cash equivalent(net) (66,053,000) NET CASH FLOW IN INVESTING ACTIVITIES B (76,871,676) -C. CASH FLOW FROM FINANCING ACTIVITIES Proceeds from issuance of share capital 70,000,000 20,608,000 Secured borrowings(net) 531,995,697 - Unsecured borrowings(net) 51,800,000 - Net cash generated from financing activities C 653,795,697 20,608,000

NET INCREASE(DECREASE)IN CASH AND CASH EQUIVALENTS A+B+C 5,329,389 20,511,692 Cash and cash equivalents at the beginning of the year 20,622,692 111,000 Cash and cash equivalents at the end of the year 25,952,081 20,622,692

Signed in terms of our report of even date For SANJOY K. DAS & CO

CHARTERED ACCOUNTANTS

(PROPRIETOR)MEMBERSHIP NO-050691DATE: 30.06.2011

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

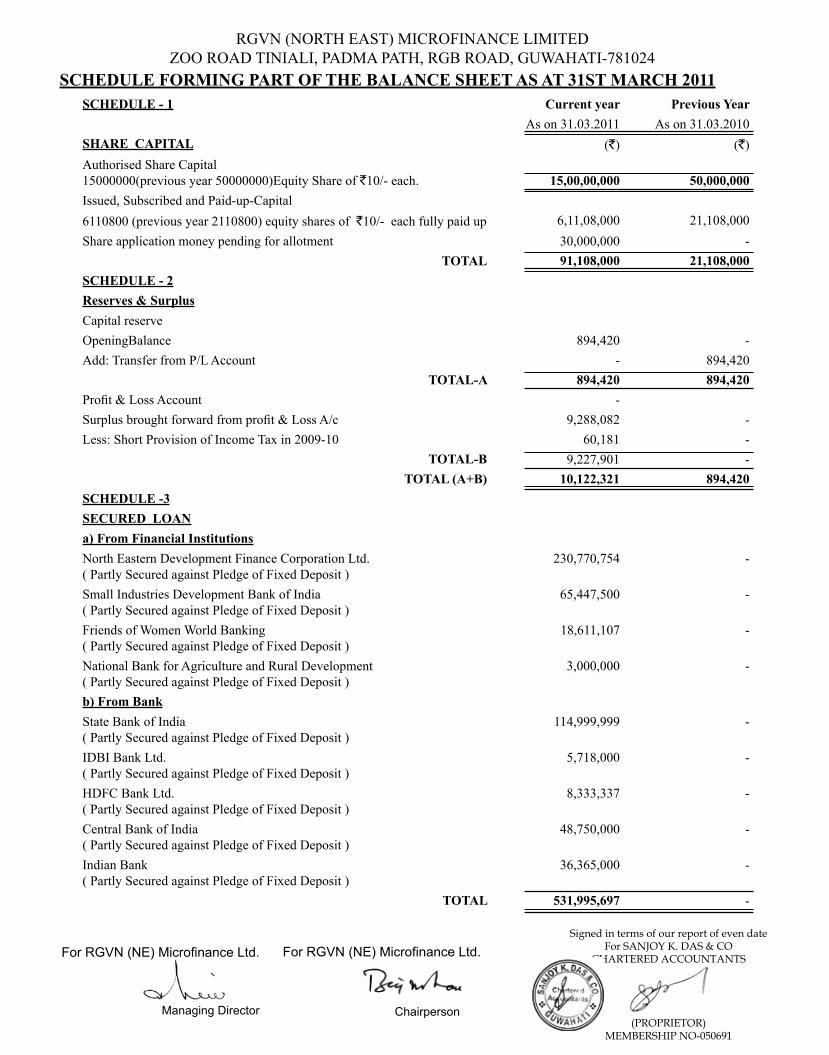

SCHEDULE - 1 Current year Previous Year As on 31.03.2011 As on 31.03.2010

SHARE CAPITAL (`) (`)Authorised Share Capital15000000(previous year 50000000)Equity Share of `10/- each. 15,00,00,000 50,000,000 Issued, Subscribed and Paid-up-Capital6110800 (previous year 2110800) equity shares of `10/- each fully paid up 6,11,08,000 21,108,000 Share application money pending for allotment 30,000,000 -

TOTAL 91,108,000 21,108,000 SCHEDULE - 2Reserves & SurplusCapital reserveOpeningBalance 894,420 - Add: Transfer from P/L Account - 894,420

TOTAL-A 894,420 894,420 Profit & Loss Account -Surplus brought forward from profit & Loss A/c 9,288,082 - Less: Short Provision of Income Tax in 2009-10 60,181 -

TOTAL-B 9,227,901 -TOTAL (A+B) 10,122,321 894,420

SCHEDULE -3SECURED LOANa) From Financial InstitutionsNorth Eastern Development Finance Corporation Ltd.( Partly Secured against Pledge of Fixed Deposit )

230,770,754 -

Small Industries Development Bank of India( Partly Secured against Pledge of Fixed Deposit )

65,447,500 -

Friends of Women World Banking( Partly Secured against Pledge of Fixed Deposit )

18,611,107 -

National Bank for Agriculture and Rural Development( Partly Secured against Pledge of Fixed Deposit )

3,000,000 -

b) From BankState Bank of India( Partly Secured against Pledge of Fixed Deposit )

114,999,999 -

IDBI Bank Ltd.( Partly Secured against Pledge of Fixed Deposit )

5,718,000 -

HDFC Bank Ltd.( Partly Secured against Pledge of Fixed Deposit )

8,333,337 -

Central Bank of India( Partly Secured against Pledge of Fixed Deposit )

48,750,000 -

Indian Bank( Partly Secured against Pledge of Fixed Deposit )

36,365,000 -

TOTAL 531,995,697 -

Signed in terms of our report of even date For SANJOY K. DAS & CO

CHARTERED ACCOUNTANTS

(PROPRIETOR)MEMBERSHIP NO-050691

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

Current year Previous Year

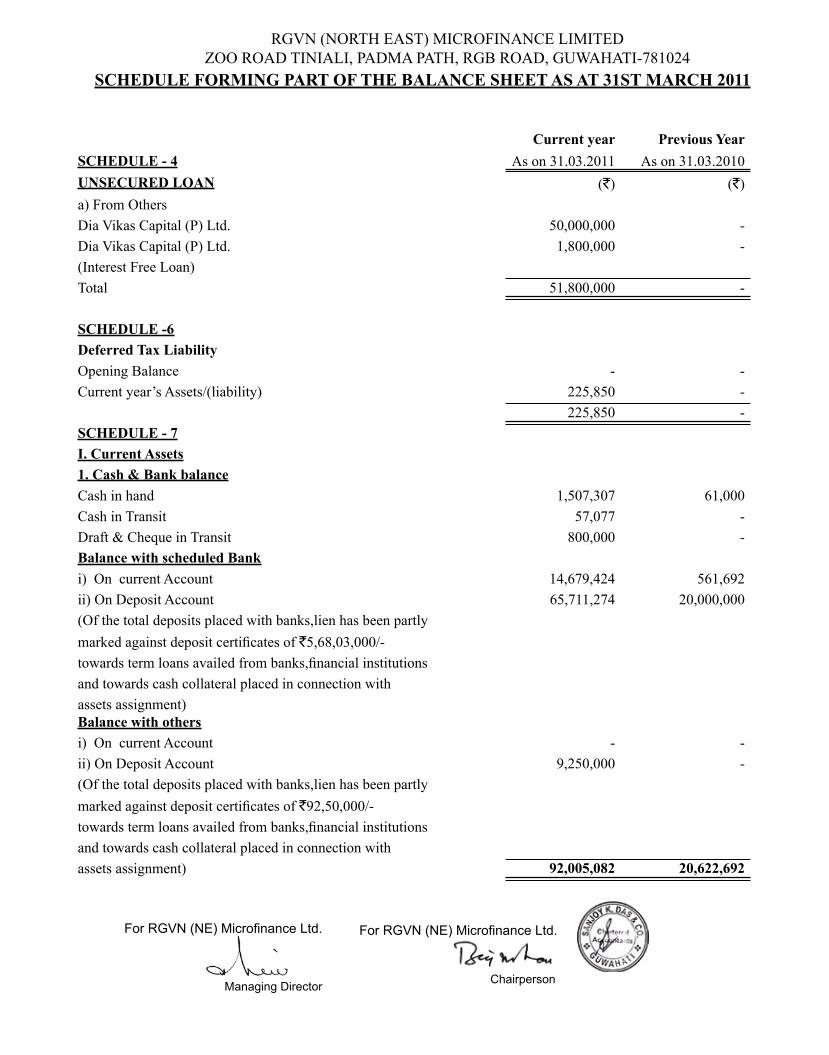

SCHEDULE - 4 As on 31.03.2011 As on 31.03.2010UNSECURED LOAN (`) (`)a) From OthersDia Vikas Capital (P) Ltd. 50,000,000 -Dia Vikas Capital (P) Ltd. 1,800,000 -(Interest Free Loan)Total 51,800,000 -

SCHEDULE -6Deferred Tax LiabilityOpening Balance - - Current year’s Assets/(liability) 225,850 -

225,850 -SCHEDULE - 7I. Current Assets1. Cash & Bank balanceCash in hand 1,507,307 61,000 Cash in Transit 57,077 -Draft & Cheque in Transit 800,000 -Balance with scheduled Bank i) On current Account 14,679,424 561,692 ii) On Deposit Account 65,711,274 20,000,000 (Of the total deposits placed with banks,lien has been partlymarked against deposit certificates of `5,68,03,000/-towards term loans availed from banks,financial institutionsand towards cash collateral placed in connection withassets assignment)Balance with othersi) On current Account - -ii) On Deposit Account 9,250,000 -(Of the total deposits placed with banks,lien has been partly marked against deposit certificates of `92,50,000/-towards term loans availed from banks,financial institutionsand towards cash collateral placed in connection withassets assignment) 92,005,082 20,622,692

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

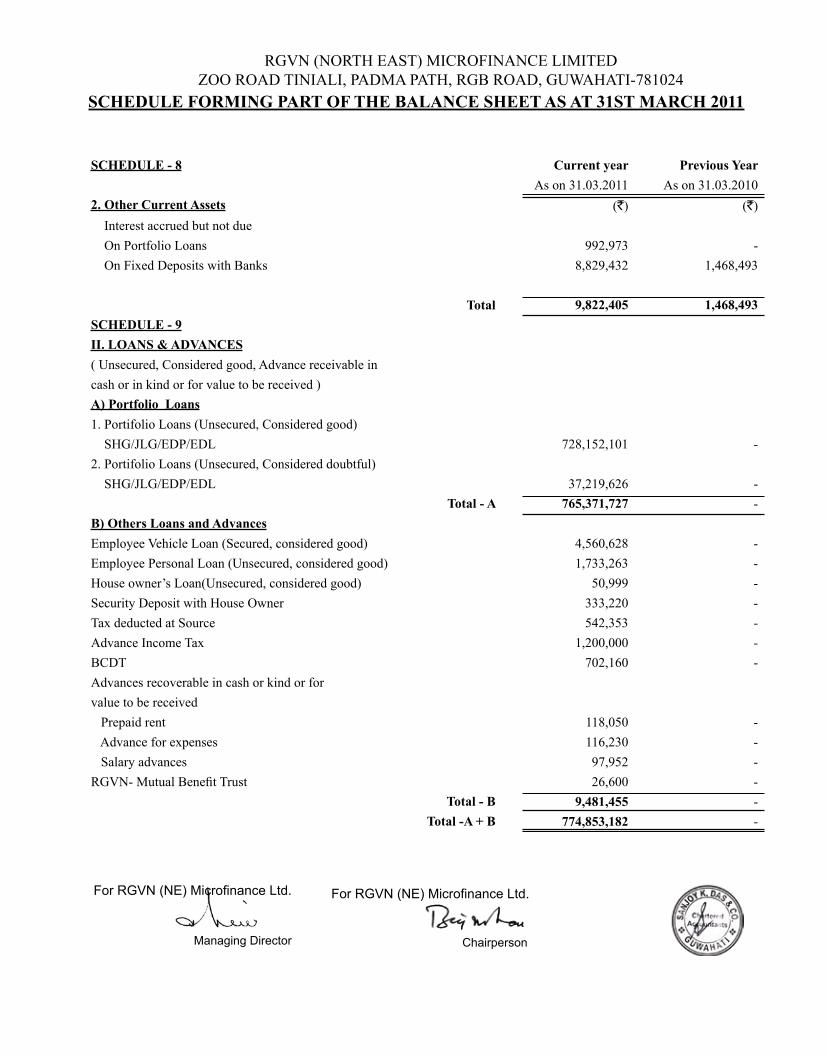

SCHEDULE - 8 Current year Previous YearAs on 31.03.2011 As on 31.03.2010

2. Other Current Assets (`) (`) Interest accrued but not due On Portfolio Loans 992,973 - On Fixed Deposits with Banks 8,829,432 1,468,493

Total 9,822,405 1,468,493 SCHEDULE - 9II. LOANS & ADVANCES( Unsecured, Considered good, Advance receivable incash or in kind or for value to be received )A) Portfolio Loans1. Portifolio Loans (Unsecured, Considered good) SHG/JLG/EDP/EDL 728,152,101 -2. Portifolio Loans (Unsecured, Considered doubtful) SHG/JLG/EDP/EDL 37,219,626 -

Total - A 765,371,727 -B) Others Loans and AdvancesEmployee Vehicle Loan (Secured, considered good) 4,560,628 -Employee Personal Loan (Unsecured, considered good) 1,733,263 -House owner’s Loan(Unsecured, considered good) 50,999 -Security Deposit with House Owner 333,220 -Tax deducted at Source 542,353 -Advance Income Tax 1,200,000 -BCDT 702,160 -Advances recoverable in cash or kind or for value to be received Prepaid rent 118,050 - Advance for expenses 116,230 - Salary advances 97,952 -RGVN- Mutual Benefit Trust 26,600 -

Total - B 9,481,455 -Total -A + B 774,853,182 -

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

SCHEDULE - 10 Current year Previous Year As on 31.03.2011 As on 31.03.2010

I. CURRENT LIABILITIES (`) (`)Securities against Loans 140,953,103 - Risk and welfare a/c 4,446,065 -Settlement due to employee 248,221 -EGM 4,376,423 -LIC-Members Death claim pending settlement 90,370 -Insurance premium pending Remittance to Birla Sunlife 506,071 -Insurance premium pending Remittance to LIC-GSLI 15,368 -Payable to MBT Members 176,320 -Surrender/Maturity received from BSLI 17,820 -Death claim received from ICICI 36,124 -Others 17,869 -Welfare support fund 1,970,000 -

- Total - I 152,853,754 -

SCHEDULE - 11II .PROVISIONS :Provision for Income Tax 5,484,472 399,965 For Provident Fund 372,552 - Provision for Standard and non- perfoming assets 30,787,567 - Sanjay K Das & Co. 100,000 - TDS 29,924 - Interest accrued but not due on loan 11,151,394 - Staff Salary Payable 1,532,739 - Canteen dues 7,800 - Others 494,427 -

Total -II 49,960,875 399,965 Total - I & II 202,814,629 399,965

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

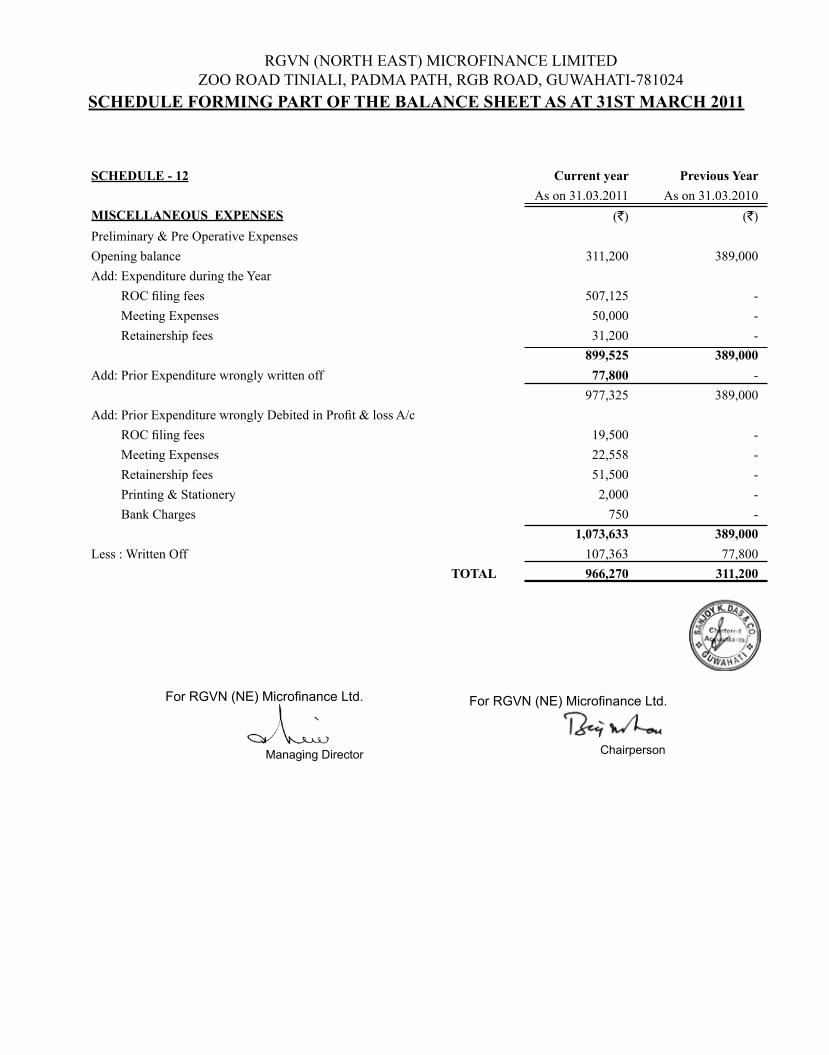

SCHEDULE - 12 Current year Previous YearAs on 31.03.2011 As on 31.03.2010

MISCELLANEOUS EXPENSES (`) (`)Preliminary & Pre Operative ExpensesOpening balance 311,200 389,000 Add: Expenditure during the Year ROC filing fees 507,125 - Meeting Expenses 50,000 - Retainership fees 31,200 -

899,525 389,000 Add: Prior Expenditure wrongly written off 77,800 -

977,325 389,000 Add: Prior Expenditure wrongly Debited in Profit & loss A/c ROC filing fees 19,500 - Meeting Expenses 22,558 - Retainership fees 51,500 - Printing & Stationery 2,000 - Bank Charges 750 -

1,073,633 389,000Less : Written Off 107,363 77,800

TOTAL 966,270 311,200

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

SCHEDULE -K Current year Previous YearINCOME FROM OPERATION As on 31.03.2011 As on 31.03.2010Income from portfolio loan (`) (`)Adminstrative Charges 27,270,480 -Interest on Loan 60,080,748 -Stationery Charges 320,991 -

Total 87,672,219 - SCHEDULE -LOTHER INCOMEInterest on Bank Deposit 3,984,736 1,468,493 Insurance Commission 305,065 -Other Commission Income 723 -Interest On House Owner’s Loan 5,189 -Interest On Employee,s personal Loan 76,738 -Interest On Employee’s Vehicle Loan 271,187 -Misc. Income 23,571 -Up- Front Fees Refund by SBI 750,000 -

Total 5,417,209 1,468,493 SCHEDULE - MFINANCIAL EXPENSESINTERESTOn Loan from Financial Institutions 15,080,018 -On Loans from Banks 18,948,974 -On Other loans 7,042,084 -Bank commission & Charges 583,629 750

Total 41,654,705 750 SCHEDULE - NPERSONNEL EXPENSESSalary & Incentive 24,983,069 -Staff Welfare 317,225 -Performance Pay 1,137,932 -Gratuity Premium 544,783 -Medical Insurance Premium 203,463 -Provident Fund 1,010,996 -Administrative Charges on Provident Fund 169,148 -

Total 28,366,616 -

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

Current year Previous YearSCHEDULE - O As on 31.03.2011 As on 31.03.2010ADMINISTRATIVE & OTHER EXPENSES (`) (`)Rent 2,090,576.00 -Electricity Charges 239,982.00 -Internet Charges 67,059.00 -Generator running Expenses 12,112.00 -Insurance premium 27,352.00 -Conveyance Expenses 5,889.00 -Office Shifting expenses 3,460.00 -Rating Expenses(CRISIL) 268,725.00 -Recruitment Expenses 66,007.00 -Professional fees 152,760.00 51,500.00 Legal & Consultancy Charges 20,000.00 -Office expenses 10,685.00 -Miscellenous Expenses 60,086.00 -Books & Periodicals 85,489.00 -Carrying charges 48,487.00 -Postage & Telegram 32,150.00 -Printing & Stationery 924,040.00 2,000.00 Telephone Charges 267,935.00 -Travelling Expenses 1,090,406.00 -Repairs & MaintenancePlant & Machinery 456,738.00 -Others 123,068.00 -Documentation Expenses 10,000.00 19,500.00 Donation 3,495.00 -Sign board & Hoarding 88,934.00 -Vehicle Hiring charges Expenses 37,965.00 -Vehicle running Expenses 15,040.00 -Water Supply 8,695.00 -Survey and market Research expenses 60,000.00 -Meeting Expenses 420,342.00 22,558.00 Training and seminar expenses 200,127.00 -Transformation Expenses 169,553.00 -Auditors Remuneration 100,000.00 -

Total 7,167,157.00 95,558.00

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

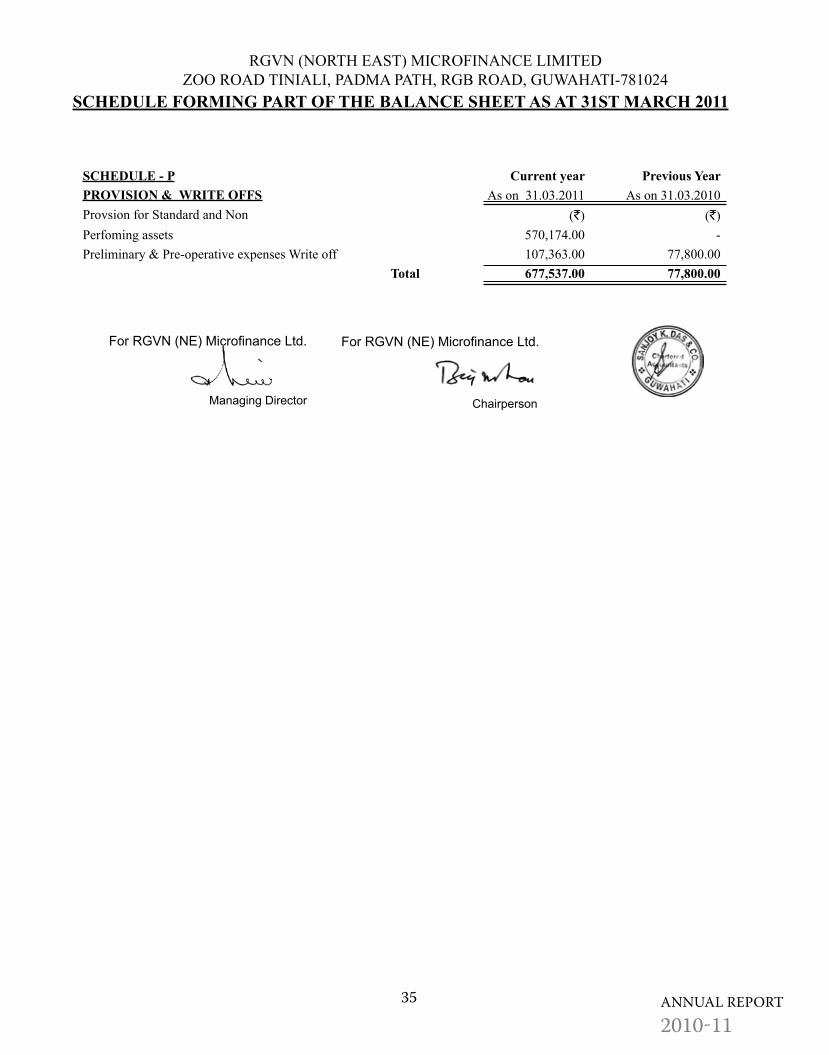

�� AnnuAl report 2010-11

SCHEDULE - P Current year Previous YearPROVISION & WRITE OFFS As on 31.03.2011 As on 31.03.2010Provsion for Standard and Non (`) (`)Perfoming assets 570,174.00 -Preliminary & Pre-operative expenses Write off 107,363.00 77,800.00

Total 677,537.00 77,800.00

RGVN (NORTH EAST) MICROFINANCE LIMITEDZOO ROAD TINIALI, PADMA PATH, RGB ROAD, GUWAHATI-781024

SCHEDULE FORMING PART OF THE BALANCE SHEET AS AT 31ST MARCH 20112011

Chairperson

For RGVN (NE) Microfinance Ltd.

Managing Director

For RGVN (NE) Microfinance Ltd.

SL.

D E

S C

R I

P T

I O N

GR

OSS

BLO

CK

RAT

E D

EPR

ICIA

TIO

N

NET

BLO

CK

As o

n A

dditi

on

Del

etio

nsA

S O

Nof

Dep

.C

urrr

ent

Prev

ious

D

elet

ions

T o

t a l

As o

nA

s on

1.4

.201

031

.03.

2011

In %

Year

Year

31.0

3.20

1131

.03.

2010

1FU

RN

ITU

RE

& F

IXTU

RE

- 4

,233

,299

-

4,2

33,2

99

18.

10

383

,114

-

- 3

83,1

14

3,8

50,1

85

- 2

PLA

NT

& M

AC

HIN

ERY

--

--

--

- -

- -

OFF

ICE

EQU

IPM

ENT

- 2

,015

,103

-

2,0

15,1

03

13.

91

140

,150

-

- 1

40,1

50

1,8

74,9

53

- C

O M

P U

T E

R -

991

,164

-

991

,164

4

0.00

1

98,2

33

- -

198

,233

7

92,9

31

- G

ENER

ATO

R S

ET -

352

,119

-

352

,119

2

0.00

3

5,21

2 -

- 3

5,21

2 3

16,9

07

- 3

OFF

ICE

VEH

ICLE

- -

- C

AR

- 6

94,1

57

- 6

94,1

57

25.

89

89,

859

- -

89,

859

604

,298

-

BIC

YC

LE -

32,

834

- 3

2,83

4 2

5.89

4

,250

-

- 4

,250

2

8,58

4 -

TO

TAL

- 8

,318

,676

-

8,3

18,6

76

850

,818

-

- 8

50,8

18

7,4

67,8

58

- Pr

evio

us y

ear fi

gure

s -

- -

- -

- -

- -

SL.

D E

S C

R I

P T

I O N

GR

OSS

BLO

CK

RAT

E A

MO

RTIS

ATIO

N

NET

BLO

CK

As o

n A

dditi

on

Del

etio

nsA

S O

NC

urrr

ent

Prev

ious

D

elet

ions

T o

t a l

As o

nA

s on

1.4

.201

031

.03.

2011

Year

Year

-31

.03.

2011

31.0

3.20

101

GO

OD

WIL

L -

2,5

00,0

00

- 2

,500

,000

- -

- -

2,5

00,0

00 -

TOTA

L 2

,500

,000

-

2,5

00,0

00

-

- -

- 2

,500

,000

-

Prev

ious

yea

r figu

res

- -

- -

- -

-

Cha

irper

son

For R

GV

N (N

E) M

icro