50

Annual Report 2011

A n n u a l R e p o r t 2 0 1 1

Mission stateMent

As the pioneer in leisure community development in the Philippines, Belle Corporation

remains steadfast with its commitment in shaping and influencing the real estate

industry by promoting a holistic approach in its developments. Exclusive homes, clean

natural surroundings, and round-the-clock security and utilities in its gated communities keep in

mind the conscious effort of preserving the environment and general ecosystem. Value-added

services and world-class amenities in its clubs and other leisure facilities transcend into a legacy

for generations to come.

Annual Repor t 2011 Belle Corporation 1

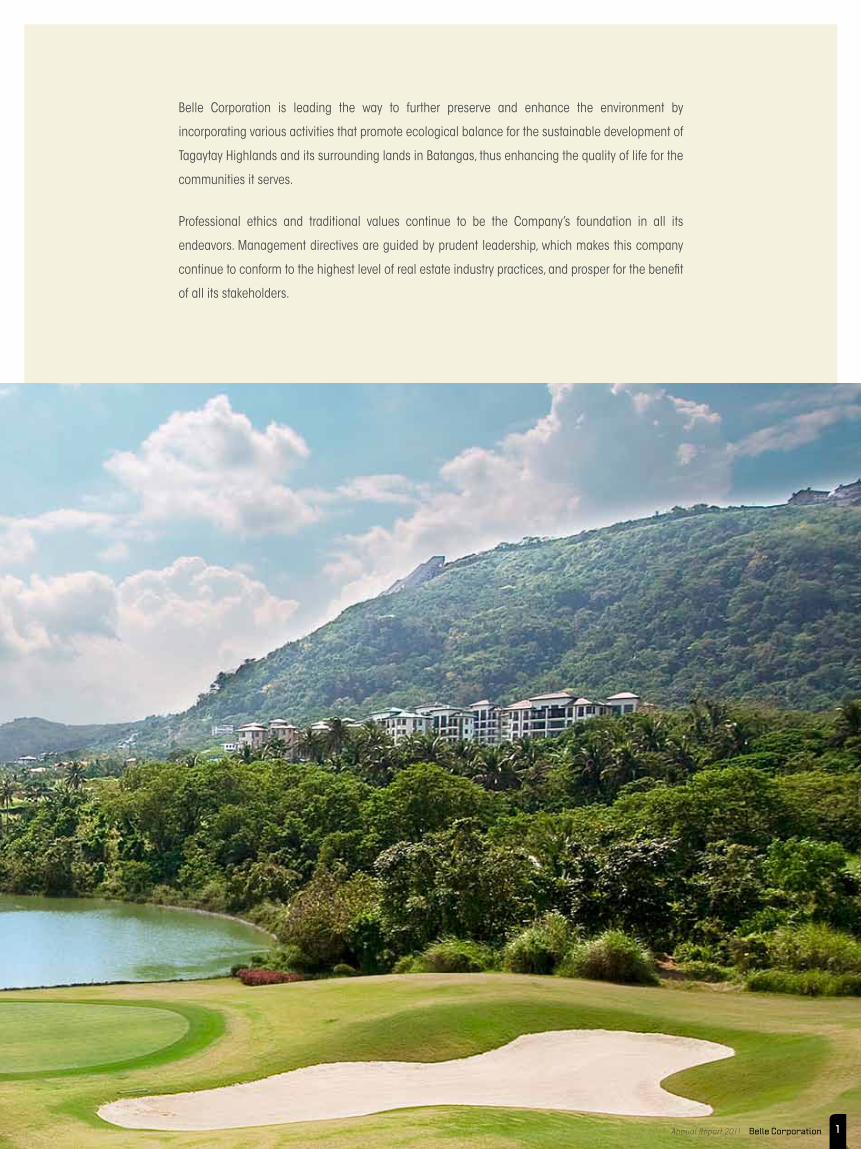

Belle Corporation is leading the way to further preserve and enhance the environment by

incorporating various activities that promote ecological balance for the sustainable development of

Tagaytay Highlands and its surrounding lands in Batangas, thus enhancing the quality of life for the

communities it serves.

Professional ethics and traditional values continue to be the Company’s foundation in all its

endeavors. Management directives are guided by prudent leadership, which makes this company

continue to conform to the highest level of real estate industry practices, and prosper for the benefit

of all its stakeholders.

Belle Corporation Annual Repor t 20112

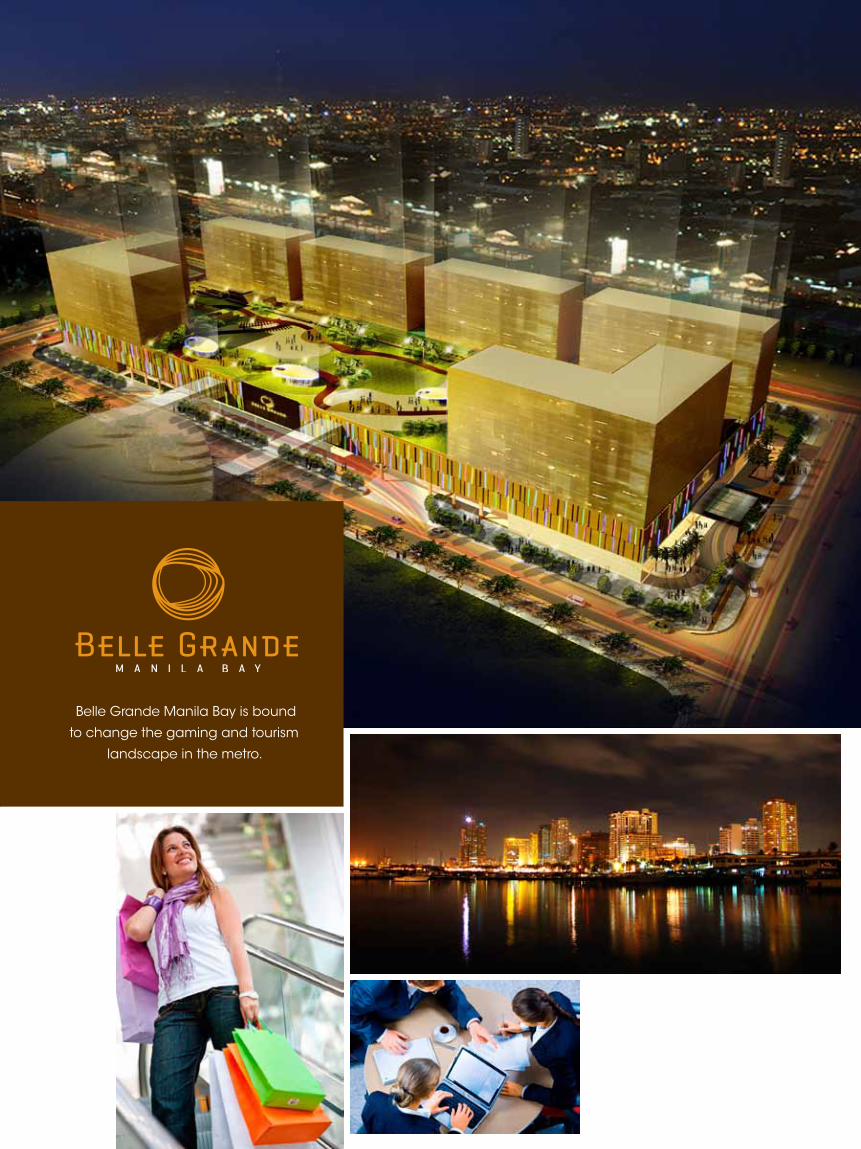

Belle Grande is being constructed on more

than 6 hectares of land in a central area in

the Aseana Business Park in Parañaque City,

with three of its sides facing major thoroughfares -

Roxas Boulevard, Diosdado Macapagal Avenue and

Aseana Avenue. The integrated resort has a very

advantageous location at the entrance of Bagong

Nayong Pilipino. It is also conveniently close to the

SM Mall of Asia complex, Ninoy Aquino International

Airport and all major tourist destinations in Old

Manila. Belle Grande will extend the visitors’ Manila

During 2011, Belle Corporation took giant strides

towards achieving the next level in its evolution

as a leading player in the Philippine high-end

property and leisure industry. Your Company’s

integrated resort, Belle Grande Manila Bay, has

risen prominently in what used to be undeveloped

grassy sand flats. The structure for the main

podium of Belle Grande is now a visible signal to

all of Metro Manila of the forthcoming emergence

of Bagong Nayong Pilipino (literally translated

to “New Philippine Village”), which the Philippine

Department of Tourism and Philippine Amusement

& Gaming Corporation are aiming to make

into a major international leisure destination

within a 15-minute drive from the Ninoy Aquino

International Airport.

Message to shareholders

Belle Grande will extend the visitors’ Manila experience beyond sightseeing and gaming.

Annual Repor t 2011 Belle Corporation 3

experience beyond sightseeing and gaming - with

its own entertainment, leisure and hospitality

options; and with its links to the SM Mall of Asia

for quality shopping, the SMX Convention Center

for conferences and trade fairs, and the SM Arena

for sporting events and entertainment spectacles.

Belle Grande will be a premiere leisure

destination comprising the main podium and the

adjacent Mall, with a total gross floor area of over

25 hectares and each approximately 45 meters

high. The main podium will feature six luxury hotel

towers with more than 800 rooms and the Belle

Grande Casino, which will occupy its first two floors.

The Belle Grande Casino will have a total gaming

area of approximately 1.8 hectares surrounded

by food and beverage outlets, with luxury retail

stores at the margins. The Mall will feature a

world-class performing arts theater and high-end

shopping. The entire resort will contain more than

2 hectares of retail and dining options. We expect

Belle Grande to be a key attraction in the Bagong

Nayong Pilipino area, and as such it will help to

redefine the Manila experience for both tourists

and residents alike.

We broke ground in January 2010, and expect

to complete and launch the entire complex in 2013.

By the end of 2011, the structure of the gaming

facility has already taken shape. We broke ground

on the Mall in February 2012, with its completion

projected for 2014.

While we are excited about the expected

long-term contribution of the Belle Grande project

to your Company’s value, we continue to focus on

our “franchise” business in the Tagaytay Highlands

area. Belle still owns about 780 hectares of

landbank that provides us with the opportunity to

offer to the market ideal lots and residences in the

level of quality that Belle is known for.

Financial Review

2011 was a particularly challenging year,

with the Philippine real estate markets being

affected by global financial disruptions that stifled

growth, coupled with more intensive competition,

as Belle’s gross revenues decreased by 45%

between 2010 and 2011, from P=1.3 billion to

P=697 million. However, Belle has continued to

attain profitable operations, with operating income

at P=225 million and consolidated net income of

about P=200 million for 2011. Our consistent focus

on cost control has helped your Company maintain

sufficient operating flexibility to be able to continue

to post positive operating results even under difficult

market conditions. Moreover, we have maintained

our longstanding reputation for product quality, as

well as a loyal following in our traditional niche

Topping-off ceremony of Belle Grande Manila Bay attended by members of the

Board of Directors and Management Team

1 As of December 31, 2011, Belle had P=2.8 billion in cash and marketable securities, and P=901 million in receivables.

Belle Corporation Annual Repor t 20114

market for high-end property. We have planned a

number of product launches and sales initiatives

for 2012, which we believe will help boost revenues

and operating profits significantly during 2012.

Belle’s balance sheet has continued to

be solid. As of December 31, 2011, Belle had

about P=3.7 billion in liquid assets1, as well as

approximately P=3 billion in available credit lines.

Our current ratio stands at 3.17X and effectively

assures funding for all of our pending and planned

projects. The Company’s balance sheet further

strengthened with its total debt to equity ratio at

29% as of December 31, 2011, the lowest level

since 1996, prior to the Asian Financial Crisis.

Affiliates

Highlands Prime, Inc. (HPI), Belle’s 36%-owned

real estate affiliate, realized a net loss of P=35 million

in 2011, compared to net income of P=8 million in

2010. HPI plans to turn around its operations with

promising new project launches during 2012,

including a new leisure lot development within

Tagaytay Highlands, envisioned to have modern

log homes which highlight the use of rustic wood

elements in modern architecture. HPI is also slated

to come out with another themed residential lot

development in the vicinity of Tagaytay Midlands.

Pacific Online Systems Corporation (Pacific

Online), a 35%-owned gaming affiliate, realized

net income of P=392 million for 2011, compared

to P=430 million in 2010. Pacific Online supplies

lottery equipment to the Philippine Charity

Sweepstakes Office (PCSO) in the Visayas and

Mindanao, for which it collects a percentage

of PCSO’s revenues from these areas. Pacific

Online’s decrease in net income during 2011

Debt to Equity Ratio

2004 2005 2006 2007 2008 2009 2010 2011

180%

160%

140%

120%

100%

80%

60%

40%

20%

0%

54% 49% 54% 50% 49% 45% 44%

29%

Consolidated Net Income

2004 2005 2006 2007 2008 2009 2010 2011

900.0

800.0

700.0

600.0

500.0

400.0

300.0

200.0

100.0

0.0

118.9

832.9

152.3

331.7

205.8

385.8

465.5

200.5Am

ou

nts

(in

P m

illio

ns)

Members of the Board of Directors of Belle Corporation and Philippine Stock Exchange during the listing of the stock rights offering last October 10, 2011

Annual Repor t 2011 Belle Corporation 5

Benito Tan GuatChairman

Willy N. OcierVice Chairman

Elizabeth Anne C. UychacoVice Chairperson

From left to right:

Willy N. OcierVice Chairman

Benito Tan Guat Chairman

Elizabeth Anne C. UychacoVice Chairperson

was because gains arising from its marketable

securities portfolio fell from about P=173 million

during 2010 to P=69 million during 2011, due to

volatile market conditions during 2011. Excluding

gains in marketable securities, Pacific Online’s net

income would have shown an increase of about

P=66 million during 2011. Further earnings growth

is expected in future years, as it benefits from

continued penetration by the PCSO of its regions

with terminals leased from it, coupled with growth

in the PCSO’s gaming revenues. We expect Pacific

Online’s earnings momentum to continue during

2012.

Future Plans

With the continuing demand for green

minimalist style of architecture present in Japanese

structural design, Belle plans on expanding the

Japanese-inspired community of Yume in Lakeside

Fairways with the same surreal design elements

that has endeared it to its first patrons. Sycamore

Heights, also in Lakeside Fairways, will welcome

an expansion as well. Similar to the homes in

Yume, the ones in Sycamore Heights designed by

L.V. Locsin and Partners follow a green or energy

efficient design with an Asian Contemporary

theme that provides high ceilings, large picture

windows and more open spaces to make the living

spaces harmoniously blend and work with the

environment.

The vision for Lakeside Fairways to be a

community embraced by the love of golf will

soon be realized with the opening of the Midlands

Lucky 9 in the second quarter of 2012. Golf course

designer John Olenoski has made an exciting

work of art with the new nines, giving it a breath of

mystery in every challenge that is distinctly Lucky

9. He is currently working on the design of the

fourth nines at the Tagaytay Midlands golf course

which will be a reality in the next three to four

years. With this, Belle will be bringing the number

of 18-hole international championship golf

courses in Tagaytay Highlands to a total of three,

with its own clubhouse and recreational facilities.

We are proud of your Company’s performance

and progress, and are very excited about its

expanding opportunities for 2012 and beyond.

Your Company continues to maintain its leadership

position in the high-end leisure real estate industry,

and is on track to enter the lucrative integrated

resort industry within a year.

We can assure you, our shareholders,

that we will continue to work diligently towards

delivering profitable results and strive to enhance

shareholders’ value.

Thank you for your continued support.

6 Belle Corporation Annual Repor t 2011

Tagaytay Highlands continues

to be the country’s premier destination

for luxury living.

Tagaytay Highlands

Belle Grande Manila Bay is bound

to change the gaming and tourism

landscape in the metro.

Belle Corporation Annual Repor t 20118

Benito Tan GuatChairman

Willy N. OcierVice Chairman

Elizabeth Anne C. UychacoVice Chairperson

Rogelio R. CabuñagDirector and President

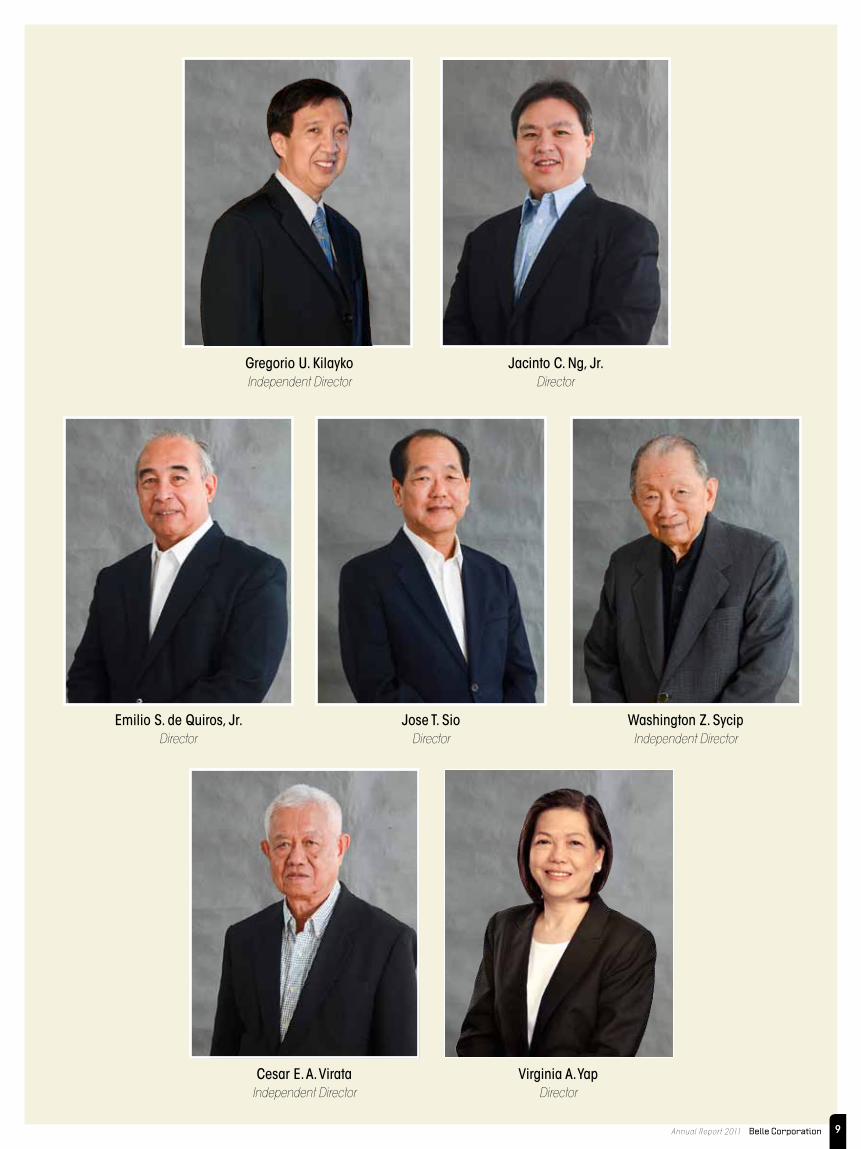

Board of directors

Annual Repor t 2011 Belle Corporation 9

Gregorio U. KilaykoIndependent Director

Jose T. SioDirector

Washington Z. SycipIndependent Director

Jacinto C. Ng, Jr.Director

Virginia A. Yap Director

Emilio S. de Quiros, Jr.Director

Cesar E. A. Virata Independent Director

Belle Corporation Annual Repor t 201110

ManageMent teaM

Willy N. OcierVice Chairman

Rogelio R. CabuñagPresident

Joselito R. ConsunjiExecutive Vice President and

Chief Operating Officer

Frederic C. Dy BuncioHead - Business UnitPortfolio Investment

Armin B. Raquel SantosHead - Business Unit Casino Operations

Shirley C. OngHead - Business Unit

Project Development and Sales & Marketing

Claire T. KramerHead - Business Unit

Clubs

Manuel A. GanaExecutive Vice President and

Chief Financial Officer

Annual Repor t 2011 Belle Corporation 11

Nancy O. HuiExecutive Assistant to the Chairman

Emmanuel J. MoralesAsst. Vice President for Project

Management and External Affairs

Donn Frank C. RabanesAsst. Vice President for

Corporate Planning PremiumLeisure & Amusement, Inc.

Marilyn G. RicoVice President for Internal Audit

Rudy P. AninipotVice President for Property Maintenance

Rogelio I. RobangVice President for Project Management

and External Affairs

Margaret Y. HernandoVice President for Treasury

Melvin U. CadampogVice President for Corporate Planning

Maricer S. MendiolaAsst. Vice President for Sales

Michelle T. HernandezVice President for Marketing

Rosemarie S. RamosAsst. Vice President for Accounting

Atty. A. Bayani K. TanCorporate Secretary

Atty. Arthur A. SyAsst. Corporate Secretary

Sharlie B. CoAsst. Vice President for

Corporate Services

Zenia K. SyHead of Sales

Edwin M. PangilinanAsst. Vice President for Sales

The following data should be read in conjunction with the consolidated financial statements and related notes thereto and management’s discussion and analysis of operating performance and financial condition included elsewhere in this annual report. Years Ended December 31 2011 2010 2009 20081 20071

(amounts in P=millions)

CONSOLIDATED INCOME STATEMENT DATA:

Real Estate Operations:

Gross revenues P=696.5 P=1,263.1 P=1,403.2 P=1,349.3 P=658.3

Cost of real estate and club shares sold (236.0) (509.0) (566.3) (587.0) (210.5)

Gross margin 460.5 754.1 836.9 762.3 447.7

General and administrative expenses (235.1) (221.4) (305.4) (279.7) (222.6)

Income from real estate operations 225.3 532.7 531.5 482.6 225.1

Equity in net earnings of associates 140.5 156.2 117.9 81.3 72.2

Financial and other income (expenses) - net2 (142.3) (146.9) (189.4) (329.7) 41.3

Tax benefits (provisions) (23.1) (76.6) (73.9) (28.4) (6.9)

Minority interest (0.1) (0.1) (0.1) (0.1) (0.1)

Consolidated net income after taxes 200.5 465.5 385.8 205.8 331.7

CONSOLIDATED BALANCE SHEET DATA:

Total assets P=22,643.5 P=10,528.1 P=9,973.5 P=9,912.6 P=9,418.2

Total debt 4,715.4 2,708.1 2,564.5 2,598.2 2,535.0

Total liabilities3 6,568.5 4,349.8 4,273.6 4,576.8 4,320.6

Stockholders’ equity4 16,075.0 6,178.3 5,699.9 5,335.8 5,097.6

1 Income statement data were restated in order to conform to new financial reporting and presentation requirements. Such restatements had no effect on net income figures. Total assets and stockholders’ equity as of December 31, 2008 were restated from P=9,915.0 million and P=5,338.3 million, respectively, in order to reflect the fair market value of Belle shares held by Primary Data, Inc. (a subsidiary of APC Group, Inc.).

2 Inclusive of net foreign exchange gain of P=270 thousand in 2011, P=51.5 million in 2010, P=28.9 million in 2009, P=135.4 million in 2008, P=166.1 million in 2007 and P=88.5 million in 2006, mainly due to US$ denominated loans. For foreign exchange translation purposes, exchange rates used were P=43.84:US$1 as of December 31, 2011 and December 31, 2010, P=46.20:US$1 as of December 31, 2009, P=47.52:US$1 as of December 31, 2008, and P=41.28:US$1 as of December 31, 2007.

3 Including total debt.4 Net of minority interest.

Belle Corporation Annual Repor t 201112

selected financial and oPerating data

REVENUES

Gross revenue for 2011 of P=696.5 million was lower by P=566.6 million (45%), compared to P=1,263.1 million during 2010. Gross profit as of December 2011 of P=460.5 million was also lower than gross profit as of December 2010 of P=754.1 million by P=293.6 million (39%), due to the lower sales of real estate and club shares. The Company’s revenues for the 2010 period were stimulated by the launches of Katsura and Fairfield, and the grand launch of Cotswold, during 2009. These three projects comprised a total of 487 saleable lots and 165,175 square meters (“sqm”) in net saleable area. In contrast, the Company’s project launches during 2010 (Nob Hill and Yume), which were to help stimulate its revenues for 2011, comprised a total of approximately 162 saleable lots and 70,741 sqm in saleable area. During 2011, the Company has been devoting significant resources to development activities connected with Belle Grande Manila Bay (“Belle Grande”), its integrated resort project located in Parañaque City, which is targeted for its grand opening in 2013. During the year ended December 31, 2011, the Company recorded net

rental income of P=62.1 million on land and buildings leased by the Company to AB Leisure Global, Inc. (“ABLGI”) for the site of Belle Grande, starting January 14, 2011. In the second quarter of 2011, Belle introduced Lakeside Fairways Phase 8 (Sycamore Heights), with more than 23 hectares of gross saleable area and 309 residential lots. In the third quarter of 2011, the Company introduced extensions of existing projects, namely three new pads for log cabins at The Woodlands and nine new lots in Lakeside Fairways Phase 6 (Cotswold). These project extensions will carry total potential sales of about P=225.0 million.

Cost of Real Estate and Club Shares SoldCost of real estate and clubs shares sold decreased by P=273.0 million (54%) to P=236.0 million in 2011 from P=509.0 million in 2010 due mainly to lower unit sales of real estate and club shares sold in 2011.

General and Administrative ExpensesThe increase by P=13.8 million (6%) from P=221.4 million in 2010 to P=235.2 million in 2011 was caused by the following: higher marketing expenses and registration fees. The increase was partially offset by lower taxes and licenses and professional fees.

Financial Income (Expense)Interest expense decreased by P=33.2 million (17%), to P=158.2 million, from P=191.4 million in 2010 due to lower interest rates. In 2011, the Company also capitalized borrowing costs amounting to P=107.3 million.

Interest income increased by P=24.9 million (701.4%), from P=3.6 million to P=28.5 million in 2011 due to placement of funds. The significant increase in 2011 fund level of the Company was brought by new long-term loan drawdown and proceeds from the stock rights offering.

Equity in Net Earnings of AssociatesThe Company’s equitized net earnings from associated companies decreased by P=15.7 million (10%) to P=140.5 million in 2011, from P=156.2 million in 2010. Equitized earnings were mainly from its 36%-owned associate, Highlands Prime, Inc. (HPI), and from its 35%-owned associate, Pacific Online Systems Corporation (Pacific Online). HPI is also engaged in real estate development within the Tagaytay Highlands and Midlands complexes, while Pacific Online leases on-line equipment to the Philippine Charity Sweepstakes Office for their lottery operations in the Visayas and Mindanao.

TABLE 1: Year Ended December 31 Horizontal Analysis Vertical Analysis 2011 2010 Increase (Decrease) 2011 2010 (In Thousands) (Percentages)

REVENUE Sale of real estate and club shares P=520,176 P=1,163,986 (P=643,810) -55.3% 74.7% 92.2% Lease income 62,070 - 62,070 100.0% 8.9% 0.0% Others 114,275 99,137 15,138 15.3% 16.4% 7.8% 696,521 1,263,123 (566,602) -44.9% 100.00% 100.0%COST OF REAL ESTATE AND CLUB SHARES (235,983) (508,979) (272,996) -53.6% -33.9% -40.3%GENERAL AND ADMINISTRATIVE ExPENSES (235,158) (221,431) 13,727 6.2% -33.8% -17.5%INTEREST ExPENSE (158,160) (191,353) (33,193) -17.3% -22.7% -15.1%EQUITY IN NET EARNINGS OF ASSOCIATES 140,484 156,184 (15,700) -10.1% 20.2% 12.4%NET FOREIGN ExCHANGE GAIN 270 51,522 (51,252) -99.5% 0.0% 4.1%INTEREST INCOME 28,498 3,556 24,942 701.4% 4.1% 0.3%OTHER CHARGES - Net (12,910) (10,600) 2,310 21.8% -1.9% -0.8%INCOME BEFORE INCOME TAx 223,562 542,022 (318,460) -58.8% 32.1% 42.9%PROVISION FOR INCOME TAx Current 15,972 49,006 (33,034) -67.4% 2.3% 3.9% Deferred 7,130 27,548 (20,418) -74.1% 1.0% 2.2% 23,102 76,554 (53,452) -69.8% 3.3% 6.1%NET INCOME 200,460 465,468 (265,008) -56.9% 28.8% 36.9%Net profit attrbutable to: Equity holders of the parent 200,517 465,535 (265,018) -56.9% 28.8% 36.9% Non-controlling interests (57) (67) (10) -14.9% 0.0% 0.0% P=200,460 P=465,468 (P=265,008) -56.9% 28.8% 36.9%

DECEMBER 31, 2011 vs DECEMBER 31, 2010 RESULTS OF OPERATIONS (Table 1)

Net Foreign Exchange GainWith the exchange rate of the Philippine Peso against the US Dollar to P=43.84:US$1.00 as of December 31, 2011 and 2010, the Company posted a minimal P=0.3 million foreign exchange translation gain from its foreign currency deposits. While in 2010, the foreign exchange translation gain amounted to P=51.5 million.

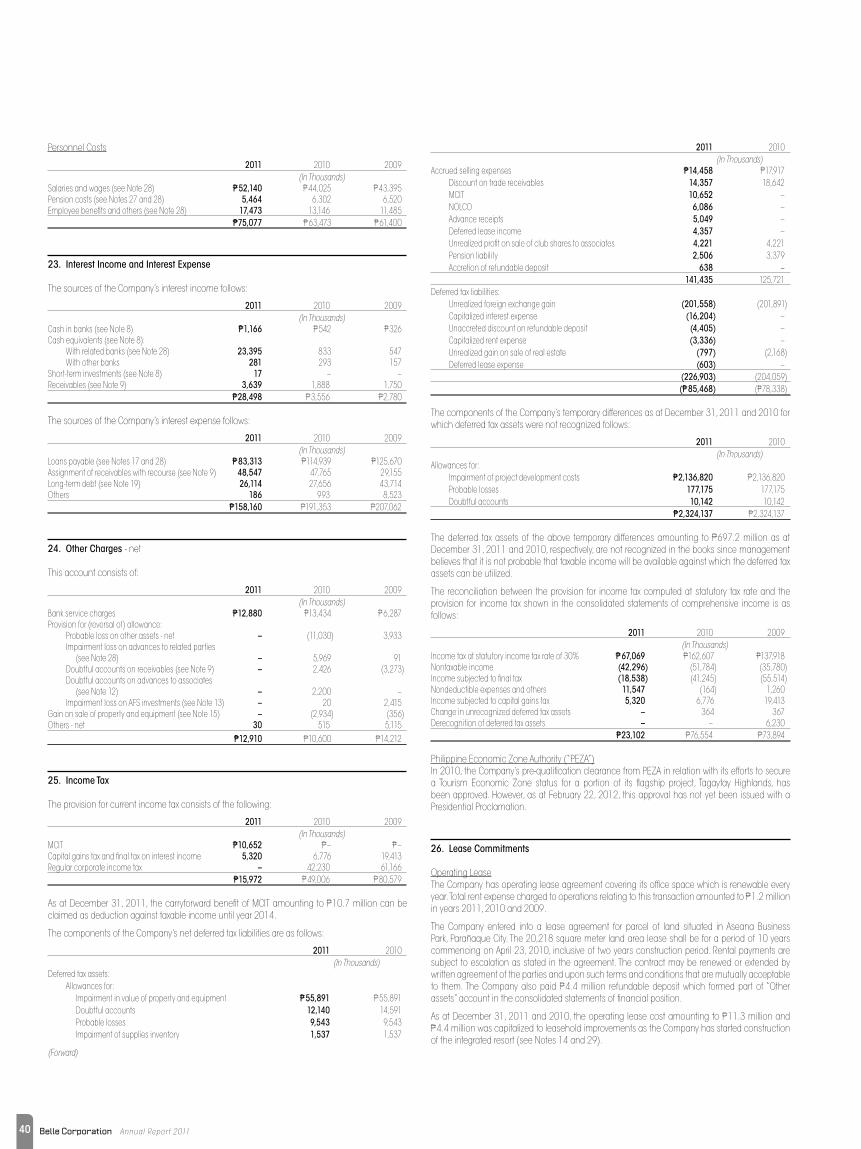

Provision for Income TaxCurrent provision for income tax was lower by P=33.0 million (67%) in 2011 due to lower sales in real estate and club shares.

Deferred income tax decreased by P=20.4 million (74%) in 2011 mainly due to recognition of deferred income tax assets on MCIT and NOLCO amounting to P=10.7 million and P=6.1 million, respectively.

Net IncomeAs a result of the foregoing, Belle Corporation realized consolidated net income of P=200.5 million for the year ended December 31, 2011. This is P=265.0 million (57%) lower than the consolidated net income of P=465.5 million for the year ended December 31, 2010. Moreover, the Company’s consistent profitability has allowed it to post positive consolidated retained earnings of P=338.2 million as of December 31, 2011.

13 Annual Repor t 2011 Belle Corporation

ManageMent discUssion and analYsis of oPerating PerforMance and financial condition

ASSETS

Total assets of the Company increased by P=12,115.4 million (115%), to P=22,643.5 million as of December 31, 2011, from P=10,528.1 million as of December 31, 2010, due to the increases in cash and cash equivalents, value of investments, subscription receivable from stock rights offering and acquisition of intangible assets.

Cash and cash equivalentsCash and cash equivalents increased by P=2,725.8 million to (6,640%) P=2,766.9 million in 2011 from P=41.1 million in 2010, due mostly to (i) subscription payments received from stockholders under the Company’s stock rights offering in September 2011 of P=977.0 million (ii) net proceeds from loans and long-term debt of P=2,751.0 million million (iii) cash generated from operations of P=417.7 million. The increases in cash and cash equivalents were offset by the expenditures for the construction of Belle Grande of P=1,940.9 million, an integrated resort complex to be located

TABLE 2: Horizontal Analysis Vertical Analysis December Increase (Decrease) 2011 2010 Amount % 2011 2010 (In Thousands) (Percentages)

ASSETSCash and Cash Equivalents P=2,766,880 P=41,052 P=2,725,828 6639.9% 12.2% 0.4%Short-term Investments 9,668 - 9,668 100.0% 0.0% 0.0%Receivables 930,124 1,116,402 (186,278) -16.75 4.1% 10.6%Subscription Receivables 2,082,920 - 2,082,920 100.0% 9.2% 0.0%Real Estate for Sale - at cost 3,036,153 3,012,896 23,257 0.8% 13.4% 28.6%Club Shares - at cost 2,786,148 2,816,442 (30,294) -1.1% 12.3% 26.8%Investments in and Advances to Associates 2,118,166 2,050,882 67,284 3.3% 9.4% 19.5%Available-for-sale Investments 22,336 13,751 8,585 62.4% 0.1% 0.1%Advances to Related Parties - net 457,764 449,958 7,806 1.7% 2.0% 4.3%Investment Properties under Construction 2,434,194 493,245 1,940,949 393.5% 10.8% 4.7%Property and Equipment 175,599 178,458 (2,859) -1.6% 0.8% 1.7%Intangible Asset 5,261,186 - 5,261,186 100.0% 23.2% 0.0%Other Assets 562,390 354,970 207,420 58.4% 2.5% 3.4% P=22,643,528 P=10,528,056 P=12,115,472 115.1% 100.0% 100.0%

LIABILITIES AND EQUITYLiabilitiesLoans payable P=2,155,857 P=1,743,069 P=412,788 23.7% 9.5% 16.6%Accounts payable and other liabilities 1,750,935 1,547,077 203,858 13.2% 7.7% 14.7%Income tax payable 8,258 - 8,258 100.0% 0.0% 0.0%Long-term debt 2,559,584 964,993 1,594,591 165.2% 11.3% 9.2%Pension liability 8,354 11,262 (2,908) -25.8% 0.0% 0.1%Deferred tax liabilities - net 85,468 78,338 7,130 9.1% 0.4% 0.7%Assignment of receivables with recourse - 5,027 (5,027) -100.0% 0.0% 0.0% Total Liabilities 6,568,456 4,349,766 2,218,690 51.1% 29.0% 41.3%

EquityAttributable to equity holders of the parent: Preferred stock - issued 1,000,000 1,000,000 - 0.0% 4.4% 9.5% Common stock - issued 9,170,770 6,350,900 2,819,870 44.45 40.5% 60.3% Common stock - subscribed 1,388,613 - 1,388,613 100.0% 6.1% 0.0% Additional paid-in capital 5,503,731 - 5,503,731 100.0% 24.3% 0.0% Equity share in cost of Parent Company shares held by associates (731,696) (731,696) - 0.0% -3.2% -6.9% Cost of Parent Company common shares held by subsidiaries (497,758) (497,758) - 0.0% -2.2% -4.7% Unrealized loss on available-for-sale investments 8,585 - 8,585 100.0% 0.0% 0.0% Retained earnings 338,243 137,726 200,517 145.6% 1.5% 1.3% Other reserves (52,369) (27,892) (24,477) 87.8% -0.2% -0.3%Total Equity Attributable to Equity Holders of the Parent 16,128,119 6,231,280 9,896,839 158.8% 71.2% 59.2%Non-controlling interests (53,047) (52,990) 57 0.1% -0.2% -0.5% Total Equity 16,075,072 6,178,290 9,896,782 160.2% 71.0% 58.7% P=22,643,528 P=10,528,056 P=12,115,472 115.1% 100.0% 100.0%

on approximately 6.2 hectares of land (of which 4.2 hectares are owned by the Company) along Roxas Boulevard in Parañaque City.

ReceivablesReceivables decreased by P=186.3 million (17%), to P=930.1 million in 2011 from P=1,116.4 million in 2010, the reduction was mainly due to collection of trade receivables.

Real Estate for Sale and Club SharesReal estate for sale increased by P=23.3 million (1%), to P=3,036.2 million in 2011 from P=3,012.9 million in 2010, due to the development of raw lands for various projects.

Club shares held by the Company, valued at historical cost, decreased by P=30.3 million (1%), to P=2,786.1 million in 2011 from P=2,816.4 million in 2010 due to sales made in 2011.

DECEMBER 31, 2011 vs DECEMBER 31, 2010 STATEMENT OF FINANCIAL POSITION (Table 2)

Belle Corporation Annual Repor t 201114

ManageMent discUssion and analYsis of oPerating PerforMance and financial condition

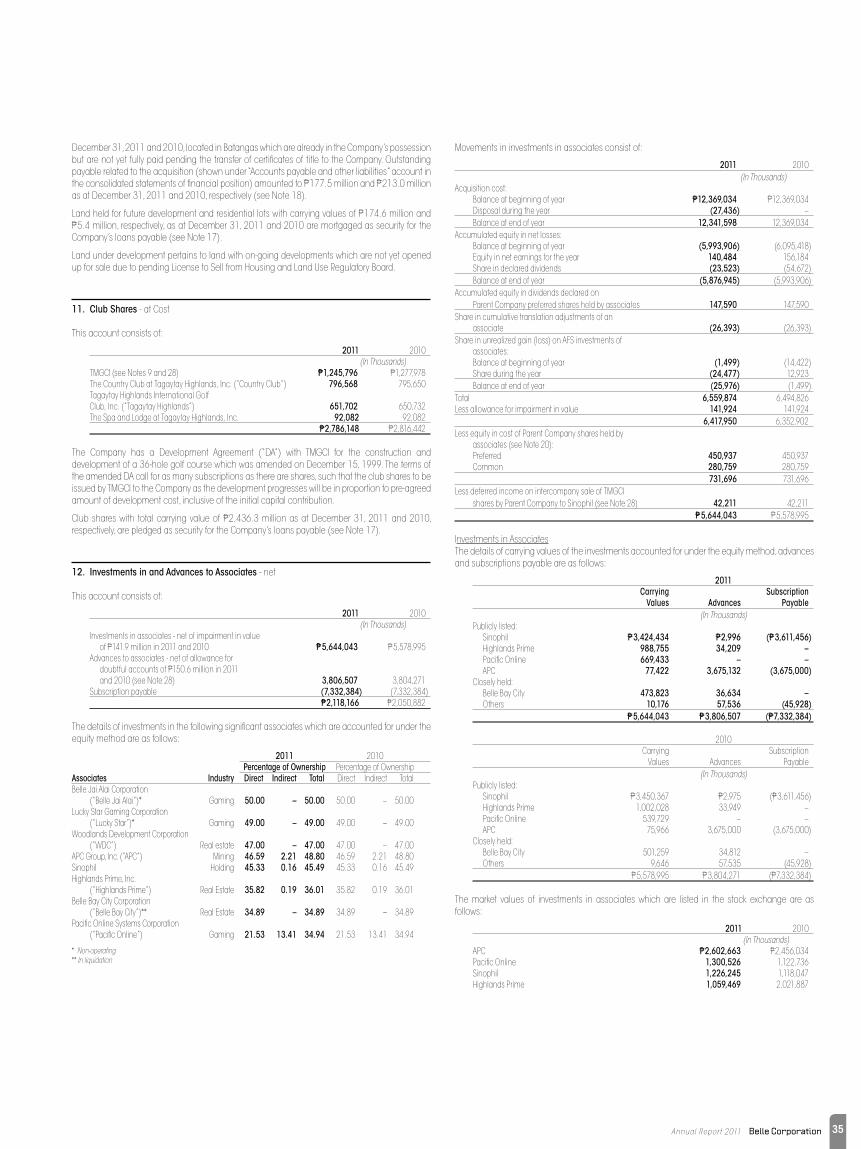

Investments in and Advances to AssociatesInvestments and advances increased by P=67.3 million (3%), to P=2,118.2 million in 2011 from P=2,050.9 million in 2010, due mainly to equity in net earnings of associates for the year.

Investment propertiesInvestment properties increased by P=1,941.0 million (394%), from P=493.2 million as of December 31, 2010 to P=2,434.2 million as of December 31, 2011, due mainly to the continuing construction of Belle Grande.

Intangible AssetIntangible asset increased by P=5,261.2 million (100%) of December 31, 2011, from nil as of December 31, 2010, due mainly to the acquisition of PLAI, a grantee by the Philippine Amusement and Gaming Corporation (PAGCOR) of a license to operate integrated resorts, including casinos.

On April 14, 2011, Belle has issued 2.7 billion new common shares valued at P=1.95 per share in exchange for 100% of the outstanding capital stock of PLAI.

LIABILITIES

Total liabilities increased by P=2,218.7 million (51%) to P=6,568.5 million as of December 31, 2011, from P=4,349.8 million as of December 31, 2010, due to borrowings for the construction of Belle Grande.

Loans Payable and Long-Term DebtTotal debt amounting to P=4,715.4 million in 2011 were comprised mostly of Peso loans from various local financial institutions, with interest at an approximate range of 7.0% to 7.5% per annum amounting to P=2,155.9 million, foreign-currency denominated Floating Rate Notes (“FRNs”), with a peso equivalent amounting to P=965.0 million and new peso long-term debt of P=1,594.6 million. The FRNs have a principal amount of US$22 million due on May 10, 2014 and carry interest at 2% per annum above the six-month LIBOR.

Total debt increased by P=2,007.3 million (74%), from P=2,708.1 million in 2010 to P=4,715.4 million in 2011, due to the availment of new peso long-term loans for the construction of Belle Grande.

Accounts payable and other liabilitiesAccounts payable and other liabilities increased by P=203.8 million (13%), to P=1,750.9 million in 2011 compared to P=1,547.1 million in 2010. Comprising accounts payable and other liabilities are principally trade payables of P=750.6 million, advances from related parties of P=214.6 million, accrued expenses of P=418.0 million, non-trade payables of P=332.5 million and customers’ deposits of P=35.2 million in 2011. The increase in the accounts payable and other liabilities is attributed to the construction of Belle Grande.

EQUITY

The Company’s equity as of December 31, 2011 of P=16,075.1 million was higher by P=9,896.8 million compared to the year-end 2010 level of P=6,178.3 million, due to: (i) the net income for 2011; (ii) the issuance of 2.7 billion new common shares for the acquisition of PLAI in April 2011 and (iii) the issuance and subscription of 1.5 billion new common shares in September 2011 as a result of the Company’s stock rights offering. The issuances and subscription of these new common shares also resulted in additional paid-in-capital of P=5,503.7 million as of December 31, 2011. Due to its consistent profitability, the Company had consolidated retained earnings of P=338.2 million as of December 31, 2011, compared to consolidated retained earnings of P=137.7 million as of December 31, 2010.

Below are the comparative key performance indicators of the Company and its subsidiaries:

Dec 31, 2011 (audited)

Dec 31, 2010 (audited)

Asset-to-equity ratio Total assets over stockholders’ equity 1.41 : 1.00 1.70 : 1.00

Current or Liquidity Ratio

Current assets over current liabilities 3.17 : 1.00 2.27 : 1.00

Debt-to-equity ratio Interest-bearing debt over stockholders’ equity 0.29 : 1.00 0.44 : 1.00

Net debt-to-equity ratio

Interest-bearing debt less cash and cash equivalents over stockholders’ equity

0.12 : 1.00 0.43 : 1.00

Interest rate coverage ratio EBIT over interest expense 2.41 : 1.00 3.83 : 1.00

Return on assets Net income over average total assets during the period 1.2% 4.5%

Return on equityNet income over average stockholders’ equity during the period

1.8% 7.8%

The Company does not foresee any cash flow or liquidity problems over the next twelve months. The P=2,155.9 million of debt obligations classified as loans payable have historically been mostly renewed or rolled-over, while the P=1,594.6 million long-term debt from the P=5.6 billion project finance facility from Banco de Oro Unibank for the Belle Grande project, will be amortized over a 5-year period starting December 2012. The Company’s FRN of P=965.0 million is due on May 10, 2014. Aside from the planned Belle Grande integrated resort project, Belle also has a number of revenue-generating real estate projects in the pipeline to enhance cash flow. Meanwhile, the Company continues to be in compliance with the terms of all of its debt obligations.

As of December 31, 2011, except for what has been noted in the preceding, there were no material events or uncertainties known to management that had a material impact on past performance, or that would have a material impact on the future operations, in respect of the following:

• Known trends,demands,commitments,eventsoruncertainties thatwouldhaveamaterialimpact on the Company;

• Material commitments for capital expenditures that are reasonably expected to have amaterial impact on the Company’s short-term or long-term liquidity;

• Knowntrends,eventsoruncertaintiesthathavehadorthatarereasonablyexpectedtohavea material favorable or unfavorable impact on net sales/revenues/income from continuing operations;

• Significant elements of income or loss that did not arise from the Company’s continuingoperations;

• SeasonalaspectsthathadamaterialimpactontheCompany’sresultsofoperations;and

• Material changes in the financial statements of the Company from the year ended December 31, 2010 to December 31, 2011.

REVENUES

Gross revenue for 2010 of P=1,263.1 million was lower by P=140.0 million (10%), compared to P=1,403.2 million during 2009. Gross profit as of December 2010 of P=754.1 million was also lower than gross profit as of December 2009 of P=836.9 million by P=82.8 million (10%), due to the lower revenues. However, the gross profit margin during 2010 of 59% was higher compared to 56% in 2009. This is due to the greater proportion in the 2010 revenue mix of Cotswold, which had a project gross margin of 62% and comprised 25% of 2010 gross revenues (compared to 10% of gross revenues in 2009) and Fairfield, which had a project gross margin of 65% and comprised 11% of 2010 gross revenues (compared to 3% in 2009). In contrast, a combined 27% of gross revenues in 2009 were comprised of Lakeside Fairways Phases 1- 5 (with an average project gross margin of 49% and a proportion to gross revenues of 12%) and Katsura (with a project gross margin of 50% and a proportion to gross revenues of 15%).

Cost of Real Estate and Club Shares SoldThe decrease of P=57.3 million (10%) in the cost of real estate and club shares sold from P=566.3 million in 2009 to P=509.0 follows the level of decrease in the sales of real estate and club shares.

General and Administrative ExpensesThe decrease of P=84.0 million (28%) in 2010 is mainly caused by the reduction in marketing and

advertising expense. It is partially offset by increased expenditures on professional fees and repairs and maintenance.

Equity in Net Earnings of AssociatesThe Company’s equitized net earnings from associated companies increased by P=38.3 million (32%) to P=156.2 million in 2010, from P=117.9 million in 2009. Equitized earnings were mainly from its 36%-owned associate, Highlands Prime, Inc. (HPI) and from its 35%-owned associate, Pacific Online Systems Corporation (Pacific Online). HPI is also engaged in real estate development within the Tagaytay Highlands and Midlands complexes, while Pacific Online leases on-line equipment to the Philippine Charity Sweepstakes Office for their lottery operations in the Visayas and Mindanao.

Financial Income (Expense)Interest expense decreased by P=15.7 million (8%), to P=191.4 million, from P=207.1 million in 2009 due to lower interest rates.

Foreign Exchange GainWith the appreciation of the Philippine Peso against the US Dollar to P=43.84:US$1.00 as of December 31, 2010, from P=46.20:US$1.00 as of December 31, 2009, the Company posted a P=51.5 million foreign exchange translation gain in 2010 from its US$22 million US Dollar-denominated debt, compared to a foreign exchange translation gain of P=28.9 million in 2009.

DECEMBER 31, 2010 VERSUS DECEMBER 31, 2009 RESULTS OF OPERATIONS (Table 3)

15 Annual Repor t 2011 Belle Corporation

TABLE 3: Year Ended December 31 Horizontal Analysis Vertical Analysis 2010 2009 Increase (Decrease) 2010 2009 (In Thousands) (Percentages)

REVENUE Sale of real estate and club shares P=1,163,986 P=1,259,814 (P=95,828) -7.6% 92.2% 89.8% Others 99,137 143,342 (44,205) -30.8% 7.8% 10.2% 1,263,123 1,403,156 (140,033) -10.0% 100.00% 100.0%COST OF REAL ESTATE AND CLUB SHARES (508,979) (566,300) (57,321) -10.1% -40.3% -40.4%GENERAL AND ADMINISTRATIVE ExPENSES (221,431) (305,421) (83,990) -27.5% -17.5% -21.8%INTEREST ExPENSE (191,353) (207,062) (15,709) -7.6% -15.1% -14.8%EQUITY IN NET EARNINGS OF ASSOCIATES 156,184 117,901 38,283 32.5% 12.4% 8.4%NET FOREIGN ExCHANGE GAIN 51,522 28,883 22,639 78.4% 4.1% 2.1%INTEREST INCOME 3,556 2,780 776 27.9% 0.3% 0.2%OTHER CHARGES - Net (10,600) (14,212) (3,612) -25.4% -0.8% -1.0%INCOME BEFORE INCOME TAx 542,022 459,725 82,297 17.9% 42.9% 32.8%PROVISION FOR INCOME TAx Current 49,006 80,579 (31,573) -39.2% 3.9% 5.7% Deferred 27,548 (6,685) 34,233 -512.1 2.2% -0.5% 76,554 73,894 2,660 3.6% 6.1% 5.3%NET INCOME 465,468 385,831 79,637 20.6% 36.9% 27.5%

Net profit attrbutable to: Equity holders of the parent 465,535 385,917 79,618 20.6% 36.9% 27.5% Non-controlling interests (67) (86) (19) -22.1% 0.0% 0.0% P=465,468 P=385,831 P=79,637 20.6% 36.9% 27.5%

Net IncomeBelle Corporation realized consolidated net income of P=465.5 million for the year ended December 31, 2010. This is P=79.7 million (21%) higher than the consolidated net income of P=385.8 million for the year ended December 31, 2009. Moreover, the Company’s consistent and substantial profitability has allowed it to post positive consolidated retained earnings of

P=137.7 million as of December 31, 2010. The Company’s consolidated retained earnings became positive for the first time since 1998, wiping out a consolidated deficit that peaked at P=5.8 billion as of December 31, 2001.

DECEMBER 31, 2010 VS DECEMBER 31, 2009 STATEMENT OF FINANCIAL POSITION (Table 4)

ASSETS

Total assets of the Company increased by P=554.6 million (6%), to P=10,528.1 million as of December 31, 2010, from P=9,973.5 million as of December 31, 2009, due mainly to the increases of the investments in advances and advances to associates and investment properties.

Cash and cash equivalentsCash and cash equivalents decreased by P=45.3 million (52%), to P=41.1 million from P=86.4 million in 2009. The decreases were mainly accounted for by the expenditure for the construction of investment properties (P=493.2 million) and payment of interest expense (P=189.0 million). The decreases in cash and cash equivalents were offset by the cash generated from operations of P=458.1 million.

ReceivablesReceivables decreased by P=108.6 million (9%), to P=1,116.4 million in 2010 from P=1,225.0 million in 2009, due to collection of trade receivables.

Real estate for sale and Club SharesReal estate for sale increased by P=77.0 million (3%), to P=3,012.9 million in 2010 from P=2,935.9 million in 2009, due to the development of raw lands for various projects.

Club shares held by the Company, valued at historical cost, increased by P=22.3 million (1%), to P=2,816.4 million in 2010 from P=2,794.1 million in 2009.

Investments in and advances to AssociatesInvestments in and advances to associates increased by P=119.0 million (6%), to P=2,050.9 million in 2010 from P=1,931.9 million in 2009, due mainly to equity in net earnings of associates for the year.

Investment properties and Property and EquipmentInvestment properties and property and equipment increased by P=500.3 million (292%), from P=171.4 million as of December 31, 2009 to P=671.7 million as of December 31, 2010, due mainly to the construction cost of the “Belle Grande Manila Bay”, an integrated resort complex located along Roxas Boulevard in Parañaque City.

LIABILITIES

Total liabilities increased by P=76.2 million (2%) to P=4,349.8 million as of December 31, 2010, from P=4,273.6 million as of December 31, 2009.

Loans Payable and Long-Term DebtTotal debt amounting to P=2,708.1 million were comprised mostly of Peso loans from various local financial institutions, with interest at an approximate range of 7.0% to 7.5% per annum, with the total of such Peso loans amounting to P=1,743.1 million, and which are predominantly secured. Foreign-currency denominated debt (Floating Rate Notes), with a Peso equivalent amounting to P=965.0 million as of December 31, 2010, comprise the balance of Belle’s total debt. The Floating Rate Notes have a principal amount of US$22 million due on May 10, 2014 and carry interest at 2% per annum above the six-month LIBOR. Total debt increased by P=145.3 million (6%), from P=2,562.8 million in 2009 to P=2,708.1 million in 2010. The increase was due mainly to the availment of new peso loans.

Accounts payable and other liabilitiesAccounts payable and other liabilities decreased by P=80.7 million (5%), to P=1,547.1 million in 2010 compared to P=1,627.8 million in 2009. Comprising accounts payable and other liabilities are principally trade payables of P=558.9 million, advances from related parties of P=212.7 million, accrued expenses of P=411.9 million, non-trade payables of P=316.6 million and customers’ deposits of P=47.0 million.

EQUITY

The Company’s equity as of December 31, 2010 of P=6,178.3 million was higher by P=478.4 million (8%) compared to the year-end 2009 level of P=5,699.9 million, due mainly to the net income recorded for 2010. Due to its consistent profitability since 2002, the Company attained consolidated retained earnings of P=137.7 million as of December 31, 2010, compared to a consolidated deficit of P=327.8 million as of December 31, 2009.

Belle Corporation Annual Repor t 201116

TABLE 4: Horizontal Analysis Vertical Analysis December Increase (Decrease) 2010 2009 Amount % 2010 2009 (In Thousands) (Percentages)

ASSETSCash and Cash Equivalents P=41,052 P=86,382 (P=45,330) -52.5% 0.4% 0.9%Receivables - net 1,116,402 1,225,046 (108,644) -8.9% 10.6% 12.3%Real Estate for Sale - at cost 3,012,896 2,935,901 76,995 2.6% 28.6% 29.4%Club Shares - at cost 2,816,442 2,794,066 22,376 0.8% 26.8% 28.0%Investments in and Advances to Associates 2,050,882 1,931,885 118,997 6.2% 19.5% 19.4%Available-for-sale Investments 13,751 13,014 737 5.7% 0.1% 0.1%Advances to Related Parties - net 449,958 460,342 (10,384) -2.3% 4.3% 4.6%Investment Properties 493,245 - 493,245 100.0% 4.7% 0.0%Property and Equipment - net 178,458 171,364 7,094 4.1% 1.7% 1.7%Other Assets - net 354,970 355,462 (492) -0.1% 3.4% 3.6% P=10,528,056 P=9,973,462 P=554,594 5.6% 100.0% 100.0%LIABILITIES AND EQUITYLiabilitiesLoans payable P=1,743,069 P=1,545,828 P=197,241 12.8% 16.6% 15.5%Accounts payable and other liabilities 1,547,077 1,627,774 (80,697) -5.0% 14.7% 16.3%Long-term debt 964,993 1,016,941 (51,948) -5.1% 9.2% 10.2%Assignment of receivables with recourse 5,027 16,417 (11,390) -69.4% 0.0% 0.2%Pension liability 11,262 14,093 (2,831) -20.1% 0.1% 0.1%Obligations under finance lease - 1,720 (1,720) -100.0% 0.0% 0.0%Deferred tax liabilities - net 78,338 50,970 27,548 54.2% 0.7% 0.5% Total Liabilities 4,349,766 4,273,563 76,203 1.8% 41.3% 42.8%EquityAttributable to equity holders of the parent: Preferred stock - issued 1,000,000 1,000,000 - 0.0% 9.5% 10.0% Common stock - issued 6,350,900 6,350,900 - 0.0% 60.3% 63.7% Equity share in cost of Parent Company shares held by associates (731,696) (731,696) - 0.0% -6.9% -7.3% Additional paid-in capital 5,503,731 - 5,503,731 100.05 24.35 0.0% Cost of Parent Company common shares held by subsidiaries (497,758) (497,758) - 0.0% -4.7% -5.0% Retained earnings (Deficit) 137,726 (327,809) 465,535 -142.0% 1.3% -3.3% Other reserves (27,892) (40,815) 12,923 -31.7% -0.3% -0.4%Total Equity Attributable to Equity Holders of the Parent 6,231,280 5,752,822 478,458 8.3% 59.2% 57.7%Non-controlling interests (52,990) (52923) (67) 0.1% -0.5% -0.5% Total Equity 6,178,290 5,699,899 478,391 8.4% 58.7% 57.2% P=10,528,056 P=9,973,462 P=554,594 5.6% 100.0% 100.0%

Below are the comparative key performance indicators of the Company and its subsidiaries:

Dec 31, 2010(audited)

Dec 31, 2009(audited)

Asset-to-equity ratio

Total assets over stockholders’ equity 1.70 : 1.00 1.75 : 1.00

Current or Liquidity Ratio

Current assets over current liabilities 2.27 : 1.00 2.36 : 1.00

Debt-to-equity ratio

Interest-bearing debt over stockholders’ equity 0.44 : 1.00 0.45 : 1.00

Net debt-to-equity ratio

Interest-bearing debt less cash and cash equivalents over stockholders’ equity

0.43 : 1.00 0.43 : 1.00

Interest rate coverage ratio

EBIT over interest expense 3.83 : 1.00 3.22 : 1.00

Return on assets Net income over average total assets during the period 4.5% 3.9%

Return on equityNet income over average stockholders’ equity during the period

7.8% 7.0%

The Company does not foresee any cash flow or liquidity problems over the next twelve months. The P=1,743.1 million of debt obligations classified as loans payable have historically been mostly renewed or rolled-over, with Belle paying only interest. Belle has also a number of revenue-generating real estate projects in the pipeline to enhance cash flow. The Company is in compliance with all of its debt obligations.

As of December 31, 2010, except for what has been noted in the preceding, there were no material events or uncertainties known to management that had a material impact on past performance, or that would have a material impact on the future operations, in respect of the following:

• Known trends,demands,commitments,eventsoruncertainties thatwouldhaveamaterialimpact on the Company;

• Material commitments for capital expenditures that are reasonably expected to have amaterial impact on the Company’s short-term or long-term liquidity;

• Knowntrends,eventsoruncertaintiesthathavehadorthatarereasonablyexpectedtohavea material favorable or unfavorable impact on net sales/revenues/income from continuing operations;

• Significant elements of income or loss that did not arise from the Company’s continuingoperations;

• SeasonalaspectsthathadamaterialimpactontheCompany’sresultsofoperations;and

• MaterialchangesinthefinancialstatementsoftheCompanyfromtheyearendedDecember31, 2009 to December 31, 2010.

17 Annual Repor t 2011 Belle Corporation

February 22, 2012

SECURITIES AND EXCHANGE COMMISSIONSEC Building, EDSA GreenhillsMandaluyong City, Metro Manila

The management of Belle Corporation and Subsidiaries is responsible for the preparation and fair presentation of the consolidated financial statements for the years ended December 31, 2011 and 2010, including the additional components attached therein, in accordance with Philippine Financial Reporting Standards. This responsibility includes designing and implementing internal controls relevant to the preparation and fair presentation of the consolidated financial statements that are free from material misstatement, whether due to fraud or error, selecting and applying appropriate accounting policies, and making accounting estimates that are reasonable in the circumstances.

The Board of Directors reviews and approves the consolidated financial statements and submits the same to the stockholders.

SyCip Gorres Velayo & Co., the independent auditors, appointed by the stockholders has examined the consolidated financial statements of the Company in accordance with Philippine Standards on Auditing, and in its report to the stockholders, has expressed its opinion on the fairness of presentation upon completion of such examination.

BENITO TAN GUATChairman of the Board

ROGELIO R. CABUÑAGPresident

MANUEL A. GANAExecutive Vice President and Chief Financial Officer

Belle Corporation Annual Repor t 201118

stateMent of ManageMent’s resPonsiBilitY for consolidated financial stateMents

The Stockholders and the Board of DirectorsBelle Corporation

We have audited the accompanying consolidated financial statements of Belle Corporation and Subsidiaries, which comprise the consolidated statements of financial position as at December 31, 2011 and 2010, and the consolidated statements of comprehensive income, statements of changes in equity and statements of cash flows for each of the three years in the period ended December 31, 2011, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with Philippine Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Philippine Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Belle Corporation and Subsidiaries as at December 31, 2011 and 2010, and their financial performance and their cash flows for each of the three years in the period ended December 31, 2011 in accordance with Philippine Financial Reporting Standards.

SYCIP GORRES VELAYO & CO.

ROEL E. LUCASPartnerCPA Certificate No. 98200SEC Accreditation No. 1079-A (Group A), February 3, 2011, valid until February 2, 2014Tax Identification No. 191-180-015BIR Accreditation No. 08-001998-95-2011, February 4, 2011, valid until February 3, 2014PTR No. 3174806, January 2, 2012, Makati City

February 22, 2012

19 Annual Repor t 2011 Belle Corporation

indePendent aUditor’s rePort

Belle Corporation Annual Repor t 201120

consolidated stateMents of financial Position (amounts in thousands)

December 31 2011 2010ASSETS Cash and Cash Equivalents (Notes 8, 28, 32 and 33) P=2,766,880 P=41,052Short-term Investments (Notes 8, 28, 32 and 33) 9,668 –Receivables (Notes 9, 28, 32 and 33) 930,124 1,116,402Subscription Receivables (Notes 20 and 33) 2,082,920 –Real Estate for Sale - at cost (Notes 10, 17, 18 and 33) 3,036,153 3,012,896Club Shares - at cost (Notes 11, 17, 28 and 33) 2,786,148 2,816,442Investments in and Advances to Associates - net (Notes 12, 17, 19, 20, 28, 32 and 33) 2,118,166 2,050,882Available-for-sale Investments (Notes 13 and 32) 22,336 13,751Advances to Related Parties - net (Notes 28, 32 and 33) 457,764 449,958Investment Properties under Construction (Notes 14, 26 and 29) 2,434,194 493,245Property and Equipment (Notes 15 and 22) 175,599 178,458Intangible Asset (Notes 16, 29 and 34) 5,261,186 –Other Assets (Notes 19 and 26) 562,390 354,970 P=22,643,528 P=10,528,056

LIABILITIES AND EQUITY Liabilities Loans payable (Notes 10, 11, 12, 13, 17, 28, 32 and 33) P=2,155,857 P=1,743,069Accounts payable and other liabilities (Notes 10, 18, 28, 32 and 33) 1,750,935 1,547,077Income tax payable 8,258 –Long-term debt (Notes 19, 28 and 32) 2,559,584 964,993Pension liability (Note 27) 8,354 11,262Deferred tax liabilities - net (Note 25) 85,468 78,338 Assignment of receivables with recourse (Notes 9, 28, 32 and 33) – 5,027 Total Liabilities 6,568,456 4,349,766Equity Attributable to equity holders of the parent: Preferred stock - issued (Notes 20 and 28) 1,000,000 1,000,000 Common stock (Note 20): Issued 9,170,770 6,350,900 Subscribed 1,388,613 – Additional paid-in capital (Notes 16 and 20) 5,503,731 – Equity share in cost of Parent Company shares held by associates (Notes 12 and 20) (731,696) (731,696) Cost of Parent Company common shares held by subsidiaries (Note 20) (497,758) (497,758) Unrealized gain on available-for-sale investments (Note 13) 8,585 – Retained earnings (Note 20) 338,243 137,726 Other reserves (Note 12) (52,369) (27,892) Total Equity Attributable to Equity Holders of the Parent 16,128,119 6,231,280Non-controlling interests (53,047) (52,990) Total Equity 16,075,072 6,178,290 P=22,643,528 P=10,528,056 See accompanying Notes to Consolidated Financial Statements.

21 Annual Repor t 2011 Belle Corporation

consolidated stateMents of coMPrehensiVe incoMe (amounts in thousands, except Per share amounts)

Years Ended December 31 2011 2010 2009REVENUE Sale of real estate and club shares (Note 28) P=520,176 P=1,163,986 P=1,259,814Lease income (Note 29) 62,070 – –Others (Notes 9 and 21) 114,275 99,137 143,342 696,521 1,263,123 1,403,156COST OF REAL ESTATE AND CLUB SHARES SOLD (Note 22) (235,983) (508,979) (566,300)GENERAL AND ADMINISTRATIVE ExPENSES (Notes 15, 22, 26, 27 and 28) (235,158) (221,431) (305,421)INTEREST ExPENSE (Notes 9, 17, 19, 23 and 28) (158,160) (191,353) (207,062)EQUITY IN NET EARNINGS OF ASSOCIATES (Note 12) 140,484 156,184 117,901INTEREST INCOME (Notes 8, 9, 23 and 28) 28,498 3,556 2,780NET FOREIGN ExCHANGE GAIN 270 51,522 28,883OTHER CHARGES - Net (Notes 9, 12, 13, 15, 24 and 28) (12,910) (10,600) (14,212)INCOME BEFORE INCOME TAx 223,562 542,022 459,725PROVISION FOR (BENEFIT FROM) INCOME TAx (Note 25) Current 15,972 49,006 80,579Deferred 7,130 27,548 (6,685) 23,102 76,554 73,894

NET INCOME (Note 31) 200,460 465,468 385,831

OTHER COMPREHENSIVE INCOME (LOSS) Unrealized gain (loss) on available-for-sale investments of associates (Note 12) (24,477) 12,923 (21,721)Unrealized gain on available-for-sale investments (Note 13) 8,585 – – (15,892) 12,923 (21,721)TOTAL COMPREHENSIVE INCOME FOR THE YEAR P=184,568 P=478,391 P=364,110Net profit attributable to: Equity holders of the parent (Note 31) P=200,517 P=465,535 P=385,917 Non-controlling interests (57) (67) (86) P=200,460 P=465,468 P=385,831Total comprehensive income attributable to: Equity holders of the parent P=184,625 P=478,458 P=364,196 Non-controlling interests (57) (67) (86) P=184,568 P=478,391 P=364,110Basic/Diluted Earnings Per Share (Note 31) P=0.023 P=0.075 P=0.062 See accompanying Notes to Consolidated Financial Statements.

Belle Corporation Annual Repor t 201122

consolidated stateMents of changes in eQUitY (amounts in thousands)

for the Years ended december 31, 2011, 2010 and 2009

Attributable to Equity Holders of the Parent Attributable to Equity Holders of the Parent Other Reserves Equity Share Share in in Cost Cost of Unrealized of Parent Parent Unrealized Share in Gain (Loss) on Company Company Gain on Cumulative Available- Preferrred Additional Shares Held Common Available- Translation for-Sale Retained Stock Common Paid-in by Associates Share Held for-Sale Adjustments of Investments Earnings (Notes 20 Stock Capital (Notes 12 by Subsidiaries Investments an Associate of Associates (Deficit) Non-controlling and 28) (Note 20) (Note 20) and 20) (Note 20) (Note 13) (Note 12) (Note 12) (Note 20) Total Interests Total EquityBalance at December 31, 2010 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P26,393) (P=1,499) P=137,726 P=6,231,280 (P=52,990) P=6,178,290Issuance during the year – 2,819,870 2,776,140 – – – – – – 5,596,010 – 5,596,010Subscriptions during the year – 1,388,613 2,727,591 – – – – – – 4,116,204 – 4,116,204Net income – – – – – – – – 200,517 200,517 (57) 200,460Other comprehensive income (loss) – – – – – 8,585 – (24,477) – (15,892) – (15,892)Total comprehensive income for the year (loss) – – – – – 8,585 – (24,477) 200,517 184,625 (57) 184,568Balance at December 31, 2011 P=1,000,000 P=10,559,383 P=5,503,731 (P=731,696) (P=497,758) P=8,585 (P=26,393) (P=25,976) P=338,243 P=16,128,119 (P=53,047) P=16,075,072

Balance at December 31, 2009 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=14,422) (P=327,809) P=5,752,822 (P=52,923) P=5,699,899Net income – – – – – – – – 465,535 465,535 (67) 465,468Other comprehensive income – – – – – – – 12,923 – 12,923 – 12,923Total comprehensive income for the year – – – – – – – 12,923 465,535 478,458 (67) 478,391Balance at December 31, 2010 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=1,499) P=137,726 P=6,231,280 (P=52,990) P=6,178,290

Balance at December 31, 2008 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) P=7,299 (P=713,726) P=5,388,626 (P=52,837) P=5,335,789Net income – – – – – – – – 385,917 385,917 (86) 385,831Other comprehensive loss – – – – – – – (21,721) – (21,721) – (21,721)Total comprehensive income (loss) for the year – – – – – – – (21,721) 385,917 364,196 (86) 364,110Balance at December 31 , 2009 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=14,422) (P=327,809) P=5,752,822 (P=52,923) P=5,699,899

See accompanying Notes to Consolidated Financial Statements.

23 Annual Repor t 2011 Belle Corporation

Attributable to Equity Holders of the Parent Attributable to Equity Holders of the Parent Other Reserves Equity Share Share in in Cost Cost of Unrealized of Parent Parent Unrealized Share in Gain (Loss) on Company Company Gain on Cumulative Available- Preferrred Additional Shares Held Common Available- Translation for-Sale Retained Stock Common Paid-in by Associates Share Held for-Sale Adjustments of Investments Earnings (Notes 20 Stock Capital (Notes 12 by Subsidiaries Investments an Associate of Associates (Deficit) Non-controlling and 28) (Note 20) (Note 20) and 20) (Note 20) (Note 13) (Note 12) (Note 12) (Note 20) Total Interests Total EquityBalance at December 31, 2010 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P26,393) (P=1,499) P=137,726 P=6,231,280 (P=52,990) P=6,178,290Issuance during the year – 2,819,870 2,776,140 – – – – – – 5,596,010 – 5,596,010Subscriptions during the year – 1,388,613 2,727,591 – – – – – – 4,116,204 – 4,116,204Net income – – – – – – – – 200,517 200,517 (57) 200,460Other comprehensive income (loss) – – – – – 8,585 – (24,477) – (15,892) – (15,892)Total comprehensive income for the year (loss) – – – – – 8,585 – (24,477) 200,517 184,625 (57) 184,568Balance at December 31, 2011 P=1,000,000 P=10,559,383 P=5,503,731 (P=731,696) (P=497,758) P=8,585 (P=26,393) (P=25,976) P=338,243 P=16,128,119 (P=53,047) P=16,075,072

Balance at December 31, 2009 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=14,422) (P=327,809) P=5,752,822 (P=52,923) P=5,699,899Net income – – – – – – – – 465,535 465,535 (67) 465,468Other comprehensive income – – – – – – – 12,923 – 12,923 – 12,923Total comprehensive income for the year – – – – – – – 12,923 465,535 478,458 (67) 478,391Balance at December 31, 2010 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=1,499) P=137,726 P=6,231,280 (P=52,990) P=6,178,290

Balance at December 31, 2008 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) P=7,299 (P=713,726) P=5,388,626 (P=52,837) P=5,335,789Net income – – – – – – – – 385,917 385,917 (86) 385,831Other comprehensive loss – – – – – – – (21,721) – (21,721) – (21,721)Total comprehensive income (loss) for the year – – – – – – – (21,721) 385,917 364,196 (86) 364,110Balance at December 31 , 2009 P=1,000,000 P=6,350,900 P=– (P=731,696) (P=497,758) P=– (P=26,393) (P=14,422) (P=327,809) P=5,752,822 (P=52,923) P=5,699,899

See accompanying Notes to Consolidated Financial Statements.

Belle Corporation Annual Repor t 201124

consolidated stateMents of cash floWs (amounts in thousands)

Years Ended December 31 2011 2010 2009

CASH FLOWS FROM OPERATING ACTIVITIES Income before income tax P=223,562 P=542,022 P=459,725Adjustments for: Interest expense (Note 23) 158,160 191,353 207,062 Equity in net earnings of associates (Note 12) (140,484) (156,184) (117,901) Amortization of discount on trade receivables (Notes 9 and 21) (54,465) (44,409) (74,185) Interest income (Note 23) (28,498) (3,556) (2,780) Depreciation and amortization (Notes 15 and 22) 27,059 21,179 29,878 Gain on sale of: Investment (Note 12) (10,234) – – Property and equipment (Note 24) – (2,934) (356) Pension costs (Notes 22 and 27) 5,464 6,302 6,520 Dividend income (278) (371) (245) Unrealized foreign exchange loss (gain) - net 31 (51,620) (29,055) Provision for (reversal of) allowance: Probable loss on other assets (Note 24) – (11,030) 3,933 Impairment loss on advances to related parties (Note 24) – 5,969 91 Impairment loss on advances to associates (Notes 12, 24 and 28) – 2,200 – Impairment loss on available-for-sale investments (Notes 13 and 24) – 20 2,415Income before changes in working capital 180,317 498,941 485,102Decrease (increase) in: Receivables 246,136 170,190 (228,914) Club shares 30,294 (22,376) 191,381 Real estate for sale (23,257) (76,995) 163,475 Other assets (207,420) (67,831) 13,303Increase (decrease) in accounts payable and other liabilities 184,607 (31,478) (313,778)Contributions to the retirement fund (Note 27) (8,372) (9,133) (9,381)Net cash generated from operations 402,305 461,318 301,188Income tax paid (7,714) (6,776) (19,413)Interest received 23,105 3,556 2,780Net cash provided by operating activities 417,696 458,098 284,555

CASH FLOWS FROM INVESTING ACTIVITIES Acquisitions of: Short-term investments (9,668) – – Available-for-sale investments (Note 13) – (757) – Property and equipment (Note 15) (24,200) (28,393) (82,308)Expenditures on investment properties under construction (Note 14) (1,940,949) (493,245) –Decrease (increase) in investments in and advances to associates and related parties (19,123) (2,345) (7,118)Dividends received 44,692 37,906 36,490Proceeds from disposal of: Investments in an associate (Note 12) 25,125 – 11,900 Property and equipment – 3,054 741Net cash used in investing activities (1,924,123) (483,780) (40,295)

CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from: Availment of loans (Notes 17 and 19) 2,379,855 607,547 – Stock rights offering (Note 20) 2,368,108 – –Payments of: Loans payable (371,868) (410,306) (1,184) Interest (140,783) (188,978) (215,944) Assignment of receivables with recourse (5,027) (11,390) (24,273) Obligations under capital lease – (1,720) (3,471)Increase (decrease) in advances from related parties 1,874 (14,473) 25,815Net cash provided by (used in) financing activities 4,232,159 (19,320) (219,057)

EFFECT OF ExCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS 96 (328) –NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 2,725,828 (45,330) 25,203CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 41,052 86,382 61,179CASH AND CASH EQUIVALENTS AT END OF YEAR (Note 8) P=2,766,880 P=41,052 P=86,382

See accompanying Notes to Consolidated Financial Statements.

1. General Information

Corporate InformationBelle Corporation (“Belle” or “Parent Company”) is a stock corporation organized in the Philippines on August 20, 1973 and was listed at the Philippine Stock Exchange (“PSE”) on February 2, 1977. The businesses of Belle, direct and through subsidiaries and associates, include mainly real estate development, principally in the high-end leisure property market, and various investment holdings (see Note 12).

The registered office address of Belle is 28th Floor, East Tower, Philippine Stock Exchange Centre, Exchange Road, Ortigas Center, Pasig City.

Authorization of the Issuance of the Consolidated Financial StatementsThe accompanying consolidated financial statements were authorized for issue in accordance with a resolution of the Board of Directors (“BOD”) on February 22, 2012.

2. Basis of Preparation and Statement of Compliance

Basis of PreparationThe consolidated financial statements have been prepared on a historical cost basis, except for certain available-for-sale (“AFS”) investments that have been measured at fair value (see Note 13). The consolidated financial statements are presented in Philippine peso, the Parent Company’s functional and presentation currency, and all values are rounded to the nearest thousands, except when otherwise indicated.

Statement of ComplianceThe consolidated financial statements of the Company have been prepared in accordance with Philippine Financial Reporting Standards (“PFRS”).

Basis of ConsolidationThe consolidated financial statements comprise the financial statements of Belle and the following subsidiaries (collectively referred to as “the Company”) that it controls:

Subsidiaries Percentage of Ownership 2011 2010 2009Belle Bay Plaza Corporation* (Belle Bay Plaza) 100 100 100Colossal Construction Corporation* 100 100 100Metropolitan Leisure and Tourism Corporation* 100 100 100Parallax Resources, Inc. (Parallax) 100 100 100SLW Development Corporation* (SLW) 100 100 100PremiumLeisure and Amusement, Inc. (PLAI) 100 – –Highland Gardens Corporation* (HGC) 80 80 80* Non-operating

The subsidiaries are all incorporated in the Philippines.

The subsidiaries are consolidated from the date of acquisition, being the date on which the Parent Company obtains control, and continue to be consolidated until the date that such control ceases.

The financial statements of the subsidiaries are prepared for the same reporting year as the Parent Company using consistent accounting policies. All significant intercompany balances, transactions, income and expense and profits and losses from intercompany transactions are eliminated in full in the consolidation.

3. Changes in Accounting Policies and Disclosures

The accounting policies adopted in the preparation of the consolidated financial statements are consistent with those of the previous financial year, except for the adoption of the following new, revised and amended Philippine Accounting Standards (“PAS”), PFRS and Philippine Interpretations from International Financial Reporting Interpretations Committee (“IFRIC”) which were adopted as at January 1, 2011. The adoption of the following amendments and interpretations did not have material effect on the accounting policies, financial position or performance of the Company, except for additional disclosures.

• PAS 24, Related Party Disclosures (Amendment)

PAS 24 clarifies the definitions of a related party. The new definitions emphasize a symmetrical view of related party relationships and clarify the circumstances in which persons and key management personnel affect related party relationships of an entity. In addition, the amendment introduces an exemption from the general related party disclosure requirements for transactions with government and entities that are controlled, jointly controlled or significantly influenced by the same government as the reporting entity.

• PAS 32, Financial Instruments: Presentation (Amendment) - Classification of Rights Issues

The amendment alters the definition of a financial liability in PAS 32 to enable entities to classify rights issues and certain options or warrants as equity instruments. The amendment is applicable if the rights are given pro rata to all of the existing owners of the same class of an entity’s non-derivative equity instruments, to acquire a fixed number of the entity’s own equity instruments for a fixed amount in any currency.

• Philippine Interpretation IFRIC 14 (Amendment), Prepayments of a Minimum Funding Requirement

The amendment removes an unintended consequence when an entity is subject to minimum funding requirements and makes an early payment of contributions to cover such requirements. The amendment permits a prepayment of future service cost by the entity to be recognized as a pension asset. The Company is not subject to minimum funding requirements in the Philippines.

Improvements to PFRS (Issued 2010)

Improvements to PFRSs, an omnibus of amendments to standards, deal primarily with a view to removing inconsistencies and clarifying wording. There are separate transitional provisions for each standard. The adoption of the following amendments resulted in changes to accounting policies but did not have any impact on the financial position or performance of the Company.

• PFRS 3, Business Combinations: The measurement options available for non-controlling interest (“NCI”) were amended. Only components of NCI that constitute a present ownership interest that entitles their holder to a proportionate share of the entity’s net assets in the event of liquidation should be measured at either fair value or at the present ownership instruments’ proportionate share of the acquiree’s identifiable net assets. All other components are to be measured at their acquisition date fair value.

The amendments to PFRS 3 are effective for annual periods beginning on or after July 1, 2011. The Company, however, adopted these as of January 1, 2011 and changed its accounting policy accordingly as the amendment was issued to eliminate unintended consequences that may arise from the adoption of PFRS 3.

• PFRS 7, Financial Instruments - Disclosures — The amendment was intended to simplify the disclosures provided by reducing the volume of disclosures around collateral held and improving disclosures by requiring qualitative information to put the quantitative information in context. The Company reflects the revised disclosure requirements in Note 32.

• PAS1,Presentation of Financial Statements — The amendment clarifies that an entity may present an analysis of each component of other comprehensive income maybe either in the statement of changes in equity or in the notes to the financial statements. The Company provides this analysis in the consolidated statement of changes in equity.

Other amendments resulting from the 2010 improvements to PFRSs to the following standards did not have any impact on the accounting policies, financial position or performance of the Company:

• PFRS3,Business Combinations [contingent consideration arising from business combination prior to adoption of PFRS 3 (as revised in 2008)]

• PFRS3, Business Combinations (un-replaced and voluntarily replaced share-based payment awards)

• PAS27,Consolidated and Separate Financial Statements• PAS34,Interim Financial Statements

The following interpretation and amendments to interpretations did not have any impact on the accounting policies, financial position or performance of the Company:

• PhilippineInterpretationIFRIC13, Customer Loyalty Programmes (determining the fair value of award credits)

• PhilippineInterpretationIFRIC19,Extinguishing Financial Liabilities with Equity Instruments

4. Summary of Significant Accounting Policies

Cash and Cash EquivalentsCash includes cash on hand and in banks. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash with original maturity of three months or less from date of acquisition and are subject to an insignificant risk of change in value.

Financial Assets

Initial Recognition and Classification. Financial assets are recognized initially at fair value plus, in the case of investments not fair value through profit or loss (“FVPL”), directly attributable transaction costs.

Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the marketplace (regular way purchases) are recognized on the settlement date, i.e., the date that an asset is delivered to or by the Company.

Financial assets are classified as financial assets as at FVPL, loans and receivables, held-to-maturity (“HTM”) investments or AFS investments. The Company determines the classification of its financial assets at initial recognition and where allowed and appropriate, re-evaluates such classification every financial reporting date. The Company has no financial assets as at FVPL and HTM investments as at December 31, 2011 and 2010.

25 Annual Repor t 2011 Belle Corporation

notes to consolidated financial stateMents

Subsequent Measurement. The subsequent measurement of financial assets depends on their classification as follows:

• LoansandReceivables

Loans and receivables are nonderivative financial assets with fixed or determinable payments that are not quoted in an active market. Such financial assets are carried at amortized cost using the effective interest rate method less any allowance for impairment. Gains and losses are recognized in profit or loss in the consolidated statement of comprehensive income when the loans and receivables are derecognized or impaired, as well as through the amortization process.

This category includes the Company’s cash in banks and cash equivalents, short-term investments, receivables, advances to associates as shown under “Investments in and advances to associates” account in the consolidated statement of financial position and advances to related parties (see Note 32).

• AFSInvestments

AFS investments are those nonderivative financial assets that are designated as AFS investments or are not classified as FVPL, loans and receivables and HTM. The Company designates financial instruments as AFS if they are purchased and held indefinitely and may be sold in response to liquidity requirements or changes in market conditions. After initial measurement, AFS investments are measured at fair value with unrealized gains or losses recognized as other comprehensive income in the consolidated statement of comprehensive income until the investment is derecognized or determined to be impaired, at which time, the cumulative gain or loss is recognized in profit or loss in the consolidated statement of comprehensive income. AFS investments in equity instruments that do not have a quoted market price in an active market, or derivatives linked to such equity instruments are measured at cost because its fair value cannot be measured reliably.

For a financial asset reclassified out of the AFS investment category, any previous gain or loss on that asset that has been recognized in other comprehensive income is amortized to profit or loss in the consolidated statement of comprehensive income over the remaining life of the investment using the effective interest method. Any difference between the new amortized cost and the expected cash flows is also amortized over the remaining life of the asset using the effective interest method. If the asset is subsequently determined to be impaired, then the amount recorded in the consolidated statement of changes in equity is reclassified to the profit or loss in the consolidated statement of comprehensive income.

Where the Company holds more than one investment in the same security, these are deemed to be disposed of on a moving average basis. Interest earned on holding AFS investments are reported as interest income using the effective interest rate. Dividends earned on holding AFS investments are recognized in profit or loss in the consolidated statement of comprehensive income when the right to receive payment has been established. The losses arising from impairment of such financial assets are recognized in profit or loss in consolidated statement of comprehensive income.

This category includes the Company’s investments in quoted and unquoted equity securities shown under “Available-for-sale Investments” account in the consolidated statement of financial position (see Note 32).

Financial Liabilities

Initial Recognition and Classification. Financial liabilities are recognized initially at fair value and in the case of other financial liabilities, inclusive of any directly attributable transaction costs.

Financial liabilities are classified as financial liabilities as at FVPL or other financial liabilities which are measured at amortized cost. The Company determines the classification of its financial liabilities at initial recognition. The Company has no financial liabilities as at FVPL as at December 31, 2011 and 2010.

Subsequent Measurement. After initial recognition, interest-bearing other financial liabilities are subsequently measured at amortized cost using the effective interest rate method. Gains and losses are recognized in profit or loss in the consolidated statement of comprehensive income when the liabilities are derecognized as well as through the amortization process.

This category includes the Company’s loans payable, accounts payable and other liabilities (excluding statutory payables and other liabilities to the government), long-term debt and assignment of receivables with recourse (see Note 32).

Offsetting of Financial Assets and Financial LiabilitiesFinancial assets and financial liabilities are offset and the net amount is reported in the consolidated statement of financial position if, and only if, there is a currently enforceable right to offset the recognized amounts and there is intention to settle on a net basis, or to realize the asset and settle the liability simultaneously.

Determination of Fair Value and Fair Value Hierarchy of Financial Assets and Financial Liabilities The fair value for financial assets and financial liabilities traded in active markets at reporting date is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and asking prices are not available, the price of the most recent transaction provides evidence of the current fair value as long as there has not been a significant change in economic circumstances

since the time of the transaction.