156

ANNUAL REPORT 2013 - 14 LANCO INFRATECH LIMITED

ANNUAL REPORT 2013 - 14LANCO INFRATECH LIMITED

With a core mandate of “Always Inspiring” driving our business mandate, it’s not surprising

that our initiatives come with the imperative of far reaching outcomes. Our customary far-

sightedness has helped us understand the dynamics of challenging environments and

accordingly align ourselves to consolidate and deliver. Across our business interests - EPC,

Power, Solar, Natural Resources, Infrastructure, Property Development - our goal is one of

consolidation and consistencies. An outcome-oriented approach has enabled us to reach this

far. In these challenging times, we have persevered with the conviction that our long-term

strategies will have a positive impact on all those we are associated with and the world at large.

EPC

POWER CSRSOLAR

NATURALRESOURCES INFRASTRUCTURE

PROPERTYDEVELOPMENT

EPC

Our reputation for impeccable project management competencies has established us as the

first choice amongst leading enterprises for EPC projects. An ability to straddle a project from

“concept to commissioning” bringing together the crucial parameters of cost and quality has

earned us a rich portfolio of EPC projects.

With strong engineering competencies across industry verticals such as power, transmission,

industrial and transportation segments, our decade-old expertise in EPC is definitely one of

our many strengths.

POWER

Our proven prowess in power generation has made us one of the nation’s leading power

producers and one of largest private sector players in the Indian power trading market. We

have consolidated our strengths and integrated our presence across the value chain. This in

turn has facilitated us in capturing an elevated value addition across the businesses.

We currently have an installed capacity of 4722 MW and a capacity under construction of

4636 MW. One of our under construction project has recently signed a Long Term Power

Purchase Agreement of 25 years with UPPCL Discoms under Case 1 Bid.

SOLAR

Renewable energy is all about being sustainable, innovative and cost-effective, while catering

to the ever-increasing energy needs. Our goal of indigenizing alternate technologies with

the aim to reduce costs and achieve grid parity is manifested in our fully integrated strategy

- ‘Sand to Power’. We are focused on commercializing technologies for green and efficient

energy generation systems such as solar thermal and solar photovoltaic (PV).

Currently we have a solar farm development portfolio of 143 MW (Operating - 43 MW and

Under Construction - 100 MW).

NATURAL RESOURCES

The coal business has always been our key area of focus. Our strategic move towards ‘Project

Integration’ has enabled us to extend our natural resources’ operating portfolio and under-

development assets in India and across the globe. With more than 2 billion tonnes of coal

resources in our business portfolio, we are reckoned as one of the exclusive members among

the mine developers & operators in India.

The recent appointment as Mine Developer & Operator (MDO) by Steel Authority of India

Ltd., for the Tasra Coal Block including washery and captive power project has reiterated our

strengths in Natural Resources.

INFRASTRUCTURE

The successful execution and completion of impressive civil & urban projects has earned us

our prominent position in the Infrastructure development sector. Today, we are proving our

mettle in selective infrastructure projects by leveraging our EPC experience and construction

expertise.

The projects currently under our highway portfolio include two major National Highway (NH)

projects in the State of Karnataka and one project in the State of Uttar Pradesh.

PROPERTY DEVELOPMENT

Foraying into Property Development, we have created one of Hyderabad’s most desired

destinations - Lanco Hills. Conceptualized to be ‘a world within’, it is spread over 100 acres

and comprises of residential spaces, office space & IT SEZ, retail and entertainment options.

This USD 1.5 billion mega project owes its magnificence to the meticulous detailing by

renowned architects & consultants. With breathtaking vistas, esthetically landscaped gardens

and high-rise living, Lanco Hills is reckoned to be one of the world’s largest single-phase

development projects.

Board of Directors

Mr. L. Madhusudhan RaoExecutive Chairman

Mr. G. Venkatesh BabuManaging Director

Mr. P. AbrahamDirector

Mr. G. Bhaskara RaoExecutive Vice - Chairman

Mr. S. C. ManochaDeputy Managing Director

Dr. Uddesh Kumar KohliDirector

Mr. L. SridharVice - Chairman

Dr. Pamidi KotaiahDirector

Mr. R. KrishnamoorthyDirector

7

Contents Year at a Glance 9Directors’ Report 10Management Discussion and Analysis 16Report on Corporate Governance 32Abridged Financial Statements

Auditors’ Report 47Balance Sheet 54Statement of Profit and Loss Account 55Cash Flow Statement 56Notes to Abridged Financial Statements 56Consolidated Financial StatementsAuditors’ Report 79Balance Sheet 82Statement of Profit and Loss Account 83Cash Flow Statement 84Notes to Consolidated Financial Statements 85

Bankers and Financial Institution of the CompanyAllahabad Bank Andhra BankAxis Bank LimitedBank of Baroda Bank of MaharashtraCanara BankCentral Bank of India Corporation BankDena BankHDFC Bank Limited ICICI Bank LimitedIDBI Bank Limited Indian Overseas BankIDFC LimitedING Vysya Bank Limited Kotak Mahindra Bank Limited Life Insurance Corporation of India Oriental Bank of Commerce Punjab & Sind BankPunjab National BankSrei Equipment Finance Private Limited State Bank of Bikaner & JaipurState Bank of HyderabadState Bank of India State Bank of MysoreState Bank of PatialaSiemens Financial Services Private LimitedTATA Capital Financial Services LimitedCatholic Syrian Bank Limited The Jammu & Kashmir BankUnion Bank of IndiaUnited Bank of IndiaYes Bank Limited

Board of Directors

Mr. L. Madhusudhan Rao - Executive Chairman

Mr. G. Bhaskara Rao - Executive Vice-Chairman

Mr. L. Sridhar - Vice-Chairman

Mr. G. Venkatesh Babu - Managing Director

Mr. S. C. Manocha - Deputy Managing Director

Dr. Pamidi Kotaiah - Director

Mr. P. Abraham - Director

Dr. Uddesh Kumar Kohli - Director

Mr. R. Krishnamoorthy - Director

Chief Operating Officer Finance Mr. T. Adi Babu

Compliance Officer Mr. A. Veerendra Kumar

Auditors Brahmayya & Co.,(Registration No. - 000511S)Chartered Accountants48, Masilamani Road, Balaji Nagar, RoyapettahChennai - 600 014Tamil Nadu, India

Registered Office Plot No.4, Software Units Layout, HITEC CityMadhapur, Hyderabad – 500 081, Telangana, IndiaPhone: +91-40-4009 0400, Fax: +91-40-2311 6127E-mail: [email protected]: www.lancogroup.comCorporate Identity Number: L45200TG1993PLC015545

Corporate OfficeLanco House, Plot No. 397, Udyog Vihar, Phase-3Gurgaon–122 016, Haryana, IndiaPhone: +91-124-474 1000, Fax: +91-124-474 1878

Registrar & Share Transfer AgentAarthi Consultants Private Limited1-2-285, Domalguda, Hyderabad – 500 029 Telangana, India Phone: +91-40-2763 8111, 2763 4445 Fax: +91-40-2763 2184E-mail: [email protected]: www.aarthiconsultants.com

Corporate InformationAnnual Report 2013-2014

8

(` Crores) Change

PARTICULARS 2013-2014 2012-2013 (%)

Profit and Loss AccountGross Revenue 10,875.27 15,295.86 -29

Less: Elimination of Inter Segment Revenue 277.42 1,408.20 -80

Net Revenue 10,597.85 13,887.66 -24

Profit Before Depreciation, Interest and Taxation (PBITDA) 1,671.87 2,653.33 -37

Depreciation and Amortisation 1,171.91 1,125.81 4

Profit Before Interest and Taxation 499.96 1,527.52 -67

Eliminated Profit on transactions with Subsidiaries (15.05) (17.58) -14

Profit Before Interest and Taxation Plus Elimination 484.91 1,509.94 -68

Interest and Finance Charges 2,762.12 2,421.44 14

Profit / (Loss) Before Taxation, Exceptional Item Plus Elimination (2,277.21) (911.50) 150

Exceptional Item (179.26) - 100

Profit / (Loss) Before Taxation Plus Elimination (2,456.47) (911.50) 169

Provision for Taxation (Including Deferred Tax and MAT Credit Entitlement) (129.44) 179.62 -172

Profit / (Loss) After Tax (Before Minority Interest & Share of Profits from Associates) (2,327.03) (1,091.12) 113

Share of Minority Interest (115.64) (11.22) 931

Share of Profits / (Loss) from Associates (33.89) (2.88) 1,077

Profit / (Loss) After Tax (After Minority Interest and Share of Profits from Associates) Plus Elimination (2,245.28) (1,082.78) 107

Prior Period Items 43.50 (12.62) -445

Elimination of Profit on Transactions with Subsidiaries and Associates (14.90) 3.14 -575

Profit / (Loss) After Tax (After Minority Interest and Share of Profits from Associates) (2,273.88) (1,073.30) 112

Cash Profit (743.40) 232.92 -419

Cash Flow Cash from Operating Activities before Elimination 1,345.37 1,869.51 -28

Balance SheetShare Capital 239.24 239.24 0

Reserves & Surplus 1,218.30 3,433.22 -65

Minority Interest 837.48 934.18 -10

Net Worth Plus Minority 2,295.02 4,606.64 -50

Eliminated Profit on Transactions with Subsidiaries and Associates (Cumulative) 1,501.17 1,516.06 -1

Net Worth Plus Minority & Elimination 3,796.19 6,122.70 -38

Non Current Liabilities 34,354.22 30,971.56 11

Current Liabilities 14,194.93 15,243.06 -7

Total of Net Worth Plus Minority & Liabilities 50,844.17 50,821.26 0.05

Non Current Assets 40,253.03 39,333.96 2

Current Assets 10,591.14 11,487.30 -8

Total of Assets 50,844.17 50,821.26 0

Key indicatorsEarning Per Share (In `)

Basic (9.68) (4.58) 111

Diluted (9.68) (4.58) 111

No. of Employees 4,000 5,710 -30

Year at a glance - Consolidated

9

Dear Members,

Your Directors are pleased to present the Twenty First Annual Report on the Business and Operations of the Company together with the Audited Accounts for the year ended March 31, 2014.

FINANCIAL RESULTS

(` Crores)

PARTICULARSCONSOLIDATED STANDALONE

Year ended March 31 Year ended March 312014 2013 2014 2013

INCOMERevenue from operations and other income 10,597.85 13,887.66 2,339.37 4,822.75

Profit Before Taxation (2,441.42) (893.92) (959.99) 10.23

Provision for Taxation (129.44) 179.62 - (3.11)

Net Profit after Taxation (2,311.98) (1,073.54) (959.99) 13.34

Less: Prior period items 43.50 (12.62) - -

Add: Share of Profit/(Loss) of Associates (33.89) (2.88) - -

Less: Elimination of Unrealized Profit on Transactions with Associate Companies

0.15 20.72 - -

Less: Share of Minority Interest (115.64) (11.22) - -

Net Profit/ (Loss) after Taxation, Minority Interest and Share of Profit/ (Loss) of Associates (Balance Carried to Balance Sheet)

(2,273.88) (1,073.30) (959.99) 13.34

Surplus brought forward 382.23 1,455.54 1,479.10 1,465.76

Balance carried to Balance Sheet (1,891.65) 382.23 519.11 1,479.10

DIRECTORS’ REPORT

OPERATIONS AND BUSINESS REVIEw

On a Consolidated basis, your Company has reported Gross Revenues of ` 10,597.85 Crores as against ` 13,887.66 Crores of Revenues registered in the previous year. Total Expenditure for the Year was ` 12,860.01 Crores as against ` 14,781.58 Crores in the previous year. The Earnings Before Interest, Tax, Depreciation and Amortization (EBITDA) amounted to ` 1,671.87 Crores while the same was ` 2,653.33 Crores for the previous year i.e. a decrease of 37%. The Profit before taxation stood at ` (2,441.42) Crores, a decrease of 173.11 % as compared to ` (893.92) Crores in the last year.

The Net Profit/(Loss) after Tax after adjustment of Minority Interest and Share of Profits of Associates was ` (2,273.88) Crores as against ` (1,073.30) Crores for the previous year.

Gross Interest and Finance charges on consolidated basis amounted to ̀ 2,762.12 Crores in comparison to ̀ 2,421.44 Crores due to increase in loans and Working Capital Requirements for Project Execution.

During the year your company sold 10 MW wind based power plant situated near Tirunalveli, Tamilnadu and recognised the profit on sale of assets of ` 8.99 Crores.

A detailed discussion on the results of the operations, financial condition and business review is included in the Management Discussion and Analysis section placed at Annexure-II to this Report.

CDR PACKAGE:

Corporate Debt Restructuring Empowered Group (CDR EG) in its meeting held on December 11, 2013 has approved the CDR package submitted by the Company and issued letter of approval on December 20, 2013. As on March 31, 2014 CDR related documents have been executed and creation of security has been completed partly and the balance is in the process.

The proposal is only for the Company and not for any of its subsidiaries and associates.

Terms of CDRl Re-schedule of Term loan and short term loans are having

moratorium period of 2 years from the cut off date of April 1, 2013 and are repayable in 30 quarterly instalments starting from June 30, 2015.

l Portion of CDR Working Capital Loans on the cut off date i.e. April 1, 2013, has been carved out as Working Capital Term Loan - I (WCTL- I). LC/ BC/ BG devolved from cut off date till December 31, 2013 has been carved out as Working Capital Term Loan - II (WCTL- II).

l Funded Interest on Term Loans, WCTL - I and WCTL - II can be funded for a period of 2 years from cut off date i.e. April 1, 2013 to March 31, 2015 and on regular Cash Credit limit for an initial period of 6 months from cut off date i.e. April 1, 2013 to

Annual Report 2013-2014

10

September 30, 2013 is converted into Funded Interest Term Loan (FITL). Interest on FITL to be paid on monthly basis from April 30, 2013.

l ` 2,500 Crores Priority Loan sanctioned with a moratorium period of 2 years at an interest rate of 12.5% and is repayable in 18 quarterly instalments starting from June 30, 2015.

l Rate of interest on restructured facilities being 11% p.a. to be increased in a stepped up manner up to 16% p.a. starting from financial year 2016-17.

l Waiver of penal charges from the cut-off date to the date of implementation of the package.

l The Company shall raise funds by sale of assets/divestment of shares in SPV’s/securitisation/QIP/IPO etc. to repay the above restructured facilities under CDR scheme.

In relation to the amount outstanding as at March 31, 2014 against the loans restructured by the CDR lenders, a total amount of ` 2,224.89 Crores would qualify for the conversion into 354.50 Crores shares at the sole discretion and on demand of the CDR lenders.

In terms of CDR Package, the promoters brought into the company as unsecured loan a total amount of ` 152.00 Crores and the same would qualify for the conversion into 24.40 Crores shares at the sole discretion of the promoters.

The CDR gives your Company critical support to tide over the present difficult business environment. The decision of the banks to consider and approve CDR also reflects the faith these institutions have in the long term business model of the Company.

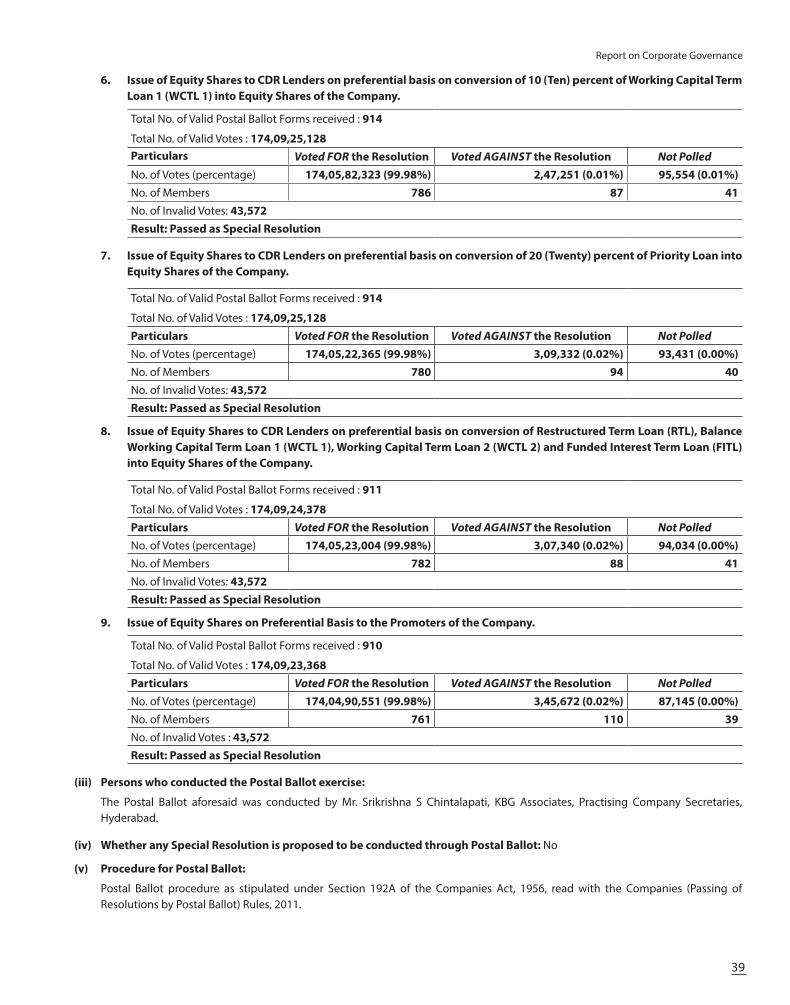

RESOLUTIONS PASSED THROUGH POSTAL BALLOT

During the reporting period, your Company had obtained shareholders approval by passing of resolutions through Postal Ballot. The results of the Postal Ballot were announced on April 17, 2014. The details of the resolutions passed through Postal Ballot forms part of the Report on Corporate Governance, annexed to this report.

AMEMDMENT TO MEMORANDUM AND ARTICLES OF ASSOCIATION

During the period under review, the Memorandum of Association of the Company was amended to increase the Authorised Share Capital of the Company from ` 500,00,00,000/- (Rupees Five Hundred Crores only) to ` 12,000,00,00,000/- (Rupees Twelve Thousand Crores only). This increase was necessitated to provide option to the CDR Lenders for conversion of loans into equity. The Articles of Association of the Company was also amended to reflect the increase of Authorised Capital and to provide option for buy-back of securities of the Company.

DIRECTORS

Mr. G. Bhaskara Rao and Mr. L. Sridhar retire by rotation at the ensuing Annual General Meeting and being eligible offer themselves for appointment. Dr. Pamidi Kotaiah retires by rotation at the ensuing

Annual General Meeting. Your Directors place on record their appreciations of the valuable contribution by Dr. Pamidi Kotaiah during his tenure as Director.

Mr. P. Abraham, Dr. Uddesh Kumar Kohli and Mr. R. Krishnamoorthy were appointed as Independent Directors of the Company in terms of Section 149 of the Companies Act, 2013.

The Company had received approvals from the Ministry of Corporate Affairs, Government of India, New Delhi, in respect of waiver from recovery of excess remuneration paid to Mr. L. Madhusudhan Rao, Executive Chairman and Mr. G. Bhaskara Rao, Executive Vice-Chairman, by the Company for the financial year 2012-13 and for payment of managerial remuneration to Mr. L. Madhusudhan Rao, Executive Chairman and Mr. G. Bhaskara Rao, Executive Vice-Chairman for the financial year 2013-14, by the Company.

Applications are being submitted to the Ministry of Corporate Affairs, Government of India, New Delhi, seeking approval for payment of managerial remuneration to Mr. L. Madhusudhan Rao, Executive Chairman, Mr. G. Bhaskara Rao, Executive Vice-Chairman, Mr. G. Venkatesh Babu, Managing Director and Mr. S.C. Manocha, Deputy Managing Director, for the period starting from April 01, 2014 till the tenure of their current appointment.

Dr. B. Vasanthan resigned as Director of the Company with effect from May 23, 2014.

DIVIDEND

Your Directors have not recommended dividend for the year ended March 31, 2014.

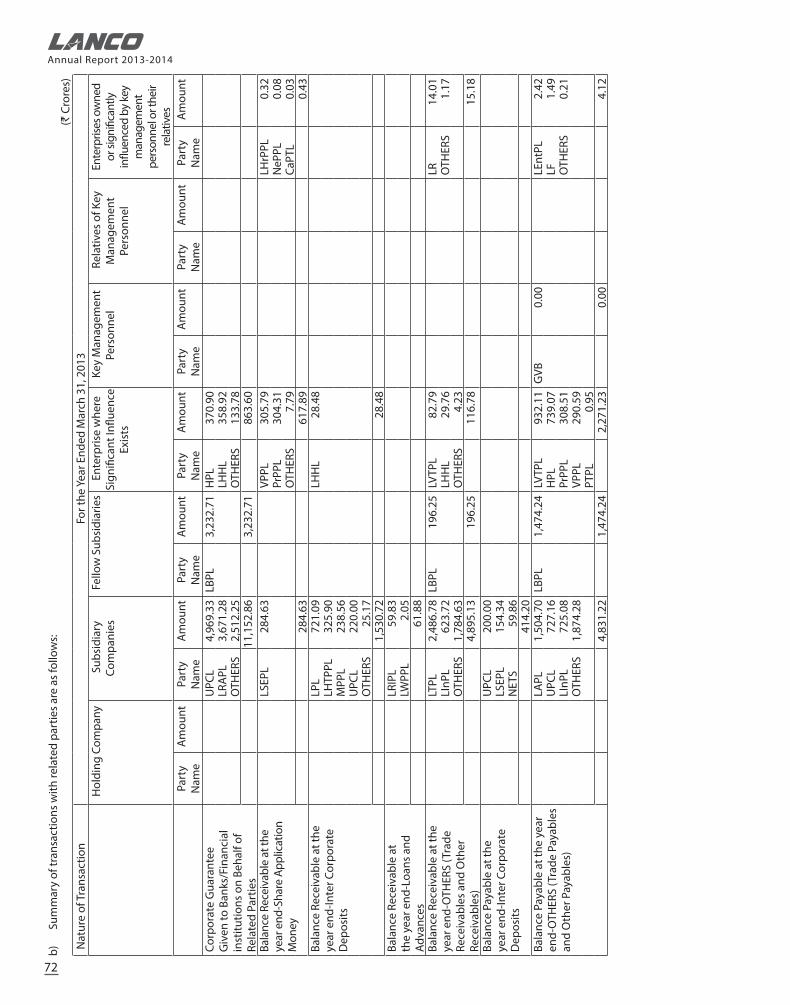

SUBSIDIARY COMPANIES

During the year under review, Tasra Mining & Energy Company Private Limited and Sirajganj Electric (Pvt) Limited had become subsidiaries of the Company. Further, Approve Choice Investments Limited, Apricus S.R.L, Bar Mount Trading (Pty.) Limited, Barrelake Investments (Pty.) Limited, Belara Trading (Pty.) Limited, Caelamen (Pty.) Limited, Dupondius (Pty.) Limited, Gamblegreat Trading (Pty.) Limited, Lexton Trading (Pty.) Limited, Lanco Rocky Face Land Holdings LLC and Lanco Tracy City Land Holdings LLC, had ceased to be Subsidiaries of the Company. Also during the reporting period, Lanco Teesta Hydro Power Limited, Subsidiary of the Company had changed its status from Private Limited to Public Limited Company.

The Ministry of Corporate Affairs vide their General Circular No. 2/2011, dated February 08, 2011 had granted general exemption to the Companies under Section 212(8) of the Companies Act, 1956 from the requirement to attach detailed financial statements of each subsidiary. The detailed financial statements and audit reports of each subsidiary are available for inspection at the Registered Office of the Company during office hours and upon written request from shareholder(s), your Company will arrange to send the financial statements of subsidiary companies to the said shareholder(s).

In terms of the Ministry of Corporate Affairs, General Circular 08/2014 No.1/19/2013-CL-V, dated April 04, 2014, the Auditors Report and Board’s Report in respect of financial years that commenced earlier

Directors’ Report

11

than April 01, 2014 shall be governed by the relevant provisions/Schedules/rules of the Companies Act, 1956. The financial information of the Subsidiaries of the Company was provided accordingly.

INVESTOR EDUCATION AND PROTECTION FUND

During the year under review, pursuant to Section 205C and other applicable provisions of the Companies Act, 1956, an amount of ` 1,16,640/- (Rupees One Lakh Sixteen Thousand Six Hundred and Forty only) was transferred to Investor Education and Protection Fund, with respect to share application money remained unclaimed for a period of 7 years by the unsuccessful bidders of the Initial Public Offering (IPO) of the Company.

HEALTH, SAFETY AND ENVIRONMENT

Lanco has taken up a very good initiative in implementing a world-class Health, Safety & Environment (HSE) Management System by implementing British 5 Star Safety Programs. The entire leadership supported this initiative and sites personnel were instrumental in giving a perfect shape to this new initiative.

The group has started its process improvement programs in HSE and is in process to bring out a compliance based tool to enhance the HSE performance across the group.

Lanco’s HSE performance is realized with an excellent recognition of our efforts in HSE and its sustenance. The world renowned “Sword of Honour” by British Safety Council, UK was conferred to Lanco’s Tanjore Site soon after getting awarded with 5-Star rating. Also, Lanco’s HSE culture got further boost as Kondapalli & Anuppur sites won the Prestigious “Prashansha Patra” conferred by National Safety Council of India (NSCI). Other sites, which have participated in various HSE awards and won during the year, make us proud. A brief description is below:

Company AwardLanco Infratech Limited- EPC Division

l NSCI Safety Awards, “Prashansha Patra” to Anuppur Site

Lanco Tanjore Power Company Limited

l “Sword of Honour” by British Safety Council

l Environment protections and management award from Government of Tamilnadu

l CII 4 Star ESH Awards, Southern RegionLanco Amarkantak Power Limited

l NSCI Safety Awards, “Prashansha Patra”

Udupi Power Corporation Limited

l CII 4 Star ESH Awards, Southern Region

l Golden Peacock “Environment Management Award”

Lanco Kondapalli Power Limited

l NSCI Safety Awards, “Prashansha Patra”

FIxED DEPOSITS

Your Company has not accepted fixed deposits falling within the provisions of Section 58A of the Companies Act, 1956 read with the Companies (Acceptance of Deposits) Rules, 1975, during the year under review.

AUDITORS

The Auditors of the Company, Brahmayya & Co., Chartered Accountants, (Firm Registration No. 000511S) retire at the conclusion of the ensuing Annual General Meeting of the Company and have confirmed their willingness and eligibility for appointment for the four consecutive years and have also confirmed that their appointment, if made, will be within the limits prescribed under the Companies Act, 2013.

COST AUDITORS

DZR & Co., Cost and Management Accountants have been reappointed as the Cost Auditors for the year ending March 31, 2014, as recommended by the Audit Committee. The Cost Audit Report for the year ended March 31, 2013 was due for filing on September 30, 2013 and was filed on September 29, 2013.

DISCLOSURE OF PARTICULARS wITH RESPECT TO CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION AND FOREIGN ExCHANGE EARNINGS AND OUTGO

Your Directors present the abridged accounts under Section 219 of the Companies Act, 1956. Pursuant to the Companies (Central Government’s) General Rules and Forms, 1956 read with Section 219(1)(b)(iv) of the Companies Act, 1956, the Particulars of Conservation of Energy, Technology Absorption and Foreign Exchange Earnings and Outgo as required under Section 217(1)(e) of the Companies Act, 1956, read with the Companies (Disclosure of Particulars in the Report of Board of Directors) Rules, 1988 have not been provided. However, these particulars are available for inspection at the Registered Office of the Company and upon written request from a shareholder, we will arrange to mail these details.

DISCLOSURE ON COMPANY’S EMPLOYEES STOCK OPTION PLANS

The Employees Stock Option Plan - 2006 and the Employees Stock Option Plan–2010 were approved by shareholders by passing Special Resolutions in the Extraordinary General Meeting held on June 07, 2006 and Annual General Meeting held on July 31, 2010, respectively.

The required information pursuant to Clause 12 of the Securities and Exchange Board of India (Employee Stock Option Scheme and Employee Stock Purchase Scheme) Guidelines, 1999, as amended, is enclosed as Annexure-I to this Report.

PARTICULARS OF EMPLOYEES

Your Directors present the abridged accounts under Section 219 of the Companies Act, 1956. Pursuant to the Companies (Central Government’s) General Rules and Forms, 1956 read with Section 219(1)(b)(iv) of the Act, the Particulars of Employees as required by Section 217(2A) of the Companies Act, 1956, read with the Companies (Particulars of Employees) Rules, 1975 have not been provided. However, these particulars are available for inspection at the Registered Office of the Company and upon written request from a shareholder, we will arrange to mail these details.

Annual Report 2013-2014

12

MANAGEMENT DISCUSSION AND ANALYSIS

The Management Discussion and Analysis as required under Clause 49 of the Listing Agreement is enclosed as Annexure-II to this Report.

CORPORATE GOVERNANCE

In compliance with the conditions of Corporate Governance, pursuant to Clause 49 of the Listing Agreements with Stock Exchanges, the Report on Corporate Governance with the Certificate from a Practicing Company Secretary certifying compliance in this regard forms part of this Report.

DIRECTORS’ RESPONSIBILITY STATEMENT

As required by Section 217(2AA) of the Companies Act, 1956, your Directors hereby confirm that:

(i) in the preparation of the annual accounts, the applicable accounting standards have been followed and that no material departures are made from the same;

(ii) we have selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give true and fair view of the state of affairs of the Company at the end of the financial year and of the profit/loss of the Company for the period;

(iii) we have taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of the Companies Act, 1956, for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities; and

(iv) we have prepared the annual accounts on a going concern basis.

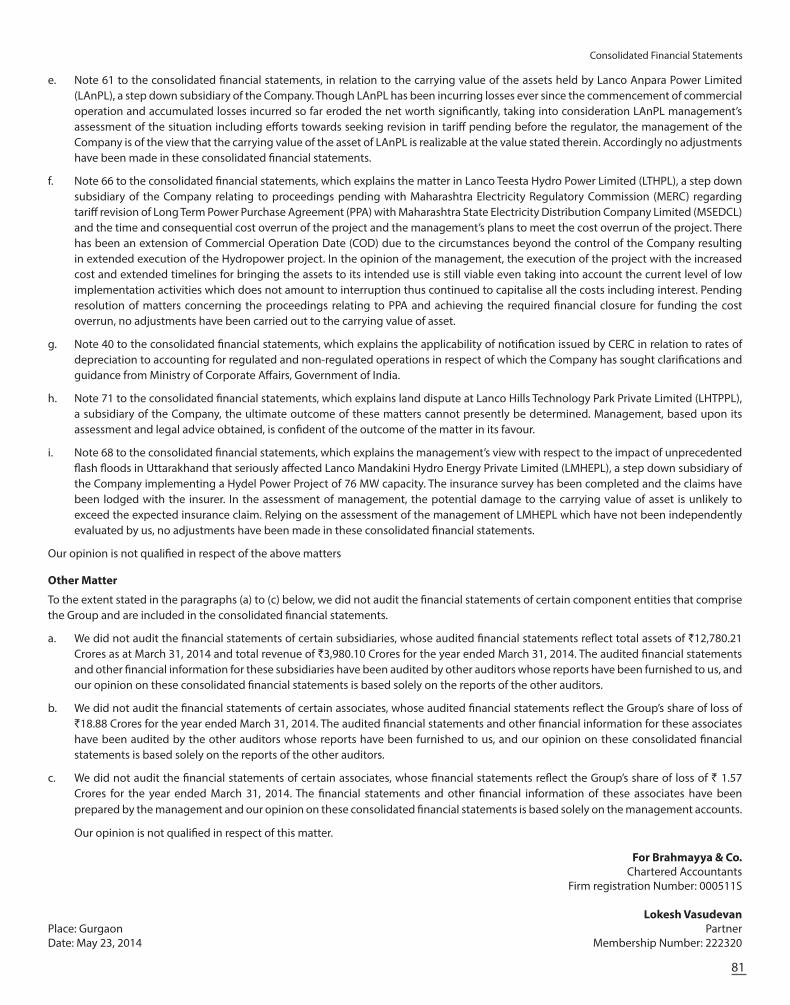

INFORMATION ON AUDITORS’ QUALIFICATIONS:

The information and explanations of your Directors on the qualifications by the Auditors on Abridged and Consolidated Statements are as follows:

l Qualification on reorganization of Investments in Power SPV’s:

The qualification by the Auditor is not about deviation from the Accounting Standards but on the pending approval of the lenders for the shares transfer to wholly owned subsidiaries. To meet the business requirements of augmenting the equity funding from private equity investors, strategic investors, the Power Holding Company structure was created and shares were transferred to the wholly owned subsidiaries. The share transfer does not alter the financial statements at the consolidated level/standalone level. The Company’s investment as of March 30, 2012 in various subsidiaries and associates was transferred to wholly owned step down subsidiaries and to an associate of wholly owned step down subsidiary aggregating to ` 6,815.51 Crores that require lenders and customer approvals. Management has received many such approvals aggregating to 88% in value, of the lenders consenting to the restructuring, the management is confident of receiving balance approvals

from lenders and customer in near future and has taken the effect of these transfers while preparing these consolidated financial results.

The delay in getting the balance lenders approval is only procedural and the Management is confident of getting the same.

The Company is hopeful of resolving the qualification during current financial year 2014-15.

The above Qualification is also a qualification in Abridged Stand alone Financial Statements.

l Qualification on Revenue Recognition by a step down subsidiary:

The qualification by the Auditor is not about deviation from the Accounting Standards but on the interpretation of the realisability of the revenue. There is a dispute between a step down subsidiary company and a customer on the method of tariff determination apart from other issues.

During the financial year, Appellate Tribunal for Electricity, India ordered the HERC (state regulatory commission of the customer) to re-determine the tariff as per HERC Tariff Regulations, 2008 and CERC Regulations, 2009 where no specific operational or financial norms have been specified in the HERC Tariff Regulations. The power tariff determination under HERC Regulations by and large follows the same principles and methodology of tariff determination as per the CERC Regulations.

Relied upon the legal opinions obtained and taking into consideration the latest APTEL order, the management opines that there is no significant uncertainty in recoverability of the recognised revenue for the power supplies made as per the judicial orders. In addition to that the Management is confident of obtaining the tariff approvals in near future and the rate to be determined by HERC will be the same rate as adopted by the step down subsidiary company on provisional basis as per the CERC norms.

l Qualification on Capitalization of Borrowing cost by step down subsidiary:

Due to non availability/non allocation of natural gas by Government of India to the step down subsidiary Company’s Phase-III Project and considering present economic conditions of Power Sector, the step down subsidiary company has made an application to the Ministry of Corporate Affairs (MCA) requesting to provide relaxation from Accounting Standard - 16 and allow the Company to capitalize the borrowing costs till commencing its commercial operations. The application is under consideration of MCA.

The management is of the opinion that the Government of India is likely to respond positively on the said request by considering the specific problems being faced by Gas based power plants in the country.

Directors’ Report

13

l Qualification on Unaudited financials of SPV’s consideration in Consolidation:

The qualification by the Auditor is not about deviation from the Accounting Standards but on considering some of the foreign subsidiary companies non-audited financials in the consolidation.

Out of those, some subsidiary companies were acquired by the company in February, 2011. These companies were “under administrator” before acquisition. On account of this, audited financial statements were not available for 2008-09 and 2009-10. After acquisition, audit was completed for 5 years and audit for the current year is under progress.

The remaining entities are either non-material/non-operational during the year and audit for all these entities is under process.

Hence forth the management is expecting the audited financials of these companies in time and consolidation can be done with the audited accounts which will avoid the qualification in future.

ACKNOwLEDGEMENT AND APPRECIATION

Your Directors take this opportunity to thank all the stakeholders including Shareholders, Financial Institutions, Banks, Customers, Suppliers, Service Providers and Regulatory and Governmental Authorities for their consistent co-operation. Your Directors also wish to place on record the sincere appreciation of the hard work, dedication and commitment of Employees at all levels. We look forward to your continued support in the future.

For and on behalf of the Board

L. Madhusudhan Rao G. Venkatesh BabuExecutive Chairman Managing DirectorDIN - 00074790 DIN - 00075079

Place: GurgaonDate: August 14, 2014

Annual Report 2013-2014

14

Annexure I - Disclosure in compliance with Clause 12 of the SEBI (Employee Stock Option Scheme) and (Employee Stock Purchase Scheme) Guidelines, 1999, as amendedS. No. Description Employee Stock Options Plan 2006

1 Total Number of Options under the plan 11,11,80,960

2 Options granted during the year NIL

3 Pricing Formula The options issued by the ESOP Trust shall be at Par Value subject to the adjustments for corporate actions such as Bonus, Consolidation and Split.

4 Options vested as of March 31, 2014 6,97,63,125

5 Options Exercised during the year 1,50,24,047

6 The total number of shares arising as a result of exercise of option (As of March 31, 2014) 6,42,16,468

7 Options lapsed during the year 22,14,305

8 Variation of Terms of options upto March 31, 2014 NIL

9 Money realised by exercise of Options during the year (in `) 36,50,843

10 Total Number of options in force as on March 31, 2014 5,43,59,980

11 Employee wise details of options granted to

(i) Senior Management during the Year NIL

(ii) Employees holding 5% or more of the total number of options granted during the year

NIL

(iii) Identified employees who were granted option during any one year, equal to or exceeding 1% of the issued capital (excluding warrants and conversions) of the Company at the time of grant.

NIL

12 Diluted Earnings Per Share pursuant to issue of shares on exercise of option calculated in accordance with Accounting Standard (AS) 20

(4.08)

13 Where the Company has calculated the employee compensation cost using the intrinsic value of the stock options, the difference between the employee compensation cost so computed and the employee compensation cost that shall have been recognised if it had used the fair value of the options. The impact of the difference on profits and on EPS of the Company.

Since these options were granted at a nominal exercise price, intrinsic value on the date of grant approximates the fair value of options.

14 Weighted average exercise prices and weighted average fair values of options seperately for options whose exercise price either equals or exceeds or is less than the market price of the stock.

Exercise Price ` 0.243 Per Option.

No new options were granted during the year.

15 A description of the method and significant assumptions used during the year to estimate the fair values of options, including the following weighted average information:

NA

(a) risk free interest rate

(b) expected life

(c) expected volatility

(d) Expected dividends, and

(e) the price of the underlying share in market at the time of option grant.

Directors’ Report

15

ECONOMIC REVIEw

Global

The world economic activity, led by advanced economies, improved in the second half of 2013 and is expected to improve further in 2014-15. World GDP grew at a pace of 3% in 2013 and global growth is expected to increase to 3.6% in 2014 and 3.9% in 2015. In advanced economies, growth is expected to increase to 2.3% vis-à-vis 1.3% in 2013. Growth in the developing economies is expected to be at 5% in 2014 as against 4.7% in 2013.

GDP Growth Rates (%)Country 2012 2013 2014(E)USA 2.8 1.9 2.8UK 0.3 1.8 2.9China 7.7 7.7 7.5Japan 1.4 1.5 1.4Euro Area -0.7 -0.5 1.2World 3.2 3.0 3.6

(Source: World Economic Outlook, IMF April 2014)

India

India’s GDP grew at a modest rate of 4.7% during the year 2013-14. Continued struggle with high inflation, high interest rates, infrastructure constraints and lack of policy reforms pushed the nation’s growth rate to sub five percent for the second straight year. The growth rate in the previous year was 4.5%. Agriculture grew at a pace of 4.7% for the year whilst ‘Mining and Quarring’ and Manufacturing contracted by 1.4% and 0.7% respectively.

India Industry Growth Rates (%) FY13 FY14

1. Agriculture, forestry and fishing 1.4 4.7

2. Mining and quarrying -2.2 -1.4

3. Manufacturing 1.1 -0.7

4. Electricity, gas and water supply 2.3 5.9

5. Construction 1.1 1.6

6. Trade, hotels, transport and communication

5.1 3.0

7. Financing, insurance, real estate and business services

10.9 12.9

8. Community, Social and personal services

5.3 5.6

Gross Domestic Product 4.5 4.7

(Source: Central Statistical Organisation, India)

COMPANY REVIEw

Lanco Infratech Limited (Lanco) is amongst the largest private independent power producers in the country and one of India’s leading business entities. We possess more than 25 years of experience in the fields of Engineering, Procurement and Construction (EPC), Power, Solar, Natural Resources and Infrastructure. The company is emerging as one of the top private sector power developers in India.

Installed Power Capacity

Power Capacities under Construction

Power Capacities under

Development4,722 MW* 4,636 MW 6,840 MW

*732 MW getting ready for operations

The country witnessed a continued slowdown in economic activity during the year 2012-13 and Lanco being amongst the nation’s largest players in the infrastructure sector, too got affected by the continued slowing economy. During the year 2013-14, Lanco Infratech Ltd initiated the process of Corporate Debt Restructuring (CDR) for the Standalone Company, Lanco Infratech Limited. The company opted for CDR as due to a significant unforeseen drop in the level of its operations due to the deteriorating external business environment, the company was not able to generate the requisite cash flows to meet its obligations to vendors and service providers, hence it became imperative to restructure the company’s debt. The CDR proposal does not include restructuring of debt for any of the subsidiaries of the company. The primary objective of restructuring is to assist the company to bring back the EPC operations to normal levels of business and make overdue payments.

Lanco Infratech provides EPC services to the infrastructure sector with prime focus on the power sector. The company is heavily involved in the construction of power plants and other infrastructure projects. The company’s EPC revenues got affected due to various unresolved issues especially in the power sector. The envisaged growth in the power sector has been affected due to factors like unavailability of fuel, both coal and gas, unviable power tariffs not reflecting the true cost of generation, delays in obtaining vital clearances, poor financial and commercial health of the State Electricity Boards leading to lower power procurement by SEBs, high interest rates and weakening Indian Rupee. These have all resulted in a continued slowdown in the sector with more projects being shelved than being announced. The slowing pace of infrastructure development in the country affected the business of the company and its cash flows. The company’s plans to raise long term capital for infusion into the business were also affected because of investor apathy towards investing in the sector both as private equity and primary market investors. Hence the company had to opt for the option of corporate debt restructuring.

During the year 2013-14, Lanco Infratech Ltd initiated the process of Corporate Debt Restructuring (CDR) for the Standalone Company, Lanco Infratech Limited. The CDR proposal does not include restructuring of debt for any of the subsidiaries of the company. The primary objective of restructuring is to assist the company to bring back the EPC operations to normal levels of business and make payments to overdue vendors and service providers.

However given the vital role the power sector plays in the growth of the nation, the government has introduced several measures aimed at alleviating the concerns that are hampering the growth of the sector. Some of the initiatives include financial restructuring package for State Electricity Boards, signing new fuel supply agreements and

Annexure II - MANAGEMENT DISCUSSION AND ANALYSISAnnual Report 2013-2014

16

formulating new standard bidding documents etc. Recognising the need to improve their financial health, some states have hiked electricity tariffs. Given the favourable demand supply dynamics, the outlook for the power sector is encouraging especially for the private developers as majority of the upcoming capacity will be developed by the private sector.

The company is confident that with the help of the restructuring exercise, it will return to optimum level of operations. The Corporate Debt Restructuring Empowered Group (CDR EG) approved the CDR proposal at its meeting held on December 11, 2013 and the scheme is being implemented. As on March 31, 2014 CDR related documents have been executed and creation of security has been completed partly and the balance is in the process.

Salient features of the restructuring proposal approved under CDR system-

l Re-schedule of Term loan and short term loans are having moratorium period of 2 years from the cut off date of April 1, 2013 and are repayable in 30 quarterly instalments starting from June 30, 2015.

l Portion of CDR Working Capital Loans on the cut off date i.e. April 1, 2013, carved out as Working Capital Term Loan - I (WCTL- I). LC/ BC/ BG devolved from cut off date till December 31, 2013 has been carved out as Working Capital Term Loan - II (WCTL- II).

l Funded Interest on Term Loans, WCTL - I and WCTL - II can be funded for a period of 2 years from cut off date i.e. April 1, 2013 to March 31, 2015 and on regular Cash Credit limit for an initial period of 6 months from cut off date i.e. April 1, 2013 to September 30, 2013 is converted into Funded Interest Term Loan (FITL). Interest on FITL to be paid on monthly basis from April 30, 2013.

l ` 2,500 Crores Priority Loan sanctioned with a moratorium period of 2 years at an interest rate of 12.5% and is repayable in 18 quarterly instalments starting from June 30, 2015.

l Rate of interest on restructured facilities being 11% p.a. to be increased in a stepped up manner up to 16% p.a. starting from financial year 2016-17.

l Waiver of penal charges from the cut-off date to the date of implementation of the package

In relation to the loans restructured by the CDR lenders a total amount to ` 2,224.89 Crores would qualify for the conversion of 354.50 Crores shares at the sole discretion and on demand of the

CDR lenders.

In terms of CDR scheme the promoters brought into the company as unsecured loan a total amount to ` 152.00 Crores and the same would qualify for the conversion of 24.40 Crores shares at the sole discretion of the promoters.

The CDR gives your Company critical support to tide over the present difficult business environment. The decision of the banks to consider and approve CDR also reflects the faith these institutions have in the long term business model of the Company.

INDUSTRY REVIEw – DEVELOPMENTS AND OUTLOOK

POwER

The total installed generation capacity in India as of end FY14 stood at 243.03 GW. Out of the total installed generating capacity, 59.8% was coal based, 16.7% was hydro and 9.0% was gas based.

All India Installed Generation Capacity (As on 31-03-2014)

Thermal Nuclear Hydro RES Grand

Coal Gas Diesel Total Renewable (MNRE) Total

MW 145273 21782 1200 168255 4780 40531 29463 243029

Percentage 59.8 9.0 0.5 69.2 2.0 16.7 12.1 100.0

(Source: CEA)

The total electricity generation in India during FY14 was at 966.38 Billion Units (BUs) versus 912.06 BUs in FY13, an increase of 5.96% YoY.

Electricity Generation during April 2013 to March 2014 (BU)

Type FY13 FY14 % ChangeThermal 761 792 4Hydro 114 135 18Nuclear 33 34 4Bhutan Import 5 6 17All India 912 966 6

(Source: CEA)

The generating capacity addition during 2013-14 stood at 17,825 MW as against 20,623 MW in 2012-13, a decline of 13.57% YoY.

Generation Capacity Addition during FY14 (Mw)

Type FY13 FY14 % ChangeThermal 20122 16767 -17Hydro 501 1058 111Nuclear 0 0 NAAll India 20623 17825 -14

(Source: CEA)

All India Installed Generation Capacity (Mw) – Region wise (As on 31-03-2014)Region Thermal Nuclear Hydro RES Grand

Coal Gas Diesel Total TotalNorthern 35284 5281 13 40578 1620 16331 5730 64258Western 58020 10139 17 68176 1840 7448 9925 87389Southern 26583 4963 939 32485 1320 11398 13127 58330Eastern 25328 190 17 25535 0 4113 417 30066North-East 60 1209 143 1411 0 1242 253 2906Islands 0 0 70 70 0 0 10 80All India 145273 21782 1200 168255 4780 40531 29463 243029

(Source: CEA)

Management Discussion and Analysis

17

The western region has the highest installed capacity with 35% of the nation’s total installed capacity followed by the northern region at 26% of the total installed capacity.

All India Installed Generation Capacity (Mw) – Sector wise (As on 31-03-2014)Sector Thermal Nuclear Hydro RES Grand

Coal Gas Diesel Total TotalCentral 45925 7066 0 52991 4780 10355 0 68126State 53828 6548 603 60979 27482 3727 92188Private 45520 8168 597 54286 2694 25736 82715All India 145273 21782 1200 168255 4780 40531 29463 243029

(Source: CEA)

The share of the states in the total installed capacity is the highest at 38% followed by the private sector at 34%.

Capacity Addition Targets in the 12th Plan

Type/Sector Central State Private TotalThermal 14878 13922 43540 72340Hydro 6004 1608 3285 10897Nuclear 5300 0 0 5300Total 26182 15530 46825 88537

(Source: CEA)

The 12th plan targets a capacity addition of 88,537 MW with 53% of the capacity being added by the private sector.

Achievements up to March 2014 during the 12th Plan

Type/Sector Central State Private TotalThermal 6683 7233 22973 36889Hydro 1288 102 169 1559Nuclear 0 0 0 0Total 7971 7335 23142 38448Achievement % 30 47 49 43

(Source: CEA)

All India yearly Coal Consumption for Power Generation (Utilities)

Year Coal Consumption Million Tonnes

2008-09 3552009-10 3672010-11 3872011-12 4182012-13 4552013-14 488

(Source: CEA)

All India Annual per Capita consumption of Electricity

Year Per Capita Consumption (kwh)

2007-08 7172008-09 7342009-10 7792010-11 8192011-12 8842012-13 917

(Source: CEA)

Transmission Lines added during April 2013 to March 2014 (ckms)

Voltage Level FY13 FY14

+/- 500 KV HVDC 0 0

765 KV 1209 4637

400 KV 11361 7777

220 KV 4537 4334

All India 17107 16748

(Source: CEA)

All India Transformation Capacity Addition during April 2013 to March 2014 (MVA)

Voltage Level FY13 FY14

+/- 500 KV HVDC 3750 0

765 KV 24000 34000

400 KV 16795 9630

220 KV 19120 13700

All India 63665 57330

(Source: CEA)

Annual Report 2013-2014

18

OUTLOOK

The power sector will continue to play a central role in the country’s growth story. As can been seen from the data given above, out of the 12th plan target capacity addition of 88,537 MW, 53% of the capacity is estimated to be added by the private sector. Although recently the sector has witnesses a slowdown in its envisaged growth path, several measures such as structural reforms in domestic fuel availability and power distribution are being planned to alleviate the concerns that are hampering the growth of the sector.

Some of the initiatives introduced recently to address the issues hampering the sector are-

1. State Electricity Board (SEB) financial restructuring package: A healthy distribution sector is imperative for the long term growth of the whole industry. Keeping this in mind, the government had introduced the SEB debt restructuring package in 2012 aimed at improving the financial health of the discoms by easing their debt burden. Subsequently, a number of states including Uttar Pradesh, Rajasthan, Haryana and Tamil Nadu have opted in for the restructuring exercise. The restructuring package for discoms will increase cash flow to the SEBs which will in turn help power generators as increased cash flows will enable the discoms to procure more electricity for meeting the growing demand.

2. Compensatory tariff for External/Uncontrollable factors: The regulators have allowed compensatory tariff for some developers for reasons beyond the developers’ control which led to an unforeseen increase in the price of inputs that was not captured in the bid tariffs. This is a positive development for the whole sector and has allayed both developer and investor concerns.

3. CCEA approval for coal supply mechanism to power developers: Under the mechanism approved by the Cabinet Committee on Economic Affairs (CCEA), Coal India is to sign Fuel Supply Agreements (FSA) for a total capacity of 78,000 MW including cases of tapering linkage, which are likely to be commissioned by 31.03.2015. Actual coal supplies would however commence when long term Power Purchase Agreements (PPAs) are tied up. To meet FSA obligations which cannot be met by domestic coal, CIL may import coal and supply the same to the willing Thermal Power Plants (TPPs) on cost plus basis. TPPs may also import coal themselves as well. Higher cost of imported coal is to be considered for pass through as per modalities suggested by CERC. As of end FY14, Coal India had signed close to 160 new FSAs.

4. Standard Bidding Documents: During the 2013-14, the Empowered Group of Ministers cleared standard bidding documents for Case II thermal plants. As fuel has been made a pass through, the new Case II bidding norms will take care of risk associated with fuel price volatility and fuel availability.

Given the favourable demand supply dynamics, the outlook for the power sector is encouraging especially for the private developers as a majority of the upcoming capacity will be developed by the private sector.

SOLAR

Amongst the various renewable energy resources, solar energy is considered to have the highest potential in the country. The Jawaharlal Nehru National Solar Mission (JNNSM) was launched in January 2010 to make India a global leader in solar energy. As per the National Tariff Policy of January 2011, solar specific Renewable Purchase Obligation (RPO) is envisaged to increase from a minimum of 0.25 percent in 2012 to 3 percent in 2022.

The solar power capacity requirement for RPO compliance by 2022 is illustrated below-

Year Energy Demand

(MUs)

Solar RPO (%)

Solar Energy Requirement (MUs) for RPO

compliance

Solar Capacity Requirement for RPO compliance

(Mw)2013-14 1,095,555 0.50% 5,478 3,2912018-19 1,544,936 2.25% 34,761 20,8852021-22 1,894,736 3.00% 56,842 34,152

(Source: Government of India, Ministry of New and Renewable Energy)

The nation would need an installed solar capacity of approximately 34,000 MW in order to achieve the 3% RPO compliance by 2022.

RESOURCES

Coal generated power will continue to be the major source of energy for the nation. With the current per capita commercial primary energy consumption in India at about 350 kgoe/year well below that of developed countries, energy usage in India is expected to rise. The increasing demand for energy will be driven by an expanding economy, improvements in infrastructure, rising population and enhanced standard of living. As of April 2014, the geological resources of coal in the country have been estimated to be a cumulative total of 301.56 billion tonnes with the state of Jharkhand having the highest resources at 80,716 million tonnes (MTs) followed by the state of Orissa at 75,073 MTs.

Cumulative geological resources of coal-

Proved (MT)

Indicated (MT)

Inferred (MT)

Total (MT)

All India 1,25,909 1,42,506 33,149 3,01,564

(Source: Government of India, Ministry of Coal)

INFRASTRUCTURE

According to the planning commission, infrastructure investment should be on average almost 10% of GDP during the twelfth plan in order to attain a 9% real GDP growth rate.

Projected Investment in Infrastructure during the Twelfth Five Year Plan

Year Base Year FY12 Total 12th PlanGDP at FY07 Prices (` Crs) 6,314,265 41,190,063Infrastructure Investment as % of GDP

8.37% 9.95%

Infrastructure Investment (` Crs in FY07 Prices)

528,316 4,099,239

Infrastructure Investment (` Crs in Current Prices)

721,781 6,579,463

(Source: Planning Commission, Government of India)

Management Discussion and Analysis

19

BUSINESS REVIEw

EPC*Order book

(As of end March 2014)Revenues (FY14) EBIDTA (FY14)

₹ 26,178 Cr ₹ 2,368 Cr ₹ -393 Cr

Order book (As of end March 2013)

Revenues (FY13) EBIDTA (FY13)

₹ 26,284 Cr ₹ 5,382 Cr ₹ 785 Cr

* Including Solar EPC

Lanco with its unique ‘concept to commissioning’ EPC execution model offers Engineering, Procurement and Construction services in the infrastructure business segments of power projects, transmission, transportation, industry and large scale building projects. The total EPC order book (including Power and Solar Projects) as at end FY14 stood at ` 262 billion.

For the year 2013-14, revenue for the EPC division was ` 2,368 crores and EBITDA was ` -393 crores. The revenue for the year was less than the normal level due to the deteriorating external business environment which led to a slowdown in the execution of infrastructure projects. Lower revenue led to lower recovery of fixed costs affecting the margins. Also due to delays in execution of contracts the cost associated with price escalations, claims of the service providers, subcontractors and upward revision of estimated cost, comprising of provision for expected loses on some ongoing projects and additional costs in recently completed/discontinued projects resulted in losses for the year.

Key Developments in 2013-14l Completed construction and start of commercial operations of

81 km NH4 road project in Karnataka (Hoskote)

l Successful bidder of the prestigious EPC Contract for establishing “1 x 660 MW Super Critical Ennore Thermal Power Station Expansion Project” by Tamil Nadu Generation and Distribution Corporation Limited.

MAJOR PROJECTS UNDER ExECUTION

Externall EPC of 2x600 MW Annupur Thermal Power Project for Moser

Baer

l BOP of 3x660 MW Koradi Thermal Power Project for Mahagenco

l EPC of 2x125 MW Akaz Gas Power Project for Government of Iraq

Internal (All EPC Contract Projects)l 2x660 MW Amarkantak Thermal Power Project

l 2x660 MW Vidarbha Thermal Power Project

l 2x660 MW Babandh Thermal Power Project

l 500 MW of Teesta Hydro Power Project

l 76 MW Mandakini Hydro Power Project

POwER*

Installed Power Capacity (As of end March 2014)

Revenues (FY14) EBIDTA (FY14)

4,722 MW** ₹ 7,561 Cr ₹ 2,318 Cr

Installed Power Capacity (As of end March 2013)

Revenues (FY13) EBIDTA (FY13)

4,732 MW** ₹ 8,663 Cr ₹ 1,926 Cr

* Including Solar

**732 MW Kondapalli Phase 3 getting ready for operations

Lanco Infratech is one of the largest independent private producers in the country with an installed capacity 4,722 MW and the capacity under construction of 4,636 MW. Out of the current installed capacity, 64% is coal based, 34% is gas based and 2% is renewables including hydro. During the year, Lanco Babandh (2*660 MW under construction plant) signed a Long Term Power Purchase Agreement (25 years) with Uttar Pradesh Power Corporation Limited Discoms and Rajasthan discoms respectively for supply of power under Case 1 Bid.

PERFORMANCE OF THE PROJECTS UNDER OPERATION

Kondapalli Phase-I

The gas based power station located in Andhra Pradesh with an installed capacity of 368 MW has a long term Power Purchase Agreement (PPA) with Andhra Pradesh discoms. Fixed charges are recoverable based on alternative fuel based availability under the PPA. The unit has tied up fuel supply arrangements with GAIL. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

1,768 1,441 55 45

Generation during the year compared to the previous year was lower by 327 MUs on account of lower availability of gas as well as carrying out major inspection works. The unit was however able to recover full fixed charge based on availability of natural gas and naphtha.

Kondapalli Phase-II

The gas based power station located in Andhra Pradesh has an installed capacity of 366 MW has tied up fuel supply with RIL (KG-D6). Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

664 0 21 0

The generation for the year ended March 2014 was nil on account of non supply of gas from KG-D6.

Kondapalli Phase-III

The 732 MW gas based unit could not get commissioned during the year due to non supply of gas.

Annual Report 2013-2014

20

Tanjore

Gas based power station located in Tamil Nadu with an installed capacity of 120 MW. The plant has a long term PPA with Tamil Nadu with fuel supply arrangement with GAIL. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

893 733 85 70

PLF is lower year on year due to short supply of gas by GAIL.

Amarkantak Unit-I

Domestic coal based power station located in Chhattisgarh with an installed capacity of 300 MW. The unit started supplying power under a long term PPA to Madhya Pradesh effective December 2012, hence there has been a significant increase in gross generation during the year over the previous year. The plant also maintained an availability factor of 96% during the year. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

1,798 2,259 68 86

Amarkantak Unit-II

Domestic coal based power station unit located in Chhattisgarh with an installed capacity of 300MW. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

1,351 0 51 0

There was nil generation during the year due to non availability of linkage coal as well as regulatory issues. Unit two’s PPA with PTC for supply of power to HPGCL (Haryana) was terminated for non-compliance of certain PPA covenants. The litigation hearings are currently being held. Linkage coal supply was suspended by Coal India due to the non existence of a PPA. Supply of power using non linkage sources was not considered prudent as the tariff being paid by the customer was not workable.

Udupi

Coal based power plant located in Karnataka having an installed capacity of 1200 MW. The plant maintained an availability factor of 75% during the year 2013-14. The availability was less than optimal due to non availability of coal. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

6,423 6,806 76* 65

*One unit was operational for only a part of the year hence PLF is higher

PLF was lower year on year due to shortage of coal.

Anpara

Located in Uttar Pradesh with an installed capacity of 1200 MW, the unit has a long term PPA with Uttar Pradesh discoms for 1100 MW of supply. During the year, the unit also started supplying 100 MW of power to Tamil Nadu discoms starting June 2013. Performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

3,979 6,919 38 66

The plant maintained an availability factor of 72% during the year. There has been a significant increase in PLF during the year 2013-14 due to improvement in coal handling and infrastructure facilities at the plant and better operational performance after the initial stabilisation period.

Budhil

Hydro based power plant is located in Himachal Pradesh with an installed capacity of 70MW. Plant was commissioned in May 2012 and performance of the plant during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

155 221 30 36

PLF was low during the year due to maintenance work. The company has signed an agreement with Tejassarnika Hydro Energies Private Limited, a subsidiary of Hyderabad based Greenko Energies limited to divest 100% stake in the asset.

PROGRESS OF THE PROJECTS UNDER CONSTRUCTION (As at end March 2014) AS % OF BILLING Project Name Percentage

Completion (%)

Expected Commissioning

DateAmarkantak 3&4 (1320 MW) 67 FY16Vidarbha (1320 MW) 24 FY17Babandh (1320 MW) 33 FY17Kondapalli III (732 MW) 98 FY15Teestha (500 MW) 48 FY17Phata Byung (76 MW) 62 FY17Moser Baer (2&600 MW) 77 FY15Mahagenco (3*660 MW BOP) 73 FY16Akaz (2*125 MW) 96 FY15

SOLAR

Lanco Solar is one of the largest solar power players in the country today that provides solutions across the entire Solar Power Value Chain. The Company has expertise in managing the entire life cycle of any type of solar project development. As of end March 2014, the solar EPC order book was ₹ 2,949 Cr with 57% of orders from external parties. The major solar plants under construction include Lanco’s 100 MW solar thermal power plant at Chinnu in Rajasthan. The order book also includes a 100 MW solar thermal power plant being developed by Lanco for KVK energy ventures private limited

Management Discussion and Analysis

21

also at Chinnu in Rajasthan. The company is also setting up a fully-integrated manufacturing project for high-purity Polysilicon, silicon ingots/ wafers and modules in a SEZ facility at Chhattisgarh. The project is the first of its kind in India with a targeted capacity of 300MWp/year. The plant has an operational module line with a 75 MW capacity. The company is in the process of setting up a 1,800 MT polysilicon facility and 100 MW wafer facility and plans to enter into solar cell manufacturing as well. Foray into manufacturing not only supports the company’s internal requirements, but also reduces margin volatility through the business cycles.

Performance of all solar generating capacity of 41 MW during the year is as follows-

Gross generation (MUs) Plant Load Factor (PLF %)FY13 FY14 FY13 FY14

56 60 16 17

RESOURCES

The Natural Resources business of the Lanco currently consists of the following assets-

1. Griffin Coal Mine

The Griffin Coal Mining Company Pty Ltd is based in Collie, located approximately 220 kilometres south east of Perth, Western Australia’s capital city. The Company is the largest individual supplier of coal to Western Australia’s industrial coal market. With coal resources of approximately 1.1 billion tonnes, coal from Griffin caters to the export markets as well. Production at the mine during the year 2013-14 was 2.83 MT with sales of 2.95 MT. Steps are underway to reach the short term production target of 5 MT by March 2015. Capacity enhancement program with capacity being raised from current to 15 MTPA is in the planning phase. The company also recently received environmental clearance for developing a new berth (Berth 14 A) at Bunbury port for export of coal from Griffin.

2. Mahatamil Project

Gare Palma Sector- 2 Coal Block jointly allocated to TNEB (74%) and MSMC (26%) awarded to Lanco Infratech Limited for Mines Development and Operations along with the development of end use thermal power plant for TNEB share of coal. 23% of the coal produced will go to the state of Maharashtra and the remaining coal (77%) will be used to generate power. Out of the total power produced, 37.5% of the power will go to the state of Chattisgarh as home state share and the remaining power will be shared between Tamil Nadu state and Lanco in a 50:50 ratio. Coal mining fees of ` 112/Ton is to be paid by Lanco. Lanco targets the coal mine capacity to be developed to produce over 20 MTPA of coal output and approximately ~2000 MW of power plant. According to the geological report prepared by Mineral Exploration Corporation of India Ltd, the geological reserves of the block are around 1 Billion Ton with extractable reserves as per the mine plan of around 655 MT. The mining and mine closure plan were submitted to the Ministry of Coal (MoC) in October 2013 for approval and presentation made

to the expert committee of MoC. A revised mining plan was submitted to MoC in April 2014 after receiving some comments and final approval is expected shortly. The application for forest clearance has also been submitted. The suitable site for the power plant has been identified in Raigarh district.

3. Tasra Open Cast Project

Tasra Opencast coal project (Tasra OCP) was awarded to Lanco by Steel Authority of India Limited (SAIL) for Mine Development and Operations. The project includes setting up of 4 MTPA mine infrastructure, 3.5 MTPA Washery and a captive power plant (CPP) of 300 MW capacity based on the secondary coal from the Washery. Tasra OCP was allocated to SAIL for captive use and detailed exploration of mine has been completed by MECL and CMPDI (Govt. of India enterprise) and estimated extractable coking coal reserves are around 100 million tons. The project is located in well-established Jharia coal-fields region of District Dhandbad, Jharkhand and has a life span of around 28 years. Captive Power Project of 300 MW capacity will be setup under a JV company between Lanco (74%) and SAIL (26%). With this project, Lanco as MDO will develop and operate 4 MTPA coal production capacity, 3.5 MTPA washery capacity, and add around 300 MW of coal based power capacity to its existing business portfolio. For Tasra Coal Block, key project approvals like Mining Plan, Environmental Clearance etc are already in place. No forest land is involved. For Tasra Washery, approved ToR is available and Environmental Impact Assessment Report has been prepared. For Tasra Power Project suitable site has been identified and development activities shall be initiated.

INFRASTRUCTURE

ROAD INFRASTRUCTURE PORTFOLIO:

The road portfolio of the company currently consists of the following assets:

Project Status82 km Neelamangla Junction (Bangalore) – Devihalli (NH-48)

Operational; Collected ₹ 44 Cr in toll revenue during the year FY14

81 Km of Mulbagal – Hoskote – Bangalore (NH-4)

Commissioned in December 2013; Collected ₹ 15 Cr in toll revenue during the year FY14

283 km - Aligarh- Kanpur (NH-91) Achieved financial closure, construction to start after obtaining necessary clearances

REAL ESTATE

Located in Hyderabad, Lanco Hills is the group’s lone foray into property development. The project comprises of residential space, office space, IT SEZ and non SEZ space, retail and hospitality space and is spread over a land parcel of 100 acres. During the year 2013-14, revenue from operations increased by 17% to ₹ 196 Cr.

Annual Report 2013-2014

22

CONSOLIDATED FINANCIAL REVIEw

SEGMENT REVIEw

Revenues

(₹ Crores)Segment Revenue

FY14 Contribution to Total

Revenues

FY13 Contribution to Total

Revenues

YoY growth

(%)(a) EPC &

Construction*2,368 22% 5,382 35% -56%

(b) Power* 7,561 69% 8,663 57% -13%(c) Property

Development196 2% 168 1% 17%

(d) Infrastructure 0 0% 0 0%(e) Resources 681 6% 954 6% -29%(f ) Unallocated 93 1% 93 1% 0%Total 10,899 100 15,260 100 -29%Less: Inter Segment Revenue

277 1,408 -80%

Net Sales/Income from Operations

10,622 13,852 -23%

* Including Solar

Lanco Infratech’s total segmental revenue (post elimination of inter-segment revenue) decreased by 23% during 2013-14. This was primarily due to fall in EPC and Construction revenues and power segment revenues. The share of the power segment in the total revenue before inter segment revenue in FY14 was 69% vis-à-vis 57% in FY13. Power revenues declined by 13% YoY due to fuel supply and regulatory issues. The share of EPC and Construction segment in the total revenue declined to 22% in FY14 against 35% in FY13. Prior to elimination, the revenue for 2013-14 decreased by 29%. The property development segment witnessed a 17% growth in revenue for 2013-14.

SEGMENT PROFITS

(₹ Crores)

Segment Results (Profit(+)/Loss(-) before tax and interest from each segment)

FY14 FY13 YoY growth

(%)(a) EPC & Construction* -497 686 -172%

(b) Power* 1,411 1,099 28%

(c) Property Development 16 2 746%

(d) Infrastructure 0 0

(e) Resources -556 -301 85%

(f ) Unallocated -44 -12 266%

Total 330 1,474 -78%

Less: Inter Segment Profit on transactions with Subsidiaries

-15 -18 -17%

Total 345 1,491 -77%

* Including Solar

Consolidated segmental profit before interest and taxes and before elimination of inter-segment profit on transactions with subsidiaries declined by 78% in FY14 against FY13. The profit from the EPC & Construction segment decreased by 172% as there has been a slowdown in execution of projects affecting both revenues and profits. The segmental profit before tax and interest from the power vertical increased by 28% during the year.

FINANCIAL REVIEw

Principles of Consolidation

The financial statements of the Company and its subsidiaries have been consolidated on a line by line basis. This is done by adding together the book values of like items of assets, liabilities, income and expenses and after eliminating intra-group balances, transactions and the unrealized profits/losses on intra-group transactions. Unrealised losses resulting from intragroup transactions are eliminated to the extent that cost can be recovered.

The consolidated financial statements are drawn up by using uniform accounting policies for like transactions and other events in similar circumstances. These are then presented to the extent possible in the same manner, as the Company’s individual financial statements.

The financial statements of the subsidiaries are consolidated from the date on which effective control is transferred to the company, till the date such control exists. The difference between the cost of investments in subsidiaries over the company’s share of book value of subsidiaries’ net assets on the date of acquisition is recognized as goodwill or capital reserve in the consolidated financial statements.

Equity method of accounting is followed for investments in Associates in accordance with Accounting Standard (AS) 23 – Accounting for Investments in Associates in Consolidated Financial Statements. In this case, goodwill/capital reserve arising at the time of acquisition and share of profit or losses after the date of acquisition are included in carrying amount of investment in associates.

Unrealized profits and losses resulting from transactions between the company and its associates are eliminated to the extent of company’s interest. Unrealised losses resulting from transactions between the company and its associates are also eliminated, unless the cost cannot be recovered. Investments in associates, made for temporary purposes, are not considered for consolidation and are accounted for as investments.

Putting it simply, while consolidating the subsidiary company, the elimination takes place at the top line where the entire amount of revenue and expenditure is eliminated. In the case of associate consolidation, the entire revenue is recognised. But the profit or loss earned from the associate is eliminated proportionately to the holding in the associate. This adjustment is for the profit and loss account. For adjustment to the balance sheet in case of subsidiaries, the amount equal to profit or loss eliminated will be net off against fixed assets. In the case of associates, it will be net off against investments. Essentially, it is an adjustment which does not impact the cash flow.

Management Discussion and Analysis

23

ANALYSIS OF PROFIT AND LOSS ACCOUNT

(₹ Crores)FY14 FY13 YoY growth %

1 (a) Income from operations 10,103 12,883 -22%(b) Income from power trading 539 2,188 -75%(c) Other operating income 66 76 -14%Total income from operations (Gross) 10,707 15,147 -29%Less: Elimination of intersegment operating income 277 1,408 -80%Total income from operations (Net) 10,430 13,739 -24%

2 Expenses(a) Cost of materials consumed 6,336 6,469 -2%(b) Purchase of traded goods 530 2,161 -75%(c) Subcontract cost 169 561 -70%(d) Construction, transmission, site and mining expenses 1,061 1,319 -20%(e) Change in inventories of finished goods and work in progress -151 -454 -67%(f ) Employee benefits expense 385 618 -38%(g) Depreciation & amortisation expenses 1,172 1,126 4%(h) Other expenses 225 482 -53%Total expenses 9,727 12,283 -21%

3 Profit/(loss) from operations before other income, foreign exchange fluctuations, finance costs, prior period items & exceptional items (1-2)

703 1,456 -52%

4 Other income 168 149 13%5 Add: Eliminated profit on transactions with subsidiaries -15 -18 -14%6 Profit/(loss) from ordinary activities before foreign exchange fluctuations,

finance costs, prior period items & exceptional items plus elimination (3+4+5)856 1,587 -46%

7 (Gain)/loss on foreign exchange fluctuations (Net) 371 77 378%8 Finance costs 2,762 2,421 14%9 Profit/(loss) from ordinary activities after finance costs but before prior period

items & exceptional Items plus elimination (6-7-8)-2,277 -912 150%

10 Exceptional items -179 100%11 Profit/(loss) from ordinary activities before tax, prior period items plus

elimination (9+10)-2,456 -912 169%

12 Tax expense -129 180 -172%13 Net profit/(loss) from ordinary activities after tax but before prior period items plus

elimination (11-12)-2,327 -1,091 113%

14 Extraordinary Item (net of tax expense) -15 Net profit/(loss) for the period before prior period items plus elimination (13+14) -2,327 -1,091 113%

Less : Prior Period Items 44 -13 -445%16 Net profit/(loss) for the period plus elimination -2,371 -1,078 120%

Less : Minority interest -116 -11 931%Add: Share of profit/(loss) of associates -34 -3 1077%

17 Net profit/(loss) for the period plus elimination after Minority and share profit/(loss) of associates

-2,289 -1,070 114%

18 Less: elimination of profit on transactions with subsidiaries and associates

-15 3 -575%

19 Net profit/(loss) after taxes, minority interest and share of profits/(loss) of associates (17-18)

-2,274 -1,073 112%

20 Cash profit (17 + 2(g) + deferred tax – MAT credit + forex loss- forex gain)

-743 233 -419%

21 Profit (+)/Loss (-) from ordinary activities before tax (11 – 5) -2,441 -894 173%

l Gross Revenue before eliminations (including other income) declined by 29% YoY to ₹ 10,875 Crores in FY14 from ₹ 15,296 Crores in FY13

l Reported loss of ₹ 2,274 Crores in FY14 vs. loss of ₹ 1,073 Crores in FY13

l Forex loss of ₹ 371 Crores in FY14 vs. Forex loss of ₹ 78 Crores in FY13.

Annual Report 2013-2014

24

There was a reported loss of ` 2,274 crores due to losses in the EPC division, losses at Griffin coal mine and losses in some operating power plants that were hampered by fuel supply and regulatory issues. The EPC division suffered due to a slowdown in the economic environment that in turn affected its operations and revenues. Griffin coal mine is currently in the expansion phase where the capacity enhancement program from the current production of 3 MTPA to 15 MTPA is underway. The performance of Lanco’s gas based power plant at Kondapalli was affected due to non supply of gas. One unit of Lanco Amarkantak (300MW thermal plant) could not operate due to regulatory issues.

Revenues from Operations

The consolidated net revenue from our operations decreased by 24% during 2013-14. This was primarily on account of decrease in revenue from contract operations by 48% during the year due to slowdown in EPC activity because of a slowing economy. Income from sale of electrical energy declined by 13% during the year as some operating plants suffered due to lack of fuel supply and regulatory issues. Income from property development increased by 16% during the year.

(₹ Crore)FY14 FY13 YoY

Growth %Contract Operations 2,097 4,038 -48%Property Development 193 166 16%Management Consultancy 3 3 0%Operations and Maintenance 5 5 -9%Electrical Energy 7,405 8,558 -13%Coal 679 947 -28%Other Goods 36 8 347%Income from Lease Rentals 2 0 380%Other Operating Income 11 13 -20%Net Revenue from Operations 10,430 13,739 -24%

Other Income

Other income for FY14 increased by 13% over FY13 led primarily by an increase in interest income.

(₹ Crore)FY14 FY13 YoY

Growth %Interest Income 144 95 51%Dividend Income 1 2 -37%Net Gain on sale of investments

0 0 -80%

Other Non Operating Income 22 51 -56%Total 168 149 13%

ExPENDITURE

There was a 21% decline in total expenditure for the year 2013-14. There was 75% de-growth in purchase of traded goods primarily power purchase. Power trading division (NETS) traded 2089 million units in 2013-14, lower by 66% YoY. Subconctract costs declined by 70% during the year and employee benefit expenses declined by 38% YoY.

(₹ Crore)

ExPENSES FY14 % of Total FY14

Expenses

FY13 % of Total FY13

Expenses

YoY Growth

%

Cost of Materials Consumed

6,336 71% 6,469 58% -2%

Purchase of Traded Goods

530 6% 2,161 19% -75%

Subcontract Cost 169 2% 561 5% -70%

Construction, Transmission, Site and Mining Expenses

1,061 12% 1,319 12% -20%

(Increase)/Decrease in Inventories of Finished Goods and Construction/Development Work in Progress

-151 -2% -454 -4% -67%

Employee Benefits Expenses

385 4% 618 6% -38%

Other Expenses 595 7% 560 5% 6%

Total Expenses 8,926 11,234 -21%

Cost of Material Consumed

The total cost of material decreased by 15% during 2013-14. This was due a fall in EPC related activity during the year. The cost of gas for power consumption decreased by 21% in FY14 over FY13 due to fall in gas supply for power plants especially at Kondapalli.

(₹ Crore)FY14 % of

TotalFY13 % of

TotalYoY

Growth %

Construction Material Consumed

1,903 30% 2,249 35% -15%

Property Development Cost

208 3% 188 3% 11%

Coal for Power Generation

3,316 52% 2,916 45% 14%

Gas for Power Generation

629 10% 797 12% -21%

Oil (HFO, LDO & HSD) for Power Generation

33 1% 67 1% -51%

Other consumables for Power Generations

22 0% 22 0% -2%

Raw Materials Consumed - Coal Mining

180 3% 202 3% -11%

Raw Materials Consumed - Solar Modules

45 1% 29 0% 57%

Total 6,336 6,469 -2%