98

Annual Report 2015

Annual Report

2015

1

Annual Report 2015

1

Contents2 Group Highlights4 Strategic Report: Executive Summary South Staffs Water SSI Services Echo Financial Review

32 Corporate Social Responsibility 38 Executive Team39 Corporate Information40 Directors’ Report 42 Corporate Governance 51 Directors’ Responsibilities Statement 52 Independent Auditor’s Report 54 Consolidated Profit & Loss Account 55 Consolidated Balance Sheet 56 Company Balance Sheet57 Consolidated Statement of Total Recognised Gains & Losses 57 Reconciliation of Movements in Consolidated Shareholders’ Funds58 Consolidated Cash Flow Statement 59 Notes to the Consolidated Cash Flow Statement61 Notes to the Financial Statements91 Group Five Year Summary 92 Contact Details

Group Highlights

South Staffs

Water bills reducing by

4% in real terms over the next

5 years

Echo successfully implement RapidXtra

into Dŵr Cymru (Welsh Water)

Growth in Group turnover, pre-tax profits

and free cash generation

South Staffs Water confirmed as top performing company

in Ofwat’s customer service SIM

ranking for the three years to 2013/14

SSI Services

establishes new Onsite Rail business

Group health and safety

targets achieved

with a significant

reduction in

RIDDOR

reportable incidents

Annu

al R

epor

t 201

5

4

Group OverviewSouth Staffordshire Plc is a highly respected integrated services group of businesses with a regulated water supply company, South Staffs Water, comprising two operational regions, South Staffs and Cambridge, and two non-regulated service divisions, SSI Services and Echo.

Group StrategyThe Group’s strategy is to continue to grow by providing high levels of service quality while remaining price competitive and maintaining a safe working environment in all of the Group’s operations. Details of how the strategy is implemented across the Group are provided throughout the Strategic Report.

South Staffs WaterSouth Staffs Water has seen a year of change, partly resulting from the challenges arising from Ofwat’s Final Determination. Customers will see

water bills reduce by 4% in real terms over the five-year period to March 2020, meaning that customers will continue to see one of the lowest bills in the industry. The business has therefore had to make some difficult decisions to align its costs with this reduction in charges, including a reduction in manpower. It has become clear during the year that significant work is required at Seedy Mill Treatment Works to improve water quality performance. This is a priority for the business, which is working closely with the Drinking Water Inspectorate to enhance the site’s assets and performance.

During the year, it was confirmed that, for the three years to 2013/14, the business was ranked top out of the 18 companies in the England and Wales water industry for SIM, Ofwat’s measure of customer experience.

The business is now focussed on the challenges and opportunities that the AMP 6 investment period presents, including increased competition in the non-household sector, all of which will require the continued focus on operating efficiency and an excellent customer experience.

SSI ServicesSSI Services has seen a challenging year, being the last year of the AMP 5 investment period in the water industry when spending by some of its largest clients is typically lower than normal. Despite this, the division has managed to grow revenue through a combination of contract awards, successful new service offerings and one-off projects. However, profit margins have been impacted, due partly to start-up costs on some contracts and less emphasis by clients on planned work.

Strategic Report:Executive Summary

Annual Report 2015

5

In the Clean Water business, Hydrosave has continued to expand the interest in its proprietary valve release and maintenance system, and continues to develop its relationships with both Scottish Water and Thames Water. In the Wastewater Services business, the establishment of OnSite Rail promises to deliver future growth in the division. The Water Hygiene business secured a number of new clients and anticipates further growth in the current year.In this new year, SSI Services expects to see an upturn in water industry expenditure as well as an increase in profit margins following a series of efficiency and cost control measures that have been taken.

EchoEcho has had another successful year, with RapidXtra, its market leading customer information and billing system, going live in Dŵr Cymru (Welsh Water) and new contract awards and successful implementations to service Anglian Water Business and Severn Trent Services with their non-household

retail system requirements. Echo’s debt collection offering has been further strengthened with the acquisition of Grosvenor Services Group, which complements Echo’s office based collections expertise with Grosvenor’s field based skills. During the year Echo received recognition for its customer service excellence with nominations for three highly regarded awards. The introduction of increased non-household retail competition in the UK water industry is creating opportunities for Echo across all its service areas. The business is also working on a strategy to develop the Echo brand in sectors which offer opportunities for long term growth.

FinancialThe Group achieved year-on-year growth in turnover, pre-tax profits and free cash flows that were also ahead of the Group’s budget, despite some significant challenges being experienced in the year. However, operating profit and EBITDA both reduced, largely due to the impact of non-recurring charges.

EmployeesThe Group and its businesses continue to invest in its some 2,500 employees, with their safety and wellbeing of paramount importance. It has been a challenging year for many of our employees and we recognise and thank them for their hard work, innovation and commitment. All of our businesses have health and safety as a top focus, with health and safety targets met or exceeded during the year. All businesses are working towards the aim of a year-on-year reduction of workplace accidents.

OutlookWith many difficult decisions made last year in order to respond to changing environments, the focus in the Group is now very much on the present and the future which presents both further challenges and opportunity for development across all of the Group’s divisions. The Group will face these challenges head on and will look to maximise the impact of the opportunities that are apparent and which develop during this new year.

Annu

al R

epor

t 201

5

Strategic Report:

South Staffs Water

Annual Report 2015

Annu

al R

epor

t 201

5

8

South Staffs Water is a water only company, supplying around 1.6 million customers in the South Staffordshire and Cambridge regions. The business bills customers for sewerage services on behalf of both Severn Trent Water and Anglian Water Services.

A period of changeThis has been a year of challenge and change, during which the business has maintained its firm focus on delivering both high quality service and value for money.

In December the business received its Final Determination from Ofwat, representing the culmination of the regulatory price review process (PR14) for the period 2015-2020. This will see bills reduce by 4% in real terms over the five year period with customers continuing to enjoy the benefits of one of the lowest bills in the industry. Levels of service in a number of areas will also increase in

addition to the business’ commitment to the community and affordability assistance for customers in need. In order to provide these important benefits to customers the business has, during the course of the year, had to make a number of difficult decisions as we sought to align our costs and performance with the new benchmark. These changes have included a reduction in manpower, the closure of the defined benefit pension scheme to future accrual as well as a variety of other changes to improve efficiency.

We are especially grateful for the dedication of our staff as they have continued to seamlessly provide the vital 24/7 service to our 1.6 million customers in South Staffordshire and Cambridge throughout these challenging times.

During the year to 31 December 2014, the Cambridge region met the required drinking water quality standard on 100% of all tests carried out, with the South Staffs region achieving a compliance rate of 99.98%. It has though become clear that the water quality performance at Seedy Mill treatment works requires investment. The business is committed to responding to the Drinking Water Inspectorate’s (DWI) legitimate criticisms about Seedy Mill and has already put in place a number of tactical mitigating actions ahead of agreeing a more strategic investment with the DWI which will restore the asset’s performance to the expected level and remove any immediate risk of quality failures. Similar investment is being actively considered in relation to Hampton Loade treatment works. We will work tirelessly to ensure customer interests continue to be protected in this key area of our operation.

As the UK water industry’s landscape changes, South Staffs Water remains committed to driving the delivery of exceptional customer service, high quality water and affordable bills.

Annual Report 2015

9

The last 12 months has seen the completion of our new nitrate treatment works at Fleam Dyke in Cambridge. This new plant will provide compliance with the regulatory standards for nitrate concentration through to 2035.

During the year it was confirmed that, for the three years to 2013/2014, the business was top in the industry for SIM, Ofwat’s measure of customer experience. This ranking is especially important as it acknowledges South Staffs Water and Cambridge Water as delivering the best customer experience out of the 18 companies in the England and Wales water industry. Whilst we are delighted with this achievement, the work continues on customer service and we are determined to maintain the business’ leading position. 4% reduction

in bills over next 5 years

top in theindustry for SIMfor the 3 yearsto 2013/14

£

10

Annu

al R

epor

t 201

5

• Weaimtoachieve100%waterquality compliance across both regions.

• Wearecommittedtoimprovinghow our customers perceive the quality of our water through its appearance, taste and odour, particularly in the South Staffs region.

In addition to our regulatory commitments, we have set improving the quality of our water as the pre-eminent target for the business moving forward. The period ahead will likely see significant investment into key production assets both in the South Staffs and Cambridge areas of operation as we seek to improve the water quality for customers in the long-term.

Secure and reliable suppliesAn unusually dry autumn period brought some challenge to the water resource position but this was managed effectively and resulted in no customer impact. We are pleased to report that we have a healthy resource position for the 25-year planning horizon with no new resource development required,

A plan for our futureThe last 12 months has brought about the completion of the PR14 regulatory process. The resulting plan has been founded on one of the largest pieces of customer engagement we have undertaken to date. This direction is expressed through 5 Outcomes and 15 specific Outcome Delivery Incentives, covering all aspects of our operations from excellent water quality and customer service to fair customer bills and environmentally sustainable operations, as well as the provision of secure and reliable water supplies. In addition, we have also developed further targets which will create sustained focus on employee satisfaction, health and safety and readiness for business retail competition.

Continued commitmentExcellent water quality now and in the futureThe quality of water we deliver to customers daily is ultimately the most important thing we do. Our commitment is to invest more in our treatment works and networks over the next five years and beyond.

Planning is at an advanced stage on the UK’s largest rainwater recycling system at the North West Cambridge development. The innovative development, in partnership with the University of Cambridge, has two water supplies installed on the 150 hectare site – one which recycles rain and surface water to use for flushing toilets, clothes washing and garden watering, and another supplying high quality treated water for drinking, cooking and bathing. Both are designed to minimise potable water consumption at the £1 billion development which will include 3,000 homes, 2,000 student rooms, a supermarket, hotel and school, as well as other community facilities.

We have finished the AMP 5 investment period having delivered our plans and commitments yet remain mindful of the challenge and opportunity that AMP 6 presents. The next five years will undoubtedly require increased innovation and greater customer engagement alongside our traditional focus on operating efficiency, long-term asset stewardship and excellent customer experience.

Annual Report 2015

11

although we have increased our long-term focus on water resource planning in the Cambridge region as this area is more constrained than the South Staffs region. Water efficiency will continue to be a key focus and we are committed to helping all of our customers change the way they value and use water every day. We need to protect our water supplies as our communities grow and demand increases. We are anticipating significant population growth in the Cambridge region over the coming years accompanied by increased pressure on water resources. We will work closely with the Environment Agency to balance the needs of customers with the environment.

We will continue to:• Ensuresupplyinterruptionsareless

than 10 minutes when supply is affected.

• Ensureourpipesandnetworksarewell maintained.

• Investinefficientpumpingstationsacross our regions to make sure supplies are secure and reliable.

• Increaseeducationalengagementconcerning water efficiency.

Excellent service to customers and the communityWe remain committed to exceeding our customers’ expectations. With the introduction of new SIM measures, we will continue to target being in the industry upper quartile. We will continue to invest in the training and

development of all of our front line staff both in our contact centre and out in the field to ensure we deliver a seamless experience with first time resolution of customer issues where possible.

As communication channels grow and expectations change, our investment in a new website and multi-channel contact system will provide greater choice and flexibility for our customers – making it simple, flexible and accessible whatever the channel of choice.

We will deliver at least 400 days of employee volunteering within our communities per year. From help with events, education programmes and

UK’s largest rainwater recycling system at the North West Cambridge development will supply

3000homes

2000student homes

school andsupermarket

12

Annu

al R

epor

t 201

5

Over the next five years, we will engage each year with 30,000 customers in debt, helping them manage their water accounts and take control of their water consumption through metering. Many customers are better off on a meter, particularly if they combine this with water efficiencies in the home and in the garden. We will continue working to support customers switching to a meter where they choose to or it is in their interests.

Our people are our businessWe recognise the outstanding commitment of our employees. There has been an even greater focus on employee safety and this is endorsed by our target to reduce accidents within the workplace by a further 10% over the next 12 months.

We are also committed to making South Staffs Water a great place to work. Our employee survey has played an important role in us understanding the feelings and motivations of our people and we will continue to use

school visits to biodiversity projects that will enhance the environment, we will raise our profile and develop strong and lasting partnerships.

Operations that are environmentally sustainableOur long term track record on leakage is good and we will aim to maintain this high level of performance. The average level of leakage during 2014/15 was below the target set by Ofwat although higher than 2013/14, primarily due to an increase in burst mains.

Our commitment to the environment will see us deliver innovative biodiversity projects across our regions, and at the same time, we are committed to reducing our carbon emissions from the power we use to pump water around our networks.

We will continue to invite our communities to visit our sites that are open to the public and continue to promote an active education programme to support local

school children in growing their knowledge of the water cycle and the environment we live in.

Fair customer billsWe are committed to making sure our bills remain affordable. Our customer bills have been 24% lower than the national average and, over the next five years, we are committed to ensuring our bills will fall by 4% in real terms and will continue to support our most vulnerable customers with help when they need it most. During 2014/2015, we provided debt support to 17,866 customers across both regions.

For customers that struggle with bills, we have a range of solutions including our Charitable Trust, Water Direct and WaterSure. The year ahead will see us develop our strategy on affordability and shape our approach to offering a social tariff for customers that need additional financial support, which is expected to launch in April 2016.

13

Annual Report 2015

this measure to develop training programmes that will enable people to develop new skills.

Retail readinessAs the blueprint for competition within the non-household sector is now almost complete, we are preparing systems, processes and organisational structures to accommodate this shifting landscape. We fully understand the proposed direction and welcome the prospects that retail will bring to our industry and how it will shape and transform our business.

The year aheadThe business remains focused on delivering its primary objective of supplying excellent water quality consistently to customers as well as achieving our broad range of other performance commitments. We see our commitment to stakeholder engagement, customer challenge and transparency increasing still further. We will continue to provide our people with a safe and rewarding working environment.

As we begin the next five year regulatory cycle we are focused on ensuring that the predicted benefits of investing £480 million are realised to their full extent.

£480millionplanned AMP 6investment

Strategic Report:

SSI Services

Annu

al R

epor

t 201

5

16

SSI Services is made up of three business areas: Clean Water, comprising IWS and Hydrosave; Wastewater, made up of OnSite, OnSite Specialist Maintenance and Perco Engineering Services; and Water Hygiene which also trades as IWS. In addition Omega Red, which provides lightning protection and electrical earthing services, also trades as part of SSI Services.

Review of last yearLast year was a challenge for SSI Services, being the last year of the water industry five-year AMP cycle when spending by some of our largest clients is typically lower than normal. In spite of this, the division has managed to grow revenue through a combination of new contract awards, new service offerings that have been developed and one off projects. However profit margins have been impacted, partly

services through a number of specialist operating companies using a nationwide mobile operation and maintaining long-term relationships with our customers, providing a quality service at competitive prices.

The division has around 1,500 employees, all of whom are key to us being successful, with the majority operating remotely and in often challenging environments. Health and safety is therefore very important to us and we continue to focus on developing a strong health and safety based culture across all of our businesses. We have seen frequency and severity rates of accidents reduce further in the year, as well as achieving a number of awards and maintaining our existing accreditations.

SSI Services is the Group’s specialist infrastructure contracting division. We provide a broad range of specialist infrastructure based services from design through to installation, testing and repair to long-term maintenance. Our focus is on regulated environments and legislative needs, managing client risk and using specialist technologies to provide added value.

We have developed a broad customer base across both the public and private sectors from all major water utilities, government agencies and local authorities through to major contractors and facilities management (FM) companies. Whilst we historically mainly worked in the water and wastewater sector, we are now increasingly operating in the water hygiene, rail, power generation, industrial and construction markets. Our strategy is to deliver these

SSI Services is focusing on enhancing productivity, including investment in technology, to fully benefit from opportunities that are arising.

Annual Report 2015

17

due to the mix of work available with less emphasis by our clients on planned work, and start-up costs on some contracts. In response to changes in activity and margin, SSI Services has sought to drive productivity and to reduce overhead, putting itself in a good position to benefit from an anticipated increased expenditure from our clients in this new year and new AMP cycle.

Clean Water ServicesThe Clean Water business includes three operating units – IWS Mechanical and Electrical (M&E) Services, IWS Pipeline Services and Hydrosave, which provides water management services; with a number of common clients across the three businesses.

Busi

ness

are

as:

cleanwater

waterhygienewastewater

1500employees

lightningprotection

Annu

al R

epor

t 201

5

18

The business continued to provide its specialist services to a number of the Water and Sewerage companies, together with government agencies, which also includes the provision of versatile temporary and environmentally friendly dams (branded as Portadam). The new contract secured in Canada to provide CCTV and sonar surveys was mobilised during the year and represents a step up in the scale of work by OnSite in that country. A key development has been the successful establishment of OnSite Rail which provides OnSite’s wastewater services to the rail sector, focussing on drains, culverts and water courses on and under the tracks and stations, thereby reducing the impact on OnSite of the AMP cycle in the water industry.

During the year, OnSite’s sewer lining business continued to work closely with our key customers, including a number of the Water and Sewerage companies, providing CIPP and UV lining services.

its work with Thames Water. In addition, Hydrosave has continued to expand the interest in its proprietary valve release system and the offering of a complete valve maintenance service, as well as building on its track record of non-destructive testing of pipes and other specialist technical services which are used across the water utility industry.

Wastewater ServicesOnSite, which offers specialist wastewater services, including flow monitoring, sewer rehabilitation and CCTV surveys, had a difficult year due to the expected cyclical reduction in demand associated with the end of the water industry’s AMP period being more significant than had been expected. Although lower margin reactive work continued at higher levels in the year, OnSite has now terminated this reactive work following the year end to focus on its higher margin activities.

The M&E business has continued to see revenue growth in the year with its key clients and has a number of important long-term framework contracts that it is tendering for which provide good opportunities for further growth and will replace the loss of work with the Coal Authority with whom the business had worked for a number of years.

Pipeline Services has also grown its revenue in the year. In addition to work carried out for South Staffs Water, the business has increased work for a range of other water industry customers and the current year should see margins on this new work improve.

Hydrosave specialises in leak detection and water management services. Hydrosave will continue to focus on providing leading leakage detection services to framework customers across the UK from Scotland to the South coast. During the year Hydrosave became sole supplier to Scottish Water and since the year end has significantly grown

Annual Report 2015

19

The specialist repair services of Perco, which offers no-dig technology services, and OnSite Specialist Maintenance, our specialist structural repairs and waterproofing business, both undertook a number of successful projects for a range of customers across different sectors during the year.

Water HygieneIWS Water Hygiene is a market leading provider of legionella control services and water hygiene risk assessment, maintenance and remedial works, together with a comprehensive water treatment service, to a wide range of customers including local authorities, housing associations and FM

companies. The business offers a 24 hours a day, 365 days a year national mobile service supported by the use of technology, which we continue to invest in.

IWS Water Hygiene secured a number of new clients during the year and continued to enhance operating efficiency following the investment in business development resources as well as operational initiatives. Further growth is anticipated reflecting the full year benefit of contracts already secured and the pipeline of opportunities being pursued.

Looking to the futureLooking ahead, SSI Services is well placed to see further growth as it pursues a number of opportunities and expects to start seeing the upturn in water industry expenditure during the year, coupled with a reversal of the decline in profit margins following a series of initiatives to improve efficiency and control cost. A number of new activities such as Onsite Rail are also looking promising to support this future growth.

Nationwide mobile

operation

Strategic Report:

Echo

Annu

al R

epor

t 201

5

22

The expansion of non-household retail competition in 2017 is a significant priority for UK water companies. Acknowledging this, we have been heavily engaged with water companies on the potential for RapidXtra to service their commercial customer retail system requirements.

This engagement, combined with the significant investment made in product development, has already resulted in contracts being secured for Anglian Water Business and Severn Trent Services. These successes should provide the foundation for RapidXtra to be the water billing system of choice within the new ‘competition’ based market.

2014/15 was a year of growth for Echo with some significant contract wins, strategically important contract renewals and an array of ongoing implementations. Over achieving against both profit and cash targets, Echo also launched a new corporate website and created a vision, mission statement and a set of values that outline the company’s core purpose, ethos and culture, which will underpin the business strategy moving forward.

Market leading customer billingEcho’s billing and customer information system, RapidXtra, continues to hold a market leading position within the UK water sector. With nine client implementations already delivered, RapidXtra’s single largest client, Dŵr Cymru (Welsh Water), serving approximately 1.5 million homes and businesses, went live successfully with the system in 2015.

Echo Managed Services (Echo) is a specialist outsourced provider of complex multi-channel customer contact services, comprehensive debt management solutions and the developer of the market leading water billing and customer information system, RapidXtra.

Echo’s key focus is to help its customers deliver a high quality end-to-end customer journey. Combining best practice specialist services and solutions with highly skilled and knowledgeable people, our three core services help our customers to improve their billing, debt recovery and customer contact processes to enhance their customers’ experience, build loyalty and enhance profitability.

Echo works closely with its customers in all areas of its core services, demonstrating a total commitment to quality customer experiences.

Annual Report 2015

23

Strengthening our collections divisionThe market for debt collection services remains buoyant and the demand for services is strong. The challenges of universal credit, protection for vulnerable customers, innovative methods of collections and ways of ascertaining customers’ ability to pay are key issues affecting the sector. Quality data, efficient systems and positive customer engagement are at the forefront of debt recovery strategies.

Our position in the sector has been further strengthened with the acquisition of utilities market specialist, Grosvenor Services Group in February 2015. Combining Grosvenor’s field based skills with our existing office based collections expertise and

888,246ceramic poppies

£30mEcho’s turnovergrew to over

for the first time £30m

93,000 calls handled for

Annu

al R

epor

t 201

5

24

comprehensive multi-site contact centre resource further strengthens the end-to-end customer contact proposition. The acquisition of Grosvenor follows our 2011 purchase of Inter-Credit International, which continues to demonstrate a consistent ability to outperform competitors on the contracts in which it operates.

Customer contact service excellenceOur Bristol operation continues to provide specialist outsourced, managed and insourced multi-channel customer contact services to leading public and private sector organisations, offering end-to-end contact management capabilities, from entry level bureau services through to comprehensive, analytics-enabled multi-channel programmes.

We were particularly proud to be chosen, due to our agile and flexible approach, to provide the customer contact service for the high profile Tower of London Remembers

campaign, an installation of 888,246 ceramic poppies to commemorate the fallen in World War I. In addition, Echo Bristol developed its 24/7 and out of hours services during the year with contract awards to deliver incident management services for Mouchel and Anglian Water.

In the water sector, SIM continues to shape companies’ approaches to improving the service provided to customers, including a focus on first contact resolution and reducing repeat and unwanted contacts. Echo works closely with its clients to improve their SIM performance, demonstrating a total commitment to quality customer experiences.

Since the new Northern Ireland Water contract was signed last July, Echo has been busy delivering service whilst implementing the structure and updated technology set to support the new contract. The new service combines innovative new functionality within RapidXtra including knowledge management

and multi-channel capabilities. The contract transition went smoothly and phase one of new technology deployment was successfully deployed in May 2015, with further software releases planned in September 2015 and in early 2016.

Our expertise in managing multi-channel customer contact programmes has assisted South Staffs Water in delivering their Digital Programme, providing enhanced Intelligent Voice Recognition (IVR) capability, a new website with extended “My Account” functionality and a richer, more flexible approach to handling multi-channel customer enquiries, designed to make it easy for customers to engage with their water company and resolve queries.

During the year, Echo’s customer service excellence received external recognition, as we were named as finalists for two European Contact Centre and Customer Service awards

Annual Report 2015

25

and one UK National Contact Centre award. We also joined the Institute of Customer Service, the UK’s independent professional body for customer service, a further indication of our ongoing commitment to deliver exceptional customer experiences on behalf of our clients.

Looking to the futureThis new year promises to be a year rich in opportunities for growth. In particular, it is anticipated that the expansion of non-household retail competition in the UK water industry in 2017 will create opportunities for Echo across all service areas.

Proud to be a member of the Institute of Customer Service

Through our focus on pursuing opportunities to add new clients, continuing to expand the services provided to existing clients and the ongoing process of identifying and acquiring businesses aligned with our strategy and which add value to our client base, we expect to see a period of sustained growth across our three core business areas.

To support this, Echo has strengthened the sales and marketing team and put in place a renewed strategy to establish our brand in sectors which offer opportunities for long-term growth.

Strategic Report:

Financial Review

Annu

al R

epor

t 201

5

28

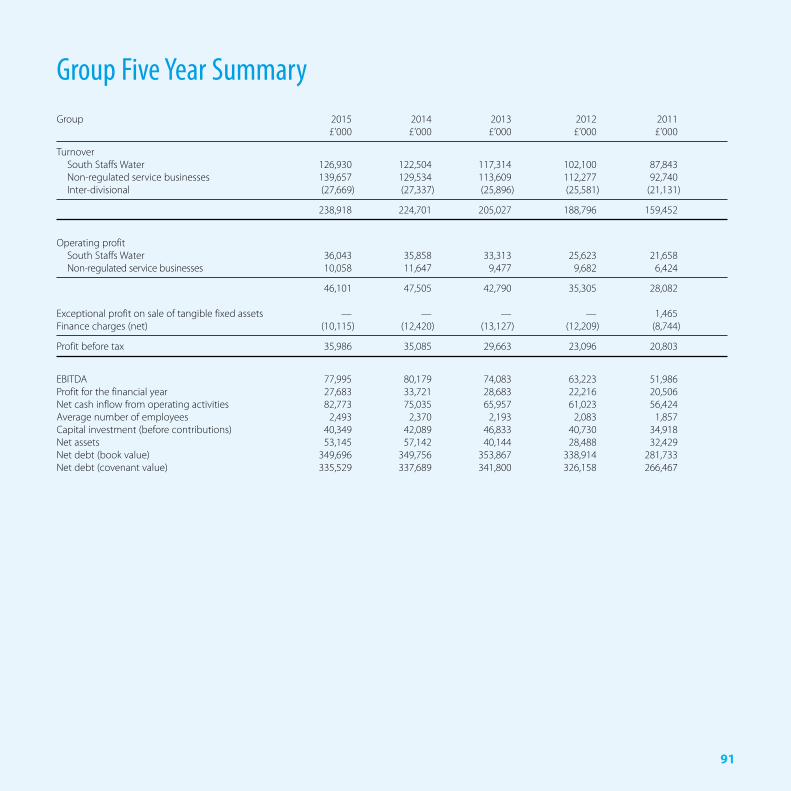

OverviewIn the year ended 31 March 2015, the Group achieved year-on-year growth in turnover, pre-tax profits and free cash flows that were also ahead of the Group’s budget, despite some significant challenges being experienced in the year.

The Group monitors its financial performance through its success in achieving or outperforming certain targeted Key Performance Indicators which include but are not limited to EBITDA, operating and pre-tax profits, free cash flow, net debt and trade debtor days.

Turnover & ProfitGroup turnover increased by £14.2m (6.3%) to £238.9m (2014: £224.7m) in the year, with growth experienced in all of the Group’s divisions. Turnover in South Staffs Water increased by £4.4m to £125.9m, largely due to the price increase on water bills allowed by Ofwat of 2.0%, being an increase in the Retail Price Index of 2.6% and a “k” factor for the year

of -0.6%, and also an increase in water consumption compared to the previous year. Turnover from the Group’s non-regulated service businesses increased by £9.9m (9.6%) to £113.0m, with another very successful year for Echo, including the positive impact of the completion in the year of significant projects and sales growth from new contracts awarded in the year. SSI Services also experienced sales growth particularly in the Clean Water operations although, as explained below, due partly to a change in the mix of work delivered compared to the previous 12 months this has not led to higher levels of profitability in the division.

The Group’s operating profit of £46.1m (2013: £47.5m) represents, a reduction of £1.4m from 2013/14 due largely to the impact of non-recurring costs in 2014/15 including restructuring charges that were necessary in all three divisions. However, the level of profitability was ahead of expectations at the start of the year.

Operating profit from South Staffs Water of £36.0m was marginally higher than 2013/14 and reflects the turnover growth detailed above, further operating cost efficiencies achieved in the business during the year, but partly offset by some specific cost increases, including energy related costs and non-recurring charges including those related to the necessary restructuring of the business in preparation for the new 5-year AMP 6 period which commenced in April 2015. Operating profit from our non-regulated businesses reduced to £10.1m (2014: £11.6m). This was despite higher turnover with the growth in sales more than offset by the impact of the change in the mix of work carried out in the SSI Services division, which saw a reduction in sales in more specialist higher margin activities, particularly in the water sector in the final year of the AMP 5 expenditure cycle, where customer budgets were tightened significantly and more than had been anticipated. The sales growth came in lower margin work and also there

The Group remains deeply committed to its focus on cash generation and to keeping working capital at efficient levels.

Annual Report 2015

29

were some non-recurring charges, again including restructuring costs in both Echo and SSI Services. Group EBITDA amounted to £78.0m (2014: £80.2m).

Group finance charges (net of interest receivable) reduced significantly to £10.1m (2014: £12.4) in the year mainly representing the full year impact of the refinancing of bank debt in 2013/14 at lower interest rates. Overall, profit before tax increased from £35.1m to £36.0m.

Tax The Group’s current tax charge increased by £0.7m to £4.9m, partly reflecting higher Group pre-tax profits. The total corporation tax charge for the year increased to £8.3m (2014; £1.3m) largely due to the charge in 2013/14 being reduced by a non-cash credit to deferred tax in respect of a reduction to future tax rates (£3.2m) and also the non-cash deferred tax impact of a reduction in discount rates at 31 March 2015

Group turnover increased by£14.2m to

£238.9m

compared to the previous year, which have increased the Group’s discounted deferred tax liabilities. Total corporation tax payments in the year amounted to £3.3m (2014: £2.4m).

Cash Flow Group cash flow from operating activities was well ahead of the target for the year and increased by £7.8m to £82.8m (2014: £75.0m) mainly as a result of favourable working capital movements compared to the previous year which is encouraging, especially given the sales growth achieved, which required working

2011 2012 2013 2014 2015

£66.0m£61.0m£56.4m£75.0m

£82.8mOperating cash flows

Annu

al R

epor

t 201

5

30

capital investment and that collection of trade debtors remains challenging. The Group remains deeply committed to its focus on cash generation and to keeping working capital at efficient levels.

The Group’s net cash interest payments of £6.0m reduced from the previous year by £1.9m again largely reflecting, as with the profit and loss charge, the full year effect of lower interest payments being made in the year due to lower rates achieved on bank debt that was refinanced in quarter 4 of 2013/14.

Group capital investment (net of disposals and capital contributions) was £34.1m compared to £35.6m in 2013/14. In total, South Staffs Water invested £32.0m (2014: £32.5m) in capital assets, (net of contributions), resulting in the overall 5-year cumulative AMP 5 expenditure (for the two regions of South Staffs and Cambridge) of £168.1m being in line with Ofwat’s Final Determination.

Overall, due to higher operating cash flows, lower interest payments and the planned reduction in capital expenditure in the year, free cash flow increased by £10.3m to £39.3m.

DividendsTotal dividends paid and proposed in the year to 31 March 2015 were £27.1m. This includes final dividends of £12.9m paid in the year but being in respect of the 2013/14 year and £14.2m interim dividends in respect of 2014/15.

Net Debt and LiquidityThe book value of Group net debt at 31 March 2015 amounted to £349.7m, largely the same as that at 31 March 2014 (£349.8m).This book value differs from the value used for borrowing covenant reporting purposes of £335.5m (2014: £337.7m) which excludes unamortised premium and issue costs and uses actual inflation at the relevant dates as opposed to the long-term inflation assumption used in the book value of index-linked debt. The reduction in the covenant value of net debt from March 2014 of £2.2m largely reflects overall cash generation of £5.6m, after acquisition payments and payment of dividends, partly offset by the impact of higher values for index-linked debt of £4.1m, representing indexation of these borrowings during the year.

In South Staffs Water, net debt for covenant reporting purposes was £217.0m (2014: £220.6m) being 63.3% (2014: 64.4%) of its Regulated Asset Value (RAV) of £342.8m (2014: £342.5) representing the PR09 Final Determination RAV uplifted for inflation. This ratio reflects the net impact of better than expected free cash generation in the year and inflation (RPI) at March 2015 of 0.9% (March 2014: 2.5%), which is used to inflate RAV, whereas the majority of index-linked debt was inflated using RPI at July 2014 which was higher at 2.5% (July 2013: 3.1%). While the dividend policy for South Staffs Water allows dividends to be paid up to 77% of net debt/RAV, the expectation for this ratio is in the region of 66%. The Group and South Staffs Water have maintained, and continue to forecast to maintain, significant headroom in respect of all borrowing covenants. Standard and Poor’s continues to rate South Staffs Water as BBB+ and South Staffordshire Plc continues to be investment grade rated.

At 31 March 2015, the Group had available £42.7m of undrawn bank borrowing facilities (2014: £37.4m) and surplus cash of £4.7m (2014: £8.1m), providing significant liquidity headroom.

Annual Report 2015

31

PensionsThe Group’s contribution to all of its occupational pension schemes in the year was a significant £6.1m (2014: £5.3m). During the year, the Group enrolled over 1,300 employees into a new Group Personal Pension Plan under the government’s Automatic Enrolment initiative. In order to reduce operating costs and cash flow uncertainty and increase pension benefit consistency across the Group, on 1 April 2015, the South Staffordshire section of the final salary Water Companies Pension Scheme (WCPS) was closed to future accrual with active member benefits accrued up to that date being preserved and increasing by inflation each year to retirement with contributions now being paid into an alternative defined contribution Group Personal Pension Plan to provide additional benefits.

The Cambridge Water section of WCPS was closed to future accrual in 2010. The Group’s current funding deficit contributions in respect of both of its sections of WCPS of £2.2m per annum plus inflation will continue to be paid. As at 31 March 2015 the actuarial valuation of the Group’s final salary pension schemes (prepared in accordance with FRS 17 for accounting as opposed to funding purposes) showed a post-tax surplus of £12.5m (2014: £12.2m).

Principal Risks and UncertaintiesThe Group has an established risk management framework which aims to ensure that all significant business and financial risks and uncertainties that the Group is exposed to are identified and appropriately managed. Significant risks and uncertainties of the Group that are

required to be managed include, but are not limited to, health and safety, water resources and quality, market reform in addition to product and service quality. The main financial risk the Group is exposed to is credit risk. Further details of financial risks and the way they are managed are provided in note 28 to the Financial Statements. The Board of Directors believe these risks are appropriately managed by the Group.

The Strategic Report on pages 4 to 31 is approved on behalf of the Board of Directors.

A PageGroup Chief Executive30 July 2015

1,300+employeesauto-enrolled into a new pension plan

South Staffs Water AMP 5 capital target of

£168 million invested

Corporate Social Responsibility

Annu

al R

epor

t 201

5

34

The Group recognises the obligations that come with Corporate Social Responsibility (CSR) and aims to be responsible and accountable in the way that we operate. In 2014/15, our CSR focus has remained on our employees, the environment, the communities in which we operate, and of course our customers.

EmployeesThe Group has around 2,500 employees, all of whom are critical to our continued success and development. All of our businesses continue to invest in their people, their health, safety and wellbeing and we aim to ensure South Staffordshire Plc remains a safe Group to work for and to provide a good working environment for everyone. -Health and safetyThe effective management of health, safety and wellbeing of our employees is of paramount importance to the Group.

Each business takes responsibility for the health and safety of all of its

employees. A Group level Health and Safety Strategy Forum, led by the Group Chief Executive and supported by the Group Health and Safety Manager, continues to oversee activities in this area of the business.

During the year, the Group established a long term Health and Safety Strategy, aimed at a year-on-year reduction in workplace accidents. The strategy covers five elements: Leadership, Management Reporting, Workforce Involvement, Risk Reduction and Accident Reduction.

Several initiatives were highlighted during the year, including:• Theimplementationofonline

driver licence checking within the Group’s fleet;

• Thedesignanddevelopmentofa Group Accident Database for the collation and reporting of all accident data, which should improve our response to accidents and help reduce them in future;

• Wellbeingweekswererunatvarious Group businesses;

• InOnSite,employeeswereengagedthrough a health and safety poster competition for their children;

• TheintroductionofHydrosave’sone minute safety check for van drivers provided a good visual communications safety campaign.

The majority of our businesses have external accreditation for their health, safety and environmental management systems. For example, IWS has been awarded five consecutive RoSPA Gold Medal Awards for Occupational Health and Safety, and in 2014 was a winner of the British Safety Council International Safety Awards. Many Group companies also hold ISO 9001 quality management and OHSAS 18001 Occupational Health and Safety management accreditations, and are part of the Safe Contractor schemes.

All employees have access to specialist health advisors who can provide proactive health surveillance and advice.

The Group carried out a range of CSR activities during the year, with specific focus on health and safety, biodiversity and charity involvement.

Annual Report 2015

35

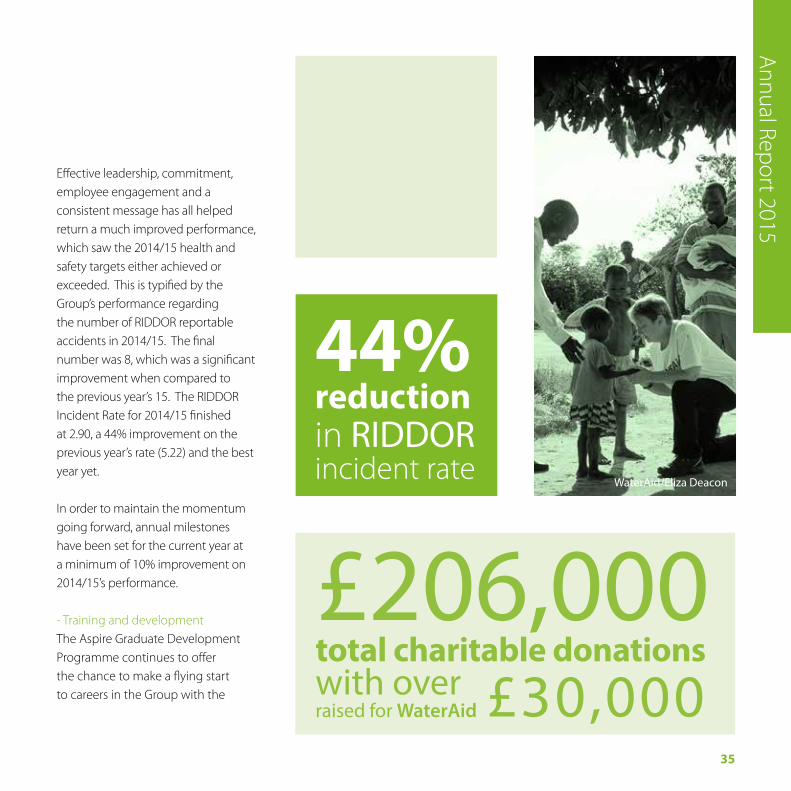

Effective leadership, commitment, employee engagement and a consistent message has all helped return a much improved performance, which saw the 2014/15 health and safety targets either achieved or exceeded. This is typified by the Group’s performance regarding the number of RIDDOR reportable accidents in 2014/15. The final number was 8, which was a significant improvement when compared to the previous year’s 15. The RIDDOR Incident Rate for 2014/15 finished at 2.90, a 44% improvement on the previous year’s rate (5.22) and the best year yet.

In order to maintain the momentum going forward, annual milestones have been set for the current year at a minimum of 10% improvement on 2014/15’s performance.

- Training and developmentThe Aspire Graduate Development Programme continues to offer the chance to make a flying start to careers in the Group with the

WaterAid/Eliza Deacon

44% reductionin RIDDOR incident rate

£206,000total charitable donations with over raised for WaterAid £30,000

Annu

al R

epor

t 201

5

36

opportunity for development in varied, challenging and fulfilling careers. Areas covered include project management, engineering, customer services, planning, people management, commercial and financial management.

During the year Echo started to create and develop a programme where each individual employee’s learning and development journey becomes a personalised experience, where the information that employees need is always within easy reach. The first stage of the project has been to create Echo’s new e-pod platform, where employees can access new articles and industry websites, call recordings demonstrating best practice, and e-learning modules, classroom sessions and open coaching sessions. Echo will also offer access to external development sites such as Future Learn and the Open University.

Our subsidiaries, Echo and Perco hold Investors In People (IIP) accreditations which recognise talent and reward success at every opportunity.

- Equality and fair treatmentThe Group has a policy of equal opportunities and non-discrimination in all forms of employment. All businesses are committed to a positive working environment, free from any discrimination or unfair treatment. Every reasonable effort is made to provide disabled people with equal opportunities for employment, training and promotion, having regard to their particular aptitudes and abilities.

EnvironmentMuch of the Group’s energy use is related to the essential water treatment and pumping activities of South Staffs Water. The Group continues to identify opportunities to reduce its energy consumption, by improving efficiency of operations and to investigate opportunities for generating renewable energy. This is key in managing and reducing carbon emissions and energy use for environmental benefit and the associated cost savings. The Group also works on a number of biodiversity, water efficiency and community education programmes.

The South Staffs Water Employee Volunteer Scheme presents staff with the opportunity to work in the community on various projects. The partnership with the Black Country and Birmingham Wildlife Trust, which began in March 2014, has continued throughout the year with a range of activities to increase biodiversity at an area of land owned by South Staffs Water with public access at Sedgley Beacon.

South Staffs Water also actively took part in Water Saving Week. Activities included visiting key accounts, local Citizens Advice Bureaux and community groups to encourage customers and businesses to become more water efficient.

SSI Services also makes environmental matters a priority. Each of the businesses within the division has a QUENSH manager who coordinates their business’ environmental activities. These range from working to reduce site waste to promoting safe and efficient driving and procuring materials and equipment with consideration to reducing the environmental impact of our operations.

Annual Report 2015

37

As a result of their activities in this area, a number of businesses have achieved and maintained ISO14001 Environmental Management status.

CommunitiesOur CSR programme is focused on giving something back, at a grass roots level, to the communities we serve and operate in, as well as further afield.

The Group made charitable donations of £206,000 during 2014/15, in addition to the Group’s coordination of WaterAid fundraising activities continuing in force. South Staffs Water was able to raise its highest ever sum of £12,000 at its annual dinner dance, which included a talk from our education co-ordinator, who spent a week in Uganda seeing first-hand the services WaterAid is able to provide. Over £30,000 was raised for the charity during the year.

During the year, South Staffordshire Plc employees took part in a Wolf Run 10km obstacle course and Hydrosave employees organised a cake bake, raising a total of over £4,000 for Acorns Children’s Hospice, a Midlands-based charity offering a network of care for life limited and life threatened children and young people, and their families.

Echo Managed Services were proud to be involved with planting poppies at the Tower of London, through their contract with Historic Royal Palaces to handle public orders for the ceramic works of art. Downing Street beckoned for one South Staffs Water employee as a thank you for his awareness raising and fundraising activities for the Liam Fairhurst Foundation.

Education also plays a vital role in all our community engagement activity. Throughout recent years we have continued to develop our portfolio of education support to enable us to offer benefits to the wider community. We work closely with a range of schools and education partners to offer children and adults opportunities to enhance their understanding of the world of work and the water industry, as well as

more global subjects such as water and the environment.

For example, to help raise awareness of Water Saving Week, South Staffs Water invited pupils from a local primary school to design a water saving advert, with the winning design reading “Let’s all save water because we have some and some don’t” being featured in the Express and Star.

CustomersPutting customer satisfaction at the top of the Group’s agenda, building and further developing relationships with our customers, whether household or business customers, and innovation are all key to the future of the Group.

38

Annu

al R

epor

t 201

5

38

3. Dave TaylorManaging Director of SSI ServicesAppointed Managing Director of SSI Services in May 2015, having been the Managing Director and founder of OnSite Specialist Maintenance, formerly Data Contracts, for several years before moving into a divisional role at SSI Services as Commercial Director in January 2015.

4. Nigel BakerManaging Director of EchoAppointed as Managing Director of Echo in April 2014 having been Operations Director since October 2005. Prior to working with Echo, Nigel worked with Barclays Stockbrokers and Charles Schwab Europe.

1. Adrian PageGroup Chief ExecutiveAppointed as Group Chief Executive in January 2013, having been Group Finance Director since April 2004. Previously Group Finance Director of South Staffordshire Group Plc from 1998 to 2002. Prior to this Adrian was with ACT Group and KPMG. Adrian is also a Board member for the Water Companies Pension Scheme Trustee Company.

2. Phil NewlandManaging Director of South Staffs Water Appointed Managing Director of South Staffs Water in April 2014 having previously been Managing Director of Echo. Prior to joining Echo, Phil was a Management Consultant with Automatic Data Processing (ADP) and Terence Chapman Associates.

The Executive Team

5. Jason GoodwinDirector of Finance and Company SecretaryAppointed as Director of Finance in October 2007 having joined the Group as Group Financial Controller in March 2004 prior to its demerger from Homeserve Plc. Prior to this Jason spent over six years with Deloitte. Jason is also Company Secretary and a Trustee of the South Staffordshire Money Plan Pension Scheme.

1. 3. 4. 5.2.

39

Annual Report 2015

39

Directors Jesús Olmos - Chairman

Adrian Page

Ram Kumar

Roger Ammoun

Secretary Jason Goodwin

Registered Office Green Lane, Walsall, West Midlands, WS2 7PD

Telephone: 01922 638282 Registered in England, Number 4295398

Auditor Deloitte LLP

Four Brindleyplace, Birmingham, B1 2HZ

Corporate Information

40

Annu

al R

epor

t 201

5

40

Directors’ Report

Appointed

Mr A Page (Group Chief Executive) 4 December 2003

Mr J Olmos* (Chairman) 30 July 2013

Mr R Kumar* 30 July 2013

Mr R Ammoun* 30 July 2013

* Denotes a Non-Executive Director

The Directors have pleasure in presenting their Annual Report for the year ended 31 March 2015.

Major Corporate TransactionsThere were no major corporate transactions occurring in the year ended 31 March 2015.

Except for any matters referred to elsewhere in this Annual Report, there have been no other significant events affecting the Group since 1 April 2015.

Financial ResultsThe Group’s turnover increased to £238.9m (2014: £224.7m) with operating profit of £46.1m (2014: £47.5m) and profit before tax of £36.0m (2014: £35.1m). The Group’s financial results and position are explained in more detail in the Financial Review section of the Strategic Report on pages 26 to 31 and shown in the consolidated profit and loss account, consolidated balance sheet and consolidated cash flow statement on pages 54, 55 and 58.

Financial and Treasury RiskDetails of the Group’s policy in respect of financial and treasury risk are provided in note 28 to the financial statements.

Fixed AssetsCapital expenditure before contributions from third parties, including infrastructure renewals, amounted to £40.3m (2014: £42.1m) during the year.

DirectorsNo Director had any material interest in any contract of significance with the Company or Group during the year under review.

Details of the Directors who held office during the year and subsequently are provided in the table below:

Indemnities have been given to all of the Directors to the extent permitted by the Companies Act. Directors and Officers insurance has been established for all Directors, executives and senior management to provide cover against any actions bought against them as Officers of the South Staffordshire Plc group of companies.

Retirement and Re-Election of DirectorsIn accordance with the Companies Act 2006 and the Articles of Association, Mr Page and Mr Ammoun will retire by rotation and being eligible will offer themselves for re-election.

41

Annual Report 2015

41

Corporate Social ResponsibilitySouth Staffordshire Plc regards compliance with relevant environmental laws, the adoption of responsible social and ethical standards and the health, safety, wellbeing and development of its employees, including disabled persons, as integral to its businesses. A summary of the Group’s practices and activities in this regard is provided on pages 32 to 37.

Corporate GovernanceA report on corporate governance is set out on pages 42 to 50.

Payment of Suppliers and Commercial ArrangementsThe Group’s policy is to pay suppliers in line with the terms of payment agreed with each of them when contracting for their products or services. Group trade creditors at 31 March 2015 represent 59 days of purchases during the year (2014: 50 days). The increase over the previous year is as a result of the high level of capital expenditure in March 2015 compared to March 2014. The Group is not reliant on any single commercial arrangement.

Going ConcernThe Directors consider each year the appropriateness of the assumption of preparing the financial statements on a going concern basis. This is based upon a review of the Company’s and the Group’s business plan, budget, financial forecasts, investment programme, and the forecast compliance with borrowing covenants, availability of undrawn borrowing facilities and surplus cash to provide liquidity and also based on the Group’s strong track record of renewing or replacing the Group’s borrowing facilities when they mature to provide liquidity.

The Group’s business activities, together with the factors likely to affect its future development, performance and position, are set out in the Strategic Report from pages 4 to 31. The financial performance and position of the Group, its cash flows, liquidity position and borrowing facilities are described in the Financial Review on pages 26 to 31. After making enquiries, the Directors have a reasonable expectation that the Company and the Group have

adequate resources to continue in operational existence for the foreseeable future. Accordingly, they continue to adopt the going concern basis in preparing the accounts.

Independent AuditorIn accordance with the Companies Act 2006, the Directors confirm that as far as they are aware, there is no relevant audit information of which the Company’s auditor is unaware and that the Board has taken all reasonable steps to make itself aware of any relevant audit information and to establish that the Company’s auditor is aware of that information.

A resolution proposing the reappointment of Deloitte LLP as auditor will be put to the Annual General Meeting.

By Order of the Board

J GoodwinCompany Secretary30 July 2015

42

Annu

al R

epor

t 201

5

42

The Group seeks to apply the principles of the UK Corporate Governance Code (“the UK Code”), where considered applicable to a private, unlisted group. The Group also applies the Walker Guidelines on transparency and disclosure and regularly monitors corporate governance best practice and the applicability of any developments to the Group. Any changes to the Group’s governance arrangements considered appropriate are implemented within agreed timescales.

South Staffordshire Water PLC Corporate GovernanceSouth Staffordshire Water PLC continues to apply the principles of its own Corporate Governance Code (the “SSW Code”) which it implemented in response to Ofwat’s published principles on board leadership, transparency and governance. Although South Staffordshire Water PLC is not a public listed company, its Board of Directors recognises that they should act, where applicable, as if it were

and therefore the SSW Code has also specifically drawn on certain principles of the UK Code that may be applicable to a privately owned regulated company. A copy of the SSW Code can be found on South Staffs Water’s website (www.south-staffs-water.co.uk).

As the immediate parent company of South Staffordshire Water PLC, South Staffordshire Plc and its Board of Directors recognise the responsibilities that come from providing a public service and the Company is therefore fully committed to maintaining high standards of leadership, transparency and governance as a parent of a regulated business. The Company maintains an open dialogue with all of its subsidiaries and fully supports South Staffordshire Water PLC in complying with its statutory and regulatory obligations, including but not limited to Condition P of its licence and the SSW Code and ensuring that it can make strategic and sustainable decisions that are in the long-term interests of the

regulated business. Details of how South Staffordshire Water PLC follows the principles in the SSW Code are provided separately in its own Report and Accounts for the year ended 31 March 2015. Details of how South Staffordshire Plc, as the immediate parent of South Staffordshire Water PLC, follows Ofwat’s Holding Company Principles are detailed in this Corporate Governance report.

The Board can also confirm, on behalf of KKR Infrastructure Limited, that it, as the ultimate controlling party of the Group, also fully supports these Holding Company Principles from Ofwat and it will continue to apply high standards of board leadership and governance.

There have been no material changes to Corporate Governance arrangements in the Group during the year. The Board confirms that, to the best of its knowledge, there are no issues or risks at the Group level which may negatively impact on South Staffordshire Water PLC.

Corporate Governance

43

Annual Report 2015

43

Group StructureThe Group is owned by the Global Infrastructure Fund of the investment business Kohlberg Kravis Roberts & Co. L.P. (KKR), which is quoted on the New York Stock Exchange, and which holds a majority interest in the Group, together with infrastructure funds of certain co-investors of KKR. The KKR Infrastructure Fund is controlled and managed by KKR Infrastructure Limited, a company registered in the Cayman Islands (the “Holding Company”).

South Staffordshire Plc, as the immediate parent company of South Staffordshire Water PLC, ensures through its detailed knowledge of all of its subsidiaries and the water industry that it understands the duties and obligations of a regulated company including Condition P of its licence and, although some Directors sit on both Boards, South Staffordshire Water PLC acts, where applicable, with the support of the Company, as if it were a separate listed company. South Staffordshire Plc has processes in place to provide

South Staffordshire Water PLC with information that it requires about the wider Group. South Staffordshire Plc provides management, professional and administrative support services to South Staffordshire Water PLC and other of its subsidiaries on a cost basis. There is no direct interaction between South Staffordshire Water PLC and the Holding Company.

There are a number of UK registered intermediate holding companies above South Staffordshire Plc in the Group structure, headed by Hydriades IV Limited, the ultimate holding company registered in the UK. There are also intermediate holding companies above Hydriades IV Limited which are registered in Jersey but which are resident in the UK for tax purposes. In line with other KKR investments in Europe, the parent of the Jersey resident companies is a company registered in Luxembourg (Selena Luxco S.à.r.l.), which is the company in which the long-term infrastructure funds of KKR and their co-investors invest. The KKR fund investing in this company is controlled

and managed by the Holding Company. Two of the UK holding companies have loans payable to South Staffordshire Water PLC, both of which bear interest which is paid in full each year. Any UK tax losses surrendered to South Staffordshire Water PLC are paid for at face value.

Details of the borrowings of the Group are provided in the financial statements including the analysis of net debt and the notes to the financial statements. Similarly, details of the borrowings of South Staffordshire Water PLC are provided in its own Report and Accounts.

The Board of DirectorsThe Board is collectively responsible for the long-term success of the Group’s businesses. The Board comprises one Executive Director and three Non-Executive Directors.

Directors may be appointed by the Company by Ordinary Resolution or by the Board. As set out in the Company’s Articles of Association, a Director appointed by the Board

44

Annu

al R

epor

t 201

5

44

businesses and those prepared at a Group level. The Non–Executive Directors, headed by the Chairman, have a duty to oversee this work, and to scrutinise management performance. They constructively challenge and help develop proposals on strategy.

In conjunction with the Audit Committee, the Board is also responsible for the Group’s systems of internal control, evaluating and managing significant risks to the Company and the Group.

On joining the Board, Directors receive induction material appropriate to their needs. This may include information on the Group structure, the financing structure, the regulatory framework of the operating businesses within the Group and strategic and financial plans. The Board carries out site visits to maintain familiarity with the Group’s operations and to refresh their skills and knowledge. The Board also keeps up to date with

and all of the UK registered holding companies in the Group structure.

Functions of the BoardUnder the UK Code, a company should be headed by an effective Board, with duties aligned to the success and interests of the company, setting strategic goals and ensuring that company strategy is fulfilled.

In compliance with the UK Code, all Board members are provided with sufficient information prior to any Board meeting to allow appropriate preparation to ensure that they can properly discharge their duties.

The Board sets standards of conduct to promote the success of the Company and the Group, provides leadership, and reviews the Group’s internal controls, risk management policies and governance structure. It approves major financial and investment decisions over senior management thresholds and evaluates the performance of the individual businesses and the Group as a whole by monitoring reports received directly from the subsidiary

will hold office until the next Annual General Meeting (AGM). At each AGM one third of the Directors will retire by rotation and will submit themselves for re-election at least once every three years.

All Directors and senior management are covered by a Directors & Officers Insurance policy against any actions taken against them as Officers of the Group.

Senior Executives of KKR or its affiliates and its co-investors who hold positions on the Board of the Company are Jesús Olmos and Ram Kumar, both of whom are also Non-Executive Directors of South Staffordshire Water PLC and Directors of holding companies above South Staffordshire Plc in the Group structure, and Roger Ammoun. Adrian Page, Group Chief Executive of South Staffordshire Plc, is also the Chairman of South Staffordshire Water PLC and is a Director of all of South Staffordshire Plc’s subsidiaries

45

Annual Report 2015

45

• Reviewandapprovalofmajorcontracts

• Powerstodelegateauthority

Whilst South Staffordshire Water PLC acts, where applicable, as though it were a separate public listed company, a limited number of matters in respect of this subsidiary company also need the approval of the Board of South Staffordshire Plc. These include:

• MaterialsubmissionstoOfwat,particularly in respect of Price Reviews and major structural reform

• AppointmentandremovalofanyDirector, in its role as shareholder

• Prosecution,defenceorsettlement of litigation above £1 million; and

• Materialchangestopensionarrangements where operated on a Group basis

The Board carries out an informal evaluation of its own performance, the performance of the individual Directors and various Committees.

All Directors are aware of the procedure for those wishing to seek independent legal and other professional advice. The Board also has access to the advice and services of the Company Secretary.

Matters Reserved for the BoardA schedule of matters specifically reserved for the Board’s decision has been adopted based on Institute of Chartered Secretaries and Administrators (ICSA) best practice.

The matters include, but are not limited to:• Reviewingandapprovingthe

Group’s strategy• Approvalofcapitalandoperating

budgets• Reviewingandapprovingany

material changes to the Group’s capital structure

• Reviewandapprovaloffinancialreports

legal and regulatory changes and developments by receiving written updates from both internal and external advisers.

The Board maintains a flexible approach to Board matters with the delegation of power to a Committee, with precise terms of reference, being used for specific routine purposes. Both the terms of reference and composition of the Committees are regularly reviewed to ensure their ongoing effectiveness.

The Directors are supported by an executive team and by other senior managers who have responsibility for assisting them in the development and achievement of the Group’s strategy and reviewing the financial and operational performance of the Group and its individual businesses. Senior management is responsible, along with the Board, for monitoring policies and procedures and other matters that are not reserved for the Board. There are written procedures containing a regime of authorisation levels for key decision-making.

46

Annu

al R

epor

t 201

5

46

and associated guidance and to obtain reliable, up-to-date information about remuneration in other companies

• Approvethedesignof,and determine targets for, any performance related remuneration packages operated within the Group

• Ensurethatcontractualtermson termination are fair and that failure is not rewarded

• Overseeanymaterialchangesin employee benefits structures throughout the Group.

– Nomination CommitteeIn addition to conducting a rigorous process when making appointments to the Board, the Nomination Committee is responsible for reviewing the balance of skills and knowledge on the Board. It also keeps under review the possibility of any actual or potential conflicts of interest.

The Nomination Committee is formed on an ad hoc basis, when the need for an appointment to the

Board Committees– Remuneration CommitteeThe Remuneration Committee is responsible for the Group’s remuneration policy and the setting of the remuneration packages of the Board, executive team and other senior management. No Director is involved in determining his or her own remuneration. During the year the Remuneration Committee comprised of Jesús Olmos, Ram Kumar and Adrian Page.

The key terms of reference for the Committee are to:• Agreeremunerationthatwill

ensure that the Executive Director, the executive team and other senior management are provided with appropriate incentives to achieve high standards of performance and reward them for their individual contributions to the success of the Group

• Determinesuchpackagesandarrangements with regard to any relevant legal requirements

RemunerationRemuneration packages are designed to attract, retain and motivate high-calibre senior executives. The Remuneration Committee has overall responsibility for determining the Executive Director’s remuneration package and those of the executive team and other senior management. Non-Executive Directors do not receive any remuneration or fee from the Company.

The total remuneration package of the Executive Director, executive team and other senior management includes basic salary, benefits and an annual bonus that is linked to individual business and Group targets and personal performance related objectives. Performance related objectives are designed to encourage and reward continuing improvement in the Group’s performance and value.

47

Annual Report 2015

47

The members of the Audit Committee are Ram Kumar and Adrian Page, who receive written reports from Internal Audit and the external auditor twice a year.

Deloitte LLP (the Group’s external independent auditor), the Company Secretary, the Group Internal Audit Manager and, where appropriate, other financial management also receive this information and are invited to Audit Committee meetings. The Board is satisfied that the members of the Audit Committee have recent and relevant financial experience and are able to approach matters with a level of independent judgement.

The work of the Audit Committee specifically covers group business risks, and the work of Internal Audit and the external auditor.

In order to facilitate the Group’s risk management process, key risks facing each business within the Group and the Group as a whole are regularly reviewed, documented and

Board is identified or as otherwise considered appropriate by the Board.

– Audit CommitteeThe main role and responsibilities of the Audit Committee are set out in written terms of reference and include:• Monitoringtheintegrityof

financial statements and reviewing significant financial reporting judgements contained therein

• ReviewingtheGroup’sinternalfinancial controls

• Monitoringandreviewingtheeffectiveness of the Group’s Internal Audit function

• RecommendingtotheBoardthe appointment of the external auditor and monitoring the auditor’s independence, performance and effectiveness and approving the nature and scope of material external audits and approving the auditor’s remuneration.

summarised by senior management. Every six months the management teams of each business formally discuss, review, approve and document the relevant business risks. The objective of this process is to ensure that each management team is identifying, prioritising and rating all key business risks, and implementing and amending, where necessary, appropriate procedures and controls as required to mitigate these risks. It also allows management to highlight, document and prioritise as appropriate any outstanding actions with respect to the implementation of these procedures and controls. The Internal Audit function also critically assesses the risks, controls and procedures identified and the rating assigned to them. This information is reviewed by the Audit Committee.

Every year the Audit Committee receives an Internal Audit report on the results of internal audit work together with agreed management actions in relation to audit recommendations.

48

Annu

al R

epor

t 201

5

48

The internal audit work covers financial and operational risk assurance, regulatory assurance, testing of legal compliance and financial controls and other business commercial support work.

The Group’s external auditors, Deloitte LLP, attend Audit Committee meetings and provide detailed reports regarding audit planning and the results of their external independent audit.

The responsibilities of the external independent auditor in the area of financial reporting are set out in their report in each year’s Annual Report.

Accountability and Audit– Financial Reporting and SystemsThe Board of Directors recognises the need to present a balanced, understandable and clearly defined assessment of the Group’s operational and financial performance and position including its future

prospects. This is provided by a review of the Group’s performance as set out in the Strategic Report of each year’s Annual Report.

Business plans, annual budgets and investment proposals for each business, and for the Group, have been formally prepared, reviewed and approved by the Board. These include profit and loss and cash flow forecasts. Actual financial results and cash flows, including a comparison with budgets and forecasts, are regularly reported to the Board with variances being identified and used to initiate any action deemed appropriate. Forecasts of the Group’s compliance with its borrowing covenants are also prepared on a regular basis, and forecasts of the Group’s level of its undrawn and available borrowing facilities for liquidity purposes are also prepared and reported to the Board.