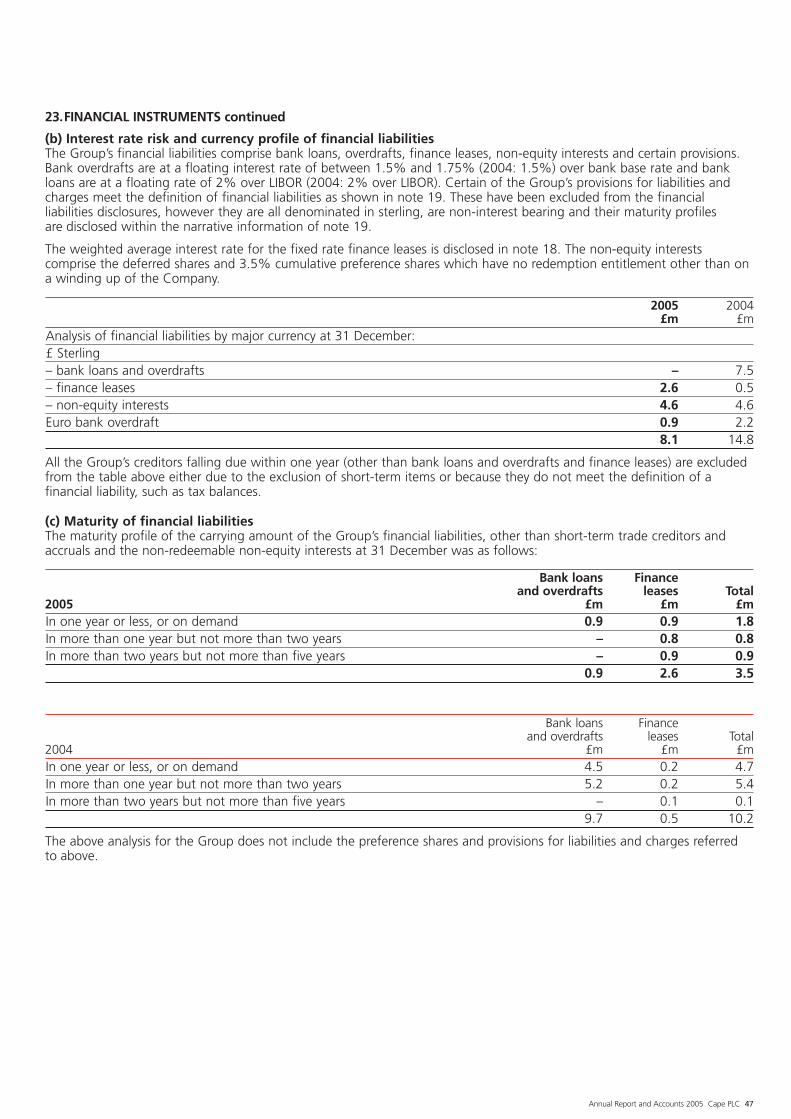

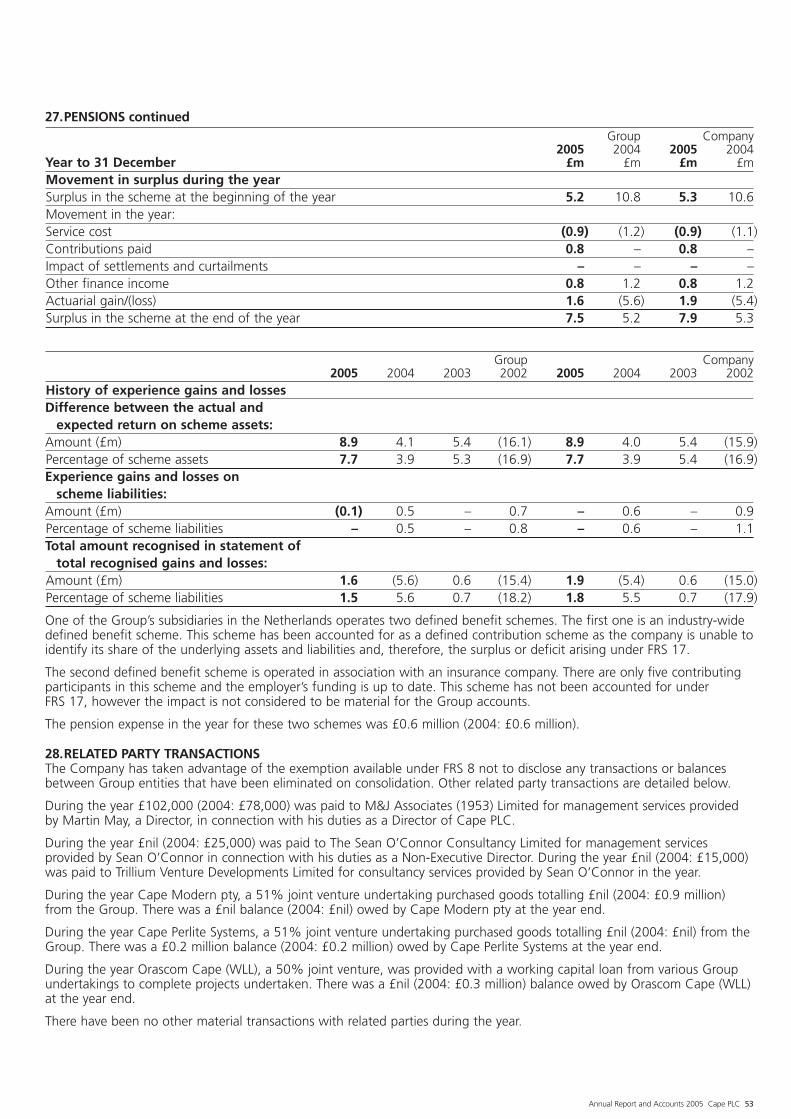

64

ANNUAL REPORT AND ACCOUNTS 2005

ANNUAL REPORT AND ACCOUNTS 2005

Cape PLCCape House3 Red Hall AvenueParagon Business VillageWakefieldWest YorkshireWF1 2UL

AN

NU

AL R

EPO

RT A

ND

AC

CO

UN

TS 2

005

162311 Cape Cover_spine 16/5/06 10:54 Page 1

£261.8mTURNOVER UP 9.6% (2004: £238.9m)

£14.9mCAPE INDUSTRIAL SERVICES OPERATING PROFIT UP 30.7%(2004: £11.4m)

£8.2mGROUP OPERATING PROFIT BEFORE OPERATINGEXCEPTIONAL ITEMS UP 41.4% (2004: £5.8m)

£9.7mOPERATING EXCEPTIONAL EXPENDITURE RELATINGTO PROPOSED SCHEME OF ARRANGEMENT (2004: £1.1m)

£1.3mTOTAL OPERATING LOSS (2004: PROFIT £5.1m)

£23.7mYEAR END NET FUNDS (2004: DEBT £2.4m)

Contents2 Cape Industrial Services

– Overview6 Chairman’s statement and review12 Health, safety and the

environment19 Directors’ report23 Independent auditors’ report24 Consolidated profit and loss

account25 Consolidated and Company

balance sheets26 Consolidated cash flow statement26 Reconciliation of net cash flow to

movement in net funds/(debt)27 Consolidated statement of total

recognised gains and losses Note of consolidated historicalcost profit and losses Reconciliation of movements inshareholders’ funds

28 Accounting policies30 Notes to the financial statements54 Five year financial summary56 Principal subsidiary undertakings

Directors, officers and advisers58 Notice of Annual General

Meeting

0504030201

8.25.83.54.4(1.1)

0504030201

262239228192217

TURNOVER £m OPERATING PROFIT BEFORE EXCEPTIONAL ITEMS £m Designed and produced by Rare Corporate Design, London. www.rarecorporate.co.uk

162311 Cape Cover_spine 16/5/06 10:54 Page 2

Annual Report and Accounts 2005 Cape PLC 1

FOUNDED IN 1893, CAPE PLC ISTHE PARENT COMPANY OF ANUMBER OF SERVICE PROVIDINGORGANISATIONS OPERATINGPRIMARILY IN THE OIL AND GAS,PETROCHEMICAL AND POWERGENERATION INDUSTRIES.THE COMPANY IS BASED IN THEUK AND OPERATES IN 23 COUNTRIESWORLDWIDE.

United KingdomAustraliaAzerbaijanBahrainBelgiumBruneiEgyptGermanyHollandIndonesiaIrelandKazakhstanMalaysiaMaltaNew CaledoniaOmanPhilippinesQatarRussiaSaudi ArabiaSingaporeThailandUnited Arab Emirates

162311 Cape front end 16/5/06 10:55 Page 1

2 Cape PLC Annual Report and Accounts 2005

COMPANYPROVIDING ESSENTIAL SERVICESCAPE INDUSTRIAL SERVICES IS A MARKET LEADER IN THEPROVISION OF INDUSTRIAL SERVICES WHERE THE REQUIREMENTFOR QUALITY, RELIABILITY AND SAFETY IS PARAMOUNT.

The lining of boilers, furnaces,kilns and high temperaturepetrochemical reactors withmaterials to withstandtemperatures in excess of 1,000ºC.

This activity also incorporates thebusiness of RB Hilton, and offersdesign, supply and installationservices.

The provision of a comprehensiverange of cleaning services toindustry in a broad variety ofindustrial environments carriedout in a safe and controlled way.

Cleaning services are provided asplanned programmes carried outon a fixed price, schedule of ratesor daywork basis. Cape can providean emergency response capabilityand adapt the range of disciplinesto meet clients’ particular needs.

The supply and erection ofscaffolding to enable site operatorsand other contractors to haveaccess to all parts of an industrialplant. This can be for routinemaintenance, shutdowns, newconstruction or other majorprojects. Computer aided designis used where appropriate.

The provision of thermal andacoustic insulation for industrialapplications. Thermal insulationis provided for temperaturemaintenance, personnel protection,heat conservation and efficientcryogenic insulation attemperatures down to –160ºC.

An additional service is thecalculation of heat loss andprovision of infrared equipmentfor evaluating thermal insulationefficiency.

TYPICAL PROJECTS+ new construction+ plant maintenance+ plant shutdowns+ plant upgrades

+ new construction+ plant maintenance+ plant shutdowns+ plant upgrades

+ plant maintenance+ plant shutdowns

+ new construction+ plant maintenance+ plant shutdowns+ plant upgrades

MARKETS+ power generation + offshore oil and gas + refineries + LNG terminals + petrochemicals + pharmaceuticals + process industries + food and beverages + ship repair/module yards

+ power generation + offshore oil and gas + refineries + petrochemicals + process industries

+ power generation + offshore oil and gas + refineries + petrochemicals + process industries

+ power generation + refineries + LNG terminals + petrochemicals + process industries + smelting/metal processing

SCAFFOLDING INSULATION INDUSTRIALCLEANING

REFRACTORYLININGS

162311 Cape front end 16/5/06 10:56 Page 2

Annual Report and Accounts 2005 Cape PLC 3

T

Through its Hire & Sales Division,Cape supplies scaffolding, accessand non-mechanical plant on a hireor sales basis to clients in theconstruction and engineeringindustries and to organisers ofspecific entertainment events.

As well as traditional tube, fittingsand boards, Cape Hire offerssystem scaffolding, temporaryfencing and hoarding, alloy towersand a full range of metal andtimber plant.

In response to client needs, therange of industrial services includestrace heating, asbestos management,security, training and facilitiesmanagement. For offshoreinstallations, services include lifting,crane operation, abseiling, cateringand logistics. In addition, inspectionservices are provided identifyingcorrosion, the efficiency of thermalinsulation and refractory liningsand the survey and removal ofhazardous materials.

The application of passive fireprotection to a variety of structuresin environments ranging from theextreme weather conditions in theNorth Sea to onshore petrochemicaland other installations with highexposure to fire risk.

The provision of a range of coatingsfor a variety of structures includingpetrochemical plants, refineries andoffshore installations. This providessurface protection and theprevention of corrosion on baresurfaces or those to be insulatedor clad.

+ new construction+ plant maintenance+ plant shutdowns+ plant upgrades

+ new construction+ plant maintenance+ plant shutdowns+ plant upgrades

+ new construction+ plant shutdowns+ plant upgrades+ entertainment events

+ new construction + plant maintenance + plant shutdowns + plant upgrades

+ power generation + offshore oil and gas + refineries + LNG terminals + petrochemicals + pharmaceuticals + process industries + food and beverages + ship repair/module yards

+ power generation + offshore oil and gas + refineries + LNG terminals + petrochemicals + ship repair/module yards + construction industry

+ civil engineering + industrial sites+ commercial building sites + entertainment venues

+ offshore oil and gas + refineries + LNG terminals + petrochemicals + ship repair/module yards

SPECIALISTCOATINGS

FIRE PROTECTION HIRE & SALES ASSOCIATEDSERVICES

Cape Industrial Services (‘CIS’) aims to provide best valuesolutions, tailored to meet the needs of its clients, supplyingthem individually or as a seamlessly integrated multi-disciplinarypackage. The Group’s commitment is to its clients, workingcontinuously to improve delivery through its structuredapproach to the management of safety, quality and costs.

Whilst being proud of its international reputation, CIS is able to deliver its services locally through its network of offices anddepots in the UK and in Holland, Belgium and Germanythrough its Cleton division. Its other international activities aremainly incorporated in Cape East which, through its overseassubsidiaries and branches, provides the local knowledge andpresence required to respond effectively to its clients’ needs.

The Group now employs a total of approximately 7,700 peopleoperating in 23 countries across the world.

162311 Cape front end 16/5/06 10:56 Page 3

UK HOLLAND

4 Cape PLC Annual Report and Accounts 2005

GLOBALREACHCAPE’S TECHNICAL EXPERTISE GIVES IT A STRONGPOSITION IN EACH OF THE INTERNATIONAL MARKETS ITSERVES. IT OPERATES PRIMARILY IN THE OIL AND GAS,PETROCHEMICAL AND POWER GENERATION INDUSTRIES.

Refinery Maintenance(2003 – to date)Cleton consolidated its leadingpresence in Holland’s Europort withannual maintenance services at theShell, Nerefco (BP) and KuwaitPetroleum oil refineries.

EDF(2006 – 2011)CIS is the sole supplier to EDF ofaccess and insulation services forboth the West Burton and CottamPower Stations.

Alcan Smelting & Power(2006 – 2011)CIS has been awarded a new long-term multi-discipline maintenancecontract as sole provider of access,insulation and facilities cleaningservices at the Alcan smelting andpower facility in Northumberland.

British Energy(2005 – 2010)CIS provides a full range of access andmaintenance services to British Energyon five of its nine power stations.

BNG Sellafield(2005 – 2010)CIS provides site wide accessservices including scaffolding,rope and powered access as solesupplier on BNG’s nuclearprocessing facility at Sellafield.

BP PLC(2006 – 2009)CIS provides platform and fabricmaintenance services (whichincludes the disciplines of scaffolding,painting and insulation) on anumber of BP’s onshore sites andoffshore platforms.

Heerema Hartlepool(2004 – to date)CIS provides access and paintingservices on the Buzzard UtilitiesPlatform under constructionat Heerema’s Hartlepool yard.The continued success of thisproject has seen the award of asimilar contract on the BritSatellite module beingconstructed concurrently.

Huntsman Petrochemicals Ltd(2005 – 2009)CIS provides integratedmaintenance services includingaccess, insulation, painting,cleaning and grounds maintenanceservices across all Huntsman assetsin the Teesside region.

SOME OF OUR CLIENTS

162311 Cape front end 16/5/06 10:56 Page 4

RUSSIA BAHRAIN / UAE SAUDI ARABIA AUSTRALIA/PHILIPPINES

Annual Report and Accounts 2005 Cape PLC 5

Safco(2005 – to date)RB Hilton Saudi Arabia has beenawarded two contracts totallingUS$10.40 million for the provisionof thermal insulation andscaffolding services, forming partof the Saudi Arabia FertiliserCompany’s upgrade and extensionat their plant in Jubail.

Aramco Berri Gas Plant(2005 – to date)RB Hilton Saudi Arabia hasbeen awarded a US$5.10 millionrefractory and scaffolding servicescontract on the Aramco BerriGas Plant.

Bayu Undan offshoredevelopment(2003 – to date)Cape East Philippines has beenawarded a multi-disciplinemaintenance contract by AmecClough on the Bayu Undandevelopment offshoreAustralia/Timor.

Inco Goro Nickel Project(2006 – 2008)Cape Industrial Services Pty Ltd hasbeen awarded a US$17.5 millionaccess contract in relation theUS$1.8 billion Inco Goro NickelProject located in New Caledonia,a French overseas territorialcommunity. The contract willrequire Cape Industrial Servicesover an 18 month period tomanage and construct over 2,000tonnes of scaffold with a site teampeaking at 300 personnel.

Bahrain Petroleum Company(2006 – to date)RB Hilton has been awarded aUS$2.8 million thermal insulationand scaffolding services contracton the Bapco Low Sulphur DieselProduction Project.

Gasco(2005 – 2010)Cape East LLC has been awardedthe renewal of a five year multi-discipline maintenance contractwith Gasco (a joint venturebetween the Abu Dhabi NationalOil Company, Shell, Total andPartex). The contract is to carry outinsulation, painting and scaffoldingservices on Gasco’s LNG plants atAsab, Bu Hasa and Ruwais in theUnited Arab Emirates.

Sakhalin 2 LNG Project(2004 – to date)CIS is supporting the onshorefield works and offshore supply ofmaterials and equipment, providingcommon user scaffolding,insulation, fire protection andrefractory services on the Sakhalin 2LNG Project for CTSD, a jointventure between the Chiyoda andToyo Engineering Corporationsfrom Japan.

Client list includes:Abu Dhabi Gas IndustriesAlbaAlcanAmec CloughAramcoBapcoBechtelBG Group

BPBritish EnergyBritish Nuclear GroupConsolidated ContractorsCompany InternationalChevron TexacoChiyodaConoco Phillips

EDFEntreposeExxon Mobil (Esso)Foster WheelerHeeremaHuntsmanKellogg JGCInco Management

Malta ShipyardsMitsui BabcockNerefcoQatar PetroleumQatargas LNGParsons Fluor DanielPetronasPX

SabicSafcoShellTechnipToyo Engineering

Main officesworldwide(from left to right):BelfastWarringtonAberdeenBillinghamWakefieldDoncasterElshamSt AlbansVlaardingen (Netherlands)Valetta (Malta)Jubail (Saudi Arabia)Sitra (Bahrain)Doha (Qatar)Abu DhabiSingaporeManilaYuzhno-Sakhalinsk(Sakhalin)

162311 Cape front end 16/5/06 10:57 Page 5

6 Cape PLC Annual Report and Accounts 2005

I am pleased to report that Cape Industrial Services (‘CIS’)has had another excellent year in which it has deliveredstrong organic growth in its core markets in the UK and the Middle East and has successfully maintained its marketshare elsewhere.

CIS, which specialises in the provision of scaffolding,insulation, fire protection and other essential servicesto the energy sector, performed significantly ahead offorecast. Turnover, including its share of joint ventures,at £261.8 million, rose by 9.6% (2004: £238.9 million).

The total operating loss, including the Group’s share of jointventures, of £1.3 million (2004: profit £5.1 million) is aftertaking into account the operating exceptional item of£9.7 million (2004: £1.1 million) relating to the costsof the proposed scheme of arrangement (‘Scheme’).

I am also delighted to be able to announce significantprogress with the proposed Scheme as well as a numberof new contracts, contract renewals, extensions and awardsthat have been achieved in 2005 and the early part of 2006.

CIS has now delivered growth in turnover and underlyingprofitability consistently for the last four years. These resultsdemonstrate CIS’s position as one of the leading internationalproviders of essential support services to the energy sector.

CHAIRMAN’SSTATEMENT AND REVIEW

CIS HAS NOWDELIVERED GROWTHIN TURNOVER ANDUNDERLYINGPROFITABILITY

CONSISTENTLY FORTHE LAST FOUR YEARS.

0504030201

8.25.83.54.4(1.1)

OPERATING PROFIT BEFORE EXCEPTIONAL ITEMS £m

162311 Cape front end 16/5/06 10:57 Page 6

Annual Report and Accounts 2005 Cape PLC 7

Financial summaryTurnover for the year, including the Group’s share of jointventures, was £261.8 million (2004: £238.9 million), anincrease of 9.6%. Of the £22.9 million increase, £14.1 millionwas generated in the UK and £8.8 million in the rest ofthe world.

On this strong, organic growth in turnover, CIS has made an operating profit, including its share of joint ventures,of £14.9 million, up 30.7% from £11.4 million and increasedits return on net operating assets to 29.2% (2004: 23.9%).

Group operating profit before operating exceptional items was£8.2 million (2004: £5.8 million) an increase of 41.4%.However, the costs of the proposed Scheme of £9.7 million,have resulted in a total operating loss for the year, includingthe Group’s share of joint ventures, of £1.3 million (2004:profit £5.1 million). Further details of the Scheme are set outbelow. On the assumption that the Scheme Creditors vote infavour of the establishment of the Scheme and that the Courtsanctions the Scheme before 30 June 2006, the Directors donot anticipate that there will be any further exceptional costsrelating to the Scheme.

The net charge to the profit and loss account for industrialdisease claims was £4.6 million (2004: £3.7 million).

The Group continues to generate cash and, despite industrialdisease costs and costs associated with the Scheme, closedthe year with a net cash inflow from operating activities of£7.3 million (2004: £10.7 million). Further investment ingrowth in the business resulted in a net cash outflow beforefinancing of £2.2 million (2004: inflow £3.6 million). Thisresulted, after financing, including the proceeds of the shareissue and repayment of borrowings, in a £22.4 million netinflow (2004: outflow of £1.5 million). The Group endedthe year with net funds of £23.7 million (2004: net debt£2.4 million).

THESE RESULTSDEMONSTRATE CIS’SPOSITION AS ONE OF THELEADING INTERNATIONALPROVIDERS OF ESSENTIALSUPPORT SERVICES TOTHE ENERGY SECTOR.

£14.9mCAPE INDUSTRIAL SERVICES OPERATINGPROFIT UP 30.7% 2004: £11.4m

£261.8mTURNOVER UP 9.6%2004: £238.9m

Although the exceptional charge resulted in basic earningsper share (‘EPS’) of 0.2 pence (2004: 10.7 pence), beforeexceptional items the adjusted basic EPS was 9.8 pence (2004:11.2 pence). The issue of shares to part fund the Scheme hasaffected the EPS in 2005. For comparison, the adjusted basicEPS for 2004, restated using 2005’s weighted average numberof shares, would have been 8.9 pence.

In last year’s statement, I said that the Group would announcedetailed proposals for the long-term financing of the Group’sasbestos-related claims in the UK. On 16 June 2005, Capeannounced a proposed scheme of arrangement to provide forthe long term financing of a great majority of all future UKasbestos-related claims likely to be successfully made againstthe Company and those of its subsidiaries included in theScheme. On 11 July 2005, the Company’s shareholdersapproved the Scheme and on 15 July 2005 the Companycompleted the issue of 29,090,910 new ordinary shares toraise approximately £32 million before expenses to part fundthe Scheme. The balance of the initial Scheme funding isbeing provided by a new £15 million bank facility with theremainder coming from the Group’s own resources.

The full, formal Scheme documents together with votingforms and a letter from the Forum of Asbestos VictimsSupport Groups have been sent out convening creditors’meetings on 16 May 2006. More details on progress with theScheme are given below.

Largely as a result of the £32 million fundraising in July 2005,shareholders’ funds increased from £30.9 million to£64.9 million.

A dividend is not being proposed (2004: £nil).

162311 Cape front end 16/5/06 10:57 Page 7

8 Cape PLC Annual Report and Accounts 2005

Business highlights 2005 has been another successful year in terms of winningnew contracts, contract extensions, contract renewals andsafety awards with CIS continuing to grow both the rangeof services and international spread of its operations to bothnew and existing clients.

Notable contract successes in 2005 included:

• a new five year contract with CNR International (UK) Limitedfor maintenance work on four of its platforms in the NorthSea. The contract has an estimated annual value of morethan £3 million;

• a new three year contract (with the option to renewannually thereafter up to a total of five years) with BritishNuclear Group (‘BNG’) under which CIS will provide sitewide access services as sole supplier on BNG’s nuclearprocessing facility at Sellafield. The contract has an estimatedannual value of £6 million;

• the renewal of CIS’s contract with British Energy to performmaintenance work on five of British Energy’s nine powerstations for an initial period of three years with the option to renew for a further two years. This contract has anestimated annual value of in excess of £6 million;

• a new £8 million per annum contract with Huntsman for thedelivery of multi-disciplinary services on their North Easternpetrochemicals sites. The contract is for an initial three yearperiod with a further two year renewal option;

• the renewal of CIS’s contract with BP to provide the fullrange of platform and fabric maintenance services on anumber of BP’s offshore and onshore locations. Thecontract, which commenced in 1 January 2006, will befor an initial three year term with the option to renew forthree further two year periods, potentially therefore for upto nine years. The contract has an estimated annual value ofin excess of £20 million;

• receiving approval from the Saudi Arabian national oilcompany, Aramco, for RB Hilton Limited, CIS’s operatingsubsidiary in Saudi Arabia, to provide scaffolding workson its facilities throughout the Kingdom. RB Hilton’spre-qualified status led directly to the award of a newscaffolding contract on Aramco’s Riyadh refinery – a part ofthe Aramco business for which RB Hilton had not previouslyworked; and

• the renewal of a five year multi-discipline maintenancecontract with Gasco (a joint venture between the Abu DhabiNational Oil Company, Shell, Total and Partex). The contractis to carry out insulation, painting and scaffolding serviceson Gasco’s LNG plants at Asab, Bu Hasa and Ruwais in theUnited Arab Emirates. This contract maintains CIS’scontinuous association with Gasco which goes back to 1980when CIS was involved in the construction of the Bu Hasaand Ruwais plants.

CHAIRMAN’S STATEMENT AND REVIEW CONT

£9.7mOPERATING EXCEPTIONAL EXPENDITURE RELATING TOPROPOSED SCHEME OF ARRANGEMENT 2004: £1.1m

£8.2mGROUP OPERATING PROFIT BEFORE OPERATINGEXCEPTIONAL ITEMS UP 41.4% 2004: £5.8m

162311 Cape front end 16/5/06 10:57 Page 8

Annual Report and Accounts 2005 Cape PLC 9

We are also pleased to be able to announce the followingsignificant contract awards in early 2006:

• a new £7.5 million contract to provide access and industrialcleaning services for the next five years at the Alcan smeltingand power facility in Northumberland;

• an £8 million contract renewal with EDF as sole provider ofaccess and insulation services for the next five years at theWest Burton and Cottam power stations;

• the renewal of a three year multi-discipline contract with BPto provide access, insulation and coatings at the Sullom VoeTerminal in Shetland. The contract has an estimated annualvalue of c. £5 million;

• two contracts in Saudi Arabia with a total value ofc. US$10.4 million with the Saudi Arabia Fertiliser Company(‘Safco’) for the provision of thermal insulation andscaffolding services on Safco’s upgrade and extensionof their plant in Jubail; and

• a US$17.5 million access services contract on the Inco GoroNickel Project. This US$1.8 billion nickel-cobalt project,which will be one of the largest projects of its kind in theworld, is located in New Caledonia, a French overseasterritorial community in the Coral Sea, west of Australia.The contract, which is expected to last for c.18 months,will require CIS to manage and construct over 2,000 tonnesof scaffolding with a site team peaking at 300 personnel.

We are delighted to be working so closely with these andmany other blue-chip companies.

Key to the Group’s success is its safety proposition: CIScontinues to place the highest emphasis on health and safety.Another highlight of 2005 was the award of the British SafetyCouncil Five Star Award. CIS has now held this awardcontinuously since 2002. Subsequently, and in competitionwith other recipients of Five Star Awards in the sector, CISwon the British Safety Council’s prestigious Sword of Honour.The Sword of Honour is one of only 40 awarded worldwideby the British Safety Council and recognises organisations thathave implemented safety systems that are among the best inthe world. This is the second time that CIS has won the BritishSafety Council’s Sword of Honour, the last time being in 2003.

This was followed by the presentation in February 2006of the winner’s trophy in British Energy’s inaugural Supplierof the Year of Award. Nominations for the award, whichwas presented by the Chairman of British Energy,Sir Adrian Montague, were judged against a range ofmeasures including safety, quality of performance,capability and responsiveness.

StrategyOver the past six months, the Board together with the keymanagement group, which includes its regional operationsdirectors, has carried out a review of the Group’s strategy.The core principles which underpin the strategy remainunchanged. They are:

• to become the recognised expert and leader in each of ourchosen markets;

• to reinforce, develop and build upon existing relationshipswith clients and to secure new blue-chip clients;

£1.3mTOTAL OPERATING LOSS 2004: PROFIT £5.1m

CIS CONTINUES TO PLACETHE HIGHEST EMPHASISON HEALTH AND SAFETY.ANOTHER HIGHLIGHT OF2005 WAS THE AWARDOF THE BRITISH SAFETYCOUNCIL’S SWORD OFHONOUR.

162311 Cape front end 16/5/06 10:57 Page 9

10 Cape PLC Annual Report and Accounts 2005

CHAIRMAN’S STATEMENT AND REVIEW CONT

• to increase leverage from our safety proposition andcontinue to set challenging safety standards across all areasof the business;

• to extend the service offering to all clients and broaden therange of services offered; and

• to build value for shareholders through improving our returnon managed assets.

As a result of the review it has been agreed that the Groupwill:

• accelerate investment in, and the development of, long-termalliances and partnerships;

• improve the Group’s international perspective through theestablishment of a regional HQ in the Middle East; and

• establish an Operating Board with HR development, andstrategic planning and marketing responsibilities.

Scheme of Arrangement Since the fundraising in July 2005, Cape has been continuingdiscussions with interested parties including claimants,asbestos victims support groups and their representatives.The reasons for these discussions have been:

• to give sufficient time and information to interested partiesto examine and understand the proposal in detail and forthem to make recommendations; and

• to give comfort to interested parties, and in particularclaimants’ lawyers, that the proposals are in the interests ofclaimants and future claimants and that the commercial andlegal arrangements underpinning the Scheme are justifiableand robust.

As a result:

• as announced on 17 January 2006, Cape has funded anindependent legal review of the Scheme by solicitors andcounsel (including a leading national asbestos claimant firmof solicitors, Thompsons); and

• as also announced on 17 January 2006, Cape has funded anindependent financial review of the Scheme by accountantsKPMG.

The legal and financial reviews have raised a number of issueson the proposed Scheme as a result of which Cape hasagreed to make a number of amendments. None of the issuesraised is considered by the Directors to be fundamental to theworking of the Scheme or to the benefits which it is intendedto deliver.

On 17 January 2006, Cape also announced that discussionswere continuing with its bank regarding an extension of itsloan facilities pursuant to which some of the initial Schemefunding of £40 million is to be provided. These discussionshave now been concluded and a further extension to thefacilities agreed. It is a condition to Cape’s draw down of the£15 million loan facility that the Scheme becomes effectiveby no later than 30 June 2006.

On 28 February 2006 Cape made an application to the HighCourt to seek an order to convene meetings of the Schemecreditors – in other words to authorise meetings at whichclaimants will be able to vote on the Scheme. On 8 March2006, Mr Justice David Richards made an order authorisingCape to convene the meetings. The full, formal schemedocuments together with voting forms and a letter from theForum of Asbestos Victims Support Groups have been sentout convening creditors’ meetings on 16 May 2006.

£64.2mSHAREHOLDERS’ FUNDS2004: £30.9m

£23.7mYEAR END NET FUNDS2004: DEBT £2.4m

162311 Cape front end 16/5/06 10:57 Page 10

Annual Report and Accounts 2005 Cape PLC 11

The Scheme also requires Cape’s shareholders to have passeda resolution approving a number of the amendments to theScheme. At an extraordinary general meeting on 12 April2006 Cape’s shareholders voted unanimously in favour of theproposed amendments.

A summary of the independent actuarial estimate of the rangeof potential UK asbestos-related liabilities assessed as part ofthe proposed Scheme is set out in note 26(i). Although thenet charge to the profit and loss account for industrial diseaseclaims was £4.6 million (2004: £3.7 million), should theScheme not be approved, given the outlook for the Groupand assuming that future settlements broadly follow recenthistory, the Directors remain confident that future claims, tothe extent not matched by insurance recoveries, can be metfrom operating cash flows.

Our peopleI am sorry to report that following the serious accident inwhich he was involved on 31 October 2005, the Group’sManaging Director, Paul Ainley, has been making a slowrecovery and the prognosis remains uncertain. His absence iskeenly felt and we all hope very much that he will make a fullrecovery over time. We wish Paul and his family the very bestfor the future.

Since November, Mike Reynolds has been combining hisduties as Finance Director with those of Acting ManagingDirector. The Board acknowledges the considerableadditional workload that this involves and, on their behalf,I would like to express our appreciation of his efforts overthe past few months.

Against this background, the Board has begun the task ofrecruiting a Chief Executive Officer. Whilst the results of thesearch so far have been encouraging, and a number ofexceptional candidates have been identified, it is not possible,at this stage, to say when an appointment will be made.

The Board recognises that the Group’s success depends heavilyon the quality of its people. None of our contract wins orsafety awards would have been achieved without their dailyfocus on the Group’s strategic objectives. On behalf of theBoard, I would like to thank the Group’s management, staffand employees at all levels worldwide for their hard work andcommitment throughout 2005.

OutlookSales in the second half of 2005 continued to grow both inthe UK and overseas. In January and February, sales have alsobeen ahead of budget. The order book in the UK is lookinghealthy and the number and quality of opportunities in theMiddle East is particularly encouraging. The Group remainswell placed to benefit from these and other new opportunities.

With energy prices remaining at high levels and a marketlooking to ensure continuity of supply from a number ofsources, the Directors view the Group’s prospects over theshort and medium term with confidence.

Martin K MayChairman20 April 2006

ON BEHALF OF THE BOARD,I WOULD LIKE TO THANKTHE GROUP’S MANAGEMENT,STAFF AND EMPLOYEES ATALL LEVELS WORLDWIDEFOR THEIR HARD WORKAND COMMITMENTTHROUGHOUT 2005.

162311 Cape front end 16/5/06 10:57 Page 11

TECHNOLOGCIS PRIDES ITSELF ON USINGINDUSTRY LEADING TECHNOLOGYAND TECHNIQUES.

12 Cape PLC Annual Report and Accounts 2005

ELECTRONICIMAGETRANSFER

Design offices areequipped with computeraided design (CAD)facilities and areelectronicallyinterconnected toensure the high speedtransmission of schemesand documentationbetween CIS’s offices andfrom CIS to its clients.

SCAFFOLDDESIGN

We employ qualified andexperienced scaffoldengineers who usecomputer modellingsoftware to design alltypes of ‘special’ steeland aluminium scaffoldstructures. In addition,comprehensive technicaladvice is provided on allaspects of scaffoldstructure, componentsand alternative means ofaccess to satisfy therequirements of both CISand the client.

162311 Cape front end 16/5/06 10:57 Page 12

YFIREMATS

CIS has developed aremovable insulated jacketsystem, particularly suitedfor the petrochemicalindustry that canwithstand the extremeconditions of anexplosion, followed by ajet fire and then providinga 2 hour hydrocarbonrating. The system holdsLloyds certification.

Annual Report and Accounts 2005 Cape PLC 13

UV CURED GRPCLADDING

CIS embraces thechallenge to findinnovative ways toinsulate onerous typesof plant and in onesuch development haspioneered the use ofglass reinforced plasticcladding cured by ultraviolet light.

THERMALIMAGING

To demonstrate theeffectiveness of thermalinsulation systems, CISuses thermal imagingequipment to identifylevels of heat loss. Areasof insulation breakdownand areas requiringupgrade are highlightedin a visual display andcomprehensive report.

162311 Cape front end 16/5/06 10:57 Page 13

14 Cape PLC Annual Report and Accounts 2005

TRAININGCIS DELIVERS INTERNATIONALLYACCREDITED TRAINING.

TRAINING TOTHE INDUSTRY

Not only do our trainingcentres and coursessupport our own workforce,they are also being usedto provide extensivetraining to clients andother industry bodies.

ACCREDITEDTRAINING

A number of the trainingcourses available arecertified by internationallyaccepted authorities suchas CITB, IOSH, PASMAand ACAD.

DIVERSITY OFTRAINING

As Cape continues todiversify its disciplines andskills to meet its client’sneeds, the portfolio oftraining courses continuesto expand to meet thesedemands. Current trainingcourses and contactdetails can be foundvia our websitehttp://www.cisgl.com/capetraining.htm.

162311 Cape front end 16/5/06 10:59 Page 14

Annual Report and Accounts 2005 Cape PLC 15

ASBESTOSREMOVAL ANDAWARENESS

CIS has developed a rangeof asbestos removal andawareness courses thatmeet the stringentrequirements of theHealth & Safety Executivewhich are open tooperatives, managers,clients and otherinterested parties.

TRAININGCENTRES

CIS has establishedtraining centres across theUK, Middle East and FarEast to continue to raiseskill levels and competenciesof its entire workforcethroughout the world.

162311 Cape front end 16/5/06 10:59 Page 15

CENTRALTECHNICALSERVICES

The Central TechnicalServices Departmentprovides the catalyst forcontinuous improvementthroughout the organisation.It controls the IntegratedManagement System andfacilitates information flowfor all health, safety andenvironmental issues.

CLIENTRELATIONSHIPS

CIS is strongly focused onmaintaining and developingexcellent relationships withour clients and we are proudto have been working witha number of clients for over25 years. Due to the diversenature of contracts awarded,CIS has developed a varietyof systems to providesynergy with whicheverexisting or new approachis required.

TEAMWORKCIS BELIEVES IN THE VALUE OF GOODTEAMWORK AT ALL LEVELS.

WORKFORCE

An organisation is onlyas good as the peoplewho work for it. CISencourages theparticipation of allemployees in thedevelopment of goodworking practice.

16 Cape PLC Annual Report and Accounts 2005

162311 Cape front end 16/5/06 11:00 Page 16

WORKING GROUPS

CIS representatives sit on anumber of committees andworking groups created byvarious enforcementagencies and as a result isable to have input into andinstigate the latest industryrecommendationsand standards.

INTERNATIONALTEAM

The Cape Group is aninternational organisationcurrently operating inover 20 countries. Ournetwork of offices aroundthe world provides theopportunity to shareexpertise, developmarkets and source themost skilled workforce ona global scale.

INDUSTRY BODIES

Involvement with industrybodies and tradeassociations such as NASC,OCA, FESI, TICA and ACADprovides CIS with the abilityto pinpoint industrydevelopments at an earlystage and ensure that ourideas and points of view arediscussed.

Annual Report and Accounts 2005 Cape PLC 17

162311 Cape front end 16/5/06 11:01 Page 17

18 Cape PLC Annual Report and Accounts 2005

CIS’s Health and Safety Policy was originally developed in theUK to define its obligations to employees and others who maybe affected by its operations and to form the basis of theGroup’s integrated approach health and safety. CIS is keen totake the best health and safety practices from its operationsaround the world and, where appropriate, to replicate themthroughout its business. As a result, a ‘Global Safety Policy’has been produced to better serve the needs of a trulyinternational business.

In 2005:

• CIS successfully piloted an enhanced health surveillanceprogramme in the UK as part of which experiencedoccupational health nurses travel to individual site locationsin mobile surgeries. This arrangement when rolled outnationally will facilitate cost effective and efficient accessto medical examinations together with minimum disruptionto worksite operations.

• CIS instigated a system for the rehabilitation of UKemployees who have been injured by an accident at work,the overall objective being that of accelerating the injuredparty’s recovery and return to work.

As the Group has diversified and its workload has expanded,the demand for skilled workers has increased. Therefore, tomeet current and future demands, great emphasis is placedon training. CIS has established training centres in the UK, theMiddle East and the Far East, to raise the skill levels andcompetencies of the indigenous work forces. Each centrecontinues to expand its range of courses to meet continuallyincreasing requirements. The training centres provide bothinternal bespoke courses and training certified byinternationally accepted authorities such as CITB, IOSH,PASMA and ACAD for employees, clients and other industrybodies.

With these initiatives and the achievement of a combinedaccident frequency rate (AFR) of 0.07 (per 100,000 man-hours), CIS has sustained its commitment to improving itssafety culture and driving down the number of accidents,with the involvement of staff at all levels of the organisation.

One of the highlights of 2005 was the award of the BritishSafety Council Five Star Award. CIS has now held this awardcontinuously since 2002. Subsequently, and in competitionwith other recipients of Five Star Awards in the sector, CISwon the British Safety Council’s prestigious Sword of Honour.The Sword of Honour is one of only 40 awarded worldwideby the British Safety Council and recognises organisations thathave implemented safety systems that are among the best inthe world. This is the second time that CIS has won the BritishSafety Council’s Sword of Honour, the last time being in 2003.

During 2005, the ISO 14001 environmental standard wasraised to a new level of specification. CIS is pleased to notethat the environmental systems in place were of sufficientcalibre for upgrading to the new specification to be achievedwith no significant issues raised. In addition, furthercertification was gained during the year with the successfulISO 14001 implementation and accreditation of the Qatarbusiness unit.

HEALTH, SAFETY AND THE ENVIRONMENT

CIS IS KEEN TO TAKETHE BEST HEALTH ANDSAFETY PRACTICESFROM ITS OPERATIONSAROUND THE WORLDAND, WHEREAPPROPRIATE, TOREPLICATE THEMTHROUGHOUT ITSBUSINESS.

162311 Cape front end 16/5/06 11:01 Page 18

Annual Report and Accounts 2005 Cape PLC 19

The Directors have pleasure in submitting their report andaudited financial statements of the Group and the Companyfor the year ended 31 December 2005.

PRINCIPAL ACTIVITIESThe Company and its subsidiaries form an international groupprimarily engaged in the supply of a wide range of servicesincluding industrial scaffolding, thermal and acousticinsulation, fire protection, painting, asbestos removal, andrelated services to major industrial groups, principally in theenergy sector. The Company’s subsidiary undertakings arelisted on pages 56 and 57.

REVIEW OF BUSINESS AND FUTURE DEVELOPMENTSA review of the Group’s activities during the year, its strategyand outlook for 2006 is contained in the Chairman’sstatement on pages 6 to 11.

RESULTSThe financial results for the year ended 31 December 2005 areset out in the financial statements on pages 24 to 53. Thetotal operating loss for the year is £1.3 million (2004: a profitof £5.1 million). The loss on ordinary activities before tax is£0.9 million (2004: profit of £5.8 million).

DIVIDENDSNo interim dividend was paid for the year ended 31 December2005 (2004: nil pence). The Directors are unable torecommend the payment of a final dividend for the yearended 31 December 2005 (2004: nil pence).

FIXED ASSETSDetails of the movements in tangible fixed assets are given innote 11(b) to the accounts on page 37.

DONATIONSDuring the year the Group made charitable donations of£11,845 (2004: £21,100) towards various local and nationalcauses. There were no political donations (2004: £nil).

SHARE LISTINGThe Company’s ordinary shares are admitted to and traded onAIM, a market operated by the London Stock Exchange.

INTERNATIONAL FINANCIAL REPORTING STANDARDSThe Group is not required to adopt International FinancialReporting Standards (‘IFRS’) until the year ending31 December 2007.

INCREASE IN SHARE CAPITALThe Company’s authorised and issued share capital increasedduring year through a placing of 29,090,910 ordinary shares.Further details are provided in note 20 to the accounts onpage 42.

DIRECTORSThe Directors at the date of this report and their biographicaldetails are as follows:

Martin May (52)Appointed a Director of the Company in 2002 and becameChairman in 2003. He is also Chairman of Volex Group PLCand a number of private companies, a Fellow of the Instituteof Chartered Management Accountants and a foundermember and Fellow of the Society of Turnaround Practitioners.

Paul Ainley (60)Appointed a Director of the Company in 1999. He joined theGroup in 1976, was appointed as a Director of one of theGroup’s subsidiaries in 1978 and has been Managing Directorof the Cape Industrial Services division since 1995. He has alsobeen a board member of the Offshore Contractors Associationsince 2002. Paul Ainley was involved in a serious car accidenton 31 October 2005, since when he has been unable toreturn to work.

Mike Reynolds (47)Appointed Group Finance Director in 2003. He is a CharteredAccountant who has been Finance Director of the CapeIndustrial Services division since 1998. Since 1 November2005, Mike Reynolds has been combining his duties asFinance Director with those of Acting Managing Director.

John Pool (67)Appointed Non-Executive Director in 1997. A CharteredSecretary who has spent most of his career with AngloAmerican and Charter PLC, he was Managing Director ofPandrol International Limited, Charter’s railway trackmaintenance subsidiary from 1985 to 1995. Since June 2004he has been a Non-Executive Director of McNicholasConstruction Limited.

David McManus (53)Appointed Non-Executive Director in November 2004. Hewas President of ARCO Europe until ARCO’s merger with BPin 2000 and then Executive Vice President with BG Groupuntil 2004. He is currently Vice President of InternationalOperations and an Officer of Pioneer Natural Resources,an independent American oil and gas company.

The Company’s articles provide that at each Annual GeneralMeeting one third of the Directors shall retire from office andmay, if being eligible and willing to act, offer themselves forreappointment.

Martin May is the Director retiring by rotation under Article100 and, being eligible, offers himself for reappointment atthe Annual General Meeting.

Details of the interests of the Directors in the shares and shareoption schemes of the Company are shown over the page.No Director had any interests in any contract with theCompany or its subsidiaries at any time during the year otherthan their service contracts and through the share optionschemes. No Executive Director has a service contract for aperiod in excess of one year’s duration or with provision forpredetermined compensation for loss of office or an amountwhich equals or exceeds one year’s salary and benefits in kind.The Company has maintained insurance to cover theDirectors’ and officers’ liability as defined in s.310(3)(a) of theCompanies Act 1985.

DIRECTORS’ REPORT

162311 Cape front end 16/5/06 11:01 Page 19

20 Cape PLC Annual Report and Accounts 2005

DIRECTORS’ INTERESTSSharesThe beneficial interests of the Directors of the Company and their families in the ordinary shares of the Company as at31 December 2005 are set out below:

2005 2004Number Number

MK May 85,000 50,000

PR Ainley 27,580 2,580

MT Reynolds 12,779 2,779

JA Pool 30,000 10,000

D McManus 25,000 –

None of the Directors had an interest in the shares of any other company in the Group.

On the 21 March 2006 MK May acquired 15,000 ordinary shares of the Company (bringing his total shareholding to100,000 shares) and on the same day JA Pool acquired 10,000 ordinary shares of the Company (bringing his total shareholdingto 40,000 shares).

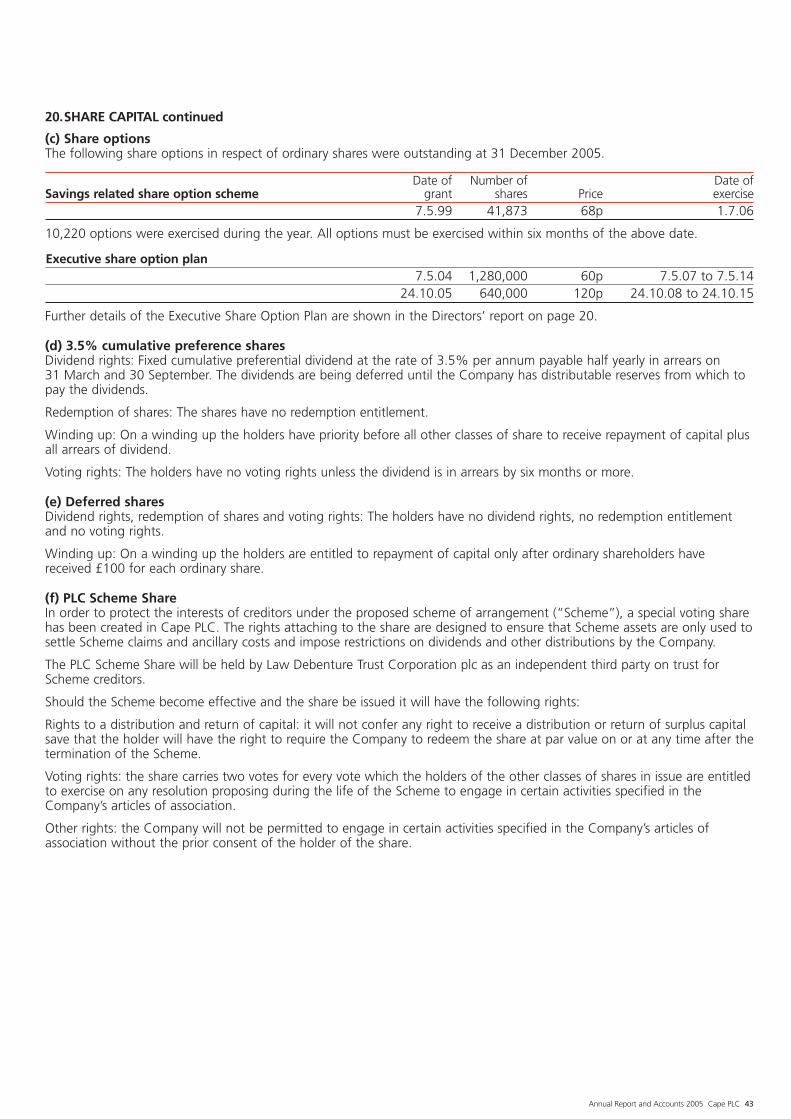

SHARE OPTIONSThe following Directors held options in the Company’s share option schemes during the year:

Earliest At Atexercise Surrendered/ Exercise 31 December 31 December

Date of grant date expiry date price 2004 Granted 2005

PR AinleyShare Option Plan* 07.05.04 07.05.07 07.05.14 £0.60 400,000 – 400,000

MT ReynoldsShare Option Plan* 07.05.04 07.05.07 07.05.14 £0.60 100,000 – 100,000

Share Option Plan* 24.10.05 24.10.08 24.10.15 £1.20 – 100,000 100,000

MK MayShare Option Plan* 07.05.04 07.05.07 07.05.14 £0.60 400,000 – 400,000

*Performance condition applies.

On 24 October 2005, the Board awarded a total of 640,000options over ordinary shares of 25p each to its seniorexecutives, including MT Reynolds. The options were grantedfor nil consideration at an exercise price of 120p per ordinaryshare under the Company’s Share Option Plan.

The middle market price of the shares on 31 December 2005was 114p and the range during the twelve months ended31 December 2005 was 111p to 171.5p.

No other Directors have been granted share options in theshares of the Company or other group entities. None ofthe terms and conditions of the share options were variedduring the year. All options were granted in respect ofqualifying services.

DIRECTORS’ REPORTcontinued

The options were granted at nil cost to the Directors and aresubject to the condition that they will not be exercisableunless the performance of the Company’s adjusted earningsper share over a set three year period exceeds the growth inthe Consumer Prices Index over the same period by 3 per centper annum.

There were no changes to the Directors’ interests in shareoptions in the period from 1 January 2006 to 20 April 2006.

162311 Cape front end 16/5/06 11:01 Page 20

Annual Report and Accounts 2005 Cape PLC 21

GAINS MADE BY DIRECTORS ON SHARE OPTIONSNo gains were made on the exercise of share options duringthe year.

DIRECTORS INDEMNITIESThe Company has provided qualifying third party indemnitiesto Andrew Gillespie, Claire Craigie and Benjamin Whitworth in their capacity as officers of two Group companies that wereput into liquidation on 6 January 2006.

SUPPLIER PAYMENT POLICYThe supplier payment policy for Group companies is to agreeterms and conditions for business transactions with suppliers.Payment is then made subject to these terms and conditionsbeing met. The Company did not have any amounts owed totrade creditors at the end of the year (2004: nil). The Groupowed £17.3 million to trade creditors at the end of the year(2004: £16.4 million) which represented 54 creditor days(2004: 53).

TREASURY POLICYThe Group’s policy on treasury and financial risk is set by theboard and is subject to regular reporting and review. The mainrisks faced by the Group relate to foreign currency risk andliquidity risk.

A significant proportion of the Group’s business is conductedoverseas. The Group is therefore subject to exchange riskwhen translating the results and assets of its overseassubsidiaries into Sterling. Where significant transactionalexchange risks are identified, then appropriate currencycontracts are used to hedge these transactions.

The Group currently has a large liquid fund balance as a resultof the fund raising for the proposed scheme of arrangement.Committed bank facilities have been negotiated to provide theappropriate level of finance to support the current and futurerequirements of the Group should the scheme of arrangementbecome effective.

EMPLOYMENT POLICIESThe companies in the Group operate within broadly prescribedpersonnel and employment policies. Each company developsprocedures which are most appropriate to the circumstanceswithin which it operates. The Group’s training, careerdevelopment and promotion policies provide equalopportunities for all employees.

EMPLOYMENT OF DISABLED PERSONSIt is Group policy to encourage, wherever practicable, theemployment of disabled persons and to provide appropriateopportunities for their training, career development andpromotion. Where employees have become disabled in theservice of the Group, every effort is made to rehabilitate themin their former occupation or in some suitable alternative.

EMPLOYEE INVOLVEMENTThe Group continues its practice of keeping all employeesinformed on matters affecting them and the Group, so thata common awareness amongst all employees is developed inrelation to the financial and economic factors that affect theperformance of the Group. Where applicable, the Groupconsults employees or their representatives on a regular basisso that the views of employees can be taken into account inmaking decisions that are likely to affect their interests.

Senior management is kept abreast of developments infinancial, commercial and personnel matters and this enablesit to ensure that employees at operational level are keptinformed. The Group operates pension schemes for thebenefit of eligible employees in the UK and overseas. Thefunds of the pension schemes are administered by trusteesand they are held separately from Group funds.

HEALTH AND SAFETYThe Group has issued a policy statement on its commitmentto a safe working environment for all employees. The CISManaging Director is responsible for the implementation ofthe Group policy on Health and Safety within his area ofresponsibility. During the year Group operations throughoutthe UK and the rest of the world, were subjected to internaland third party audits to monitor compliance with Companyprocedures and statutory requirements, as set out in moredetail on page 18.

STATEMENT OF DIRECTORS’ RESPONSIBILITIESCompany law requires the Directors to prepare financialstatements for each financial year which give a true and fairview of the state of affairs of the Company and the Groupand of the profit or loss and cash flows of the Group forthat period.

In preparing those financial statements, the Directors arerequired to:

– select suitable accounting policies and then apply themconsistently,

– make judgements and estimates that are reasonable andprudent,

– state whether applicable accounting standards have beenfollowed subject to any material departures disclosed andexplained in the financial statements,

– prepare the financial statements on the going concern basis,unless it is inappropriate to presume that the Group willcontinue in business.

The Directors confirm that they have complied with the aboverequirements in preparing the financial statements.

The Directors are responsible for keeping proper accountingrecords that disclose with reasonable accuracy at any time thefinancial position of the Company and the Group to enablethem to ensure that the financial statements comply with theCompanies Act 1985. They are also responsible forsafeguarding the assets of the Company and the Group andhence for taking reasonable steps for the prevention anddetection of fraud and other irregularities.

It is the intention of the Group that this document (theAnnual Report and Accounts 2005) will be published on theCompany’s website (in addition to the normal paper version).The maintenance and integrity of the Cape website is theresponsibility of the Directors and the work carried out by theauditors does not involve consideration of these matters.

Legislation in the UK governing the preparation anddissemination of financial statements may differ fromlegislation in other jurisdictions.

162311 Cape front end 16/5/06 11:01 Page 21

22 Cape PLC Annual Report and Accounts 2005

DIRECTORS’ REPORTcontinued

SUBSTANTIAL HOLDINGSThe Directors have been advised that as at 4 April 2006 thefollowing have interests of 3 per cent or more in the issuedordinary share capital of the Company:

Number of Percentage ofordinary issued share

shares capital

M & G Investment Management 12,527,814 15.00

Schroder Investment Management 9,922,803 11.88

Merrill Lynch Investment Managers 8,002,764 9.58

Artemis Fund Managers 7,052,191 8.44

Gartmore Investment Management 6,165,265 7.38

F & C Asset Management 3,212,634 3.85

Slater Investments 3,058,566 3.66

Morley Fund Management 3,041,000 3.64

Bluehone Investors 3,000,000 3.59

Marlborough Fund Managers 2,650,000 3.17

The Company has not received notification of any otherinterests held by persons acting together which at 4 April2006 represented 3 per cent or more of the issued ordinaryshare capital.

ANNUAL GENERAL MEETINGAt the Annual General Meeting to be held on 19 June 2006,resolutions will be proposed on the following items ofspecial business:

(a) To approve the rules of the Cape PLC 2006 Sharesave Plan(“Plan”).

The Directors believe that the incentivisation of the Group’semployees is in the best interests of the Company.Accordingly, they propose to introduce a new InlandRevenue approved Save As You Earn scheme which willbe open to all employees with more than one year’scontinuous service.

(b) To authorise the Directors to be counted in the quorumand to vote in meetings and on matters connected withthe Plan.

The Directors consider that such a measure is necessary inorder to enable them to implement the Plan provided that(as set out in the resolution) no Director is permitted tovote on any matter solely concerning his own participation.

(c) To disapply statutory pre-emption rights under Section 89of the Companies Act 1985.

The Directors consider it to be in the best interests of theCompany that they should continue to have the powerto allot equity securities for cash other than to existingshareholders up to a maximum amount of 5 per centof the Company’s issued ordinary share capital at31 December 2005. A Special Resolution will be proposedat the Annual General Meeting authorising the Directors toallot ordinary shares up to a nominal amount of£1,044,038.

The text of all the resolutions is set out in full in the noticeconvening the Annual General Meeting on pages 58 and 59.

The Annual General Meeting is to be held on 19 June 2006 atthe offices of Travers Smith at 10 Snow Hill, London EC1A 2AL.

INDEPENDENT AUDITORSThe auditors PricewaterhouseCoopers LLP have indicated theirwillingness to continue in office, and a resolution concerningtheir reappointment will be proposed at the Annual GeneralMeeting.

By order of the BoardBW WhitworthSecretary20 April 2006

Cape House3 Red Hall AvenueParagon Business Village WakefieldWest Yorkshire WF1 2UL

162311 Cape front end 16/5/06 11:01 Page 22

Annual Report and Accounts 2005 Cape PLC 23

We have audited the group and parent company financialstatements (the ‘‘financial statements’’) of Cape PLC for theyear ended 31 December 2005 which comprise theconsolidated profit and loss account, the consolidated andcompany balance sheets, the consolidated cash flowstatement, the reconciliation of net cash flow to movementin net funds/(debt), the consolidated statement of totalrecognised gains and losses, the note of consolidated historicalcost profit and losses, the reconciliation of movements inshareholders’ funds and the related notes to the financialstatements. These financial statements have been preparedunder the accounting policies set out therein.

RESPECTIVE RESPONSIBILITIES OF DIRECTORS ANDAUDITORSThe directors’ responsibilities for preparing the Annual Reportand the financial statements in accordance with applicable lawand United Kingdom Accounting Standards (United KingdomGenerally Accepted Accounting Practice) are set out in theStatement of Directors’ Responsibilities.

Our responsibility is to audit the financial statements inaccordance with relevant legal and regulatory requirementsand International Standards on Auditing (UK and Ireland). Thisreport, including the opinion, has been prepared for and onlyfor the company’s members as a body in accordance withSection 235 of the Companies Act 1985 and for no otherpurpose. We do not, in giving this opinion, accept or assumeresponsibility for any other purpose or to any other person towhom this report is shown or into whose hands it may comesave where expressly agreed by our prior consent in writing.

We report to you our opinion as to whether the financialstatements give a true and fair view and are properly preparedin accordance with the Companies Act 1985. We also reportto you if, in our opinion, the Directors’ Report is not consistentwith the financial statements, if the company has not keptproper accounting records, if we have not received all theinformation and explanations we require for our audit, or ifinformation specified by law regarding directors’ remunerationand other transactions is not disclosed.

We read other information contained in the Annual Report,and consider whether it is consistent with the audited financialstatements. This other information comprises the Financialhighlights, the Chairman’s statement and review the Directors’report and the other items listed on the contents page. Weconsider the implications for our report if we become awareof any apparent misstatements or material inconsistencies withthe financial statements. Our responsibilities do not extend toany other information.

BASIS OF AUDIT OPINIONWe conducted our audit in accordance with InternationalStandards on Auditing (UK and Ireland) issued by the AuditingPractices Board. An audit includes examination, on a testbasis, of evidence relevant to the amounts and disclosuresin the financial statements. It also includes an assessmentof the significant estimates and judgments made by thedirectors in the preparation of the financial statements, andof whether the accounting policies are appropriate to thegroup’s and company’s circumstances, consistently appliedand adequately disclosed.

We planned and performed our audit so as to obtain all theinformation and explanations which we considered necessaryin order to provide us with sufficient evidence to givereasonable assurance that the financial statements are freefrom material misstatement, whether caused by fraud or otherirregularity or error. In forming our opinion we also evaluatedthe overall adequacy of the presentation of information in thefinancial statements.

OPINIONIn our opinion the financial statements:

• give a true and fair view, in accordance with UnitedKingdom Generally Accepted Accounting Practice, of thestate of the group’s and the parent company’s affairs as at31 December 2005 and of the group’s profit and cash flowsfor the year then ended; and

• have been properly prepared in accordance with theCompanies Act 1985.

EMPHASIS OF MATTER – CONTINGENT LIABILITY FORINDUSTRIAL DISEASE CLAIMSIn forming our opinion, which is not qualified, we haveconsidered the adequacy of the disclosures made in note 26to the financial statements concerning the impact of, andaccounting for, potential future claims for industrial diseasecompensation. An independent actuarial estimate of therange of certain potential liabilities has been performed,however, given the wide range of the estimates and significantdegree of uncertainty surrounding them, it is not possible forthe Directors to quantify, with sufficient reliability, the amountrequired to settle future claims and accordingly claims aregenerally accounted for on the basis of claims lodged orsettlements reached and outstanding at the balance sheetdate. However, if it were possible to assess reliably the presentvalue of the amount required to settle future claims such thatthis was provided in the balance sheet, there would be amaterially adverse effect on the Group’s financial position.

PricewaterhouseCoopers LLPChartered Accountants and Registered AuditorsLeeds20 April 2006

INDEPENDENT AUDITOR’S REPORT TO THEMEMBERS OF CAPE PLC

162311 Cape front end 16/5/06 11:01 Page 23

24 Cape PLC Annual Report and Accounts 2005

CONSOLIDATED PROFIT AND LOSS ACCOUNTfor the year ended 31 December 2005

2005 2004Note £m £m

Turnover 1 261.8 238.9Less share of turnover of joint ventures (0.3) (5.3)Group turnover 261.5 233.6

Group operating (loss)/profit 3 (1.5) 4.7Share of operating profit in joint ventures 1 0.2 0.4Total operating (loss)/profit: group and share of joint ventures 2 (1.3) 5.1Profit on sale of fixed assets – continuing 5 0.3 –Profit on sale of fixed assets – discontinued 5 – 0.5(Loss)/profit on ordinary activities before interest 1 (1.0) 5.6Net interest payable 8 (0.7) (1.0)Other finance income 27 0.8 1.2(Loss)/profit on ordinary activities before taxation (0.9) 5.8Tax credit on profit on ordinary activities 9 1.0 –Profit for the year 21 0.1 5.8

Earnings per ordinary share:– Basic 10 0.2p 10.7p– Diluted 10 0.2p 10.6p

The notes and information on pages 28 to 53 form part of these financial statements.

Group operating profit before exceptional items 8.2 5.8Operating exceptional items 4 (9.7) (1.1)

162311 Cape back end 16/5/06 11:03 Page 24

Annual Report and Accounts 2005 Cape PLC 25

CONSOLIDATED AND COMPANY BALANCE SHEETSat 31 December 2005

Group Company2005 2004 2005 2004

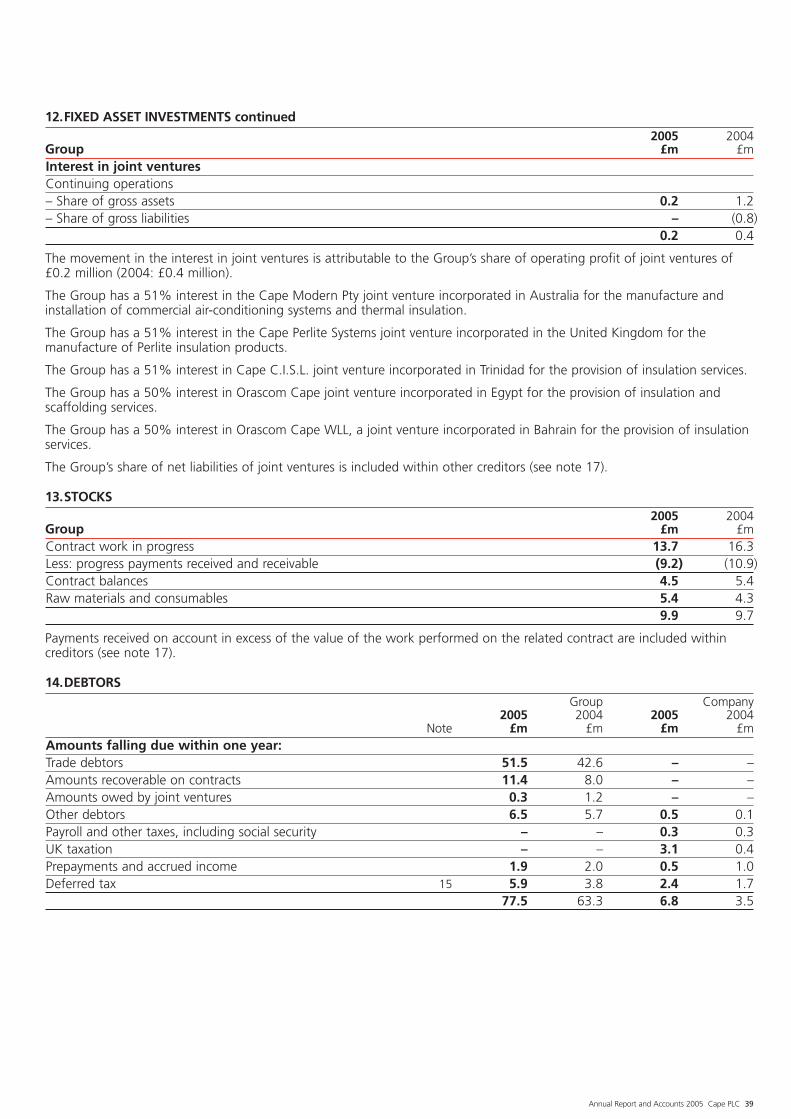

Note £m £m £m £mFixed assetsIntangible assets 11 0.6 0.1 – –Tangible assets 11 29.4 23.4 – –Investments 12 – – 83.5 72.5Interest in joint ventures:

Share of gross assets 12 0.2 1.2 – –Share of gross liabilities 12 – (0.8) – –

0.2 0.4 – –30.2 23.9 83.5 72.5

Current assetsStocks 13 9.9 9.7 – –Debtors 14 77.5 63.3 6.8 3.5Cash at bank and in hand 16 27.2 7.8 1.3 1.4

114.6 80.8 8.1 4.9

Creditors: amounts falling due within one yearShort-term borrowings 17 (1.8) (4.7) – –Other creditors 17 (63.2) (51.1) (2.5) (2.6)

(65.0) (55.8) (2.5) (2.6)Net current assets 49.6 25.0 5.6 2.3Total assets less current liabilities 79.8 48.9 89.1 74.8Creditors: amounts falling due after more than one year 18 (1.7) (5.5) (19.4) (41.6)Provisions for liabilities and charges 19 (19.2) (16.1) (11.0) (6.0)Net assets excluding pension asset 58.9 27.3 58.7 27.2Pension asset 27 5.3 3.6 5.5 3.7Net assets including pension asset 64.2 30.9 64.2 30.9

Capital and reservesCalled up share capital 20 25.5 18.2 25.5 18.2Share premium account 21 25.0 1.7 25.0 1.7Revaluation reserve 21 2.2 2.3 45.9 35.1Profit and loss account 21 11.5 8.7 (32.2) (24.1)Shareholders’ funds (includes non-equity interests) 64.2 30.9 64.2 30.9Equity interests 59.6 26.3 59.6 26.3Non-equity interests 20 4.6 4.6 4.6 4.6Shareholders’ funds 64.2 30.9 64.2 30.9

These accounts were approved by the Board of Directors on 20 April 2006 and were signed on its behalf by:

MK May Chairman

MT Reynolds Group Finance Director

The notes and information on pages 28 to 53 form part of these financial statements.

162311 Cape back end 16/5/06 11:03 Page 25

26 Cape PLC Annual Report and Accounts 2005

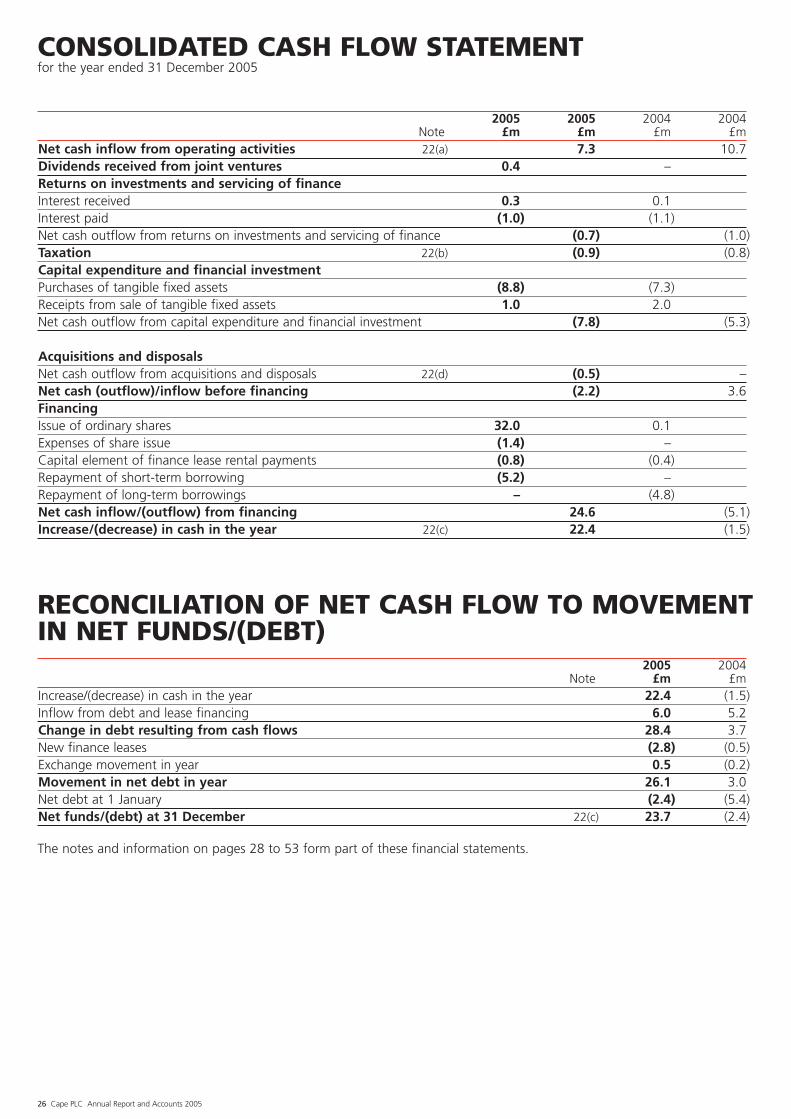

CONSOLIDATED CASH FLOW STATEMENTfor the year ended 31 December 2005

2005 2005 2004 2004Note £m £m £m £m

Net cash inflow from operating activities 22(a) 7.3 10.7Dividends received from joint ventures 0.4 –Returns on investments and servicing of financeInterest received 0.3 0.1Interest paid (1.0) (1.1)Net cash outflow from returns on investments and servicing of finance (0.7) (1.0)Taxation 22(b) (0.9) (0.8)Capital expenditure and financial investmentPurchases of tangible fixed assets (8.8) (7.3)Receipts from sale of tangible fixed assets 1.0 2.0Net cash outflow from capital expenditure and financial investment (7.8) (5.3)

Acquisitions and disposals Net cash outflow from acquisitions and disposals 22(d) (0.5) –Net cash (outflow)/inflow before financing (2.2) 3.6Financing Issue of ordinary shares 32.0 0.1Expenses of share issue (1.4) –Capital element of finance lease rental payments (0.8) (0.4)Repayment of short-term borrowing (5.2) –Repayment of long-term borrowings – (4.8)Net cash inflow/(outflow) from financing 24.6 (5.1)Increase/(decrease) in cash in the year 22(c) 22.4 (1.5)

RECONCILIATION OF NET CASH FLOW TO MOVEMENTIN NET FUNDS/(DEBT)

2005 2004Note £m £m

Increase/(decrease) in cash in the year 22.4 (1.5)Inflow from debt and lease financing 6.0 5.2Change in debt resulting from cash flows 28.4 3.7New finance leases (2.8) (0.5)Exchange movement in year 0.5 (0.2)Movement in net debt in year 26.1 3.0Net debt at 1 January (2.4) (5.4)Net funds/(debt) at 31 December 22(c) 23.7 (2.4)

The notes and information on pages 28 to 53 form part of these financial statements.

162311 Cape back end 16/5/06 11:03 Page 26

Annual Report and Accounts 2005 Cape PLC 27

CONSOLIDATED STATEMENT OF TOTAL RECOGNISEDGAINS AND LOSSESfor the year ended 31 December 2005

2005 2004Note £m £m

Profit for the year 0.1 5.8Currency translation differences net of taxation on foreign currency net investments 21 1.4 (1.0)Actuarial gain/(loss) recognised in the pension scheme 27 1.6 (5.6)Movement on deferred tax relating to pension asset 27 (0.5) 1.8Total recognised gains relating to the year 2.6 1.0

NOTE OF CONSOLIDATED HISTORICAL COST PROFITSAND LOSSESfor the year ended 31 December 2005

2005 2004£m £m

Reported (loss)/profit on ordinary activities before taxation (0.9) 5.8Realisation of property revaluation gains of previous years 0.1 0.1Historical cost (loss)/profit on ordinary activities before taxation (0.8) 5.9Historical cost profit for the year retained after taxation 0.2 5.9

RECONCILIATION OF MOVEMENTS INSHAREHOLDERS’ FUNDSfor the year ended 31 December 2005

2005 2004Group Note £m £mProfit for the year 0.1 5.8Currency translation differences net of taxation on foreign currency net investments 21 1.4 (1.0)Issue of new share capital (net of issue costs) 30.6 0.1UITF17 credit in respect of share options 0.1 0.1Actuarial gain/(loss) in pension scheme net of deferred tax 1.1 (3.8)Net increase in shareholders’ funds 33.3 1.2Shareholders’ funds at 1 January 30.9 29.7Shareholders’ funds at 31 December 64.2 30.9

The notes and information on pages 28 to 53 form part of these financial statements.

162311 Cape back end 16/5/06 11:03 Page 27

ACCOUNTING POLICIES

1. ACCOUNTING CONVENTIONThe financial statements are prepared under the historicalcost convention, except for certain fixed assets which areincluded at valuation, and in accordance with theCompanies Act 1985 and applicable accounting standardsin the United Kingdom. A summary of the more importantGroup accounting policies are set out below.

2. BASIS OF CONSOLIDATION(a) The consolidated financial statements comprise the

financial statements of the Company and all subsidiaryundertakings for the year ended 31 December 2005.

(b) The results of subsidiary undertakings acquired ordisposed of during the year are included in theconsolidated profit and loss account from or to theireffective dates of acquisition or disposal. Intercompanytransactions, balances, and unrealised profits and losseson transactions between Group Companies areeliminated on consolidation.

(c) The Group’s interest in joint ventures is accounted forunder the gross equity method. The consolidatedfinancial statements include the Group’s share of theprofits or losses of joint ventures and the consolidatedbalance sheet includes the investments in joint venturesat cost, including attributable goodwill, plus theGroup’s share of post-acquisition reserves.

3. FOREIGN CURRENCIESTransactions in foreign currencies are recorded at the rateof exchange ruling at the date of transaction. Profits andlosses of subsidiary undertakings, joint ventures andbranches which have currencies of operation other thansterling are translated into sterling at average rates ofexchange. Assets and liabilities denominated in foreigncurrencies are translated at the year end exchange rate.

Exchange differences arising from the retranslation of theopening net assets of subsidiary undertakings, joint venturesand branches that have currencies of operation other thansterling, net of any matching exchange differences onrelated foreign currency loans taken out to hedge overseasinvestments, are taken to reserves, together with thedifferences arising when the profit and loss accounts aretranslated at average rates and compared with rates rulingat the year end. Other exchange differences are taken tothe profit and loss account.

4. TURNOVERTurnover for manufactured goods is the invoiced value ofsales and services of the Group, net of value added taxes.The policy for recognition of turnover in respect of shortand long-term contracts is disclosed in the policy on stocksand work in progress.

5. COST OF SALESOperating expenses, to the extent that they are directlyrelated to contracting activities, are recoverable againstcontracts and classified within cost of sales.

28 Cape PLC Annual Report and Accounts 2005

6. GOODWILLPurchased goodwill (representing the excess of the fairvalue of the consideration paid over the fair value of theseparable net assets acquired) is stated at cost (lessprovision for impairment) and is amortised through theprofit and loss account on a straight line basis over itsestimated useful economic life, which is considered to be20 years. The carrying value of goodwill is reviewed forimpairment in accordance with FRS 11 ‘Impairment of fixedassets and goodwill’. Any impairment is recognised in theprofit and loss account.

On the implementation of FRS 10 ‘Goodwill and IntangibleAssets’, the Group adopted the transitional arrangementssuch that all goodwill that had been written off directlyto reserves would only be charged to the profit and lossaccount on subsequent disposal of the business to whichit related.

7. TANGIBLE FIXED ASSETS AND DEPRECIATIONTangible fixed assets are stated at cost or valuation netof depreciation and any provision for impairment. Costcomprises purchase cost together with any incidental costsof acquisition. Under FRS 15, the Group followed theoption within the transitional arrangements to retain thebook values of land and buildings, certain of which werelast revalued in 1992. Depreciation is provided to write offthe cost or valuation less the estimated residual value oftangible fixed assets by equal instalments over theirestimated useful economic lives with the exception that nodepreciation is provided on freehold land. The followingrates are applied:

– Freehold buildings – 2% per annum

– Leasehold land and buildings – the period of the lease

– Plant, machinery, fixtures and fittings – 62⁄3% to 331⁄3% perannum.

The carrying value of tangible fixed assets are reviewed forimpairment if events or change in circumstances indicatethat the carrying value may not be recoverable.

Any impairment in the value of fixed assets is dealt with inthe profit and loss account in the period in which it arises.

8. LEASED PLANT AND MACHINERYWhere assets are financed by leasing agreements that giverights approximating to ownership (finance leases), theamount representing the outright purchase price iscapitalised and the corresponding leasing commitments areshown as obligations to the lessor. The relevant assets aredepreciated in accordance with the Group’s depreciationpolicy or over the lease term if shorter. Net finance charges,calculated on the reducing balance method, are included ininterest costs.

All other leases are treated as operating leases and theannual rentals charged to the operating profit for the yearon a straight line basis.

162311 Cape back end 16/5/06 11:03 Page 28

Annual Report and Accounts 2005 Cape PLC 29

9. COMPENSATION FOR INDUSTRIAL DISEASEProvision is made for compensation for industrial diseasewhere it is possible to estimate the liability with sufficientreliability. As explained in note 26, this is generally onlycurrently possible in respect of claims lodged andoutstanding at the year end. Where this is not possible,a contingent liability is noted. Benefit is recognised forinsurance recoveries for claims provided when they areanticipated with virtual certainty.

10.STOCKS AND WORK IN PROGRESSStocks are valued at the lower of cost and net realisablevalue. Contracts are undertaken for customers either on ashort or long-term basis. For short-term contracts, workdone is substantially billed as performed and for long-termcontracts, work is carried out on a substantially fixed orlimited-price basis. With respect to short-term contracts,turnover and profit are recognised according to workexecuted. Amounts taken to turnover in respect of workdone not billed are included within amounts recoverableon contracts. Costs incurred, including an appropriateallocation of overheads, in respect of long-term contractsare included in work in progress net of progress paymentsreceived and provisions for foreseeable losses. Anypayments on account or provisions for foreseeable lossesin excess of contract balances are included in creditors.Turnover and attributable profit on long-term contracts isrecognised according to the percentage of estimated totalcontract value completed or the achievement of contractualmilestones provided that the outcome of the contract canbe assessed with reasonable certainty.

11.DEFERRED TAXATIONDeferred taxation is recognised in respect of all timingdifferences that have originated but not reversed at thebalance sheet date where transactions or events haveoccurred at that date that will result in an obligation to paymore, or a right to pay less, tax in the future. Resultantdeferred tax assets are recognised only to the extent that it isconsidered more likely than not that there will be suitabletaxable profits from which the underlying timing differencescan be deducted, or where there are deferred tax liabilitiesagainst which the assets can be recovered. Deferred tax ismeasured on an undiscounted basis at the tax rates that areexpected to apply in the periods in which timing differencesreverse, based on tax rates and laws enacted or substantivelyenacted at the balance sheet date.

12.INVESTMENTS IN SUBSIDIARY UNDERTAKINGSThe cost of investments is revalued each year to the netasset value of the Group’s subsidiaries with changes aboveand below cost dealt with through the revaluation reserveand profit and loss account reserve accordingly. Provisionhas not been made for any taxation liability on capital gainsthat might arise on the disposal of subsidiary undertakingsat the amount at which they are stated in the balance sheet.

13.PENSIONS AND RETIREMENT BENEFITSThe Group operates two major pension schemes in the UK,one is a defined benefit type and the other of the definedcontribution type. Full valuations of the defined benefitscheme are performed every three years, using theprojected unit method.

The pension expense for defined contribution schemesrepresents amounts payable in the year. Under the definedbenefit scheme any current and past service costs arecharged to operating profit and interest costs and expectedreturns on assets to financing costs or income. Actuarialgains and losses arising from new valuations and fromupdating the latest actuarial valuation to reflect conditionsat the balance sheet date are recognised in the statementof total recognised gains and losses.

The Group continues to account for its pension schemesin the UK in line with the requirements of FRS 17‘Retirement Benefits’.

Further information is provided in note 27.

14.FINANCIAL INSTRUMENTSA derivative instrument is considered to be used forhedging purposes when it alters the risk profile of anexisting underlying exposure of the Group in line withthe Group’s risk management policies.

The Group uses derivative financial instruments primarilyto manage exposures to fluctuations in foreign currencyexchange rates. As in previous years, it is the Group’s policynot to trade in financial instruments.

Gains and losses on foreign currency contracts are deferredand recognised in the profit and loss account when thehedged transaction occurs. Gains and losses arising fromthe translational hedges of foreign currency investments aretaken to reserves.

15.EMPLOYEE SHARE OPTION PLANSThe cost of share awards to employees are recognised overthe period to which the employee’s performance relates. Theamount recognised is based on the fair value of the awardat the date the award is made.

The Company has taken advantage of the exemption underUITF 17 (revised), in relation to Inland Revenue approvedSAYE schemes from the need to apply a charge to the profitand loss account based on the difference between the fairvalue of the shares and the exercise price at the date theaward is made.

162311 Cape back end 16/5/06 11:03 Page 29

30 Cape PLC Annual Report and Accounts 2005

NOTES TO THE FINANCIAL STATEMENTS

1. SEGMENTAL ANALYSIS

Profit before taxNon-

Pre- Operating operating Netexceptional exceptional exceptional operating

Turnover items items items Total assets£m £m £m £m £m £m

(a) Business analysis (Note 4) (Note 5)2005Continuing operations– Cape Industrial Services 261.5 14.7 – 0.3 15.0 51.0– Joint ventures 0.3 0.2 – – 0.2 –Total Cape Industrial Services 261.8 14.9 – 0.3 15.2 51.0– Head Office – (1.9) (9.7) – (11.6) 3.2– Compensation for industrial disease – (4.6) – – (4.6) (14.5)Total continuing 261.8 8.4 (9.7) 0.3 (1.0) 39.7

Discontinued operations– Cape Calsil – – – – – 0.8Total operations 261.8 8.4 (9.7) 0.3 (1.0) 40.5Net interest/net cash (0.7) 23.7Other finance income 0.8 –

(0.9) 64.2

There are no significant inter-segment sales between business units.

Profit before taxNon-

Pre- Operating operating Netexceptional exceptional exceptional operating

Turnover items items items Total assets£m £m £m £m £m £m

(Note 4) (Note 5)2004Continuing operations– Cape Industrial Services 233.6 11.0 – – 11.0 47.4– Joint ventures 5.3 0.4 – – 0.4 0.2Total Cape Industrial Services 238.9 11.4 – – 11.4 47.6– Head Office – (1.5) (1.1) – (2.6) 1.8– Compensation for industrial disease – (3.7) – – (3.7) (16.9)Total continuing 238.9 6.2 (1.1) – 5.1 32.5

Discontinued operations– Cape Calsil – – – 0.5 0.5 0.8

Total operations 238.9 6.2 (1.1) 0.5 5.6 33.3Net interest/net borrowings (1.0) (2.4)Other finance income 1.2 –

5.8 30.9

Net operating assets represents the net assets of each business unit after adjusting for Group funding loans.

162311 Cape back end 16/5/06 11:03 Page 30

Annual Report and Accounts 2005 Cape PLC 31

1. SEGMENTAL ANALYSIS continued

Profit before taxNon-