Annual Report and Financial Statements for the year ended 31 st March 2017 The Financial Conduct Authority: 29516R The Homes and Communities Agency: L4361 Cobalt Housing Limited is part of Onward Homes

Transcript

Annual Report and Financial Statements

for the year ended 31st March 2017

The Financial Conduct Authority: 29516R

The Homes and Communities Agency: L4361

Cobalt Housing Limited is part of Onward Homes

Association Statements

Foreword by the Chair of the Board 1

Board, Senior Management and Professional Advisors 2

Report of the Board and Financial Statements

Strategic Report 3 - 16

Report of the Board 17 - 21

Independent Auditor’s Report 22

Statement of Comprehensive Income 23

Statement of Financial Position 24

Statement of changes in Equity 25

Statement of Cash Flow 26

Notes to the Financial Statements 27 - 50

TABLE OF CONTENTS

FOREWORD BY THE CHAIR OF THE BOARD

1

The Board of Cobalt and I

are pleased to report, that

our financial results last

year far exceeded our

expectations and give us a

really sound financially

footing from which to move

forward.

This has never been more

important as we look to

leave Onward Homes and

start a new chapter as a

standalone organisation.

Our financial highlights include:

£11.5m operating surplus

£9.8m net surplus

£16.6m cash inflow from operating activities

£0.7m reduction in our borrowing

£8.2m increase in cash balances

These surpluses are generated for a purpose and will

be reinvested back into our homes and communities.

In 2016-17 our investment activities included:

The investment of £2.0m to complete 55 new

homes that handed over in the year

Securing a further £0.53 in HCA grant

The investment of £4.2m into continuing to

improve our existing homes

Our improved financial results are especially welcome

as our rents reduced by 1% at the start of the 2016-17

financial year. This was the first of four rent reductions

meaning that by 2019 our rental income will be around

12% lower in real terms that is was in 2015.

On the national stage housing still has a high political

profile. Although the Government is primarily focused

on housing for sale, there are signs that limited funding

may be available to support homes for rent as part of

mixed tenure developments.

Cobalt’s robust financial position means that we can

develop homes of all tenures including affordable rent

even if no grant subsidy is available.

As I reported in last year’s statement Onward Homes

(was Symphony Housing) is on a journey to simplify its

federated partnership of member organisations.

Throughout 2016 the board carefully examined the

options available to Cobalt, exploring the implications

of leaving the group to continue on as a standalone

organisation.

Tenants’ views were paramount in this process and a

ballot was undertaken in 2016. The strength of view

expressed was extremely encouraging with 98% of the

2,800 votes cast in favour of independence.

We reached a formal agreement on demerger with

Onward Homes and the target date is 29th September

2017. The board and all our employees are working

extremely hard in preparation so that none of our

services that you receive will be disrupted.

I would like to take this opportunity to thank Cobalt’s

voluntary board members, its directors and its staff for

their hard work, dedication and commitment over the

last year.

I would also like to acknowledge and thank the large

number of tenants and residents, including the

members of our award winning scrutiny panel who give

up their time to help make Cobalt the successful

organisation it is today. Our tenants are at the heart of

everything we are trying to achieve and their

contribution to helping set our agenda, scrutinising our

services and monitoring our performance is greatly

appreciated.

These are challenging but also exciting times as we are

about to enter a new chapter in the Cobalt story.

Peter Mitchell

Cobalt Chair

BOARD, SENIOR MANAGEMENT AND PROFESSIONAL ADVISORS

2

Members of the Board Peter Mitchell (Chair) Kieran Timmins (Deputy Chair) Jean Myers Alan Walker Andy Pritchard Mairie Gollock

Nick Crofts

Eddie Wright Sharon Ross (to December 2016)

Principal Legal Advisors Brabners Chaffe Street LLP 58 King Street Manchester M2 4LQ

Trowers and Hamlin LLP Heron House Albert Square Manchester M2 5HD

Anthony Collins LLP 134 Edmund Street Birmingham B3 2ES

Principal Banker National Westminster Plc 33 Piccadilly Manchester M1 1LR

Registered Head Office Cobalt Housing Limited 199 Lowerhouse Lane Liverpool L11 2SF

Principal Funder Abbey National Treasury Services c/o Santander UK plc 2 Triton Square Regent’s Place London

NW1 3AN

External Auditor KPMG LLP

1 St Peter’s Square Manchester

M2 3AE

STRATEGIC REPORT

3

Overview and background

The Association was formed in February 2003

following the transfer of homes from Liverpool City

Council. We are controlled by a Board of

Management of between five and twelve members.

The Association is a member of Onward Homes and

a subsidiary of Onward Homes Limited. The

Association has agreed terms for its formal

demerger from Onward Homes in September 2017.

Onward Homes was previously known as

Symphony Housing Group. It changed its name to

Onward Homes on the 2nd May 2017.

Onward Homes is one of the largest housing and

regeneration organisations operating in the North

West of England, is a significant player in the region.

Operating as a federated partnership it has 8

member organisations providing services to over

40,000 homes.

Principal Activities

The Association is a public benefit entity whose

principal activities are the management,

maintenance and development of affordable homes

for rent. It owns 5,999 homes and manages 6,002

homes (as at March 2016) located on the north-

eastern outskirts of Liverpool.

The Association is also actively engaged in

improving the social, economic and environmental

problems faced by the communities within which it

operates.

Legal structure

The Association is a charitable Registered Society

under the Cooperative and Community Benefit

Societies Act 2014. It is registered with the

Financial Conduct Authority with a registration

number of IP29516R.

The Association is registered with the Homes and

Communities Agency as a Registered Provider of

social housing with a registration number of L4361.

Cobalt’s mission, vision and purpose

We take great pride in the part we play in meeting a

wide range of housing and community needs. Our

business strategy is to maintain our focus on core

social housing activity and do fewer things; but do

them extremely well and efficiently. By

safeguarding the social housing in our care we will

make sure that it continues to meet housing needs

in our area for generations to come.

Our Mission

To improve people’s lives by providing affordable,

high quality homes and services in thriving

communities.

Our Vision

To be the landlord, employer and partner of choice,

delivering lasting physical, economic and social

regeneration.

Our Purpose

To meet people’s housing and support needs

To be a successful well-managed organisation

that improves wellbeing and regenerates local

communities

To help our residents to realise their potential

and gain skills and confidence

Our Values:

The Cobalt Way describe how we approach our

work and what customers and partners can expect

of us. We want to be known as much for the way

we do things as for the things we do.

Co-operative: We actively seek effective

partnerships in order to deliver the

best possible outcomes.

Open: We are open, honest and

accountable in everything we do.

Balanced: Our business decisions are

balances with our social purpose.

“Doing the right things in the right

way to achieve the right outcomes.”

Ambitious: Our ambition is to inspire people

and help them achieve success and

overcome barriers.

Learning: We take every chance to learn,

adapt and improve

Tenant We value the involvement of our

Focussed: tenants in shaping our services and

scrutinising our performance.

STRATEGIC REPORT

4

Corporate Priorities

Cobalt is in a period of transition as it prepares to leave Onward Homes and become a standalone organisation

in September 2017. For 2018 the board has determined that it will prepare a revised suite of strategies and

corporate objectives that will reflect the new freedoms that independence will bring.

Our key corporate priories for 2016-21 are aligned around six strategic themes:

Best for Value for money

VfM Culture i. Set and achieve challenging efficiency targets and embed a culture of actively seeking

value for money in everything that we do.

Best for customers

Customer excellence i. Understand our different customer segments and deliver a high quality standard of

service tailored to meet their needs. ii. Tenants and staff are engaged in determining the priorities for our future service offer in

light of the rent reduction regime and independence. iii. Support tenants who need help with budgeting, banking or other financial inclusion to

sustain their tenancies and maintain our financial viability.

Best for customers and

people

Closing the digital divide i. Develop our digital service offer promoting and supporting digital access for our

customers. ii. Work with partners to identify practical solutions to help improve access for all tenants

and residents to services through the internet.

Best for neighbourhoods & communities

Active asset and neighbourhood management i. A holistic approach to management and investment in our homes and neighbourhoods

keeps them desirable and fit for the future. ii. Our stock of homes better matches the demand for smaller homes as a result of the

bedroom tax. iii. Sustainable development opportunities are pursued that deliver real and lasting benefits

to Cobalt, our residents and their communities. iv. To refine and utilise our active asset management model to inform our neighbourhood

and investment plans.

Best for customers

Our repairs service offer

i. Develop and expand on the success and savings being delivered through our in-house

Cobalt Plus service.

Partnerships, future and

VfM

Fit for independence i. Robust arrangements to replace current group services are put in place ii. All necessary funding, regulatory and stakeholder consents are secured iii. Standalone governance arrangements are put in place that fully comply with all

regulatory requirements iv. Appropriate funding facilities will be put in place to support independence and future

development plans

Best for customers and people

Behaviours and competency framework i. We enjoy a positive working environment where our staff are well trained, feel valued

and are motivated to go the extra mile for customers and colleagues. ii. To implement a systematic approach to performance management assessing the

achievements of our people through actions and behaviours.

STRATEGIC REPORT

5

Financial and Operating Review

The board is pleased to report that the association

achieved a surplus on ordinary activities for the year

of £9.8m (2016 £6.3m).

This represents a £3.5m (55%) increase on the

surplus achieved in the previous financial year and

puts the Association in a robust financial position as

it prepares for independence form Onward Homes.

Turnover:

Turnover reduced by £0.5m (1.7%) to £28.1m (2016

£28.6m). In April 2016 we implemented the first of

four 1% rent reductions in line with the current rent

setting regime.

Operating Costs:

Our operating costs reduced by £3.7m (18%) to

£17.0m (2016 £20.7m). The main factors behind

this reduction were:

The past service pension liabilities attributable to

Cobalt from other members of Onward were

reduced by £2.1m

Management costs reduced by £0.3m

Routine maintenance costs reduced by £0.3m

Planned and major repair costs reduced by

£0.4m

Impairment charges reduced by £0.3m (90%) to

£37k (2016 £0.4m)

Operating Surplus

Our operating surplus increased by £3.5m (44%) to

£11.5m (2016 £8.0m).

Interest Receivable and Payable

Net interest charges after amounts receivable and

other financing amounts reduced by £0.1m (6.6%)

to £1.7m (2016 £1.8m).

Cash Flows and Treasury Position

The net cash inflow from operating activities

increased by 17% to £16.7m (2016 £14.2m). This

operating cash inflow was sufficient to fund all of the

associations investing activities in the year. The

Association generated net cash from all activities of

£8.9m.

After repaying loans of £0.7m in the year the

Association increased its retained cash and

equivalent balances by £8.1m to £16.4m.

Financial Trends

These results are extremely positive and reflect the association’s commitment to maintaining its financial health.

Despite a fall in turnover as rent levels reduce, the association has improved its bottom-line and significantly

improved its operating margins.

The association creates this surplus for a purpose, re-investing it into improving its existing homes as well as

developing much needed new ones. The improved financials show the impact of the Association’s drive to

improve value for money and deliver more with the resources available.

Accounting Policies

The Association’s principle accounting policies are set out on pages 27 to 33 of the financial statements. The

policies that are most critical to the financial results relate to accounting for housing properties and include:

capitalisation of costs; deduction of capital grant from the cost of assets; housing property depreciation;

investment properties and the treatment of pensions.

STRATEGIC REPORT

6

Five year financial highlights

Properties 2017 2016 2015 2014 2013

Number of properties in management at the year end 6,019 6,002 6,028 5,906 5,878

Gain (loss) on disposal of housing properties 0.4 0.2 - - -

Operating surplus 11.5 8.0 8.5 5.3 7.5

Net interest charge (1.7) (1.8) (1.6) (1.7) (1.7)

Surplus on disposal of assets - 0.1 - 0.5 0.3

Surplus for the year 9.8 6.3 6.9 4.1 6.1

Statement of Financial Position 2017 £’m

2016 £’m

2015 £’m

2014 £’m*

2013 £’m*

Fixed assets at cost less depreciation 159.1 161.2 159.1 154.5 143.5

Net current assets/(liabilities) 12.1 5.9 1.4 1.5 12.6

Pension asset - 0.5 - - -

Total assets less current liabilities 171.2 167.6 160.5 156.0 156.1

Creditors due after more than one year (81.6) (87.2) (86.7) (86.4) (90.8)

Total Net Assets 89.6 80.4 73.8 69.6 65.3

Reserves 89.6 80.4 73.8 69.6 65.3

Financial Statistics 2017 2016 2015 2014* 2013*

Operating margin 40.8% 28.0% 30.2% 20.9% 31.0%

Net margin 34.8% 22.0% 24.5% 16.0% 25.1%

Return on Net Assets (RONA) 5.7% 3.8% 4.3% 3.6% 5.2%

Return on Capital Employed (ROCE) 6.7% 4.8% 5.3% 5.0% 6.7%

EBITDA Margin% 62.9% 49.4% 51.6% 43.9% 53.1%

EBITDA MRI Margin % 48.4% 33.4% 31.6% 23.3% 20.2%

Indebtedness Statistics

EBITDA MRI Interest cover %

762% 522% 511% 328% 267%

Gearing (total loans as a % of grants and reserves) 33.6% 36.1% 37.8% 39.7% 47.2%

Debt per unit owned £7,093 £7,240 £7,320 £7,472 £8,505

Operational Performance

Current tenant rent arrears 8.6% 8.9% 8.9% 8.4% 8.5%

% of rent collected 99.4% 98.6% 98.0% 98.5% 99.4%

Rent losses on void properties 1.0% 0.8% 1.3% 1.4% 1.0%

* Results for 2012 to 2014 were prepared on pre FRS102 reporting basis

STRATEGIC REPORT

7

Operational Performance Review

The Board is pleased to provide details in relation to

our key housing management and maintenance

performance overleaf. These reflect the type of

indicators that the senior management team and

Board review to ensure the Association is achieving

its objectives and strategies.

Property Portfolio

The Association provides a range of tenancy and

property types located in the north-eastern outskirts

of Liverpool.

Development of new homes

The Association continues to pursue development

opportunities within its area, where these contribute

to its sustainable neighbourhoods. In 2016-17 we

developed 55 new homes.

Development of new homes 2017 2016 2015

Homes developed 55 3 149

Homes acquired - - 4

Home acquired from leaseholder - - 1

Total 55 3 154

Property Sales

The majority of our tenants are able to purchase their

home at a discount through either their protected right

to buy or through the right to acquire.

Property Sales 2017 2016 2015

Homes sold under the Right to Buy and Right to Acquire 38 29 31

Average market value of homes sold (before discount) £64.3k £64.1k £67.2k

Rent Levels

Social housing rents are determined by the

Government’s rent setting regime and the

requirements of the Homes and Communities

Agency’s Rent Standard.

Closing average weekly rent (excluding service charges)

2017 2016 2015

General Housing (social rent) £87.10 £87.97 £86.08

General Housing (affordable rent) £103.09 £103.55 £102.09

In April 2016 the social and affordable rents for all

existing tenancies were reduced by 1%. This was the

first of four annual rent reductions of 1% to take effect

between 2016 and 2019.

Occupancy Rates

Our average occupancy rate reduced slightly to

99.0% (2016 99.2%). With void losses of just 1.0%

of rental income we compare favourably with the

1.7% average for the sector in 2016.

Rent Collection Rates and Arrears

Our rent collection rate increased to 99.4% (2016

98.6%) and our rent arrears fell by 0.3% to 8.6%.

Performance was well ahead of our expectations of

the adverse impact of welfare reform.

Properties as at 31 March 2017 2016 2015

Properties Owned

General Housing (social rent) 5,703 5,736 5,753

General Housing (affordable rent) 300 245 242

Intermediate rents - - 3

Low cost home ownership 3 3 3

Rent to Home-buy - 5 14

Used by Tenant Associations 2 2 2

Non-Social Housing 8 8 8

Total Homes Owned 6,016 5,999 6,025

Leasehold 3 3 3

Total Homes in Management 6,019 6,002 6,028

STRATEGIC REPORT

8

Quality of Accommodation

All our homes meet the Government’s definition of

‘decent homes’ and through effective asset

management we have ensured this 100%

compliance has been maintained.

Accommodation Measure 2017 2016 2015

Homes meeting Decent Homes 100% 100% 100%

Homes with valid Gas Safe certificates

100% 100% 100%

Energy Efficiency SAP rating* 71 71 71

Customer satisfaction with the quality of their home**

91% 91% 91%

Complaints Analysis

We do not always get everything right, but when we

do get it wrong we are determined to learn why. This

learning is then used to help us improve and make

sure we get it right the next time.

Complaints Measure 2017 2016 2015

Number of complaints closed 106 91 104

Satisfaction with the outcome of complaint

73% 73% 76%

Satisfaction with the complaints process

82% 81% 93%

Future Prospects

Onward Homes Group has determined that it no

longer sees its future as a federated partnership and

is proposing that the operations of all its members are

consolidated into single entity. The Cobalt Board

believes that it is in the best interests of its tenants to

leave the group and operate as an independent

registered provider.

This terms for this demerger have been agreed and

were signed by both Cobalt and Onward in May 2017.

The agreed date for the demerger is 29th September

2017.

The Association has robust financial plans for

independence in place and has secured in principle

approval from its funders. The restatement and

renegotiation of the current funding facility will

increase the costs of current borrowing, but will also

allow the Association to better utilise its financial

capacity.

The Association’s ability to development new homes

has been constrained by the restrictions within its

current funding facility. The board has expressed its

aspiration to develop between 250 to 500 new homes

in its first five years after demerger.

Operating Environment Government policies designed to reform the welfare

state will continue to impact on the Association and

the communities it serves.

Almost 70% of the Association’s properties have

three or more bedrooms and the Under Occupancy

Penalty (better known as the bedroom tax) has

resulted in a significant mismatch between the size of

homes available and what those in housing need are

deemed to qualify for.

Housing benefit claims continue to be migrated into

Universal Credit under which the Association will no

longer receive housing benefit directly from the local

authority. Experience to date indicates that arrears

levels rise dramatically on transition.

The level of grant available to support social housing

is very much reduced with the Government preferring

to target help towards home ownership and first time

buyers. The Housing Association sector has more

recently been recognised by Government as a key

player in helping address the housing shortage,

however it is unlikely that significantly more funding

will be made available.

The new Government plans to extend the right to buy

to all social housing tenants. The intention is that this

will increase the number of homes sold to sitting

tenants and provide the resources to build new

homes. The challenge will be whether the funds are

sufficient to build one for one or like for like

replacements for the homes sold.

April 2016 saw the Association reduce all its social

and affordable housing rents are to be reduced by

1%. This was the first of four annual reductions of

1% after which rent levels will be around 10% lower

in real terms. The Association future financial

forecasts and business plan fully reflect this.

In July 2016 the UK electorate voted to leave the

European Union. Exactly how this will impact on UK

businesses is unclear. The increase in inflation

caused by the fall in sterling are already feeding

through and will increase the real terms impact of the

rent reduction regime.

The challenges ahead are daunting; however the

Association’s strong financial position and affordable

cost base mean that it is looking to the future with

confidence and ambition.

STRATEGIC REPORT

9

Risk and uncertainty

Effective risk management is vital to the success of the Association. The Association’s risk map details those

risks that could prevent the business from achieving its strategic objectives. The Group Audit, Risk and

Assurance Committee (GARAC) reviews and scrutinises the risk maps, on a quarterly basis, for all Group

members. The Cobalt Board considers the following risks the most likely to affect future performance and our

ability to achieve our five year plan.

Strategic Risk Area Comment and risk mitigation

Demerger risks

Failure to make a successful transition to independence in 2017 is a key short term risk. This is managed through robust project plans, regular programme meetings with our current and future service suppliers and active engagement with staff at all levels.

Threats to our income from welfare reform and government rent policy

The Association’s plan makes prudent assumptions about the future, stress tests the impact of adverse scenarios and keeps these under review. The Association’s in-house welfare benefits support team provides expert advice and support for staff and customers to maximise income.

Operating cost pressures outstrip growth in our income

The Association operates careful cost control, regular market testing and robust procurement. Limits on total cumulative commitments are in place to ensure the Association can react to adverse economic conditions.

Defined benefit pension liabilities

The Association has taken a number of steps to limit its exposure to pension deficits. It closed all its defined pension schemes to new entrants several years ago. In March 2016 the SHPS defined benefit schemes were closed to further service accrual for existing members.

Difficult funding conditions

Funding renegotiation should be concluded during the summer of 2017. This should secure the Association’s funding needs for the next five years. No commitments will be entered into until and unless adequate funding is agreed and put in place. The majority of the Association’s debt is on fixed interest rates.

Adverse economic conditions including uncertain impact of Brexit

Our projections are realistic and our financial plan projections have been independently assessed. Robust multi-variate stress testing demonstrates a high level of resilience to adverse eventualities.

Treasury risks

Effective monitoring arrangements and forward planning ensure that we meet all the conditions attached to our long term funding and there is early warning of potential future problems.

Ineffective governance and leadership

The Board regularly assesses its own performance and the performance of the Senior Management Team. A robust self-assessment against regulatory standards is carried out every year. The proposed new sub-committee structure is operating in shadow form in advance of demerger.

Service delivery risks

Realistic but challenging targets for project delivery, service standards and performance are set against which the Association regularly assesses its performance.

STRATEGIC REPORT

10

Treasury risk management

The Association defines its treasury management

activities as the management of the Association’s

cash flows, its banking, money market and capital

market transactions; the effective control of the risks

associated with those activities; and the pursuit of

optimum performance consistent with those risks.

The Association regards the successful

identification, monitoring and control of risk to be the

prime criteria by which the effectiveness of its

treasury management activities will be measured.

Accordingly, the analysis and reporting of treasury

management activities focuses on their risk

implications for the Association.

The Association also acknowledges that effective

treasury management will provide support towards

the achievement of its business and services

objectives. It is therefore committed to the principles

of achieving best value in treasury management,

and to employing suitable performance

measurement techniques, within the context of

effective risk management.

In addition to these core objectives, the Board of

Management sets annual targets/parameters within

which the treasury management function operates

including:

A limit on exposure to variable interest rates,

currently 40%

Use of derivative instruments

Approved sources of borrowing and

investment

Funding and liquidity

The Association is financed by a combination of

retained reserves, long-term loan facilities and

project specific grants to part fund the acquisition

and development of new homes. It has fully drawn

all its available loan facilities and in 2016-17 made

a scheduled repayment of loan principle of £0.76m

reducing total borrowing to £42.7m.

The Association had cash and equivalent balances

at the year-end of £16.4m (2016 £8.2m). All

deposits and investments are time limited and

restricted to institutions or money market funds that

meet prudent counterparty credit criteria.

This cash balance is sufficient to fund the

Association’s cash requirements for three years.

Interest rate risk

At the 31st March 2017 the Association had total

borrowing of £42.7m. To protect the Association

from adverse movements in interest rates the

Association fixes the cost of a proportion of its

borrowing.

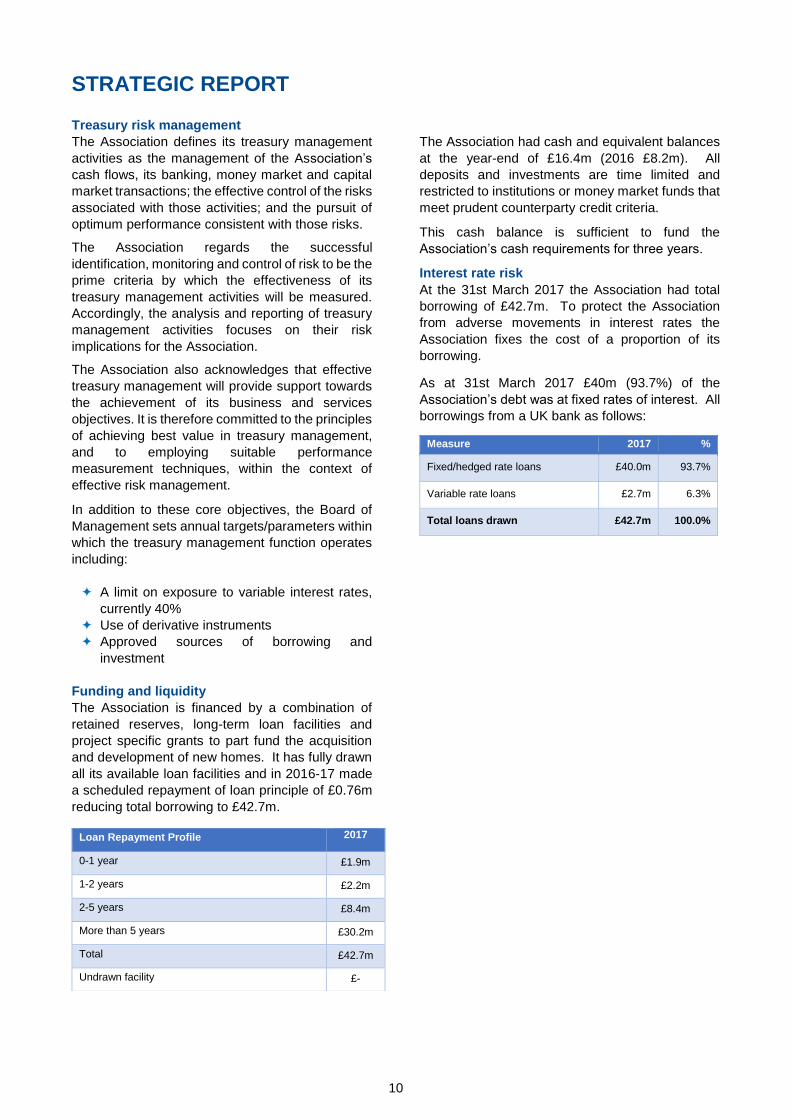

As at 31st March 2017 £40m (93.7%) of the

Association’s debt was at fixed rates of interest. All

borrowings from a UK bank as follows:

Measure 2017 %

Fixed/hedged rate loans £40.0m 93.7%

Variable rate loans £2.7m 6.3%

Total loans drawn £42.7m 100.0%

Loan Repayment Profile 2017

0-1 year £1.9m

1-2 years £2.2m

2-5 years £8.4m

More than 5 years £30.2m

Total £42.7m

Undrawn facility £-

STRATEGIC REPORT

11

Value for Money (VfM) and Benchmarking

VfM is a journey rather than a destination.

Squeezing every last drop of value from the assets

and resources the Association has available is the

key to maximising its investment into its homes,

neighbourhoods and services; as well as improving

performance and protecting its financial viability.

VfM Self-Assessment

The Board of Management and Executive

Management Team have conducted a rigorous self-

assessment of how Cobalt Housing is achieving

value for money in delivering its purpose and

objectives. This report aims to provide a robust and

evidenced based analysis of:

what we are aiming to achieve

how we allocate scarce resources between

competing priorities

how efficiently do we use the resources

available

how good are our service standards and

performance results

how successful are we in achieving the desired

outcome

The full self-assessment report is available on the

Association’s website:

http://www.cobalthousing.org.uk/about-us/value-

for-money-vfm

What VFM means to the Association

VfM is not just about costs, it is about getting the

most for our money. Good VfM is about competitive

costs, high productivity and successful outcomes.

The objective is to achieve the right balance

between cost, quantity and quality and then to keep

this under regular review.

Delivering VfM is not a separate or discrete function

within the organisation. It should, be integral to the

way we work and part of the day job for everyone

we employ or we work with. Onward Homes defines

VfM as:

“Making the most efficient use of our assets

and resources to deliver high quality and

innovative services that successfully meet

customer needs and expectations at lowest

possible cost”.

At its core it is about being a well-run effective social

business. It is having a clear understanding of what

we are here to achieve and then engineering our

business in such a way to maximise its delivery. Our

approach to VfM is framed around:

Our VfM Strategy

The Association’s VfM Strategy based around the

six aims listed below. This strategy is aimed at

maximising VfM for the benefit of our customers and

efficiency gains to be achieved last year of £193k.

This target reflected the fact that our cost base was

already in the lowest 25%. We are pleased to report

however we exceeded this target and secured gains

of £1.1m.

VfM Gains Achieved Target

£’000

Actual

£’000

Asset Management 38 492

Administration 80 274

Capital and Development: 75 340

Total Efficiencies 193 1,106

How these gains were achieved is set out in the full

self-assessment. . In more general terms value for

money in an integrated part of how we do business

that manifests itself in the following ways:

Challenging targets for annual improvement;

Effective scrutiny, measuring and monitoring;

A culture of looking for ways to save money,

improve efficiency and eliminate waste;

Refining the way we are organised and

restructuring to improve efficiency and reduce

costs

Best practice procurement and contract

management;

How do we use the gains we achieve?

We generate a “surplus for a purpose” and after

paying our interest costs, our surplus operating

cash is re-invested into our existing homes and into

supporting the development of new homes.

Our total cash receipts of £29.2m exceeded our

cash outflows by £8.9m and we reduced our net

debt. Our aim is to fund at least 50% of the spend

on developing new homes from operating cash

flows and in 2016-17 we were able to funded the

entire 100%. The 55 new homes that we completed

are therefore debt free and making an immediately

positive financial contribution.

These cash flows clearly demonstrate our capacity

to support additional development activity and

deliver more new homes. The reason why it has not

been possible to utilise this capacity is the

constraints of our existing funding facility.

Releasing this capacity is a priority for the board and

we will renegotiate the terms of our current funding

facility later in 2017. It will take time for us to gear

up and identify appropriate development

opportunities, but we are targeting increased

activity in 2018 onwards.

Targets for the future

The Board has set a target for efficiency gains of

£950k to be achieved over the next three years.

VfM Gains Target 2018

£’000

2019

£’000

2020

£’000

Asset Management 100 200 300

Administration 150 300 500

Capital and Development: 50 100 150

Total Gains vs 2017 300 600 950

We aim to deliver these targets by:

Establishing new back office support functions

for demerger in 2017 at a reduced cost

Introduce improved ICT capabilities to support

efficient ways of working

Review the delivery of all our neighbourhood

and asset services

Secure cost efficiencies through outsourcing

and partnership arrangements

Explore options to optimise the balance of in-

house and contractor repairs

Improving neighbourhood sustainability

Reducing instances of tenant damage and

misuse of our homes

STRATEGIC REPORT

13

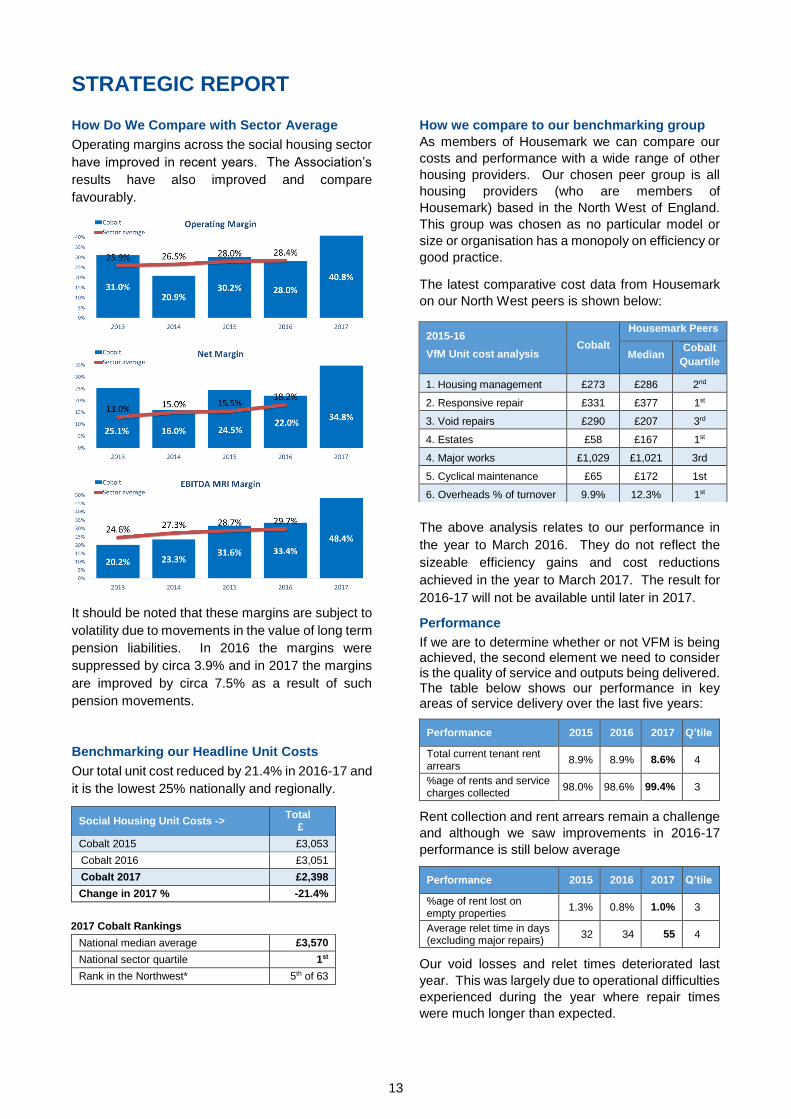

How Do We Compare with Sector Average

Operating margins across the social housing sector

have improved in recent years. The Association’s

results have also improved and compare

favourably.

It should be noted that these margins are subject to

volatility due to movements in the value of long term

pension liabilities. In 2016 the margins were

suppressed by circa 3.9% and in 2017 the margins

are improved by circa 7.5% as a result of such

pension movements.

Benchmarking our Headline Unit Costs

Our total unit cost reduced by 21.4% in 2016-17 and

it is the lowest 25% nationally and regionally.

Social Housing Unit Costs -> Total

£

Cobalt 2015 £3,053

Cobalt 2016 £3,051

Cobalt 2017 £2,398

Change in 2017 % -21.4%

2017 Cobalt Rankings

National median average £3,570

National sector quartile 1st

Rank in the Northwest* 5th of 63

How we compare to our benchmarking group

As members of Housemark we can compare our

costs and performance with a wide range of other

housing providers. Our chosen peer group is all

housing providers (who are members of

Housemark) based in the North West of England.

This group was chosen as no particular model or

size or organisation has a monopoly on efficiency or

good practice.

The latest comparative cost data from Housemark

on our North West peers is shown below:

The above analysis relates to our performance in

the year to March 2016. They do not reflect the

sizeable efficiency gains and cost reductions

achieved in the year to March 2017. The result for

2016-17 will not be available until later in 2017.

Performance

If we are to determine whether or not VFM is being achieved, the second element we need to consider is the quality of service and outputs being delivered. The table below shows our performance in key areas of service delivery over the last five years:

Performance 2015 2016 2017 Q’tile

Total current tenant rent arrears

8.9% 8.9% 8.6% 4

%age of rents and service charges collected

98.0% 98.6% 99.4% 3

Rent collection and rent arrears remain a challenge

and although we saw improvements in 2016-17

performance is still below average

Performance 2015 2016 2017 Q’tile

%age of rent lost on empty properties

1.3% 0.8% 1.0% 3

Average relet time in days (excluding major repairs)

32 34 55 4

Our void losses and relet times deteriorated last

year. This was largely due to operational difficulties

experienced during the year where repair times

were much longer than expected.

2015-16

VfM Unit cost analysis Cobalt

Housemark Peers

Median Cobalt

Quartile

1. Housing management £273 £286 2nd

2. Responsive repair £331 £377 1st

3. Void repairs £290 £207 3rd

4. Estates £58 £167 1st

4. Major works £1,029 £1,021 3rd

5. Cyclical maintenance £65 £172 1st

6. Overheads % of turnover 9.9% 12.3% 1st

STRATEGIC REPORT

14

Performance 2015 2016 2017 Q’tile

% of repairs appointments kept

99.9% 98.1% 100% 1st

Average days taken to complete a repair

2.7 3.0 3.6 1st

%age of homes with a valid gas safety certificate

100% 100% 100% 1st

%age of properties meeting the decent homes standard

100% 100% 100% 1st

On repairs our performance remains positive.

Every property was covered by a valid gas safety

certificate and all homes were compliant with

decent homes. The length of time our tenants wait

for repairs is comparable with the best performance

in the sector.

Not all our performance results are where we would

want them to be. We recognise that we operate in

some deprived neighbourhoods, but this does not

stop us from aspiring to match the best performers

in the region.

Customer Satisfaction

The key to demonstrating VFM is to achieve

efficiencies and improve or maintain high customer

satisfaction at the same time. All our services

measure satisfaction on an ongoing basis, to

ensure we are delivering what our tenants want and

to the standard they expect.

Every two years we conduct a survey of all tenants,

to ask nationally defined questions. As shown in the

table below our key satisfaction results are all top

quartile and actually are amongst the best of any

provider in the country. A new survey is being

undertaken in 2017.

Tenant Survey Results 2010 2012 2014 Q’tile

Overall satisfaction with the services provided by Cobalt?

93% 93% 95% 1st

How satisfied are you that your views are taken into account

84% 85% 86% 1st

Satisfied with the way landlord deals with repairs and maintenance

92% 89% 91% 1st

Satisfaction with the quality of your home

N/A 90% 91% 1st

Satisfaction with the area / neighbourhood as a place to live

83% 84% 89% 1st

Do you think the rent you pay represents value for money?

86% 88% 89% 1st

How likely would you be to recommend Cobalt to family or friends

- 93% 94%

No data

Understanding the return on our assets

The properties that Cobalt owns are an extremely

valuable social asset. It is vital therefore that we

clearly demonstrate:

‘An understanding of the return on

assets and a proactive approach to

managing those assets’

The Group-wide Asset Management Strategy

Guide “Asset Management Our Approach”

establishes the requirements across the Group to

have a much more “dynamic approach” to using our

resources, to maintain and develop our homes and

services, delivering on business objectives and

meeting residents’ expectations.

Financial returns on our assets

Our headline financial results demonstrate a

significant improvement in the headline returns and

contributions from our assets in the last 12 months.

Properties 2015 2016 2017

Homes managed 6,028 6,002 6,019

Financial Statistics

Return on Net Assets (RONA)

4.3% 3.8% 4.5%

Return on Capital Employed (ROCE)

5.3% 4.9% 5.5%

The operating surplus generated on social housing

increased from £8.7m to £9.7m last year. The

operating surplus on lettings per property increased

from £1,455 to £1,949.

STRATEGIC REPORT

15

The average of £1,949 includes a range of results from our different neighbourhoods. This enables us to identify

trends and assets that are potentially performing less well. The chart below demonstrates that while some

areas are less “profitable”, all our neighbourhoods make a positive financial contribution.

Asset Performance Evaluation (APE)

The Group uses financial and non-financial indicators to inform strategic decision making on future investment, usage and retention or disposal of particular assets. This approach evaluates the predicted financial performance of all Onward Homes member’s stock based on their Net Present Value (NPV). This is being used to help us understand and improve over time the return on our assets including:

Measuring the long term performance of our properties

Modelling analysis of our assets value and contribution

Providing an objective baseline from which to make investment decisions

Identify properties requiring an option appraisal

Social Investment and Social Impact

We continue to drive to get better results for our

customers as some residents suffer

disproportionately from poor health, low educational

attainment and higher levels of unemployment. We

are committed to continuing to invest to improve the

neighbourhoods in which we work and to improve

the opportunities that are available for our residents.

In addition to meeting the long term accommodation

needs of over 6,000 social housing tenants and

their families, we create significant social impact

and social value through our work.

In 2016-17 we made a direct social investment of

£1.24m into key areas of activity that promote:

Sustainable tenancies

Community cohesion

Improved life chances & opportunities

Financial inclusion

Social Investment Activity 2016-17

£’000

Anti-social behaviour 299

Financial inclusion & welfare benefit advice 216

Community regeneration (net of grant) 122

Resident involvement and empowerment 112

Property adaptations 208

Free gardening & handyman service 87

Environmental improvements 196

Total Social Investment 1,240

Sustainable Tenancies

In the last year we successfully met the housing

need of 414 new tenants and their families. By

helping them to settle into their new homes our

investment in pre-tenancy support has seen starter

tenancy failure reduce significantly. Examples of

our tailored approach include:

Reusing furniture, giving new tenants a

positive start to their tenancy.

Providing tailored property incentives providing

items such as carpeting and laminate flooring.

Timely and effective response to any

dissatisfaction or issues raised.

Visits and courtesy calls after move in, making

sure tenants have settled in and any issues are

STRATEGIC REPORT

16

dealt with as soon as possible so the tenancy

is sustained.

Transfer inspection visits to check on property

condition and to provide appropriate advice

including promotion of mutual exchange as an

alternative to transfer.

Community Cohesion

We invest in a wide range of community cohesion

and development activities working in partnership

with other local agencies. These promote feelings

of belonging, understanding and community pride.

Managing £151k LCC Youth Grant Funding -

working with youth providers to share

resources and to deliver activities for young

people across our neighbourhoods.

Investing £69k through our Community Fund to

support local community and voluntary

organisations and projects that increase

community cohesion

Improved Life Chances and Opportunities

In the spirit of hand up rather than hand out we are

committed to helping our customers overcome any

obstacles or barriers that they may face. Our

support work is particularly focused on:

Employability, employment and training

opportunities

Health and wellbeing initiatives

Digital awareness

Financial Inclusion

Many of our customers face increased financial

hardship as a result of austerity and welfare reform.

In 2016-17 we delivered:

Completed 9,475 tenant advice contacts,

securing benefits with a total value of £3.5m

including £0.8m in housing-related benefits

Represented 38 tenants at benefit appeals

tribunals and were successful in 32

Successfully applied for 420 discretionary

housing payments on behalf of our tenants

worth a total of around £371,000.

Board VfM Self-Assessment 2017

The regulatory framework includes a specific

standard for VfM. Our regulator, the Homes and

Communities Agency, expects us to ‘have a

strategy for optimising VfM, and systems to

ensure that this strategy is delivered’. The

regulatory framework also includes the requirement

to publish a self-assessment report for

stakeholders, setting out how we comply with the

VfM standard, and our plans for future

improvement.

Sources of Assurance

The Board of Management has gained assurance that Cobalt complies with the regulators VfM standard through:

Annual review of VfM aims and objectives and VfM strategy to ensure it reflects regulatory updates and changes within the organisation

Reviewed half yearly VfM progress reports and on-going VfM updates

Active engagement in the self-assessment process and in reviewing this self-assessment document

Review of our self-assessment against the specific requirements of the standard

Independent review and feedback from Onward on their expectations of member organisations

VfM gains claimed are matched by improved financial results

It is the Board’s assessment that Cobalt Housing fully meets the requirements of the VfM standard. It has a robust and comprehensive approach which demonstrates value for money outcomes and tangible benefits for its tenants and other stakeholders.

The full VfM self-assessment can be found on the Association’s website:

Introduction The Board presents the Annual Report (the ‘Annual Report’) and the audited financial statements for Cobalt Housing Limited (the ‘Association’) for the year ended 31 March 2017.

Principle activities and future prospects

Details of Cobalt’s principle activities, its

performance during the year and factors likely to

affect its future development are contained within

the Strategic Report which precedes this Report.

Board members and executive directors

The current board members and executive directors

of the association (and others who served during

the period) are set out on page 2. The Board

members are drawn from a wide background

bringing together professional, commercial and

other experiences. Board members were not

remunerated for their services to the association but

were permitted to claim expenses incurred in the

performance of their duties.

Executive director’s remuneration

The remuneration of the executive directors is

reviewed by the Appointments and Remuneration

Committee, who make recommendations to be

considered and determined by the Board. Full

details of executive emoluments are set out in note

7 to the financial statements.

Service contracts

The executive directors are appointed on

permanent contracts of employment with a notice

period of three months. Details of the remuneration

of the executive directors is set out in note 7 to the

financial statements.

Pensions

The company closed future service accrual to the

Social Housing Pension Scheme defined benefit

schemes on 31st March 2016.

All company employees, including the executive

directors are able to participate in this defined

contribution schemes on the same terms as all

other eligible staff. The association contributes to

the schemes on behalf of its employees.

Non-executive directors are not eligible to

participate in any Group pension scheme.

Other benefits

The executive directors are not entitled to other

benefits.

Statement of compliance

The Board report and financial statements have

been prepared in accordance with applicable

reporting standards and legislation.

The Association confirms that these financial statements comply with United Kingdom Generally Accepted Accounting Practice (UK GAAP), including FRS 102 ‘The Financial Reporting Standard applicable in the UK and Republic of Ireland’.

Health and safety

Health and Safety is an integral part of the proper

management of all the undertakings over which the

Group has control. The Group has comprehensive

and robust Health and Safety policies and promotes

safe practices and continuous improvement

through a Health and Safety Forum on which all

parts of the Group are represented. Onward

Homes Group is committed to ensuring:

The health, safety and welfare of all our

tenants, leaseholders, staff, contractors and

third parties involved in the operations of the

Group

The safety of the general public who use or

have access to premises or sites under our

control

The way in which we operate contributes to the

wellbeing of the community at large

Donations

The Board has made no charitable or political

donations during the year.

Corporate governance

The Association is governed by a Board of non-executive members who delegate day-to-day operational control to the Managing Director and executive directors.

The Board complies with the 2015 National Housing

Federation Code of Governance and is committed

to upholding the Code of Practice for Board

members. The Board meets frequently to

determine policy and to monitor the performance of

the Association.

The Group operates an Audit Risk and Assurance

Committee which receives reports from Group

Business Assurance and validates and advises on

performance and the effectiveness of internal

controls. An annual report on activity goes to each

Board.

The Group also operates an Appointment and

Remuneration Committee which has responsibility

REPORT OF THE BOARD

18

for ensuring that each Board has effective

Governance arrangements and that these are fully

implemented.

Executive management team

The Board has delegated day to day management

to a group of Executive Directors, who meet as an

Executive Management Team (EMT) to control the

operations of the Association. The EMT meets on

a regular basis and recommends policy decisions to

the Board.

Lead by the Managing Director, the EMT ensures

the effective performance and successful delivery of

services to customers and investment in

neighbourhoods, in line with the agreed business

plan objectives.

Regulation of social housing

The Association is registered with and regulated by

the Homes and Communities Agency (HCA). The

HCA conducts this regulation through our parent

Onward Homes.

Under a co-regulation approach the onus is on each

registered provider to self-regulate, assess and

scrutinise service provision and demonstrate clearly

that services provided represent value for money.

Regulatory Compliance

The Governance and Financial Viability Standard

requires registered providers to assess their

compliance with the Standard at least annually and

Boards are now required to report their compliance

with the Standard within their annual accounts.

An annual self-assessment of the compliance with

the all the HCA standards, including the

Governance and Financial Viability Standard was

carried out in January 2017 and approved by the

Board in April 2017. It is the judgement of the Board

that the Association complies in full with the

Standard and is satisfied it has complied with all

laws and regulations that are relevant.

Group Regulatory Compliance

Onward is regulated as a group and its members

are not awarded their own regulatory judgements.

As a result of control failures at a group level

identified by Onward in 2016 Onward is currently

judged to be non-compliant with the requirements of

the Governance and Viability Standard and

downgraded to G3.

G3 is defined by the regulator as “The provider does not meet our governance requirements. There are issues of serious regulatory concern and in

agreement with us the provider is working to improve its position.”

Work to address the issues identified has been

undertaken and an independent assessment of

whether sufficient progress has been made to

request a regrading by the HCA is underway.

Onward Homes’ viability rating has remained

unchanged at V1 throughout.

Employee involvement

The Board recognises that its employees are its

greatest asset and that it cannot achieve its aims

and objectives without their involvement and

contribution towards running the organisation. The

Association communicates and consults with its

employees through a variety of structures including

regular team briefings, employee emails,

newsletters and trade union meetings (consultation

through staff forum).

The Association is committed to developing a

culture in which equality and diversity is integral to

all of its activities, including the recruitment and

development of staff. We aim to achieve an

inclusive culture that respects and values

differences and eliminates discrimination in all

areas.

Corporate social responsibility

The Board are committed to being a socially

responsible organisation. Managing in a socially

responsible way, ensuring adherence to legislation

and ethical operation. The Association is actively

working with local communities and partners to

improve the life chances of our tenants and

residents.

REPORT OF THE BOARD

19

Statement of internal control

The Group Board acknowledges its ultimate

responsibility for ensuring that the Group has in

place a system of internal control and risk

management that is appropriate to the various

business environments in which they operate and

for review of the effectiveness of that system during

the year.

The Group Audit and Risk Committee is responsible

to the Group Board for monitoring this system and

reporting on its effectiveness.

Internal controls are designed to identify and

manage rather than eliminate risks which may

prevent an organisation from achieving its

objectives.

The system of internal control is designed to

manage risk and give reasonable rather than

absolute assurance with respect to:

The achievement of key business objectives

and expected outcomes

The preparation and reliability of financial and

operational information used within

the organisation and for publication

The maintenance of proper accounting and

management records

The safeguarding of assets against

unauthorised use or disposition

Internal assurance activities

The process followed to identify, evaluate and

manage significant risks faced by the Group is

ongoing and has been in place during the past

financial year and up to the date of the annual report

and accounts.

Internal audit assurance

The Group’s in-house internal audit function is used

to provide assurance on the operation of the control

framework and the management of risk. Internal

audit are not responsible for the design and

construction of control systems but provide an

assessment as to their effectiveness.

The Group Audit and Risk Committee oversee the

work of internal auditors and review reports issued

by them. The Committee is responsible for

monitoring the actions identified as a result of

internal audit findings that are implemented in a

timely fashion.

External audit assurance

The work of the external auditors provides some

independent assurance over the adequacy of the

internal control environment. The Group receives a

management letter from the external auditors which

identifies any internal control weaknesses. The

Board itself and through the activities of the Group

Audit and Risk Committee has reviewed the

outcome of external audit work and the external

audit management letter.

Fraud

The Group Board has a current policy on fraud

which includes both fraud prevention and detection.

A register of frauds and losses is maintained and is

available and reported to the Group Audit and Risk

Committee

Review of risk management and governance

arrangements

During 2015-16 the Group identified that risks

relating to compliance with statutory health and

safety responsibilities were not being effectively

managed which led to a number of control failures.

The Group notified the regulator of its concerns and

in early July 2016 it received a regulatory judgement

that the Group is non-compliant with the

governance requirements set out in the

Governance and Viability Standard and as a result,

the Group’s governance rating has been

downgraded to G3. The Group’s Viability rating

remains unchanged at V1.

The Group established improvement plans, utilising

specialist external advice to improve management,

governance and assurance arrangements.

During 2016-17 the group has implemented the

improvement plans agreed with the regulator and

the regulator may review these arrangements

during 2017 to support a re-grading.

The Group Board acknowledges that their

responsibility applies to the full range of risks and

controls across all Group activities and is to ensure

that planned remedial and improvement action

agreed is implemented in a timely and

comprehensive manner.

The Group Board has considered the effectiveness

of the system of internal control in place in the year

ended 31st March 2017. The Group Board

acknowledges that historically internal control and

risk management arrangements were not working

adequately. We have made good progress in

implementing the improvement plans agreed with

the regulator and we are satisfied that, when

complete, this will address the issues identified

within our systems of internal control, governance

and risk management arrangements.

REPORT OF THE BOARD

20

Going concern

The Association has long-term debt facilities in place and cash and equivalent holdings of £16.4m which provide adequate resources to finance committed reinvestment and development programmes. The Association’s long-term financial plans shows that it is able to service these debt facilities and continue to comply with lenders’ covenants.

On this basis, the Board has a reasonable expectation that the Association has adequate resources to continue in operational existence for the foreseeable future, being a period of twelve months after the date on which the annual report and financial statements are signed. For this reason, it continues to adopt the going concern basis in the financial statements.

Effects of material estimates and judgements

upon performance

Preparation of the financial statements requires management to make significant judgements and estimates. The estimates and assumptions that can have the most significant effect on recognition and measurement of assets, liabilities, income and expenses is provided below.

Impairment

Management assesses the housing properties for indicators of impairment at each balance sheet date. Where indicators exist a detailed assessment is undertaken to compare the carrying amount of assets or cash generating units for which impairment is indicated to their recoverable amounts. Judgements in assessing the level of a cash generating units and the recoverable amounts could lead to increases or decreases in the impairment provision.

The impairment review at 31st March 2017 lead to 16 properties having their carrying value impaired by a total of £37,000. (2016 £367,000). Useful lives of depreciable assets

Management reviews its estimate of the useful lives

of its depreciable assets at each reporting date

based upon the expected utility of the assets.

Uncertainty in these estimates relate to changes in

decent homes standards, component failure or

obsolescence and customer abuse or misuse. Any

of these could lead to more frequent replacement of

key components.

Defined benefit pension obligations

Management’s estimate of the association’s

defined benefit pension obligations is based upon a

number of critical underlying assumptions such as

rates of inflation, mortality, discount rates,

investment returns and future salary increases.

Variation in these assumptions may significantly

impact upon the obligation amount and the annual

defined benefit expenses (as shown in note 36). At

31st March 2017 the association had a pension

deficit of £67,000 (2016 £504,000 surplus).

Provisions for doubtful debt

Management reviews the provision held against the risk of failure to recover current and former tenant rent and service charge arrears at each reporting date. The provision made has an impact upon the value of the current assets recognised at the reporting date and any change in value of the provision during the period is recognised as an operating cost in the statement of comprehensive income in the period.

Disclosure of information to auditors

So far as each of the directors of the Group is

aware, at the time this report is approved:

There is no relevant information which the

Group’s auditor is unaware; and

The directors have taken all the steps that they

ought to have taken as a director in order to

make themselves aware of any relevant audit

information and to establish that the Group’s

auditor is aware of that information.

Independent auditor

The Association will make arrangements to procure

and appoint auditors following its demerger from

Onward Homes in September 2017.

REPORT OF THE BOARD

21

Statement of Board’s responsibilities in respect of the Board’s report and the financial statements

The Board is responsible for preparing the Board’s

Report and the financial statements in accordance

with applicable law and regulations.

Co-operative and Community Benefit Society law

requires the Board to prepare financial statements

for each financial year. Under those regulations the

Board have elected to prepare the financial

statements in accordance with UK Accounting

Standards, including FRS 102 The Financial

Reporting Standard applicable in the UK and

Republic of Ireland.

The financial statements are required by law to

give a true and fair view of the state of affairs of

the association and of its income and expenditure

for that period.

In preparing these financial statements, the Board

is required to:

select suitable accounting policies and then

apply them consistently;

make judgements and estimates that are

reasonable and prudent;

state whether applicable UK Accounting

Standards and the Statement of

Recommended Practice have been

followed, subject to any material departures

disclosed and explained in the financial

statements; and

prepare the financial statements on the

going concern basis unless it is

inappropriate to presume that the

association will continue in business.

The Board is responsible for keeping proper books

of account that disclose with reasonable accuracy

at any time the financial position of the association

and enable them to ensure that its financial

statements comply with the Co-operative and

Community Benefit Societies Act 2014, the Housing

and Regeneration Act 2008 and the Accounting

Direction for Private Registered Providers of Social

Housing 2015.

The Board has general responsibility for taking such

steps as are reasonably open to it to safeguard the

assets of the association and to prevent and detect

fraud and other irregularities.

The Board is responsible for the maintenance and

integrity of the corporate and financial information

included on the association’s website. Legislation

in the UK governing the preparation and

dissemination of financial statements may differ

from legislation in other jurisdictions.

The Report of the Board, including the financial

statements, was approved by the Board on 3rd July

2017 and signed on its behalf by:

Annette Brandwood

Company Secretary

INDEPENDENT AUDITOR’S REPORT

22

Independent auditor’s report to Cobalt Housing

Limited

We have audited the financial statements of Cobalt

Housing Limited for the year ended 31 March 2017,

which comprise the Statement of Comprehensive

Income, Statement of Financial Position, Statement

of Changes in Equity, Statement of Cash Flows and

the related notes. The financial reporting

framework that has been applied in their

preparation is applicable law and UK Accounting

Standards (UK Generally Accepted Accounting

Practice), including FRS 102 The Financial

Reporting Standard applicable in the UK and

Republic of Ireland.

This report is made solely to the association in

accordance with section 87 of the Co-operative and

Community Benefit Societies Act 2014 and section

128 of the Housing and Regeneration Act 2008.

Our audit work has been undertaken so that we

might state to the association those matters we are

required to state to it in an auditor’s report and for

no other purpose. To the fullest extent permitted by

law, we do not accept or assume responsibility to

anyone other than the association as a body, for our

audit work, for this report, or for the opinions we

have formed.

Respective responsibilities of the Board and auditor As more fully explained in the Statement of Board’s Responsibilities set out on page 21 the association’s Board is responsible for the preparation of financial statements which give a true and fair view. Our responsibility is to audit, and express an opinion on, the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statements A description of the scope of an audit of financial statements is provided on the Financial Reporting Council’s website at:

www.frc.org.uk/auditscopeukprivate.

Opinion on financial statements In our opinion the financial statements:

give a true and fair view, in accordance with

UK Generally Accepted Accounting Practice,

of the state of affairs of the association as at

31 March 2017 and of its income and

expenditure for the year then ended;

comply with the requirements of the Co-

operative and Community Benefit Societies

Act 2014; and

have been properly prepared in accordance

with the Housing and Regeneration Act 2008

and the Accounting Direction for Private

Registered Providers of Social Housing

2015.

Matters on which we are required to report by exception We have nothing to report in respect of the following

matters where the Co-operative and Community

Benefit Societies Act 2014 requires us to report to

you if, in our opinion:

the association has not kept proper books of account; or

the association has not maintained a satisfactory system of control over transactions; or

the financial statements are not in agreement with the association’s books of account; or

we have not received all the information and explanations we need for our audit.

Hywel Jones for and on behalf of KPMG LLP, Statutory Auditor Chartered Accountants, 1 St Peter’s Square Manchester M2 3AE

(Loss) / Gain on disposal of fixed assets 6 (11) 123

Interest receivable and similar income 9 44 34

Interest payable and similar charges 10 (1,753) (1,802)

Other financing amounts 37 19 (42)

Surplus on ordinary activities before taxation 9,768 6,299

Taxation on surplus on ordinary activities 11 - -

Surplus for the year after taxation 9,768 6,299

Other Comprehensive Income

Actuarial (loss) / gain in respect of pension schemes 37 (574) 311

Other comprehensive Income for the year (574) 311

Total Comprehensive Income for the year 9,194 6,610

Statement of Financial Position

As at 31st March 2017

24

Note

s 2017

£’000

2016 restated

£’000

Fixed Assets

Housing Properties 12 155,088 155,995

Other Tangible Fixed Assets 13 2,671 2,753

Intangible Fixed Assets 14 138 2

Investments including properties 15 1,174 1,164

159,071 159,914

Debtors Due after more than one year 17 - 1,284

Current Assets

Trade and other debtors 17 3,069 3,113

Cash and cash equivalents 16,397 8,249

19,466 11,362

Creditors

Amounts Falling Due Within One Year 18 (7,306) (5,510)

Net Current Assets 12,160 5,852

Pension Asset 19 - 504

Total Assets less Current Liabilities 171,231 167,554

Creditors: Amounts Falling due After More Than One Year

Deferred grant income 20 (39,102) (39,394)

Loans 21 (40,559) (42,440)

Recycled Capital Grant Fund & Disposal Proceeds Fund 22 (845) (614)

Other Creditors 23 (980) (4,605)

(81,486) (87,053)

Provisions for Liabilities and Charges 25 (68) (85)

Pension Liability 19 (67) -

Total Net Assets 89,610 80,416

Capital and Reserves

Non-Equity Share Capital 26 - -

Revenue Reserves 27 89,610 80,416

Total Capital and Reserves 89,610 80,416

The financial statements were approved by the Board and signed on its behalf on 3rd July 2017 by:

………………………… ………………………… …………………………

Chair Board Member Company Secretary

Statement of Changes in Equity

For the year ended 31st March 2017

25

Notes

Non-equity share

capital £’000

Revenue Reserves

£’000

Total £’000

Balance at 1 April 2016 28 - 80,416 80,416

Total comprehensive income for the period

Surplus for the year ending 31 March 2017 - 9,768 9,768

Actuarial Gains / (Losses) in respect of pension schemes - (574) (574)

Balance at 31 March 2017 - 89,610 89,610

Comprehensive Statement of Cash Flows

For the year ended 31st March 2017

26

Notes 2017

£’000 2016

£’000

Cash flows from Operating Activities 32 16,683 14,225

Cash flow from investing activities

Purchase and Construction of Housing Properties (2,051) (3,707)

Housing component renewal (4,138) (4,354)

Social Housing Grant Received 320 1,985

Sale of Land & Offices 1 (2)

Purchase of Other Fixed Assets (153) (59)

Interest received 45 32

Cash flow from investing activities (5,976) (6,105)

Cash flow from financing activities

Interest Paid (1,799) (1,812)

Repayment of existing borrowing (760) (673)

Cash flow from financing activities (2,559) (2,485)

Net increase / (decrease) in cash and cash equivalents 8,148 5,635

Cash and cash equivalents at the beginning of the year 8,249 2,614

Cash and Cash Equivalents at the End of the Year 34 16,397 8,249

NOTES TO THE FINANCIAL STATEMENTS

27

1. Accounting Policies

Basis of accounting

The financial statements of the association are prepared in accordance with Financial Reporting Standard 102 – the applicable financial reporting standard in the UK and Republic of Ireland (“FRS102”) and the Statement of Recommended Practice: Accounting by Registered Social Providers Update 2014, and comply with the Accounting Direction for Private Registered Providers of Social Housing 2015.

The accounting policies set out below have, unless otherwise stated, been applied consistently to all periods presented in these financial statements. The presentation currency of these financial statements is sterling. All amounts in the financial statements have been rounded to the nearest £1,000.

The association’s ultimate parent undertaking,

Onward Homes Group, includes the association in

its consolidated financial statements.

Measurement convention

The financial statements are prepared on a historical

cost basis except for investment properties which

are stated at their fair value.

Provisions for doubtful debt

The provision is calculated for each individual

tenancy in line with the age of the debt and most

recent payment patterns. The provision rates used

at the reporting date were:

Age of Arrears Static or increasing

arrears

Reducing arrears

Up to 4 weeks 25% 10%

5-8 weeks 50% 25%

9 to 16 weeks 75% 50%

17 to 32 weeks 100% 75%

Above 32 weeks 100% 90%

Former tenant arrears 100% 100%

Other debtor amounts are dealt with on a case by case basis.

Basic financial instruments

Tenant arrears, trade and other debtors

Tenant arrears, trade and other debtors are

recognised initially at transaction price less

attributable transaction costs. Subsequent to initial

recognition they are measured at amortised cost

using the effective interest method, less any

impairment losses. If the arrangement constitutes a

financing transaction, for example if payment is

deferred beyond normal business terms, then it is

measured at the present value of future payments

discounted at a market rate of instrument for a

similar debt instrument.

Trade and other creditors

Trade and other creditors are recognised initially at

transaction price plus attributable transaction costs.

Subsequent to initial recognition they are measured

at amortised cost using the effective interest method.

If the arrangement constitutes a financing

transaction, for example if payment is deferred

beyond normal business terms, then it is measured

at the present value of future payments discounted

at a market rate of instrument for a similar debt

instrument.

Interest-bearing borrowings classified as basic

financial instruments

Interest-bearing borrowings are recognised initially