52

ANNUAL REPORT 1986 STATE SUPERANNUATION BOARD OF VICTORIA

ANNUAL REPORT 1986

STATE SUPERANNUATION BOARD OF VICTORIA

No. 2

VICTORIA

Fifty-sixth Report

of the

STATE SUPERANNUATION BOARD OF VICTORIA

for the

Year ended 30 June 1986

Ordered by the Legislative Assembly to be printed

MELBOURNE F D ATKINSON GOVERNMENT PRINTER

1987

BOARD OF MANAGEMENT

Peter Leonard-Kanevsky

Jesse D. Malone

David L.Eisum President

Carll Stevenson

Ja.ne M. Harvey

John W. Mathie

The Hon Robert A. Jolly, M.P., The Treasurer, I Treasury Place, MELBOURNE 3002

Sir,

Annual Report 1985-86

35 Spring Street, MELBOURNE 3000 Telephone: 651 3222 2 February 1987

In accordance with the provisions of Section 63 of the Superannuation Act 1958, and Section 10 of the Pensions Supplementation Act 1966, the Board submits to you for presentation to Parliament its Report on the administration of both acts for year ended 30 June 1986, together with financial statements for that year.

The Board is also responsible for the Superannuation Lump Sum Fund and includes details on the Fund's operation. Entry to this Fund ceased on I July 1984.

Yours faithfully,

~~fl~s~)r~~ l'<~id<m Mo""~ ~ M~bo'

------'""""' J.W. Mathie, Member (Elected)

?~~-~6~,~ Member (Elected) Member (Elected)

3

CONTENTS

INTRODUCfiON AND SCHEME OUTLINE ORGANISATION AND FUNCfiON FUND OPERATIONS-ADMINISTRATION

FUND OPERATIONS-FINANCIAL

Balance Sheet Income and Expenditure Statement Sources and Applications of Funds

Notes to Accounts INVESTMENTS

ACfUARY'S REPORT PENSIONS SUPPLEMENTATION FUND REPORT SUPERANNUATION LUMP SUM FUND REPORT APPENDICES

Page

7-9 10-11 12-19 20-21

22 23 24

25-31 32-33 34-36 37-39 40-45 46-50

COVER: ''Superanruu:Jtion Spans the Thars.' 'As well as aged retirees the Board has a number of children receiving a pension benefit.

5

INTRODUCTION AND SCHEME OUTLINE

The State Superannuation Board of Victoria came into existence in 1925 as an incorporated body. Today, it operates under the Superannuation Act 1958 with a Board of Management consisting of six members-three appointed by the Government and three elected by contributors, the latter three for a term of five years.

The State Superannuation Fund is a scheme provided for permanent staff of the Public Service, the Teaching Service, the Police Force, the State Transport Authority (Railways) and participating statutory authorities. Currently the net assets of the Fund exceed $1,100 million. (Details on membership and fund growth are contained in the Appendices).

The State Fund is the largest public sector superannuation scheme in Victoria having some 50% of the total public sector membership of 200,000. While there are some 42 separate schemes, the largest ten of these account for 95% of total membership.

Briefly stated the major provisions of the scheme are as follows:

I. A basic pension on retirement subject to full benefits classification and 30 years recognised service, for disability, or at age 65, of 70% of salary at retirement;

2. On age retirement before age 65, but after age 55, the pension reduces on a pro-rata basis;

3. Officers' compulsory contributions limited to a maximum of 9% of salary;

4. Surviving spouse pensions at the rate of two-thirds of officers' pensions;

5. Right to convert part of the pension into a lump sum in respect of age retirement or spouse benefit; and

6. Entry to the fund is subject to medical examination and classification by the Board.

The Year in Brief

• Optional early retirement benefits, from age 55, introduced (age 50 for police).

• Lump sum pension conversion entitlements increased from 30% to 50%.

• New wider definition of "disability" introduced.

• Improved preservation entitlements for resignation after 50.

• Recognition of medical classification on transfer from Funds approved by the Treasurer.

• The total number of contributors increased by only 0.3% to 101,271.

• The total number of pensioners increased by 4.7% to 32,919.

• Of the former contributors receiving pensions, the largest group (26%) were within the range of $!0,000 to $15,000 per annum.

• Earning rate on investments increased from 13.6% to 14.4% This rate is calculated on face value of investments and does not include market fluctuations or revaluation of assets.

Board of Management

The Board of Management is constituted under Section 49 of the Superannuation Act 1958 and consists of six members. Three are appointed by the Government and three are elected by contributors, all for a term of up to five years.

Mr David L Elsum, B Eng (Eiec) (Hons), B Comm, MSc, FASA, was appointed to the office of President of the Board for a tenn of three years ending 24 March 1989.

Mr Carl J Stevenson, FIA, FIAA, BSc, General Manager of the Motor Accidents Board and Mrs Jane M Harvey, B Comm, ACA, MBA, Acting Director Financial Policy and Operations, Department of Management and Budget were also appointed for the same term.

As a result of elections held in late 1985 the following were appointed as contributor representatives for a term of five years ending 23 December 1990:

Mr Peter Leonard-Kanevsky, TPTC, Cert A, representing contributors employed in the Teaching Service, Mr John W Mathie, representing those employed in the State Transport Authority, and Mr Jesse D Malone, representing all other contributors.

The Board meets monthly and at all meetings the General Manager and Secretary are in attendance. Other managers and consultants attend when required during that part of the meeting relevant to their responsibilities.

7

Acknowledgement

The Board places on record its appreciation of the service given during their time as members of the Board by Mr J M Ryder and Mr G P Ballard.

Mr Ryder was a member of the Board from December 1975 to December 1985 and Chairman from 21 December 1982 to 23 December 1985. During this time he contributed to the Board's deliberations and in particular as Consultant Actuary advised the Board on actuarial matters.

Mr Ballard, who was a member of the Board from July 1982 to December 1985, contributed greatly to the investment programme of the Board within the provisions of the legislation. He was responsible for the Board taking a more pro-active role in the fixed interest area and in particular, investments in New Zealand Government Stock.

The Board also thanks the members of staff for their assistance and dedication during the year which has not been an easy one having regard to the legislative changes and the procedures which resulted from it. A particular word of thanks is extended to Mr Ted Doh who retired in February 1986 after being the Board's Accountant and Investments Officer for nearly 20 years.

Empl9ying Authorities

The Board has received from the majority of employing authorities co-operation during the year. However, a small number of authorities continue to lodge returns late thus causing administrative delays and payment of interest by the Board.

General Information

• Declaration of Pecuniary Interest

Members of the Board including the General Manager have completed the required declarations which are held by the Treasurer.

• Senior Officers of the Board are:

MS Hastie R Aspinall Dip Bus Stud (EDP), AACS S G Belcher B Comm, AASA, CPA

General Manager Manager EDP Manager Operations

R D Collins AASA, CPA R Imison P J Glennie A Coghlan BA, LLB I S Boyd MBA, BEe, AASA, CPA J Fazio AASA, CPA

• Professional Advisers

Actuaries (Triennial Investigation) Consultant Actuaries (Medical)

Legal

Auditor Auditor (Property) Medical (Consultant) Medical (Freedom of Information)

• Publications

Manager, Management Services Property Manager Secretary Solicitor Senior Internal Auditor Manager, Fixed Interest Securities

J M Ryder, FIA, FIAA, FSS, ASA, Government Actuary J M Anderson, FIA, FIAA, ASA A L Truslove, BESc (Hons) PHD, AlA, FIA Crown Solicitor's Office Price, Brent & MacPherson Auditor-General Duesburys W C Heath, MBBS, FRACP W White, MBBS, DPM, FRANZCP, MRC, Psych

Superannuation Manual (Salaries and Personnel Officers) (Major up-date April 1986) Brochure-Summary of Rights and Entitlements (January 1985) Brochure-Age 55 Retirement (December 1985) Report to Members (May 1986)

Administration of Other Superannuation Funds

The Board is responsible for the administration of the Pensions Supplementation Fund, the Superannuation Lump Sum Fund, the Parliamentary Contributory Superannuation Fund, the State Superannuation Board Employees Benefits Fund and the Holmesglen Construction Superannuation Plan. It is responsible under direction for the administration of the Coal Mine Workers' pension scheme and the Coal Miners Accident Relief Payments. The Board is also responsible under direction for payments authorised under the fOllowing Acts: Superannuation Benefits Act 1977, Section 9(2) of the Ombudsman Act 1973, and the Constitution (Governor's Pension) Act 1978.

8

In addition, the Board provides the following pension services for pensions and allowances paid by the Government although it is not responsible for the administrative arrangements:

- Additions to pensions payable pursuant to Act No. 3408 Section 36 - To supplement annual subsidy to the Royal Mint

Allowances to sufferers of Miners' Phthisis Allowances to ex-members and dependants of the Police Force

- Judges-Supreme and County Courts - Chairman-General Sessions

The Mint Casual Fire Fighters Compensation Fund

- Police Pensions Fund - Port Philip Pilot Sick and Superannuation Fund

Triennial Investigation

The report (Part l) of the consulting actuaries of the investigation of the Fund as at 30 June 1983 was received in September 1985. This report has been printed and is available to the public. The report discloses a surplus of $129.8 million. The actuaries have certified that the surplus is sufficient to pay increases of benefit under the Pensions Supplementation Act until receipt of the next report. The Board agreed that as a result of the changes in benefits included in the 1985 Amendments, Part 2 of the report need not be completed due to the imminent requirement for a further report as at June 1986 which will include these changes.

9

ORGANISATION CHARI'

B I

General Manager

Internal Executive

I Audit Support

EDP Section

J I _1 I

! Data Data Base Systems & Preparation Unit Maintenance

Unit Unit

Management Services Section

I I I

Personnel I Finance I & Office & Accounts

i Services Unit J Unit

_I Investments

I Section

I 1 l ! Property

I Housing Fixed

I Unit

I Loans Interest Unit Unit

Operations

I Section

I I I I

Fund I Medicals & Member Membership Rehabilitation Services

Unit Unit Unit

10

OBJECTIVES, ORGANISATION AND FUNCTION

The SuperonnUJJtion Schemes Amendment Act 1985 provided objectives and duties for the Board from I January 1986. These are shown below in full:

(I) "The following are the objectives of the Board.

(a) To collect contributions under this Act;

(b) To manage and invest the Fund in such manner as to maximize the return earned on tbe Fund, having regard to-

(i) the need to make provision for payments out of the Fund under this Act; and

(ii) the need to exercise reasonable care and prudence in order to maintain the integrity of the Fund;

(c) To administer the payment of benefits under this Act having due regard to the need for equity among contributors and pensioners.

(2) lt is the duty of the Board to-

( a) establish policies in respect of the administration of this Act and the investment of money standing to the credit of the Fund and to adopt strategies designed to achieve those policies;

(b) determine, authorize or approve programmes for the administration of this Act and the investment of money standing to the credit of the Fund;

(c) ensure that the decisions and operations of the Board are directed towards achieving its objectives;

(d) ensure that the Board has, or has access to, the skills, facilities and resources required to achieve its objectives;

(e) subject to sub-section (3), inform contributors about the management and investment of the Fund including making available to contributors at least once in each year a summary of information relating to the management and investment of the Fund;

(f) subject to sub-section (3), liaise with relevant industrial organizations concerning the interests of contributors and inform those organizations about the management and investment of the Fund;

(g) ensure that the Board conducts its operations in an efficient manner.

(3) The Board must, in performing its duties under paragraphs (e) and (f) of sub-section (2) have regard to the need to protect information the disclosure of which could adversely affect the financial position or the commercial or other operations of the Board.

(4) If the Treasurer at any time gives to the President a statement of Government policy on any matter that is relevant to the performance of the duties of the Board, together with a request that the Board consider that policy in the performance of its duties, the Board must ensure that consideration is given to that policy.

(5) If the Treasurer gives a statement to the President under sub-section (4), the Board must publish that statement in its next annual report." No statements were given during the year.

Corporate Plan

The Board accepted a draft corporate plan during the period under review. This plan has been implemented and is currently under review to take into account change in legislation and conditions.

Stamng Arrangements

Implementation of the recommendations contained in tbe management review team's report of February 1984 have now largely been completed. Tbe final stage of the review process will illVOlve conducting a 1\)st Implementation Review, which will examine the effectiveness of the initial review and allow the opportunity to fine tune any factors affecting the organisation's operational efficiency.

11

FUND OPERATIONS-ADMINISTRATION Legislation

The Superannuation Schemes Amendment Act 1985 became operative from I January 1986 with the exception of Section 3(ld) which dealt with rights of contributors employed in TAPE colleges and Section 32B which enabled increases in pension supplementation to be converted to lump sum in certain circumstances. The legislation in principal dealt with two areas, optional early retirement and administration.

(a) Optional Early Retirement

The legislation provided that contributors may now retire on or after attaining age 55, with police officers having this right from age 50. This option was introduced as part of the Government's Youth Employment Scheme. Conversion of pension to a lump sum on age retirement was increased from 30% to 50%. Rights were also given for contributors to convert part of future spouse benefit. If this right is exercised, payment of the additional lump sum is ntade, at the date of conversion, by the Consolidated Fund. Provision was ntade for the payment of deferred benefits from age 55 to any person resigning after the effective date of the legislation who had completed 15 years recognised service for superannuation purposes and had attained age 50.

{b) Administration

A number of definitions including that of "actuary" and "disability" were included in the legislation.

Provision was made for the Fund to pay the employer cost of pension benefit in respect of former officers of the Board who retired on or after I July 1981, the date on which the Board became responsible for its own administration costs.

Investment powers were altered to provide that the Board could make investment in mortgages on property outside Victoria which constituted a principle home of a contributor.

A requirement was inserted in the legislation for the Actuarial Investigation Report to be tabled within 12 months of the due date.

The Board was given discretion to accept retirement or death on the grounds of traumatic bodily injury for periods beyond the previous 6 months limitation.

It was agreed that the Reserve Unit Account be wound up with contributors' equities being refunded to them. This decision was taken as the benefit of reserve units disappeared in 1975 when normal contributions were limited to 9 % of salary.

A provision was introduced to accept transfers from superannuation funds approved by the Treasurer with recognition of medical classification held in the previous funds. Such provisions are accepted where a refund is paid to the State Superannuation Fund or a preserved pension is accepted by the contributor from the previous scheme.

The Act provides that where payments are made to dependant persons, children's benefits are paid at the normal rate not at the "double orphan" rate.

As a result of complaints to the Ombudsman provision was ntade that interest is to be paid where payment of benefits is delayed for a period in excess of 2 months.

The provision for consideration of gainful employment was amended to enable the Board to reduce pension where a person was gainfully employed instead of being, as previously required, fit for gainful employment.

Litigation.

The Board has a Solicitor who provides a range of legal services to the Board and its staff.

These services include advice to the Board on matters involving statutory interpretation, particularly relating to the Superannuation Act and other acts administered by the Board, the conduct of conveyancing work associated with housing loans granted to contributors and the conduct of legal actions for and on behalf of the Board.

During the year three cases were heard in the County Court. The first involved a disability pensioner who appealed against the Board's determination to reduce his pension to nil on the basis that he was capable of gainful employment. His appeal was allowed and pension increased to 15%. The basis of the decision was that there was no power to reduce the pension to nil. The Act has since been amended and the Board now has power to continue, increase, reduce or suspend pension, when a pensioner is gainfully employed.

The second involved a former full-benefits contributor who retired prematurely on account of disability. The Board in exercise of its powers under the Act reclassified him as a limited benefits contributor with retrospective effect on the grounds of failure to fully and honestly disclose infbrntation relevant to his classification. The contributor appealed against the Board decision. This appeal was by way of Ordinary Summons rather than by Notice of Appeal as had always been the case. The procedural question was finally determined by the Full Supreme Court and all appeals are now to be commenced by way of summons. In the substantive action the plaintiff/contributor withdrew his action.

12

The final case involved a contributor appealing against the Board's determination that he could not retire on the grounds of disability. His appeal was upheld on the medical evidence produced in Court by the contributor.

Freedom of Information

During the year 864 new requests were received plus a further 3 on transfer from other agencies. Final decisions were made on 855 of the requests with 2 internal reviews later conducted by the Principal Officer. There were no cases determined by the Administrative Appeals Tribunal.

787 were granted in full 52 were granted in part 11 were refused 2 were transferred in full 3 were tranferred in part

12 were carried over to the next year.

The vast increase in requests was largely due to the Supreme Court judgment handed down on 26 June 1985, on the Board's appeal against two County Court decisions that medical reports should be released to a pensioner and to a contributor (Booth/O'Connor).

Of the total requests, some 250 were identified as coming from contributors and pensioners who had been awaiting the judgment and many of the others were generated by the publicity provided by the press and the Board following the decision. Approximately 60% of requests for the year were specifically for medical reports with a further 35% of applicants requesting either the full client file or documents relative to their classification.

Towards the end of the reporting period, requests were being r~ceived at the rate of 50 per month and being processed within an average time of 3 weeks.

The high volume of requests is significant when compared to the Australian Government Fund (AGRBO) where the majority of requests are also for medical reports. That fund which has a membership of approximately three times that of the State Superannuation Board received 258 requests for 1984-85. At the time of writing the Board had agreed to provide reasons for classification to contributors medically examined after 1 April 1985. The reason for this date is that relevant records are readily available. The statement of reasons will be provided upon written request to the Medical Services Unit as an administrative process apart from the FOI Act. It is expected that this process will lead to some reduction in the number of FOI requests for the following year.

The Medical Unit conducted 7,286 initial medical examinations for the year and 2,152 of these contributors were classified as limited or service benefits contributors. Understandably, few of these have an appreciation of the actuarial principles which apply to the insurance industry. particularly for this fund which has an extremely high incidence of disability and which rates contributors by risk of disability rather than by risk of death. This together with a lack of knowledge of the purpose of the medical review process has had a significant bearing on why the number of requests remains extremely high.

Increased efforts will therefore be necessary in the future to publicise the Board's activities to its membership, particularly in the area of medical examination, review and determination of classification.

Personnel Function:

(a) Delegation of Personnel Powers-

The Department of Management and Budget is currently in the process of devolving the Personnel function to its larger branches. The Board has now accepted Chief Administrator Delegations in respect to Personnel Services matters. Base grade Recruitment and Organisation and Classification matters will be accepted when the appropriate approvals have been obtained. These delegations will enable the provision of a more efficient personnel function for management and staff of the Board.

(b) Staff Training and Development-

The Board is in the process of recruiting a Human Resource Development Officer. This officer will provide a comprehensive program -Jf staff training and development activities. These programs will be designed to enhance and develop skills in areas such as supervision and management and to itnprove staff morale and career opportunities.

(c) Co-operative Student Programs-

The Board continues to recruit students from tertiary colleges and institutions for the purpose of allowing them the opportunity to receive appropriate work experience in relation to their course of study.

(d) Youth Guarantee-

The Board is a participant in the government's Youth Guarantee Scheme, whereby disadvantaged young people are given job opportunities, in conjunction with TAFE training, for a twelve month period. Upon successful completion of the twelve month training period they are eligible for appointment to permanent, full time positions within the Board.

13

Occupational Health and Safety

During the course of the year ergonomically designed furniture was provided for all operators using word processing equipment.

Data entry staff have undergone eye tests at the Occupational Medicine Unit in order to check and monitor their eye sight and all keyboard staff are encouraged to take the recommended rest breaks.

Office Automation

Word processing facilities have been introduced to the Board and development has commenced in the following areas:

(a) Records management;

(b) Stores;

(c) Time recording; and

(d) Personal Computing.

Electronic Data Processing

General

During the financial year the Board maintained its commitment towards Data Processing to ensure it maintained an effective and efficient contribution towards meeting the organisations objectives.

In the last quarter of 1985 computer hardware was upgraded by installing additional disk storage and a more powerful processor to allow users more efficient access to data held on the computer. Throughout the year additional terminals were installed. Database software was also upgraded in the first quarter of 1986 in order to maximise efficiencies in the development of new systems.

Pension System

In January 1986 the Board implemented a new system to provide online access to pension data. This system interfaces with the Pensions payment system and extracts the latest possible data available about pensioners. Staff are therefore able to submit enquiries to obtain accurate up to date infurmation to answer queries, supply infurmation to pensioners as requested, and to satisfy internal decision making.

At a later date, this system will be extended to include an update service allowing users to make immediate changes to pension data when and as required.

Contribution Processing Systems

Existing systems supporting the collection of superannuation contributions and reconciliation continued to run satisfactorily.

Earlier in the period a project team was fOrmed to investigate and implement major modifications resulting from both legislative changes and user requested enhancements.

The modifications include leave without pay, permanent part-time, calculation of contributions since 1.7.83 (fOr tax purposes) and calculation of age 55 retirement benefits.

These areas require greater modifications to existing systems than was first anticipated, as they effect not only Board systems but those of other government departments.

The project team has completed investigation and specification of required changes and is presently proceeding with their implementation.

Staff Appointments

Difficulty in obtaining suitably qualified and experienced data processing staff continued throughout the first two quarters despite extensive advertising and interviewing. Only in the third quarter was the Board able to fill all vacant positions in both the systems development and operations sections.

The above delay has restricted the organisations ability to reach full operational status within the EDP Section and has caused some delay in the implementation of certain user requested changes.

Despite resource difficulties the Board has continued to develop systems and sub-systems which improve service to members.

EDP Staff Training

As data processing employment demands considerable training and experience an ongoing training program has been implemented to assist staff in maintaining a high level of Board requirement and data processing knowledge and experience.

14

As no one resource can provide for all training requirements, the program utilises various methods including audio visual courses, seminars and external courses in accordance with the skills required of staff.

The main aim of the program is to broaden data processing knowledge and to enable staff to introduce new EDP techniques for assisting the Board in delivering a timely and efficient service.

Ex.isting Systems and Maintei'Ulnce

All production systems have continued to operate reliably and consistently, however certain systems have required a degree of maintenance. This has involved both emergency and planned maintenance together with implementing enhancements to increase or extend the usefulness of existing systems.

Many of the resources used in this area have also been allocated to satisfying user requests for information not normally produced. It is the intention of the Board to provide education to users in order that they are able to use data processing facilities to access computer files and to satisfy their own information needs.

Strategic Planning

Since the last major planning exercise undertaken in 1983, changes in the EDP plan have resulted from the interplay of several basic planning elements. These include changes in Board policy and philosophy, legislation changes and changes in the business environment in which EDP must operate. Recognising that past plans did not necessarily reflect current Board strategies, the EDP plan was updated during the last quarter to more accurately identify priorities for implementation and resource allocation.

Internal Audit and Review

The Board established a multi-disciplinary Internal Audit and Review function during the year to provide senior line management with authoritative advice on policy options to ensure that the Board is effectively managing its resources, that information systems are reliable, that the risk of fraud is minimized and the Board's objectives are achieved.

A comprehensive Internal Audit Strategic Plan and Prognunme covering financial, operational and organisational internal control systems on a cyclical basis has commenced.

Medical Examinations and Classifications

Initial Ex.amii'Ultions

Initial Examinations are generally conducted at the Board's office, the Government Medical Office, State Transport Authority or at other locations as determined by the number of requests at hand. The purpose of the examination is to determine fitness for permanency when this is required by the employing authority and to assist in determining the examinee's benefit classification.

Review Ex.amii'Ultions

Contributors who are assessed as having an increased disability risk of retiring on account of disability prior to reaching the normal age for retirement are classified as Limited or Service Benefits Contributors.

The Board has changed its policy in relation to the review of medical classification of these contributors. The practice has been to automatically review the classification within one year of the initial classfication being determined. These contributors will now be offered a review examination at the time recommended by the Actuary. In many cases the review will not take place until a later year, depending on the nature of any medical conditions which have been noted. The revised practice is expected to result in savings to the Fund whilst also meeting the needs of the contributors concerned.

A Total of 2,115 review examinations were conducted for the year.

Classification

As part of the assessment process the Consultant Actuaries required additional information in 39% of cases. This information was either by way of an additional medical report from the private medical practitioner, obtained with the consent of the contributor, or a special questionnaire completed by the contributor in respect of a specific illness or complaint.

The Consultant Actuary is responsible for assessing review medical examinations, but assessing of initial medical examinations is by the Board's Assessing staff under the co-ordination of the Office of the Government Statist and Actuary.

IS

Classifications Determined (Initial Examinations) 1985-86

Employing Authority Full Limited Service

No % No % No %

Education 1942 74 358 14 319 12

State Transport Authority(Railways) 368 62 112 19 113 19

Police 472 93 26 5 ll 2

All Other Departments 2352 66 584 16 629 18

Total 5134 70 1080 15 1072 15

CLASSIFICATIONS DETERMINED (INITIAL EXAMINATIONS) 1982-1986

FULL 5889 73%

1981-82

SERVICE 1692 16%

FULL 6799 66%

1982-83

Appeals Against Medical Classification

SERVICE 1373 17%

FULL 5170 65%

1983-84

FULL 5235 70%

1984-85

FULL 5134 70%

1985-86

Total

No

2619

593

509

3565

7286

Section 68A of the Act provides that a contributor who is dissatisfied with the determination of his or her medical classification may on payment of$25 require the Board to refer the question of classification to a review panel consisting of a member of the Board appointed by the Board, an independent actuary and an independent legally qualified medical practitioner both mutually agreed upon, or in default of agreement appointed by the Treasurer.

16

The Review Panel examines the evidence upon which the Board classified or reclassified the contributor and determines the medical classification.

Where the determination of the Board is varied by the review panel, the fee paid by the contributor is refunded.

The panel met eight times during the year and made determinations on twenty-two cases of which thirteen were from limited benefit contributors and nine from service benefit contributors.

No service benefit contributor was raised to either limited or full benefits. Of the thirteen limited benefit contributors four of the appellants were raised to full benefits and one was lowered to service benefits.

One decision of the Review Panel to raise a contributors classification to full benefits effectively changed existing Board policy in respect of blind persons who are contributors to the Fund. Where a blind contributor can demonstrate a consistently and significantly better than average sick leave record and suffers no other disablity, full benefit classsification may be provided.

There were no appeals to the County Court against medical classifications.

Fund Membership Records

The Board's efforts to include membership records in its data base system were hampered during the past year as a result of loss of experienced staff to other areas of the administration. At the close of the year some 80,000 members' records were in the data base system and work was continuing on the remaining 21 ,000 members' records for the purpose of preparing them for inclusion in the system.

Member Services

The introduction of provisions which enable retirements to take place at any time after a contributor reaches the age of 55 (or 50 in the case of police officers) has resulted in a sharp increase in age retirements since the provisions became effective on l January 1986. The opportunity for contributors to commute up to 50% of their pension entitlements to a lump sum (previously the limit was 30%) has had further impact on the level of retirements. The upshot has been that age retirements in the six months to 30 June 1986 were up by some 99% over those for the corresponding period last year.

The Board appointed two additional field officers during the year with the intention of stepping up its field services. However, faced with the large increase in age retirements the field officers have been mainly used to conduct pre-retirement interviews.

As a result of large numbers of contributors electing to retire on or about the same date the Board has not been able to pay benefits within the normal period of2-3 weeks after the final date of service for much of 1986. However all payments have been made within 2 months and accordingly the Fund has not been required to pay interest. Action is being taken to reduce delays where possible, however the Board is not able, nor does it consider it justified, to provide a permanent staff structure to meet peak work loads instead of normal loads.

For the purpose of advising members of the details of the new provisions relating to early retirement and commutation of pensions the Board produced an explanatory brochure and conducted a series of public seminars in Melbourne and in a number of regional centres.

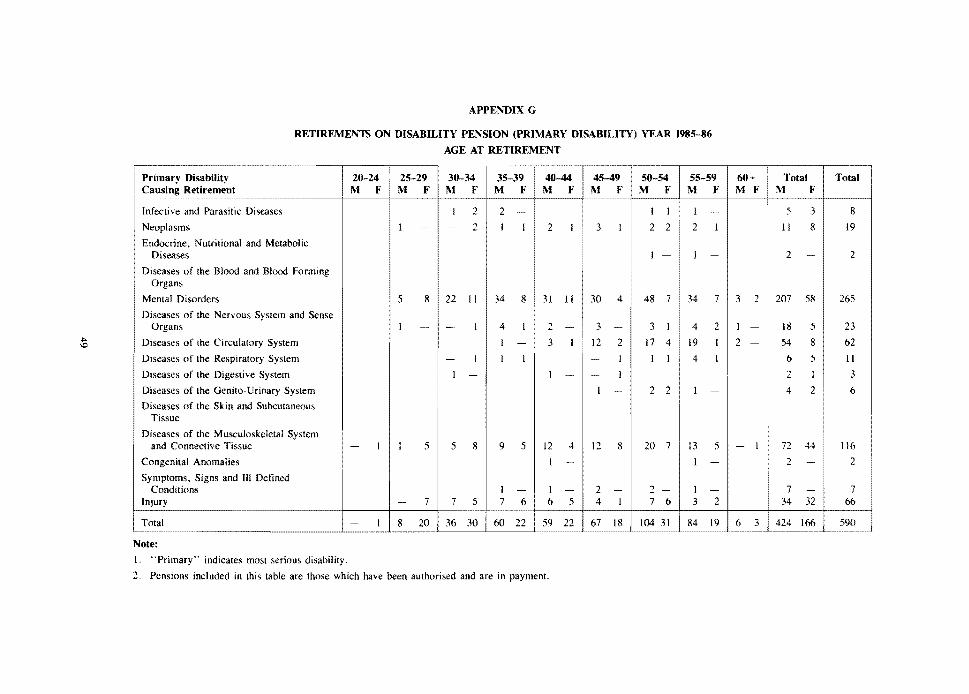

Disability Retirements

During the course of the year 672 contributors retired on account of disability of whom 590 received pensions and 82 received lump sum payments. The number of new disability pensions granted represents 29% of retirements on pension for the year. For the previous year the corresponding figure was 36% . The significant decrease was due to the effect of early retirement provisions which were introduced in January 1986.

The following table provides a break-down on disability retirement pensions for the four employing authorities plus the miscellaneous authorities:

Employing Authority

Education

State Transport Authority

Police (Force)

Public Service Board

Miscellaneous Authorities

The Fund

17

Pensions

179

86

81

202

42

590

Pensions Granted per Thousand Contributors

4.1

7.3

9.4

7.8

3.6

5.8

Average age of officers was 46 years, with the greatest frequency group being 55-59 years:

Average Greatest Frequency Employing Authority Age (yrs) Group (yrs incl)

Education 45 55 to 59 State Transport Authority 49 55 to 59

Police (Force) 42 35 to 39

Public Service Board 48 55 to 59 Miscellaneous Authorities 51 55 to 59

The Fund 46 SS to 59

Average length of contributory service was 16 years, with the greatest frequency group being 5 to 9 years:

Average Greatest Frequency Employing Authority Service (yrs) Group (yrs incl)

Education 16 5 to 9 State Transport Authority 22 25 to 29 Police (Force) 19 25 to 29 Public Service Board 12 5 to 9 Miscellaneous Authorities 16 5 to 9

The Fund 16 5 to 9

The primary (most serious) disability leading to retirement for each major employer is contained in the following table:

Employing Authority

Education

State Transport Authority

Police (Force)

Public Service Board

Miscellaneous Authorities

The Fund

Note: For full table see appendix G.

Disability pensions-by classification

Education

State Transport Authority

Police (Force)

Public Service Board

Miscellaneous Authorities

Total

Mental Disorders

%

56 24

58 38 45

45

18

Musculo.

%

12

26 15 25 24

19

Full

165

83

79

163 39

529

Circul. Other

% %

7 25

15 35 12 15 12 25 10 21

11 25

Limited Total

14 179

3 86

2 81 39 202 3 42

61 590

6.5

6.0

5.5 -

5.0 11 I'T/7-78 1'178-79

DISABILITY PENSIONS GRANTED EACH YEAR -PER mOUSAND CONTRIBUTORS

,--

~-

,--

,---

~

-

r--

1979-80 1980-81 1981-82 1982-83 1983-84 1984-85 1985-86

The Board has appointed an officer to work in close co-operation with employing authorities to facilitate the re-employment of disabled members. This appointment is one of several made by the Board during the year for the purpose of strengthening the Board's work in relation to the review of disabled members.

The legislative amendments introduced in December 1985 also included a new definition of "disability" with the aim of making it easier to re-employ contributors who might be regarded as being unfit to carry out their accustomed duties but who would be fit for alternative duties. The change has not so far had the desired impact of reducing the incidence of disability retirement but there has been some improvement in the rate of disability pensioners returning to work. The Board is seeking the co-operation of employing authorities in its endeavours to efficiently administer the disability retirement provisions. Without that co-operation the rate of disability retirement is likely to remain unacceptably high.

Fund Membership

There were IOI,Z7l officers contributing on 30 June 1986. This represents a 0.3% increase over the previous year.

Of these contributors there were 43,154 from the Teaching Service, ll,836 from the State Transport Authority (Railways). 8,592 from the Police Force and 25,967 from the Public Service Departments. The remaining ll,722 contributors were from the Government Authorities, Corporations, Boards, Colleges and Educational Institutions.

At 30 June 1986, there were a total of 32,919 pensions in force. This represents a 4.7% increase over the previous year. Of these pensions 15,783 were for officers who retired on account of age, 7,057 were disability retirements. 9,023 widows'/widowers' pensions were payable and 1.056 pensions were payable to children (including 201 pensions to full time students between the age of 18 and 25 years).

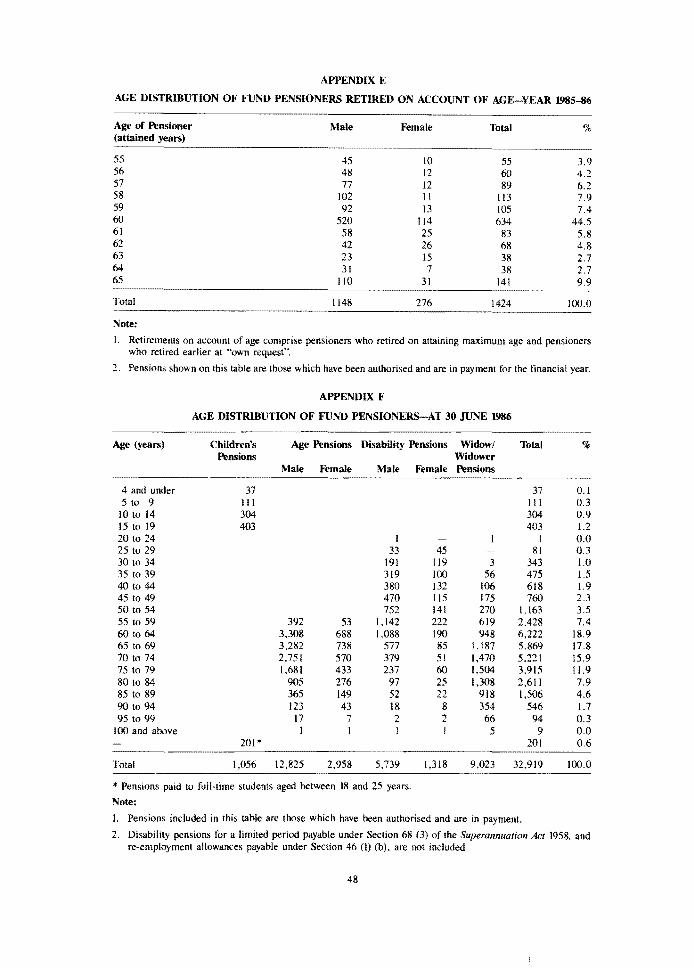

During the year the number of new pensions commenced for officers who retired between the age of 50 and 65 on account of age was 1,423 and the new pensions commenced in respect of contributors who retired on account of disability was 590. These totals represent 71% and 29% of retirements on pension during the year.

Of the officers who retired between the age of 50 and 65 on account of age, the most common age for retirement was at 60 years-44.5% of such retirements took place at this age. A further 29.6% of retirements were by officers aged 55 to 60 who took advantage of the new early retirement provisions.

Statistical information on Fund Membership may be found in the Appendices.

19

FUND OPERATIONS-FINANCIAL

Financial Results

The overall increase in the Fund for the year ended 30 June 1986 was $111.4 million compared to $172.7 million for 1984-85. This represents a 35.5% decrease in the total funds utilised by the Board over the previous year.

The introduction of optional early retirement and the increase from 30% to 50% of pension available for conversion to lump sum which eventuated in payment of increased benefits from the fund resulted in a slower growth of total investments excluding cash options.

Total investments rose by $156.7 million for the year to $1,062.4 million being an increase of 17.3% over the previous year.

The operation of the Fund for the year showed an aggregate revenue increase of$4.9 million to $413.8 million, an increase of 1.2% compared with 1984-85. Expenditure increased by $66.3 million to $302.4 million, an increase of 28.1% over the previous year. This resulted in the net revenue being increased by $111.4 million for the year.

Consolidated Revenue Share of Pension 38.6%

1UfAL INCOME 1985/86 $432.7m

100%

20

Employees' contributions 34.0%

Interest on Investments 27.4%

Pensions 55.5%

TOTAL EXPENDITURE 1985/86 $321.3m

100%

Net Loss on Cash Options 5.9%

21

Lump Sums and Cash Options 17.2%

Administration 3.6%

Transfers to Pension Supplementation 12.5%

THE SUPERANNUATION FUND BALANCE SHEET

AS AT 30 JUNE 1986

1986 1985 Note $'000 $'000

Members Equity Members Funds 1,234,024 1,122,581 Mortgage Reserve 2 2,638 2,433 Asset Revaluation Reserve 6(a) 93,654 23,039

1,330,316 1,148,053

Represented by:

Assets

Current Assets Cash at Bank (811) (113) Debtors 3 26,935 23,266 Benefits-Government Share Receivable 4 3,253 1,297 Contributions Due 5 605 643 Prepayments 270 220 Stores and Stationery 23 15

30,275 25,328

Investments 6 1,062,388 905,723

Non-Current Assets Cash Option Reimbursement 7 260,000 222,000 Office Furniture, Motor Vehicles & Equipment 8 451 359 Other Assets 9 2 3

260,453 222,362

Intangible Assets 10 1,516 1,737

Total Assets 1,354,632 1,155,150

Less: Liabilities

Current Liabilities Accounts Payable 2,045 1,530 Benefits Payable lOa 16,205 2,674 Provision for Annual Leave I 101 14

18,351 4,218

Deferred Liabilities Provision for Deferred Maintenance I 598 453 Reserve Unit Account 11 1,955 Provision for Long Service Leave I 562 471 Provision for Superannuation Liability (Employer) I 4,805

5.965 2,879

Total Liabilities 24,316 7,097

Net Assets 1,330,316 I, 148,053

The accompanying notes form part of these accounts.

22

THE SUPERANNUATION FUND INCOME AND EXPENDITURE STATEMENT

FOR THE YEAR ENDED 30 JUNE 1986

Note Income

Investment Income 12 Net Realised Gain (Loss) from sale of Investments 13

Realised Investment Income

Net Income on Cash Options

Total Income

Less: Operating expenses

Net Gain

Plus: Members Funds Opening Balance

Contributions Received from Members Consolidated Fund Share of Pensions

Less: Benefits Paid

Pensions Cash Options (Fund Share Only) Lump Sums Refund of Contributions Pension Supplementation Interest Allocated to Reserve Units

Members Funds Closing Balance

The accompanying notes form part of these accounts.

23

7

14

16

7 15

1986 1985 $'000 $'000

126,513 104,792 (7,853) 4,814

118,660 109,606

(18,853) 25,973

99,807 135,579

ll,722 5,789

88,085 129,790

1,122,581 949,878

147,201 135,645 166,802 137,705

314,003 273,350

178,354 157,364 34,879 13,996 20,482 5,412 16,905 16,419 39,942 37,103

83 143

290,645 230,437

1,234,024 1,122,581

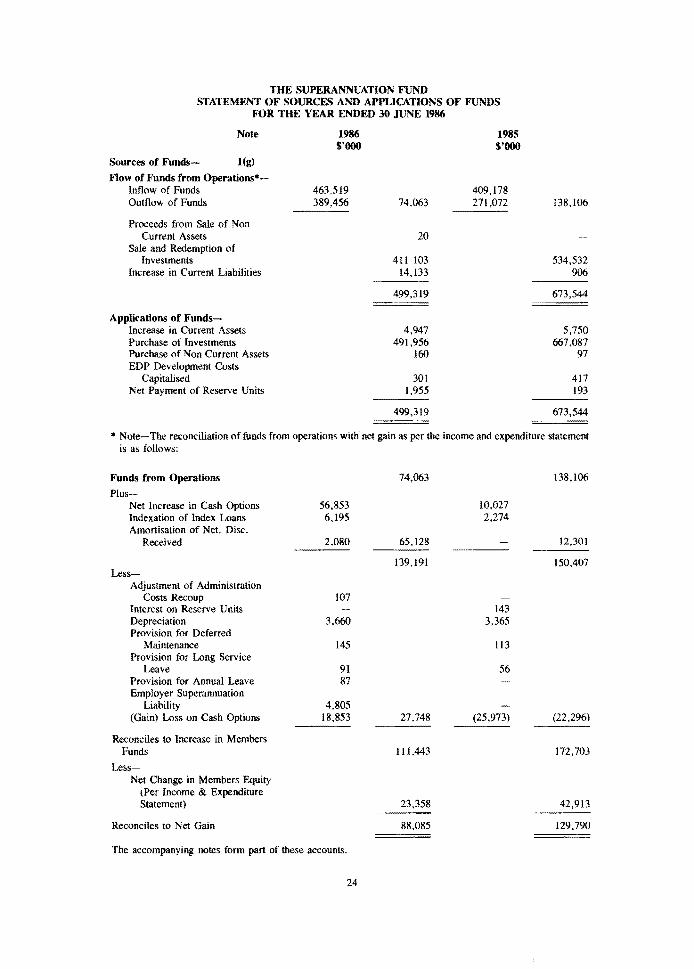

THE SUPERANNUATION FUND STATEMENT OF SOURCES AND APPLICATIONS OF FUNDS

FOR THE YEAR ENDED 30 JUNE 1986

Note

Sources of Funds- I {g)

Flow of Funds from Operations•Inflow of Funds Outflow of Funds

Proceeds from Sale of Non Current Assets

Sale and Redemption of Investments

Increase in Current Liabilities

Applications of Funds-Increase in Current Assets Purchase of Investments Purchase of Non Current Assets EDP Development Costs

Capitalised Net Payment of Reserve Units

1986 $'000

463,519 389,456 74,063

20

411 !03 14,133

499,319

4,947 491,956

160

301 1,955

499,319

1985 $'000

409,178 271,072 138,106

534,532 906

673,544

5,750 667,087

97

417 193

673,544

• Note-The reconciliation of funds from operations with net gain as per the income and expenditure statement is as follows:

Funds from Operations 74,063 138,106

Plus-Net Increase in Cash Options 56,853 I0,027 Indexation of Index Loans 6,I95 2,274 Amortisation of Net. Disc.

Received 2,080 65,128 12,301

139,191 150,407 Less-

Adjustment of Administration Costs Recoup !07

Interest on Reserve Units 143 Depreciation 3,660 3,365 Provision for Deferred

Maintenance 145 113 Provision for Long Service

Leave 91 56 Provision for Annual Leave 87 Employer Superannuation

Liability 4,805 (Gain) Loss on Cash Options 18,853 27,748 (25,973) (22,296)

Reconciles to Increase in Members Funds 111,443 172,703

Less-Net Change in Members Equity

(Per Income & Expenditure Statement) 23,358 42,913

Reconciles to Net Gain 88,085 129,790

The accompanying notes form part of these accounts.

24

SUPERANNUATION FUND NOTES TO AND FORMING PARr OF THE ACCOUNTS

1. Statement of Accounting Policies

(a) The Financial Statements have been prepared in accordance with the proposed Regulations for Public Sector Superannuation Schemes under the Annual Reporting Act

(b) These accounts have been prepared under the historical cost convention and have, except for certain assets which are included at valuation (refer Notes 6 and 7), not been adjusted to take account of the current cost of specific assets.

(c) Depreciation is provided on all fixed assets progressively over their usefullifes, using the straight line method. It is the Board's policy to amortise its EDP Development costs over five years.

(d) Long Service Leave. The provision for long service leave is in respect of all employees who had five (5) or more years of relevant service at balance date.

(e) Lease Agreement. The Board has financial lease agreements for the use of computer hardware and software. During the transition period allowed by Australian Accounting Standard 17, "Accounting for Leases", the Board has adopted a policy of treating all minimum lease payments as periodic expenses (refer Operating Expenses, Note 14).

(f) Provision for Deferred Maintenance is used for future contingent expenditure on maintenance of a major nature. No amount was written off against this provision during the year.

(g) Sources and Applications or Funds. The 1985-86 format of this Statement has been prepared to comply with Australian Accounting Standard AAS12 "Statement of Sources and Applications of Funds". The comparative figures have been amended to comply with this statement.

(h) The following items have been brought to account for the first time in 1985-86:

(i) Any discount or premium on the purchase of fixed interest securities have been amortised over the term of the security purchased using the present value method (refer Investments, Note 5 and Investment Income, Note 12).

(ii) Annual Leave Provision. In previous years, the annual leave provision was disclosed separately for property operations and included in accounts payable. The 1985-86 provisions is made for all employees and calculated on their outstanding entitlements at balance date.

(iii) Superannuation Liability Provision. This provision represents the liability of the Board fur the employer share of superannuation benefits payable to current and retired employees who are members of the State Superannuation Fund (refer Operating Expenses, Note 14).

2. Mortgage Reserve. Mortgagors granted housing or commercial loans are chal:ged a percentage of loans advanced which is credited to this reserve.

The reserve's purpose is to offSet any losses that the Board may incur in the event of foreclosures on these loans.

3. Debtors

1986 1985 $'000 $'000

Interest on Investments 26,838 23 077 Operating Debtors 97 189

26,935 23 266

4. Benefits-Government Share Receivable

1986 1985 $'000 $'000

Pensions 1,890 1,297 Conversion of Spouse's Pension 1,363

3,253 1,297

25

5. Contributions Due by Employee

Contributors Interest on Deferred contributions

6. Investments

Investments are valued at cost with the exception of:

1986 $'000

604 I

605

1985 $'000

642 I

643

(a) Land and Buildings which were revalued by J H Beckwith, Thomson, Maloney and Partners. and Richard Ellis Pty Ltd as at 30 June 1986.

It is the Board's policy to have its properties revalued at three yearly intervals, and the independent revaluation was adopted by the Board on 17 July 1986.

The next revaluation is due as at 30 June 1989.

(b) Indexed. Loans are at indexed value in accordance with the loan agreement. Indexation accounted for $6,194,760 of the year's increase in value and is included as income in Note 12.

1986 1985 $'000 $'000

Investments (at cost) Short Term Deposits 34,633 55,084

Fixed Interest Investments (at cost) Indexed Loans 88,759 61,062 Commonwealth Securities 8,238 35,595 New Zealand Securities 2,284 Semi-Government Securities 299,749 263,200 Local Government 53,346 55,317 Government Guaranteed Loans ll6,320 116,320 Transferable Deposits 8,920 6,049 Loans under Agreement 14,903 10,851 Commercial Mortgage Loans 170,551 134,915 Housing Mortgage Loans: Contributors 72,374 74,556

4,099 3,193 Joint Ventures 4 10 Accumulated Amortization of Net Discount Received 2,080

Total Investments (at cost) 876,260 816,152

Property Investments (at valuation) Land and Buildings (less Ace. Depreciation) 186.128 89,571

Total Investments 1,062,388 905,723

26

The comparative fuce values and market values for the fixed interest Government and Semi-Government loans are as follows. The market valuations have been estimaled by management in conjunction with appropriate investment brokers and consultants.

$'000 $'000 $'000 Cost Market Face

Value Value

Commonwealth Securities 8,238 8,226 8,000 New Zealand Securities 2,284 2,299 2,318 Semi-Government Securities 299,749 313,735 298,203 Local Government Securities 53,346 33,859 54,909 Government Guaranteed Loans 116,320 115,786 116,320 Transferable Deposits 8,920 9,476 9,450

488,857 483.381 489,200

7. Cash Option Reimbursement

Cash Options Reimbursement from Consolidaled Fund is an actuarial valuation representing the present value of future amounts receivable from the Consolidated Fund which reimburses on a fortnightly basis those pensions converted to a lump sum as if no conversion were made.

The Income on Cash Option is the imputed interest on the asset valuation of Cash Option Reimbursement calculated as follows:

1986 1985 $'000 $'000

Increase per Actuarial Valuation Closing Balance (per Actuarial Valuation) 260,000 222,000 Plus adjustment 17,000*

277,000 222,000

Less Opening Balance 212,000t 186,000

Increase 65,000 36.000

Increase per Payments made and Reimbursement received Total payments made 122,076 48,985 Less Board's share 34,879 13,996

87,197 34,989

Less Consolidated Fund Share (Reimbursement) 30,344 24,962

Increase 56,853 10,027

Income on Cash Options 8,147 25,973 Less adjustments 27,000*t

(18,853) 25,973

t The 1984-85 Actuarial Valuation of $222 million was based on inadequate data. The adjusted valuation is $212 million leading to a net adjustment of $10 million.

* In 1985-86 the Actuarial Valuation was provided in two parts. Valuation I, of$277 million, has been made on a basis consistent with prior years. Valuation 2, of$260 million, reflects more accurately the current experience of the State Superannuation Fund. Net adjustment $17 million.

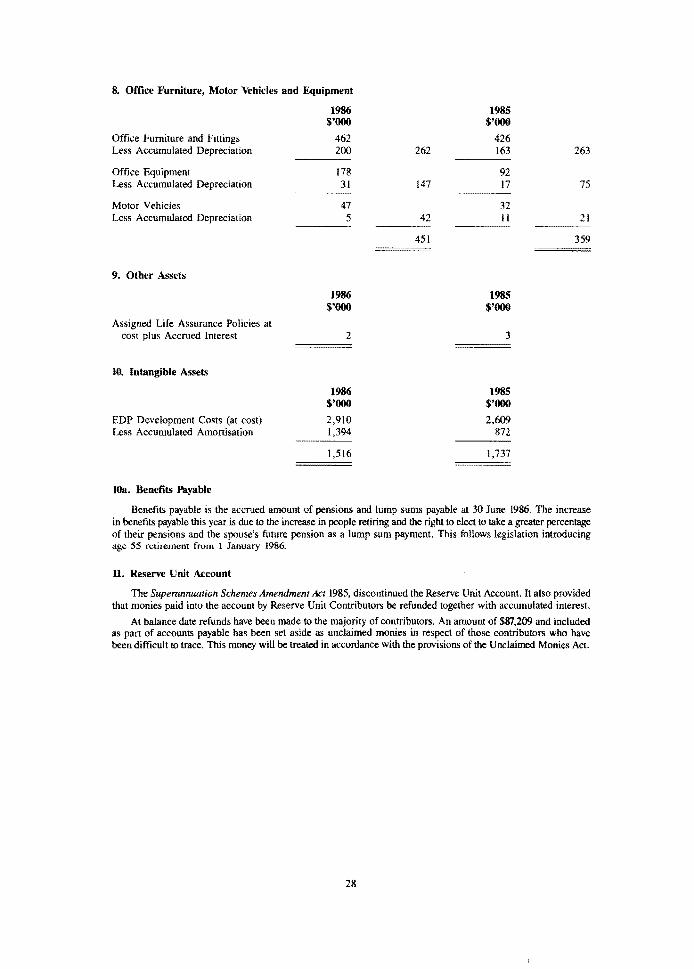

8. Office Furniture, Motor Vehicles and Equipment

Office Furniture and Fittings Less Accumulated Depreciation

Office Equipment Less Accumulated Depreciation

Motor Vehicles Less Accumulated Depreciation

9. Other Assets

Assigned Life Assurance Policies at cost plus Accrued Interest

10. Intangible Assets

EDP Development Costs (at cost) Less Accumulated Amortisation

lOa. Benefits Payable

1986 $'000

462 200

178 31

47 5

1986 $'000

2

1986 $'000

2,910 1,394

1,516

262

147

42

451

1985 $'000

426 163

92 17

32 11

1985 $'000

3

1985 $'000

2,609 872

1.737

263

75

21

359

Benefits payable is the accrued amount of pensions and lump sums payable at 30 June 1986. The increase in benefits payable this year is due to the increase in people retiring and the right to elect to take a greater percentage of their pensions and the spouse's future pension as a lump sum payment. This follows legislation introducing age 55 retirement from I January 1986.

11. Reserve Unit Account

The Supemnnuation Schemes Amendment Act 1985, discontinued the Reserve Unit Account. It also provided that monies paid into the account by Reserve Unit Contributors be refunded together with accumulated interest.

At balance date refunds have been made to the majority of contributors. An amount of $87,209 and included as pan of accounts payable has been set aside as unclaimed monies in respect of those contributors who have been difficult to trace. This money will be treated in accordance with the provisions of the Unclaimed Monies Act.

28

U. Investment Income

1986 $'000

Interest on Investments was derived from-Short Term Deposits and Bank

Accounts 7.402 Commonwealth Securities 521 Semi-Government Securities 43,023 Local Government Securities 4,059 Convertible Notes Government Guaranteed Loans 16,103 Transferable Deposits 1,149 Loans under Agreement 1,809 Commercial Mortgage Loans 22,210 Housing Mortgage Loans-

Contributors 10,377 Others 535

Indexed Loans (Interest plus Indexation) 8,588

Land and Buildings (Rent less Outgoings and Depreciation) 8,658

Interest on Life Assurance Policies Amortisation of Discount Received 2,080 P & L on Sale of Inv (Joint

Venture Inv) (l)

126,513

13. Net Realised Gain (Loss) from Sale of Investments

1986 $'000

Commonwealth Securities New Zealand Investments Exchange Rate Gain NZ

Investments Semi-Government Securities Local Government Securities Convertible Notes Indexed Loans Transferable Deposits

(1,765) 317

1,078 2,657 (181)

(9,959)

(7,853)

1985 $'000

2,036 l1,613 30,573 4,495

64 14,810

1,664 798

17,618

10,168 517

4,045

6,390 1

104,792

1985 $'000

933 1,762

2,560 (419)

(45)

23

4,814

It is Board policy to continue to actively engage in a switching operation in order to take advantage of rises or falls in interest rates.

Switches have been made on the basis of an increased yield together with recoupment of the loss of capital on realisation and a higher yielding income over the balance of the remaining term of the new security purchased.

29

14. Operating Expenses

The Management Account covers all costs of administering the Fund and consisted of:

1986 1985 $'000 $'000

Board Share of Staff Pensions 49 Board Members' Allowances 16 12 Salaries and Associated Items 3.285 2,503 Office Requisites 169 74 Post and Telephone 151 170 Medical Reports and Examinations 757 604 Office Accommodation 473 380 EDP Expenses 930 1,182 Depreciation and EDP Development Written Off 577 482 Long Service Leave 84 56 Annual Leave 83 Superannuation Liability 4,805 Incidental Expenses 460 453

11,839 5,916

Less: Recoup of Operating Expenses in administering other funds ( 117) (127)

----11,722 5,789

----

15. Lump sums were paid in respect of:

198() 1985 $'000 $'000

Service Benefit Contributors 1,248 849 Limited Contributors 142 41 Invalid Pensioners 1,049 1,129 Retrenched Contributors 306 427 Spouses of Deceased Contributors/Pensioners 4,286 2,966 Conversion of Spouse's Pension 13,451

20,482 5,412

16. The Consolidated Fund Share of Pensions covers pensions and lump sums. It does not include the Consolidated Fund Share of Pensions Supplementation which is included in the financial statements of the Pensions Supplementation Fund.

17. Contingent Liabilities exist in respect of an unascertained amount in unclaimed refunds of contributions to members who have left the fund.

18. Actuarial Investigation

An actuarial investigation as to the state and sufficiency of the Superannuation Fund was made as at 30 June 1983, by the joint Actuaries of the State Superannuation Board and revealed a surplus of $129.8 million. This has been used for updating pensions in accordance with the Pensions Supplementation Act. This report dated September 1985, stated "at present rates of interest, and with the existing contribution rates, the State Superannuation Fund is in a satisfactory financial state''.

The financial position of the Superannuation Fund as at 30 June 1986 has been subject to a preliminary actuarial valuation. It appears likely that sufficient surplus will be disclosed, on a basis consistent with current valuation practice, to meet the expected costs of pensions supplementation to at least 30 June 1987.

30

STATE SUPERANNUATION FUND STATEMENTS OF FINANCIAL ACCOUNTS

Statement on behalf of the Board Members

In the opinion of the State Superannuation Board the accompanying Balance Sheet, Income and Expenditure Statement, Statement of Sources and Applications of Funds and the notes to and forming part of the accounts are drawn up so as to present fairly the state of affairs of the Fund as at 30 June 1986 and of the results of the Fund. for the year then ended.

Dated this 12th day of December 1986

Statement by Principal Accounting Officer

DAVID L ELSUM President

I. R D Collins being the person in charge of the preparation of the accompanying financial statements of the Superannuation Fund for the year ended 30 June 1986 state that in my opinion such statements present fairly the results for the period and of the state of affairs of the Fund as at 30 June 1986.

Dated this 11th day of December 1986

Auditor-General's Report

R D COLLINS, AASA, CPA Manager

Management Services

The accompanying financial statements, comprising a Balance Sheet. Income and Expenditure Statement, Statement of Sources and Applications of Funds and the notes to and forming part of the accounts of the Superannuation Fund have been audited as required by the Supemnnuation Act 1958 and in accordance with Australian Auditing Standards.

In my opinion, the financial statement~ present fuirly the state of affairs of the Superannuation Fund as at 30 June 1986 and the results of its operations for the year ended on that date.

MELBOURNE R G HUMPHRY 3111/87 Auditor-Genera/

31

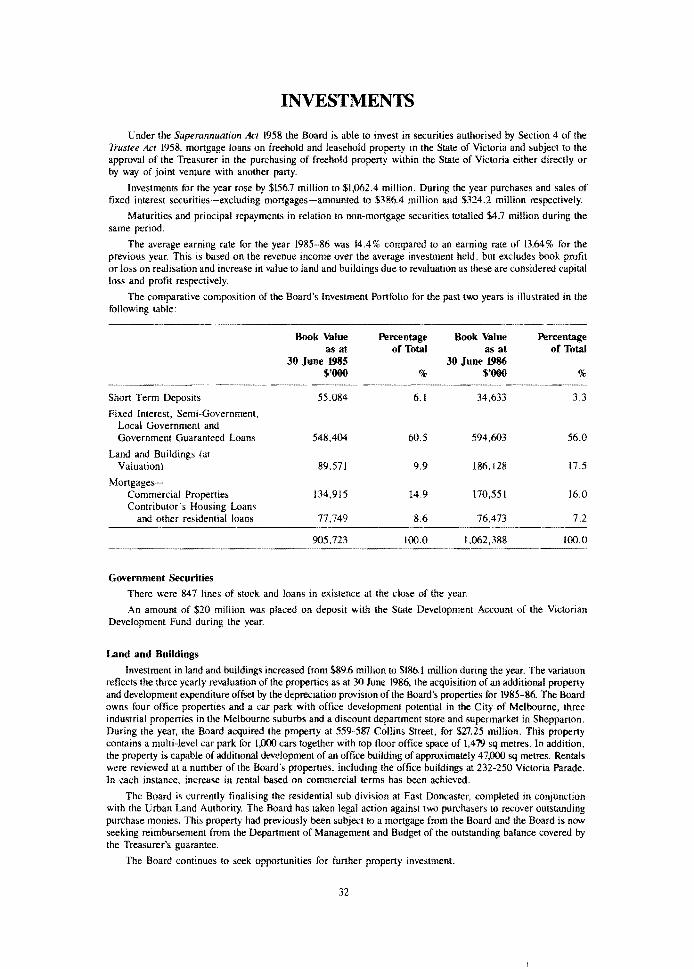

INVESTMENTS

Under the Superannuation Act 1958 the Board is able to invest in securities authorised by Section 4 of the Trustee Act 1958, mortgage loans on freehold and leasehold property in the State of Victoria and subject to the approval of the Treasurer in the purchasing of freehold property within the State of Victoria either directly or by way of joint venture with another party.

Investments for the year rose by $156.7 million to $1,062.4 million. During the year purchases and sales of fixed interest securities-excluding mortgages-amounted to $386.4 million and $324.2 million respectively.

Maturities and principal repayments in relation to non-mortgage securities totalled $4.7 million during the same period.

The average earning rate for the year 1985-86 was 14.4% compared to an earning rate of 13.64% for the previous year. This is based on the revenue income over the average investment held, but excludes book profit or loss on realisation and increase in value to land and buildings due to revaluation as these are considered capital loss and profit respectively.

The comparative composition of the Board's Investment Portfolio for the past two years is illustrated in the following table:

·---Book Value Percentage Book Value Percentage

as at of Total as at of Total 30 June 1985 30 June 1986

$'000 % $'000 %

Short Term Deposits 55.084 6.1 34,633 3.3

Fixed Interest, Semi-Government, Local Government and Government Guaranteed Loans 548,404 60.5 594,603 56.0

Land and Buildings (at Valuation) 89.571 9.9 186,128 17.5

Mortgages-Commercial Properties 134,915 14.9 170,551 16.0 Contributor's Housing Loans

and other residential loans 77,749 8.6 76,473 7.2

905,723 100.0 1.062,388 100.0

Government Securities

There were 84 7 lines of stock and loans in existence at the close of the year.

An amount of $20 million was placed on deposit with the State Development Account of the Victorian Development Fund during the year.

Land and Buildings

Investment in land and buildings increased from $89.6 million to $186.1 million during the year. The variation reflects the three yearly revaluation of the properties as at 30 June 1986, the acquisition of an additional property and development expenditure offset by the depreciation provision of the Board's properties for 1985-86. The Board owns four office properties and a car park with office development potential in the City of Melbourne, three industrial properties in the Melbourne suburbs and a discount department store and supermarket in Shepparton. During the year, the Board acquired the property at 559-587 Collins Street, for $27.25 million. This property contains a multi-level car park for 1,000 cars together with top floor office space of 1,479 sq metres. In addition, the property is capable of additional development of an office building of approximately 47,000 sq metres. Rentals were reviewed at a number of the Board's properties, including the office buildings at 232-250 Victoria Parade. In each instance, increase in rental based on commercial terms has been achieved.

The Board is currently finalising the residential sub-division at East Doncaster, completed in conjunction with the Urban Land Authority. The Board has taken legal action against two purchasers to recover outstanding purchase monies. This property had previously been subject to a mortgage from the Board and the Board is now seeking reimbursement from the Department of Management and Budget of the outstanding balance covered by the Treasurer's guarantee.

The Board continues to seek opportunities for further property investment.

32

Mortgage Loans

During the year $11.5 million was provided by the Board to contributors for housing loans. At the close of the financial year there were 2,790 active loans.

The rate of interest charged on variable interest charged mortgages ranged between 13.5% and 15.25%.

The Board's decision of 28 September 1983, setting the variable interest rate as that charged by RESI/Statewide Permanent Building Society was rescinded by the Board on 23 October !985. The rate is presently determined by current market conditions and the rate charged by RESI/Statewide from time to time.

The Board also amended policy to allow for spouse income to be taken into account when determining the maximum repayment rate to a combined total of 25% of gross joint income.

DISTRIBUTION OF INVESTMENTS-TEN YEARS 30 June 1977 to 30 June 1986 (inclusive)

($ million)

1977 1978 1979 1980 1981 1982 1983 1984 1985 1986

Short Term Deposits 17.4 4. I 13.4 14.4 4.9 16.7 36.6 16.9 55.1 34.6 Commonwealth Securities 10.1 2.8 4.4 80.2 35.6 10.5 Semi-Government Securities 155.7 168.1 194.0 187.0 190.3 215.2 179.7 150.8 263.2 299.8 Local Government Securities 41.1 48.8 56.3 58.4 60.6 60.9 60.2 59.8 55.3 53.3 Accumulated Amortization of Discount Received 2.1 Investments in Loans secured by

State Government Guarantee 3.2 3.9 4.2 4.2 27.0 32.3 55.3 96.3 116.3 116.3 Investment Bank Transferable

Deposits 1.0 6.5 9.3 6.3 4.2 8.9 6.0 8.9 Loans under Agreement 4.7 4.7 5.5 5.3 5.0 4.9 4.6 4.3 10.9 14.9 Mortgages-

Commercial Loans 60.8 72.8 78.5 ll7.5 137.1 138.7 135.1 124.9 134.9 170.6 Housing Loans 27.4 35.2 43.2 52.2 64.0 76.4 80.4 81.1 77.7 76.5

Land and Building-Freehold 28.5 34.5 34.1 35.0 36.7 45.6 77.9 91.6 89.6 186.1 Indexed Loans 20.0 58.8 61.1 88.8

338.8 382.2 430.2 480.5 537.7 597.0 658.4 773.6 905.7 1062.4

Comparative Rate of Return to Consumer Price Index

As stated in the Board's corporate objectives it is a primary object to ensure that the overall rate of interest returned on investments of contributors' funds exceeds the Consumer Price Index. This has been achieved in seven of the past eight years.

Board's Return on Consumer Price Year Investments Index

% %

1978-79 8.7 8.21 1979-80 8.9 10.12 1980-81 9.9 9.41 1981-82 11.5 10.4 1982-83 13.5 11.5 1983-84 13.6 6.9 1984-85 13.6 6.7 1985-86 14.4 8.4

33

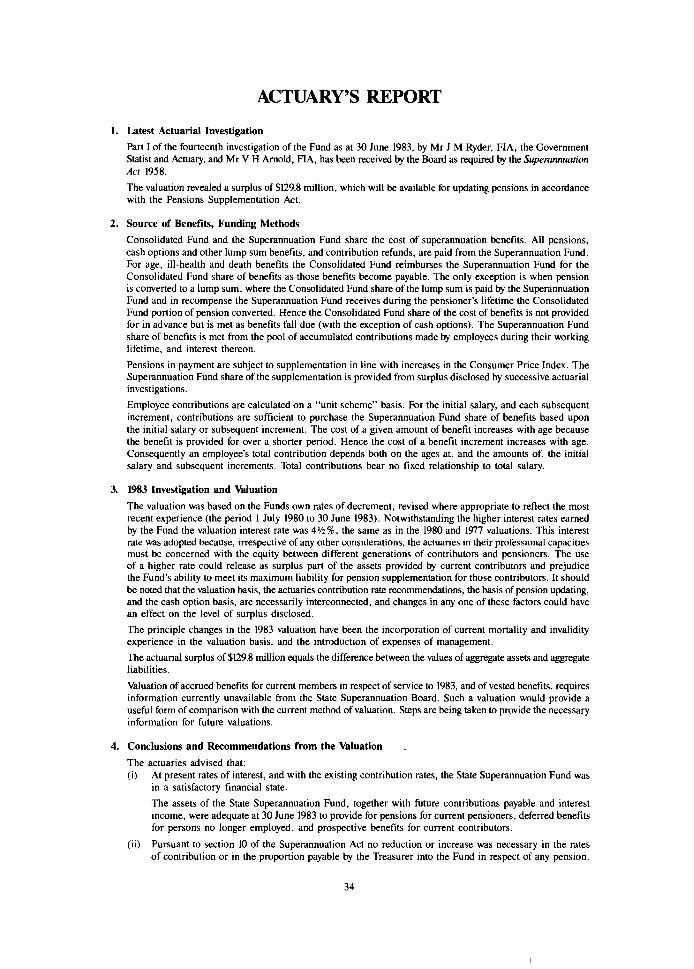

ACTUARY'S REPORT

l. Latest Actuarial Investigation

Part I of the fourteenth investigation of the Fund as at 30 June 1983, by Mr J M Ryder, FIA, the Government Statist and Actuary, and Mr V H Arnold, FIA, has been received by the Board as required by the Superonnuation Act 1958.

The valuation revealed a surplus of $129.8 million, which will be available for updating pensions in accordance with the Pensions Supplementation Act.

2. Source of Benefits, Funding Methods

Consolidated Fund and the Superannuation Fund share the cost of superannuation benefits. All pensions, cash options and other lump sum benefits, and contribution refunds, are paid from the Superannuation Fund. For age, ill-health and death benefits the Consolidated Fund reimburses the Superannuation Fund for the Consolidated Fund share of benefits as those benefits become payable. The only exception is when pension is converted to a lump sum, where the Consolidated Fund share of the lump sum is paid by the Superannuation Fund and in recompense the Superannuation Fund receives during the pensioner's lifetime the Consolidated Fund portion of pension converted. Hence the Consolidated Fund share of the cost of benefits is not provided for in advance but is met as benefits fall due (with the exception of cash options). The Superannuation Fund share of benefits is met from the pool of accumulated contributions made by employees during their working lifetime, and interest !hereon.

Pensions in payment are subject to supplementation in line with increases in the Consumer Price Index. The Superannuation Fund share of the supplementation is provided from surplus disclosed by successive actuarial investigations.

Employee contributions are calculated on a "unit scheme" basis. For the initial salary, and each subsequent increment, contributions are sufficient to purchase the Superannuation Fund share of benefits based upon the initial salary or subsequent increment. The cost of a given amount of benefit increases with age because the benefit is provided for over a shorter period. Hence the cost of a benefit increment increases with age. Consequently an employee's total contribution depends both on the ages at, and the amounts of, the initial salary and subsequent increments. Total contributions bear no fixed relationship to total salary.

3. 1983 Investigation and Valuation

The valuation was based on the Funds own rates of decrement, revised where appropriate to reflect the most recent experience (the period I July 1980 to 30 June 1983). Notwithstanding the higher interest rates earned by the Fund the valuation interest rate was 41/2%, the same as in the 1980 and 1'!77 valuations. This interest rate was adopted because, irrespective of any other considerations, the actuaries in their professional capacities must be concerned with the equity between different generations of contributors and pensioners. The use of a higher rate could release as surplus part of the assets provided by current contributors and prejudice the Fund's ability to meet its maximum liability for pension supplementation for those contributors. It should be noted that the valuation basis, the actuaries contribution rate recommendations, the basis of pension updating, and the cash option basis, are necessarily interconnected, and changes in any one of these factors could have an effect on the level of surplus disclosed.

The principle changes in the 1983 valuation have been the incorporation of current mortality and invalidity experience in the valuation basis, and the introduction of expenses of management.

The actuarial surplus of $129.8 million equals the difference between the values of aggregate assets and aggregate liabilities.

Valuation of accrued benefits for current members in respect of service to 1983, and of vested benefits, requires information currently unavailable from the State Superannuation Board. Such a valuation would provide a useful form of comparison with the current method of valuation. Steps are being taken to provide the necessary information for future valuations.

4. Conclusions and Recommendations from the Valuation

The actuaries advised that: (i) At present rates of interest, and with the existing contribution rates, the State Superannuation Fund was

in a satisfactory financial state.

The assets of the State Superannuation Fund, together with future contributions payable and interest income, were adequate at 30 June 1983 to provide for pensions for current pensioners, deferred benefits for persons no longer employed, and prospective benef1ts for current contributors.

(ii) Pursuant to section 10 of the Superannuation Act no reduction or increase was necessary in the rates of contribution or in the proportion payable by the Treasurer into the Fund in respect of any pension.

34

(iii) The surplus disclosed was, when assessed on a number of different sets of assumptions as to future conditions, likely to be adequate to meet the cost of pension supplemenlation to the date of the next valuation. The question of whether future actuarial valuation surpluses are likely to be adequate to provide fur the Fund's future maximum liability fur supplementation CNer a much longer period was to be considered in Part II of the Investigation Report. This has now been deterred due to changes in the legislation.

5. Changes to Legislation

The legislation gCNeming the operation of the Slate Superannuation Fund was amended by the Superannuation Schemes Amendment Act 1985, effective from 7 January 1986.

The amendments of financial significance, and their effect, are:

(i) The determination of pension commulation factors by way of a schedule (schedule 6) incorporated in the Act.

The factor prescribed for age 60 is consistent with the recommended actuarial factor for a lump sum providing the retiree with the actuarial equivalent value of the pension benefit furegone. At ages between 50 and 60, and between 60 and 65, the factors prescribed provide lump sums which produce costs exceeding, for current proportions of male and female retirees, the actuarial equivalent of the pension benefit foregone. These increases were introduced, as a matter of policy, in order that the lump sum payable to an individual should not diminish with age at any appreciable rate.

The extra costs imposed by the prescribed factors do not reduce the surplus disclosed at the 1983 valuation, but will reduce the surplus disclosed in future valuations.

(ii) Commulation of spouse's pensions

Prior to amendment of the Act the proportion of a spouse's pension payable from the Fund was identical to the proportion of the former employee's pension entitlement payable from the Fund. An apparent drafting error in the amending Act has increased the proportion of spouse's pension payable from the Fund in respect of pension commuted. This reduces the surplus disclosed at the 1983 valuation by $3.5 million. The surplus disclosed at future valuations will also be reduced.

(iii) Introduction of early optional retirement

An option to allow early retirement on grounds of age, from age 55 for public servants, teachers and railwaymen, and from age 50 for police was introduced. No pTCNision against surplus for increased costs has previously been necessary because the original early retirement proposals agreed with the relevant unions were predicated on no increase in cost. It has since been decided as a matter of policy that the benefits payable to early retirees having less than 30 years service should be increased CNer the original proposals. On the assumption that amongst such short-service retirees 5% elect to retire early at each age the Fund share of the additional cost is about $18 million for existing employees. The surplus available for indexation is reduced correspondingly.

(iv) Changed conditions for transfers from other slatutory funds

It had been originally proposed as a matter of policy that employees transferring into the Slate Superannuation Fund should have both their years of past service and previous medical classification recognised. Such transferees generally vrould obtain an increased level of benefit. In those circumstances the amount transferred in vrould generally be inadequate to meet the cost of the higher level of benefit payable, in respect of the period of prior service, on disability retirement. This vrould have resulted in a significant subsidy of transferees by the existing body of employees.

The Board on 26 February 1986 minuted:

"It was agreed that transfers of contributions and entitlements vrould not be accepted where the contributor has an entitlement to a preserved benefit which included employer content as a result of his membership of a previous fund."

In these circumslances the Fund subsidises transferees to the extent that the disability retirement benefit is based on medical classification in the former fund. If that classification is better than that evidenced by examination on entry to the Fund then the disability retiree oblains a more valuable benefit than provided for by contributions paid. However, since this subsidy is generally confined to a relatively small number of transferees the financial effect in terms of current number is not particularly significant. It has not been thought necessary at the moment to reduce the surplus available for indexation from the last valuation on this account.

35

6. Current position

Although the surplus available for indexation has been reduced the balance is adequate for the likely cost of pension indexation to 30 June 1986.

Under section 4(5B) of the Pensions Supplementation Act a transfer to the Supplementation Fund is permitted of such amounts as the valuing actuary certifies are likely to be surplus to the requirements of the Superannuation Fund.

The financial position of the Superannuation Fund as at 30 June 1986 has been subject to a preliminary actuarial valuation. It appears likely that sufficient surplus will be disclosed, on a basis consistent with current valuation practice, to meet the expected costs of pension supplementation to at least 30 June 19!f7.

36

J M RYDER Government Actuary

7/10/86

PENSIONS SUPPLEMENTATION FUND REPORT

Pensions supplementation commenced following introduction of the Pensions Supplementation Act 1966 (No. 7417) in May 1966.

The Pensions Supplementation Act 1973 provided for automatic updating of pensions based on the movement in the Consumer Price Index for "All Groups" Melbourne.

On 9 January 1980, the Supplementation Amendment Act 1979, No. 9358 was proclaimed. This Act included an amendment to the Pensions Supplementation Ac-1 1966, which provided that pen.~ion increases resulting from increases in the Consumer Price Index would be paid h~lf-yearly.

On 29 November 1985, pensions were raised by 4.25% for the half-year ending 30 June 1985. The 4.25% increase was applied to all pensions which commenced on or prior to 31 January 1985, and pro-rata increases were granted to pensions which commenced during the period I February 1985 to 30 June 1985.

On 30 May 1986, pensions were raised by 3.79% for the half-year ending 31 December 1985. The 3.79% increase was applied to all pensions which commenced on or prior to 31 July 1985, and pro-rata increases were granted to pensions which commenced during the period 1 August 1985 to 31 December 1985.

PENSIONS SUPPLEMENTATION FUND BALANCE SHEET

AS AT 30 JUNE 1986