128

Annual Report 2002/2003 Brought to you by Global Reports

Annual Report 2002/2003

Brought to you by Global Reports

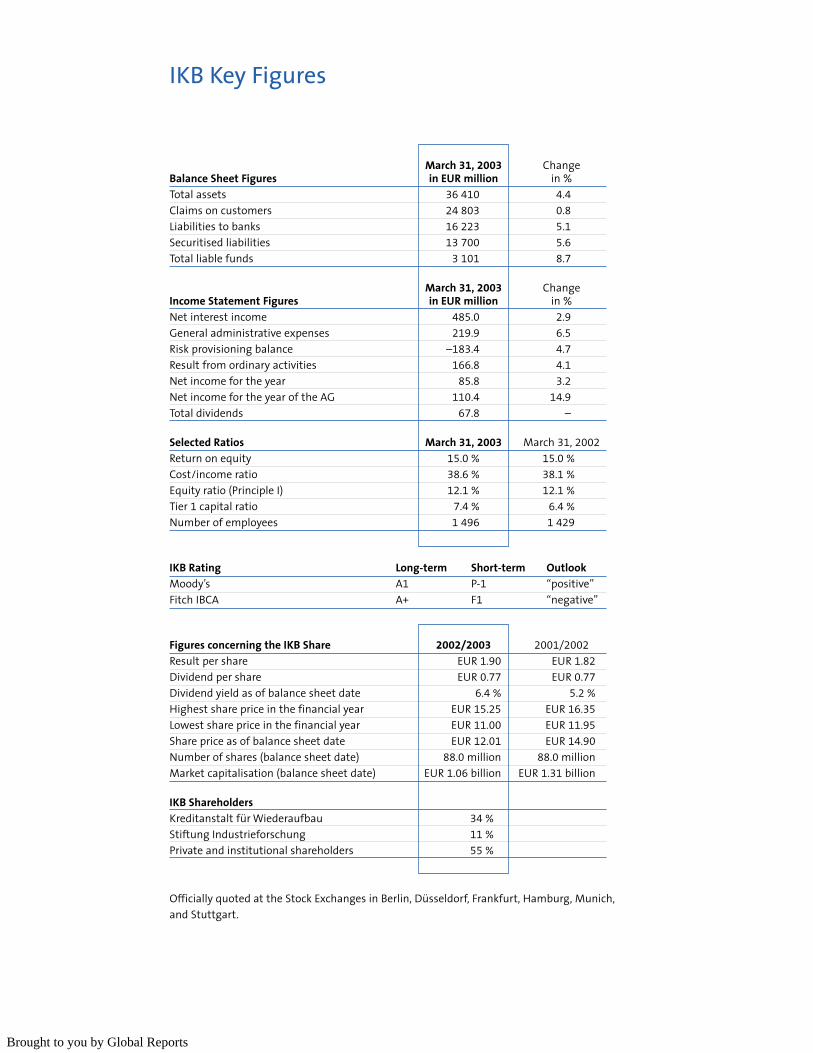

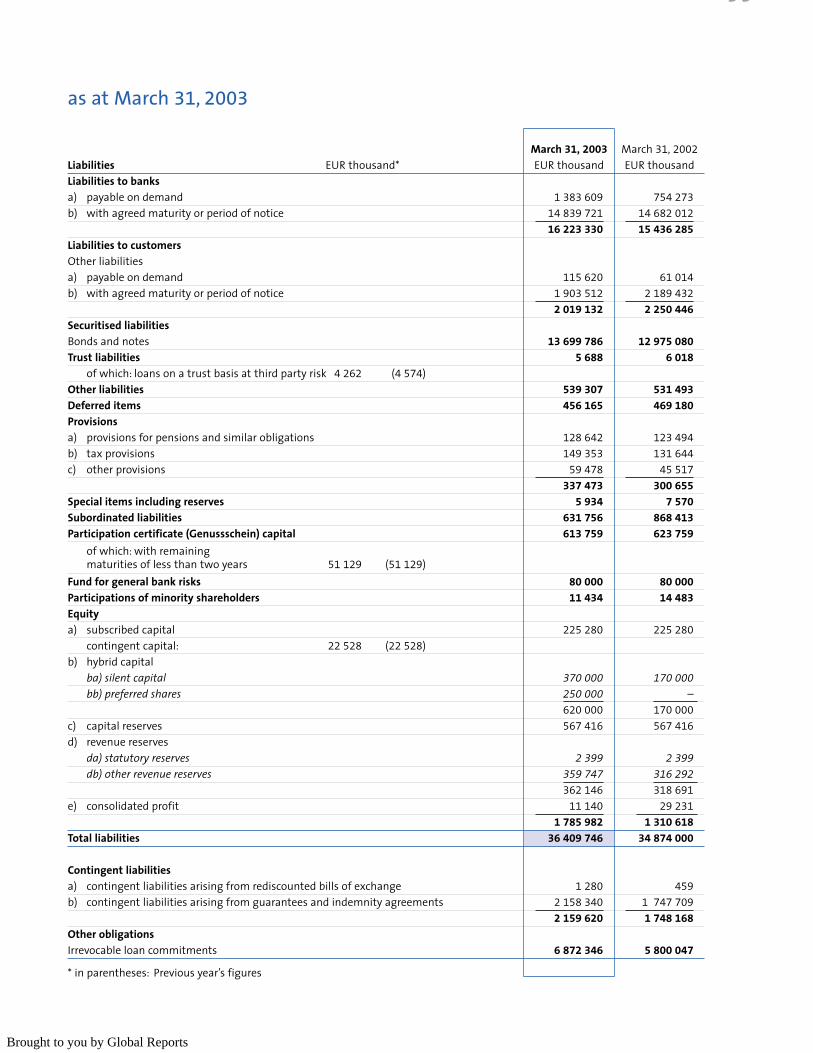

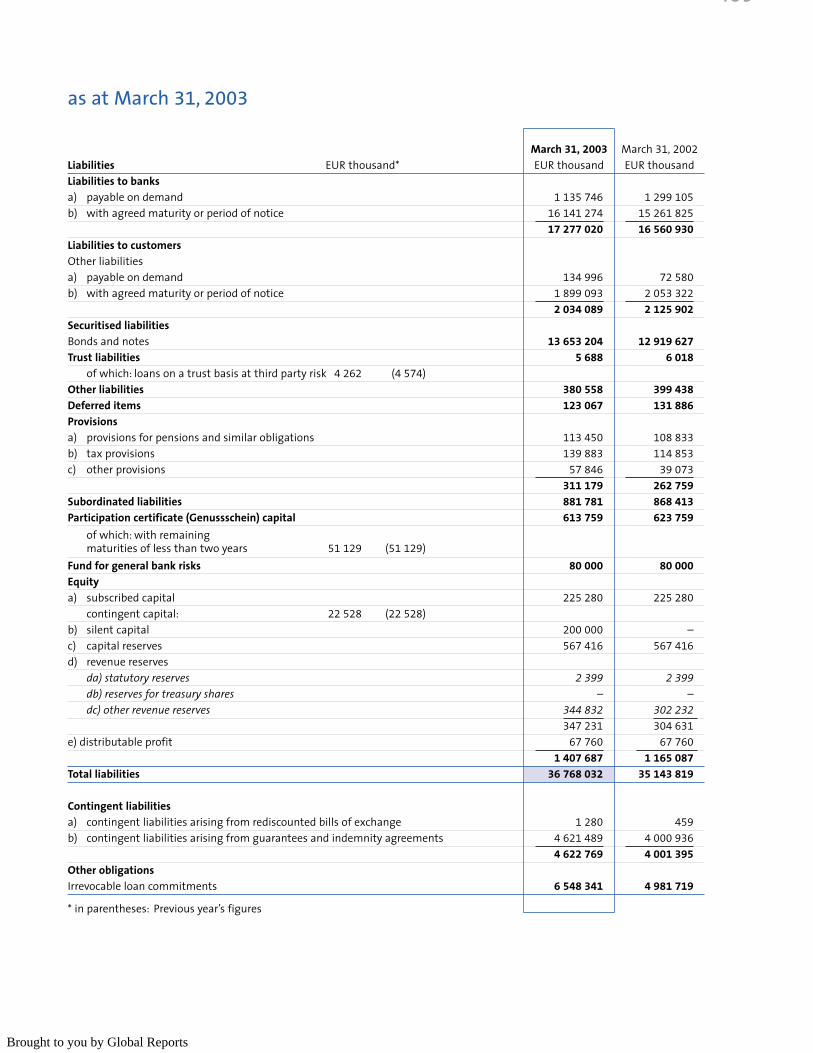

March 31, 2003 ChangeBalance Sheet Figures in EUR million in %Total assets 36 410 4.4

Claims on customers 24 803 0.8

Liabilities to banks 16 223 5.1

Securitised liabilities 13 700 5.6

Total liable funds 3 101 8.7

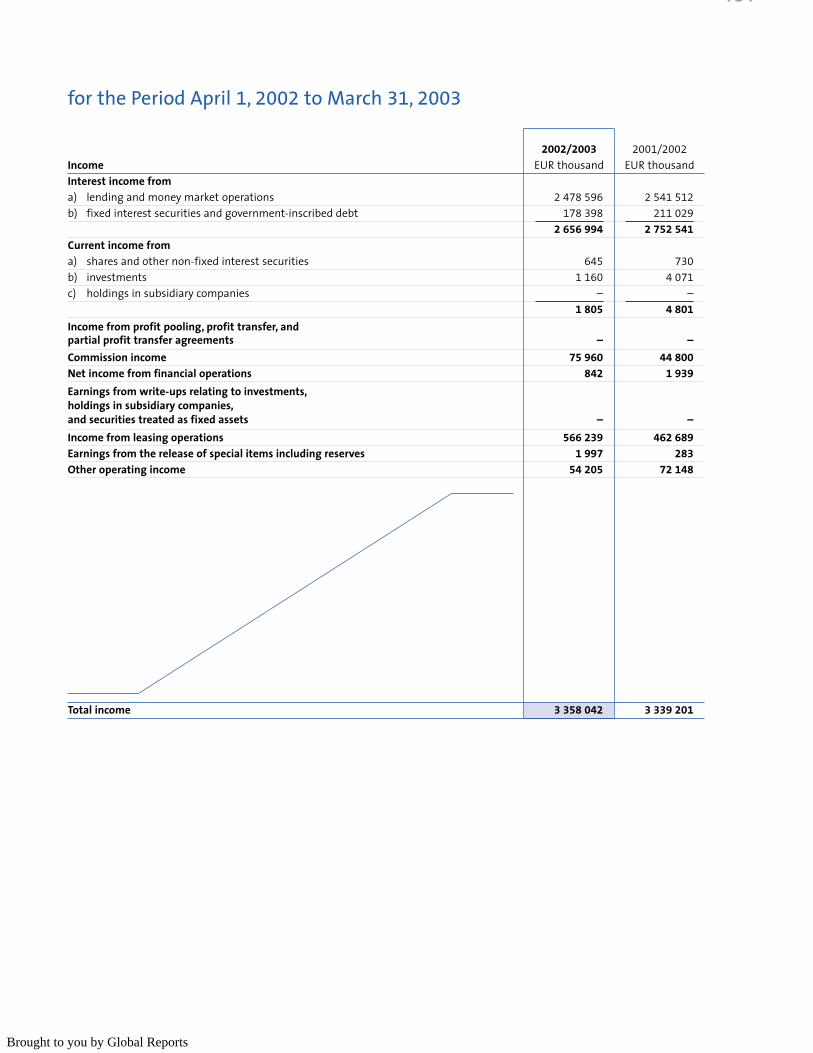

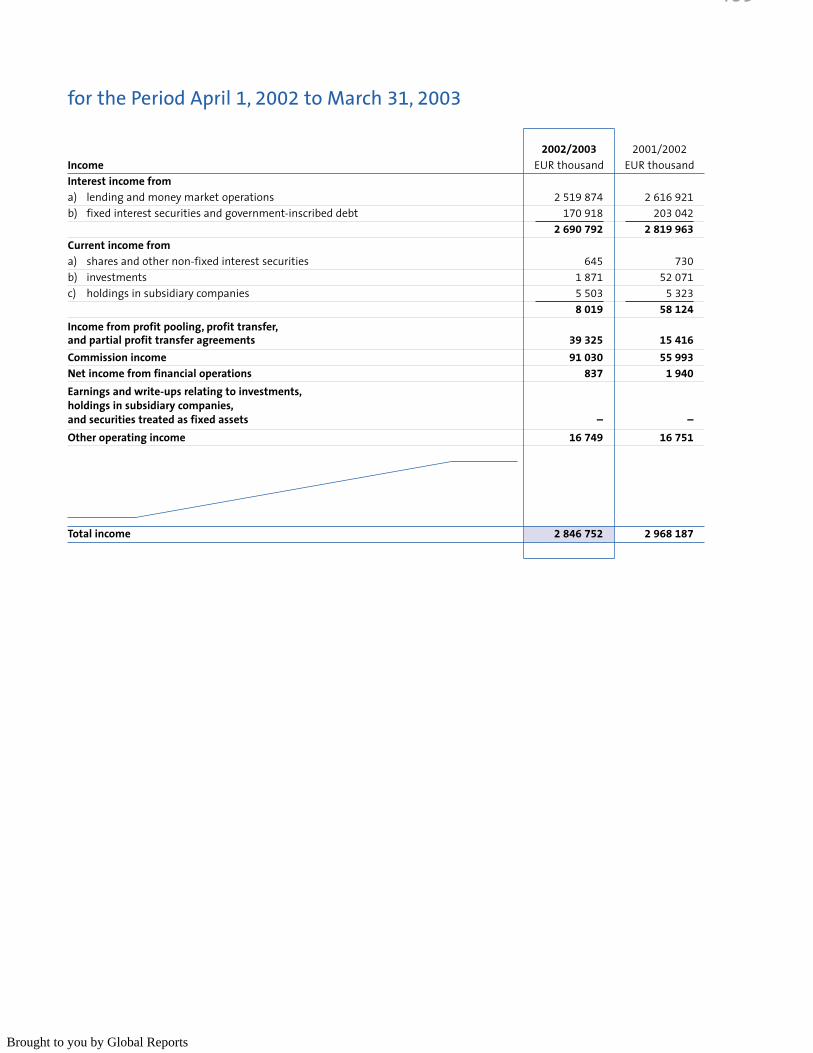

March 31, 2003 ChangeIncome Statement Figures in EUR million in %Net interest income 485.0 2.9

General administrative expenses 219.9 6.5

Risk provisioning balance –183.4 4.7

Result from ordinary activities 166.8 4.1

Net income for the year 85.8 3.2

Net income for the year of the AG 110.4 14.9

Total dividends 67.8 –

Selected Ratios March 31, 2003 March 31, 2002

Return on equity 15.0 % 15.0 %

Cost/income ratio 38.6 % 38.1 %

Equity ratio (Principle I) 12.1 % 12.1 %

Tier 1 capital ratio 7.4 % 6.4 %

Number of employees 1 496 1 429

IKB Rating Long-term Short-term OutlookMoody’s A1 P-1 “positive”Fitch IBCA A+ F1 “negative”

Figures concerning the IKB Share 2002/2003 2001/2002

Result per share EUR 1.90 EUR 1.82

Dividend per share EUR 0.77 EUR 0.77

Dividend yield as of balance sheet date 6.4 % 5.2 %

Highest share price in the financial year EUR 15.25 EUR 16.35

Lowest share price in the financial year EUR 11.00 EUR 11.95

Share price as of balance sheet date EUR 12.01 EUR 14.90

Number of shares (balance sheet date) 88.0 million 88.0 millionMarket capitalisation (balance sheet date) EUR 1.06 billion EUR 1.31 billion

IKB ShareholdersKreditanstalt für Wiederaufbau 34 %

Stiftung Industrieforschung 11 %

Private and institutional shareholders 55 %

Officially quoted at the Stock Exchanges in Berlin, Düsseldorf, Frankfurt, Hamburg, Munich,

and Stuttgart.

IKB Key Figures

Brought to you by Global Reports

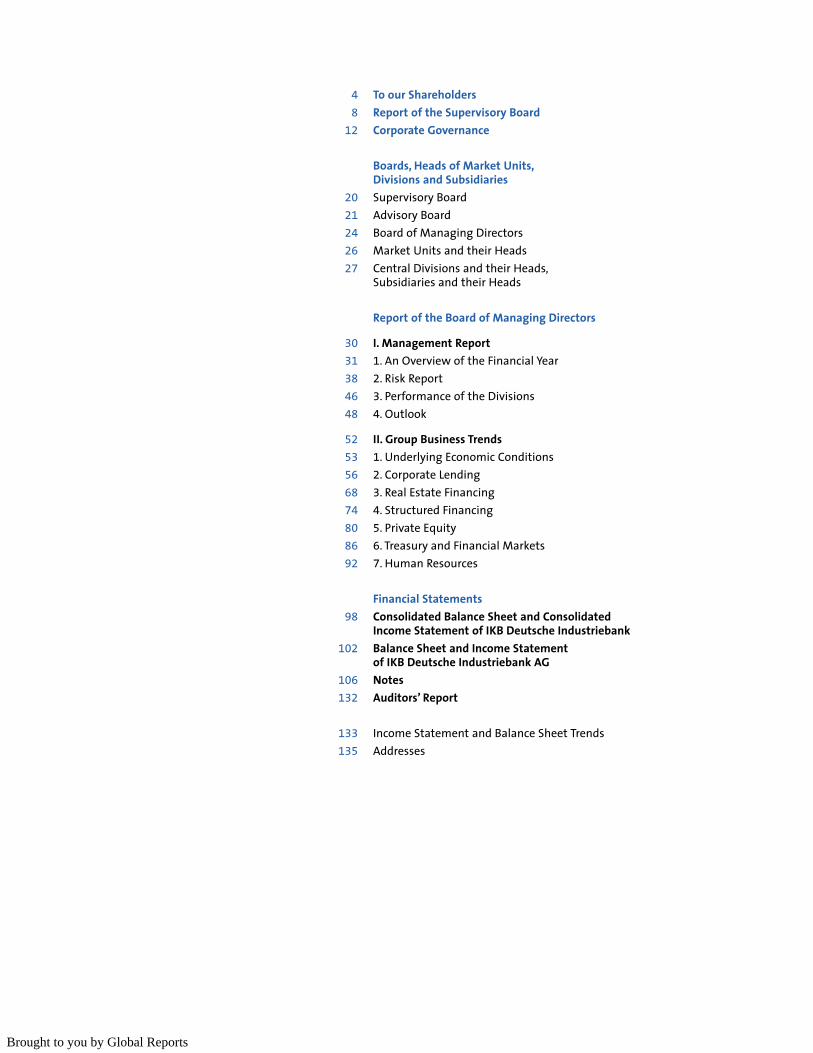

4 To our Shareholders8 Report of the Supervisory Board

12 Corporate Governance

Boards, Heads of Market Units,Divisions and Subsidiaries

20 Supervisory Board21 Advisory Board24 Board of Managing Directors26 Market Units and their Heads27 Central Divisions and their Heads,

Subsidiaries and their Heads

Report of the Board of Managing Directors

30 I. Management Report31 1. An Overview of the Financial Year38 2. Risk Report46 3. Performance of the Divisions48 4. Outlook

52 II. Group Business Trends53 1. Underlying Economic Conditions56 2. Corporate Lending68 3. Real Estate Financing74 4. Structured Financing80 5. Private Equity86 6. Treasury and Financial Markets92 7. Human Resources

Financial Statements98 Consolidated Balance Sheet and Consolidated

Income Statement of IKB Deutsche Industriebank102 Balance Sheet and Income Statement

of IKB Deutsche Industriebank AG106 Notes132 Auditors’ Report

133 Income Statement and Balance Sheet Trends

135 Addresses

Brought to you by Global Reports

Despite the disappointing performance of theGerman economy, many medium-sized companiesremain remarkably successful. They are benefitingfrom a greater division of labour in the economy and arestructuring of the value-added chain. Whether aspart suppliers, development partners or serviceproviders, they make a huge contribution to strength-ening the international competitiveness of Germanproducts.

IKB too is firmly integrated in this process – as areliable financing partner, ready and willing to backthe growing investment activities of medium-sized

companies with a wide array of consulting and financ-ing services. This annual report documents the way inwhich the bank has once again supported a greatnumber of companies in implementing their strate-gies for the future. Thus, on behalf of Germany indus-try, I would also like to express my sincere thanks andappreciation to the men and women of the IKB staff.

Dr. Michael Rogowski

PresidentFederation of German Industry

Brought to you by Global Reports

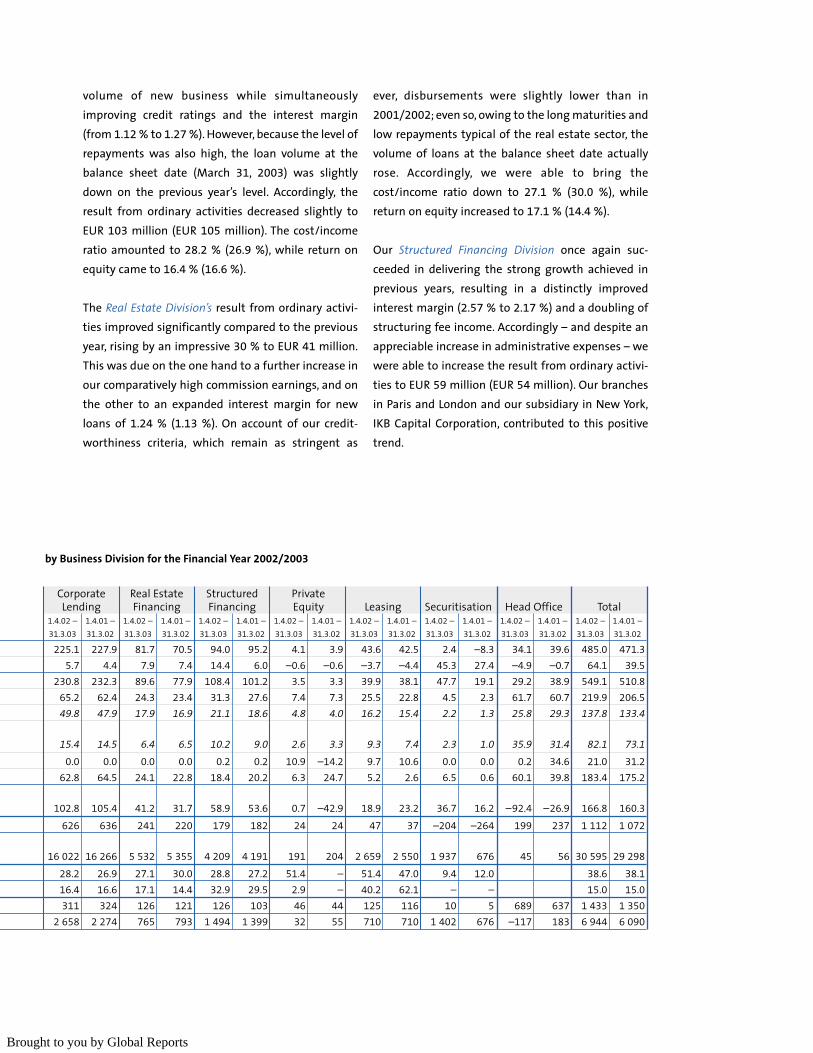

Contrary to the general trend in the German bankingsector, IKB continued to develop along positive linesduring the 2002/2003 financial year. Despite the dif-ficult economic conditions, we were able to increaseour result from ordinary activities by 4.1 % to EUR 167

million.

Specifically,• net interest income increased by 2.9 % to EUR 485

million

• the interest margin for new loan accommodationsin the Group expanded to 1.68 % (previous year:1.44 %)

• net commission income rose by EUR 25 million toEUR 64 million

To our Shareholders

Brought to you by Global Reports

• administrative expenses increased by 6.5 % to EUR220 million and

• risk provisioning balance increased by EUR 8 mil-lion to EUR 183 million.

The cost/income ratio for the period under reviewcame to 38.6 % (38.1 %) while return on equityremained unchanged at 15.0 %.

In light of this generally positive performance, theManagement Board and Supervisory Board proposeto the General Meeting payment of an unchangeddividend to shareholders of EUR 0.77 per share forthe 2002/2003 financial year. This corresponds to adividend yield of 6.4 % based on the share price at thebalance sheet date.

The reasons for IKB’s comparatively robust businessand earnings growth lie in the excellent strategicpositioning of the bank, giving us a crucial advantagecompared to our competitors. At a time when manybanks have withdrawn from lending business in theMittelstand market, or have in any case becomehighly volatile in their behaviour, we have succeededin getting the message across to our customers thatIKB is a dependable, predictable and trustworthypartner.

This message has become all the more persuasivenow that we are cooperating even more closely withKfW, a bank that shares our commitment to the long-term financing of the Mittelstand. Indeed, our part-nership with KfW has met with an exceptionally pos-itive response from our customers.

The rating agencies have taken an equally sanguineview of developments. In spring 2002, for instance,Moody’s – contrary to the general trend in the bank-ing sector – upgraded our rating to A1, while Fitchhad already given us an A+. Moreover, Moody’s

combined its rating of IKB with a “positive outlook”statement and reinforced this assessment only a fewdays before our balance sheet date. In justifying thesegood ratings, both agencies pointed to IKB’s stableearning performance as well as our partnership withKfW.

And indeed, the results of our first full year of cooper-ation with KfW have been highly encouraging. Forexample, we cooperated in developing a global loanfacility that enables us to set margins based on thecreditworthiness of the individual borrower ratherthan imposing a uniform margin of 1 %. On the onehand this is precisely in line with the requirements ofBasle II, while on the other it makes it attractive forbanks to extend industrial development loans again.

The division of labour between IKB and KfW thusbecomes clear: because we have our ear to theground, we can keep our partner apprised of theevolving demand and needs of the Mittelstand. Inturn, KfW applies its unsurpassed expertise in thejoint development of new financing instrumentsspecifically designed for the medium-sized corporatesector. It is not least because of this that the twoorganisations succeeded in generating a combinedEUR 0.8 billion in additional new loan business duringthe past financial year, something neither bank couldhave achieved without assistance from the other.

Two New Cooperation Agreements

In order further to improve our competitive positionin the German banking market, we entered into twonew cooperation agreements during the periodunder view: one with Sal. Oppenheim, the otherwith UniCredito Italiano.

Brought to you by Global Reports

The prime motivation behind our cooperation agree-ment with Sal. Oppenheim is the fact that our targetgroups are nearly identical. Whereas at IKB the mainfocus during an acquisition is on the company, at Sal.Oppenheim the emphasis is on the entrepreneur.Thanks to our complementary range of products,there is plenty of potential for adding to the businessof both banks. Thanks to our new cooperation partnerwe are able to offer our customers a comprehensivearray of ECM products, greater assistance duringM&A transactions as well as full range of asset man-agement services. For its part, Sal. Oppenheim cannow supply its customers with long-term corporateand acquisition financing, and also arrange forcertificates of indebtedness (Schuldscheindarlehen).In order to strengthen ties between the two banks,Sal. Oppenheim has taken up an initial 3 % of IKBshare capital.

Apart from the immediate business benefits of coop-erating with Sal. Oppenheim, there is another impor-tant aspect here. I refer to the message that thiscooperation agreement sends to our customers, com-petitors and the public at large: the fact that IKB verymuch remains a private sector, market-oriented bank.

At the end of the period under review we also en-tered into a cooperation agreement with UniCreditoItaliano. Together with its investment unit, UniCreditBanca Mobiliare (UBM), we will be establishing a jointventure in Luxembourg this autumn called IKBCorporateLab. This company will offer consulting andfinancial services for optimising the balance sheetstructures of our customers.

In cooperating with UniCredito, we will have one ofEurope's strongest performing banks on our side –and one which has been working successfully in thefield of financial risk management since 1998. Now,in comprehensive and professional fashion, we will beable to offer our customers a full range of interestand foreign currency derivatives without having tocouple these with a loan, something which hithertotended to be the case.

Step by step, IKB CorporateLab will enable us to makeup with the competitive edge enjoyed by the bigbanks in this advice-intensive sector – and withoutthe need for major investments in management andIT resources. While our Italian partners will be respon-sible for the products, we will focus on acquisitionand consulting.

We aim to make IKB CorporateLab the leading sourceof financial risk management for Germany’s Mittel-stand.

Viewed against the backdrop of our partnership withKfW and our cooperation agreements with Sal.Oppenheim and UniCredito Italiano, an analysis ofthe strategic positioning of IKB quickly makes clearthe pivotal position we now occupy in the Germanbanking market, providing us with excellent opportu-nities for continued increased earnings.

Also contributing to this are our investments in inter-national loan portfolios, part of our systematic step-by-step transition from risk taker to risk manager. Forby investing in international loan portfolios, not onlyare we able to diversify our risks from the regionaland sector standpoint, but – and even more impor-tantly – we can substantially increase our earnings.

Brought to you by Global Reports

The IKB Share

This positive business performance has made a bigcontribution to keeping IKB’s share price relativelystable over the past two years, stock market crashesand investor reluctance notwithstanding. As thegraph shows, the IKB share price has largely decou-pled itself from the poor performance of the DAX andthe CDAX Banks. Though the downturn in the stockmarket also led to some selling of IKB shares, we wereimmediately able to place these with new institu-tional investors, having already presented our bankto them during one-on-one meetings and investorconferences over the past two years.

But this placement was certainly also facilitated bythe revival of investor interest in strong-earningshares. Of course, up until 2000/2001 the mood wasvery different. A company that paid a dividend inthose heady days was considered to be “Old Econo-my” and branded as unimaginative. But after thestock market crash of 2001/2002, a significant reori-entation took place among analysts and investors.A convincing corporate strategy, strong earningpower and the payment of a dividend havere-emerged today as the most important criteria inprompting an investor to buy a share. Because IKBstock meets all these criteria and has paid a dividendever since the bank’s post-war foundation, andbecause this dividend has never been scaled back, ourshares have performed correspondingly well.

You will find further information concerning ourshares and Investor Relations activities at our web-site, www.ikb.de.

You are cordially invited to attend this year's GeneralMeeting, which will be held at 10:00 a.m. on Septem-ber 5 at the CCD. Stadhalle, Congress Center Düssel-dorf, Rotterdamer Straße, 40474 Düsseldorf. We verymuch look forward to seeing you there.

Dr. Alexander v. Tippelskirch

Chairman of the Board of Managing Directors IKB Deutsche Industriebank AG

Source:Bloomberg

%

2001 2002 2003-70

-60

10

-50

-40

-30

-20

-10

0

■ IKB■ DAX■ CDAX Banks/Prime Banks

IKB Share Performance

Brought to you by Global Reports

Report of theSupervisory Board

During the 2002/2003 financial year, the SupervisoryBoard has kept itself thoroughly informed concern-ing the condition of the bank and Group on a regularbasis, as well as monitoring senior management. Dur-ing the period under review, the Supervisory Boardheld four regular meetings on June 26, August 30,

and November 7, 2002, and March 13, 2003. Allmembers of the Supervisory Board took part in morethan half of the meetings of the Supervisory Boardheld during their period of tenure.

Brought to you by Global Reports

The Supervisory Board has formed two committees.The Presiding Board, consisting of the Chairman ofthe Supervisory Board and the two Deputy Chairmen,met on four occasions. The Finance and AuditingCommittee met once on June 25, 2002 prior to thebalance sheet meeting of the Supervisory Board. Thiscommittee consists of the members of the PresidingCommittee plus one representative from the group ofstaff representatives in the Supervisory Board.

Issues discussed by the Supervisory Board weretreated in greater depth at meetings of the PresidingCommittee. The Presiding Committee organised themeetings of the Supervisory Board, handled person-nel matters relating to the Management Board, aswell as approving the acceptance of seats on thesupervisory bodies of other companies by membersof the Management Board. In the form of a writtenstatement, the Finance and Auditing Committeeauthorised loan transactions requiring its approvalunder German banking law, and carried out a prelim-inary audit of the 2001/2002 annual accounts of theAG and Group on behalf of the entire SupervisoryBoard.

The Chairman of the Supervisory Board reported tothe Plenum on the activities of the two SupervisoryCommittees. Furthermore, in addition to these meet-ings, the Chairman of the Supervisory Board and theChairman of the Management Board also conferredin depth on issues and items of general importance atregular working meetings.

Among the main items discussed at meetings of theSupervisory Board were business policy matters andother critical aspects of corporate planning, balancesheet and profit statement developments, as well asplanning and results in the individual divisions, andparticipation investments. The development of risksin the loan business as well as measures of the bankto further enhance the loan portfolio and to strength-en regulatory capital were discussed in depth. A topicof intense discussion was the IKB Mittelstand ratingsystem, based on proposals of the Basel Committeefor Bank Supervision (Basel II), as well as measuresmade necessary by the imposition of future regulato-ry requirements on the banking industry in this area.Also dealt with in depth was the development of ourcooperation with Kreditanstalt für Wiederaufbau ofFrankfurt am Main, as well as the new strategic part-nership with Bankhaus Sal. Oppenheim jr. & Cie.KGaA of Cologne and the agreement to cooperatewith UniCredit Banca Mobiliare of Milan. The Super-visory Board was informed about the duties and fun-damental findings of the regular inspections con-ducted by the Group auditing unit. The results of asurvey of the staff conducted in November 2002

concerning their views of the bank was anotherimportant topic of discussion.

Much space was allocated to consultations relatingto the IKB Principles of Corporate Governance which,based on the recommendations and suggestions ofthe German Corporate Governance Code, wereadopted at the meeting of the Management Boardand the Supervisory Board on November 7, 2002, aswell as to amending the internal regulations govern-ing the Management Board and the SupervisoryBoard so as to conform with these regulations. In thiscontext, the Supervisory Board arranged for a person-al and thorough briefing by the auditor concerning

Brought to you by Global Reports

the German Corporate Governance Code and theresulting obligations. The following obligation wasalso added to the bank’s Principles of CorporateGovernance and the internal regulations covering theSupervisory Board: Members of the SupervisoryBoard must disclose potential conflicts of interestrelating to their tenure to the Supervisory Board. Inits annual report to the General Meeting, the Super-visory Report informs of any conflicts of interestoccurring and the steps taken as a result. No suchconflicts of interest emerged during the period underreview.

At the November meeting, the Supervisory Board alsopassed the Declaration of Conformity with the Ger-man Corporate Governance Code pursuant to Section161 of the German Stock Corporation Act (AktG).Additional information on this can be found in thechapter of this Annual Report entitled “CorporateGovernance”.

The annual accounts and consolidated Groupaccounts, as well as the Management Report of boththe AG and the Group, including the accounting, werereviewed and unreservedly confirmed by the auditor.The report submitted by the Management Board con-

cerning relations with related companies for the2002/2003 financial year was also scrutinised by theauditor. The Report of Dependency was granted thefollowing unrestricted audit certificate: “Followingour duly conducted audit and evaluation, we herebyconfirm that the actual statements in this report arecorrect and that payments made by the companyrelating to transactions listed in this report were notinappropriately high”.

The Supervisory Board received the accounting docu-mentation well ahead of the balance sheet meeting,as well as the draft Annual Report and the reports ofthe auditors. The Finance and Auditing Committeethoroughly scrutinised the annual accounts docu-mentation, the Report of Dependency and the reportsof the auditors. The auditors also briefed the Com-mittee, discussing the findings and results of theaudit. The auditors furnished all the informationrequired. The Finance and Auditing Committee pre-sented the results of the audit to the entire Supervi-sory Board at the balance sheet meeting. The audi-tors took part in the meeting, commenting on thebasic results of the audit and answering the ques-tions of individual members of the Supervisory Board.

In conformity with the final results of its own audit,the Supervisory Board raised no objections concern-ing the Report of Dependency or the declaration ofthe Management Board at the end of the report. TheSupervisory Board agreed to the auditor’s result ofthe audit of the report. Nor did the Supervisory Boardraise any objections concerning the audit of theannual accounts, the joint Management Report of theAG and Group or the Management Board’s proposal

Brought to you by Global Reports

for the appropriation of profits. The SupervisoryBoard took note of the results of the audit, expressingits approval. At today's meeting, the annual accountsand consolidated annual accounts received theapproval of the Supervisory Board, and are now defi-nite. The Management Board’s proposal for theappropriation of profits has met with our approval.

At the General Meeting on August 30, 2002, JörgBickenbach, Dr. Jürgen Heraeus, Roland Oetker andHans W. Reich were re-elected, and Dr. MichaelRogowski elected, as members of the SupervisoryBoard. Roswitha Loeffler and Rita Röbel, both mem-bers of the IKB staff, were also re-elected on thatdate. At the conclusion of last year's General Meeting,Hans Peter Stihl stepped down from the SupervisoryBoard. The Supervisory Board would like to thank tohim for his many years of valuable service.

At the end of the General Meeting on August 30,2002, the Supervisory Board convened a constituentmeeting at which Hans W. Reich was re-elected asDeputy Chairman of this body. Gunnar John, electedto the Supervisory Board at the suggestion of theGerman Government, resigned from this body effec-tive December 31, 2002. Exercising its statutory rightof proposal, on March 27, 2003 the German Govern-ment proposed Ministerial Councillor Jörg Asmussen,Head of the Department for National and Interna-tional Financial Market and Currency Policy of theFederal Ministry of Finance in Berlin, for electionto the Supervisory Board. By a declaration of theMunicipal Courts of Düsseldorf and Berlin, JörgAsmussen has been appointed as member of theSupervisory Board effective April 9, 2003 until theGeneral Meeting on September 5, 2003.

Düsseldorf, June 27, 2003

The Supervisory Board

Dr. h.c. Ulrich Hartmann

Chairman

Brought to you by Global Reports

Corporate Governance

Joint Report of the Management Board

and Supervisory Board of IKB Deutsche

Industriebank AG on Corporate Governance

Confidence in the business policy of IKB essentiallydepends on transparent and responsible corporategovernance and control, oriented to the sustainedincrease in corporate value. Good corporate govern-ance thus forms the foundation of our decision-making and control processes. This is particularlyapplicable to the way we interact with our sharehold-ers. The Management Board and Supervisory Boardcooperate closely on behalf of the bank, and are ded-icated to increasing its corporate value. An open flowof timely, equal information encourages confidencein the bank among our shareholders, other investors,business partners, employees and the public.

We welcome the introduction of the German Corpo-rate Governance Code as well as the approach of pro-gressively updating this Code so as to comply withinternational standards. We see in this an importantstep in the ongoing development of the regulatoryframework and practice of corporate governance andcontrol in Germany.

Principles of Corporate Governance of IKB

In November 2002, the Management Board and theSupervisory Board agreed a set of IKB Principles ofCorporate Governance, updated for the first time inJune 2003. In line with the specific corporate natureof IKB, these Principles were elaborated on the basisof the German Corporate Governance Code, and aresteadily updated to conform to new requirements.They have been disseminated throughout the entireorganisation, and their content assured through com-

pany directives. In addition, the Supervisory Boardhas adapted the internal regulations of the Manage-ment Board and Supervisory Board with the rulescontained in the IKB Principles. The IKB Principles ofCorporate Governance are published on the IKB web-site (www.ikb.de); furthermore, a hardcopy versioncan be requested at no charge.

IKB Corporate Governance Officer

In order to monitor the conformity with the GermanCorporate Governance Code and the IKB Principles,the Management Board, acting in consultation withthe Supervisory Board, has appointed as CorporateGovernance Officer Joachim Neupel, a member of theManagement Board. The Supervisory Board notedwith approval the report on the implementation of,and conformity with, the Principles submitted by theCorporate Governance Officer to the SupervisoryBoard at the meeting on June 27, 2003.

With six exceptions, the bank is currently in compli-ance with the recommendations of the Code andessentially follows its suggestions. The proposal tothe General Meeting on September 5, 2003 to

Brought to you by Global Reports

permit the proceedings of the General Meeting to berecorded and transmitted using electronic and othermedia, and requiring a corresponding change in theArticles of association, means that a further sugges-tion is now being acted upon. The deviations from therecommendations of the Code arise from the annualDeclaration of Conformity pursuant to Article 161 ofthe German Stock Corporation Act (AktG), whichappears at the end of this report.

Cooperation of the Management Board and

Supervisory Board

Intensive, continuous cooperation between the Man-agement Board and the Supervisory Board is a vitalprerequisite for successful corporate governance. Inthe last years this cooperation was steadily strength-ened and improved. On a regular basis, the Manage-ment Board keeps the Supervisory Board promptlyand comprehensively informed on all matters of plan-ning, business trends, the risk situation and risk man-agement pertaining to the IKB Group. The Manage-ment Board explains deviations of the actual busi-ness development from formulated plans and tar-gets, indicating the reasons therefore. The definitionof corporate strategy is coordinated with the Supervi-sory Board. The bank's internal regulations requirethe Management Board to obtain the approval of theSupervisory Board in transactions of vital significanceto the bank. The internal regulations also contain theinformation and reporting requirements of the Man-agement Board vis-à-vis the Supervisory Board.

Committees of the Supervisory Board

In order to increase its operational efficiency and dealmore effectively with complex issues, the SupervisoryBoard has formed two committees composed ofmembers of its own ranks, assigning to them certaintasks.

The Presiding Committee of the Supervisory Board,consisting of the Chairman of the Supervisory Boardand his two deputies, remains in continuous contactwith the Management Board between meetings ofthe Supervisory Board, coordinates the work of theSupervisory Board and prepares for the meetings ofthe Supervisory Board. It decides on loans and majortransactions requiring Supervisory Board approval.Furthermore, it decides whether or not to approvethe acceptance of directorships, offices or other sig-nificant outside occupations by members of the Man-agement Board. In addition, it handles personnelissues pertaining to the Management Board and rep-resents IKB in its dealing with members of the Man-agement Board, as well as taking care of special tasksassigned to it by the plenum.

The Finance and Auditing Committee, made up of themembers of the Presiding Committee as well as onemember from the body of Staff Representatives, isresponsible for questions of accounting and forinspecting the annual financial statement and con-solidated financial statement, as well as for risk man-agement and assuring the independence of the audi-tor. It decides on which auditor to engage, specifyingpoints of focus for the audit if necessary, as well asnegotiating the auditor's fee.The committee also pre-pares for the Supervisory Board’s audit of the annualfinancial statement and consolidated financial state-ment and the report on relations with related compa-nies. Furthermore, it decides on loans requiring theapproval of the Supervisory Board but which do notcome under the purview of the Presiding Committee,as well as measures relating to capital requirements.

Rules for Avoiding Conflicts of Interest

The IKB Principles contain numerous rules for avoid-ing potential conflicts of interest on the part of theManagement Board and the Supervisory Boardextending well beyond the recommendations of theGerman Corporate Governance Code. During the past

Brought to you by Global Reports

financial year, there were no conflicts of interest withthe bank involving members either of the Manage-ment Board or the Supervisory Board. No transactionsrequiring approval of the Supervisory Board wereconcluded during the period under review.

Compensation of the Management Board and

Supervisory Board

The compensation package of members of theManagement Board contains fixed and variablecomponents. The variable component is oriented tocorporate results and the individual performance ofthe particular member of the Management Boardbased on mutually agreed targets. A subsequentrevision of success criteria is not permitted.

The compensation of members of the SupervisoryBoard is specified in the IKB Articles of Association.Apart from the remuneration of expenses, eachmember of the Supervisory Board receives a paymentof EUR 4,000 per financial year; the Chairman receivestwice that amount, while each Deputy Chairmanreceives EUR 6,000. In addition, the Supervisory Boardas whole receives compensation oriented to the per-formance of the bank amounting to EUR 15,000 forevery cent of dividend per share in excess of adividend of 25 cents per share. The total amount ofvariable compensation is distributed according to thesame formula as the fixed compensation component.In addition, the member of the Finance and AuditingCommittee from the group of Staff Representativeson the Supervisory Board receives fixed compensa-tion amounting to EUR 10,000 per financial year.

Total compensation of the Management Board andthe Supervisory Board for the 2002/2003 financialyear is stated in the Notes and Group Notes, dividedinto fixed and variable components. Furthermore,during the past financial year, members of the Super-

visory Board received neither payment nor advan-tages for personally performed services.

Managing Risks

Good corporate governance also implies a responsi-ble approach to handling corporate risks. The entireManagement Board is responsible for IKB risk man-agement inasmuch as it defines risk policy in theform of a clearly stated risk strategy, as well as thetypes of business and the acceptable degree of aggre-gate risk within the context of the bank's ability tobear risk. Subject to inspection by the auditor, the riskmanagement system of IKB is continuously updatedand modified to reflect changing circumstances.Details on this can be found in the “Risk Report” sec-tion of the Management Report of the AG and Group.

Transparency and Information

We place great emphasis on transparency and infor-mation. Through a policy of timely and open commu-nication with shareholders and other participants inthe capital market, we intend to make the valuepotential of IKB stock completely transparent. Indoing so, we adhere to the principle of equal treat-ment: the same information must be made availableto all target groups at the same time. By checking theIKB website, private investors too can inform them-selves of the latest developments (including ad hocannouncements) in the Group without delay. More-over, significant events at the bank are reported inpress releases which also appear on the IKB website.In addition, the bank immediately publishes notifica-

Brought to you by Global Reports

tions from shareholders who, through purchase orsale or other means have obtained, exceeded orundershot 5 %, 10 %, 25 %, 50 % or 75 % of the votingrights in IKB. Furthermore, so-called Directors’ Deal-ings are published in the Notes and Group Notes withcorresponding information. At March 31, 2003,property requiring notification pursuant to Item 6.6

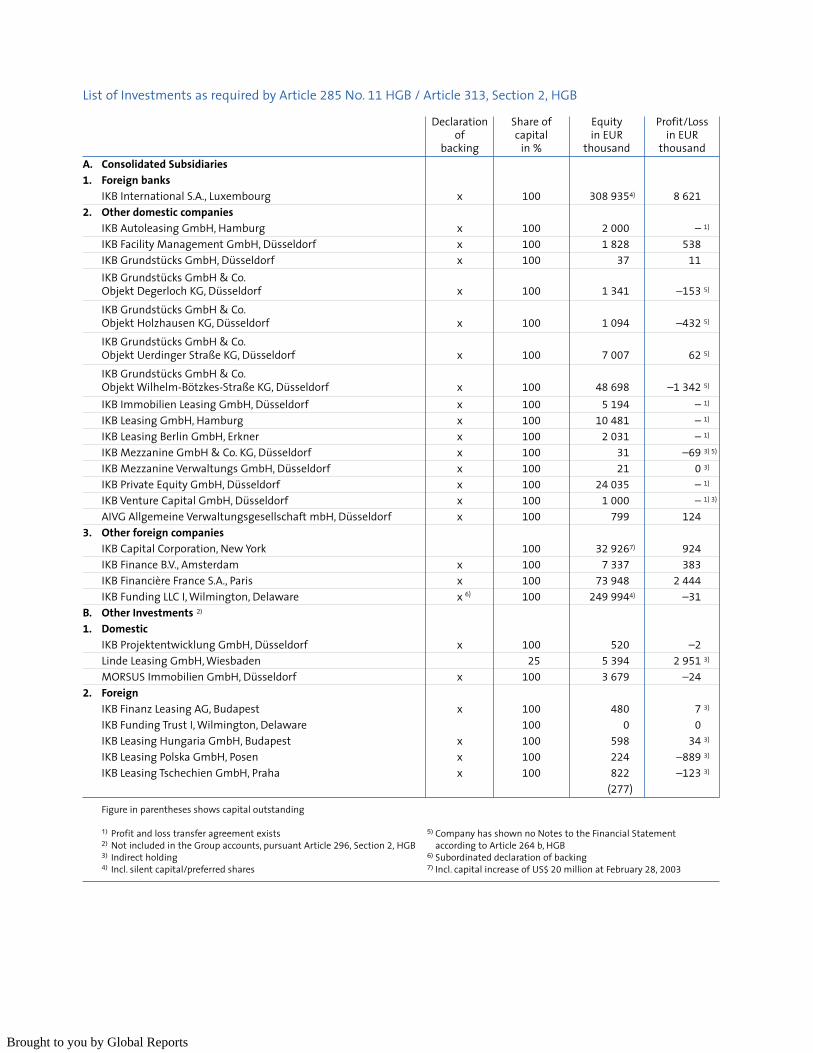

of the German Corporate Governance Code did notexist. The directorships of members of the Manage-ment Board and Supervisory Board are listed in theNotes and Group Notes. There are no share optionprogrammes or similar securities-related incentivesystems. All of our significant participations are listedat the IKB website, and can also be viewed in thecatalogue of our holdings contained in the Notes andGroup Notes.

Anyone interested can subscribe to our electronicnewsletter, which features up-to-date information onfinancial reports as well as containing ad hocannouncements and press releases.

Accounting and Auditing

The consolidated financial statement and the finan-cial statement of IKB are prepared in accordance withthe regulations contained in the German CommercialCode (HGB) In conjunction with the Accounting Regu-lations for Financial Institutions (RechKredV), as wellas taking into account relevant provisions of the Ger-man Stock Corporation Act (AktG). Furthermore, thefinancial statements of IKB Group are drawn up inaccordance with the Seventh Council Directive ofJune 13, 1983 based on Article 54 (3) (g) of the Treatyon consolidated accounts (83/349/EWG) and CouncilDirective of December 8, 1986 on the annualaccounts and consolidated accounts of banks andother financial institutions (86/635/EWG) and publi-cation requirements of the European Union. The

implementation of internationally recognisedaccounting principles is planned for the 2005/2006

financial year.

The Management Board has prepared a report onrelations with related companies for the 2002/2003

financial year, which has been submitted to theSupervisory Board. All agreements in connection withthe audit of the annual accounts recommended inthe German Corporate Governance Code have beenagreed with the auditor, KPMG Deutsche Treuhand-Gesellschaft Aktiengesellschaft Wirtschaftsprüfungs-gesellschaft of Düsseldorf.

First Declaration of Conformity pursuant

to Article 161 of the German Stock Corporation

Act (AktG)

On November 7, 2002, the Management Board andthe Supervisory Board submitted the first Declarationof Conformity pursuant to Article 161 of the GermanStock Corporation Act (AktG), declaring that IKB hadcomplied with all but four of the recommendationsof the Government Commission on the GermanCorporate Governance Code. One of these exceptionswas that a proxy named by IKB to exercise the votingrights of shareholders at the General Meeting in linewith their instructions had so far not been appointed.This is no longer applicable, because the bank willoffer voting by proxy at the General Meeting onSeptember 5, 2003.

In light of this innovation and the recommendationsof the Government Commission on the German Cor-porate Governance Code of May 21, 2003 for moretransparency in Management and Supervisory Boardcompensation, on July 7, 2003 the ManagementBoard and Supervisory Board submitted the follow-ing annual Declaration of Conformity, which share-holders can access at the IKB website (www.ikb.de)on a permanent basis.

Brought to you by Global Reports

Annual Declaration of Conformity pursuant to

Article 161 of the German Stock Corporation

Act (AktG)

The Management Board and Supervisory Board of IKBhereby declare that the recommendations of theGovernment Commission on the German CorporateGovernance Code published by the Federal Ministryof Justice in the official section of the electronic Fed-eral Gazette of July 4, 2003 since submission of thefirst Declaration of Conformity on November 7, 2002

and/or since the publication on July 4, 2003 of newrecommendations regarding greater transparency inManagement Board and Supervisory Board compen-sation, have been adhered to with the followingexceptions:

1. The corporation shall facilitate the personal exerciseof shareholders' voting rights. The corporation shallalso assist the shareholders in the use of proxies. TheManagement Board shall arrange for the appoint-ment of a representative to exercise shareholders'voting rights in accordance with instructions(Code Item 2.3.3).

The appointment of a proxy has not yet takenplace. Prior to the General Meeting on September5, 2003, for the first time we will be offering ourshareholders the services of proxies appointed bythe bank and empowered to vote in accordancewith their instructions. Thus, this recommendationof the German Corporate Governance Code willalso be acted upon.

2. If the company takes out D&O (directors and offi-cers' liability insurance) policy for the ManagementBoard and Supervisory Board, a suitable deductibleshall be agreed (Code Item 3.8).

Under the current Directors & Officers insurancepolicy for the Management Board and SupervisoryBoard, a retention has thus far not been agreed. In

our view, a retention would not be a suitablemeans of improving the motivation and sense ofresponsibility with which members of the Man-agement Board and Supervisory Board of IKB goabout their assigned tasks and functions. Besides,the primary object of this insurance is to protectthe bank against operational risks, not to protectthe personal assets of members of ManagementBoard and Supervisory Board. Furthermore, this is agroup insurance policy that also covers senior IKBexecutives. We do not consider it appropriate todifferentiate between members of the Manage-ment Board and Supervisory Board and employeesof the bank.

3. The salient points of the compensation system forthe Board of Managing Directors as well as the con-crete form of a share option programme or similararrangements of components with long-term incen-tives and risk character shall be published on thecompany’s website in generally understandableform and detailed in the annual report. In this con-text also information on the value of share optionsshall be provided (Code Item 4.2.3).

The Chairman of the Supervisory Board willprovide information concerning the principles ofthe compensation system and respective changesat the annual General Meeting of IKB.

4. Compensation of the members of the ManagementBoard shall be published in the Notes to the Consol-idated Financial Statement, subdivided into fixedand performance-oriented components and com-ponents relying on long-term incentives. Detailsshall be disclosed on an individualised basis (CodeItem 4.2.4).

Compensation of the members of the Manage-ment Board is listed, divided into fixed and variablecomponents. This is the first time this informationhas been provided in an IKB annual report. It is

Brought to you by Global Reports

essential for evaluating whether the ratio of fixedto performance-oriented compensation is appro-priate, and if the necessary performance incentiveshave been established for the members of theManagement Board. Compensation componentsrelying on long-term incentives, such as stockoptions or similar formulas, are not employed byIKB. We consider this information concerning theBoard of Managing Directors to be sufficient.

5. Compensation of the members of the SupervisoryBoard shall also take into account the chair andmembership in committees (Code Item 5.4.5).

Among the members of the two committees of theSupervisory Board (the Presiding Committee andthe Finance and Auditing Committee), only thework of the Staff Representative on the Financeand Auditing Committee is separately compen-sated. The chairman of the committees and theother members (shareholders’ representatives)receive no additional compensation. This involvesthe Chairman of the Supervisory Board and his twodeputies, who are in any case already compensatedfor taking on these responsibilities. The Chairmanreceives double, and each Deputy Chairman oneand a half times, the amount received by a regularmember of the Supervisory Board.

6. The compensation of members of the SupervisoryBoard shall be published in the Notes to the Consol-idated Financial Statement on an individualisedbasis and subdivided into components (Code Item5.4.5).

The compensation of members of the SupervisoryBoard is shown divided into fixed and variable pay-ments. The amount of fixed compensation and theformula for calculating the variable component areset by the General Meeting in the Articles of Asso-ciation of IKB. The Chairman of the SupervisoryBoard receives double, and each Deputy Chairman

one and a half times, the amount of a regularmember of the Supervisory Board. In addition, themember of the Finance and Auditing Committeefrom the group of Staff Representatives on theSupervisory Board receives EUR 10,000 per finan-cial year. We consider this information concerningthe compensation of the Supervisory Board to besufficient.

7. The Consolidated Financial Statements and theinterim reports shall be prepared under observanceof internationally recognised accounting principles(Code Item 7.1.1).

The implementation of internationally recognisedaccounting principles is planned for the2005/2006 financial year. Adherence to interna-tional standards of accounting for publicly tradedcompanies does not become compulsory untilthe financial year beginning on or after January1, 2005. We will comply with this deadline.

With the exception of the aforementioned Items2–7, the recommendations of the GovernmentCommission on the German Corporate GovernanceCode will also be complied with in future.

Düsseldorf, July 7, 2003

IKB Deutsche Industriebank AG

For the Supervisory Board For the Management Board

Brought to you by Global Reports

Honorary ChairmanProf. Dr. Dr.-Ing. E. h. Dieter Spethmann, DüsseldorfAttorney

ChairmanDr. h. c. Ulrich Hartmann, DüsseldorfChairman of the Supervisory Board E.ON AG

Deputy ChairmanProf. Dr.-Ing. E. h. Hans-Olaf Henkel, BerlinPresidentWissenschaftsgemeinschaftGottfried Wilhelm Leibniz e.V.

Deputy ChairmanHans W. Reich, Frankfurt (Main)Chairman of the Board of Managing DirectorsKreditanstalt für Wiederaufbau

Jörg Asmussen, BerlinMinisterial CouncillorFederal Ministry of Finance

Dr. Jürgen Behrend, LippstadtManaging PartnerHella KG Hueck & Co.

Jörg Bickenbach, DüsseldorfUndersecretary of StateNorth Rhine-Westphalia Ministry of Economicsand Labour

Wolfgang Bouché, Düsseldorf *

Hermann Franzen, DüsseldorfPersonally Liable PartnerPorzellanhaus Franzen KG

Herbert Hansmeyer, MunichFormer Member of the Board ofManaging DirectorsAllianz Aktiengesellschaft

Dr. Jürgen Heraeus, HanauChairman of the Supervisory BoardHeraeus Holding GmbH

Roswitha Loeffler, Berlin *

Wilhelm Lohscheidt, Düsseldorf *

Jürgen Metzger, Hamburg *

Roland Oetker, DüsseldorfAttorneyManaging Partner ROI Verwaltungsgesellschaft mbH

Dr.-Ing. E. h. Eberhard Reuther, HamburgChairman of the Supervisory Board Körber Aktiengesellschaft

Randolf Rodenstock, MunichManaging PartnerOptische Werke G. Rodenstock KG

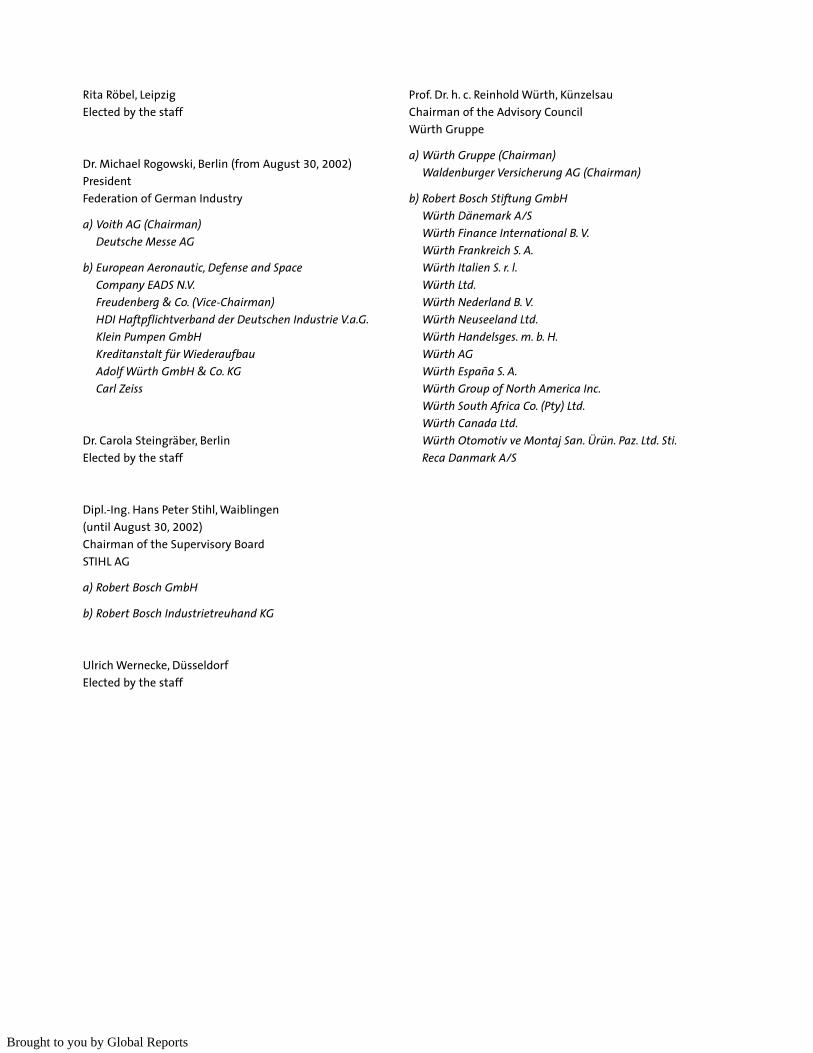

Rita Röbel, Leipzig *

Dr. Michael Rogowski, Berlin PresidentFederation of German Industry

Dr. Carola Steingräber, Berlin *

Ulrich Wernecke, Düsseldorf *

Prof. Dr. h. c. Reinhold Würth, KünzelsauChairman of the Advisory CouncilWürth Gruppe

Supervisory Board

* Elected by the staff

Brought to you by Global Reports

Advisory Board

ChairmanProf. Dr.-Ing. E. h. Hans-Olaf Henkel, BerlinPresidentWissenschaftsgemeinschaftGottfried Wilhelm Leibniz e.V.

Deputy ChairmanJürgen R. Thumann, DüsseldorfManaging Partner Heitkamp und Thumann GmbH & Co.

Dieter Ammer, HamburgChairman of the Board of Managing DirectorsTchibo Holding AG

Dr. rer. nat. Peter Barth, NeuwiedMember of the Advisory CouncilLohmann GmbH & Co. KG

Dipl.-Ing. Norbert Basler, GroßhansdorfDeputy Chairman of the Supervisory BoardBasler AG

Prof. Dipl.-Kfm. Thomas Bauer, SchrobenhausenChairman of the Board of Managing Directors BAUER Aktiengesellschaft

Josef H. Boquoi, StraelenChairman of the Advisory Councilbofrost*Familienunternehmen

Dr. Walter Botermann, WuppertalMember of the Boards of Managing DirectorsBarmenia Versicherungs-Gesellschaften

Dr.-Ing. Dirk Busse, GrefrathChairman of the Board of Managing DirectorsGirmes GmbH

Dr. Claus-Michael Dill, CologneChairman of the Board of Managing DirectorsAXA Colonia Konzern AG

Dipl.-Kfm. Martin Dreier, DortmundManaging PartnerDreier-Werke GmbH + Dreier Immobilien

Prof. Dr. phil. Hans-Heinrich Driftmann, ElmshornManaging PartnerPeter Kölln KGaA

Dr. Peter Fleischer, BonnChairman of the Board of Managing DirectorsDeutsche Ausgleichsbank

Hans-Michael Gallenkamp, OsnabrückManaging PartnerFelix Schoeller Holding GmbH & Co. KG

Werner Gegenbauer, BerlinPresidentBerlin Chamber of Industry and Commerce

Heinz Greiffenberger, BayreuthExecutive Director and Principal ShareholderGreiffenberger AG

Wolfgang Gutberlet, FuldaChairman of the Board of Managing Directorstegut ... Gutberlet Stiftung & Co.

Brought to you by Global Reports

Dipl.-Kfm. Dietmar Harting, EspelkampPersonally Liable PartnerHarting KGaA

Dr. Thomas Hertz, BerlinManaging DirectorBerlin Chamber of Industry and Commerce

Dr. Stephan J. Holthoff-Pförtner, EssenAttorney and Notary

Dr. Franz Wilhelm Hopp, DüsseldorfMember of the Board of Managing DirectorsERGO Versicherungsgruppe AG

Dr. Edgar Jannott, DüsseldorfMember of the Supervisory BoardERGO Versicherungsgruppe AG

Dr. Eckart John von Freyend, BonnChairman of the Board of Managing DirectorsIVG Immobilien AG

Martin Kannegiesser, VlothoManaging PartnerHerbert Kannegiesser GmbH & Co.

Dr. Jochen Klein, DarmstadtManaging PartnerDöhler-Euro Citrus Natural BeverageIngredients GmbH

Jan Kleinewefers, KrefeldManaging PartnerKleinewefers Beteiligungs-GmbH

Caio K. Koch-Weser, BerlinUndersecretary of StateFederal Ministry of Finance

Dr. Hermut Kormann, HeidenheimMember of the Board of Managing DirectorsJ. M. Voith AG

Prof. Dr.-Ing. Eckart Kottkamp, Bad OldesloeManaging DirectorHako Holding GmbH & Co.

Andreas Langenscheidt, MunichManaging PartnerLangenscheidt Verlagsgruppe KG

Erik Lescar, ParisDeputy Chief ExecutiveHead of Corporate & International BankingNatexis Banques Populaires

Dr. Kurt Merse, DüsseldorfChairman of the Supervisory BoardGARANT SCHUH + MODE AG

Josef Minderjahn, BerlinPartnerMKF-Folien GmbH Minderjahn + Kiefer

Siegmar Mosdorf, MunichMember of the Board of Managing DirectorsCNC-The Communication &Network Consulting AG

Brought to you by Global Reports

Klaus Oberwelland, BerlinPersonally Liable PartnerAugust Storck KG

Dipl.-Kfm. Jürgen Preiss-Daimler,WilsdruffManaging PartnerP-D Management Consulting GmbHand Preiss-Daimler Group

Dr. Günther Radtke, MeerbuschFormer Member of theBoard of Managing DirectorsAMB Aachener und MünchenerBeteiligungs-Aktiengesellschaft

Wolfgang Roth, LuxembourgVice-PresidentEuropean Investment Bank

Dr. Ingeborg von Schubert, BielefeldChairman of the Advisory CouncilE. Gundlach GmbH & Co. KG

Dr. Eberhard Schwarz, LahnsteinManaging DirectorZschimmer & Schwarz Chemie GmbH

Dr.-Ing. Hans-Jochem Steim, SchrambergManaging PartnerHugo Kern und Liebers GmbH & Co.

Dr. Alfred Tacke, BerlinUndersecretary of StateFederal Ministry of Economicsand Technology

Dipl.-Kfm. Rainer Thiele, Halle/SaaleManaging PartnerKATHI Rainer Thiele GmbH

Dr. Karl V. Ullrich, Freiburg i. Br.Managing DirectorWVIB Wirtschaftsverband IndustriellerUnternehmen Baden e. V.

Dr. Martin Wansleben, BerlinManaging Director Association of German Chambers ofIndustry and Commerce (DIHK)

Dr. Ludolf v. Wartenberg, BerlinManaging DirectorFederation of German Industry

Clemens Freiherr von Weichs, HamburgChairman of the Board of Managing DirectorsHERMES Kreditversicherungs-Aktiengesellschaft

Dr. Axel Wiesenhütter, KaiserslauternManaging PartnerSchuster & Sohn Kommanditgesellschaft

Dipl.-Ing. Albrecht Woeste, VelbertOwnerR. Woeste & Co. GmbH & Co. KG

Horst R. Wolf, HeidelbergMember of the Board of Managing DirectorsHeidelbergerCement AG

Brought to you by Global Reports

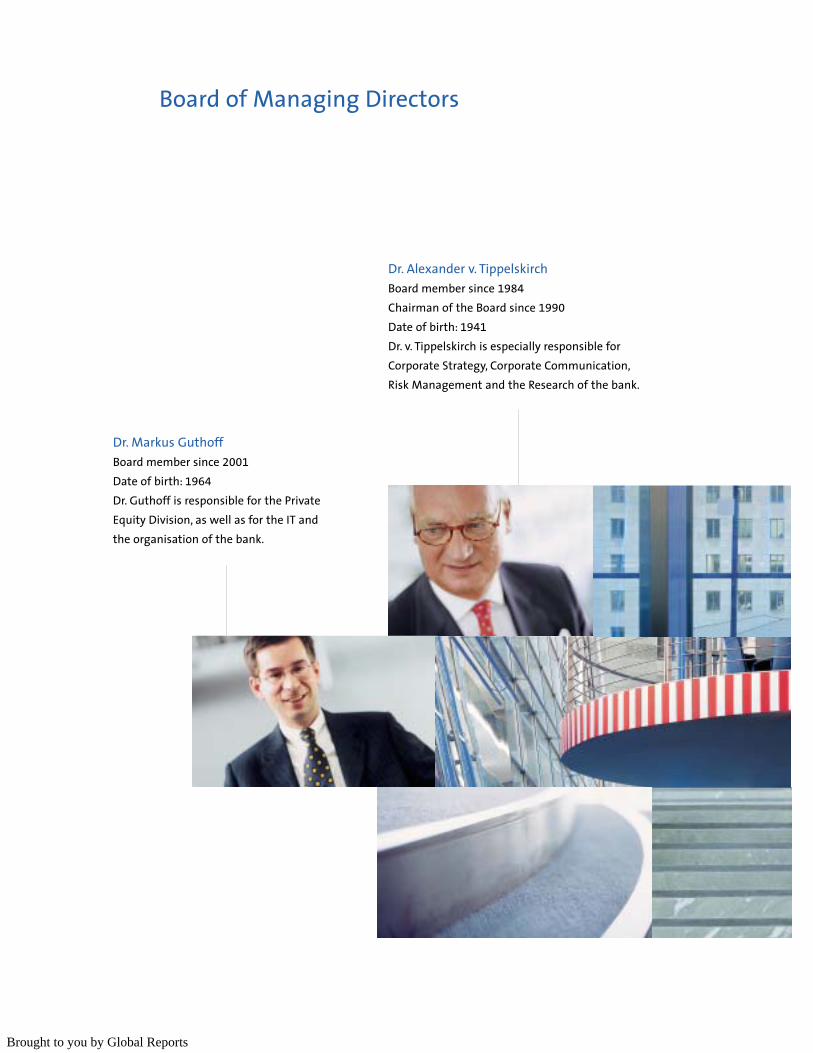

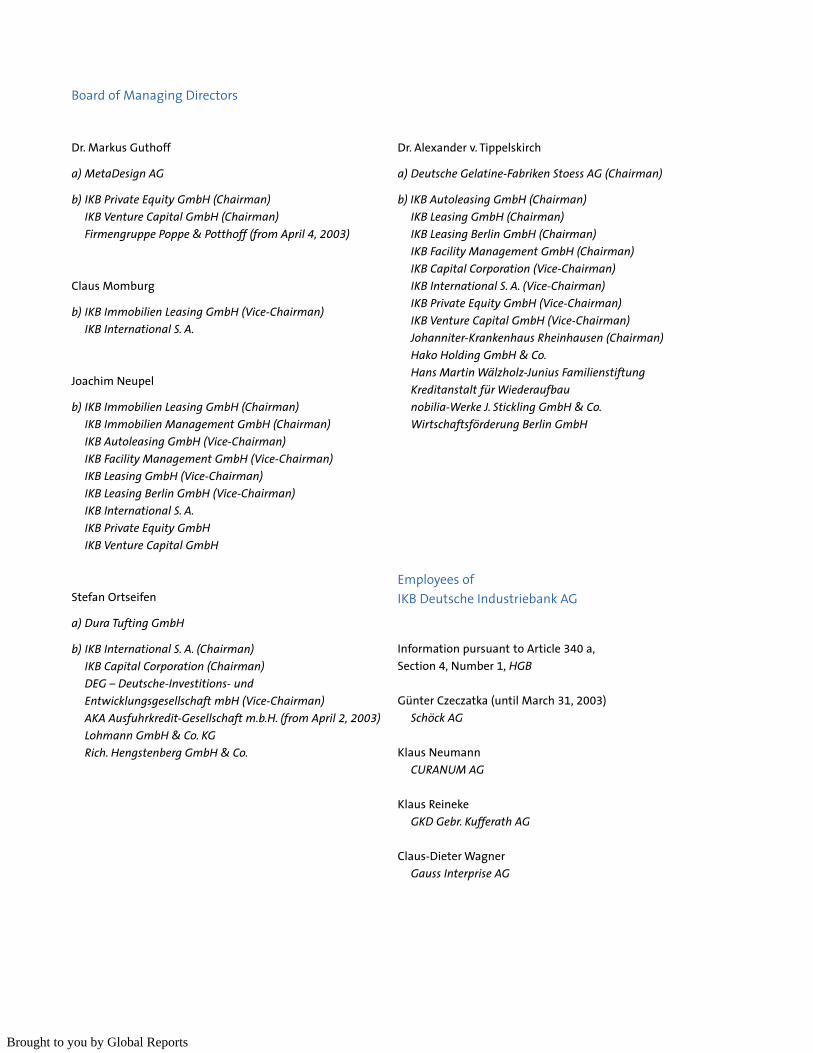

Board of Managing Directors

Dr. Markus GuthoffBoard member since 2001

Date of birth: 1964

Dr. Guthoff is responsible for the PrivateEquity Division, as well as for the IT andthe organisation of the bank.

Dr. Alexander v. TippelskirchBoard member since 1984

Chairman of the Board since 1990

Date of birth: 1941

Dr. v. Tippelskirch is especially responsible forCorporate Strategy, Corporate Communication,Risk Management and the Research of the bank.

Brought to you by Global Reports

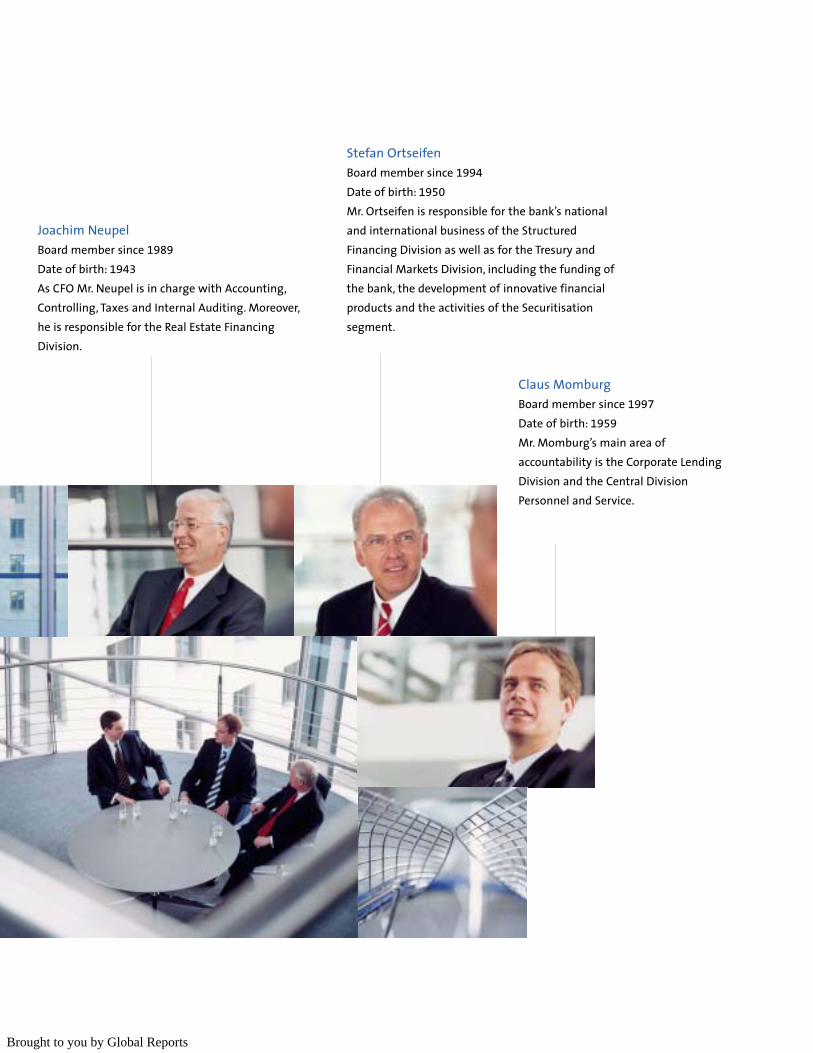

Claus MomburgBoard member since 1997

Date of birth: 1959

Mr. Momburg’s main area ofaccountability is the Corporate LendingDivision and the Central DivisionPersonnel and Service.

Joachim NeupelBoard member since 1989

Date of birth: 1943

As CFO Mr. Neupel is in charge with Accounting,Controlling, Taxes and Internal Auditing. Moreover,he is responsible for the Real Estate FinancingDivision.

Stefan Ortseifen Board member since 1994

Date of birth: 1950

Mr. Ortseifen is responsible for the bank’s nationaland international business of the StructuredFinancing Division as well as for the Tresury andFinancial Markets Division, including the funding ofthe bank, the development of innovative financialproducts and the activities of the Securitisationsegment.

Brought to you by Global Reports

Corporate LendingLeo von Sahr Berlin-LeipzigWolf-Herbert Weiffenbach

Helmut Laux Düsseldorf

Udo Belz Frankfurt

Hajo Köhler HamburgBurckhard W. Richers

Norbert Mathes Munich

Dr. Klaus Eisele StuttgartJoachim Rostek

Environment and Transport UnitHelmut Laux Düsseldorf

Division CoordinationClemens Jahn Düsseldorf

Real Estate FinancingKlaus Neumann DüsseldorfJoachim Schwarz

Private EquityRolf Brodbeck DüsseldorfRoland Eschmann

Structured FinancingDr. Frank Schaum DüsseldorfStefan Rensinghoff Frankfurt

London BranchFriedrich Frickenhaus

Paris BranchEric Schaefer

Treasury and Financial MarketsMichael Braun DüsseldorfWinfried Reinke

Market Units and their Heads

Brought to you by Global Reports

Central Divisionsand their Heads

Accounting, Controlling and TaxesChristoph Müller-MasiáJürgen Rauscher

Internal AuditingOliver Zakrzewski

Organisation and Information ManagementManfred Knols

Personnel and ServiceMartin Verstege

Legal Department and Officeof the Board of Managing DirectorsPanagiotis Paschalis

Risk ManagementFrank BraunsfeldClaus-Dieter Wagner

Corporate DevelopmentFrank Schönherr

Economics, Investor Relationsand Public RelationsDr. Kurt DemmerDr. Gert Schmidt

Subsidiariesand their Heads

IKB Capital Corporation, New YorkDavid Snyder

IKB International S.A., LuxembourgDr. Alfons SchmidRobert SpliidRaphael Karl Walisko

IKB Private Equity GmbH, DüsseldorfRolf BrodbeckRoland Eschmann

IKB Leasing GmbH, HamburgWolfgang BrzuskaMichael FichterWilhelm LindemannJoachim Mertzenich

IKB Immobilien Leasing GmbH, DüsseldorfAlexander BoyeHeribert Wicken

IKB Immobilien Management GmbH, DüsseldorfTheodor HonrathMauritz von StrachwitzHeribert Wicken

IKB Facility Management GmbH, DüsseldorfThomas Damrosch

Brought to you by Global Reports

I. Management Report

1. An Overview of the Financial Year

2. Risk Report

3. Performance of the Divisions

4. Outlook

Brought to you by Global Reports

Major Steps in Business Strategy

Moves of major strategic importance during the2002/2003 financial year were

• the ongoing development of our partnership withKfW;

• the opening of cooperations with Sal. Oppenheimand UniCredito Italiano; and

• expanded investment in international loan portfo-lios in a wide variety of asset categories.

Following the first full financial year of our strategicpartnership with KfW, the impact thus far has beenunreservedly positive, resulting in EUR 800 million inadditional loan business for the two organisationswith earnings of EUR 10 million.

But even more important is the fact that – in cooper-ation with KfW – we can continue to pursue withgreat commitment our role as a leading financier ofGermany’s medium-sized companies (Mittelstand).Particularly in difficult times like these, and especial-ly against the backdrop of Basel II and the highlyvolatile business behaviour of many of our competi-tors, this is an important message to our customers.

Likewise, a great deal was achieved during the pastfinancial year with regard to the concrete implemen-tation of our joint objectives. For example, we cooper-ated in developing a global loan facility that enablesus to set margins oriented to the creditworthiness ofthe individual borrower when extending public

industrial development loans rather than at a fixedmargin of 1 % as was previously the case. In themeantime, a number of other banks have applied forglobal loan facilities with KfW, a desirable develop-ment from the standpoint of regulatory and competi-tion policy.

In November 2002, furthermore, we set up a EUR 100

million mezzanine fund with KfW. This fund offerssilent participations at an amount of EUR 2.5 millionand EUR 8 million to our clients. This enables thesecompanies to improve their balance sheet ratios andratings, and thus to expand their room for manoeuvrewith respect to credit finance.

In February of this year we entered into a cooperationagreement with Sal. Oppenheim. Both banks havealmost identical target groups and a complementaryrange of products. Thanks to this agreement, we arenow able to offer our customers a complete array ofcapital market products, support during M&A trans-actions as well as comprehensive asset managementservices. For its part, Sal. Oppenheim can now offer itscustomers long-term corporate and acquisitionfinancing and arrange for Schuldscheindarlehen(certificates of indebtedness). As a means of under-scoring this agreement to cooperate, Sal. Oppenheimhas taken up an initial 3 % of IKB share capital.

In March 2003 we concluded an agreement to coop-erate with UniCredito Italiano. Together with itsinvestment unit, UniCredit Banca Mobiliare (UBM),we will be establishing a new subsidiary in Luxem-bourg offering consulting and financial services foroptimising the balance sheet structures of our cus-tomers.

1. An Overview of the Financial Year

Brought to you by Global Reports

During the past financial year we also expanded ourinvestments in international loan portfolios. Earningsfrom these transactions have since become signifi-cant enough to be reported separately; in this annualreport, and in conformity with the rules of DRSC(Deutsches Rechnungslegungs Standards Committee),these earnings are shown separately for the first timeunder the rubric of “Securitisation” as part of our seg-ment reporting procedures.

Our goal is to make a consistent, systematic transi-tion from Risk Taker to Risk Manager. This is mani-fested in our policy of using collateralised loan obliga-tions (CLOs) to outplace our own credit risks, therebyimproving our Principle I ratio. Moreover, by defreez-ing capital in this way we are able to invest in otherasset items like Mittelstand financing or loan portfo-lios. This also enables us to diversify our risk withregard to regions and sectors, while simultaneouslyleading to increased earnings in the form of commis-sion income.

A further important measure taken during the periodunder review was the increase in tier 1 capital,achieved by issuing EUR 450 million in hybrid capital.As a result, we succeeded in increasing our tier 1 cap-ital ratio to 7.4 % (2001/2002: 6.4 %).

Key Data

The business performance of the IKB Group duringthe 2002/2003 financial year is reflected in thefollowing key data:

• net interest income increased by 2.9 % to EUR 485

million (in the AG: a decline of 5.1 % to EUR 422

million)• net commission income rose by EUR 25 million to

EUR 64 million (AG: by EUR 28 million to EUR 82

million)• the interest margin for new loan accommodations

in the Group expanded to 1.68 % (previous year:1.44 %)

• administrative expenses increased by 6.5 % to EUR220 million (AG: by 6.0 % to EUR 173 million)

• other operating income declined by EUR 9 millionto EUR 20 million, while

• risk provisioning balance increased by EUR 8 mil-lion to EUR 183 million (AG: by EUR 12 million toEUR 153 million), with a simultaneous rise in netrisk provisions by EUR 44 million to EUR 248 millionas well as a EUR 36 million-increase in the result ofsecurities trading to EUR 65 million.

For the Group, this equates to an increase in the resultfrom ordinary activities of 4.1 % to EUR 167 million;for the AG the corresponding figure increased by14.2 % to EUR 183 million. The cost/income ratio forthe Group during the period under review came to38.6 % (previous year: 38.1 %); at 15.0 %, return onequity before tax remained unchanged from theprevious year’s level.

The Management Board has proposed to the Super-visory Board the payment of an unchanged dividendto shareholders of EUR 0.77 per share for the 2002/

2003 financial year. To reinforce the bank’s equitybase, EUR 43 million was transferred to reserves fromGroup net income for the year (AG: EUR 43 million).

Report of Dependency

We have prepared a report of dependency for theperiod under review for the first time. Please see ourcomments on this in the Notes to the financial state-ments. The final declaration of the ManagementBoard of the bank in the Report of Dependencystates: “In each of the transactions stated in thereport on relations with subsidiary companies, IKBreceived an appropriate consideration. This evalua-tion is based on the circumstances known to us at thetime of the reportable transactions. Measures pur-suant to Article 312 of the German Stock CorporationAct (AktG) were neither taken nor omitted.“

Brought to you by Global Reports

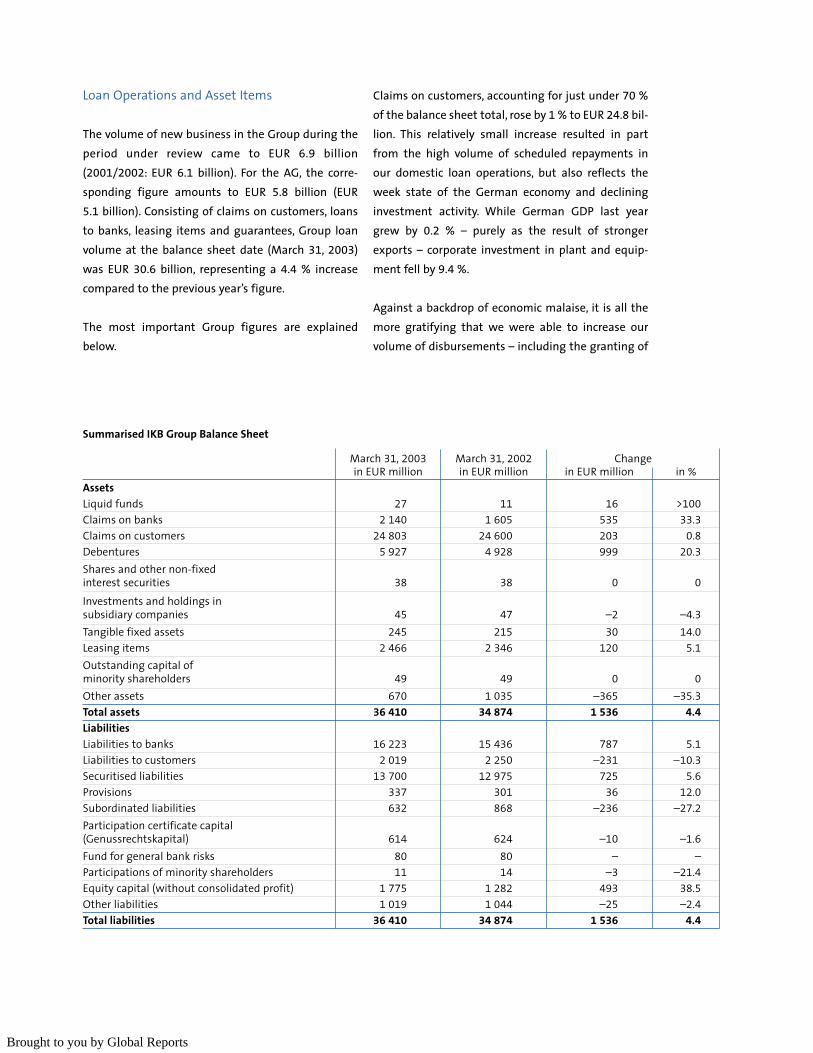

Loan Operations and Asset Items

The volume of new business in the Group during theperiod under review came to EUR 6.9 billion(2001/2002: EUR 6.1 billion). For the AG, the corre-sponding figure amounts to EUR 5.8 billion (EUR5.1 billion). Consisting of claims on customers, loansto banks, leasing items and guarantees, Group loanvolume at the balance sheet date (March 31, 2003)was EUR 30.6 billion, representing a 4.4 % increasecompared to the previous year’s figure.

The most important Group figures are explainedbelow.

Claims on customers, accounting for just under 70 %of the balance sheet total, rose by 1 % to EUR 24.8 bil-lion. This relatively small increase resulted in partfrom the high volume of scheduled repayments inour domestic loan operations, but also reflects theweek state of the German economy and declininginvestment activity. While German GDP last yeargrew by 0.2 % – purely as the result of strongerexports – corporate investment in plant and equip-ment fell by 9.4 %.

Against a backdrop of economic malaise, it is all themore gratifying that we were able to increase ourvolume of disbursements – including the granting of

March 31, 2003 March 31, 2002 Changein EUR million in EUR million in EUR million in %

AssetsLiquid funds 27 11 16 >100

Claims on banks 2 140 1 605 535 33.3

Claims on customers 24 803 24 600 203 0.8

Debentures 5 927 4 928 999 20.3

Shares and other non-fixedinterest securities 38 38 0 0

Investments and holdings insubsidiary companies 45 47 –2 –4.3

Tangible fixed assets 245 215 30 14.0

Leasing items 2 466 2 346 120 5.1

Outstanding capital of minority shareholders 49 49 0 0

Other assets 670 1 035 –365 –35.3

Total assets 36 410 34 874 1 536 4.4

LiabilitiesLiabilities to banks 16 223 15 436 787 5.1

Liabilities to customers 2 019 2 250 –231 –10.3

Securitised liabilities 13 700 12 975 725 5.6

Provisions 337 301 36 12.0

Subordinated liabilities 632 868 –236 –27.2

Participation certificate capital(Genussrechtskapital) 614 624 –10 –1.6

Fund for general bank risks 80 80 – –

Participations of minority shareholders 11 14 –3 –21.4

Equity capital (without consolidated profit) 1 775 1 282 493 38.5

Other liabilities 1 019 1 044 –25 –2.4

Total liabilities 36 410 34 874 1 536 4.4

Summarised IKB Group Balance Sheet

Brought to you by Global Reports

certificates of indebtedness (Schuldscheindarlehen) –by nearly 17 % during the year under review. We thussucceeded in expanding our share in a more or lessstagnant credit market. This was the result of inten-sive, goal-oriented marketing as well as the highstanding enjoyed by IKB in the German banking sec-tor. Because this coincided with a high volume ofrepayments – as already mentioned – the loan vol-ume of our Corporate Lending Division at the balancesheet date was slightly lower than at March 31, 2002.

A different state of affairs pertained in the Real EstateFinancing Division, where a slightly lower volume ofnew business compared to the previous year – owingto the special repayment structure involved in realestate assets – was offset by an increase in loan vol-ume. An upsurge in new business in the StructuredFinancing Division also resulted in a moderate rise inloan volume.

However, the clearest increases in new business andloan volume alike occurred in the Securitisation seg-ment, which – as already stated – encompasses ourinvestments in international loan portfolios in differ-ent asset categories. While new business in thissegment rose to EUR 1.4 billion (EUR 0.7 billion), theloan volume at the balance sheet date increased toEUR 1.9 billion (EUR 0.7 billion). Liabilities arisingfrom guarantees, which should be seen in the contextof claims on customers, rose by EUR 0.4 billion toEUR 2.2 billion.

Owing to the balance sheet date, claims on banksrose by 33 % to EUR 2.1 billion. This increase relatesexclusively to overnight loans, whereas medium- andlong-term claims on banks both declined.

We augmented our portfolio of debentures by 20 %to EUR 5.9 billion, the bulk of which was used as col-lateral in tendering operations with the Bundesbank.

Under the rubric of debentures, we grew our securi-tised loan business by EUR 0.6 billion to EUR 1 billionby specifically acquiring securities representing ashare in a pool of securitised portfolios.

Our portfolio of leasing items also increased, growingby 5 % to EUR 2.5 billion (real estate leasing: EUR 1.8

billion; equipment leasing: EUR 0.7 billion); this risereflects the ongoing expansion of our activities in thisdomain.

The Group balance sheet total grew by 4 % or EUR 1.5

billion to EUR 36.4 billion; for the AG, the increasecame to 5 %, resulting in a balance sheet total of EUR36.8 billion.

Funding

We funded our operations by taking up money mar-ket funds, by issuing debentures, and by taking uphybrid capital. Owing to the moderate trend in claimson customers, long-term liabilities to banks con-tracted slightly. Conversely, securitised liabilities roseby EUR 0.7 billion to EUR 13.7 billion.

Equity

Our objective continues to be to strengthen theGroup’s equity position without dilution of our sharecapital. Accordingly, we issued two silent participa-tions during the past financial year, thereby increas-ing our hybrid capital by EUR 450 million to EUR 620

million. Specifically, we placed a EUR 250 million bondwith private investors in June of last year, whichcounts as tier 1 capital in the Group. In addition, viaCapital Raising GmbH, we took in a silent participa-tion worth EUR 200 million in November. Moreover,we augmented our revenue reserves by EUR 43 mil-lion to EUR 362 million. The bullet maturity havingbeen reached, subordinated liabilities fell by EUR 236

Brought to you by Global Reports

million to EUR 632 million. The measures outlinedhere led to a EUR 0.5 billion-increase in tier 1 capitalto EUR 1.9 billion; following regulatory definitionequity grew by a good EUR 0.2 billion to EUR 3.1

billion.

At March 31, 2003, the Group fulfilled Principle Icapital ratio with 12.1 % (2000/2001: 12.1 %); the tier1 capital ratio was 7.4 % (6.4 %). In the AG, the corre-sponding figures came to 12.0 % (11.9 %) and 6.4 %(6.0 %). These ratios show that we possess sufficientequity to keep the bank growing.

April 1, 2002 to April 1, 2001 to ChangeMarch 31, 2003 March 31, 2002in EUR million in EUR million in EUR million in %

Interest income from loan operations andmoney market transactions, fixed interestsecurities and government-inscribed debt,and earnings from leasing operations 3 223.2 3 215.2 8.0 0.2

Earnings from securities and holdings 1.8 4.8 –3.0 –62.5

Interest expenditure,expenditure and scheduled depreciationrelating to leasing operations 2 740.0 2 748.7 –8.7 –0.3

Net interest income 485.0 471.3 13.7 2.9

Commission income 76.0 44.8 31.2 69.6

Commission expenditure 11.9 5.3 6.6 >100

Net commission income 64.1 39.5 24.6 62.3

Net result from financial operations 0.8 1.9 –1.1 –57.9

Personnel expenditure 137.8 133.4 4.4 3.3

Salaries and wages 110.7 101.1 9.6 9.5

Social security contributions/expenditurefor retirement benefits and pensions 27.1 32.3 –5.2 –16.1

Other administrative expenditure 82.1 73.1 9.0 12.3

Administrative expenditure 219.9 206.5 13.4 6.5

Balance of other operating income and expenditure 20.2 29.3 –9.1 –31.1

Risk provisioning balance –183.4 –175.2 8.2 4.7

Result from ordinary activities 166.8 160.3 6.5 4.1

IKB Group Operating Results

March 31, 2003 March 31, 2002 Changein EUR million in EUR million in EUR million in %

Subscribed share capital 225 225 – –

Hybrid capital 620 170 450 >100

Capital reserves 568 568 – –

Revenue reserves 362 319 43 13.5

Fund for general bank risks 80 80 – –

Tier 1 capital 1 855 1 362 493 36.2

Participation certificate capital(Genussrechtskapital) 614 624 –10 –1.6

Subordinated liabilities 632 868 –236 –27.2

Total liable funds 3 101 2 854 247 8.7

IKB Group Total Liable Funds

Brought to you by Global Reports

Earnings

Group net interest income grew by 2.9 % to EUR 485

million. This increase was due primarily to expansionin the volume of new loans as well as the improve-ment of the interest margin.

Also encouraging is the increase in net commissionincome by EUR 25 million to EUR 64 million. A goodthird of net commission income during the periodunder review resulted from revenue generated by thedivisions, while roughly two thirds derived from theSecuritisation segment.

Administrative expenses rose by 6.5 % to EUR 220

million. Here, the increase in personnel expenditure,which rose by 3.3 % to EUR 138 million, reflects twoopposing trends: on the one hand, wages and salariesgrew by 9.5 % – due not least to the increase in theaverage number of staff, which rose by 83 to 1,433;on the other hand, owing to the relatively low alloca-tion to pension provisions compared to the previousyear, social contributions and expenditure for retire-ment benefits and pensions declined by 16.1 %. Otheradministrative expenses grew by 12.3 % to EUR 82.1

million. Contributing first and foremost to this trendwere higher spending on data processing and adver-tising, as well as increased consulting, expert andlegal costs relating to projects for fulfilling regulatoryand legal requirements such as Basel II, the MinimumRequirements for the Lending Business of CreditInstitutions (MaK), or preparations for the transitionto International Accounting Standards.

At EUR 20 million, other operating income was EUR9 million below the figure for the 2001/2002 finan-cial year, when we generated considerable incomefrom the sale of our former headquarters building inDüsseldorf. During the period under review, otheroperating income came chiefly from exit earnings

from investments by our Private Equity Division. Inthe AG, other operating income rose to EUR 4 million(–EUR 37 million), since no further losses by PrivateEquity needed to be absorbed following the success-ful turnaround of the division.

Risk Situation

The risk situation during the period under reviewremained difficult. Two years in a row of economicstagnation in Germany have taken a conspicuous tollon business, with the number of corporate insolven-cies soaring to 37,700, up from 32,400 the yearbefore.

The chief reasons for this unsatisfactory – and in cer-tain sectors, such as retail and construction, even dra-matic – development, are the weak state of the worldeconomy and (even more so) growth-restraining eco-nomic policies at home. A glance at corporate earn-ings on the one hand and the jobless figures on theother makes this abundantly clear.

According to initial estimates of the German Federa-tion of Industry, some 40 % of German companiesfailed to make a profit in 2002. This is due in part tothe country’s comparatively heavy levels of taxation,of course, but most of all it has to do with the highsocial welfare contributions. The German govern-ment’s stated intention was to push the ratio of socialwelfare contributions to gross wages to below 40 %.But in 2002 this ratio was 42 % with a continuingtrend to increase.

On top of this comes the added burden of the Ger-many’s environmental tax. Introduced in 1999 withthe aim of reducing the pressure on the country’spension system, it has thus far failed to do so, despiteno fewer than four rate hikes. In concrete terms, if weadd the impact of the environmental tax to the cur-rent social welfare contribution ratio of 42 %, the bur-den this year rises to over 44 %.

Brought to you by Global Reports

Two things should be clear here: (1) German compa-nies are caught in a cost trap, with their internationalcompetitiveness further impeded by the rise in thevalue of the euro; (2) at home, a decline in real dis-posable income in private households has led to a col-lapse in consumer demand in many sectors. For com-panies, this has meant a drop in orders, sales andprofits. They have cut their investment spendingaccordingly – by more than 15 % over the last twoyears – leading in turn to layoffs and greater numbersof unemployed.

The country’s government and the social securityadministration responded by raising the level of con-tributions again, further undermining the interna-tional competitiveness of German companies. Theseinterrelationships represent a veritable vicious circlefrom which there can be no escape without deep-running reform.

This was the environment in which our customershad to operate during the year under review. Theearnings performance of many of our borrowers wascorrespondingly disappointing. As a result – asalready mentioned – we were forced to increase ournet provisions for risk by EUR 44 million to EUR 248

million. However, because our liquidity reserveincome grew by EUR 36 million to EUR 65 million, therisk provisioning balance expanded by just EUR 8

million to EUR 183 million. For the AG the correspon-ding figures are EUR 12 million and EUR 153 million.

A close analysis of our provisions for bad and doubt-ful debts reveals that we remained unscathed by Ger-many’s more spectacular corporate failures, e.g. Kirch,Babcock or Holzmann. We were affected instead by ahost of smaller cases – especially in western Germany– in which we had to take charges ranging in sizefrom EUR 1 million to EUR 3 million. In eastern Ger-many a different pattern is apparent: here we had to

make additional provisions for old loans in particular.Though we had already substantially adjusted thevalue of these loans in recent years, it has sincebecome apparent that there is practically no second-ary market for these assets – and therefore no accept-able prices.

A regional breakdown for the period under reviewshows that 43 % of provisions for bad and doubtfuldebts relate to companies in eastern Germany,though the region accounts for only 23 % of totalloan exposure. This means that we will have to con-tinue to set aside a disproportionate amount of pro-visions for loans in eastern Germany. The oppositesituation pertains in western Germany, whichaccounts for 40 % of provisions for bad debts but59 % of total loan exposure. Comprising 14 % of totalloan volume, our international operations account for12 % of provisions for bad debts.

At March 31, 2002, Group’s stock of provisions forspecific and general bad debts totalled EUR 953

million (previous year: EUR 875 million), and in the AGto EUR 833 million (EUR 788 million).

Result from Ordinary Activities

The result from ordinary activities for the Group cameto EUR 167 million, thus exceeding the previous year’stotal by 4.1 %. The corresponding figures for the AGwere EUR 183 million and 14.2 %. The EUR 16 million-difference is explained primarily by leasing-typicalcosts and earnings patterns in the real estate leasingdomain, where full consolidation affected the Groupbut not the AG.

Brought to you by Global Reports

Proposal for the Allocation of Profits

Group net income for the year for the period underreview amounted to EUR 85.8 million (EUR 83.1 mil-lion). A loss resulting primarily from the consolidationof special purpose entities of IKB Immobilien LeasingGmbH was carried forward from the 2000/2001

financial year. Following the allocation of EUR 43 mil-lion to other revenue reserves, unappropriated profitin the Group came to EUR 11.1 million.

Net income for the year in the AG amounted to EUR110.4 million (EUR 96.1 million). After the allocationof EUR 42.6 million to other revenue reserves, unap-propriated profit came to EUR 67.8 million. Wepropose to the General Meeting that this profit bedisbursed in the form of an unchanged dividend ofEUR 0.77 per share.

2. Risk ReportObjectives, Strategies and Organisationof Risk Management

Objectives and Strategies

Bearing the stamp of a risk culture characterised by aconservative approach, risk management at IKB isbased on the ability of the bank to bear risk, and theupper limits of risk derived there from and prescribedby the Management Board. Measurement of the abil-ity to bear risk is oriented to the current rating of IKB,A1 and A+ respectively. This means that the extent ofrisk coverage defined by the Management Board issufficient to protect the bank even in scenarios ofextreme risk. The cornerstone of our risk strategy con-

tinues to be the comprehensive and continuous iden-tification, measurement and monitoring of all risksrelating to the operations of the bank, and embed-ding the findings in the risk/profit managementof IKB.

Risk Organisation

The clearly defined, highly functional organisation ofour risk management system guarantees the func-tionality and effectiveness of the bank’s risk manage-ment process. The delimitation of tasks and areas ofresponsibility is documented in a risk managementhandbook. Embracing all bank-internal and legalrequirements, this regulation lays down guidelines,which, in connection with specific organisationaldirectives, establish the principles of the IKB risk man-agement system.

Drawing on the concepts of the Basel Committee onBank Supervision regarding the Capital Backing ofBanks (Basel II), as well as the Minimum Require-ments for the Lending Business of Credit Institutions(MaK), published by Germany’s Federal FinancialSupervision Authority on December 20, 2002, princi-ples on the management of loan risk were formulat-ed which define quality standards of the organisationof risk management, and which, in accordance withthe MaK, are to be implemented by mid 2004.

Central elements of the MaK are above all a morerestrictive organisational separation of market unitsfrom back-office functions (independent voting andrisk monitoring), as well as directives on the structur-ing of loan processes and reporting arrangements.IKB has always separated the Risk ManagementDepartment as back-office unit from the marketunits with respect to disciplinary power and function.Whereas our customer service officers act as the pri-mary point of contact for customers on all questionsof loan operations, the Risk Management Depart-

Brought to you by Global Reports

ment carries out an objective and independent analy-sis of each individual loan commitment, as well asassessing its creditworthiness. By dividing risk man-agement from risk controlling, IKB has adopted addi-tional measures necessary for monitoring risks, mov-ing beyond the requirements defined in the MaK. Inthis context a close intermeshing of the expertiseembodied in these departments Is guaranteed whileat the same time maintaining different points ofemphasis with regard to the respective tasks.

Management Board. The entire Management Boardis responsible for IKB’s risk management inasmuch asit defines risk policy in the form of a clear definitionof strategy, the types of business, and the acceptableaggregate risk within the framework of the bank’sability to bear risk. Thus, the bank is already in com-pliance with many of the requirements contained inthe MaK with respect to the formulation of a loan riskstrategy.

Risk Committees. The setting up of specific commit-tees for combining and monitoring risk-relevant deci-sions (asset/liability management, investment, creditrisk and product committees) supports the risk man-agement activities and decision-making process ofthe Management Board. These committees areresponsible both for fundamental questions of policyand decisions on specific transactions, based on theparameters defined by the Board. They are composedof members of the Board and the operational divi-sions as well as representatives of the Risk Manage-ment and Risk Control Departments.

Risk Management. The Risk Management Depart-ment is responsible for the implementation andenforcement of Group-wide risk standards for theloan business in the divisions and departments, aswell as for loan portfolio management. Among the

basic tasks of the Risk Management Department is,in particular, the entire loan sanctioning process,in which it exercises its own loan approval powers.Risk Management is also responsible for calculatingand recommending an appropriate risk provisionfor identified risks. Thus, the Risk ManagementDepartment represents a back-office function asdefined by the MaK.

In order to control loan risk, Risk Management issupported in the individual divisions by loan offices,which, however, are not defined as back-office unit.Loan decisions – with the exception of minor deci-sions permitted by the MaK – are made exclusively bythe back-office units.