60

Anti-fraud & Corruption Strategy January 2012

Anti-fraud & Corruption Strategy

January 2012

CONTENTS Page ANTI FRAUD POLICY 3 Section 1 INTRODUCTION 5 Section 2 CULTURE 6 Section 3 PREVENTION 7 3.1 The Council's Responsibilities 7 3.2 The Role of Members 7 3.3 The Role of Managers 7 3.4 Recruitment Procedures 8 3.5 Responsibilities of Staff 8 3.6 Conflicts of interest 9 3.7 Official Guidance 9 3.8 The Role of Internal Audit 9 3.9 The Role of Fraud and Error Team 9 3.10 The Role of External Audit 10 3.11 Co-operation with others 10 Section 4 DETERRENCE 11 4.1 Prosecution Policy 11 4.2 Recovery 11 4.3 Disciplinary Action 11 4.4 Publicity 12 Section 5 DETECTION AND INVESTIGATION 13 Section 6 AWARENESS AND TRAINING 15 Section 7 MONEY LAUNDERING 16 Section 8 BRIBERY ACT 17 Section 9 CONCLUSIONS 18 Appendix 1 Fraud Response Plan 19 Appendix 2 Confidential Reporting Policy 33 Appendix 3 Prevention of Money Laundering Procedures 38 Appendix 4 Officer Code of Conduct 42 Appendix 5 Ant-Bribery Policy Statement 56

2

ANTI-FRAUD POLICY

Broxbourne Borough Council is committed to high legal, ethical and moral standards, and the proper accountability of public funds. The Council views fraud and corruption very seriously and will not tolerate fraud and corruption in the administration of its responsibilities, whether from inside or outside the authority. The Council’s expectation of propriety and accountability is that members and staff at all levels will lead by example in ensuring adherence to legal requirements, rules, procedures and practices. The Council also expects that individuals and organisations with which it comes into contact will act towards the authority with integrity, and without thought or actions involving fraud and corruption. The framework in place to reduce the likelihood of fraud is: The Council has an effective anti fraud and corruption policy and maintains a culture that

will not tolerate fraud or corruption.

Officer and Member Codes of Conduct are in place to ensure that members and staff act with integrity and lead by example.

Senior managers are required to deal swiftly and firmly with those who defraud or attempt to defraud the Council or who are corrupt.

High standards of conduct are promoted amongst members by the Standards Committee.

The maintenance of registers of interests in which any hospitality or gifts accepted by members or officers must be recorded.

Confidential reporting procedures are in place, are publicised and operate effectively.

Standard contract clauses are used which prohibit fraud and corruption.

A benefits fraud hotline is operational, details of which are displayed on the Council's website. It is also possible to report suspected fraud by downloading a ‘report suspected fraud’ form from the Council’s website or emailing the Fraud and Error Team, details of which are provided on the Council’s website.

Additionally, the Council:

maintains an Internal Audit Section to be an independent appraisal function for the review of the Council’s internal control system as a contribution to the proper, economic, efficient and effective use of resources.

maintains a Fraud and Error Team who play a key role in both the prevention, detection and investigation of housing benefit and council tax benefit fraud.

recognises the importance of criminal prosecution in deterring fraud and will seek the prosecution of offenders where appropriate and in line with stated policy.

supports the work of the police and other external agencies, such as the Department for Work and Pensions, in fighting fraud and corruption in the public sector.

is a member of the National Anti-Fraud Network (NAFN).

subscribes to the Housing Benefit Matching Service (HBMS).

participates in the National Fraud Initiative (NFI).

3

This policy applies to any irregularity or suspected irregularity which concerns Broxbourne Borough Council, involving staff, members and/or external parties. Any investigation required will be conducted without regard to any person's relationship to the Council, position or length of service.

This document details the Council's overall strategy for dealing with fraud and corruption. It should be read in conjunction with the Fraud Response Plan (Appendix 1) which details the operational procedures put in place by the Council to respond to suspicions or allegations of fraud.

4

Section 1 INTRODUCTION

Broxbourne Borough Council provides community leadership and quality services. The 2009 Corporate Assessment confirmed that the Council is performing well in carrying out its functions and responsibilities. The Council will always adopt a culture of openness and fairness. It expects members and staff to adopt the highest standards of propriety and accountability. It expects the same from organisations that it has dealings with, e.g. suppliers, contractors and partners. This strategy document embodies a series of measures designed to frustrate any attempted fraudulent or corrupt act and the steps to be taken if such an act occurs or is suspected. It should be read in conjunction with the Fraud Response Plan which is included at Appendix 2. The Council is firmly committed to dealing with fraud and corruption and will deal equally with perpetrators from inside (members and staff) and outside the Council. In addition, there will be no distinction made in investigation and action between cases that generate financial benefits and those that do not. In applying this strategy regard will be had to all relevant Council policies. The Council is aware of the high degree of external scrutiny of its affairs by a variety of bodies. These are important in highlighting any areas where improvements can be made and give guidance to the Council. The Audit Commission defines fraud and corruption as: Fraud – “the intentional distortion of financial statements or other records by persons

internal or external to the authority which is carried out to conceal the misappropriation of assets or otherwise for gain”. In addition, fraud can also be defined as “the intentional distortion of financial statements or other records by persons internal or external to the authority, which is carried out to mislead or misrepresent”.

Corruption – “the offering, giving, soliciting or acceptance of an inducement or reward

which may influence the action of any person”.

This definition can be extended to cover “the failure to disclose an interest in order to gain financial or other pecuniary gain.”

5

Section 2 CULTURE

Members and employees play an important role in creating and maintaining a culture where fraud and corruption are not tolerated. They are positively encouraged to raise concerns regarding fraud and corruption, irrespective of seniority, rank or status, in the knowledge that such concerns will, wherever possible, be treated in confidence. The prevention and detection of fraud and corruption and the protection of the public purse are everyone’s responsibility. In addition, fraud risk is considered as part of the Council’s overall risk management arrangements. Concerns must be raised when members or employees reasonably believe that one or more of the following has occurred is in the process of occurring or is likely to occur:

a criminal offence

a failure to comply with a statutory or legal obligation

improper unauthorised use of public or other funds

improper use or misappropriation of assets

a miscarriage of justice

maladministration, misconduct or malpractice

endangering of an individual’s health and safety

damage to the environment

any other similar occurrences

deliberate concealment of any of the above.

The procedure for raising concerns is detailed in the Fraud Response Plan.

Management will ensure that any allegations received in any way, including anonymous letters or phone calls, will be taken seriously and investigated in an appropriate manner, subject to legislative requirements.

Broxbourne Borough Council will deal firmly with those who defraud the Authority, or who are corrupt, or who are responsible for financial malpractice.

When fraud or corruption has occurred because of a breakdown in the Council's systems or procedures, the Borough Management Team (BMT) will ensure that appropriate improvements in systems of control are implemented to prevent a recurrence.

Any significant control issues are required to be reported in the Annual Governance Statement along with actions taken to address the issue.

6

Section 3 PREVENTION

3.1 The Council's Responsibilities

The Local Government Act 1972 states that “every local authority shall make arrangements for the proper administration of their financial affairs and shall secure that one of their officers has responsibility for the administration of those affairs”. At Broxbourne Borough Council, the Director of Resources takes on this responsibility. It is for this reason that Financial Regulations (paragraph 6.1) require that the Director of Resources be informed of any actual or suspected fraud or irregularity.

The Statement on the Role of the Finance Director in Local Government states that the Director of Resources has a responsibility for ‘implementing appropriate measures to prevent and detect fraud and corruption’. However, it is recognised that the performance of this responsibility will fall directly on line management and may involve any of the Council's staff. 3.2 The Role of Members As elected representatives, all members of the Council have a duty to citizens to maintain the highest standards of conduct and ethics. This is achieved through compliance with the Members’ Code of Conduct, the Council’s financial regulations and standing orders, and other relevant legislation.

Members sign to the effect that they have read, understood and will comply with the Code of Conduct when they take office. These conduct and ethical matters are specifically brought to members' attention during induction and include the declaration and registration of interests. The Head of Legal Services, as the Council's appointed Monitoring Officer, advises members of new legislative or procedural requirements. 3.3 The Role of Managers Managers are responsible for ensuring that an adequate system of internal control exists within their area of business activity and that these controls operate effectively. Thus, the responsibility for the prevention and detection of fraud and corruption rests primarily with managers. Managers must assess the types of risk involved in their area, and review and test the control systems for which they are responsible. Internal Audit has a role in facilitating this process by supporting managers. Managers at all levels are responsible for the communication and implementation of this strategy in their work area. They are also responsible for ensuring that staff are aware of expected standards of conduct as detailed in the Officer Code of Conduct, the Council’s financial regulations and standing orders, and that the requirements of each are being met in their everyday business activities. Managers are expected to strive to create an environment in which their staff feel able to approach them with any concerns they may have about suspected irregularities. Where they are unsure of the procedures, they must refer to the information in the Confidential Reporting Policy (see Appendix 2 and Working for Broxbourne). Special arrangements will apply where staff are responsible for cash handling or are in charge of financial systems and systems that generate payments, for example payroll, benefits or council tax. Managers must ensure that relevant training is provided for staff

7

(see Section 6 - Awareness and Training). Checks must be carried out at least annually to ensure that proper procedures are being followed. During any investigation procedure, the investigator will work closely with management. 3.4 Recruitment Procedures

The Council recognises that a key preventative measure in dealing with fraud and corruption is for managers to take effective steps at the recruitment stage to establish, as far as possible, the honesty and integrity of potential employees, whether for permanent, temporary or casual posts.

The Council has a formal recruitment checking process, which contains appropriate safeguards on matters such as written references and verifying qualifications held. As with other public bodies, criminal record checks are undertaken on staff seeking to work with children and vulnerable adults. In addition, disclosure of criminal records is obtained for staff seeking to work in professional fields. Further checks will be introduced in areas where an increased risk of potential fraud and corruption has been identified. The Head of Personnel and Payroll will keep under review the checks that legislation allows. 3.5 Responsibilities of Staff

Every member of staff has a duty to ensure that public funds are safeguarded, whether they are involved with cash or payments systems, receipts, stock or dealing with contractors or suppliers. Staff should alert their line manager where they believe the opportunity for fraud exists because of poor procedures or lack of effective overview.

Employees are governed in their work by the Council’s standing orders and financial regulations, and various policies (e.g. health and safety, IT strategy and IT security). These documents can be found on the Council’s intranet. Included in the Officer Code of Conduct are guidelines on gifts and hospitality and guidelines associated with professional and personal conduct and conflicts of interest.

As stewards of public funds, Council staff must have, and be seen to have, high standards of personal integrity. This is achieved through compliance with the Officer Code of Conduct. For example, staff should not accept gifts, hospitality or benefits of any kind from a third party, which might be seen to compromise their integrity. The Council supports the Seven Principles of Public Life set out in the Nolan Report: Standards in Public Life. These are included in the Officer Code of Conduct at Appendix 4.

Staff are responsible for ensuring that they follow the instructions given to them by management, particularly in relation to the safekeeping of the assets of the Council. These will be included in induction training and procedure manuals.

Staff are always expected to be aware of the possibility that fraud, corruption or theft may exist in the workplace and be able to share their concerns with management. If for any reason, they feel unable to speak to their manager they should raise the matter in accordance with the Council’s Confidential Reporting Policy. 3.6 Conflicts of Interest Both members and staff must ensure that they avoid situations where there is a potential for a conflict of interest. Such situations can arise with externalisation of services, internal tendering, planning and land issues, etc. Effective role separation will ensure decisions made are seen to be based upon impartial advice thereby avoiding questions about improper disclosure of confidential information.

8

3.7 Official Guidance In addition to financial regulations and standing orders, individual sections will have their own procedures to prevent and detect fraud. There may also be audit reports that recommend systems changes to minimise losses to the Council. Managers and staff must be made aware of these various sources of guidance and alter their working practices accordingly. 3.8 The Role of Internal Audit Internal Audit plays a vital preventative role in trying to ensure that risks are identified and assessed, and systems and procedures are in place to prevent and detect fraud and corruption. In this way they are able to support managers in their responsibilities. The role of Internal Audit is explained in detail in Financial Regulation 5. As part of any investigation, Internal Audit liaises with management to recommend changes in procedures to prevent potential or further losses to the Council. 3.9 The Role of the Fraud and Error Team The Fraud and Error Team plays a pro-active role in the prevention, detection and investigation of all instances of suspected housing and council tax benefit fraud. The Council operates its own benefit fraud hotline, details of which are publicised on the Council's website. In cases where the suspected fraudulent claimant is in receipt of housing benefit/council tax benefit as well as income support/job seeker’s allowance, either Broxbourne Borough Council or the Department for Work and Pensions (DWP) will investigate. Fraud awareness training is given to officers within the benefits service as well as other sections of the Council to ensure that any cases referred to the team contain good quality information. The Council subscribes to the Housing Benefit Matching Service (HBMS), which matches data files from Broxbourne throughout the year to government databases and other local authority files. The results of these data mis-matches are actively pursued and form a significant area of activity for the Fraud and Error Team. The Team is also involved with interventions work, taking a pro-active role in reviewing claims to identify un-notified changes of details and circumstances which impact on benefit entitlement. The Borough of Broxbourne has adopted a Prosecutions and Other Sanctions Policy in respect of benefit fraud. It sets out the different types of enforcement action that may be taken and is designed to ensure consistent and proportionate enforcement of the Council's benefit fraud sanction role. It recognises that it may not always be in the public interest to refer cases for criminal proceedings. All investigations are carried out in accordance with relevant benefit legislation, including PACE and the Human Rights Act 1998. In cases of proven fraud, an appropriate sanction will be applied in accordance with the Prosecutions and Other Sanctions Policy. In cases where staff are involved, the Fraud and Error Team will liaise with Internal Audit, Personnel and appropriate senior management to ensure that correct procedures are followed and that this strategy is adhered to.

9

3.10 The Role of External Audit Independent external audit is an essential safeguard in the stewardship of public money. This role is delivered through the carrying out of specific reviews that are designed to test (amongst other things) the adequacy of the Council’s financial systems, and arrangements for preventing and detecting fraud and corruption. It is not the external auditor’s function to prevent fraud and irregularity, but the integrity of public funds is at all times a matter of general concern. External auditors are always alert to the possibility of fraud and irregularity, and will act without undue delay if grounds for suspicion come to their notice. The external auditor has a responsibility to review the Council’s arrangements to prevent and detect fraud and irregularity, and arrangements designed to limit the opportunity for corrupt practices.

3.11 Co-operation with Others Internal Audit has arranged and will keep under review procedures and arrangements to develop and encourage the exchange of information on national and local fraud and corruption activity in relation to local authorities with external agencies such as:

Police

External Audit

Audit Commission

Department for Work and Pensions

Government departments.

This co-operation is of course subject to current legislative requirements, in particular the Freedom of Information Act, Data Protection Act, Access to Information Act and Public Interest Disclosure Act.

10

Section 4 DETERRENCE

4.1 Prosecution Policy After proper investigation, the Council will take legal and/or disciplinary action in all cases where it is considered appropriate. The Council's policy in relation to proven frauds or suspected frauds which come to light, whether perpetrated by persons external to the Council or by staff or members, is that the case will be referred to the police as early as possible, and a crime number obtained. The Council will co-operate fully with police enquiries and these may result in the offender(s) being prosecuted. When considering whether to seek to pursue action through the police where they have advised the Council that action is possible, the Director of Resources, the Chief Executive Officer and the Head of Legal Services will jointly decide based upon the following criteria:

Seriousness of the offence (but the starting point will be that any suspected fraud will be reported to the police subject to the factors set out below)

Strength of the evidence available Impact on internal resources and whether this is likely to outweigh the benefits of

pursuing a prosecution Nature of the fraud and whether a prosecution will send out a clear message. Police appetite for the particular case and whether it is likely to receive prioritisation

given their stretched resources. The code for Crown Prosecutors.

4.2 Recovery Every effort will be made to recover any losses resulting from an occurrence of fraud. In certain cases, a civil action against the perpetrator may be appropriate.

4.3 Disciplinary Action Theft, fraud and corruption are serious offences against the Council and staff will face disciplinary action if there is evidence that they have been involved in these activities. Disciplinary action will be taken in addition to, or instead of, criminal proceedings, depending on the circumstances of each individual case, but in a consistent manner and after consultation with the Chief Executive, Director of Resources and Head of Personnel and Payroll. Where investigations consider that there has been any failure of supervision, appropriate disciplinary action will be taken against those responsible.

11

4.4 Publicity During an investigation, confidentiality must be maintained to protect the processes of disciplinary action and the rights of the suspected fraudster. However, in cases of proven fraud, there are significant deterrent effects in publicising the fraud. Broxbourne Borough Council’s Communication's Section will optimise the publicity opportunities associated with anti-fraud and corruption activity within the Council. The Communication Section will also try to ensure that the results of any action taken, including prosecutions, are reported positively in the media. The Council's website includes details of successful benefits prosecutions. In all cases where financial loss to the Council has occurred, the Council will seek to recover the loss, in so far as it is practicable, and advertise this fact. All anti-fraud and corruption activities, including the update of this strategy, will be publicised in order to make staff and the public aware of the Council’s commitment to taking action on fraud and corruption when it occurs. Regular reports will be made to the Audit Committee about countering fraud and corruption activities and their success or otherwise.

12

Section 5 DETECTION AND INVESTIGATION

It is important that all cases of fraud or suspected fraud are vigorously and promptly investigated and appropriate action taken. Managers should be alert to the possibility that unusual events or transactions could be symptoms of fraud or attempted fraud. Fraud may also be highlighted as a result of specific management checks or be brought to management's attention by a third party. Internal Audit plays an important role in the Council's risk management strategy and in the detection of fraud and corruption, although ultimate responsibility for the detection of fraud lies with managers. Included in its risk based three year Internal Audit Plan are risk reviews and testing of systems and financial controls which have been designed to mitigate these risks, along with specific fraud and corruption tests. Internal Audit will review systems implemented by management for adequate prevention and detection controls and also have a proactive role in not only auditing the anti-fraud control environment but identifying fraudulent activity through data matching techniques. In addition to Internal Audit, there are numerous systems controls in place to deter fraud and corruption, but it is often the vigilance of staff and members of the public that aids detection. In some cases, frauds are discovered by chance or ‘tip-off’ and arrangements are in place to deal with such information properly. The Council’s external auditors, the Audit Commission, provide a confidential reporting telephone hotline to enable concerns to be raised independently of the Council. See the Confidential Reporting Policy at Appendix 3. As required by Financial Regulation 6.1 all suspected irregularities are required to be reported to the Director of Resources. The reporting can be orally or in writing, either by the person with whom the initial concern was raised or by the originator as detailed in the Council’s Confidential Reporting Policy. This will:

ensure the consistent treatment of information regarding fraud and corruption.

facilitate a proper and thorough investigation by an experienced audit team, in accordance with the Fraud Response Plan and the requirements of current legislation.

The Director of Resources will call a case conference of senior officers including the Head of Legal Services, the Head of Personnel and Payroll, the Service Director and, if appropriate, the Chief Executive Officer. This will ensure that all relevant information is shared and that the course of the investigation can be determined.

The Fraud Response Plan at Appendix 1 details the procedures to be followed where fraud or corruption is detected or suspected.

This process will apply to all the following areas:

fraud/corruption by Members

fraud/corruption by Council staff, whether internal or external

fraud/corruption by contractors' staff

fraud/corruption by the public/ external parties

Depending on the nature of the case, any of the above may be referred to the police.

13

Except in the case of benefit fraud, any decision to refer a matter to the police will be taken by the Director of Resources in consultation with the Chief Executive Officer and the Head of Legal Services by applying the criteria stated in paragraph 4.1. The Council will normally wish the police to be made aware of, and investigate independently, offenders where financial impropriety is discovered. However, the mere fact that a police investigation leads to them taking no further action will not compromise any private action/procedure or investigation that the Council pursue. Depending on the nature of an allegation, the Investigating Officer will normally work closely with the Head of Service concerned to ensure that all allegations are thoroughly investigated and reported on. The Council’s disciplinary procedure will be used to facilitate a thorough investigation of any allegation of improper behaviour by employees. The processes as outlined in section 4.3 of this policy will cover Members. Learning from Experience Where a fraud has occurred, management must make any necessary changes to systems and procedures to ensure that similar frauds will not recur. The investigation may have highlighted where there has been a failure of supervision, breakdown or absence of control. Internal Audit will advise and assist on matters relating to internal control.

14

Section 6 AWARENESS AND TRAINING

This strategy clearly shows that the Council, the Director of Resources, managers and all staff have responsibilities in relation to the detection and prevention of fraud. Consequently, Broxbourne Borough Council recognises that the continuing success of this strategy and its credibility will depend in part on the effectiveness of programmed training and an awareness of Members and staff throughout the Council. The Director of Resources is responsible for ensuring that appropriate training is provided for all staff on this subject. To facilitate this, positive and appropriate provision has been made through the staff induction process and for existing staff via a corporate awareness programme of briefing sessions. This includes specialist training for certain Members and staff. New staff are made aware of the existence and importance of the Officer Code of Conduct, financial regulations, contract standing orders, the role of internal audit and computer usage policies and procedures on their first day at the Council. All new Council staff are required to attend training on financial regulations, and existing staff attend refresher courses on a periodic basis. The Fraud and Error Team runs an awareness training session for other sections to raise awareness of their work. At the operational level, managers should provide formal training on localised systems and ensure that controls and procedures are operating correctly. The Confidential Reporting Policy is available to all staff with access to the Council's Intranet in the staff handbook ‘Working for Broxbourne' Appendix 5.

15

Section 7 MONEY LAUNDERING

Money laundering means exchanging money or assets that were obtained criminally for money or other assets that are 'clean'. The clean money or assets do not have an obvious link with any criminal activity. Money laundering also includes money that is used to fund terrorism, however it is obtained. The Money Laundering Regulations 2007 only apply to regulated businesses and therefore the Council is outside the provisions of the regulations. Notwithstanding that, the Council has taken steps to safeguard against becoming involved in the processing of illegal or improper gains. As an area which deals with substantial sums of money, property transactions are particularly attractive to criminals wishing to convert gains to a respectable status. The Council’s Money Laundering Reporting Officer (MLRO) is the Director of Resources. The MLRO’s responsibilities are to: -

Ensure that satisfactory internal procedures are maintained; Arrange for periodic training for all relevant personnel; Receive and record reports of suspicious circumstances; Direct officers as to what action (if any) to take when suspicion arises and a report is

made; Report to the Borough Management Team as necessary on the operation of the anti-

money laundering policy and procedures (see Appendix 3). Although the risk to the Council of contravening the legislation is low, it is important that employees are aware of their responsibilities and that the Council ensures compliance with the Money Laundering Regulations 2007. There are transactions and business undertaken within the Council which could involve money laundering. An example would be an offer of large sums of cash to clear arrears.

Although closure of the Council’s cash office has reduced the risk, all offers to pay a significant amount of cash (in excess of 15,000 euros) to Council staff should be reported to the Director of Resources. The Council’s policy to advise on the risks of money laundering is at Appendix 3.

When processing requests for the refunds of large credits, staff should consider whether there is an innocent explanation for the credit. Where there is no obvious explanation this should be reported to the Director of Resources.

The Director of Resources will report transactions to the authorities if satisfied that this is appropriate. It should be noted that in most cases, the Council would not expect to hear anything further after making a report, but will have discharged its duty in doing so.

16

Section 8 BRIBERY ACT

The Bribery Act 2010 (http://www.opsi.gov.uk/acts/acts2010/ukpga_20100023_en_1) makes it an offence to offer, promise or give a bribe (Section 1). It also makes it an offence to request, agree to receive, or accept a bribe (Section 2). Section 6 of the Act creates a separate offence of bribing a foreign public official with the intention of obtaining or retaining business or an advantage in the conduct of business. There is also a corporate offence under Section 7 of failure by a commercial organisation (Borough of Broxbourne is a commercial organisation under the Act) to prevent bribery that is intended to obtain or retain business, or an advantage in the conduct of business, for the organisation. The Council will have a defence to this corporate offence if it can show that it had in place adequate procedures designed to prevent bribery by or of persons associated with the Council.

Bribery is a serious offence against the Council and employees will face disciplinary action if there is evidence that they have been involved in this activity, which could result in summary dismissal for gross misconduct.

The Council’s Anti-Bribery Policy Statement is included at Appendix 5. This policy covers all staff, of all levels and grades, those permanently employed, temporary agency staff, contractors, agents, members (including co-opted members), volunteers and consultants.

17

Section 9 CONCLUSIONS

The Borough of Broxbourne has always prided itself on setting and maintaining high standards and a culture of openness. This strategy fully supports the Council’s desire to remain free from fraud and corruption. The Council has in place a network of systems and procedures to assist it in dealing with fraud and corruption when it occurs. It is determined that these arrangements will keep pace with any future developments in techniques to both prevent and detect fraudulent or corrupt activity that may affect its operation. Through Internal Audit, the Council will continually review all of these systems and procedures, the details of which form the annual audit plan. This strategy will be reviewed bi-annually.

18

Appendix 1

FRAUD RESPONSE PLAN

Contents

Introduction 20 Section One Responsibilities when Fraud is Suspected 20 Section Two Managing the investigation 23 Section Three Gathering evidence 25 Section Four Reporting and learning from the experience 27

19

INTRODUCTION

This Fraud Response Plan describes the practical action that will be taken in response to any concerns of irregularity. The document also contains a series of flowcharts, which provide a framework of procedures to ensure there is a consistent and professional approach to investigations. This Fraud Response Plan does not apply to the investigation of benefit fraud. If you have any questions about the contents of this document please ask your line manager or feel free to ask the Internal Audit Manager who will be pleased to help you.

SECTION ONE – RESPONSIBILITIES WHEN FRAUD IS SUSPECTED

See Chart 1 on page 28 Identification of Fraud Investigators need to identify where fraudulent activity is taking place. Suspected fraud or irregularity can come to light in three ways: Routine investigations/audit - Proactive Internal notification - Reactive External notification - Reactive As required by Financial Regulation 6.1, all notifications should be brought to the attention of the Director of Resources as soon as possible. There may be circumstances where it is appropriate for local managers to undertake some preliminary exploration to check on the validity of an allegation or irregularity to establish whether there is a case to be investigated. Where this occurs, advice should be sought from the Director of Resources as such activity may alert the fraudster so that evidence is destroyed or the possibility of collecting further evidence may be compromised. As soon as possible after a concern has been raised it is important to decide whether the member of staff under suspicion should be suspended so that a full investigation can proceed unhindered. The vast majority of investigations will be reported to the police at an early stage. Fraud is a criminal offence and failure to report a crime to the police could potentially cause serious difficulties. Roles and Responsibilities Director of Resources Investigating suspected fraud and irregularity is the responsibility of the Director of Resources as set out in Financial Regulation 6. While the Director of Resources will retain overall responsibility and control, responsibility for leading any investigation will be delegated to an Investigating Officer. Where appropriate or necessary the Director of Resources is also responsible for informing third parties such as the external auditors and the police about the investigations. The Director of Resources will ensure that all suspected irregularities are reported to the Head of Legal Services (the Council’s Monitoring Officer), the Head of Personnel and Payroll and Chief Executive Officer, as appropriate.

20

The Director of Resources will: Maintain a log of all investigated suspicions. The log will contain details of actions taken

and conclusions reached. A report will be presented to the Audit Committee at least annually. Significant matters will be reported as soon as practical.

Call a case conference involving the Chief Executive Officer, Head of Legal Services,

Head of Personnel and Payroll and the Service Director as appropriate. The purpose of the case conference is to share the information and to determine the approach to be adopted to investigate the suspicions. The actions agreed at the case conference will be included in the investigation terms of reference prepared by the Investigating Officer, which should include as a minimum the objectives, scope, reporting deadlines and resources required. The terms of reference will need to be revisited and revised during the life of the investigation as results of the investigation emerge.

The Investigating Officer The Director of Resources will appoint an appropriately experienced and trained officer to lead the investigation of the suspected fraud. The Investigator may be a member of the Internal Audit Section or, in some specific cases, a manager. The Investigating Officer is responsible for the day to day on-going investigation control. Investigations of suspected fraud should only be undertaken by officers authorised by the Director of Resources. The Investigating Officer must ensure that proper records of each investigation are kept from the outset, including accurate notes of when, where and from whom evidence was obtained and by whom. All investigation records will be timed and dated and comply with the Criminal Procedures and Investigations Act 1996. Head of Legal Services – Monitoring Officer The Monitoring Officer’s role includes providing advice on the scope of powers and authority to take decisions, maladministration, financial impropriety, and probity. As such the Monitoring Office should be made aware of any suspicions of financial impropriety at an early stage. Head of Personnel and Payroll Where a member of staff is to be interviewed or disciplined as part of the disciplinary procedure, the Director of Resources and/or the Investigating Officer will consult with, and take advice from, the Head of Personnel and Payroll. The Head of Personnel and Payroll will advise those involved in the investigation in matters of employment law, policies and other procedural matters (such as disciplinary or complaints procedures) as necessary. A distinction needs to be made between those advising the investigation team and those advising the member of staff being investigated. Directors Directors must notify the Director of Resources immediately of any suspected fraud, theft, irregularity, improper use or misappropriation of the Council's property or resources. Internal Audit will be alerted and secure all relevant records. Pending investigation and

21

reporting, Directors should take all necessary steps to prevent further loss and to secure records and documentation against removal or alteration. Line and other managers If, in accordance with the Confidential Reporting Policy, a member of staff raises a concern with their line manager, Director or the Head Personnel and Payroll, the details must be immediately passed to the Director of Resources for investigation. Staff All staff have a responsibility to protect the assets of the Council and to report any suspicions of irregularities. However, staff should never put themselves at risk in any way in protecting Council assets or property. Confidentiality Investigators should ensure that details of all investigations remain confidential unless authorised to release information. Any disclosure of information will only be made where the law permits i.e. in accordance with the Data Protection Act 1998 and the Freedom of Information Act 2000. It is essential that in cases where allegations made about individuals prove to be unfounded, if possible, the investigation should not become generally known.

22

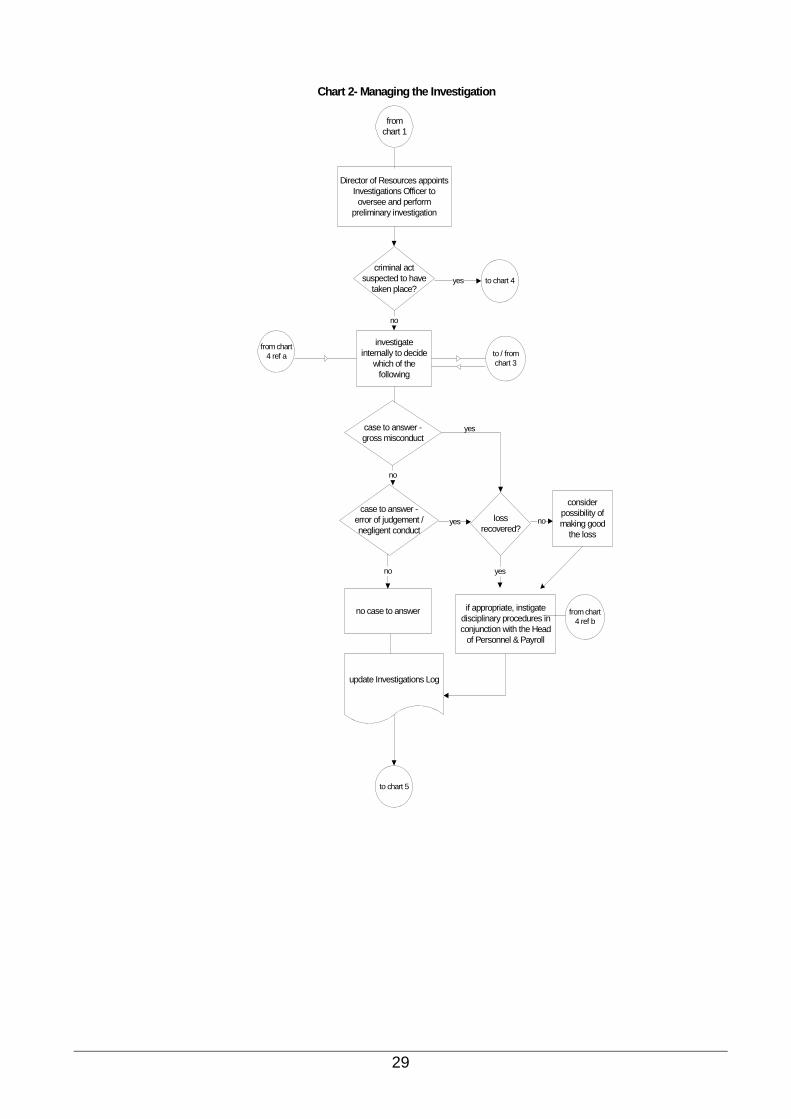

SECTION TWO - MANAGING THE INVESTIGATION See chart 2 on page 29 Objectives with respect to fraud Before any work is started, the purpose and nature of the investigation must be defined by senior officers through holding a case conference meeting to establish: Terms of engagement of the investigating team Resource and access requirements Nature of the allegations being investigated Location and nature of potential evidence sources Required output including provisional reporting deadlines Frequency of meetings for regular case conferences involving senior officers.

Investigations will try to establish at an early stage whether it appears that a criminal act has taken place. It is vital that all suspected criminal acts are reported to the police at an early stage to establish whether they will take action as this will shape the way the investigation is handled and determine the likely course of action. Preliminary Investigation Initially, a preliminary investigation should be performed. At its conclusion, a preliminary report should be produced for the Director of Resources for discussion at a case conference. This report should: Describe the allegation and its implications State the conclusions made and any police comments, if applicable Highlight recommendations for further action, e.g. full investigation, police referral Outline investigation and evidence obtained to date Include Terms of Reference for the full investigation, if applicable. This report will form the basis for decisions on any further action to be taken. No Criminal Act Taken Place If it appears that a criminal act has not taken place, an internal investigation will be undertaken to: Determine the facts Consider what, if any, action should be taken against those involved Consider what may be done to recover any loss incurred; and Identify any system weaknesses and look at how internal controls could be improved to

prevent a recurrence. Investigation of Staff In some investigations where staff are involved, situations may occur where it is not possible to determine the full extent of any evidence that exists, but where the evidence that has been disclosed is sufficient to clearly identify the suspect(s). In order to protect the integrity of any unsecured evidence, and to prevent any influence the suspect(s) may bring to bear on associates, it may be necessary for the investigator to consider recommending to

23

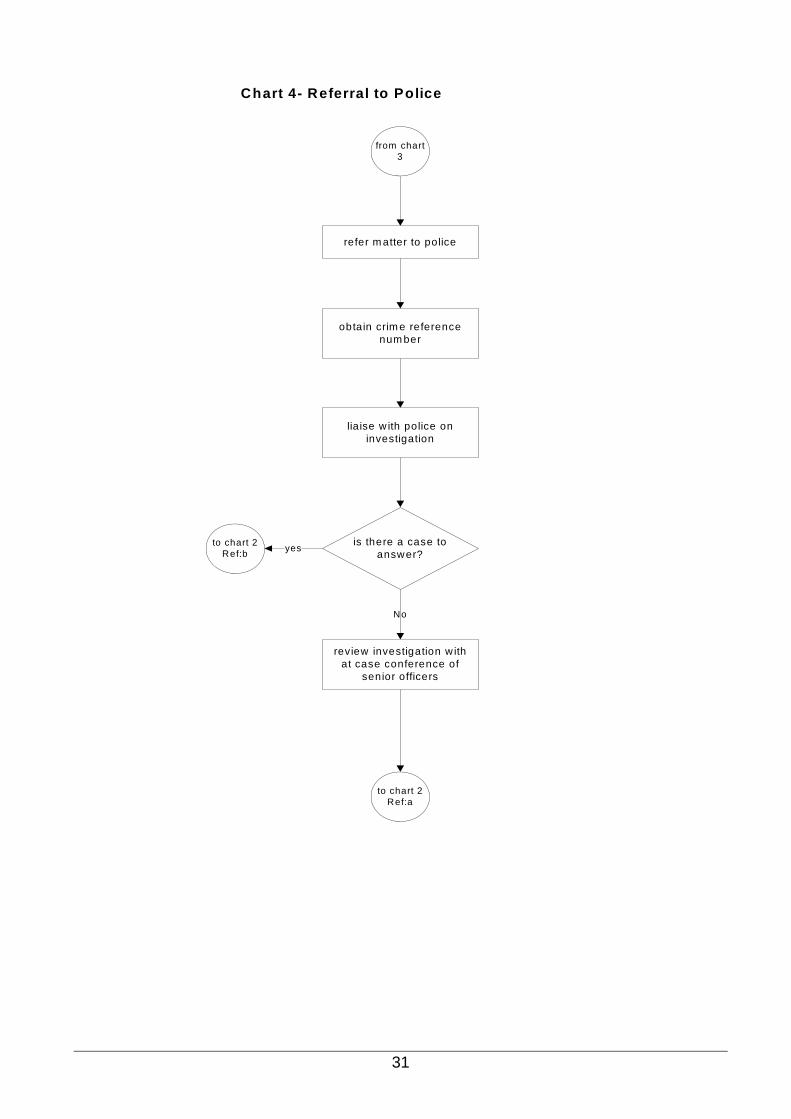

the service head, or the Chief Executive, the suspension from duty of the individual concerned. It should however be noted that any such action will always be taken as a neutral act. The Investigating Officer will present the findings of the investigation to the Director of Resources who will make the necessary decisions after consultation with senior officers through a case conference, and maintain a record of the subsequent actions in relation to closing the case. When considering the findings of the investigation, it is necessary to determine which of the following has occurred and therefore whether, under the circumstances, disciplinary action is appropriate: Gross misconduct Misconduct Negligence or error of judgement No case to answer. Disciplinary Process Investigators will have the opportunity to guide management through the evidence and to the possible courses of action using the Investigation Report. Hence, all evidence should be presented clearly and concisely. The Investigator is only responsible for disciplinary action in so far as they report and evaluate findings of an investigation and recommend a course of action to management. The investigation report will normally form part of the management case and be distributed to all parties involved with the disciplinary case, the Chief Executive Officer, the Director of Resources, the Head of Personnel and Payroll, the Head of Legal Services and the Service Director. The Investigator is not responsible for controlling the disciplinary process, but can become involved in either the presentation of evidence to the disciplinary hearing or be called as a witness to support that evidence. The Investigator is never involved in the actual decision making process of what disciplinary action to apply. The disciplinary procedures of the Council will be followed in any disciplinary action taken. The Director of Resources will take internal legal advice in deciding whether to pursue a civil action to recover any losses. Criminal Act Taken Place See charts 3 and 4 on pages 30 and 31

Where initial investigations point to the likelihood of a criminal act having taken place, the Director of Resources or Head of Legal Services will inform the police. Their advice will be sought when pursuing an internal investigation. In some cases it may be appropriate for an internal investigation to run in parallel with the police investigation.

The Head of Legal Services will guide the Director of Resources and the Chief Executive Officer in arriving at the decision on whether a civil prosecution is to be pursued in cases where a criminal prosecution is not being pursued by the police themselves. The criteria to

24

be considered when making this decision are listed in the Prosecutions Policy at 4.1 of the Anti – Fraud Strategy. Where appropriate the Director of Resources will consider the possibility of recovering losses from the Council’s insurers.

SECTION THREE – GATHERING EVIDENCE See chart 3 on page 30 It is imperative that prompt steps are taken to preserve evidence in whatever form: electronic, documentary and physical. The Investigating Officer, as nominated by the Director of Resources, will be responsible for managing the investigation, including interviewing witnesses and gathering any necessary evidence. By its nature, each fraud is likely to be different and the methods applied to conceal fraudulent activity are often complex or deliberately misleading. Therefore, the Investigator must adopt a systematic approach whilst at the same time retaining flexibility to react to changing situations as they arise during the process. Each case will be treated according to the particular circumstances and professional advice will be sought where necessary. Where there are reasonable grounds for suspicion, the police will be involved at an early stage. However, the Investigating Officer may still undertake part or all of the investigation on their behalf or as part of a separate internal investigation running in parallel, as agreed between the Director of Resources and the police. Documentation Standards Crucial to taking any action following a fraud investigation is comprehensive, accurate and formally structured documentation. Investigators must ensure that at all times during an investigation, files and associated documents are maintained in an orderly manner and files are fully cross-referenced. All rough notes drafted during the investigation should be retained. Actions of investigators must also be fully recorded, for example, the hand delivery of correspondence should be noted on file. Where appropriate, officers completing file notes with regard to action taken should sign these notes. Witness Statements

If a witness is prepared to give a written statement, the Investigating Officer will take a witness statement. If required, members of staff will be expected to comply with a request to provide a statement. The police will be able to edit such statements into the format as required by the Criminal Justice Act, Section 9. To ultimately achieve a successful prosecution, it is important to use the correct format as provided by the police (currently MG11 7/07).

25

Physical evidence The Investigating Officer will take control of any physical evidence, maintain a record of where, when and from whom it was taken and ensure it is properly handled.

Wherever possible, the original of any document should be obtained. If the original is not available, a copy is acceptable where it can be certified that it is a true copy.

Care must be taken not to undermine possible future criminal proceedings by destroying potential forensic evidence. All primary documents should be retained in plastic sleeves. No alterations or notes should be made on primary documents. Computer-Held Data Where information held on a computer system might provide evidence, the investigator needs to obtain a printout of the relevant information and treat it as a prime document. The date and time of its production should be included as part of the printed data. Interviewing Suspects Before interviewing any suspects the Investigating Officer will provide an oral or written report of the investigation to the Director of Resources. The Director of Resources may consult with others e.g. Head of Legal Services, Head of Personnel and Payroll, Chief Executive or the police before reaching a decision on how to proceed. If a suspect is to be interviewed, the Investigating Officer and the Director of Resources will seek advice from Legal Services. Interviews will be carried out in accordance with PACE and will only be conducted by trained and qualified officers. Where external organisations/individuals are involved, the police will generally undertake the interviews unless the Director of Resources is able to gain the co-operation of the organisation's management or auditors. Surveillance Surveillance is usually the last resort that an investigator will utilise to prove or disprove an allegation of fraud. It would only be undertaken where there is no reasonable and effective alternative means of achieving the desired objective and would only be carried out where necessary and appropriate to do so. Any surveillance activity must comply with the Regulation of Investigatory Powers Act (RIPA) and must be authorised by the Head of Legal Services.

26

SECTION FOUR - REPORTING AND LEARNING FROM THE EXPERIENCE See chart 5 on page 32 The conclusion of investigations should be accompanied by the submission of a detailed report to the Director of Resources. The Director of Resources, and possibly the police, will use this document upon which to base their conclusions and decide further action. In order to achieve these aims, the report must: completely and accurately document all material aspects of the investigations set out the facts clearly and unambiguously highlight areas where there is conflicting evidence be addressed and presented to the appropriate level of management be timely and drafted when the investigation stage is largely complete and no new

evidence is likely to emerge be produced under confidential cover with each issue numbered and a record kept of the

recipient of each issue be free from bias. The report should be structured as follows: introduction and background to the investigation, including terms of reference allegation and specification of the alleged offence management summary covering the overall conclusion and recommended course of

action proposed by the Investigating Officer and flowing from the evidence reviewed body of the report detailing the findings/evidence with a commentary and implications separate section on the systems weaknesses which allowed the irregularity to occur and

recommendations to minimise the risk of a re-occurrence by improving internal control. The full range of options for subsequent action should be considered and should include: seeking restitution disciplinary proceedings civil action referral to the police. The final report should be issued to the Director of Resources, the Chief Executive, the Head of Legal Services, the Head of Personnel and Payroll, the Service Director and members of the Audit Committee as appropriate. The Investigating Officer should report back to the person raising the concern (if appropriate) or indicate that they will not be doing so. The investigation files should be held securely in Internal Audit for two years if no action is required, but for six years for all other cases. Internal audit investigation reports and any information received during the course of an investigation may be considered exempt information under the Freedom of Information Act 2000 section 30. Further guidance relating to this can be obtained from www.ico.gov.uk/what_we_cover/freedom_of_information.aspx. The Investigating Officer will carry out a follow up review to check that recommendations have been implemented and to assess the effectiveness of changes made.

27

become aware of concern by:

line managementletter

telephone callvisit/in personfraud hotline

elected Member

person in receipt of information to notify

Director of Resources

Audit Manager to record concern in a log

Case conference called of senior officers to discuss

and scope the review

to chart 2

Chart 1- Raising a Concern

Investigations Log

Investigations Log reported to Audit

Committee

audit findingindividual has a concern

matter to be dealt with by audit?

yes

noRefer matter to Personnel/

line management as appropriate

28

Chart 2- Managing the Investigation

from chart 1

Director of Resources appoints Investigations Officer to oversee and perform

preliminary investigation

investigate internally to decide

which of the following

update Investigations Log

criminal act suspected to have

taken place?to chart 4yes

to chart 5

to / from chart 3

from chart 4 ref a

case to answer - gross misconduct

case to answer - error of judgement / negligent conduct

consider possibility of making good

the loss

loss recovered?

no case to answer if appropriate, instigate disciplinary procedures in conjunction with the Head

of Personnel & Payroll

from chart 4 ref b

yes

no

no

no

yes

no

yes

29

from chart 2

Any physical evidence inc.

records?

collect evidence with documentary record of

time and place

are there any witnesses?

obtain written statements

Chart 3 - Gathering Evidence

yes

yes

case to answer?

no

no

interview suspect?

review by calling a case conference of senior

officers

to chart 2

no

refer to police?

no

yes

update Investigations Log

yesto chart 4 yes

no

sufficient evidence to proceed?

no

update Investigations

Log

yes

30

Chart 4- Referral to Police

from chart 3

obtain crim e reference num ber

is there a case to answer?

review investigation w ith at case conference of

senior officers

No

to chart 2Ref:a

refer m atter to police

lia ise w ith police on investigation

to chart 2Ref:b

yes

31

from chart 2

Confidential Reportingissue final report on the

irregularity to Director of Resources

report back to person raising concern

(where appropriate)

hold files securely (2 years if no action, 6

years for others)

report to BMT and Audit Committee on

weaknesses identified which allowed the

irregularity to occur

discuss and formally agree actions to

minimise the risk of a similar event occuring

Internal Audit to review effectiveness of

changes

Chart 5 - Reporting and Learning from the Experience

32

Appendix 2

CONFIDENTIAL REPORTING POLICY PREAMBLE Employees are often the first to realise that there may be something seriously wrong within the Council. However, they may not express their concerns because they feel that speaking up would be disloyal to their colleagues or to the Council. They may also fear harassment or victimisation. In these circumstances it may be easier to ignore the concern rather than report what may just be a suspicion of malpractice. The Council is committed to the highest possible standards of openness, probity and accountability. In line with that commitment we encourage employees and others with serious concerns about any aspect of the Council’s work to come forward and voice those concerns. We recognise that some cases will have to be dealt with on a confidential basis and this document makes it clear that staff can raise matters confidentially without fear of reprisal. This policy is intended to encourage and enable staff to raise serious concerns within the Council rather than overlooking or ignoring a problem or “blowing the whistle” outside. This policy has been discussed with the relevant trade unions/staff side group and has their support.

AIMS AND SCOPE OF THIS POLICY This policy aims to: provide an avenue for you to raise any concern you might have and to receive feedback

on action taken. allow you to take the matter further if you are dissatisfied with the initial response you

receive, and reassure you that you will be protected from reprisals or victimisation for “whistle

blowing” in good faith. There is in place a Grievance Procedure to allow you to raise any concerns relating to your own employment. Copies of the Grievance Procedure can be obtained from the Personnel section and is included as Appendix 21 of “Working for Broxbourne”. This policy is intended to cover concerns that fall outside the scope of the Grievance Procedure. Such concern may be about something that: is unlawful; or a health and safety risk including risks to the public as well as other employees; or damages the environment; or is an unauthorised use of public funds; or is possible fraud and corruption; or

33

is unethical conduct or improper conduct; or makes you feel uncomfortable in terms of known standards, your experience or the

standards you believe the Council subscribes to; or is against the Council’s Standing Orders and policies; or falls below established standards of practice

SAFEGUARDS Harassment or Victimisation The Council recognises that a decision to report a concern may be difficult, not least because you may fear reprisal from those about whose behaviour you are expressing concern. The Council wishes to make it clear that harassment or victimisation (including informal pressures) of a person “whistle blowing” in good faith will not be tolerated and action will be taken to protect you when you raise a concern. This does not mean that if you are the subject of disciplinary or redundancy procedures or investigations that those proceedings will be halted as a result of your “whistle blowing”. CONFIDENTIALITY The Council will do its best to protect your identity when you raise a concern, if you do not wish your name to be disclosed. However, you must appreciate that the investigation process may have to reveal the source of the information and a statement by you may be required as part of the evidence gathered. Although every effort will be made to protect your identity if you wish it, no guarantee can be given. ANONYMOUS ALLEGATIONS You will be encouraged to give your name when you “whistle blow”. This is because a concern expressed by a named individual carries much more weight than one expressed anonymously. Anonymous concerns will be considered at the discretion of the Council but they are less powerful. In exercising discretion on whether or not to consider anonymous concerns, the factors to be taken into account would include: the seriousness of the issues raised the credibility of the concern; and the likelihood of confirming the allegation from attributable sources. UNTRUE ALLEGATIONS If you make an allegation in good faith, but it is not confirmed by the investigation, no action will be taken against you. If however you make malicious or vexatious allegations, disciplinary action may be taken against you.

34

HOW TO RAISE A CONCERN Initially, you should raise any concern you have with your immediate manager or their manager who will pass the issue on to the appropriate person. However, this depends of course on the seriousness and/or sensitivity of the matters causing you concern and who you think might be involved in the malpractice, e.g. if you believe management may be involved, you should approach the Chief Executive, the Director of Resources, or the Council’s Internal Audit Manager. Alternatively concerns may be raised with the Audit Commission via their confidential reporting line 0845 0522 646. This number can be called if you ever wish to take a concern to someone totally independent of the Council. Obviously it is better if you present your concerns in writing. This will give you the opportunity to set out the background and history of the concern giving as many details as possible e.g. names, dates and places and the reasons why you are particularly concerned about the situation. However, if you do not feel able to put your concern in writing, you can ask for a meeting with whichever of the officers you consider to be appropriate. Remember that the first step in any journey is the hardest. In this particular case, the sooner you express the concern the easier it will be for you and for the Council to take any appropriate action. Although you will not be expected to prove the truth of an allegation, you will be expected to demonstrate to the manager to whom you reported the issue that there are sufficient grounds for concerns. ADVICE AND GUIDANCE ON HOW MATTERS OF CONCERN MAY BE PURSUED CAN BE OBTAINED FROM: Chief Executive Mike Walker ext 5533 Head of Legal Services Gavin Miles ext 5750 Director of Resources Gillian Clelland ext 5518 Internal Audit Manager Julie Sharp ext 5527 Head of Personnel and Payroll Richard Pennell ext 5536 Audit Commission 0845 0522 646 You may invite your trade union, professional association representative or a friend to be present during any meetings or interviews in connection with the concerns you have raised. HOW THE COUNCIL WILL RESPOND Any action taken by the Council will depend upon the nature of the concern you have raised. It may: be investigated internally; be investigated by the Audit Commission; be referred to the police; form the subject of an independent enquiry.

35

In order to protect your identity and the Council, initial enquiries will be made to decide whether an investigation is appropriate and, if so, what form it should take. It may be possible to resolve some concern by agreed action without the need to carry out an investigation. However if this is not the case then within ten working days of a concern being raised, the person to whom the concern has been forwarded will write to you: acknowledging that the concern has been received; indicating how the matter will be dealt with; giving an estimate of how long it will take to provide a final response; telling you what initial enquiries have been made, if any; and telling you whether further investigations will take place and if not, why not. The amount of contact between the officers considering the issues and you will depend on the nature of the matters raised, the potential difficulties involved and the clarity of the information provided. If necessary, the Council will seek further information from you. Whether any meeting is arranged, off-site if you so wish, you can be accompanied by a union or professional association representative or a friend. The Council will take steps to minimise any difficulties which you may experience as a result of raising a concern. For instance, if you are required to give evidence in criminal or disciplinary proceedings the Council will arrange for you to receive advice about the procedure. The Council accepts that you need to be assured that the matter has been properly addressed. Thus, subject to legal constraints, we will inform you of the outcome of any investigation. The Council fully understand that if you have raised a complaint you will need to be reassured that the complaint has been properly addressed. Therefore, unless legal constraints prevent it, you will be fully informed about the outcome of any investigation which is carried out. HOW THE MATTER CAN BE TAKEN FURTHER This policy is intended to provide you with a way to raise concerns within the Council. It is hoped you will be satisfied with any outcome. If you are not, you will have the opportunity to raise the matter with the Council’s Internal Audit Manager. If you feel unable to report your concern within the Authority, then you can report your concern to a prescribed person such as: The Health and Safety Executive The Audit Commission The Commissioners of Customs and Excise The Data Protection Registrar

1. Note that to report externally you must not only have an honest and reasonable suspicion but should also honestly and reasonably believe that

36

any information and allegation made is substantially true. You can also make a wider disclosure to other bodies such as:

The Police Members of Parliament The Media Non prescribed persons (e.g. Unison whistleblowers hotline 0800 5 97 97 50, or Public

Concern at Work website: www.pcaw.co.uk) However certain conditions have to apply to make such wider disclosures protected namely: The concern must be serious The relevant failure is continuing or is likely to occur in the future The concern is not raised internally or with a prescribed person, because you

reasonably fear you would suffer a detriment (victimisation) The concern is not raised internally because you reasonably believe that evidence

would be concealed or destroyed (a cover-up) The concern was raised internally or with a prescribed person but was not dealt with

properly. The disclosure must not be for personal gain. If you do take the matter outside the Council, you should ensure that you do not disclose confidential information. THE RESPONSIBLE OFFICER The Head of Legal Services, as the Council’s appointed Monitoring Officer, has overall responsibility for the maintenance and operation of this Policy. He will maintain a record of all concerns raised and their outcomes (but in a form which will not endanger your confidentiality) and will report as necessary to the Council.

37

Appendix 3

BROXBOURNE BOROUGH COUNCIL PREVENTION OF MONEY LAUNDERING PROCEDURES

INTRODUCTION The Council is committed to the prevention of money laundering and to working with the appropriate authorities to apprehend those who commit offences under the anti-money laundering regulations. These procedures are to be followed to ensure compliance with the Terrorism Act 2000, the Proceeds of Crime Act 2002 and the Money Laundering Regulations 2003. Council employees who fail to follow these procedures could themselves be in breach of the legislation and liable to prosecution. TRAINING The Council will train all current employees who may come into contact with persons engaged in money laundering of the risks and how to identify possible problems. The Council will also give such employees training in how to recognise and deal with transactions which may be related to money laundering. New employees who may come into contact with persons engaged in money laundering will receive training as specified above as part of their induction process. IDENTIFICATION PROCEDURES In the following circumstances the Council MUST take appropriate steps to verify the identity of a person who is (or who is applying to) do business with the Council:-

where an officer involved in the transaction knows or suspects that the transaction involves money laundering, or

where a one off cash transaction involves the payment to or by the other party of

15000 euro or more, or

in respect of two or more one off transactions with the same party which appear to the officer to be linked (whether at the outset or later) the total payment to or by the other party will be 15000 euro or more.

At the rate of exchange prevailing at the date of writing these procedures 15000 euro was just over £12480. Officers should check the exchange rate if they believe the 15000 euro limit may be reached. Where the Council has a duty to verify identity in the circumstances listed above, as soon as possible after the first contact between the other party (if an individual) and the Council has been made the officer dealing with the transaction will:-

38

require the other party to produce satisfactory evidence of identity in the form of:-

a passport a driving licence a birth certificate a marriage certificate require the other party to produce evidence of current address in the form of:- a bank statement a credit card statement mortgage or insurance details a utility bill

If for any reason it is not practicable for the other party to be physically present when identified consideration must be given to the greater potential for money laundering. In such cases the other party should be required to provide copy documents certified as true copies of the originals by a practicing solicitor. The officer should check with the Law Society (this can be done on-line at www.lawsociety.org.uk ‘Find a solicitor’) to ensure that the solicitor is known to them and then obtain confirmation from the solicitor that he or she signed the copies. As the solicitor for any person dealing with the Council also has the money laundering prevention responsibilities the identification requirement can also be met by that solicitor certifying they have proof of identity of their client. Where the Council has a duty to verify identity in the circumstances listed above, as soon as possible after the first contact between the other party (if a company) and the Council has been made the officer dealing with the transaction will:-

require the individual representing the company to provide the company’s full name and company registration number, details of the registered office address and any separate trading address relevant to the contract concerned. The officer will then carry out a company search to verify details given and will check the location of any relevant trading address.

in the event that the company is effectively owned by one or only a few individuals

the officer should verify the identity of that or those individuals in accordance with production of the documents listed above.

Where the other party is acting or appears to act for another person that person’s identity should be verified as above. WHERE SATISFACTORY EVIDENCE OF IDENTITY IS NOT AVAILABLE THE BUSINESS ARRANGEMENT OR ONE OFF TRANSACTION SHOULD NOT PROCEED FURTHER RECORD KEEPING Where evidence of identification is obtained in accordance with the above the Council is required to keep records of that evidence. The records required to be kept are:-

39

a copy of that evidence (note 1) information as to where a copy of that evidence may be obtained (note 2) where it is not reasonably practicable to comply with the above, information as to

where the evidence of identity may be re-obtained. In all cases the Council must also keep a record containing details relating to all transactions carried out by the Council in the course of relevant business. Records must be maintained:-

Note 1 - for a period of 5 years commencing from the date the business relationship ends or (in the case of a one off transaction or transactions) five years from the conclusion of all activities arising in the course of that transaction or (if a series of transactions) the last of them to end.

Note 2 - the period is at least five years commencing with the date on which all

activities taking place in the course of the transaction in question were completed.

Copies of identification documents and the records required to be kept by this paragraph shall be kept on the relevant transaction file or files.

INTERNAL REPORTING PROCEDURES The Council is required to nominate one of its officers for the purpose of receiving reports under the legislation. The Council’s nominated officer for this purpose (the Money Laundering Reporting Officer - MLRO) is the Council’s Director of Resources. Officers are required to make a disclosure to the MLRO of any information which comes into their possession in the course of their employment as a result of which he or she knows or suspects or has reasonable grounds for knowing or suspecting that a person is engaged in money laundering. The time for making the disclosure is as soon as reasonably practicable after the information comes into the officer’s possession. In the absence of the MLRO then the officer with such information should disclose the information to the Head of Legal Services. Where a disclosure is made to the MLRO he or she must consider it in the light of any relevant information which is available to the Council and determine whether it gives rise to such knowledge or suspicion or such reasonable grounds for knowledge or suspicion that a person is engaged in money laundering. Where the MLRO does so determine he or she shall disclose the information to NCIS as soon as is reasonably practicable. The disclosure will be in writing and sent by fax to 0207 238 8286. Details of the information to be disclosed are set out at paragraph below. Further guidance as to the information required can be obtained from the NCIS website www.ncis.co.uk . However the online form is not user friendly and should not be used. Instead the disclosure should be in the form of a letter and sent by fax to 0207 238 8286. If the MLRO determines that it is not necessary to disclose information to NCIS he or she will record all information known to the Council at that time and the reasons why he or she has decided that such information does not give rise to knowledge or suspicion or

40

reasonable grounds for knowledge or suspicion that a person is engaged in money laundering When disclosure is made to NCIS, such disclosure should include the following details where known:-

name of persons or companies involved date of birth all known addresses including previous addresses, post codes and any separate

trading addresses company names directorships passport details phone numbers any other relevant data full details of the reasons for suspicion including copies of any relevant

documentation if a decision is required urgently to enable a transaction to proceed a clear statement

as to when a decision is required by and the reason for the request RESTRICTION ON TRANSACTIONS Where the MLRO has made or is contemplating making a disclosure to NCIS or a disclosure to NCIS has been made or is contemplated by another officer in the absence of the MLRO. the MLRO or other officer as the case may be shall notify all officers involved in any transactions which are the subject of such disclosure or contemplated disclosure that no further steps are to be taken with regard to any transactions involving the same party for a period of seven (7) days unless within that period NCIS have indicated that it consents to the transaction proceeding. In the event that NCIS refuses consent to the transaction or transactions proceeding within seven (7) days the MLRO or other officer who made the disclosure shall forthwith notify all officers involved in any such transactions that no further steps are to be taken with regard to any transactions involving the same party for a period of thirty one (31) days unless within that period NCIS have indicated that it consents to the transaction proceeding. TIPPING OFF OFFICERS ARE REMINDED THAT TIPPING OFF IS A SERIOUS OFFENCE An officer who knows or suspects that a disclosure to NCIS has been made or may be made must not disclose to any other person anything which may prejudice the investigation. Where an officer knows or suspects that a disclosure has or will be made by another officer to the MLRO he or she is likely to have grounds to suspect that a disclosure has or will be made by the MLRO to NCIS unless the MLRO has confirmed that he is not making such a disclosure. Where as a result of a disclosure being made a transaction is unable to proceed, it follows that officers are prevented from disclosing the reason for delay.

41

42

Appendix 4

BROXBOURNE COUNCIL - OFFICER CODE OF CONDUCT

Version 2 – January 2010

CONTENTS A Core Principles B Core Standards C Core Standards – Guidance D Referral Points E Checklist for Assessing Potential Conflict – Gifts & Hospitality F List of Politically Restricted Posts

Broxbourne Borough Council Anti-fraud Strategy

A. CORE PRINCIPLES The following core principles underpin the concept of public service and apply to all employees of the Council regardless of the nature of the job they do.

SELFLESSNESS Employees must take decisions solely in the terms of the public interest. They must not do so nor use their position in order to gain financial or other material benefits for themselves, their family or their friends.

INTEGRITY Employees must not place themselves under any financial or other obligations to outside individuals or organisations that might influence them in the performance of their official duties.

OBJECTIVITY In carrying out public business, including making public appointments, awarding contracts or recommending individuals for rewards and benefits, employees must make decisions on merit.

ACCOUNTABILITY Employees are accountable for their decisions and actions to the public and must submit themselves to whatever scrutiny is appropriate to their office.

OPENNESS Employees must be as open as possible about all decisions and actions that they take. They must give reasons for their decisions and restrict information only when the wider public interest clearly demands it.

HONESTY Employees have a duty to declare any private interests relating to their public duties and to take steps to resolve any conflicts arising in a way that protects the public interest.

RESPECT FOR OTHERS Employees must treat other people with respect and not discriminate unlawfully or unfairly against any person. They must treat Councillors and other co-opted members of the authority professionally.