60

The More You See... “Creating new opportunities” Annual Report 2007/2008

The More You See...

“Creating new opportunities” Annual Report 2007/2008

(in F thousand/%) 2007/2008 in percent 2006/2007 in percent

Net sales 68,286 89 % 51,289 88 %

Capitalized work 8,033 11 % 7,297 12 %

Total output 76,319 100 % 58,586 100 %

Material costs 16,478 22 % 13,096 22 %

Personnel costs excluding depreciation 15,552 20 % 11,766 20 %

Production costs excluding depreciation 32,031 42 % 24,862 42 %

Gross Profit 44,289 58 % 33,723 58 %

Research and development costs, total 10,803 14 % 9,598 16 %

Sales and marketing costs 10,818 14 % 8,640 15 %

Administration costs 4,322 6 % 4,454 8 %

Sales and administration costs excluding depreciation 15,138 20 % 13,094 22 %

Other operational revenue 256 0 % –94 0 %

EBITDA 18,603 24 % 10,938 19 %

Depreciation and amortization 5,666 7 % 4,787 8 %

Total costs 31,608 41 % 27,479 47 %

EBIT 12,937 17 % 6,150 10 %

Financial result -1,601 -2 % 174 0 %

EBT 11,336 15 % 6,325 11 %

Income taxes 3,346 4 % 786 1 %

Net profit for the period 7,990 10 % 5,539 9 %

Minority interests 409 1 % 418 1 %

Net profit for the period after minority interests 7,581 10 % 5,121 9 %

Consolidated total operating revenue EBITDA-EBIT-statement

Selected financial data

Key Figures

Percentage(in F thousand/%) 30.9.2008 30.9.2007 change

ROCE (Return on Capital Employed) 11% 7%

Equity Ratio 51% 49%

Cash-flow from operating activities 6,375 6,699 -5%

Fund assets September, 30 12,544 22,292 -44%

Earnings per share in E 1.76 1.18 49%

Dividend per share in E 0.15* 0.15 0%

Equity per share in E 17.45 16.13 9%

Shares issued 4,317,050 4,337,940 0%

No of employees (annual average) 372 300 24%

* subject to the agreement of the General Meeting

11ISRA VISION Annual Report 2007/2008

Disclaimer - Forward looking statements, Variances for technical reasons This annual report contains forward-looking statements that reflect management’s current views with respect to future events. Such statements are subject to risks and uncertainties that are beyond ISRA VISION AG’sability to control or estimate precisely, such as future market and economic conditions, the behavior of other market participants, the ability to successfully integrate acquired businesses and achieve anticipated syn-ergies and the actions of government regulators. If any of these or other risks and uncertainties occur, or if the assumptions underlying any of these statements prove incorrect then actual results may be materiallydifferent from those expressed or implied by such statements. ISRA VISION AG does not intend or assume any obligation to update any forward-looking statements to reflect events or circumstances after the dateof these materials. For technical reasons (e.g. conversion of electronic formats) there may be variances between the accounting documents contained in this annualreport and those submitted to the electronic Federal Gazette (Bundes -anzeiger). In this case, the version submitted to the electronic Federal Gazette shall be binding. Both language versions of the annual report can be downloaded from the internet at http://www.isravision.com. An interactive online version of the annual report for the media is also available on our website in bothlanguages. On request we would be pleased to send you further copies and additional information about the ISRA VISION AG free of charge. Telephone +49 6151 948-209 Fax +49 6151 948-140 or [email protected]

Creating new opportunities - Focus on “100 +” 2

Generating short term Return on Investment for the customer - Machine Vision automation offers large potential 4

Beyond the “electronical eye” - Innovations as a competitive advantage for production intelligence 6

A wealth of new opportunities - Exploiting the potential of the solar and print industries 8

New market insights - ISRA’s 3D gauging make the “seeing” robots produce “quality” cars 10

Looking forward out of the “storm” - Staying on course with sustainable profitability 12

Group Management Report 14

Report of Supervisory Board 24

Corporate Governance 26

Consolidated Financial Statements (IFRS) 28

Reproduction of the Auditor´s Report 57

Contents

2

Creating new opportunitiesFocus on “100 +”

Dear Shareholders, Business Partners and Friends of ISRA; valued Employees:

We are pleased to report that ISRA was able to continue its long-term track record of dynamic and prof-itable growth in financial year 2007/2008. The fact that we not only fulfilled but partly even exceeded ourtargets underscores the high degree of planning reliability we have achieved. Thus, revenue rose by 33percent to more than 68 million Euros. Profit performance was even more impressive: our gross result(EBT) of 11.3 million Euros represents an almost 80 percent improvement over the prior year. Followingthe successful integration of its recent acquisitions, ISRA has been able to return to the profitability tar-gets established by the Executive Board. The EBT margin (based on total output) improved by 4 per-centage points to 15 percent, while the gross operating margin (EBT in relation to revenues) rose by 5percentage points to 17 percent.

ISRA management intends to stick resolutely to its growth strategy. In the context of our “100 +” target, we have set our-selves the goal of breaking through the revenue threshold of 100 million Euros in the coming years. All in all, ISRA is wellpoised to master the current challenges on the global market, thanks to its leading market position, its innovative prod-ucts, and its global corporate customers, who come from a diversity of geographic regions and sectors of the “old econ-omy”. Moreover, our financial position is on a solid footing. The equity ratio of the ISRA Group currently amounts to 51percent. Long-term financing for our acquisition activities has been secured on favorable terms. Due to the partially vari-able nature of our interest-payment obligations, we have been able to profit from the current low level of interest rates.Besides having adequate liquid assets, ISRA also has access to a substantial number of secured financing options.

The management believe that the current global recession presents us with numerous opportunities, from which ISRA, asone of the global top five suppliers of Industrial Image Processing and the world leader in Surface Inspection, will be ableto profit. This is because ISRA solutions offer customers precisely what they are looking for, especially in economicallytroubled times: reduction in costs coupled with increase in quality. A common advantage of all our products is their abil-ity to generate a rapid return on investment (ROI), given that they allow our customers to boost profitability and competi-tiveness in short order. Now more than ever, this will be a keyfactor in the investment decisions of customers. ISRA helpsits customers to rationalize processes, increase efficiency andultimately enhance profitability. Thus, ISRA expects to benefitfrom the massive economic rescue and stimulus packagesbeing implemented practically all over the world. On the otherhand, it is true that certain key customers are currently sub-jecting all their investment activities to an intensive review.Since budget planning has come to a standstill and manyprojects are being postponed, certain investment decisionswill be significantly delayed.

Given the highly volatile state of the global economy – withsome established forecasters making downward revisionsalmost weekly and others throwing in the towel altogether – itgoes without saying that any estimate of future revenues andprofits must be highly tentative. Based on our latest analysis– which strikes a balance between the growing trend to boostefficiency on the one hand and the need to cut back invest-ments on the other – we expect profitability level to be able tomaintain in financial year 2008/2009.

ISRA VISIONAnnual Report 2007/2008

Enis Ersü, CEO

Sales (in Mio G) Total Operating Revenue (in Mio G)

98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08

10,0

20,0

30,0

40,0

50,0

60,0

0

70,0

80,0

90,0

3

Based on a review of our customers’ budgets and on the assumption that the global economy willnot worsen significantly, ISRA is reckoning with slightly lower revenues in financial year 2008/2009.During this phase, ISRA at this stage intends to exploit its full potential by intensifying sales and mar-keting efforts. Furthermore, we are actually in the process of negotiating a number of namable neworders. Some of these discussions are in an advanced stage. This should allow us to keep any rev-enue adaption within a manageable range.

In the prior financial year 2007/2008, a number of acquisitions were successfully integrated into theISRA Group. Our strategic focus will now be on increasing profitability, which will involve optimizingproduction, organization and administration throughout the entire ISRA Group. This is currently beingsupported by external expertise. Given the uncertain outlook for the global economy, we have alreadyadopted and implemented a raft of pre-emptive measures to cut costs and boost efficiency. This

process is not yet complete, however. Depending on the future economic trend, we will be ready to take additional orga-nizational adjustments. Our objective will be to stabilize the ISRA Group’s profitability in the range presently achieved, whilestriving to further enhance our net income over the medium term.

In the course of our managerial and entrepreneurial decision-making, we are always conscious of our responsibility forthe ISRA Group of Companies and their economic future. Our basic approach can be summed up as follows: The sustainable loop of values such as customer and employee satisfaction increases profitability under the assumptionof sustainability. This in turn ensures ISRA's long-term success.

We believe the best way to keep our customers happy is to provide them with reliable solutions that help them boost theirprofitability and competitiveness. And by offering our employees rewarding, long-term jobs in a dynamic high-tech work-place, we motivate them to fully apply their talents and skills for the benefit of ISRA. Continual increase in efficiency throughoptimization of production and organization will safeguard ourprofitability and lead to value enhancement of the Group. Aspart of our corporate responsibility for our customers, employ-ees and business partners, as well as for the natural environ-ment in which we live, our products and services in keepingwith a sustainable use of scarce resources.

On behalf of the entire ISRA Management Team, I would liketo thank our employees for their personal contributions to theoutstanding performance of the Group. As for our esteemedcustomers, shareholders and business partners, I would liketo gratefully acknowledge your confidence and support.

Sincerely yours,

Enis ErsüChairman of the BoardOn behalf of ISRA Management

ISRA VISION Annual Report 2007/2008

98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08

0,9

1,5

2,6

3,4

4,1

10

EBT (in Mio G)

5,7

8,3

6,3

0,20

0,40

0,60

0,80

1,00

1,20

0,00

1,40

1,60

1,80

2,00

11,3

EPS (

G p

er

shar

e)

EPS

Dr.-Ing. h.c. H. J. Wiedenhues,Chairman of Supervisory Board

4

As one of the global leaders in the booming Machine Vision industry, ISRA offers a broad range of products and solutionsfor all aspects of Industrial Image Processing. These allow the production of most types of goods to be made more rapid,efficient and economical while maintaining optimal quality. New applications for this key technology are being discoveredon an almost daily basis, and we estimate that only a third of its worldwide potential has been exploited thus far. Clearly,Machine Vision/Industrial Image Processing will remain a dynamic growth industry in the future.

ISRA operations comprise two main divisions. In the Industrial Automation division, industrial robots are taught how to “seeintelligently” with the aid of cameras and sophisticated hardware/software. Meanwhile, the Surface Vision division focus-es on providing 100-percent surface inspection technology to severed sectors all over the world. These solutions alloweven the smallest material flaws to be identified, located and evaluated at ultra-high speeds. Surface Vision is a sector inwhich ISRA is now the undisputed global leader.

ISRA offers turnkey systems consisting of self-developed strategic components and in-house hardware/software. These inturn contain the so-called “brainware” that represents the strategic core competence of the company: technical know-howinvolving complex mathematics, optics and physics. But technological sophistication is just part of the picture at ISRA. Forus, the absolute key is providing optimal cost/benefit to the customer, which is why ISRA systems and solutions alwaysoffer such a rapid return on investment (ROI).

At ISRA, innovation is the engine of growth. One of the salient innovations of financial year 2007/2008 was a new softwarearchitecture for “Enterprise Production Management Intelligence”. Normally inspection solutions provide huge variety ofdata about product quality. In order to take rapid and targeted production decisions, a customer needs access to the rel-evant information for his case as well as the capacity to process and valuate it. This where our groundbreaking system forEnterprise PROduction Management Intelligence EPROMI comes in. It not only provides the user with all available pro-duction data in a clear and condensed form, but also links up to operating functions such as order management andresource planning. The ISRA’s EXPERT5i modules, the customer can then synthesize all available information and gener-ate objective, logically sound decision options for the customer. This in turn enables managers on all organizational lev-els to optimize production and boost profitability in a sustained fashion. A broad portfolio of variously configured EXPERT5i

modules allow the user to access and exploit data over a worldwide network from any location, both locally and globally.

Generating short term Return on Investment for the customerMachine Vision automation offers large potential

ISRA VISIONAnnual Report 2007/2008

5ISRA VISION Annual Report 2007/2008

6

ISRA’s EXPERT5i modules enable the user to quickly find answers to a whole range ofquestions relevant to optimizing processes and profitability. By weighting and evaluat-ing data according to specific questions, these modules are able to generate knowl-edge-based suggestions for the decision-maker - not just at one location but worldwidethroughout the entire company. For example, comprehensive data regarding a specificsteel strip can be analyzed in order to determine a better allocation of materials. Thiscan help rationalize the use of resources as well as improve profit margins. Thus, ISRA’sEnterprise Production Management Intelligence solution not only lowers the customer’sproduction costs, but also boosts the profitability he can achieve with his products.

ISRA’s profitable growth strategy is straightforward: Convincing our existing clientele ofthe benefits of our new products while at the same time expanding our customer base.

When it comes to the Security/Specialty Paper segment, ISRA is already the worldwide leader. For years now, we haveproven our mettle as a reliable partner to a number of central banks in the highly specialized field of inspecting bank notepaper. In financial year 2007/2008, ISRA was proud to introduce a cutting-edge product which quickly won over a num-ber of strategically important customers. Based on sophisticated camera technology, this powerful new solution offers qual-ity control and 100-percent inspection of bank note paper that is truly state-of-the art, one that satisfies the increasinglystringent requirements of central banks all over the world.

Display Glass is a key strategic growth segment for ISRA. The glass surfaces used for computers and TV displays arebecoming larger all the time, which makes quality control all the more crucial. This is because bigger surfaces requiremore intensive processing, which exponentially increases not only added value but also the follow-up costs of correctingany flaws. Right from the earliest production steps, our automated optical inspection modules monitor the quality of theseglass surfaces and help to analyze and classify any flaws, thus optimizing overall plant management.

Moreover, manufacturers of flat-panel displays will now be able to benefit from an innovative solution developed by ISRAin collaboration with an Asian partner. This consists of a turnkey system that uses five different inspection functions tocheck fully assembled displays for a full range of flaws, whether they be in the glass itself, in the various coating layersand filters. This allows displays that are not 100-percent perfect to be pulled off the line before they can move into thecost-intensive finishing stages of the production cycle.

Beyond the “electronical eye” Innovations as a competitive advantage for production intelligence

EXPE

RT 5

i

ISRA VISIONAnnual Report 2007/2008

7ISRA VISION Annual Report 2007/2008

8

With its new inspection systems for the Solar Industry, ISRA has already been able to acquire its first customers in one ofthe future’s most promising growth sectors. The exploitation of solar energy relies, among other things, on the use of par-abolic mirrors, a method especially widespread in sunny regions. When producing such mirrors, one must ensure thatthey are formed in such a way as to accurately direct the reflected rays of the sun towards a built-in pipeline. The thermalenergy created by heating up the liquid in this pipeline is then converted into electric power. The new solutions offered byISRA make the inspection of solar parabolic mirrors quicker, easier and more accurate. These enhanced inspections cansignificantly boost energy output on a sustainable basis. During the production process, our inspection system takes accu-rate measurements of variances between the actual mirror’s angle and the defined target angle. This is done with a cut-ting-edge camera system that is far more accurate and rapid than existing laser-based technologies.

ISRA has also developed a solution for the automated inspection of thin-film solar cells, which can be used in a wide rangeof highly complex production steps. The end result: optimal quality and increased yield in the production of thin-film mod-

ules. In fact, our system is so flexible that it can be successfully deployed in other segments of the photovoltaic industryas well. Thus, ISRA inspection systems ensure maximum process reliability and output efficiency. The combination of fullyautomated inspection with tools for 100-percent defect detection and process optimization helps to boost the output ofproduction plants, giving customers a competitive advantage on the global market. ISRA intends to play a formative rolein both of these new growth segments as well, and will thereby help to develop the market for clean and efficient alterna-tive energies.

Fancy packaging seems to be gaining in importance in the marketing strategies pursued by our customers. Just thisrequirement increases the need for 100-percent inspection: ISRA now additionally offers its customers even greater func-tionality with a new range of products for the Print Industry. Our comprehensive inspection systems cover the gamut ofproduction steps, and are supported by key ancillary functions. For example, our standard inspection system can be sup-plemented with an optional color-monitoring feature, which ensures that a specific shade of color remains consistentthroughout its long journey through the printing machinery. Another optional module can monitor repetitive features andattributes in certain product-specific graphics. At the end of the production process, when printed packaging sheets arerolled back up for example, an automatic “rewind manager” allows defective portions to be removed. In financial year2007/2008, ISRA’s innovative products allowed it to break into a new market segment: Printed Electronics. The first sys-tems have already been installed for customers.

A wealth of new opportunitiesExploiting the potential of the solar and print industries

ISRA VISIONAnnual Report 2007/2008

9ISRA VISION Annual Report 2007/2008

10

To thrive in the fiercely competitive Automotive Industry, one must be able to offer top quality, maximum flexibility and lowcosts, all the same time. This is because the automobile production process requires precise measurements and a highaccuracy of fit. This can only be assured with image processing systems that are custom-tailored to specific productionsteps. Thus, ISRA boasts a complete range of innovative systems and solutions for the most complicated measurementtasks associated with the assembly of car bodies. In addition, we provide an intelligent toolkit comprising in-line meas-urement technologies as well as software for in-process analysis.

Our intelligent, multi-process software allows our customers to perform comprehensive quality management of process-measurement data. Thanks to a continuous, end-to-end monitoring, visualization, analysis and optimization of the pro-duction cycle, dimensional variations and off-size conditions can be quickly spotted. Thus, manufacturing problems areidentified directly and can be immediately corrected, before defects give rise to rejects and excess costs. In addition, our

systems provide detailed analyses and statistical reports that facilitate the evaluation of process capability as well asprocess optimization. Thus, they offer end-to-end quality control and quality measurement functions, not just locally (foreach measurement cell), but for each vehicle assembled at a given plant. Moreover, our systems can be linked up onlineinto a global network. Hence they already have become key decision-making tools for managers, especially in the auto-motive industry. In December 2008, ISRA’s 3D in-line measurement technology was approved for use by a leadingGerman car manufacturer. This success validates our strategic decision to expand the product pallette to include theMeasurement Technology and Production Decision Intelligence sectors.

New market insights ISRA’s 3D gauging make the “seeing” robots produce “quality” cars

ISRA VISIONAnnual Report 2007/2008

11ISRA VISION Annual Report 2007/2008

12

For the past ten years, ISRA has been continuously profitable, with annual average revenue and net-income growth ofmore than 30 percent. This outstanding performance has allowed us to further expand our leading market position. Witha solid capitalization and plenty of financial leeway, the Group is well positioned to exploit whatever opportunity rises fromthe present crisis. ISRA products provide customers with a quick return on investment (ROI), which is exactly what theyurgently need in economically troubled times: a way to cut costs. All in all, Machine Vision is the most effective solutionfor boosting the efficiency of production, for enhancing quality, and for optimizing yields.

With a broad range of innovative solutions, ISRA is committed to a long-term growth strategy. As a response to the chal-lenging economic environment by redoubling our sales and marketing efforts, which is already beginning to fruit. After thesuccessful integration of a wide variety of recent acquisitions, we are now focusing on boosting efficiency by optimizingproduction, organization and administration throughout the entire ISRA Group. Our objective will be to keep profitability

stable, even in the face of possible revenue reductions. To this end, ISRA has developed a stringent cost-savings program,partially with the support of external experts. Some of these measures have already been implemented, while others arealready prepared as a rapid and efficient reaction option in case of changing circumstances.

Thanks to its solid financial position and its outstanding product and service portfolio, ISRA is well poised to operate suc-cessfully even in a difficult market environment. This is repeatedly confirmed by the many project enquires we receive fromcustomers all over the world.

Looking forward out of the “storm” Staying on course with sustainable profitability

ISRA VISIONAnnual Report 2007/2008

13ISRA VISION Annual Report 2007/2008

14 ISRA VISIONAnnual Report 2007/2008

Reports und Consolidated Financial Statements

15ISRA VISION Annual Report 2007/2008

Reports and ConsolidatedFinancial Statements - Group Management Report- Report of the Supervisory Board- Corporate Governance Report

Reports und Consolidated Financial Statements

16

1. Business Situation and Operating Environment1.1. ISRA is a specialist in intelligent systems for industrial image processingThe ISRA group develops, produces and markets intelligent systems for industrial image processing (Machine Vision) using application-

specific modular standard software solutions for surface inspection (Surface Vision), robot guidance (Robot Vision) and quality control

(Quality Vision). ISRA has structured itself according to industry sectors in order to maintain a close dialog with the respective industry’s

global players, thus applying itself where it most benefits the customer. The company offers solutions for various process steps. In the area

of industrial automation, ISRA has focused on the automotive, general industries and food & packaging markets and offers surface inspec-

tion solutions for the glass, display glass, solar industry, plastics, films, nonwovens, print, printed electronics, paper, specialty paper and metal

markets.

ISRA VISION – DIVISIONS AND BUSINESS UNITS (BU)

1.2. The ISRA Vision Group is geared towards the marketsThe ISRA Vision group is broken down into two business divisions and nine business units. In the 2007/2008 fiscal year, the Industrial

Automation business division includes the Automotive, General Industries and Food & Packaging Units. The Surface Vision business divi-

sion comprises the Glass, Display Glass, Plastics, Print, Paper and Metal units.

1.2.1. ISRA VISION AG takes on holding responsibilitiesISRA VISION AG in Darmstadt is taking on the holding functions in the ISRA Group. The central departments of Finance, Research &

Development, Marketing, Purchasing and Electrical Production are all concentrated at this location. The Industrial Automation division, with

the automotive industry as its primary focus, will be managed from Darmstadt. The expansion of the business toward the business unit Food

Inspection is to be promoted from here. The business unit Print from the Surface Vision division is also concentrated at this location.

1.2.2. Acquisitions have significantly expanded the businessThanks to the acquisition of its competitor Parsytec at the end of July 2007, ISRA has significantly expanded its business in the surface vision

division. ISRA is now the world market leader in the surface inspection of metal and one of the leading specialists in the paper sector.

Parsytec has largely been successfully integrated into the ISRA Group. On December 14, 2007, it was decided at the special General

Meeting of the Aachen-based company to rename the company ISRA VISION PARSYTEC AG. At the end of the 2007/2008 fiscal year, ISRA

held around 93 percent of the Parsytec shares.

ISRA VISION PARSYTEC AG in Aachen is focused on the metal and paper industry. This is where the innovative sector solutions are devel-

oped, enhanced and marketed. The new software architecture for the “Enterprise Production Decision Intelligence” will likewise be devel-

oped in Aachen and marketed from there. The EPROMI architecture with its EXPERT5i modules will help optimize management decisions

by enabling production management to exercise direct control over the production hall.

ISRA took over the Mainz company metronom Automation GmbH (Metronom) as of October 1, 2007. Metronom is specialized in the areas

of quality measurement technology for car body construction in the automobile industry and for general industrial image processing. With

its control and automation of measurement procedures, Metronom has earned itself a good market position.

1.2.3. Concentration of the Surface Vision business in HertenThe surface inspection business has been concentrated into ISRA SURFACE VISION GmbH, Herten. Sales, sector specific development,

engineering and part of the production are all based here. The markets for glass, display glass, plastics, specialty paper, bank note inspec-

tion and laser scanners are all supervised from Herten.

The final mechanical integration in production for several Surface Vision systems is concentrated at ISRA VISION LASOR GmbH,

Group Management Report, ISRA VISION AGFiscal Year 2007/2008

ISRA VISION

GROUP

INDUSTRIAL

AUTOMATION

SURFACEVISION

BUGlass

BUDisplay Glass

BUPlastics

BUPrint

BUPaper

BUAutomotive

BU

General

Industries

BU

Food &

Packaging

BUMetal

Group Management Report

ISRA VISIONAnnual Report 2007/2008

17

Oerlinghausen (Germany). Another field of activity at this location is basic development of software (shared with Darmstadt) for all Surface

Vision systems.

1.2.4. ISRA subsidiaries and branch in North America, South America and the UKISRA VISION SYSTEMS, INC., of Lansing (Michigan), USA, runs the entire North American automotive business of the Industrial Automation

division. All Surface Vision activities in America were brought together at ISRA SURFACE VISION INC., of Duluth (Georgia), USA. ISRA

VISION Parsytec Inc., Chicago, IL, USA was also successfully integrated into this company. The South American market is being handled

from the branch in Sao Paulo, Brazil.

In the 2007/2008 fiscal year, ISRA continued to expand its position as a global innovation and market leader in the glass sector. The British

company ISRA VISION Ltd., London, UK offers a good basis for growth in the geographic markets of the UK and Ireland. The American affil-

iate, Image Automation Inc., Worthington, Ohio, USA, has also been successfully integrated into the ISRA Group.

1.2.5. Expansion in AsiaISRA VISION (Shanghai) Co. LTD, Shanghai, China, is the production headquarters for the entire Asian market, and in particular for the fast-

growing Chinese market. Activities there are currently concentrated on the Surface Vision division.

ISRA VISION, Taiwan – Activities in the Display Glass sector (for flat screens) were substantially expanded with the establishment of a busi-

ness presence in Taiwan. The sales and engineering team takes care of this business unit’s activities in Taiwan, Korea, Japan and China.

The representative office in Hong Kong is attached organizationally to ISRA VISION Taiwan. Activities in Calcutta, India, have been initiated.

Through Parsytec, the ISRA Group has greatly augmented its market position in Asia thanks to a sales team that is well-established on the

market in Japan and Korea. The Parsytec Asia Pacific Co., Ltd. in Korea and the Parsytec Japan Co., Ltd. in Japan are sales companies for

surface solutions from ISRA.

1.3. Machine Vision is a key technologyMachine Vision technology constitutes a key technology in the area of automation, production control and fully automatic quality assurance.

The Machine Vision market is characterized by a continually increasing degree of automation in industrial production, joined with continu-

ous, fully automatic optimization of productivity and production quality.

The competitive environment is characterized by fragmentary distribution since there are many suppliers with a relatively small share of the

market. In Europe and the US, there are only a few large companies with revenue in excess of 10 million Euros and more than 100 employ-

ees. The majority of companies are smaller niche-suppliers operating mainly locally, with few employees. The larger suppliers – such as

ISRA – focus on highly specialized system solutions and modular standard components for sectors and markets whose economic cycles

remain largely unaffected by global economic influences.

1.4. Global economy grows by only 3.7 percent in 2008 In the fall report from September 2008, the Kieler Institut für Weltwirtschaft (IfW) was expecting the global economy to grow in 2008 by around

3.7 percent. That notwithstanding, the various institutes are dropping their estimates on a nearly daily basis. One thing is certain: there was

a definite downturn in comparison to previous years. In the last four years, the growth rates were more than 5 percent. The experts all agree

that the market’s slowdown is the direct result of the financial crisis that started in the USA and infected other industrial nations. Faster and

stronger than initially expected, the crisis expanded to include emerging countries and other developing nations. In the Eurozone, the econ-

omy is estimated to have grown in 2008 by around 1.4 percent, and in the USA by around 2 percent.

According to a November 2008 estimate by the International Monetary Fund, the BRIC states have grown in the past year as follows: Brazil

by around 5.2 percent, Russia by around 6.8 percent, India by around 7.8 percent and China by around 9.7 percent. The Middle East

increased by 6.1 percent.

1.5. Slower growth for Machine Vision Due to the global financial crisis, the German image processing industry did not entirely attain the six percent growth in revenue that had

been forecast for 2008. In the meanwhile, the industry in this country has reached a volume of around 1.2 billion Euros. Despite the robust

domestic business, the foreign markets remain the most important growth drivers, observed the VDMA. The German companies with image

processing technology therefore earn almost 60 percent of their revenue abroad. The market for Machine Vision products is primarily con-

centrated on the highly developed industrial regions of North America, Europe and Japan, and on rapidly developing Asian nations such

as Taiwan, South Korea and the BRIC states.

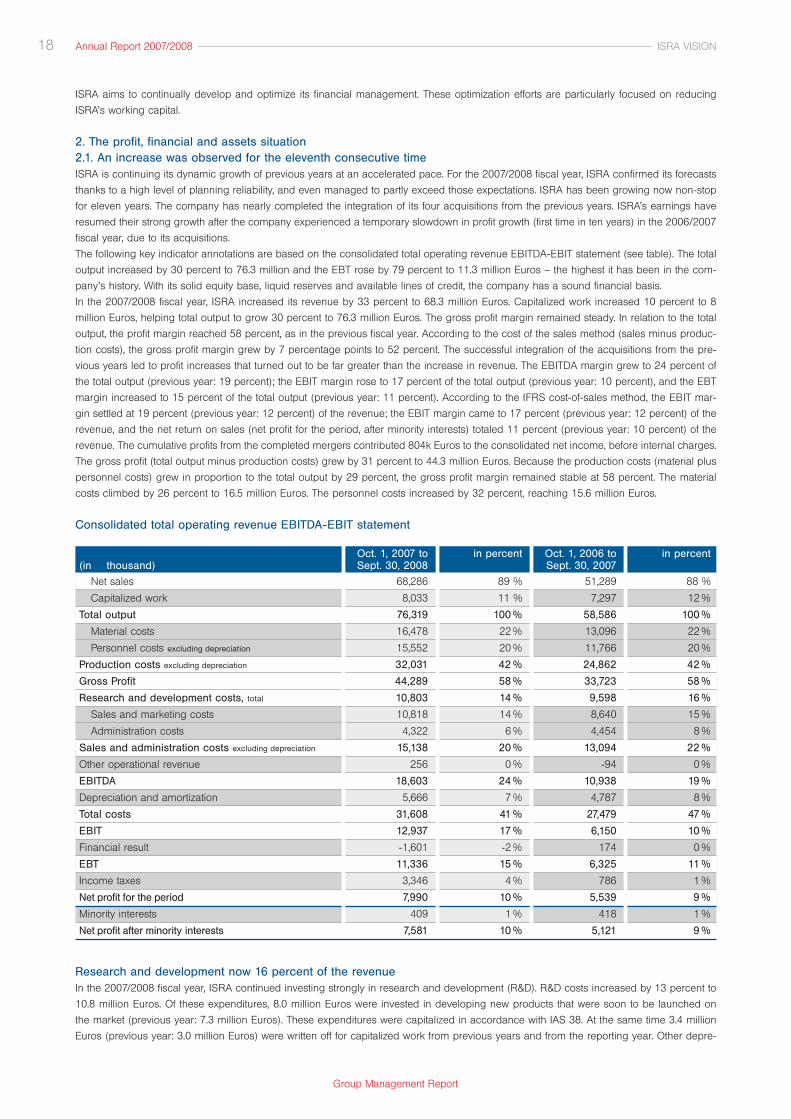

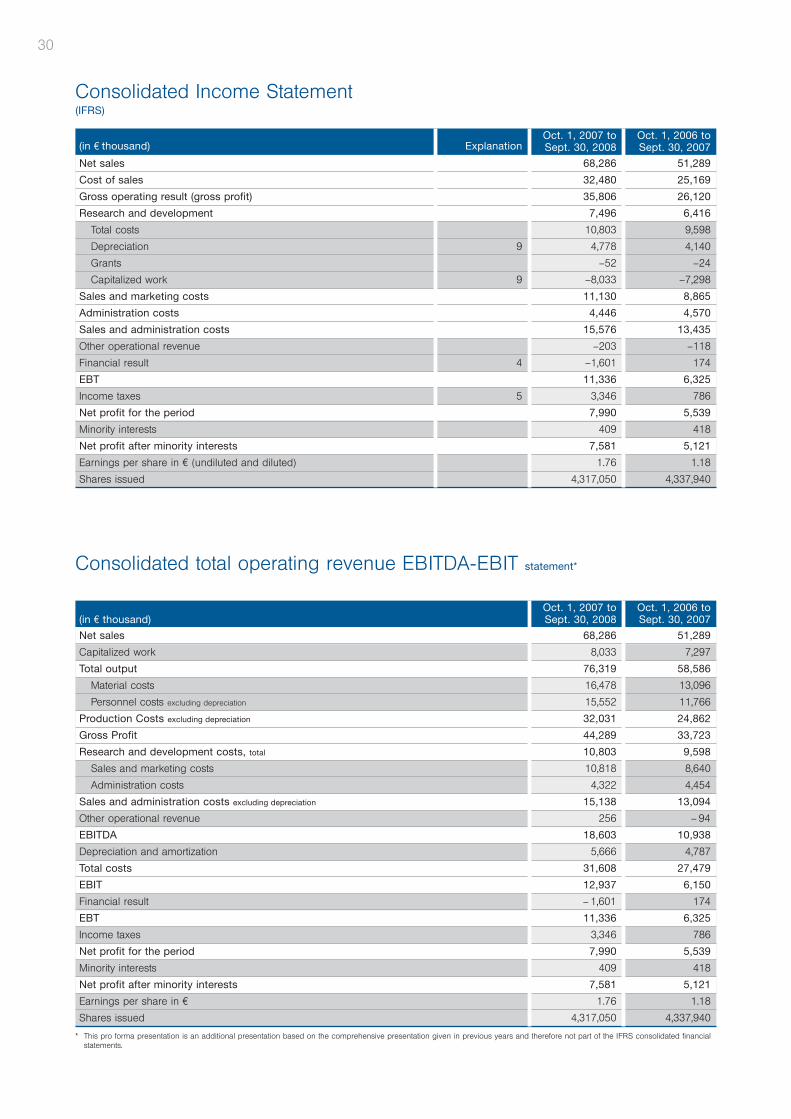

1.6. Corporate governance through value-oriented managementThe company’s most important performance indicators stem from the consolidated total operating revenue EBITDA-EBIT statement. This

provides a view of the company’s efficiency and profitability that is relevant to the industry. The most important components here are the

gross margin (gross profit to total output), the EBITDA, the EBT and the EBT margin (EBT to total output) (see table).

1.7. The great importance of ISRA’s financial managementOur financial management’s top priority is to safeguard the company’s liquidity at all times. The liquidity reserves are always set up in such

a way that all payment obligations can be met on time. The group is basically financed centrally through the parent company in Darmstadt,

ISRA VISION AG. The liquidity is safeguarded through in-depth financial planning. The operational business is financed from the cash flow

and the available liquid funds.

Group Management Report

ISRA VISION Annual Report 2007/2008

18

ISRA aims to continually develop and optimize its financial management. These optimization efforts are particularly focused on reducing

ISRA’s working capital.

2. The profit, financial and assets situation2.1. An increase was observed for the eleventh consecutive timeISRA is continuing its dynamic growth of previous years at an accelerated pace. For the 2007/2008 fiscal year, ISRA confirmed its forecasts

thanks to a high level of planning reliability, and even managed to partly exceed those expectations. ISRA has been growing now non-stop

for eleven years. The company has nearly completed the integration of its four acquisitions from the previous years. ISRA’s earnings have

resumed their strong growth after the company experienced a temporary slowdown in profit growth (first time in ten years) in the 2006/2007

fiscal year, due to its acquisitions.

The following key indicator annotations are based on the consolidated total operating revenue EBITDA-EBIT statement (see table). The total

output increased by 30 percent to 76.3 million and the EBT rose by 79 percent to 11.3 million Euros – the highest it has been in the com-

pany’s history. With its solid equity base, liquid reserves and available lines of credit, the company has a sound financial basis.

In the 2007/2008 fiscal year, ISRA increased its revenue by 33 percent to 68.3 million Euros. Capitalized work increased 10 percent to 8

million Euros, helping total output to grow 30 percent to 76.3 million Euros. The gross profit margin remained steady. In relation to the total

output, the profit margin reached 58 percent, as in the previous fiscal year. According to the cost of the sales method (sales minus produc -

tion costs), the gross profit margin grew by 7 percentage points to 52 percent. The successful integration of the acquisitions from the pre-

vious years led to profit increases that turned out to be far greater than the increase in revenue. The EBITDA margin grew to 24 percent of

the total output (previous year: 19 percent); the EBIT margin rose to 17 percent of the total output (previous year: 10 percent), and the EBT

margin increased to 15 percent of the total output (previous year: 11 percent). According to the IFRS cost-of-sales method, the EBIT mar-

gin settled at 19 percent (previous year: 12 percent) of the revenue; the EBIT margin came to 17 percent (previous year: 12 percent) of the

revenue, and the net return on sales (net profit for the period, after minority interests) totaled 11 percent (previous year: 10 percent) of the

revenue. The cumulative profits from the completed mergers contributed 804k Euros to the consolidated net income, before internal charges.

The gross profit (total output minus production costs) grew by 31 percent to 44.3 million Euros. Because the production costs (material plus

personnel costs) grew in proportion to the total output by 29 percent, the gross profit margin remained stable at 58 percent. The material

costs climbed by 26 percent to 16.5 million Euros. The personnel costs increased by 32 percent, reaching 15.6 million Euros.

Consolidated total operating revenue EBITDA-EBIT statement

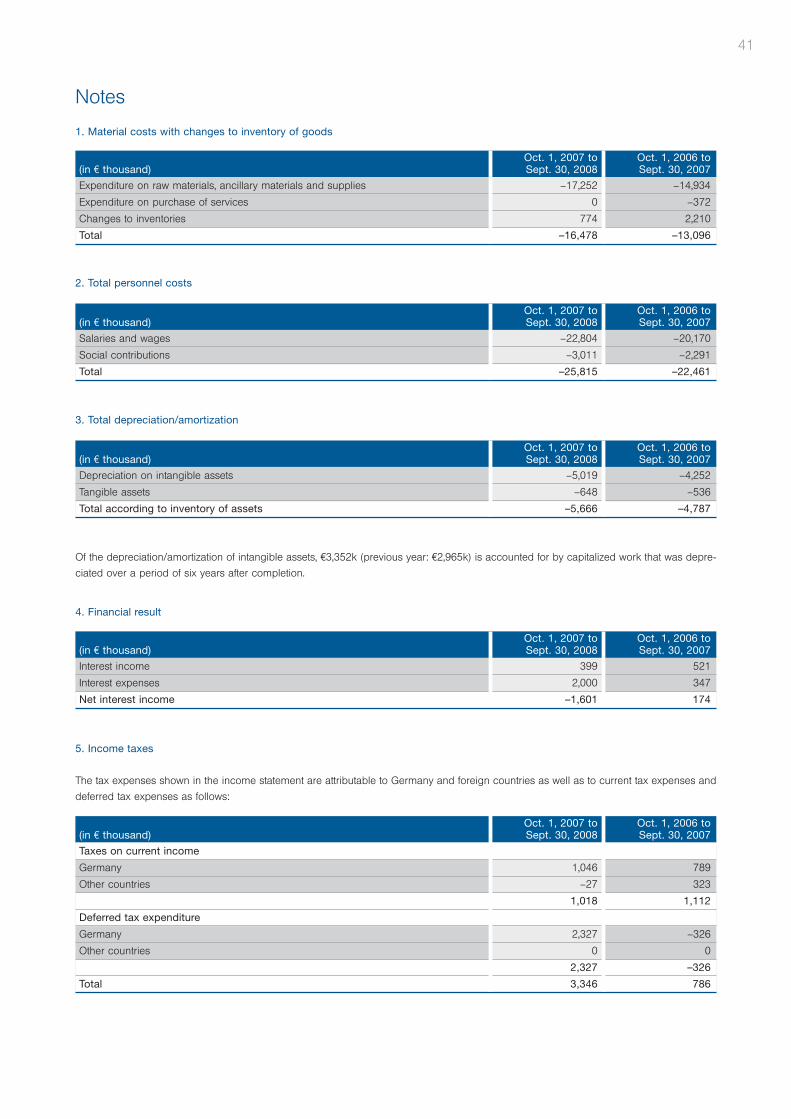

Research and development now 16 percent of the revenueIn the 2007/2008 fiscal year, ISRA continued investing strongly in research and development (R&D). R&D costs increased by 13 percent to

10.8 million Euros. Of these expenditures, 8.0 million Euros were invested in developing new products that were soon to be launched on

the market (previous year: 7.3 million Euros). These expenditures were capitalized in accordance with IAS 38. At the same time 3.4 million

Euros (previous year: 3.0 million Euros) were written off for capitalized work from previous years and from the reporting year. Other depre-

Group Management Report

Oct. 1, 2007 to in percent Oct. 1, 2006 to in percent(in € thousand) Sept. 30, 2008 Sept. 30, 2007

Net sales 68,286 89 % 51,289 88 %

Capitalized work 8,033 11 % 7,297 12 %

Total output 76,319 100 % 58,586 100 %

Material costs 16,478 22 % 13,096 22 %

Personnel costs excluding depreciation 15,552 20 % 11,766 20 %

Production costs excluding depreciation 32,031 42 % 24,862 42 %

Gross Profit 44,289 58 % 33,723 58 %

Research and development costs, total 10,803 14 % 9,598 16 %

Sales and marketing costs 10,818 14 % 8,640 15 %

Administration costs 4,322 6 % 4,454 8 %

Sales and administration costs excluding depreciation 15,138 20 % 13,094 22 %

Other operational revenue 256 0 % -94 0 %

EBITDA 18,603 24 % 10,938 19 %

Depreciation and amortization 5,666 7 % 4,787 8 %

Total costs 31,608 41 % 27,479 47 %

EBIT 12,937 17 % 6,150 10 %

Financial result -1,601 -2 % 174 0 %

EBT 11,336 15 % 6,325 11 %

Income taxes 3,346 4 % 786 1 %

Net profit for the period 7,990 10 % 5,539 9 %

Minority interests 409 1 % 418 1 %

Net profit after minority interests 7,581 10 % 5,121 9 %

ISRA VISIONAnnual Report 2007/2008

19

ciation and amortization for software and licenses amounted to 1.7 million Euros (previous year: 1.3 million Euros). Application-oriented

developments that can be brought onto the market quickly are currently the focus of the R&D strategy, and the reduction of the time-to-

market is a decisive control variable.

Sales, administration and marketing costsSales and administration expenses (without depreciation and amortization) climbed by 16 percent to 15.1 million Euros, which is less than

the growth in revenue. The sales and marketing costs increased by 25 percent to 10.8 million Euros, while ISRA managed to decrease its

administrative costs by 3 percent to 4.3 million Euros. The EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) grew by

70 percent to 18.6 million Euros. Depreciation and amortization increased by 18 percent to 5.7 million Euros. The depreciation and amorti-

zation of capitalized work account for 3.4 million Euros (previous year: 3.0 million Euros) of the above-stated figure.

EBIT doublesThe EBIT (Earnings before Interest and Taxes) rose by 110 percent to 12.9 million Euros. Because of the extensive credit financing of the

Parsytec acquisition, the financial result is no longer positive. The financial result for the period dropped to negative 1.6 million Euros. The

EBT (Earnings before Taxes) rose by 79 percent to 11.3 million Euros. The EBT margin reached 15 percent in relation to total output (pre-

vious year: 11 percent), and 17 percent in relation to revenue (previous year: 12 percent). Tax charges rose to 3.3 million Euros (previous

year: 0.8 million Euros), thus staying within normal parameters. In the previous fiscal year, ISRA had already started profiting from the tax

reform that took effect in Germany as of January 1, 2008. Due to the revaluation of the deferred taxes (required by the IFRS), there was a

tax revenue of 2.2 million Euros in the previous year.

The annual net profit (after minority interests) increased by 48 percent to 7.6 million Euros. This corresponds to earnings of 1.76 Euros per

share (previous year: 1.18 Euros), with the total shares numbering 4,317,050 (previous year: 4,337,940).

Growth in the individual segments and markets In the largest division, Surface Vision, ISRA is one of the world-wide leading companies. The total output for this segment rose by 37 per-

cent to 58.3 million Euros in the 2007/2008 fiscal year. ISRA has thus once more expanded its solid position on the market. The EBIT rose

by 153 percent to 9.9 million Euros. The Industrial Automation division increased by 12 percent to 18 million Euros. The EBIT for the divi-

sion grew 36 percent to 3 million Euros.

The strongest growth impulse for the Surface Vision division came from the business unit glass and metal, which recorded particular growth

in the Asian business. There was even sales growth in specialty paper and print. In the Industrial Automation division, the automotive busi-

ness unit managed to show the greatest growth.

2.2. Fund assets of 12.5 million EurosIn the 2007/2008 fiscal year, the operational cash-flow reached 6.4 million Euros (previous year: 6.7 million Euros). As of September 30,

2008, the cash flow from investment activities totaled 13.5 million Euros and was primarily affected by both the acquisition of metronom

Automation GmbH as well as the acquisition of additional shares in ISRA VISION Parsytec AG. The cash flow from investment activities

ended at -22.5 million Euros (previous year: -26.3 million Euros). The cash flow from financing activities reached 6.3 million Euros (previous

year: 26.8 million Euros). The previous year’s figures primarily involved a loan to finance the acquisition of Parsytec. Due to the other acqui-

sition activities, the net cash flow was negative at 9.7 million Euros (previous year: 6.8 million Euros), which caused the fund assets to drop

to 12.5 million Euros (previous year 22.3 million Euros) at the end of the fiscal period. At the same time, the liquid assets rose in the fourth

quarter by 0.6 million Euros. Cash in the amount of 2.1 million Euros was deposited as security.

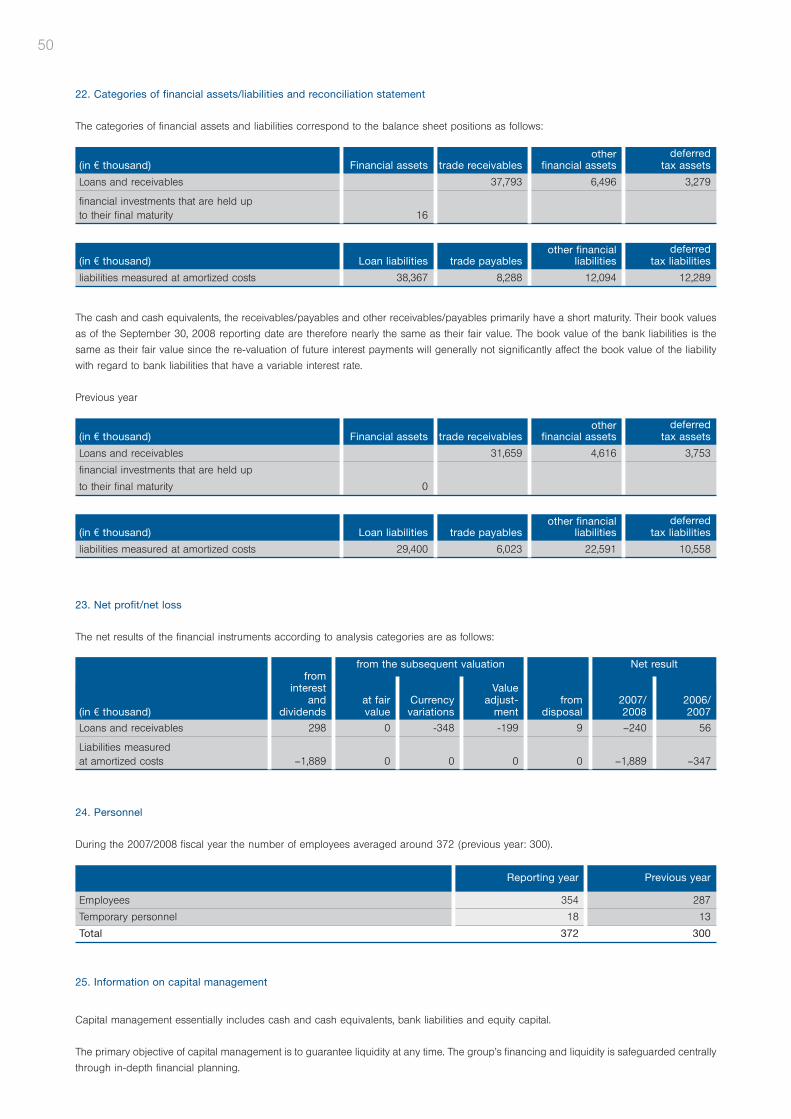

2.3. Solid financing at a 51 percent equity ratioIn the 2007/2008 fiscal year, ISRA increased the group’s total assets by 6.7 million to 149.7 million Euros. The liquid assets decreased to

12.5 million Euros (previous year: 22.3 million Euros), mainly due to other acquisition activities. This means that cash assets now make up

just under 8 percent of the total assets (previous year: 16 percent). The trade receivables grew by 6.1 million to 37.8 million Euros. 17.3 mil-

lion Euros (previous year: 14.6 million Euros) account for receivables from unfinished orders, as assessed according to the “percentage-

of-completion” method.

Current assets dropped to a portion of 49 percent of the total assets (previous year: 52 percent). At 51 percent (previous year: 48 percent)

of the total assets, the long-term fixed assets reached 75.6 million Euros (previous year: 68.5 million Euros). Due to M&A transactions, good-

will increased by 4.1 million to 38.7 million Euros.

The tax loss carryforwards for the entire ISRA group totaled 20.9 million Euros as of September 30, 2008. Deferred tax assets were estab-

lished for 9.8 million Euros of the loss carryforwards.

On the liabilities side of the balance sheet, equity capital rose to 75.7 million Euros (previous year: 70.0 million Euros). The equity ratio totaled

51 percent.

The short-term loan contracts were converted into a long-term financing that allowed the company the most flexible repayment options pos-

sible. The interest was set up based on the Euribor so that the company will be able to participate in the Euribor’s latest interest develop-

ments in 2009. The company has the option to hedge the interest at any time. As of the end of the fiscal year, ISRA furthermore possesses

available financing options of over 15 million Euros.

The short-term liabilities dropped from 56.7 million Euros in the previous year to 35.1 million Euros. The short-term bank liabilities decreased

by 11.7 million Euros to 13.5 million Euros in favour of a long-term financing. Other liabilities decreased by 11.1 million Euros to 11.5 mil-

lion Euros.

Group Management Report

ISRA VISION Annual Report 2007/2008

Under the long-term liabilities, the bank liabilities increased to 24.9 million Euros (previous year: 4.2 million Euros). There is furthermore a

liability of 4.1 million Euros from the ERP Innovation Program of the Reconstruction Loan Corporation (Kreditanstalt für Wiederaufbau).

3. Non-financial performance indicatorsThe success of the ISRA group depends to a considerable degree on its staff. The company is therefore continuing to invest in Human

Resource Management in order to strategically strengthen and expand its future and succession planning in the coming years. ISRA attach-

es great importance to well-trained, educated employees and to their qualifications and abilities. This can be seen in the number of employ-

ees with academic degrees.

Mature, long lasting relationships with key industry customers in combination with high quality products and professional project manage-

ment are a result of an intensive, strategic key account management.

4. EmployeesIn the 2007/2008 fiscal year, the ISRA group employed an average of 372 people worldwide (previous year: 300). 388 people were emplo-

yed as of September 30, 2008. The majority work in Germany at the locations in Darmstadt (25 percent), Aachen (14 percent), Karlsruhe (4

percent), Herten (23 percent), Oerlinghausen (8 percent) and Mainz (4 percent). 11 percent of the employees work in the USA and 8 per-

cent in Asia. Another 3 percent work in London and Brazil. Of the staff employed world-wide as of September 30, 2008, 48 percent work in

production and engineering and approximately 16 percent in research and development. 17 percent of ISRA employees work in sales and

marketing and 19 percent in the field of administration.

5. Remuneration Report The structure of the remuneration system for the Executive Board is determined by the Supervisory Board. Criteria used to assess the app-

ropriateness of the remuneration include particularly the tasks of the respective Executive Board member, their personal performance, the

performance of the entire Executive Board, and the company's economic position, success and future prospects, all in comparison to other

people in equivalent positions. The remuneration for Executive Board members comprises short-term components and elements with long-

term incentives. The non-performance based components involve fixed remuneration, payments in kind and other types of benefits. The

short-term components comprise performance-based and non-performance based elements. The non-performance based fixed base remu-

neration is paid monthly as a salary and is reviewed on a yearly basis. The Executive Board members also receive other benefits, in parti-

cular allowances for a private pension plan, health insurance and long-term care insurance; they also receive benefits in kind that primarily

involve the use of a company car. The payments to the members of the Executive Board include performance-based, variable components

which may, in individual cases, total up to 30 percent of their base pay. They are annually revised by the Supervisory Board on base of

objectives.

As a publicly traded company, ISRA VISION AG has the singular opportunity to have its employees and the Executive Board participate

directly in its success via a stock option program, a variable element of their remuneration in the form of a long-term incentive. Options may

only be exercised after a blocking period has expired. According to the stock option program, the options can be exercised for either cash

or shares; however, ISRA VISION AG’s internal practice tends towards offering cash for stock options. An option holder’s options expire if

the option holder has terminated the employment relationship with the Company, or if they are no longer a member of a statutory body of

ISRA VISION AG or of a group company. Irrespective of this, options remain in force unchanged if the employment relationship ends due

to the employee retiring or owing to professional disability. Options cannot be inherited or transferred. In addition, option rights expire 5 years

after the day they are issued.

Options may only be exercised if at least one of the two predefined targets for success has been reached. These are based on the stock

performance in relation to purchase price and time of exercise. The subscription price for a share is given by the arithmetic average of the

closing prices in XETRA trading for the share in the period between the 15th and 5th trading day (before the option is issued), multiplied by

a factor of 1.1.

The Supervisory Board is authorized to define the further details of the subscription conditions and of the issue and structure of the options

for the Executive Board. In addition, the Supervisory Board is authorized to transfer for the Executive Board the shares needed to fulfill the

option rights by issuing acquired treasury shares or by issuing new shares through a capital increase.

The members of the Supervisory Board receive adequate remuneration for their membership on the Supervisory Board every full fiscal year;

this remuneration is determined by the General Meeting and is payable after the end of the fiscal year. The Chairman receives double the

amount; the vice chairman receives 1.5 times the amount. Supervisory Board members who have not belonged to the Board for a full fis-

cal year will be remunerated based on the duration of their membership on the Supervisory Board.

The members of the Supervisory Board will be reimbursed for all expenses and for the value added tax that they must pay on their remu-

neration and expenses.

6. Risks and opportunities for the company’s future developmentA commercial approach goes hand-in-hand with risks. A company’s success is characterized by successful opportunities exceeding the

downside risks in all important decisions. To compare risks against opportunities, ISRA uses a qualified risk management system. Using this

risk management system, all important risks are made visible both retrospectively and prospectively. The system is build on an effective

management information system, in particular the internal reporting structure. The system is continually readjusted in line with the insights

gained from previous years and the new requirements of the German Stock Companies Act (Aktiengesetz) and the German Corporate

Governance Code. The risk management system is especially aimed at recognizing risk early on, controlling it and monitoring it.

Group Management Report

ISRA VISIONAnnual Report 2007/200820

21

ISRA endeavors to realize risks quickly. Owing to the globalization of the company and the growing number of locations, it is increasingly

important to promptly procure, distribute and process detailed information.

ISRA is exposed to the general legal and economic risks in the countries where the group companies operate. In addition to this, the group’s

net sales and profit situation may also be significantly influenced by the risks described below. These are the risks that have been identified

until now. This does not preclude the existence of other risks not yet realized by the management, nor does it preclude the possibility of

these risks being under-estimated as negligible. Sufficient provisions were made for all likely risks. There have not been any risks identified

which threaten the existence of the company.

Financial crisis: Preventative measuresOne of the possible scenarios for the current fiscal year assumes a slowdown on the market. Some projects and delivery deadlines may be

postponed. Decisions for new investments may be delayed, and some major customers may temporarily halt their investment activities. The

management is expecting the majority of the key customers’ budget decisions for the current fiscal year to be concretized in

January/February 2009.

Because of the current trend, the company has modified its risk management system to suit the current needs and has increased its sen-

sitivity in all sectors. Reporting intervals have been significantly shortened to allow risks to be detected early on. Quarterly reports have been

shortened to a monthly cycle, and monthly reports to a bi-weekly interval. This intensive oversight pertains to all of the company’s key per-

formance indicators such as the revenue forecast, the liquidity planning, outstanding receivables and production capacity planning. The cus-

tomers and markets are being more intensively monitored with much closer scrutiny. New customers in particular will be subject to a stricter

credit check. Bad debt losses will be countered by modifying the payment agreements with the customer. Additional measures to boost pro-

ductivity and efficiency have already been started. To guarantee the company’s ability to pay and be financially flexible, a liquidity reserve

in the form of a line of credit and cash is being held in reserve. As of September 30, 2008, ISRA disposed of lines of credit totaling more

than 15 million Euros.

If the world-wide turbulence on the financial markets perseveres, and if the economy weakens as a result of this, the economic situation of

our customers may be negatively impacted, along with the demand for our products. This may result in commensurate risks to our revenue

and profits. The management has therefore simulated various risk scenarios to be prepared for all eventualities. The executed simulations

pertain especially to delays in orders, drops in orders, bad debts and overdue incoming payments.

Further risks and opportunities for the company’s future developmentAs a rule, ISRA bills customers in Euros. Only in the USA are quotations made both in the local currency and in Euros. The Management

regularly adjusts the sales calculations to changes in the exchange rates. This prevents currency-based risks. There is only the risk of ISRA's

competitive edge over local suppliers being dulled in the event that the dollar drops. This risk is, however, limited because the administra-

tive and sales costs in the USA are also in dollars.

ISRA’s core technology is Machine Vision technology for industry. The basis of this technology is the combination of specialized basic and

application technology knowledge from the fields of robotics and vision, plus process knowledge, with software technology in marketable

standard hardware and software components. Consequently, protecting intellectual property rights – especially where know-how and soft-

ware are concerned – is particularly important to ISRA. These technologies are characterized by continuous ongoing development. ISRA’s

success depends on its capability to promptly develop, acquire and bring onto the market new or improved products that conform to

changes in technology and meet customer demands.

ISRA’s success so far shows that the company is characterized by a high level of innovation. In the last few years, ISRA has demonstrated

its ability to put the necessary investment in a highly focused research and development, to recognize risks promptly and start measures to

innovate at a very early stage.

The global Machine Vision market is highly fragmented. ISRA is therefore competing here with a variety of suppliers – a few large ones and

many smaller ones. In order to maintain its success in the future as well, ISRA continues to work nonstop on raising the barrier for com-

petitors looking to enter the market – both in R&D and in the fields of customer relationships and customer satisfaction. To achieve this, the

company will in future invest even more, particularly in sales and customer support.

ISRA counteracts the dependency on economic fluctuations with the strategy of diversifying in various industries in different countries.

Consequently, ISRA will continue to concentrate on products that guarantee the customer a high ROI (Return On Investment) and therefore

bring about a fast decision to invest.

In all areas of its business, ISRA has customer relationships to many large enterprises. These companies are chiefly multinationals from the

automotive, glass, paper, print, plastics, metal and automation industries. None of these companies contributes more than ten percent of

ISRA’s revenue. Because ISRA products guarantee a high ROI and ensure a competitive edge for customers who are themselves constantly

in cost competition, customers likewise share a symbiotic relationship with ISRA. Nevertheless, it remains ISRA’s constant objective to con-

tinue increasing its number of customers through the “dual multi-segment strategy”. Using new products, smaller, regionally-based compa-

nies will also be acquired as customers in the relevant target markets.

The majority of ISRA customers show a high degree of credit worthiness. Splitting the overall receivable into a number of smaller amounts

(e.g. payable prior to work being conducted, during system construction and after initialization) works against a loss of receivables. In the

2007/2008 fiscal year, the level of unpaid receivables was less than one percent of the revenue and thus in line with the average of the past

few years.

The company intends to continue its global expansion, not just through internal growth, but also by means of strategic alliances, consoli-

dations and the acquisition of companies or parts of companies. With the acquisitions of the past few years, ISRA has demonstrated its abil-

Group Management Report

ISRA VISION Annual Report 2007/2008

22

ity to also integrate large companies successfully, thus making a considerable contribution to the growth of both revenue and profit. The

most recent acquisitions have been financed through a long-term loan at a variable interest rate. ISRA bears the risk of changes in the inter-

est rate. Because of the current development in the capital markets and because of the expected cash flow, management considers this

type of financing to be optimal at this time. There is, however, still the possibility that the acquired companies will not immediately earn back

the paid interest through their operative business. At this time, the management estimates the probability to be minimal.

The Management is working to counteract the risks involved in project business, such as fixed prices for a defined scope of services and a

fixed completion date, through intensive and rigorous controlling of proposals and project costs.

To date, no major liability claims due to defective products or sub-standard services have been made against the companies of the ISRA

group. Despite our taking the utmost care, we cannot exclude the possibility of this happening in the future.

7. Important occurrences after the balance sheet dateWith collapse of the American investment bank Lehman Brothers at the beginning of September 2007, the smoldering financial crisis has

been escalating since the middle of 2007. Other banks have also encountered difficulties in the wake of this freefall. Offering billions in aid

packages, the various governments around the globe are attempting to prevent the global financial system from collapsing. Originating in

the USA, the economic slow-down gained momentum, stoking people's fear of recession. Since then, the economic expectations for near-

ly all national economies have been adjusted downwards on a nearly weekly basis. The incoming orders in German mechanical engineer-

ing have since taken nose dive of two digit percentage points. At this current time, it is hard to tell the difference between true recession

trends and self-fulfilling prophecy. To produce a reliable growth forecast for ISRA, it is necessary to evaluate all information on the pertinent

markets. The executive board is expecting to be able to produce a reasonably reliable forecast in February of 2009.

Because of the events throughout the world on the financial market and based on various planning scenarios, individual structural adjust-

ments have already been made to reinforce the company. Consequently, individual changes have already been made to personnel, and the

production capacity has been prepared for possible adjustments.

To pay off the part of the purchase price in shares that arose from acquiring metronom Automation GmbH, the ISRA VISION AG executive

board, with the authorization pursuant to § 4 Paragraph 5 of the articles of association and the approval of the Supervisory Board, decided

on October 24, 2008 to use an investment in kind of EUR 43,300.00 to increase its capital from EUR 4,337,940.00 to EUR 4,381,240.00 by

issuing 43,300 new no-par value bearer shares from the authorized capital. As of the time of this report, this increase still had to be entered

in the commercial register.

8. Forecast Report8.1. World economy: Significant economic down-turnIn 2009, the global economy is expected to slow down. According to the IMF, the drop in demand in industrial nations and intensified loan

requirements in emerging nations are responsible for the low growth expectations. For the first time in 60 years, the IMF is expecting all

industrial nations to slip into a recession in 2009. They are forecasting that the countries will shrink by 0.3 percent. The IMF is expecting for

Germany to drop by 0.8 percent, for the USA to drop by 0.7 percent, for France to drop by 0.5 percent and for the UK to drop by 1.3 per-

cent.

Globally, the IMF predicts that the economy will only grow by 2.2 percent, which falls under the IMF’s definition of a recession. The largest

growth drivers will come from the emerging and developing nations. The experts are expecting growth of 3 percent for Brazil, 8.5 percent

for China, 6.3 percent for India, 3.5 percent for Russia and 5.3 percent for the Middle East.

In 2009, the VDMA is expecting “headwinds” for the German image processing industry. In 2009, most of the customer industries will either

dwindle or maintain their high level. The VDMA has not yet developed a clear forecast for industrial image processing. They are expecting

consolidation at a high level. Since only around a quarter of all potential applications have been realized so far, and since further areas will

open up as technology continues to develop, the machine vision industry will remain a growth sector in the mid- and long-term.

8.2. ISRA is focusing on opportunities in the crisisISRA intends to continue its many years of growth in the next several years. The current global crisis represents more than risk - it may also

provide opportunities. In particularly hard economic times, companies are thus under increasing pressure to reduce costs and improve their

competitive edge. It is precisely the solutions from ISRA that will be in demand in economically hard times, especially for automating pro-

duction, improving product quality, preventing rejects and optimizing output. There are aid packages currently being provided by the gov-

ernments to save companies from financial ruin. ISRA’s executive board is convinced that the companies will spend a significant portion of

these funds on increasing efficiency and improving their competitive edge.

With an order backlog of more than 34 million Euros, ISRA intends to continue down the previous years’ path of profitable organic and exter-

nal growth in the 2008/2009 fiscal year. Based on the current market trend - provided that there are no other significant blows to the eco-

nomic situation – the management is not expecting any drop in revenue for the current fiscal year. The prepared measures are targeted at

preventing the profit margins from deviating significantly from the previous fiscal years. It is difficult to quantify expectations at the beginning

of this fiscal year. At the current time, there is still no forecast for ISRA's customer industries. For a certified forecast, ISRA is waiting for the

major budget conferences of its key customers to happen, which are scheduled for January/February 2009.

9. Supplementary information pursuant to § 315 Paragraph 4 of the German Commercial Code (HGB)As of the balance sheet date, the company’s share capital totaled €4,337,940. It is divided into 4,337,940 common stocks registered to hold-

ers with a nominal value of one Euro. Each share conveys one vote. It is forbidden to securitize the shares.

Group Management Report

ISRA VISIONAnnual Report 2007/2008

23

EVWB GmbH & Co. KG, headquartered in Darmstadt, (majority shareholder and CEO Enis Ersü) holds a share in excess of 10 percent of

ISRA VISION AG.

The Supervisory Board consists of six members. Mr. Enis Ersü, Darmstadt, is entitled to depute a member of the Supervisory Board as long

as he holds his portion of the company’s share capital. The remaining members are selected by the General Meeting.

Pursuant to §§ 84, 85 of the German Stock Corporation Law (AktG) in conjunction with § 6 of the company’s Articles of Association, the

Executive Board is appointed and dismissed by the Supervisory Board. According to § 19 of the Articles of Association, changes to the

Articles of Association must be ratified at the annual General Meeting through a simple majority of the base capital entitled to vote that is

represented at the adoption of the resolution. According to § 179 of the German Stock Corporation Law (AktG), changes to the Articles of

Association that pertain to the objective of the company must be ratified at the annual General Meeting through at least a three-fourths major-

ity of the base capital entitled to vote that is represented at the adoption of the resolution. Pursuant to § 15 of the Articles of Association, the

Supervisory Board of the company is furthermore only authorized to make modifications to the company’s Articles of Association that con-

cern their version.

The General Meeting held on March 20, 2007 resolved an amendment to the Articles of Association. This amendment authorizes the

Executive Board to increase the Company’s share capital until March 19, 2012 once only or on multiple occasions by issuing new bearer

held no-par value shares against cash or non-cash contributions, up to a maximum amount of €2,168,970.00 (authorized capital). The

Executive Board is authorized, with the agreement of the Supervisory Board, to exclude the statutory subscription rights of shareholders

• for residual amounts,

• to secure shares in return for contributions of fixed assets, in particular in the context of mergers with other companies or the purchase

of other companies, parts of companies or of an interest in other companies.

• if the capital increase takes place by means of an equity contribution and the issued value is not, at the time of the final determination of

the issued value by the Executive Board, significantly less than the share price of the shares of a similar nature and scope which are

already quoted on the stock markets, when judged in terms of the provisions of § 203 Paragraphs 1 and 2 and § 186 Paragraph 4 of

the German Stock Corporation Law (AktG) and the amount of the base capital attributable to the shares issued under exclusion of the sta-

tutory subscription rights does not exceed €433,794.00 and 10 percent of the recorded base capital at the time of the issue of the new

shares. Realization of stocks have to be charged against this 10 percent limitation of base capital if they come to effect due to authoriza -

- tion under shareholder exception from subscription according to § 71 Paragraph 1 Clause 8 (German Stock Corporation Law (AktG) in

connection with § 186 Paragraph 3 Clause 4 of the German Stock Corporation Law (AktG). In addition, stocks issued to service bonds

under option and/or conversion right shall be charged to the 10 percent limitation of base capital if the bonds were issued with the

exclusion of subscription rights due to an authorization applicable at the moment or an authorization acting on its behalf, as found in

§ 186 Paragraph 3 Clause 4 of the German Stock Corporation Law (AktG).

On the basis of a resolution passed by the General Meeting on March 28, 2006, ISRA VISION AG increased its capital by €250,000.00 by

issuing up to 250,000 no-par value bearer shares to implement an employee equity compensation plan (conditional capital).

On the basis of a resolution passed by the General Meeting on March 20, 2007, the base capital has been increased by up to €1,918,970.00

of no-par value bearer shares (conditional capital II). The conditional capital increase may only be carried out to the extent that the holder

of convertible or negotiable option bonds, issued on the basis of the authorization given to the Executive Board by the general meeting on

March 20, 2007, makes use of this conversion or option right, or to the extent that the holders obliged to make the conversion fulfill their

obligation to undertake the conversion.

Based on the decision of the General Meeting held on March 19, 2008, the Executive Board of ISRA VISION AG has been authorized to

acquire its own shares until September 18, 2009, complying with the principle of equal treatment (§ 53a of the German Stock Corporation

Law (AktG). They are authorized to acquire up to 433,794 shares of the company, corresponding to 10 percent of the current share capital,

under the provision that the shares which are purchased in accordance with this authorization, when added to the other shares in the com-

pany which the company has already purchased and still possesses, do not represent more than 10 percent of the base capital of the com-

pany. This authorization may be implemented in full or in parts. Purchases may be undertaken within the period covered by the authoriza-

tion up to the point where the maximum purchase volume has been reached by partial purchases on various purchasing dates. Purchases

may also be undertaken by subsidiary enterprises of the company in the context of § 17 of the German Stock Corporation Law (AktG) or

on its or their behalf by third parties.

Darmstadt, December 28, 2008

The Executive Board

Group Management Report

ISRA VISION Annual Report 2007/2008

24

As in previous years, the Supervisory Board exercised in the 2007/2008 fiscal year its legal and statutory responsibilities by monitoring the

management of the ISRA VISION group and by advising the Executive Board. The Supervisory Board was involved in a timely manner and

in depth in all decisions of fundamental or strategic importance. Following thorough consultation, the Supervisory Board cast its vote – when

necessary.

The Supervisory Board currently consists of Dr. Ing. h. c. Heribert J. Wiedenhues (Chairman), Dr. Wolfgang Witz (Deputy Chairman), Dr. Erich

W. Georg, Stefan Müller, Falko Schling and Prof. Dr. rer. nat. Dipl.-Ing. Hennig Tolle.

Dr. Dieter Willasch resigned from his position, effective as of the General Meeting on March 19, 2008. Mr. Falko Schling was appointed to

take his place on the supervisory board. Mr. Schling is the chief representative of Volkswagen AG and was previously the head of the group’s

quality assurance. He resides in Hofheim (Taunus). Mr. Schling is not a member of any other supervisory board as defined in § 125 Clause

3, second Sub-Clause of the German Stock Corporation law.

In October 2007, Dr. Erich W. Georg assumed the position of Dr. Folker Weißgerber, who had died unexpectedly on August 25, 2007.

Dr. Georg is managing partner of the MCIC GmbH (Management Consulting International Cooperation GmbH). He was furthermore

employed at Siemens AG as president and CEO of Instrumentation & Control, Power Generation. Dr. Erich W. Georg was similarly appoint-

ed to take his place in the supervisory board by the general meeting.

The Executive Board regularly and comprehensively informed the Supervisory Board about business activities, corporate planning and

events of great importance, both verbally and in writing. They provided thorough explanations when the business results deviated from plan-

ning. In addition to this, the Chairman of the Supervisory Board remained in regular contact with the Chairman of the Executive Board.

Together they thoroughly discussed current business developments.

The Supervisory Board convened four meetings by personal attendance in the 2007/2008 fiscal year. They provided in depth advice and

made decisions on the following topics:

Meeting on November 26, 2007

The Supervisory Board authorized the agenda for the General Meeting on March 19, 2008 and decided according to the June 14, 2007

version of the Declaration of Compliance of the Corporate Governance Codex.

Meeting on January 23, 2008

The Supervisory Board approved without objection the annual financial statement for ISRA VISION AG, the corporate accounts and the

report on the corporate position, thus confirming the annual statement of accounts. The Supervisory Board decided on a dividend payout

of 15 cents.

Meeting on May 27, 2008

The Executive Board has given the Supervisory Board an overview of the 3rd quarter of the 2007/2008 fiscal year along with a forecast for

the entire fiscal year; the Supervisory Board approved the forecast.

Meeting on September 11, 2008

The Supervisory Board discussed in depth the budget for the 2008/2009 fiscal year and approved it. The Supervisory Board was provided

an overview of the status of the acquisition projects and was brought up to speed on ISRA’s current organizational and corporate structure.

Furthermore, the corporate planning for the 2008/2009 fiscal year was presented and approved.

The date for the General Meeting was set for March 24, 2009.

The Supervisory Board concentrated its advice on matters concerning: The financial, sales and profit situation; investments; the risk

management system; the international growth of the markets for industrial image processing, especially an analysis of the drop in orders in

the second half of the year; expansion opportunities and risks for ISRA in Asia, Eastern Europe and South America. The various acquisition

targets were analyzed in depth and the proceedings were very carefully tracked during the integration of Parsytec. The Supervisory Board

furthermore concerned itself with the impact of new legal developments, in particular with the increased disclosure requirements of the IFRS