Page 1

AAPPCCAA

Maize and Ethanol: Maize and Ethanol: Are Are the Current High Prices the Current High Prices

Sustainable?Sustainable?

Harwood D. SchafferUniversity of Tennessee

Agricultural Policy Analysis Center

FENALCEBogotá, Colombia

June 21, 2007

Page 2

AAPPCCAA

Recent Corn PricesRecent Corn Prices

Page 3

AAPPCCAA

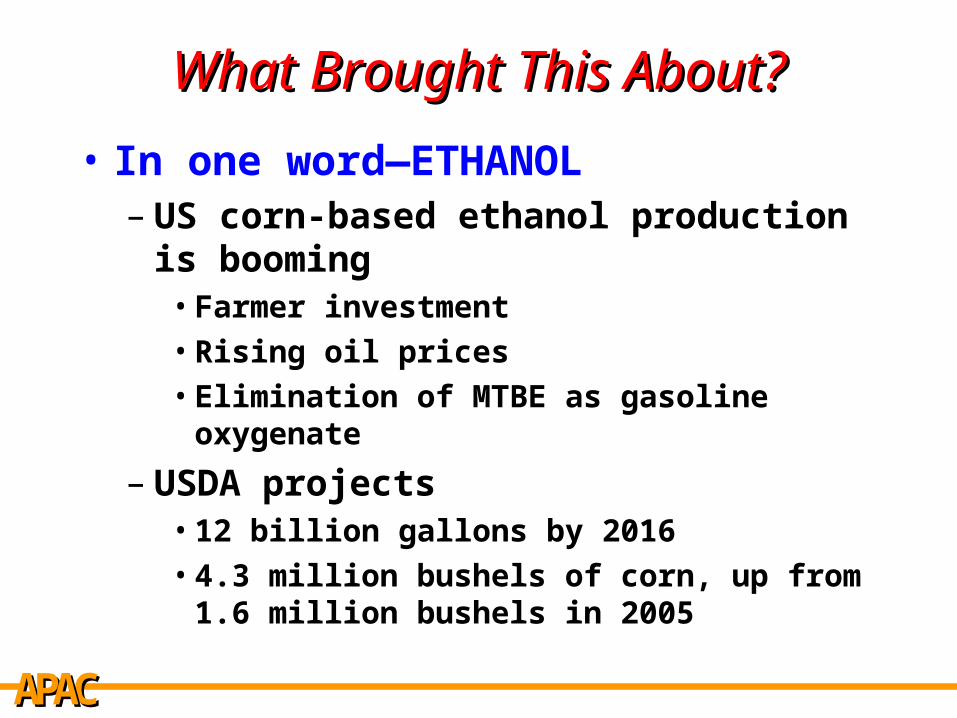

What Brought This About?What Brought This About?

• In one word—ETHANOL– US corn-based ethanol production is

booming• Farmer investment• Rising oil prices• Elimination of MTBE as gasoline oxygenate

– USDA projects• 12 billion gallons by 2016• 4.3 million bushels of corn, up from 1.6

million bushels in 2005

Page 4

AAPPCCAA

Projected Ethanol DemandProjected Ethanol Demand

Source: UDSA 2007-2016 Projections

Page 5

AAPPCCAA

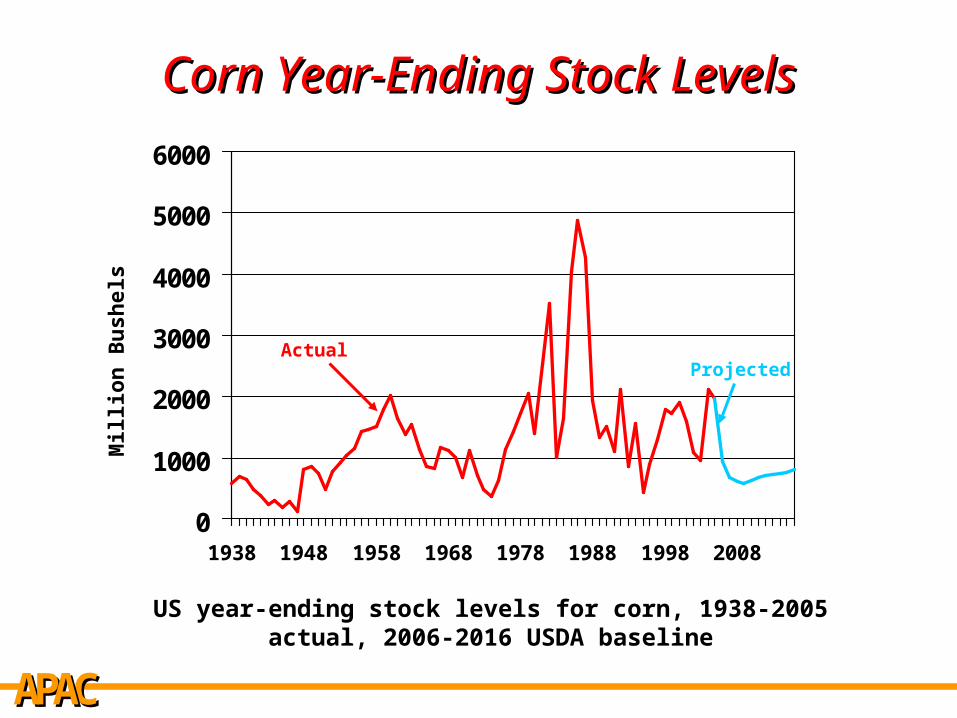

Corn Year-Ending Stock LevelsCorn Year-Ending Stock Levels

0

1000

2000

3000

4000

5000

6000

1938 1948 1958 1968 1978 1988 1998 2008

Mill

ion

Bu

shel

s

US year-ending stock levels for corn, 1938-2005 actual, 2006-2016 USDA baseline

ActualProjected

Page 6

AAPPCCAA

1995 (4.6%)

Uncharted TerritoryUncharted Territory

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1938 1947 1958 1968 1978 1988 1998 2008

Year ending commercial stocks-to-use ratio for US corn1938-2005 (actual), 2006-2016 (2007 USDA Baseline)

1947 (4.9%) 1983 (5.4%) 2009 (4.5%)

Page 7

AAPPCCAA

Projected Corn PriceProjected Corn Price

Source: UDSA 2007-2016 Projections

Page 8

AAPPCCAA

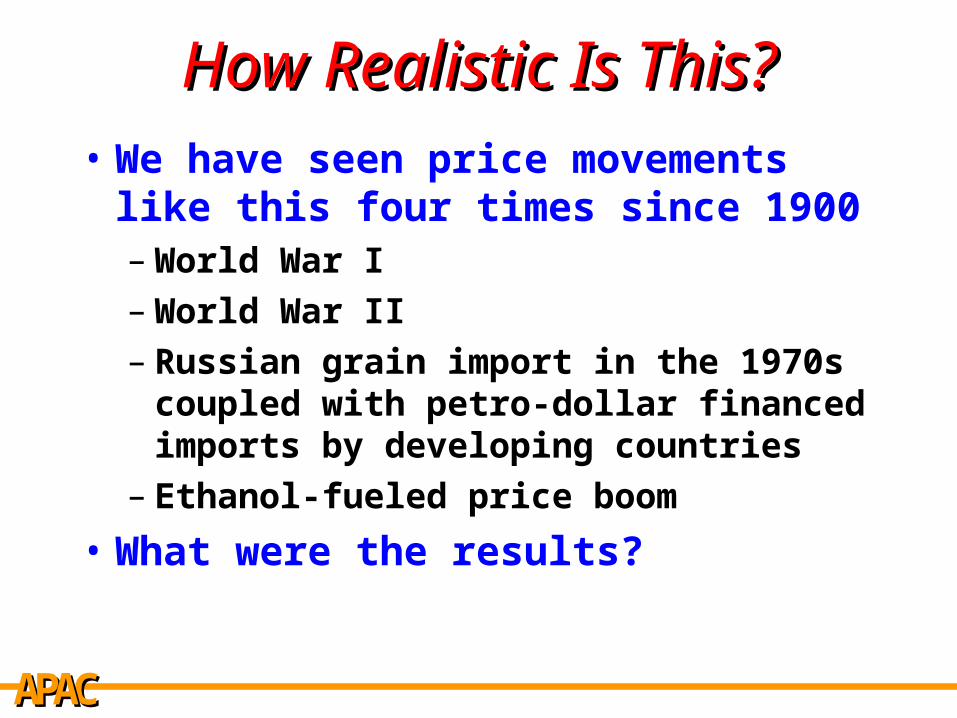

How Realistic Is This?How Realistic Is This?• We have seen price movements like

this four times since 1900– World War I– World War II– Russian grain import in the 1970s

coupled with petro-dollar financed imports by developing countries

– Ethanol-fueled price boom

• What were the results?

Page 9

AAPPCCAA

Characteristics of Ag SectorCharacteristics of Ag Sector

• Agriculture is different from other

economic sectors.

On the demand side:

– With low food prices—

• People don’t eat more meals a day

• They may change mix of foods

• Aggregate intake remains relatively stable

Page 10

AAPPCCAA

Characteristics of Ag SectorCharacteristics of Ag Sector

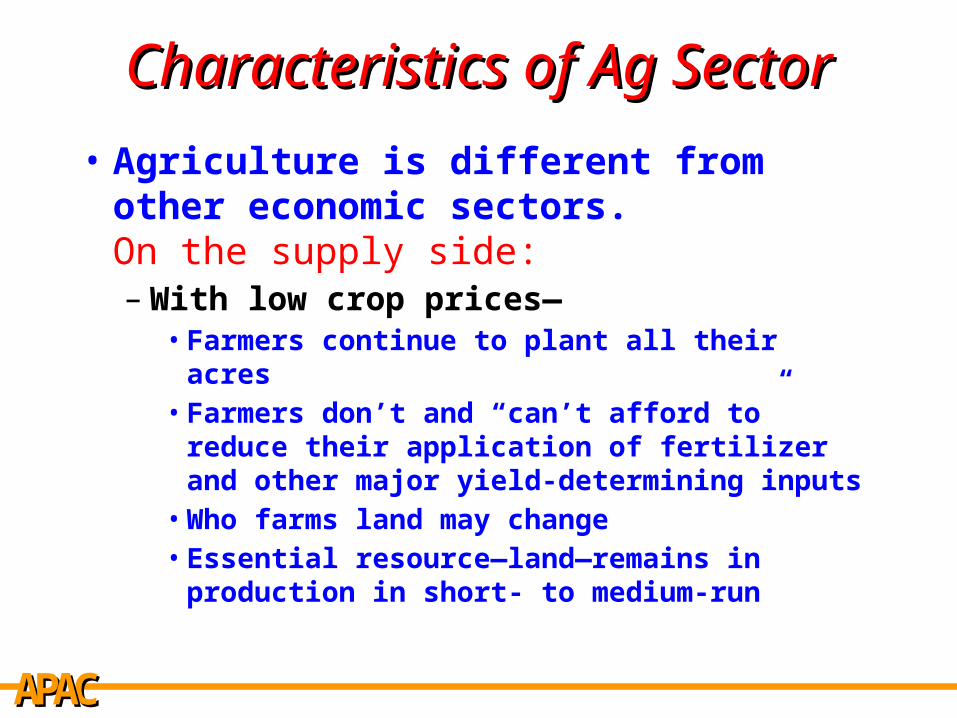

• Agriculture is different from other economic sectors.On the supply side:– With low crop prices—

• Farmers continue to plant all their acres• Farmers don’t and “can’t afford to” reduce

their application of fertilizer and other major yield-determining inputs

• Who farms land may change• Essential resource—land—remains in

production in short- to medium-run

Page 11

AAPPCCAA

Why Chronic Problems In Ag? Why Chronic Problems In Ag?

• Technology typically expands output faster than population and exports expand demand– Historically, much of this technology

has been paid for by US taxpayers

• The growth in supply now is being additionally fueled by– increased acreages in Brazil, etc.– technological advance worldwide

Page 12

AAPPCCAA

Change in Non-US Crop AcreageChange in Non-US Crop Acreage

-60

-40

-20

0

20

40

60

1995 1996 1997 1998 1999 2000

Page 13

AAPPCCAA

Why Chronic Problems In Ag?Why Chronic Problems In Ag?

• Lower prices should automatically correct itself—Econ 101 says so– Consumers buy more– Producers produce less– Prices recover—problem solved!

• But in agriculture lower prices do not solve the problem– Little self-correction on the demand side

• People do consume significantly more food

– Little self-correction on the supply side• Farmers do not produce significantly less output

Page 14

AAPPCCAA

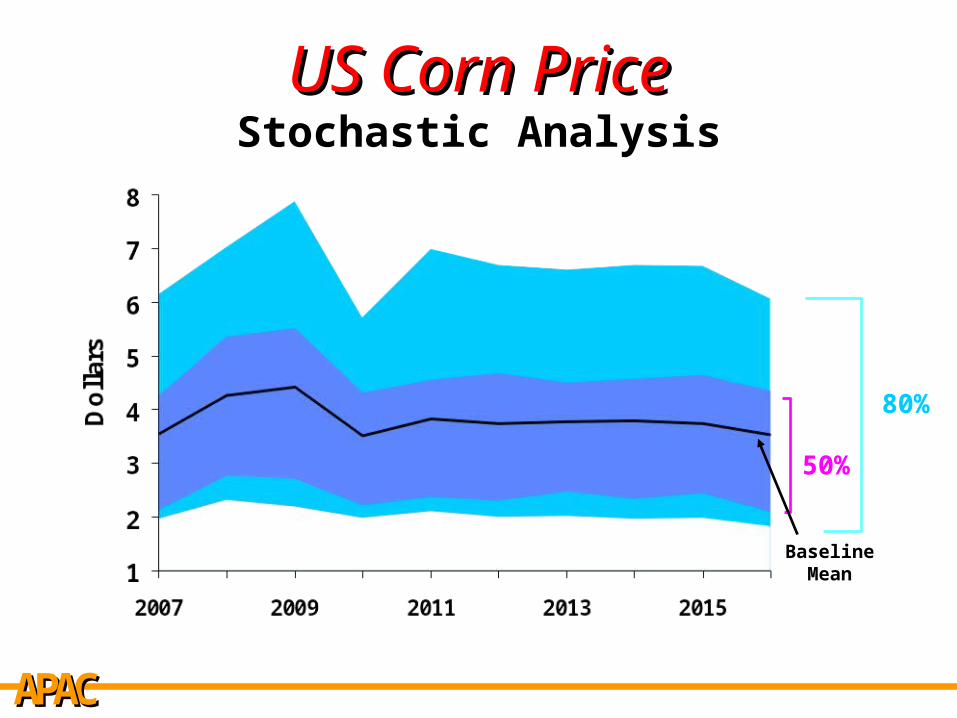

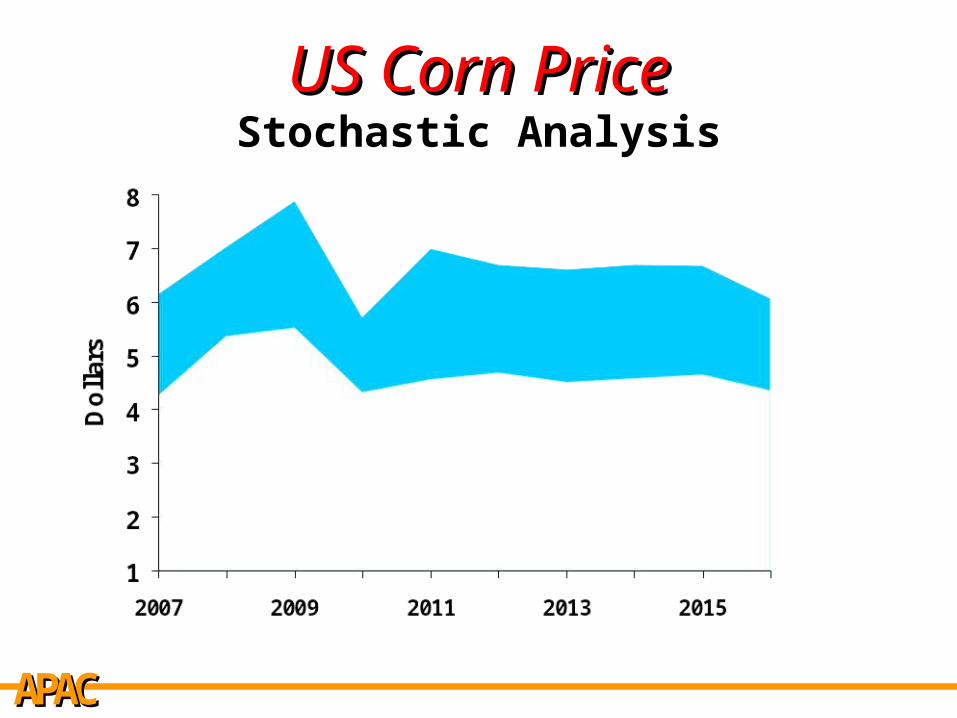

US Corn PriceUS Corn PriceStochastic Analysis

Baseline MeanUSDA Deterministic Baseline

Page 15

AAPPCCAA

US Corn PriceUS Corn PriceStochastic Analysis

Baseline Mean

50%

Page 16

AAPPCCAA

US Corn PriceUS Corn PriceStochastic Analysis

Baseline Mean

50%

80%

Page 17

AAPPCCAA

US Ethanol Corn DemandUS Ethanol Corn Demand Stochastic Analysis

50%80%

Baseline Mean

USDA Deterministic Baseline

Page 18

AAPPCCAA

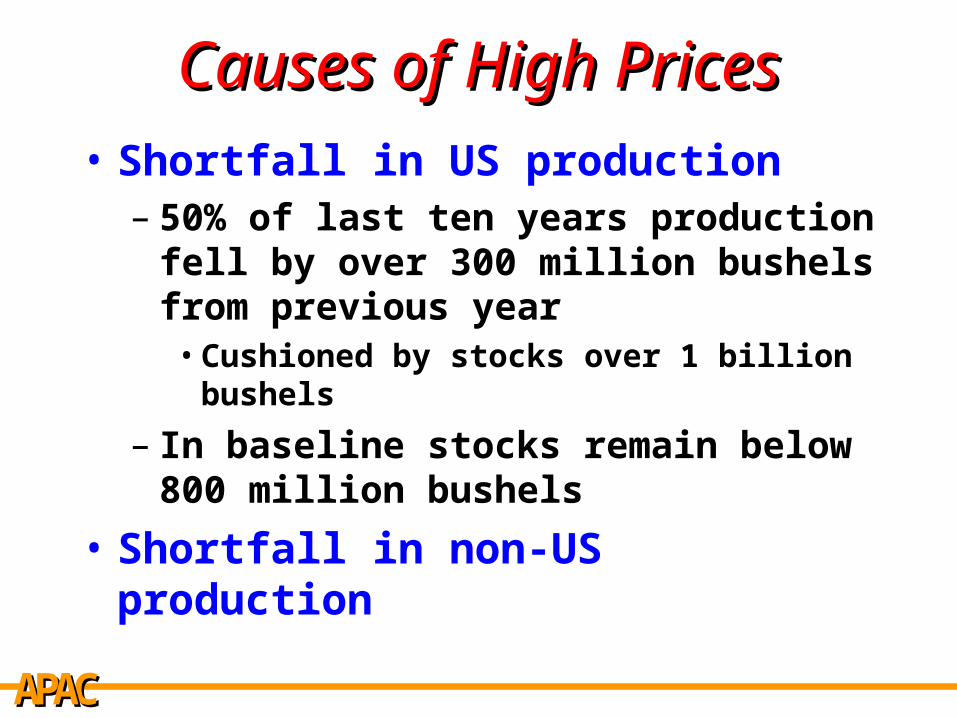

Causes of High PricesCauses of High Prices• Shortfall in US production

– 50% of last ten years production fell by over 300 million bushels from previous year

• Cushioned by stocks over 1 billion bushels

– In baseline stocks remain below 800 million bushels

• Shortfall in non-US production

Page 19

AAPPCCAA

Exports, Exports, ExportsExports, Exports, Exports• For the last quarter century, exports

have been heralded—and continue to be by some—as crop agriculture’s salvation– Exports is the production safety valve that

can rebalance agricultural markets– Exports will grow at accelerating rates

• US policymakers have misunderstood role of US in bulk agricultural export markets

Page 20

AAPPCCAA

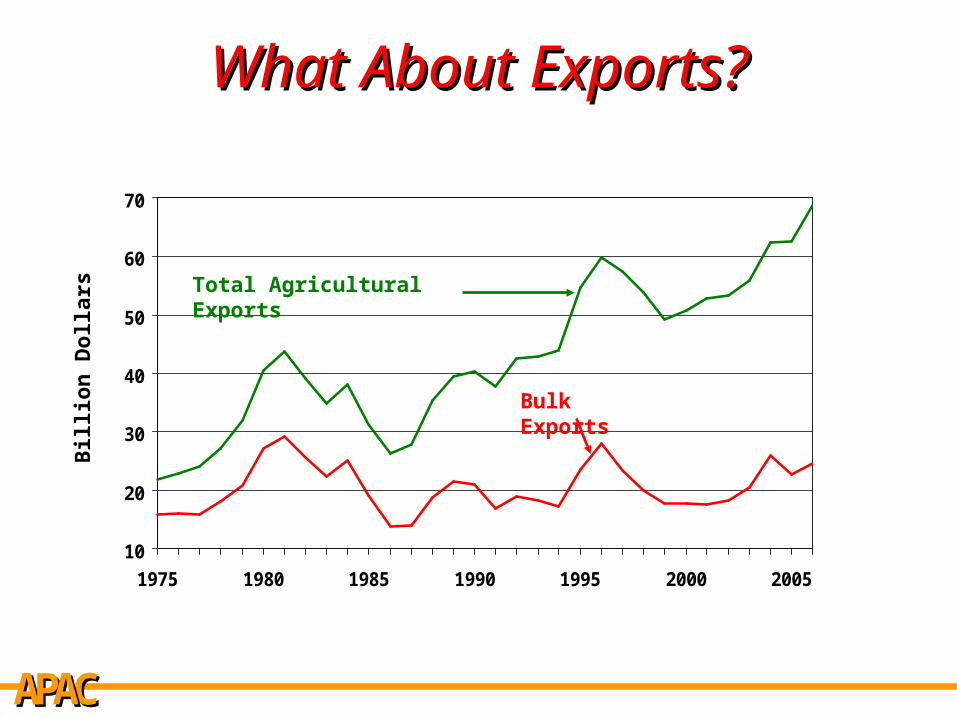

What About Exports?What About Exports?

10

20

30

40

50

60

70

1975 1980 1985 1990 1995 2000 2005

Bill

ion

Do

llars

Bulk Exports

Total Agricultural Exports

Page 21

AAPPCCAA

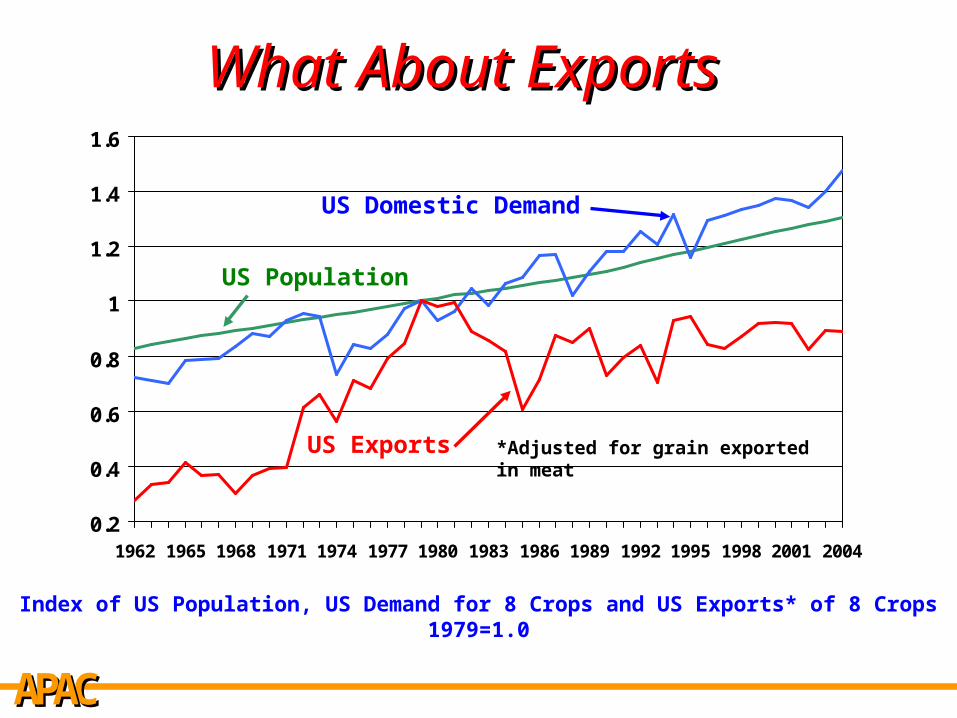

What About ExportsWhat About Exports

Index of US Population, US Demand for 8 Crops and US Exports* of 8 Crops1979=1.0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

US Population

US Exports

US Domestic Demand

*Adjusted for grain exported in meat

Page 22

AAPPCCAA

US Exported AcresUS Exported Acres

Percentage of US acres used to produce crops for export have declined from a high of 43 percent in 1980 and 1980 to 33 percent for 2006

0%

10%

20%

30%

40%

50%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

% of US Acres Producing Crops for Export

Page 23

AAPPCCAA

Net Export AcreageNet Export Acreage for 8 Major Crops for 8 Major Crops

0

20

40

60

80

100

120

140

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

Million

Acres

103.6

76-85 Average86.8

86-95 Average77.0

96-02 Average

Page 24

AAPPCCAA

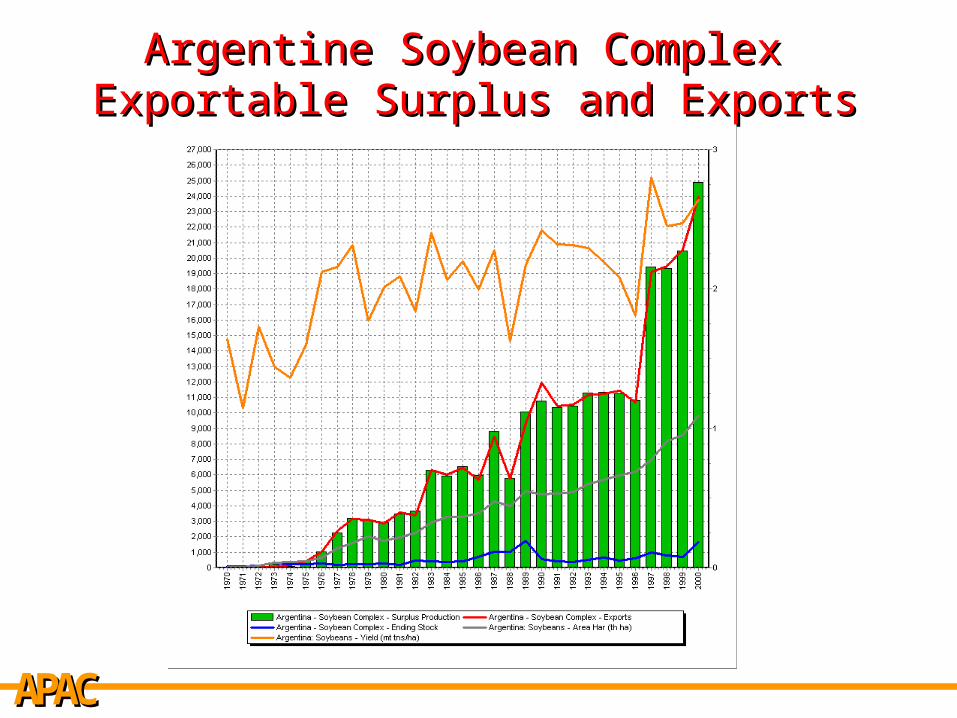

Argentine Soybean Complex Argentine Soybean Complex Exportable Surplus and ExportsExportable Surplus and Exports

Page 25

AAPPCCAA

Brazilian Soybean Complex Brazilian Soybean Complex Exportable Surplus and Exports Exportable Surplus and Exports

Page 26

AAPPCCAA

What About Exports?What About Exports?

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Developing competitors: Argentina, Brazil, China, India, Pakistan, Thailand, Vietnam15 Crops: Wheat, Corn, Rice, Sorghum, Oats, Rye, Barley, Millet, Soybeans, Peanuts, Cottonseed, Rapeseed, Sunflower, Copra, and Palm Kernel

Th

ou

san

d M

etri

c T

on

s

US Exports

Developing Competitors’ Exports

Page 27

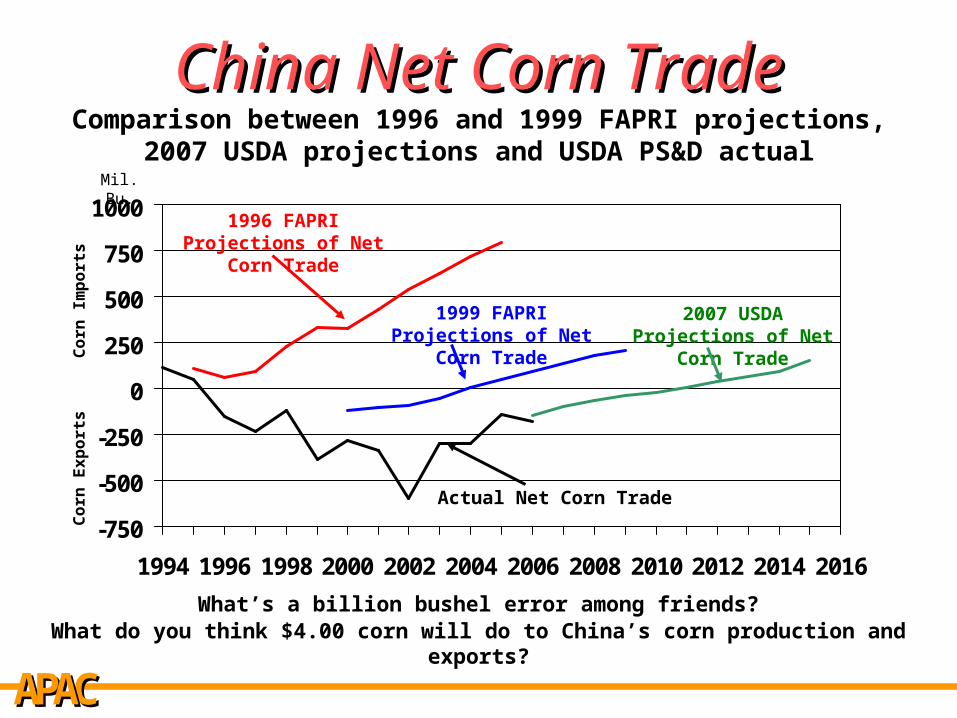

AAPPCCAA

China Net Corn TradeChina Net Corn TradeComparison between 1996 and 1999 FAPRI projections, 2007

USDA projections and USDA PS&D actual

-750

-500

-250

0

250

500

750

1000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

1996 FAPRI Projections of Net Corn Trade

Actual Net Corn Trade

1999 FAPRI Projections of Net Corn Trade

Co

rn E

xp

ort

sC

orn

Im

po

rts

Mil. Bu.

What’s a billion bushel error among friends?What do you think $4.00 corn will do to China’s corn production and exports?

2007 USDA Projections of Net Corn Trade

Page 28

AAPPCCAA

What About Exports?What About Exports?

• Why have exports not fulfilled US hopes?– Export demand is braked by issues of food

security/food sovereignty– International crop production is impacted by:

• Increased acreage: Stage of development• Yield advances: World-wide distribution of

technology• US role as the leading nation in the world

– Politically, economically, technologically, and militarily– And in prices too: Others price off US prices

Page 29

AAPPCCAA

US Role in ExportsUS Role in Exports

• US is the oligopoly price leader– 20+ years of US policies to reduce US

prices to “World Price” are futile– US price is the “World Price”– US has been playing limbo with itself

• US is the residual supplier

• US is the world’s “Ever-Normal Granary”

Page 30

AAPPCCAA

Causes of Low PricesCauses of Low Prices• Random high US production

– Prices are very sensitive– Any increase in year-ending stocks

could send prices plummeting

• Predictable increases in non-US production– Acreage in Brazil, India, Colombia– Increases in yields due to technology

adoption

Page 31

AAPPCCAA

Causes of Low PricesCauses of Low Prices• Low crude oil prices

– Puts pressure on ethanol prices– Reduce incentives to bring on new

plants– Existing plants may reduce production

or go off-line for periods of time

Page 32

AAPPCCAA

US Corn PriceUS Corn PriceStochastic Analysis

Page 33

AAPPCCAA

Causes of Low PricesCauses of Low Prices• Extremely high prices

– Increase the rate at which resources flow into corn production

• Additional savannah land• Return to production of land in some states

of Former Soviet Union• Yield enhancing technologies

– 15 to 18 tonnes/per hectare corn yields

Page 34

AAPPCCAA

Causes of Low PricesCauses of Low Prices• Cellulosic ethanol production

– More cost efficient than corn-to-ethanol production

– Conversion of front end of current corn-to-ethanol plants

• Sources of cellulose– Forest waste products– Corn stover– Switchgrass, hybrid poplars and willows – Urban waste

Page 35

AAPPCCAA

Feedstock for EnergyFeedstock for Energy**

0

200

400

600

800

2006 2011 2016

Mil

lio

n T

on

s

Corn Grain Corn Stover Wheat Straw Energy Crop Wood Residue Soybeans

* Does not include forest harvest

Page 36

AAPPCCAA

Worldwide Excess Capacity Will Again Be a Worldwide Excess Capacity Will Again Be a Long-run Problem (Despite Ethanol)Long-run Problem (Despite Ethanol)

• Dramatic yield increases in other countries (and in this country)– Cargill, Monsanto, John Deere, etc., etc., etc.

• Acreage once in production will be brought back in– Russia, Ukraine and others

• New Acreage– Brazil– China

Page 37

AAPPCCAA

What Do You Think?What Do You Think?• Given the history:

– World War I– World War II– Russian grain import in the 1970s

coupled with petro-dollar financed imports by developing countries

• Given the analysis I have presented

• Will the ethanol-fueled price boom be different?

Page 38

AAPPCCAA

Policy for All SeasonsPolicy for All Seasons• Realistic about the way aggregate

agricultural markets work

• Takes into account consumer behavior

• Takes into account producer behavior

• Recognizes limited ability of exports to rebalance aggregate agricultural markets

• Recognizes demand growth seldom outstrips supply growth for long

Page 39

AAPPCCAA

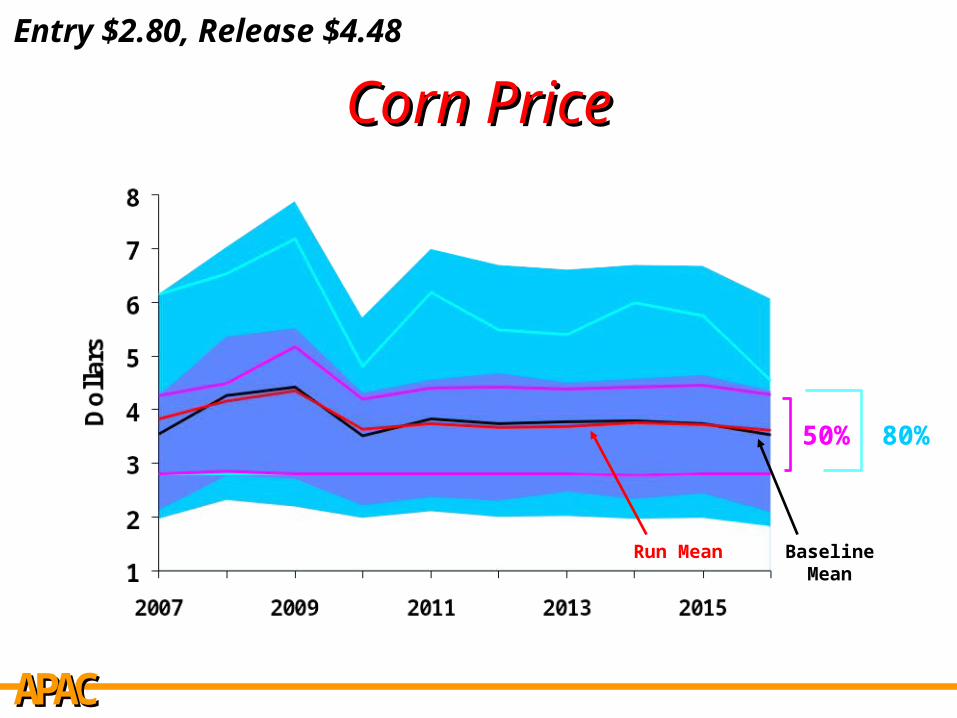

Corn PriceCorn PriceEntry $2.80, Release $4.48

Baseline Mean

50% 80%

Run Mean

Page 40

AAPPCCAA

Agricultural Policy Analysis Center The University of Tennessee 310 Morgan Hall 2621 Morgan Circle Knoxville, TN 37996-4519

www.agpolicy.org

Thank YouThank You

Page 41

AAPPCCAA

To receive an electronic version of our weekly ag policy column send an email to: [email protected] to be added to APAC’s Policy Pennings listserv

Weekly Policy ColumnWeekly Policy Column

Page 42

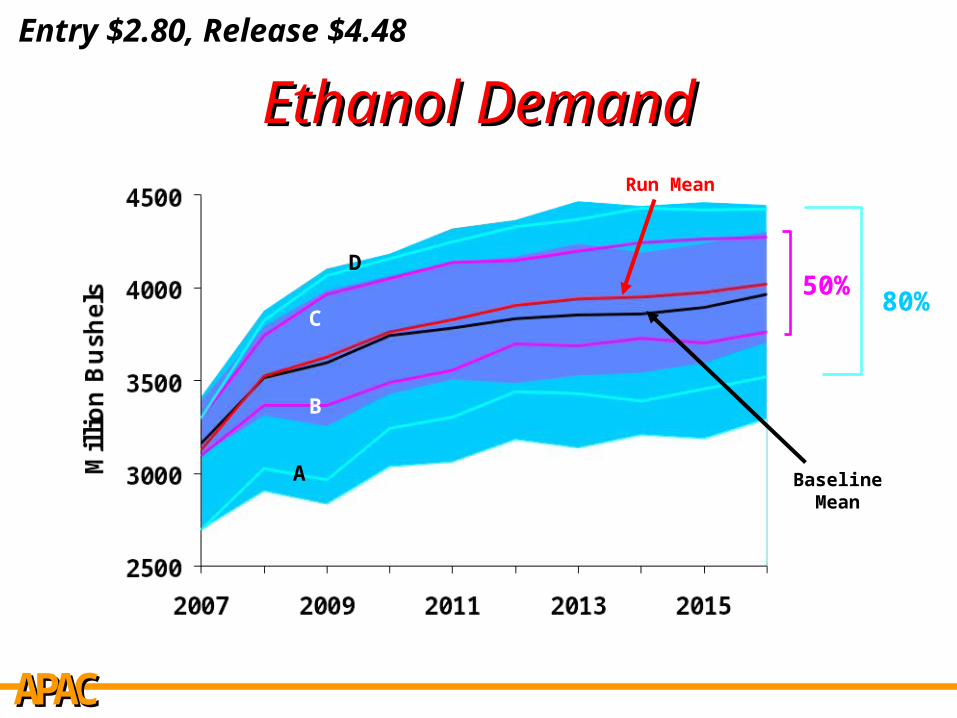

AAPPCCAA

Ethanol DemandEthanol DemandEntry $2.80, Release $4.48

50%80%

Baseline MeanA

B

C

D

Run Mean

Page 43

AAPPCCAA

Uncharted TerritoryUncharted Territory

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Year ending commercial stocks-to-use ratio for US corn1960-2005 (actual), 2006-2016 (2007 USDA Baseline)

1974 (7.4%) 1983 (5.4%) 1995 (4.6%) 2009 (4.5%)