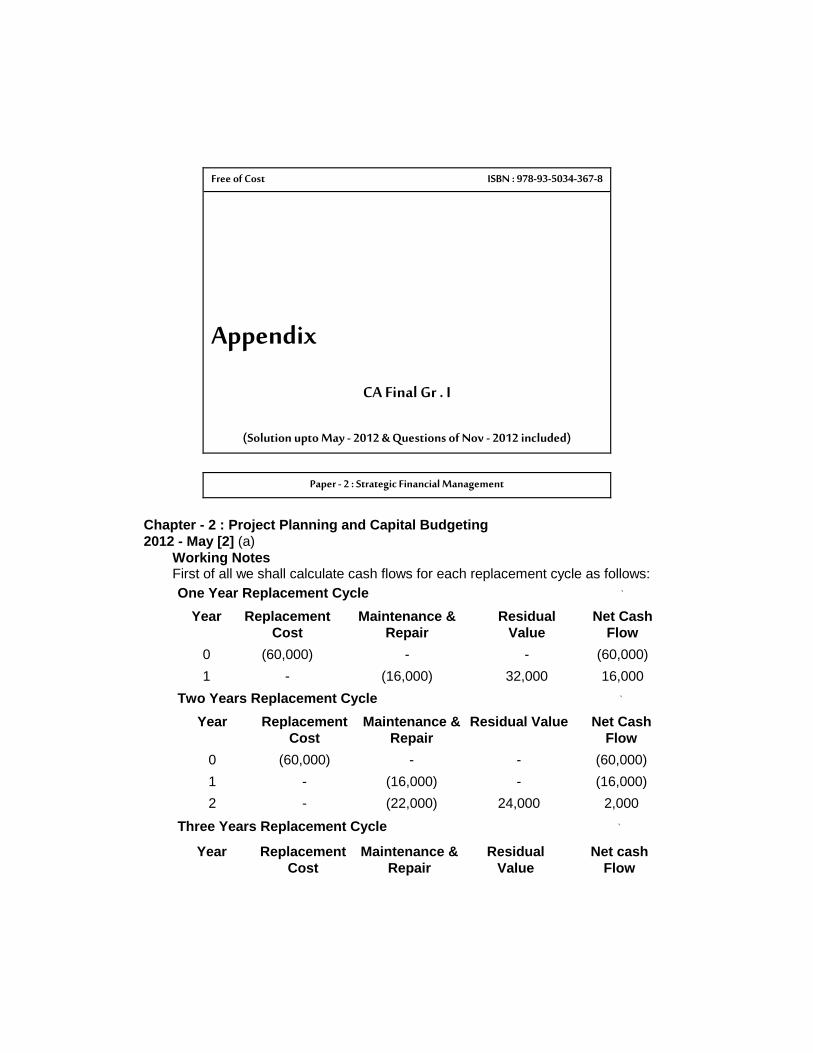

Free of Cost ISBN : 978-93-5034-367-8 Appendix CA Final Gr . I (Solution upto May - 2012 & Questions of Nov - 2012 included) Paper - 2 : Strategic Financial Management Chapter - 2 : Project Planning and Capital Budgeting 2012 - May [2] (a) Working Notes First of all we shall calculate cash flows for each replacement cycle as follows: One Year Replacement Cycle ` Year Replacement Cost Maintenance & Repair Residual Value Net Cash Flow 0 (60,000) - - (60,000) 1 - (16,000) 32,000 16,000 Two Years Replacement Cycle ` Year Replacement Cost Maintenance & Repair Residual Value Net Cash Flow 0 (60,000) - - (60,000) 1 - (16,000) - (16,000) 2 - (22,000) 24,000 2,000 Three Years Replacement Cycle ` Year Replacement Cost Maintenance & Repair Residual Value Net cash Flow

Transcript

Free of Cost ISBN : 978-93-5034-367-8

Appendix

CA Final Gr . I

(Solution upto May - 2012 & Questions of Nov - 2012 included)

Paper - 2 : Strategic Financial Management

Chapter - 2 : Project Planning and Capital Budgeting

2012 - May [2] (a)

Working Notes First of all we shall calculate cash flows for each replacement cycle as follows: One Year Replacement Cycle

`

Year

Replacement

Cost

Maintenance &

Repair

Residual

Value

Net Cash

Flow

0

(60,000)

-

-

(60,000)

1

-

(16,000)

32,000

16,000 Two Years Replacement Cycle

`

Year

Replacement

Cost

Maintenance &

Repair

Residual Value

Net Cash

Flow

0

(60,000)

-

-

(60,000)

1

-

(16,000)

-

(16,000)

2

-

(22,000)

24,000

2,000 Three Years Replacement Cycle

`

Year

Replacement

Cost

Maintenance &

Repair

Residual

Value

Net cash

Flow

0 (60,000) - - (60,000)

1

-

(16,000)

-

(16,000)

2

-

(22,000)

-

(22,000)

3

-

(28,000)

16,000

(12,000)

Four Years Replacement Cycle

`

Year

Replacement

Cost

Maintenance &

Repair

Residual

Value

Net Cash

Flow

0

(60,000)

-

-

(60,000)

1

-

(16,000)

-

(16,000)

2

-

(22,000)

-

(22,000)

3

-

(28,000)

-

(28,000)

4

-

(36,000)

8,000

(28,000)

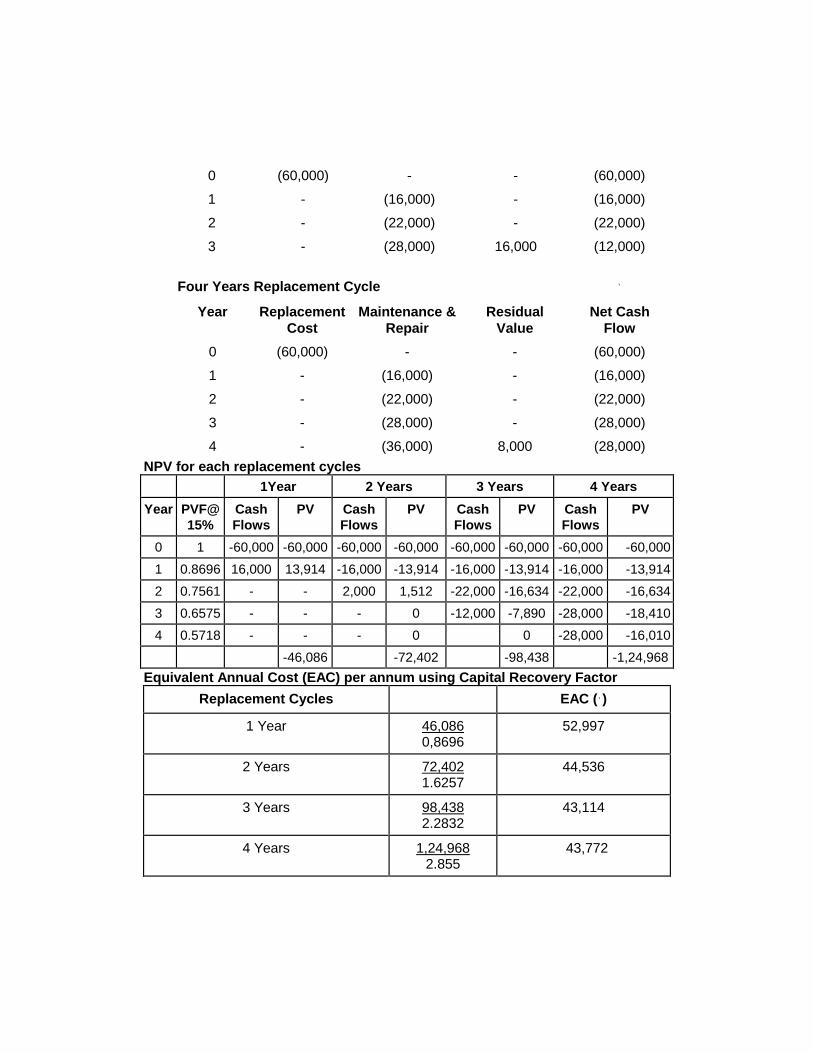

NPV for each replacement cycles

1Year

2 Years

3 Years

4 Years

Year

PVF@

15%

Cash

Flows

PV

Cash

Flows

PV

Cash

Flows

PV

Cash

Flows

PV

0

1

-60,000

-60,000

-60,000

-60,000

-60,000

-60,000

-60,000

-60,000

1

0.8696

16,000

13,914

-16,000

-13,914

-16,000

-13,914

-16,000

-13,914

2

0.7561

-

-

2,000

1,512

-22,000

-16,634

-22,000

-16,634

3

0.6575

-

-

-

0

-12,000

-7,890

-28,000

-18,410

4

0.5718

-

-

-

0

0

-28,000

-16,010

-46,086

-72,402

-98,438

-1,24,968

Equivalent Annual Cost (EAC) per annum using Capital Recovery Factor

Replacement Cycles

EAC (`)

1 Year

46,086 0,8696

52,997

2 Years

72,402 1.6257

44,536

3 Years

98,438 2.2832

43,114

4 Years

1,24,968

2.855

43,772

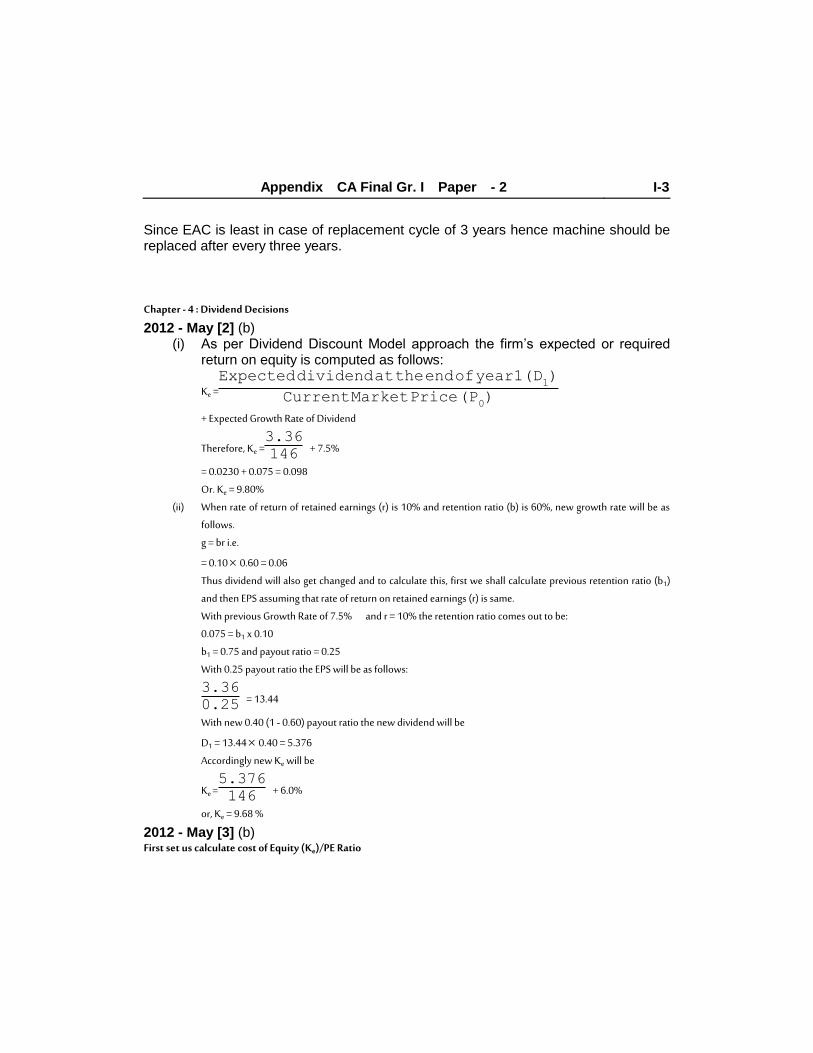

Appendix CA Final Gr. I Paper - 2 I-3

Since EAC is least in case of replacement cycle of 3 years hence machine should be replaced after every three years. Chapter - 4 : Dividend Decisions

2012 - May [2] (b) (i) As per Dividend Discount Model approach the firm’s expected or required

return on equity is computed as follows:

Ke =Expecteddividendattheendofyear1(D

1)

CurrentMarketPrice(P0)

+ Expected Growth Rate of Dividend

Therefore, Ke =3.36

146 + 7.5%

= 0.0230 + 0.075 = 0.098

Or. Ke = 9.80%

(ii) When rate of return of retained earnings (r) is 10% and retention ratio (b) is 60%, new growth rate will be as

follows.

g = br i.e.

= 0.10 0.60 = 0.06

Thus dividend will also get changed and to calculate this, first we shall calculate previous retention ratio (b1)

and then EPS assuming that rate of return on retained earnings (r) is same.

With previous Growth Rate of 7.5% and r = 10% the retention ratio comes out to be:

0.075 = b1 x 0.10

b1 = 0.75 and payout ratio = 0.25

With 0.25 payout ratio the EPS will be as follows:

3.36

0.25 = 13.44

With new 0.40 (1 - 0.60) payout ratio the new dividend will be

D1 = 13.44 0.40 = 5.376

Accordingly new Ke will be

Ke =5.376

146 + 6.0%

or, Ke = 9.68 %

2012 - May [3] (b) First set us calculate cost of Equity (Ke)/PE Ratio

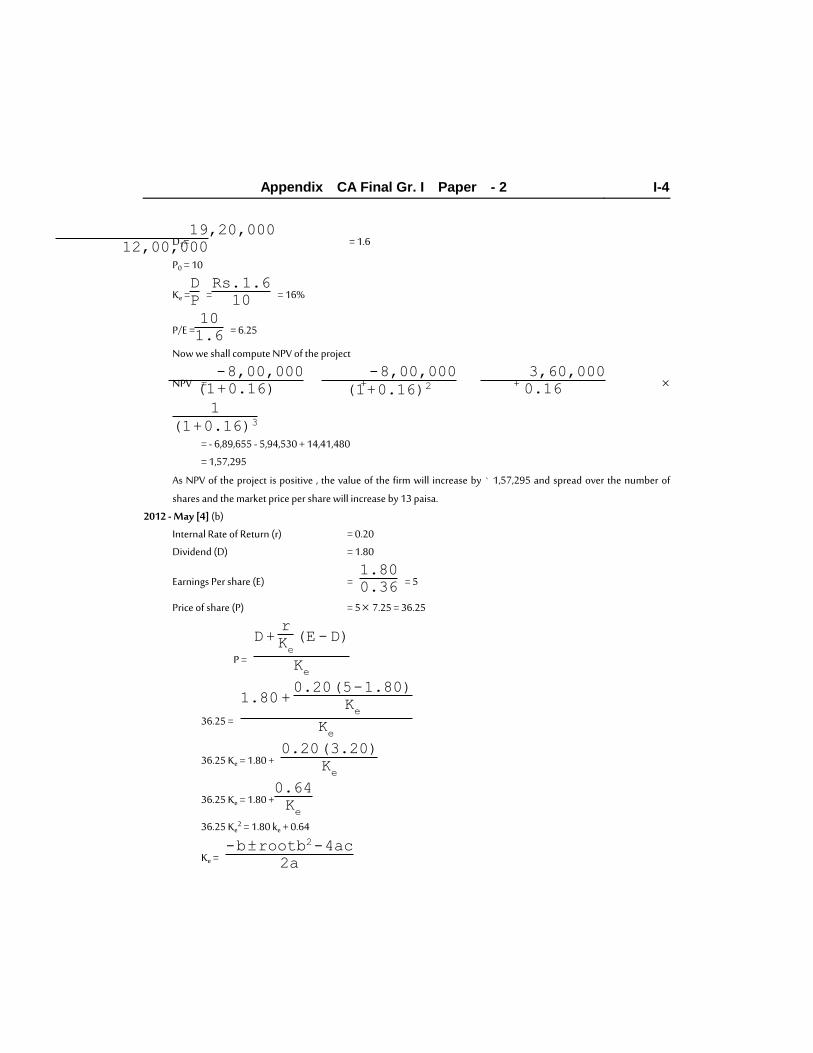

Appendix CA Final Gr. I Paper - 2 I-4

D1=19,20,000

12,00,000 = 1.6

P0 = 10

Ke =D

P =Rs.1.6

10 = 16%

P/E =10

1.6 = 6.25

Now we shall compute NPV of the project

NPV = -8,00,000

(1+0.16) +-8,00,000

(1+0.16)2 +

3,60,000

0.16

1

(1+0.16)3

= - 6,89,655 - 5,94,530 + 14,41,480

= 1,57,295

As NPV of the project is positive , the value of the firm will increase by ` 1,57,295 and spread over the number of

shares and the market price per share will increase by 13 paisa.

2012 - May [4] (b)

Internal Rate of Return (r) = 0.20

Dividend (D) = 1.80

Earnings Per share (E) = 1.80

0.36 = 5

Price of share (P) = 5 7.25 = 36.25

P =

D+r

Ke

(E-D)

Ke

36.25 =

1.80+0.20(5-1.80)

Ke

Ke

36.25 Ke = 1.80 + 0.20(3.20)

Ke

36.25 Ke = 1.80 +0.64

Ke

36.25 Ke2 = 1.80 ke + 0.64

Ke = -b±rootb2-4ac

2a

Appendix CA Final Gr. I Paper - 2 I-5

= -1.80±root(1.80)2-4´(-36.25)´0.64

2´(-36.25)

= -1.80±root3.24+92.80

-72.50

Ke = 16%

Since the firm is a growing firm, then 100% payout ratio will give limiting value of share

P =

1.80+0.20(5-5)

0.16

0.16

= 1.80

1.16

= `11.25

Thus limiting value is `11.25

Chapter - 5 : Indian Capital Market and Security Analysis

2012 - May [1] {C} (b), (d)

(b) The duration of future contract is 4 months. The average yield during this period will be:

3%+3%+4%+3%

4 = 3.25%

As per Cost to Carry model the future price will be

F = Se(rf-D)t

Where S = Spot Price

rf = Risk Free interest

D = Dividend Yield

t = Time Period

Accordingly, future price will be

= ` 2,200 e(0.08-0.0325) 4/12

= ` 2,200 e0.01583

= ` 2,200 1.01593.

= ` 2235.05

(d) The optional hedge ratio to minimize the variance of Hedger’s position is given by:

H = pσS

σF

Where

σS = Standard deviation of S

σF = Standard deviation of F

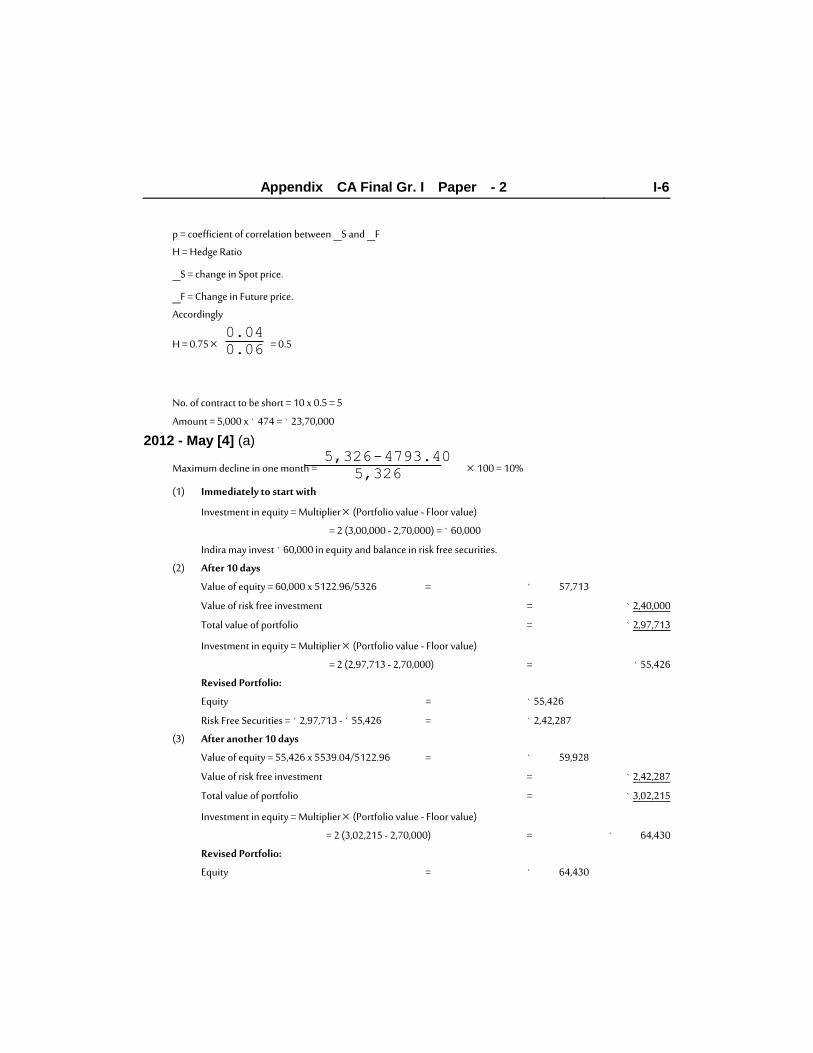

Appendix CA Final Gr. I Paper - 2 I-6

p = coefficient of correlation between S and F

H = Hedge Ratio

S = change in Spot price.

F = Change in Future price.

Accordingly

H = 0.75 0.04

0.06 = 0.5

No. of contract to be short = 10 x 0.5 = 5

Amount = 5,000 x ` 474 = ` 23,70,000

2012 - May [4] (a)

Maximum decline in one month = 5,326-4793.40

5,326 100 = 10%

(1) Immediately to start with

Investment in equity = Multiplier (Portfolio value - Floor value)

= 2 (3,00,000 - 2,70,000) = ` 60,000

Indira may invest ` 60,000 in equity and balance in risk free securities.

(2) After 10 days

Value of equity = 60,000 x 5122.96/5326 = ` 57,713

Value of risk free investment = ` 2,40,000

Total value of portfolio = ` 2,97,713

Investment in equity = Multiplier (Portfolio value - Floor value)

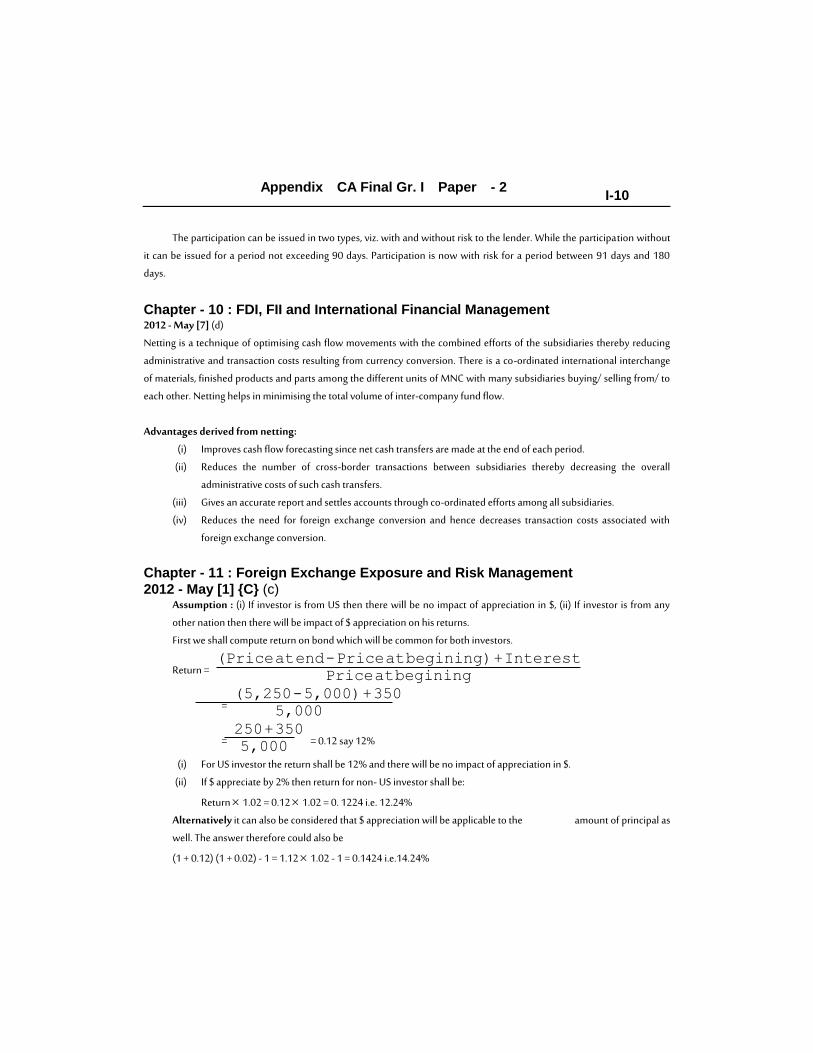

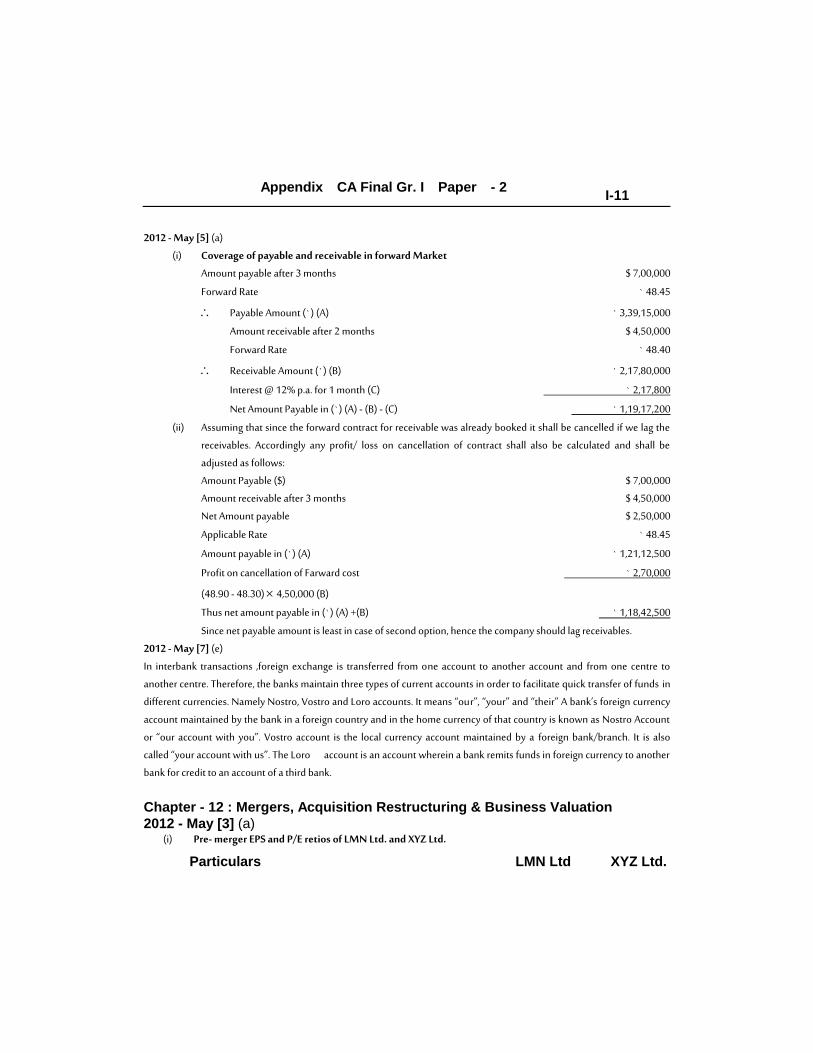

(i) Coverage of payable and receivable in forward Market

Amount payable after 3 months $ 7,00,000

Forward Rate ` 48.45

Payable Amount (`) (A) ` 3,39,15,000

Amount receivable after 2 months $ 4,50,000

Forward Rate ` 48.40

Receivable Amount (`) (B) ` 2,17,80,000

Interest @ 12% p.a. for 1 month (C) ` 2,17,800

Net Amount Payable in (`) (A) - (B) - (C) ` 1,19,17,200

(ii) Assuming that since the forward contract for receivable was already booked it shall be cancelled if we lag the

receivables. Accordingly any profit/ loss on cancellation of contract shall also be calculated and shall be

adjusted as follows:

Amount Payable ($) $ 7,00,000

Amount receivable after 3 months $ 4,50,000

Net Amount payable $ 2,50,000

Applicable Rate ` 48.45

Amount payable in (`) (A) ` 1,21,12,500

Profit on cancellation of Farward cost ` 2,70,000

(48.90 - 48.30) 4,50,000 (B)

Thus net amount payable in (`) (A) +(B) ` 1,18,42,500

Since net payable amount is least in case of second option, hence the company should lag receivables.

2012 - May [7] (e)

In interbank transactions ,foreign exchange is transferred from one account to another account and from one centre to

another centre. Therefore, the banks maintain three types of current accounts in order to facilitate quick transfer of funds in

different currencies. Namely Nostro, Vostro and Loro accounts. It means “our”, “your” and “their” A bank’s foreign currency

account maintained by the bank in a foreign country and in the home currency of that country is known as Nostro Account

or “our account with you”. Vostro account is the local currency account maintained by a foreign bank/branch. It is also

called “your account with us”. The Loro account is an account wherein a bank remits funds in foreign currency to another

bank for credit to an account of a third bank.

Chapter - 12 : Mergers, Acquisition Restructuring & Business Valuation

2012 - May [3] (a) (i) Pre- merger EPS and P/E retios of LMN Ltd. and XYZ Ltd.

Particulars

LMN Ltd

XYZ Ltd.

Appendix CA Final Gr. I Paper - 2

I-12

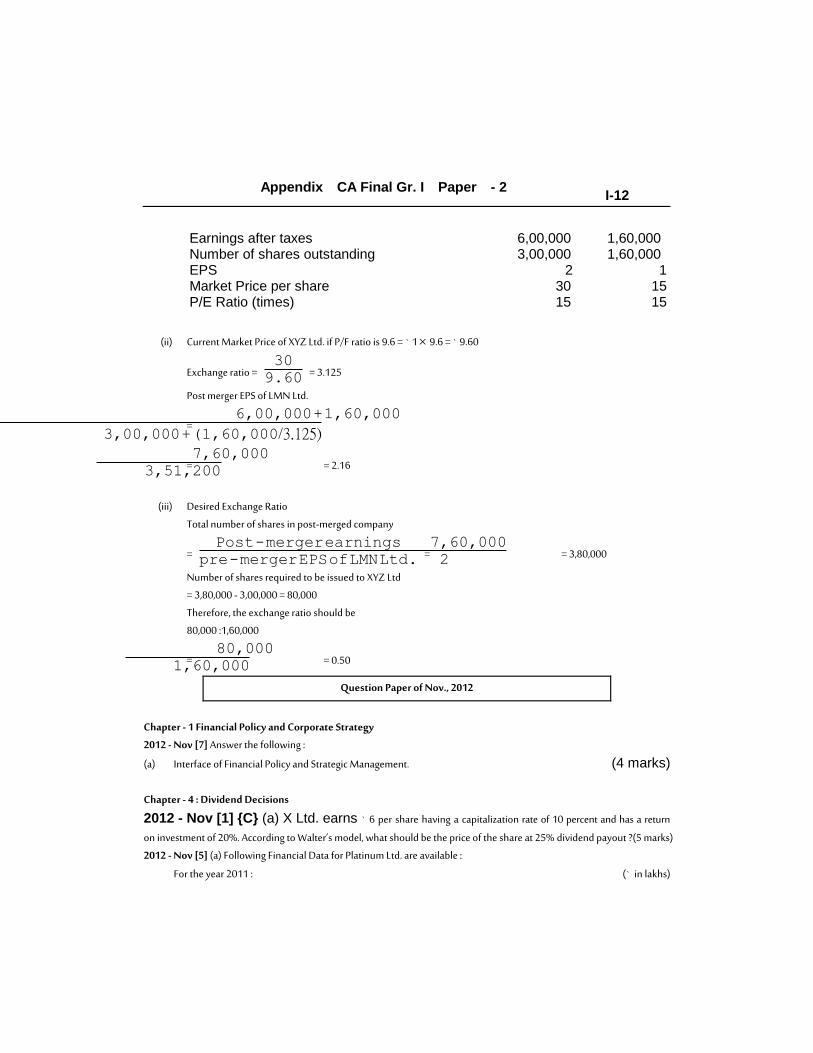

Earnings after taxes Number of shares outstanding EPS Market Price per share P/E Ratio (times)

6,00,000 3,00,000 2 30 15

1,60,000 1,60,000

1 15 15

(ii) Current Market Price of XYZ Ltd. if P/F ratio is 9.6 = ` 1 9.6 = ` 9.60

Exchange ratio = 30

9.60 = 3.125

Post merger EPS of LMN Ltd.

= 6,00,000+1,60,000

3,00,000+(1,60,0003.125)

=7,60,000

3,51,200 = 2.16

(iii) Desired Exchange Ratio

Total number of shares in post-merged company

= Post-mergerearnings

pre-mergerEPSofLMNLtd. =7,60,000

2 = 3,80,000

Number of shares required to be issued to XYZ Ltd

= 3,80,000 - 3,00,000 = 80,000

Therefore, the exchange ratio should be

80,000 :1,60,000

=80,000

1,60,000 = 0.50

Question Paper of Nov., 2012

Chapter - 1 Financial Policy and Corporate Strategy

2012 - Nov [7] Answer the following :

(a) Interface of Financial Policy and Strategic Management. (4 marks)

Chapter - 4 : Dividend Decisions

2012 - Nov [1] {C} (a) X Ltd. earns ` 6 per share having a capitalization rate of 10 percent and has a return

on investment of 20%. According to Walter’s model, what should be the price of the share at 25% dividend payout ?(5 marks)

2012 - Nov [5] (a) Following Financial Data for Platinum Ltd. are available :

For the year 2011 : (` in lakhs)

Appendix CA Final Gr. I Paper - 2

I-13

Equity Shares (` 10 each) 100

8% Debentures 125

10% Bonds 50

Reserves and Surplus 200

Total Assets 500

Assets Turnover Ratio 1.1

Effective Tax Rate 30%

Operating Margin 10%

Required rate of return of investors 15%

Dividend payout ratio 20%

Current market price of shares ` 13

You are required to :

(i) Draw income statement for the year

(ii) Calculate the sustainable growth rate

(iii) Compute the fair price of the company’s share using dividend discount model, and

(iv) Draw your opinion on investment in the company’s share at current price.

(8 marks)

2012 - Nov [6] (b) Given the following information :

Current Dividend

` 5.00

Discount Rate

10%

Growth rate

2%

(i) Calculate the present value of the stock.

(ii) Is the stock over valued if the price is ` 40, ROE = 8% and EPS = ` 3.00. Show your calculations under the PE

Multiple approach and Earnings Growth model. (8 marks)

Chapter - 5 : Indian Capital Market and Security Analysis

2012 - Nov [3] (a) You as an investor had purchased a 4 month call option on the equity shares of X Ltd. of ` 10, of which

the current market price is ` 132 and the exercise price ` 150. You expect the price to range between ` 120 to ` 190. The

expected share price of X Ltd. and related probability is given below: Expected Price (`)

120

140

160

180

190

Probability

.05

.20

.50

.10

.15

Compute the following:

Appendix CA Final Gr. I Paper - 2

I-14

1.Expected Share price at the end of 4 months.

2.Value of Call Option at the end of 4 months, if the exercise price prevails.

3.In case the option is held to its maturity, what will be the expected value of the call option? (8 marks)

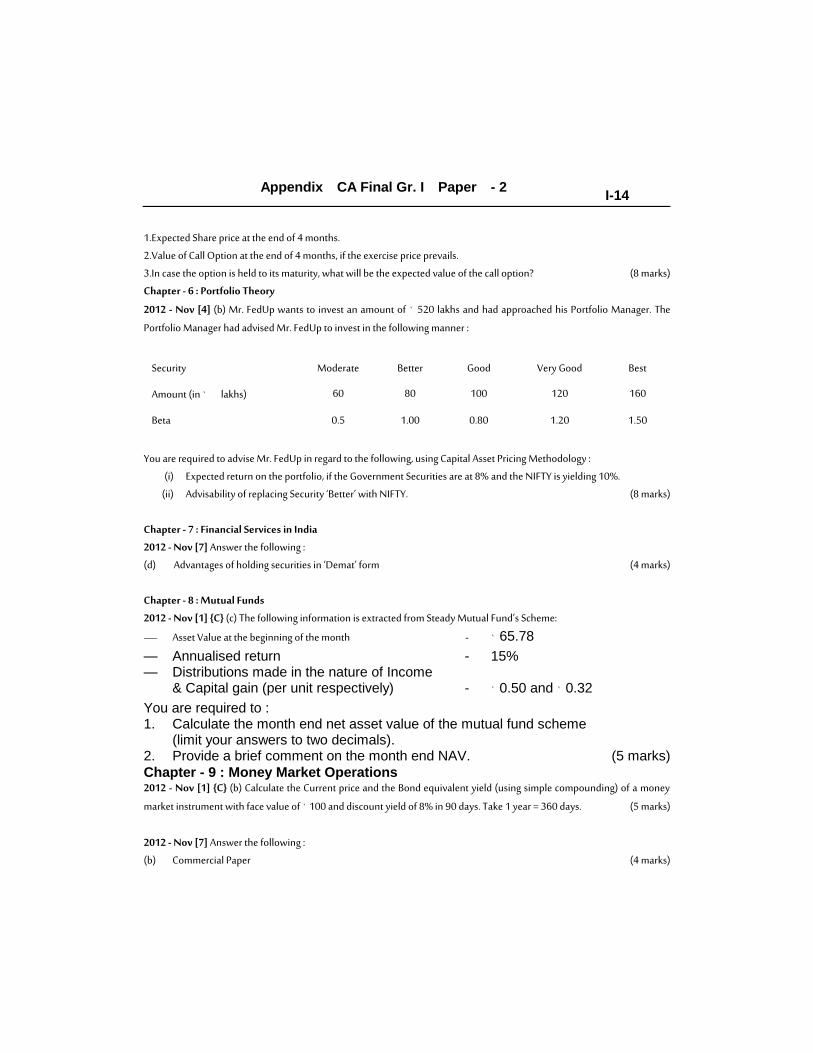

Chapter - 6 : Portfolio Theory

2012 - Nov [4] (b) Mr. FedUp wants to invest an amount of ` 520 lakhs and had approached his Portfolio Manager. The

Portfolio Manager had advised Mr. FedUp to invest in the following manner :

Security

Moderate

Better

Good

Very Good

Best

Amount (in ` lakhs)

60

80

100

120

160

Beta

0.5

1.00

0.80

1.20

1.50

You are required to advise Mr. FedUp in regard to the following, using Capital Asset Pricing Methodology :

(i) Expected return on the portfolio, if the Government Securities are at 8% and the NIFTY is yielding 10%.

(ii) Advisability of replacing Security ‘Better’ with NIFTY. (8 marks)

Chapter - 7 : Financial Services in India

2012 - Nov [7] Answer the following :

(d) Advantages of holding securities in ‘Demat’ form (4 marks)

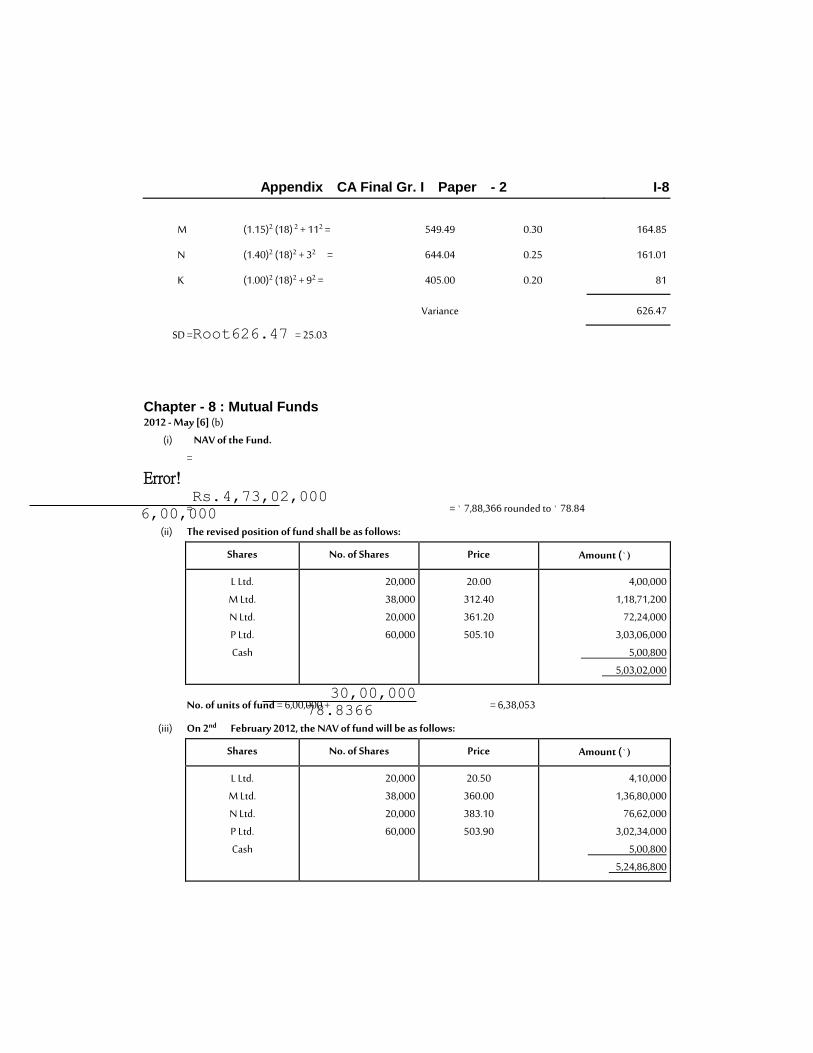

Chapter - 8 : Mutual Funds

2012 - Nov [1] {C} (c) The following information is extracted from Steady Mutual Fund’s Scheme:

— Asset Value at the beginning of the month - ` 65.78

— Annualised return - 15% — Distributions made in the nature of Income

& Capital gain (per unit respectively) - ` 0.50 and ` 0.32

You are required to : 1. Calculate the month end net asset value of the mutual fund scheme

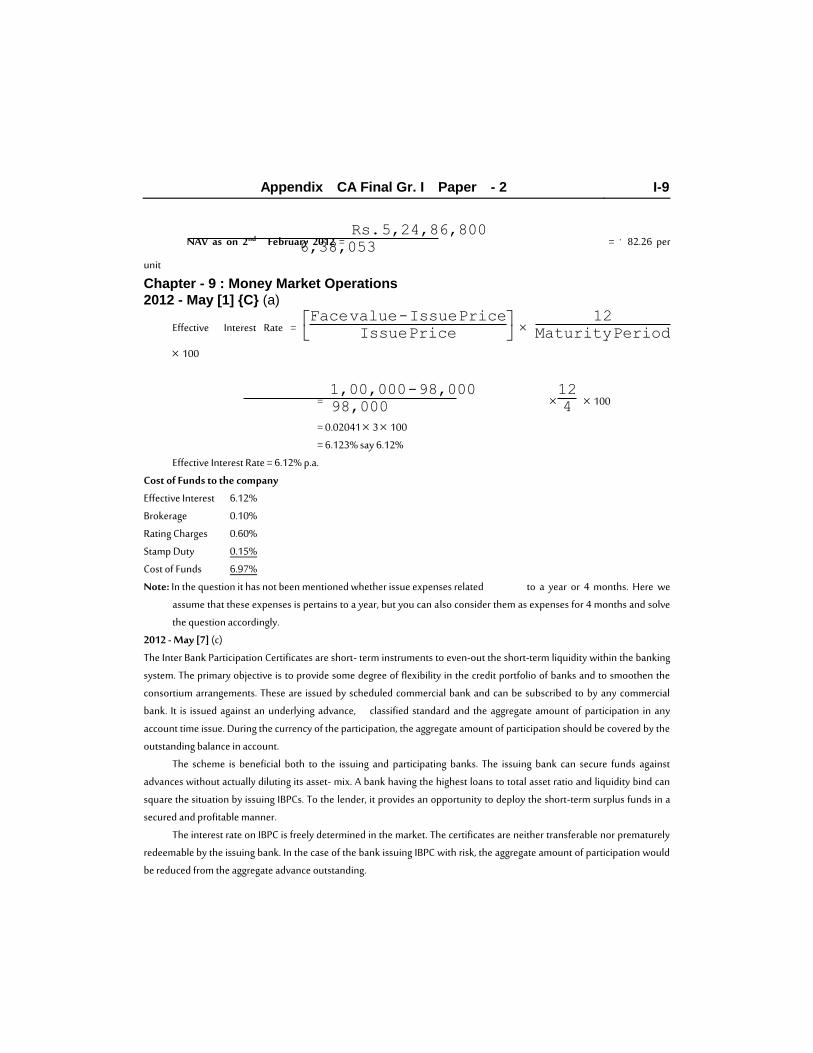

(limit your answers to two decimals). 2. Provide a brief comment on the month end NAV. (5 marks) Chapter - 9 : Money Market Operations 2012 - Nov [1] {C} (b) Calculate the Current price and the Bond equivalent yield (using simple compounding) of a money

market instrument with face value of ` 100 and discount yield of 8% in 90 days. Take 1 year = 360 days. (5 marks)

2012 - Nov [7] Answer the following :

(b) Commercial Paper (4 marks)

Appendix CA Final Gr. I Paper - 2

I-15

Chapter - 10 : FDI, FII and International Financial Management

2012 - Nov [7] Answer the following :

(c) American Depository Receipt (4 marks)

Chapter - 11 : Foreign Exchange Exposure and Risk Management 2012 - Nov [1] {C} (d) The US dollar is selling in India at ` 55.50. If the interest rate for a 6 months

borrowing in India is 10% per annum and the corresponding rate in USA is 4%: (i) Do you expect that US dollar will be at a premium or at discount in the Indian

Forex Market ? (ii) What will be the expected 6 - months forward rate for US dollar in India? and (iii) What will be the rate of forward premium or discount ? (5 marks) 2012 - Nov [3] (b) Z Ltd. importing goods worth USD 2 million, requires 90 days to make the payment. The overseas

supplier has offered a 60 days interest free credit period and for additional credit for 30 days an interest of 8% per annum.

The bankers of Z Ltd offer a 30 days loan at 10% per annum and their quote for foreign exchange is as follows:

` Spot 1 USD - 56.50

60 days forward for 1 USD - 57.10

90 days forward for 1 USD - 57.50

You are required to evaluate the following options :

(I) Pay the supplier in 60 days, or

(II) Avail the supplier’s offer of 90 days credit. (8 marks)

Chapter - 12 : Mergers, Acquisition Restructuring & Business Valuation

2012 - Nov [2] (a) H Ltd. agrees to buy over the business of B Ltd. effective 1st April, 2012.

The summarized Balance Sheets of H Ltd. and B Ltd. as on 31st March 2012 are as follows :

Balance Sheet as at 31st March, 2012

(in Crores of Rupees) Liabilities:

H Ltd.

B Ltd.

Paid up Share Capital :

— Equity Shares of ` 100 each

350.00

— Equity Shares of ` 10 each

6.50

Reserves & Surplus

950.00

25.00

Total

1,300.00

31.50

Appendix CA Final Gr. I Paper - 2

I-16

Assets: Net Fixed Assets

220.00

0.50

Net Current Assets

1,020.00

29.00

Deferred Tax Asset

60.00

2.00

Total

1,300.00

31.50

H Ltd. proposes to buy out B Ltd. and the following information is provided to you as part of the scheme of buying:

1.The weighted average post tax maintainable profits of H Ltd. and B Ltd. for the last 4 years are ` 300 crores and 10 crores

respectively.

2.Both the companies envisage a capitalization rate of 8%.

3.H Ltd. has a contingent liability of ` 300 crores as on 31st March, 2012.

4.H Ltd. to issue shares of ` 100 each to the shareholders of B Ltd. in terms of the exchange ratio as arrived on a Fair Value

basis. (Please consider weights of 1 and 3 for the value of shares arrived on Net Asset basis and Earnings

capitalization method respectively for both H Ltd. and B Ltd.)

You are required to arrive at the value of the shares of both H Ltd. and B Ltd. under:

(i) Net Asset Value Method

(ii) Earnings Capitalisation Method

(iii) Exchange ratio of shares of H Ltd. to be issued to the shareholders of B Ltd. on a Fair value basis (taking into

consideration the assumption mentioned in point 4 above) (12 marks)

2012 - Nov [4] (a) Eagle Ltd. reported a profit of ` 77 lakhs after 30% tax for the financial year 2011-12. An analysis of the

accounts revealed that the income included extraordinary items of ` 8 lakhs and an extraordinary loss of ` 10 lakhs. The

existing operations, except for the extraordinary items, are expected to continue in the future. In addition, the results of the

launch of a new product are expected to be as follows :

` in lakhs

Sales 70

Material costs 20

Labour costs 12

Fixed costs 10

You are required to :

(i) Calculate the value of the business, given that the capitalization rate is 14%.

(ii) Determine the market price per equity share, with Eagle Ltd.’s share capital being comprised of 1,00,000 13%

preference shares of ` 100 each and 50,00,000 equity shares of ` 10 each and the P/E ratio being 10 times.

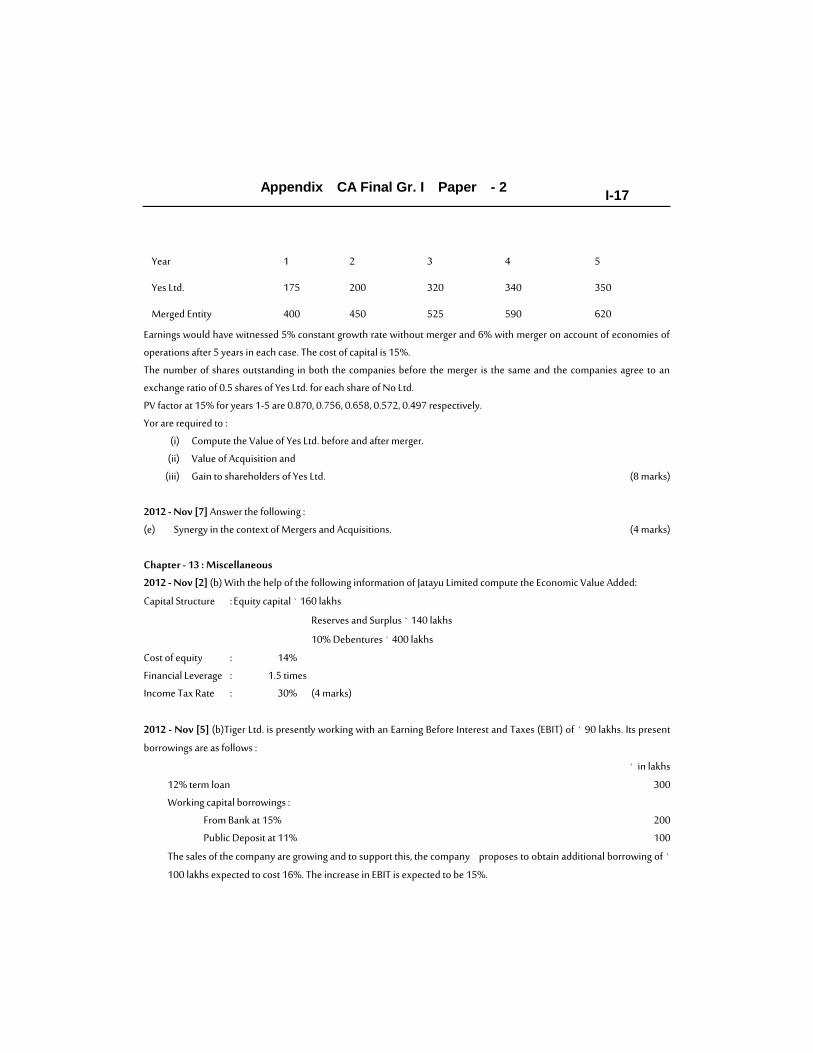

(8 marks) 2012 - Nov [6] (a) Yes Ltd. Wants to acquire No Ltd. and the cash flows of Yes Ltd. and the merged entity are given below :(` in lakhs)

Appendix CA Final Gr. I Paper - 2

I-17

Year

1

2

3

4

5

Yes Ltd.

175

200

320

340

350

Merged Entity

400

450

525

590

620

Earnings would have witnessed 5% constant growth rate without merger and 6% with merger on account of economies of

operations after 5 years in each case. The cost of capital is 15%.

The number of shares outstanding in both the companies before the merger is the same and the companies agree to an

exchange ratio of 0.5 shares of Yes Ltd. for each share of No Ltd.

PV factor at 15% for years 1-5 are 0.870, 0.756, 0.658, 0.572, 0.497 respectively.

Yor are required to :

(i) Compute the Value of Yes Ltd. before and after merger.

(ii) Value of Acquisition and

(iii) Gain to shareholders of Yes Ltd. (8 marks)

2012 - Nov [7] Answer the following :

(e) Synergy in the context of Mergers and Acquisitions. (4 marks)

Chapter - 13 : Miscellaneous

2012 - Nov [2] (b) With the help of the following information of Jatayu Limited compute the Economic Value Added:

Capital Structure : Equity capital ` 160 lakhs

Reserves and Surplus ` 140 lakhs

10% Debentures ` 400 lakhs

Cost of equity : 14%

Financial Leverage : 1.5 times

Income Tax Rate : 30% (4 marks)

2012 - Nov [5] (b)Tiger Ltd. is presently working with an Earning Before Interest and Taxes (EBIT) of ` 90 lakhs. Its present

borrowings are as follows :

` in lakhs

12% term loan 300

Working capital borrowings :

From Bank at 15% 200

Public Deposit at 11% 100

The sales of the company are growing and to support this, the company proposes to obtain additional borrowing of `

100 lakhs expected to cost 16%. The increase in EBIT is expected to be 15%.

Appendix CA Final Gr. I Paper - 2

I-18

Calculate the change in interest coverage ratio after the additional borrowing is effected and comment on the arrangement made. (8 marks)