41

Application : Hedging and Derivatives Interest Rate Swap and Futures Aramsri Choowongse, CFA Nopadol Prateepratana

Application : Hedging and Derivatives

Interest Rate Swap and Futures

Aramsri Choowongse, CFA

Nopadol Prateepratana

2Major heading

Presentation Outline

Hedging : Basics

BIBOR : Development in Derivative Market

Interest Rate Swap (IRS)

BIBOR Futures

3Major heading

Hedging : Basics

4Major heading

Hedge Accounting

IFRS 9 Roadmap : Implemented by 2013 to replace IAS 39

BOT’s Requirements

Study and Gap Analysis : H2/2011 – Q1/2012

System Planning : 2012-2013

Parallel Run : 2014

Implementation : 2015

Schedule for Corporate Implementation is not yet confirmed.

5Major heading

Types of Hedges

1. Cash Flow Hedge (CFH)

Change floating-rate profile to fixed-rate profile to reduce interest rate

risk.

Need to prove effectiveness of floating profile and floating index.

No mark-to-market for accounting.

6Major heading

Types of Hedges

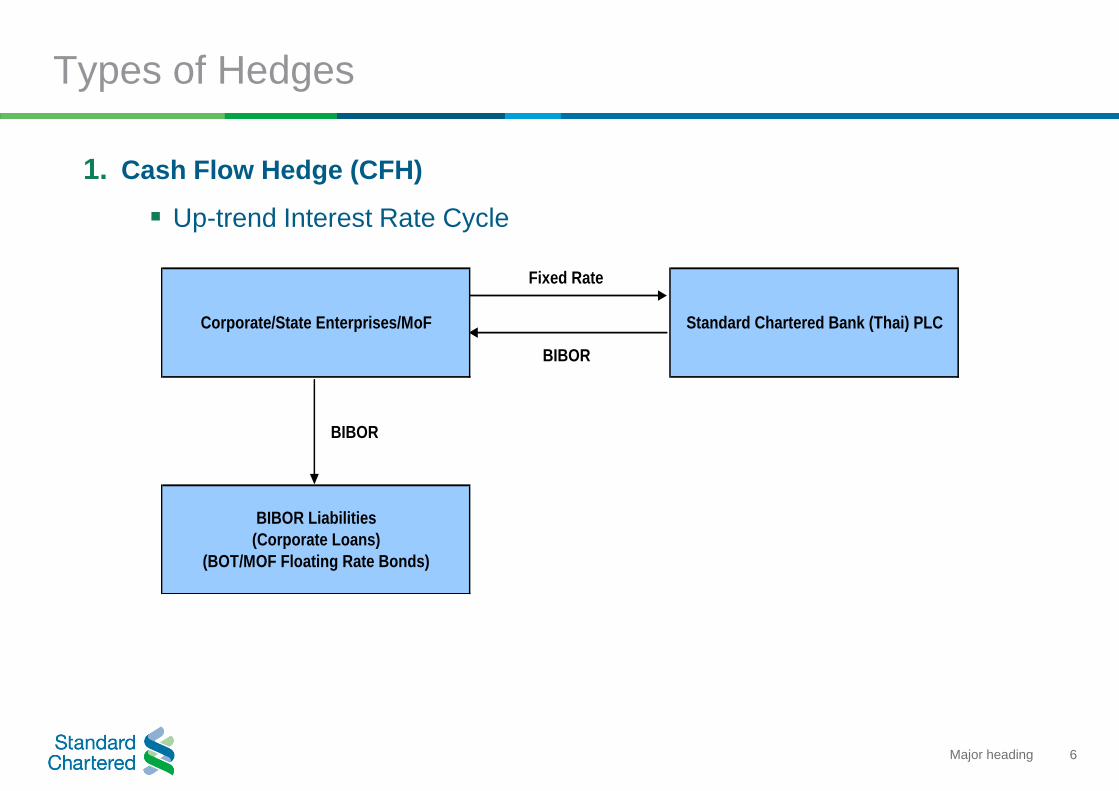

1. Cash Flow Hedge (CFH)

Up-trend Interest Rate Cycle

Corporate/State Enterprises/MoF Standard Chartered Bank (Thai) PLC

BIBOR Liabilities

(Corporate Loans)

(BOT/MOF Floating Rate Bonds)

BIBOR

BIBOR

Fixed Rate

7Major heading

Types of Hedges

1. Cash Flow Hedge (CFH)

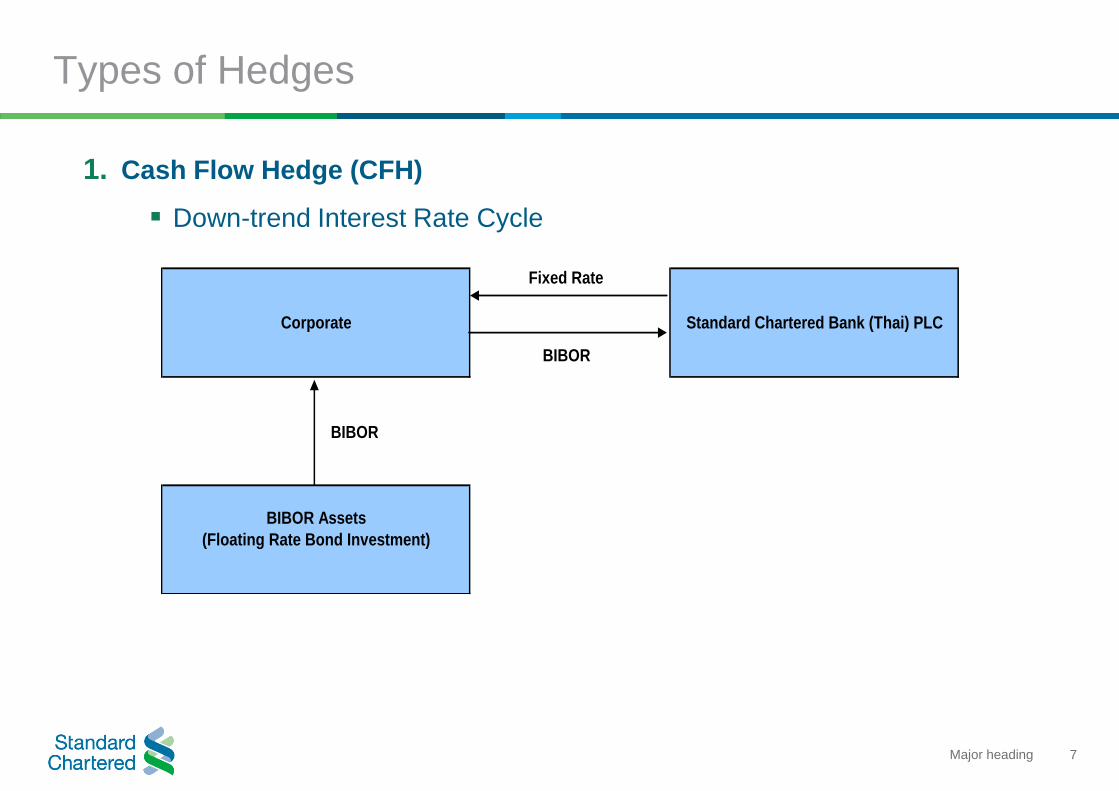

Down-trend Interest Rate Cycle

Corporate Standard Chartered Bank (Thai) PLC

BIBOR Assets

(Floating Rate Bond Investment)

BIBOR

BIBOR

Fixed Rate

8Major heading

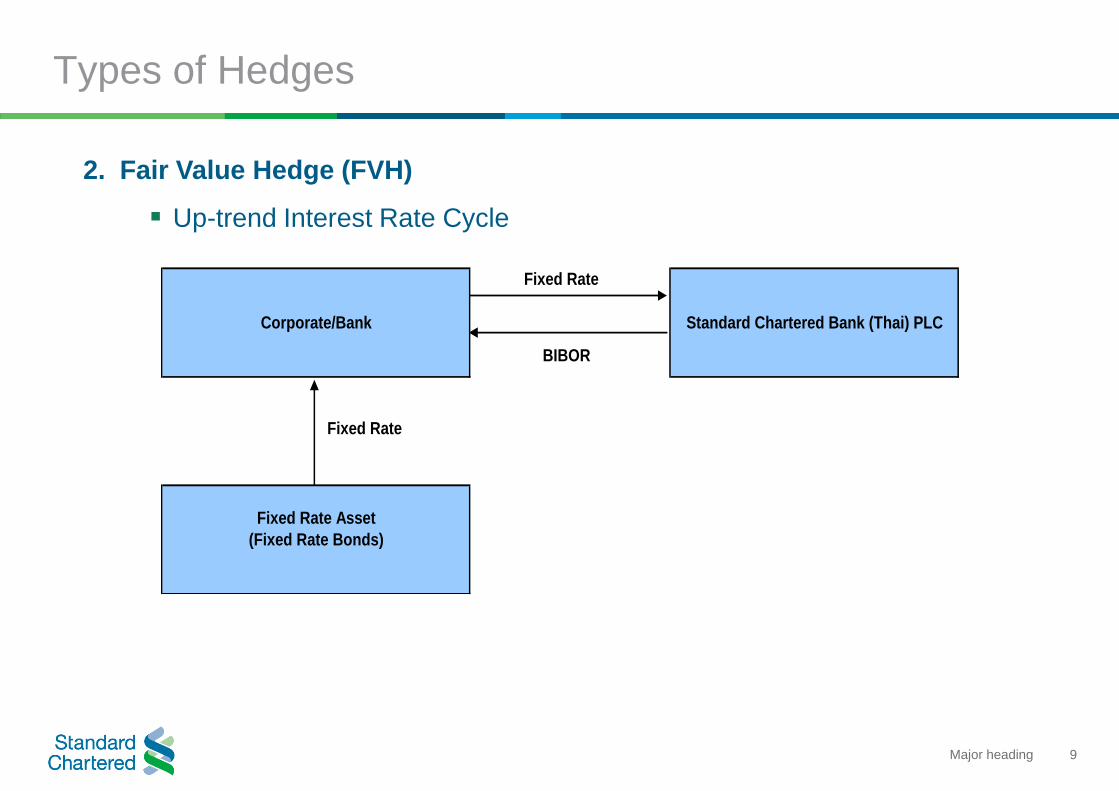

Types of Hedges

2. Fair Value Hedge (FVH)

Change fixed-rate profile to floating-rate profile to reduce interest rate

risk.

Need to mark-to-market both underlyings and hedges.

Neutral PnL impact if 100% hedged.

9Major heading

Types of Hedges

2. Fair Value Hedge (FVH)

Up-trend Interest Rate Cycle

Corporate/Bank Standard Chartered Bank (Thai) PLC

Fixed Rate Asset

(Fixed Rate Bonds)

BIBOR

Fixed Rate

Fixed Rate

10Major heading

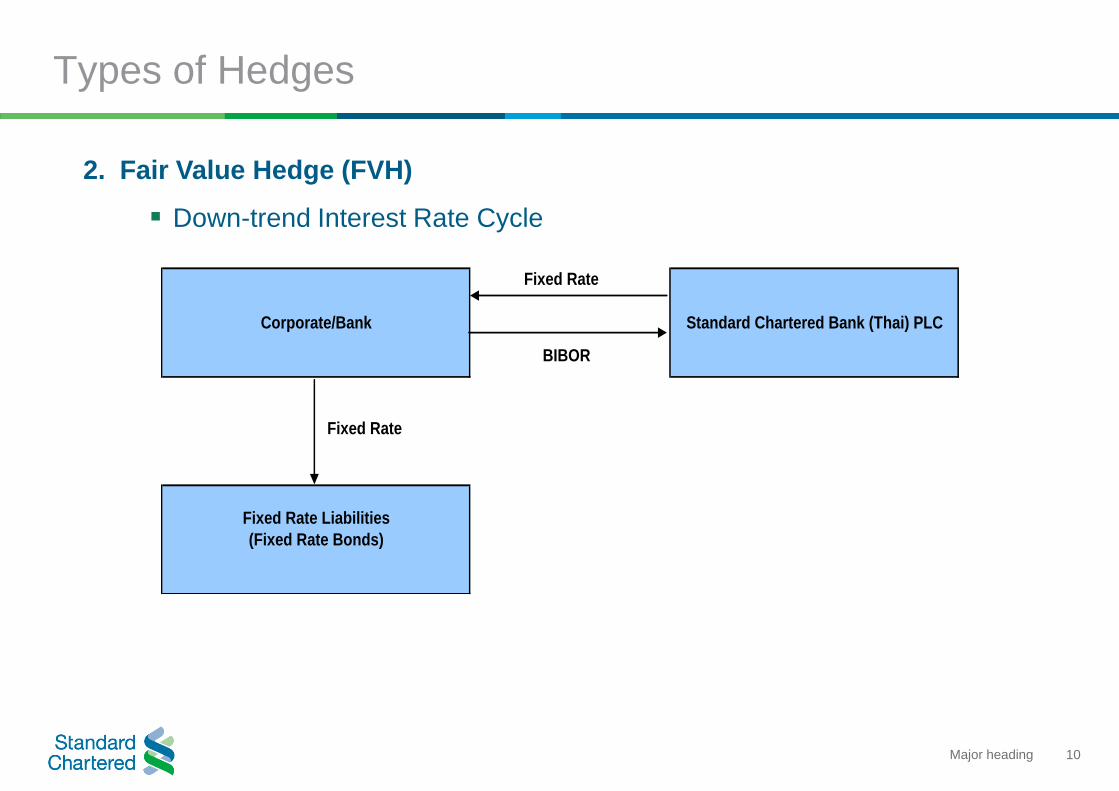

Types of Hedges

2. Fair Value Hedge (FVH)

Down-trend Interest Rate Cycle

Corporate/Bank Standard Chartered Bank (Thai) PLC

Fixed Rate Liabilities

(Fixed Rate Bonds)

BIBOR

Fixed Rate

Fixed Rate

11Major heading

Types of Hedges

3. Economic Hedge

All kinds of hedges can be done.

Need to mark-to-market.

Impact on PnL.

Some companies or banks might have internal guidelines that prohibits

economic hedge to avoid PnL volatility.

12Major heading

BIBOR : Development in Derivative Market

13Major heading

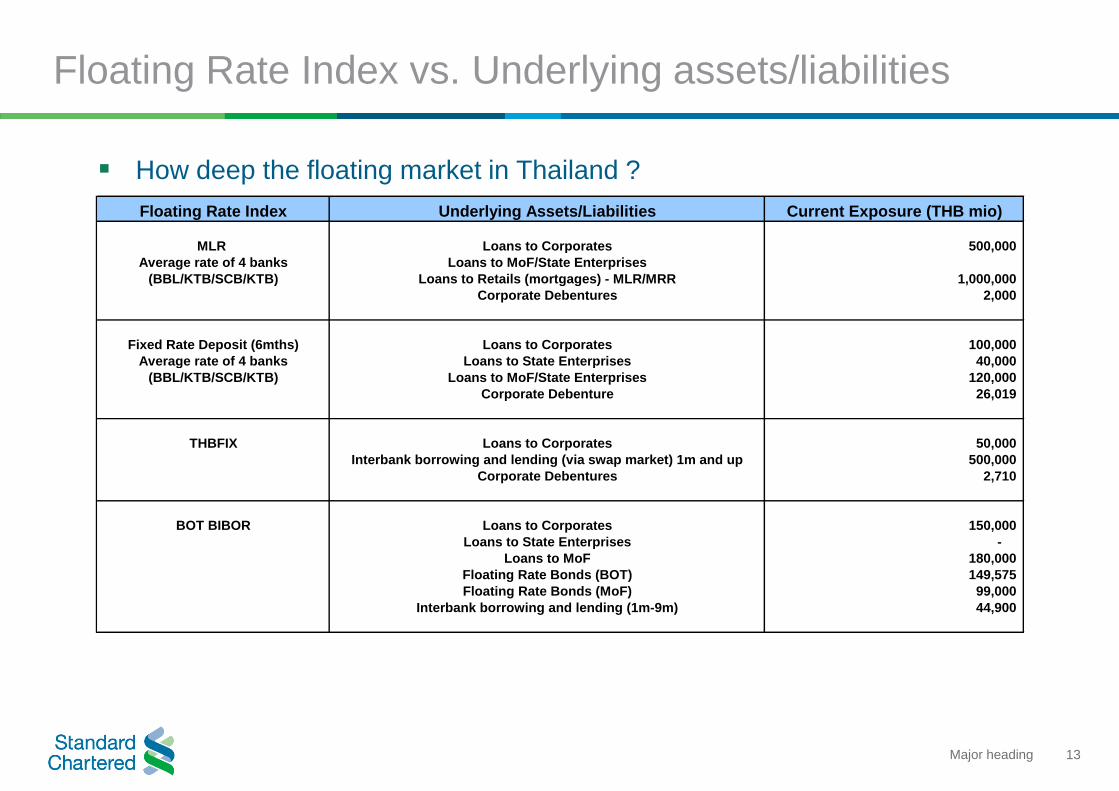

Floating Rate Index vs. Underlying assets/liabilities

How deep the floating market in Thailand ?

Floating Rate Index Underlying Assets/Liabilities Current Exposure (THB mio)

MLR Loans to Corporates 500,000

Average rate of 4 banks Loans to MoF/State Enterprises

(BBL/KTB/SCB/KTB) Loans to Retails (mortgages) - MLR/MRR 1,000,000

Corporate Debentures 2,000

Fixed Rate Deposit (6mths) Loans to Corporates 100,000

Average rate of 4 banks Loans to State Enterprises 40,000

(BBL/KTB/SCB/KTB) Loans to MoF/State Enterprises 120,000

Corporate Debenture 26,019

THBFIX Loans to Corporates 50,000

Interbank borrowing and lending (via swap market) 1m and up 500,000

Corporate Debentures 2,710

BOT BIBOR Loans to Corporates 150,000

Loans to State Enterprises -

Loans to MoF 180,000

Floating Rate Bonds (BOT) 149,575

Floating Rate Bonds (MoF) 99,000

Interbank borrowing and lending (1m-9m) 44,900

14Major heading

Interest Rate Swap (IRS)

15Major heading

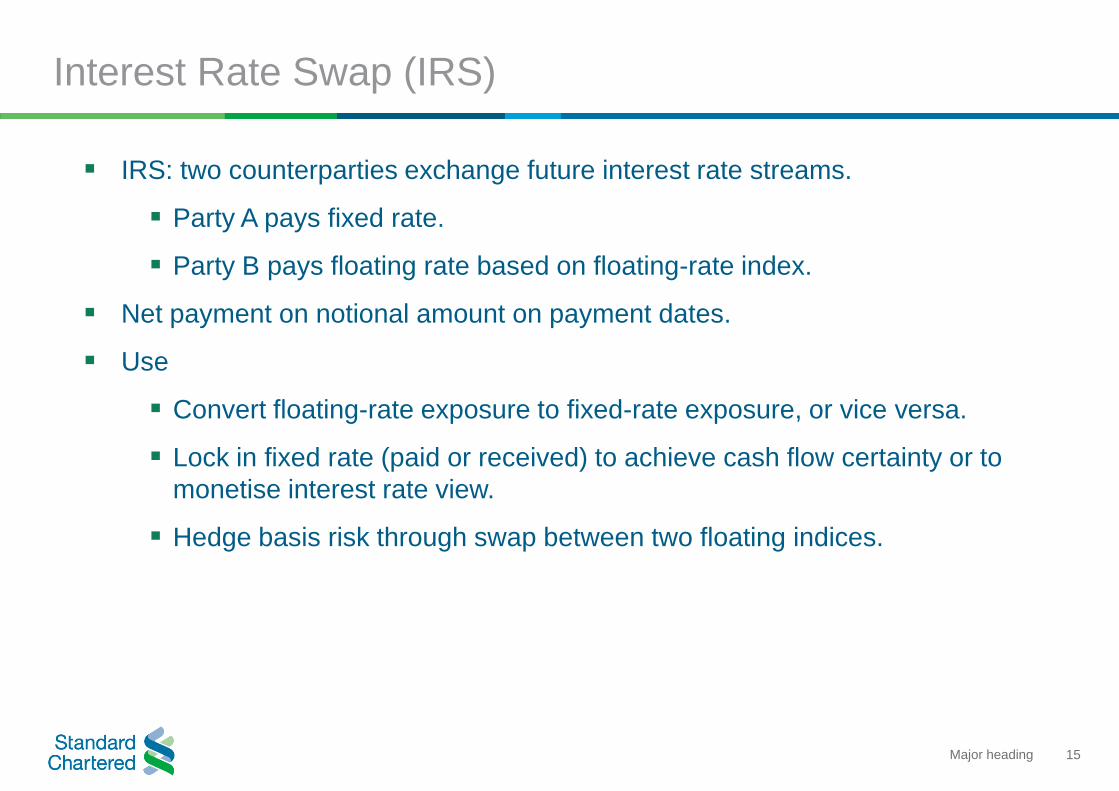

Interest Rate Swap (IRS)

IRS: two counterparties exchange future interest rate streams.

Party A pays fixed rate.

Party B pays floating rate based on floating-rate index.

Net payment on notional amount on payment dates.

Use

Convert floating-rate exposure to fixed-rate exposure, or vice versa.

Lock in fixed rate (paid or received) to achieve cash flow certainty or to

monetise interest rate view.

Hedge basis risk through swap between two floating indices.

16Major heading

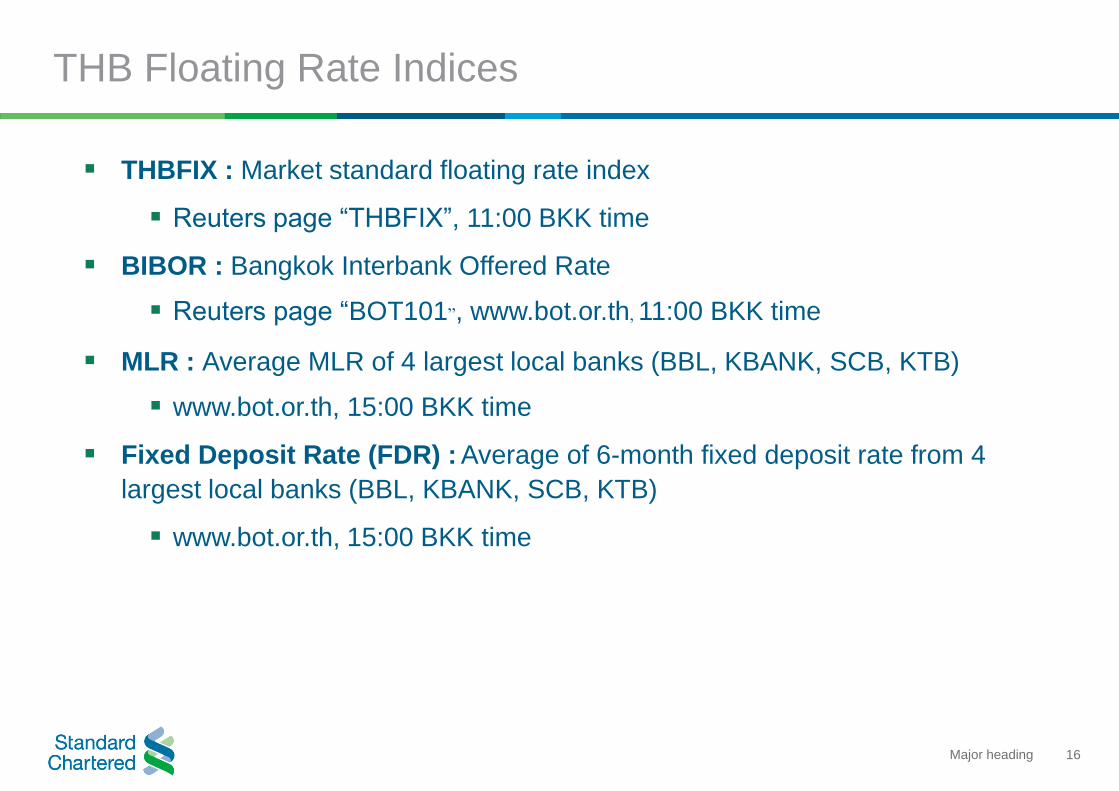

THB Floating Rate Indices

THBFIX : Market standard floating rate index

Reuters page “THBFIX”, 11:00 BKK time

BIBOR : Bangkok Interbank Offered Rate

Reuters page “BOT101”, www.bot.or.th, 11:00 BKK time

MLR : Average MLR of 4 largest local banks (BBL, KBANK, SCB, KTB)

www.bot.or.th, 15:00 BKK time

Fixed Deposit Rate (FDR) : Average of 6-month fixed deposit rate from 4

largest local banks (BBL, KBANK, SCB, KTB)

www.bot.or.th, 15:00 BKK time

17Major heading

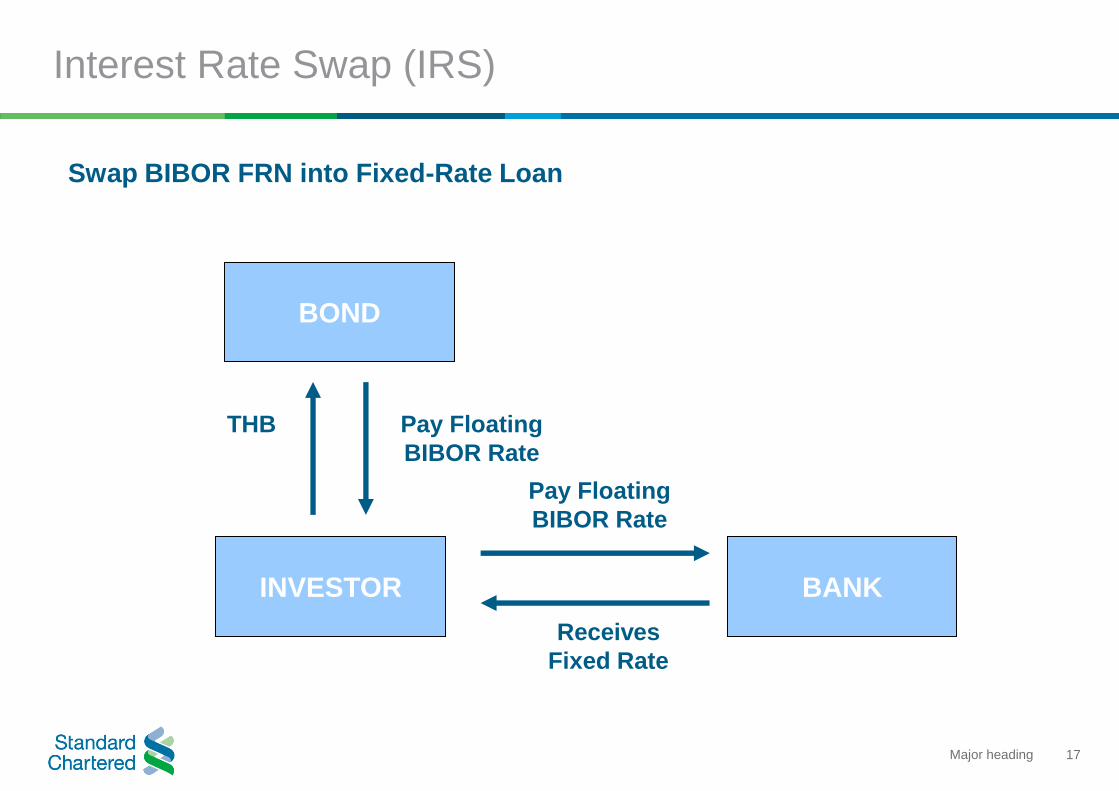

Interest Rate Swap (IRS)

Swap BIBOR FRN into Fixed-Rate Loan

INVESTOR BANK

BOND

Receives

Fixed Rate

Pay Floating

BIBOR Rate

Pay Floating

BIBOR Rate

THB

18Major heading

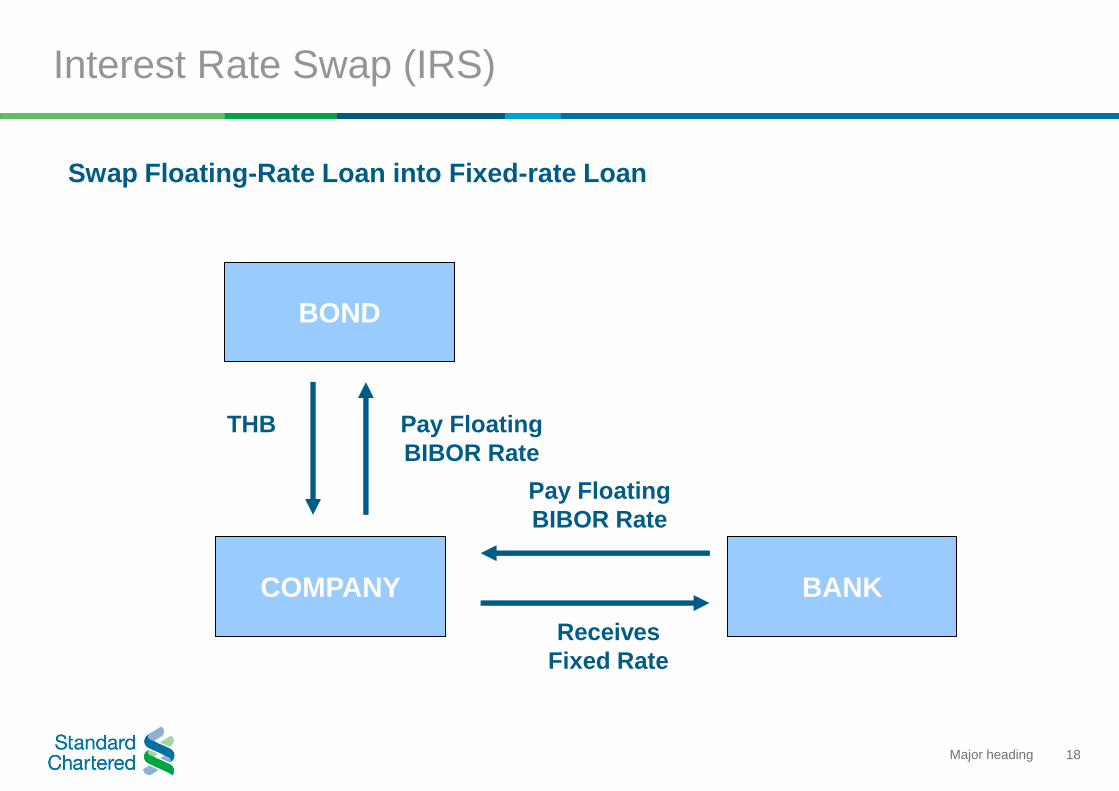

Interest Rate Swap (IRS)

Swap Floating-Rate Loan into Fixed-rate Loan

COMPANY BANK

BOND

Receives

Fixed Rate

Pay Floating

BIBOR Rate

Pay Floating

BIBOR Rate

THB

19Major heading

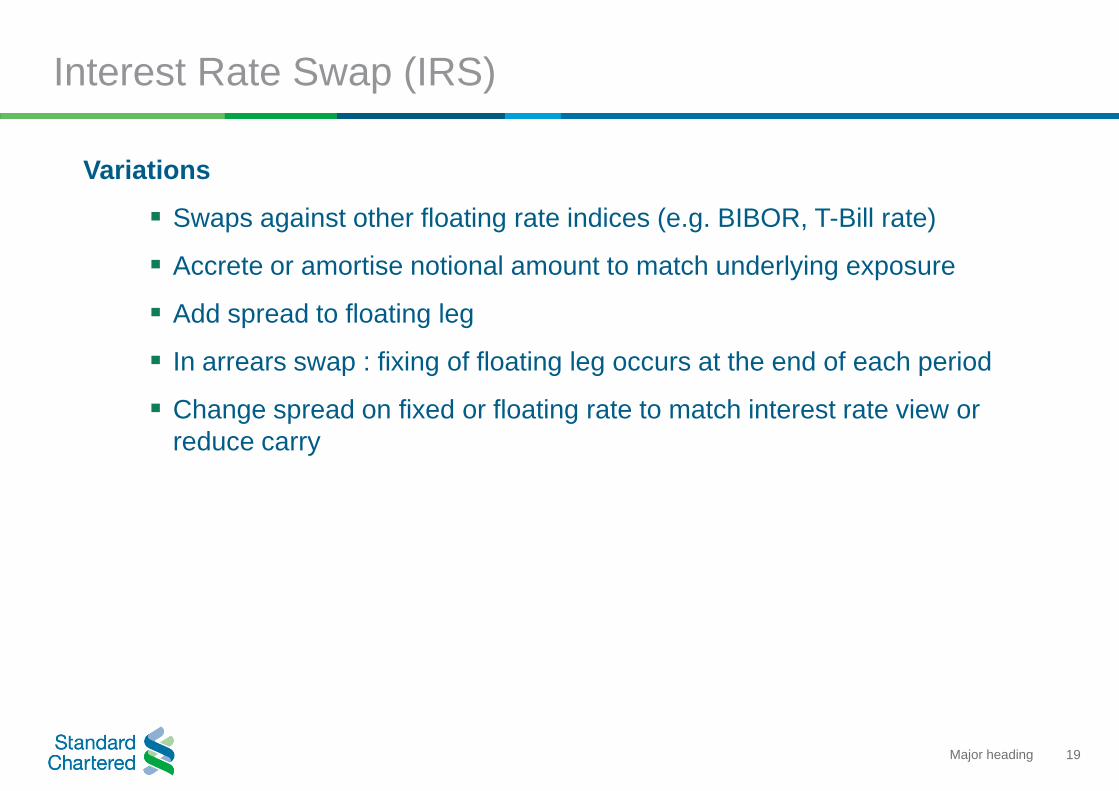

Interest Rate Swap (IRS)

Variations

Swaps against other floating rate indices (e.g. BIBOR, T-Bill rate)

Accrete or amortise notional amount to match underlying exposure

Add spread to floating leg

In arrears swap : fixing of floating leg occurs at the end of each period

Change spread on fixed or floating rate to match interest rate view or

reduce carry

20Major heading

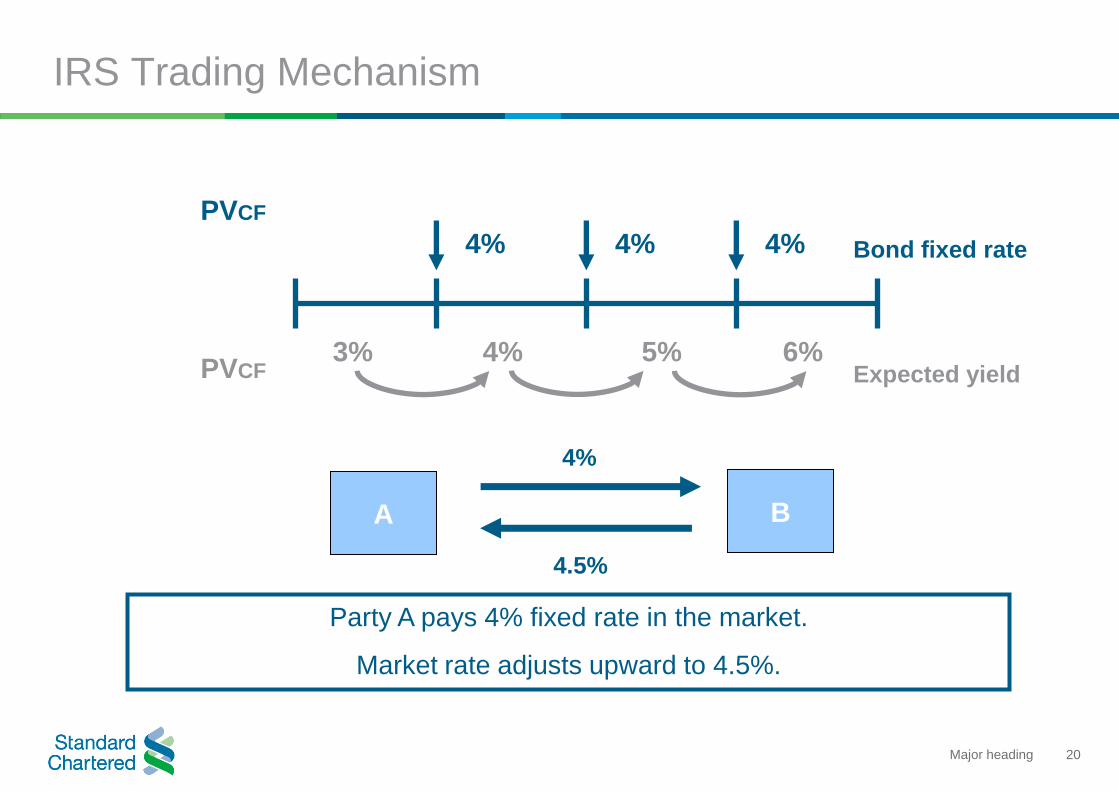

IRS Trading Mechanism

4% 4% 4%

PVCF

PVCF4% 5% 6%3%

Expected yield

Bond fixed rate

Party A pays 4% fixed rate in the market.

Market rate adjusts upward to 4.5%.

A B

4%

4.5%

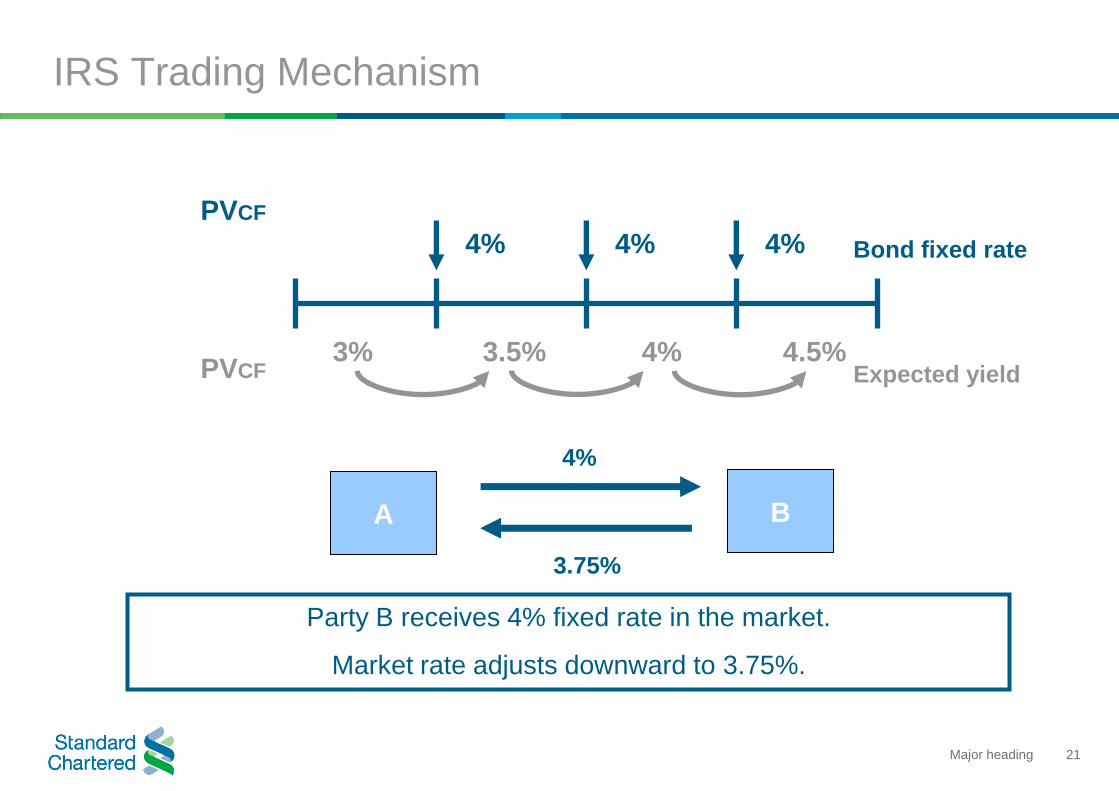

21Major heading

IRS Trading Mechanism

4% 4% 4%

PVCF

PVCF3.5% 4% 4.5%3%

Expected yield

Bond fixed rate

Party B receives 4% fixed rate in the market.

Market rate adjusts downward to 3.75%.

A B

4%

3.75%

22Major heading

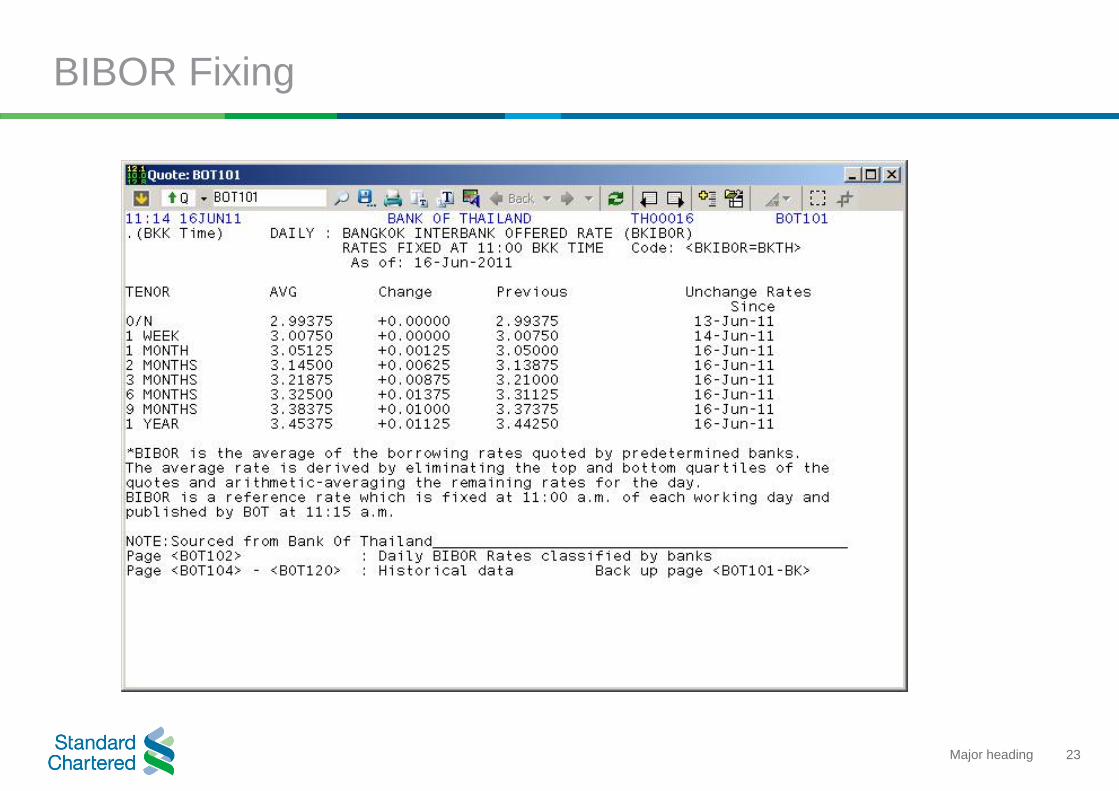

BIBOR Fixing

BIBOR is the average of borrowing rates quoted by predetermined banks.

BIBOR is derived by eliminating the top and bottom quartiles of the quotes

and arithmetic-averaging the remaining quotes.

BIBOR is a reference rate which is fixed at 11:00 of each working day and

published by BOT at 11:15.

23Major heading

BIBOR Fixing

24Major heading

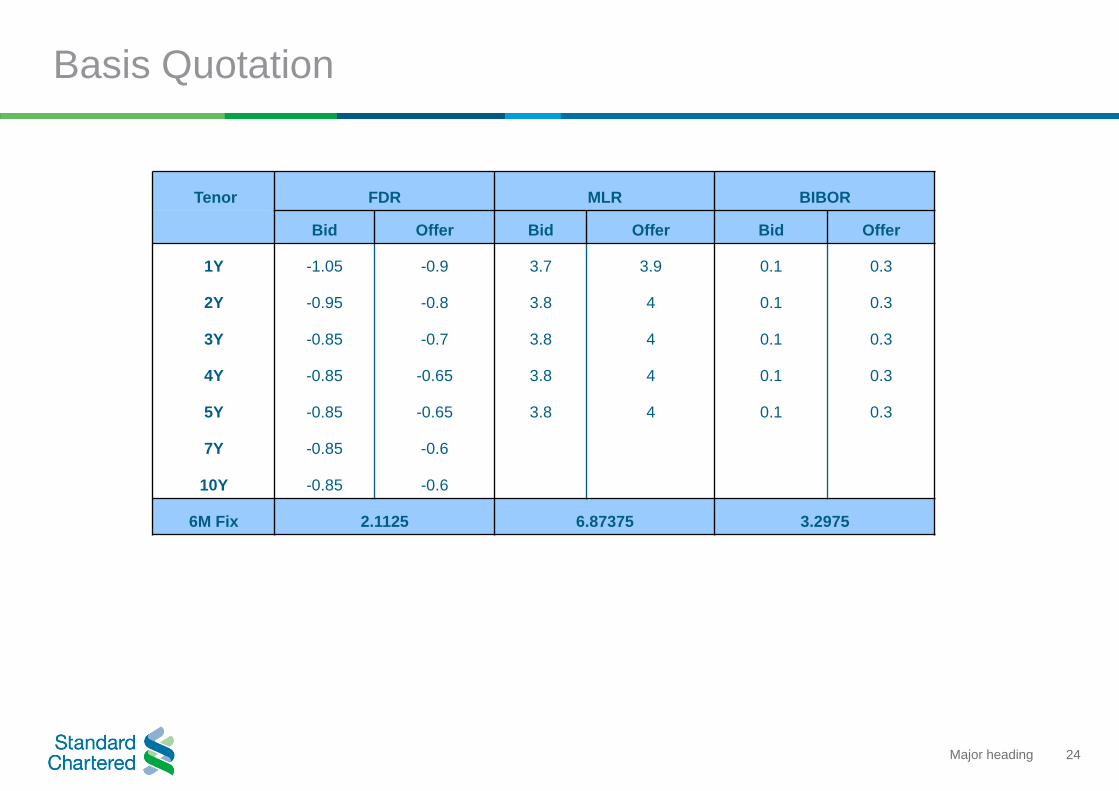

Basis Quotation

Tenor FDR MLR BIBOR

Bid Offer Bid Offer Bid Offer

1Y -1.05 -0.9 3.7 3.9 0.1 0.3

2Y -0.95 -0.8 3.8 4 0.1 0.3

3Y -0.85 -0.7 3.8 4 0.1 0.3

4Y -0.85 -0.65 3.8 4 0.1 0.3

5Y -0.85 -0.65 3.8 4 0.1 0.3

7Y -0.85 -0.6

10Y -0.85 -0.6

6M Fix 2.1125 6.87375 3.2975

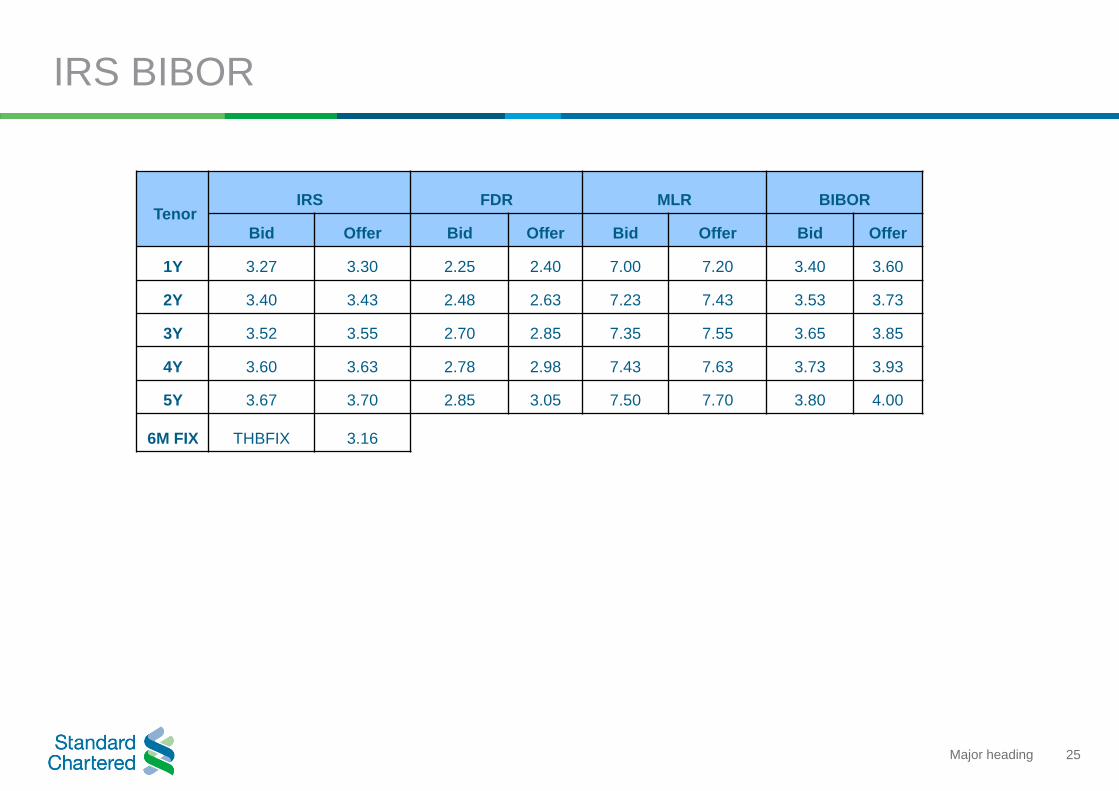

25Major heading

IRS BIBOR

TenorIRS FDR MLR BIBOR

Bid Offer Bid Offer Bid Offer Bid Offer

1Y 3.27 3.30 2.25 2.40 7.00 7.20 3.40 3.60

2Y 3.40 3.43 2.48 2.63 7.23 7.43 3.53 3.73

3Y 3.52 3.55 2.70 2.85 7.35 7.55 3.65 3.85

4Y 3.60 3.63 2.78 2.98 7.43 7.63 3.73 3.93

5Y 3.67 3.70 2.85 3.05 7.50 7.70 3.80 4.00

6M FIX THBFIX 3.16

26Major heading

IRS BIBOR

Bid-offer spread of BIBOR IRS is wider than normal IRS.

Cash BIBOR market to become more active soon.

Illiquid and non-tradable cash borrowing and lending.

Illiquid and sizable in future market.

Banks need to allocate reserves for illiquid index.

Market players run basis risk among the curve.

27Major heading

IRS Curve

Drivers

Historical rate movement

Market view of future rate movement

Market demand and supply

28Major heading

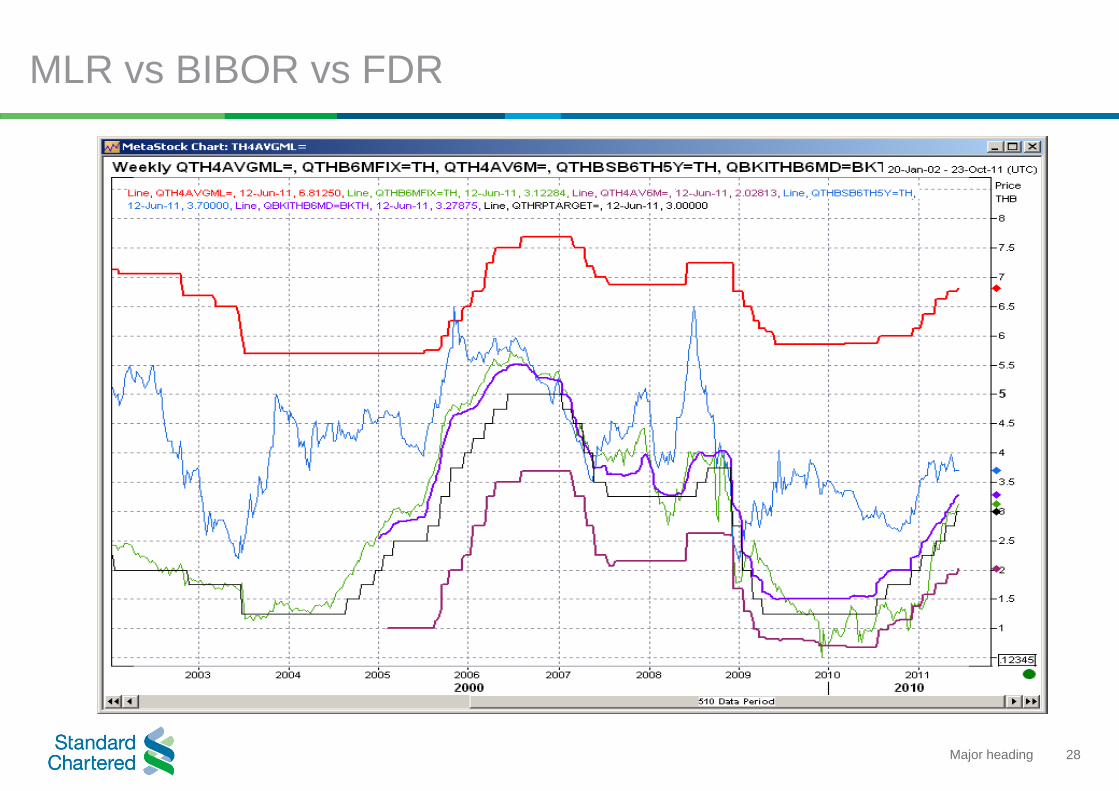

MLR vs BIBOR vs FDR

29Major heading

Trading Ideas

Risk and Opportunity in BIBOR vs MLR : market may misprice given

market demand and supply.

BIBOR swap allows investors to achieve higher return than fixed rate

bond

BIBOR swap is a better hedge if client wants to pay fixed rate

BIBOR can move faster than MLR in tightening cycle

MLR fixed rate at historical high offers investment opportunity

Make no sense to convert to fixed

30Major heading

BIBOR Futures

31Major heading

BIBOR Futures

Eurodollar futures (ED)

A future contract based on eurodollar deposits.

Prices are determined by expected 3-month USD LIBOR that are

expected to prevail on settlement date.

Settlement price is 100 minus 3-month LIBOR fixing on settlement date.

32Major heading

BIBOR Futures

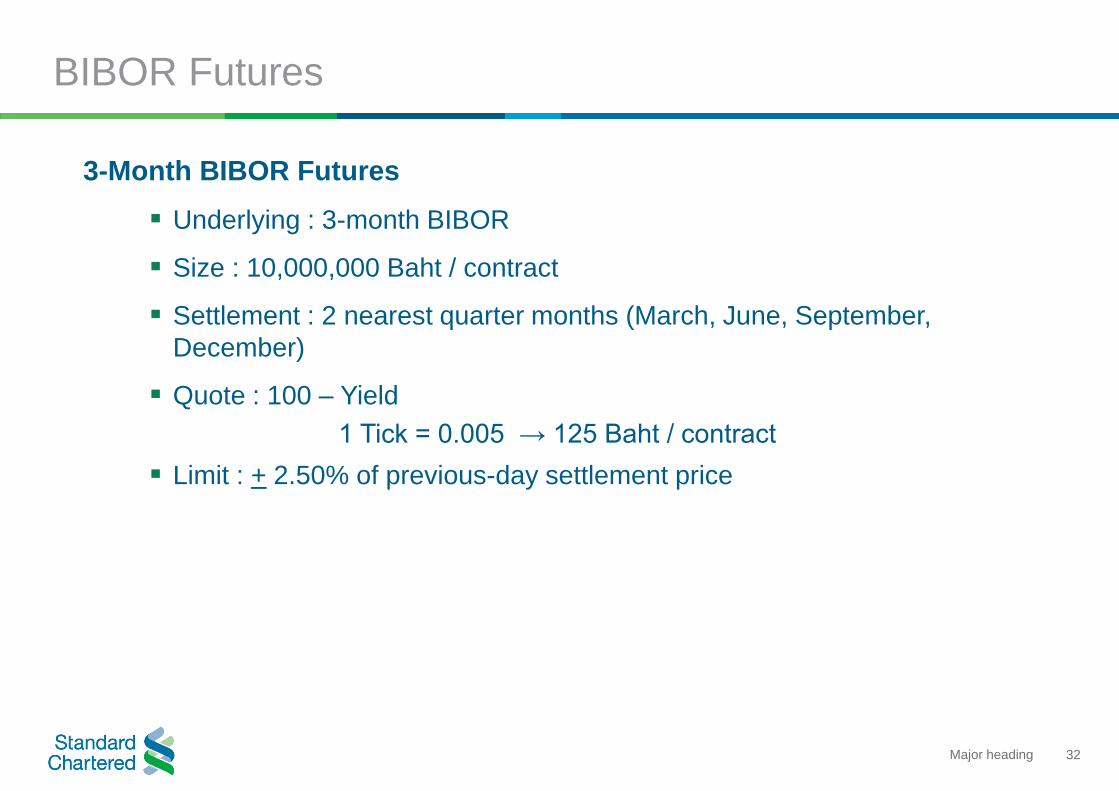

3-Month BIBOR Futures

Underlying : 3-month BIBOR

Size : 10,000,000 Baht / contract

Settlement : 2 nearest quarter months (March, June, September,

December)

Quote : 100 – Yield

1 Tick = 0.005 → 125 Baht / contract

Limit : + 2.50% of previous-day settlement price

33Major heading

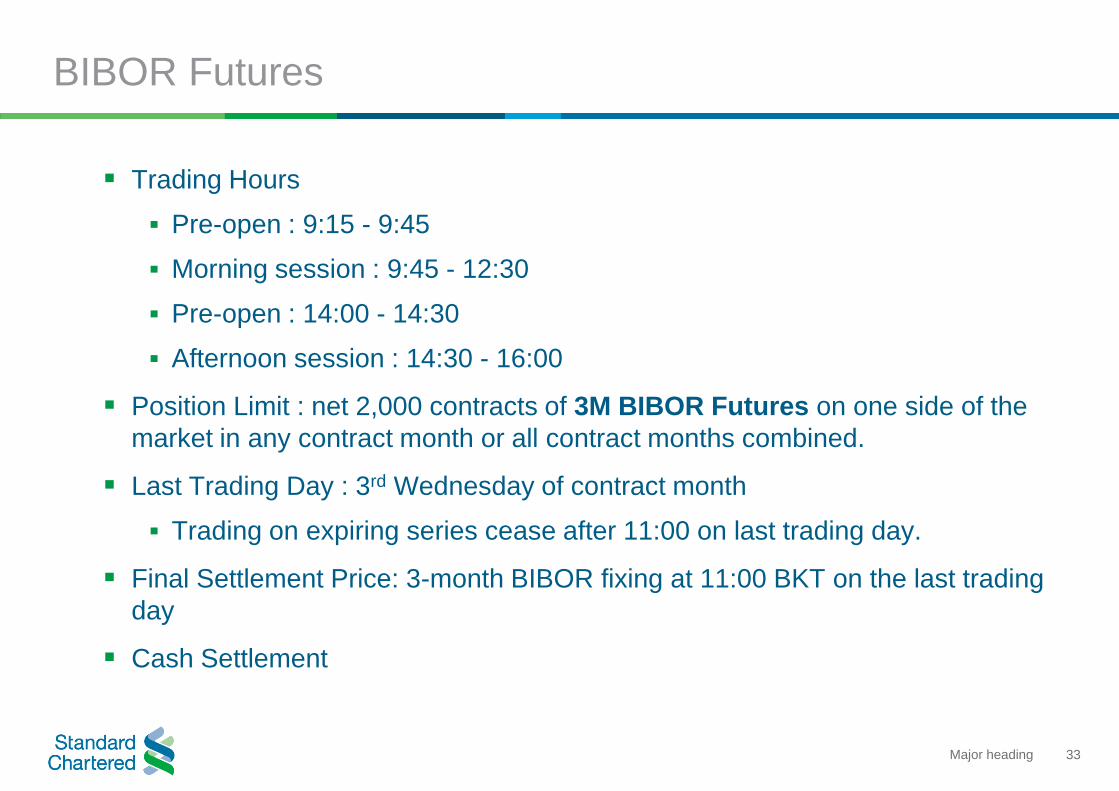

Trading Hours

Pre-open : 9:15 - 9:45

Morning session : 9:45 - 12:30

Pre-open : 14:00 - 14:30

Afternoon session : 14:30 - 16:00

Position Limit : net 2,000 contracts of 3M BIBOR Futures on one side of the

market in any contract month or all contract months combined.

Last Trading Day : 3rd Wednesday of contract month

Trading on expiring series cease after 11:00 on last trading day.

Final Settlement Price: 3-month BIBOR fixing at 11:00 BKT on the last trading

day

Cash Settlement

BIBOR Futures

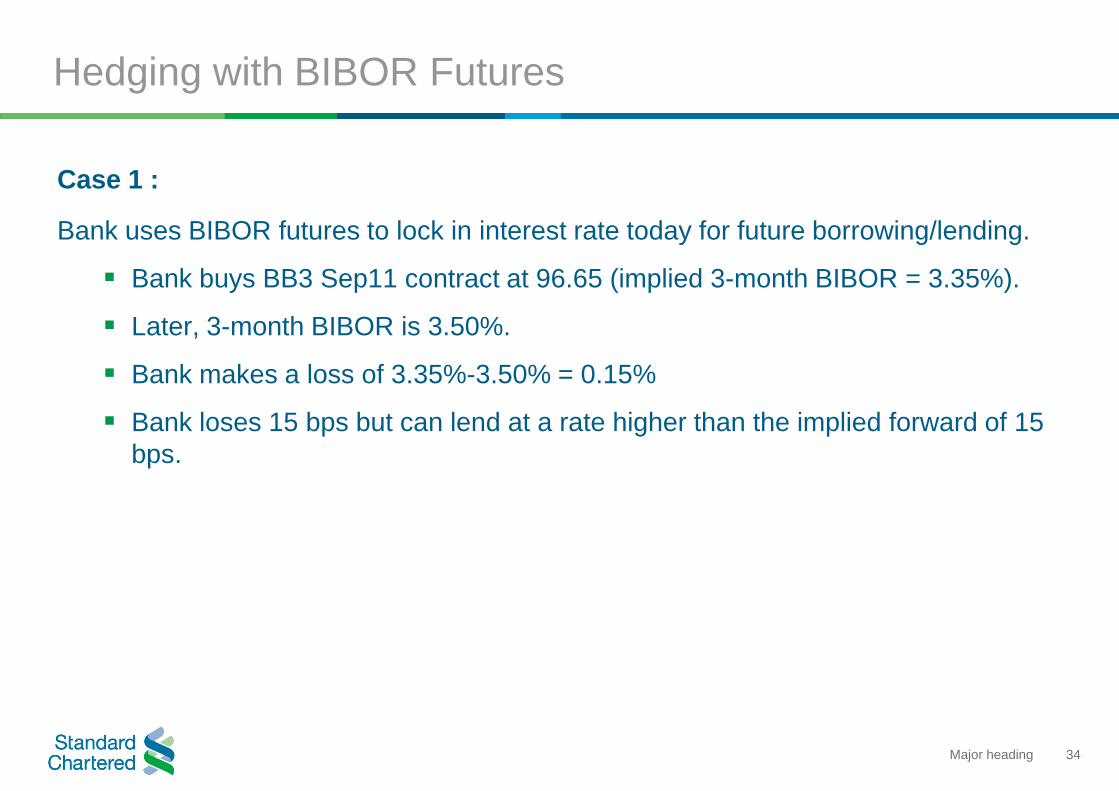

34Major heading

Hedging with BIBOR Futures

Case 1 :

Bank uses BIBOR futures to lock in interest rate today for future borrowing/lending.

Bank buys BB3 Sep11 contract at 96.65 (implied 3-month BIBOR = 3.35%).

Later, 3-month BIBOR is 3.50%.

Bank makes a loss of 3.35%-3.50% = 0.15%

Bank loses 15 bps but can lend at a rate higher than the implied forward of 15

bps.

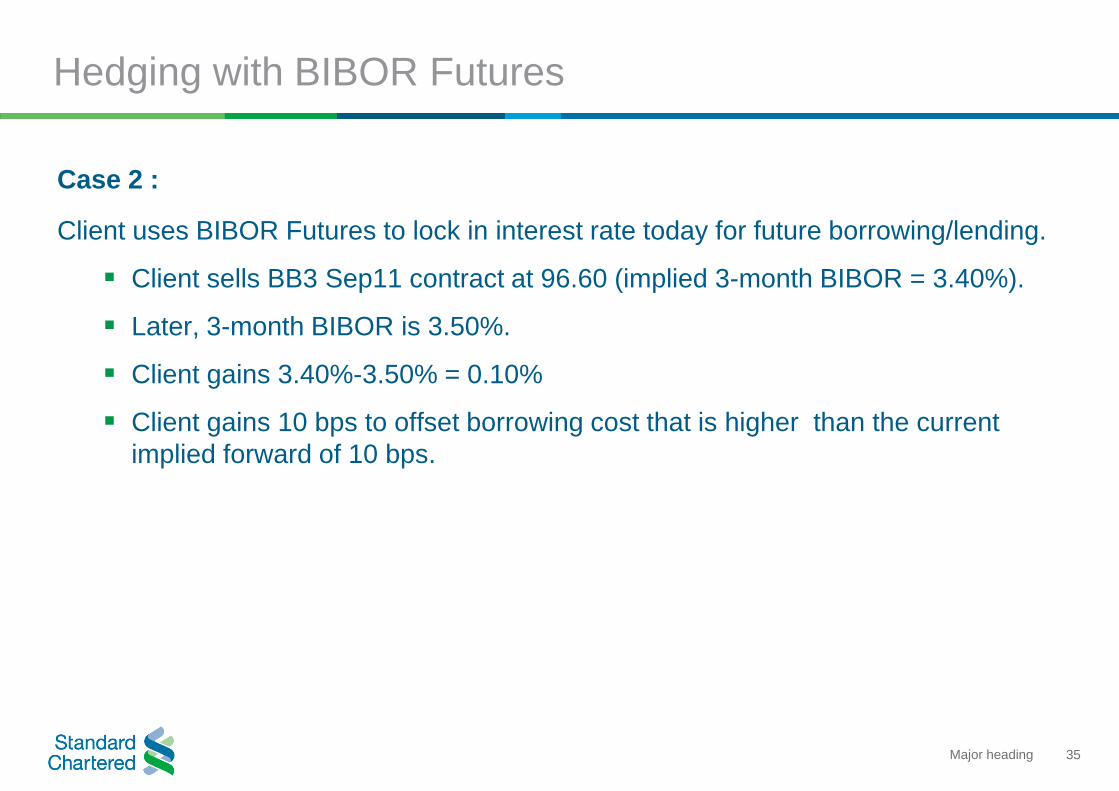

35Major heading

Hedging with BIBOR Futures

Case 2 :

Client uses BIBOR Futures to lock in interest rate today for future borrowing/lending.

Client sells BB3 Sep11 contract at 96.60 (implied 3-month BIBOR = 3.40%).

Later, 3-month BIBOR is 3.50%.

Client gains 3.40%-3.50% = 0.10%

Client gains 10 bps to offset borrowing cost that is higher than the current

implied forward of 10 bps.

36Major heading

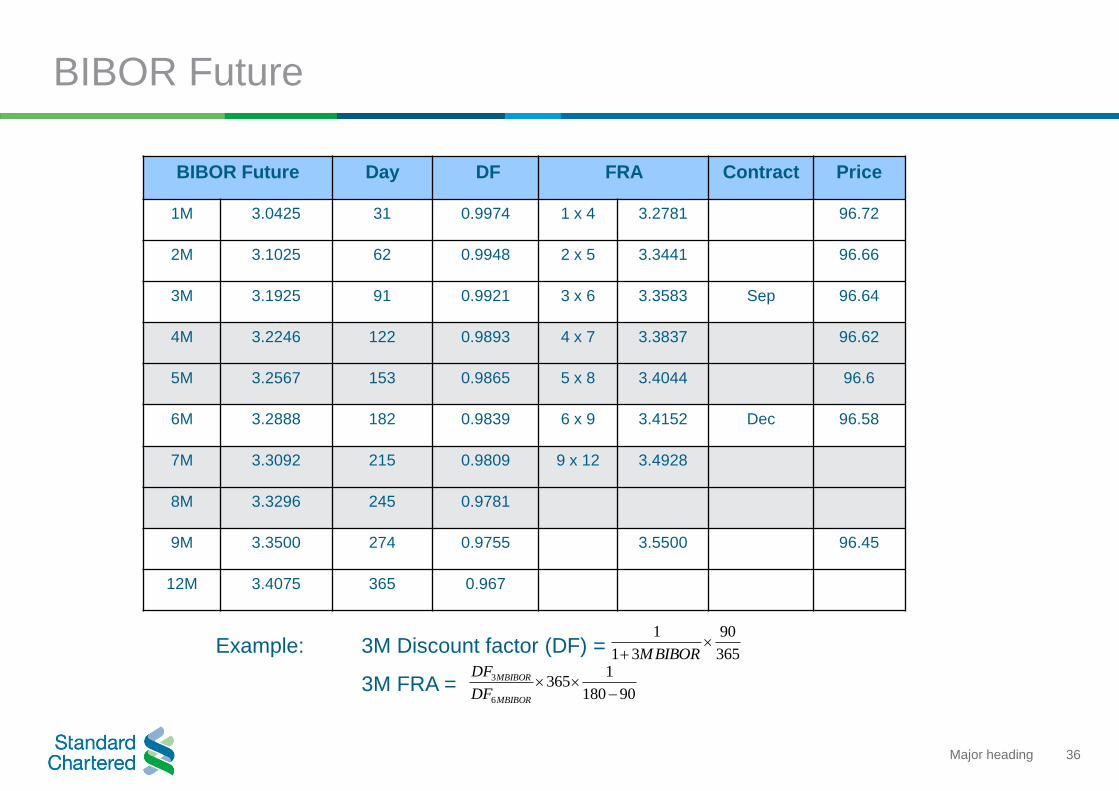

BIBOR Future

BIBOR Future Day DF FRA Contract Price

1M 3.0425 31 0.9974 1 x 4 3.2781 96.72

2M 3.1025 62 0.9948 2 x 5 3.3441 96.66

3M 3.1925 91 0.9921 3 x 6 3.3583 Sep 96.64

4M 3.2246 122 0.9893 4 x 7 3.3837 96.62

5M 3.2567 153 0.9865 5 x 8 3.4044 96.6

6M 3.2888 182 0.9839 6 x 9 3.4152 Dec 96.58

7M 3.3092 215 0.9809 9 x 12 3.4928

8M 3.3296 245 0.9781

9M 3.3500 274 0.9755 3.5500 96.45

12M 3.4075 365 0.967

Example: 3M Discount factor (DF) =

3M FRA =

365

90

31

1

BIBORM

90180

1365

6

3

MBIBOR

MBIBOR

DF

DF

37Major heading

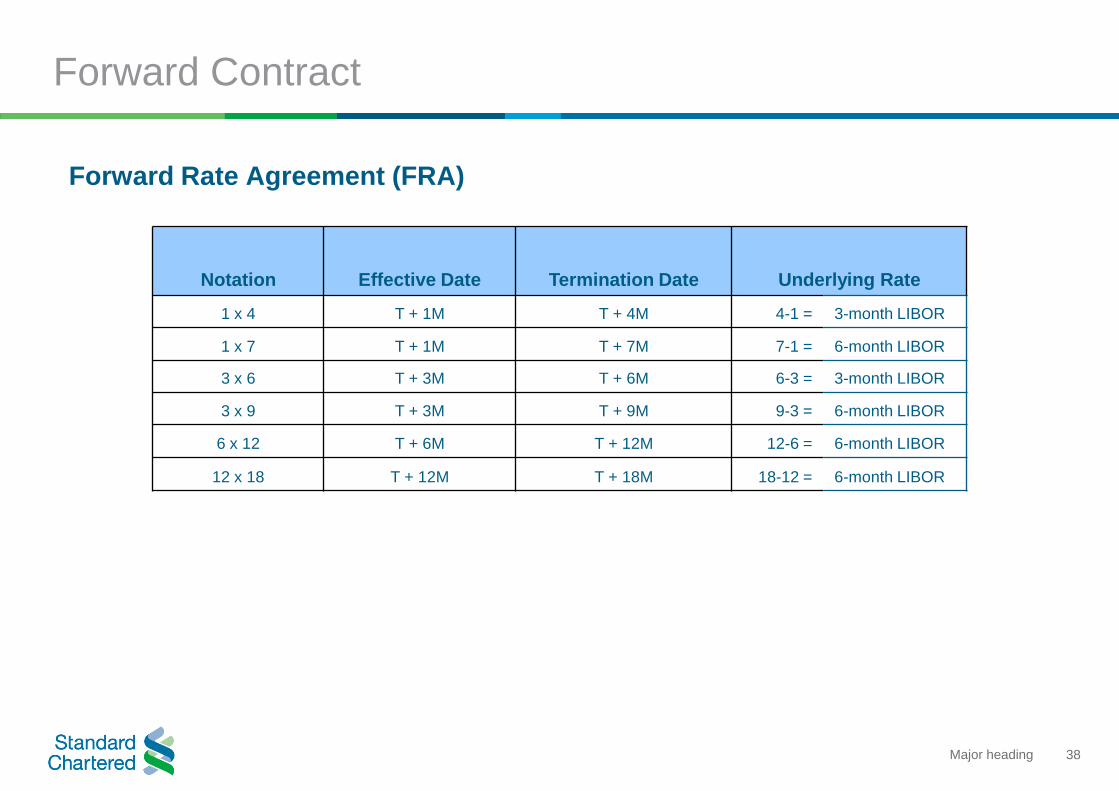

Forward Contract

Forward Rate Agreement (FRA)

Over-the-counter (OTC) forward contract

Specify interest rate and notional amount to be paid or received on an

obligation beginning at a future start date (expiration date).

Similar to futures but with more customized tenor e.g. 1x4, 1x7, 3x6, 3x9,

6x12 and 12x18

38Major heading

Forward Contract

Forward Rate Agreement (FRA)

Notation Effective Date Termination Date Underlying Rate

1 x 4 T + 1M T + 4M 4-1 = 3-month LIBOR

1 x 7 T + 1M T + 7M 7-1 = 6-month LIBOR

3 x 6 T + 3M T + 6M 6-3 = 3-month LIBOR

3 x 9 T + 3M T + 9M 9-3 = 6-month LIBOR

6 x 12 T + 6M T + 12M 12-6 = 6-month LIBOR

12 x 18 T + 12M T + 18M 18-12 = 6-month LIBOR

39Major heading

Q + A

40Major heading

Any other questions, please contact …

Rate Trading Desk

Derivatives : 02-724-8830-31

Teerapol Rattakul (Pom) / Pichanun Aranyanark (Om)

Bonds : 02-724-8820-22

Nopadol Prateepratana (Nop) / Pathamaporn Tankanit (Dew)

Assets and Liabilities Management (ALM) Desk

at 02-724-8825-7 and 724-8953-5

Aramsri Choowongse, CFA (Pui)

Achavaphol Chabchitrchaidol, CFA (Ome)

Wanthicha Kanjanaouthai, CFA (Toey)

Disclaimer

This communication is made by Standard Chartered Bank (Thai) Public Company Limited, a financial institution regulated and supervised by the Bank of Thailand pursuant to

the Financial Institution Business Act B.E. 2551 (AD 2008) ("SCBT"). It is not directed at Retail Clients in the European Economic Area as defined by Directive 2004/39/EC

neither has it been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on

dealing ahead of the dissemination of investment research. It is for information and discussion purposes only and does not constitute either an offer to sell or the solicitation of

an offer to buy any security or any financial instrument or enter into any transaction or recommendation to acquire or dispose of any investment. The information herein may not

be applicable or suitable to the specific investment objectives, financial situation or particular needs of recipients and should not be used in substitution for the exercise of

independent judgment.

Information contained herein, which is subject to change at any time without notice, has been obtained from sources believed to be reliable. While all reasonable care has been

taken in preparing this communication, no responsibility or liability is accepted for any errors of fact, omission or for any opinion expressed herein. SCBT may not have the

necessary licenses to provide services or offer products in all countries or such provision of services or offering of products may be subject to the regulatory requirements of

each jurisdiction and you should check with your relationship manager or usual contact. You are advised to exercise your own independent judgment (with the advice of your

professional advisers as necessary) with respect to the risks and consequences of any matter contained herein. We expressly disclaim any liability and responsibility for any

losses arising from any uses to which this communication is put and for any errors or omissions in this communication.

© Copyright 2010 Standard Chartered Bank (Thai) Public Company Limited. All rights reserved. All copyrights subsisting and arising out of these materials belong to Standard

Chartered Bank (Thai) Public Company Limited and may not be reproduced, distributed, amended, modified, adapted, transmitted in any form, or translated in any way without

the prior written consent of Standard Chartered Bank (Thai) Public Company Limited.