FERS Applying for Immediate Retirement Under the Federal Employees Retirement System Federal Employees Retirement System This pamphlet is for you if you are currently a Federal employee covered by the Federal Employees Retirement System (FERS) and you want to apply for retirement which begins within 30 days after the date of your final separation from Federal service. United States Office of Personnel Management Retirement and insurance Service SF 3113 Revised May 2001 Previous edition is not usable.

Transcript

FERS

Applying forImmediateRetirementUnder the

FederalEmployeesRetirement

System

Federal EmployeesRetirement System

This pamphlet is for you if youare currently a Federal employeecovered by the Federal Employees

Retirement System (FERS) and youwant to apply for retirement which

begins within 30 days after thedate of your final separation from

Federal service.

United States

Office of

Personnel

Management

Retirement

and

insurance

Service

SF 3113Revised May 2001

Previous edition is not usable.

We provide retirement information on theInternet. You will find retirement brochures,forms, and other information at:

This pamphlet, along with form SF 3107, FERSApplication for Immediate Retirement, is for youif you are currently a Federal employee coveredby the Federal Employees Retirement System(FERS), and you want to apply for retirementwith an immediate annuity (annuity beginningwithin 30 days after the date of final separationfrom Federal service). This includes individualswho transferred to FERS from the Civil ServiceRetirement System (CSRS) and who are eligibleto have part of their annuity computed underCSRS rules.

Do not use this pamphlet, or form SF 3107, FERSApplication for Immediate Retirement, if you areapplying for a deferred annuity. A deferred annu-ity begins more than 30 days after the date offinal separation. If you want to apply for adeferred annuity, you should request an RI92-19, FERS Application for Deferred orPostponed Retirement, from the:

U.S. Office of Personnel Management

Federal Employees Retirement System

P.O. Box 200

Boyers, PA 16017-0200.

1

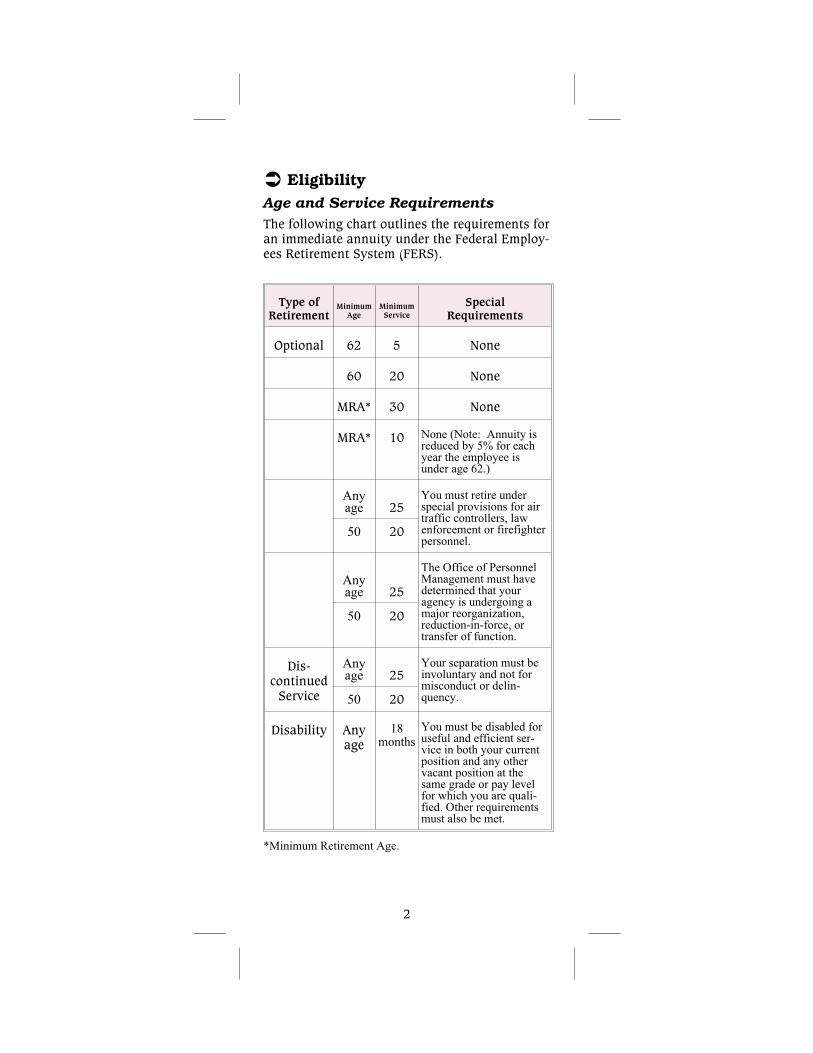

� Eligibility

Age and Service Requirements

The following chart outlines the requirements foran immediate annuity under the Federal Employ-ees Retirement System (FERS).

Type ofRetirement

MinimumAge

MinimumService

SpecialRequirements

Optional 62 5 None

60 20 None

MRA* 30 None

MRA* 10 None (Note: Annuity isreduced by 5% for eachyear the employee isunder age 62.)

Anyage

50

25

20

You must retire underspecial provisions for airtraffic controllers, lawenforcement or firefighterpersonnel.

Anyage

50

25

20

The Office of PersonnelManagement must havedetermined that youragency is undergoing amajor reorganization,reduction-in-force, ortransfer of function.

Dis-continued

Service

Anyage

50

25

20

Your separation must beinvoluntary and not formisconduct or delin-quency.

Disability Anyage

18months

You must be disabled foruseful and efficient ser-vice in both your currentposition and any othervacant position at thesame grade or pay levelfor which you are quali-fied. Other requirementsmust also be met.

*Minimum Retirement Age.

2

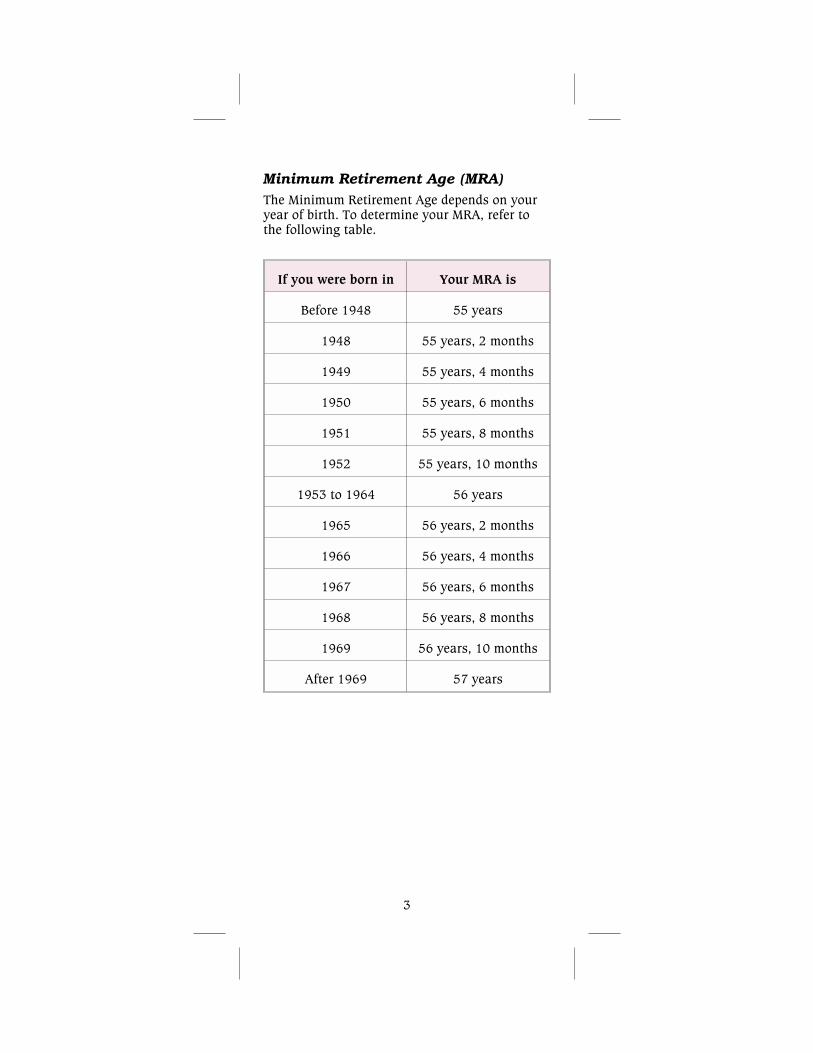

Minimum Retirement Age (MRA)

The Minimum Retirement Age depends on youryear of birth. To determine your MRA, refer tothe following table.

If you were born in Your MRA is

Before 1948 55 years

1948 55 years, 2 months

1949 55 years, 4 months

1950 55 years, 6 months

1951 55 years, 8 months

1952 55 years, 10 months

1953 to 1964 56 years

1965 56 years, 2 months

1966 56 years, 4 months

1967 56 years, 6 months

1968 56 years, 8 months

1969 56 years, 10 months

After 1969 57 years

3

Age Reduction

If you have 10 or more years of service and areretiring at the Minimum Retirement Age, yourannuity will be reduced for each month that youare under age 62. The reduction is 5 percent peryear (5/12 of a percent per month). However,your annuity will not be reduced if you com-pleted at least 30 years of service, or if you com-pleted at least 20 years of service and yourannuity begins when you reach age 60.

You can reduce or eliminate this age reduction,by postponing the beginning date of your annu-ity.

Postponing the Beginning Date ofAnnuity to Reduce or Avoid the AgeReduction

You can reduce or eliminate the age reduction ifyou choose to have your annuity begin at a datelater than your MRA. You can choose any begin-ning date between your MRA and 2 days beforeyour 62nd birthday. However, you cannot beginyour annuity while you are reemployed. Youragency retirement counselor can provide youwith the annuity rates with and without the agereduction. If you decide to postpone the begin-ning date of your annuity, do not complete formSF 3107, FERS Application for Immediate Retire-ment. Write to the Office of Personnel Manage-ment 60 days before the date you want yourannuity to begin and request an RI 92-19, FERSApplication for Deferred or Postponed Retire-ment. The address is:

U.S. Office of Personnel Management

Federal Employees Retirement System

P.O. Box 200

Boyers, PA 16017-0200.

4

If you choose to postpone thebeginning date of your annuity, youshould be aware of the following

Life Insurance

You cannot continue your life insurancecoverage unless you are receiving an annu-ity. Therefore, if you postpone the beginningdate of your annuity, your life insuranceenrollment will terminate. When your annu-ity begins, the life insurance coverage youhad when you separated from your employ-ment will resume.

Health Insurance

If you postpone the beginning date of yourannuity, you will be eligible to temporarilycontinue your health benefits coverage for 18months from the date of separation fromyour employing agency; however, you mustcontact your agency within 60 days and paythe total premium, plus a 2% administrativecharge. When your annuity payments begin,you will again have the opportunity to enrollin a health benefits plan under the regularFederal Employees Health Benefits Program,and the Office of Personnel Management(OPM) will pay the government share of thepremium.

COLA’s

If you delay your annuity beginning date,your annuity rate will not include anycost-of-living adjustments (COLA’s) that occurbefore you begin to receive the annuity. Onceyour annuity begins, you will be entitled toCOLA’s on any portion of your annuity whichwas computed under Civil Service RetirementSystem (CSRS) rules. However, you will notreceive COLA’s on the Federal EmployeesRetirement System (FERS) part of your bene-fit until you are 62.

5

Survivor Benefits

If you defer receipt of your annuity and diebefore you begin to receive it, your spousecan still receive FERS survivor benefits.

� Continuing Health Benefits andLife Insurance Coverage intoRetirement

If you wish to continue your Federal EmployeesHealth Benefits (FEHB) and/or Federal Employ-ees Group Life Insurance (FEGLI) coverage as aretiree, you must meet the following basicrequirements. You must be retiring on an imme-diate annuity and you must have been enrolledin the program for the five years of Federal serv-ice immediately preceding your retirement, or ifless than five years, since your earliest opportu-nity to enroll. FEHB coverage as a family mem-ber counts toward the five-year requirement.Uniform Services Health Benefits Programcoverage also counts provided you are anFEHB enrollee when you retire.

If you are eligible to continue your FEHB cover-age, your agency will automatically transferyour enrollment to the Office of Personnel Man-agement (OPM). You do not need to do anythingunless you want to make some change in yourcoverage.

The pamphlet, RI 76-21, FEGLI Federal Employ-ees Group Life Insurance Program, has moreinformation about eligibility to continue yourFEGLI coverage as a retiree and the cost of cover-age. If you are eligible to continue your FEGLIbasic coverage, you must complete an SF 2818,Election of Post-Retirement Basic Life InsuranceCoverage. Any optional FEGLI coverage you haveand are eligible to retain as a retiree will auto-matically be continued unless you make somechange. Our experience has been that many peo-ple cancel all or a portion of their life insurancecoverage at retirement due to its cost. Therefore,you should let OPM know at retirement, if you donot want to continue a portion of your life insur-ance coverage. You may also want to file an

6

SF 2823, FEGLI Designation of Beneficiary form.(The designation of beneficiary form for yourFERS retirement contributions and any lumpsum of accrued annuity is SF 3102.)

Based on the documentation your employingagency is required to submit with your retire-ment application, OPM will determine whetheryou are eligible to continue your health and lifeinsurance coverage as a retiree. However, if youhave any questions about your eligibility, askyour employing office for assistance before youretire.

� Applying for Benefits

Form to Use

Use form SF 3107, FERS Application for Imme-diate Retirement, to apply for immediate retire-ment. You can obtain the form from youremploying agency.

Submitting the Application

Submit the completed application to youremploying agency. Give your agency at least 60days notice before the date you intend to retire.Your agency will then complete the Schedule D,Agency Checklist of Immediate Retirement Proce-dures and the SF 3107-1, Certified Summary ofFederal Service, which are included in theSF 3107, FERS Application for ImmediateRetirement.

Your agency will complete the SF 3107-1, Certi-fied Summary of Federal Service, and forward itto you for your review and signature. You shouldreview it carefully before signing it. Any errors,omissions, or discrepancies will delay the proc-essing of your application, and may result inincomplete credit for service in the initial com-putation of your annuity.

If you are applying for disability retirement, askyour employing agency for a copy of the formspackage SF 3112, Documentation in Support ofDisability Retirement Application.

Your agency will forward the application to OPM.

7

What to do if your Address Changes BeforeProcessing is Complete

If your address changes before you receive yourclaim number, write to us, giving your name,date of birth, and your social security number. Ifyou have received your claim number you caneither telephone us or write to us to report yournew address. Please refer to your claim numberin any correspondence. You can phone us at1-888-767-6738. Customers within local callingdistance to Washington, DC must contact us on202-606-0500. If you prefer to write to us, youshould report your new address to:

U.S. Office of Personnel Management

ATTN: Change of Address

P.O. Box 440

Boyers, PA 16017-0440

In addition, notify your old post office of yourforwarding address.

What Happens After You File Your RetirementApplication

Your employing office will close out your rec-ords, using the Agency Checklist to assure thatall necessary steps are taken. When this process(which includes paying you any unpaid com-pensation, such as for unpaid annual leave) hasbeen completed, the agency will forward yourapplication and records to the Office of PersonnelManagement (OPM). You should receive a noticefrom your former employing agency when yourapplication and records have been forwarded toOPM. In most cases, the agency should forwardthe retirement package to OPM so it is receivedwithin 30 days after your separation. Until OPMhas received the application and supportingdocuments, OPM does not know that you haveretired.

Note: Applications for disability retirement areprocessed differently. Your agency normally willforward your application, evidence supportingyour claim of disability and preliminary records,to OPM for a disability determination based on a

8

review of both medical and non-medical evi-dence.

After it receives your application, OPM willassign your claim number, which will begin withthe letters “CSA.” This number will be veryimportant to you as a retiree because you willneed to refer to it any time you write or call OPMin connection with your annuity.

When we finish processing your application, wewill send you a statement explaining your bene-fits. We will also send you a pamphlet calledInformation for FERS Annuitants, RI 90-8, whichcontains information you will need after youretire, including how to contact OPM to makevarious changes (tax withholding, address,health benefits, etc.), the effect of other benefits(Social Security, Office of Workers’ Compensa-tion Program [OWCP]) on your Federal Employ-ees Retirement System (FERS) benefit, the effectof reemployment on your FERS benefit and bene-fits payable upon your death.

� Payments

Beginning Date of Annuity

The beginning date of most annuities is the firstday of the month after separation. However, dis-ability annuities and annuities based on militaryreserve technician provisions begin no later thanthe day after pay stops and all other require-ments for title to annuity are met. Annuitiesbased on involuntary separations begin on theday after separation.

Payment and Accrual of Annuity

All annuities are payable in monthly install-ments on the first business day of the monthfollowing the one for which the annuity hasaccrued. For example, payments for the month ofJune will be paid in your check dated July 1.

9

How to Have Annuity Payments Sentto a Bank or Financial Institution

Public Law 104-134 requires that most Federalpayments be paid by Direct Deposit through Elec-tronic Funds Transfer (EFT) into a savings orchecking account at a financial institution. How-ever, if receiving your payment electronicallywould cause you a financial hardship, or a hard-ship because you have a disability, or because ofa geographic, language or literacy barrier, youmay invoke your legal right to a waiver of theDirect Deposit requirement, and continue toreceive your payment by check.

Direct deposit is a win-win situation all around.You avoid the bother of traveling to a bank orother financial institution to cash or deposit yourcheck. You may earn a few days extra interesteach month, and save travel costs and time. Bothyou and the Office of Personnel Management(OPM) are saved the worry that checks will belost in the mail. It also assures that paymentsare deposited and available for your use, evenwhen you are away from home.

When you elect direct deposit, you will continueto receive other information at your mailingaddress. Complete Section H of SF 3107, FERSApplication for Immediate Retirement, to haveyour payments sent to a financial institution orto request a waiver of the direct deposit require-ment. If you change to this option or changeaccounts after your payments begin, you shouldcall us at 1-888-767-6738. Customers withinlocal calling distance to Washington, DC mustcontact us on 202-606-0500. If you prefer, youcan send form SF 1199A, Direct Deposit Sign-UpForm, to OPM. You can obtain the form whereyou bank. Both you and your bank need to com-plete the form. Include your claim number on theform. It’s a good idea to leave your old accountopen until you have verified that a payment hasbeen deposited in your new one.

10

Federal Income Tax Withholding

If we do not receive a W-4 form from you indicat-ing the rate at which (or a specific dollaramount) you want federal income tax withheld,tax will be withheld from your annuity at therate for a married person with 3 exemptions. Ifyou want to have the tax withheld at the ratecurrently being withheld from your salary,attach a copy of the W-4 form on file with youremploying agency, to your application for retire-ment. If you do not want federal income taxwithheld from your annuity payments, indicatethis in Section H of SF 3107, Application forImmediate Retirement.

� Survivor Benefits

Married Applicants

The maximum survivor benefit available is 50%of your unreduced annuity. Your annuity isreduced by 10% to provide this benefit. If you aremarried when your annuity begins, it will becomputed with a reduction to provide maximumsurvivor benefits for your spouse upon yourdeath. You can elect to provide a partial survivorbenefit (25% of your unreduced annuity, with a5% reduction in your annuity) or no survivorbenefits; however, you must get your spouse’sconsent to elect either of these options.SF 3107-2, Spouse’s Consent to Survivor Elec-tion, which is part of form SF 3107, FERS Appli-cation for Immediate Retirement, must becompleted by your spouse and forwarded to theOffice of Personnel Management (OPM) alongwith your application for retirement.

If your spouse is covered under your FederalEmployees Health Benefits plan and you do notelect survivor benefits for your spouse, yourspouse will not be eligible to continue this healthbenefits coverage after your death.

Waiving the Spousal Consent Requirement

OPM may waive the spousal consent requirementif you show that your spouse’s whereabouts can-not be determined. A request for waiver on thisbasis must be accompanied by:

11

� a judicial determination that your spouse’swhereabouts cannot be determined; or

� affidavits by you and two other persons, atleast one of whom is not related to you,attesting to the inability to locate the cur-rent spouse and stating the efforts made tolocate the spouse. You must also give doc-umentary evidence, such as tax returns filedseparately, or newspaper stories, about thespouse’s disappearance.

The Office of Personnel Management (OPM) mayalso waive the spousal consent requirement ifyou present a judicial determination regardingthe current spouse that would warrant waiver ofthe consent requirement based on exceptionalcircumstances. (Illness or injury of the retiringemployee is not justification for waiving thespousal consent requirement.)

Electing a Survivor Annuity for a FormerSpouse

To elect a survivor annuity for a former spouse,you must have been married to the person for atotal of at least 9 months. A former spouse whoremarries before reaching age 55 is not eligiblefor a former spouse survivor annuity.

You may elect to provide a survivor annuity formore than one former spouse. The total of thesurvivor annuities must equal either 25% or 50%of your unreduced annuity. Also, if you are mar-ried, you must have your spouse’s consent tochoose this option, because any benefit electedfor a former spouse limits what can be electedfor your current spouse. The maximum combinedsurvivor benefits that can be elected for your cur-rent and former spouse(s) is 50% of your benefit.

Electing a Survivor Annuity for a CurrentSpouse When a Court Order Gives aSurvivor Annuity to a Former Spouse

If a court order has given a survivor annuity to aformer spouse, you still may make your electionconcerning a survivor annuity for your current

12

spouse as if there were no court-ordered formerspouse annuity. By electing survivor benefits foryour current spouse at retirement, you can pro-tect your spouse’s rights in case your formerspouse loses entitlement in the future (becauseof remarriage before age 55, death, or under theterms of the court order). Another option thatyou should consider is outlined on page 14under “Electing an Insurable Interest Annuity fora Current Spouse When a Court Order Gives aSurvivor Annuity to a Former Spouse.” The fol-lowing paragraphs explain in more detail howyour election at the time of retirement can affectyour current spouse’s future rights if the courthas given a survivor annuity to a former spouse.

If a court order gives a survivor annuity to aformer spouse, your annuity will be reduced toprovide it. If you elect a survivor annuity foryour current spouse (or another former spouse),your annuity will be reduced no more than itwould be to provide a survivor annuity equal to50% of your unreduced annuity. Your currentspouse will be eligible for any portion of thebenefit not ordered for the former spouse.

If you die before your current and formerspouses, the total amount of the survivor annui-ties paid cannot exceed 50% of your annuity andthe Office of Personnel Management (OPM) musthonor the terms of the court order before it canhonor your election. The former spouse havingthe court-ordered survivor benefit would receivean annuity according to the terms of the courtorder. If the court order gives the entire survivorannuity to the former spouse, your widow(er)would receive no survivor annuity until the for-mer spouse loses entitlement. Then your wid-ow(er) would receive a survivor annuity accord-ing to your election. If the court order gives lessthan the entire survivor annuity to the formerspouse, your widow(er) would receive an annuityno greater than the difference between the court-ordered survivor annuity and 50% of your annu-ity. However, if the former spouse loses entitle-ment to the survivor annuity (through remar-riage before age 55, death, or under the terms ofthe court order), your widow(er) would thenreceive the survivor annuity you elected.

13

For example, if there is a court-ordered formerspouse survivor annuity that equals 40% of yourannuity, you elect a maximum survivor annuityfor your current spouse, and you die before theformer spouse’s entitlement to a survivor annu-ity ends, the former spouse would receive a sur-vivor annuity equal to 40% of your annuity andyour widow(er) would receive a survivor annuityequal to 10% of your annuity. However, if theformer spouse later loses entitlement to the sur-vivor annuity, your widow(er) would then receivea survivor annuity equal to 50% of your annuity.

Electing an Insurable Interest Annuity fora Current Spouse When a Court OrderGives a Survivor Annuity to a FormerSpouse

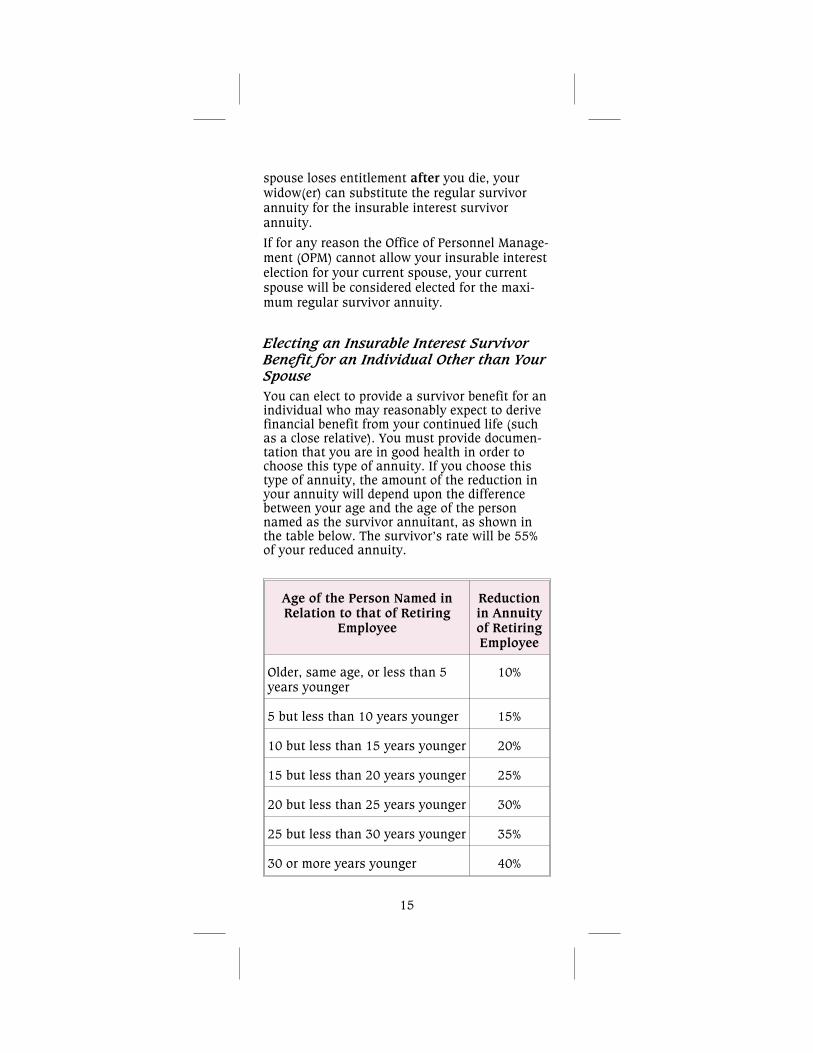

If a former spouse’s court-ordered survivor annu-ity will prevent your current spouse from receiv-ing a survivor annuity that is sufficient to meethis or her anticipated needs, you may want toelect an insurable interest annuity for yourspouse. You must provide documentation thatyou are in good health in order to choose thisbenefit. The amount of the benefit and theamount of the reduction in your annuity to pro-vide it are explained on page 15 in “Electing anInsurable Interest Survivor Benefit for an Indi-vidual Other Than Your Spouse”.

If you elect an insurable interest survivor annu-ity for your current spouse, your current spousemust sign form SF 3107-2, Spouse’s Consent toSurvivor Election, which is part of SF 3107,FERS Application for Immediate Retirement, con-senting to receive the insurable interest annuityinstead of a regular survivor annuity. (Chooseitem a. in Part 1 of the SF 3107-2).

If you elect an insurable interest survivor annu-ity for your current spouse and your formerspouse loses entitlement before you die, youmay request that the reduction in your annuityto provide the insurable interest annuity be con-verted to the regular survivor annuity reduction.Your current spouse would then be entitled tothe regular survivor annuity. If your former

14

spouse loses entitlement after you die, yourwidow(er) can substitute the regular survivorannuity for the insurable interest survivorannuity.

If for any reason the Office of Personnel Manage-ment (OPM) cannot allow your insurable interestelection for your current spouse, your currentspouse will be considered elected for the maxi-mum regular survivor annuity.

Electing an Insurable Interest SurvivorBenefit for an Individual Other than YourSpouse

You can elect to provide a survivor benefit for anindividual who may reasonably expect to derivefinancial benefit from your continued life (suchas a close relative). You must provide documen-tation that you are in good health in order tochoose this type of annuity. If you choose thistype of annuity, the amount of the reduction inyour annuity will depend upon the differencebetween your age and the age of the personnamed as the survivor annuitant, as shown inthe table below. The survivor’s rate will be 55%of your reduced annuity.

Age of the Person Named inRelation to that of Retiring

Employee

Reductionin Annuityof RetiringEmployee

Older, same age, or less than 5years younger

10%

5 but less than 10 years younger 15%

10 but less than 15 years younger 20%

15 but less than 20 years younger 25%

20 but less than 25 years younger 30%

25 but less than 30 years younger 35%

30 or more years younger 40%

15

You can elect this insurable interest survivorannuity in addition to a regular survivor annuityfor a current or former spouse.

Termination of the reduction in yourannuity to provide a survivor benefit

Current Spouse

The reduction in your annuity to provide a sur-vivor annuity for your current spouse stops ifyour marriage ends because of death, divorce, orannulment.

Former Spouse

The reduction in your annuity to provide a sur-vivor annuity for a former spouse ends if the for-mer spouse dies, if the former spouse remarriesbefore reaching age 55, or under the terms of thecourt order that required you to provide the sur-vivor annuity for the former spouse when youretired. (Modifications to the court order issuedafter you retire do not affect the former spousesurvivor annuity.)

Insurable Interest

The reduction in your annuity to provide aninsurable interest annuity ends if the person youname to receive the insurable interest annuitydies or if the person you name is your currentspouse and you change your election because aformer spouse has lost entitlement to a survivorannuity. The reduction also ends if, after youretire, you marry the insurable interest benefici-ary and elect to provide a spousal survivor annu-ity for that person. If you marry someone otherthan the insurable interest beneficiary after youretire and elect to provide a survivor annuity foryour spouse, you may elect to cancel the insur-able interest reduction at that time.

16

Changing the Survivor Election AfterRetirement

If it is within 30 days of your first regularannuity payment

You may change your election if, not later than30 days after the date of your first regularmonthly payment, you file a new election in writ-ing. You should write to:

U.S. Office of Personnel Management

Federal Employees Retirement System

P.O. Box 200

Boyers, PA 16017-0200.

Your first regular monthly payment is the firstannuity check payable on a recurring basis(other than an estimated payment or an adjust-ment check) after the Office of Personnel Man-agement (OPM) has computed the regular rate ofannuity payable under the Federal EmployeesRetirement System (FERS) and has paid the firstregular annuity amount.

When the 30-day period following the date ofyour first regular monthly payment has passed,you cannot change your election, except underthe circumstances explained in the followingparagraphs.

If it is more than 30 days from the date ofyour first regular monthly payment, butless than 18-months from the beginningdate of your annuity

If you are married at retirement, you may changeyour decision not to provide a survivor annuity,or you may increase the survivor annuityamount. You must request the change in writingno later than 18 months after the beginning dateof your annuity.

In addition, you must pay a deposit representingthe difference between the reduction for the newsurvivor election and the original survivor elec-tion, plus a percentage of your annual annuity.This percentage is 24.5% of your annual annuity(at retirement) if you are changing from no sur-vivor benefit to a full survivor benefit, and

17

12.25% if you are changing from none to a par-tial benefit or from a partial benefit to a fullbenefit. Interest on the deposit must also bepaid.

Electing Survivor Benefits for a SpouseAcquired After Retirement

If you get married after retirement, you can electa reduced annuity to provide a survivor annuityfor your spouse, if you contact the Office of Per-sonnel Management (OPM) to request the benefitwithin two years of the date of the marriage. Youmay elect either a full survivor annuity (50% ofyour unreduced annuity) or a partial survivorannuity (25% of your unreduced annuity). If youremarry the same person you were married to atretirement and that person consented to eitherno survivor annuity or a partial survivor annu-ity, you cannot elect a survivor annuity greaterthan the amount provided in your original elec-tion.

There will be two reductions in your annuity ifyou elect to provide the survivor benefit. One willbe the reduction to provide the survivor benefit.The amount of the reduction depends on whetheryou have elected to provide a full survivor annu-ity (10% reduction) or a partial survivor annuity(5% reduction). The reduction to provide the sur-vivor benefit will be eliminated if your marriageends.

The other reduction in your annuity is a perma-nent actuarial reduction to pay the survivorbenefit deposit. The deposit equals the differencebetween the new annuity rate and the annuitypaid to you for each month since retirement, plus6% interest. The reduction is determined bydividing the amount of the deposit by an actu-arial factor for your age on the date your annu-ity is reduced to provide the survivor benefit. Theactuarial reduction will not be eliminated fromyour annuity if your marriage ends.

18

Notes

19

Retirement & Insurance Service

Serving over 10 million customers, Federal employees,