Approaches to lift sectoral mitigation potential with markets in transition DEHSt Side Event 2 nd of December 2014, Lima, Peru Carsten Warnecke Hanna Fekete [email protected][email protected]

Transcript

Approaches to lift sectoralmitigation potential with markets in transitionDEHSt Side Event

Non-profit research institute founded Nov. 2014 by 7 former Ecofys colleagues

Offices in Berlin and Cologne (Germany)

Areas of expertise Climate negotiationsTracking climate action Climate and development Climate financingCarbon market mechanisms

2www.newclimate.org02/12/2014

Background

Insights from DEHSt research project

Bilateral Agreements as Basis Towards Piloting SectoralMarket Mechanisms

Duration: Sept 2012 – Aug 2015

Activity gap in market-based mechanisms challenges maintaining the expertise of stakeholders and testing of new approaches in practice

Demand for „reduction units“ could be created based on bilateral agreements between Parties

Theoretically, the EU ETS with article 11a (5),(6) considers bilateral agreements

02/12/2014 www.newclimate.org 3

Objectives

Theoretic research to develop approaches based on a bilateral crediting system that allows pilot activitiesPilot activities shall have a

sectoral coverage based on benchmarkshigh level of environmental integritygenerate net emission reductions

Open to further ETS and regional markets to join the initiativeResearch shall

Identify suitable countries and sectors for piloting Develop initial sector approaches including proposals for benchmark conceptsElaborate recommendations for the design of such bilateral agreements

02/12/2014 www.newclimate.org 4

Country Selection methodology

First part

02/12/2014 www.newclimate.org 5

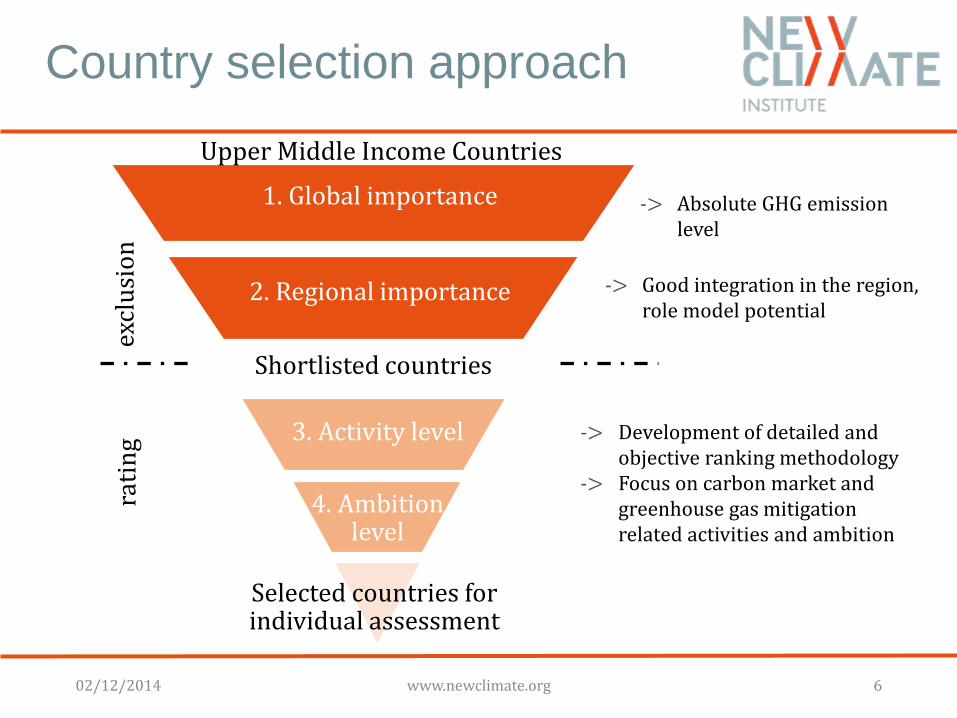

Country selection approach

1. Global importance

2. Regional importance

Upper Middle Income Countries

3. Activity level

4. Ambition level

Selected countries for individual assessment

rati

ng

excl

usi

on

Shortlisted countries

-> Absolute GHG emissionlevel

-> Good integration in the region,role model potential

-> Development of detailed and objective ranking methodology

-> Focus on carbon market and greenhouse gas mitigation related activities and ambition

02/12/2014 www.newclimate.org 6

Criteria for ranking

Indicators for criterion “level of activity”:

Participation in the Clean Development Mechanisms

Activities under the Partnership for Market Readiness (PMR) of the World Bank

Activities around Nationally Appropriate Mitigation Actions (NAMAs)

Activities around Monitoring, Reporting and Verification (MRV) of greenhouse gases;

further described with the following sub-indicators:

o Submission of National Communications to the UNFCCC; existence of greenhouse gas

inventories

o Activities under the Global Environment Facility (GEF) and the MRV partnership

Indicators for criterion “level of ambition”:

Emission reduction pledges on an international level

Further targets: National energy efficiency or renewable targets

Engagement in Low Emission Development Strategies (LEDS)

Participation in regional or global networks

02/12/2014 www.newclimate.org 7

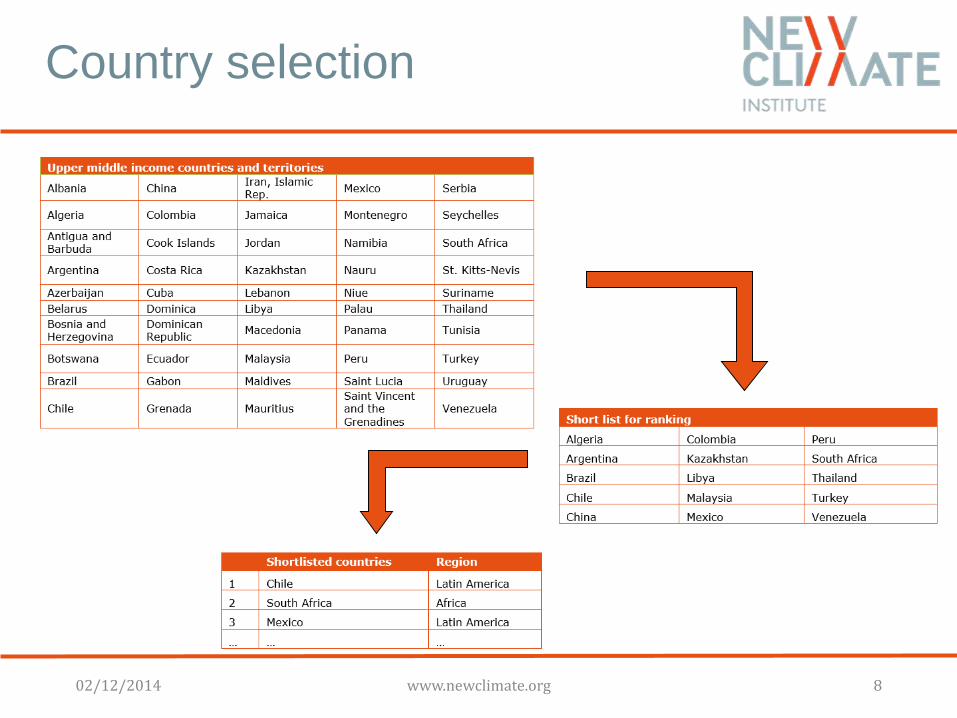

Country selection

02/12/2014 www.newclimate.org 8

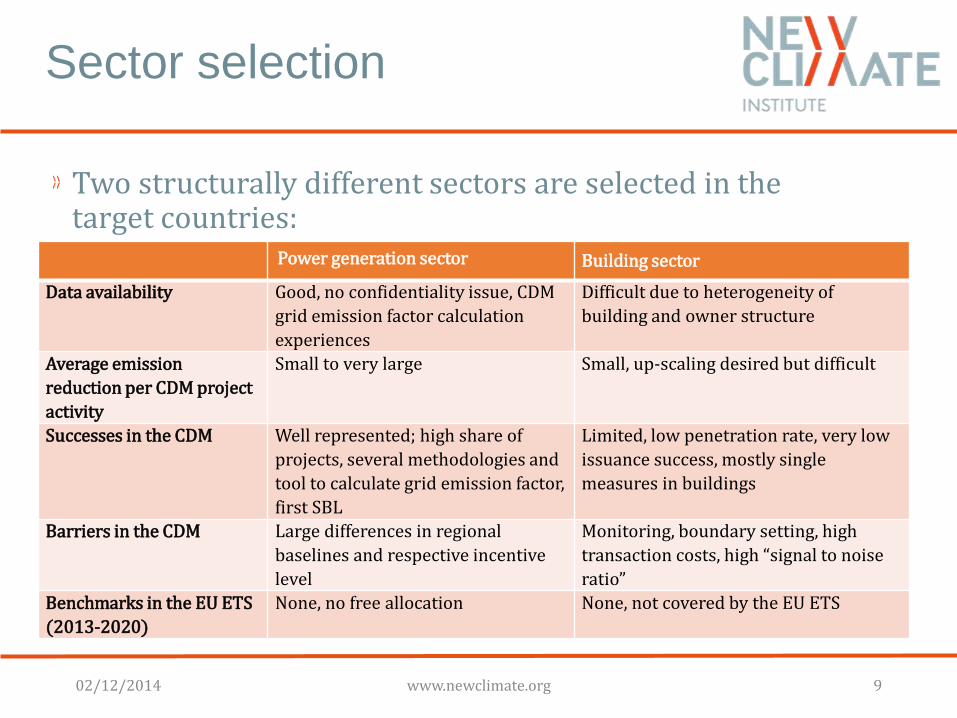

Sector selection

Two structurally different sectors are selected in the target countries:

Power generation sector Building sector

Data availability Good, no confidentiality issue, CDM

grid emission factor calculation

experiences

Difficult due to heterogeneity of

building and owner structure

Average emission

reduction per CDM project

activity

Small to very large Small, up-scaling desired but difficult

Successes in the CDM Well represented; high share of

projects, several methodologies and

tool to calculate grid emission factor,

first SBL

Limited, low penetration rate, very low

issuance success, mostly single

measures in buildings

Barriers in the CDM Large differences in regional

baselines and respective incentive

level

Monitoring, boundary setting, high

transaction costs, high “signal to noise

ratio”

Benchmarks in the EU ETS

(2013-2020)

None, no free allocation None, not covered by the EU ETS

02/12/2014 www.newclimate.org 9

Concepts for credited reference levels based on benchmarks

Second part

02/12/2014 www.newclimate.org 10

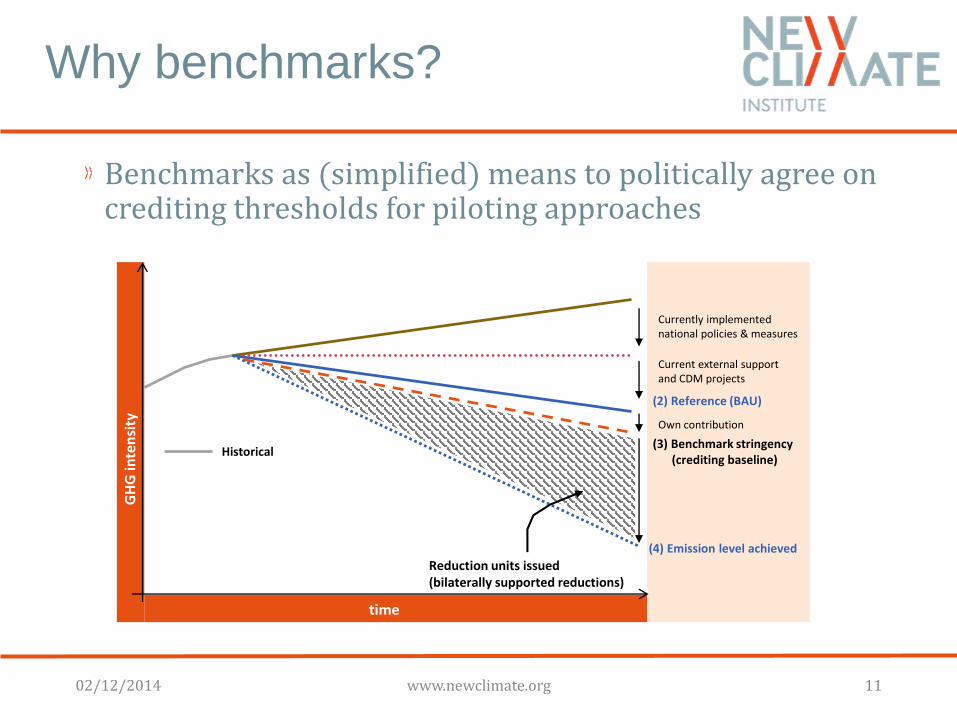

Why benchmarks?

Benchmarks as (simplified) means to politically agree on crediting thresholds for piloting approaches

GH

G in

ten

sity

time

Historical

Reduction units issued(bilaterally supported reductions)

Currently implemented national policies & measures

(2) Reference (BAU)

Own contribution

(3) Benchmark stringency (crediting baseline)

(4) Emission level achieved

Current external support and CDM projects

02/12/2014 www.newclimate.org 11

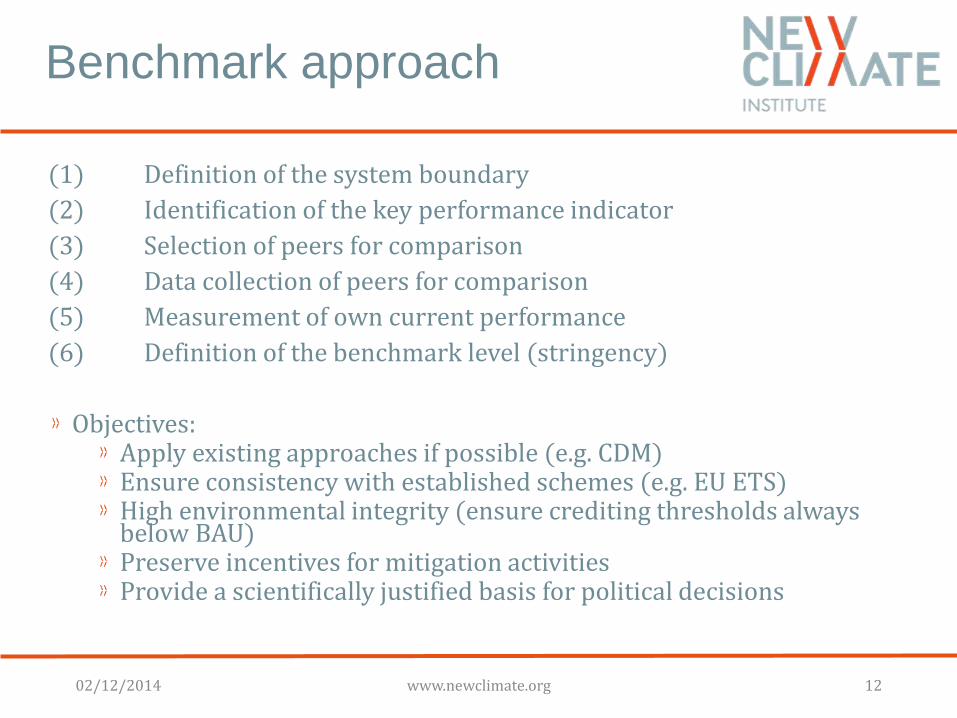

Benchmark approach

(1) Definition of the system boundary

(2) Identification of the key performance indicator

(3) Selection of peers for comparison

(4) Data collection of peers for comparison

(5) Measurement of own current performance

(6) Definition of the benchmark level (stringency)

Objectives:Apply existing approaches if possible (e.g. CDM)Ensure consistency with established schemes (e.g. EU ETS)High environmental integrity (ensure crediting thresholds always below BAU)Preserve incentives for mitigation activitiesProvide a scientifically justified basis for political decisions

02/12/2014 www.newclimate.org 12

Chile‘s power generation sector

Almost 1/3 of the GHG emissions stem from electricity and heat generation

Electricity generation dominated bygas and hydro power plants

Future capacity additions likely based on coal

Vast potential for renewable energy

Chile requires large electricity companies to have a share of at least 5% of renewable energy; increasing by 0.5ppts annually

Chile is developing plans for a domestic ETS under the PMR

Chile’s renewable energy NAMA is one of the first NAMAs to receive international finance

02/12/2014 www.newclimate.org 13

Benchmark concept

CDM is a valuable framework with application potential

CDM has addressed most of the identified sector challenges and describes solutions being a consensus for many stakeholders

The benchmark proposal follows the CDM to the extent possible but require a few modifications to increase pragmatism, ambition and suitability for sector coverage, e.g.

Geographic scope of the benchmarkExistence of a grid connectionExclusion of low-cost/must-run power unitsStringency levels beyond pure offsetting

02/12/2014 www.newclimate.org 14

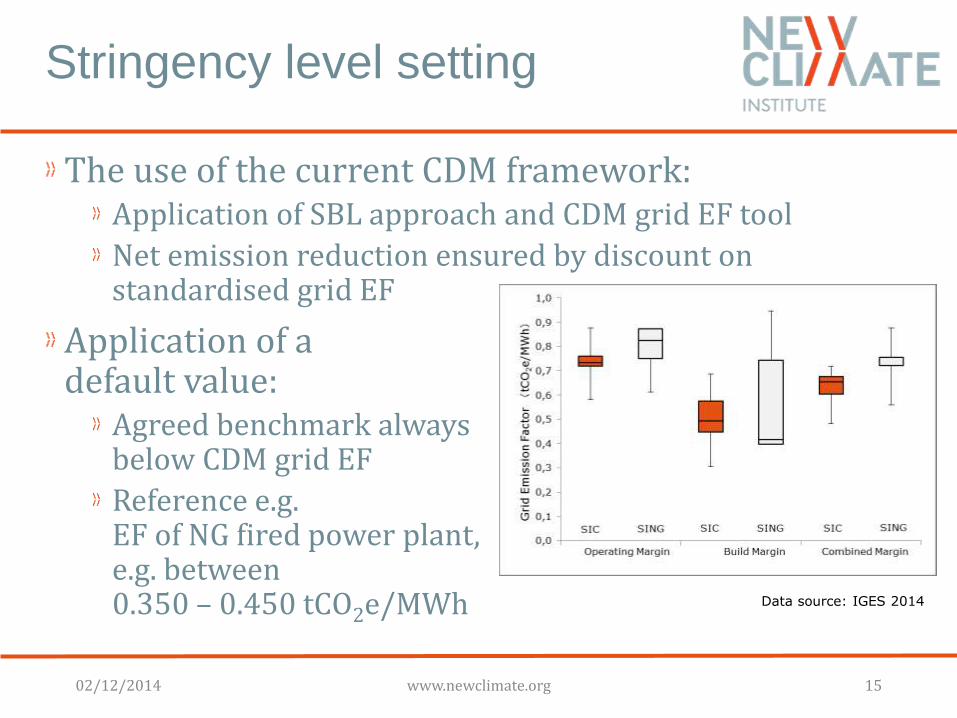

Stringency level setting

The use of the current CDM framework:Application of SBL approach and CDM grid EF tool

Net emission reduction ensured by discount on standardised grid EF

Application of a default value:

Agreed benchmark alwaysbelow CDM grid EF

Reference e.g. EF of NG fired power plant,e.g. between0.350 – 0.450 tCO2e/MWh Data source: IGES 2014

02/12/2014 www.newclimate.org 15

Stringency level setting

Hybrid approach:Combination of approaches

RE by default get reduction units according to default BM value while fossil fuel based activities apply for BM based on the (adapted) CDM approach

Incentives also for new NG fired power plants and for efficiency increase in existing fossil fuel fired power plants

02/12/2014 www.newclimate.org 16

CDM in the building sector

CDM projects mostly refer to single measures in buildingsCDM application in its current form to entire buildings lags behind its enormous potentialLow “signal to noise” ratio, high complexityMost available methodologies are either too specific or do not provide practicable solutions to sector challengesCDM experiences show the need for

Pragmatic MRV approachesValuation of indirect and long term effectsBundling of less homogeneous single activities to facilitate reaching a large coverage

02/12/2014 www.newclimate.org 17

South Africa‘s building sector

Large demand for low cost buildings to supply the growing population with adequate housing facilitiesGovernment targets for new buildingsLow income housing segment provides free housing to poorest parts of the populationLow income houses usually constructed in a standard way, resulting in a large number of similar homes

Focus on sector sub-segment: „low income housing“Lessons learned with the use of the CDM and upscaling approaches exist

02/12/2014 www.newclimate.org 18

Benchmark concept

Suggestion: Overcome existing barriers by using pragmatic approaches, deviating from exact GHG quantification

GHG emissions per standard housing unitEx-ante modeling (default/unit)Simplified ex-post MRV

The increase in uncertainty is levelled out by ambitious crediting thresholds or conservative BAU definitions

Transaction costs are reduced

02/12/2014 www.newclimate.org 19

Stringency level setting

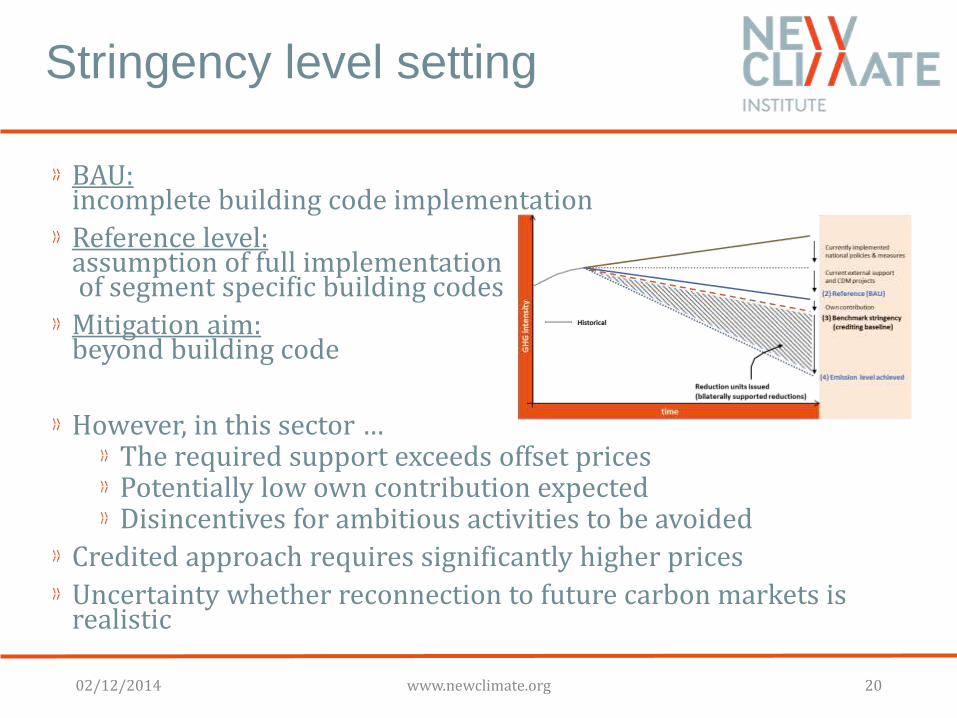

BAU:incomplete building code implementation

Reference level:assumption of full implementationof segment specific building codes

Mitigation aim:beyond building code

However, in this sector …The required support exceeds offset pricesPotentially low own contribution expectedDisincentives for ambitious activities to be avoided

Uncertainty whether reconnection to future carbon markets is realistic

02/12/2014 www.newclimate.org 20

Conclusions

Bilateral agreements provide temporal solution to test design and implementation of sectoral market-based approaches

Transition period of international carbon market can be used toenter into methodical discussions (also towards NMMs) prepare for suitable sector definitions and approaches andraise awareness about countries’ capabilities, own contributions and potential sectoral crediting thresholds

Staying closely to existing rules and knowledge ensures that concepts are understood while simplifications regain confidence in the instruments