16

1 April 2013 Oliver Mangan Chief Economist AIB The Irish Economic Update – Doing Relatively Well September 2014 aibeconomicresearch.com

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | hayden-sellers |

| View: | 20 times |

| Download: | 1 times |

1

April 2013Oliver ManganChief EconomistAIB

The Irish Economic Update – Doing Relatively Well

September 2014

aibeconomicresearch.com

2

Irish economy recovering after deep recession

Irish economy boomed from 1993 to 2007 with GDP up by over 250% – Celtic Tiger

Very severe three year long recession in Ireland from 2008-2010. GDP fell by 10%

Collapse in construction activity and banking system, severe fiscal tightening, high unemployment

GDP in 2010 back to 2005 levels but still over 25% higher than in 2000, highlighting that the economic crash came after a very strong period of growth, unlike in other countries

Ireland entered a three year EU/IMF bail-out programme at end 2010 as it could no longer access funding on global capital markets

Ireland exited its financial assistance programme on schedule in December 2013, without a precautionary credit line - has very large cash balances and no problem with market access

Budget deficit has declined at quicker than expected pace in past four years

Ireland benefits from the pick up underway in world economy, given its large export base

Domestic economy recovering, led by rebound in investment and labour market

GNP rose by 1.9% in 2012 and 3.2% in 2013. GNP up by 3.4% yoy in Q1 2014

3

Upbeat tone to Irish data continues in 2014

GNP rose by 3.2% in 2013. GNP up by 3.4% yoy in Q1 2014 with GDP up by 4.1% yoy

Strong pick up in mfg PMI in past year – hits highest level since 1999 in August

Surge in manufacturing output in H1 2014 – up 24% yoy in Q2

Exports rebound strongly in H1 2014. BoP remains in large surplus

Very strong services PMI data this year – index well over 60 in recent months, at 7 year highs

Housing market improving, while commercial property market recovering strongly

Construction PMI soars to above 60 – averages over 60 year-to-date, at record highs

OECD leading indicator for Ireland rises strongly – hits best level in H1 2014 since 2008

Consumer confidence in July at its best level since early 2007

Strong rise in core retail sales in recent quarters – up by 4% yoy in Q2 2014

Car sales surge by 30% year-to-date – best sales since 2008

Employment rises for 7 consecutive quarters, up 1.7% yoy in Q2 2014

Declining Live Register, with jobless rate falling from 15% in H1 2012 to 11.2% by Aug 2014

Further large fall in budget deficit in 2014: spending below target, taxes ahead of schedule

4

Strong Irish economic indicators

-15

-10

-5

0

5

10

15

20

25

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Industrial Production ( 3 Mth Moving Average Vol Y/Y %)

Source: Thomson Datastream

30

50

70

90

110

Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14

Consumer Confidence (ESRI - KBC)

Source: ESRI - KBC, Thomson Datastream

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

Q1 04 Q1 05 Q1 06 Q1 07 Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

GNP & Employment

GNP % YoY (3Qtr.Mov.Avg.) Employment % YoY

%

Source: CSO & Thomson Datastream

30

35

40

45

50

55

60

65

70

Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14

Ireland Mfg and Services PMIs

Source: Thomson Datastream, Investec

Services

Manufacturing

5

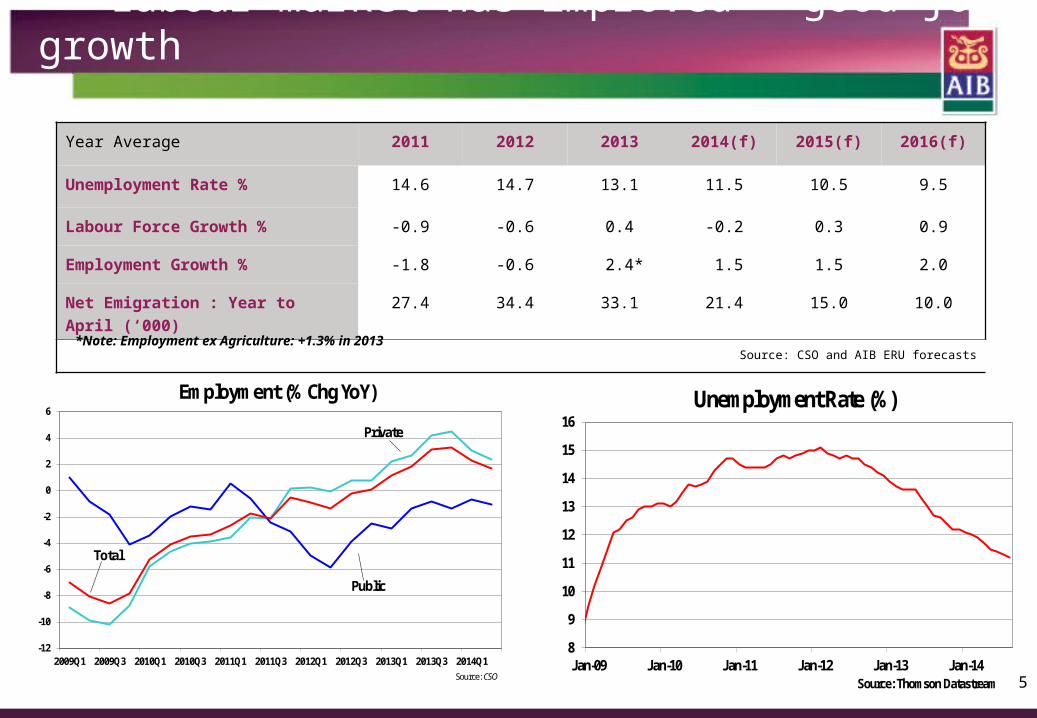

Labour market has improved – good job growth

Year Average 2011 2012 2013 2014(f) 2015(f) 2016(f)

Unemployment Rate % 14.6 14.7 13.1 11.5 10.5 9.5

Labour Force Growth % -0.9 -0.6 0.4 -0.2 0.3 0.9

Employment Growth % -1.8 -0.6 2.4* 1.5 1.5 2.0

Net Emigration : Year to April (‘000) 27.4 34.4 33.1 21.4 15.0 10.0

Source: CSO and AIB ERU forecasts*Note: Employment ex Agriculture: +1.3% in 2013

-12

-10

-8

-6

-4

-2

0

2

4

6

2009Q1 2009Q3 2010Q1 2010Q3 2011Q1 2011Q3 2012Q1 2012Q3 2013Q1 2013Q3 2014Q1

Employment (% Chg YoY)

Source: CSO

Public

Total

Private

8

9

10

11

12

13

14

15

16

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Unemployment Rate (%)

Source: Thomson Datastream

6

Exports pick up again as pharma patent cliff abates

Ireland a very open economy – exports, driven by

huge FDI, equated to 105% of GDP in 2013

Major gains in Irish competitiveness since 2009

Goods exports fell by 4% in 2013 on sharp drop in

pharma output (patents expire). Rebound in H1 2014

Service exports rise strongly since 2010 as new FDI

broadens export base and global recession ends

Total exports rise by 7.4% yoy in Q1 2014

-14 -12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12 14

Germany

France

Italy

Eurozone

UK

Ireland

Spain

Portugal

Unit Labour Costs 2009-2013 (% Change)

Source: EU Commission

0 10 20 30 40 50 60 70 80 90 100 110

Spain

Portugal

Ireland

Italy

France

Germany

UK

Finland

Exports as % of GDP 2013

Source: Thomson Datastream

-10

-5

0

5

10

15

20

Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014

Irish Exports of Services(Volume, 3 Qtr Moving Average, YoY% Change)

Source : CSO

7

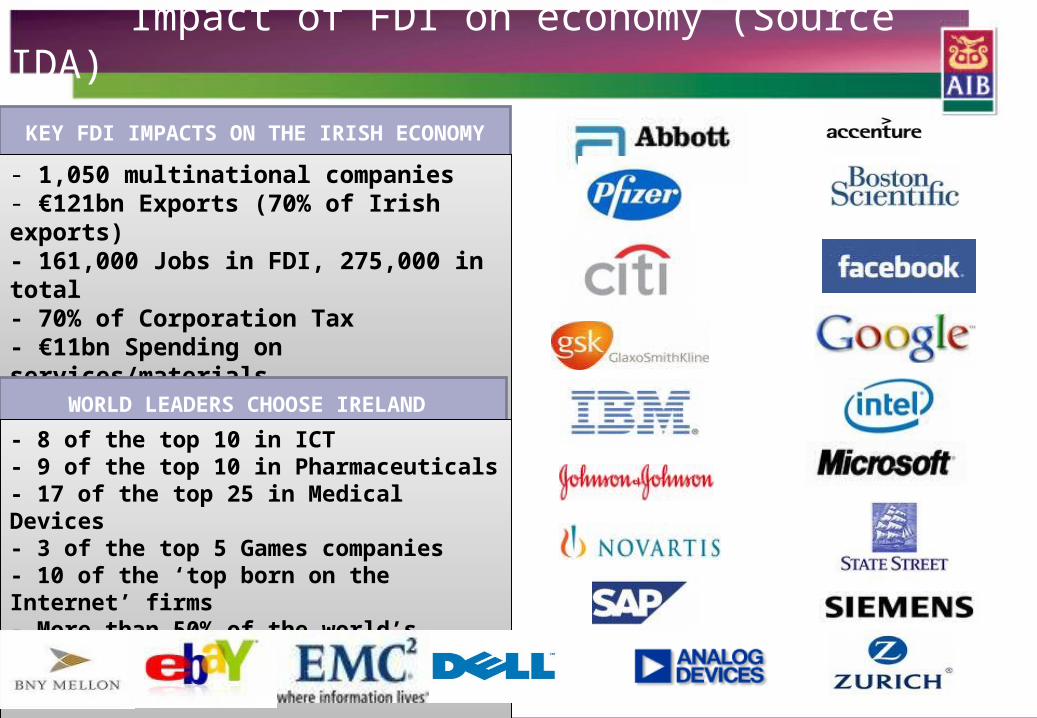

Impact of FDI on economy (Source IDA)

KEY FDI IMPACTS ON THE IRISH ECONOMY

- 1,050 multinational companies- €121bn Exports (70% of Irish exports)- 161,000 Jobs in FDI, 275,000 in total- 70% of Corporation Tax- €11bn Spending on services/materials- €8bn in Payroll- 67% of Business R&D expenditure

- 1,050 multinational companies- €121bn Exports (70% of Irish exports)- 161,000 Jobs in FDI, 275,000 in total- 70% of Corporation Tax- €11bn Spending on services/materials- €8bn in Payroll- 67% of Business R&D expenditure

WORLD LEADERS CHOOSE IRELAND

- 8 of the top 10 in ICT - 9 of the top 10 in Pharmaceuticals - 17 of the top 25 in Medical Devices- 3 of the top 5 Games companies- 10 of the ‘top born on the Internet’ firms - More than 50% of the world’s leading Financial Services firms

- 8 of the top 10 in ICT - 9 of the top 10 in Pharmaceuticals - 17 of the top 25 in Medical Devices- 3 of the top 5 Games companies- 10 of the ‘top born on the Internet’ firms - More than 50% of the world’s leading Financial Services firms

8

Domestic economy recovers over past year

Domestic economy contracted by 23% from its peak

in Q1 2008 to mid-2012

Construction investment big drag on GDP growth - fell

from 13-14% of GDP in 2004-08 to 5% in 2012

Total construction output rose by 13.7% in 2013

House building stabilised last year and has started to

pick up in 2014 from very low levels

Pick-up in commercial property market last year which

has continued in 2014

Business investment (ex volatile transport, mainly

planes) rebounding – up 40% yoy in Q1 2014

Total investment (ex transport) up 14.5% yoy in Q1

Strong rise in retail spending over past year, up 3.4%

yoy in H1 2014, with car sales up by 30% year-to-date

Fiscal drag has eased considerably in 2013-14

Domestic spending (ex transport) rose by 0.4% in

2013 and up by 3.3% yoy in Q1 2014

-40

-30

-20

-10

0

10

20

30

Q1 2005 Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014

Construction Investment (% YoY)

Source : CSO

%

-8

-6

-4

-2

0

2

4

Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014

Irish Retail Sales (ex autos) (Volume, Yr-on-Yr % Change)

Source: Thomson Datastream

9

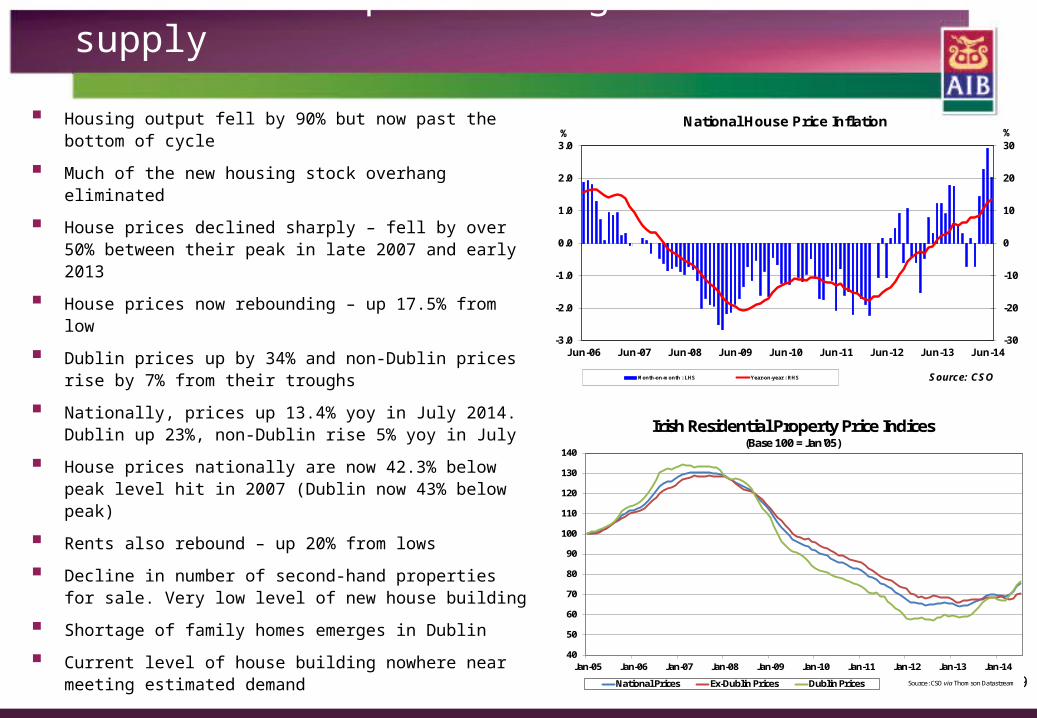

Dublin house prices surge amidst a lack of supply

Housing output fell by 90% but now past the bottom of cycle

Much of the new housing stock overhang eliminated

House prices declined sharply – fell by over 50% between their peak in late 2007 and early 2013

House prices now rebounding – up 17.5% from low

Dublin prices up by 34% and non-Dublin prices rise by 7% from their troughs

Nationally, prices up 13.4% yoy in July 2014. Dublin up 23%, non-Dublin rise 5% yoy in July

House prices nationally are now 42.3% below peak level hit in 2007 (Dublin now 43% below peak)

Rents also rebound – up 20% from lows

Decline in number of second-hand properties for sale. Very low level of new house building

Shortage of family homes emerges in Dublin

Current level of house building nowhere near meeting estimated demand

-30

-20

-10

0

10

20

30

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14

National House Price Inflation

Month-on-month : LHS Year-on-year : RHS Source: CSO

% %

40

50

60

70

80

90

100

110

120

130

140

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irish Residential Property Price Indices(Base 100 = Jan'05)

National Prices Ex-Dublin Prices Dublin Prices Source: CSO via Thomson Datastream

10

House building rising from very depressed levels

Housing completions 8,300 in 2013; 8,500 in 2012

House building is beginning to pick up but activity is

still at very low levels

Big jump in new housing registrations and

commencements, but still at depressed levels

Latest data show housing completions also picking

up (+32% in 2014), especially in Dublin

Recovery in house prices should help spur more

building activity

Housing affordability, though, still at levels pertaining

in 1997, before the boom started

Mortgage lending up almost 50% in H1 2014,

though still at low level in absolute terms

Government announces measures to help boost

house building activity

Completions may hit 11,000 this year but will take a

couple of years to get near 25,000 demand level0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015(f) 2017(f)

Housing Completions

Source: CSO; DoEHLG and AIB ERU

10

14

18

22

26

30

Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Housing Repayment Affordability *

* % of disposable income required for mortgage repayments for 2 income household, 30 year 92% mortgage. Based on permanent tsb/ESRI national house price & CSO House price index

Sources: AIB, permanent tsb/ESRI, CSO, Dept of Finance,

%

11

AIB Model of Potential Housing Demand 2010-2016

Calendar Year 2010 2011 2012 2013 2014 2015 2016

Household Formation

21,500 16,500 15,500 16,000 17,500 18,500 18,000

of which

Indigenous Population Growth

27,500 24,500 24,000 23,500 23,000 22,500 22,000

Migration Flows -9,000 -6,500 -10,000 -9,500 -6,000 -5,000 -4,000

Increased Headship

3,000 3,000 3,000 3,000 3,000 3,000 3,000

Second Homes 1,000 1,000 1,000 1,000 1,000 1,000 1,000

Replacement of Obsolete Units

4,000 4,000 4,000 4,000 4,000 4,000 4,000

Total POTENTIAL Demand

26,500 25,000 22,000 22,000 25,000 24,500 25,000

Completions 14,500 10,500 8,500 8,300 11,000 15,000 20,000

POTENTIAL Impact on Vacant Stock

-12,000 -14,500 -13,500 -13,700 -14,000 -9,500 -5,000

Sources: CSO, DoECLG, AIB ERU

12

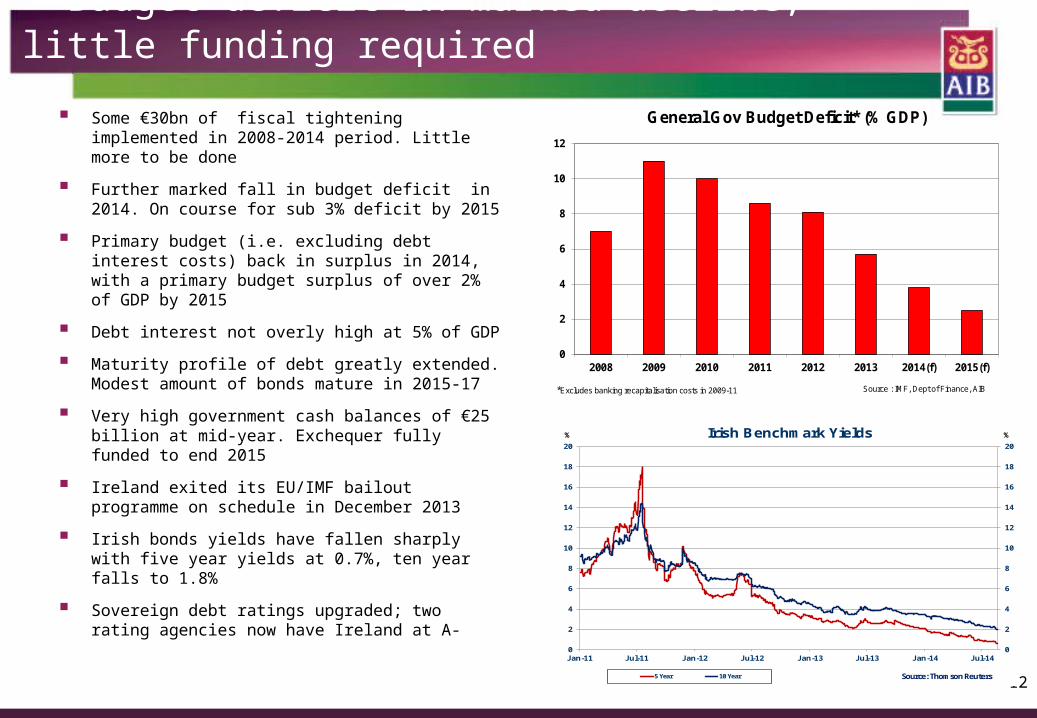

Budget deficit in marked decline, little funding required

Some €30bn of fiscal tightening implemented in 2008-2014 period. Little more to be done

Further marked fall in budget deficit in 2014. On course for sub 3% deficit by 2015

Primary budget (i.e. excluding debt interest costs) back in surplus in 2014, with a primary budget surplus of over 2% of GDP by 2015

Debt interest not overly high at 5% of GDP

Maturity profile of debt greatly extended. Modest amount of bonds mature in 2015-17

Very high government cash balances of €25 billion at mid-year. Exchequer fully funded to end 2015

Ireland exited its EU/IMF bailout programme on schedule in December 2013

Irish bonds yields have fallen sharply with five year yields at 0.7%, ten year falls to 1.8%

Sovereign debt ratings upgraded; two rating agencies now have Ireland at A-

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Irish Benchmark Yields

5 Year 10 Year Source: Thomson Reuters

% %

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013 2014(f) 2015(f)

General Gov Budget Deficit* (% GDP)

Source : IMF, Dept of Finance, AIB*Excludes banking recapitalisation costs in 2009-11

13

Gov debt stabilises; private sector deleveraging

0

1

2

3

4

5

6

7

8

9

10

1980 1985 1990 1995 2000 2005 2010 2015

Debt Interest (% GDP)

Source: NTMA; Dept of Finance

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013(e) 2014(f) 2015(f) 2016(f) 2017(f) 2018(f)

General Gov Net Debt* (% GDP)

Source: IMF* Gross General Gov Debt Less Gov Cash Balances/Deposits

150,000

160,000

170,000

180,000

190,000

200,000

210,000

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013

Irish Household Debt (€M)

Source : Central Bank of Ireland

75

100

125

150

175

200

225

250

275

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014(f)

Irish Private Sector Credit (Inc Securitisations) as % GDP%

Sources: Central Bank, CSO, AIB ERU Calculations

14

Ireland benefits from improving global economy

The adjustment on the domestic side of economy is over so no longer a drag on growth

Housing, labour market and domestic demand are all on an improving path

Construction rebounding from very depressed activity levels

Little further fiscal tightening required in 2015 to get budget deficit down below 3% of GDP

Major gains made on the competitiveness front

Large, diversified export base means Ireland benefits from improving global growth

Irish lead indicators pointing to more strong growth

GDP growth of 3% forecast for 2014 as pharma cliff eases. GNP to rise by 3% also

GDP growth of 3.5% in 2015 and 3.7% in 2016 as domestic demand improves further

Scope for upside surprises on growth, especially if exports and/or investment perform very strongly

-12

-9

-6

-3

0

3

6

2008 2009 2010 2011 2012 2013 2014(f) 2015(f) 2016(f)

GDP Contributions (2008-2016)

Net Exports Fixed Investment Govt Spending Personal Spending

%

Source: CSO and AIB ERU forecasts

-4

-2

0

2

4

6

Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14

Irish, Eurozone & UK Inflation (HICP Rates)

Ireland

Eurozone

Source: Thomson Datastream

UK

15

% change in real terms unless

stated

2011 2012 2013 2014 (f) 2015 (f) 2016 (f)

GDP 2.8 -0.3 0.2 3.0 3.5 3.7

GNP -0.8 1.9 3.2 3.0 3.0 3.2

Personal Consumption -1.2 -1.2 -0.8 0.5 1.5 1.8

Government Spending -2.1 -2.1 1.4 1.3 1.5 2.0

Fixed Investment -2.9 5.0 -2.4 3.0 5.0 6.0

Domestic Spending (ex planes) -1.3 -0.5 0.4 1.5 2.0 2.5

Exports 5.5 4.7 1.1 5.0 5.0 5.0

Imports -0.6 6.9 0.6 3.7 4.0 4.2

HICP Inflation (%) 1.1 2.0 0.5 0.5 1.0 1.5

Unemployment Rate (%) 14.6 14.7 13.1 11.5 10.5 9.5

Budget Deficit (% GDP) 8.6 8.1 5.7 3.8 2.5 1.5

BoP Current A\C as % GDP 0.8 1.6 4.4 4.4 4.2 4.0

Source: CSO, AIB ERU Forecasts

AIB Irish Economic Forecasts

16

Risks to the Irish economic recovery

Recovery in the global economy is not yet secure, especially in the eurozone, with on-going risks and headwinds. This is a concern given importance of exports to the Irish economy

Major changes to corporation tax, although this would have to be agreed to by Ireland

Supply bottlenecks in the construction sector, especially new house building

High indebtedness and scale of balance sheet repair by households (mortgage debt is very high, as are mortgage arrears). Major deleveraging has already taken place but difficult to estimate its duration

Continuing credit contraction – fewer banks, tighter credit conditions, on-going deleveraging

Note: All Irish data in tables are sourced from the CSO unless otherwise stated. Non-Irish data are from the IMF, OECD and Thomson Financial. Irish forecasts are from AIB Economic Research Unit. This presentation is for information purposes and is not an invitation to deal. The information is believed to be reliable but is not guaranteed. Any expressions of opinions are subject to change without notice. This presentation is not to be reproduced in whole or in part without prior permission. In the Republic of Ireland it is distributed by Allied Irish Banks, p.l.c. In the UK it is distributed by Allied Irish Banks, plc and Allied Irish Banks (GB). In Northern Ireland it is distributed by First Trust Bank. In the United States of America it is distributed by Allied Irish Banks, plc. Allied Irish Banks, p.l.c. is regulated by the Central Bank of Ireland. Allied Irish Bank (GB) and First Trust Bank are trade marks used under licence by AIB Group (UK) p.l.c. (a wholly owned subsidiary of Allied Irish Banks, p.l.c.), incorporated in Northern Ireland. Registered Office 4 Queens Square, Belfast BT1 3DJ. Registered Number NI 18800. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. In the United States of America, Allied Irish Banks, p.l.c., New York Branch, is a branch licensed by the New York State Department of Financial Services. Deposits and other investment products are not FDIC insured, they are not guaranteed by any bank and they may lose value. Please note that telephone calls may be recorded in line with market practice.

CPD Hours. The code for this presentation is 2014-0604