prices drop backPrices dropped back further in the week’s opening session. Towards 4.30pm in London the Argus May North Sea price was $65.07/bl, a drop of 27¢/bl from the same time in the previous session.

Espo Blend loadings at 11-month highSeaborne exports of ESPO Blend crude from Russia’s Kozmino port could rise to an 11-month high of 696,000 b/d in April, according to a preliminary loading programme.

Trafigura in deal to supply UK Lindsey refineryUK-based Prax Group said it has agreed a crude and feed-stocks supply deal with trading firm Trafigura for the 110,000 b/d Lindsey refinery in northeast England.

Congo loadings to slow in aprilCrude loadings from Congo (Brazzaville) will fall to 215,000 b/d in April from the 237,000 b/d planned in March, accord-ing to programmes.

ContEnts

Futures and forward markets 2North Sea Dated 3Commentary and prices 4-22Deals done 24Daily netbacks 26Industry and infrastructure news 28

Dated components-establishing North Sea Dated $/bl

hh

65.30

65.40

65.50

65.60

65.70

65.80

65.90

66.00

66.10

10 Mar 19 Mar 29 Mar

BrentForties

Ose. with QPEko. with QPTroll with QP

North Sea forward curve establishing Anticipated Dated $/bl

63.50

64.00

64.50

65.00

65.50

66.00

2 Mar 20 Apr 8 Jun 27 Jul

CFD weekMAY JUNE JULY

North Sea flat priceArgus derives a flat price from trade of a month-ahead forward contract for the delivery of Brent, Forties, Oseberg, Ekofisk or Troll, taking a weighted average of trade between 4:29pm and 4:30pm in London. In the absence of trade, a combination of the Ice Brent futures one-minute marker and the exchange of futures for physical (EFP) market is used.Anticipated Dated We then look at contracts for difference (CFDs), with which the market anticipates North Sea Dated in the coming weeks at differentials to the forward month. Prices falling between 10 days and a full calendar month ahead are averaged.Physical differentials Argus assesses trade in physical cargoes of Brent, Forties, Oseberg, Ekofisk and Troll crude, assigning differentials to North Sea Dated to each grade for the 10-days to month-ahead range.Dated components The combination of the Anticipated Dated and the physical values gives each grade’s component of North Sea Dated. Quality premiums are deducted from Oseberg, Ekofisk and Troll for benchmarking purposes. The lowest-priced of the five components is used to set the price of North Sea Dated.

Components of North Sea Dated $/bl

65.50

65.55

65.60

65.65

65.70

65.75

65.80

65.85

Brent Forties Oseberg Ekofisk Troll

North Sea Dated calculation $/bl

North Sea flat price

North Sea partial trade Delivery period

Volume bl Price

volume weighted average (VWA) May 300,000 65.07

CFD value against relevant basis month

Basis Midpoint

8 Mar-12 Mar May +0.05

15 Mar-19 Mar May -0.09

22 Mar-26 Mar May -0.18

29 Mar-2 Apr May -0.35

5 Apr-9 Apr May -0.50

12 Apr-16 Apr May -0.64

CFD value for 11 Mar-1 Apr May -0.17

North Sea Anticipated Dated calculation

Month Price

VWA of North Sea partial trade May 65.07

CFD value for 11 Mar-1 Apr May -0.17

Anticipated Dated 64.90

Physical differentials for 11 Mar-1 Apr

Grade Basis Diff midpoint

Brent Dated +0.85

Forties Dated +0.90

Oseberg Dated +1.10

Ekofisk Dated +0.86

Troll Dated +1.30

North Sea quality premiums (QP) for 11 Mar-1 Apr

Oseberg +0.31

Ekofisk +0.23

Troll +0.47

North Sea Dated calculation

Anticipated Dated

Add Diff midpoint

Subtract QP Price

Brent component of Dated 64.90 +0.85 65.75

Forties component of Dated 64.90 +0.90 65.80

Oseberg component of Dated 64.90 +1.10 +0.31 65.69

Ekofisk component of Dated 64.90 +0.86 +0.23 65.53

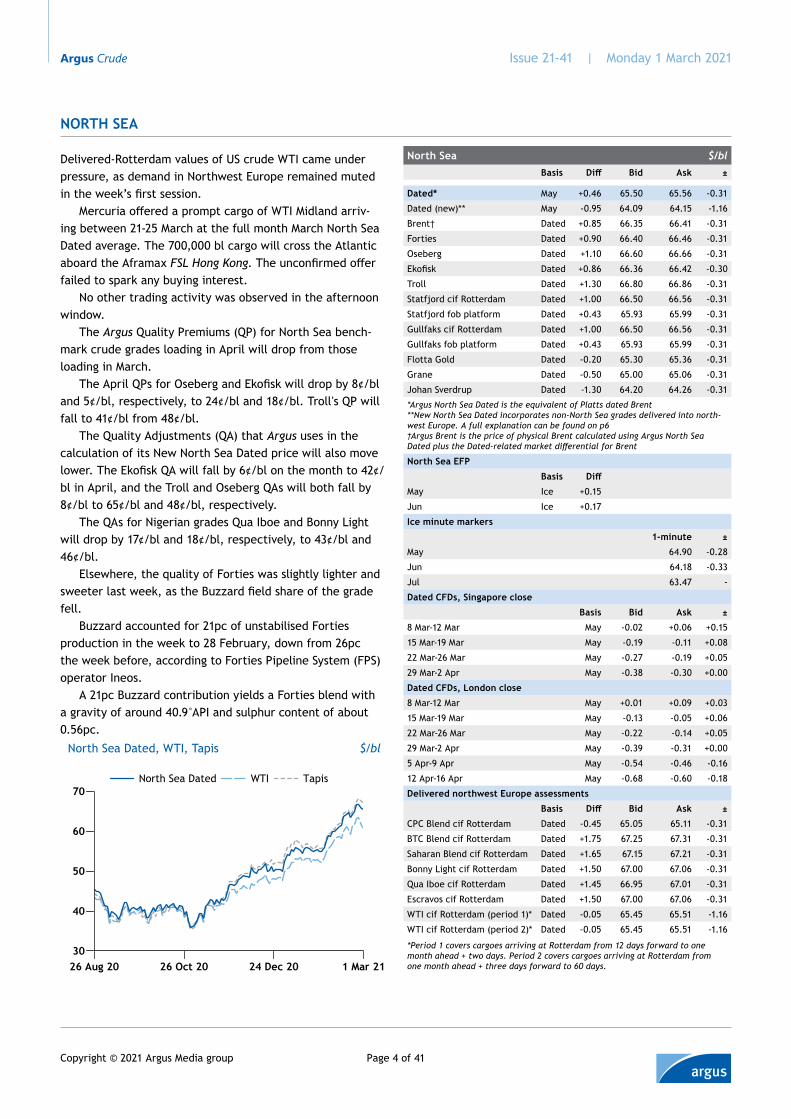

Delivered-Rotterdam values of US crude WTI came under pressure, as demand in Northwest Europe remained muted in the week’s first session.

Mercuria offered a prompt cargo of WTI Midland arriv-ing between 21-25 March at the full month March North Sea Dated average. The 700,000 bl cargo will cross the Atlantic aboard the Aframax FSL Hong Kong. The unconfirmed offer failed to spark any buying interest.

No other trading activity was observed in the afternoon window.

The Argus Quality Premiums (QP) for North Sea bench-mark crude grades loading in April will drop from those loading in March.

The April QPs for Oseberg and Ekofisk will drop by 8¢/bl and 5¢/bl, respectively, to 24¢/bl and 18¢/bl. Troll's QP will fall to 41¢/bl from 48¢/bl.

The Quality Adjustments (QA) that Argus uses in the calculation of its New North Sea Dated price will also move lower. The Ekofisk QA will fall by 6¢/bl on the month to 42¢/bl in April, and the Troll and Oseberg QAs will both fall by 8¢/bl to 65¢/bl and 48¢/bl, respectively.

The QAs for Nigerian grades Qua Iboe and Bonny Light will drop by 17¢/bl and 18¢/bl, respectively, to 43¢/bl and 46¢/bl.

Elsewhere, the quality of Forties was slightly lighter and sweeter last week, as the Buzzard field share of the grade fell.

Buzzard accounted for 21pc of unstabilised Forties production in the week to 28 February, down from 26pc the week before, according to Forties Pipeline System (FPS) operator Ineos.

A 21pc Buzzard contribution yields a Forties blend with a gravity of around 40.9°API and sulphur content of about 0.56pc.

*Argus North Sea Dated is the equivalent of Platts dated Brent **New North Sea Dated incorporates non-North Sea grades delivered into north-west Europe. A full explanation can be found on p6 †Argus Brent is the price of physical Brent calculated using Argus North Sea Dated plus the Dated-related market differential for Brent

*Period 1 covers cargoes arriving at Rotterdam from 12 days forward to one month ahead + two days. Period 2 covers cargoes arriving at Rotterdam from one month ahead + three days forward to 60 days.

Ineos expects Buzzard's contribution to average 25.2pc this month, which would give Forties an average gravity of around 40.3°API and sulphur content near 0.62pc. Forties quality will be slightly sweeter and lighter next month, as Ineos forecast a 23.5pc Buzzard contribution.

The UK's crude production declined in January, when domestic demand was constrained by a third national lock-down.

Production averaged 860,000 b/d, down by 9pc from December's revised 945,000 b/d and around 18pc below the 1mn b/d achieved in January 2020, according to latest government figures.

The Argus May North Sea price was $65.07/bl, a drop of 27¢/bl based on 300,000 bl of trade in the minute leading up to the timestamp. CFDs climbed. The front-week 8-12 March CFD increased by 3¢/bl to May North Sea +5¢/bl, while the second-week 15-19 March CFD gained 6¢/bl to May North Sea -9¢/bl.

North Sea $/bl

North Sea quality premiums (QP)

Mar apr

Ekofisk 0.23 0.18

Oseberg 0.32 0.24

Troll 0.48 0.41

De-escalators

Sulphur +0.09

North Sea calculations

Basis Price

Volume-weighted average of North Sea partial traded May 65.07

Ice Brent marker May 64.90

Exchange of futures for physical (EFP) May +0.15

North Sea basis (flat price) May 65.07

anticipated Dated based on 10 days-month ahead CFD strip:

Price ±

11 Mar-01 Apr 64.90 -0.32

Argus Brent component of Dated 65.75 -0.32

Argus Forties component of Dated 65.80 -0.32

Argus Oseberg component of Dated (QP applied) 65.69 -0.31

Argus Oseberg component of Dated (no QP applied) 66.00 -0.32

Argus Ekofisk component of Dated (QP applied)* 65.53 -0.31

Argus Ekofisk component of Dated (no QP applied) 65.76 -0.31

Argus Troll component of Dated (QP applied) 65.73 -0.31

*the lowest component sets Dated

argus alternative Dated illustrations

Basis Diff Price ±

Argus Dated Average May +0.83 65.90 -0.32

Argus Dated BFOE* May +0.46 65.75 -0.32

Argus Dated BFO May +0.62 65.75 -0.32

Argus Dated FOE May +0.46 65.76 -0.32

Quality premiums (QP) not applied to above *Argus Dated BFOE is equivalent to North Sea Dated (no QP)

argus North Sea reference Price

Argus North Sea Reference Price (NSRP) 65.65 -0.30

North Sea flat priceArgus derives a flat price from trade of a month-ahead forward contract for the delivery of Brent, Forties, Oseberg, Ekofisk or Troll, taking a weighted average of trade between 4:29pm and 4:30pm in London. In the absence of trade, a combination of the Ice Brent futures one-minute marker and the exchange of futures for physical (EFP) market is used.

Anticipated Dated We then look at contracts for difference (CFDs), with which the market anticipates North Sea Dated in the coming weeks at differentials to the forward month. Prices falling between 10 days and a full calendar month ahead are averaged.

Physical differentials Argus assesses fob trade in physical cargoes of Brent, For-ties, Oseberg, Ekofisk and Troll crude, assigning differentials to North Sea Dated to each grade for the 10-days to month-ahead range. Argus then assesses cif Rotterdam trade in Bonny Light, Qua Iboe and WTI. Prices falling between 12 days and a calendar month ahead — plus two days — are then averaged. Then a freight value based on a five-day average of the Argus UK-UK Continent rate is applied to the cif values in order to construct virtual North Sea fob values for the three non-North Sea grades.

Dated components The combination of the Anticipated Dated and the physical values gives each grade’s component of North Sea Dated. Quality adjustments are deducted from Oseberg, Ekofisk, Troll, Bonny Light and Qua Iboe for benchmarking purposes. The lowest-priced of the eight components is used to set the price of North Sea Dated.

New North Sea Dated calculation $/bl

North Sea flat price

North Sea partial trade Delivery period

Volume bl Price

volume weighted average (VWA) May 300,000 65.07

CFD value against relevant basis month

Basis Midpoint

8 Mar-12 Mar May +0.05

15 Mar-19 Mar May -0.09

22 Mar-26 Mar May -0.18

29 Mar-2 Apr May -0.35

5 Apr-9 Apr May -0.50

12 Apr-16 Apr May -0.64

CFD value for 11 Mar-1 Apr May -0.17

North Sea Anticipated Dated calculation

Month Price

VWA of North Sea partial trade May 65.07

CFD value for 11 Mar-1 Apr May -0.17

Anticipated Dated 64.90

Physical differentials for 11 Mar-1 Apr

Grade Basis Diff midpoint

Brent Dated +0.85

Forties Dated +0.90

Oseberg Dated +1.10

Ekofisk Dated +0.86

Troll Dated +1.30

Bonny Light cif Rotterdam Dated +1.50

Qua Iboe cif Rotterdam Dated +1.45

WTI cif Rotterdam (period 1) Dated -0.05

Freight adjustment

Five-day average UK-UK continent rate 22-26 Feb 0.73

Five-day average UK-UK continent rate 23 Feb-1 Mar 0.73

North Sea quality adjustments (QA) for 11 Mar-1 Apr

Urals fob Novo (Aframax) Dated -2.49 63.01 63.07 -0.78

CPC Blend fob Dated -2.43 63.07 63.13 -0.48

Turkish straits demurrage

Delay days 12

Aframax demurrage rate $/d 30,000

Suezmax demurrage rate $/d 27,500

CPC Blend vs Saharan Blend $/bl

hh

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

4 Sep 20 2 Nov 20 31 Dec 20 1 Mar 21

Saharan Blend = 0

Bonny Light vs Azeri Light $/bl

hh

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

4 Sep 20 2 Nov 20 31 Dec 20 1 Mar 21

Azeri Light = 0

Urals values in northwest Europe lost ground amid muted regional demand for March-loading supplies, while details emerged on Turkish refiner Tupras’ latest buy tender.

Trading firm Trafigura offered a 100,000t cargo of Urals crude loading at Primorsk or Ust-Luga on 11-15 March at Dated -2.35 cif Rotterdam, but was unable to attract a buyer at that level. The offer, which was not confirmed, came in some 15¢/bl below reported traded levels for marginally earlier March dates last week.

Signs of lacklustre regional demand for Russian export blend emerged elsewhere, as Turkish refiner Tupras was said to have eschewed the medium sour grade in its latest buy tender. Traders suggested the firm opted instead for low-sulphur Siberian Light from trader Maddox and Libyan Es Sider from Total trading-arm Totsa instead, though further information did not surface.

Maddox is expected to supply Socar’s 85,000t parcel of Siberian Light scheduled to load at Novorossiysk is the Black Sea on 30-31 March. Tupras’ tender originally listed 80,000t to 100,000t of Urals, Siberian Light or Es Sider as eligible for 29 March-10 April delivery to Tutunciftlik or Aliaga.

Urals differentials in northwest Europe have held at their lowest levels since April last year in recent sessions, though signs emerged that a bulk shipment could soon be set for delivery east of Suez. As of 1 March, vessel tracking indicated three cargoes of Urals were en route for the Skaw, where they could be transferred onto a larger vessel. Lukoil trading-arm Litasco had booked the very large crude carrier (VLCC) Antigone to ship a 270,000t parcel to Ningbo in China on 25 March, though port reports indicated this fixture had now failed.

Elsewhere, Azeri crude was en route for the Ukraine, according to shipping reports. The Socar-chartered Heydar

Aliyev departed Turkey’s Ceyhan on 27 February laden with a roughly 675,000 bl and is currently signalling for Yuzhny, to the east of Odessa.

The majority of Azeri crude that sails for the Ukraine discharges at Odessa, from which it is often scheduled for onward delivery to Ukrtatnafta’s 363,000 b/d Kremenchug refinery in Poltava Oblast. It can also head along the Odessa-Brody pipeline to Belarusian state-owned BNK’s 323,000 b/d Mozyr facility.

Azeri crude values were otherwise unchanged in thin trade, with the latest deals for mid-March dates reportedly struck at around Dated +0.80 cif Augusta, pressured by a limited arbitrage outlook and ample competing Libyan crude supplies.

No activity on Russian export blend, Siberian Light or Azeri crude was confirmed.

Turkish refiner Tupras booked Libyan crude in its latest tender, following depressed interest in the grade in recent trade sessions.

Traders said Tupras bought Libyan flagship Es Sider crude from equity producer Total and a cargo of Russian Siberian Light from Maddox in its latest tender. Both grades and Russian Urals were listed as options for supply of 80,000t to 100,000t for 29 March-10 April delivery to Tutunciftlik or Aliaga. While many Mediterranean refiners turn to Es Sider as a light sweet crude feedstock, Tupras tends to use the grade and Siberian Light as indirect substitutes for sour supplies. Results from the latest tender were not confirmed, and the award levels were not immediately known.

Es Sider discounts to the North Sea benchmark widened at the end of last week, with market participants report-ing offers at small discounts to the yet-unpublished official March formula price. Market participants expected Libya’s state-run NOC to release said official formula prices over the following sessions. It was unclear if Tupras procured its crude at deeper discounts to this basis than the latest spot offers, given its extended 90-day payment requirements in its tender.

Es Sider was otherwise most recently viewed at levels equivalent to North Sea Dated -1.80 fob Libya at the end of last week.

Iraqi crude exports marketed by federal company Somo added 3pc on the month to 2.96mn b/d in February, driven by increases in Basrah shipments, Iraq’s oil ministry said. Combined Basrah crude loadings rose by 2pc from January to 2.83mn b/d in February.

Somo-marketed Kirkuk blend volumes dropped by 36pc on the month to 63,000 b/d in February. The company’s figures do not capture the majority of Kirkuk blend supplies, which are sold by the Kurdistan Regional Government.

Somo’s revenues gained 5pc on the month to around $5bn in February, while the company achieved an average crude price of $60.33/bl on the month, up by 13pc from January.

The Opec basket price picked up by a sharp $6.67/bl — of 12pc — on the month to $61.05/bl in February, up from $54.38/bl in January.

Basrah Light cif Augusta vs Urals Med $/bl

hh

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2 Dec 20 4 Jan 21 1 Feb 21 1 Mar 21

Urals Med = 0

Mediterranean $/bl

Basis Diff Bid Ask ±

Saharan Blend Dated -0.05 65.45 65.51 -0.31

Zarzaitine Dated -0.10 65.40 65.46 -0.31

Es Sider Dated -1.80 63.70 63.76 -0.31

Kirkuk Dated -3.75 61.75 61.81 -0.31

Basrah Light cif Augusta Dated -0.25 65.25 65.31 -0.31

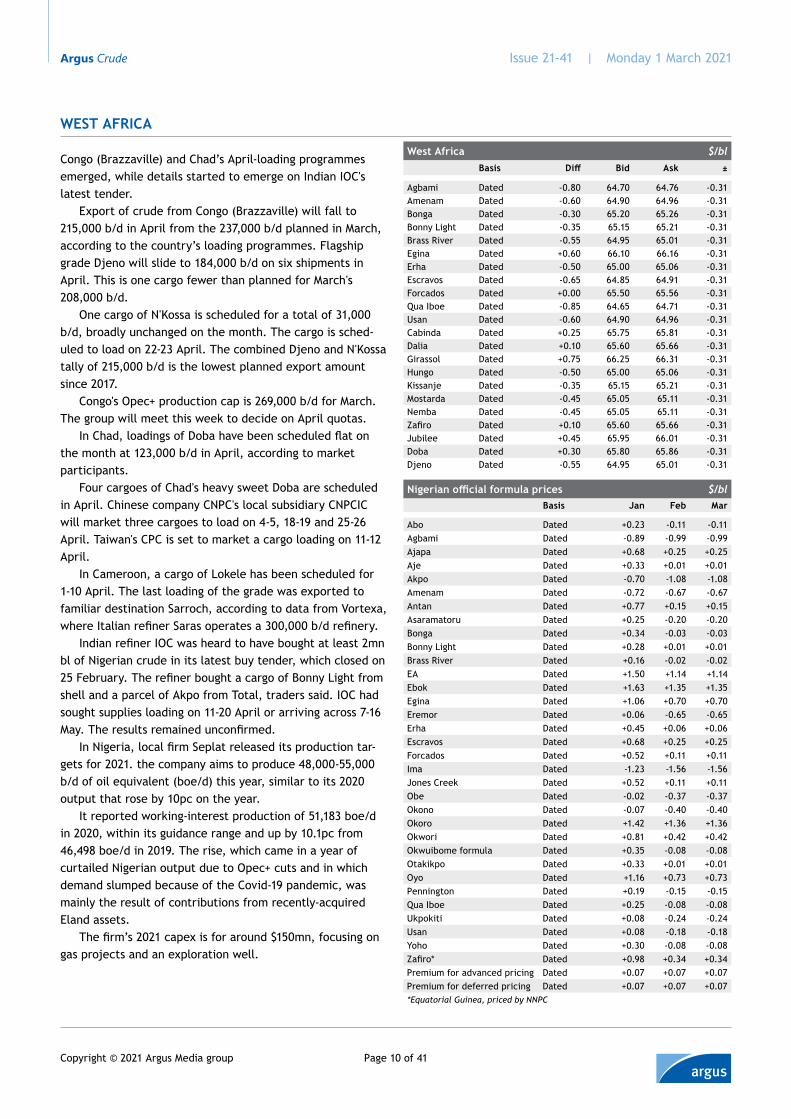

Congo (Brazzaville) and Chad’s April-loading programmes emerged, while details started to emerge on Indian IOC's latest tender.

Export of crude from Congo (Brazzaville) will fall to 215,000 b/d in April from the 237,000 b/d planned in March, according to the country’s loading programmes. Flagship grade Djeno will slide to 184,000 b/d on six shipments in April. This is one cargo fewer than planned for March's 208,000 b/d.

One cargo of N'Kossa is scheduled for a total of 31,000 b/d, broadly unchanged on the month. The cargo is sched-uled to load on 22-23 April. The combined Djeno and N'Kossa tally of 215,000 b/d is the lowest planned export amount since 2017.

Congo's Opec+ production cap is 269,000 b/d for March. The group will meet this week to decide on April quotas.

In Chad, loadings of Doba have been scheduled flat on the month at 123,000 b/d in April, according to market participants.

Four cargoes of Chad's heavy sweet Doba are scheduled in April. Chinese company CNPC's local subsidiary CNPCIC will market three cargoes to load on 4-5, 18-19 and 25-26 April. Taiwan's CPC is set to market a cargo loading on 11-12 April.

In Cameroon, a cargo of Lokele has been scheduled for 1-10 April. The last loading of the grade was exported to familiar destination Sarroch, according to data from Vortexa, where Italian refiner Saras operates a 300,000 b/d refinery.

Indian refiner IOC was heard to have bought at least 2mn bl of Nigerian crude in its latest buy tender, which closed on 25 February. The refiner bought a cargo of Bonny Light from shell and a parcel of Akpo from Total, traders said. IOC had sought supplies loading on 11-20 April or arriving across 7-16 May. The results remained unconfirmed.

In Nigeria, local firm Seplat released its production tar-gets for 2021. the company aims to produce 48,000-55,000 b/d of oil equivalent (boe/d) this year, similar to its 2020 output that rose by 10pc on the year.

It reported working-interest production of 51,183 boe/d in 2020, within its guidance range and up by 10.1pc from 46,498 boe/d in 2019. The rise, which came in a year of curtailed Nigerian output due to Opec+ cuts and in which demand slumped because of the Covid-19 pandemic, was mainly the result of contributions from recently-acquired Eland assets.

The firm’s 2021 capex is for around $150mn, focusing on gas projects and an exploration well.

Traders were awaiting the release of Mideast Gulf formula prices, which may emerge after the Opec+ ministerial meet-ing on 4 March.

The premium of front-month April Dubai prices to the third-month June contract was at 69¢/bl on average in Feb-ruary. This was wider by around 22¢/bl from the front-month to third-month spread in January, and the widest since the Dubai backwardation averaged 76¢/bl in June 2020.

The intermonth Dubai structure in February raised expectations of an increase to April’s Mideast Gulf formula prices. The Dubai intermonth spreads are one factor that producers like Saudi Arabia consider when setting official prices.

But some refiners expect state-controlled Saudi Aramco to lift only the prices of its lighter sour crudes, leaving its heavier sour grades unchanged, due to the overall softer demand for April-loading medium sour supplies.

Yemen’s technical committee for crude oil marketing (YCOMD) issued a tender to sell 2mn bl of April-loading

Differentials to DME Oman futures, 4:30pm Singapore $/bl Month Basis Diff ±

Murban May May DME -0.55 -1.14

Upper Zakum May May DME -0.55 -0.59

Das May May DME -0.90 -1.04

Dubai May May DME -0.20 -0.25

Basrah Light fob Iraq† May May DME -0.52 -0.75

Basrah Heavy fob Iraq† May May DME -0.77 -0.75

Qatar Land May May DME -0.30 -0.47

Qatar Marine May May DME 0.00 -0.42

Qatar Al-Shaheen May May DME -0.55 -0.84

Banoco Arab Medium May May DME +0.10 -0.22

†Asia-Pacific destination-restricted cargoes

Oman vs Dubai $/bl

hh

-1.0

-0.5

0.0

0.5

1.0

1.5

4 Sep 20 2 Nov 20 30 Dec 20 1 Mar 21

Dubai = 0

Urals vs Oman $/bl

hh

-3

-2

-1

0

1

2

3

3 Sep 20 30 Oct 20 30 Dec 20 1 Mar 21

Oman = 0

Differentials to Murban, 4:30pm Singapore $/bl Month Basis Diff ±

Mideast Gulf

Dubai May May Mur- +0.36 +0.90

Oman May May Mur- +0.55 +1.14

Das May May Mur- -0.35 +0.10

Upper Zakum May May Mur- 0.00 +0.55

Umm Lulu May May Mur- -0.05 +0.10

Qatar Land May May Mur- +0.25 +0.67

Qatar Marine May May Mur- +0.55 +0.72

Qatar Al-Shaheen May May Mur- 0.00 +0.30

Banoco Arab Medium May May Mur- +0.65 +0.92

Basrah Light fob Iraq Apr May Mur- +0.03 +0.39

Basrah Medium fob Iraq Apr May Mur- +0.33 +0.39

Basrah Heavy fob Iraq Apr May Mur- -0.22 +0.39

DFC fob Qatar May May Mur- +0.55 +0.30

LSC fob Qatar May May Mur- +0.25 +0.30

Asian-timestamp WTI Houston Apr May Mur- +0.35 +0.61

Russia Asia-Pacific

ESPO Blend May Mur- +1.20 +0.90

Sokol May Mur- +1.15 +0.30

Sakhalin Blend May Mur- +0.65 +0.30

Substitute North Sea Dated May Mur- +1.45 +0.07

Mideast Gulf $/bl Month Basis Diff Bid Ask ±

Dubai May 63.99 64.09 -0.05Oman May May* +1.30 64.18 64.28 -0.01Murban May Adnoc +0.00 63.63 63.73 -Das May Adnoc +0.00 63.28 63.38 -0.90Upper Zakum May Adnoc +0.00 63.63 63.73 -0.45Umm Lulu Jun Adnoc +0.00 63.58 63.68 -0.90Qatar Land May QP +0.00 63.88 63.98 -Qatar Marine May QP +0.00 64.18 64.28 -Qatar Al-Shaheen May May* +0.75 63.63 63.73 -Banoco Arab Medium May Aramco +0.00 64.28 64.38 -Basrah Light fob Iraq† Apr Somo -1.00 63.66 63.76 -Basrah Medium fob Iraq† Apr Somo +0.60 63.96 64.06 -

Basrah Heavy fob Iraq† Apr Somo +1.30 63.41 63.51 -DFC fob Qatar May May* +1.30 64.18 64.28 -LSC fob Qatar May May* +1.00 63.88 63.98 -*basis is Dubai swaps †Asia-Pacific destination-restricted cargoes

Masila Blend. Bids must be submitted by 2 March and remain valid until 5 March. YCOMD last sold February-loading Masila Blend to Glencore at a 65¢/bl discount to North Sea Dated.

The front-month May Brent-Dubai EFS, or the spread be-tween Ice Brent futures and Dubai swaps, rose to a premium of $2.66/bl, from $2.47/bl in the previous session.

May Dubai partials were heard to have traded at $64.15-64.20/bl.

Cabinda vs Dubai month 1 $/bl

hh

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3 Sep 20 30 Oct 20 30 Dec 20 1 Mar 21

Dubai month 1 = 0

Dubai vs North Sea Dated, MEG freight $/bl

-3

-2

-1

0

1

2

Dec 20 Jan 21 Feb 21 Mar 21

North Sea Dated = 0

Mideast Gulf-UKC 260,000t Dubai vs North Sea Dated

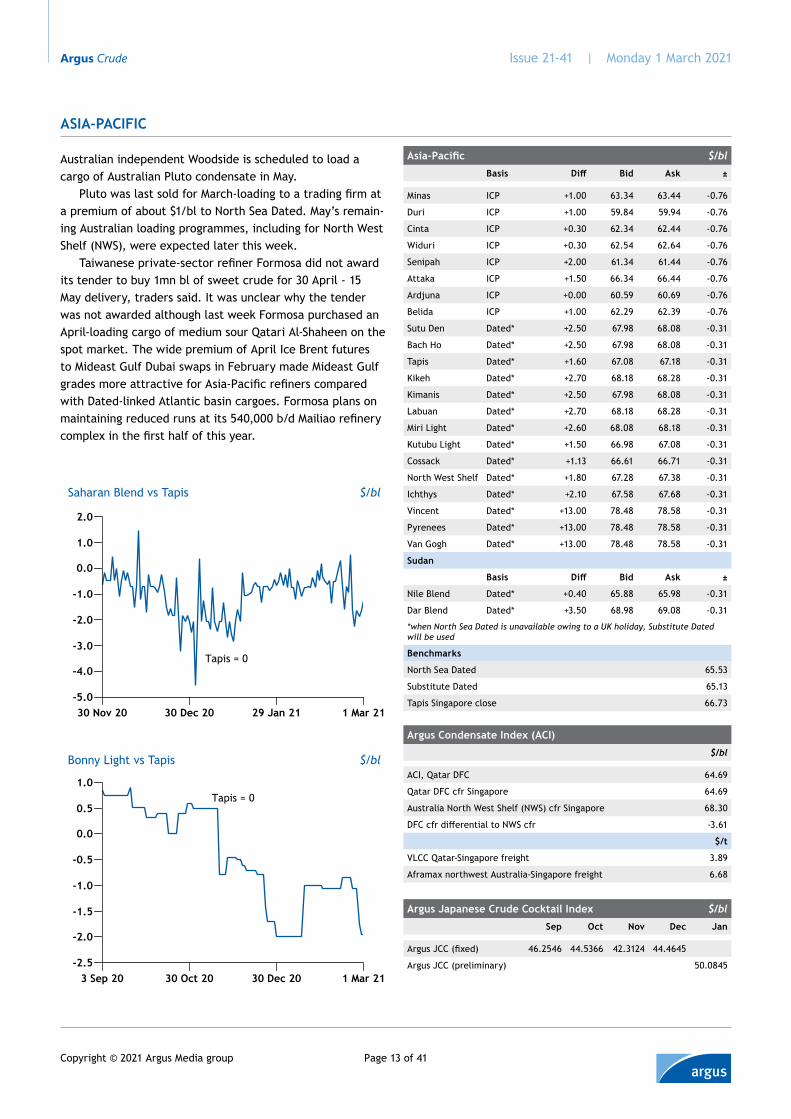

Australian independent Woodside is scheduled to load a cargo of Australian Pluto condensate in May.

Pluto was last sold for March-loading to a trading firm at a premium of about $1/bl to North Sea Dated. May’s remain-ing Australian loading programmes, including for North West Shelf (NWS), were expected later this week.

Taiwanese private-sector refiner Formosa did not award its tender to buy 1mn bl of sweet crude for 30 April - 15 May delivery, traders said. It was unclear why the tender was not awarded although last week Formosa purchased an April-loading cargo of medium sour Qatari Al-Shaheen on the spot market. The wide premium of April Ice Brent futures to Mideast Gulf Dubai swaps in February made Mideast Gulf grades more attractive for Asia-Pacific refiners compared with Dated-linked Atlantic basin cargoes. Formosa plans on maintaining reduced runs at its 540,000 b/d Mailiao refinery complex in the first half of this year.

Argus condensate index (Aci)

$/bl

ACI, Qatar DFC 64.69

Qatar DFC cfr Singapore 64.69

Australia North West Shelf (NWS) cfr Singapore 68.30

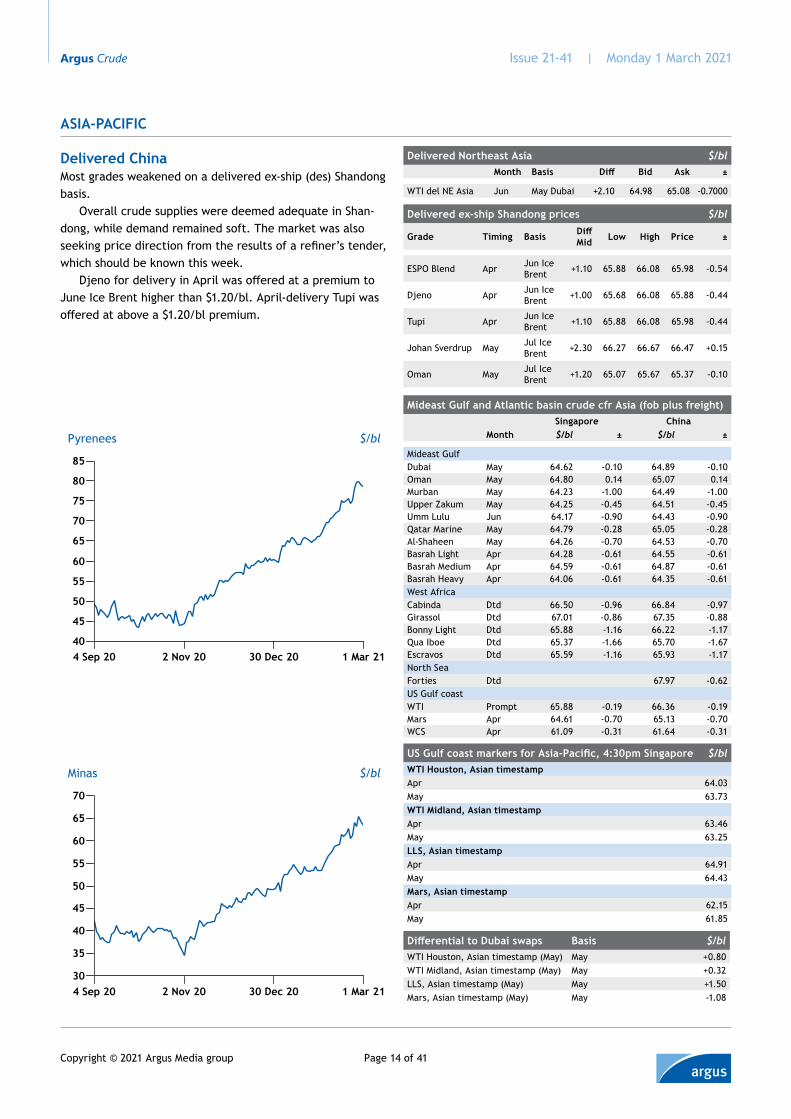

Delivered ChinaMost grades weakened on a delivered ex-ship (des) Shandong basis.

Overall crude supplies were deemed adequate in Shan-dong, while demand remained soft. The market was also seeking price direction from the results of a refiner’s tender, which should be known this week.

Djeno for delivery in April was offered at a premium to June Ice Brent higher than $1.20/bl. April-delivery Tupi was offered at above a $1.20/bl premium.

AsiA-PACifiC

Pyrenees $/bl

hh

40

45

50

55

60

65

70

75

80

85

4 Sep 20 2 Nov 20 30 Dec 20 1 Mar 21

Minas $/bl

hh

30

35

40

45

50

55

60

65

70

4 Sep 20 2 Nov 20 30 Dec 20 1 Mar 21

US Gulf coast markers for Asia-Pacific, 4:30pm Singapore $/blWTI Houston, Asian timestampApr 64.03May 63.73WTI Midland, Asian timestampApr 63.46May 63.25LLS, Asian timestampApr 64.91May 64.43Mars, Asian timestampApr 62.15May 61.85

Differential to Dubai swaps Basis $/blWTI Houston, Asian timestamp (May) May +0.80WTI Midland, Asian timestamp (May) May +0.32LLS, Asian timestamp (May) May +1.50Mars, Asian timestamp (May) May -1.08

Sakhalin Blend May Dubai swaps +1.40 64.28 64.38 -0.70

*Apr-loading cargoes

Russia-caspian crude cif basis singapore

Bid ask ±

BTC Blend 67.78 67.84 -0.23

Urals (Black Sea) 65.84 65.90 -0.31

Dirty freight rates from Kozmino (EsPO) 100,000t $/blRate

To Yosu 0.40

To north China 0.51

To Chiba 0.51

To Singapore 0.53

Urals NWE vs ESPO Blend $/bl

hh

-6

-5

-4

-3

-2

-1

0

1

3 Sep 20 30 Oct 20 30 Dec 20 1 Mar 21

ESPO Blend = 0

ESPO Blend vs ANS USWC $/bl

hh

-2

-1

0

1

2

3

4

28 Aug 20 27 Oct 20 28 Dec 20 1 Mar 21

ANS USWC = 0

Azeri Light vs Tapis $/bl

-4

-3

-2

-1

0

1

2

3

30 Nov 20 30 Dec 20 29 Jan 21 1 Mar 21

India’s state-controlled ONGC sold late April-loading Sokol at a firm premium to Dubai.

ONGC sold the Sokol cargo loading on 27 April - 3 May, to a trading firm via tender at a premium of around $2.60/bl to front-line Dubai assessments in April, on a cfr STS Yosu basis. April-loading Sokol cargoes traded in February at premiums of around $1.85-2.30/bl to Dubai.

Traders said the ONGC cargo was the last Sokol cargo for April-loading and may have prompted the buyer to pay a higher premium. It was unclear where the trading firm plans to take the cargo.

South Korean refiner Hyundai was heard to have taken a cargo of ESPO Blend, at a premium to Dubai on a delivered Korea basis. The cargo was purchased by Saudi Aramco's trading arm ATC through a spot tender, to supply Hyundai, traders said. A Chinese oil firm may have sold the cargo al-though the deal was not confirmed. Aramco has a 17pc stake in Hyundai Oilbank. Hyundai is not a regular buyer of ESPO Blend, but lower prices for April-loading ESPO Blend relative to Mideast Gulf grades like light sour Murban could be one reason for the purchase, traders said.

assessment rationaleESPO Blend fob Kozmino (PA0007196) is assessed on the basis of transactions, as and when these are identified in the mar-ket commentary, in accordance with the methodology.

Abu Dhabi Jan Feb MarMurban premium to Dubai +0.50 +0.75 +0.75Murban 55.27 61.61 naDas premium to Murban -0.35 -0.35 -0.35Umm Lulu premium to Murban -0.05 -0.05 -0.05Upper Zakum premium to Murban +0.00 +0.05 +0.00Qatar Jan Feb MarDukhan/Land premium to Oman/Dubai avg +0.00 +0.40 +0.35Marine premium to Oman/Dubai avg +0.20 +0.70 +0.65Oman Feb Mar AprOman 50.00 54.79 60.85Indonesia Nov Dec JanMinas 42.80 49.47 54.41Duri 47.17 53.35 58.91Widuri 41.64 48.31 53.25Belida 39.68 47.70 53.00Attaka 39.48 47.71 53.08Ardjuna 35.34 45.91 51.00Cinta 41.09 47.76 52.70Senipah 43.00 47.86 54.73Malaysia Nov Dec JanTapis 41.26 49.26 55.83MCO Alpha Premium +0.00 +0.80 +2.25Labuan 42.66 50.66 57.09Miri 42.66 50.66 57.09Kikeh 42.66 50.66 57.09Bintulu 40.46 48.46 56.49Dulang 42.46 50.46 57.65Brunei Oct Nov DecSeria Light 39.08 41.29 49.29Champion 39.13 41.34 49.34

Official formula prices $/blBasis

Saudi Arabia Jan Feb MarSaudi Arabia to US: fob Ras Tanura Berri (Extra Light) ASCI +0.90 +1.10 +1.20Arab Light ASCI +0.55 +0.75 +0.85Arab Medium ASCI -0.15 +0.05 +0.15Arab Heavy ASCI -0.50 -0.30 -0.20Saudi Arabia to US: delivered US GulfBerri (Extra Light) ASCI +2.20 +2.40 +2.50Arab Light ASCI +1.85 +2.05 +2.15Arab Medium ASCI +1.15 +1.35 +1.45Arab Heavy ASCI +0.80 +1.00 +1.10Saudi Arabia to NW Europe: fob Ras Tanura*Berri (Extra Light) Ice Brent Settlement -1.30 -1.80 -0.40Arab Light Ice Brent Settlement -1.40 -1.90 -0.50Arab Medium Ice Brent Settlement -1.80 -2.30 -0.90Arab Heavy Ice Brent Settlement -2.20 -2.70 -1.30Saudi Arabia to Mediterranean: fob Sidi Kerir*Berri (Extra Light) Ice Brent Settlement -0.20 -0.90 +0.50Arab Light Ice Brent Settlement -0.30 -1.00 +0.40Arab Medium Ice Brent Settlement -0.90 -1.60 -0.20Arab Heavy Ice Brent Settlement -1.40 -2.10 -0.70Saudi Arabia to Mediterranean: fob Ras Tanura*Berri (Extra Light) Ice Brent Settlement -0.90 -1.40 -0.10Arab Light Ice Brent Settlement -1.00 -1.50 -0.20Arab Medium Ice Brent Settlement -1.60 -2.10 -0.80Arab Heavy Ice Brent Settlement -2.10 -2.60 -1.30Saudi Arabia to Asia-Pacific: fob Ras TanuraArab (Super Light) Oman/Dubai avg +1.25 +1.85 +1.85Berri (Extra Light) Oman/Dubai avg +0.10 +0.60 +0.60Arab Light Oman/Dubai avg +0.30 +1.00 +1.00Arab Medium Oman/Dubai avg +0.35 +0.75 +0.75Arab Heavy Oman/Dubai avg +0.10 +0.30 +0.30Iran Jan Feb MarIran to Mediterranean: fob Sidi KerirIranian Light Ice Bwave na na naIranian Heavy Ice Bwave na na naForoozan Blend Ice Bwave na na naIran to Mediterranean: fob Kharg IslandIranian Light Ice Bwave -1.65 -2.50 -1.65Iranian Heavy Ice Bwave -2.90 -4.00 -3.20Foroozan Blend Ice Bwave -2.90 -3.95 -3.15Soroush Ice Bwave -6.60 -7.70 -6.90Nowruz Ice Bwave -6.60 -7.70 -6.90Iran to NW Europe: fob Kharg IslandIranian Light Ice Bwave -1.65 -2.50 -1.55Iranian Heavy Ice Bwave -2.80 -3.90 -3.00Foroozan Blend Ice Bwave -2.80 -3.85 -2.95Iran to Asia-Pacific: fob Kharg IslandIranian Light Oman/Dubai avg +0.25 +0.80 +0.85Iranian Heavy Oman/Dubai avg -0.20 +0.05 +0.05Foroozan Blend Oman/Dubai avg -0.20 +0.00 +0.15Soroush Oman/Dubai avg -3.40 -3.35 -3.35Nowruz Oman/Dubai avg -3.40 -3.35 -3.35Kuwait Jan Feb MarKuwait to Asia-PacificKuwait Oman/Dubai avg +0.25 +0.65 +0.65Kuwait to USKuwait ASCI +0.10 +0.05 +0.15Kuwait Arab Medium +0.25 +0.00 +0.00Kuwait to Mediterraneanfob Kuwait Dated -0.40 -1.20 -0.20fob Sidi Kerir Dated +0.30 -0.70 +0.40Kuwait to northwest Europefob Kuwait Dated -1.35 -2.15 -0.95

Reference prices $/bl

Opec reference basket monthly avg Dec Jan FebOpec 49.17 54.38 61.05Argus Japanese Crude Cocktail Index Oct Nov DecArgus JCC 44.54 42.31 44.46The Argus Japanese Crude Cocktail Index is created by Argus based on data pub-lished by the Customs and Tariff Bureau of Japan’s Ministry of Finance.

Official formula prices (continued) $/blBasis

Dubai Mar Apr MayDubai fob Oman MOG OSP -0.25 -0.10 -0.15Yemen fob Salif/Ash ShihrMarib Light Dated na na naMasila Dated na na naIraq Jan Feb MarIraq to EuropeKirkuk (fob Ceyhan) Dated +0.50 -0.30 +0.60Basrah Light Dated -0.50 -1.50 -0.60Basrah Medium Dated -2.05 -3.15 -2.05Basrah Heavy Dated -3.30 -4.50 -3.50Iraq to USKirkuk (fob Ceyhan) ASCI +1.00 +0.90 +0.95Basrah Light ASCI +0.00 +0.05 +0.25Basrah Medium ASCI -0.90 -0.80 -0.50Basrah Heavy ASCI -1.75 -1.75 -1.50Iraq to Asia-PacificBasrah Light Oman/Dubai avg +0.40 +1.10 +1.15Basrah Medium Oman/Dubai avg -0.65 -0.25 -0.15Basrah Heavy Oman/Dubai avg -1.60 -1.40 -1.40*OSPs for pre-2021 export streams†Somo-issued December reference OSPs for its 2021 quality crude export streams

Europe US Asia-PacficBasrah Light Dated -0.60 ASCI +0.20 Oman/Dubai average -0.35Basrah Medium Dated -1.90 ASCI -0.60 Oman/Dubai average -1.15Basrah Heavy Dated -3.00 ASCI -1.40 Oman/Dubai average -2.10

*months prior to July were priced against Ice Bwave

Thunder Horse vs ASCI (5 day MA)Thunder Horse vs WTI (5 day MA)

Mars vs WTI $/bl

hh

-1

-0.5

0

0.5

1

1.5

2

31 Aug 20 28 Oct 20 29 Dec 20 1 Mar 21

WTI = 0

assessment rationaleThe minimum volume was met and volume-weighted average calculated according to the methodology for LLS, Mars, WCS Cushing, WTI Diff to CMA Nymex, WTI Houston, WTI Midland Enterprise, WTI Midland and WTS.The Bakken at Clearbrook assessment was set on the basis of fresh trade. Bakken at Clearbrook sold at a premium of $1.05-$1.20/bl.

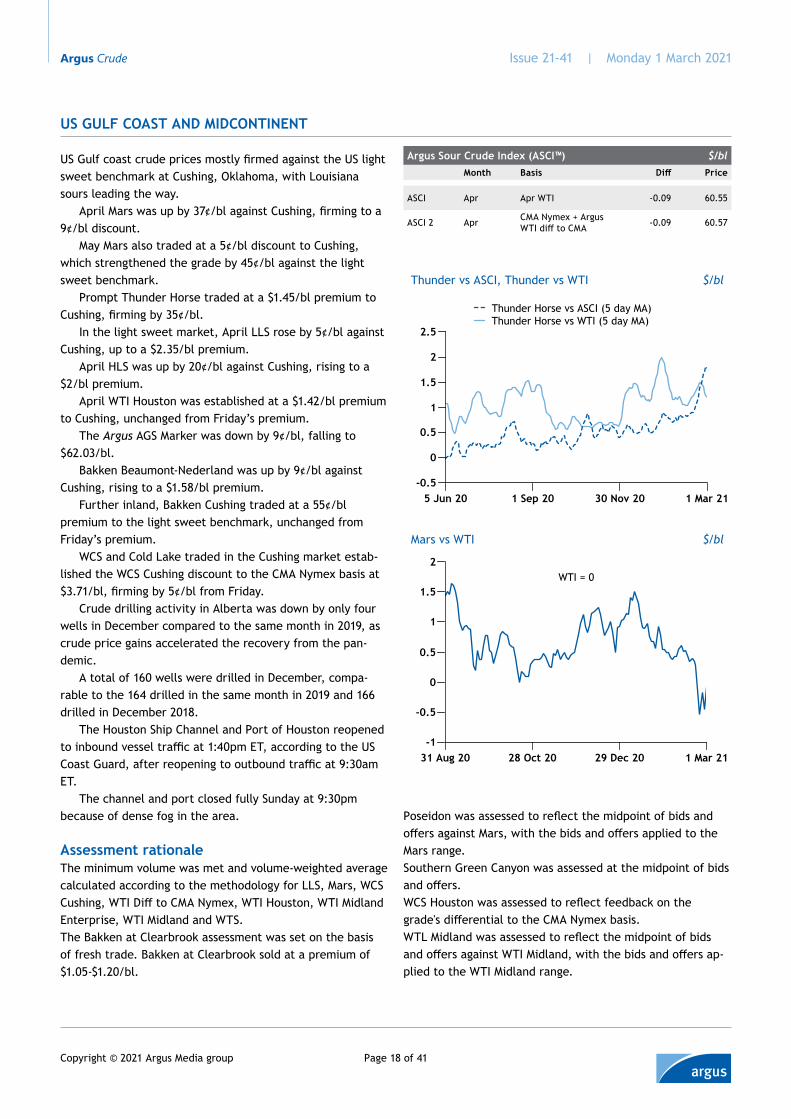

US Gulf coast crude prices mostly firmed against the US light sweet benchmark at Cushing, Oklahoma, with Louisiana sours leading the way.

April Mars was up by 37¢/bl against Cushing, firming to a 9¢/bl discount.

May Mars also traded at a 5¢/bl discount to Cushing, which strengthened the grade by 45¢/bl against the light sweet benchmark.

Prompt Thunder Horse traded at a $1.45/bl premium to Cushing, firming by 35¢/bl.

In the light sweet market, April LLS rose by 5¢/bl against Cushing, up to a $2.35/bl premium.

April HLS was up by 20¢/bl against Cushing, rising to a $2/bl premium.

April WTI Houston was established at a $1.42/bl premium to Cushing, unchanged from Friday’s premium.

The Argus AGS Marker was down by 9¢/bl, falling to $62.03/bl.

Bakken Beaumont-Nederland was up by 9¢/bl against Cushing, rising to a $1.58/bl premium.

Further inland, Bakken Cushing traded at a 55¢/bl premium to the light sweet benchmark, unchanged from Friday’s premium.

WCS and Cold Lake traded in the Cushing market estab-lished the WCS Cushing discount to the CMA Nymex basis at $3.71/bl, firming by 5¢/bl from Friday.

Crude drilling activity in Alberta was down by only four wells in December compared to the same month in 2019, as crude price gains accelerated the recovery from the pan-demic.

A total of 160 wells were drilled in December, compa-rable to the 164 drilled in the same month in 2019 and 166 drilled in December 2018.

The Houston Ship Channel and Port of Houston reopened to inbound vessel traffic at 1:40pm ET, according to the US Coast Guard, after reopening to outbound traffic at 9:30am ET.

The channel and port closed fully Sunday at 9:30pm because of dense fog in the area. Poseidon was assessed to reflect the midpoint of bids and

offers against Mars, with the bids and offers applied to the Mars range.Southern Green Canyon was assessed at the midpoint of bids and offers.WCS Houston was assessed to reflect feedback on the grade's differential to the CMA Nymex basis.WTL Midland was assessed to reflect the midpoint of bids and offers against WTI Midland, with the bids and offers ap-plied to the WTI Midland range.

US Gulf coast prices vs global benchmarks $/bltiming basis Price Differential

WTI Houston May May Dubai swaps* 63.73 +0.80

Apr Jul Ice Brent -0.27

Apr Jul Dubai -0.87

WTI Midland May May Dubai swaps* 63.25 +0.32

Apr Jul Ice Brent -0.79

Apr Jul Dubai -1.39

LLS May May Dubai swaps* 64.43 +1.50

Apr Jul Ice Brent +0.66

Apr Jul Dubai +0.06

Mars May May Dubai swaps* 61.85 -1.08

Apr Jul Ice Brent -1.78

Apr Jul Dubai -2.38

Bakken Beaumont/Nederland Apr Jul Ice Brent -0.32

Apr Jul Dubai -0.92

USGC-China

270,000t 16.30

130,000t 26.92

USGC/Carib-Singapore

130,000t 23.08

USGC-east coast Canada

70,000t 15.16 USGC-Europe

70,000t 20.84

Argus uses today’s US pipeline outright prices at Nymex settlement to cal-culate spreads to today’s Ice Brent settlement and Argus Dubai prices three months forward, to account for travel time from the US to Asia-Pacific.*Outright prices are calculated by applying the previous day’s US pipeline differentials to today’s Singapore Nymex WTI 4.30pm timestamp, to then calculate spreads to Dubai swaps at that timestamp.

US light sweet waterborne crude discounts to Ice Brent were roughly steady this session as offers surfaced for April load-ing cargoes becoming prompt on Friday.

A 720,000 bl cargo of Midland-sourced WTI for loading between 11-30 April was heard offered at an 80¢/bl discount to June Ice Brent this session, though buyer interest could not be confirmed at that level. The low side of WTI fob Houston was assessed at a $1.20/bl discount to the European marker, based on the prior day’s spread to pipeline WTI Houston.

April WTI Houston was unchanged at a $1.42/bl volume-weighted average premium to the US light sweet crude benchmark at Cushing, Oklahoma, or roughly $1/bl under June Ice Brent.

Separately, a cargo of Midland-sourced WTI for loading in March was heard offered at a $1.30/bl discount to May Ice Brent, equivalent to a roughly 65¢/bl discount to June Ice Brent.

A cargo of March loading Eagle Ford crude was mean-while heard offered this session at a $1.60/bl discount to May Ice, equivalent to a roughly $1/bl discount to June Ice Brent.

The midpoint of Bakken fob Beaumont was meanwhile assessed at a $1.20/bl discount the international benchmark to maintain a roughly 20¢/bl discount to waterborne WTI.

Plains All American Pipeline has lifted a force majeure on 15 Texas crude pipelines and gathering systems which had been in place since mid-February following severe winter weather and power outages.

The company has resumed normal operations on the pipeline systems, Plains said in a notice to shippers last ses-

ANS del concurrent Apr Apr WTI +3.13/+3.23 63.77-63.87

ANS vs WTI $/bl

hh

0

1

2

3

4

5

31 Aug 20 28 Oct 20 29 Dec 20 1 Mar 21

WTI = 0

ANS vs Ice $/bl

hh

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

31 Aug 20 28 Oct 20 29 Dec 20 1 Mar 21

Ice = 0

Assessment rationaleThe ANS assessment against CMA Nymex WTI was adjusted to maintain the spread to CMA Ice Brent established when the grade last traded.

ANS del USWC monthly volume-weighted average $/blBasis Diff

Jan Ice CMA -0.50

Feb Ice CMA +0.32

Mar Ice CMA +0.35

Apr MTD Ice CMA +0.28

US waterBorne

sion. The force majeure was lifted for: the Cactus pipeline,

the Alpha Crude Connector, Sunrise 2 pipeline, the Basin system, the Iatan gathering system, the McCamey pipeline, the Mesa pipeline, the Midland South pipeline, the Spraberry pipeline system, the Pinon pipeline, the Scurry pipeline, the Mesa pipeline, the Permian basin system, the west Texas gathering system and the Wolverine gathering system.

Separately, offers are due 9 March for a term tender by Sri Lanka's state-owned refiner Ceypetco to buy 8.4mn bl of light crude for delivery to the port of Colombo between June 2021 and February 2022 in which Midland-sourced WTI will compete with Algerian Saharan Blend, Abu Dhabi Das Blend and Murban crude.

Ceypetco lists three possible options for potential sell-ers in its latest term tender, with the first being 12 ship-ments each of 700,000 bl of Murban. The second option is a combination of nine 700,000 bl cargoes of Murban and three 700,000 bl cargoes of either Saharan Blend or WTI.

The third option calls for eight 700,000 bl cargoes of Das Blend crude and four 700,000 bl cargoes of either Saharan Blend or WTI.

In shipping news, Indian private-sector refiner Nayara placed the Suezmax Silverway on subjects to load a possible cargo of WCS or Cold Lake crude from Beaumont, Texas, to western India around 14 March, according to this morning’s fixture reports.

Argentinian heavy sweet Escalante firmed Monday on the back of a recent sale and following higher prices for similar-quality African crudes.

April-loading Escalante was assessed at between $1.65/bl and $2.15/bl over June Ice Brent. The price climb mirrors that of Angolan heavy sweet Dalia crude which firmed in the last two weeks over its benchmark North Sea Dated.

Mexico’s March formula adjustments went into effect Monday with the K-factor for heavy sour bellwether Maya crude to the US Gulf coast, Americas' Atlantic coast and the Caribbean widening to a $3.85/bl discount in March from a $3.35/bl discount in February. Maya to the US west coast and Americas' Pacific coast will deepen to a $4.65/bl discount from a $4.15/bl discount.

Maya bound for Europe, India and the Middle East will narrowed to a $4.75/bl discount in March from a $5.10/bl discount in February, while Maya cargoes to Asia-Pacific will narrowed slightly by 5¢/bl to a $3.60/bl discount.

Ecuadorean state-owned PetroEcuador will next session close a pair of tenders offering medium sour Oriente and heavy sour Napo crude for March-loading from the port of Esmeraldas.

The South American company was heard offering four 360,000 bl cargoes of Oriente and two 360,000 bl cargoes of Napo. This will be the third consecutive month that PetroEc-uador issues tenders for the crudes whose spot volumes have until recently been scarce amid oil-backed agreements with Asia-Pacific companies.

Separately, shipping fixtures Monday indicate ExxonMo-bil plans to charter the Suezmax Front Coral from Guyana to the Caribbean or the US Gulf coast. Brazilian state-run Petrobras placed on subjects the Suezmax Marlin Somerset from Brazil to Singapore or other options starting 14 March. The company also fixed the Suezmax Advantage Sun from Brazil to Europe or Chile starting 17 March.

Heavy sour crude was down slightly while bidding interest returned to condensate markets in the first session of the April trade window.

April-delivery of Western Canadian Select (WCS) at Hardisty, Alberta, saw its outright price slip below $50/bl for the first time in four sessions, settling at an implied $48.99/bl. This is down by $1.10/bl day-over-day as both a widening differential and sliding basis weighed on Canada’s heavy sour benchmark.

The differential for April WCS was assessed 30¢/bl lower to start the week as liquidity returned to the market. WCS’ discount of $11.25/bl to the April Nymex WTI CMA is the strongest start to the April trade cycle since 2019 when a $10.50/bl discount was recorded. The current outright price remains more than $3/bl higher compared to that time.

Condensate at Edmonton, Alberta, was assessed at a $1.60/bl premium to the April CMA. This is the highest dif-ferential since 10 March last year and the first time over $1/bl since October.

South of the Border, Bakken at Clearbrook, Minnesota, traded between a $1.05-1.20/bl premium to the April basis. At least 5,000 b/d traded at this level which is the highest differential since May of last year.

In upstream news, crude drilling activity in Alberta was down by only four wells in December compared to the same month in 2019, as crude price gains accelerated the recovery from the pandemic.

A total of 160 wells were drilled in December, compa-rable to the 164 drilled in the same month in 2019 and 166 drilled in December 2018. Drilling was down by 15 wells from November, not uncommon as activity typically slumps to close the year, according to statistics from the Alberta Energy Regulator (AER) dating back to 2000.

Canada waterborne prices $/bl

Timing Basis Diff low/high Low/High

Hibernia Dated North Sea -0.80/-0.30 64.73/65.23

Terra Nova Dated North Sea -0.90/-0.40 64.63/65.13

Assessment rationaleThe minimum volume was met and volume-weighted average calculated according to the methodology for WCS Houston.WCS Houston was assessed to reflect feedback on the grade's differential to the CMA Nymex basis.

Canada domestic $/bl

Timing Basis Diff low/high Low/High

Condensate Apr CMA Nym +1.35/+1.85 61.59/62.09

MSW Apr CMA Nym -2.15/-1.65 58.09/58.59

LSB Apr CMA Nym -2.15/-1.65 58.09/58.59

LLB Apr CMA Nym -11.25/-9.35 48.99/50.89

Drilling activity had been on the upswing since hitting a record low of only four wells drilled in April. But the gap between previous years remained wide, peaking in August when drilling typically starts to pick up. Only 299 wells drilled that month, 269 fewer than in August 2019.

There were 70 wells targeting bitumen in December, up by 64 from December 2019 but down from 108 in November.

Canadian pipeline Mar 21 trade monthCumulative trade month weighted average

Syncrude (SPP) Pembina AOSP at Edmonton PA0008308 0.00WCS Husky at Hardisty PA0008320 -12.70

Differential to CMA Nymex

Bakken (Canadian Pipeline Schedule) Clearbrook, Minnesota PA0009012 -1.68Note: This table is licensed for use by authorized users and may not be redistributed without seeking additional licenses. By reading this publication you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of the publisher. The data and other information published in the above table are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, ad-equacy, timeliness, or completeness of the data or fitness for any particular purpose. Prices included in this table are subject to change or correction after publication. The averages are trade-day averages of prices published for the trade month listed. Argus only publishes on days when the New York Mercantile Exchange is open for trade, and so only those days are averaged. Weekends and holidays are not included. The trade month is the period beginning with the 26th day of the month that is two months prior to the month of delivery through and including the 25th day of the month immediately prior to the month of delivery. Should the first day of the trade month fall on a day when the market is closed, the trade month will begin on the first trading day thereafter. Should the last day of the trade month fall on a day when the market is closed, the trade month will end on the last trading day prior. The absolute prices for Argus US domestic crude grades are calculated using the Argus “WTI Formula Basis” value. The “WTI Formula Basis” average plus the crude grade’s differential average equals the absolute price for the crude grade. The “WTI Formula Basis” price is an average of the Nymex WTI settlement price from the 26th of the month up to and including futures expiry, and the Argus WTI Cushing price from the day following futures expiry up to and including the 25th of the month. Each price component is rounded independently. Discrepancies due to this independent rounding must be accommodated by the user.

Monthly data corrections

Grade Location PA code Publication date

Published diff

Corrected diff

Published price

Corrected price

Bakken Beaumont/Nederland Beaumont/Nederland, Texas PA0022255 25 Feb 64.76 64.77

Northwest Europe North Sea 1 Mar 21 May 100,000 65.05Northwest Europe North Sea 1 Mar 21 May 100,000 65.06Northwest Europe North Sea 1 Mar 21 May 100,000 65.09Northwest Europe North Sea 1 Mar 21 Jun 100,000 63.34Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea +0.05 8 Mar 21 12 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea +0.03 8 Mar 21 12 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 200,000 May North Sea - 0.10 15 Mar 21 19 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 500,000 May North Sea - 0.10 15 Mar 21 19 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea - 0.15 15 Mar 21 19 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea - 0.20 22 Mar 21 26 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 200,000 May North Sea - 0.19 22 Mar 21 26 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 300,000 May North Sea - 0.19 22 Mar 21 26 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea - 0.16 22 Mar 21 26 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 May North Sea - 0.16 22 Mar 21 26 Mar 21Northwest Europe North Sea Dated CFD 1 Mar 21 100,000 Jun North Sea +0.35 29 Mar 21 1 Apr 21

Plains lifts force majeure on texas pipelinesPlains All American Pipeline has lifted a force majeure on 15 Texas crude pipelines and gathering systems which had been in place since mid-February following severe winter weather and power outages.

The company has resumed normal operations on the pipe-line systems, Plains said in a 26 February notice to shippers.

The force majeure was lifted for: the Cactus pipeline, the Alpha Crude Connector, Sunrise 2 pipeline, the Basin system, the Iatan gathering system, the McCamey pipeline, the Mesa pipeline, the Midland South pipeline, the Spraberry pipeline system, the Pinon pipeline, the Scurry pipeline, the Mesa pipeline, the Permian basin system, the west Texas gathering system and the Wolverine gathering system.

Plains issued the force majeure on 15 February “due to the ongoing impacts from the below-freezing temperatures, ice and snow from the winter storm, which has caused power outages, road closures, and other delays which are impacting operations of the pipeline systems.” The company warned shippers that the force majeure "may cause shippers to see reductions to nominations for February.”

The cold snap that crippled Texas' power grid cut deeply into US crude production and refining, but the impact may be relatively short-lived.

US oil output fell by 1.1mn b/d, or 10pc, in the week ended 19 February, according to Energy Information Adminis-tration estimates. Refinery inputs fell more steeply as wide-spread power cuts and natural gas curtailments forced many units to shut. US Gulf coast refinery processing fell by 27pc

to 6mn b/d — the lowest since Hurricane Harvey flooded the Texas coast in September 2017.By Eunice Bridges

Trafigura to supply crude to Lindsey refineryUK-based Prax Group said today that it has agreed a crude and feedstocks supply deal with trading firm Trafigura for the 110,000 b/d Lindsey refinery in northeast England.

Under the agreement, all the crude and refinery feed-stocks for Lindsey will come from Trafigura. No other details were forthcoming.

Prax took control of Lindsey from Total today, upon completion of a deal initially agreed in late July last year. It had been to close by the end of 2020.

The acquisition is part of a "long-term strategy to be fully integrated across the oil value chain" in the UK, Prax said. It does downstream marketing and distribution through its Harvest Energy brand.By Saleem Rizvi

announcement

Argus Sour Crude Index (“ASCI”)Proportional assessmentFollowing the end of the first trading quarter of 2021 and in accordance with the ASCI price methodology, Argus has revised the proportionality assigned to Mars, Poseidon and SGC to be used in the event that the combined volume minimum of 6,000 b/d is not met in any given trade day. The latest proportional assessment values are based on the volume of trade over the last six trade months and will be applicable for the next three trade months starting 26 February 2021 and ending 25 May 2021 Each grade has been assigned the following percentage values:

� Mars: 67pc � Poseidon: 27pc � SGC: 6pc

A table containing a history of the proportional assess-ment values can be found in the ASCI price methodol-ogy, which is available at http://www.argusmedia.com/asci. If you have any questions or would like to comment on these changes, please contact Gustavo Vasquez at [email protected] and (713) 968-0014, or Amanda Smith at [email protected] and (713) 968-0013.

announcement

Argus successfully completes annual Iosco assurance review Argus has completed the ninth external assurance review of its price benchmarks covering crude oil, products, LPG, petrochemicals, biofuels, thermal coal, coking coal, iron ore, steel, natural gas and biomass benchmarks. The review was carried out by profes-sional services firm PwC. Annual independent, external reviews of oil benchmarks are required by international regulatory group Iosco’s Principles for Oil Price Report-ing Agencies, and Iosco encourages extension of the re-views to non-oil benchmarks. For more information and to download the review visit our website https://www.argusmedia.com/en/about-us/governance-compliance

US keeps offer of Iran talks The US still sees a diplomatic path forward to reviving the Iran nuclear deal, despite Tehran's initial rejection of EU-sponsored talks.

President Joe Biden's administration last month offered to join talks with Tehran hosted by the EU and the Euro-pean members of the Joint Comprehensive Plan of Action (JCPOA) nuclear deal — France, Germany and the UK. Tehran rejected the proposal yesterday, demanding relief of US sanctions as a precondition for talks.

"We are disappointed in Iran's response," the White House said today, but added that the US is ready to "reengage in meaningful diplomacy to achieve a mutual return to compli-ance with JCPOA commitments."

For now, it appears that Washington and Tehran continue to publicly frame their future negotiations, keeping a path-way to a diplomatic solution while maintaining hardline posi-tions. The timing and prospect of the US return to the Iran nuclear deal is relevant for oil markets, as it would involve the lifting of US sanctions that since 2018 cut off more than 2mn b/d of Iranian crude exports.

"The path forward is quite clear: The US must end its unlawful and unilateral sanctions and return to its JCPOA commitments," Iran's foreign ministry said yesterday. Imple-mentation of commitments by all parties to the JCPOA is not a matter of negotiation and give and take, it said.

In turn, the White House said it will hold consultations with the remaining JCPOA members. Biden's administra-tion says it will not lift sanctions or provide an economic lifeline to Tehran to facilitate talks.

"What we are seeing is a little bit of a test of wills — I believe the Iranians truly do want to come back to the JCPOA, but they are really trying to test the Biden admin-istration. They are trying to see how desperate is Biden to rejoin the JCPOA," Harvard University's geopolitics of energy project direct Meghan O'Sullivan told the CERAWeek by IHS Markit conference today.

Biden's administration early on took steps to defuse confrontation with Iran in hopes it would help facilitate outreach to Tehran. But tensions are rising in the Middle East again. The Pentagon on 25 February carried out mis-sile strikes in eastern Syria against what it said were camps occupied by Iran-backed militias that the US concluded were behind a 15 February attack in northern Iraq that injured US military personnel. And Israeli prime minister Benjamin Ne-tanyahu, who fiercely opposes the US' return to the JCPOA, today blamed Iran for an explosion on an Israeli-owned ves-

sel in the Gulf of Oman last week.The timing of the Syria attack and accusations leveled by

Washington against Tehran may be behind Iran's initial rejec-tion of talks. "“In view of the recent stances and measures taken by the US and the three European countries, the Islamic Republic of Iran believes this is not a good time for holding an unofficial meeting on the accord as proposed by the EU foreign policy chief, Josep Borrell," Iran's foreign ministry said.By Haik Gugarats

Somo crude exports up in FebruaryIraqi crude exports marketed by federal company Somo were up by 3pc on the month to 2.96mn b/d in February, driven by increases in Basrah shipments, Iraq’s oil ministry said.

Combined Basrah crude loadings rose by 2pc on the month to 2.83mn b/d on February. The oil ministry signalled just last week that monthly grade exports for most of Febru-ary were at a lower 2.7mn b/d.

Somo-marketed Kirkuk blend volumes dropped by 36pc on the month to 63,000 b/d in February. The company’s figures do not capture the majority of Kirkuk blend supplies, which are sold by the Kurdistan Regional Government (KRG).

Somo’s revenues rose by 5pc to around $5bn in Febru-ary, while the company achieved an average crude price of $60.33/bl on the month, up by 13pc from January. By Ruxandra Iordache

Abu Dhabi appoints Adnoc board Abu Dhabi’s crown prince Mohammad bin Zayed al-Nahyan, issued a decree today forming a new board of directors and executive committee for state-owned energy giant Adnoc.

The use of an executive committee is usually to expedite decision making and maintain oversight over the day to day management on a regular basis. In Adnoc’s case, the forma-tion of the board and committee could be an indication of plans to increase activity, one UAE-based consultant said.

The board of directors will be chaired by Sheikh Mohammad, but also includes his son, Sheikh Khalid bin Mohammad, as well as his full brothers, Hazza bin Zayed and Mansour bin Zayed.

Sultan al-Jaber, Adnoc’s current CEO, is also represented on the committee, alongside Khaldoon al-Mubarak, the CEO of sovereign wealth fund Mubadala. Al-Jaber, who is also the UAE’s minister of industry and advanced technology, was named the company’s managing director in a separate decree. He retains his position as chief executive officer.

UAE minister of energy and infrastructure Suhail al-Maz-rouei is also on the board, as well as secretary general of Abu

Dhabi Executive Council Ahmed al-Mazrouei, Adnoc chief fi-nancial officer Jassem al-Zaabi, minister of state and chairman of Abu Dhabi Global Market Ahmed al-Sayegh and chairman of Abu Dhabi Department of Energy Awaidha al-Marar.

The new Adnoc executive committee will be chaired by Sheikh Khaled, and also includes al-Jaber, Mubarak, Zaabi, Mazreoui and al-Sayegh.

Adnoc previously reported to the Supreme Petroleum Council (SPC), which was merged into a new entity, the Supreme Council for Financial and Economic Affairs(SCFE) in late-December to oversee the emirate's overall economic affairs, including the management of oil and gas resources. The SCFE is chaired by UAE president Khalifa bin Zayed al-Nahyan, while Sheikh Mohammed is the vice chairman. The ill health of the president, however, has left Mohammed bin Zayed as the de facto ruler of Abu Dhabi.

The SPC would oversee the work of state-owned Adnoc, in-cluding setting its budgets and approving contracts with interna-tional oil companies such as BP, Total and China's CNPC. Adnoc’s latest capital spending plan for the next five years, stands at $122bn, as it works to boost long-term production capacity to 5mn b/d by 2030 from around 4mn b/d currently. Abu Dhabi also hopes to develop new technically challenging gas resources that would enable the UAE to transition from a net gas importer to an exporter and pursue gas-to-chemicals growth opportunities.By Adal Mirza

Buzzard share of Forties crude declinesThe North Sea's Forties crude stream was slightly lighter and sweeter last week, as the Buzzard field share of the grade fell.

Buzzard accounted for 21pc of unstabilised Forties produc-tion in the week to 28 February, down from 26pc the week be-fore, according to Forties Pipeline System (FPS) operator Ineos.

A 21pc Buzzard contribution yields a Forties blend with a gravity of around 40.9°API and sulphur content of about 0.56pc.

Ineos expects Buzzard's contribution to average 25.2pc

this month, which would give Forties an average gravity of around 40.3°API and sulphur content near 0.62pc. Forties quality will be slightly sweeter and lighter next month as Ineos forecast a 23.5pc Buzzard contribution.

UK crude production down in JanuaryThe UK's crude production declined in January, when domes-tic demand was constrained by a third national lockdown.

Production averaged 860,000 b/d, down by 9pc from December's revised 945,000 b/d and around 18pc below the 1mn b/d achieved in January 2020, according to lat-est government figures.

The figure for January suggests that total UK liquids output averaged 932,000 b/d in January, down by 8pc from December, with the latest national lockdown playing a part in the decline.

Output fell at key assets. Crude production at Buz-zard — the UK's largest field, which feeds into the For-ties benchmark crude stream — fell by around 4pc on the month to 315,000 b/d in January, according to Forties Pipeline System (FPS) operator Ineos.By Riyan Zerrouki

North Sea quality premiums drop in AprilThe Argus Quality Premiums (QP) for North Sea benchmark crude grades loading in April will drop from those for loading in March.

The April QPs for Oseberg and Ekofisk will drop by 8¢/bl and 5¢/bl, respectively, to 24¢/bl and 18¢/bl. Troll's QP will fall to 41¢/bl from 48¢/bl.

QPs are calculated at 60pc of the difference between each grade and the most competitive Brent, Forties, Oseberg, Ekofisk or Troll grade in the second month prior to the month of loading.

QPs compensate sellers for settling North Sea forward contracts using Ekofisk, Oseberg or Troll cargoes rather than Forties, which is usually of a lower value. The lower the QP, the less likely that a cargo of one of these three grades will be used to settle a forward contract. The differential — with QP deducted — is also used to set North Sea Dated as the lowest priced of the five benchmark grades.

The Quality Adjustments (QA) that Argus uses in the calculation of its New North Sea Dated price will also move lower. QAs are calculated in the same way as QPs but use an expanded basket of crude grades.

The Ekofisk QA will fall by 6¢/bl on the month to 42¢/bl in April, and the Troll and Oseberg QAs will both fall by 8¢/bl to 65¢/bl and 48¢/bl, respectively.

The QAs for Nigerian grades Qua Iboe and Bonny Light will drop by 17¢/bl and 18¢/bl, respectively, to 43¢/bl and 46¢/bl.

iNDUSTRY NewS

Change to CPC Blend fob terminal netback methodologyFollowing consultation, Argus will change its CPC Blend fob Terminal netback methodology from 8 March. Argus will assess freight costs specifically for voyages originat-ing at the terminal, rather than using a Novorossiysk rate minus a CPC Terminal discount. Insurance and demurrage costs will continue to be added. Argus will also apply freight costs for 80,000t vessels, rather than for 135,000t vessels.

New North Sea Dated is based on fob assessments of the five existing Dated grades, along with the freight-adjusted values of cif-Rotterdam priced US WTI, as well as Bonny Light and Qua Iboe. Argus deducts a QA from Ekofisk, Oseberg, Troll, Bonny Light and Qua Iboe when establishing which grade is the cheapest.By Riyan Zerrouki

Dutch liquids production fell in 2020Dutch liquids output hit a new low in 2020, at an average of 17,600 b/d. Crude and condensate production was down by 5pc from 2019 and 32pc below the average of the past five years, according to Nlog, which provides production data on behalf of the economy ministry.

The country's production has been declining for several years and even though a new asset — the Q16-Maasmond or Charlie-North — coming on stream in September last year, output will probably continue to decline.

The Netherlands' monthly liquids production fell by 6pc to 19,300 b/d in December, of which around 87pc or around 16,800 b/d was crude. This was 6pc below November’s aver-age, but 4pc above the same month the previous year.

Field-by-field data show that output fell at several Dutch as-sets, but that this was partly offset by increased output at the country's largest fields Schoonebeek Olie and Amstel. Schoone-beek Olie produced 7,400 b/d of crude in December, compared with 7,200 b/d the month before. Amstel production was higher by 9pc on the month at 2,300 b/d in December.By Riyan Zerrouki

Kozmino ESPO Blend exports may rise in AprilSeaborne exports of ESPO Blend crude from Russia’s Kozmino port could rise to an 11-month high of 2.82mn t (696,000b/d) in April, according to a preliminary loading programme.

This would be the highest export volume since May 2020 when 766,000 b/d of ESPO Blend was exported from Kozmino. Scheduled March exports from Kozmino are on course to reach 668,000 b/d, after a cargo was added to the programme late last month.

The April Kozmino programme comprises 24 cargoes of 100,000t each and three cargoes of 140,000t. Russian producers Surgutneftgaz and Rosneft will each load eight cargoes from Kozmino in April, Paramount Energy will load seven while state-controlled Gazpromneft and private-sector Lukoil will each load two. Lukoil is due to load two 140,000t cargoes while Gapromneft is expected to load the remaining one. If there are no changes in the April loading programme, it would be the first time since October 2019 that three 140,000t cargoes load from Kozmino in a month.

The rise in Kozmino exports in April could be due to lower domestic demand ahead of spring refinery mainte-nance season in Russia.

The majority of April-loading ESPO Blend cargoes from Kozmino were sold last month. April-loading ESPO Blend traded at premiums of $1.35-2.23/bl to front-month Dubai assessments on a fob Kozmino basis, up from premiums of 55¢-$1.58/bl to Dubai for March-loading cargoes. April-load-ing cargoes likely achieved firmer premiums due to a steep backwardation in benchmark Dubai. The wide premium of Brent to Dubai also made Dubai-linked grades such as ESPO Blend more attractive for Asia-Pacific refiners.By Yvette Choo

iNDUSTRY NEwS

Change to Urals Mediterranean assessmentsFollowing consultation, on 1 June 2020 Argus will change its Urals Mediterranean 80,000t and 140,000t crude as-sessments to expand the range of allowable cargo sizes and to include supplies of Baltic Urals in the reporting of delivered Mediterranean prices.

Under this proposal: � The Urals Med 80,000t assessment will be renamed

Urals Med Aframax, and will include cargoes in an 80,000-100,000t range. The location and timing of the assessment remain unchanged — cargoes will be as-sessed on a cif Augusta, Italy, basis for loading 10-25 days ahead. Pre-loaded cargoes will continue to be considered for inclusion in the assessment, if they are accepted by buyers as meeting their requested loading dates. For the avoidance of doubt, the proposed change will effectively allow deliveries of Baltic Sea Urals to contribute towards the Urals Mediterranean Aframax assessment.

� The Urals Med 140,000t assessment will be renamed Urals Med Suezmax. The basis, timing and cargo size of the assessment will not change.

� The Siberian Light assessment will include cargoes in an 80,000-85,000t range. The basis and timing of the as-sessment will not change.

� The Urals fob Novorossiysk 80,000t netback will be renamed Urals fob Novorossiysk Aframax, and will be the netback value of 80,000-100,000t cargoes.

� The Urals fob Novorossiysk 140,000t netback will be renamed Urals fob Novorossiysk Suezmax, and will be the netback value of 140,000t cargoes.

Congolese crude exports to fall in AprilExport loadings of crude from Congo (Brazzaville) will fall to 215,000 b/d in April from the 237,000 b/d planned in March, according to programmes.

Exports of flagship grade Djeno will slide to 184,000 b/d on six shipments in April. This is one cargo fewer than planned for March's 208,000 b/d.

One cargo of N'Kossa is scheduled for a total of 31,000 b/d, broadly unchanged on the month. The cargo is sched-uled to load on 22-23 April.

The combined Djeno and N’Kossa tally of 215,000 b/d is the lowest planned export amount since 2017.

Congo's Opec+ production cap is 269,000 b/d for March. The group will meet this week to decide on April quotas.By Andy Devine

Chad's Doba exports flat in AprilLoadings of Chad’s flagship grade Doba have been sched-uled flat on the month at 123,000 b/d in April, according to market participants.

Four cargoes of Chad’s heavy sweet Doba are scheduled in April. Chinese company CNPC's local subsidiary CNPCIC will market three cargoes to load on 4-5, 18-19 and 25-26 April, traders told Argus. Taiwan's state-owned CPC is set to market a cargo loading on 11-12 April.By Andy Devine

Netanyahu blames Iran for vessel blastIsraeli prime minister Benjamin Netanyahu today has blamed Iran for an explosion on an Israeli-owned vessel in the Gulf of Oman last week, further stoking regional tensions.

The Helios Ray, a car carrier vessel owned by an Israeli investment firm with the same name, was af-fected by an explosion late on 25 February, according to security company Dryad Global.

“This is indeed an action of Iran. It is clear,” Netanyahu told state-owned Kan Radio early this morning. “It is Israel’s biggest enemy and we are beating it in the whole region,” he said.

Asked if Israel would respond, Netanyahu only reiterated that Iran “will not have nuclear weapons — with or without an agreement.” He was referring to the 2015 nuclear deal, which the US has suggested it would be open to returning to after former US president Donald Trump exited the deal in 2018. Tensions in the region are already high due the esca-lating nuclear dispute between Tehran and Washington DC.

Later this morning, Tehran rebuked the Israeli premier’s comments and dismissed them outright. “The Persian Gulf and Oman Sea is our immediate area of security and we will not allow them to intimidate us,” Iran’s foreign ministry spokesman

Saeed Khatibzadeh said. “Netanyahu is suffering from a panic disorder about Iran… When it comes to security, Israel knows that Iran’s response will be accurate and technical.”

The Helios Ray was located around 44 nautical miles northwest of the Omani capital of Muscat when the incident occurred. It anchored in Dubai on 27 February, according to vessel tracker MarineTraffic.

Although the vessel in question is not a tanker, the Gulf of Oman is the main artery for oil exports from the Mideast Gulf.

An explosion on an oil product tanker in the Saudi Ara-bian port of Jeddah late last year, as well as damage to four tankers close to UAE territorial waters and a drone strike on two Saudi Arabian pumping stations in May 2019, have con-tributed to heightened security concerns in the region. By Nader Itayim

Australian exploration spend at 16-year low Oil and gas exploration spending in Australia dropped

to a 16-year low in calendar 2020 on a plunge in offshore exploration activity last year when spending fell to its low-est in 29 years. But onshore spending rose to a five-year high, according to the latest official quarterly data. Total oil and gas exploration spending for both onshore and offshore fell by 28pc in calendar 2020 compared with 2019 to the lowest annual exploration spend since A$917.6mn in 2004 when offshore spending dominated, according to mineral and petroleum exploration data for October-December from the Australian Bureau of Statistics (ABS).

Offshore upstream spending dropped by 52pc on the year in 2020 and was around 89pc below the A$3.32bn spend in 2014. It was the lowest offshore spend since A$341.7mn in 1991, the ABS data showed.

By contrast, onshore upstream spending rose to A$604.9mn in 2020 from A$585.8mn in 2019 and was the highest onshore spend since A$904mn in 2015, according to the latest data.

Offshore spending was more impacted than onshore upstream exploration expenditure by the effects of the Covid-19 pandemic because of a plunge in oil prices in early 2020 and restrictions on worker travel to offshore plat-forms where social distancing was more challenging than for onshore exploration activities.

Australian upstream firms such as Woodside Petroleum and Santos deferred spending for exploration and project devel-opment earlier last year in response to weaker oil and gas prices at the time, although energy prices started to recover in the October-December quarter, leading to a rise in offshore exploration spending in the last three months of 2020, it said.

The decline in offshore spending was reflected in lower expenditure in Australia’s largest offshore oil and gas pro-

ducing state of Western Australia, where spending dropped to a 23-year low of A$421mn in 2020. By contrast, the rise in onshore expenditure underpinned an increase in exploration spending in Queensland, Australia’s largest gas-producing state, where most of the gas produced is used as feedstock for the three LNG plants located at the port of Gladstone.

The decline in exploration spending is heavily influenced by oil price expectations. Ice Brent crude prices averaged around $41.96/bl last year, down from $64.30/bl in 2019 and the lowest average since $38.26/bl in 2004.By Kevin Morrison

Nigeria's Seplat to maintain output in 2021Nigerian upstream firm Seplat Petroleum said it aims to pro-duce 48,000-55,000 b/d of oil equivalent (boe/d) this year, similar to its 2020 output that rose by 10pc on the year.

Seplat reported working-interest production of 51,183 boe/d in 2020, within its guidance range and up by 10.1pc from 46,498 boe/d in 2019. The rise, which came in a year that Opec+ cuts curtailed Nigerian output and in which demand slumped because of the Covid-19 pandemic, was mainly the result of contributions from recently-acquired Eland assets.

Considering Opec+ quotas, the firm's 2021 production guidance is 48,000-55,000 boe/d, similar to its 2020 guid-ance of 47,000-57,000 boe/d, although it said that this is "subject to market conditions."

Seplat's 2021 capex is for around $150mn, focusing on gas projects and an exploration well. The firm increased its capex by 20pc last year to $120mn.

Seplat's fully-funded joint ANOH project with the Nigerian Gas Company is underway, with major gas processing units scheduled for delivery in the third quarter of this year and first gas expected in the first half of 2022. Six production wells will be drilled, four of which will be completed this year. Seplat chief executive Roger Brown said that the project will facilitate "Nigeria’s transition away from spending scarce foreign cur-rency on imported, expensive, high-emission diesel-generated electricity" to cleaner and cheaper generation fuels.

Seplat reported revenue of $530.5mn in 2020, down by almost a quarter from $697.8mn in 2019, primarily a result of lower oil prices. It made a loss of $85.3mn, compared with a profit of $277mn in 2019.By Saleem Rizvi

Woodside pauses Burmese activity Australian independent Woodside Petroleum plans to reduce its presence in Myanmar (Burma) and demobilise its offshore exploration drilling team in the coming weeks amid escalat-ing civil unrest in the country.

“Until we see the outlook for Myanmar and its politi-cal stability has improved, Woodside will keep all business decisions under review,” the company said. Woodside does not have any direct commercial arrangements with any of Myanmar’s armed forces organisations, it said.

The statement, on 27 February, came a day before a major escalation in violence following the military takeover and the arrest of the country’s elected leaders at the start of February. At least 18 protestors were killed yesterday, the UN said, by far the worst death toll so far.

The US government said it was alarmed by the latest violence, which it described as an escalation of the secu-rity forces’ crackdown on pro-democracy protestors. “We are preparing additional actions to impose further costs on those responsible for this latest outbreak of violence and the recent coup,” national security adviser Jake Sullivan said.

Washington imposed sanctions on individuals involved in the coup last month.

Woodside’s main interest in Myanmar, where it has been operating since 2013, is in several offshore exploration blocks. In January it started its fourth drilling campaign, including on its exploration block A-7 and in AD-1 and AD-8.By Kevin Morrison and Kevin Foster

NYSE to delist China’s CNOOCThe New York Stock Exchange (NYSE) is moving ahead with plans to delist Chinese state-controlled energy firm CNOOC, in line with an executive order issued by previ-ous US president Donald Trump.

CNOOC said today it had received notice from the NYSE that it would be delisted on 9 March. “The company regrets the NYSE’s aforesaid decision and actions,” it said, advising investors to be cautious when dealing in its securities.

The NYSE actions are in line with a late-January state-ment by the US Treasury's sanctions enforcement arm the Office of Foreign Assets Control, confirming that the prohibi-tion on trading in CNOOC shares will take effect on 9 March. Divesting of securities will still be allowed until 11 Novem-ber, so long as the buyer is not a US person.

CNOOC is among 35 Chinese companies targeted by ex-ecutive orders issued by former president Trump in his final months in office under a previously unused law that cuts off access to the US financial system for entities Washington contends are tied to the Chinese military. President Joe Biden's administration plans to review those actions.

CNOOC said today that investors had the option to transfer their American depositary shares (ADS) to Hong Kong shares. Each ADS can be cancelled in exchange for 100 ordinary shares with JP Morgan Chase Bank, the depositary

for CNOOC’s ADS. Shareholders can continue to directly own the shares while the bank remains the agent, CNOOC said.

CNOOC’s ADS listing in NYSE accounts for only a small proportion of its shares, equivalent to just 0.5pc of CNOOC shares listed on the Hong Kong Exchange, the company said. The average daily trading volume of ADS accounted for about 14.5pc of its total shares traded in Hong Kong, New York and Toronto in 2020. CNOOC had issued a total of 44.65bn com-mon shares in Hong Kong as of February.

CNOOC shares fell by as much as 4.5pc in intraday trading after the announcement, but ended down by just 1.1pc today.